GOLD CLOSED DOWN $10.40 TO $2919.60

SILVER CLOSED DOWN 16 CENTSTO $32.77

GOLD ACCESS CLOSED 2935.30

Silver ACCESS CLOSED: $32.77

Bitcoin morning price:$95,650 UP 565DOLLARS.

Bitcoin: afternoon price: $96,219 UP 1174 DOLLARS

Platinum price closing DOWN $10.15 TO $973.40

Palladium price; DOWN $11.35TO $975.40

END

*CANADIAN GOLD: $4176.12UP 12.89CDN dollars per oz( * NEW ALL TIME HIGH 4176.12CDN DOLLARS PER OZ//FEB 19 2025)

*BRITISH GOLD: 2332.00 UP 7.93Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2,339.25 BRITISH POUNDS/OZ) FEB 10/2025

*EURO GOLD: 2,815,518UP 4.43 Euros per oz //* (ALL TIME CLOSING HIGH: 2,815.52EUROS PER OZ/FEB 18 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,931.600000000 USD

INTENT DATE: 02/18/2025 DELIVERY DATE: 02/20/2025

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 1

092 C DEUTSCHE BANK 17

118 C MACQUARIE FUT 156

118 H MACQUARIE FUT 370

167 C MAREX 234

190 H BMO CAPITAL 81

323 C HSBC 320 149

323 H HSBC 2

332 H STANDARD CHARTE 2

363 H WELLS FARGO SEC 548

435 H SCOTIA CAPITAL 182

555 C BNP PARIBAS SEC 300

657 C MORGAN STANLEY 3

657 H MORGAN STANLEY 1266

661 C JP MORGAN 537

686 C STONEX FINANCIA 32 40

690 C ABN AMRO 11 28

709 C BARCLAYS 2

732 C RBC CAP MARKETS 3

732 H RBC CAP MARKETS 11

737 C ADVANTAGE 23

880 C CITIGROUP 1

880 H CITIGROUP 6

905 C ADM 23

TOTAL: 2,174 2,174

MONTH TO DATE: 71,651

JPMorgan stopped (received) 01574contracts/3655

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2024. CONTRACT: 2174 NOTICES FOR 217,400 OZ 6.7670TONNES

total notices so far: 71,651 contracts for 7165100 Oz (228.86 tonnes)

FOR FEB.

SILVER NOTICES: 146 NOTICE(S) FILED FOR 0.730 MILLION OZ/

total number of notices filed so far this month : 4370 for 21.850 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $10.40 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF 6.38ONNES

INVENTORY RESTS AT 869.44TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN 16 CENTS AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.276 MLLION OX

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 436.718 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 722CONTRACTS TO 170,107 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS GOOD SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0,56 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUMONGOUS GAIN OF 942 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE//MONDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON MONDAY COMEX TRADING/ AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON TUESDAY WITH SILVER’S RISE IN PRICE BY 56 CENTS. WE HAD A HUGE T.A.S. LIQUIDATION TUESDAY COUPLED WITH ANOTHER NEW STRONG T.A.S. ISSUANCE OF 468 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.00 DOLLAR MARK. WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND 95 CENTS AND A LEASE RATE OF 6%. WE HAD A FAIR 220 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 468 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUMONGOUS SIZED 942 CONTRACTS ON OUR TWO EXCHANGES WITH OUR STRONG GAIN IN PRICE. WE HAD HUGE TAS LIQUIDATION THROUGHOUT MONDAY’S COMEX TRADING SESSION/

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT/WEDNESDAY MORNING: A STRONG 468 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.56 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS GAIN IN OUR TWO EXCHANGES OF 1284 CONTRACTS WE HAD A MASSIVE LIQUIDATION OF T.A.S. CONTRACTS TRYING TO CONTAIN SILVER’S PRICE RISE

WE HAD A FAIR 220 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 165 CONTRACT QUEUE JUMP FOR 0.825MILLION OZ

// STANDING FOR SILVER//FEB ADVANCES TO 21.915MILLION OZ

WE HAD:

/ MEGA HUGE SIZED COMEX OI GAIN+// A FAIR SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 468 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 338CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 12 DAYS, total 9517 contracts: OR 47.585 MILLION OZ (793 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 47,585 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 47.585 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 722 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 220 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 10.105 MILLION OZ ON FIRST DAY NOTICE,FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 0.825 MILLION OZ TO LONDON//NEW STANDING ADVANCES TO 21.915 MILLION OZ

WE HAVE 1). A HUMONGOUS SIZED GAIN OF 942 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR GAIN IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 468 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//MONSTER FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION. HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON THURSDAY WITH THE SLIGHT LOSS IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (468 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE

WE HAD 146 NOTICE(S) FILED TODAY FOR 0.730 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIRSIZED 1689 OI CONTRACTS TO 522,330 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A STRONG SIZED 1578 CONTRACTS//

WE HAD A FAIR SIZED INCREASE IN COMEX OI (1689 CONTRACTS) OCCURRED WITH OUR HUGE GAIN OF $43.40 IN PRICE MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 184.40 TONNES FOLLOWED BY A HUGE 2189 CONTRACT QUEUE JUMP//218,900 OZ (6.622ONNES)

/NEW STANDING ADVANCES TO 225.486TONNES +18.4527

= 243.839 7TONNES.

/ ALL OF THIS HAPPENED WITH OUR $43.40 GAIN IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD A STRONG SIZED GAIN OF 4339 OI CONTRACTS (13.476APER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE FRONT FEBRUARY CONTRACT MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2650 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 523,905

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4339 CONTRACTS WITH 1,689 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2650 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5914 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED AND CRIMINAL 1142 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2650 CONTRACTS) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 1689 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 4339 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB 184.40 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 2129 CONTRACTS FOR 212,900OZ( 6.622TONNES). AND THEN WE ADD OUR 5 EXCHANGE FOR RISK TOTALS OF 18.4527 TONNES//NEW TOTAL OF GOLD STANDING AT THE COMEX ADVANCES TO 243.937TONNES

.

NEW STANDING FOR FEB ADVANCES TO:

225.486 NORMAL DELIVERY + .18,4527 TONNES OF EXCHANGE FOR RISK/PRIOR

EQUALS 243.939TONNES

//NEW STANDING FEB: 243,939 TONNES WHICH IS THE HIGHEST EVER GOLD STANDING FOR A FEBRUARY DELIVERY MONTH. AND FOR ANY COMEX MONTH.

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE FRIDAY WITH LITTLE SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WITH OUR1) $43.40 PRICE GAIN WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG GAIN OF 5914 CONTRACTS ON OUR TWO EXCHANGES ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR RECORD NUMBER OF GOLD TONNES STANDING FOR FEBRUARY.

