JAN 8//MASSIVE FIRE IN LOS ANGELES PALISADES AREA HOME TO MANY HOLLYWOOD STARS// GOLD CLOSED UP $5.35 TO $2656.25//SILVER DOWN ONE CENT TO $30.08//PLATINUM UP $6.40 TO $959.05 WHILE PALLADIUM WAS UP $1.15 TO $930.45//GOLD COMMENTARY TONIGHT COURTESY OF JOHN RUBINO//IN GERMANY AFD PARTY GAINS IN THE POLLS/UK SEES POUND FALTER AND YIELDS RISE AS THE COUNTRY HAS ITS TRUSS MOMENT//ISRAEL VS HAMAS //ISRAEL AND THE WEST BANK//COVID UPDATES/VACCINE INJURY REPORT//DR PAUL ALEXANDER/SLAY NEWS ETC//USA NEWS: LOOKS LIKE FAKE CNN NEWS ON TRUMP’S TARIFFS//SWAMP STORIES FOR YOU TONIGHT///

072 H GOLDMAN 51 118 C MACQUARIE FUT 5 118 H MACQUARIE FUT 200 190 H BMO CAPITAL 1498 363 C WELLS FARGO SEC 9 363 H WELLS FARGO SEC 14 435 H SCOTIA CAPITAL 22 624 H BOFA SECURITIES 1410 657 C MORGAN STANLEY 21 661 C JP MORGAN 99 686 C STONEX FINANCIA 10 16 730 C PTG DIVISION SG 21 732 C RBC CAP MARKETS 6 737 C ADVANTAGE 2 34 905 C ADM 2

TOTAL: 1,710 1,710

JPMorgan stopped 99/1710

GOLD: NUMBER OF NOTICES FILED FOR JANUARY/2024. CONTRACT: 1710 NOTICES FOR 171,000 OZ 5.319 TONNES

total notices so far: 5636 contracts for 563600 Oz (12.2115 tonnes)

FOR JANUARY

SILVER NOTICES: 56 NOTICE(S) FILED FOR 280,000 OZ/

total number of notices filed so far this month : 1544 for 7.720 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $5.35 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 871.08 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.01 AT THE SLV:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 459.353 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED472CONTRACTS TO 151,590 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG GAIN OF $0,48 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. WE HAD A MONSTER GAIN OF 1322 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE//TUESDAY’S TRADING.. WE HAD A ZERO LIQUIDATION OF T.A.S. CONTRACTS ON TUESDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 2 WEEKS WHERE THE RAIDS WERE CALLED UPON AGAIN AND AGAIN TO QUELL MASSIVE DERIVATIVE LOSSES BY OUR BULLION BANKS AND TO STOP THE RISE IN SILVER’S PRICE. THEY FAILED WITH //TUESDAY PRICING WITH ZERO LONGS BEING KNOCKED OFF. DERIVATIVE LOSSES CONTINUE TO MOUNT. WE HAD ZERO T.A.S. LIQUIDATION TUESDAY BUT A MASSIVE ISSUANCE OF 1453 CONTRACTS AND THAT SIGNALS RED THAT WE ARE GOING TO HAVE ANOTHER RAID SHORTLY.

WE HAD A MONSTER 850 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A HUMONGOUS 1453 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUMONGOUS SIZED 1312 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE. WE HAD ZERO TAS LIQUIDATION THROUGHOUT TUESDAY’S COMEX SESSION

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: A HUMONGOUS 1453 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS ESPECIALLY WITH MONDAY’S TRADING. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.48) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS GAIN IN PRICE WITH ZERO TAS LIQUIDATION AND A HUMONGOUS GAIN IN OUR TWO EXCHANGES OF 1312 CONTRACTS.

WE HAD A 850 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 8.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 30,000 OZ QUEUE JUMP//NEW STANDING REDUCES TO 8.220 MILLION OZ

// STANDING FOR SILVER//JAN RISES TO 8.2200 MILLION OZ

WE HAD:

/ FAIR SIZED COMEX OI GAIN +// A MONSTER 910 SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 660 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED 10 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN

TOTAL CONTRACTS for 4 DAYS, total 2260 contracts: OR 11.300 MILLION OZ (557 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 11.300 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 11.300 MILLION OZ///

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 472 CONTRACTS WITH OUR STRONG GAIN IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A 850 EFP ISSUANCE CONTRACTS: 850 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 8.110 MILLION OZ ON FIRST DAY NOTICE,FOLLOWED BY TODAY’S QUEUE JUMP OF 30,000 OZ

//NEW TOTAL STANDING FOR JAN ADVANCES TO 8.220 MILLION OZ

WE HAVE A HUMONGOUS SIZED GAIN OF 1322 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS 1453 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION BUT THEY STILL NEED THESE ISSUANCE FOR REPLENISHMENT FOR FUTURE TRADING /THE HUGE TA.S. ISSUANCE// STRONG LIQUIDATION DISTORTS THE TOTAL OI CONTRACTS STANDING AT THE COMEX. NO NET LONG SPECULATORS WERE BURNED ON TUESDAY WITH THE GAIN IN PRICE. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE TUESDAY NIGHT (1450) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE, AND PROBABLY NOT TODAY.

WE HAD 56 NOTICE(S) FILED TODAY FOR 280,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY STRONG SIZED 13,043 OI CONTRACTS TO 476,905 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW GETTING CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED A HUGE SIZED 138 CONTRACTS//

WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI (13,043 CONTRACTS) OCCURRED WITH OUR GAIN OF $14.50 IN PRICE TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 10.1331 TONNES FOLLOWED BY TODAY’S MONSTER QUEUE JUMP OF 543 CONTRACTS OR 54,300 OZ TO WHICH WE ADD THE FIRST ISSUANCE FOR EXCHANGE FOR RISK CONTRACTS TOTALLING 1700 CONTRACTS OR 170,000 OZ (5.28775 TONNES) ISSUED JAN 6/2025 TO WHICH WE ADD TODAY’S EXCHANGE FOR RISK ISSUANCE OF 150 CONTRACTS OR 15,000 OZ OR .4665 TONNES . NEW STANDING FOR JAN ADVANCES TO 19.757 TONNES + 5.28775 TONNES EX FOR RISK/PRIOR + .4665 EX FOR RISK TODAY = 25.510 TONNES

/NEW STANDING 25.510 TONNES

/ ALL OF THIS HAPPENED WITH OUR $14.50 GAIN IN PRICE WITH RESPECT TO TUESDAY’S COMEX ///. WE HAD A VERY STRONG GAIN OF 14,493 OI CONTRACTS (45.08 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE VIOLENT ACTION AT THE COMEX WITH RESPECT TO QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1450 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 477,043

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 14,493 CONTRACTS WITH 13,043 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 1450 EFP OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 14,493 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUMONGOUS SIZED AND CRIMINAL 10,184 CONTRACTS ISSUED. WE HAD A ZERO LIQUIDATION OF T.A.S CONTRACTS WITH OUR GAIN IN PRICE TUESDAY. MORE MONSTER ISSUANCE OF T.A.S IS NEEDED FOR REPLENISHMENT TO CARRY OUT ITS PRICE CONTAINMENT STRATEGY IN FUTURE TRADING. (FUTURE RAIDS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1450 CONTRACTS) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 13,043 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 14,493 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JAN 10.1331 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 543 CONTRACTS OR 54300 OZ (1.688 TONNES) TO WHICH WE ADD THAT CRAZY “DELIVERY” CALLED EXCHANGE FOR RISK TODAY OF .4665 TONNES// NEW STANDING FOR JAN ADVANCES TO: 25.510 TONNES

