GOLD CLOSED UP $2.10 TO $2918.65

SILVER CLOSED UP $0.16 CENTS TO $32.75

GOLD ACCESS CLOSED 2909.60

Silver ACCESS CLOSED: $32.62

Bitcoin morning price:$90,979 UP2841 DOLLARS.

Bitcoin: afternoon price: $88,970 UP 832 DOLLARS

Platinum price closing UP $6.60 TO $971.10

Palladium price; UP $8.85 TO $949.40

END

*CANADIAN GOLD: $4160.60 DOWN 23.70 CDN dollars per oz( * NEW ALL TIME HIGH 4208.15CDN DOLLARS PER OZ//FEB 24 2025)

*BRITISH GOLD: 2259.60 DOWN 4.20 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,339.25 BRITISH POUNDS/OZ) FEB 10/2025

*EURO GOLD: 2,698.90 DOWN 4.48 Euros per oz //* (ALL TIME CLOSING HIGH: 2,819,78UROS PER OZ/FEB 24 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,915.300000000 USD

INTENT DATE: 03/05/2025 DELIVERY DATE: 03/07/2025

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 32

072 H GOLDMAN 667

118 C MACQUARIE FUT 333

132 C SG AMERICAS 8 9

190 H BMO CAPITAL 335

323 C HSBC 463

363 H WELLS FARGO SEC 338

523 C INTERACTIVE BRO 2

624 H BOFA SECURITIES 288

657 C MORGAN STANLEY 68

661 C JP MORGAN 12

686 C STONEX FINANCIA 8 83

690 C ABN AMRO 11

709 C BARCLAYS 18

737 C ADVANTAGE 8

905 C ADM 19

TOTAL: 1,351 1,351

JPMORGAN STOPS 12/1351 CONTRACTS

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2024. CONTRACT: 1351 NOTICES FOR 135,100 OZ 4.202 TONNES

total notices so far: 12,458 contracts for 1,245,800 Oz (38.874 tonnes)

FOR MARCH

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 454 NOTICE(S) FILED FOR 2.270 MILLION OZ/

total number of notices filed so far this month : 12,458 for 62.290 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $2.10 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44TONNES

INVENTORY RESTS AT 900.36 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP 16 CENTS AT THE SLV: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .455 MILLION OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 436.501 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA MEGA MONSTER SIZED 4231 CONTRACTS TO 150,166 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS MONSTER SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE GAIN OF $0,82 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A MEGA MEGA HUMONGOUS GAIN OF 5277 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR HUGE GAIN IN PRICE//WEDNESDAY’S TRADING.. WE HAD LITTLE LIQUIDATION OF T.A.S. CONTRACTS ON WEDNESDAY COMEX TRADING / AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON WEDNESDAY WITH SILVER’S HUGE GAIN IN PRICE. WE HAD A LITTLE T.A.S. LIQUIDATION WEDNESDAY CONSERVING THEIR ENERGY FOR TODAY. BUT THIS WAS COUPLED WITH ANOTHER HUGE T.A.S. ISSUANCE OF 926 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.00 DOLLAR MARK. THUS OUR RAID TODAY! WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND 95 CENTS AND A LEASE RATE OF 6%. WE HAD A HUGE 1046 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 926 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY.S TRADING//RAID AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUMONGOUS 5277 CONTRACTS ON OUR TWO EXCHANGES WITH OUR HUGE GAIN IN PRICE. WE HAD SMALL TAS LIQUIDATION THROUGHOUT WEDNESDAY’S COMEX TRADING SESSION WHICH ACCOUNTS FOR THE HUGE GAIN IN OI ON OUR TWO EXCHANGES.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY!

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE 928 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.82 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A MEGA MEGA MONSTER GAIN IN OUR TWO EXCHANGES OF 5277 CONTRACTS WE HAD A LITTLE LIQUIDATION OF T.A.S. CONTRACTS TRYING TO CONTAIN SILVER’S PRICE RISE AND THAT ACCOUNTS OF MOST OF OUR OPEN INTEREST RISE.

WE HAD A 1046 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 78.753 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0.290 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON

INITIAL STANDING FOR MARCH REDUCES TO 73.930 MILLION OZ

WE HAD:

/ MEGA MEGA COMEX OI GAIN+// A HUGE SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 926 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 369 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR

TOTAL CONTRACTS for 4 DAYS, total 2076 contracts: OR 10.380 MILLION OZ (519 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 10.380 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 10.38 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4231 CONTRACTS WITH OUR GAIN IN PRICE OF 82 CENTS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A 1046 CONTRACT EFP ISSUANCE CONTRACTS: 1046 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH OF 78.455 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 0.290 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON//NEW STANDING REDUCES TO 73.930 MILLION OZ

WE HAVE 1). A MEGA MEGA HUMONGOUS SIZED GAIN OF 5231 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR STRONG GAIN IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 926 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//LITTLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION SAVING THEIR ENERGY FOR TODAY (THURSDAY). HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON WEDNESDAY WITH THE HUGE GAIN IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (926 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 454 NOTICE(S) FILED TODAY FOR 2.270 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3083 OI CONTRACTS TO 492,353 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A STRONG SIZED 1151 CONTRACTS//

WE HAD A FAIR SIZED INCREASE IN COMEX OI (3083 CONTRACTS) OCCURRED WITH OUR GAIN OF $6.75 IN PRICE WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 31.757 TONNES FOLLOWED BY TODAY’S HUGE 52,600 OZ QUEUE JUMP (1.633 TONNES)//NEW STANDING ADVANCES TO 30.309 TONNES

/NEW STANDING FOR MARCH; 39.309 TONNES

/ ALL OF THIS HAPPENED WITH OUR $6.75 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX ///. WE HAD A GOOD SIZED GAIN OF 3888 OI CONTRACTS (12.093 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE FRONT MARCH CONTRACT MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 805 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 492,353

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3888 CONTRACTS WITH 3083 CONTRACTS INCREASED AT THE COMEX// AND A SMALL SIZED 805 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3888 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE SIZED AND CRIMINAL 3772 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (805 CONTRACTS) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 3083 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3888 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH 31.757 TONNES FOLLOWED BY TODAY’S HUGE 1.633 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 39.309 TONNES

NEW STANDING FOR MARCH ADVANCES TO:

39.309 TONNES

//NEW STANDING MARCH: 39.309 TONNES

.

