GOLD CLOSED UP $3.05 TO $3036.00

SILVER CLOSED DOWN $0.15 TO $33.41

GOLD ACCESS CLOSED 3045.00

Silver ACCESS CLOSED: $33.53

Bitcoin morning price:$83,194 DOWN 440 DOLLARS.

Bitcoin: afternoon price: $84,332 UP 698 DOLLARS

Platinum price closing DOWN $10.35 TO $986.25

Palladium price; DOWN $9.75 TO $950.20

END

*CANADIAN GOLD: $4358.80 DOWN 3.00 CDN dollars per oz( * NEW ALL TIME HIGH 4361.64- CDN DOLLARS PER OZ//MARCH 19 2025)

*BRITISH GOLD: 2344.11 UP 1.31 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,343.17 BRITISH POUNDS/OZ) MARCH 19/2025

*EURO GOLD: 2,805.95UP 10.83Euros per oz //* (ALL TIME CLOSING HIGH: 2,819,78UROS PER OZ/FEB 24 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,035.900000000 USD

INTENT DATE: 03/19/2025 DELIVERY DATE: 03/21/2025

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 100

118 H MACQUARIE FUT 33

323 C HSBC 100

357 C WEDBUSH 25

363 H WELLS FARGO SEC 133

435 H SCOTIA CAPITAL 1

523 C INTERACTIVE BRO 2

523 H INTERACTIVE BRO 1

624 H BOFA SECURITIES 33

661 C JP MORGAN 31

686 C STONEX FINANCIA 73 54

709 C BARCLAYS 5

726 C PLUS500US FINAN 1

737 C ADVANTAGE 1 3

905 C ADM 8

TOTAL: 302 302

JPMORGAN stopped 31/302 contracts

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2024. CONTRACT: 302 NOTICES FOR 30,200 OZ 0.9393 TONNES

total notices so far: 17,870 contracts for 1,787,000 Oz (55.583 tonnes)

FOR MARCH

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 195 NOTICE(S) FILED FOR 0.975 MILLION OZ/

total number of notices filed so far this month : 14,934 for 74.670 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $3.05 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 909,28 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $.15 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV:

CLOSING INVENTORY

CLOSING INVENTORY: 444.054 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 1159 CONTRACTS TO 169,407 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS OF $0,45 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A HUMONGOUS LOSS OF 1159 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR SMALL LOSS IN PRICE//WEDNESDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON WEDNESDAY COMEX TRADING / AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED SLIGHTLY ON WEDNESDAY WITH SILVER’S SMALL LOSS IN PRICE. WE HAD A HUGE T.A.S. LIQUIDATION WEDNEDAY. BUT THIS WAS COUPLED WITH ANOTHER HUGE T.A.S. ISSUANCE OF 847 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS METALS WILL COMMENCE AGAIN! WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND 57 CENTS AND A LEASE RATE OF 7.3%. WE HAD A 0 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 847 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TODAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUMONGOUS 1159 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR SMALL LOSS IN PRICE. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT WEDNESDAY’S COMEX TRADING SESSION WHICH ACCOUNTS FOR A HUGE PORTION IN THE LOSS OF OI ON OUR TWO EXCHANGES.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.00 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE 847 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.45 AND WERE SUCCESSFUL IN KNOCKING OFF SOME NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS LOSS IN OUR TWO EXCHANGES OF 1079 CONTRACTS WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS TRYING TO CONTAIN SILVER’S PRICE RISE AND THAT ACCOUNTS FOR LOTS OF OUR OPEN INTEREST FALL. HOWEVER THE CME NOTIFIED US THAT FOR THE FIRST TIME IN MARCH, WE HAVE BEEN ISSUED 70 CONTRACTS OF EXCHANGE FOR RISK FOR 350,000 OZ. THIS TOTAL WILL BE ADDED TO OUR REGULAR DELIVERY TOTALS FOR MARCH.

