GOLD CLOSED UP $19.05 TO $2909.80

SILVER CLOSED UP 9 CENTS TO $31.77

GOLD ACCESS CLOSED 2914.50

Silver ACCESS CLOSED: $31.90

Bitcoin morning price:$83,945 DOWN 2100 DOLLARS.

Bitcoin: afternoon price: $87,566 UP 1521. DOLLARS

Platinum price closing UP $10.55 TO $965.25

Palladium price; UP $5.70 TO $950.85

END

*CANADIAN GOLD: $4197.25 UP 6.72 CDN dollars per oz( * NEW ALL TIME HIGH 4208.15CDN DOLLARS PER OZ//FEB 24 2025)

*BRITISH GOLD: 2277.42 UP 1.23 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,339.25 BRITISH POUNDS/OZ) FEB 10/2025

*EURO GOLD: 2,744.27 DOWN 12.51 Euros per oz //* (ALL TIME CLOSING HIGH: 2,819,78UROS PER OZ/FEB 24 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE

EXCHANGE: COMEX

CONTRACT: MARCH 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,890.200000000 USD

INTENT DATE: 03/03/2025 DELIVERY DATE: 03/05/2025

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 127

118 C MACQUARIE FUT 333

118 H MACQUARIE FUT 324

363 H WELLS FARGO SEC 83

624 H BOFA SECURITIES 56

657 C MORGAN STANLEY 270

661 C JP MORGAN 21

686 C STONEX FINANCIA 20 33

690 C ABN AMRO 16

709 C BARCLAYS 71

737 C ADVANTAGE 4 4

TOTAL: 681 681

JPMORGAN STOPS 11/686 CONTRACTS

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2024. CONTRACT: 681 NOTICES FOR 68100 OZ 2.118 TONNES

total notices so far: 11,067 contracts for 1,106,700 Oz (34.388 tonnes)

FOR MARCH

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 659 NOTICE(S) FILED FOR 3.295 MILLION OZ/

total number of notices filed so far this month : 11,774 for 58.870 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $19.05 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 3.45TONNES

INVENTORY RESTS AT 900.93 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP 9 CENTS AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 436.673 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 342 CONTRACTS TO 145,957 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE GAIN OF $0,78 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A SMALL GAIN OF 138 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR HUGE GAIN IN PRICE//MONDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON MONDAY COMEX TRADING / AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON MONDAY WITH SILVER’S HUGE GAIN IN PRICE. WE HAD A HUGE T.A.S. LIQUIDATION MONDAY COUPLED WITH ANOTHER NEW HUGE T.A.S. ISSUANCE OF 949 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.00 DOLLAR MARK. WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND 95 CENTS AND A LEASE RATE OF 6%. WE HAD A GOOD 480 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 949 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY.S TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A SMALL SIZED 138 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR HUGE GAIN IN PRICE. WE HAD HUGE TAS LIQUIDATION THROUGHOUT MONDAY’S COMEX TRADING SESSION WHICH ACCOUNTS FOR THE SMALLISH GAIN IN OI ON OUR TWO EXCHANGES.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A HUGE 949 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.78 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A FAIR GAIN IN OUR TWO EXCHANGES OF 303 CONTRACTS WE HAD A MASSIVE LIQUIDATION OF T.A.S. CONTRACTS TRYING TO CONTAIN SILVER’S PRICE RISE AND THAT ACCOUNTS OF MOST OF OUR OPEN INTEREST FALL.

WE HAD A 480 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 78.753 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE 1.02 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON

INITIAL STANDING FOR MARCH REDUCES TO 74.666 MILLION OZ

WE HAD:

/ FAIR COMEX OI LOSS+// A STRONG SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 949 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 165 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 2 DAYS, total 830ontracts: OR 4.150 MILLION OZ (415 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 4.150 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 4.15 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 342 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE OF 78 CENTS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A 480 CONTRACT EFP ISSUANCE CONTRACTS: 480 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH OF 78.455 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S MASSIVE 1.04 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON//NEW STANDING REDUCES TO 74.555 MILLION OZ

WE HAVE 1). A SMALL SIZED GAIN OF 138 OI CONTRACTS ON THE TWO EXCHANGES DESPITE OUR HUGE GAIN IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 949 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//MONSTER FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON MONDAY WITH THE HUGE GAIN IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (949 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 659 NOTICE(S) FILED TODAY FOR 3.295 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 787 OI CONTRACTS TO 488,842 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A STRONG SIZED 646 CONTRACTS//

WE HAD A SMALL SIZED DECREASE IN COMEX OI (787 CONTRACTS) OCCURRED DESPITE OUR GAIN OF $50.85 IN PRICE MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 31.757 TONNES FOLLOWED BY TODAY’S HUGE 50,300 OZ QUEUE JUMP (1.5675 TONNES)//NEW STANDING ADVANCES TO 35.042 TONNES

/NEW STANDING FOR MARCH; 35.042 TONNES

/ ALL OF THIS HAPPENED WITH OUR $50.85 GAIN IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD A FAIR SIZED GAIN OF 2548 OI CONTRACTS (7.925 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE FRONT MARCH CONTRACT MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3335 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 489,488

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2548 CONTRACTS WITH 787 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3194 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2548 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1658 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3335 CONTRACTS) ACCOMPANYING THE SMALL SIZED DECREASE IN COMEX OI OF 787 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3194 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH 31.757 TONNES FOLLOWED BY TODAY’S HUGE 1.5645 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 35.042 TONNES

NEW STANDING FOR MARCH ADVANCES TO:

35.042 TONNES

//NEW STANDING MARCH: 35.042 TONNES

.

