GOLD CLOSED DOWN 4.30 TO $2905.00

SILVER CLOSED UP 1 CENTTO $32.21

GOLD ACCESS CLOSED 2928,50

Silver ACCESS CLOSED: $32.37

Bitcoin morning price:$96,321 DOWN 1000 DOLLARS.

Bitcoin: afternoon price: $96600 DOWN 721 DOLLARS

Platinum price closing UP $10.45 TO $995.80

Palladium price; UP $0.00 TO $978.95

END

*CANADIAN GOLD: $4158.02 UP 12.00 CDN dollars per oz( * NEW ALL TIME HIGH 4153.60 CDN DOLLARS PER OZ//FEB 10 2025)

*BRITISH GOLD: 2331.20 DOWN 9 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2,339.25 BRITISH POUNDS/OZ) FEB 10/2025

*EURO GOLD: 2,799.20 UP 4 Euros per oz //* (ALL TIME CLOSING HIGH: 2,807.66 EUROS PER OZ/FEB 10 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE

CONTRACT: FEBRUARY 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,909.000000000 USD

INTENT DATE: 02/12/2025 DELIVERY DATE: 02/14/2025

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 70

072 H GOLDMAN 1667

092 C DEUTSCHE BANK 6

104 C MIZUHO 2

118 C MACQUARIE FUT 1

118 H MACQUARIE FUT 333

132 C SG AMERICAS 7

190 H BMO CAPITAL 1031

323 C HSBC 986

323 H HSBC 86

332 H STANDARD CHARTE 78

363 C WELLS FARGO SEC 13

363 H WELLS FARGO SEC 406

435 H SCOTIA CAPITAL 287

624 C BOFA SECURITIES 12

657 C MORGAN STANLEY 127

657 H MORGAN STANLEY 816

661 C JP MORGAN 36 935

686 C STONEX FINANCIA 38 98

690 C ABN AMRO 7

700 C UBS 333

709 C BARCLAYS 97

709 H BARCLAYS 41

730 C PTG DIVISION SG 3

732 C RBC CAP MARKETS 125

737 C ADVANTAGE 11 22

880 C CITIGROUP 23

880 H CITIGROUP 50

905 C ADM 27

TOTAL: 3,887 3,887

MONTH TO DATE: 64,266

JPMorgan stopped (received) 0 contracts/3887

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2024. CONTRACT: 3887 NOTICES FOR 3887,00 OZ 12.090 TONNES

total notices so far: 64,286 contracts for 6,4286,00 Oz (199.96 tonnes)

FOR FEB.

SILVER NOTICES: 197 NOTICE(S) FILED FOR 0.985 MILLION OZ/

total number of notices filed so far this month : 4093 for 20.465 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $4.30 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.901 TONNES

INVENTORY RESTS AT 866.500 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.01 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.593MILLION OZ INTO THE SLV///

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 438.994MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGIZED SIZED 1088 CONTRACTS TO 165,339 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0,01 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A HUMONGOUS GAIN OF 1879 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE//WEDNESDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON WEDNESDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED A BIT ON WEDNESDAY WITH SILVER’S RISEIN PRICE BY 1 CENT. WE HAD A HUGE T.A.S. LIQUIDATION WEDNESDAY COUPLED WITH ANOTHER NEW MEGA MEGA HUGE T.A.S. ISSUANCE OF 6628 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.00 DOLLAR MARK. WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND 95 CENTS AND A LEASE RATE OF 6%. WE HAD A STRONG 791 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR MEGA HUGE 6628 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUMONGOUS SIZED 2005 CONTRACTS ON OUR TWO EXCHANGES WITH OUR SLIGHT GAIN IN PRICE. WE HAD HUGE TAS LIQUIDATION THROUGHOUT WEDNESDAY’S COMEX TRADING SESSION/

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE 6628 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.01 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS DESPITE HAVING A HUGE GAIN IN OUR TWO EXCHANGES OF 2005 CONTRACTS WE HAD A MASSIVE LIQUIDATION OF T.A.S. CONTRACTS ACCOUNTING FOR THE SMALL GAIN IN PRICE.

WE HAD A STRONG 791 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 67 CONTRACT QUEUE JUMP FOR 0.335MILLION OZ OZ

// STANDING FOR SILVER//FEB ADVANCES TO 20.835 MILLION OZ

WE HAD:

/ MEGA HUMONGOUS SIZED COMEX OI GAIN+// A STRONG SIZED EFP ISSUANCE/ VI) MEGA MEGA HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 6628 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 126CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 9 DAYS, total 7577 contracts: OR 37.785 MILLION OZ (841 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 37,785 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 33.80 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1088 CONTRACTS DESPITE OUR SMALL GAIN IN PRICE OF SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 791 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 10.105 MILLION OZ ON FIRST DAY NOTICE,FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 0.335 MILLION OZ TO LONDON//NEW STANDING ADVANCES TO 20,835MILLION OZ

WE HAVE 1). A MEGA HUMONGOUS SIZED GAIN OF 1879 OI CONTRACTS ON THE TWO EXCHANGES DESPITE OUR SMALL GAIN IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MEGA HUGE 6628 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//MONSTER FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION. HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON WEDNESDAY WITH THE SLIGHT GAIN IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (6628) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE

WE HAD 197 NOTICE(S) FILED TODAY FOR 0.985million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 668 OI CONTRACTS TO 528,081 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A STRONG SIZED 345 CONTRACTS//

WE HAD A SMALL SIZED DECREASE IN COMEX OI (413 CONTRACTS) OCCURRED DESPITE OUR LOSS OF $4.30 IN PRICE WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIALD STANDING IN GOLD TONNAGE FOR FEB AT 184.40 TONNES FOLLOWED BY A HUGE 1083 CONTRACT QUEUE JUMP//108300 OZ (3.368ONNES)

/NEW STANDING ADVANCES TO 206.034TONNES +18.4527

= 224.4867TONNES.

/ ALL OF THIS HAPPENED WITH OUR $4.30 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX ///. WE HAD A FAIR SIZED GAIN OF 2620 OI CONTRACTS (8.15PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE FRONT FEBRUARY CONTRACT MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3288 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 528,206

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1879 CONTRACTS WITH 668 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3288 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2620 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED AND CRIMINAL 2155 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3288 CONTRACTS) ACCOMPANYING THE SMALLSIZED DECREASE IN COMEX OI OF 668 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2620 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB 184.40 TONNES FOLLOWED BY TODAY’S MAMMOTH QUEUE JUMP OF 1083CONTRACTS FOR 108,300 OZ( 3.365 TONNES). AND THEN WE ADD OUR 4 EXCHANGE FOR RISK TOTALS OF 18.1413 TONNES//NEW TOTAL OF GOLD STANDING AT THE COMEX ADVANCES TO 224.4837TONNES

.

NEW STANDING FOR FEB ADVANCES TO:

206,038TONNES NORMAL DELIVERY (INCLUDING TODAY’S 3.368 TONNES QUEUE TUMP + .3114 TONNES OF EXCHANGE FOR RISK/TODAY + 18,1413 TONNES EX FOR RISK/PRIOR EQUALS 224.4867 TONNES

//NEW STANDING FEB: 224.4867TONNES WHICH IS THE HIGHEST EVER GOLD STANDING FOR A FEBRUARY DELIVERY MONTH. AND FOR ANY COMEX MONTH.