WE HAD A 0 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 78.753 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0.430 MILLION OZ QUEUE JUMP TO WHICH WE ADD .350 EXCHANGE FOR RISK

INITIAL STANDING FOR MARCH ADVANCES TO 80.800 MILLION OZ

WE HAD:

/ HUMONGOUS COMEX OI LOSS+// A ZERO SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 847 CONTRACTS)/A 70 CONTRACT EX. FOR RISK FOR 350,000 OZ/SECOND WEEK OF MARCH

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 80 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR

TOTAL CONTRACTS for 13 DAYS, total 8604 contracts: OR 43.020 MILLION OZ (662 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 43.020 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 43.020 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1159 CONTRACTS WITH OUR LOSS IN PRICE OF 45 CENTS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG 860 CONTRACT EFP ISSUANCE CONTRACTS: 860 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH OF 78.455 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 0.430 MILLION OZ QUEUE JUMP//NEW STANDING ADVANCES TO 80.450 MILLION OZ + .350 EX. FOR RISK//NEW TOTAL 80.800 MILLION OZ.

WE HAVE 1). A HUMONGOUS SIZED LOSS OF 1159 OI CONTRACTS ON THE TWO EXCHANGES DESPITE OUR LOSS IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 847 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION. HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON WEDNESDAY WITH OUR LOSS IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (847 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 195 NOTICE(S) FILED TODAY FOR 0.975 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 4270 OI CONTRACTS TO 537,836 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE SIZED 924 CONTRACTS//

WE HAD A STRONG SIZED INCREASE IN COMEX OI (4270 CONTRACTS) OCCURRED WITH OUR SMALL GAIN OF $0.40 IN PRICE TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 31.757 TONNES FOLLOWED BY TODAY’S STRONG 7400 OZ QUEUE JUMP (0.2302 TONNES), ////NEW STANDING ADVANCES TO 57.511 TONNES + .4655 TONNES EX FOR RISK/PRIOR = 57.9775 TONNES

/NEW STANDING FOR MARCH; 57.511 TONNES + .4655 TONNES EX FOR RISK/PRIOR = 57.9775 TONNES.

/ ALL OF THIS HAPPENED WITH OUR $0.40 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX ///. WE HAD A STRONG SIZED GAIN OF 5420 OI CONTRACTS (16.85 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE FRONT MARCH CONTRACT MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1150 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 537,836

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5420 CONTRACTS WITH 4270 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 1150 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5420 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1489 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1150 CONTRACTS) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 4270 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5420 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH 31.757 TONNES FOLLOWED BY TODAY’S 0.2302 TONNES QUEUE JUMP. TO WHICH WE MUST ADD OUR NEW .4655 TONNES OF EX FOR RISK/PRIOR

//NEW STANDING ADVANCES TO 57.511 TONNES + .4655 TONNES EX FOR RISK = 57.9775 TONNES

//NEW STANDING MARCH: 57.9775 TONNES

.

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE TUESDAY WITH ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WE HAD 1) $0.40 PRICE GAIN AND WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG GAIN OF 5420 CONTRACTS ON OUR TWO EXCHANGES ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN MARCH. ALL OF THE GAIN IN OI WAS DUE TO THE HUGE NUMBER OF T.A.S. LIQUIDATION WEDNESDAY.

4) STRONG SIZED COMEX OPEN INTEREST INCREASE 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1489 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH :

TOTAL EFP CONTRACTS ISSUED: 26,463 CONTRACTS OF 2,646,300 OZ OR 82.31 TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 2035 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES 82.31 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 82.31 DIVIDED BY 3550 x 100% TONNES = 2.30% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 82.31 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUMONGOUS SIZED 1159 CONTRACTS OI TO 169,407 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 0 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 0 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1079 CONTRACTS AND ADD TO THE 0 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1079 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 5.395 MILLION OZ OCCURRED DESPITE OUR SMALL $0.40 IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 17.48 PTS OR 0.51%

//Hang Seng CLOSED DOWN 551.19 PTS OR 2.23%

// Nikkei CLOSED HOLIDAY%//Australia’s all ordinaries CLOSED UP 1.16%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2428 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2488/ Oil UP TO 67.38 dollars per barrel for WTI and BRENT UP TO 70.87 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

END

END

END

ASIA TRADING THURSDAY MORNING/WEDNESDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 4270 CONTRACTS TO 537,836 DESPITE OUR VERY TINY GAIN IN PRICE OF $0.40 WITH RESPECT TO WEDNESDAY’S TRADING/. WE LOST ZERO NET LONGS WITH THAT PRICE GAIN FOR GOLD. BUT AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1150 ).

