GOLD CLOSED DOWN $9.50 TO $2708.50

SILVER CLOSED DOWN 49 CENTS TO $30.83

Gold ACCESS CLOSED $2700.00

Silver ACCESS CLOSED: $30.27

Bitcoin morning price:$102,740 UP 2130 DOLLARS.

Bitcoin: afternoon price: $104,580 up 3970 DOLLARS

Platinum price closing UP $5.30 TO $943.40

Palladium price; UP $8.45 TO $952.60

END

*CANADIAN GOLD: $3908.62 down 1.20 CDN dollars per oz( * NEW ALL TIME HIGH 3,909.09 CDN DOLLARS PER OZ//JAN 16 2025)

*BRITISH GOLD: 2218.90 down 0.50 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2,219.40 BRITISH POUNDS/OZ) JAN 16/2025

*EURO GOLD: 2,628.68 down 6.21 Euros per oz //* (ALL TIME CLOSING HIGH: 2,635.88 EUROS PER OZ/JAN 16 //.2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE

EXCHANGE: COMEX

CONTRACT: JANUARY 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,746.400000000 USD

INTENT DATE: 01/16/2025 DELIVERY DATE: 01/21/2025

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 8

323 C HSBC 385

332 H STANDARD CHARTE 280

363 H WELLS FARGO SEC 521

435 H SCOTIA CAPITAL 2

624 H BOFA SECURITIES 1021

657 C MORGAN STANLEY 1

661 C JP MORGAN 18

686 C STONEX FINANCIA 30 13

709 C BARCLAYS 190

737 C ADVANTAGE 50 26

905 C ADM 13

TOTAL: 1,279 1,279

JPMorgan stopped 18/1279

GOLD: NUMBER OF NOTICES FILED FOR JANUARY/2024. CONTRACT: 1279 NOTICES FOR 127,900 OZ 3.978 TONNES

total notices so far: 11,808 contracts for 1,180,800 Oz (36.728 tonnes)

FOR JANUARY

SILVER NOTICES: 38 NOTICE(S) FILED FOR 190,000 OZ/

total number of notices filed so far this month : 1892 for 9.460 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $9.50 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.74 TONNES OF GOLD FROM THE GLD./

INVENTORY RESTS AT 868.78 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.49 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.568 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 463.315 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 1098 CONTRACTS TO 154,314 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR SMALL ADVANCE OF $0,23 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. WE HAD A HUGE GAIN OF 1669 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE//THURSDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON THURSDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 2 WEEKS WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS. THEY FAILED MISERABLY WITH THURSDAY PRICING WITH ZERO LONGS BEING KNOCKED OFF. DERIVATIVE LOSSES CONTINUE TO MOUNT. WE HAD CONSIDERABLE T.A.S. LIQUIDATION THURSDAY COUPLED WITH ANOTHER NEW STRONG T.A.S. ISSUANCE OF 656 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.00 DOLLAR MARK. THE FRONT MONTH OF FEB HAS A HUGE $1.23 CONTANGO TO SPOT AS THE CROOKS NEED TO PAY A HUGE PRICE AS A SHORT (AND THUS SUPPLIER TO OUR PATIENT WAITING LONGS) THIS UPCOMING FEB CONTRACT MONTH. WE HAD A STRONG 570 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR 656 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 1669 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE. WE HAD HUGE TAS LIQUIDATION THROUGHOUT THURSDAY’S COMEX SESSION

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH YESTERDAY’S FAILED RAID.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: A STRONG 656 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS ESPECIALLY WITH OUR RAID ON JANUARY 13. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.23 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS GAIN IN OUR TWO EXCHANGES OF 1669 CONTRACTS.

WE HAD A 570 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 8.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 295,000 OZ QUEUE JUMP//NEW STANDING RISES TO 10.015 MILLION OZ

// STANDING FOR SILVER//JAN 10.015 MILLION OZ

WE HAD:

/ MEGA HUMONGOUS SIZED COMEX OI GAIN +// A STRONG 570 SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 656 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 75 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN

TOTAL CONTRACTS for 11 DAYS, total 7319 contracts: OR 36.595 MILLION OZ (665 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 36.595 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 36.595 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1098 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX/THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A 570 EFP ISSUANCE CONTRACTS: 570 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 8.110 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S QUEUE JUMP OF 295,000 OZ

//NEW TOTAL STANDING FOR JAN REMAINS AT 10.015 MILLION OZ

WE HAVE 1. A MEGA HUMONGOUS SIZED GAIN OF 1669 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR GAIN IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 656 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION BUT THEY STILL NEED THESE ISSUANCE FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON THURSDAY WITH THE GAIN IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE THURSDAY NIGHT (656) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE, NO DOUBT PRIOR TO TRUMP’S INAUGURATION.

WE HAD 38 NOTICE(S) FILED TODAY FOR 190,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUMONGOUS SIZED 16,688 OI CONTRACTS TO 552,723 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE SIZED 1742 CONTRACTS//

WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI (16,429 CONTRACTS) OCCURRED WITH OUR STRONG GAIN OF $24.10 IN PRICE THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 10.1331 TONNES FOLLOWED BY TODAY’S MONSTER QUEUE JUMP OF 1028 CONTRACTS OR 102,800 OZ TO WHICH WE ADD THE FIRST ISSUANCE FOR EXCHANGE FOR RISK CONTRACTS TOTALLING 1700 CONTRACTS OR 170,000 OZ (5.28775 TONNES) ISSUED JAN 6/2025 TO WHICH WE ADD JAN 8 EXCHANGE FOR RISK ISSUANCE OF 150 CONTRACTS OR 15,000 OZ OR .4665 TONNES AND THEN FINALLY TODAY’S ISSUANCE OF 85 CONTRACTS//8500 OZ OR .2644 TONNES . NEW STANDING FOR JAN ADVANCES TO 38.8506 TONNES (NORMAL DELIVERY) + 5.753 TONNES EX FOR RISK/PRIOR + .2644 TONNES TODAY EQUALS 43.8633 TONNES

/NEW STANDING 43.8633 TONNES

/ ALL OF THIS HAPPENED WITH OUR $24.10 GAIN IN PRICE WITH RESPECT TO THURSDAY’S COMEX ///. WE HAD A MEGA HUMONGOUS GAIN OF 23,318 OI CONTRACTS (72,53 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE VIOLENT ACTION AT THE COMEX WITH RESPECT TO QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCES ON 3 OCCASIONS .

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 6889 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 552,464

IN ESSENCE WE HAVE A MEGA HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 23,318 CONTRACTS WITH 16,429 CONTRACTS INCREASED AT THE COMEX// AND A HUGE SIZED 6889 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 23,318 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED AND CRIMINAL 1526 CONTRACTS ISSUED.(ON WEDNESDAY WE WITNESSED THE END OF 5TH CONSECUTIVE 30,000+ T.A.S CONTRACT ISSUED BY THE CME.) WE HAD A HUGE LIQUIDATION OF T.A.S CONTRACTS WITH OUR STRONG GAIN IN PRICE THURSDAY. MORE MONSTER ISSUANCE OF T.A.S WAS NEEDED FOR REPLENISHMENT TO CARRY OUT ITS PRICE CONTAINMENT STRATEGY IN FUTURE TRADING (FUTURE RAIDS). WE WILL NO DOUBT SEE A FINAL RAID ORCHESTRATED BY THE CROOKS PRIOR TO TRUMP’S INAUGURATION ON MONDAY

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6889 CONTRACTS) ACCOMPANYING THE HUMONGOUS SIZED INCREASE IN COMEX OI OF 16,429 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 23,318 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JAN 10.1331 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 1028 CONTRACTS OR 120800 OZ (3.1972 TONNES) TO WHICH WE ADD THAT CRAZY “DELIVERY” CALLED EXCHANGE FOR RISK JAN 17 OF .2644 PRECEEDED BY JAN 8 OF .4665 TONNES AND EX FOR RISK OF 5.2867 TONNES JAN 6////

NEW STANDING FOR JAN ADVANCES TO:

38.8506 TONNES NORMAL DELIVERY +

6.0177 TONNES OF EXCHANGE FOR RISK ON OUR THREE OCCASIONS IN JANUARY (6TH AND 8TH,17TH)

EQUALS: 43,8633 TONNES

//NEW STANDING JAN: 43.8633 TONNES WHICH I BELIEVE IS THE HIGHEST EVER GOLD STANDING FOR JANUARY.

