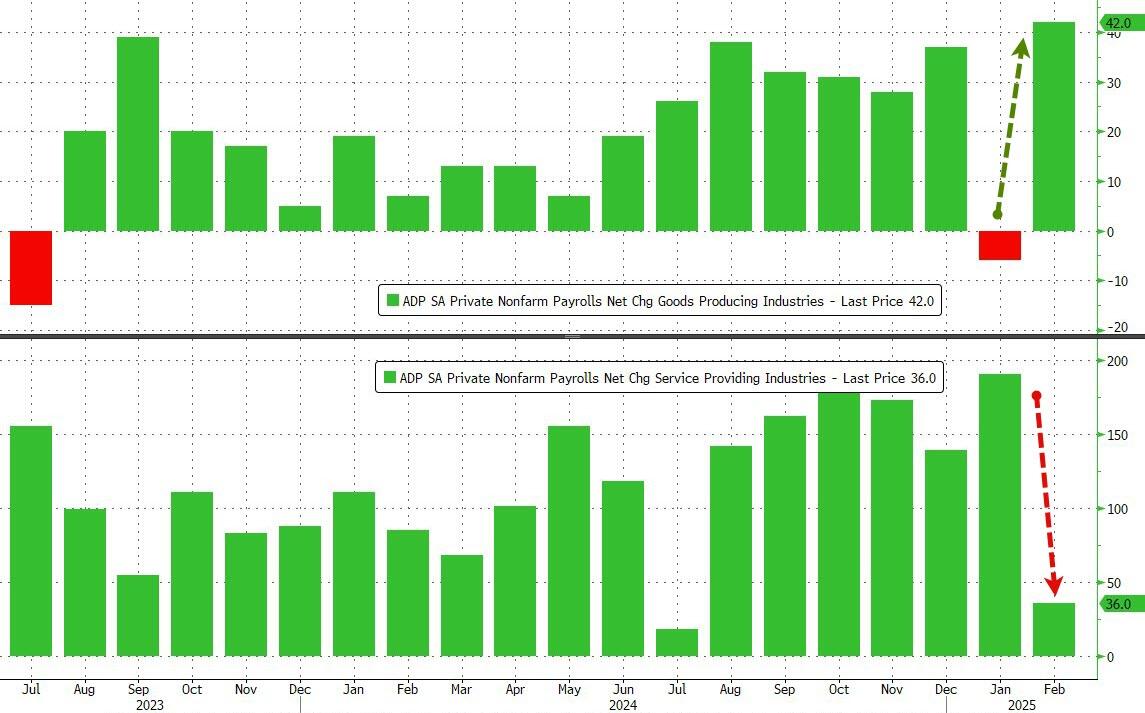

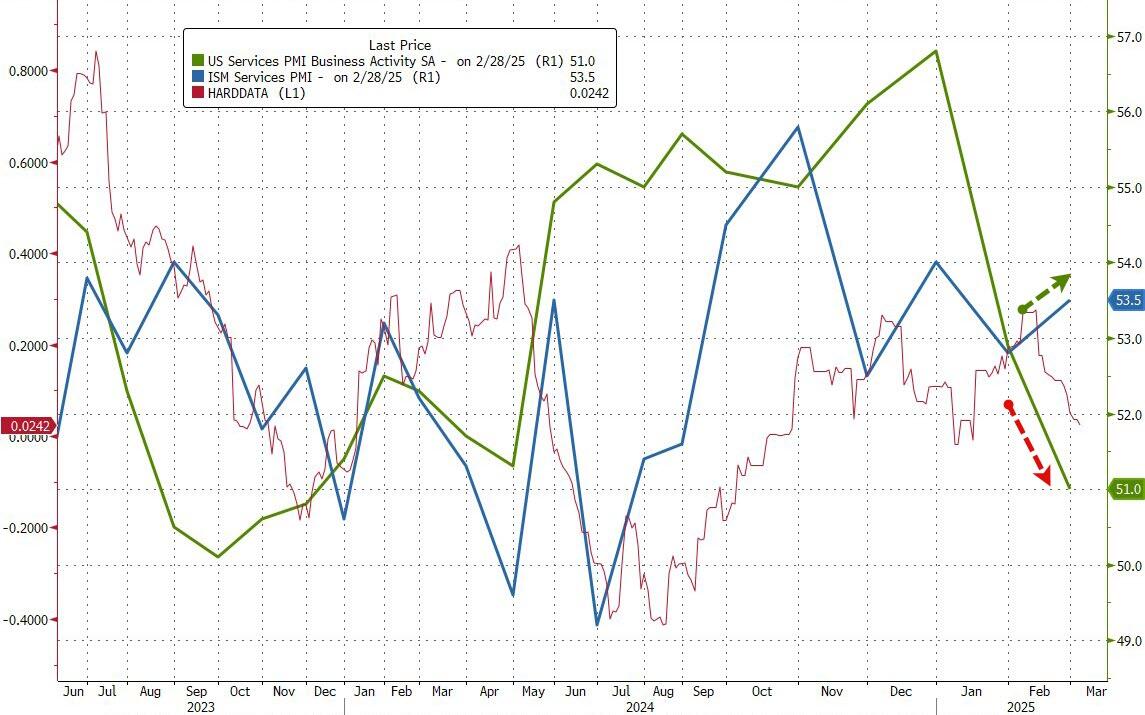

MARCH 5/GOLD CLOSED UP $6.75 TO $2916.55//SILVER HAD A STELLAR DAY UP 82 CENTS TO $32.59//PLATINUM CLOSED DOWN $0.75 TO $964.50//PALLADIUM CLOSED DOWN $10.30 TO $940.55//JAPAN’S DEMOGRAPHICS CONTINUE TO DETERIORATE AS JAPAN INC HEADING FOR BANKRUPTCY//CHAOS IN GERMANY AS AUTHORITIES WILL GO ON A SPENDING BINGE OFFSETTING THEIR MORIBUND ECONOMY//ISRAEL VS HAMAS; ISRAEL REJECTS EGYPT’S PROPOSAL : EXPECT WAR TO RESUME IN A FEW DAYS//COVID UPDATES/VACCINE INJURY REPORT/DR PAUL ALEXANDER/SLAY NEWS ETC//USA NEWS; ADP PRIVATE WAGES SHOWS HUGE DOWNFALL//USA SERVICE SECTOR SHOWING GROWTH//SWAMP STORIES FOR YOU TONIGHT///

072 C GOLDMAN 4 132 C SG AMERICAS 1 190 H BMO CAPITAL 33 323 C HSBC 10 363 H WELLS FARGO SEC 35 624 H BOFA SECURITIES 21 657 C MORGAN STANLEY 8 661 C JP MORGAN 1 686 C STONEX FINANCIA 33 8 690 C ABN AMRO 21 1 709 C BARCLAYS 1 737 C ADVANTAGE 4 905 C ADM 1

TOTAL: 91 91 MONTH TO DATE: 11,147

JPMORGAN STOPS 1/91 CONTRACTS

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2024. CONTRACT: 91 NOTICES FOR 9100 OZ 0.2830 TONNES

total notices so far: 11,147 contracts for 1,114700 Oz (34.672 tonnes)

FOR MARCH

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 227 NOTICE(S) FILED FOR 1.135 MILLION OZ/

total number of notices filed so far this month : 12.001 for 60.005 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $6.75 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.87TONNES

INVENTORY RESTS AT 901.80 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP 82 CENTS AT THE SLV: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 436.501 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED22 CONTRACTS TO 145,935 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZEDLOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL GAIN OF $0,09 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. WE HAD A FAIR GAIN OF 178 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR SMALL LOSS IN PRICE//TUESDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON TUESDAY COMEX TRADING / AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON TUESDAY WITH SILVER’S GAIN IN PRICE. WE HAD A HUGE T.A.S. LIQUIDATION TUESDAY COUPLED WITH ANOTHER STRONG T.A.S. ISSUANCE OF 366 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.00 DOLLAR MARK. WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND 95 CENTS AND A LEASE RATE OF 6%. WE HAD A FAIR 200 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 366 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN WEDNESDAY.S TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A FAIR SIZED 290 CONTRACTS ON OUR TWO EXCHANGES WITH OUR SMALL GAIN IN PRICE. WE HAD HUGE TAS LIQUIDATION THROUGHOUT TUESDAY’S COMEX TRADING SESSION WHICH ACCOUNTS FOR THE SMALLISH GAIN IN OI ON OUR TWO EXCHANGES.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT/WEDNESDAY MORNING: A STRONG 366 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.09 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A FAIR GAIN IN OUR TWO EXCHANGES OF 178 CONTRACTS WE HAD A MASSIVE LIQUIDATION OF T.A.S. CONTRACTS TRYING TO CONTAIN SILVER’S PRICE RISE AND THAT ACCOUNTS OF MOST OF OUR OPEN INTEREST FALL.

