FEB 25//COMEX EXPIRY TODAY AND THUS OUR USUAL AND CUSTOMERY RAID AT THE COMEX: GOLD CLOSED DOWN $40.85 TO $2906.20 WHILE SILVER WAS HIT FOR A LOSS OF 90 CENTS TO $31.51//PLATINUM ROSE BY 85 CENTS TO $966.55//PALLADIUM WAS DOWN $18.20 TO $925.50//GOLD COMMENTARY TONIGHT FROM ALASDAIR MACLEOD //TRUMP SEEKS TOUGHER CONTROLS ON CHIPS EXPORTED TO CHINA//ISRAEL VS HAMAS: A FEW DAYS LEFT BEFORE THE END OF FIRST PHASE OF THE DEAL: ISRAEL WANTS THE 4 DEAD HOSTAGES WITH NO CEREMONY FROM HAMAS: ISRAEL VS WEST BANK ETC//COVID UPDATES//RUSSIA VS UKRAINE UPDATES//COVID INJURY REPORTS//DR PAUL ALEXANDER/SLAY NEWS//NEWS ADDICTS/EVOL NEWS/COMMENTARY TONIGHT FROM MIKE EVERY//USA NEWS: HOME PRICES ACCELERATE AGAIN//TUCKER CARLSON INTERVIEW ON GOLD AT FORT KNOX//SWAMP STORIES FOR YOU TONIGHT

104 C MIZUHO 1 118 H MACQUARIE FUT 1 435 H SCOTIA CAPITAL 6 624 C BOFA SECURITIES 8 624 H BOFA SECURITIES 234 657 C MORGAN STANLEY 1 661 C JP MORGAN 291 686 C STONEX FINANCIA 16 4 690 C ABN AMRO 39 6 726 C PLUS500US FINAN 1 737 C ADVANTAGE 7 905 C ADM 21 991 H CME 16

TOTAL: 326 326

MONTH TO DATE: 74,518

JPMorgan stopped (received) 291/326

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2024. CONTRACT: 326 NOTICES FOR 32600 OZ 1.0139 TONNES

total notices so far: 74,844 contracts for 7,484,400 Oz (232.79 tonnes)

FOR FEB.

SILVER NOTICES: 80 NOTICE(S) FILED FOR 0.400MILLION OZ/

total number of notices filed so far this month : 4563 for 22.815 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $ 40.85 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 3.45TONNES

INVENTORY RESTS AT 907.83 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN 90 CENTS AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.245 MILLION OZ

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 441.406MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED949 ONTRACTS TO 168,057 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALLL LOSS OF $0,15 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A FAIR GAIN OF 401 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE//MONDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON MONDAY COMEX TRADING/ AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON MONDAY WITH SILVER’S FALL IN PRICE BY 15 CENTS. WE HAD A HUGE T.A.S. LIQUIDATION MONDAY COUPLED WITH ANOTHER NEW STRONG T.A.S. ISSUANCE OF 937 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.00 DOLLAR MARK. WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND 95 CENTS AND A LEASE RATE OF 6%. WE HAD A 1350 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 937 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A FAIR SIZED 401 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE. WE HAD HUGE TAS LIQUIDATION THROUGHOUT MONDAY’S COMEX TRADING SESSION DUE TO IT BEING COMEX OPTIONS EXPIRY!!

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A STRONG 937 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.15 BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A FAIR GAIN IN OUR TWO EXCHANGES OF 401 CONTRACTS WE HAD A MASSIVE LIQUIDATION OF T.A.S. CONTRACTS TRYING TO CONTAIN SILVER’S PRICE RISE AND THAT ACCOUNTS OF ALL OF OUR OPEN INTEREST FALL.

WE HAD A 1350 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 111CONTRACT QUEUE JUMP FOR 5550000 OZ

// STANDING FOR SILVER//FEB INCREASES TO 23.455 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS+// A HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 937 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED 783 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 16 DAYS, total 11,627ontracts: OR 58,135 MILLION OZ (726 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 58,135 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.135 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 947 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A 1350 CONTRACT EFP ISSUANCE CONTRACTS: 1350 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 10.105 MILLION OZ ON FIRST DAY NOTICE,FOLLOWED BY TODAY’S 550 ,000 OZ EQUEUE JUMP TRANSFER TO LONDON//NEW STANDING ADVANCESTO 23.455 MILLION OZ

WE HAVE 1). A FAIR SIZED GAIN OF 401 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR LOSS IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 937 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//MONSTER FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON MONDAY WITH THE LOSS IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (937 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE

WE HAD 80 NOTICE(S) FILED TODAY FOR 0.400 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 4465 OI CONTRACTS TO 529,785 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A STRONG SIZED 913 CONTRACTS//

WE HAD A GOOD SEIZED INCREASE IN COMEX OI (4465 CONTRACTS) OCCURRED WITH OUR GAIN OF $7.65 IN PRICE MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR FEB AT 184.40 TONNES FOLLOWED BY A HUGE 280 CONTRACT QUEUE JUMP//28000 OZ (0.8709 TONNES)

/NEW STANDING ADVANCES TO 233.80TONNES +18.4527

= 252.2527TONNES.

/ ALL OF THIS HAPPENED WITH OUR $7.65 GAIN IN PRICE WITH RESPECT TO MONAY’S COMEX ///. WE HAD A STRONG SIZED GAIN OF 7213 OI CONTRACTS (22.44PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE FRONT FEBRUARY CONTRACT MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2750 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 529,785

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7215 CONTRACTS WITH 4465 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2750 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 7215 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 918 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2750 CONTRACTS) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 4465CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 7215 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB 184.40 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 280 CONTRACTS FOR 28000OZ( 0.8709TONNES). AND THEN WE ADD OUR 5 EXCHANGE FOR RISK TOTALS OF 18.4527 TONNES//NEW TOTAL OF GOLD STANDING AT THE COMEX ADVANCES TO 252.2529TONNES

.

NEW STANDING FOR FEB ADVANCES TO:

233.80 NORMAL DELIVERY + .18,4527 TONNES OF EXCHANGE FOR RISK/PRIOR

EQUALS 252.2527 TONNES

//NEW STANDING FEB: 252.2527 TONNES WHICH IS THE HIGHEST EVER GOLD STANDING FOR A FEBRUARY DELIVERY MONTH. AND FOR ANY COMEX MONTH.