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE MONDAY WITH NO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WITH OUR1) $50.85 PRICE GAIN WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A FAIR GAIN OF 2548 CONTRACTS ON OUR TWO EXCHANGES ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN MARCH

4) SMALL SIZED COMEX OPEN INTEREST DECREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1658 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH :

TOTAL EFP CONTRACTS ISSUED: 5999 CONTRACTS OF 599,900 OZ OR 18.659 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 3000 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 18.659 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 18.659 DIVIDED BY 3550 x 100% TONNES = 0.525% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 18.659 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A FAIR SIZED 342 CONTRACTS OI TO 146,957 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 480 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 480 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 480 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 342 CONTRACTS AND ADD TO THE 480 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 138 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.6900 MILLION OZ OCCURRED WITH OUR $0.78 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 7.29 PTS OR 0.22%

//Hang Seng CLOSED DOWN 64.50 PTS OR 0.28%

// Nikkei CLOSED DOWN 454.29OR 1,20%//Australia’s all ordinaries CLOSED DOWN .68%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2572 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2613/ Oil UP TO 67/12 dollars per barrel for WTI and BRENT UP TO 70.37 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

END

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 787 CONTRACTS TO 488,842 DESPITE OUR HUGE GAIN IN PRICE OF $50.85 WITH RESPECT TO MONDAY’S TRADING/. WE LOST ZERO NET LONGS WITH THAT PRICE LOSS FOR GOLD. BUT AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3335 ).

THE CME ANNOUNCED MONDAY NIGHT, ZERO EXCHANGE FOR RISK CONTRACTS FOR NIL OZ OR 0 TONNES.

IN FEBRUARY: WE HAD FIVE EXCHANGE FOR RISKS TOTALLING 18.4527 TONNES!. THE RECIPIENT OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY.

THUS IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 2548 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON MONDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW CLIMBED TO 10% AS GOLD IN LONDON IS NOW EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY TODAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION// MONDAY // THEY ISSUED A FAIR 1658 CONTRACT ANNOUNCEMENT (MONDAY NIGHT/TUESDAY MORNING). THE T.A.S. LIQUIDATION IS WHY WE ARE HAVING A NEGATIVE COMEX OPEN INTEREST AND THIS IS COUPLED WITH HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 16+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, , 203 , ,205 , 207 209 AND TODAY’S 211 AND 212 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST FEW WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF MARCH .… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3335 EFP CONTRACTS WERE ISSUED: : /APRIL 3335 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3335 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2548 CONTRACTS IN THAT 3335 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL LOSS OF 787 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF $50.85 FOR MONDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A STRONG SIZED SIZED 1658 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER 4 WEEKS AGO, THE FED WAS EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH COMEX OPTIONS EXPIRY AND OTC LONDON OPTIONS EXPIRY.

THE RAIDS ON OPTIONS EXPIRY DOES TWO IMPORTANT THINGS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER 2024

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS.

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: MARCH (33.872 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE MARCH DELIVERY MONTH / FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH.

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

AND NOW MARCH:

STANDING FOR GOLD : 35.042 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527

= 256.607 TONNES.

MARCH: 35.042 TONNES

COMEX GOLD TRADING/MARCH CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $50.85/)/AND WERE UNSUCCESSFUL IN KNOCKING OFF APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OUR TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION MONDAY AS THEY WERE TRYING TO QUELL GOLD’S RISE AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING. LAST TUESDAY ENDED COMEX OPTIONXS EXPIRY. HOWEVER AS I EXPLAINED ON WEDNESDAY, WE HAVE THE MUCH BIGGER OTC.LONDON.OTC EXPIRY.THE BANKERS WERE UNSUCCESSFUL IN SLOWING THEIR DERIVATIVE LOSSES IN PRECIOUS METAL BETS WITH OPTIONS EXPIRY FOR BOTH COMEX AND LONDON OTC!!

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD)

EXCHANGE FOR RISK EXPLANATION/DECEMBER AND JANUARYTRADING

DECEMBER MONTH EXCHANGE FOR RISK!

88 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 6 FOR 14.6836 TONNES A NEW RECORD. THE COMEX IS TOTALLY SHATTERED TO PIECES.

EXCHANGE FOR RISK // JANUARY MONTH!!