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE THURSDAY WITH ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WE HAD A 1) $24.10 PRICE GAIN, AND 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A TOTAL GAIN OF 23,318 CONTRACTS ON OUR TWO EXCHANGES. ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) HUGE SIZED COMEX OPEN INTEREST INCREASE 5) HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 1526 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

TOTAL EFP CONTRACTS ISSUED: 53,289 CONTRACTS OF 5,328,900 OZ OR 165.75 TONNES IN 11 TRADING DAY(S) AND THUS AVERAGING: 4844 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES 165.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 165.76 DIVIDED BY 3550 x 100% TONNES = 4.67% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 165.75 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH AND MUCH LOWER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 1099 CONTRACTS OI TO 154,314 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 570 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 570 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 570 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1173 CONTRACTS AND ADD TO THE 570 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1669 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS A HUGE 8.715 MILLION OZ OCCURRED DESPITE OUR SMALL $0.23 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS FRIDAY MORNING THURSDAY NIGHT

SHANGHAI CLOSED UP 8.91 PTS OR 0.28%

//Hang Seng CLOSED UP 236.82 PTS OR 1.23%

// Nikkei CLOSED UP 128.02 OR 0.33%//Australia’s all ordinaries CLOSED UP 1.33%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.3323 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3478// Oil UP TO 79L69 dollars per barrel for WTI and BRENT DOWN AT 81.58 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING A

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

ASIA TRADING FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 5.79 PTS OR 0.18%

//Hang Seng CLOSED UP 61.17 PTS OR 0.31%

// Nikkei CLOSED DOWN 121.14 OR 0.31%//Australia’s all ordinaries CLOSED DOWN 0.20%%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.3289 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3558// Oil DOWN TO 78.25 dollars per barrel for WTI and BRENT DOWN AT 81.08 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING A

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUMONGOUS SIZED 16,429 CONTRACTS TO 552,723 WITH OUR STRONG GAIN IN PRICE OF $24.10 WITH RESPECT TO THURSDAY’S TRADING. WE LOST ZERO NET LONGS WITH OUR PRICE GAIN FOR GOLD AS WE HAD ALSO, AS YOU WILL SEE BELOW, A HUMONGOUS NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (6889) . THE CME ANNOUNCED TO MY DISMAY 85 EXCHANGE FOR RISK CONTRACTS THIS EARLY FRIDAY MORNING FOR 8500 OZ OR .2649 TONNES OF GOLD.

THUS IN TOTAL WE HAD A MEGA MEGA HUMONGOUS GAIN ON OUR TWO EXCHANGES OF 23,318 CONTRACTS WITH OUR GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED TRADING AS THEY ABSORBED EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE PAST WEEK WITH OUR MAMMOTH T.A.S. ISSUANCES. WE HAD A HUGE T.A.S. LIQUIDATION DURING THE THURSDAY COMEX SESSION. WE FINISHED WITH OUR 5 CONSECUTIVE HUGE 30,000+ ISSUANCES WITH TODAY’S STRONG 1526 CONTRACT ANNOUNCEMENT (FRIDAY MORNING).

THE FED IS THE MAJOR SHORT OF AROUND 82+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, 202, 203 , 204 AND 205 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP IS COMING INTO OFFICE MONDAY MORNING. TRUMP WOULD PROBABLY BE FURIOUS WITH THE FED IF IT FOUND OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING THE LAST WEEK OF DECEMBER AND THEN THIS WEEK, IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD. AS YOU WILL SEE BELOW, WE HAD ANOTHER HUGE QUEUE JUMPING SESSION TODAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF JANUARY.… THE CME REPORTS THAT THE BANKERS ISSUED A HUMONGOUS SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 6889 EFP CONTRACTS WERE ISSUED: : /FEB 6889 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6689 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A MEGA HUMONGOUS SIZED TOTAL OF 23,318 CONTRACTS IN THAT 6889 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUMONGOUS SIZED GAIN OF 16,688 COMEX CONTRACTS..AND THIS HUGE GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $24.10 THURSDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A STRONG SIZED SIZED 1526 CONTRACTS, AS AGAIN, THE FED(FRBNY) CALLED FOR THE FED-MOBILE TO BE USED TO ORCHESTRATE ANOTHER RAID BEFORE THE TRUMP-MOBILE TAKES OFFICE.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S THIS WEEK, THE FED WAS EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED NOTHING AS NOBODY LEFT OUR GOLD METAL ARENA AS THE GOLD PRICE SKYROCKETED!!

MECHANICS OF T.A.S CONTRACTS

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON DEC. 27, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE DECEMBER’S OPTIONS EXPIRY TRADING. T.A.S. LIQUIDATION WAS EVIDENT IN JAN 6 COMEX TRADING//RAID AND THEN AGAIN WITH TUESDAY’S FAILED ATTEMPT AT A RAID ON GOLD PRICE. HOWEVER NOT TO BE UNDONE, THE CROOKS ISSUED ANOTHER MONSTER 39,913 T.A.S CONTRACTS WEDNESDAY MORNING. THIS WAS THE FIFTH CONSECUTIVE 30,000+ CONTRACT ISSUANCE. ALL OF THESE T.A.S. ISSUANCES WERE USED TO THWART GOLD TRADING ESPECIALLY BEFORE TRUMP’S INAUGURATION AS THE FED MUST REDUCE ITS MASSIVE PHYSICAL GOLD SHORT OF 82 TONNES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION WITH RESPECT TO THURSDAY’S COMEX TRADING. (WHICH DISTORTS OPEN INTEREST)

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JAN (43.8633 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE JAN DELIVERY MONTH AND I BELIEVE THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR A JANUARY.

JANUARY: 10.1331 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

January 2025: 37.8506 TONNES + 5.753 EX FOR RISK/PRIOR + .2644 TONNES TODAY = 43.8633 TONNES

COMEX GOLD TRADING

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $24.10/)//AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A MEGA HUMONGOUS GAIN IN OUR TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION THURSDAY AS THEY WERE TRYING TO QUELL GOLD’S RISE AND HUGE COMEX/OTC DERIVATIVE LOSSES BUT TO NO AVAIL.

THE CROOKS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING.

EXCHANGE FOR RISK EXPLANATION/DECEMBER AND JANUARYTRADING

DECEMBER

47 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 14.6836 TONNES. THE COMEX IS TOTALLY SHATTERED TO PIECES.

EXCHANGE FOR RISK THIS JANUARY MONTH

WE NOW BEGIN OUR NEW MONTH OF JANUARY AND LO AND BEHOLD, THE CROOKS ISSUED ANOTHER MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THEN TO MY HORROR, THEY ISSUED THEIR SECOND EXCHANGE FOR RISK ON JAN 8, TOTALLING 150 CONTRACTS FOR 15000 OZ OR .4665 TONNES. THIS TONNAGE WILL BE ADDED TO THE FIRST ISSUANCE. THUS TOTAL EXCHANGE FOR RISK ISSUANCE FOR JANUARY: 5.7533 TONNES. MERCILESSLY THEY CONSUMATED FOR THE THIRD TIME THIS MONTH 85 EXCHANGE FOR RISK LAST NIGHT FOR 8500 OZ OR .2649 TONNES OF GOLD. HERE THE BUYER ASSUMES THE RISK OF DELIVERY FROM THE SELLER WHICH IS TOTALLY ASSININE.

TOTAL DELIVERIES JANUARY TRADING

WE HAVE GAINED A MONSTER TOTAL OF 73.33 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN (10.133TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S MONSTER QUEUE JUMP OF 1028 CONTRACTS OR 102,800 OZ (3.1975TONNES) TO WHICH WE MUST ADD OUR 5.7533 TONNES OF EXCHANGE FOR RISK ISSUANCE PRIOR TO TODAY’S EXCHANGE FOR RISK ISSUANCE OF .2649 TONNES: NEW TOTAL OF EX FOR RISK = 6.0177 TONNES WHERE THE BUYERS ASSUMES THE RISK FOR DELIVERY.(ISSUED JAN 6/2025, JAN 8, AND JAN 17).. THIS IS ,OF COURSE, AGAINST ALL RULES OF THE COMEX FORMULATED IN 1974 AS IT IS TOTALLY INSANE FOR A BUYER TO ASSUME RISK OF DELIVERY.

NEW STANDING FOR JAN: 37.8506 TONNES + 5.753 TONNES EX FOR RISK/PRIOR + .2644 TONNES EX FOR RISK TODAY = 43.8633 TONNES (WHICH IS HUGE FOR OUR VERY NON ACTIVE DELIVERY MONTH) A NORMAL AMOUNT STANDING FOR A JANUARY IN EARLIER TIMES HAS BEEN GENERALLY AROUND 1/4 TONNE OF GOLD. HOWEVER THESE PAST 4 YEARS QUEUE JUMPING HAS BEEN VERY PRONOUNCED AND THUS STANDING INCREASES DRAMATICALLY.