4) FAIR SIZED COMEX OPEN INTEREST INCREASE 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 1142 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

TOTAL EFP CONTRACTS ISSUED: 51,077 CONTRACTS OF 5,107,700 OZ OR 158.87 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 4084 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 158,87TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 158.87 DIVIDED BY 3550 x 100% TONNES = 4.47% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 150.63TONNES ISSUANCE

FEB: 158.87 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A GOOD SIZED ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG SIZED 722 CONTRACTS OI TO 170,107 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 220CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 475 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1245 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 722 CONTRACTS AND ADD TO THE 220 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 942 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.71MILLION OZ OCCURRED WITH OUR $0.56 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 27.05PTS OR 0.81%

//Hang Seng CLOSED DOWN 32.57PTS OR 0.14%

// Nikkei CLOSED DOWN 105.79 OR 0.27%//Australia’s all ordinaries CLOSED DOWN 0.66%

//Chinese yuan (ONSHORE) CLOSED UDOWN TO 7.2796CHINESE YUAN OFFSHORE CLOSED DOWNTO 7.2899/ Oil UP TO 72.47 dollars per barrel for WTI and BRENT UP AT 76.43 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVELEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

END

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1689 CONTRACTS TO 522,330 WITH OUR GAIN IN PRICE OF $43.40 WITH RESPECT TO MONDAY’S TRADING/RAID. WE LOST ZERO NET LONGS WITH THAT PRICE GAIN FOR GOLD. BUT AS YOU WILL SEE BELOW, THE GAIN WAS NOT AS LARGE AS EXPECTED. WE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2650) .

THE CME ANNOUNCED FRIDAY NIGHT, ZERO EXCHANGE FOR RISK CONTRACTS FOR NIL OZ OR 0 TONNES

AND SO FAR IN FEBRUARY: WE HAVE HAD FIVE EXCHANGE FOR RISKSNOW TOTALLING 18.4527TONNES!. THE RECIPIENT OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY.

THUS IN TOTAL WE HAD A GOOD SIZED GAIN ON OUR TWO EXCHANGES OF 4339CONTRACTS WITH OUR GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW CLIMBED TO 10% AS GOLD IN LONDON IS NOW EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY TODAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND STRONG T.A.S. LIQUIDATION. MONDAY NIGHT, THEY ISSUED A STRONG 1142 CONTRACT ANNOUNCEMENT (MONDAY NIGHT/TUESDAY MORNING).

THE FED IS THE OTHER MAJOR SHORT OF AROUND 16+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, 202, 203 , 204 ,205 206, 207 208 AND TODAY’S 209, AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING LAST WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE ACTIVE DELIVERY MONTH OF FEBRUARY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2650 EFP CONTRACTS WERE ISSUED: : /FEB 2650 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2650 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 4339 CONTRACTS IN THAT 2650 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1689 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $43.40F OR TUESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. THE MAJOR PART OF THE LOSS IN TOTAL OI ON OUR TWO EXCHANGES WAS DUE TO LIQUIDATION OF T.A.S. SPREADERS!

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A STRONG SIZED SIZED 1142 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER A FEW WEEKS AGO, THE FED WAS EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( MONDAY TRADING// JAN 27) AS THE GOLD PRICE GOT HAMMERED A BIT WITH COMEX OPTIONS EXPIRY. AS YOU SAW WITH LAST TUESDAY’S TRADING// JAN 28 IT HAS NO EFFECT ON GOLD AS IT SHOT UP AGAIN IN PRICE AND IT CONTINUED TO RISE THROUGHOUT THE WEEK. LONDON’S ANNOUNCEMENT LAST THURSDAY THAT THEY WERE OUT OF PHYSICAL GOLD SURELY HELPED TO PROPEL GOLD’S METEORIC RISE IN PRICE THESE PAST SEVERAL DAYS PROPELLING IT THROUGH THE 2800 DOLLAR BARRIER TO THE LEVEL IT IS NOW TRADING READY TO CLOSE IN ON THE 2900 DOLLAR LEVEL.

MECHANICS OF T.A.S CONTRACTS/DECEMBER 2024

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON DEC. 27, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE DECEMBER’S OPTIONS EXPIRY TRADING AND AGAIN WITH JANUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE. ALL OF THESE T.A.S. ISSUANCES WERE USED IN AN ATTEMPT TO THWART GOLD TRADING ESPECIALLY BEFORE TRUMP’S INAUGURATION AS THE FED MUST REDUCE ITS MASSIVE PHYSICAL GOLD SHORT OF 79 TONNES. THEY FAILED MISERABLY AS GOLD SKYROCKETED IN PRICE THIS WEEK AND NOW TO ALL TIME RECORD HIGHS IN USA DOLLAR TERMS AND OTHER CURRENCIES.

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAD A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (243.939 TONNES) WHICH IS HUGE FOR OUR ACTIVE FEB DELIVERY MONTH AND THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH.

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 243.939 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY: 225.486 TONNES OF GOLD+ + 18.4527 TONNES EX FOR RISK PRIOR=//NEW TOTAL STANDING 243.939 TONNES

COMEX GOLD TRADING/FEB CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $43.40//AND WERE UNSUCCESSFUL IN KNOCKING OFF SOME APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED LOSS IN OUR TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION MONDAY AS THEY WERE TRYING TO QUELL GOLD’S RISE AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING. THE BANKERS WERE UNSUCCESSFUL IN SLOWING THEIR DERIVATIVE LOSSES IN PRECIOUS METAL BETS WITH OPTIONS EXPIRY JAN 28 AT THE COMEX. OUR T.A.S. SPREADER LIQUIDATIONS THIS 2ND WEEK OF FEB, WERE DISTORTING OPEN INTEREST AS I EXPLAINED ABOVE, BUT IS HAVING NO EFFECT ON GOLD’S METEORIC RISE IN PRICE. PRIOR TO FRIDAY . THE RAID ON FRIDAY WAS NEEDED TO QUELL PRICE RISES IN GOLD AND SILVER,. SILVER IS A BIG HEADACHE FOR OUR CROOKS AS THE PHYSICAL METAL IS BASICALLY UNATTAINABLE. DERIVATIVE LOSSES ON BOTH GOLD AND SILVER ARE HUGE!

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING WEDNESDAY MORNING AND THUS OUR RECORD NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD)

EXCHANGE FOR RISK EXPLANATION/DECEMBER AND JANUARYTRADING

DECEMBER MONTH EXCHANGE FOR RISK!

75 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 6 FOR 14.6836 TONNES A NEW RECORD. THE COMEX IS TOTALLY SHATTERED TO PIECES.

EXCHANGE FOR RISK // JANUARY MONTH!!