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE WEDNESDAY WITH ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WITH OUR1) $4.30PRICE LOSS, WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A FAIR GAINOF 1879 CONTRACTS ON OUR TWO EXCHANGES ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR RECORD NUMBER OF GOLD TONNES STANDING FOR FEBRUARY.

4) STRONG SIZED COMEX OPEN INTEREST DECREASE 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 2155 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

TOTAL EFP CONTRACTS ISSUED: 40,427 CONTRACTS OF 4042700 OZ OR 125,74 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 4642EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 125.74 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 125.74 DIVIDED BY 3550 x 100% TONNES = 3,54% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 125.74 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A GOOD SIZED ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 1088 CONTRACTS OI TO 165,339 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 791 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 791 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 791 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1088 CONTRACTS AND ADD TO THE 791 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1879 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 10.025 MILLION OZ OCCURRED DESPITE OUR $0.01 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 13.90 PTS OR 0.42%

//Hang Seng CLOSED DOWN 43.55 PTS OR 0.20 %

// Nikkei CLOSED UP 497.77 OR 1,28%//Australia’s all ordinaries CLOSED DOWN 0.55%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2970CHINESE YUAN OFFSHORE CLOSED UP TO 7.3109// Oil DOWNTO 70.45 dollars per barrel for WTI and BRENT DOWN AT 74.21 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

END

ASIA TRADING THURDAY MORNING/WEDNESDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 668 CONTRACTS TO 528,081 DESPITE OUR LOSS IN PRICE OF $4.30 WITH RESPECT TO WEDNESDAY’S TRADING. WE LOST ZERO NET LONGS HOWEVER WITH THAT PRICE LOSS FOR GOLD AS WE HAD ALSO, AS YOU WILL SEE BELOW, A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3288) . THE CME ANNOUNCED WEDNESDAY NIGHT, 100 EXCHANGE FOR RISK CONTRACTS FOR 10000 OZ OR .3114 TONNES

AND SO FAR IN FEBRUARY: WE HAVE HAD FIVE EXCHANGE FOR RISKSNOW TOTALLING 18.4527TONNES!. THE RECIPIENT OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY.

THUS IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1879 CONTRACTS WITH OUR LOSS IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE THURSDAY NIGHT (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW CLIMBED TO 10% AS GOLD IN LONDON IS NOW EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE WEEK INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND STRONG T.A.S. LIQUIDATION. WEDNESDAY NIGHT THEY ISSUED A STRONG 2155 CONTRACT ANNOUNCEMENT (WEDNESDAY NIGHT/THURDAY MORNING).

THE FED IS THE OTHER MAJOR SHORT OF AROUND 16+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, 202, 203 , 204 ,205 206, 207 208 AND TODAY’S 209, AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING LAST WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE ACTIVE DELIVERY MONTH OF FEBRUARY… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2875 EFP CONTRACTS WERE ISSUED: : /FEB 2875& ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2875 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2875 CONTRACTS IN THAT 3288 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 413 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $4.30 FOR WEDNESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. THE LOW GAIN IN TOTAL OI ON OUR TWO EXCHANGES WAS DUE TO LIQUIDATION OF T.A.S. SPREADERS!

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A STRONG SIZED SIZED 2114 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER A FEW WEEKS AGO, THE FED WAS EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( MONDAY TRADING// JAN 27) AS THE GOLD PRICE GOT HAMMERED A BIT WITH COMEX OPTIONS EXPIRY. AS YOU SAW WITH TUESDAY’S TRADING// JAN 28 IT HAS NO EFFECT ON GOLD AS IT SHOT UP AGAIN IN PRICE AND IT CONTINUED TO RISE THROUGHOUT THE WEEK. LONDON’S ANNOUNCEMENT LAST THURSDAY THAT THEY WERE OUT OF PHYSICAL GOLD SURELY HELPED TO PROPEL GOLD’S METEORIC RISE IN PRICE THESE PAST SEVERAL DAYS PROPELLING IT THROUGH THE 2800 DOLLAR BARRIER TO THE LEVEL IT IS NOW TRADING READY TO CLOSE IN ON THE 2900 DOLLAR LEVEL.

MECHANICS OF T.A.S CONTRACTS/DECEMBER 2024

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON DEC. 27, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE DECEMBER’S OPTIONS EXPIRY TRADING AND AGAIN WITH JANUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE. ALL OF THESE T.A.S. ISSUANCES WERE USED IN AN ATTEMPT TO THWART GOLD TRADING ESPECIALLY BEFORE TRUMP’S INAUGURATION AS THE FED MUST REDUCE ITS MASSIVE PHYSICAL GOLD SHORT OF 79 TONNES. THEY FAILED MISERABLY AS GOLD SKYROCKETED IN PRICE THIS WEEK AND NOW TO ALL TIME RECORD HIGHS IN USA DOLLAR TERMS AND OTHER CURRENCIES.

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAD A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (224.4867 TONNES) WHICH IS HUGE FOR OUR ACTIVE FEB DELIVERY MONTH AND THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH.

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 224.4867 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY: 206.034TONNES OF GOLD+ .3114 TONNES + 9.3264 TONNES OF EX. FOR RISK /PRIOR + 8.8149 TONNES EX FOR RISK PRIOR=//NEW TOTAL STANDING 224.4867 TONNES

COMEX GOLD TRADING/FEB CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELLBY $4.30//BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OUR TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION WEDNESDAY AS THEY WERE TRYING TO QUELL GOLD’S RISE AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING. THE BANKERS WERE UNSUCCESSFUL IN SLOWING THEIR DERIVATIVE LOSSES IN PRECIOUS METAL BETS WITH OPTIONS EXPIRY JAN 28 AT THE COMEX. OUR T.A.S. SPREADER LIQUIDATIONS THIS WEEK WERE DISTORTING OPEN INTEREST AS I EXPLAINED ABOVE, BUT IS HAVING NO EFFECT ON GOLD’S METEORIC RISE IN PRICE. ON FRIDAY , JAN 31 WAS OPTIONS EXPIRY FOR LONDON’S OTIC/LBMA OPTIONS/JAN 31/ AS OUR BANKER CROOK’S DESPERATELY TRIED TO CONTAIN GOLD’S PRICE FROM ATTAINING THE 2800 DOLLAR LEVEL AND THEY FAILED AND THE PRICE OF GOLD SKYROCKETED SINCE. THEIR DERIVATIVE LOSSES CONTINUE TO MOUNT EACH AND EVERY DAY!@!

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING THURDAY MORNING AND THUS OUR RECORD NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD)

EXCHANGE FOR RISK EXPLANATION/DECEMBER AND JANUARYTRADING

DECEMBER MONTH EXCHANGE FOR RISK!

57 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 6 FOR 14.6836 TONNES A NEW RECORD. THE COMEX IS TOTALLY SHATTERED TO PIECES.

EXCHANGE FOR RISK // JANUARY MONTH!!

