GOLD CLOSED UP $24.35 TO $2693.90

SILVER CLOSED UP 79 CENTS TO $30.60

Gold ACCESS CLOSED $2696.30

Silver ACCESS CLOSED: $03.72

Bitcoin morning price:$97,167 UP 626 DOLLARS.

Bitcoin: afternoon price: $99581 up 3040 DOLLARS

Platinum price closing DOWN $0.55 TO $935.75

Palladium price; UP $20.15 TO $963.25

END

*CANADIAN GOLD: $3863.99 UP 30.60 CDN dollars per oz( * NEW ALL TIME HIGH 3,884.98 CDN DOLLARS PER OZ//JAN 10 2025)

*BRITISH GOLD: 2202.48 UP 11.53 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2,202.84 BRITISH POUNDS/OZ) JAN 10/2025

*EURO GOLD: 2,619.40 UP 23.47 Euros per oz //* (ALL TIME CLOSING HIGH: 2,628.05 EUROS PER OZ/JAN 10 //.2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE

EXCHANGE: COMEX

CONTRACT: JANUARY 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,677.500000000 USD

INTENT DATE: 01/14/2025 DELIVERY DATE: 01/16/2025

FIRM ORG FIRM NAME ISSUED STOPPED

072 H GOLDMAN 2

118 C MACQUARIE FUT 666 1

118 H MACQUARIE FUT 154

190 H BMO CAPITAL 162

323 C HSBC 301

363 C WELLS FARGO SEC 1

363 H WELLS FARGO SEC 60

435 H SCOTIA CAPITAL 70

624 H BOFA SECURITIES 256

657 C MORGAN STANLEY 2

661 C JP MORGAN 762

686 C STONEX FINANCIA 6 14

730 C PTG DIVISION SG 2

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 6 21

905 C ADM 102 1

TOTAL: 1,295 1,295

MONTH TO DATE: 9,109

JPMorgan stopped 762/1295

GOLD: NUMBER OF NOTICES FILED FOR JANUARY/2024. CONTRACT: 1295 NOTICES FOR 129,500 OZ 4.028 TONNES

total notices so far: 9109 contracts for 910,900 Oz (28.333 tonnes)

FOR JANUARY

SILVER NOTICES: 32 NOTICE(S) FILED FOR 160,000 OZ/

total number of notices filed so far this month : 1840 for 9.20 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $24.35 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD

INVENTORY RESTS AT 872.52 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.79 AT THE SLV: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.646 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 464.863 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 324 CONTRACTS TO 150,364 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS FAIR SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL GAIN OF $0,15 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. WE HAD A HUMONGOUS GAIN OF 1009 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR SMALL GAIN IN PRICE//TUESDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON TUESDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 2 WEEKS WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TO QUELL MASSIVE DERIVATIVE LOSSES BY OUR BULLION BANKS AND TO STOP THE RISE IN SILVER’S PRICE. THEY FAILED WITH //TUESDAY PRICING WITH ZERO LONGS BEING KNOCKED OFF. DERIVATIVE LOSSES CONTINUE TO MOUNT. WE HAD CONSIDERABLE T.A.S. LIQUIDATION TUESDAY COUPLED WITH ANOTHER NEW MASSIVE T.A.S. ISSUANCE OF 1418 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS RED THAT WE ARE GOING TO HAVE ANOTHER RAID SHORTLY. WE HAD A STRONG 685 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR ILLUSTRIOUS HUMONGOUS 1418 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 1021 CONTRACTS ON OUR TWO EXCHANGES WITH OUR SMALLISH GAIN IN PRICE. WE HAD HUGE TAS LIQUIDATION THROUGHOUT TUESDAY’S COMEX SESSION

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH YESTERDAY’S FAILED RAID.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: A HUMONGOUS 1418 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS ESPECIALLY WITH LAST YESTERDAY’S RAID (JAN 13). IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.15 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE HAD A STRONG GAIN IN OUR TWO EXCHANGES OF 1021 CONTRACTS.

WE HAD A 685 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 8.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 160,000 OZ QUEUE JUMP//NEW STANDING RISES TO 9.650 MILLION OZ

// STANDING FOR SILVER//JAN 9.650 MILLION OZ

WE HAD:

/ FAIR SIZED COMEX OI GAIN +// A STRONG 685 SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1418 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 12 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN

TOTAL CONTRACTS for 9 DAYS, total 6139 contracts: OR 30.695 MILLION OZ (682 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 30.695 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 30.695 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 324 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A 685 EFP ISSUANCE CONTRACTS: 685 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 8.110 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S QUEUE JUMP OF 160,000 OZ

//NEW TOTAL STANDING FOR JAN REMAINS AT 9.650 MILLION OZ

WE HAVE 1. A HUGE SIZED GAIN OF 1021 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR SMALLISH GAIN IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS 1418 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION BUT THEY STILL NEED THESE ISSUANCE FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON TUESSSDAY WITH THE SMALL GAIN IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE TUESDAY NIGHT (1418) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE, NO DOUBT PRIOR TO TRUMP’S INAUGURATION.

WE HAD 32 NOTICE(S) FILED TODAY FOR 160,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A MEGA HUMONGOUS SIZED 21,578 OI CONTRACTS TO 526,788 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A SMALL SIZED 321 CONTRACTS//

WE HAD A MEGA HUMONGOUS SIZED INCREASE IN COMEX OI (21,578 CONTRACTS) OCCURRED DESPITE OUR SMALL GAIN OF $9.40 IN PRICE TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 10.1331 TONNES FOLLOWED BY TODAY’S MONSTER QUEUE JUMP OF 638 CONTRACTS OR 63,800 OZ TO WHICH WE ADD THE FIRST ISSUANCE FOR EXCHANGE FOR RISK CONTRACTS TOTALLING 1700 CONTRACTS OR 170,000 OZ (5.28775 TONNES) ISSUED JAN 6/2025 TO WHICH WE ADD JAN 8 EXCHANGE FOR RISK ISSUANCE OF 150 CONTRACTS OR 15,000 OZ OR .4665 TONNES . NEW STANDING FOR JAN ADVANCES TO 30.236 TONNES (NORMAL DELIVERY) + 5.753 TONNES EX FOR RISK/PRIOR EQUALS 35.989 TONNES

/NEW STANDING 35.989 TONNES

/ ALL OF THIS HAPPENED WITH OUR $9.40 GAIN IN PRICE WITH RESPECT TO TUESDAY’S COMEX ///. WE HAD A MEGA MEGA HUMONGOUS GAIN OF 26,844 OI CONTRACTS (83.50 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE VIOLENT ACTION AT THE COMEX WITH RESPECT TO QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 5266 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 526,788

IN ESSENCE WE HAVE AMEGA MEGA HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 26,844 CONTRACTS WITH 21,578 CONTRACTS INCREASED AT THE COMEX// AND A VERY STRONG SIZED 5266 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 26,844 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A MEGA HUMONGOUS SIZED AND CRIMINAL 39,913 CONTRACTS ISSUED.(THIS IS THE 5TH CONSECUTIVE 30,000+ T.A.S CONTRACT ISSUED BY THE CME.) WE HAD A HUGE LIQUIDATION OF T.A.S CONTRACTS WITH OUR SMALL GAIN IN PRICE TUESDAY. MORE MONSTER ISSUANCE OF T.A.S IS NEEDED FOR REPLENISHMENT TO CARRY OUT ITS PRICE CONTAINMENT STRATEGY IN FUTURE TRADING (FUTURE RAIDS). WE WILL NO DOUBT SEE ANOTHER RAID ORCHESTRATED BY THE CROOKS PRIOR TO TRUMP’S INAUGURATION.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A VERY STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5266 CONTRACTS) ACCOMPANYING THE HUGE SIZED INCREASE IN COMEX OI OF 21,578 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 26.844 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JAN 10.1331 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 638 CONTRACTS OR 63800 OZ (1.984 TONNES) TO WHICH WE ADD THAT CRAZY “DELIVERY” CALLED EXCHANGE FOR RISK JAN 8 OF .4665 TONNES TOGETHER WITH OUR EARLIER EX FOR RISK OF 5.2867 TONNES//// NEW STANDING FOR JAN ADVANCES TO:

30.236 TONNES NORMAL DELIVERY +

5.753 TONNES OF EXCHANGE FOR RISK ON OUR TWO OCCASIONS IN JANUARY (6TH AND 8TH )

EQUALS: 35.989 TONNES

//NEW STANDING JAN: 35.989 TONNES

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE TUESDAY WITH ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WE HAD A 1) $9.40 PRICE GAIN, AND 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A TOTAL GAIN OF 26,844 CONTRACTS ON OUR TWO EXCHANGES. ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) MEGA HUMONGOUS SIZED COMEX OPEN INTEREST INCREASE 5) VERY STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///MEGA HUMONGOUS T.A.S. ISSUANCE: 39.913 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

TOTAL EFP CONTRACTS ISSUED: 38,005 CONTRACTS OF 3,800,500 OZ OR 118.22 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 4092 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 118.22 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 118.22 DIVIDED BY 3550 x 100% TONNES = 3.37% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 118.22 TONNES (ISSUANCE WILL BE PRETTY SMALL THIS MONTH AND MUCH LOWER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR SIZED 324 CONTRACTS OI TO 150,376 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.20233EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 685 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 685 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 336 CONTRACTS AND ADD TO THE 685 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1021 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS A HUGE 5.105 MILLION OZ OCCURRED WITH OUR SMALL $0.15 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS WEDNESDAY MORNING TUESDAY NIGHT

SHANGHAI CLOSED DOWN 13.82 PTS OR 0.43%

//Hang Seng CLOSED UP 66.29 PTS OR 0.34%

// Nikkei CLOSED DOWN 29.72 OR 0.08%//Australia’s all ordinaries CLOSED DOWN 0.18%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.3316 CHINESE YUAN OFFSHORE CLOSED UP TO 7.3427// Oil DOWN TO 78,06 dollars per barrel for WTI and BRENT DOWN AT 80.18 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING A

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

ASIA TRADING WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 80.19 PTS OR 2.54%

//Hang Seng CLOSED UP 345.64 PTS OR 1.83%

// Nikkei CLOSED DOWN 716.10 O 1.83%//Australia’s all ordinaries CLOSED UP 0.47%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.3312 CHINESE YUAN OFFSHORE CLOSED UP TO 7.3491// Oil DOWN TO 78,54 dollars per barrel for WTI and BRENT DOWN AT 80.68 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING A

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A MEGA HUMONGOUS SIZED 21,578 CONTRACTS TO 526,467 DESPITE OUR RELATIVELY SMALL GAIN IN PRICE OF $9.40 WITH RESPECT TO WEDNESDAY’S TRADING. WE LOST ZERO NET LONGS WITH OUR PRICE GAIN FOR GOLD AS WE HAD ALSO, AS YOU WILL SEE BELOW, A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (5266) . THE CME ISSUED ZERO EXCHANGE FOR RISK THIS EARLY WEDNESDAY MORNING

THUS IN TOTAL WE HAD A MEGA MEGA HUMONGOUS GAIN ON OUR TWO EXCHANGES OF 26,844 CONTRACTS DESPITE OUR SMALLISH GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON MONDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED TRADING AS THEY ABSORBED EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE PAST WEEK WITH OUR MAMMOTH T.A.S. ISSUANCES. WE HAD A HUGE T.A.S. LIQUIDATION DURING THE WEDNESDAY COMEX SESSION AS WE HAD AN ATTEMPTED FAILED RAID ON PRICE. WE HAD ANOTHER HUMONGOUS 39,913 T.A.S. ISSUANCE (WEDNESDAY MORNING).THIS IS THE 5TH CONSECUTIVE 30,000 PLUS ISSUANCE. THIS SHOULD END THEIR MEGA ISSUANCE AS I HAVE NEVER SEEN 6 CONSECUTIVE MEGA ISSUANCES BEFORE. WE HOWEVER MUST WAIT FOR TOMORROW’S DATA.

THE FED IS THE MAJOR SHORT OF AROUND 82+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, 202, 203 , 204 AND 205 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP IS COMING INTO OFFICE IN 6 TRADING DAYS. TRUMP WOULD PROBABLY BE FURIOUS WITH THE FED IF IT FOUND OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING THE LAST WEEK OF DECEMBER AND THEN THIS WEEK, IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD. AS YOU WILL SEE BELOW, WE HAD ANOTHER HUGE QUEUE JUMPING SESSION TODAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF JANUARY.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 5266 EFP CONTRACTS WERE ISSUED: : /FEB 5266 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5266 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A MEGA MEGA HUMONGOUS SIZED TOTAL OF 26,844 CONTRACTS IN THAT 5266 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUMONGOUS SIZED GAIN OF 21,578 COMEX CONTRACTS..AND THIS HUGE GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR SMALLISH GAIN IN PRICE OF $9.40 TUESDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A MEGA HUMONGOUS SIZED SIZED 39,913 CONTRACTS, AS THE FED(FRBNY) CALLED FOR THE FED-MOBILE AS THESE WAS USED TO ORCHESTRATE A MASSIVE RAID BEFORE THE TRUMP-MOBILE TAKES OFFICE.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). THE FED WAS EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED NOTHING AS NOBODY LEFT OUR GOLD METAL ARENA.

MECHANICS OF T.A.S CONTRACTS

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON DEC. 27, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE DECEMBER’S OPTIONS EXPIRY TRADING. T.A.S. LIQUIDATION WAS EVIDENT IN JAN 6 COMEX TRADING//RAID AND THEN AGAIN YESTERDAY’S FAILED ATTEMPT AT A RAID ON GOLD PRICE. HOWEVER NOT TO BE UNDONE, THE CROOKS ISSUED ANOTHER MONSTER 39,913 T.A.S CONTRACTS. THIS IS THE FIFTH CONSECUTIVE 30,000+ CONTRACT ISSUANCE. THIS T.A.S. ISSUANCE WILL BE USED IN OUR NEXT RAID IN GOLD TRADING NO DOUBT BEFORE TRUMP’S INAUGURATION AS THE FED MUST REDUCE ITS MASSIVE PHYSICAL GOLD SHORT OF 82 TONNES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION WITH RESPECT TO TUESDAY’S COMEX TRADING. (WHICH DISTORTS OPEN INTEREST)

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JAN (35.989 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE JAN DELIVERY MONTH.

JANUARY: 10.1331 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

January 2025: 30.236 TONNES + 5.753 EX FOR RISK/PRIOR = 35.969 TONNES

COMEX GOLD TRADING

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $9.40/)//AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A MEGA HUMONGOUS GAIN IN OUR TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION TUESDAY BUT TO NO AVAIL. THUS WE HAVE ANOTHER MONSTER ISSUANCE OF T.A.S. OF 39,913 CONTRACTS TRYING TO QUELL GOLD’S RISE AND HUGE COMEX/OTC DERIVATIVE LOSSES.

THE CROOKS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING.

EXCHANGE FOR RISK EXPLANATION/DECEMBER TRADING AND NOW JANUARY!!

46 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 14.6836 TONNES. THE COMEX IS TOTALLY SHATTERED TO PIECES.