/ 3) SMALL T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE WEDNESDAY WITH NO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WITH OUR1) $6.75 PRICE GAIN WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A GOOD GAIN OF 3888 CONTRACTS ON OUR TWO EXCHANGES ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN MARCH

4) STRONG SIZED COMEX OPEN INTEREST INCREASE 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 3772 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH :

TOTAL EFP CONTRACTS ISSUED: 8384 CONTRACTS OF 838,400 OZ OR 26.077 TONNES IN 4 TRADING DAY(S) AND THUS AVERAGING: 2,096 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES 26.077 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 26.077 DIVIDED BY 3550 x 100% TONNES = 0.732% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 26.077 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA MEGA HUMONGOUS SIZED 4231 CONTRACTS OI TO 150,166 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1046 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1046 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1046 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 4231 CONTRACTS AND ADD TO THE 1046 E.FP. ISSUED

WE OBTAIN A MEGA MEGA HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 5277 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 26.385 MILLION OZ OCCURRED WITH OUR $0.82 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 39.13 PTS OR 0.17%

//Hang Seng CLOSED UP 775.50 PTS OR 3.29%

// Nikkei CLOSED UP 286,64 OR 0.77%//Australia’s all ordinaries CLOSED DOWN .44%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2481 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2482/ Oil UP TO 66.81 dollars per barrel for WTI and BRENT DOWN TO 69.73 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

END

ASIA TRADING THURSDAY MORNING/WEDNESDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3083 CONTRACTS TO 492,353 WITH OUR STRONG GAIN IN PRICE OF $6.75 WITH RESPECT TO WEDNESDAY’S TRADING/. WE LOST ZERO NET LONGS WITH THAT PRICE GAIN FOR GOLD. BUT AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (805 ).

THE CME ANNOUNCED WEDNESDAY NIGHT, ZERO EXCHANGE FOR RISK CONTRACTS FOR NIL OZ OR 0 TONNES.

IN FEBRUARY: WE HAD FIVE EXCHANGE FOR RISKS TOTALLING 18.4527 TONNES!. THE RECIPIENT OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY.

THUS IN TOTAL WE HAD A GOOD SIZED GAIN ON OUR TWO EXCHANGES OF 3888 CONTRACTS WITH OUR STRONG GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW CLIMBED TO 10% AS GOLD IN LONDON IS NOW EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY TODAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION// WEDNESDAY // THEY ISSUED A HUGE 3772 CONTRACT ANNOUNCEMENT (WEDNESDAY NIGHT/THURSDAY MORNING). THE T.A.S. LIQUIDATION IS WHY WE ARE HAVING A LOWER COMEX OPEN INTEREST GAIN BUT THIS IS COUPLED WITH HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY TODAY AS YOU WILL SEE.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 16+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, , 203 , ,205 , 207 209 AND TODAY’S 211 AND 212 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST FEW WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF MARCH .… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 805 EFP CONTRACTS WERE ISSUED: : /APRIL 805 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 805 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 3888 CONTRACTS IN THAT 805 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR GAIN OF 3083 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $6.75 FOR WEDNESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A SMALL SIZED SIZED 805 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER 4 WEEKS AGO, THE FED WAS EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH COMEX OPTIONS EXPIRY AND OTC LONDON OPTIONS EXPIRY.

THE RAIDS ON OPTIONS EXPIRY DOES TWO IMPORTANT THINGS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER 2024

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS.

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: MARCH (39.309 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE MARCH DELIVERY MONTH / FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH.

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

AND NOW MARCH:

STANDING FOR GOLD : 39;309 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527

= 256.607 TONNES.

MARCH: 39.309 TONNES

COMEX GOLD TRADING/MARCH CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $6.75/)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OUR TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION WEDNESDAY AS THEY WERE TRYING TO QUELL GOLD’S RISE AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING. LAST TUESDAY ENDED COMEX OPTIONXS EXPIRY. HOWEVER AS I EXPLAINED ON LAST WEDNESDAY, WE HAD THE MUCH BIGGER OTC.LONDON.OTC EXPIRY.THE BANKERS WERE UNSUCCESSFUL IN SLOWING THEIR DERIVATIVE LOSSES IN PRECIOUS METAL BETS WITH OPTIONS EXPIRY FOR BOTH COMEX AND LONDON OTC!!

LAST NIGHT/THIS MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD)

EXCHANGE FOR RISK EXPLANATION/DECEMBER AND JANUARYTRADING

DECEMBER MONTH EXCHANGE FOR RISK!

88 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 6 FOR 14.6836 TONNES A NEW RECORD. THE COMEX IS TOTALLY SHATTERED TO PIECES.

EXCHANGE FOR RISK // JANUARY MONTH!!