LO AND BEHOLD, THE CROOKS ISSUED THEIR FIRST ISSUANCE A MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THEN TO MY HORROR, THEY ISSUED THEIR SECOND EXCHANGE FOR RISK ON JAN 8, TOTALLING 150 CONTRACTS FOR 15000 OZ OR .4665 TONNES. THIS TONNAGE WILL BE ADDED TO THE FIRST ISSUANCE. THUS TOTAL EXCHANGE FOR RISK ISSUANCE FOR OUR TWO EARLY JANUARY EX FOR RISK: 5.7533 TONNES. THEN MERCILESSLY THEY CONSUMMATED FOR THE THIRD TIME THIS MONTH 85 EXCHANGE FOR RISK LAST THURSDAY NIGHT (JAN 17) FOR 8500 OZ OR .2649 TONNES OF GOLD. THEN TO MY HORROR THEY ISSUED THEIR 4TH EXCHANGE FOR RISK THIS MONTH (JAN 22) FOR A MONSTER 5000 CONTRACTS OR 5,000,000 OZ.(15.562 TONNES).NOT TO BE UNDONE, THE CROOKS ISSUED THEIR FIFTH EXCHANGE FOR RISK LAST NIGHT FOR 500 CONTRACTS REPRESENTING 50,,000 OZ OR 1.555 TONNES OF GOLD. REMEMBER THAT THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON WHICH IS TOTALLY ASININE!! THUS FOR THE 5 EXCHANGE FOR RISK ISSUED THIS MONTH TOTALS 23.134 TONNES OF GOLD. THIS BRINGS US TO , JAN 25 WHERE THE CME ANNOUNCED ITS SIXTH MAJOR EXCHANGE FOR RISK ISSUANCE OF 6454 CONTRACTS FOR 645,400 OZ OR 20.074 TONNES OF GOLD. THIS IS THE HIGHEST EVER RECORDED ISSUANCE IN NUMBER OF EXCHANGE FOR RISK, AT 6, AND FOR NEW TOTALS FOR THE MONTH OF JANUARY: 43.208 TONNES!!! AND A NEW RECORD FOR ISSUANCE.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO, THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. THIS TOTAL WILL NOW BE ADDED TO OUR REGULAR DELIVERIES THROUGHT THE MONTH. MONDAY ZERO EXCHANE FOR RISK WAS ISSUED.

FINAL STANDING GOLD/COMEX FOR JANUARY

FINAL STANDING FOR JAN: 70.102TONNES + 43.206 TONNES EX FOR RISK = 113.310 TONNES (WHICH IS HUGE FOR OUR VERY NON ACTIVE DELIVERY MONTH) A NORMAL AMOUNT STANDING FOR A JANUARY IN EARLIER TIMES HAS BEEN GENERALLY AROUND 1/4 TONNE OF GOLD. HOWEVER THESE PAST 4 YEARS QUEUE JUMPING HAS BEEN VERY PRONOUNCED AND THUS STANDING INCREASES DRAMATICALLY.

TOTAL INITIAL DELIVERIES FEB GOLD TRADING

WE HAVE GAINED A FAIR TOTAL OF 8,15 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB (184.40TONNES) ON FIRST DAY NOTICE FOLLOWED BY A MASSIVE SIZED 1083 CONTRACT QUEUE JUMP FOR 108,300OZ. NEW STANDING ADVANCES TO 206.034TONNES OF GOLD. TO WHICH WE ADD OUR 18.4527TONNES OF EXCHANGE FOR RISK//NEW TOTALS STANDING 224.4867TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.30

WE HAD 345 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 2620 CONTRACTS OR 262000 OZ (8.15ONNES)

confirmed volume WEDNESDAY 218,896contracts: FAIR///

//speculators have left the gold arena

END

// THE FEB 2025 GOLD CONTRACT

FEB 12

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | . |

| Deposit to the Dealer Inventory in oz | 0 i) Brinks dealer 258,010.326 oz 8(025 kilobars) 2. ASAHI dealer 64,121.026 oz 3. Loomis 28,935,900 oz 900 kilobars total dealer 351,067.252 oz 10.919 tonnes |

| Deposits to the Customer Inventory, in oz | 2 ENTRIES i)Into Brinks customer acct 237,583.797 oz ii) into Malca 12,860.400 oz ( 400 kilobars) total weight 250,444.197 oz or 7.78 tonnes total weight dealer and customer: 18.708 oz |

| No of oz served (contracts) today | 3887 notice(s) 388,700 OZ 12.090TONNES |

| No of oz to be served (notices) | 1954contracts 195400 0OZ 6.077 TONNES |

| Total monthly oz gold served (contracts) so far this month | 64,286notices 6,428,600oz 199.96 ONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 3

i) Brinks dealer 258,010.326 oz

8(025 kilobars)

2. ASAHI dealer 64,121.026 oz

3. Loomis 28,935,900 oz 900 kilobars

total dealer 351,067.252 oz

10.919 tonnes

we have 52customer deposits

2 ENTRIES

i)Into Brinks customer acct 237,583.797 oz

ii) into Malca 12,860.400 oz ( 400 kilobars)

total weight 250,444.197 oz or 7.78 tonnes

total weight dealer and customer: 18.708 oz

withdrawals: 0

adjustments:3//comex is in chaos

first 2 customer to dealer

a) Brinks 64,334.151 oz

b)Manfra 64,237,698 oz

d

next //dealer to customer

A) HSBC 179.656 oz

thus basically what comes into eligible is transferred to dealer accounts and then out.

I

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB

FEB HAD A LOSS OF 1213 CONTRACTS TO STAND AT 5841 WE HAD 2296 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED A HUGE 1083 CONTRACTS OR A MONSTER 108,300 OZ QUEUE JUMP OR 3.308TONNES

MARCH HAD A GAIN OF 64 CONTRACTS UP TO 15,199

APRIL HAD A LOSS OF 769 CONTRACTS UP TO 394,504 CONTRACTS

We had 3887contracts filed for today representing 388,700 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 816 notices issued from their client or customer account. The total of all issuance by all participants equate to 3887 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2025. contract month, we take the total number of notices filed so far for the month (64,286x 100 oz ) to which we add the difference between the open interest for the front month of FEB.(5841 CONTRACTS) minus the number of notices served upon today (3887 x 100 oz per contract) equals 6,624,000 OZ OR 206.034TONNES to which we must add our latest 2834 contract exchange for risk TODAY FOR .3114 TONNES TO WHICH WE ADD 18.1413 tonnes ex for risk //NEW EXCHANGE FOR RISK 18.4527 TONNES//NEW TOTAL STANDING 224.4867 TONNES

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (64,286x 100 oz +we add the difference for front month of FEB ( 5841 OI} minus the number of notices served upon today (3887 x 100 oz) which equals 6,624,000oz (195.8690 TONNES + 0.3114tonnes ex for risk/TODAY + 818.1414 tonnes ex for risk PRIOR = 224.4867 tonnes

TOTAL COMEX GOLD STANDING FOR FEB.: 224.4867 ONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR AND THIS IS THE HIGHEST EVER RECORDED FOR ANY FEBRUARY AND THE HIGHEST FOR ANY MONTH FOR THAT MATTER IN COMEX HISTORY!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,075,081.256 oz 64.54 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 37,055,805.165 oz