LO AND BEHOLD, THE CROOKS ISSUED THEIR FIRST ISSUANCE A MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THEN TO MY HORROR, THEY ISSUED THEIR SECOND EXCHANGE FOR RISK ON JAN 8, TOTALLING 150 CONTRACTS FOR 15000 OZ OR .4665 TONNES. THIS TONNAGE WILL BE ADDED TO THE FIRST ISSUANCE. THUS TOTAL EXCHANGE FOR RISK ISSUANCE FOR OUR TWO EARLY JANUARY EX FOR RISK: 5.7533 TONNES. THEN MERCILESSLY THEY CONSUMMATED FOR THE THIRD TIME THIS MONTH 85 EXCHANGE FOR RISK LAST THURSDAY NIGHT (JAN 17) FOR 8500 OZ OR .2649 TONNES OF GOLD. THEN TO MY HORROR THEY ISSUED THEIR 4TH EXCHANGE FOR RISK THIS MONTH (JAN 22) FOR A MONSTER 5000 CONTRACTS OR 5,000,000 OZ.(15.562 TONNES).NOT TO BE UNDONE, THE CROOKS ISSUED THEIR FIFTH EXCHANGE FOR RISK LAST NIGHT FOR 500 CONTRACTS REPRESENTING 50,,000 OZ OR 1.555 TONNES OF GOLD. REMEMBER THAT THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON WHICH IS TOTALLY ASININE!! THUS FOR THE 5 EXCHANGE FOR RISK ISSUED THIS MONTH TOTALS 23.134 TONNES OF GOLD. THIS BRINGS US TO , JAN 25 WHERE THE CME ANNOUNCED ITS SIXTH MAJOR EXCHANGE FOR RISK ISSUANCE OF 6454 CONTRACTS FOR 645,400 OZ OR 20.074 TONNES OF GOLD. THIS IS THE HIGHEST EVER RECORDED ISSUANCE IN NUMBER OF EXCHANGE FOR RISK, AT 6, AND FOR NEW TOTALS FOR THE MONTH OF JANUARY: 43.208 TONNES!!! AND A NEW RECORD FOR ISSUANCE.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO, THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WILL NOW BE ADDED TO OUR REGULAR DELIVERIES THROUGHT THE MONTH. FOR TUESDAY FEB 19 ZERO EXCHANGE FOR RISK WAS ISSUED.

FINAL STANDING GOLD/COMEX FOR JANUARY

FINAL STANDING FOR JAN: 70.102TONNES + 43.206 TONNES EX FOR RISK = 113.310 TONNES (WHICH IS HUGE FOR OUR VERY NON ACTIVE DELIVERY MONTH) A NORMAL AMOUNT STANDING FOR A JANUARY IN EARLIER TIMES HAS BEEN GENERALLY AROUND 1/4 TONNE OF GOLD. HOWEVER THESE PAST 4 YEARS QUEUE JUMPING HAS BEEN VERY PRONOUNCED AND THUS STANDING INCREASES DRAMATICALLY.

TOTAL INITIAL DELIVERIES FEB GOLD TRADING

WE HAVE GAINED A FAIR TOTAL OF 13.496 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB (184.40TONNES) ON FIRST DAY NOTICE FOLLOWED BY A STRONG SIZED 21,29 CONTRACT QUEUE JUMP FOR 212,900OZ. NEW STANDING ADVANCES TO 225.486TONNES OF GOLD. TO WHICH WE ADD OUR 18.4527TONNES OF EXCHANGE FOR RISK//NEW TOTALS STANDING 243.939TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $43.40

WE HAD 1578 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 4339CONTRACTS OR 4339,00 OZ (13.496ONNES)

confirmed volume TUESDAY 248,880ontracts: POOR///

//speculators have left the gold arena

END

// THE FEB 2025 GOLD CONTRACT

FEB 19

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entry 1.out of Brinks enhanced 232,326.985 oz 580 London Good delivery bars . |

| Deposit to the Dealer Inventory in oz | 3 ENTRIES i) Brinks dealer 142,268.175oz 4425KILOBARS ii)Asahi 32,483.570 oz iii)Loomis 32,151.000 oz (1000 kilobars) total dealer 215,744.240 oz 6.710 tonnes |

| Deposits to the Customer Inventory, in oz | 4 ENTRIES i) into Asahi 32,022.498 oz (9971 kilobars) ii) into brinks 121,274.881 oz 3772 kilobars iii into jpmorgan 160,755.000 (5000 kilobars iv)into Manfra 45,393.79 0z total customer 393,597,79 oz 12.24 tonnes total dealer and customer 18.95 tonnes |

| No of oz served (contracts) today | 2174 notice(s) 217400 OZ 6.7620TONNES |

| No of oz to be served (notices) | 873contracts 87300OZ 2.715TONNES |

| Total monthly oz gold served (contracts) so far this month | 71,651 notices 7,165,100oz 228.86 ONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 3

ENTRIES 3

i) Brinks dealer 142,268.175oz

(4425 KILOBARS)

ii)Asahi 32,483.570 oz

iii)Loomis 32,151.000 oz (1000 kilobars)

total dealer 215,744.240 oz 6.710 tonnes

we have 4customer deposits:

4 ENTRIES

i) into Asahi 32,022.498 oz (9971 kilobars)

ii) into brinks 121,274.881 oz 3772 kilobars

iii into jpmorgan 160,755.000 (5000 kilobars

iv)into Manfra 45,393.79 0z

total customer 393,597,79 oz 12.24 tonnes

total dealer and customer 18.95 tonnes

withdrawals: 1

1 entry

1.)out of Brinks enhanced

232,326.985 oz

580 London Good delivery bars

xxxxxxxxxxxxxxxxxxxxxxxxxxxxx

adjustments:2/comex is in chaos

3 customer to dealer

a) Brinks 316,076.479 oz oz

b)jpm 7716.240oz

c) 166,545.835 oz

thus basically what comes into eligible is transferred to dealer accounts and then out.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB

FEB HAD A GAIN OF 573 CONTRACTS TO STAND AT 3047 WE HAD 1556 CONTRACTS SERVED ON MONDAY SO WE GAINED A HUGE 2129 CONTRACTS OR A 212,900 OZ QUEUE JUMP OR 6.622 TONNES,.(THURSDAY, FEB 13 WE WITNESSED THE HIGHEST EVER QUEUE JUMP RECORDED AT THE COMEX AT 12.12 TONNES)

MARCH HAD A LOSS OF 193 CONTRACTS DOWN TO 14,819

APRIL HAD A GAIN OF 477CONTRACTS UP TO 388,168 CONTRACTS

We had 2174 contracts filed for today representing 217,400 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 2174contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 537 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2025. contract month, we take the total number of notices filed so far for the month (71,651x 100 oz ) to which we add the difference between the open interest for the front month of FEB.(3047CONTRACTS) minus the number of notices served upon today (2174 x 100 oz per contract) equals 7,249,400OZ OR 225.486TONNES TO WHICH WE ADD NEW EXCHANGE FOR RISK 18.4527 TONNES//NEW TOTAL STANDING 243.939TONNES

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (71,651x 100 oz +we add the difference for front month of FEB ( 3047OI} minus the number of notices served upon today (2174 x 100 oz) which equals 7,249,400 Oz (225.486TONNES + 18,4527 tonnes ex for risk PRIOR = 243.939onnes