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE MONDAY WITH LITTLE SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WITH OUR1) $7.65 PRICE GAIN WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG GAIN OF 1871 CONTRACTS ON OUR TWO EXCHANGES ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR RECORD NUMBER OF GOLD TONNES STANDING FOR FEBRUARY.

4) STRONG SIZED COMEX OPEN INTEREST INCREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///SMALL T.A.S. ISSUANCE: 918 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

TOTAL EFP CONTRACTS ISSUED: 63,061CONTRACTS OF 6,306,100 OZ OR 196,146 TONNES IN 16 RADING DAY(S) AND THUS AVERAGING: 3941 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16TRADING DAY(S) IN TONNES 196,146 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 196,146 DIVIDED BY 3550 x 100% TONNES = 5.52% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 196.146 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A GOOD SIZED ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 949 CONTRACTS OI TO 167,274 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 130 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1350 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2299 CONTRACTS AND ADD TO THE 1350 E.FP. ISSUED

WE OBTAIN A GOODSIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 401 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 2.005 MILLION OZ OCCURRED WITH OUR $0.15 LOSS IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 26,99PTS OR 0.80%

//Hang Seng CLOSED DOWN 307,59 PTS OR 1,32%

// Nikkei CLOSED DOWN 539,15 OR 1,39%//Australia’s all ordinaries CLOSED DOWN 0.73%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2481 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2624// Oil UP TO 71,01 dollars per barrel for WTI and BRENT UP TO 74.91Stocks in Europe OPENED ALL MIXED

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED4465CONTRACTS TO 529785 WITH OUR GAIN IN PRICE OF $7.65 WITH RESPECT TO MONDAY’S TRADING/. WE LOST ZERO NET LONGS WITH THAT PRICE GAIN FOR GOLD. BUT AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2750 ).

THE CME ANNOUNCED MONDAY NIGHT, ZERO EXCHANGE FOR RISK CONTRACTS FOR NIL OZ OR 0 TONNES.

AND SO FAR IN FEBRUARY: WE HAVE HAD FIVE EXCHANGE FOR RISKS NOW TOTALLING 18.4527TONNES!. THE RECIPIENT OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY.

THUS IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 7215 CONTRACTS WITH OUR GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON MONDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW CLIMBED TO 10% AS GOLD IN LONDON IS NOW EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY TODAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND FAIR T.A.S. LIQUIDATION. MONDAY // THEY ISSUED A FAIR 918 CONTRACT ANNOUNCEMENT (MONDAY NIGHT/TUESDAY MORNING).

THE FED IS THE OTHER MAJOR SHORT OF AROUND 16+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, , 203 , ,205 , 207 209 AND TODAY’S 210 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST FEW WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE ACTIVE DELIVERY MONTH OF FEBRUARY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2750 EFP CONTRACTS WERE ISSUED: : /FEB 2750 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2750 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7215 CONTRACTS IN THAT 2750 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD GAIN OF 4465 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $7.65 FOR MONDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED SIZED 918 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER A FEW WEEKS AGO, THE FED WAS EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( MONDAY TRADING// JAN 27) AS THE GOLD PRICE GOT HAMMERED A BIT WITH COMEX OPTIONS EXPIRY. AS YOU SAW WITH LAST TUESDAY’S TRADING// JAN 28 IT HAS NO EFFECT ON GOLD AS IT SHOT UP AGAIN IN PRICE AND IT CONTINUED TO RISE THROUGHOUT THE WEEK. LONDON’S ANNOUNCEMENT LAST THURSDAY THAT THEY WERE OUT OF PHYSICAL GOLD SURELY HELPED TO PROPEL GOLD’S METEORIC RISE IN PRICE THESE PAST SEVERAL DAYS PROPELLING IT THROUGH THE 2900 DOLLAR BARRIER TO THE LEVEL IT IS NOW TRADING READY TO CLOSE IN ON THE 3000 DOLLAR LEVEL.

MECHANICS OF T.A.S CONTRACTS/DECEMBER 2024

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON DEC. 27, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE DECEMBER’S OPTIONS EXPIRY TRADING AND AGAIN WITH JANUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE. ALL OF THESE T.A.S. ISSUANCES WERE USED IN AN ATTEMPT TO THWART GOLD TRADING ESPECIALLY BEFORE TRUMP’S INAUGURATION AS THE FED MUST REDUCE ITS MASSIVE PHYSICAL GOLD SHORT OF 79 TONNES. THEY FAILED MISERABLY AS GOLD SKYROCKETED IN PRICE THIS WEEK AND NOW TO ALL TIME RECORD HIGHS IN USA DOLLAR TERMS AND OTHER CURRENCIES.

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAD A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (252.2527 TONNES) WHICH IS HUGE FOR OUR ACTIVE FEB DELIVERY MONTH AND THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH.

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 252.2527 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY: 233.80TONNES OF GOLD+ + 18.4527 TONNES EX FOR RISK PRIOR=//NEW TOTAL STANDING 252,2527 TONNES

COMEX GOLD TRADING/FEB CONTRACT MONTH

THE SPECS/HFT WERE UNUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $7.65/)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OUR TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION MONDAY AS THEY WERE TRYING TO QUELL GOLD’S RISE AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING. TODAY ENDS COMEX OPTIONXS EXPIRY. HOWEVER THIS UPCOMING FRIDAY WE HAVE THE MUCH BIGGER OTC.LONDON.OTC EXPIRY.THE BANKERS WERE UNSUCCESSFUL IN SLOWING THEIR DERIVATIVE LOSSES IN PRECIOUS METAL BETS WITH OPTIONS EXPIRY LAST JAN 28 AT THE COMEX. OUR T.A.S. SPREADER LIQUIDATIONS THIS 3RD WEEK OF FEB, WERE DISTORTING OPEN INTEREST AS I EXPLAINED ABOVE, BUT IS HAVING NO EFFECT ON GOLD’S METEORIC RISE IN PRICE. PRIOR TO FRIDAY . THE RAIDS ON FRIDAYS,INCLUDING MONDAY AND TODAY WERE NEEDED TO QUELL PRICE RISES IN GOLD AND SILVER,. SILVER IS A BIG HEADACHE FOR OUR CROOKS AS THE PHYSICAL METAL IS BASICALLY UNATTAINABLE. DERIVATIVE LOSSES ON BOTH GOLD AND SILVER ARE HUGE!