LO AND BEHOLD, THE CROOKS ISSUED THEIR FIRST ISSUANCE A MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THEN TO MY HORROR, THEY ISSUED THEIR SECOND EXCHANGE FOR RISK ON JAN 8, TOTALLING 150 CONTRACTS FOR 15000 OZ OR .4665 TONNES. THIS TONNAGE WILL BE ADDED TO THE FIRST ISSUANCE. THUS TOTAL EXCHANGE FOR RISK ISSUANCE FOR OUR TWO EARLY JANUARY EX FOR RISK: 5.7533 TONNES. THEN MERCILESSLY THEY CONSUMMATED FOR THE THIRD TIME THIS MONTH 85 EXCHANGE FOR RISK LAST THURSDAY NIGHT (JAN 17) FOR 8500 OZ OR .2649 TONNES OF GOLD. THEN TO MY HORROR THEY ISSUED THEIR 4TH EXCHANGE FOR RISK THIS MONTH (JAN 22) FOR A MONSTER 5000 CONTRACTS OR 5,000,000 OZ.(15.562 TONNES).NOT TO BE UNDONE, THE CROOKS ISSUED THEIR FIFTH EXCHANGE FOR RISK LAST NIGHT FOR 500 CONTRACTS REPRESENTING 50,,000 OZ OR 1.555 TONNES OF GOLD. REMEMBER THAT THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON WHICH IS TOTALLY ASININE!! THUS FOR THE 5 EXCHANGE FOR RISK ISSUED THIS MONTH TOTALS 23.134 TONNES OF GOLD. THIS BRINGS US TO , JAN 25 WHERE THE CME ANNOUNCED ITS SIXTH MAJOR EXCHANGE FOR RISK ISSUANCE OF 6454 CONTRACTS FOR 645,400 OZ OR 20.074 TONNES OF GOLD. THIS IS THE HIGHEST EVER RECORDED ISSUANCE IN NUMBER OF EXCHANGE FOR RISK, AT 6, AND FOR NEW TOTALS FOR THE MONTH OF JANUARY: 43.208 TONNES!!! AND A NEW RECORD FOR ISSUANCE.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO, THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WILL NOW BE ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FOR FRIDAY FEB 28 ZERO EXCHANGE FOR RISK WAS ISSUED.

TOTAL INITIAL DELIVERIES MARCH GOLD TRADING

MARCH: 33.872 TONNES

WE HAVE GAINED A FAIR SIZED TOTAL OF 7.925 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH (31.753TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 50,300 OZ OR 1.5645 TONNES: NEW TOTAL STANDING 35/042 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $50.85

WE HAD 646 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 2548 CONTRACTS OR 254,800 0Z (7.925 TONNES)

confirmed volume MONDAY 227,387ontracts: fair///

//speculators have left the gold arena

END

MARCH

// THE MARCH 2025 GOLD CONTRACT

MARCH 3

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entry i) Out of Brinks enhanced: 129,400.950 oz 323 London good delivery bars at 400 oz each. . |

| Deposit to the Dealer Inventory in oz | 2 ENTRIES i) Asahi dealer 93,849.769 oz (2919 kilobars ii) Brinks dealer: 27,701.560 oz total dealer weight: 121,550.329 oz(3.78 tonnes) |

| Deposits to the Customer Inventory, in oz | 2 ENTRIES i) HSBC 32,151.000 oz (1000 kilobars) ii) Into Manfra: 16009.57 oz total customer weight: 48160.570 oz or 1.498 tonnes total weight dealer and customer: 5.278 tonnes |

| No of oz served (contracts) today | 681 notice(s) 68100 OZ 2.118 TONNES |

| No of oz to be served (notices) | 210 contracts 21000 OZ 0.653 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,056notices 1,105,600 oz 34.388 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 1

2 ENTRIES

i) Asahi dealer 93,849.769 oz (2919 kilobars

ii) Brinks dealer: 27,701.560 oz

total dealer weight: 121,550.329 oz(3.78 tonnes)

xxxxxxxxxxxxxxxx

we have 2 customer deposits:

2 ENTRIES

i) HSBC 32,151.000 oz (1000 kilobars)

ii) Into Manfra: 16009.57 oz

total customer weight: 48160.570 oz or 1.498 tonnes

total weight dealer and customer: 5.278 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 1

1 entry

i) Out of Brinks enhanced: 129,400.950 oz

323 London good delivery bars at 400 oz each.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxx

adjustments:1/comex is in chaos

a)customer to dealer

a) Loomis: 32,118.849 oz

thus basically what comes into eligible is transferred to dealer accounts and then out.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MARCH

THE FRONT MONTH OF MARCH HAD A LOSS OF 262 CONTRACTS TO STAND AT 897. WE HAD 644 CONTRACTS SERVED ON MONDAY SO WE GAINED A HUGE 503 CONTRACTS FOR 50,300 OZ (1.5645 TONNES AS A PHYSICAL GOLD QUEUE JUMP. THIS IS CENTRAL BANKS LOOKING FOR BADLY NEEDED GOLD.

APRIL HAD A LOSS OF 7646 CONTRACTS DOWNTO 345,696 CONTRACTS AS THIS MONTH BECOMES THE FRONT MONTH.

MAY GAINED 27 CONTRACTS UP TO 369.