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $24.10

WE HAD 259 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 23,318 CONTRACTS OR 2,331,800 OZ (72,53 TONNES)

confirmed volume THURSDAY 227,416 contracts: fair ////nobody wishes to play with the crooks

//speculators have left the gold arena

END

/ /// THE JAN 2025 GOLD CONTRACT

JAN 17

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil . i) Out of Brinks 32.151 oz l kilobar ii) Out of Loomis: 64,302.000 oz 2000 kilobars total: 63,334.151 oz 2001 kilobars |

| Deposit to the Dealer Inventory in oz | I) Into Brinks dealer; 6484/542 oz (202 kilobars) .202 tonnes of gold |

| Deposits to the Customer Inventory, in oz | i)208,143.114 BRINKS (6474 KILOBARS) ii) 176,830.500 oz (LOOMIS) 5500 kilobars iii) 155,868.048 HSBC customer acct (4848 KILOBARS) iv)385,813.500 oz JPMorgan (12,000 kilobars) v) 65,941.701 oz Malca (2050 kilobars total customer acct 1,022,164.856 oz or 31.79 tonnes customer total dealer and customer deposit: 31.995 tonnes |

| No of oz served (contracts) today | 1279 notice(s) 127900 OZ 3.978 TONNES |

| No of oz to be served (notices) | 361 contracts 36100 OZ 1.122 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,808 notices 1,180,800 oz 36.728 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 1

I) Into Brinks dealer; 6484/542 oz

(202 kilobars)

.202 tonnes of gold

we have 5 customer deposits

i)208,143.114 BRINKS

(6474 KILOBARS)

ii) 176,830.500 oz (LOOMIS)

5500 kilobars

iii) 155,868.048 HSBC customer acct

(4848 KILOBARS)

iv)385,813.500 oz JPMorgan

(12,000 kilobars)

v) 65,941.701 oz Malca

(2050 kilobars

total customer acct 1,022,164.856 oz

or 31.79 paper tonnes customer

total dealer and customer deposit: 31.995 paper tonnes

withdrawals: 2

i) Out of Brinks 32.151 oz

l kilobar

ii) Out of Loomis: 64,302.000 oz

2000 kilobars

total: 63,334.151 oz

2001 kilobars

2,001 paper tonnes

adjustments:4/customer to dealer

i) Out of Manfra 37,989.564 oz

ii) Out of JPMorgan 160,690..698 oz(4998 kilobars)

iii) out of Brinks 64.302 oz 2 kilobars

iv) out of Loomis: 64,334.151

(2001 kilobars)

total customer to dealer: 263,079.078 oz or 8.182 tonnes

thus basically what comes into eligible is transferred to dealer accounts and then out.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JAN.

For the front month of JAN: we have an oi of 1640 contracts having GAINED 134 contracts. We had a strong 1420 contract issuance on THURSDAY. Thus ANOTHER MEGA HUGE QUEUE JUMP (GAIN) of 1028 contracts on our two exchanges. (102800 oz or 3.197 tonnes). THIS IS CENTRAL BANKERS STANDING FOR PHYSICAL GOLD WITH LONDON VAULTS RUNNING OUT OF PHYSICAL TO SUPPLY THEM. THIS IS ALSO THE 2ND HIGHEST QUEUE JUMP EVER WITH THE HIGHEST ONE HAPPENING A FEW YEARS AGO AT OVER 5 TONNES.

FEBRUARY SURPRISINLY GAINED ANOTHER 5058 CONTRACTS TO 287,252 AS IT BEGINS ITS COUNTDOWN BEFORE FIRST DAY NOTICE (JAN 31.2025) EXPECT A MEGA WOPPER OF A FEB DELIVERY MONTH AS THE FRONT MONTH IS NOT DECLINING AT ALL.

MARCH HAD A LOSS OF 29 CONTRACTS DOWN TO 6494

APRIL HAD A GAIN OF ONLY 9441 CONTRACTS UP TO 181,434 CONTRACTS AS MANY ARE REFUSING TO ROLL TO JUNE.

We had 1279 contracts filed for today representing 127,900 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1279 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 18 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JAN /2025. contract month, we take the total number of notices filed so far for the month (11,808 x 100 oz ) to which we add the difference between the open interest for the front month of JAN(1640 CONTRACTS) minus the number of notices served upon today (1279 x 100 oz per contract) equals 1,216,900 OZ OR 37.8506 TONNES. to which we add those criminal exchange for risk issuance of .4665 TONNES (JAN 8) AND 5.28775 tonnes/JAN 6//TOTAL EXCHANGE FOR RISK TO TODAY;S .2644 TONNES = 6.0177 TONNES. THUS NEW STANDING FOR GOLD AT THE COMEX FOR JAN IS 37.8506 TONNES PLUS 6.0177 TONNES EX FOR RISK = 43.8683 TONNES

thus the INITIAL standings for gold for the JAN contract month: No of notices filed so far (11,808 x 100 oz +we add the difference for front month of JAN (1640 OI} minus the number of notices served upon today (1279 x 100 oz which equals 1,216,900 oz (37.8506 TONNES) + 5.753 tonnes ex for risk ( JAN 6 AND 8TH) AND THEN TODAY;S .2644 TONNES = 43.8633 tonnes

TOTAL COMEX GOLD STANDING FOR JAN.: 43.8633 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR AND I BELIEVE THE HIGHEST EVER RECORDED FOR A JANUARY.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,111,518.168 oz 65.67 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 24,581.865.000 OZ

TOTAL REGISTERED GOLD 11,221,444.433 or 349.03 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 13,360,420.567 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,109,926 oz (REG GOLD- PLEDGED GOLD)= 283.335 tonnes //

JPMorgan enhanced inventory is 3.511 million oz

END

SILVER/COMEX

JAN 17. 2025

INITIAL

//2025// THE JAN 2025 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | a) Out of Loomis 600,620.100 oz b) Out of Brinks 1006.36 oz total: 601,626.46 oz . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | i) Into Loomis: 771,078.000 oz ii) Into JPMorgan: 1166,099.400 oz total 1,937,177.400 oz |

| No of oz served today (contracts) | 38 CONTRACT(S) (190,000 OZ) |

| No of oz to be served (notices) | 111 contracts (0.555 MILLION oz) |

| Total monthly oz silver served (contracts) | 1892 Contracts (9.460 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

deposits:2

i) Into Loomis: 771,078.000 oz

ii) Into JPMorgan: 1166,099.400 oz

total 1,937,177.400 oz

WITHDRAWALS 2

a) Out of Loomis 600,620.100 oz

b) Out of Brinks 1006.36 oz

total withdrawal: 601,626.46 oz

ADJUSTMENT 1 customer to dealer DELAWARE

i) 49,272.318 oz

JPMorgan has a total silver weight: 136.702million oz/330.737million or 41.33%

TOTAL REGISTERED SILVER: 71.909 MILLION OZ//.TOTAL REG + ELIGIBLE. 330.737 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF JAN /2024 OI: 149 OPEN INTEREST FOR A GAIN OF 45 CONTRACT(S).

WE HAD A 14 CONTRACT ISSUANCE ON THURSDAY. THUS WE GAINED 59 CONTRACTS, THAT IS WE HAD A 59 CONTRACT QUEUE JUMP FOR 295,000 OZ

FEBRUARY SAW A GAIN 0F 19 CONTRACTS TO STAND AT 1011

MARCH SAW A GAIN OF 148 CONTRACTS UP TO 117,323. THE FRONT ACTIVE DELIVERY MONTH OF MARCH ALSO IS NOT DECLINGING MUCH AND WE SHOULD ALSO HAVE A HUMDINGER OF A DELIVERY MONTH FOR MARCH.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 38 for 190,000 oz

CONFIRMED volume; ON THURSDAY 51,746 poor//

To calculate the number of silver ounces that will stand for delivery in JAN we take the total number of notices filed for the month so far at 1892x 5,000 oz = 9.460 MILLION oz

to which we add the difference between the open interest for the front month of JAN (149) and the number of notices served upon today (38)x (5000 oz)

Thus the standings for silver for the JAN 2025 contract month: 1892 Notices served so far) x 5000 oz + OI for the front month of JAN(149) minus number of notices served upon today (38)x 5000 oz equals silver standing for the JAN contract month equating to 10.015 MILLION OZ.