EXCHANGE FOR RISK THIS JANUARY MONTH

WE NOW BEGIN OUR NEW MONTH OF JANUARY AND LO AND BEHOLD, THE CROOKS ISSUED ANOTHER MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THEN TO MY HORROR, THEY ISSUED THEIR SECOND EXCHANGE FOR RISK ON JAN 8, TOTALLING 150 CONTRACTS FOR 15000 OZ OR .4665 TONNES. THIS TONNAGE WILL BE ADDED TO THE FIRST ISSUANCE. THUS TOTAL EXCHANGE FOR RISK ISSUANCE FOR JANUARY: 5.7533 TONNES. THANKFULLY THEY ISSUED 0 EXCHANGE FOR RISK LAST NIGHT.

TOTAL DELIVERIES JANUARY TRADING

WE HAVE GAINED A MONSTER TOTAL OF 83.50 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN (10.133TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S MONSTER QUEUE JUMP OF 638 CONTRACTS OR 63,800 OZ (1.984 TONNES) TO WHICH WE MUST ADD OUR 5.7533 TONNES OF EXCHANGE FOR RISK ISSUANCE WHERE THE BUYERS ASSUMES THE RISK FOR DELIVERY.(ISSUED JAN 6/2025 AND JAN 8).. THIS IS ,OF COURSE, AGAINST ALL RULES OF THE COMEX AS IT IS MEANT TO DECEIVE US. IT IS TOTALLY INSANE FOR A BUYER TO ASSUME RISK OF DELIVERY.

NEW STANDING FOR JAN: 30.236 TONNES + 5.753 TONNES EX FOR RISK/PRIOR = 35.236 TONNES (WHICH IS HUGE FOR OUR VERY NON ACTIVE DELIVERY MONTH) A NORMAL AMOUNT STANDING FOR A JANUARY IN EARLIER TIMES HAS BEEN GENERALLY AROUND 1/4 TONNE OF GOLD. HOWEVER THESE PAST 4 YEARS QUEUE JUMPING HAS BEEN VERY PRONOUNCED AND THUS STANDING INCREASES DRAMATICALLY.

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $9.40

WE HAD 321 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 26,844 CONTRACTS OR 2,684,400 OZ (83.50 TONNES)

confirmed volume WEDNESDAY 262m816 contracts: fair ////nobody wishes to play with the crooks

//speculators have left the gold arena

END

/ /// THE JAN 2025 GOLD CONTRACT

JAN 15

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil . 482.265 oz JPMorgan 15 kilobars |

| Deposit to the Dealer Inventory in oz | I) Into Brinks dealer; 53,049.150 oz (1650 kilobars) |

| Deposits to the Customer Inventory, in oz | i)330,356.525 JPM ii) 96,453.000 oz (LOOMIS) 3000 kilobars iii) 196,728.113 of Manfra total 623,569.789 oz 19.39 tonnes customer total deliver and customer deposit: 21.04 tonnes |

| No of oz served (contracts) today | 1295 notice(s) 129500 OZ 4.028 TONNES |

| No of oz to be served (notices) | 612 contracts 61200 OZ 1.903 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9109 notices 910900 oz 28.333TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 1

i) Into Brinks dealer: 53,049.150 oz (1650 kilobars)

total dealer deposits: 53,049.150 oz

we have 3 customer deposits

i)330,356.525 JPM

ii) 96,453.000 oz (LOOMIS)

3000 kilobars

iii) 196,728.113 of Manfra

total 623,569.789 oz

19.39 tonnes customer

total deliver and customer deposit: 21.04 tonnes

withdrawals: 1

482.265 oz

JPMorgan 15 kilobars

adjustments:3/customer to dealer

i) Out of Brinks 32,247.453 oz (1003 kilobars)

ii) Out of JPMorgan 160,690..698 oz(4998 kilobars)

iii) Out of Manfra: 20,617.387 oz

total customer to dealer: 6.64 tonnes

thus basically what comes into eligible is transferred to dealer accounts and then out.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JAN.

For the front month of JAN: we have an oi of 1907 contracts having GAINED 273 contracts. We had a strong 365 contract issuance on TUESDAY. Thus ANOTHER HUGE QUEUE JUMP (GAIN) of 638 contracts on our two exchanges. (63800 oz or 1.984 tonnes). THIS IS CENTRAL BANKERS STANDING FOR PHYSICAL GOLD WITH LONDON VAULTS RUNNING OUT OF PHYSICAL TO SUPPLY THEM.

FEBRUARY LOST 5749 CONTRACTS TO 282,448 AS IT BEGINS ITS COUNTDOWN BEFORE FIRST DAY NOTICE (JAN 31.2025) EXPECT A WOPPER OF A FEB DELIVERY MONTH.

MARCH HAD A GAIN OF 1991 CONTRACTS UP TO 6515

APRIL HAD A GAIN OF 20,847 CONTRACTS UP TO 163,926 CONTRACTS

We had 1295 contracts filed for today representing 129,500 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1295 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 762 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JAN /2025. contract month, we take the total number of notices filed so far for the month (9109 x 100 oz ) to which we add the difference between the open interest for the front month of JAN(1907 CONTRACTS) minus the number of notices served upon today (1295 x 100 oz per contract) equals 972,100 OZ OR 30.236 TONNES. to which we add those criminal exchange for risk issuance of .4665 TONNES (JAN 8) AND 5.28775 tonnes/JAN 6//TOTAL EXCHANGE FOR RISK = 5.753 TONNES. THUS NEW STANDING FOR GOLD AT THE COMEX FOR JAN IS 30.236 TONNES PLUS 5.753 TONNES EX FOR RISK = 35.989 TONNES

thus the INITIAL standings for gold for the JAN contract month: No of notices filed so far (9109 x 100 oz +we add the difference for front month of JAN (1907 OI} minus the number of notices served upon today (1295 x 100 oz which equals 972,100 oz (30.236 TONNES) + 5.753 tonnes ex for risk ( JAN 6 AND 8TH) = 35.989 tonnes

TOTAL COMEX GOLD STANDING FOR JAN.: 35.989 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,137,828.584 oz 66.49 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 23,274,190.439 OZ

TOTAL REGISTERED GOLD 10,589,412.641 or 329 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 12,684,777.798 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,451,584 oz (REG GOLD- PLEDGED GOLD)= 262.879 tonnes //

JPMorgan enhanced inventory is 3.511 million oz

END

SILVER/COMEX

JAN 15. 2025

INITIAL

//2025// THE JAN 2025 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | a) Out of Delaware: 1972.400 oz ii) Out of HSBC 50,347.65 total 52,320.05 oz . |

| Deposits to the Dealer Inventory | 101,924.54 oz Brinks |

| Deposits to the Customer Inventory | i) Into ASHAI 611,563.100 oz ii) Into HSBC: 50,580.255 oz iii) Into Delaware 977.40 oz total deposit 1,160,169.095 oz |

| No of oz served today (contracts) | 32 CONTRACT(S) (160,000 OZ) |

| No of oz to be served (notices) | 90 contracts (0.450 MILLION oz) |

| Total monthly oz silver served (contracts) | 1840 Contracts (9.200 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

deposits:3

i) Into ASHAI 611,563.100 oz

ii) Into HSBC: 50,580.255 oz

iii) Into Delaware 977.40 oz

total deposit 1,160,169.095 oz

WITHDRAWALS

a) Out of Delaware: 1972.400 oz

ii) Out of HSBC 50,347.65

total 52,320.05 oz

total withdrawal: 52,320.05 oz

ADJUSTMENT 1 customer to dealer CNT

i) 49,830.00 oz

JPMorgan has a total silver weight: 135.536million oz/328.799million or 41.05%

TOTAL REGISTERED SILVER: 71.804 MILLION OZ//.TOTAL REG + ELIGIBLE. 328.799 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF JAN /2024 OI: 122 OPEN INTEREST FOR A LOSS OF 0 CONTRACT(S).