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENINGTUESDAY MORNING AND THUS OUR RECORD NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD)

EXCHANGE FOR RISK EXPLANATION/DECEMBER AND JANUARYTRADING

DECEMBER MONTH EXCHANGE FOR RISK!

78 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 6 FOR 14.6836 TONNES A NEW RECORD. THE COMEX IS TOTALLY SHATTERED TO PIECES.

EXCHANGE FOR RISK // JANUARY MONTH!!

LO AND BEHOLD, THE CROOKS ISSUED THEIR FIRST ISSUANCE A MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THEN TO MY HORROR, THEY ISSUED THEIR SECOND EXCHANGE FOR RISK ON JAN 8, TOTALLING 150 CONTRACTS FOR 15000 OZ OR .4665 TONNES. THIS TONNAGE WILL BE ADDED TO THE FIRST ISSUANCE. THUS TOTAL EXCHANGE FOR RISK ISSUANCE FOR OUR TWO EARLY JANUARY EX FOR RISK: 5.7533 TONNES. THEN MERCILESSLY THEY CONSUMMATED FOR THE THIRD TIME THIS MONTH 85 EXCHANGE FOR RISK LAST THURSDAY NIGHT (JAN 17) FOR 8500 OZ OR .2649 TONNES OF GOLD. THEN TO MY HORROR THEY ISSUED THEIR 4TH EXCHANGE FOR RISK THIS MONTH (JAN 22) FOR A MONSTER 5000 CONTRACTS OR 5,000,000 OZ.(15.562 TONNES).NOT TO BE UNDONE, THE CROOKS ISSUED THEIR FIFTH EXCHANGE FOR RISK LAST NIGHT FOR 500 CONTRACTS REPRESENTING 50,,000 OZ OR 1.555 TONNES OF GOLD. REMEMBER THAT THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON WHICH IS TOTALLY ASININE!! THUS FOR THE 5 EXCHANGE FOR RISK ISSUED THIS MONTH TOTALS 23.134 TONNES OF GOLD. THIS BRINGS US TO , JAN 25 WHERE THE CME ANNOUNCED ITS SIXTH MAJOR EXCHANGE FOR RISK ISSUANCE OF 6454 CONTRACTS FOR 645,400 OZ OR 20.074 TONNES OF GOLD. THIS IS THE HIGHEST EVER RECORDED ISSUANCE IN NUMBER OF EXCHANGE FOR RISK, AT 6, AND FOR NEW TOTALS FOR THE MONTH OF JANUARY: 43.208 TONNES!!! AND A NEW RECORD FOR ISSUANCE.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO, THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WILL NOW BE ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FOR FRIDAY FEB 21 ZERO EXCHANGE FOR RISK WAS ISSUED.

FINAL STANDING GOLD/COMEX FOR JANUARY

FINAL STANDING FOR JAN: 70.102TONNES + 43.206 TONNES EX FOR RISK = 113.310 TONNES (WHICH IS HUGE FOR OUR VERY NON ACTIVE DELIVERY MONTH) A NORMAL AMOUNT STANDING FOR A JANUARY IN EARLIER TIMES HAS BEEN GENERALLY AROUND 1/4 TONNE OF GOLD. HOWEVER THESE PAST 4 YEARS QUEUE JUMPING HAS BEEN VERY PRONOUNCED AND THUS STANDING INCREASES DRAMATICALLY.

TOTAL INITIAL DELIVERIES FEB GOLD TRADING

WE HAVE GAINED A STRONG SIZED TOTAL OF 22.44PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB (184.40TONNES) ON FIRST DAY NOTICE FOLLOWED BY A STRONG SIZED 280 CONTRACT QUEUE JUMP FOR 28,000 OZ. NEW STANDING ADVANCES TO 233.80 TONNES OF GOLD. TO WHICH WE ADD OUR 18.4527TONNES OF EXCHANGE FOR RISK//NEW TOTALS STANDING 252.2527 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $7.65

WE HAD 913CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 7215 CONTRACTS OR 712500 0Z (22.44 TONNES)

i) Into Brinks customer acct: 9677,459 oz (301 kilobars) .301 tonnes

total customer and dealer in tonnes:4.798 tonnes

No of oz served (contracts) today

326 notice(s) 32,600 OZ 1.0139 TONNES

No of oz to be served (notices)

323 contracts 32300 OZ 1.0047 TONNES

Total monthly oz gold served (contracts) so far this month

74,844 notices 7,484,400 oz 232.79 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

dealer deposits: 1

1 ENTRY

I) Brinks dealer 144,587.047oz

4.497 TONNES

we have 1 customer deposits:

1 ENTRIES

i) Into Brinks customer acct: 9677,459 oz (301 kilobars) .301 tonnes

total customer and dealer in tonnes:4.798 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 1

1 entry

i) Out of JPMorgan 83,004.724 oz 2,581 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxx

adjustments:2/comex is in chaos

a)customer to dealer

a) Manfra 15,961,408 oz oz

dealer to customer

b) ASAHI 203,465.191oz

thus basically what comes into eligible is transferred to dealer accounts and then out.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB

FEB HAD A LOSS OF 124 CONTRACTS TO STAND AT 649 WE HAD 404 CONTRACTS SERVED ON FRIDAY SO WE GAINED A HUGE 280 CONTRACTS OR A 28,000OZ QUEUE JUMP OR 0.8709TONNES,.( THURSDAY, FEB 13 WE WITNESSED THE HIGHEST EVER QUEUE JUMP RECORDED AT THE COMEX AT 12.12 TONNES)

MARCH HAD A LOSS OF 646 CONTRACTS DOWNTO 14,417

APRIL HAD A GAIN OF 4053 CONTRACTS UP TO 389,012CONTRACTS

MAY GAINED 7CONTRACTS UP TO 19.