New total standing: 10.015 million oz.

There are 71.859 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

/JAN 17 WITH GOLD DOWN $9.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.74 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 868.78 TONNES

JAN 16 WITH GOLD UP $24.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 872.52 TONNES

JAN 15 WITH GOLD UP $24.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 872.52 TONNES

JAN 14 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 874.53 TONNES

JAN 13 WITH GOLD DOWN $27.75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A DEPOSIT OF 5.74 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 876.82 TONNES

JAN 10 WITH GOLD UP $17.80 ON THE DAY; NO CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 9 WITH GOLD UP $13.85 ON THE DAY; NO CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 8 WITH GOLD UP $5.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 7 WITH GOLD DOWN $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 6 WITH GOLD DOWN $4.90 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 3 WITH GOLD DOWN $14.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 2 WITH GOLD UP $29.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 31 WITH GOLD UP $20.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 30 WITH GOLD DOWN $11.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.28 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.52 TONNES

DEC 27 WITH GOLD DOWN $17.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.80 TONNES

DEC 26 WITH GOLD UP $17.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: : ///INVENTORY RESTS AT 873.95 TONNES

DEC 24 WITH GOLD UP $6.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES OF GOLD OUT OF THE GLD. / // : .///INVENTORY RESTS AT 873.95 TONNES

DEC 23 WITH GOLD DOWN $13,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 16.66 TONNES OF GOLD VAPOUR GOLD INTO THE GLD. / // : .///INVENTORY RESTS AT 877.40 TONNES

DEC 20 WITH GOLD UP $29,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 860.74 TONNES

DEC 19 WITH GOLD DOWN $45.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF .29 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 18 WITH GOLD DOWN $8.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 17 WITH GOLD DOWN $6.85 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.23 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 16 WITH GOLD DOWN $2.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.70 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 13 WITH GOLD DOWN $24.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.78 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 868.60 TONNES

DEC 12 WITH GOLD DOWN $34.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.59 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 873.38 TONNES

DEC 11 WITH GOLD UP $29.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 9 WITH GOLD UP $31.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD. // : .///INVENTORY RESTS AT 871.94 TONNES

GLD INVENTORY: 868.78 TONNES, TONIGHTS TOTAL

SILVER

JAN 17 WITH SILVER DOWN $.49 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.568 MILLION OZ FROM THE SLV./. //INVENTORY AT SLV RESTS AT 463.315 MILLION OZ

JAN 16 WITH SILVER UP $0.23 //NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 464.863 MILLION OZ

JAN 15 WITH SILVER UP $0.79 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.745 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 464.863 MILLION OZ

JAN 14 WITH SILVER UP $0.15 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.228 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 460.218 MILLION OZ

JAN 13 WITH SILVER DOWN $0.69 //NO CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.637 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 459.990 MILLION OZ

JAN 10 WITH SILVER UP $0.19 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 459,353 MILLION OZ

JAN 9 WITH SILVER UP $0.08 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 459,353 MILLION OZ

JAN 8 WITH SILVER DOWN $0.01 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 7 WITH SILVER UP 48 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 6 WITH SILVER UP 38 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 3 WITH SILVER UP 17 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 2 WITH SILVER UP 45 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.616 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 462.128 MILLION OZ

DEC 31 WITH SILVER DOWN 14 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 30 WITH SILVER DOWN 39 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: // A WITHDRAWAL OF 1.13 MILLION OZ FROM THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 27 WITH SILVER DOWN 24 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY AT SLV RESTS AT 461.651 MILLION OZ

DEC 24 WITH SILVER UP 2 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 23 WITH SILVER UP 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 6.15 MILLION OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 20 WITH SILVER UP 43 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 183,000 OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 457.597 MILLION OZ

DEC 19 WITH SILVER DOWN 25 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV///// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 18 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 17 WITH SILVER DOWN 12 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.456 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 16 WITH SILVER DOWN 0 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 4.84 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 13 WITH SILVER DOWN 46 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .536 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 462.892 MILLION OZ

DEC 12 WITH SILVER DOWN 94 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 5.787 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 463.428 MILLION OZ

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 10 WITH SILVER DOWN 8 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.868 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 471.812 MILLION OZ

DEC 9 WITH SILVER UP $0.91 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.367 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 473.680 MILLION OZ

CLOSING INVENTORY 463.315 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

VERY IMPORTANT READ..

PETER SCHIFF….

If We Have Such A Strong Economy, Why Are So Many Americans Struggling?

Friday, Jan 17, 2025 – 06:30 AM

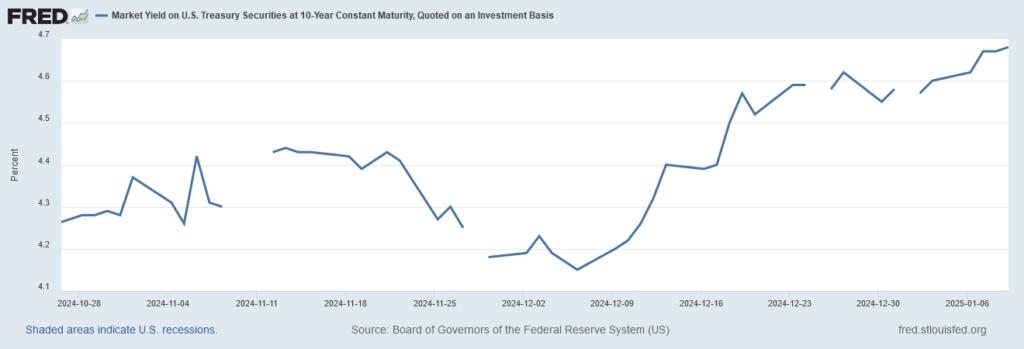

The 10-year treasury yield rocketed up to near 5%, and analysts say it’s because the economy is strong despite higher inflation.

But if the economy is so strong, why are Americans so indebted, cash-poor, and desperate?

10-Year Treasury Yields

The recent spike in 10-year yields has been explained away by many as the result of a strong economy, but they fail to mention that high inflation makes the 10-year yield harder to contain. High 10-year yields support higher rates for things like car loans and mortgages, and with the world still under the inflationary spell of COVID-era QE and free money “stimulus,” the only answer may be—you guessed it—more free money QE to “stimulate” an economy that’s already stuck in an infinite loop of inflation. As Peter Schiff said recently:

“I think that they’ve already lost control of the long end of the bond market…the Fed is going to be pressured to try to lower long-term rates, and the only way it would be able to do that is by buying the long term bonds, and the only way to get the money to do that is to print it.”

But not even the Fed has a clue for how it would deal with a stagnation scenario.

“It was almost humorous and even it got a laugh out of Powell. A reporter asked him at the last press conference, ‘What’s your plan for stagflation?’ And he laughed and says, ‘Our plan for stagflation is that we’re not going to have it.’”

But we already do. For now. markets are also still trying to figure out how to react to Trump’s win, and uncertainty breeds volatility. So, high inflation coupled with uncertainty and “strong” economic data are the three factors being attributed to the spike in yields. The inflation part is partially right; the only problem is that it doesn’t go far enough, because inflation is actually much worse than what’s being reported. The other problem is that the “strong jobs data” being partially blamed for the rise in yields is never really as strong as what gets reported, as the jobs reports and other economic data are unreliable and designed to paint as rosy a picture as possible.

As Treasury yields keep rising, mortgage rates keep going up, and basic needs keep getting more expensive, 2025 is already shaping up to be a marvel of stagflationary chaos. As predicted, the bond market and broader economy are getting spooky, and Central Banks will keep buying gold to protect themselves from the same problems that government and central bank interventions create.

The question is, how many Americans will protect themselves? The answer is very few, as the average American has hardly any money saved and is living paycheck-to-paycheck while becoming increasingly over-indebted. After all, when economies are extremely weak or extremely strong, they will always be what decides elections even if the root causes go far deeper than any one president, which they always do.

But when Americans are struggling, seeing drastic price increases, and watching with enraged awe as their government continues donating taxpayer money to proxy wars in Ukraine and Israel as American cities flood, burn, and lose their critical infrastructure, they’re going to vote for the other candidate. So, while Trump signed the inflationary COVID stimulus checks, he was able to convince voters even after losing in 2020 that he should be given another chance after the economic deterioration of the last four years..

Whether or not Trumponomics itself ends up being inflationary, central bank monetary policy will always revert back to the only real tool in its toolbox, which is printing money. Whether or not DOGE, tariffs, and other promises materialize, the result of statist intervention to bring down prices is almost always, ironically enough, higher prices. Even if the intervention causes costs to go down in one place, they generally go up somewhere else.