TOTAL REGISTERED GOLD 16,700,593.788 or 519.458tonnes

TOTAL OF ALL ELIGIBLE GOLD: 20,233,159.373 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,625,512oz (REG GOLD- PLEDGED GOLD)= 454.914tonnes //

END

SILVER/COMEX

FEB 12

INITIAL

// THE FEB 2025 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1) Brinks 25,847,220oz ii) HSBC 100,093,890 oz total 125,941.119 oz |

| Deposits to the Dealer Inventory | 604,425.34 oz Brinks dealer |

| Deposits to the Customer Inventory | 5 entries i)Brinks 2026.408 oz ii) HSBC 627,400 oz iii) JPM 1,316,114.800 oz iv) Loomis 564,927.400 oz v) Manfra 550,120,241 oz total: 3060,840.249 oz |

| No of oz served today (contracts) | 197CONTRACT(S) (0.985MILLION OZ |

| No of oz to be served (notices) | 74 contracts (0.370 MILLION oz) |

| Total monthly oz silver served (contracts) | 4093 Contracts (20.465 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 1-dealer deposit/

604,425.34 oz Brinks dealer

total 604,425.34 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

deposits:

5entries

)Brinks 2026.408 oz

ii) HSBC 627,400 oz

iii) JPM 1,316,114.800 oz

iv) Loomis 564,927.400 oz

v) Manfra 550,120,241 oz

total: 3060,840.249 oz

withdrawals 2

1) Brinks 25,847,220oz

ii) HSBC 100,093,890 oz

total 125,941.119 oz

ADJUSTMENTs 0

JPMorgan has a total silver weight: 152,004million oz/375.843million or 40.53%

TOTAL REGISTERED SILVER: 96.193 MILLION OZ//.TOTAL REG + ELIGIBLE. 375.843million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB /2025 OI: 271 OPEN INTEREST CONTRACTS FOR A LOSS OF 202 CONTRACTS.

WE HAD 269NOTICES FILED ON WEDNESDAY SO WE GAINED 67 CONTRACTS OR WE EXPERIENCED A 335,000 OZ EXCHANGE QUEUE JUMP AS THESE GUYS WILL TRY THEIR LUCK AT THE COMEX TRYING TO OBTAIN PHYSICAL SILVER.

MARCH SAW A LOSS OF 5874 CONTRACTS DOWN TO 90,517THE FRONT ACTIVE DELIVERY MONTH OF MARCH ALSO IS NOT DECLINING MUCH AND WE SHOULD ALSO HAVE A HUMDINGER OF A DELIVERY MONTH FOR MARCH.

APRIL SAW ANOTHER GAIN OF 80 CONTRACTS TO STAND AT 422

MAY SAW A GAIN OF 6342CONTRACTS UP TO 53,651 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 197 or 0.985MILLION oz

CONFIRMED volume; ON WEDNESDAY 87,595 good//

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 4093x 5,000 oz = 20.465 MILLION oz

to which we add the difference between the open interest for the front month of FEB (271) and the number of notices served upon today (197)x (5000 oz)

Thus the standings for silver for the FEB 2025 contract month: 4093 Notices served so far) x 5000 oz + OI for the front month of FEB(271)minus number of notices served upon today (197)x 5000 oz equals silver standing for the FEB contract month equating to 20.835 MILLION OZ.

New total standing: 20,835million oz which is huge for a non active delivery month of February

There are 92.849 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

FEB 13/ WITH GOLD UP 11.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 6.901 TONNES FROM THE GLD ///INVENTORY RESTS AT 866.50TONNES

FEB 12 WITH GOLD DOWN $3,40ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 10 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 7 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 6 WITH GOLD DOWN $18.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.14 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

FEB 5 WITH GOLD UP $27.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 863.05 TONNES

FEB 4 WITH GOLD UP $25.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.58 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.77 TONNES

JAN 31 WITH GOLD UP $4.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 30 WITH GOLD UP $40.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 865.34 TONNES

JAN 29 WITH GOLD DOWN $6.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.02 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 861.04 TONNES

JAN 28 WITH GOLD UP $23.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.16 TONNES OF GOLD OUT OF THE GLD //

JAN 27 WITH GOLD DOWN $36.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///

JAN 24 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 23 WITH GOLD DOWN $1.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 2.30 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 869.36 TONNES

JAN 22 WITH GOLD UP $15.15 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 7.46 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 871.66 TONNES

JAN 20 WITH GOLD UP $35.30 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 10.34 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 879.12 TONNES

/JAN 17 WITH GOLD DOWN $9.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.74 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 868.78 TONNES

JAN 16 WITH GOLD UP $24.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 872.52 TONNES

JAN 15 WITH GOLD UP $24.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 872.52 TONNES

JAN 14 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 874.53 TONNES

JAN 13 WITH GOLD DOWN $27.75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A DEPOSIT OF 5.74 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 876.82 TONNES

JAN 10 WITH GOLD UP $17.80 ON THE DAY; NO CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 9 WITH GOLD UP $13.85 ON THE DAY; NO CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 8 WITH GOLD UP $5.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD::A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD ///INVENTORY RESTS AT 871.08 TONNES

JAN 7 WITH GOLD DOWN $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 6 WITH GOLD DOWN $4.90 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 3 WITH GOLD DOWN $14.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 2 WITH GOLD UP $29.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 31 WITH GOLD UP $20.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 30 WITH GOLD DOWN $11.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.28 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.52 TONNES

DEC 27 WITH GOLD DOWN $17.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.80 TONNES

DEC 26 WITH GOLD UP $17.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: : ///INVENTORY RESTS AT 873.95 TONNES

DEC 24 WITH GOLD UP $6.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES OF GOLD OUT OF THE GLD. / // : .///INVENTORY RESTS AT 873.95 TONNES

DEC 23 WITH GOLD DOWN $13,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 16.66 TONNES OF GOLD VAPOUR GOLD INTO THE GLD. / // : .///INVENTORY RESTS AT 877.40 TONNES

DEC 20 WITH GOLD UP $29,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 860.74 TONNES

DEC 19 WITH GOLD DOWN $45.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF .29 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 18 WITH GOLD DOWN $8.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 17 WITH GOLD DOWN $6.85 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.23 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 16 WITH GOLD DOWN $2.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.70 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 13 WITH GOLD DOWN $24.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.78 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 868.60 TONNES

DEC 12 WITH GOLD DOWN $34.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.59 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 873.38 TONNES

DEC 11 WITH GOLD UP $29.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 9 WITH GOLD UP $31.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD. // : .///INVENTORY RESTS AT 871.94 TONNES

GLD INVENTORY: 866.500TONNES, TONIGHTS TOTAL

SILVER

FEB 12WITH SILVER DOWN $.03//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 12WITH SILVER UP $.01 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 8 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 10 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 7 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 6 WITH SILVER DOWN $0.17 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 12.383 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 430.39 MILLION OZ

FEB 5 WITH SILVER UP $0.45 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 3.285 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 442.773 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 3 WITH SILVER UP ONE CENT //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

JAN 31 WITH SILVER DOWN $0.19 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.369 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 448.881 MILLION OZ

jAN 30 WITH SILVER UP $0.76 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.003 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 451.249 MILLION OZ

jAN 29 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.639 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 453.252 MILLION OZ

jAN 28 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.821 MILLION OZ OUT OF THE SLV./. /

jAN 27 WITH SILVER DOWN $.61 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 24 WITH SILVER DOWN $.21 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 23 WITH SILVER DOWN $.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 4.738 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 459.035 MILLION OZ