WE HAD A 200 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 78.753 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0.3500 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON

INITIAL STANDING FOR MARCH REDUCES TO 74.205 MILLION OZ

WE HAD:

/ SMALL COMEX OI LOSS+// A FAIR SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 366 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 112 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR

TOTAL CONTRACTS for 3 DAYS, total 1030ontracts: OR 5.150 MILLION OZ (343 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 5.150 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 5.15 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 22 CONTRACTS WITH OUR GAIN IN PRICE OF 9 CENTS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A 200 CONTRACT EFP ISSUANCE CONTRACTS: 200 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH OF 78.455 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 0.350 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON//NEW STANDING REDUCES TO 74.205 MILLION OZ

WE HAVE 1). A FAIR SIZED GAIN OF 178 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR GAIN IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 366 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//MONSTER FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION. HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON MONDAY WITH THE HUGE GAIN IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE TUESDAY NIGHT (366 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 227 NOTICE(S) FILED TODAY FOR 1.135 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 428 OI CONTRACTS TO 490,015 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A STRONG SIZED 745 CONTRACTS//

WE HAD A SMALL SIZED INCREASE IN COMEX OI (428 CONTRACTS) OCCURRED WITH OUR GAIN OF $19.05 IN PRICE TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 31.757 TONNES FOLLOWED BY TODAY’S HUGE 84,900 OZ QUEUE JUMP (2.6407 TONNES)//NEW STANDING ADVANCES TO 37.677 TONNES

/NEW STANDING FOR MARCH; 37.677 TONNES

/ ALL OF THIS HAPPENED WITH OUR $19.05 GAIN IN PRICE WITH RESPECT TO TUESDAY’S COMEX ///. WE HAD A FAIR SIZED GAIN OF 2008 OI CONTRACTS (6.245 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE FRONT MARCH CONTRACT MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1580 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 489,270

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2008 CONTRACTS WITH 428 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 1580 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2008 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED AND CRIMINAL 2218 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1580 CONTRACTS) ACCOMPANYING THE SMALL SIZED INCREASE IN COMEX OI OF 428 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2753 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH 31.757 TONNES FOLLOWED BY TODAY’S HUGE 2.6404 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 37.677 TONNES

NEW STANDING FOR MARCH ADVANCES TO:

37.677 TONNES

//NEW STANDING MARCH: 37.677 TONNES

.

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE TUESDAY WITH NO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WITH OUR1) $19.05 PRICE GAIN WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A FAIR GAIN OF 2753 CONTRACTS ON OUR TWO EXCHANGES ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN MARCH

4) SMALL SIZED COMEX OPEN INTEREST INCREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 2218 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH :

TOTAL EFP CONTRACTS ISSUED: 7579 CONTRACTS OF 757,900 OZ OR 23.57 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 2,526 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN3 TRADING DAY(S) IN TONNES 23.57 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 23.57 DIVIDED BY 3550 x 100% TONNES = 0.664% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 23.57 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A SMALL SIZED 22 CONTRACTS OI TO 145,935 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 200 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 22 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A FAIR SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 178 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.890 MILLION OZ OCCURRED WITH OUR $0.09 GAIN IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS WEDNESDAY MORNING//TUESDAY NIGHT

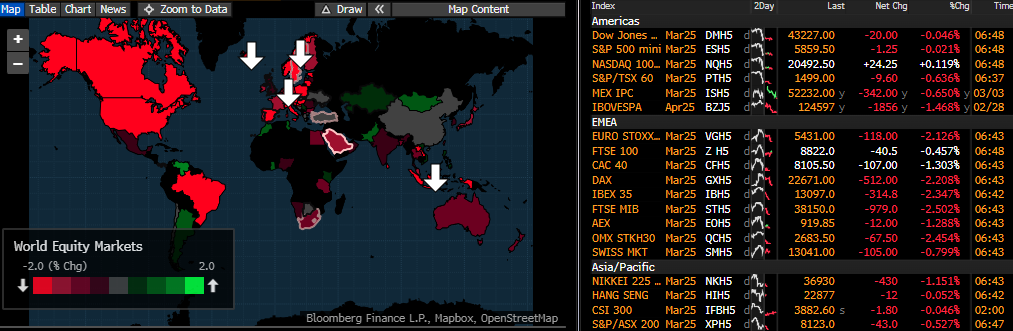

SHANGHAI CLOSED UP 17.76 PTS OR 0.53%

//Hang Seng CLOSED UP 652.44 PTS OR 2.84%

// Nikkei CLOSED UP 87.06 OR 0.23%//Australia’s all ordinaries CLOSED DOWN .69%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2635 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2616/ Oil UP TO 67.12 dollars per barrel for WTI and BRENT DOWN TO 70.16 Stocks in Europe OPENED ALL GREEN

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED428 CONTRACTS TO 489,270 DESPITE OUR STRONG GAIN IN PRICE OF $19.05 WITH RESPECT TO TUESDAY’S TRADING/. WE LOST ZERO NET LONGS WITH THAT PRICE GAIN FOR GOLD. BUT AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1580 ).

THE CME ANNOUNCED TUESDAY NIGHT, ZERO EXCHANGE FOR RISK CONTRACTS FOR NIL OZ OR 0 TONNES.

IN FEBRUARY: WE HAD FIVE EXCHANGE FOR RISKS TOTALLING 18.4527 TONNES!. THE RECIPIENT OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY.

THUS IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 2008 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW CLIMBED TO 10% AS GOLD IN LONDON IS NOW EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY TODAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION// TUESDAY // THEY ISSUED A STRONG 2218 CONTRACT ANNOUNCEMENT (TUESDAY NIGHT/WEDNESDAY MORNING). THE T.A.S. LIQUIDATION IS WHY WE ARE HAVING A LOWER COMEX OPEN INTEREST GAIN BUT THIS IS COUPLED WITH HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 16+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, , 203 , ,205 , 207 209 AND TODAY’S 211 AND 212 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST FEW WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF MARCH .… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 1580 EFP CONTRACTS WERE ISSUED: : /APRIL 1580 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1580 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2008 CONTRACTS IN THAT 1580 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL GAIN OF 428 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $19.05 FOR TUESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/MONDAY MORNING WAS A FAIR SIZED SIZED 1580 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER 4 WEEKS AGO, THE FED WAS EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH COMEX OPTIONS EXPIRY AND OTC LONDON OPTIONS EXPIRY.

THE RAIDS ON OPTIONS EXPIRY DOES TWO IMPORTANT THINGS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER 2024

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS.

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: MARCH (37.677 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE MARCH DELIVERY MONTH / FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH.