That’s because there are no free lunches in economics, no matter what central bankers may say.

END

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ALASDAIR MACLEOD….

Gold getting overbought

The sharp rise in Comex open interest suggests short-term caution. But the background for gold’s outlook just gets better and better.

| Alasdair MacleodJan 17∙Paid |

Gold and silver rallied this week, though this morning there is evidence of profit taking ahead of the weekend. In European trading this morning, spot gold was $2704, up $15 from last Friday’s close. And silver was $30.50, up 12 cents on the same timescale. Comex volumes in both were moderate.

Open interest in the gold contract has risen sharply, less so in silver. This is illustrated next.

While consistent with growing bullishness, to see gold’s Open Interest rise so sharply brings the risk of a correction with it. What we don’t know is the quality of buying: are they momentum buyers, or are they Managed Money buying on an assessment that the inflation outlook for the dollar is deteriorating, and the Fed is in a difficult position?

Monday will see Donald Trump’s inauguration as president, which will focus minds on the economic consequences of his proposed economic policies. It is commonly accepted that the US economy is growing, though this reflects a large and rising budget deficit and not genuine production. Trump’s tariffs and tax proposals and their consequences are now going to fill the headlines. It’s not hard to guess that higher consumer prices are on their way, which will lead to interest rates not falling as hoped, and potentially even higher bond yields.

This, in turn, justifies a strong dollar. This week the dollar’s trade weighted index paused, consolidating recent gains.

The dollar is likely to continue to be strong against other currencies, which is causing problems for the yen and euro, whose interest rates and bond yields have been left behind and may be forced to rise significantly. The obvious reluctance of the Bank of Japan and the ECB to condone higher rates is already weakening these currencies, with gold hitting new record highs priced in them.

Sterling bond yields already exceed those of the dollar, but with the British government on an economic suicide mission no further comment is required. Indeed, as the chart below illustrates, priced in gold (which is common law real global money) the entire fiat currency complex is losing value at an accelerating rate.

This is the reality of the global monetary situation and the context in which we must regard current market developments. Under President Trump, US inflation will rise driven by tariffs and his tax cutting policies. All major governments (Germany and Canada probably excepted) are highly indebted and cannot afford higher borrowing costs. Unless some miracle happens, the conditions for a fiat currency collapse are rapidly developing.

And finally, returning to the short-term, look at gold’s technical chart:

With Comex futures rapidly becoming overbought, further consolidation may be called for. But with Asian buyers in the market and ETF demand turning positive, any such consolidation is likely to be relatively minor. It is a situation where traders can lose money, but stackers should buy on dips.

end

JOHN RUBINO

3. CHRIS POWELL AND GATA DISPATCHES

END

ANDREW MAGUIRE A MUST MUST VIEW…YOUTUBE/KINESIS LIVE FROM THE VAULT 206

/LIVE FROM THE VAULT 206

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY

END

end

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING FRIDAY MORNING THURSDAY NIGHT

SHANGHAI CLOSED UP 5.79 PTS OR 0.18%

//Hang Seng CLOSED UP 61.17 PTS OR 0.31%

// Nikkei CLOSED DOWN 121.14 OR 0.31%//Australia’s all ordinaries CLOSED DOWN 0.20%%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.3289 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3558// Oil DOWN TO 78.25 dollars per barrel for WTI and BRENT DOWN AT 81.08 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING A

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.3289

OFFSHORE YUAN: DOWN TO 7.3558

SHANGHAI CLOSED CLOSED UP 5.79 PTS OR 0.18%

HANG SENG CLOSED CLOSED UP 61.17 PTS OR 0.31%

2. Nikkei closed DOWN 121.14 OR 0.31%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 108.99 EURO FALLS TO 1.0299 DOWN 7 BASIS PTS HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: FALLS TO. +1.200 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.73…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4815 Italian 10 Yr bond yield DOWN to 3.602 //SPAIN 10 YR BOND YIELD DOWN TO 3.140

3i Greek 10 year bond yield DOWN TO 3.269

3j Gold at $2707.10 /Silver at: 30.24 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 25/100 roubles/dollar; ROUBLE AT 102.37

3m oil into the 78 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.73 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.200% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9128 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9393 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

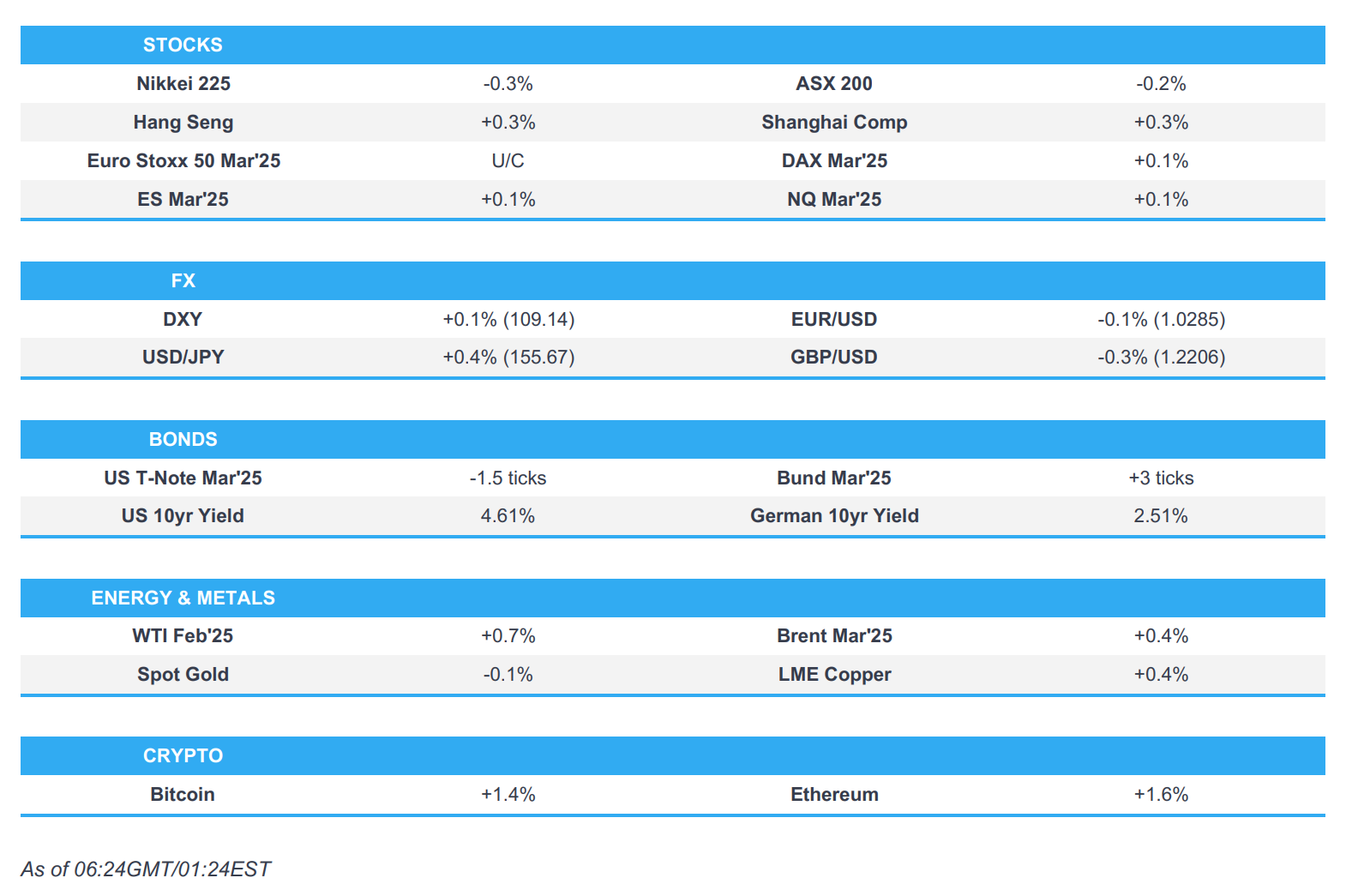

USA 10 YR BOND YIELD: 4.578 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.814. DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.232 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 35.57…