We had 681 contracts filed for today representing 68,100oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 681 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 21 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MARCH /2025. contract month, we take the total number of notices filed so far for the month (11,056 X 100 oz ) to which we add the difference between the open interest for the front month of MARCH.(891 CONTRACTS) minus the number of notices served upon today (681 x 100 oz per contract) equals 1,126,600 OZ OR 35.042 TONNES

thus the INITIAL standings for gold for the MARCH contract month: No of notices filed so far (11056x 100 oz +we add the difference for front month of MARCH ( 891 OI} minus the number of notices served upon today (681 x 100 oz) which equals 1,126,600 OR 35.042 TONNES

TOTAL COMEX GOLD STANDING FOR MARCH.: 35.042 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND MARCH IS FOLLOWING SUIT..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,085,544.431 oz 64.86 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 39,454,463.716 .oz

TOTAL REGISTERED GOLD 19,279,754.414 or 599.68 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 20,174,709.302 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 17,194,210oz (REG GOLD- PLEDGED GOLD)= 534.812 tonnes //

END

SILVER/COMEX

FEB 28

INITIAL

// THE MARCH 2025 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2731.900 oz Loomis |

| Deposits to the Dealer Inventory | 2 entries i) Into ASAHI: 606,300.120 oz ii) Into Loomis; 966,980.200 oz total deposit dealer acct 1,573,280.320 oz |

| Deposits to the Customer Inventory | 4 entries i)Into Brinks 1244,710.400 oz ii) Into CNT 304,908.390 oz iii) Into HSBC 653,204.400 oz iv) Into JPMorgan: 1,118,117.600 oz total weight: 3,390,040.790 oz |

| No of oz served today (contracts) | 659 CONTRACT(S) (3.295MILLION OZ |

| No of oz to be served (notices) | 3137 contracts (15.6850 MILLION oz) |

| Total monthly oz silver served (contracts) | 11,774 Contracts (58.870 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 2 dealer deposit/

2 entries

i) Into ASAHI: 606,300.120 oz

ii) Into Loomis; 966,980.200 oz

total deposit dealer acct 1,573,280.320 oz

total dealer withdrawals: 0 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

4 entries

i)Into Brinks 1244,710.400 oz

ii) Into CNT 304,908.390 oz

iii) Into HSBC 653,204.400 oz

iv) Into JPMorgan: 1,118,117.600 oz

total weight: 3,390,040.790 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals 1

2731.900 oz

Loomis

xxx

ADJUSTMENTs 2 customer to dealer:

i) CNT 469.925.640 oz

ii) Manfra: 801,563.934 oz

JPMorgan has a total silver weight: 162.957million oz/408.808million or 39.74%

TOTAL REGISTERED SILVER: 139.198 MILLION OZ//.TOTAL REG + ELIGIBLE. 413.769Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF MARCH /2025 OI: 3796 OPEN INTEREST CONTRACTS FOR A LOSS OF 1204 CONTRACTS.WE HAD 996 CONTRACTS SERVED ON MONDAY SO WE LOST A HUMONGOUS 208 CONTRACTS OR AN ADDITIONAL 1.04 MILLION OZ UNDERWENT AN EFP TRANSFER TO LONDON LOOKING FOR METAL OVER THERE//NEW STANDING REDUCES TO 74.555 MILLION OZ. FOR THE SECOND DAY IN ROW, THE CROOKS COULD NOT FIND ANY SILVER OVER HERE!

APRIL SAW ANOTHER GAIN OF 27 CONTRACTS TO STAND AT 1453

MAY SAW A GAIN OF 463 CONTRACTS DOWN TO 114,054 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 659 or 3.2950 MILLION oz

CONFIRMED volume; ON MONDAY 59,789 small//

AND NOW ONTO MARCH:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 11,774 X5,000 oz = 58.830MILLION oz

to which we add the difference between the open interest for the front month of MAR (3796 AND the number of notices served upon today (659 )x (5000 oz)

Thus the standings for silver for the MARCH 2025 contract month: 11,856 Notices served so far) x 5000 oz + OI for the front month of MAR(3796) minus number of notices served upon today (659)x 5000 oz equals silver standing for the MARCH contract month equating to 74.555 MILLION OZ.

New total standing: INITIAL 74.555 million oz which is huge for this very active delivery month of March.

There are 139.198million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

FEB 13/ WITH GOLD UP 11.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 6.901 TONNES FROM THE GLD ///INVENTORY RESTS AT 866.50TONNES

FEB 12 WITH GOLD DOWN $3,40ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 10 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 7 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 6 WITH GOLD DOWN $18.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.14 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

FEB 5 WITH GOLD UP $27.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 863.05 TONNES

FEB 4 WITH GOLD UP $25.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.58 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.77 TONNES

JAN 31 WITH GOLD UP $4.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 30 WITH GOLD UP $40.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 865.34 TONNES

JAN 29 WITH GOLD DOWN $6.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.02 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 861.04 TONNES

JAN 28 WITH GOLD UP $23.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.16 TONNES OF GOLD OUT OF THE GLD //

JAN 27 WITH GOLD DOWN $36.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///

JAN 24 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 23 WITH GOLD DOWN $1.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 2.30 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 869.36 TONNES