//NEW STANDING JAN: 25.510 TONNES

/ 3) ZERO T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE TUESDAY WITH ZERO SUCCESS IN REMOVING SPECULATOR LONGS, AS WE HAD A 1) $14.50 PRICE GAIN, AND 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A TOTAL GAIN OF 14,355 CONTRACTS ON OUR TWO EXCHANGES. ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) VERY STRONG SIZED COMEX OPEN INTEREST INCREASE 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///HUGE T.A.S. ISSUANCE: 10,184 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

TOTAL EFP CONTRACTS ISSUED: 14,006 CONTRACTS OF 1,400,600 OZ OR 43.56 TONNES IN 4 TRADING DAY(S) AND THUS AVERAGING: 4185 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES 43.56 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 43.56 DIVIDED BY 3550 x 100% TONNES = 1.22% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR.3,597.846

JAN. 43.56 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG SIZED 472 CONTRACTS OI TO 151,590 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.20233EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 850 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 850 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 462 CONTRACTS AND ADD TO THE 850 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1322 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS A HUGE 6.660 MILLION OZ OCCURRED WITH OUR $0.48 GAIN IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS/WEDNESDAY MORNING TUESDAY NIGHT

ASIA TRADING WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 0.52 PTS OR 0.02%

//Hang Seng CLOSED DOWN 167.74 PTS OR 0.86%

// Nikkei CLOSED DOWN 102.24 OR 0.02%//Australia’s all ordinaries CLOSED UP 0.66%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.3582 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3589// Oil UP TO 74.82 dollars per barrel for WTI and BRENT UP AT 77.47 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING AT LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY STRONG SIZED13,043 CONTRACTS TO 476,905 WITH OUR GAIN IN PRICE OF $14.50 WITH RESPECT TO TUESDAY’S TRADING. WE LOST ZERO NET LONGS WITH OUR PRICE GAIN FOR GOLD AS WE HAD ALSO, AS YOU WILL SEE BELOW, A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1450) . THEN MUCH TO MY SURPRISE,THE CME ISSUED THEIR SECOND ISSUANCE OF EXCHANGE FOR RISK: (150 CONTRACTS FOR 15000, OZ OR .4665 TONNES) . THUS IN TOTAL WE HAD A HUGE GAIN ON OUR TWO EXCHANGES OF 14,493 CONTRACTS WITH OUR GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY ABSORBED EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE PAST WEEK. WE HAD ZERO T.A.S. LIQUIDATION DURING THE TUESDAY COMEX SESSION. WE HAD A HUMONGOUS 10,184 T.A.S. ISSUANCE TUESDAY NIGHT.

THE FED IS THE MAJOR SHORT OF AROUND 82+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST 197 , 199, 2001, AND FRIDAY NIGHTS 202, 203 AND 204 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP IS COMING INTO OFFICE IN 4 TRADING DAYS. TRUMP WOULD PROBABLY BE FURIOUS WITH THE FED IF IT FOUND OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING THE LAST WEEK OF DECEMBER IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD. AS YOU WILL SEE BELOW, WE HAD ANOTHER HUGE QUEUE JUMPING SESSION TODAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF JANUARY.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1450 EFP CONTRACTS WERE ISSUED: : /FEB 1450 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1450 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VEWRY STRONG SIZED TOTAL OF 14,355 CONTRACTS IN THAT 1450 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A VERY STRONG SIZED GAIN OF 12,905 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $14.50 TUESDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A HUMONGOUS SIZED SIZED 10,184 CONTRACTS, AND THESE WILL BE USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK).

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON DEC. 27, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE DECEMBER’S OPTIONS EXPIRY TRADING. T.A.S. LIQUIDATION WAS EVIDENT IN MONDAY’S COMEX TRADING//RAID BUT NOT IN TODAY’S TRADING. HOWEVER NOT TO BE UNDONE, THE CROOKS ISSUED THEIR MONSTER 10,184 T.A.S CONTRACTS AND THIS WILL BE USED IN OUR NEXT RAID IN GOLD TRADING PROBABLY BEFORE TRUMP’S INAUGURATION.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JAN (25.510 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE JAN DELIVERY MONTH.

JANUARY: 10.1331 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 49 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year: 540.30 tonnes

January 2025: 19.757 TONNES + 5.753 EX FOR RISK/PRIOR = 25.510 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $14.50/)//AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A VERY STRONG GAIN IN OUR TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION TUESDAY BUT DID HAVE A MONSTER ISSUANCE OF T.A.S. OF 10,184 CONTRACTS.

THE CROOKS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING.

EXCHANGE FOR RISK EXPLANATION/DECEMBER TRADING AND NOW JANUARY!!

36 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 14.6836 TONNES. THE COMEX IS TOTALLY SHATTERED TO PIECES.

WE NOW BEGIN OUR NEW MONTH OF JANUARY AND LO AND BEHOLD, THE CROOKS ISSUED ANOTHER MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THEN TO MY HORROR, THEY ISSUED THEIR SECOND EXCHANGE FOR RISK TOTALLING 150 CONTRACTS FOR 15000 OZ OR .4665 TONNES. THIS TONNAGE WILL BE ADDED TO THE FIRST ISSUANCE. THUS TOTAL EXCHANGE FOR RISK ISSUANCE FOR JANUARY: 5.7533 TONNES

TOTAL DELIVERIES JANUARY TRADING

WE HAVE GAINED A TOTAL OF 45.08 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN (10.133TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S MONSTER QUEUE JUMP OF 543 CONTRACTS OR 54300 OZ (1.688 TONNES) TO WHICH WE MUST ADD OUR 5.7533 TONNES OF EXCHANGE FOR RISK ISSUANCE WHERE THE BUYERS ASSUMES THE RISK FOR DELIVERY.(ISSUED JAN 6/2025 AND JAN 8)

NEW STANDING FOR JAN: 19.757 TONNES + 5.753 TONNES EX FOR RISK/PRIOR = 25.510 TONNES (WHICH IS HUGE FOR OUR VERY ACTIVE DELIVERY MONTH)

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $14.40

WE HAD 138 CONTRACTS ADDED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 14,493 CONTRACTS OR 1,449,300 OZ (45.08 TONNES)

confirmed volume TUESDAY 192,387 contracts: weak ////nobody wishes to play with the crooks

ii) Brinks Enhanced: 4828.293 oz (12 london good delivery bars each london bar around 400. oz each)

total deposit 133,432.293 oz

No of oz served (contracts) today

1710 notice(s) 171, 000 OZ 5.319 TONNES

No of oz to be served (notices)

716 contracts 71,600 OZ 2.227 TONNES

Total monthly oz gold served (contracts) so far this month

5636 notices 563600 oz 17.530 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

dealer deposits: 0

total dealer deposits: end

we have 2 customer deposit

128,604.00 Brinks 4000 kilobars

ii) Brinks Enhanced: 4828.293 oz (12 london good delivery bars each london bar around 400. oz each)

total deposit133,432.293 oz

withdrawals: 0

adjustments:2

a) added into eligible 960.503 oz

b) adjustment customer to dealer Manfra 195.707 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JAN.