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

AND NOW MARCH:

STANDING FOR GOLD : 37.677 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527

= 256.607 TONNES.

MARCH: 37.677 TONNES

COMEX GOLD TRADING/MARCH CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $19.05/)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OUR TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION TUESDAY AS THEY WERE TRYING TO QUELL GOLD’S RISE AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING. LAST TUESDAY ENDED COMEX OPTIONXS EXPIRY. HOWEVER AS I EXPLAINED ON WEDNESDAY, WE HAVE THE MUCH BIGGER OTC.LONDON.OTC EXPIRY.THE BANKERS WERE UNSUCCESSFUL IN SLOWING THEIR DERIVATIVE LOSSES IN PRECIOUS METAL BETS WITH OPTIONS EXPIRY FOR BOTH COMEX AND LONDON OTC!!

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD)

EXCHANGE FOR RISK EXPLANATION/DECEMBER AND JANUARYTRADING

DECEMBER MONTH EXCHANGE FOR RISK!

88 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 6 FOR 14.6836 TONNES A NEW RECORD. THE COMEX IS TOTALLY SHATTERED TO PIECES.

EXCHANGE FOR RISK // JANUARY MONTH!!

LO AND BEHOLD, THE CROOKS ISSUED THEIR FIRST ISSUANCE A MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THEN TO MY HORROR, THEY ISSUED THEIR SECOND EXCHANGE FOR RISK ON JAN 8, TOTALLING 150 CONTRACTS FOR 15000 OZ OR .4665 TONNES. THIS TONNAGE WILL BE ADDED TO THE FIRST ISSUANCE. THUS TOTAL EXCHANGE FOR RISK ISSUANCE FOR OUR TWO EARLY JANUARY EX FOR RISK: 5.7533 TONNES. THEN MERCILESSLY THEY CONSUMMATED FOR THE THIRD TIME THIS MONTH 85 EXCHANGE FOR RISK LAST THURSDAY NIGHT (JAN 17) FOR 8500 OZ OR .2649 TONNES OF GOLD. THEN TO MY HORROR THEY ISSUED THEIR 4TH EXCHANGE FOR RISK THIS MONTH (JAN 22) FOR A MONSTER 5000 CONTRACTS OR 5,000,000 OZ.(15.562 TONNES).NOT TO BE UNDONE, THE CROOKS ISSUED THEIR FIFTH EXCHANGE FOR RISK LAST NIGHT FOR 500 CONTRACTS REPRESENTING 50,,000 OZ OR 1.555 TONNES OF GOLD. REMEMBER THAT THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON WHICH IS TOTALLY ASININE!! THUS FOR THE 5 EXCHANGE FOR RISK ISSUED THIS MONTH TOTALS 23.134 TONNES OF GOLD. THIS BRINGS US TO , JAN 25 WHERE THE CME ANNOUNCED ITS SIXTH MAJOR EXCHANGE FOR RISK ISSUANCE OF 6454 CONTRACTS FOR 645,400 OZ OR 20.074 TONNES OF GOLD. THIS IS THE HIGHEST EVER RECORDED ISSUANCE IN NUMBER OF EXCHANGE FOR RISK, AT 6, AND FOR NEW TOTALS FOR THE MONTH OF JANUARY: 43.208 TONNES!!! AND A NEW RECORD FOR ISSUANCE.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO, THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WILL NOW BE ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FOR FRIDAY FEB 28 ZERO EXCHANGE FOR RISK WAS ISSUED.

TOTAL INITIAL DELIVERIES MARCH GOLD TRADING

MARCH: 35.040 TONNES

WE HAVE GAINED A FAIR SIZED TOTAL OF 6.245 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH (31.753TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 84,900 OZ OR 2.6407 TONNES: NEW TOTAL STANDING 37.677 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $50.85

WE HAD 745 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 2008 CONTRACTS OR 200,800 0Z (6.245 TONNES)

i) Out of Brinks enhanced: 191,254.945 oz 478 London good delivery bars at 400 oz each. ii) Loomis 32.151 (one kilobar)

iii) 25,719.04 oz Brinks 800 kilobars

total weight 217,006.156 oz 6.74 tonnes

.

Deposit to the Dealer Inventory in oz

2 ENTRIES

i) Asahi dealer 116,129.412 oz (3612 kilobars ii) Manfra dealer: 16,009.57 oz (498 kilobars)

total dealer weight: 132,138.982 oz(4.110 tonnes)

Deposits to the Customer Inventory, in oz

4 ENTRIES

i) Brinks 179,457.773 oz ii) Into HSBC: 27,328.35 oz (850 kilobars_) iii) JPMorgan 32,118.849 oz (999 kilobars) iv) Loomis 64,269.849 oz (20 kilobars) total weight: 303,174.821 oz 3.204 tonnes

total 7.314 tonnes

No of oz served (contracts) today

91 notice(s) 9100 OZ 0.2830 TONNES

No of oz to be served (notices)

966 contracts 96600 OZ 0.653 TONNES

Total monthly oz gold served (contracts) so far this month

11,147notices 1,114700 oz 34.672 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 2

2 ENTRIES

i) Asahi dealer 116,129.412 oz (3612 kilobars ii) Manfra dealer: 16,009.57 oz (498 kilobars)

total dealer weight: 132,138.982 oz(4.110 tonnes)

xxxxxxxxxxxxxxxx

we have 4 customer deposits:

4 ENTRIES

i) Brinks 179,457.773 oz ii) Into HSBC: 27,328.35 oz (850 kilobars_) iii) JPMorgan 32,118.849 oz (999 kilobars) iv) Loomis 64,269.849 oz (20 kilobars) total weight: 303,174.821 oz 3.204 tonnes

total 7.314 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 1

i) Out of Brinks enhanced: 191,254.945 oz 478 London good delivery bars at 400 oz each. ii) Loomis 32.151 (one kilobar)

iii) 25,719.04 oz Brinks 800 kilobars

total weight 217,006.156 oz 6.74 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxx

adjustments:1/comex is in chaos

a) dealer to customer

a) Loomis: 96.457 oz

thus basically what comes into eligible is transferred to dealer accounts and then out.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MARCH

THE FRONT MONTH OF MARCH HAD A GAIN OF 168 CONTRACTS TO STAND AT 1057. WE HAD 681 CONTRACTS SERVED ON TUESDAY SO WE GAINED A HUGE 849 CONTRACTS FOR 84900 OZ (2.6407 TONNES AS A PHYSICAL GOLD QUEUE JUMP. THIS IS CENTRAL BANKS LOOKING FOR BADLY NEEDED GOLD.

APRIL HAD A LOSS OF 5787 CONTRACTS DOWNTO 339,908 CONTRACTS AS THIS MONTH BECOMES THE FRONT MONTH.

MAY LOST 68 CONTRACTS UP TO 251.

We had 91 contracts filed for today representing 9,100oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 91 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MARCH /2025. contract month, we take the total number of notices filed so far for the month (11,147 X 100 oz ) to which we add the difference between the open interest for the front month of MARCH.(1057 CONTRACTS) minus the number of notices served upon today (91 x 100 oz per contract) equals 1,211,300 OZ OR 37.677 TONNES

thus the INITIAL standings for gold for the MARCH contract month: No of notices filed so far (11,147x 100 oz +we add the difference for front month of MARCH ( 1057 OI} minus the number of notices served upon today (91 x 100 oz) which equals 1,211,300 OR 37.677 TONNES

TOTAL COMEX GOLD STANDING FOR MARCH.: 37.677 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND MARCH IS FOLLOWING SUIT..