JAN 22 WITH SILVER UP $.08 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 0.721 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 464.043 MILLION OZ

JAN 20 WITH SILVER DOWN $.09 //NO CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.568 MILLION OZ FROM THE SLV./. //INVENTORY AT SLV RESTS AT 463.315 MILLION OZ

JAN 17 WITH SILVER DOWN $.49 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.568 MILLION OZ FROM THE SLV./. //INVENTORY AT SLV RESTS AT 463.315 MILLION OZ

JAN 16 WITH SILVER UP $0.23 //NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 464.863 MILLION OZ

JAN 15 WITH SILVER UP $0.79 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.745 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 464.863 MILLION OZ

JAN 14 WITH SILVER UP $0.15 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.228 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 460.218 MILLION OZ

JAN 13 WITH SILVER DOWN $0.69 //NO CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.637 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 459.990 MILLION OZ

JAN 10 WITH SILVER UP $0.19 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 459,353 MILLION OZ

JAN 9 WITH SILVER UP $0.08 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 459,353 MILLION OZ

JAN 8 WITH SILVER DOWN $0.01 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.484 MILLION OZ OUT OF THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 7 WITH SILVER UP 48 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 6 WITH SILVER UP 38 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 3 WITH SILVER UP 17 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 2 WITH SILVER UP 45 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.616 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 462.128 MILLION OZ

DEC 31 WITH SILVER DOWN 14 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 30 WITH SILVER DOWN 39 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: // A WITHDRAWAL OF 1.13 MILLION OZ FROM THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 27 WITH SILVER DOWN 24 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY AT SLV RESTS AT 461.651 MILLION OZ

DEC 24 WITH SILVER UP 2 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 23 WITH SILVER UP 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 6.15 MILLION OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 20 WITH SILVER UP 43 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 183,000 OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 457.597 MILLION OZ

DEC 19 WITH SILVER DOWN 25 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV///// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 18 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 17 WITH SILVER DOWN 12 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.456 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 16 WITH SILVER DOWN 0 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 4.84 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 13 WITH SILVER DOWN 46 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .536 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 462.892 MILLION OZ

DEC 12 WITH SILVER DOWN 94 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 5.787 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 463.428 MILLION OZ

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 10 WITH SILVER DOWN 8 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.868 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 471.812 MILLION OZ

DEC 9 WITH SILVER UP $0.91 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.367 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 473.680 MILLION OZ

CLOSING INVENTORY 438,994 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

END

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ALASDAIR MACLEOD

Trump and Ukraine

Trump’s surprise détente with Russia is well thought out. The surprise is the speed with which it is being implemented. Zelensky and the EU have been caught off-guard.

| Alasdair MacleodFeb 13∙Paid |

The first thing to know is that with respect to the Ukraine proxy war the Biden administration and NATO establishment were driving opinion by propaganda in defiance of the facts. By pointing out the facts on the ground, seasoned experts such as Professor Jeffrey Sachs, Professor John Mearsheimer, Colonel Douglas Macgregor, and Dr Gilbert Doctorow between them have consistently exposed this propaganda as false.

So what now?

The fact of the matter is that the Biden administration miscalculated, thinking that through a Ukrainian proxy war America could destabilise Russia, overthrow Putin, and presumably face down China on her western and norther borders. Instead, Russia has not only survived the assault but is winning on the battlefield. Trump realises that Russia has no expansionary intentions other than to secure its naval base in Crimea and the Russian-speaking oblasts in Eastern Ukraine. Furthermore, it is crucial for Russia that the rest of Ukraine remains neutral and does not join NATO or the EU.

The art-of-the-deal president realises this. It is not a matter of negotiations over the principles, only the detail. And the speed with which this change in US policy is being implemented will save Ukrainian lives and recognise earlier policy errors. It is commendable.

Meanwhile, the western media, which has been spoon-fed disinformation is having difficulty adjusting to this new reality. But it will, and quite quickly as well, particularly when it gets background briefings from the White House. Other than Zelensky, the Brussels establishment is horrified, and particularly so because they were not even consulted. They have been brutally informed by U.S. Defense Secretary Pete Hegseth that there will be no American troops in Ukraine, and that Europe will have to make its own defence arrangements in future.

Effectively, it forces a reorganisation of priorities for NATO. If NATO is to survive a US withdrawal and to prevent its own redundancy, it will have to find a role coordinating European defence including the UK and EU member states.

These developments are excellent news for Germany and Hungary in particular: Germany because Russian trade will reopen for mutual benefit, and Hungary where Victor Orbán has proved right all along, defying his critics in Brussels. All that needs to follow is for Germany’s free-market AfD to gain power in forthcoming elections on 23 February, and the nonsense which has been so damaging to her economy will be properly addressed and remedied.

Good news for Germany is good news for the EU. It is bad news for the woke socialism and statism of France and Spain. But note: none of this addresses the serious financial problems of the Eurozone. Not does it change the outlook for the dollar. For the latter to happen, Musk’s DOGE will have to be on its way to achieving its mandate of saving at least a trillion dollars in wasteful spending.

4. ANDREW MAGUIRE/LIVE FROM THE VAULT NO 209

—–

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY//COFFEE

Citi Warns Arabica Coffee Rally May Have Peaked As Demand Destruction Looms

Thursday, Feb 13, 2025 – 06:55 AM

Arabica coffee futures have recorded a parabolic rally this year due to tightening supplies from top grower Brazil. However, demand may diminish at these record-high prices, potentially capping further price gains.

Citi analyst Arkady Gevorkyan told clients that arabica coffee’s three-month price target and 2025 average price target are around $3.30 per pound. He stated that high-end arabica beans – favored by Starbucks and other top brands – “have likely peaked as demand starts to curtail and supplies replenish.”

Early Wednesday morning, arabica coffee futures in New York peaked around $4.27 a pound after hitting a record $4.295 on Tuesday. Gevorkyan also expects 2025-26 Brazilian arabica supply at 62.6 million bags, down 5 million from the current market year.

However, late last week, Andrea Illy, chairman of Italian roaster Illycaffè SpA, joined Bloomberg TV for an interview in which he warned that Arabica coffee futures could surge another 20–25% in the coming months.

Illy explained that soaring prices would likely lead to demand destruction as consumers are forced to reduce coffee consumption. He added that the rally in arabica futures—currently on its longest upward streak on record—is primarily driven by supply concerns in Brazil and fears that adverse weather conditions could impact the country’s next Arabica harvest.