For the front month of JAN: we have an oi of 2426 contracts having GAINED A HUGE 466 contracts. We had a strong 77 contract issuance on TUESDAY. Thus ANOTHER MONSTER QUEUE JUMP (GAIN) of 543 contracts on our two exchanges. (54,300 oz or 1.688 tonnes)

FEBRUARY GAINED 2939 CONTRACTS TO 325,225 .

MARCH HAD A GAIN OF 54 CONTRACTS UP TO 190

APRIL HAD A GAIN OF 8373 CONTRACTS UP TO 83,281 CONTRACTS

We had 1710 contracts filed for today representing 171,000 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1710 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 99 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JAN /2025. contract month, we take the total number of notices filed so far for the month (5636 x 100 oz ) to which we add the difference between the open interest for the front month of JAN(2476 CONTRACTS) minus the number of notices served upon today (1710 x 100 oz per contract( equals 635200 OZ OR 19.757 TONNES. to which we add those criminal exchange for risk issuance of .4665 TONNES TO 5.28775 tonnes/PRIOR//TOTAL EXCHANGE FOR RISK = 5.753 TONNES. THUS NEW STANDING FOR GOLD AT THE COMEX FOR JAN IS 25.510 TONNES

thus the INITIAL standings for gold for the JAN contract month: No of notices filed so far (5636 x 100 oz +we add the difference for front month of JAN (2426 OI} minus the number of notices served upon today (1710 x 100 oz which equals 635200 oz (19.757 TONNES) + 5.753 tonnes ex for risk today +/PRIOR = 25.510

TOTAL COMEX GOLD STANDING FOR JAN.: 25.510 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 22,106.900.597 OZ

TOTAL REGISTERED GOLD 9,043,081.466 oz or 281.27 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 13,063.819.091 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,911,248 oz (REG GOLD- PLEDGED GOLD)= 214.96 tonnes //

JPMorgan enhanced inventory is 3.592 million oz/1,877,000 oz = 19.15% of entire inventory..

END

SILVER/COMEX

JAN 8. 2025

INITIAL

//2024// THE JAN 2025 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

nil

.

Deposits to the Dealer Inventory

NIL

Deposits to the Customer Inventory

i) Into Brinks 1613,867.100 oz ii) Into Loomis: 902,168.580 oz

total deposit 2,516,035.680

No of oz served today (contracts)

56 CONTRACT(S) (280,000 OZ)

No of oz to be served (notices)

100 contracts (0.500 MILLION oz)

Total monthly oz silver served (contracts)

1544 Contracts (7.720 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

deposits:2

i) Into Brinks 1613,867.100 oz ii) Into Loomis: 902,168.580 oz

total deposit 2,516,035.680

WITHDRAWALS:

NIL

total withdrawal: NIL oz

ADJUSTMENT

CUSTOMER ACCOUNT TO DEALER MANFRA: 257,371.389 OZ

JPMorgan has a total silver weight: 135.532million oz/322.281million or 42.15%

TOTAL REGISTERED SILVER: 73.499 MILLION OZ//.TOTAL REG + ELIGIBLE. 322.563 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF JAN /2024 OI: 156 OPEN INTEREST FOR A LOSS OF 178 CONTRACT(S).

WE HAD 184 CONTRACT ISSUANCE ON TUESDAY. THUS WE GAINED A SMALL 6 CONTRACTS, THAT IS WE HAD A 6 CONTRACT QUEUE JUMP FOR 30,000 OZ AS THE BOYS WILL TRY THEIR LUCK FINDING SILVER OVER ON THIS SIDE OF THE POND.

FEBRUARY SAW A GAIN 0F 4 CONTRACTS TO STAND AT 673

MARCH SAW A LOSS OF 193 CONTRACTS DOWN TO 119,182

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 56 for 280,000 oz

CONFIRMED volume; ON TUESDAY 57,281 awful//

To calculate the number of silver ounces that will stand for delivery in JAN we take the total number of notices filed for the month so far at 1544x 5,000 oz = 7.72 MILLION oz

to which we add the difference between the open interest for the front month of JAN (156) and the number of notices served upon today (56)x (5000 oz)

Thus the standings for silver for the JAN 2025 contract month: 1544 Notices served so far) x 5000 oz + OI for the front month of JAN(156) minus number of notices served upon today (56)x 5000 oz equals silver standing for the JAN contract month equating to 8.2200 MILLION OZ.

New total standing: 8.220 million oz.

There are 73.242 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

JAN 8 WITH GOLD UP $5.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 7 WITH GOLD DOWN $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 6 WITH GOLD DOWN $4.90 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 3 WITH GOLD DOWN $14.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 2 WITH GOLD UP $29.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 31 WITH GOLD UP $20.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 30 WITH GOLD DOWN $11.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.28 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.52 TONNES

DEC 27 WITH GOLD DOWN $17.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.80 TONNES

DEC 26 WITH GOLD UP $17.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: : ///INVENTORY RESTS AT 873.95 TONNES

DEC 24 WITH GOLD UP $6.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES OF GOLD OUT OF THE GLD. / // : .///INVENTORY RESTS AT 873.95 TONNES

DEC 23 WITH GOLD DOWN $13,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 16.66 TONNES OF GOLD VAPOUR GOLD INTO THE GLD. / // : .///INVENTORY RESTS AT 877.40 TONNES

DEC 20 WITH GOLD UP $29,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 860.74 TONNES

DEC 19 WITH GOLD DOWN $45.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF .29 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 18 WITH GOLD DOWN $8.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 17 WITH GOLD DOWN $6.85 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.23 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 16 WITH GOLD DOWN $2.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.70 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 13 WITH GOLD DOWN $24.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.78 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 868.60 TONNES

DEC 12 WITH GOLD DOWN $34.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.59 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 873.38 TONNES

DEC 11 WITH GOLD UP $29.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 9 WITH GOLD UP $31.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD. // : .///INVENTORY RESTS AT 871.94 TONNES

DEC 6 WITH GOLD UP $6.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD. A WITHDRAWAL OF 1.71 TONNES OF GOLD FROM THE GLD// : .///INVENTORY RESTS AT 871.94 TONNES

DEC 5 WITH GOLD DOWN $26.80 ON THE DAY; NO CHANGES IN GOLD AT THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 4 WITH GOLD UP $6.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 3 WITH GOLD UP $10.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.59 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 875.96 TONNES

DEC 2 WITH GOLD DOWN $20.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : .///INVENTORY RESTS AT 878.55 TONNES

NOV 29 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : Z WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD . .///INVENTORY RESTS AT 878.55 TONNES

NOV 27 WITH GOLD UP $18.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : . .///INVENTORY RESTS AT 879.41 TONNE

NOV 26 WITH GOLD UP $3.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : A DEPOSIT OF 1.44 TONNES OF GOLDINTO THE GLD. .///INVENTORY RESTS AT 879.41 TONNES