THE CME ANNOUNCED WEDNESDAY NIGHT, 0 EXCHANGE FOR RISK CONTRACTS FOR NIL OZ OR NIL TONNES. LAST THURSDAY WAS THE FIRST ISSUANCE FOR MARCH FOR .4665 TONNES

IN FEBRUARY: WE HAD FIVE EXCHANGE FOR RISKS IN GOLD, TOTALLING 18.4527 TONNES!. THE RECIPIENT OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY.

THUS IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 5420 CONTRACTS WITH OUR GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF MARCH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY TODAY INCLUDING WITH OUR HUMONGOUS T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION// THROUGHOUT THE WEEK. THEY ISSUED LAST NIGHT A FAIR SIZED 1489 CONTRACT THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING A LOWER COMEX OPEN INTEREST GAINS BUT THIS IS COUPLED WITH HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WEDNESDAY.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, , 203 , ,205 , 207 209 AND 211 212 213 AND FRIDAY’S 214 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF MARCH .… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1150 EFP CONTRACTS WERE ISSUED: : /APRIL 1680 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1150 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5420 CONTRACTS IN THAT 1150 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD GAIN OF 4270 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR VERY TINY GAIN IN PRICE OF $0.40 FOR WEDNESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A FAIR SIZED 1489 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER 4 WEEKS AGO AND AGAIN LAST WEEK,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND NOW ,THIS MONTH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT LAST WEDNESDAY’S 38,393 T.A.S. CONTRACT ISSUANCE IS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY DOES TWO IMPORTANT THINGS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES.THIS IS THE FIRST TIME IN COMEX HISTORY THAT WE WILL HAVE THREE CONSECUTIVE MONTHS OF MEGA HUGE T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: MARCH (57.9775 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE MARCH DELIVERY MONTH / FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH.

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

AND NOW MARCH:

STANDING FOR GOLD : 57.511 TONNES + .4665 TONNES EX FOR RISK = 57.9775 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES.

MARCH: 57.9775 TONNES (INCLUDES .4665 TONNES EX FOR RISK)

COMEX GOLD TRADING/MARCH CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $0.40/)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A GOOD SIZED GAIN IN OUR TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION WEDNESDAY/PRIOR TO FOMC AS THEY WERE TRYING TO QUELL GOLD’S ATTEMPT AT $3,000 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING AND THEY FAILED MISERABLY AS GOLD IS NOW WELL ABOVE THE $3,000 THRESHOLD!!.

LAST NIGHT/THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH MARCH TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WILL NOW BE ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FOR FRIDAY FEB 28 ZERO EXCHANGE FOR RISK WAS ISSUED.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND IS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WILL BE ADDED TO TODAY’S NORMAL DELIVERY TOTAL.

TOTAL INITIAL DELIVERIES MARCH GOLD TRADING

MARCH: 57.511 TONNES + .46556 TONNES EX FOR RISK = 57.9775 TONNES

WE HAVE GAINED A STRONG SIZED TOTAL OF 16.85 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH (31.753TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 7,400 OZ OR 0.2302 TONNES: NEW TOTAL STANDING 57.511 TONNES TO WHICH WE ADD OUR .4665 TONNES OF EXCHANGE FOR RISK//NEW TOTAL: 57.9775 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR VERY TINY GAIN IN PRICE TO THE TUNE OF $0.40