JAN 22 WITH GOLD UP $15.15 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 7.46 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 871.66 TONNES

JAN 20 WITH GOLD UP $35.30 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 10.34 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 879.12 TONNES

GLD INVENTORY: 900.93 TONNES, TONIGHTS TOTAL

SILVER

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 12WITH SILVER UP $.01 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 8 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 10 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 7 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 6 WITH SILVER DOWN $0.17 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 12.383 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 430.39 MILLION OZ

FEB 5 WITH SILVER UP $0.45 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 3.285 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 442.773 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 3 WITH SILVER UP ONE CENT //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

JAN 31 WITH SILVER DOWN $0.19 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.369 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 448.881 MILLION OZ

jAN 30 WITH SILVER UP $0.76 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.003 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 451.249 MILLION OZ

jAN 29 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.639 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 453.252 MILLION OZ

jAN 28 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.821 MILLION OZ OUT OF THE SLV./. /

jAN 27 WITH SILVER DOWN $.61 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 24 WITH SILVER DOWN $.21 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 23 WITH SILVER DOWN $.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 4.738 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 459.035 MILLION OZ

JAN 22 WITH SILVER UP $.08 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 0.721 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 464.043 MILLION OZ

JAN 20 WITH SILVER DOWN $.09 //NO CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.568 MILLION OZ FROM THE SLV./. //INVENTORY AT SLV RESTS AT 463.315 MILLION OZ

CLOSING INVENTORY 436.493MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

Alasdair Macleod..

Bear squeeze resumes

Sharp rises in gold and silver in the last two trading sessions are evidence of the bear squeeze on the shorts being resumed.

| Alasdair MacleodMar 4∙Paid |

The sudden recovery in gold and silver is not on the back of bullish demand for paper contracts. How can we describe what’s going on?

Trading volumes on Comex are not spectacular despite price rises for gold and silver. Gold has risen over $80 since Friday afternoon, and Open Interest has fallen below 490,000 contracts. And silver’s OI similarly fell back by over 12,000 contracts on Friday. These declines are down to high levels of stand-for-deliveries in both metals.

This has rarely been mentioned in any commentary that I’ve seen. But the pace of these stand-for-deliveries is remarkable. As well as the realisation that for whatever reason gold and silver are clearly heading much higher, the fact that buyers are taking futures positions to access scarce bullion must be scarry for any bullion bank trading desk. No wonder there’s a scramble to close their shorts down.

So far, 333.3 tonnes of gold have been stood for delivery since 1 January, and 2,689.7 tonnes of silver. The silver chart looks good as well.

Having again tested the 55-day MA (currently at 30.81) its base for an attack on the $35 level is in place.

And gold appears to have a runaway momentum, taking it to over $3k in a matter of days…

The next headache for the shorts is that the momentum traders have yet to join the party. It’s hard to imagine that they won’t, particularly as the dollar’s recent strength may have come to an end. Its TWI is next.

If the hedge funds, who are said to be already running short positions in equities, take the view that the credit bubble is imploding, then there will be a lemming-like rush into gold and silver as they sell dollars/buy PMs

Just saying…

3 CHRIS POWELL AND GATA DISPATCHES

Chris Powell…

4 ANDREW MAGUIRE/LIVE FROM THE VAULT NO 212//ANDREW MAGUIRE INTERVIEWING DR DANIEL LACALLE

Kinesis.money/live-from-the-vault/trump-expose-feds-gold-coverup/

Episode 212

Posted 28th February 2025

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY//EGGS

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING TUESDAY MORNING MONDAY NIGHT

SHANGHAI CLOSED UP 7.29 PTS OR 0.22%

//Hang Seng CLOSED DOWN 64.50 PTS OR 0.28%

// Nikkei CLOSED DOWN 454.29OR 1,20%//Australia’s all ordinaries CLOSED DOWN .68%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2572 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2613/ Oil UP TO 67/12 dollars per barrel for WTI and BRENT UP TO 70.37 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.2572

OFFSHORE YUAN: DOWN TO 7.2613

SHANGHAI CLOSED CLOSED UP 7.29 PTS OR 0.22%

HANG SENG CLOSED CLOSED DOWN 64.50 PTS OR 0.28%

2. Nikkei closed DOWN 454.29OR 1.20%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 105.88// EURO RISES TO 1.0552 UP 67 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: RISES TO. +1.406//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.27…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4690/Italian 10 Yr bond yield DOWN to 3.534 SPAIN 10 YR BOND YIELD DOWN TO 3.139

3i Greek 10 year bond yield DOWN TO 3.291

3j Gold at $2926.00 Silver at: 31.87 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 72 /100 roubles/dollar; ROUBLE AT 88.98

3m oil into the 67 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.27 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.406 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8874 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9364well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.144 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.460 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.906 DOWN 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 36.46…