WE HAD A 32 CONTRACT ISSUANCE ON TUESDAY. THUS WE GAINED 32 CONTRACTS, THAT IS WE HAD A 32 CONTRACT QUEUE JUMP FOR 160,000 OZ

FEBRUARY SAW A GAIN 0F 14 CONTRACTS TO STAND AT 994

MARCH SAW A LOSS OF 956 CONTRACTS DOWN TO 114,416

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 32 for 160,000 oz

CONFIRMED volume; ON TUESDAY 47,517 poor//

To calculate the number of silver ounces that will stand for delivery in JAN we take the total number of notices filed for the month so far at 1840x 5,000 oz = 9.200 MILLION oz

to which we add the difference between the open interest for the front month of JAN (122) and the number of notices served upon today (32)x (5000 oz)

Thus the standings for silver for the JAN 2025 contract month: 1840 Notices served so far) x 5000 oz + OI for the front month of JAN(122) minus number of notices served upon today (32)x 5000 oz equals silver standing for the JAN contract month equating to 9.650 MILLION OZ.

New total standing: 9.650 million oz.

There are 71.804 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

JAN 15 WITH GOLD UP $24.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 872.52 TONNES

JAN 14 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 874.53 TONNES

JAN 13 WITH GOLD DOWN $27.75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A DEPOSIT OF 5.74 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 876.82 TONNES

JAN 10 WITH GOLD UP $17.80 ON THE DAY; NO CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 9 WITH GOLD UP $13.85 ON THE DAY; NO CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 8 WITH GOLD UP $5.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 7 WITH GOLD DOWN $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 6 WITH GOLD DOWN $4.90 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 3 WITH GOLD DOWN $14.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 2 WITH GOLD UP $29.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 31 WITH GOLD UP $20.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 30 WITH GOLD DOWN $11.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.28 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.52 TONNES

DEC 27 WITH GOLD DOWN $17.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.80 TONNES

DEC 26 WITH GOLD UP $17.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: : ///INVENTORY RESTS AT 873.95 TONNES

DEC 24 WITH GOLD UP $6.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES OF GOLD OUT OF THE GLD. / // : .///INVENTORY RESTS AT 873.95 TONNES

DEC 23 WITH GOLD DOWN $13,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 16.66 TONNES OF GOLD VAPOUR GOLD INTO THE GLD. / // : .///INVENTORY RESTS AT 877.40 TONNES

DEC 20 WITH GOLD UP $29,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 860.74 TONNES

DEC 19 WITH GOLD DOWN $45.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF .29 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 18 WITH GOLD DOWN $8.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 17 WITH GOLD DOWN $6.85 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.23 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 16 WITH GOLD DOWN $2.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.70 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 13 WITH GOLD DOWN $24.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.78 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 868.60 TONNES

DEC 12 WITH GOLD DOWN $34.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.59 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 873.38 TONNES

DEC 11 WITH GOLD UP $29.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 9 WITH GOLD UP $31.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD. // : .///INVENTORY RESTS AT 871.94 TONNES

GLD INVENTORY: 872,52 TONNES, TONIGHTS TOTAL

SILVER

JAN 15 WITH SILVER UP $0.79 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.745 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 464.863 MILLION OZ

JAN 14 WITH SILVER UP $0.15 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.228 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 460.218 MILLION OZ

JAN 13 WITH SILVER DOWN $0.69 //NO CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.637 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 459.990 MILLION OZ

JAN 10 WITH SILVER UP $0.19 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 459,353 MILLION OZ

JAN 9 WITH SILVER UP $0.08 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 459,353 MILLION OZ

JAN 8 WITH SILVER DOWN $0.01 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 7 WITH SILVER UP 48 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 6 WITH SILVER UP 38 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 3 WITH SILVER UP 17 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 2 WITH SILVER UP 45 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.616 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 462.128 MILLION OZ

DEC 31 WITH SILVER DOWN 14 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 30 WITH SILVER DOWN 39 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: // A WITHDRAWAL OF 1.13 MILLION OZ FROM THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 27 WITH SILVER DOWN 24 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY AT SLV RESTS AT 461.651 MILLION OZ

DEC 24 WITH SILVER UP 2 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 23 WITH SILVER UP 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 6.15 MILLION OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 20 WITH SILVER UP 43 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 183,000 OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 457.597 MILLION OZ

DEC 19 WITH SILVER DOWN 25 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV///// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 18 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 17 WITH SILVER DOWN 12 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.456 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 16 WITH SILVER DOWN 0 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 4.84 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 13 WITH SILVER DOWN 46 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .536 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 462.892 MILLION OZ

DEC 12 WITH SILVER DOWN 94 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 5.787 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 463.428 MILLION OZ

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 10 WITH SILVER DOWN 8 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.868 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 471.812 MILLION OZ

DEC 9 WITH SILVER UP $0.91 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.367 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 473.680 MILLION OZ

CLOSING INVENTORY 460.218 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

END

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ALASDAIR MACLEOD

JOHN RUBINO

3. CHRIS POWELL AND GATA DISPATCHES

NONSENSE! Besides the bankers have hypothecated our 260 million oz by 100 fold.

It will never happen

(New York Sun)

New York Sun: The coming raid on Fort Knox

Submitted by admin on Tue, 2025-01-14 20:12 Section: Daily Dispatches

From the New York Sun

Tuesday, January 14, 2025

The news today is that the incoming Trump administration is hearing talk about selling the gold at Fort Knox. Our advice is to get on the phone right now and call Edwin Vieira, Jr., author of the definitive volume “Pieces of Eight.” That’s what we did last time we heard talk — it was in Congress — about selling the gold at Fort Knox. When he came to the phone we asked him, “Ed, do you think America should sell the gold in Fort Knox?”

“Don’t use the word ‘sell,'” Mr. Vieira exploded over the blower.

He was so alarmed we almost dropped the phone. Then we asked what was the problem.

He was so alarmed we almost dropped the phone. Then we asked what was the problem.

“You don’t sell gold,” Mr. Vieira said “You spend it.”

We got the point, but Mr. Vieira pressed it anyhow. “Don’t you see,” he boomed. “Gold is the money.”

The talk today of selling gold is part of a proposal to rectify the imbalances in global trade, like China’s record-high surplus. It is part of the president-elect’s America First policy. Among the more creative suggestions being floated was spotted by our Ira Stoll at The Editors. The idea, put forward some weeks ago by Trump’s pick to head the Council of Economic Advisers, Stephen Miran, is to deploy America’s gold reserves to devalue the dollar.

Gold reserves tend to bolster the value of currencies. Yet Mr. Miran sees selling gold — of which Uncle Sam holds some 260 million ounces — as a means to weaken, not strengthen, the dollar. “While many analysts believe there are no tools available to unilaterally address currency misvaluation, that is not true,” he writes. One way to do it, Mr. Miran says, is to “accumulate foreign exchange reserves,” boosting the value of other nations’ fiat currencies.

Here’s where gold factors in. “The Gold Reserve Act,” he writes, allows the Treasury “Secretary to sell gold” in the way “the Secretary considers most advantageous to the public interest.” Mr. Miran sees this as “providing additional potential funds for building foreign exchange reserves.” Note, though, the emphasis on the verb “sell,” the use of which reflects a misconception about the nature of money.

This point was marked in 2013 by a Sun editorial headlined “Speaking of Money.” The editorial was prompted by talk in the press about the “value” of gold. “To the ears of a copy editor of the Sun, this is like the screech of chalk pushed the wrong way on a blackboard,” we noted. That’s because, in the Sun’s stylebook, “the value of gold is, in practical terms, constant.” More noteworthy is “the value of the dollar. That’s what does all the changing.”