LO AND BEHOLD, THE CROOKS ISSUED THEIR FIRST ISSUANCE A MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THEN TO MY HORROR, THEY ISSUED THEIR SECOND EXCHANGE FOR RISK ON JAN 8, TOTALLING 150 CONTRACTS FOR 15000 OZ OR .4665 TONNES. THIS TONNAGE WILL BE ADDED TO THE FIRST ISSUANCE. THUS TOTAL EXCHANGE FOR RISK ISSUANCE FOR OUR TWO EARLY JANUARY EX FOR RISK: 5.7533 TONNES. THEN MERCILESSLY THEY CONSUMMATED FOR THE THIRD TIME THIS MONTH 85 EXCHANGE FOR RISK LAST THURSDAY NIGHT (JAN 17) FOR 8500 OZ OR .2649 TONNES OF GOLD. THEN TO MY HORROR THEY ISSUED THEIR 4TH EXCHANGE FOR RISK THIS MONTH (JAN 22) FOR A MONSTER 5000 CONTRACTS OR 5,000,000 OZ.(15.562 TONNES).NOT TO BE UNDONE, THE CROOKS ISSUED THEIR FIFTH EXCHANGE FOR RISK LAST NIGHT FOR 500 CONTRACTS REPRESENTING 50,,000 OZ OR 1.555 TONNES OF GOLD. REMEMBER THAT THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON WHICH IS TOTALLY ASININE!! THUS FOR THE 5 EXCHANGE FOR RISK ISSUED THIS MONTH TOTALS 23.134 TONNES OF GOLD. THIS BRINGS US TO , JAN 25 WHERE THE CME ANNOUNCED ITS SIXTH MAJOR EXCHANGE FOR RISK ISSUANCE OF 6454 CONTRACTS FOR 645,400 OZ OR 20.074 TONNES OF GOLD. THIS IS THE HIGHEST EVER RECORDED ISSUANCE IN NUMBER OF EXCHANGE FOR RISK, AT 6, AND FOR NEW TOTALS FOR THE MONTH OF JANUARY: 43.208 TONNES!!! AND A NEW RECORD FOR ISSUANCE.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO, THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WILL NOW BE ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FOR FRIDAY FEB 28 ZERO EXCHANGE FOR RISK WAS ISSUED.

TOTAL INITIAL DELIVERIES MARCH GOLD TRADING

MARCH: 39.306 TONNES

WE HAVE GAINED A STRONG SIZED TOTAL OF 12.093 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH (31.753TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 52,500 OZ OR 1.633 TONNES: NEW TOTAL STANDING 39.309 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $6.75

WE HAD 1151 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 3888 CONTRACTS OR 388,800 0Z (12.093 TONNES)

confirmed volume WEDNESDAY 205,124ontracts: fair///

//speculators have left the gold arena

END

MARCH

// THE MARCH 2025 GOLD CONTRACT

MARCH 6

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 3 entries i) Out of Brinks enhanced: 202,188.800 oz 505 London good delivery bars at 400 oz each. ii) Ashai: 161,756.361 oz iii) 96,453.000 oz Brinks 3000 kilobars total weight withdrawal: 460,398.161 or 14.32 tonnes . |

| Deposit to the Dealer Inventory in oz | 2 ENTRIES i) Asahi dealer 62,597.997 oz (1,947 kilobars ii) Manfra dealer: 257,240.150 oz (8001 kilobars) total dealer weight: 319,838.147 oz(9948 kilobars) in tonnage; 9.948 tonnes |

| Deposits to the Customer Inventory, in oz | 2 ENTRIES i) Brinks 89,807.700 oz oz ii) Manfra: 48,161.471 o (1498 kilobars) total weight: 137,969.171 oz 4.29 tonnes total weight deposit;; 14.138 tonnes |

| No of oz served (contracts) today | 1351 notice(s) 135100 OZ 4.202 TONNES |

| No of oz to be served (notices) | 140 contracts 14,000 OZ 0.4384 TONNES |

| Total monthly oz gold served (contracts) so far this month | 12,498notices 1,249,800 oz 38.874 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 2

2 ENTRIES

i) Asahi dealer 62,597.997 oz (1,947 kilobars

ii) Manfra dealer: 257,240.150 oz (8001 kilobars)

total dealer weight: 319,838.147 oz(9948 kilobars)

in tonnage; 9.948 tonnes

xxxxxxxxxxxxxxxx

we have 2 customer deposits:

2 ENTRIES

i) Brinks 89,807.700 oz oz

ii) Manfra: 48,161.471 o (1498 kilobars)

total weight: 137,969.171 oz

4.29 tonnes

total weight deposit;; 14.138 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 3

i) Out of Brinks enhanced: 202,188.800 oz

505 London good delivery bars at 400 oz each.

ii) Ashai: 161,756.361 oz

iii) 96,453.000 oz Brinks 3000 kilobars

total weight withdrawal: 460,398.161 or 14.32 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxx

adjustments:1/comex is in chaos

a) dealer to customer

a) Loomis: 96.457 oz

thus basically what comes into eligible is transferred to dealer accounts and then out.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MARCH

THE FRONT MONTH OF MARCH HAD A GAIN OF 434 CONTRACTS TO STAND AT 1491. WE HAD 91 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED A HUGE 525 CONTRACTS FOR 52500 OZ (1.633 TONNES AS A PHYSICAL GOLD QUEUE JUMP. THIS IS CENTRAL BANKS LOOKING FOR BADLY NEEDED GOLD.

APRIL HAD A LOSS OF 4215 CONTRACTS DOWNTO 335,694 CONTRACTS AS THIS MONTH BECOMES THE FRONT MONTH.

MAY GAINED 5 CONTRACTS UP TO 256.

We had 1351 contracts filed for today representing 135,100oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1351 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 12 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MARCH /2025. contract month, we take the total number of notices filed so far for the month (12,498 X 100 oz ) to which we add the difference between the open interest for the front month of MARCH.(1491 CONTRACTS) minus the number of notices served upon today (1351 x 100 oz per contract) equals 1,263800 OZ OR 39.309 TONNES

thus the INITIAL standings for gold for the MARCH contract month: No of notices filed so far (12,498x 100 oz +we add the difference for front month of MARCH (1491 OI} minus the number of notices served upon today (1351 x 100 oz) which equals 1,263,800 OR 39.309 TONNES

TOTAL COMEX GOLD STANDING FOR MARCH.: 39.309 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND MARCH IS FOLLOWING SUIT..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,085,544.431 oz 64.86 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 39,670,180.54 .oz

TOTAL REGISTERED GOLD 19,731,635.090 or 613.736 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 19,938,545.45 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 17,628,091oz (REG GOLD- PLEDGED GOLD)= 548.30 tonnes //