GLD INVENTORY: 871.08 TONNES, TONIGHTS TOTAL

SILVER

JAN 8 WITH SILVER DOWN $0.01 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 7 WITH SILVER UP 48 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 6 WITH SILVER UP 38 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 3 WITH SILVER UP 17 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 2 WITH SILVER UP 45 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.616 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 462.128 MILLION OZ

DEC 31 WITH SILVER DOWN 14 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 30 WITH SILVER DOWN 39 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: // A WITHDRAWAL OF 1.13 MILLION OZ FROM THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 27 WITH SILVER DOWN 24 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY AT SLV RESTS AT 461.651 MILLION OZ

DEC 24 WITH SILVER UP 2 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 23 WITH SILVER UP 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 6.15 MILLION OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 20 WITH SILVER UP 43 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 183,000 OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 457.597 MILLION OZ

DEC 19 WITH SILVER DOWN 25 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV///// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 18 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 17 WITH SILVER DOWN 12 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.456 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 16 WITH SILVER DOWN 0 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 4.84 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 13 WITH SILVER DOWN 46 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .536 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 462.892 MILLION OZ

DEC 12 WITH SILVER DOWN 94 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 5.787 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 463.428 MILLION OZ

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 10 WITH SILVER DOWN 8 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.868 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 471.812 MILLION OZ

DEC 9 WITH SILVER UP $0.91 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.367 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 473.680 MILLION OZ

DEC 6 WITH SILVER DOWN $0.00 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 4.329 MILLION OZ/// //INVENTORY AT SLV RESTS AT 475.047 MILLION OZ

DEC 5 WITH SILVER DOWN $0.23 //NO CHANGES IN SILVER INVENTORY AT THE SLV” /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 4 WITH SILVER UP 26 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV”: A WITHDRAWAL OF 2.206 MILLION OZ FORM THE SLV. /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 3 WITH SILVER UP 59 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

DEC 2 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 1,458,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

NOV 29 WITH SILVER UP 51 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 365,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 474.382 MILLION OZ

NOV 27 WITH SILVER DOWN $0.25 //NO CHANGES IN SILVER INVENTORY AT THE SLV.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 26 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:.A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV./.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

CLOSING INVENTORY 459.353 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

END

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

There have been some epic hyperinflations over the centuries, but none was as brutal — and consequential — as Germany’s in the early 1920s. Here’s a quick Chat GPT summary followed by some graphic images and a list of lessons the world should have — but apparently hasn’t — learned:

Context of Post-World War I Germany:

After Germany’s defeat in World War I in 1918, the Weimar Republic was established, inheriting the country’s economic and political turmoil. The Treaty of Versailles (1919) placed heavy reparations on Germany, requiring it to pay significant war damages to the Allied powers. This placed a huge strain on the country’s economy.

War Debt and Reparations:

In the aftermath of the war, Germany’s government struggled to meet its financial obligations. The Weimar government resorted to printing more money to cover deficits, which contributed to inflation. Additionally, the reparations payments demanded by the Allies further drained the nation’s resources.

The Ruhr Occupation (1923):

In response to Germany’s failure to meet its reparations payments in 1922, France and Belgium occupied the Ruhr Valley, the heart of Germany’s industrial production. In protest, German workers in the region went on strike, and the government continued to print money to support them. This action significantly worsened inflation.

Hyperinflation Escalates (1921-1923):

In 1921, inflation began to accelerate as the government printed more and more money. By 1923, inflation had spiraled out of control, with the value of the German mark plummeting. Prices for goods and services soared. People needed wheelbarrows full of currency just to buy basic necessities, and the value of savings vanished almost overnight.

In January 1923, the exchange rate was approximately 18,000 marks to 1 US dollar. By November 1923, it had risen to 4.2 trillion marks to 1 US dollar.

Daily life became chaotic, with businesses and workers adjusting prices constantly. People resorted to bartering, and foreign currencies like the US dollar or the French franc became more stable than the mark.

Impact on Society:

Middle Class Hardships: The middle class was hardest hit, as savings and pensions were wiped out. Many families saw their life savings evaporate, leading to widespread poverty and a collapse in confidence in the Weimar government’s ability to manage the economy.

Social Unrest: The hyperinflation fueled social unrest. There were strikes, protests, and political extremism. People lost faith in the Weimar Republic, and some turned to more radical solutions, including support for both left-wing and right-wing extremist movements (e.g., the Nazi Party).

Resolution and Stabilization:

The crisis was finally brought under control in late 1923 with the introduction of a new currency, the Rentenmark, which was backed by land and industrial resources rather than gold. The Rentenmark was introduced in November 1923 and helped restore some confidence in the German economy. This marked the end of the hyperinflation crisis and allowed for economic recovery in the following years, although the scars left on society and politics remained.

Legacy of Hyperinflation:

The hyperinflation of the Weimar Republic left lasting consequences:

It contributed to the eventual collapse of the Weimar Republic and the rise of Adolf Hitler and the Nazi Party, which capitalized on widespread discontent.

The memory of hyperinflation created a deep mistrust of paper currency and government economic management in Germany.

The instability helped foster extremist political movements, as people sought radical solutions to their financial woes.

In summary, the hyperinflation of the Weimar Republic was the result of a combination of war reparations, political instability, and economic mismanagement. It devastated the German economy, undermined public trust in the government, and played a crucial role in the events that led to the rise of Nazism in Germany.

Graphic Consequences

Here’s what gold did in Germany during this time. As the currency became worthless, sound money became priceless:

German citizens who trusted their government and held large amounts of currency ended up taking wheelbarrows full of the stuff to buy groceries and, as seen below, burning currency in furnaces for heat.

Lessons

There’s a limit to how much new currency a nation can create before people give up on it. At that point, it quickly becomes worthless, and the things valued in it — gold, real estate, food — soar in local currency terms. So if you think $2600/oz gold is expensive, revisit the last two years on the above chart.

The cultural consequences of wiping out an entire generation’s savings include a loss of trust in government institutions and a willingness to follow strong leaders who promise to do whatever it takes to stop the bleeding. Hence, Hitler.

The US tried a mini-version of this “print like crazy and hope for the best” strategy during the pandemic and got its first taste of near-double-digit inflation in 40 years. With current budget deficits at record highs and interest rates moving up despite Fed easing, the next crisis might be — like Germany in 1920 — an existential fork in the road.