TOTAL COMEX GOLD STANDING FOR FEB.: 243.939 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR AND THIS IS THE HIGHEST EVER RECORDED FOR ANY FEBRUARY AND THE HIGHEST FOR ANY MONTH FOR THAT MATTER IN COMEX HISTORY!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,082,524.203 oz 64.77onnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 37,983,093.444oz

TOTAL REGISTERED GOLD 17,562,375.957or 546.26onnes

TOTAL OF ALL ELIGIBLE GOLD: 20,420,717.487OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,790,791 oz (REG GOLD- PLEDGED GOLD)= 460.05onnes //

END

SILVER/COMEX

FEB 12

INITIAL

// THE FEB 2025 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 6,010.950oz a) Delaware 6010.950 oz |

| Deposits to the Dealer Inventory | 1 entry brinks dealer 365,859.058 oz |

| Deposits to the Customer Inventory | 3entries i) Into Ashai 595,648,500oz ii) Into JPMorgan: 1403,279.100oz iii) Into brinks 3,844,620.607 oz total 4,843,548.265 oz |

| No of oz served today (contracts) | 146 CONTRACT(S) (0.730MILLION OZ |

| No of oz to be served (notices) | 139 contracts (0.695 MILLION oz) |

| Total monthly oz silver served (contracts) | 4370 Contracts (21.850 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 1 dealer deposit/

1 entry

i)brinks dealer 365,859.058 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

3entries

3entries

i) Into Ashai 595,648,500oz

ii) Into JPMorgan: 1403,279.100oz

iii) Into brinks 3,844,620.607 oz

total 4,843,548.265 oz

oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals 1

6,010.950oz

a) Delaware 6010.950 oz

total 6010.950 oz

ADJUSTMENTs 1customer to dealer:

i) manfra 164,300.986

JPMorgan has a total silver weight: 155.099million oz/385.079million or 40.78%

TOTAL REGISTERED SILVER: 97.438MILLION OZ//.TOTAL REG + ELIGIBLE. 385.279million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB /2025 OI: 285OPEN INTEREST CONTRACTS FOR A GAIN OF 113 CONTRACTS.

WE HAD 52 NOTICES FILED ON MONDAY SO WE GAINED 165 CONTRACTS OR WE EXPERIENCED A 825,000 OZ EXCHANGE QUEUE JUMP AS THESE GUYS WILL TRY THEIR LUCK AT THE COMEX TRYING TO OBTAIN PHYSICAL SILVER.

MARCH SAW A LOSS OF 2806CONTRACTS DOWN TO 78,626 HE FRONT ACTIVE DELIVERY MONTH OF MARCH ALSO IS NOT DECLINING MUCH AND WE SHOULD ALSO HAVE A HUMDINGER OF A DELIVERY MONTH FOR MARCH.

APRIL SAW ANOTHER GAIN OF 82 CONTRACTS TO STAND AT 495

MAY SAW A GAIN OF 2740 CONTRACTS UP TO 68,217 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 146 or 0.730MILLION oz

CONFIRMED volume; ON TUESDAY 90,551 huge//

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 4370 5,000 oz = 21.850 MILLION oz

to which we add the difference between the open interest for the front month of FEB (285) and the number of notices served upon today (146)x (5000 oz)

Thus the standings for silver for the FEB 2025 contract month: 4370Notices served so far) x 5000 oz + OI for the front month of FEB(285)minus number of notices served upon today (146)x 5000 oz equals silver standing for the FEB contract month equating to 21.915MILLION OZ.

New total standing: 21.915 million oz which is huge for a non active delivery month of February

There are 97.0438million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

FEB 13/ WITH GOLD UP 11.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 6.901 TONNES FROM THE GLD ///INVENTORY RESTS AT 866.50TONNES

FEB 12 WITH GOLD DOWN $3,40ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 10 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 7 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 6 WITH GOLD DOWN $18.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.14 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

FEB 5 WITH GOLD UP $27.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 863.05 TONNES

FEB 4 WITH GOLD UP $25.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.58 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.77 TONNES

JAN 31 WITH GOLD UP $4.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 30 WITH GOLD UP $40.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 865.34 TONNES

JAN 29 WITH GOLD DOWN $6.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.02 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 861.04 TONNES

JAN 28 WITH GOLD UP $23.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.16 TONNES OF GOLD OUT OF THE GLD //

JAN 27 WITH GOLD DOWN $36.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///

JAN 24 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 23 WITH GOLD DOWN $1.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 2.30 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 869.36 TONNES

JAN 22 WITH GOLD UP $15.15 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 7.46 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 871.66 TONNES

JAN 20 WITH GOLD UP $35.30 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 10.34 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 879.12 TONNES

/

GLD INVENTORY: 863.06TONNES, TONIGHTS TOTAL

SILVER

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 12WITH SILVER UP $.01 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 8 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 10 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 7 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 6 WITH SILVER DOWN $0.17 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 12.383 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 430.39 MILLION OZ

FEB 5 WITH SILVER UP $0.45 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 3.285 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 442.773 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 3 WITH SILVER UP ONE CENT //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

JAN 31 WITH SILVER DOWN $0.19 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.369 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 448.881 MILLION OZ

jAN 30 WITH SILVER UP $0.76 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.003 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 451.249 MILLION OZ

jAN 29 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.639 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 453.252 MILLION OZ

jAN 28 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.821 MILLION OZ OUT OF THE SLV./. /

jAN 27 WITH SILVER DOWN $.61 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 24 WITH SILVER DOWN $.21 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 23 WITH SILVER DOWN $.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 4.738 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 459.035 MILLION OZ

JAN 22 WITH SILVER UP $.08 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 0.721 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 464.043 MILLION OZ

JAN 20 WITH SILVER DOWN $.09 //NO CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.568 MILLION OZ FROM THE SLV./. //INVENTORY AT SLV RESTS AT 463.315 MILLION OZ

CLOSING INVENTORY 438,994 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

END

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ALASDAIR MACLEOD

Midweek metals madness

After rising nearly 14% in just two months and the premiums on Comex futures normalising, you would have thought gold would have a correction. Instead, it threatens to rise even further…

| Alasdair MacleodFeb 19∙Paid |

Despite recent strength, gold’s chart still looks good. Speculator positions on Comex are far from extreme, suggesting that they have yet to get fully on board the trend. In the last three sessions, prices have been driven by overnight (Asian) demand. Broadly, where gold goes silver tends to follow.

The extraordinary thing is that western financial markets have missed out in this game entirely. Even momentum-playing speculators appear luke-warm about the trend, otherwise Comex’s open interest would be significantly greater whereas it has declined by some 76,000 contracts in the last 18 trading sessions.

So, what’s going on?