10 YR UK BOND YIELD: 4.678 DOWN 3 PTS

10 YR CANADA BOND YIELD: 3.334 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 3.046 DOWN 2 PTS.

2a New York OPENING REPORT

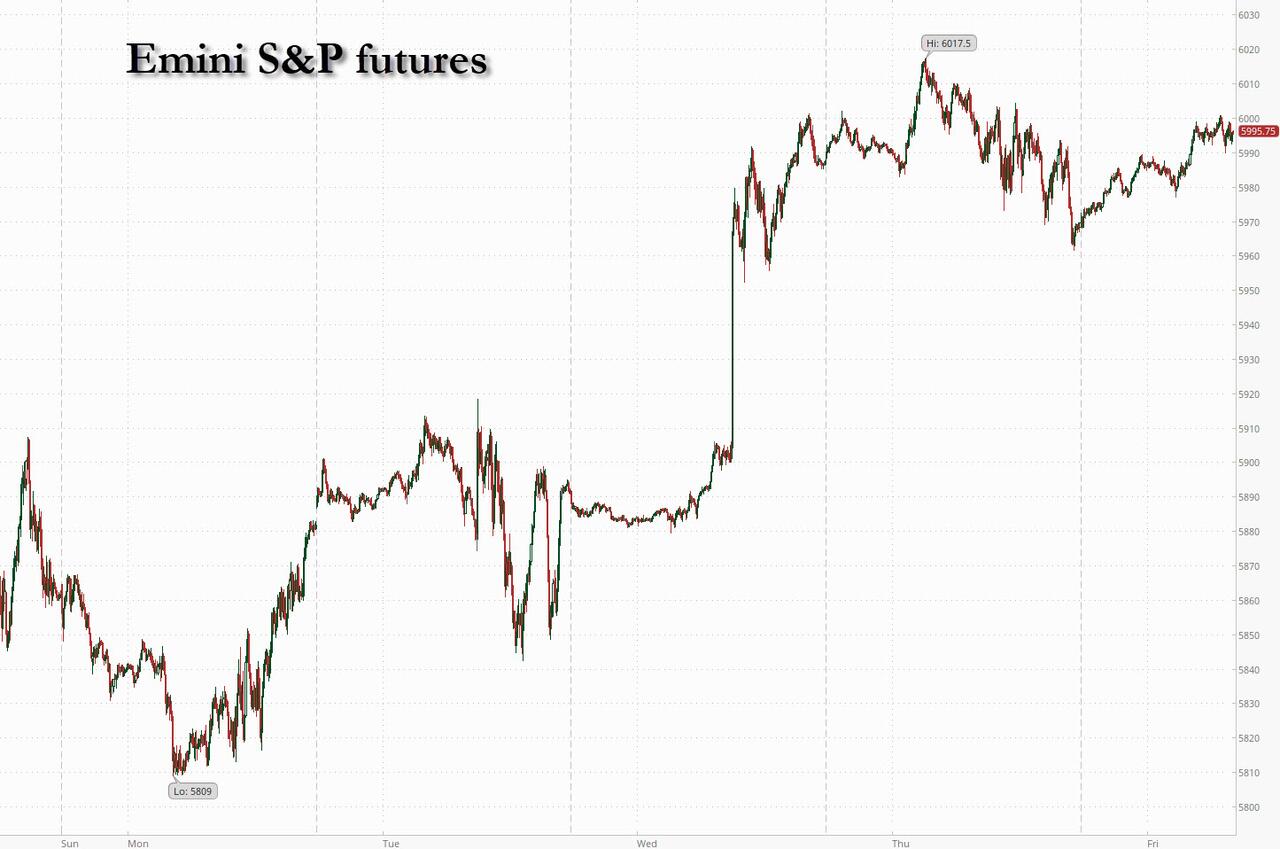

S&P Futures Rise Above 6,000 With Trump Inauguration Looming

Friday, Jan 17, 2025 – 08:17 AM

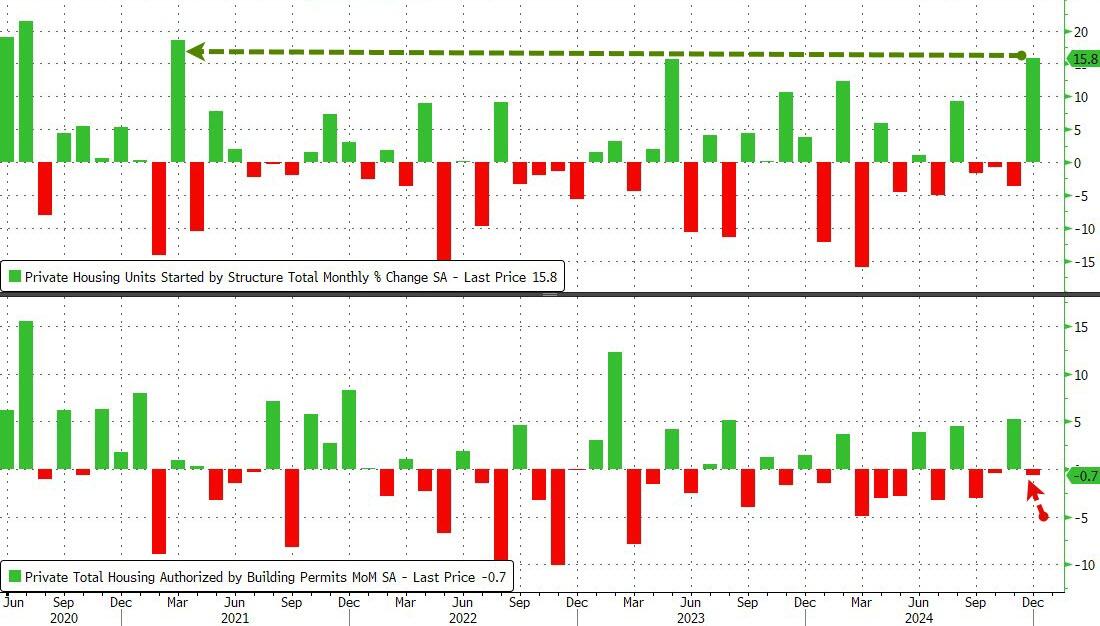

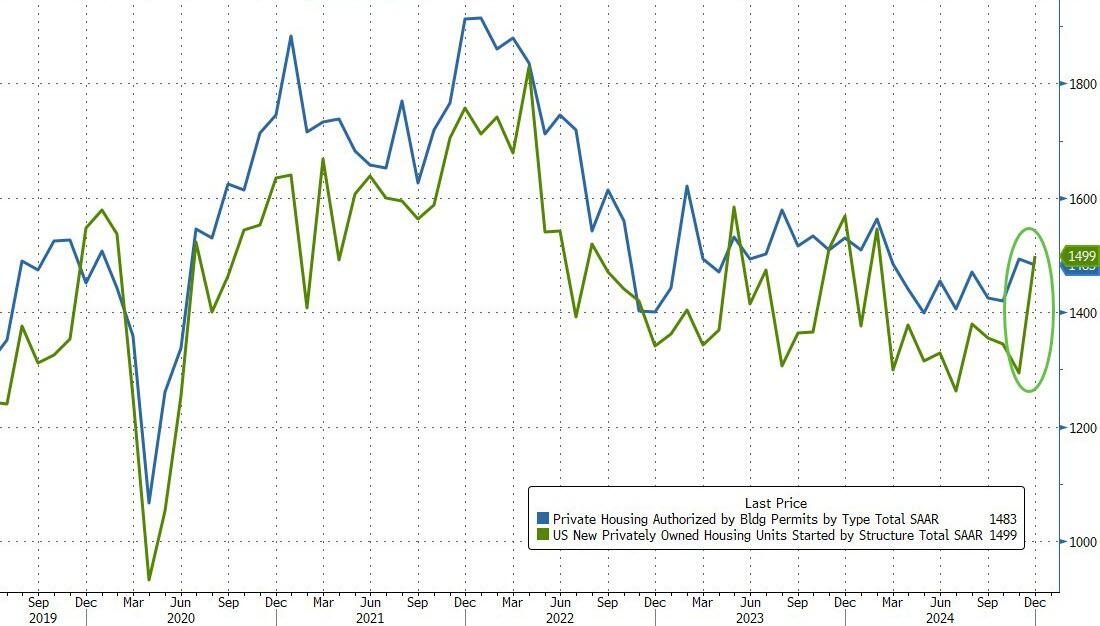

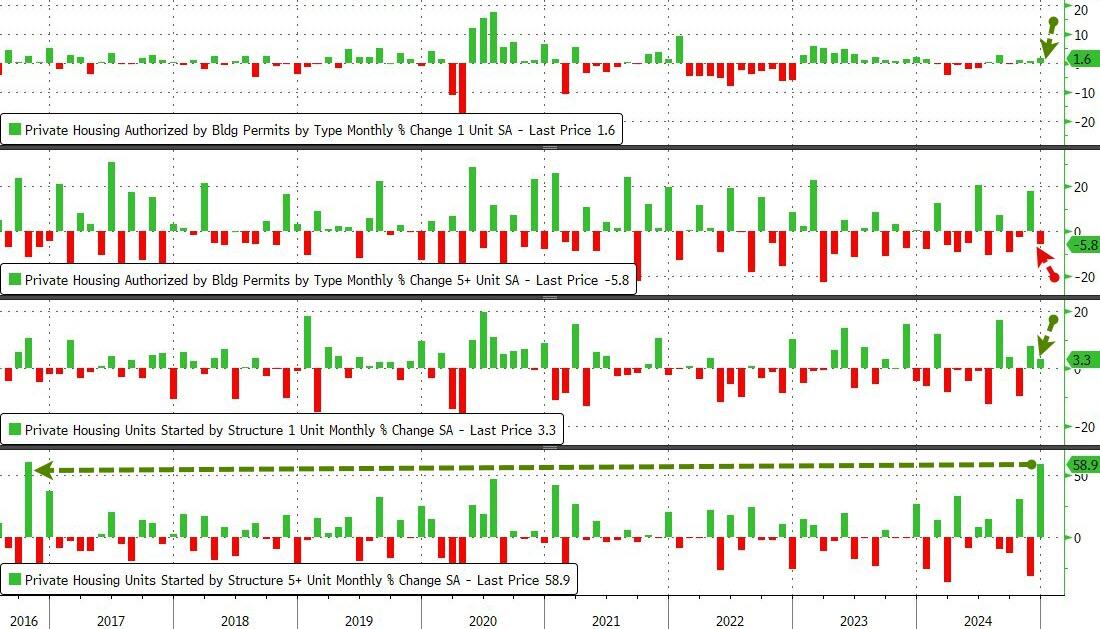

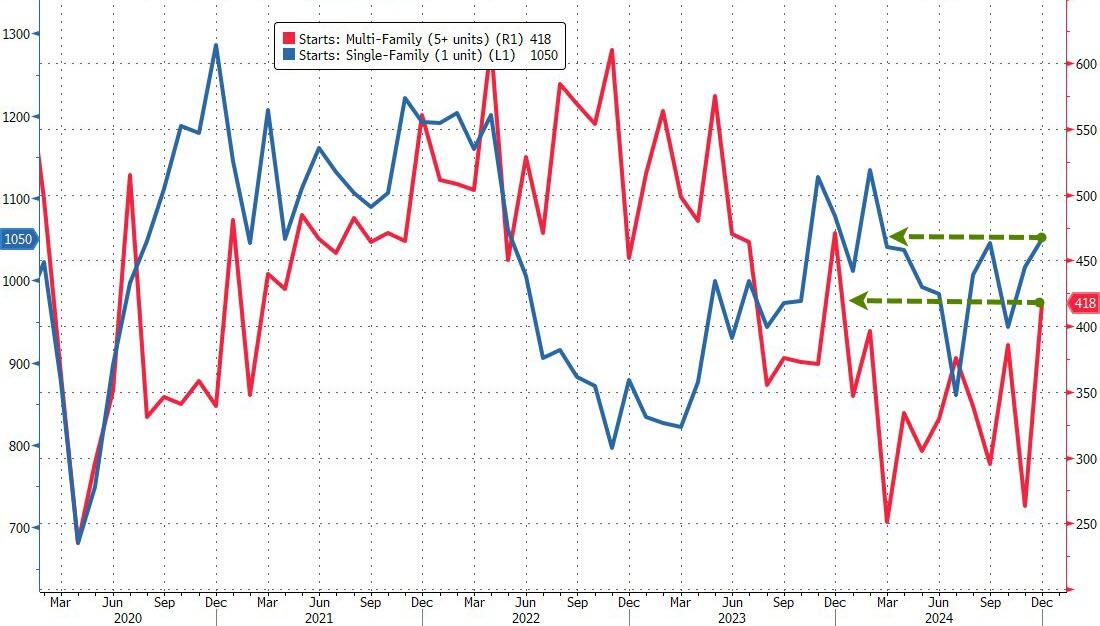

US equity futures are higher modestly, rebounding from yesterday’s just as modest loss. As of 8:00am, S&P futures rise 0.4%, with the underlying index poised for its biggest weekly gain since November’s election, while Nasdaq 100 futures advanced 0.5% thanks to Mag 7 stocks mostly higher (NVDA +1.3%, TSLA +0.9% and GOOG/L +0.6%) as the latest data and comments from Fed officials suggest the central bank will have room to cut interest rates this year. 10Y Treasury yields edged lower, slipping more than 15 basis points below recent multi-month highs, while the USD is higher. Base metals are mostly higher amid upside surprise on China Q4 and December macro data: Q4 GDP prints 5.4% vs. 5.0% survey vs. 4.6% prior; Retail Sales and IP both surprised to the upside. However, reactions from local Asian markets remain muted. Today, macro focus will be on housing data (Housing Starts and Building Permits).

In premarket trading, all members of the Magnificent Seven are higher: Alphabet (GOOGL) +0.4%, Amazon (AMZN) +0.5%, Apple (AAPL) +0.7%, Microsoft (MSFT) +0.3% , Meta Platforms (META) +0.3%, Nvidia (NVDA) +0.9%, and Tesla (TSLA) +0.7%. JetBlue and Southwest Airlines shares fall about 2% after BofA downgraded the carriers to underperform from neutral, citing their lower exposure to corporate, premium and international routes. Here are some other notable premarket movers:

- Bank OZK (OZK) ticks 1% higher after the bank posted 4Q net interest income that topped estimates.

- Fastenal (FAST) falls 6% after the construction supplies company reported 4Q sales that slightly missed as a “slow rate of growth reflects continuation of the soft manufacturing environment that has been sustained throughout 2024.”

- JB Hunt (JBHT) shares drop 9% after the transportation and logistics company reported fourth-quarter earnings per share that trailed consensus expectations.

- Lumentum (LITE) gains 6% after Barclays turned bullish on the photonics products maker, saying it’s an “underappreciated share gain story.”

- Truist Financial (TFC) gains 2% after Charlotte-based lender reported net interest income that was broadly in line with analyst estimates.