END

SILVER/COMEX

MARCH 6

INITIAL

// THE MARCH 2025 SILVER CONTRACT//INITIAL

MARCH 5

INITIAL

// THE MARCH 6 2025 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | nil withdrawals 1 1 entry i) Out of Loomis; 40,049.820 oz |

| Deposits to the Dealer Inventory | i) 2 dealer deposit/ 2 entries i)Brinks 642,391.710 oz ii) Loomis 369,332.99 oz total weight: 1,011,724.670 oz |

| Deposits to the Customer Inventory | 2 entries i)Into Brinks 1003.842 oz ii) Into JPMORGAN 1889,254.842 oz total weight: 2,490,311.982 oz 3 entries i)Into ASAHI 594,785.800 oz ii) Loomis 602,675.180 iii) Into JPMorgan: 1,241,566.900 oz total weight: 3,390,040.790 oz total weight 2,439,027.880 oz |

| No of oz served today (contracts) | 454 CONTRACT(S) (2.27MILLION OZ |

| No of oz to be served (notices) | 2328 contracts (11.640 MILLION oz) |

| Total monthly oz silver served (contracts) | 12,458 Contracts (62.290 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 2 dealer deposit/

2 entries

i)Brinks 642,391.710 oz

ii) Loomis 369,332.99 oz

total weight: 1,011,724.670 oz

total dealer withdrawals: 0 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

2 entries

i)Into Brinks 1003.842 oz

ii) Into JPMORGAN 1889,254.842 oz

total weight: 2,490,311.982 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals 1

1 entry

i) Out of Loomis;

40,049.820 oz

xxx

ADJUSTMENTs 0

JPMorgan has a total silver weight: 167.276million oz/420.227million or 39.80%

TOTAL REGISTERED SILVER: 141.152 MILLION OZ//.TOTAL REG + ELIGIBLE. 420.277Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF MARCH /2025 OI: 2782 OPEN INTEREST CONTRACTS FOR A LOSS OF 285 CONTRACTS.WE HAD 227 CONTRACTS SERVED ON WEDNESDAY SO WE LOST 58 CONTRACTS OR 0.290 MILLION COMEX OZ STANDING UNDERWENT AN EFP TRANSFER TO LONDON LOOKING FOR METAL OVER ON THAT SIDE OF THE POND//NEW STANDING REDUCES TO 73.930 MILLION OZ. FOR THE FOURTH DAY IN ROW, THE CROOKS COULD NOT FIND ANY SILVER OVER HERE!

APRIL SAW ANOTHER GAIN OF 43 CONTRACTS TO STAND AT 1537

MAY SAW A GAIN OF 2682 CONTRACTS UP TO 116,305 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 454 or 2.270 MILLION oz

CONFIRMED volume; ON WEDNESDAY 74.462 small//

AND NOW MARCH DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 12,458 X5,000 oz = 62.290MILLION oz

to which we add the difference between the open interest for the front month of MAR (2782) AND the number of notices served upon today (454 )x (5000 oz)

Thus the standings for silver for the MARCH 2025 contract month: 12,458 Notices served so far) x 5000 oz + OI for the front month of MAR(2782) minus number of notices served upon today (458)x 5000 oz equals silver standing for the MARCH contract month equating to 73.930 MILLION OZ.

New total standing: 73.930 million oz which is huge for this very active delivery month of March.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 141.152million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

MARCH 6 WITH GOLD UP $2.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 900.30 TONNES

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

FEB 13/ WITH GOLD UP 11.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 6.901 TONNES FROM THE GLD ///INVENTORY RESTS AT 866.50TONNES

FEB 12 WITH GOLD DOWN $3,40ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 10 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 7 WITH GOLD UP $10.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 864.19 TONNES

FEB 6 WITH GOLD DOWN $18.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.14 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

FEB 5 WITH GOLD UP $27.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 863.05 TONNES

FEB 4 WITH GOLD UP $25.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.58 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.77 TONNES

JAN 31 WITH GOLD UP $4.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 30 WITH GOLD UP $40.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 865.34 TONNES

JAN 29 WITH GOLD DOWN $6.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 4.02 TONNES OF GOLD INTO THE THE GLD ///INVENTORY RESTS AT 861.04 TONNES

JAN 28 WITH GOLD UP $23.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.16 TONNES OF GOLD OUT OF THE GLD //

JAN 27 WITH GOLD DOWN $36.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///

JAN 24 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 5.17 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 864.19 TONNES

JAN 23 WITH GOLD DOWN $1.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 2.30 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 869.36 TONNES

JAN 22 WITH GOLD UP $15.15 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 7.46 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 871.66 TONNES

JAN 20 WITH GOLD UP $35.30 ON THE DAY; MEGA HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 10.34 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 879.12 TONNES

GLD INVENTORY: 900.30 TONNES, TONIGHTS TOTAL

SILVER

MARCH 6 WITH SILVER UP 16 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.455 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.046 MILLION

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 12WITH SILVER UP $.01 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 8 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

FEB 10 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 7 WITH SILVER DOWN $0.26 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.73 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 428.66 MILLION OZ

FEB 6 WITH SILVER DOWN $0.17 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 12.383 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 430.39 MILLION OZ

FEB 5 WITH SILVER UP $0.45 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 3.285 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 442.773 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 4 WITH SILVER UP $0.81 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

FEB 3 WITH SILVER UP ONE CENT //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.550 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 446.331 MILLION OZ

JAN 31 WITH SILVER DOWN $0.19 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.369 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 448.881 MILLION OZ

jAN 30 WITH SILVER UP $0.76 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 2.003 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 451.249 MILLION OZ

jAN 29 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.639 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 453.252 MILLION OZ

jAN 28 WITH SILVER UP $0.34 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.821 MILLION OZ OUT OF THE SLV./. /

jAN 27 WITH SILVER DOWN $.61 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 24 WITH SILVER DOWN $.21 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 1.64 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 457.395 MILLION OZ

JAN 23 WITH SILVER DOWN $.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A MASSIVE WITHDRAWAL OF 4.738 MILLION OZ OUT OF THE SLV./. //INVENTORY AT SLV RESTS AT 459.035 MILLION OZ

JAN 22 WITH SILVER UP $.08 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 0.721 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 464.043 MILLION OZ

JAN 20 WITH SILVER DOWN $.09 //NO CHANGES IN SILVER INVENTORY AT THE SLV : A WITHDRAWAL OF 1.568 MILLION OZ FROM THE SLV./. //INVENTORY AT SLV RESTS AT 463.315 MILLION OZ

CLOSING INVENTORY 436.046 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

Alasdair Macleod..