I have often emphasised the standing for delivery problem on Comex. It is where ephemeral futures meet physical reality. Since mid-December, when the current bullish move started 290 tonnes have been stood for delivery, supposedly a staggering withdrawal of bullion from bullion banks’ reserves. In the past, they have used every trick in the book to not part with actual possession, but that only works so long as those standing for delivery accept a certificate promising ownership from the likes of Goldman Sachs or JPMorgan instead of actual delivery.

But what happens if these ownership certificates are no longer acceptable?

I believe that this is why the bullion bank establishment in New York has had to suck physical liquidity out of other financial centres and even the Bank of England, because there was a run on their US bullion reserves developing with increasing numbers of stand-for-deliveries insisting on actual possession.

Since Covid, gold stand-for deliveries on Comex have totalled over 2,500 tonnes. This conceals an enormous build-up of undelivered obligations, inevitably leading to a run on the system. But why now?

Following President Trump’s election, there has been enormous uncertainty over his own and his team’s attitudes to gold. We hear that Treasury Secretary Scott Bessant is bullish of gold, and that he supports the Treasury’s gold being transferred to a new sovereign wealth fund. But what if the rumours about Fort Knox and the New York Fed misrepresenting the actual position are true? What if most of the gold is missing?

If that is true, then precedence suggests that gold in the Comex vaults might be confiscated to make up for shortfalls in the Treasury’s stocks. And a promise to deliver made by a bullion bank (“Don’t worry, we will look after your gold for you at no storage cost — here is a piece of paper confirming the arrangement”) suddenly is not good enough.

It certainly explains the panic in New York.

Then there’s Trump’s stated objective to devalue the dollar as part of his MAGA policy, in order to make US production more competitive in export markets and shut out foreign competition. That alone points to a rush into gold.

The fact is that with all the rumours and uncertainty over Trump’s trade and financial policies, plus his seeming disregard for others’ property rights (talk to Gazans, and now Ukrainians!) any foreigner holding dollars, storing gold, or possessing gold certificates from a bullion bank for gold in US vaults is at risk of losing it all. In these turbulent times, the only safety looks like possessing physical gold held beyond America’s reach.

The only problem is that liquidity elsewhere has already been cleaned out!

.3 CHRIS POWELL AND GATA DISPATCHES

Chris Powell…..

4 ANDREW MAGUIRE/LIVE FROM THE VAULT NO 210

Episode

210

B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY//COFFE

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING TUESDAY MORNING MONDAY NIGHT

SHANGHAI CLOSED UP 27.05PTS OR 0.81%

//Hang Seng CLOSED DOWN 32.57PTS OR 0.14%

// Nikkei CLOSED DOWN 105.79 OR 0.27%//Australia’s all ordinaries CLOSED DOWN 0.66%

//Chinese yuan (ONSHORE) CLOSED UDOWN TO 7.2796CHINESE YUAN OFFSHORE CLOSED DOWNTO 7.2899/ Oil UP TO 72.47 dollars per barrel for WTI and BRENT UP AT 76.43 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVELEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2796

OFFSHORE YUAN: DOWN TO 7.2899

SHANGHAI CLOSED CLOSED UP 27.05 PTS OR 0.81%

HANG SENG CLOSED CLOSED DOWN 32.57PTS OR 0.14%

2. Nikkei closed DOWN 109.79OR 0.27%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 106.97 EURO FALL TO 1.0440 DOWN 8 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: RISES TO. +1.418Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 151.73…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.5260 Italian 10 Yr bond yield UP to 3.578 SPAIN 10 YR BOND YIELD UP TO 3.177

3i Greek 10 year bond yield UP TO 3.347

3j Gold at $2939.90 /Silver at: 32.92 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 53 /100 roubles/dollar; ROUBLE AT 91.25

3m oil into the 72dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 151.73 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.418% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9047 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.94426well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.565 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.7870 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.308 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 36.30…