A big reason for this week’s stock market outperformance is that swap markets now expect some 40 basis points worth of rate cuts from the Fed this year, following a weaker than expected core CPI print, moving from not even pricing a single quarter-point move earlier this week.

“Even equity managers were more concerned over rates than earnings,” said Kevin Thozet, a member of the investment committee at Carmignac. “What we have had is reassuring data on this front — whether retail sales or inflation — hinting that the US economy may not be overheating. This has allowed for fixed income markets to take a bit of a breather.”

With Q4 earnings just starting, investor focus is also turning to President-elect Donald Trump’s inauguration on Monday and his plans for tariff hikes, tax cuts and mass deportation of undocumented migrants. “Key things to be aware of are whether Trump goes big from the very first day, coming up with executive orders and being very vocal,” Carmignac’s Thozet said. “He has been saying a multitude of things and we will see if he is more talking than acting.”

Europe’s Stoxx 600 index also gained, rising 0.6%, and on course for its strongest week since September. Basic resources shares led the way after Bloomberg reported that Glencore and Rio Tinto held early-stage talks about combining their businesses. The news, alongside a weaker pound, helped London’s FTSE 100 hit a record high. China-focused European sectors such as retail and auto also climbed after data suggested Beijing’s stimulus blitz is succeeding in shoring up economic growth. Here are some of the biggest movers on Friday:

- European miner stocks rise after Bloomberg reported that Rio Tinto and Glencore have recently held early-stage talks about a combination; Rio Tinto +1.3%, Glencore +2.3%

- SUSS MicroTec shares rise as much as 36%, the most on record, after the German semiconductor equipment manufacturer reported preliminary results that Stifel said topped expectations due to sales and Ebit beats

- Avolta shares rise as much as 9.6%, the steepest gain since July 2022, after the world’s largest duty-free operator announced a share buyback of as much as CHF200 million

- Smiths Group shares rise as much as 4.7%, briefly hitting a record high, after one of its shareholders called on the company to explore a breakup, arguing in a letter that a sale of the entire business or its units could improve its valuation

- Evoke shares jump as much as 12%, hitting their highest level since July, after the gambling company said its annual adjusted Ebitda will be the high end of its guidance range for 2024, prompting analysts to lift their earnings estimates

- Sanofi shares rise as much as 1.8% to the highest level since Oct. 29 after Berenberg analysts said the drugmaker’s valuation is “highly attractive.”