So the Sun does not refer to “the price of gold” but the “value of the dollar,” which, incidentally, stands at less than a 2,600th of an ounce in today’s trading. Gold, not the dollar, “is the measure of value.” Plus, too, when it comes to gold, the Sun eschews using the verb “to sell.” That’s in contrast to the idea that “gold is a ‘commodity’ or an ‘asset,'” we noted. “This fits fine in an era of fiat money.” Hence Mr. Vieira’s brilliant point.

Which brings us back to Mr. Miran’s proposal to devalue the dollar by “selling” gold. He concedes it “could be politically costly,” even if it would “result in income” for Uncle Sam. Mr. Stoll reckons that the “problem” with Mr. Miran’s idea is that even if politicians “try to fix prices, there are free-market signals, such as the price of the dollar against gold, Bitcoin, groceries, or real estate, that eventually provide a true indication of a dollar’s value.”

Mr. Miran sees “a reduction in the value of the dollar” as helping “create manufacturing jobs in America” as it “reallocates aggregate demand from the rest of the world to the U.S.” Mr. Stoll replies that if Americans “get the idea that their dollars will be worth less” due to Trump’s moves, “there’s a risk that they will move money out of dollars and into other assets.” Inflation would ensue. Mr. Stoll calls it “a costly policy, in whatever units it is measured.”

* * *

END

ANDREW MAGUIRE A MUST MUST VIEW…YOUTUBE/KINESIS LIVE FROM THE VAULT 205

/LIVE FROM THE VAULT 205

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY

END

end

6 CRYPTOCURRENCY NEWS

Italy’s Largest Bank Makes Its First Bitcoin Purchase In $1 Million “Test”

Wednesday, Jan 15, 2025 – 02:45 AM

Italy’s biggest bank, Intesa Sanpaolo, has made history by becoming the first Italian financial institution to buy 11 bitcoins for a “test” purchase worth $1 million.

Initially a widespread rumor, Bloomberg has confirmed that Italy’s largest banking giant has indeed dipped its toes in Bitcoin. According to an internal memo, the financial institution completed its first proprietary Bitcoin trade, investing the funds into the world’s largest digital currency.

“It’s very small amounts, considering we have 100 billion euros in our securities portfolio,” Intesa CEO Carlo Messina told reporters on the sidelines of an event in Milan on Tuesday. “It’s an experiment, a test.”

Intesa set up a proprietary trading desk for digital assets in 2023 and started handling spot trades with cryptos last year.

The news first surfaced when the bank’s employees leaked an internal email on the image-sharing platform 4Chan. Following the leak, Niccolo Bardoscia, Intesa Sanpaolo’s head of digital assets trading and investment, officially confirmed the acquisition in an email to the media, revealing that the bank now holds 11 BTC.

While Bardoscia confirmed the purchase, the executive did not reveal exactly why the bank had acquired BTC. Therefore, it is still unclear if the purchase was to diversify Intesa Sanpaolo’s investment portfolio or if it was a pilot to offer crypto services, according to CryptoRank.

The acquisition is not the bank’s first foray into blockchain. In July last year, Intesa Sanpaolo pioneered a $25.7 million digital bond issuance on the Polygon network in collaboration with state-owned bank Cassa Depositi e Prestiti SpA. In addition, Intesa Sanpaolo broadened its crypto desk to allow spot trading. Before then, it only offered clients crypto options, futures, and exchange-traded funds (ETFs).

Intesa Sanpaolo’s purchase came as Europe eased regulations. The Markets in Crypto Assets (MiCA) regulatory guideline came into full effect in December, a milestone that’s expected to pave the way for more digital-asset adoption among financial companies.

While Intesa is currently only prop trading — buying and selling using its own balance sheet rather than on behalf of clients — the crypto desk’s activities fit with the bank’s broader blockchain projects, and it may be a stepping stone for eventually trading digital assets for institutional customers.

“We won’t become a Bitcoin provider but we need to know how to do so if our bigger clients ask us to,” Messina told reporters on Tuesday.

Intesa carried out the Bitcoin purchase through Boerse Stuttgart Digital’s institutional trading platform, a spokesperson from the German exchange group said in a statement.

After rallying in the wake of Donald Trump’s US election win in early November, Bitcoin and other cryptocurrencies have had a shaky start to the year, hurt by concerns that persistent inflation will curtail the Federal Reserve’s monetary policy easing.

Bitcoin briefly slid below $90,000 on Monday — a drop of almost 5% from the start of 2025 — before a rebound that left it slightly up for January. The largest cryptocurrency soared to a record high of $108,316 last month.

This BTC acquisition signals a shift in sentiment within Italy. As the country’s largest bank leads the way, other financial institutions may follow suit, potentially accelerating adoption.

The move stands out in Italy, where the central bank governor, Fabio Panetta, has consistently cautioned against digital assets like Bitcoin and Ethereum, describing them as “unsecured.”

That said, the bank has a long way to go to catch up with its US peers: BlackRock, the world’s largest asset manager, has amassed $51 billion in assets in the spot Bitcoin ETF it launched a year ago, and is pushing to have its money-market digital coin more widely used as collateral for crypto derivatives trades. JPMorgan is preparing to offer instant settlement for foreign-exchange conversions between the dollar and the euro through its blockchain platform.

Meanwhile, Bitcoin’s value continues to surge, with optimism growing about easing regulatory hurdles under incoming U.S. President Donald Trump. Some analysts expect it to more than double in value by the end of this year.

END

ASIA TRADING WEDNESDAY MORNING TUESDAY NIGHT

SHANGHAI CLOSED DOWN 13.82 PTS OR 0.43%

//Hang Seng CLOSED UP 66.29 PTS OR 0.34%

// Nikkei CLOSED DOWN 29.72 OR 0.08%//Australia’s all ordinaries CLOSED DOWN 0.18%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.3316 CHINESE YUAN OFFSHORE CLOSED UP TO 7.3427// Oil DOWN TO 78,06 dollars per barrel for WTI and BRENT DOWN AT 80.18 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING A

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.3316

OFFSHORE YUAN: DOWN TO 7.3427

SHANGHAI CLOSED CLOSED DOWN 13.82 PTS OR 0.43%

HANG SENG CLOSED CLOSED UP 66.29 PTS OR 0.34%

2. Nikkei closed DOWN 29.72 OR 0.08%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 108.95 EURO FALLS TO 1.0301 DOWN 5 BASIS PTS HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: RISES TO. +1.251 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.99…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5935 Italian 10 Yr bond yield DOWN to 3.773 //SPAIN 10 YR BOND YIELD DOWN TO 3.273

3i Greek 10 year bond yield DOWN TO 3.431

3j Gold at $2686.45 /Silver at: 30.05 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 54/100 roubles/dollar; ROUBLE AT 102.77

3m oil into the 78 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.99 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.251% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9099 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9398 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