JPMorgan has a total silver weight: 165.387million oz/416.815million or 39.58%

TOTAL REGISTERED SILVER: 139.808 MILLION OZ//.TOTAL REG + ELIGIBLE. 416.815Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF MARCH /2025 OI: 3067 OPEN INTEREST CONTRACTS FOR A LOSS OF 729 CONTRACTS.WE HAD 659 CONTRACTS SERVED ON TUESDAY SO WE LOST 70 CONTRACTS OR 0.350 MILLION COMEX OZ STANDING UNDERWENT AN EFP TRANSFER TO LONDON LOOKING FOR METAL OVER THERE//NEW STANDING REDUCES TO 74.205 MILLION OZ. FOR THE THIRD DAY IN ROW, THE CROOKS COULD NOT FIND ANY SILVER OVER HERE!

APRIL SAW ANOTHER GAIN OF 41 CONTRACTS TO STAND AT 1494

MAY SAW A LOSS OF 431 CONTRACTS DOWN TO 113,623 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 227 or 1.135 MILLION oz

CONFIRMED volume; ON TUESDAY 57,420 small//

AND NOW ONTO MARCH:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 12,005 X5,000 oz = 60.005MILLION oz

to which we add the difference between the open interest for the front month of MAR (3067) AND the number of notices served upon today (227 )x (5000 oz)

Thus the standings for silver for the MARCH 2025 contract month: 12,005 Notices served so far) x 5000 oz + OI for the front month of MAR(3067) minus number of notices served upon today (227)x 5000 oz equals silver standing for the MARCH contract month equating to 74.205 MILLION OZ.

New total standing: 74.205 million oz which is huge for this very active delivery month of March.

There are 139.805million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

FEB 13/ WITH GOLD UP 11.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 6.901 TONNES FROM THE GLD ///INVENTORY RESTS AT 866.50TONNES

FEB 12 WITH GOLD DOWN $3,40ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 10 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 7 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 6 WITH GOLD DOWN $18.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.14 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

FEB 5 WITH GOLD UP $27.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 863.05 TONNES

FEB 4 WITH GOLD UP $25.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.58 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.77 TONNES

JAN 31 WITH GOLD UP $4.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 30 WITH GOLD UP $40.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 865.34 TONNES

JAN 29 WITH GOLD DOWN $6.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.02 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 861.04 TONNES

JAN 28 WITH GOLD UP $23.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.16 TONNES OF GOLD OUT OF THE GLD //

JAN 27 WITH GOLD DOWN $36.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///

JAN 24 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 23 WITH GOLD DOWN $1.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 2.30 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 869.36 TONNES

JAN 22 WITH GOLD UP $15.15 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 7.46 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 871.66 TONNES

JAN 20 WITH GOLD UP $35.30 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 10.34 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 879.12 TONNES

GLD INVENTORY: 901.80 TONNES, TONIGHTS TOTAL

SILVER

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 12WITH SILVER UP $.01 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 8 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 10 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 7 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 6 WITH SILVER DOWN $0.17 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 12.383 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 430.39 MILLION OZ

FEB 5 WITH SILVER UP $0.45 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 3.285 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 442.773 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 3 WITH SILVER UP ONE CENT //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

JAN 31 WITH SILVER DOWN $0.19 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.369 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 448.881 MILLION OZ

jAN 30 WITH SILVER UP $0.76 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.003 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 451.249 MILLION OZ

jAN 29 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.639 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 453.252 MILLION OZ

jAN 28 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.821 MILLION OZ OUT OF THE SLV./. /

jAN 27 WITH SILVER DOWN $.61 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 24 WITH SILVER DOWN $.21 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 23 WITH SILVER DOWN $.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 4.738 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 459.035 MILLION OZ

JAN 22 WITH SILVER UP $.08 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 0.721 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 464.043 MILLION OZ

JAN 20 WITH SILVER DOWN $.09 //NO CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.568 MILLION OZ FROM THE SLV./. //INVENTORY AT SLV RESTS AT 463.315 MILLION OZ

CLOSING INVENTORY 436.501 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

Alasdair Macleod..

3 CHRIS POWELL AND GATA DISPATCHES

Chris Powell…

4 ANDREW MAGUIRE/LIVE FROM THE VAULT NO 212//ANDREW MAGUIRE INTERVIEWING DR DANIEL LACALLE

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY//EGGS

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING WEDNESDAY MORNING TUESDAY NIGHT

SHANGHAI CLOSED UP 17.76 PTS OR 0.53%

//Hang Seng CLOSED UP 652.44 PTS OR 2.84%

// Nikkei CLOSED UP 87.06 OR 0.23%//Australia’s all ordinaries CLOSED DOWN .69%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2635 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2616/ Oil UP TO 67.12 dollars per barrel for WTI and BRENT DOWN TO 70.16 Stocks in Europe OPENED ALL GREEN

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2635

OFFSHORE YUAN: DOWN TO 7.2616

SHANGHAI CLOSED CLOSED UP 17.76 PTS OR 0.53%

HANG SENG CLOSED CLOSED UP 652.44 PTS OR 2.84%

2. Nikkei closed UP 87.06OR 0.23%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 104.94// EURO RISES TO 1.0695 UP 72 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: RISES TO. +1.440//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 149.23…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7100/Italian 10 Yr bond yield UP to 3.769 SPAIN 10 YR BOND YIELD UP TO 3.359

3i Greek 10 year bond yield UP TO 3.488

3j Gold at $2917.00 Silver at: 32..39 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 16 /100 roubles/dollar; ROUBLE AT 89.57

3m oil into the 67 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149.23 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.440 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8880 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9498 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.228 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.5332 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.937 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 36.43…

10 YR UK BOND YIELD: 4.6955 UP 17 PTS

10 YR CANADA BOND YIELD: 2.920 DOWN 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.590 DOWN 4 PTS.

2a New York OPENING REPORT

Futures Rise On Hope For Trade War Relief, Europe Soars, Bunds Crash On “Whatever It Takes” Stimulus