A new financial crisis looms

The hope that in the face of weakening economies interest rates and bond yields will decline is wrong. They are still rising in the Eurozone and Japan, leading to a new wave of financial instability.

| Alasdair MacleodMar 6∙Paid |

Over the last ninety years there has been a growing belief held by macroeconomists and investment strategists that interest rates and bond yields are under the control of central bank monetary policies.

It has its origins in the Keynesian-inspired role of governments using deficit spending and interest rates to stimulate economic activity when the private sector suffers a downturn. However, this is one of the fundamental errors of macroeconomic beliefs as we are about to find out.

Before then and particularly before interventionist Presidents Hoover and Roosevelt, politicians knew not to interfere in the event of a slump for fear of making it worse. They, and currency-issuing central banks had learned that the role of interest rates was to manage the currency, not the economy. In those days higher interest rates would prevent a run on gold reserves, allowing credit in the form of gold substitutes to maintain their value both internationally and domestically.

We see evidence that what was true under gold standards still applies to fiat currency relationships today. Interest rates are the primary influence on exchange rates. In January 2021, as US interest rates rose from the zero bound the dollar’s trade weighted index rose from 90 to 113 while rates in other currencies remained supressed. And when they began to reflect the inevitable, the dollar backed off, consolidating in the 100—110 range.

But still, the lessons of the role of interest rates remain ignored by the mainstream. Let’s try another approach by posing a question: if credit has a greater risk of losing purchasing power, what should happen to interest rates?

The answer should be obvious: unless rates rise to compensate for the greater risk, then the value of the credit will decline. Obvious maybe, but it flies in the face of central bank policy, which persists in using interest rates in attempts to manage economic outcomes.

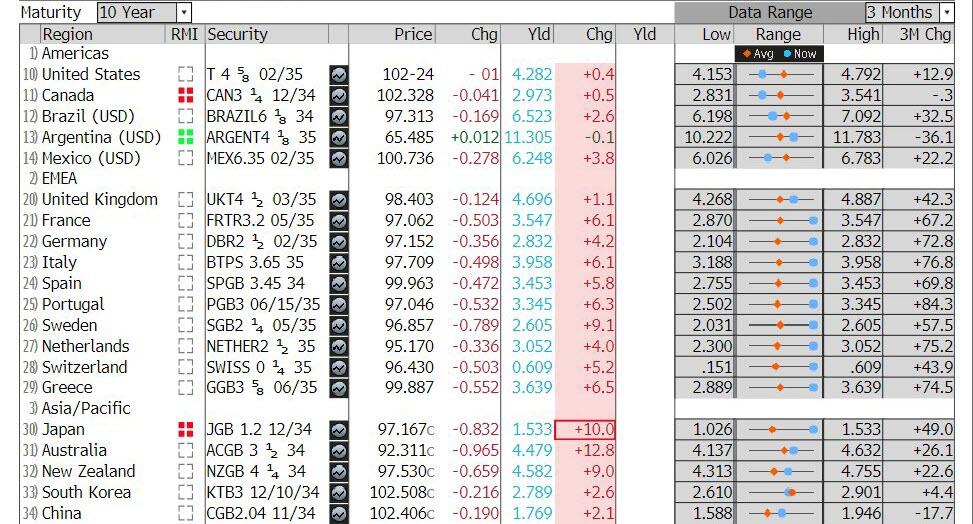

Only this week we see the true role of interest rates and bond yields being proved yet again. The background is one of increasing evidence of a US economy stalling, and expectations of a declining Fed Funds Rate to support the economy gaining momentum. At the same time, the new German chancellor proposes to relax borrowing rules to accommodate higher defence spending and to establish an off-budget €500 billion defence fund — proposals together with a further €800 billion promised by Ursula von der Leyen which are already leading to significantly higher eurobond yields. The immediate consequences for the euro and the dollar’s TWI are shown below.

The inflationary implications are also reflected in the 10-year German bund yield, which has simply soared:

As the marker for other eurozone bond markets, Germany’s bund yields have driven all the others higher. And in the case of France’s, highly exposed Japanese investors will be suffering heavy losses in addition to their losses in their own JGBs:

Round One of the bond market crisis was the unexpected rise in US bond yields between 2020—2022, leading to the failure of some regional banks. Round Two is kicking off in the Eurozone and Japan, which is set to create a second banking crisis outside America originating in the Eurozone and Japan.

Returning to the US dollar, these growing bond yield differentials appear to be only just starting to undermine the dollar’s TWI. Yet, as I have pointed out in earlier articles, the US private sector’s GDP adjusted for the contribution of the budget deficit is not growing by 4.5% as the Congressional Budget Office expects but is actually contracting by 2% in nominal terms. Add in the CBO’s forecast of inflationary debasement at 2.9%, and the private sector is already in a 5% slump. And due to Trump’s tariffs, it’s getting even worse for the US economy and those of other nations.

These negative outlooks for the US economy and the dollar are bound to be reflected in higher dollar prices for gold, silver, and the entire commodity complex. Why? because the Fed is likely to keep interest rates suppressed in a vain attempt to stave off economic decline.

But it is worse than that. A contracting private sector GDP rapidly raises government debt to GDP, and by definition intensifies the debt trap. In short, the entire financial system is becoming demonstrably unstable. That is the clear message from the last few days.