WE HAD 924 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 5420 CONTRACTS OR 542,000 0Z (16.85 TONNES)

confirmed volume WEDNESDAY 170,945 contracts: fair///

//speculators have left the gold arena

END

MARCH

// THE MARCH 2025 GOLD CONTRACT

MARCH 20

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES nil . |

| Deposit to the Dealer Inventory in oz | 1 entries: dealer deposits: 1 i) into Manfra dealer 9645.000 oz 300 kilobars weight .300 tonnes |

| Deposits to the Customer Inventory, in oz | we have 1 customer entry Deposits customer we have one customer deposit i)Into Brinks 138,249.254 oz or 4300 kilobars weight 4.3 tonnes total weight dealer and customer 4.7 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 302 notice(s) 30200 OZ 0.9393 TONNES |

| No of oz to be served (notices) | 620 contracts 62000 OZ 1.928 TONNES |

| Total monthly oz gold served (contracts) so far this month | 17870 notices 1,787,000 oz 55.583 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

:

dealer deposits: 1

i) into Manfra dealer 9,645.000 oz

300 kilobars

weight .300 tonnes

xxxxxxxxxxxxxxxxxxxxx

deposits customer

we have one customer deposit

i)Into Brinks 138,249.254 oz or 4300 kilobars

weight 4.3 tonnes

total weight dealer and customer 4.7 tonnes

xxxxxxxxxxxxxxxxI

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 0

xxxxxxxxxxxxxxxxxx

adjustments: customer to dealer:

i)Brinks 53,049.150 oz

AMOUNT OF GOLD STANDING FOR MARCH

THE FRONT MONTH OF MARCH HAD A LOSS OF 87 CONTRACTS TO STAND AT 922. WE HAD 161 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 74 CONTRACTS FOR 7400 OZ (.2302 TONNES AS A PHYSICAL GOLD QUEUE JUMP. THIS IS CENTRAL BANKS LOOKING FOR BADLY NEEDED GOLD

APRIL HAD A LOSS OF 701 CONTRACTS UP TO 252,422 CONTRACTS AS THIS MONTH BECOMES THE FRONT MONTH. APRIL IS STILL QUITE LOFTY AND NO DOUBT WE WILL HAVE A HUMONGOUS AMOUNT OF GOLD STANDING FOR THE APRIL DELIVERY MONTH!

MAY GAINED 102 CONTRACTS UP TO 1264.

We had 302 contracts filed for today representing 30,200oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 302 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 31 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MARCH /2025. contract month, we take the total number of notices filed so far for the month (17,870 X 100 oz ) to which we add the difference between the open interest for the front month of MARCH (922 CONTRACTS) minus the number of notices served upon today (305 x 100 oz per contract) equals 1,849,000 OZ OR 57.511 TONNES to which we add our .4665 tonnes exchange for risk//new total tonnage standing: 57.9775 tonnes

thus the INITIAL standings for gold for the MARCH contract month: No of notices filed so far (17,870x 100 oz +we add the difference for front month of MARCH (922 OI} minus the number of notices served upon today (302 x 100 oz) which equals 1,849,000 OZ OR 57.511 TONNES + .4665 ex for risk //new total 57.9775 tonnes

TOTAL COMEX GOLD STANDING FOR MARCH.: 57.9775 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND MARCH IS FOLLOWING SUIT..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,979,834.722oz 61.88 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 41,594,745.805.oz

TOTAL REGISTERED GOLD 20,834,059,03 or 648.02 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 20,760,686.775 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 18,8542,25oz (REG GOLD- PLEDGED GOLD)= 586.44tonnes //