10 YR UK BOND YIELD: 4.6550 UP 10 PTS

10 YR CANADA BOND YIELD: 3.190 UP 9 BASIS PTS

5 YR CANADA BOND YIELD: 2.888 UP 8 PTS.

2a New York OPENING REPORT

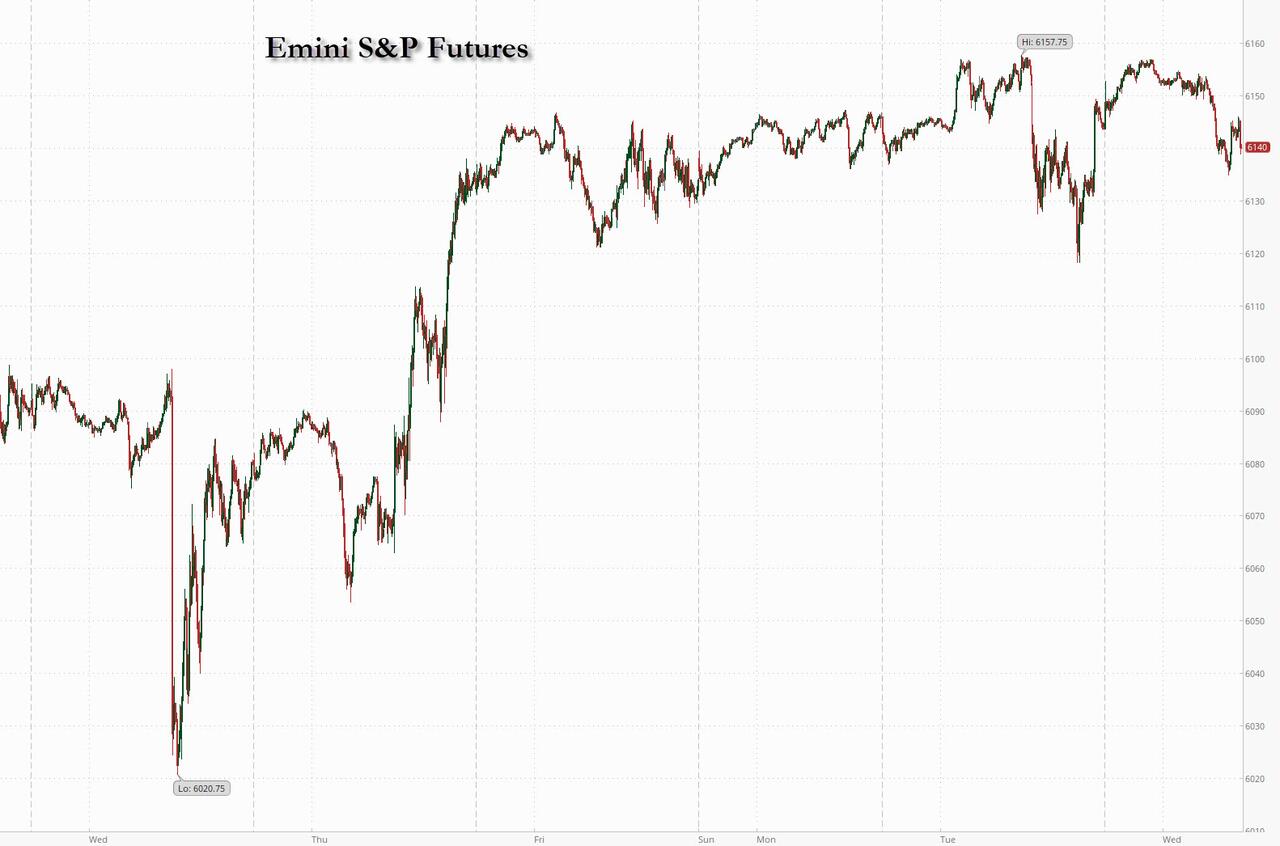

Futures Slide After Trump Threatens 25% Tariffs, FOMC Minutes Loom

Wednesday, Feb 19, 2025 – 08:25 AM

US equity futures are lower ahead of today’s FOMC minutes, with global markets also sinking and bonds extended their slide after President Trump’s latest tariff threats stoked concern about a widening trade war; hawkish UK inflation prints which sent bond yields higher did not help. As of 8:00am S&P futures are -0.3% lower after the index topped its January record on Tuesday, while Nasdaq futures traded steady after Trump raised the specter of 25% tariffs on Autos and Pharma, both coming after April 1. The Trump Admin will also keep Biden-era rules on M&A. A slew of earnings reports also dented sentiment, with Arista Networks, Occidental Petroleum, Celanese and Bumble all dropping in premarket trading after results. Super Micro Computer rallied, however, after issuing an aggressive long-term revenue outlook. Pre-mkt, Mag7 names are mixed with Semis seeing some profit-taking. The yield curve is twisting steeper as the USD appreciates. Commodities are stronger despite the USD move; Brent trades above $76 while gold is at an all time high around $2940. Today’s macro data focus will be on Housing data and the Fed Minutes.

In premarket trading, Nvidia is leading gains among the Magnificent Seven (GOOGL +0.3%, AMZN -0.1%, AAPL -0.1%, MSFT -0.02%, META -0.09%, NVDA +0.4% and TSLA -0.1%). Bumble plunged 17% after the online dating company gave a first-quarter forecast that was weaker than expected on key metrics. Etsy tumbled 7% after reporting gross merchandise sales for the fourth quarter that missed the average analyst estimate. Here are some other notable premarket movers:

- Analog Devices (ADI) gains 5% after posting adjusted earnings per share for the first quarter that beat the average analyst estimate.

- Arista Networks (ANET) falls 4% after the computer networking company posted 4Q results.

- Cadence Design Systems (CDNS) slips 3% after the electronic design automation software company gave an outlook that was seen as disappointing.

- Celanese (CE) drops 13% after the chemical firm said it sees “persistently weak global demand” in end markets including paint and coatings.

- Fiverr (FVRR) rises 4% after forecasting 1Q revenue that beat the average analyst estimate.

- Howard Hughes Holdings (HHH) falls 3% after confirming it received an revised unsolicited proposal from Pershing Square and will evaluate the offer.

- International Flavors (IFF) falls 2% after forecasting disappointing sales for 2025.

- RB Global Inc. (RBA) rises 3% after reporting quarterly revenue that beat the average analyst estimate.

- Shift4 Payments (FOUR) declines 10% after the payments processing firm gave a weaker-than-expected outlook for adjusted Ebitda.

- Global Blue (GB) jumps 18% after Shift4 agreed to acquire the shopping technology company for $7.50 per share in cash.

- Star Bulk (SBLK) slips 5% as Jefferies notes that 4Q results were weak due to lower dry bulk spot rates, which have continued into the current quarter.

- Supernus Pharmaceuticals (SUPN) drops 21% after the drugmaker said a mid-stage study of its experimental therapy for treatment-resistant depression failed to meet its primary endpoint.

- Toll Brothers (TOL) falls 5% after the luxury homebuilder reported first-quarter revenue and total home sales that fell short of consensus estimates.

- Wix.com (WIX) rises 2% after the company’s forecast for 1Q revenue disappointed.

Traders’ attention will focus turn to the latest FOMC Minutes which could offer clues on the monetary policy outlook. While inflation has been slowing, many fear the effect of Trump’s tariff push on prices. Several officials, including Governor Christopher Waller and San Francisco Fed chief Mary Daly, have signaled rates will stay on hold until inflation slows significantly.

Separately, on Wednesday, the European Central Bank’s Isabel Schnabel said the bank will have to discuss pausing or ending its rate-cut campaign. Her comments pushed the euro 0.2% lower against the dollar, while bond yields rose across Europe, with 10-year German bund yields up about five basis points. Meanwhile, British 10-year gilt yields rose about six basis points after data showed inflation at a 10-month high.

Investors are also pricing increased government spending on defense should the war in Ukraine draw to an end. “When you think about the outcome of any peace treaty between Ukraine and Russia, that will involve a huge uplift in defense spending from European countries,” said Lilian Chovin, head of asset allocation at Coutts & Co.

Europe’s Stoxx 600 Index dropped 0.5% after another record close on Tuesday. Mining, travel, retail and construction stocks underperform. Sentiment was hurt after Trump warned he is weighing tariffs of around 25% on automobile, semiconductor and pharmaceutical imports. His comments added to the a fragile market picture as hopes for an end to the war in Ukraine were tempered by the exclusion of Ukrainian and European officials from US-Russia talks held on Tuesday. Major markets are all lower ex-Italy as bond yields increase following the UK inflation print. Aero/Def, Energy, Semis among the strongest baskets. Here are some of the biggest movers on Wednesday:

- HSBC shares in London rise 1.1% following a recent strong rally that took the stock to trade at highest since 2001, after the lender reported pretax profit that beat estimates and detailed a $2 billion share buyback.

- Societe BIC shares rise as much as 5.9% to hit their highest level in more than eight months after the French consumer-goods firm posted annual earnings ahead of expectations.

- Glencore shares drop as much as 7.2% to their lowest level in over three years, with analysts pointing to the miner’s disappointing copper production guidance as well as its shareholder returns, which were weighed down by its debt.

- Jet2 shares sink as much as 11%, their biggest drop since July 2023, after the package holiday company’s guidance fell short of analysts’ expectations.

- Philips shares drop 11%, the most since Oct. 28, after the Dutch medical equipment maker said it expects lower demand in China to continue to stymie growth this year.

- Delivery Hero shares fall 5%, the most in a month, after Citigroup downgraded the stock to sell from neutral, citing risk to margins due to mounting competitive pressures in the Middle East.

- Straumann shares fall as much as 4.4% after the Swiss maker of dental equipment posted results with weaker profitability levels.

- Tate & Lyle shares fall as much as 3.5% after Berenberg cut its recommendation on the stock to hold from buy, citing the ingredient maker’s weak FY2026 outlook, and a lack of signs of improvement in pricing conditions.

- BAE Systems shares fall as much as 3.3% after the UK defense firm’s FY25 cash-flow guidance disappointed analysts, who also noted concerns around US and UK budgets and reviews.