END

3. CHRIS POWELL AND GATA DISPATCHES

4. OTHER GOLD COMMENTARIES/

END

ANDREW MAGUIRE AND ALASDAIR MACLEOD//LIVE FROM THE VAULT 204

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY

end

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING WEDNESDAY MORNING TUESDAY NIGHT

SHANGHAI CLOSED UP 0.52 PTS OR 0.02%

//Hang Seng CLOSED DOWN 167.74 PTS OR 0.86%

// Nikkei CLOSED DOWN 102.24 OR 0.02%//Australia’s all ordinaries CLOSED UP 0.66%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.3582 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3589// Oil UP TO 74.82 dollars per barrel for WTI and BRENT UP AT 77.47 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING AT LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.3582

OFFSHORE YUAN: DOWN TO 7.3589

SHANGHAI CLOSED CLOSED UP 0.52 PTS OR 0.02%

HANG SENG CLOSED CLOSED DOWN 167.74 PTS OR 0.86%

2. Nikkei closed DOWN 102.24PTS OR 0.25%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 109.02 EURO FALLS TO 1.0294 DOWN 49 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.117 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.33…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.5195 Italian 10 Yr bond yield UP to 3.667 //SPAIN 10 YR BOND YIELD UP TO 3.184

3i Greek 10 year bond yield UP TO 3.284

3j Gold at $2662.50/Silver at: 30.33 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 2 AND 67/100 roubles/dollar; ROUBLE AT 105.88

3m oil into the 74 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 158.33 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.1170% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9114 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9378 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.714 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.965 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.306 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 35.38…

10 YR UK BOND YIELD: 4.8380 UP 11 PTS

10 YR CANADA BOND YIELD: 3.372 UP 7 BASIS PTS

5 YR CANADA BOND YIELD: 3.072 UP 7 PTS.

2a New York OPENING REPORT

Futures Slump As Yields, Dollar Soar

by Tyler Durden

Wednesday, Jan 08, 2025 – 08:13 AM

US equity futures were already rolling over following yesterday’s momentum-driven rout, when a the latest report out of CNN (a polar opposite to the just as fake news from WaPo earlier this week, but fake nonetheless) claiming that Trump was “considering declaring a national economic emergency to provide legal justification for a large swath of universal tariffs on allies and adversaries” sent the dollar surging, all other G-20 currencies plunging, and sparked a broad selloff across risk assets. As of 8:00am ET, S&P futures were down 0.2%, bouncing from session lows of -0.4%, and reversing a gain of 0.4% earlier in the session; Nasdaq futures were hurting more, sliding 0.6% as many of the recent best performers were sold off hard, and none more so than quantum computers which were down about 20% as a group in premarket trading; the Mag7 was also largely red )Apple -0.5%, Nvidia +0.1%, Microsoft -0.09%, Alphabet -1%, Amazon -0.07%, Meta Platforms -0.9% and Tesla -1%). Europe’s Stoxx 600 Index lost 0.4% and Asian stocks slumped, with China tumbling as usual. Meanwhile, bonds extended their ongoing selloff, with the 10Y rising to 4.72% and triggering Goldman’s VaR shock threshold of a 60bps increase in 1 month. In the UK, 10-year bond yields rose to their highest since 2008 and the 30-year inflation-linked note is now yielding more than 2%, the most since the Truss crisis of 2022 as fears spread that Keir’s spending plans will spark a fiscal disaster.

In premarket trading Quantum stocks tumbled after Nvidia CEO Jensen Huang said that “very useful” quantum computers are likely decades away. Quantum Computing (QUBT) -20%, D-Wave Quantum (QBTS) -21%, Rigetti Computing (RGTI) -23%, IonQ (IONQ) -13%. Sana Biotechnology (SANA) soars 232% after the company reported positive data from a study of its treatment of type 1 diabetes. Here are some other notable premarket movers:

AAR (AIR) rises 3% after the provider of aviation services and parts posted fiscal 2Q sales that soared past estimates.

Flutter (FLUT) slips 2% after the gambling firm cut its guidance for US preliminary revenue 2024 due to the impact of US sports results in the fourth quarter.

Health Catalyst (HCAT) climbs 5% as KeyBanc turned bullish, saying the stock’s valuation is deeply discounted.

Jasper Therapeutics (JSPR) falls 41% after posting data from the Beacon study of briquilimab.

Olo (OLO) slips 5% after Piper Sandler downgraded the restaurant software firm, flagging concern about the 2025 outlook amid executive changes and workforce cuts.

Palo Alto Networks (PANW) declines 2% after the security software received a pair of analyst downgrades.

S&P 500 figures started spiking lower just after 6 a.m. New York time following a report from CNN that Trump is considering declaring a national economic emergency to push through his tariff plans. Europe’s Stoxx 600 Index lost 0.4% and bond yields increased.

“Higher Treasury yields are a cause for concern for equity investors, especially when combined with speculation on what Trump may do,” said Lilian Chovin, head of asset allocation at Coutts & Co. in London. “Our view is that markets can digest higher yields, provided they are driven by stronger growth rather than inflation. In the near term it will be a challenge for risk assets.”

Amundi SA, Europe’s largest asset manager, sees a “reasonable” chance that the yield on 10-year Treasuries will again test the key level of 5%, a milestone only reached a handful of times over the past two decades. Citigroup’s wealth division also said a return to 5% — while not its base case — would offer a “really appealing” level at which to add. The yield was just under 4.70% on Wednesday.

Meanwhile, equity traders are bracing for further volatility over the coming weeks. “These first trading days have been a good overview of what could happen this year,” said Mabrouk Chetouane, head of global market strategy at Natixis Investment Managers. “Inflation, tariffs, Trump, growth, monetary policy — all these concerns could bring uncertainty.” Credit supply is also continuing after corporations and banks globally have raised roughly $111 billion this year through Tuesday. Spreads of corporate bonds remain near their lowest post-financial crisis level, despite the volatility in government debt.

In Europe stocks also reversed earlier gains, and what was a 0.4% rise has reversed into a 0.4% loss for the Stoxx 600 with financial services and banks leading gains. Here are the biggest movers Wednesday:

Novo Nordisk gains as much as 2.4% after being upgraded to buy from neutral at UBS, which said shares in the Danish drugmaker are at an “attractive entry point” following an “overdone” selloff

LSEG rises as much as 3.2% after making it on the list BofA’s “25 stocks for 2025” and the bank is adding it to a European list of top ideas, say analysts

Vallourec jumps as much as 7.4%, after the French tube manufacturer announced it hit a target of zero net debt one year ahead of plan and is now ready to return capital to shareholders starting in 2025

BCP shares advance 5.3%, rising to the highest level since May 2016, after JP Morgan raised the recommendation on the Portuguese lender to overweight from neutral on positive earnings momentum and generous payout

Heidelberg Materials rally as much as 3.4% after analysts at BofA Global Research raised their price target on the building materials company, naming it one of its “25 stocks for 2025”

Pluxee surges as much as 14% to the highest in four months after the employee benefits and motivation solutions firm beat analyst expectations for the first quarter

European wind power-related stocks fall on Wednesday after President-elect Donald Trump said he would seek to prevent the construction of wind farms during his second term, threatening billions of dollars in planned projects

Shell shares decline as much as 2% after 4Q trading update shows weakness across several divisions and may cause cuts in consensus expectations, RBC says in a note

InterContinental Hotels Group slips as much as 1.6%, to trade at the lowest in six weeks, after Morgan Stanley downgraded the stock to underweight from equalweight

Trigano falls as much as 7.9% in Paris, the most in about seven months, after the leisure-vehicle manufacturer reported a year-on-year revenue decline

Asian stocks dropped as concerns over a delay in further Federal Reserve interest-rate cuts weighed on sentiment. Tech shares tracked their US peers lower. The MSCI Asia Pacific Index fell as much as 0.8%, with TSMC and Tencent among the biggest drags. A drop in US big tech after Nvidia’s product presentation failed to lift near-term prospects weighed on Asian chipmakers. Samsung Electronics bucked the trend after Nvidia’s founder expressed confidence in the Korean company.