END

SILVER/COMEX

// THE MARCH 2025 SILVER CONTRACT//INITIAL

MARCH 20

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries i) out of Loomis; 606,936.690 oz |

| Deposits to the Dealer Inventory | 2 entries i) Into Brinks dealer 304,488.800 oz ii) Into Manfra dealer: 523,384.361 oz total dealer 827,872.963 oz |

| Deposits to the Customer Inventory | 5 entries 5entries i) Into Asahi 610,472.650 oz ii) Into Brinks 512,873,741 oz iii) Into JPMorgan 1182,109.3000 oz iv) Into Loomis 310,061.520 oz v) Into Manfra 579,138.600 oz total weight 3194,659.811 oz |

| No of oz served today (contracts) | 195 CONTRACT(S) (0.975 MILLION OZ |

| No of oz to be served (notices) | 1156 contracts (5.780 MILLION oz) |

| Total monthly oz silver served (contracts) | 14,934 Contracts (74.670 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 2 entries

i) Into Brinks dealer 304,488.800 oz

ii) Into Manfra dealer: 523,384.361 oz

total dealer 827,872.963 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

5 entries

5entries

i) Into Asahi 610,472.650 oz

ii) Into Brinks 512,873,741 oz

iii) Into JPMorgan 1182,109.3000 oz

iv) Into Loomis 310,061.520 oz

v) Into Manfra 579,138.600 oz

total weight 3194,659.811 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals 1

1 entry

entries

i) out of Loomis; 606,936.690 oz

total withdrawal 606,936.690 oz

xxx

ADJUSTMENTs 1

customer to dealer:

a) Delaware 133,018.684 oz

JPMorgan has a total silver weight: 181.989million oz/456,485oz million or 39.86%

TOTAL REGISTERED SILVER: 153.428 MILLION OZ//.TOTAL REG + ELIGIBLE. 456,485Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH /2025 OI: 1351 OPEN INTEREST CONTRACTS FOR A LOSS OF 233 CONTRACTS.WE HAD 319 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 86 CONTRACTS OR 0.430 MILLION OZ UNDERWENT A STRONG QUEUE JUMP LOOKING FOR METAL OVER ON THIS SIDE OF THE POND. WE MUST NOW ADD THAT CRAZY 70 CONTRACT EX FOR RISK/PRIOR FOR 350,000 OZ. THE BANK OF ENGLAND OR ANOTHER OFFICIAL ENTITY IS ASSUMING THE RISK OF DELIVERY AND THE COUNTERPARTY ARE BULLION BANKS WHO CANNOT GUARANTEE DELIVERY.

APRIL SAW ANOTHER LOSS OF 18 CONTRACTS TO STAND AT 2382

MAY SAW A LOSS OF 1116 CONTRACTS DOWN TO 128,154 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 195 or 0.975 MILLION oz

CONFIRMED volume; ON WEDNESDAY 66,278 small//

AND NOW MARCH DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 14,934 X5,000 oz = 74.670 MILLION oz

to which we add the difference between the open interest for the front month of MAR (1351) AND the number of notices served upon today (195 )x (5000 oz)

Thus the standings for silver for the MARCH 2025 contract month: (14,934) Notices served so far) x 5000 oz + OI for the front month of MAR(1351) minus number of notices served upon today (195)x 5000 oz equals silver standing for the MARCH contract month equating to 80.450 MILLION OZ TO WHICH WE ADD .350 MILLION OZ EX FOR RISK//NEW TOTAL 80.800 MILLION OZ//

New total standing: 80.800 million oz which is huge for this very active delivery month of March.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 151.518million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

MARCH 20 WITH GOLD UP $3.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 909.28 TONNES

MARCH 19 WITH GOLD UP $0.45 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 907.27 TONNES

MARCH 18 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 907.27 TONNE

MARCH 17 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.64 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 906.41 TONNES

MARCH 14 WITH GOLD UP $9.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MONSTER DEPOSIT OF 7.17 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 905.81 TONNES

MARCH 13 WITH GOLD UP $42.85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 12 WITH GOLD UP $22.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.90 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 895.20 TONNES

MARCH 11 WITH GOLD UP $21.20 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 891.30 TONNES

MARCH 10 WITH GOLD DOWN $12.45 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 894.317 TONNES

MARCH 7 WITH GOLD DOWN $12.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 6 WITH GOLD UP $2.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 900.30 TONNES

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

GLD INVENTORY: 909.28 TONNES, TONIGHTS TOTAL

SILVER

MARCH 20 WITH SILVER DOWN $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 19 WITH SILVER DOWN $0.45 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.219 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 18 WITH SILVER UP $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.823 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.373 MILLION