Wednesday, Mar 05, 2025 – 08:20 AM

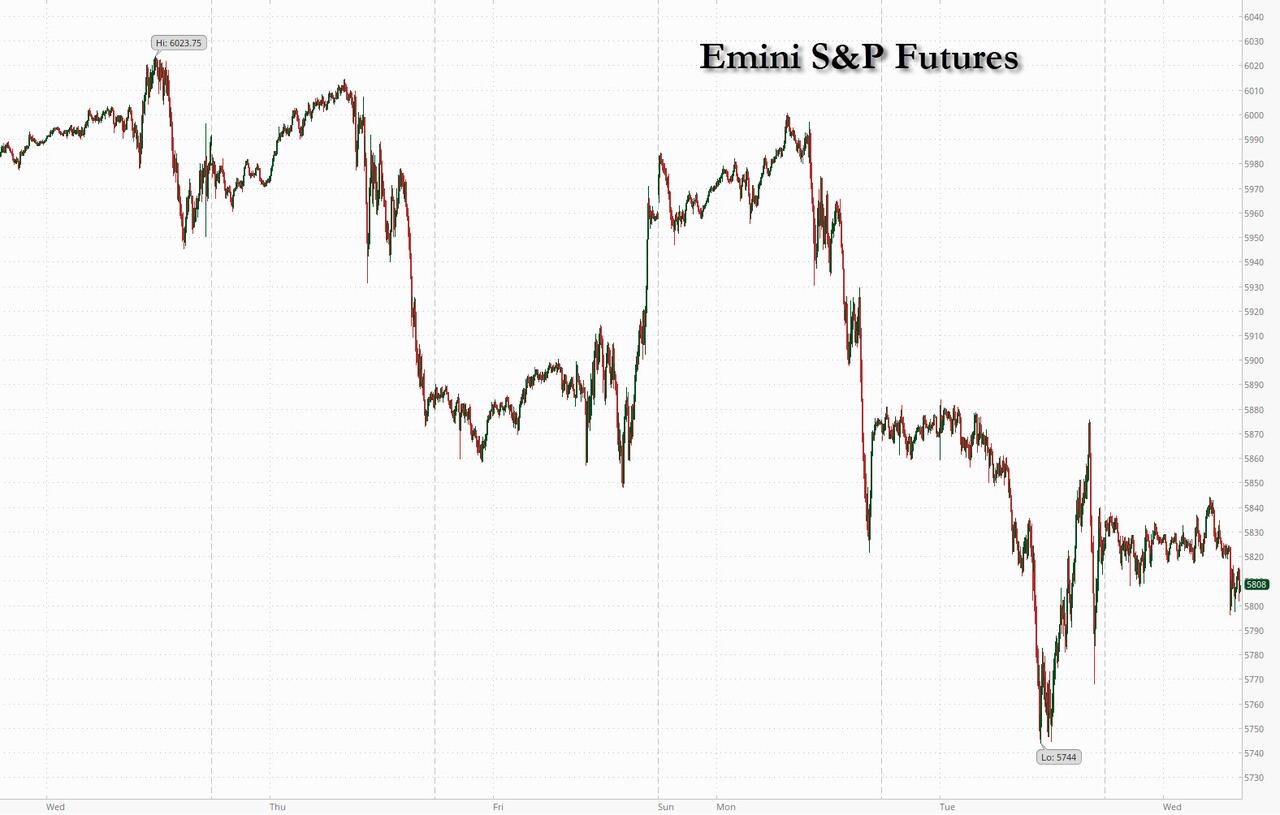

US equity futures are higher following comments from Commerce Secretary Howard Lutnick who seemed to suggest that a compromise on Canadia/Mexican tariffs could be announced today; and while Trump’s speech last night doubled-down on tariffs he but did not refute Lutnick’s comments; at the same time the US/Ukraine mineral deal also appears to be moving forward providing further de-escalatory relief for markets. As such, as of 8:00am, S&P 500 futures are up 0.3% while Nasdaq 100 contracts add 0.6% (both well off session highs) with all 7 of the Mag 7 higher and Semis are bid into MRVL earnings. Chinese stocks led a rally in Asia after Beijing set an ambitious economic growth target that boosted expectations of further stimulus.Finally, European stocks are surging (Dax +3%) after Germany unveiled plans to unlock hundreds of billions of euros for defense and infrastructure investments in a dramatic policy shift which has sent German bonds plunging by a near record 22bps. US Treasury yields are flat around 4.24% while the USD is weaker and commodities are mixed. Energy is lower, Ags higher, and precious over base. Today’s macro data focus is on ISM-Srvcs, Factory Orders, Mortgage Applications (up 20.4%), and ADP.

In premarket trading, Goldman and Citigroup rose more than 1%, while Tesla was poised to recover from a four-month low, and led gains among the Magnificent Seven stocks, putting the electric-vehicle maker’s stock on track to rebound after two sessions of losses (TSLA 1.6%, NVDA +1.5%, AMZN +0.8%, META +0.5%, GOOGL +0.6%, AAPL +0.3% and MSFT +0.3%). AeroVironment (AVAV US) shares are down 20% in premarket trading after the small unmanned aircraft maker slashed its FY forecasts. It also reported third-quarter results that missed expectations. Here are some other notable movers:

AppLovin Corp. (APP US) is downgraded to sell from neutral at Arete, which cites concerns over the firm’s e-commerce business

Carrier Global (CARR US)shares rise as much as 2.9% in US premarket trading after JPMorgan upgrades the heating and air conditioning equipment maker to overweight from neutral, seeing the stock as cheap enough

Moderna (MRNA US) shares rally 8.6% in premarket trading after Chief Executive Officer Stephane Bancel and Board Director Paul Sagan said they bought $6 million of stock, according to SEC filings

Palantir Technologies Inc. (PLTR US) shares are up 2.6% in premarket trading, after William Blair upgraded the AI software company to market perform from underperform

Shares of automakers, banks and chip firms jumped in premarket trading on Wednesday after Lutnick said the Trump administration may announce a pathway for tariff relief on goods from Canada and Mexico covered by a North American free trade agreement

US stocks capped their worst two-day slump since December on Tuesday, before the comments from Lutnick, who told Fox Business that Trump may offer a path to alleviate some tariff pressure. Traders will be watching data due later today for a snapshot of the state of the economy.

“The market doesn’t like uncertainty and tariffs will most likely continue to be an overhang risk,” Nataliia Lipikhina, EMEA equity strategy head at JPMorgan Private Bank, said on Bloomberg TV. “But if we are looking at earnings growth in the US, we actually see double-digit growth in 2025 and 2026. We are buyers of the dip at this point.”

In an address to Congress, Trump acknowledged that there may be an “adjustment period” to tariffs as he defended his policies to remake the US economy. Ten-year Treasury yields traded steady at 4.24%, while the dollar sank 0.4%.

On the corporate front, Blackrock Inc., the world’s biggest asset manager, led a consortium that will buy a controlling stake in Panama ports and a larger unit that has operations across 23 countries. It’s one of the biggest acquisitions of the year that marks a win for Trump, who had raised concerns over control of key ports near the Panama Canal.

European stocks are sharply higher on German military spending/debt brake removal, unlocking hundreds of billion of euros in defense and infrastructure spending. Shares in the region have also received a boost on hopes that the Trump administration may walk back some tariff measures and also on the increasing probability of a US/Ukraine mineral deal which is boosting the odds of a ceasefire. Construction and industrial sectors are leading the gains. Stoxx 600 rises 1.7% to 560.62 with 473 members up, 121 down and 6 unchanged. The DAX is up over 3% and set for its best day in over two years, the euro rises 0.6% and now trades above $1.07 for the first time since November. Here are some of the biggest European movers on Wednesday:

Germany’s defense, industrial and domestic stocks rise after chancellor-in-waiting Friedrich Merz said the country would unlock hundreds of billions of euros for defense and infrastructure investments.

European mining stocks and steelmakers are outperforming on Wednesday after commodity-hungry China set a bullish economic growth goal for 2025 and said it will cut output of steel in an attempt to ease a massive glut and restore profitability at mills.

Bayer shares gain as much as 6.5% after the German company reported sales and earnings for the fourth quarter that were ahead of expectations.

Campari shares rise as much as 6.3% as analysts point to the Italian spirits maker’s fourth-quarter sales beat and strength in its EMEA business and aperitifs.

Breedon Group shares jump as much as 15% after the building materials company delivered results just ahead of expectations.

Evonik shares jump as much as 11% after the specialty chemicals company said it expects earnings to grow in the current quarter.

Sandoz shares gain as much as 7% as biosimilars sales of the Swiss generic drugs maker came in slightly higher than anticipated and the company reaffirmed its mid-term outlook.

Games Workshop shares rise as much as 8.5% to hit a new record high after the Warhammer figurine maker said trading was better than expected in the first two months of 2025, which is set to see annual profit come in ahead of expectations.

Richter shares gain as much as 3.6% after the Hungarian pharmaceutical company said it plans to pay out 30%-50% of its adjusted net income in 2025-2030, providing “significant upside” to the dividend, as it focuses strategy on managing the patent cliff for its blockbuster Cariprazine drug.

Flutter shares rise as much as 3.4% in London after the FanDuel owner reported final results for 2024 in line with consensus and confident 2025 outlook.

Adidas shares fall as much as 3.9% after the sportswear company forecast FY25 operating profit that missed analyst estimates.

Lindt & Spruengli shares drop as much as 5.4% after Vontobel cut its recommendation on the chocolatier to hold from buy, citing a volatile market amid low US consumer confidence data and the strong run in the stock before results released this week.