In FX, the Bloomberg Dollar Spot Index rises 0.3% while the Swedish krona sits at the bottom of the G-10 FX leader board, falling 0.4% against the greenback after CPI surprised to the downside.

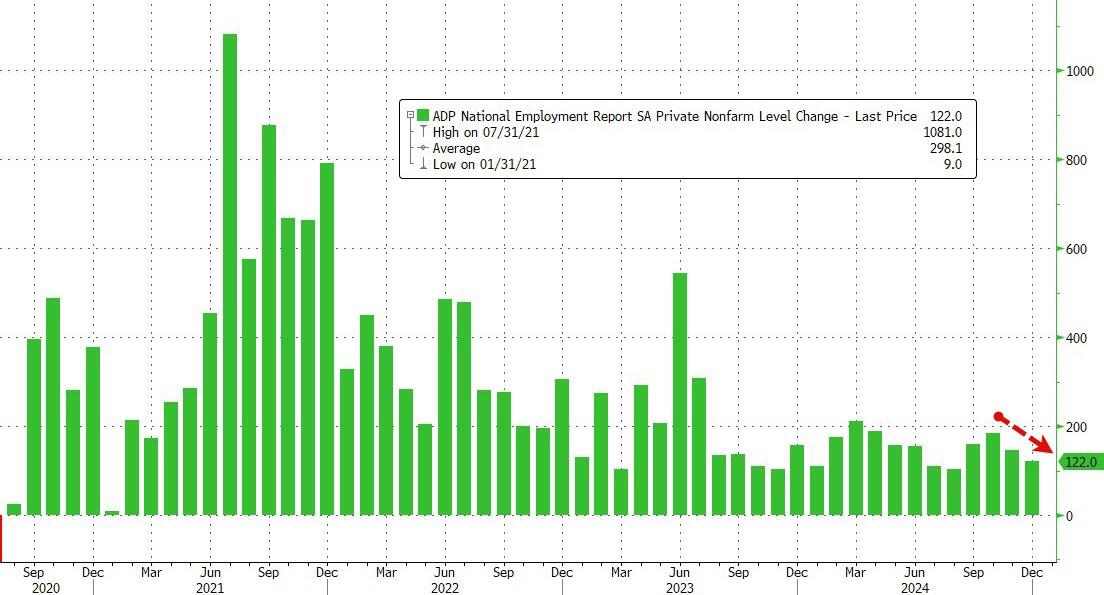

In rates, treasury futures saw continued downside pressure into early US session, reaching day’s lows amid bigger selloff in core European rates and after CNN reported that Trump was seeking an emergency declaration to push through tariffs. UK gilts led losses, with 10-year yields reaching highest level since 2008. US yields are cheaper by 1bp-3bp across maturities near session highs; 10-year, higher by 2.5bp near 4.71%, outperforms UK 10-year by about 7bp as persistent inflationary pressure continues to rattle UK markets; UK 10-year yield climbed more than 10bp to 4.789%. This week’s Treasury auction cycle concludes at 1pm New York time with $22 billion 30-year bond reopening; Tuesday’s 10-year note sale tailed slightly, by 0.2bp, as it drew highest yield since 2007. Corporate new-issue calendar is empty so far and expected to remain muted for the rest of the week after 33 offerings were priced on the past two days, topping dealers’ full-week forecasts for about $50 billion. Potential issuers today include refiner HF Sinclair, which held fixed-income investor calls Tuesday. US session includes December ADP employment change, weekly jobless claims and 30-year bond reopening poised to draw highest yield since 2007.

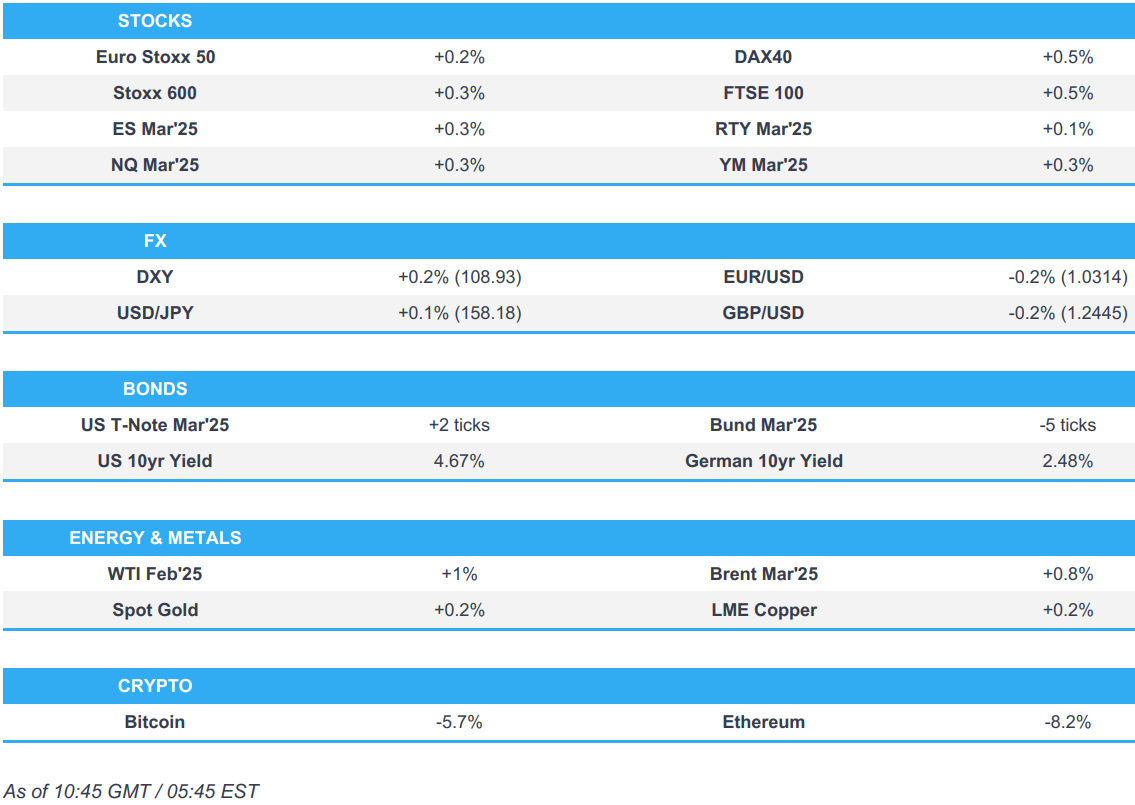

In commodities, oil prices advance, with WTI rising 0.8% to $74.80 a barrel. Spot gold adds $6 to $2,655/oz. Bitcoin falls below $96,000.