MARCH 17 WITH SILVER UP $0.03 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.096 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 439.550 MILLION

MARCH 14 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.910 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.454 MILLION

MARCH 13 WITH SILVER UP $0.46 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.774 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 434.544 MILLION

MARCH 12 WITH SILVER UP $0.57 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.032 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 435.318 MILLION

MARCH 11 WITH SILVER UP $0.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.816 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 436.410 MILLION

MARCH 10 WITH SILVER DOWN 25 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.276 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.591 MILLION

MARCH 7 WITH SILVER DOWN 40 CENTS/HUGL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.184 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 434.317 MILLION

MARCH 6 WITH SILVER UP 16 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.455 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.046 MILLION

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

CLOSING INVENTORY 444.054 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

Alasdair Macleod..

2, EGON VON GREYERZ AND OTHER GOLD COMMENTARIES

3.. CHRIS POWELL AND DAILY GATA DISPATCHES

4. ANDREW MAGUIRE PODCAST

Episode 214

youtube.com/watch?v=E_A-wvLnyL0

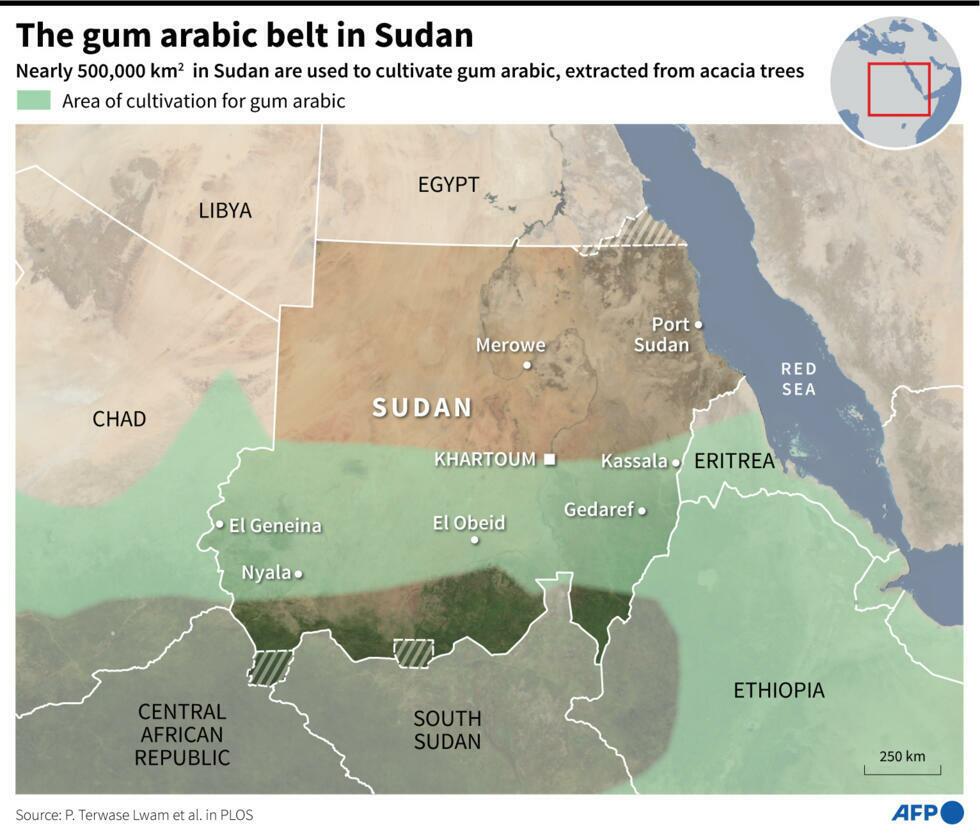

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY//GUM ARABIC

This key ingredient is controlled by the military and may not be available

(zerohedge)

Key Coca-Cola & Pepsi Ingredient ‘Controlled By RSF Paramilitary In Sudan’

by Tyler Durden

Thursday, Mar 20, 2025 – 05:00 AM

Sudan’s paramilitary Rapid Support Forces (RSF) is currently controlling access to a vital ingredient used in Coca-Cola and Pepsi across vast swathes of the country, according to a new report.