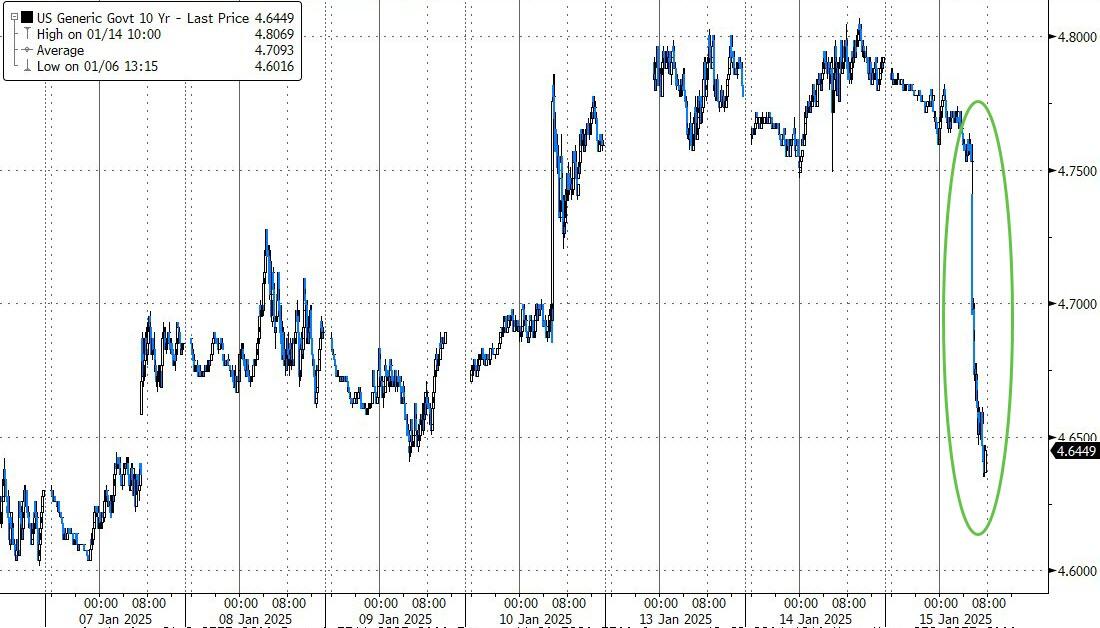

USA 10 YR BOND YIELD: 4.759 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.953. DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.354 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 35.49…

10 YR UK BOND YIELD: 4.8470 DOWN 9 PTS

10 YR CANADA BOND YIELD: 3.551 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.286 UP 1 PTS.

2a New York OPENING REPORT

Futures Rise With All Eyes On “Pivotal” CPOI

Wednesday, Jan 15, 2025 – 08:25 AM

US equity futures are higher, led by small-caps with the rally strengthening after the cooler than expected UK CPI print. As of 8:20am, S&P and Nasdaq futures are up 0.4%, with banking shares advancing in premarket trading after markets inched out a positive close on Tues following firm underlying PPI components & yields continuing to march higher. BlackRock, Bank of New York Mellon, JPMorgan and Goldman Sachs all beat estimates for the fourth quarter, with trading revenues performing strongly. All Mag7 names are also higher. Otherwise, it’s fairly quiet from a headline perspective overnight into CPI, although US reportedly will unveil more regulations to prevent advanced chips from being sold to China, with the planned rules, targeting producers TSMC, Samsung, and Intel. Bond yields are down 1-2bps as the USD is being offered, largely a function of yen strength following comment from BoJ Governor Ueda who said the BoJ will raise rates and adjust the degree of monetary support if improvement in the economy and price conditions continues, while he added that he wants to discuss and decide whether to raise rates at next week’s policy meeting. In commodities, Energy and Metals are leading the complex higher. Today’s focus is on CPI/Bank Earnings but keep an eye on the Beige Book release.

In premarket trading, Mag 7 names were mostly higher: Alphabet (GOOGL) +0.6%, Amazon (AMZN) +0.5%, Apple (AAPL) +0.4%, Microsoft (MSFT) +0.2% , Meta Platforms (META) +0.7%, Nvidia (NVDA) +0.1%, and Tesla (TSLA) +0.6%. Here are some other notable premarket movers:

- BlackRock shares gain 2.8% in premarket trading, after it reported adjusted earnings that exceeded analyst expectations in the fourth quarter. Assets under management missed the average analyst estimate. Shares are up 1.8%.

- Goldman Sachs reported FICC sales and trading revenue for the fourth quarter that beat the average analyst estimate.

- JPMorgan shares are little changed after the bank recorded 4Q FICC sales and trading revenue above expectations. The bank also gave a forecast for 2025 net interest income above the average analyst estimate.

- Wells Fargo shares rise 3.26% after the bank reported net interest income for the fourth quarter that beat the average analyst estimate. The bank also forecast an increase in 2025 net interest income, beating analyst expectations.

- BNY Mellon (BK) rises 2% as 4Q profit, net interest income top expectations.

- Amplify Energy (AMPY) gains 2% after agreeing to combine with some Juniper Capital portfolio companies.

- Compass (COMP) gains 8% after the residential real estate brokerage boosted its revenue guidance for the fourth quarter.

- Keros Therapeutics (KROS) falls 13% after the drug developer said it is halting all dosing in a combination trial of its experimental therapy for patients with a lung disorder, citing side effect concerns. Company is also terminating the trial early.

- NeoGenomics (NEO) rises 3% after forecasting revenue for 2025 of $735 million to $745 million.