Besides bean stocks at exchange-monitored warehouses, Illy warned it’s unclear how much supply is available in some of these top-producing countries. He described the situation: “We are navigating this market blind.”

end

6 CRYPTOCURRENCY NEWS

END

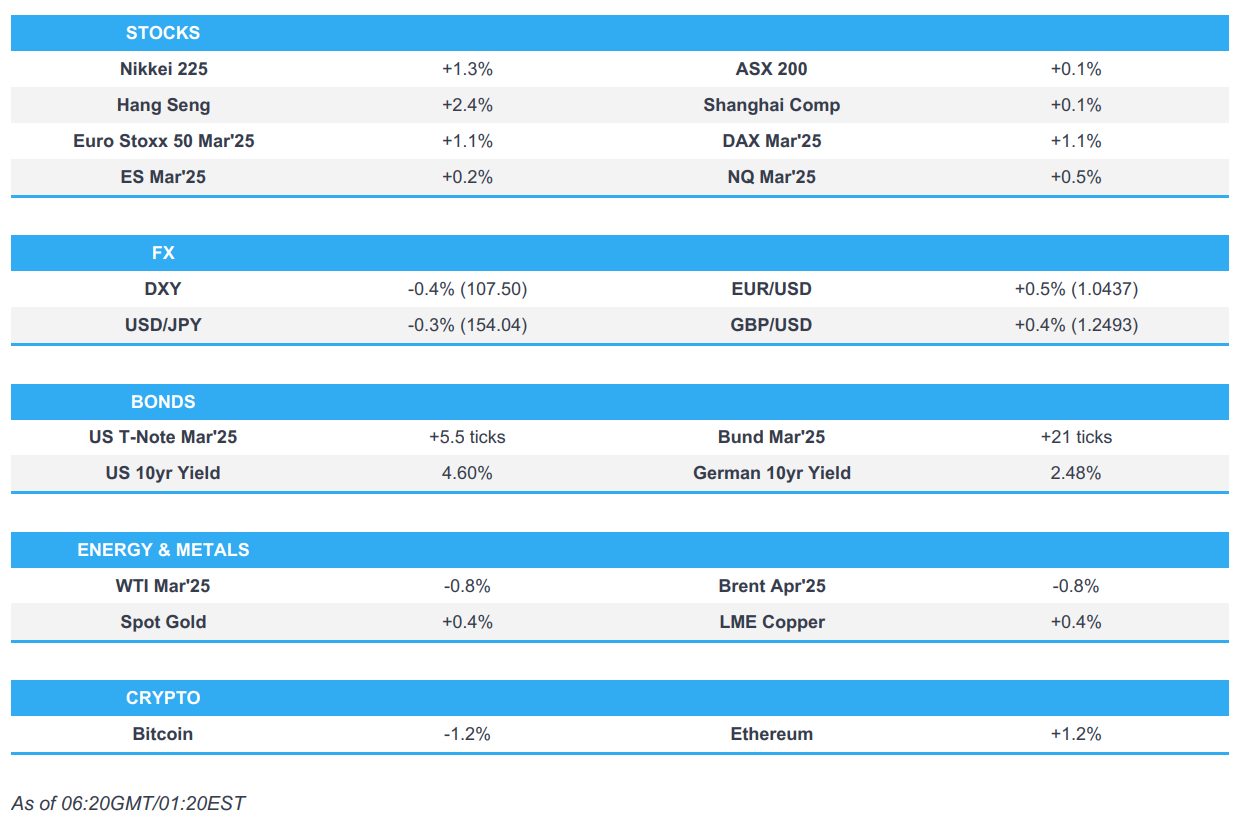

ASIA TRADING THURSDAY MORNING WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 13.90 PTS OR 0.42%

//Hang Seng CLOSED DOWN 43.55 PTS OR 0.20 %

// Nikkei CLOSED UP 497.77 OR 1,28%//Australia’s all ordinaries CLOSED DOWN 0.55%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2970CHINESE YUAN OFFSHORE CLOSED UP TO 7.3109// Oil DOWNTO 70.45 dollars per barrel for WTI and BRENT DOWN AT 74.21 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.2970

OFFSHORE YUAN: DOWN TO 7.3109

SHANGHAI CLOSED CLOSED DOWN 13.90 PTS OR 0.42%

HANG SENG CLOSED CLOSED DOWN 497.77 PTS OR 1.25%

2. Nikkei closed UP 497.77 OR 1.25%

3. Europe stocks SO FAR: MOSTLY ALL GREEN

USA dollar INDEX DOWN TO 107.52 EURO RISES TO 1.0421 UP 29 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: RISES TO. +1.336 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 153.82…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP// CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR DOWN this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4465Italian 10 Yr bond yield DOWN to 3.5044/SPAIN 10 YR BOND YIELD DOWNTO 3.094

3i Greek 10 year bond yield DOWN TO 3.276

3j Gold at $2916.85/Silver at: 32.24 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 3 AND 17/100 roubles/dollar; ROUBLE AT 90.82

3m oil into the 70 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 153,82 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.336% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9075 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9438well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.601 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.805 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.338 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 36.11…