10 YR UK BOND YIELD: 4.5605 UP 1 PTS

10 YR CANADA BOND YIELD: 2.852 UP 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.540 UP 1 PTS.

2a New York OPENING REPORT

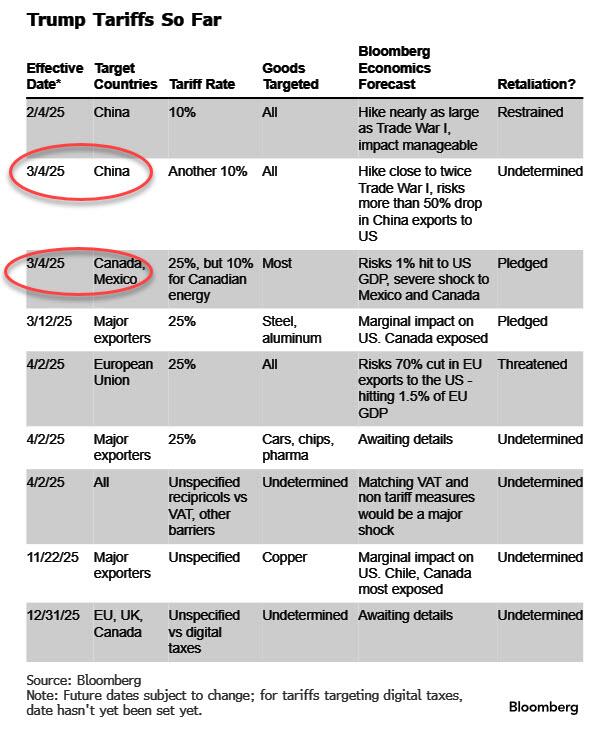

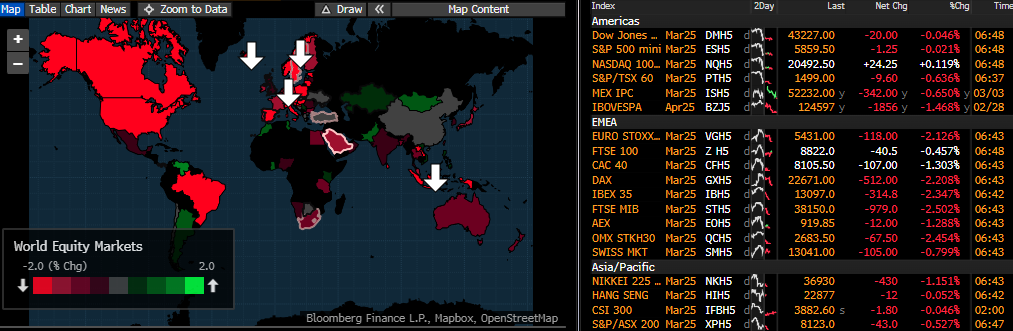

Futures Tumble As Trump Tariffs Kick In

Tuesday, Mar 04, 2025 – 08:08 AM

Futures are lower, tracking European and Asian markets, with the dollar plunging on mounting recession fears, as the Trump trade war officially started at midnight, although according to JPMorgan it could be even worse and the “downward reaction is muted given the significant, expected impact on the economy and earnings expectations.” At the same time, Canada, China, and Mexico are rolling out their retaliatory measures. As of 8:00am ET, S&P futures are down 0.5%, and near session lows, while Nasdaq futures drop 0.6%, with Mag7 names sliding premarket and NVDA tumbling another 2.4% after plunging 8.7% on Monday. Investors will also be waiting to see what Trump says in his State of the Union speech tonight (some see it as a final hope for an off-ramp). Bond yields are mixed as the curve twists steeper and USD plunges amid rising fears the tariffs will accelerate a recession. Commodities are weaker with precious outperforming while energy stocks underperform as oil prices fall further after OPEC+ announced plans to revive halted production. WTI declines 0.8% to $67.80 a barrel, the lowest since December. There are no major macro data releases today and the Fed’s Williams speaks ~2.20pm EST; Trump’s State of the Union address is at 9:00pm ET.

In premarket trading, Tesla is leading premarket losses among the Magnificent Seven stocks on Tuesday. Meanwhile, shares in Nvidia whipsaw a day after a selloff in the chipmaker wiped out almost $265 billion in market value, and extend their losses down another 2%. Walgreens Boots Alliance shares rise 6.1% after Bloomberg reported that Sycamore Partners is nearing an acquisition of the drugstore operator. Here are some other notable premarket movers:

- Okta (OKTA US) shares jump 16% after the infrastructure software company reported fourth-quarter results that beat expectations and gave an outlook that is above the analyst consensus.

- On Holding (ONON US) shares climb 11% after the Swiss sneaker maker reported fourth-quarter sales and gross margin that topped Wall Street expectations.

- Illumina (ILMN US) shares slip 3.5% after China banned the firm from selling genetic sequencing products in the country as part of a wave of retaliatory measures against fresh US tariffs on all Chinese goods.

- Viant Technology (DSP US) shares slide 10% after the digital advertising company reported fourth-quarter adjusted diluted earnings per share that missed estimates.

At midnight, a raft of new tariffs and countertariffs kicked in (full break down in the subsequent post), which mark Trump’s biggest push to remake global trade, and investors will be watching his address to Congress Tuesday for hints on future steps. Canada announced a sweeping package of tariffs in response and China retaliated by imposing tariffs as high as 15% on some US exports.