We had 326 contracts filed for today representing 32,600oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 326 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 291 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2025. contract month, we take the total number of notices filed so far for the month (74,844X 100 oz ) to which we add the difference between the open interest for the front month of FEB.(649CONTRACTS) minus the number of notices served upon today (326 x 100 oz per contract) equals 7,516,700 OZ OR 233.80 TONNES TO WHICH WE ADD NEW EXCHANGE FOR RISK 18.4527 TONNES//NEW TOTAL STANDING 251.3827TONNES

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (74,844 x 100 oz +we add the difference for front month of FEB ( 649 OI} minus the number of notices served upon today (326 x 100 oz) which equals 7,516,700Oz (233.80TONNES + 18,4527 tonnes ex for risk PRIOR = 252.2526 tonnes

TOTAL COMEX GOLD STANDING FOR FEB.: 252.2527 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR AND THIS IS THE HIGHEST EVER RECORDED FOR ANY FEBRUARY AND THE HIGHEST FOR ANY MONTH FOR THAT MATTER IN COMEX HISTORY!!

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 38,882,330.307 .oz

TOTAL REGISTERED GOLD 17,892,729.886or 556.539onnes

TOTAL OF ALL ELIGIBLE GOLD: 20,989,600.421 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,818,257oz (REG GOLD- PLEDGED GOLD)= 492.01 tonnes //

END

SILVER/COMEX

FEB 25

INITIAL

// THE FEB 2025 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

0

Deposits to the Dealer Inventory

606,053,000 oz Asahi

Deposits to the Customer Inventory

6 entries

i) Into Asahi 3,044,520 oz ii) Into Brinks: 297,224,900 oz iii) Into CNT 679,224,900 oz iv) Into Delaware 20,762,924 oz v) Into JPM 1,184,170.720 oz vi) Into Manfra: 161,115.700 oz total weight 2,345,508,114 oz

No of oz served today (contracts)

80 CONTRACT(S) (0.400MILLION OZ

No of oz to be served (notices)

148 contracts (0.740MILLION oz)

Total monthly oz silver served (contracts)

4563 Contracts (22.815million oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 1 dealer deposit/

317,690.100 Loomis

total dealer deposit 317,690.100 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

6 entries

i) Into Asahi 3,044,520 oz ii) Into Brinks: 297,224,900 oz iii) Into CNT 679,224,900 oz iv) Into Delaware 20,762,924 oz v) Into JPM 1,184,170.720 oz vi) Into Manfra: 161,115.700 oz

JPMorgan has a total silver weight: 158.884million oz/395.318million or 40.25%

TOTAL REGISTERED SILVER: 120.275MILLION OZ//.TOTAL REG + ELIGIBLE. 395.318Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB /2025 OI: 228 OPEN INTEREST CONTRACTS FOR A GAIN OF 111 CONTRACTS.

WE HAD 0 NOTICES FILED ON MONDAY SO WE GAINED 111 CONTRACTS OR WE EXPERIENCED A 555,000 OZ EXCHANGE FOR PHYSICAL TRANSFER AS THESE GUYS WILL TRY THEIR LUCK LOOKING FOR SILVER IN NEW YORK,

MARCH SAW A LOSS OF 11,779CONTRACTS UP TO 41,218THE FRONT ACTIVE DELIVERY MONTH OF MARCH ALSO IS NOT DECLINING MUCH AND WE SHOULD ALSO HAVE A HUMDINGER OF A DELIVERY MONTH FOR MARCH. WE HAVE 3 MORE READING DAYS BEFORE FIRST DAY NOTICE.

APRIL SAW ANOTHER GAIN OF 147 CONTRACTS TO STAND AT 1348

MAY SAW A GAIN OF 10,090CONTRACTS UP TO 101,253 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 80 or 0.400MILLION oz

CONFIRMED volume; ON MONDAY 104,666huge//

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 4543 X5,000 oz = 22.815 MILLION oz

to which we add the difference between the open interest for the front month of FEB (228 AND the number of notices served upon today (80 )x (5000 oz)

Thus the standings for silver for the FEB 2025 contract month: 4563 Notices served so far) x 5000 oz + OI for the front month of FEB(228)minus number of notices served upon today (80)x 5000 oz equals silver standing for the FEB contract month equating to 23.455 MILLION OZ.

New total standing: 23.455 million oz which is huge for a non active delivery month of February

There are 120.275million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

FEB 13/ WITH GOLD UP 11.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 6.901 TONNES FROM THE GLD ///INVENTORY RESTS AT 866.50TONNES

FEB 12 WITH GOLD DOWN $3,40ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 10 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 7 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 6 WITH GOLD DOWN $18.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.14 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

FEB 5 WITH GOLD UP $27.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 863.05 TONNES

FEB 4 WITH GOLD UP $25.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.58 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.77 TONNES

JAN 31 WITH GOLD UP $4.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 30 WITH GOLD UP $40.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 865.34 TONNES

JAN 29 WITH GOLD DOWN $6.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.02 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 861.04 TONNES

JAN 28 WITH GOLD UP $23.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.16 TONNES OF GOLD OUT OF THE GLD //

JAN 27 WITH GOLD DOWN $36.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///

JAN 24 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 23 WITH GOLD DOWN $1.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 2.30 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 869.36 TONNES

JAN 22 WITH GOLD UP $15.15 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 7.46 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 871.66 TONNES

JAN 20 WITH GOLD UP $35.30 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 10.34 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 879.12 TONNES

GLD INVENTORY: 907,83 TONNES, TONIGHTS TOTAL

SILVER

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 12WITH SILVER UP $.01 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 8 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 10 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 7 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 6 WITH SILVER DOWN $0.17 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 12.383 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 430.39 MILLION OZ

FEB 5 WITH SILVER UP $0.45 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 3.285 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 442.773 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 3 WITH SILVER UP ONE CENT //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

JAN 31 WITH SILVER DOWN $0.19 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.369 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 448.881 MILLION OZ

jAN 30 WITH SILVER UP $0.76 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.003 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 451.249 MILLION OZ

jAN 29 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.639 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 453.252 MILLION OZ

jAN 28 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.821 MILLION OZ OUT OF THE SLV./. /

jAN 27 WITH SILVER DOWN $.61 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 24 WITH SILVER DOWN $.21 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 23 WITH SILVER DOWN $.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 4.738 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 459.035 MILLION OZ

JAN 22 WITH SILVER UP $.08 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 0.721 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 464.043 MILLION OZ

JAN 20 WITH SILVER DOWN $.09 //NO CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.568 MILLION OZ FROM THE SLV./. //INVENTORY AT SLV RESTS AT 463.315 MILLION OZ

CLOSING INVENTORY 441.406MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

In recent decades, China which ranks fifth in global silver reserves has not only mined 3,500—4,000 tonnes annually but imported large quantities of silver doré for refining as well. Less well known is the Peoples Bank’s role in managing silver reserves, which is still regarded in China as a monetary metal. China was on a silver standard only ninety years ago.