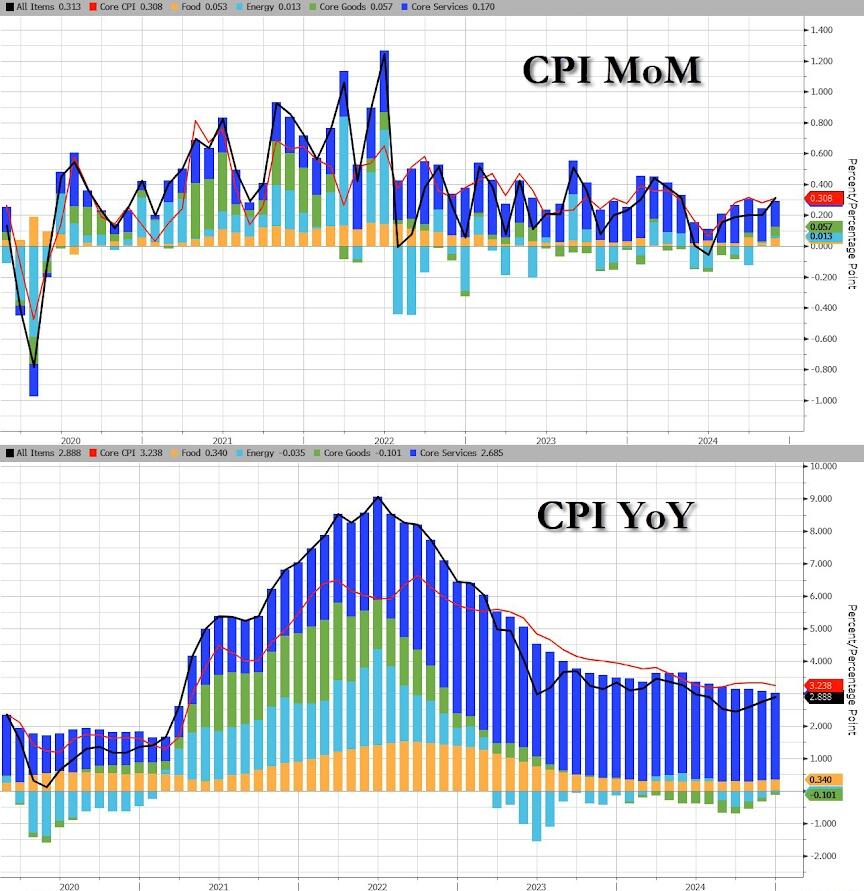

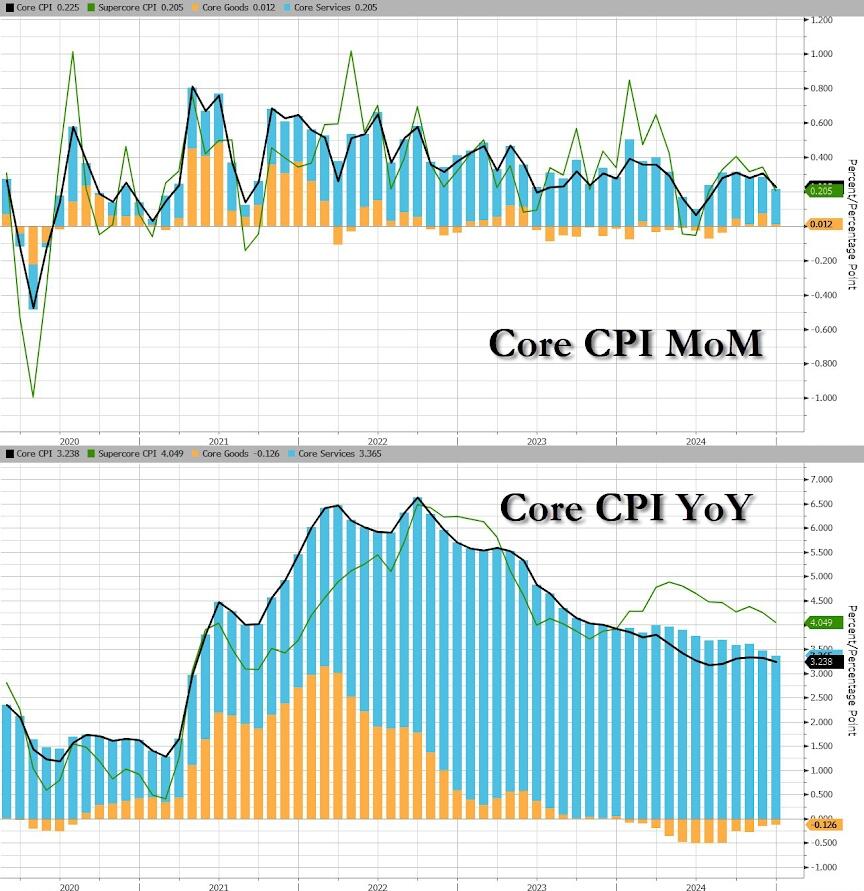

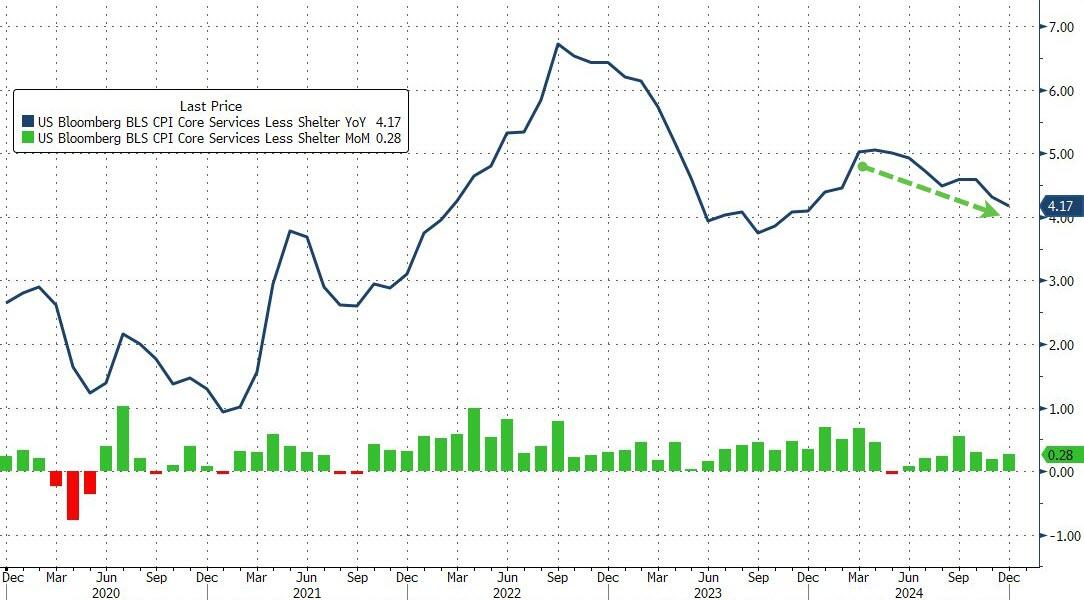

Traders remain wary of making big bets ahead of the “pivotal” CPI data (our full preview is here), which comes at a time when investors are paring their expectations of rate-cuts from the Federal Reserve. Forecasters predict CPI to show a fifth month of increases, with so-called core CPI up 0.3%. However, hopes of a benign print have been fanned by lower-than-expected US wholesale prices and slowing inflation in Britain.

“We need to see a more welcome print on the inflation front today,” said Laura Cooper, global investment strategist at Nuveen. “Today’s print will be crucial for the near-term price action as it could trigger another leg in the rate selloff, if we see a hotter-than-expected print.”

Equity traders are braced for a volatile day, with options implying moves of 1.1% in either direction for the S&P 500, the most for a CPI day since March 2023. They are also watching to see if 10-year Treasury yields could move closer to the psychologically key 5% level. Treasury 10-year yields slipped about 3.5 basis points to trade around 4.76% and Bloomberg’s dollar gauge extended Tuesday’s 0.4% drop. Thirty-year rates also eased after hitting new highs above 5% in the previous session.

European markets are trading mostly higher (Stoxx 600 index rose 0.7% while London’s FTSE 350 rallied as much as 1.6%) looking to snap a three-day losing streak. Real estate, telecommunication and retail stocks are leading gains. S&P futures rise 0.1% while Nasdaq 100 contracts add 0.2%. Inflation reading from UK unexpectedly dipped to 2.5% versus 2.6% expected. Services inflation at 3-year low, with markets now discounting 50bps of BoE easing in 2025. Germany’s economy shrank for the second consecutive year in 2024, with a 0.2% decline in GDP. Here are some of the biggest movers on Wednesday:

- Bureau Veritas shares gain 3.6%, while SGS slides, after the testing and certification firms said they’re in talks to combine, a deal that would create a company with a market value of more than $33 billion.

- Vistry shares rise as much as 8.6%, helping the housebuilder extend its recent rebound after closing at its lowest level since April 2020 on Monday.

- UK Rate-Sensitive stocks rise as inflation unexpectedly declined for the first time in three months in December, keeping alive hopes of a Bank of England interest-rate cut next month.

- Nordex shares gain as much as 5.1% after the German wind turbine producer’s fourth-quarter orders came in 30% ahead of consensus, according to Citi.

- Genus shares surge as much as 20%, the biggest jump since 2001, after the cattle breeding company said its full-year adj. pretax profit will likely come in at the top-end of forecasts.

- Currys shares jump as much as 14%, rebounding from a one-month low, after the electrical retailer said its annual adjusted pretax profit will top consensus estimates.

- Serco shares rise as much as 3.3% after the outsourcing company won a new contract from the US Army, adding to its recent wins in the US defense market.

- Hays rises as much as 3%, with the company’s warning that adjusted operating profit will be at the low-end of expectations in the first half already baked-in following recent weakness across the staffing industry that has led to consensus downgrades, according to analysts.

- Partners Group shares fall as much as 3.2% after the Swiss private equity firm’s full-year assets under management and fundraising missed consensus estimates.

- Anglo American shares fall as much as 2.3% after RBC downgraded to underperform from sector perform.

Earlier in the session, Asian stocks gained, as a rally in Indonesian shares after a surprise interest-rate cut helped to counter losses in Taiwan and mainland China. The MSCI Asia Pacific Index was up as much as 0.5%, with Japanese banks among the biggest boosts to the gains given expectations that the Bank of Japan will raise interest rates next week. The Jakarta Composite Index climbed 1.8%, the most in Asia, after Bank Indonesia defied market forecasts by cutting its key interest rate. Chinese equities were mixed, with a gauge of mainland-listed shares declining 0.6% while Hong Kong benchmarks ticked higher, as investors gauged local policymakers’ efforts to revive the economy amid the threat of higher US tariffs. The People’s Bank of China injected a near-historic amount of short-term funds into its financial system Wednesday amid a cash squeeze ahead of Lunar New Year holidays.