10 YR UK BOND YIELD: 4.5830 UP 7 PTS

10 YR CANADA BOND YIELD: 3.208 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.866 DOWN 1 PTS.

2a New York OPENING REPORT

Futures Flat Ahead Of PPI, Reciprocal Tariff

Thursday, Feb 13, 2025 – 08:21 AM

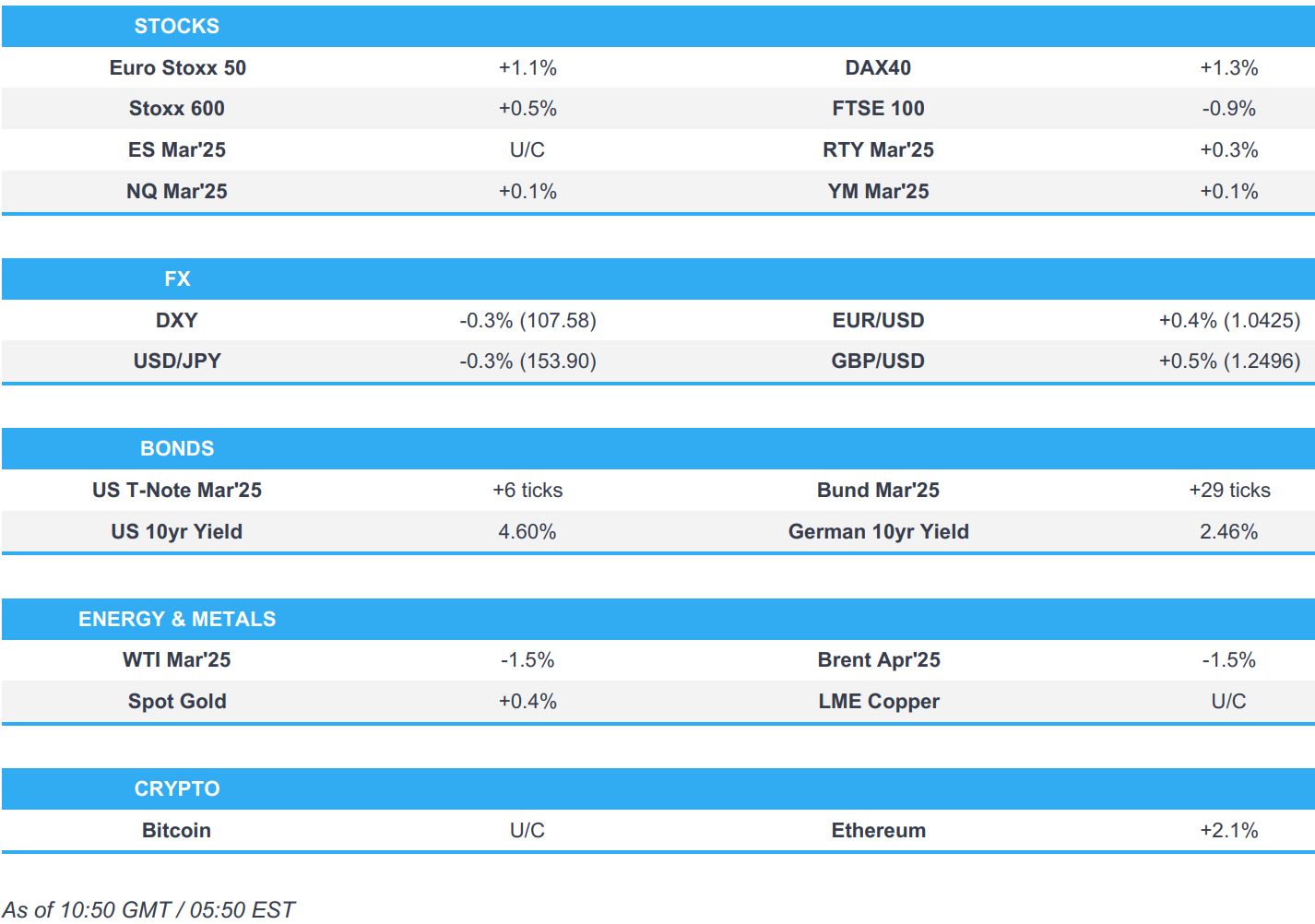

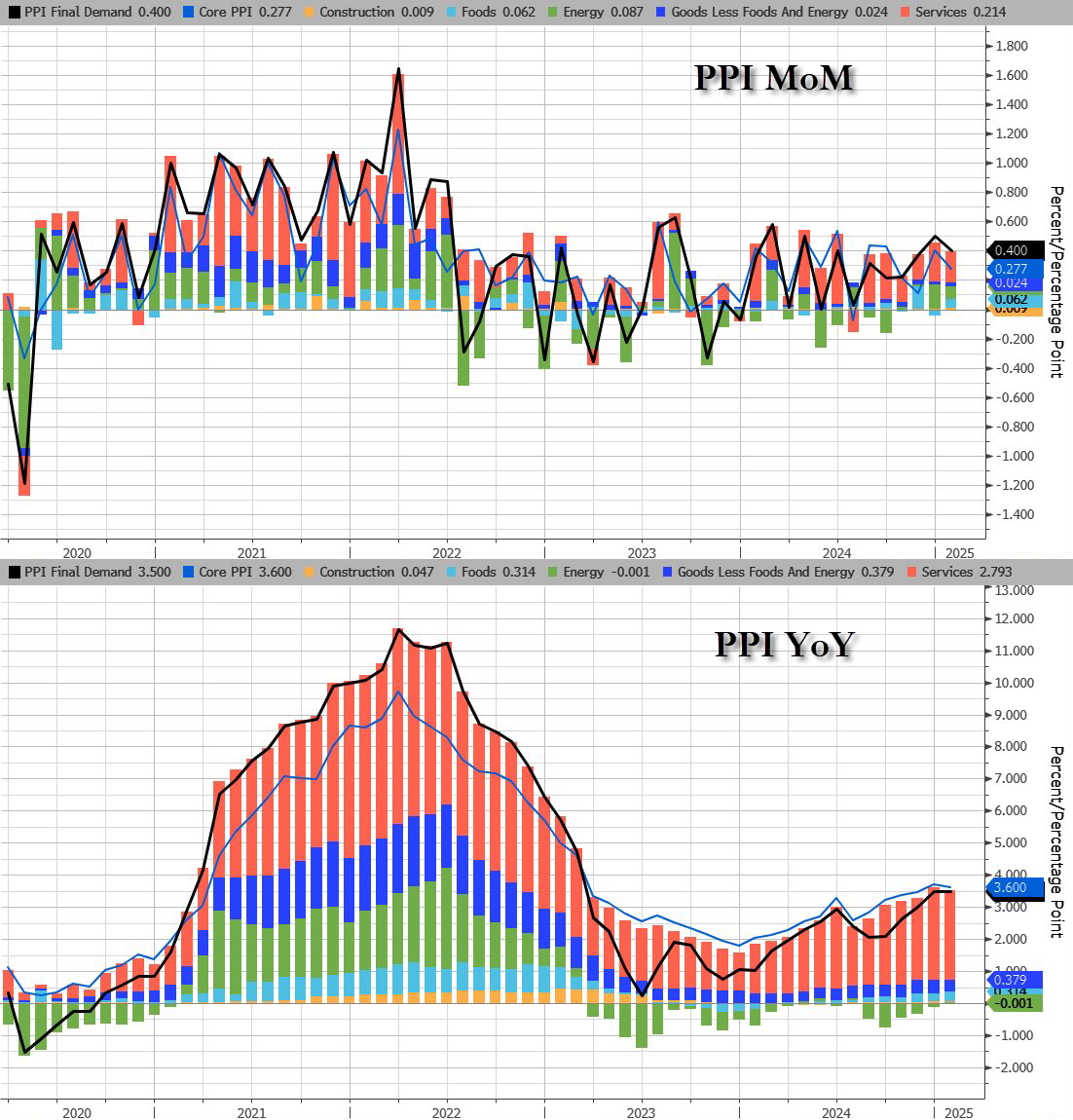

Futures are flat, Europe’s Stoxx 600 slipped from session highs and the euro gave up an earlier advance against the dollar sparked by hopes for a Ukraine war ceasefire, after President Donald Trump signaled he’s about to announce reciprocal tariffs on trading partners, just as we warned last night he would. As of 8:00am ET, S&P futures are down 0.1% while Nasdaq futures rise by a similar percentage even as Chinese technology stocks saw a dramatic intraday turnaround to finish lower. TSLA is up 2.2% pre-market with the rest of Mag 7 largely unchanged this morning; CSCO rose 6.8% on the back of a higher revenue forecast. Bond yields are 2-3bp lower, while the USD reversed an earlier loss. Commodities are mostly lower: WTI and aluminum are -1.5% and -0.9% lower, respectively. Today, the macro focus will be PPI and any updates on Trump’s reciprocal tariff plan which the president said in a social media post will be announced on Thursday. Futures contracts on the S&P 500 and Nasdaq 100 erased early gains, while