- Temenos shares fall as much as 4%, the most since November, as the Swiss banking software company’s guidance was seen dampened by the recently announced sale of Multifonds at a valuation that is deemed too low.

Some investors are also concerned about Germany’s national election on Sunday. While Friedrich Merz of the center-right opposition is expected to become chancellor, polls suggest the far-right Alternative for Germany will become the second-biggest party in parliament.

“I have been selling quite a lot over the last two days as Europe is now pricing the best possible scenario for the next catalysts, which is the Ukraine ceasefire and German elections,” said Alberto Tocchio, a portfolio manager at Kairos Partners. “The situation might get bumpy as both events are going to be more complicated than what the market thinks.”

In FX, the Bloomberg Dollar index rises 0.1%. The kiwi sits atop the G-10 FX leader board, rising 0.3% against the greenback after the RBNZ signaled it would slow the pace of interest-rate cuts after a third straight reduction of 50 bps. The yen rises 0.2%, taking USDJPY down to ~151.80 after BOJ Board Member Takata said it’s important for authorities to continue considering gradual hikes.

In rates, treasuries edged lower, pushing US 10-year yields up 2 basis points to 4.57%; long-end yields are less than 3bp cheaper on the day with 2s10s, 5s30s spreads wider by 2bp-3bp. Gilts led a selloff in European government bonds as traders trim their Bank of England interest-rate cut bets after UK inflation climbed to the highest since March 2024. UK 10-year yields rise 5 bps to 4.61%, although the pound still falls 0.1% to around $1.26. The German 10-year is ~5bp higher as expectations for ECB rate cuts decline; money markets see 72bps of easing by year-end vs about 76bps before Schnabel’s comments. Treasury coupon auctions resume with $16b 20-year sale at 1pm New York time and continue Thursday with $9b 30-year TIPS new issue. WI 20-year yield at around 4.835% is 6.5bp richer than January’s auction, which drew strong demand and stopped through by 1.1bp

In commodities, oil prices advance, with WTI rising 1% to $72.50 a barrel. European natural gas futures are flat having topped €50 a megawatt-hour at one stage. Spot gold rises $8 to around $2,944/oz.