So, what do you do? Get out of risky credit and into the safety of real, legal money which is gold!

end

this is gold used to satisfy demand from central bank buying of physical

(zerohedge)

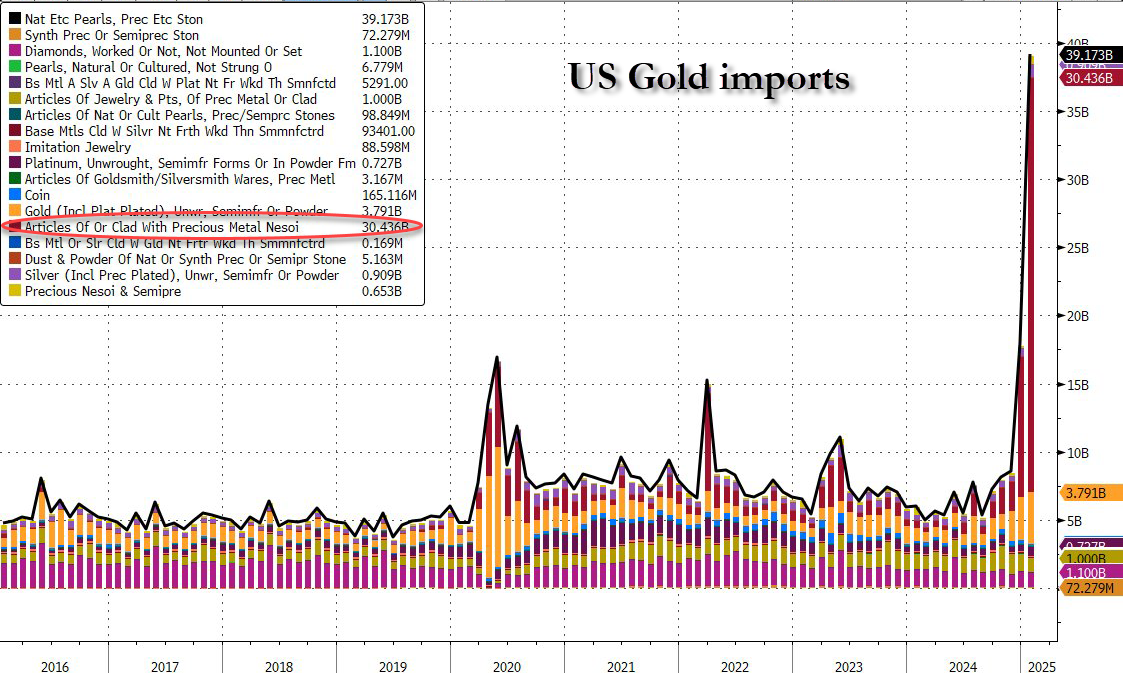

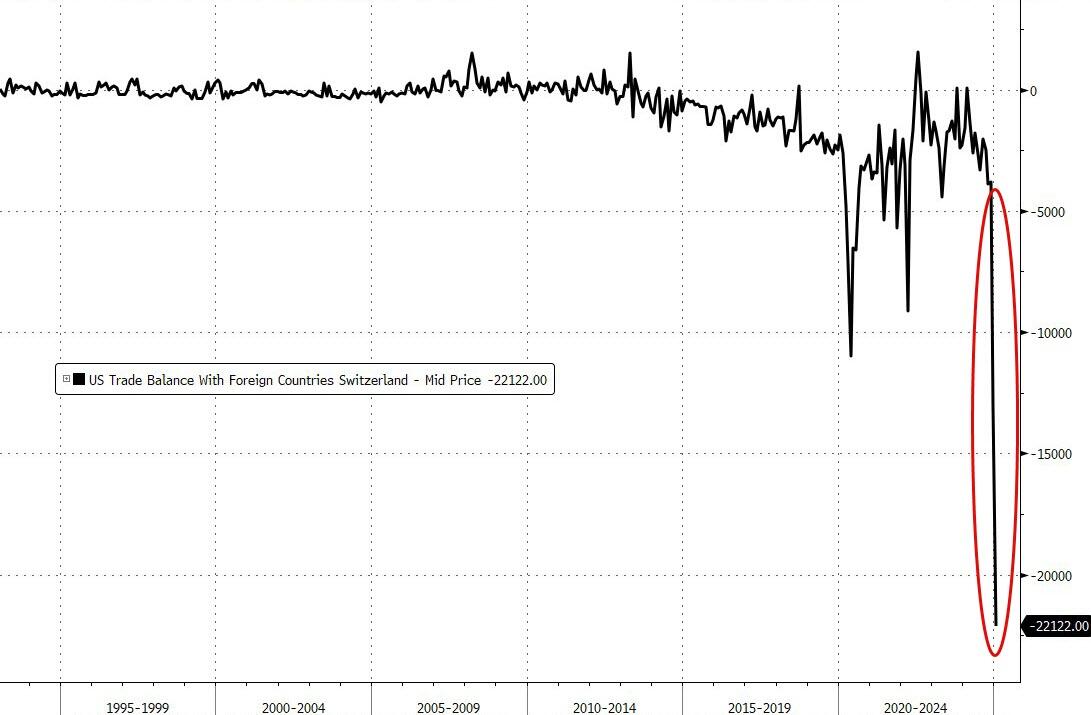

Unprecedented Surge In Swiss Bullion Imports Sends US Trade Deficit To Record High In January

Thursday, Mar 06, 2025 – 08:51 AM

The US trade deficit widened to a record in January as companies scrambled to secure goods from overseas before President Donald Trump imposed tariffs on America’s largest trading partners.

The gap in goods and services trade widened 34% from the prior month to $131.4 billion, Commerce Department data showed Thursday. The deficit was larger than all but one estimate in a Bloomberg survey of economists.

Source: Bloomberg

The value of imports rose 10% to a record $401.2 billion, while exports increased 1.2%. The figures aren’t adjusted for inflation.