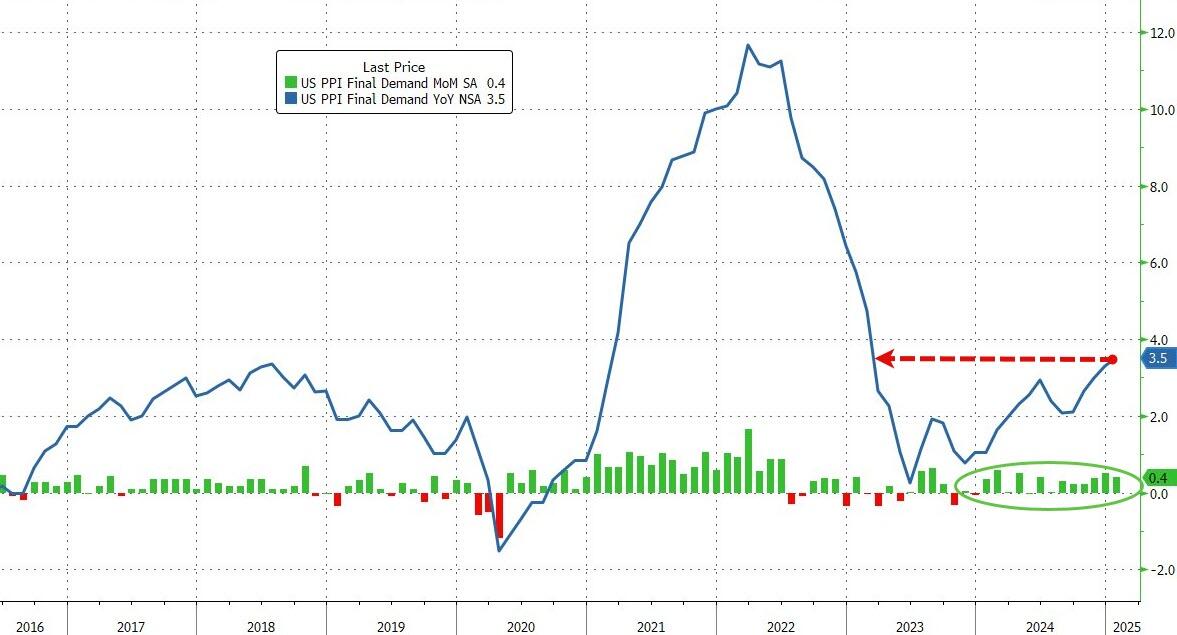

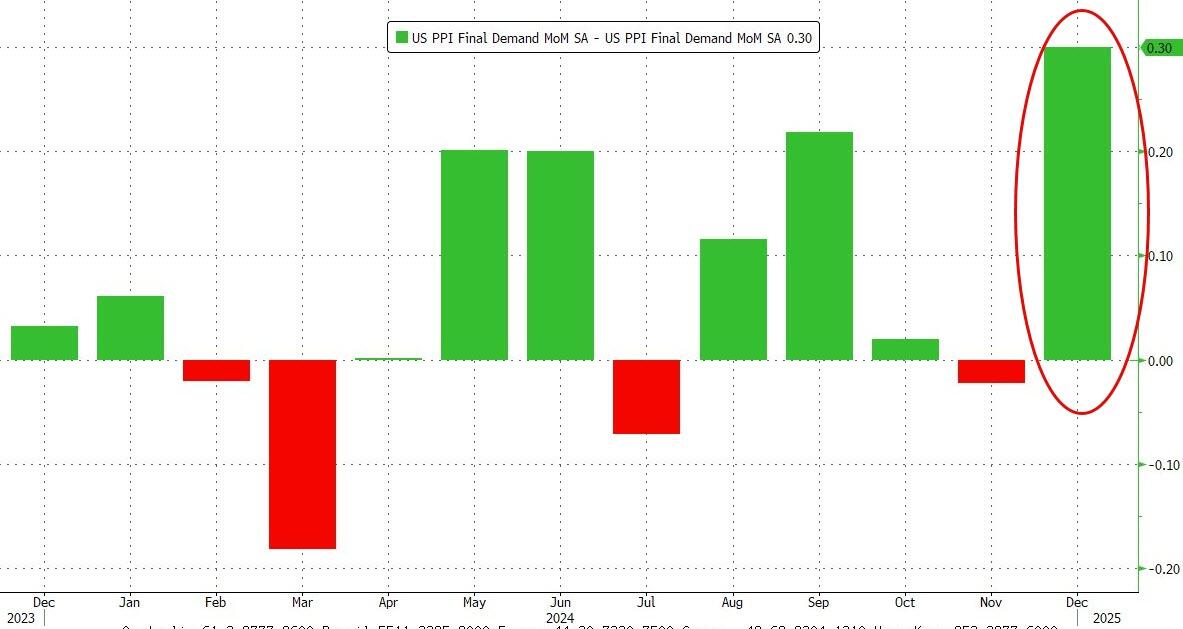

While the main economic event of the day will be the January PPI (expected at 0.3% MoM and 3.3% YoY for both headline and core), traders will be focused instead on the latest front in Trump’s trade war after the president said in a Truth Social post the new levies will be announced on Thursday.

In premarket trading, Apple leads losses for the Mag7 as Tesla shares are up, putting the stock on track to extend gains after snapping a five-session streak of losses( Apple -0.4%, Nvidia, Alphabet, Amazon, Meta Platforms were edging lower, while Tesla +2.3%). Reddit shares tumbled as much as 18% after the social network reported fewer-than-expected daily active users. Jefferies said the user miss raises growth questions. Here are some more premarket movers:

- 10X Genomics shares sink 8.3% in premarket trading after the maker of biological-research equipment forecast revenue for 2025, without accounting for impact from the National Institutes of Health’s decision to put a cap on how much research institutions can charge the government. Analysts trim their price targets citing uncertainty and risks to the firm’s guidance.

- Albemarle shares rise 3.1% in premarket trading after the lithium producer reported adjusted Ebitda for the fourth quarter that was better than Wall Street’s expectations. Analysts also see the firm reaching breakeven free cash flow in 2025.

- Aspen Aerogels shares plunge as much as 34% in US premarket trading after the thermal insulation products maker’s first-quarter guidance fell short of expectations and it refrained from giving a full-year outlook. Analysts said this impacted the company’s visibility, and raised questions over orders from its client General Motors.

- Deere shares fall as much as 8.7% in premarket trading on Thursday as the tractor maker maintained its outlook as a slumping agriculture sector continues to hit farm machinery tractor sales.

- Dutch Bros shares soar 24% in premarket trading after the drive-thru coffee chain’s total revenue forecast for 2025 exceeded analyst estimates. Additionally, the company reported fourth-quarter comparable sales that topped consensus.

- Fastly shares fall as much as 21% in US premarket trading after the infrastructure software company’s outlook for the year disappointed, with analysts pointing to a hit from investments. However, some brokers noted that the guidance could be conservative given it doesn’t include US revenues from customer TikTok.

- HubSpot shares rise as much as 5.7% in premarket trading after the software company reported fourth-quarter results that beat expectations. KeyBanc upgrades the stock saying “there are a few indicators that 2025 could see material upside.”

- Kraft Heinz shares fall 1.3% in premarket trading after BofA downgraded the packaged-food company to underperform from buy, saying its organic sales are trending in the wrong direction.

- MGM Resorts shares jump 9.2% in premarket trading after the gaming and entertainment company reported fourth-quarter adjusted earnings per share that came ahead of estimates.

- Paycom Software shares are up 2.9% in premarket trading, after the company reported fourth-quarter results that beat expectations and gave an outlook analysts see as encouraging. It also named a new CFO.

- Robinhood Markets shares jump 16% in premarket trading after the retail brokerage reported fourth-quarter net revenue that topped expectations, with cryptocurrency revenue soaring as the US election fueled trading in digital assets.

- Target and Macy’s shares fall in premarket trading after Gordon Haskett downgraded the stocks in anticipation of lackluster first-quarter and full-year forecasts from retailers reporting earnings in the coming weeks.