Gum arabic, an organic emulsifier derived from the sap of the acacia trees, is a major ingredient in a range of products, including the gigantic soft drink brands as well as soap, medicine, sweets and cosmetics. Around 70 percent of the world’s supply comes from Sudan, where the trees grow in a 200,000 square mile belt across the south of the country that is largely controlled by the RSF, according to Bloomberg.

Hisham Salih Yagoub, whose company Afritec is one of Sudan’s biggest international suppliers, told the news outlet that he regularly pays the RSF $2,500 per truck to allow transport of the product to the country’s ports.

“They stop the trucks and you have to pay for the trucks to move,” he said. “They either steal some of it or they make you pay.”

Since April 2023, Sudan has been embroiled in a brutal civil war between the RSF and the Sudanese Armed Forces (SAF). The country has fallen into a humanitarian crisis, with 12.5 million Sudanese displaced from their homes, according to UNHCR. Thousands are estimated to have been killed.

The RSF has been accused of widespread sexual assault, looting, torture and the summary execution of civilians, while the SAF has also been censured for indiscriminate bombing campaigns.

According to documents acquired by Bloomberg, the SAF has also introduced a range of fees that amount to roughly $155 per 100kg of gum arabic being sent out of Port Sudan, meaning any transportation of gum arabic out of the country likely involves payment to groups accused of war crimes.

Bloomberg said it did not receive a response to inquires put to Coca-Cola, PepsiCo and Danone over the gum arabic controversy.

Nestle said it was “committed to sourcing all our commodities in a responsible way, and in line with applicable regulatory requirements,” while Mars said it did it not tolerate bribery or corruption and was “actively engaging with our suppliers regarding the deeply concerning situation in Sudan and we remain prepared to take any appropriate action if we find any violation of our policies.”

Sudan’s gum arabic belt covers hundreds of thousands of square kilometers…

Coca-Cola and Pepsi have recently also faced a widespread boycott in the Middle East over the US role in supporting Israel’s assault on the Gaza Strip, as well as the former’s reported factory in the illegal West Bank settlement of Atarot.

According to market researcher NielsenIQ, western soft drink brands suffered a 7 percent sales decline in the first half of 2024 across the Middle East.

end

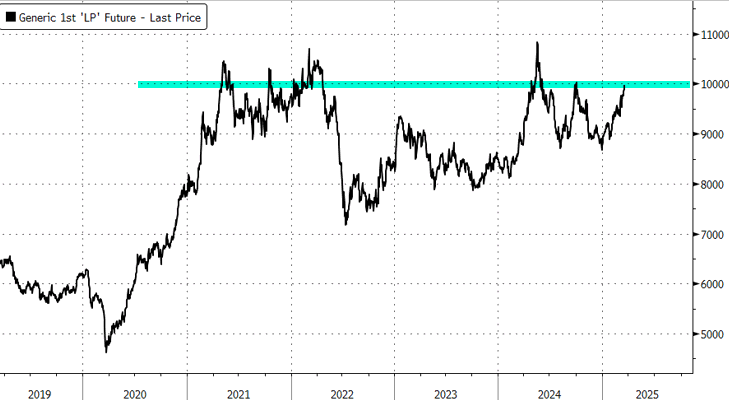

COPPER

London Copper Surges Back Above $10,000 On US Tariff-Driven Fears

Thursday, Mar 20, 2025 – 09:50 AM

Copper prices on the London Metal Exchange surpassed $10,000 per ton on Thursday, driven by concerns over President Trump’s potential tariff expansion on the crucial industrial metal used in everything from electric vehicles to power grids. Traders are rushing to deliver copper into the US before potential tariffs later this year.