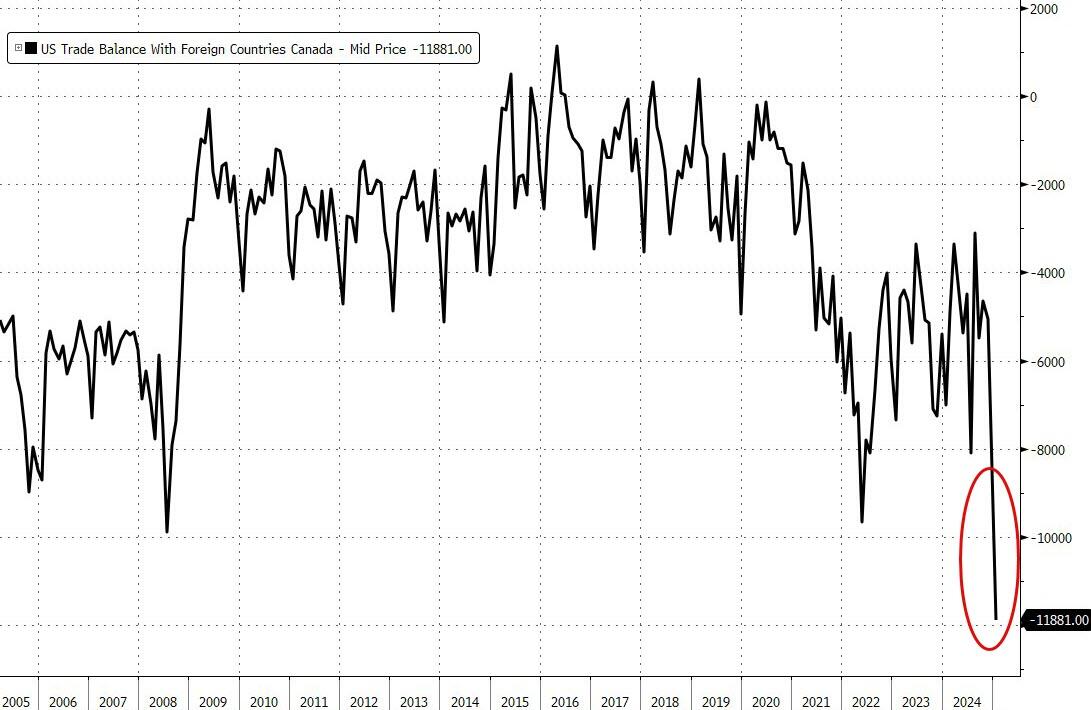

Canada’s trade surplus with the US jumped to a record at the start of the year, driven by exports of cars, auto parts and oil, separate data from Statistics Canada showed Thursday.

But, perhaps most notably, the January flurry of imports was broad and included a surge in inbound shipments of industrial supplies and materials.

Within that category, imports of finished metal shapes that include gold bullion jumped $20.5 billion, marking a a second month of steep increases.

For an even clearer picture of the magnitude of the shift in bullion imports, we note that the Swiss trade deficit (where all that bullion is coming from) rocketed higher (an order of magnitude from historical norms)…

As we detailed here, while everyone has been distracted by talk of the tariff-driven arbitrage between COMEX and LBMA (London)…

…it appears Americans have been buying bullion direct from the Swiss.

Furthermore, with tariffs now in place, the ‘front-running’ is over and the trade balances (imports) will adjust accordingly.

3 CHRIS POWELL AND GATA DISPATCHES

Chris Powell…

In interview at PDAC, Eric Sprott forces Kitco to mention market manipulation

Submitted by admin on Wed, 2025-03-05 12:10 Section: Daily Dispatches

12:08p ET Wednesday, March 5, 2025

Dear Friend of GATA and Gold (and Silver):

In an interview conducted during the PDAC conference in Toronto this week, mining entrepreneur Eric Sprott pushed silver market manipulation onto the Kitco internet site, which long has been suppressing the price-suppression issue. Silver’s price has been manipulated for 50 years, Sprott says, and gold and silver mining company shares are very undervalued. He thinks the silver price could exceed $50 soon.

The interview with Sprott is 18 minutes and can be viewed at Kitco here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Gold payments for oil suspended by Ghana’s central bank chief

Submitted by admin on Tue, 2025-03-04 21:58 Section: Daily Dispatches

By Ekow Dontoh, Moses Mozart Dzawu, and Ondiro Oganga

Bloomberg News

Sunday, March 2, 2025

Ghana’s new central bank chief has suspended the West African nation’s program of paying for oil with gold and said he expects the cedi to stabilize after its volatility of last year.

“We intend to maintain an appropriate monetary policy stance,” Bank of Ghana Governor Johnson Asiama said in an interview on Friday. Together with commitments for fiscal discipline under the administration of President John Mahama, that “should help us maintain stability in the foreign exchange markets,” he said.

With interest rates at 27% and inflation easing to 23.5% in January, Asiama said better monetary and fiscal policy coordination should help cool price pressures as the country puts the economic trauma of its 2022 debt default behind it. Africa’s biggest gold producer had to seek a $3 billion bailout from the International Monetary Fund and restructure its debt after defaulting on its obligations.

… For the remainder of the report:

end

Deutsche Bank sees risk of U.S. dollar losing safe-haven status

Submitted by admin on Tue, 2025-03-04 16:00 Section: Daily Dispatches

From Bloomberg News

Tuesday, March 3, 2025

The U.S. dollar may lose its traditional safe-haven status as global markets adjust to a new geopolitical order, according to Deutsche Bank AG.

“We do not write this lightly. But the speed and scale of global shifts are so rapid that this needs to be acknowledged as a possibility,” said George Saravelos, the bank’s global head of FX strategy, in a note to clients. “It is hard to overestimate the scale of change taking place in global economic and geopolitical relations in a matter of days.”

Deutsche Bank’s concerns follow a slump on the dollar on Tuesday that has caught out investors betting on further strength. A broad gauge of the greenback fell as much as 0.7% even as the U.S. moved forward with tariffs on its main trading partners, which many viewed as likely to bolster the currency.