Today, gold is the principal monetary metal, and silver is widely regarded as industrial only. But since 1983, along with gold the PBOC has been responsible for overseeing the accumulation of the nation’s silver bullion reserves. The key to this policy has been price management. This article tells how this was achieved.

Introduction

About twelve ago, I had a speaking gig in New York at a conference attended by about a dozen silver mining and exploration companies. At that time, conspiracy theories about JPMorgan’s dealings in the silver market were rife. But when Blythe Masters, then Head of Global Commodities at JPMorgan went on CNBC, she made JPMorgan’s position clear:

“Speculation is [rife] particularly in the blogosphere about this topic and I think the challenge is that speculation represents a misunderstanding as the nature of our business. As I mentioned earlier our business is a client driven business where we execute on behalf of clients to achieve their financial and risk management objectives. The challenge is that commentators don’t see all of that activity simultaneously. So just to give you a simple example we store significant amounts of commodities, for example silver on behalf of customers. We operate vaults in New York City, in Singapore, and in London. And often when customers have that metal stored in our facilities, they hedge it on a forward basis through JPMorgan who in turn hedges itself in the commodity markets. If you see only the hedges and our activity in the futures market, but you aren’t aware of the underlying client position then hedging it would suggest inaccurately that we’re running a large directional position. In fact, that’s not the case at all. We have offsetting positions. We have no stake in whether prices rise or decline. Rather, we’re running a flat or a relatively natural… [interviewer interrupts]”[i]

Silver bulls rushed to condemn her, calling her a liar and worse. But I was convinced that a senior executive of her undoubted ability and in her position would be telling the truth. Furthermore, I suspected that Masters did the CNBC interview specifically to quash the wild rumours about JPMorgan’s silver dealing rather than ignore them.

So, what was JPMorgan’s true role in the market? Clearly, it was dealing for clients and not taking one-sided positions. As Masters revealed, the bank only took out derivative positions to hedge their dealings with clients, maintaining a level book.

The conference in New York gave me a chance to dig a little deeper. I asked the dozen or so silver companies present there the process of how they turned their silver at the mine into cash to pay their costs. They all said that the process started with an assessment of the silver doré’s value by a specialist assessor from Glencore or Trafigura, who then arranged for payment and shipment to a refiner. None of the miners admitted they knew where the doré was shipped to for refining — it was no longer their business. But the common assumption was probably China.

Glencore and Trafigura are huge commodity traders acting for large mining corporations as well as the miners I interviewed. They obviously worked with a major bank on the payments side, which is where JPMorgan would come into the picture. As soon as the doré was shipped, the cashflow hungry miner would be paid on the assessor’s valuation. Likely, it would be shipped FOB Origin, which means the doré enters Chinese possession at the point of shipment, and payment would be through JPMorgan’s books.

Presumably, China instructed JPMorgan to hedge the silver price on Comex or London, effectively dumping silver onto the market before it was in deliverable form. Note that this is not JPMorgan acting as principal but acting for the refiner (China) as a client. The consequence was for JPMorgan to continuously feed short positions into Comex, suppressing the price. But as Masters made clear JPMorgan was not taking a position for itself, only dealing for the Chinese as client.

As well as being a large miner herself, China was refining cheaply considerable amounts of imported doré when some western refineries were closing down on environmental and cost grounds. So, the hedging book through JPMorgan would have been significant, depressing the spot price through Comex dealings. We can take this even further, in the context of a normal dealer/client relationship. As dealer and client work together, an element of dealing discretion can be given to the dealer along with dealing objectives.

So what might those objectives be?

As a major buyer of doré, it would have been in China’s interests to keep the price as low as possible. And it would have been the means for China to accumulate substantial silver reserves for monetary purposes, which she had already done with gold.

In this context, the original 1983 Regulations on the Control of Gold and Silver appointing the Peoples Bank of China states:

Article 4. The People’s Bank of China shall be the State organ responsible for the control of gold and silver in the People’s Republic of China.

The People’s Bank of China shall be responsible for the control of the State’s gold and silver reserves; responsible for the purchase and sale of gold and silver; work in conjunction with the authority responsible for commodity prices to formulate and administer a purchase and sales price for gold and silver [my emphasis]; work in conjunction with the competent department to examine and approve the operations (including processing and sales) of units (hereinafter referred to as managing units) dealing in gold and silver products, chemical products containing gold and silver, the recovery of gold and silver from residual liquid and solid wastes; control and inspect the gold and silver market and supervise the implementation of these Regulations.

Note the PBOC’s responsibility for controlling the price of silver.

We know or should know that in the period 1983—2002 when the Shanghai Gold Exchange finally came into existence under the control of the PBOC, that the PBOC was able to secretly accumulate vast quantities of gold which was in a deep bear market with American and European financial communities liquidating their bullion holdings in favour of dollars. I believe that during this period China secretly acquired as much as 20,000 tonnes, spread round various state bodies.

These easy conditions for accumulating gold were not generally true for stockpiling silver in the larger quantities required reflected in the price relationship between the two monetary metals. The PBOC had to use different tactics. The practical way to accumulate massive quantities of silver was to become the world’s refiner and manage the price — in other words keep it suppressed principally by selling as a covered bear in paper markets.

Blythe Masters had no need to lie about JPMorgan’s role in this. Between Glencore/Trafigura and China as its customers, JPMorgan would be central to achieving the outcome China desired.

There is another aspect to this puzzle rarely mentioned. Note, that under Article 4 of the Regulations appointing the PBOC that no distinction is made between gold and silver. For the purposes of the regulations, silver is as much money as gold, a reserve to be controlled by the central bank as general backing for the currency.

It should be remembered that China was on a silver standard as recently as 1935. Ordinary people accumulated silver as wealth and banks kept reserves in silver. For the Chinese population, silver was their money as much as gold was in the west. There is every reason why silver should be singled out in the Regulations to have the same status as gold.