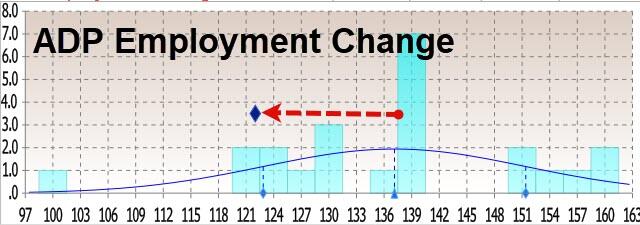

US economic data calendar includes December ADP employment change (8:15am), jobless claims (8:30am), November wholesale inventories (10am) and consumer credit (3pm). Fed speaker slate includes Waller at 8am; FOMC releases minutes from Dec. 18 meeting at 2pm

Market Snapshot

S&P 500 futures up 0.2% to 5,968.50

STOXX Europe 600 up 0.2% to 515.48

MXAP down 0.6% to 180.83

MXAPJ down 0.6% to 568.23

Nikkei down 0.3% to 39,981.06

Topix down 0.6% to 2,770.00

Hang Seng Index down 0.9% to 19,279.84

Shanghai Composite little changed at 3,230.17

Sensex down 0.1% to 78,107.00

Australia S&P/ASX 200 up 0.8% to 8,349.15

Kospi up 1.2% to 2,521.05

German 10Y yield up 3 bps at 2.51%

Euro down 0.2% to $1.0322

Brent Futures up 0.8% to $77.67/bbl

Gold spot up 0.2% to $2,654.04

US Dollar Index up 0.29% to 108.86

Top Overnight News

China will subsidize more consumer products and boost funding for industrial equipment upgrades to boost domestic consumption. Meantime, the PBOC set its yuan reference rate at the strongest compared to estimates since April. BBG

Yields on China’s 10-year sovereign debt hit record lows despite Beijing’s recent stimulus announcements, suggesting growing concern the nation will fail to avoid a deflationary spiral mirroring 1990s Japan. BBG

The Bank of Japan will likely keep raising interest rates in the coming years as inflation appears on track to sustainably hit its 2% target, said former governor Haruhiko Kuroda. RTRS

Samsung shares rose after Nvidia CEO Jensen Huang expressed confidence in the company’s ability to resolve technical issues producing a new type of memory chip for AI systems. BBG

Europe is pushing back against Trump. Describing Greenland as European territory, French Foreign Minister Jean-Noel Barrot warned him against threatening the EU’s sovereign borders. And the EU’s industry chief called on the bloc to defend itself against protectionist measures. BBG

German economic data for Nov falls short of expectations, including retail sales (-0.6% M/M vs. the Street +0.5%) and factory orders (-5.4% M/M vs. the Street -0.2%). BBG

President-elect Donald Trump is considering declaring a national economic emergency to provide legal justification for a large swath of universal tariffs on allies and adversaries, four sources familiar with the matter told CNN, as Trump seeks to reset the global balance of trade in his second term. CNN

Oil gained as an industry report pointed to a seventh weekly draw in US stockpiles. Inventories at the key hub in Cushing also slumped — by 3.1 million barrels — the API is said to have reported. That would be the biggest drop since August 2023 if confirmed by the EIA today. BBG

Microsoft plans job cuts across the company soon, targeting underperforming employees. Business Insider

A more detailed look at global markets courtesy of Newsquawk

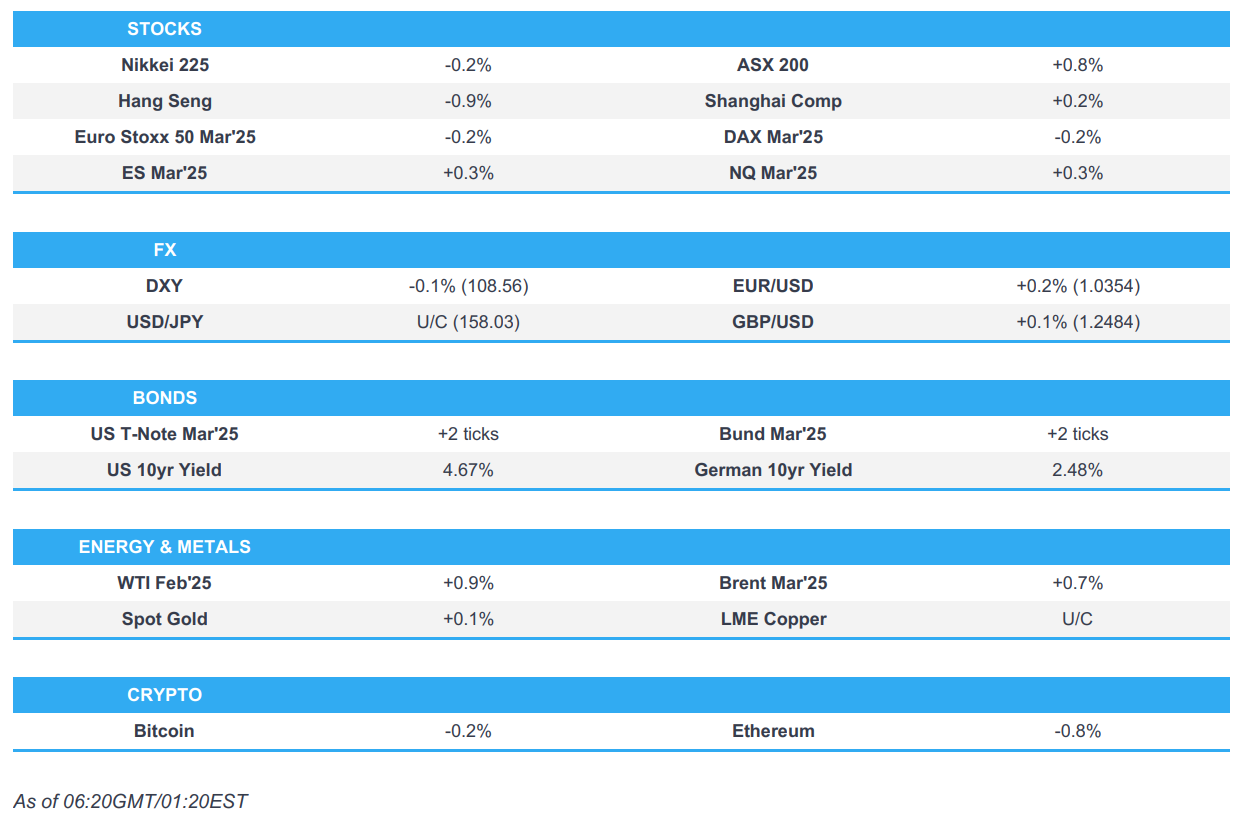

APAC stocks traded mixed following the weak handover from Wall St where tech underperformed as yields climbed after the hot ISM Services and strong JOLTS data. ASX 200 gained amid strength in mining stocks and the top-weighted financial sector, while participants digested mixed monthly inflation data in which the Weighted CPI reading topped forecasts, but the annual trimmed mean figure softened. Capital Economics suggested would provide greater confidence the RBA is on track to meet its inflation mandate if it the result is replicated in the quarterly figures due later this month. Nikkei 225 gradually nursed the majority of its opening losses and reclaimed the key 40,000 level. Hang Seng and Shanghai Comp were pressured with market participants underwhelmed by the latest press briefing in Beijing where the NDRC announced to expand the scope of home appliance trade-ins eligible for subsidies, while frictions lingered with China’s MOFCOM voicing criticism over recent US restrictions on Chinese companies.