“What stands out in today’s market reaction is that the dollar is not strengthening materially,” Saravelos wrote. “We would not have expected these market moves at the start of the year.” …

… For the remainder of the report:

end

4 ANDREW MAGUIRE/LIVE FROM THE VAULT NO 212//ANDREW MAGUIRE INTERVIEWING DR DANIEL LACALLE

Kinesis.money/live-from-the-vault/trump-expose-feds-gold-coverup/

Episode 212

Posted 28th February 2025

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY//EGGS

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING WEDNESDAY MORNING TUESDAY NIGHT

SHANGHAI CLOSED UP 39.13 PTS OR 0.17%

//Hang Seng CLOSED UP 775.50 PTS OR 3.29%

// Nikkei CLOSED UP 286,64 OR 0.77%//Australia’s all ordinaries CLOSED DOWN .44%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2481 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2482/ Oil UP TO 66.81 dollars per barrel for WTI and BRENT DOWN TO 69.73 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.2481

OFFSHORE YUAN: DOWN TO 7.2482

SHANGHAI CLOSED CLOSED UP 39.13 PTS OR 1.17%

HANG SENG CLOSED CLOSED UP 775.50 PTS OR 3.29%

2. Nikkei closed UP 286.64 OR 0.77%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 104.055// EURO RISES TO 1.0800 UP 7 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: RISES TO. +1.501//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.69…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.859/Italian 10 Yr bond yield UP to 3.923 SPAIN 10 YR BOND YIELD UP TO 3.518

3i Greek 10 year bond yield UP TO 3.660

3j Gold at $2901.20 Silver at: 32.13 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 9 /100 roubles/dollar; ROUBLE AT 89.21

3m oil into the 66 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.69 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.501 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8849 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9558 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.310 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.611 UP 5 BASIS PTS/

USA 2 YR BOND YIELD: 3.998 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 36.44…

10 YR UK BOND YIELD: 4.7815 UP 8 PTS

10 YR CANADA BOND YIELD: 3.017 UP 5 BASIS PTS

5 YR CANADA BOND YIELD: 2.670 UP 3 PTS.

2a New York OPENING REPORT

Futures Plunge As German Bond Rout Goes Gl

Thursday, Mar 06, 2025 – 08:20 AM

Futures tumble, led by Tech as the world is hammered by soaring yields from Europe to Japan. As of 8:00am ET, S&P futures are down 1.1%, and Nasdaq futures plunged 1.4% as Marvell Technology shares were among the biggest premarket losers, dropping about 15%, after the chipmaker’s result and revenue forecast failed to live up to investors’ lofty expectations. MongoDB Inc. dropped 17% after the database software company gave a disappointing forecast. Mag 7 underperform: NVDA (-1.8%), TSLA (-1.6%) and META (-1.5%) pre-market. 10y yields are +2bps higher while 2y is -1.5bp lower this morning but the move is nothing compared to Germany where yields earlier soared as much as 15bps (they have since retraced much of the move) extending yesterday’s record rout; the USD plunge continues, just as Bessent wanted, with the rest of the world about to find out what soared trade deficits really mean. Commodities are mixed: oil saw small gains (+0.5%) after yesterday’s selloff; basic metals are rallying this morning, while precious metals are lower. Since yesterday’s close, the equity weakness was not contributed by single catalyst but more due to a number of macro uncertainties (the auto tariffs delay will not resolve the tariffs risks; more evidence of sentiment impacts from Beige book) and rotation to international stocks. Today, we will hear from AVGO on AI outlooks; MRVL fell -15% post earnings release yesterday (after-market) despite numbers are mostly in line with expectation.

In premarket trading, Tesla and Nvidia fall more than 2% are leading premarket losses among the Magnificent Seven stocks on Thursday. Amazon, Microsoft, Alphabet, Meta and Apple fall less than 1%. Burlington Stores (BURL US) shares rise 14% in premarket trading after the retailer reported fourth-quarter comparable sales and profit that topped Wall Street expectations. Still, its annual forecasts fell short, with Chief Executive Officer Michael O’Sullivan saying the outlook for 2025 is “very uncertain.” Here are the other notable premarket movers:

- ALX Oncology (ALXO US) shares rise 13% in premarket trading after Jefferies upgraded the drug developer to buy from hold, citing “limited theoretical downside.”

- CoreCivic Inc. (TH US) will resume operations at the South Texas Residential Center under an amended intergovernmental services agreement (IGSA).

- JD.com ADRs (JD US) jump as much as 11% in premarket trading on Thursday after the Chinese e-commerce firm reported net revenue for the fourth quarter that beat the average analyst estimate. Peers PDD Holdings climbs 4.4% and Alibaba Group rises 3.8%. .

- MongoDB shares (MDB US) are down 18% in premarket trading Thursday, after the database software company gave a full-year forecast that is weaker than expected.

- ON Semiconductor (ON US) analysts are generally positive on the company’s bid to buy Allegro Microsystems (ALGM US), seeing synergies between the two, though some questioned the offer price, which values the company at $6.9 billion including debt.

- Shares of ECARX Holdings (ECX US), a mobility technology provider, are up 9.1% in premarket trading after the company said it won an award to provide Volkswagen and Skoda with digital cockpit solutions.

- Victoria’s Secret (VSCO US) shares fall as much as 2.7% in US premarket trading after the lingerie retailer’s forecasts for the first quarter and for the full year fell short of analyst expectations with the company citing an uncertain backdrop and shift in consumer confidence. Analysts at BMO and JPMorgan cut their price targets on the stock.

Chip shares came under renewed pressure after Alibaba Group Holding Ltd. introduced its Qwen platform, a model that it claims performs as well as Chinese start-up DeepSeek but with a fraction of the data. The news, alongside the underwhelming earnings, are denting investor confidence in US companies’ dominance in AI.

“Clearly Alibaba is weighing on sentiment,” said Alexandre Hezez, chief investment officer at Group Richelieu in Paris. “The tech sector has been weakened lately, if you combine that with Marvell, it’s a pretty sour cocktail for US stocks”

Europe’s Stoxx 600 index slipped 0.6%, as real estate and consumer product names underperform, reacting to sharply higher bond yields across the continent, following Germany’s announcement earlier this week that it would deploy hundreds of billions of euros in additional spending. Indeed, German government bonds fall again, extending their worst daily drop since 1990 and pushing 10-year yields up another 6 bps to 2.85%. And this time the selling has spilled over across Europe and is also hammering Japan.