There’s more: Trump also said Monday that the US would impose tariffs on “external” agricultural products starting on April 2, adding another layer of threats to impose trade barriers on imported goods. He didn’t detail which products would be affected, or if there would be any exceptions. Trump also ordered a pause to all military aid to Ukraine, turning up the heat on Volodymyr Zelenskiy just days after an Oval Office blowup with the Ukrainian president left the support of his country’s most important ally in doubt.

“We need to know exactly what the US plan is towards European tariffs,” said Salman Ahmed, global head of macro and strategic asset allocation at Fidelity International. “It’s likely to be different from Canadian and Mexican tariffs, because the interrelationships are different. It’s a big unknown for European equity outperformance to continue.”

Stocks in Europe retreated on concern the region could be next to face US tariffs after President Donald Trump imposed levies on Mexico, Canada and China. Europe’s Stoxx 600 index slumped 1.2%, weighed down by automakers and energy stocks, after closing at a record in the previous session. European defense stocks bucked the broader slump amid expectations of increased military spending in the region. A basket of European defense stocks hit a record high as Thales SA jumped 8% after its results beat expectations, while Hensoldt AG rallied as much as 18%. Here are some of the biggest movers on Tuesday:

- Lindt & Spruengli shares gain as much as 6.3% after the chocolate maker posted strong results and “impressive” free cash flow.

- A European defense index hits a record high, supported by Thales’s post-results jump. Hensoldt also rallied on news the company will join the Stoxx Europe 600 Index.

- Eutelsat shares more than triple in two days, their biggest back-to-back gains ever, on optimism that European leaders’ pledge to boost military spending will aid the satellite operator.

- Inchcape shares jump as much as 9.7% after the automotive retailer and distributor announced a bigger share buyback and outlined new mid-term goals that are being welcomed by markets.

- European stocks exposed to the escalating global trade war slump, including automakers, Spanish banks, metals makers, beverage stocks and freight shippers. Continental shares fall as much as 9.3% after full-year results in which analysts point out a revenue miss. Bernstein cites a challenging 2025 outlook, which includes no tariff impact.

- European energy companies’ shares drop as oil slides on OPEC+’s plans to increase production, as well as concerns around the Trump administration’s trade tariffs.

- Forbo shares drop as much as 12% after the Swiss linoleum maker’s FY24 results fell short of expectations, according to Baader, which added the FY25E outlook suggests another challenging year.

- Fresenius Medical Care shares drop as much as 8.4%, the most since July, after a share offering by Fresenius SE was priced at a discount.

- Ashtead shares drop as much as 4.5% after the equipment rental giant posted a slowdown in US rental growth in the third quarter, according to Jefferies.

- Greggs shares fall as much as 14% as weaker like-for-like sales growth at the start of this year offset a slight beat on 2024 pretax profit.

In FX, the Bloomberg Dollar Spot Index fell for a second day. Haven assets outperform with the Swiss franc at the top of the G-10 FX leaderboard, rising 0.6% against the greenback. The yen is not far behind with a 0.5% gain. The euro rose as much as 0.3% to its highest level since Feb. 26 as the European Union proposed extending €150 billion ($158 billion) in loans to boost defense spending. Elsewhere, the Mexican peso weakened 0.9% against the greenback, while the Canadian dollar was slightly stronger after retreating for seven straight sessions.

In rates, treasuries are mixed with the curve steeper as US trading day begins, off session lows reached during Asia session as US tariffs on imports from Canada, Mexico and China drew reprisals. US front-end yields are richer by nearly 5bp near session lows with long-end yields slightly higher on the day, steepening 2s10 and 5s30s curves by ~4bp; 10-year around 4.14% is lower by 1bp, trailing yield declines of 2bp and 5bp for German and UK counterparts. Traders fully priced in three 25bp Fed rate cuts this year. US 5s30s spread touched widest level since Oct. 4, paced by German 5s30s reaching steepest level in more than two years amid steep declines for European stocks. Gilts lead a rally in European government bonds, with UK 10-year yields falling 5 bps to 4.51%.

In commodities, spot gold climbs $30 to around $2,920/oz. Bitcoin falls 2% to below $84,000.

Today’s economic data calendar is blank, while Fed speaker slate includes New York Fed’s Williams at 2:20pm

Market Snapshot

- S&P 500 futures up 0.1% to 5,868.00

- STOXX Europe 600 down 0.9% to 558.13

- MXAP down 0.2% to 184.38

- MXAPJ down 0.3% to 575.62

- Nikkei down 1.2% to 37,331.18

- Topix down 0.7% to 2,710.18

- Hang Seng Index down 0.3% to 22,941.77

- Shanghai Composite up 0.2% to 3,324.21

- Sensex down 0.1% to 73,008.36

- Australia S&P/ASX 200 down 0.6% to 8,198.06

- Kospi down 0.2% to 2,528.92

- German 10Y yield little changed at 2.45%

- Euro up 0.3% to $1.0520

- Brent Futures down 1.4% to $70.59/bbl

- Gold spot up 1.0% to $2,920.89

- US Dollar Index down 0.49% to 106.23

Top Overnight News

- Trump ordered a pause on all military aid to Ukraine until he determines there’s a good-faith commitment to peace, a defense official said. The US will engage with Volodymyr Zelenskiy if he calls with a “serious proposal” to end the war, JD Vance told Fox. BBG