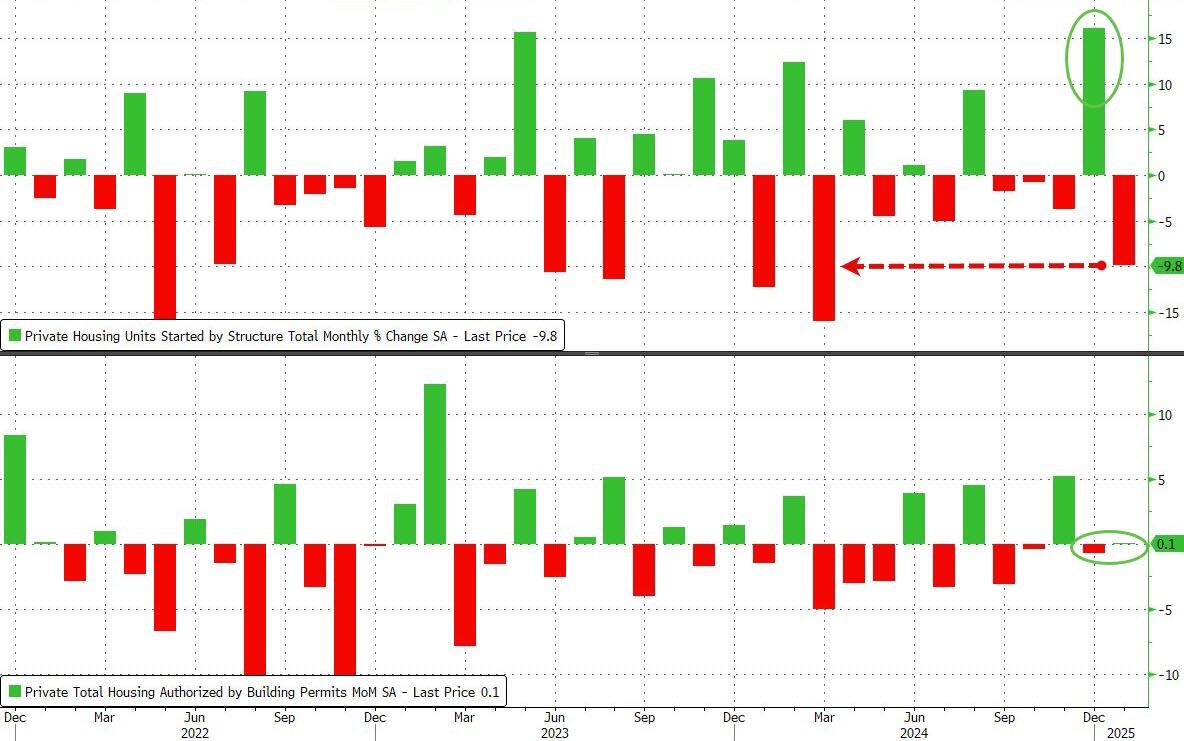

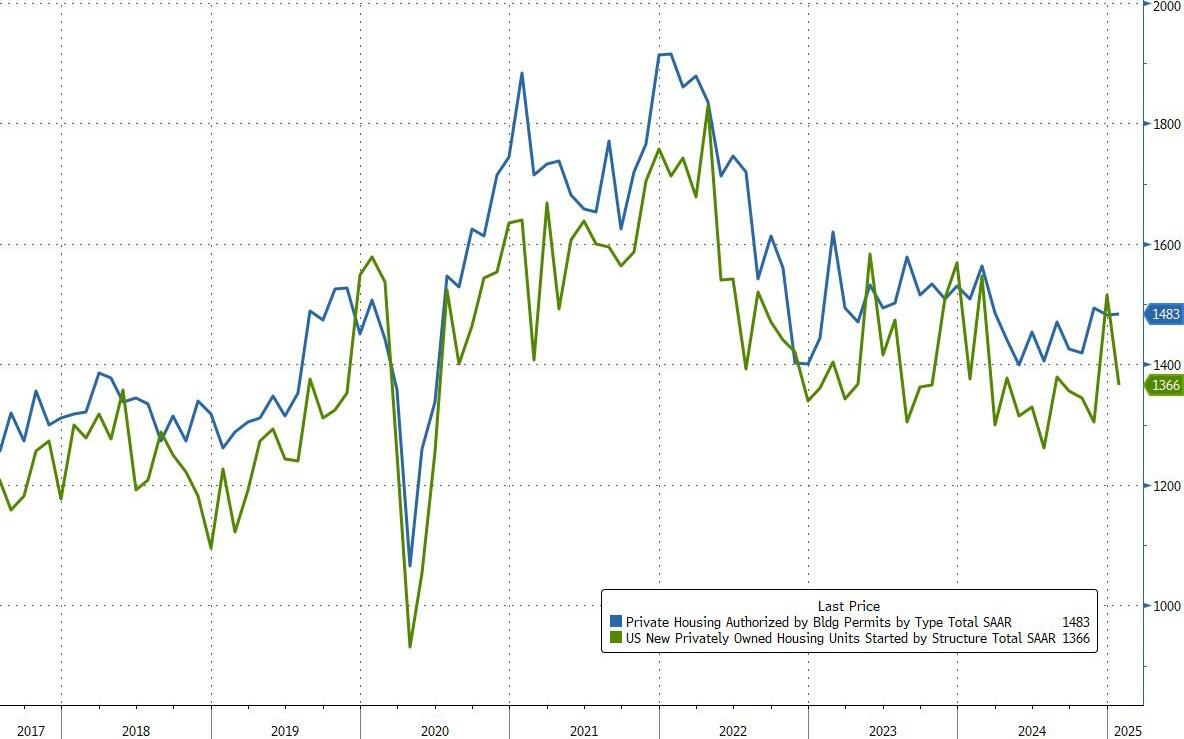

The US event calendar includes January housing starts and building permits and February New York Fed services business activity (8:30am). Fed speaker slate includes Jefferson at 5pm; minutes of January FOMC meeting to be released at 2pm

Market Snapshot

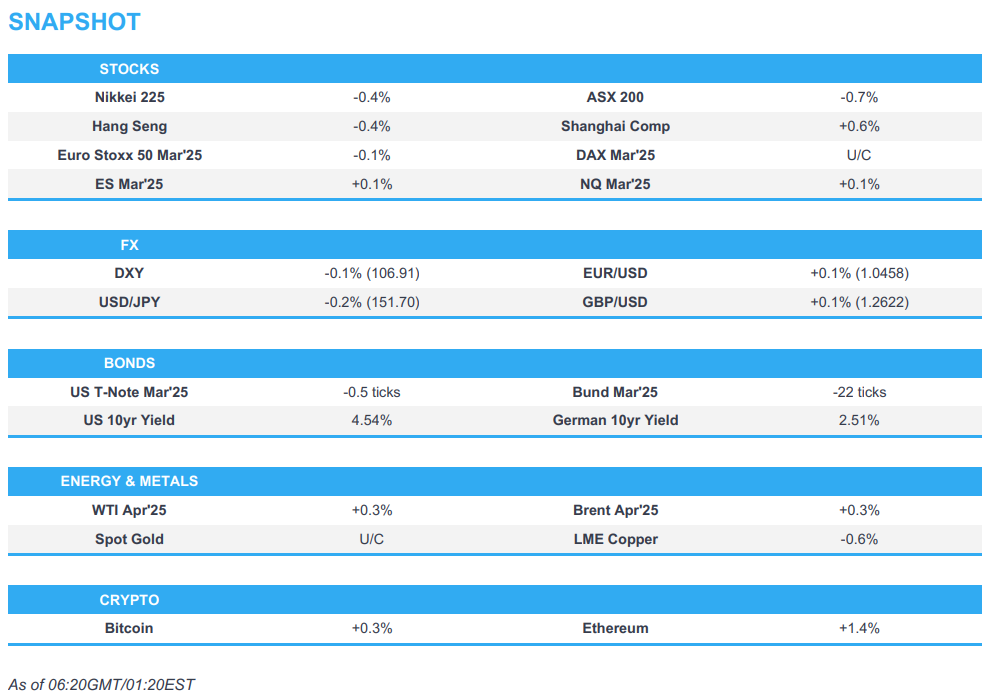

- S&P 500 futures little changed at 6,152.00

- STOXX Europe 600 little changed at 557.19

- MXAP down 0.1% to 189.67

- MXAPJ little changed at 598.35

- Nikkei down 0.3% to 39,164.61

- Topix down 0.3% to 2,767.25

- Hang Seng Index down 0.1% to 22,944.24

- Shanghai Composite up 0.8% to 3,351.54

- Sensex little changed at 75,952.51

- Australia S&P/ASX 200 down 0.7% to 8,419.19

- Kospi up 1.7% to 2,671.52

- German 10Y yield little changed at 2.53%

- Euro little changed at $1.0441

- Brent Futures up 0.8% to $76.41/bbl

- Gold spot up 0.3% to $2,943.81

- US Dollar Index little changed at 107.03

Top Overnight News

- President Donald Trump said he would likely impose tariffs on automobile, semiconductor and pharmaceutical imports of around 25%, with an announcement coming as soon as April 2 in a move that would represent a dramatic widening of the president’s trade war. BBG

- Trump said the media seeks to sow division between them when asked about the media description of Elon Musk as an ‘unelected president’, while Trump said having someone as smart as Elon Musk to work with him in running the country’s affairs is very important. Furthermore, he thinks Musk’s team will discover a trillion dollars in wasted money: Fox

- Trump posted on Truth that the Department of Justice has been politicised like never before over the past four years and he therefore instructed the termination of all the remaining “Biden Era” US attorneys.

- Intelligence from the United States and close allies shows that Russian President Vladimir Putin still wants to control all of Ukraine. While Putin is sending representatives to Saudi Arabia for negotiations with the US that are aimed at ending the war, officials said that current intelligence shows Putin still believes he can wait out Ukraine and Europe to eventually control all of Ukraine. NBC

- Trump said that Republicans would not touch Medicaid, also repeating his assertion that Medicare and Social security would not be touched: Punchbowl.

- Pharma leaders are to meet with US President Trump in a push to tweak drug policies: BBG

- China’s decline in new-home prices eased for a fifth month in January, offering hope for an end to the slump. Still, Fitch said a solid rebound in sales is needed to put a floor under prices. BBG

- China’s holdings of Treasuries have fallen to their lowest level since 2009, as Beijing holds more of its US government bonds through lower-profile accounts and diversifies into alternative assets such as gold. Analysts add that part of the change is also Beijing seeking to disguise the true extent of its Treasury holdings to accounts not captured in the data. FT

- Japan’s export growth accelerated to 7.2% year on year in January, driven by shipments to the US. Core machine orders unexpectedly fell in December. BBG

- New Zealand’s central bank slashed its policy rate by 50bp to 3.75%, a move that was expected by investors. WSJ

- UK CPI for Jan overshoots the Street on headline at +3% (vs. the Street +2.8% and up from +2.5% in Dec), although core was inline at +3.7% (vs. +3.2% in Dec) and services fell a tiny bit short at +5% (vs. the Street +5.1% and up from +4.4% in Dec). RTRS

- Traders trimmed bets on further rate cuts from the BOE this year in the wake of a surprise jump in UK inflation, and now see fewer than two more reductions through December. CPI accelerated to 3% in January, the highest level in 10 months. Two-year gilt yields gained. BBG

- Iranian oil flows to China jumped to 1.74 million barrels a day this month, the highest since October, according to Kpler, as traders work around tighter US curbs. BBG