Top Asian News

NDRC Vice Chairman announces loan discounts for equipment upgrades and expansion of trade-in program to include more consumer goods, while the number of types of household appliances eligible for recycling subsidies to increase from 8 to 12 with a maximum subsidy of 20% of the sales price for each item. NDRC said it will allocate special funds to support the recycling and treatment of waste electrical and electronic products, as well as include microwaves, water purifiers, dish-washing machines and rice cookers in the consumer goods trade-in subsidy scope. Furthermore, it will subsidise smartphones for up to 15% of the price and will support equipment upgrades of information technology, safe production and agriculture equipment.

Chinese Finance Ministry official said the government has allocated CNY 81bln for consumer goods trade-ins so far this year, while a PBoC official stated they will step up financial support for private and small firms in equipment upgrades with the central bank allocating CNY 100bln of loans for select small technology firms.

China condemned the US military blacklisting of Chinese companies and called on the US to immediately address its misconduct, while it said the US is endangering the stability of the global supply chain.

China PCA December Prelim Retail Passenger Vehicle Sales +9% M/M (prev. +7.1%); +11% Y/Y (prev. 16.5%)

European bourses initially opened with a slight negative bias, taking impetus from a mostly negative APAC session. Soon after the cash open, sentiment improved in Europe, to currently display a modestly firmer picture, with only a couple of indices residing in the red. European sectors are mixed, with no clear out/underperformer in the session thus far. Financial Services lead, followed closely by Banks. Energy is found at the foot of the pile, with losses fuelled by Shell after it trimmed its Q4 production guidance. US equity futures are modestly firmer across the board, in an attempt to recoup some of the hefty losses seen in the prior session, which were sparked by hotter-than-expected US ISM Services and JOLTS Job Openings figures.

Top European News

Banca Ifis Bids for Illimity Amid Italian Consolidation Wave

UK Prepares to Sell New Five-Year Bonds as Borrowing Costs Surge

IPT: Indonesia EUR Benchmark; 8Y MS+170 Area, 12Y MS+195 Area

Novo Nordisk Gains After UBS Upgrade on ‘Attractive’ Entry Point

FX

USD is continuing the strength from Tuesday which was facilitated by the hot ISM Services PMI data and as JOLTS data topped analysts’ forecast range. DXY re-approaches 109.00 to the upside (in a current 108.55-96 range). Attention now turns to the FOMC Minutes, ADP Employment and Initial Jobless Claims data.

EUR attempted to regain some composure overnight after its slide beneath the 1.0400 level before feeling more pressure from the continued rebound in the USD. German Retail Sales were mixed, whilst Industrial Orders were downbeat, but did have some caveats (details in the data section below). EUR/USD resides in a 1.0311-57 range with downside levels including the 6th Jan low (1.0294).

JPY traded indecisively overnight with USD/JPY on both sides of the 158.00 level amid a quiet data calendar for Japan and the mixed risk tone. Similar price action in Europe with the current intraday parameter between 157.91-158.32, with the pair eyeing yesterday’s highs (158.42).

GBP is subdued in tandem with G10 counterparts on the back of the stronger USD. GBP/USD resides in a current 1.2441-94 range with the next downside level the 6th Jan low (1.2410).

Antipodeans are feeling pressure from the firmer greenback and in the absence of major newsflow this morning. AUD/USD was choppy following the latest monthly inflation data from Australia in which the Weighted CPI printed firmer than expected but the annual trimmed mean CPI softened from the previous. AUD/USD trades within 0.6213-42 and NZD/USD within 0.5613-41.

SEK is modestly weaker after softer-than-expected consumer inflation metrics across the board. Following December’s CPIF (cooler than expected) and the Minutes from the December meeting CapEco now expects the Riksbank to cut by 25bps in January (prev. exp. March).

PBoC set USD/CNY mid-point at 7.1887 vs exp. 7.3435 (prev. 7.1879).

Fixed Income

USTs are contained into a front-loaded US session on account of the Federal Holiday for Carter on Thursday. As such, we get ADP, Jobless Claims, FOMC Minutes and 30yr supply in today’s session. Into those events, USTs trade within a slim 108-04 to 108-09+ band which is entirely and comfortably within Tuesday’s 108-01 to 108-20 parameters. Ahead, US ADP, Jobless Claims ahead of speak from Fed’s Waller and then the release of the FOMC Minutes. Additionally, we await a 30yr supply which follows a tepid 3yr tap on Monday and a relatively soft 10yr outing last night.

Bunds are similarly contained but with a slightly larger 131.90-132.14 range thus far with modest but ultimately fleeting action spurred by data this morning. A particularly soft Industrial Orders release and a mixed but largely weak Retail Sales report out of Germany sparked upside in Bunds early doors, to a retest of the above overnight peak; however, the move proved fleeting given large-order caveats to the Industrial Orders series. A 2035 outing had limited impact on Bunds.

BTPs are the relative outperformers today after lagging yesterday on the announcement of two new syndications; this morning, we have seen marketing commence for a new 10yr BTP and a new 20yr Green BTP with orders in excess of EUR 125bln and EUR 110bln respectively.

Gilts traded off highs in a 91.29-58 range ahead of a new 2030 auction; an outing which was mixed, with the b/c printing bang on 3.0 whilst the avg. yield is relatively high and a modestly wider tail, but ultimately had little impact on Gilts.

UK sells GBP 4.25bln 4.375% 2030 Gilt Auction: b/c 3.0x, average yield 4.490% & tail 0.5bps.

Germany sells EUR 3.781bln vs exp. EUR 5bln 2.00% 2035 Bund Auction: b/c 2.1x, average yield 2.51% & retention 24.38%

Orders for Italy’s new 10yr BTP bond over EUR 125bln, for 20yr Green BTP over EUR 110bln, via Reuters citing leads; spread for 10yr +7bps, for 20yr +5bps.

Commodities

Firmer trade in the crude complex despite the stronger Dollar, and extended on the prior day’s gains with upside seen after the latest private sector inventory data showed a larger-than-expected draw in headline crude. The complex saw additional upside in the European morning after reports that Ukraine had hit a Russian oil depot which served a military airfield, according to Ukraine’s Presidential Advisor. Brent Mar is currently just off highs in a USD 77.23-77.89/bbl parameter.

Mixed trade across precious metals with spot gold and silver firmer whilst palladium trades flat/subdued. Spot gold trades in a current USD 2,645.40-2,654.90/oz range.

Copper is on a firmer footing despite the stronger Dollar after the red metal lacked firm direction amid the mixed risk appetite in Asia and the subdued mood in China. 3M LME copper currently resides in a USD 8,983.00-9,056.00/t range.

Qatar set February Marine Crude OSP at Oman/Dubai + USD 0.45/bbl and Land Crude OSP at Oman/Dubai + USD 0.30/bbl.

Shell (SHEL LN) Cuts Q4 Integrated Gas Production 880-820k boepd (prev. guided 900-960k boepd), LNG Volumes 6.8-7.2Mt (prev. guided 6.9-7.5Mt); optimisation results are exp. to be significantly lower than Q3’24. Guides Q4 Upstream: Production 1.79-1.89mln boepd, Underlying Opex USD 2.2-2.8bln. Guides Q4 Chemicals and Products: Refining Utilisation 74-78%.

India has cut November gold imports by USD 5bln in the biggest revision, via Reuters citing sources; revised to USD 9.84bln (prev. estimated 14.86bln)