- Global government borrowing is expected to hit a record $12.3T this year, with the aggregate debt stock climbing to nearly $77T. FT

- The United States is drawing up a plan to potentially give Russia sanctions relief as President Donald Trump seeks to restore ties with Moscow and stop the war in Ukraine. RTRS

- Fed’s Musalem (2025 voter) said the outlook is for continued solid economic growth, but recent consumer and housing data pose some downside risk. Musalem added that restrictive monetary policy is still needed to ensure inflation returns to the 2% target, while a patient approach to policy will help achieve the Fed’s goals and sustain economic expansion.

- US Education Secretary McMahon said that President Trump has assigned them the ‘final mission’ to reduce bureaucratic inefficiencies within the Department of Education.

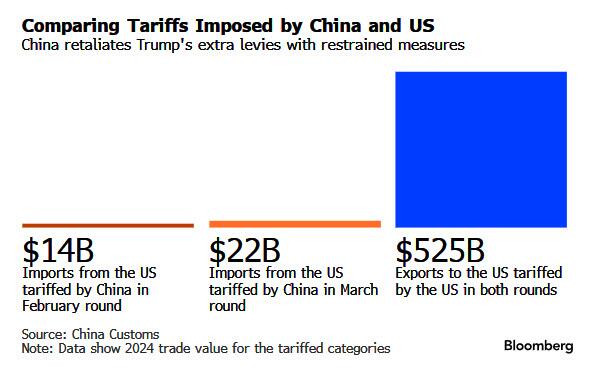

- China retaliates against Trump’s tariffs, imposing 15% duties on imports of US poultry, wheat, corn, and cotton, and 10% on soybeans, pork, beef, fruit, vegetables, and dairy, while 15 US firms were added to Beijing’s export control list and another 10 were put on the “unreliable entity list” (Illumina has been barred from exporting tools to China). SCMP

- Canada’s retaliatory tariff plan includes 25% levies on about C$30 billion ($20.8 billion) worth of goods from the US, with a second round on C$125 billion of products in three weeks. Mexican President Claudia Sheinbaum is expected to spell out her plan today.

- China plans to issue guidance encouraging domestic firms to use chips based on the RISC-V open-source standard instead of proprietary Western standards sold by the likes of ARM, AMD, and INTC. RTRS

- The RBA said last month’s rate reduction doesn’t commit the board to further easing, according to minutes of the meeting. CBA chief Matt Comyn said he expects a slower and shallower rate-cut cycle. BBG

- Leaders of Arab countries are set to meet in Cairo today to endorse a Gaza reconstruction plan to counter Trump’s proposals. BBG

Tariffs

- White House said President Trump proceeded with tariffs on imports from Canada and Mexico, while reports also noted that the extra 10% duty on Chinese goods took effect as the Tuesday deadline passed with no changes to tariff orders.

- US President Trump said on Monday that reciprocal tariffs start on April 2nd and tariffs on Canada and Mexico are to start on Tuesday, while also commented there is no room left for a deal on tariffs on Mexico and Canada, while he reiterated the plan to double the China tariff to 20% from 10%. Furthermore, Trump said will penalise countries weakening currencies with tariffs and mentioned China when talking about weak currencies and doesn’t think China will retaliate too much, while the White House said President Trump signed an order to tariff China at 20%.

- US President Trump posted on Truth “To the Great Farmers of the United States: Get ready to start making a lot of agricultural product to be sold INSIDE of the United States. Tariffs will go on external product on April 2nd. Have fun!”

- Canada said it will impose retaliatory tariffs on US imports from Tuesday if US tariffs go into effect and will start with 25% tariffs on US imports worth CAD 30bln from Tuesday, while it will impose tariffs on an additional CAD 125bln worth of US imports in 21 days. Furthermore, it said tariffs will remain in place until the US trade action is withdrawn and it is in active discussions with provinces and territories to pursue several non-tariff measures if US tariffs do not cease.

- China announced additional tariffs on US goods as retaliation for March 4th tariffs in which it is to impose additional tariffs of up to 15% on some US goods from March 10th, while it announced to impose tariffs of 15% on US chicken, wheat, corn, and cotton, as well as tariffs of 10% on US soybeans, sorghum, pork, beef, aquatic products, fruits, vegetables, and dairy products. China also added 15 US entities to the export control list and added 10 US firms to the unreliable entity list and banned Illumina Inc from exporting gene sequencing machines to China from March 4.

- China’s MOFCOM earlier stated that China will take countermeasures to firmly safeguard its rights and interests in response to US tariffs, while it urged the US to immediately withdraw its unilateral tariff measures, calling them unreasonable, groundless, harmful to others, and self-serving. Furthermore, it hopes the US will return to the right track of resolving differences through dialogue on an equal footing as soon as possible.

A more detailed look at global markets courtesy of Newsquawk