Will China continue to suppress prices? Those days are probably over. Almost certainly, China has accumulated substantial silver reserves, more than enough for a supporting monetary role to gold. The state’s monetary silver reserves are likely to be segregated from industrial production, which has become an uncontrollable source of demand.

Clearly, the PBOC understands the role of monetary metals, which is ultimately to secure the value of credit. They know that gold and silver values are generally stable, and that it is credit which declines. Their very public disposal of dollars for gold tells us that they are no longer suppressing prices of gold. What goes for gold must also apply to their policy regarding silver.

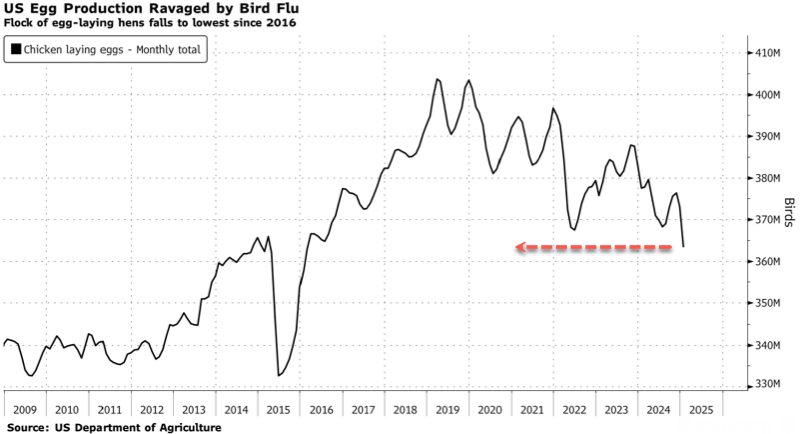

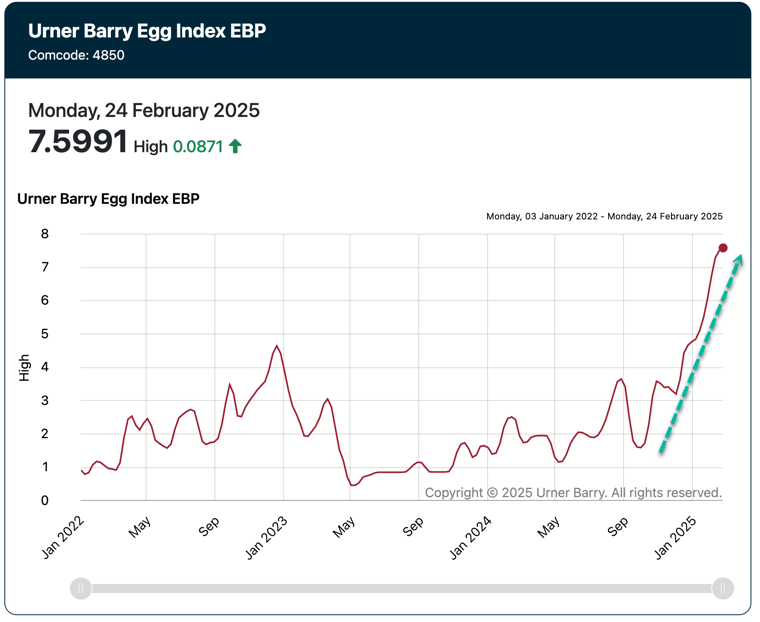

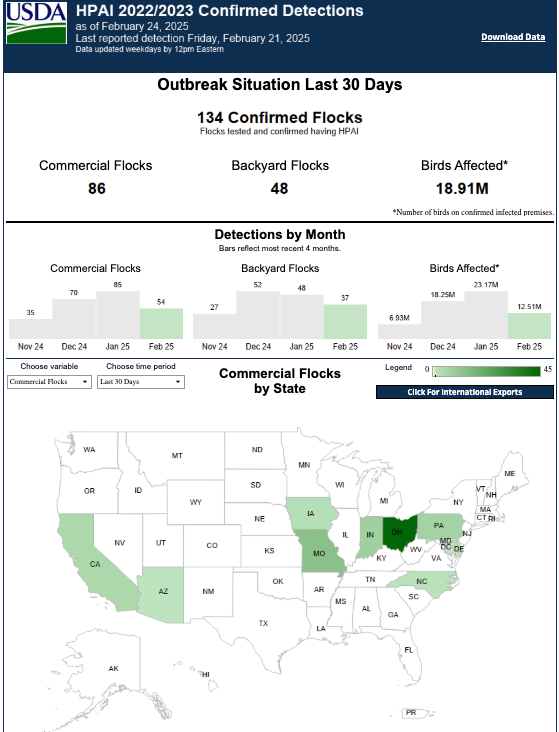

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY//EGGS

US Egg-Laying Hen Population Implodes, Wholesale Egg Prices Hit New Record

Tuesday, Feb 25, 2025 – 01:20 PM

Under the Biden-Harris administration, farmers were forced to cull tens of millions of egg-laying hens to contain the bird flu outbreak. As a direct result, the nation’s total egg-laying flock has plunged to its lowest level in nearly a decade, driving wholesale egg prices to record highs.

Trump stated this week that Secretary of Agriculture Brooke Rollins will take action on soaring egg prices, adding, “We inherited all the problems.”

Trump is correct in saying the egg-flation mess was “inherited,” as the latest Bloomberg data shows that the nation’s egg-laying hen population fell to its lowest level since 2016 last month. This decline was driven by farmers being forced to cull flocks under Biden’s first term to curb the bird flu outbreak.

“It was important to me to see firsthand an egg-laying farm facility implementing strong biosecurity measures. We have a lot of work to do as we combat avian flu, help our poultry industry recover, and bring the price of eggs down for all Americans. More coming mid-week on this,” Rollins wrote on X on Monday.

Monday’s print of the Urner Barry Egg Index EBP shows wholesale prices jumped to $7.56, a new record high. Since late Decemeber, wholesale prices have jumped to new record highs by the week, with reports of egg shortages nationwide.

According to the USDA’s bird flu dashboard, 19 million birds across the Lower 48 have been infected by avian influenza over the last 30 days.

It’s time to set up those chicken coops, folks.

Panic searching on Google.

And don’t forget honeybees and victory gardens—become self-sufficient and take back control of your own food supply chain instead of relying on mega-corporations that poison food with toxic seed oils and other chemicals in processed foods.