Earlier in the session, Asian stocks rallied as China’s ambitious growth target raised prospects of more stimulus and the Trump administration indicated it may roll back some tariffs on its allies. The MSCI Asia Pacific Index rose as much as 1.1%, the most in three weeks, with Chinese technology stocks like Tencent and Meituan among the biggest boosts. Chinese stocks in Hong Kong rallied more than 3% after the National People’s Congress in Beijing set an economic growth target of about 5% for 2025, the third straight year it has maintained that goal. Stock benchmarks also rallied in Japan, Korea and Taiwan. Donald Trump’s administration showed willingness to walk back on the 25% tariff imposed on Canada and Mexico, two of its biggest trading partners. Hong Kong and China’s “major indexes do not look expensive, trading around historical means,” Citi strategists including Pierre Lau wrote in a note. “Valuations of China’s alternatives to the US’s magnificent-seven stocks look inexpensive, in our view,” he said. Elsewhere, India’s NSE Nifty 50 Index climbed, snapping a record-setting 10-day losing streak, while stocks fell in Australia.

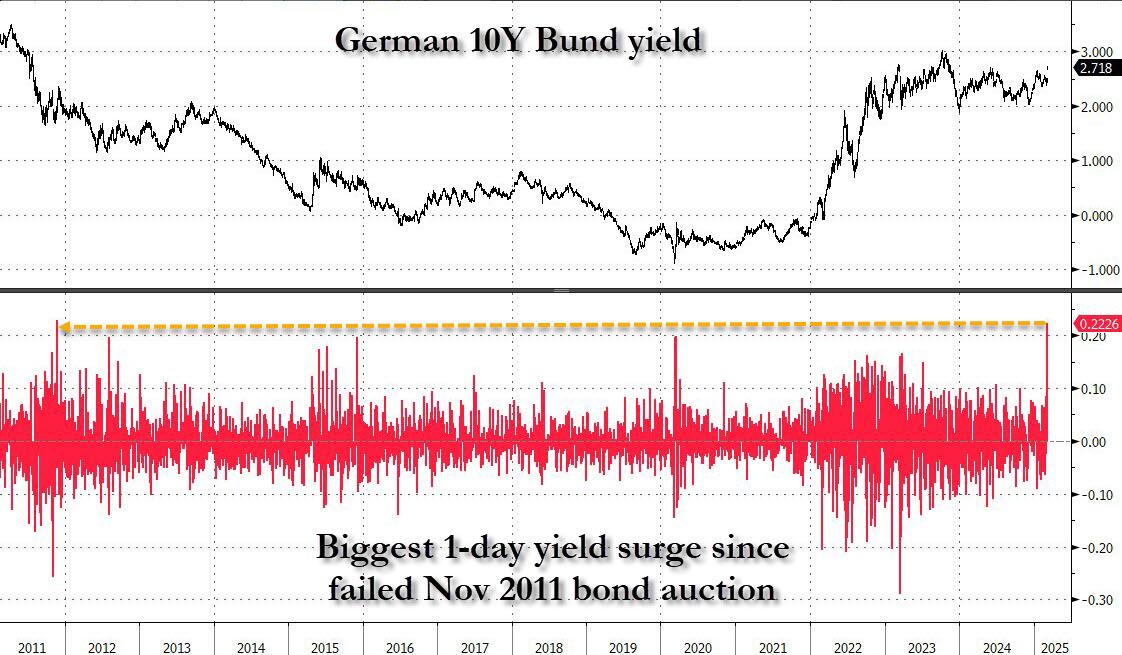

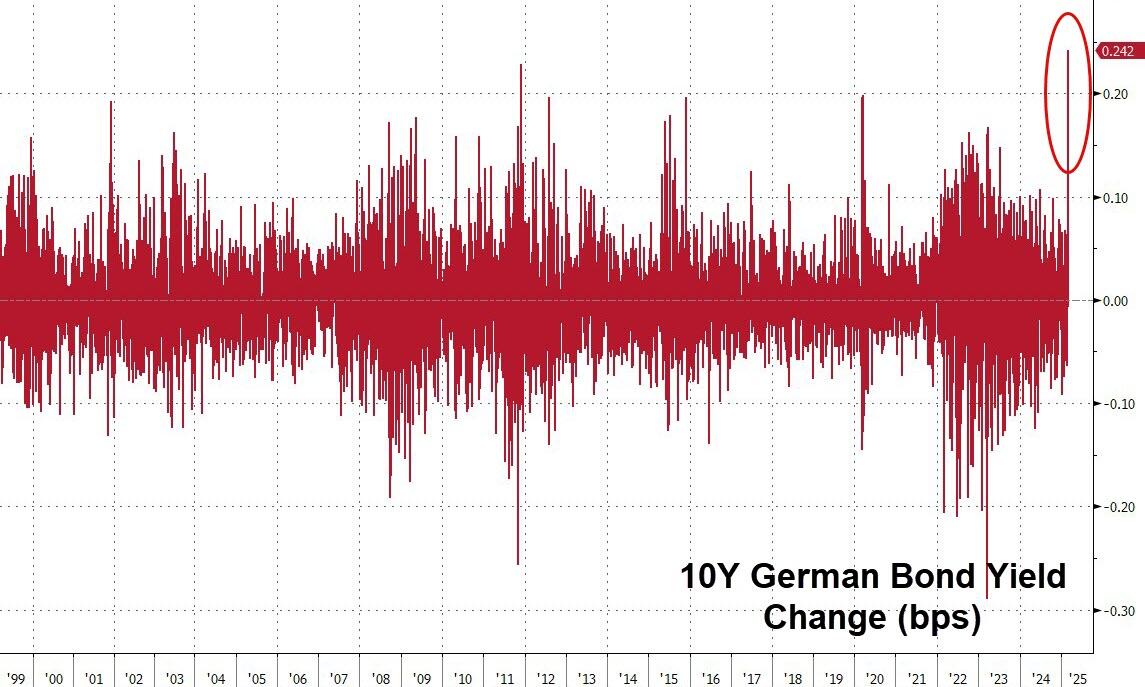

While German and European stocks are surging, German bunds lead a near-record plunge in European government bonds after Germany unveiled plans to unlock hundreds of billions of euros for defense and infrastructure investments in a dramatic policy shift. German 10-year yields soar more than 22 bps to 2.72%, the biggest one day move since the failed bund auction in Nov 2011.

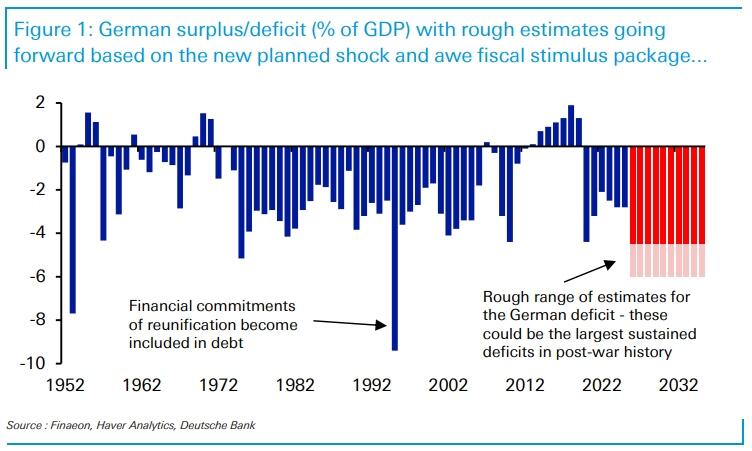

“Huge quantities of debt in the coming years is going to be quite disruptive for European bond markets, particularly the long end of the curve,” said Peter Kinsella, global head of FX strategy at Union Bancaire Privee Ubp SA in London. “We’ve not seen this type of issuance pretty much since the early 1990s when Germany was paying for reunification.