- Schroders shares rise as much as 1.8% after it said it plans to cut as much as 3% of its workforce

- Maire shares rise as much as 8.8% after Kepler Cheuvreux analyst Kevin Roger raised the recommendation on the Italian company to buy from hold, mentioning potential growth prospects

- Medcap shares fall as much as 30% after the Swedish life science investment firm’s preliminary 4Q figures showed “significantly lower earnings in business area Specialty Pharma” due to increased competition in the British market for melatonin

- Tenaris shares fall 0.5% before erasing the decline after Kepler Cheuvreux cuts to hold from buy, saying it sees limited upside for the Luxembourg-based oil-pipe maker

Earlier, Asian stocks snapped a three-day winning streak, led by losses in Japan after the yen strengthened on an outlook for higher interest rates while largely shrugging off news that China’s economy had expanded at its fastest pace in six quarters to hit the government’s growth goal last year. Analysts say the growth report for 2024 is overshadowed by looming US tariffs on Chinese exports. The MSCI Asia Pacific Index declined as much as 0.7% before erasing most of the loss. Korean companies Hyundai and Samsung were among the worst performers on the regional gauge. Shares in Hong Kong and mainland China advanced after data showed the world’s second-largest economy hit the government growth target last year. Market weakness is expected to continue into next week’s meeting as the BOJ maintains cautiousness, said Kieran Calder, head of Asia equity research at Union Bancaire Privee in Singapore. “If we get only talk and no rate hike from the BOJ, then expect a sharp reversal” toward a weaker yen. Despite Friday’s drop, the key Asian stock gauge is still on track to eke out its first weekly gain of the year.

In currency markets, Bloomberg’s dollar index rose 0.1%, as data continue to highlight the strength of the US economy relative to developed-market peers. The pound slipped as much as 0.6% to near the weakest level since November 2023, after a surprise drop in retail sales added to evidence of a struggling British economy. The yen briefly strengthened through 155 against the dollar early Friday as expectations ramp up for an interest rate hike by the BOJ; it has since retreated and was the weakest of the G-10 currencies, falling 0.4% against the dollar even as traders boost bets on the BOJ raising rates next week. Despite the drop, the Japanese currency is still up more than 1% versus the dollar for the week. Tightening in Japan comes amid uncertain prospects for cuts by the Federal Reserve amid recent US economic data.

In rates, treasury futures hold small gains as US session gets under way, with yields at or near weekly lows. Long-end tenors lead, richer by more than 3bp, flattening the curve. UK gilts pace gains for government bonds globally for a second straight day, with yields lower by 5bp-7bp, after weaker-than-expected UK retail sales figures boosted wagers on BOE easing. Fed’s self-imposed quiet period ahead of Jan. 29 rate decision begins Saturday. With US front-end yields little changed, 2s10s spread is nearly 3bp flatter on the day; US 10-year around 3bp richer at 4.59%, trails UK counterpart by 3bp in the sector while keeping pace with Germany’s. Bunds stayed higher as euro area CPI was confirmed at 2.4% year-on-year in December. IG credit new-issue slate is dormant after GSIBs dominated an eight-deal, $27.6b calendar Thursday, taking weekly supply to nearly $47b, beyond the $40b projected

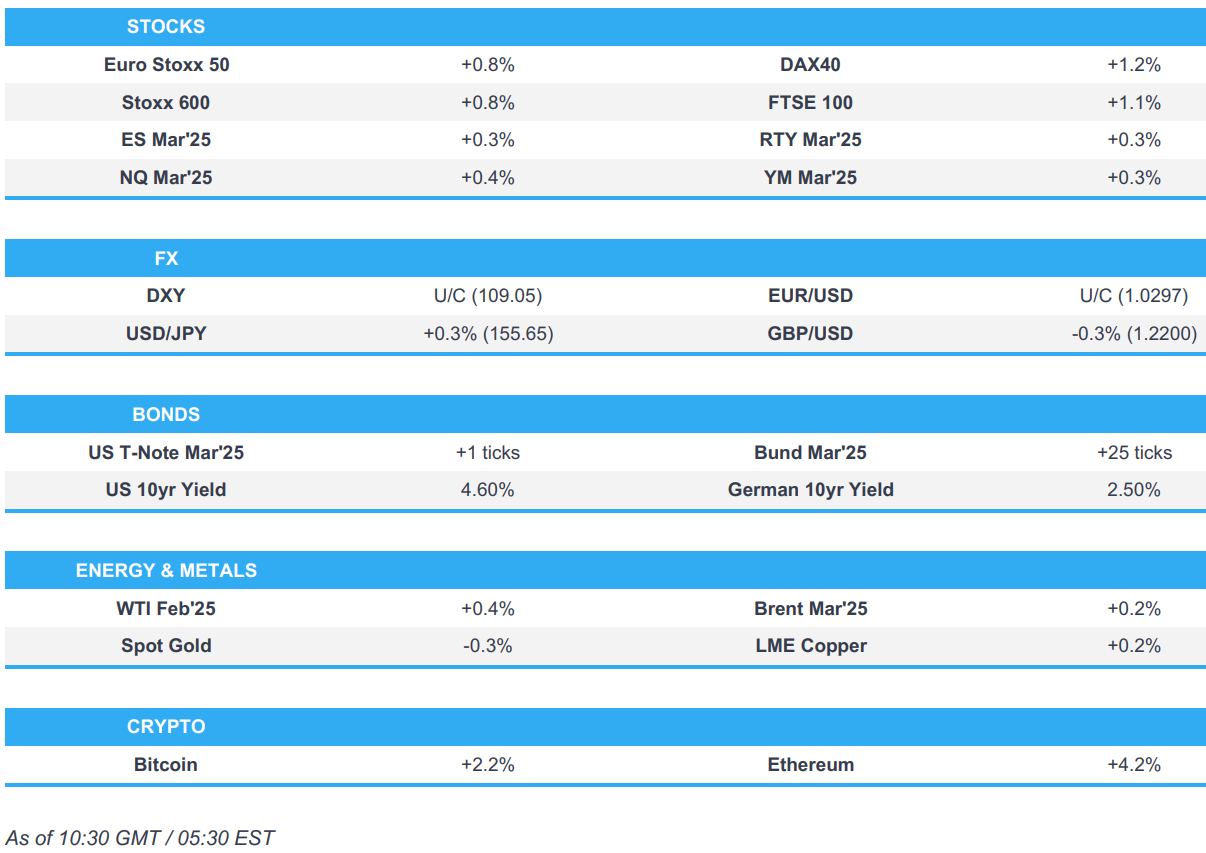

In commodities, WTI rises 0.6% to $79.20 a barrel. Spot gold drops $10 to $2,705/oz. Bitcoin rises 2% above $102,000.

The US economic data calendar includes December housing starts/building permits (8:30am), December industrial production (9:15am) and November TIC flows 4pm. Fed speaker slate is blank

Market Snapshot

- S&P 500 futures up 0.4% to 5,997.00

- STOXX Europe 600 up 0.7% to 523.45

- MXAP down 0.1% to 178.81

- MXAPJ little changed at 564.48

- Nikkei down 0.3% to 38,451.46

- Topix down 0.3% to 2,679.42

- Hang Seng Index up 0.3% to 19,584.06

- Shanghai Composite up 0.2% to 3,241.82

- Sensex down 0.5% to 76,635.61

- Australia S&P/ASX 200 down 0.2% to 8,310.38

- Kospi down 0.2% to 2,523.55

- German 10Y yield down 2 bps at 2.53%

- Euro little changed at $1.0298

- Brent Futures little changed at $81.33/bbl

- Gold spot down 0.2% to $2,708.07

- US Dollar Index up 0.11% to 109.08

Top Overnight News

- Fed’s Hammack (2026 voter; dissenter) says Fed can be patient on rate cuts; inflation remains an issue; adds that monpol is only moderately restrictive: WSJ

- BofA weekly total card spending: -0.8% Y/Y, “LA wildfire impact seems to be more localised since total card spending in California has only slowed modestly so far”.

- US President Trump reportedly planning an aggressive immigration in the first hours of his administration: “The package of actions amounts to a dramatic shift in immigration policy that will affect immigrants already residing in the United States and migrants seeking asylum at the US-Mexico border.” – CNN

- China’s economic data comes in ahead of expectations, including Q4 GDP (+5.4% vs. the Street +5%), industrial production (+6.2% vs. the Street +5.4%), and retail sales (+3.7% vs. the Street +3.6%). RTRS