// Nikkei CLOSED DOWN 539,15 OR 1,39%//Australia’s all ordinaries CLOSED DOWN 0.73%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2481 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2624// Oil UP TO 71,01 dollars per barrel for WTI and BRENT UP TO 74.91Stocks in Europe OPENED ALL MIXED

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2481

OFFSHORE YUAN: DOWN TO 7.2624

SHANGHAI CLOSED CLOSED DOWN 26.99 PTS OR 0..80%

HANG SENG CLOSED CLOSED DOWN 307.85PTS OR 0.32%

2. Nikkei closed DOWN 539,15 OR 1,39%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 106.59// EURO RISES TO 1.0463 UP 3 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: FALLS TO. +1.372 //Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 149.44…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4770/Italian 10 Yr bond yield DOWN to 3.557 SPAIN 10 YR BOND YIELD DOWN TO 3.156

3i Greek 10 year bond yield DOWN TO 3.3000

3j Gold at $2940.65 Silver at: 32.22 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 99 /100 roubles/dollar; ROUBLE AT 86.75

3m oil into the 70 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149,44 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.372 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8969 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9385 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.345 DOWN 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.613 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.125 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 36.46…

10 YR UK BOND YIELD: 4.5940 UP 3 PTS

10 YR CANADA BOND YIELD: 3.071 DOWN 4BASIS PTS

5 YR CANADA BOND YIELD: 2.763 DOWN 4 PTS.

2a New York OPENING REPORT

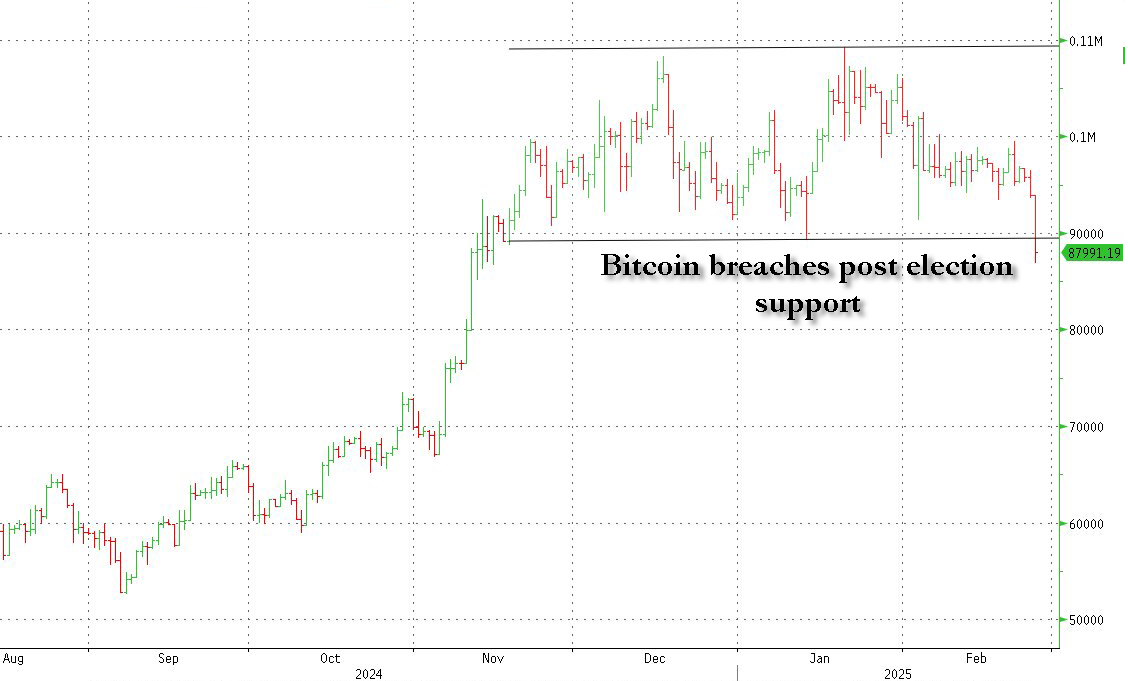

Futures Drop As Momentum Massacre Crushes Bitcoin

Tuesday, Feb 25, 2025 – 07:30 AM

US equity futures, and Asian markets are lower as the recent tech-led selloff on Wall Street accelerated, sparking further risk-off behavior and momentum liquidations, and spilling over into bitcoin which plunged to a 3 month low breaking below its post election support. As of 7:00am, S&P futures are down 0.3% and are outperforming Nasdaq futs which are down 0.5%; sentiment was dented after Trump said that Canada/Mexico tariffs would be implemented on-time. Mag7 names and semis are lower with NVDA down 1.6%; Europe’s ASML and STMicroelectronics also Bloomberg reported that the Trump admin is planning to expand efforts to limit China’s technological advancements, including tougher semiconductor curbs and pressuring allies to escalate restrictions on China’s chip industry. The ongoing stock rout sparked a rally in Treasuries that has pushed US 10-year yields down 6 bps to 4.34%. Traders also added to their Federal Reserve interest-rate cut bets with ~53 bps of easing now priced in by year end; the USD is flat. Commodities are mostly lower with crude/gasoline higher. Today’s macro data focus is on Housing, regional Fed activity indicators, and Consumer Confidence.

Meanwhile Bitcoin tumbled 7%, dropping below $90,000 and sliding to a 3 month low of $88,000 breaking post-election support levels, as the recent momentum massacre sparked a brutal crypto selloff; meanwhile DeepSeek reopened access to its core programming interface after nearly a three-week suspension.

In premarket trading, Nvidia led premarket losses among the Mag 7 stocks after Bloomberg News reported that Donald Trump’s administration is pressuring US allies to escalate their chip restrictions on China (Nvidia -1.3%, Alphabet -0.7%, Amazon, Alphabet, Microsoft, Meta and Apple were falling less than 1%, Tesla was little changed). US-listed Chinese stocks broadly rebound, with Alibaba rising 3.8% following its biggest drop since 2022; JD.com is up 1.8%, PDD +1.4%, Baidu +0.8%, Bilibili +2.8%. here are some other notable premarket movers:

Chegg shares tumble 22%, after the education technology company’s first-quarter projections for revenue and adjusted Ebitda trailed Wall Street expectations.

Hims & Hers Health shares slide 18% in premarket trading after the telehealth company reported fourth-quarter results and said it will soon stop selling some compound weight-loss drugs. While the results were solid, Piper Sandler noted that there was a high level of uncertainty for 2025.