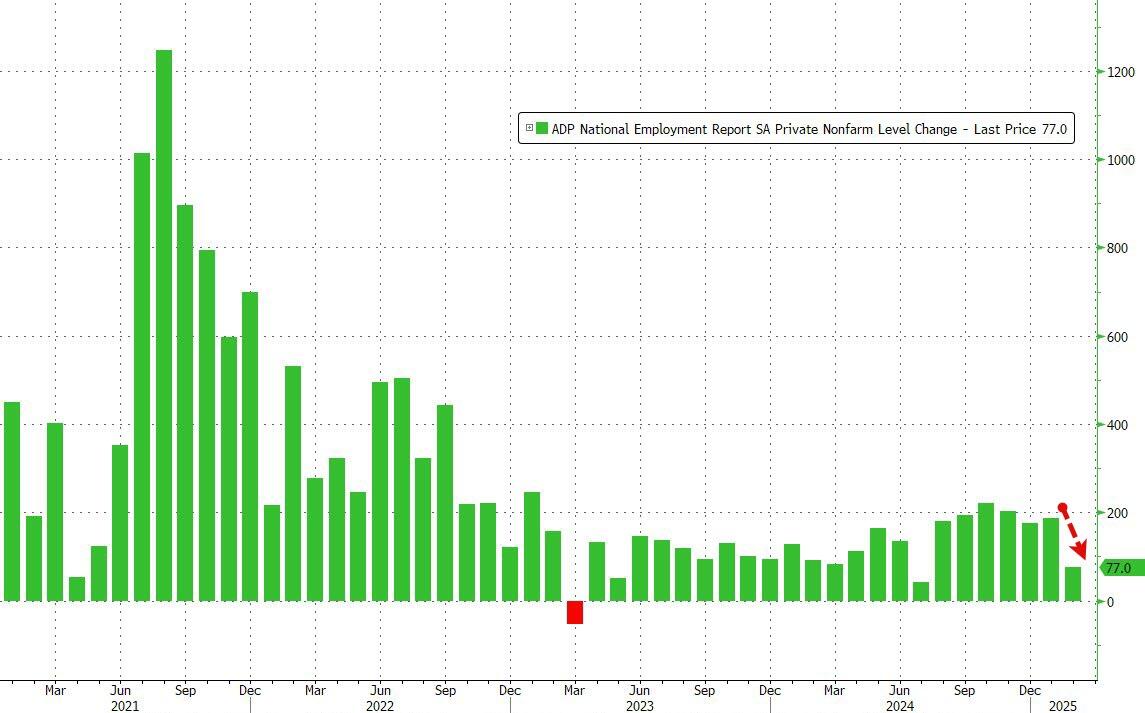

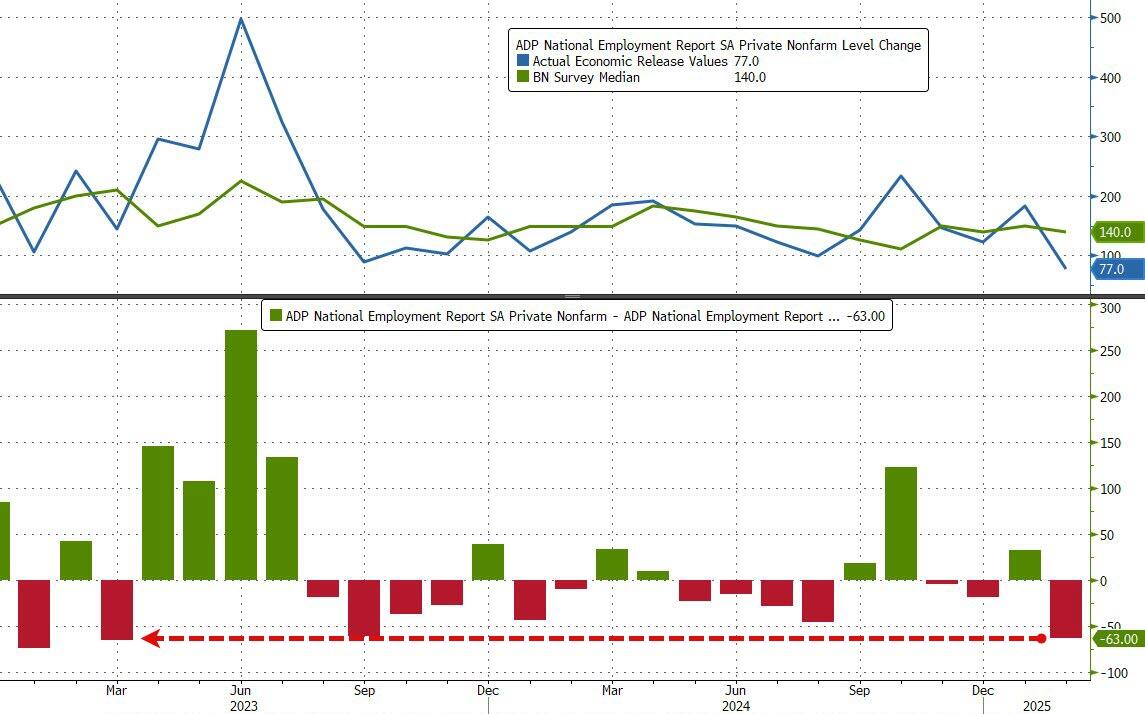

In the US, treasuries are steady as US trading gets under way with the curve steeper, as front-end yields are more than 3bps richer on the day with long end little changed. Treasury yield shift leaves 2s10s, 5s30s spreads steeper by 3bp-4bp; US 10-year yield around 4.23% is ~2bp lower on the day while Germany’s is higher by 22bp, after German policy shift to a massive debt-financed defense spending plan. US session includes February ADP employment and ISM services gauge, and possibility of Mars Inc. corporate bond sale exceeding $25 billion.

In FX, the Bloomberg Dollar Spot Index fell 0.6%, hitting its lowest since Dec. 9, led by falls versus the euro; EUR/USD jumped 0.9% to 1.0722, a level last seen on Nov. 11 after Germany pledged to unlock hundreds of billions of euros for defense and infrastructure spending; the Swedish krona takes top spot among G-10 FX, rising 1% against the greenback.

“The US economy could slow down further and force the Fed to resume its easing cycle in the second half of the year,” said Valentin Marinov, head of global FX strategy at Credit Agricole CIB. “The Fed may also have to put an end to its quantitative tightening programme to accommodate US President Donald Trump’s fiscal spending plans. This could erode the USD exceptionalism.”

In commodities, WTI falls 1.5% to $67.20 a barrel. Bitcoin rises 3% and above $90,000.

The US economic data calendar includes mortgage applications which soared by 20.4%, after dropping 6.4% last week; February ADP employment change (8:15am), S&P Global US services PMI (9:45am), January factory orders and February ISM services index (10am). Fed releases Beige book at 2pm. Fed speaker slate empty for the session

Market Snapshot

S&P 500 futures up 0.8% to 5,838.00

MXAP up 1.1% to 186.59

MXAPJ up 1.9% to 586.12

Nikkei up 0.2% to 37,418.24

Topix up 0.3% to 2,718.21

Hang Seng Index up 2.8% to 23,594.21

Shanghai Composite up 0.5% to 3,341.97

Sensex up 1.0% to 73,718.18

Australia S&P/ASX 200 down 0.7% to 8,141.11

Kospi up 1.2% to 2,558.13

STOXX Europe 600 up 1.5% to 559.12

German 10Y yield little changed at 2.68%

Euro up 0.9% to $1.0718

Brent Futures down 0.6% to $70.63/bbl

Gold spot down 0.1% to $2,915.13

US Dollar Index down 0.82% to 104.88

Top Overnight News

US President Trump said in his Address to the Joint Session of Congress that America is back and they have taken swift and relentless action and are just getting started. Trump announced he will create a new office of shipbuilding in the White House and will offer new tax incentives for shipbuilding, while he is fighting every day to make America affordable again and reiterated his call to drill for more oil. Furthermore, Trump said they will eliminate inflation by reducing all fraud, waste and theft of public money and stated that reciprocal tariffs will kick in on April 2nd.