In rates, UK government bonds jump as traders add to their Bank of England interest-rate cut bets after data showed UK inflation eased more than expected in December. UK 10-year yields fall 8 bps to 4.81%. Treasuries also rise, albeit to a lesser extent with US and German 10-year borrowing costs dropping 2 bps each.

In FX, the pound reaction was choppy with cable printing fresh session highs and lows since the figures hit. It’s settled a few pips higher at ~$1.22. The yen is the notable mover in currency space, rising 0.7% against the greenback after comments from Bank of Japan Governor Ueda and his deputy his deputy strengthened market expectations for a potential interest-rate hike next week. USD/JPY falls to ~156.80. The Bloomberg Dollar Spot Index falls 0.2%.

Oil prices advance, with WTI rising 0.3% to $77.70 a barrel. Spot gold climbs $8 to $2,686/oz. Bitcoin rises above $97,000.

Looking to the day ahead now, and data releases include the US and UK CPI reports for December, along with Euro Area industrial production for November. From central banks, the Fed will release their Beige Book, and we’ll hear from the Fed’s Barkin, Kashkari, Williams and Goolsbee, ECB Vice President de Guindos and the ECB’s Villeroy and Vujcic, and the BoE’s Taylor. Today’s earnings releases include JPMorgan, Goldman Sachs, Citigroup and BlackRock.

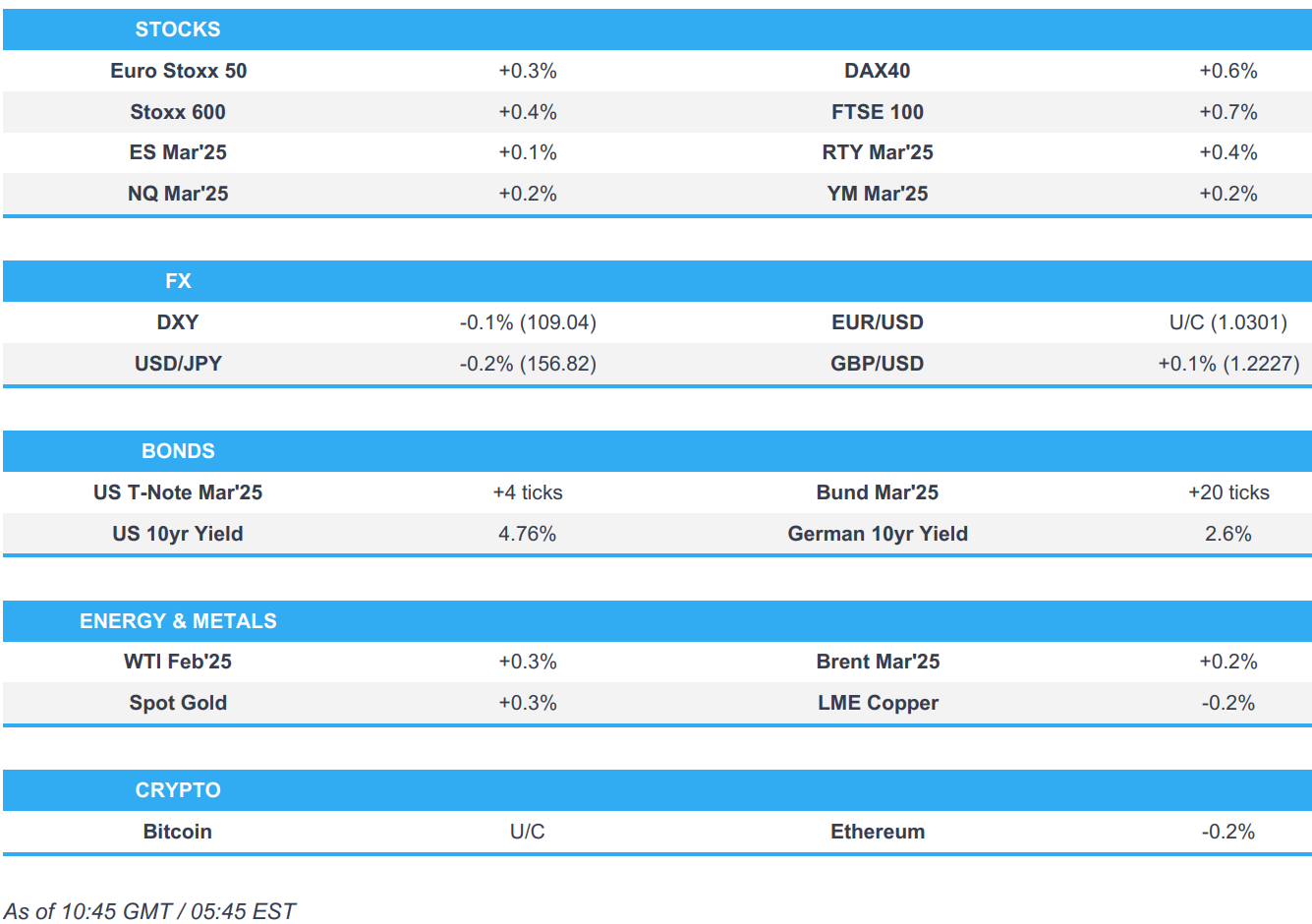

Market Snapshot

- S&P 500 futures little changed at 5,886.25

- STOXX Europe 600 up 0.4% to 510.17

- MXAP up 0.3% to 177.03

- MXAPJ little changed at 556.66

- Nikkei little changed at 38,444.58

- Topix up 0.3% to 2,690.81

- Hang Seng Index up 0.3% to 19,286.07

- Shanghai Composite down 0.4% to 3,227.12

- Sensex up 0.3% to 76,735.87

- Australia S&P/ASX 200 down 0.2% to 8,213.27

- Kospi little changed at 2,496.81

- German 10Y yield down 2.6 bps at 2.63%

- Euro little changed at $1.0309

- Brent Futures down 0.2% to $79.75/bbl

- Gold spot up 0.3% to $2,685.95

- US Dollar Index down 0.20% to 109.05

Top Overnight News

- US President-elect Trump announced on Truth Social that Keith Sonderling will serve as the next United States Deputy Secretary of Labor.

- US Treasury Secretary Yellen says the US economy is doing well, but more work needed to invest in infrastructure, labour force and R&D

- Hegseth’s odds of being confirmed as Secretary of Defense jumped after his hearing on Tues (Sen. Ernst came out Tues night and said she would back him for the role, a key endorsement). Politico

- The US is planning to unveil additional regulations designed to keep advanced chips made by TSMC (2330 TT/TSM) and Samsung Electronics (005930 KS) from flowing to China: BBG

- China’s central bank injected a near record-high amount of liquidity into the banking system to help meet demand for cash even as it looks to support the yuan. The People’s Bank of China on Wednesday pumped 959.5 billion yuan, or about $130.9 billion, worth of liquidity via seven-day reverse repurchase agreement and the second highest amount on record. WSJ

- The Bank of Japan will debate whether to raise interest rates next week, Governor Kazuo Ueda said on Wednesday, signaling its intention to take borrowing costs higher barring a Trump-driven market shock. The remarks, which echo those made by BOJ Deputy Governor Ryozo Himino on Tuesday, pushed up the yen as markets continued to price in the chance of a rate hike at the bank’s next policy meeting on Jan. 23-24. RTRS