Cryptocurrency-exposed stocks slide as Bitcoin tumbles below $90,000 to hit the lowest level since mid-November, paring the gains seen since Donald Trump’s election to the White House. MicroStrategy -5.9%, Coinbase -5.6%, Riot Platforms -4.4%, MARA Holdings -6%, Bit Digital -6.6%, CleanSpark -5.8%, Hut 8 Mining -6.7%

Zoom Communications shares fall 5%, after the communications software company gave a forecast that is modestly weaker than expected.

As broad-based selling swept markets, the VIX Index touched its highest level this year at just below 20. There didn’t appear to be a single catalyst for the selling – the suddenly pervasive pessimism was correctly described here two days ago in “Goldman Traders Hit The Panic Button: Perfect Sell Storm Of Positioning, Valuation, Breadth, Concentration And Policy“- although concerns are mounting that President Trump’s policies will hurt global economic growth. Uncertainty on trade policies has prompted investors to pare risk and switch to havens like Treasuries or gold. Trump signaled Monday that tariffs on Mexican and Canadian imports will go ahead.

“At the moment there’s a lot of uncertainty reigning in the background which is making it challenging for investors to navigate,” said Alexandra Morris, an investment director at Skagen AS. “The whole tariff discussion is the main negative catalyst.”

Nvidia’s earnings report on Wednesday could be yet another catalyst to unleash volatility given its outsized impact on the broader market.

“Bear in mind that the market impact of Nvidia’s results have often proved to be as significant as US jobs reports over the last couple of years,” Deutsche Bank AG strategist Jim Reid wrote in a note to clients.

In Europe, tech stocks also underperformed but have been offset by gains in healthcare and banks with the Stoxx 600 rising 0.3%. European defense stocks rose after Bloomberg reported that Germany’s chancellor-in-waiting Friedrich Merz is in talks with the Social Democrats to approve up to €200 billion in special defense spending. Unilever shares fell after the company announced in a surprise move that CEO Hein Schumacher would step down and pass the reins to CFO Fernando Fernandez. Here are the biggest movers Tuesday:

Smith & Nephew shares rise as much as 10%, the most since August, after reporting 4Q sales that beat estimates. The report is likely to reassure investors, RBC said, flagging particular strength in orthopaedics in the US

Novo Nordisk rises as much as 5.2%, to the highest since Dec. 20, after US firm Hims & Hers Health said it will soon stop selling some compound weight-loss drugs rivaling the Danish company’s offering

Galp Energia shares jump as much as 7.9%, the most in 10 months, after the company reported success at its latest exploration well off Namibia, boosting confidence in the company’s broader Namibia play

Thyssenkrupp shares rise as much as 15% in Frankfurt, to the highest since October 2023, after Citi increased its price target, citing the potential value unlock from the company’s marine and steel businesses

Dormakaba shares gain as much as 3.9%, to the highest level since 2021, after the Swiss security company lifted profit guidance slightly and posted solid results

European semiconductor stocks drop after Bloomberg reported that the Trump administration is pressuring US allies to escalate their chip restrictions on China

European mining stocks fell after iron ore, copper and aluminum dropped in response to moves by the US to restrict Chinese investments

Unilever shares drop as much as 3.4% in London trading after the consumer goods company said Hein Schumacher would step down as chief executive officer and board director

SIG Group shares tumble as much as 13%, the most in five years, after the Swiss carton-packaging maker reported subdued full-year results. Analysts cite falling profitability, low growth in the Americas

European automakers underperform after passenger-car registrations dropped in January, while electric vehicle sales jumped; total sales in the region declined 2.1% year on year

Earlier in the session, Asian stocks fell as US President Donald Trump’s continued attempts to pressure China and other nations dented investor sentiment. The MSCI Asia Pacific Index slid as much as 1.4% before paring some losses. Chinese stocks whipsawed throughout the day, showcasing the volatility sparked by uncertainties around Trump’s actions. His administration is said to be sketching out tougher versions of US semiconductor curbs and pressuring key allies to escalate their restrictions on China’s chip industry. According to Bloomberg, Trump officials recently met with their Japanese and Dutch counterparts about restricting Tokyo Electron Ltd. and ASML Holding NV engineers from maintaining semiconductor gear in China, according to people familiar with the matter. This comes after a directive set the stage for a more muscular use of the Committee on Foreign Investment in the United States, or CFIUS, a secretive panel that scrutinizes proposals by foreign entities to buy US companies or property, to thwart Chinese investment. The Hang Seng Tech Index had slumped as much as 4.4%, pacing losses for Chinese equities in New York. The gauge later erased most of its decline as more than $1 billion worth of money poured into Hong Kong stocks from China. JPMorgan strategists said US moves to limit investment in China tech may trigger a reversal in mainland stocks after the recent rally, while some investors saw an opportunity buy on dips. TSMC, Hitachi and Alibaba were among the biggest drags on the regional gauge. Most national benchmarks were in the red.

In FX, the Bloomberg Dollar Spot Index rises 0.1%. The Aussie and kiwi dollars underperform, falling 0.4% each.

In rates, bonds surged, pushing the yield on 10-year Treasuries down six basis to 4.34%. The treasury rally sent yields to YTD lows, fueled by risk aversion tied to the potential for US tariff policies to dent economic growth. Swap spreads are notably tighter, a sign that receiving flows are a driver. In short-term rates, Fed-dated OIS revert to fully pricing in two 25bp rate cuts by year-end. US yields are near session lows, 6bp-8bp richer across maturities with gains led by the belly, steepening 5s30s spread by 2bp; 10-year touched 4.32% and outperforms German counterpart by 7bp, UK by 3bp. 10- and 30-year swap spreads are nearly 2bp tighter on the day; Dallas Fed President Lorie Logan during London morning said the central bank when it stops balance-sheet runoff should purchase more shorter-term than longer-term securities to mirror the composition of Treasury issuance. A widely-watched gauge of the attractiveness of German debt fell to the most negative on record, reflecting expectations for higher borrowing to fund big outlays on defense spending. Gilts followed Treasuries higher, with UK 10-year yields falling 3 bps to 4.53%. German 10-year borrowing costs are flat at 2.47% as bunds were held back by reports of emergency defense spending.