President Donald Trump’s administration is considering granting relief from his 25% tariffs on Canadian and Mexican imports to products that comply with the trade pact he negotiated with the two U.S. neighbors during his first term, Commerce Secretary Howard Lutnick said on Tuesday. RTRS

Trump called for ending the bipartisan $52 billion chip subsidy program, saying it’s a “horrible, horrible thing.” An end to subsidies will end up benefiting the Chinese AI and semiconductor sector. BBG

Border crossings along the US-Mexico border plummeted to the lowest level in decades during Feb, giving Trump a major victory. Axios

German borrowing costs surged by the most in 17 years as investors bet on a big boost to the country’s ailing economy from a historic deal to fund investment in the military and infrastructure. The yield on the 10-year Bund surged 21 bps to 2.69%, its biggest one day move since 2008. FT

Google is urging DOJ officials to back away from a push to break up the company, citing national security concerns, people familiar said. The Biden administration called for changes including the sale of its Chrome web browser, with hearings scheduled for next month. BBG

China’s NPC numbers are largely consistent w/recent media reports, including a GDP growth objective of around 5%, inflation around 2%, and a fiscal deficit target of 4%, while officials pledged to boost domestic consumption. WSJ

China’s Caixin services PMI comes in ahead of expectations for Feb at 51.4 (up from 51 in Jan and above the Street’s 50.7 forecast). BBG

BOJs Uchida said the BOJ can raise interest rates at a pace in line with dominant views among financial markets and economists, keeping alive expectations that there is a chance of a near term increase in borrowing costs despite Trump tariff risks. RTRS

2B European opening report

Global Sentiment lifted on tariff optimism, European stocks at highs & Bunds hammered on German spending plans – Newsquawk US Market Open

Wednesday, Mar 05, 2025 – 06:04 AM

Sentiment lifted after the US Commerce Secretary suggested Trump could potentially reduce tariffs on Canada and Mexico, perhaps as soon as Wednesday.

European bourses at session highs; DAX 40 +3% outperforms; US equity futures broadly higher with the RTY +1.2%.

EUR surges on German spending plans, DXY around 1.05 after breaking below its 200DMA.

Bunds battered by Merz’s fiscal reform, USTs await data and tariff updates.

Crude subdued continuing recent action & failing to benefit from China’s support which has bolstered base metals.

Looking ahead, US ADP National Employment, US Factory Orders, ISM Services, Fed’s Beige Book, BoE Treasury Select Hearing, Speakers including BoE’s Bailey, Pill, Taylor and Greene. Earnings from Abercrombie & Fitch, Foot Locker & Marvell.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

TARIFFS/TRADE

US Commerce Secretary Lutnick said he thinks US President Trump will meet Mexico and Canada in the middle on tariffs and they’re probably going to be announcing that tomorrow (i.e. Wednesday 5th), while he added if USMCA rules are followed, Trump is considering relief, according to a Fox Business interview. Lutnick also said that President Trump is to move with Canada and Mexico but not all the way and that Trump may roll back Canada and Mexico tariffs on Wednesday.

US and Canadian officials are in talks to possibly roll back Trump’s tariffs, according to WSJ. However, it was separately reported that US President Trump signalled privately he will stick with tariffs, according to NYT.

US Department of Commerce preliminarily determined Canadian softwood lumber is being dumped into the US.

Canada’s Foreign Minister Joly is set to speak with US Secretary of State Rubio on Wednesday, according to the BBC.

US President Trump’s administration is readying an order to bolster US shipbuilders and punish China, while the draft order includes measures such as raising revenue from Chinese ships and tax credits and grants for shipyards, according to WSJ.

EUROPEAN TRADE

EQUITIES

European bourses (STOXX 600 +1.5%) are entirely in the green, with sentiment boosted by several factors, which include; a) Lutnick suggesting Trump will scale back Canada/Mexico tariffs, b) Germany agreeing to debt brake reform, c) China’s Official Work Report which maintained its annual growth target and pledged measures including a boost in spending. Price action today has really only been one way, and that’s upward; as it stands, indices generally reside at session highs.

European sectors hold a positive bias, with the key movers today attributed to the aforementioned German debt brake reform agreement. Construction & Materials tops the pile, joined closely by Industrial Goods and Services, Autos and then Tech; the latter two, buoyed by the risk-tone given the optimism surrounding a rolling back of US tariffs on Canada/Mexico.

US equity futures (ES +0.6% NQ +0.7% RTY +1.2%) are entirely in the green, with sentiment lifted after US Commerce Secretary Lutnick said Trump could potentially scale back tariffs on Canada and Mexico, perhaps as soon as Wednesday.

Tesla’s (TSLA) German sales fell 76% in February in rising EV market, via Bloomberg.

Saudi Aramco said to mull bid for BP’s (BP/ LN) Castrol, via Bloomberg; will study bid for part, or all of Castrol’s businesses; said to be particularly interested in Castrol India; Aramco deliberations at an early stage, may not lead to bid.

DXY is extending its downside for a third consecutive session as gains in the EUR act as a drag on the index. DXY has fallen from the 107.56 level seen at the start of the week to a current session trough at 104.85, taking out its 200DMA at 105.00 in the process. Headwinds for the DXY aren’t just a case of EUR strength, it is also in the context of domestic weakness following a recent run of soft data prints. And on the trade front, US Commerce Secretary Lutnick suggested Trump could potentially reduce tariffs on Canada and Mexico, perhaps as soon as Wednesday. Today’s data slate sees US ADP and ISM services PMI with the former taking place in the context of Friday’s NFP print.

EUR is the clear outperformer across the majors with the obvious catalyst for recent price action being the latest updates out of Germany. To recap, the measures announced by Merz and others include a special EUR 500bln 10yr fund for infrastructure investments, changes to the debt brake to exempt defence spending of more than 1% of GDP, a loosening of the regional balanced budget requirement and a new instrument to provide EUR 150bln of loans. Subsequently, EUR/USD has surged from the circa 1.0388 level seen at the start of the week to a multi-month peak at 1.0722, brining it in touching distance of its 200DMA at 1.0725.

JPY is firmer vs. the broadly weaker USD. On the domestic front, BoJ Governor Ueda noted that diverging monetary policy stance among countries could potentially increase volatility, have destabilising effects on exchange-rate dynamics. Elsewhere, BoJ Deputy Governor Uchida said he does not have a preset idea in mind on the pace of future rate hikes and does not think it is good communication for the BoJ to judge whether market pricing of future moves are appropriate or not. USD/JPY has delved as low as 149.11 but stayed clear of yesterday’s 148.08 YTD trough.

Cable is up for a third session in a row, clearing the 1.28 mark and its 200DMA at 1.2803, printing a fresh YTD peak at 1.2854. Newsflow for the UK remains on the light side asides from reporting via the BBC that the Treasury will inform the OBR of its “major measures” on Wednesday aimed at reducing spending by billions pounds.

Antipodeans both faded some of their recent gains as the greenback recouped lost ground and amid the mixed risk sentiment in Asia, while there was little reaction seen following better-than-expected Australian GDP data or from the announcement that RBNZ Governor Orr resigned.

Hotter-than-expected Swiss inflation metrics from Switzerland triggered a knee-jerk lower in EUR/CHF from 0.9470 to 0.9453 before paring almost all of the move. The release exceeded expectations but fell in-line with the SNB’s Q1 projection of 0.3%.

PBoC set USD/CNY mid-point at 7.1714 vs exp. 7.2575 (prev. 7.1739).