On Feb. 25, President Trump signed an executive order directing the US Department of Commerce to investigate the potential national security risks of copper imports, which could lead to tariffs on all copper imports—including raw mined copper, copper concentrates, refined copper, copper alloys, scrap copper, and certain derivative products. Since then, US prices have surged, and traders have been rushing to send their metal to the US ahead of tariffs, thereby tightening global supplies. The Secretary of Commerce will submit a report to the president 270 days from when the executive order was signed.

According to BMO analysts, while the destination of copper exiting LME warehouses remains unknown, US trade data shows copper imports are increasing.

“This is a round of cross-regional repricing triggered by potential US tariffs,” said Wei Lai, deputy trading head at Zijin Mining Investment Shanghai, adding, “Cargoes are lured to the US, leaving other places in shortfall. Buying sentiment is very strong.”

On Thursday, LME copper prices increased by a half percentage point to $10,046 a ton — the highest level since October — while prices on New York’s Comex inched closer to record highs.

The spread between the copper Comex futures and LME futures widened to more than $1,254 per ton this week, surpassing its February peak of around $1,149.

“Copper just keeps grinding as it takes out $10k, we said it will overshoot, and its overshooting! Nothing more to my eye than this is when GIR expect refined metal tightness to deliver deficits (2Q25 onwards) and US is dragging metal in that will be stranded,” Goldman analyst James McGeoch penned in a note to clients earlier.

Last month, Goldman’s Eoin Dinsmore and others reinitiated their coverage of copper with a new medium-run $10,500-11,500/t range forecast. This call was based on three drivers:

- Strong Electrification Demand. We believe the electrification megatrend will continue to reshape copper demand. That became clear in 2024, when despite a 10% drop in copper demand from the China construction sector, electrification drove a solid 4% YoY increase in China refined copper demand. Electrification will account for all copper demand growth to 2030. And the grid alone makes up over 50% of the growth, adding the equivalent of another US to global copper demand.

- China Copper Stimulus. Copper demand is set to disproportionately benefit from China stimulus in sectors such as appliances and EVs. We estimate China stimulus will add 2pp to China copper demand growth, while tariffs knock off only 0.8pp. We forecast China refined copper demand to grow by 4% in 2025, as the boost from structural electrification and stimulus well outweigh the drags from weakness in construction and tariffs. However, several stimulus programs pull forward demand, with copper demand growth slowing markedly from 2027.

- Ali Cap and Chile Floor. Copper demand will rise by 4Mt by 2030, requiring substantial growth in mine and scrap supply. We believe that substitution away from copper (when the copper price trades >4x the aluminium price) will cap the copper price at $10,500/t in 2025 and $11,500t in 2026. Mine supply growth will primarily come from short lead-time, low capex mines in DR Congo, but maintaining stable supply from Chile remains crucial. A price of $10,500/t will be needed by 2026 for enough new mine capacity to be developed and to avoid large deficits by the early 2030s. We think the scrap share of total demand will remain flat, offering little relief to future market tightness.

The Commerce Department’s investigation into copper imports is unlikely to deliver recommendations for the president until the end of the year. In the meantime, copper supplies flow into the US while global supplies tighten.

END

6 CRYPTOCURRENCY NEWS

ASIA TRADING THURSDAY MORNING WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 17.48 PTS OR 0.51%

//Hang Seng CLOSED DOWN 551.19 PTS OR 2.23%

// Nikkei CLOSED HOLIDAY%//Australia’s all ordinaries CLOSED UP 1.16%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2428 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2488/ Oil UP TO 67.38 dollars per barrel for WTI and BRENT UP TO 70.87 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAkER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2428

OFFSHORE YUAN: DOWN TO 7.2488

SHANGHAI CLOSED CLOSED DOWN 17.48 PTS OR 0.31%

HANG SENG CLOSED CLOSED DOWN 551.19 PTS OR 0.23%

2. Nikkei closed

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 103.55// EURO FALLS TO 1.0847 DOWN 65 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: RISES TO. +1.503//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.44…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7580/Italian 10 Yr bond yield DOWN to 3.817 SPAIN 10 YR BOND YIELD DOWN TO 3.395

3i Greek 10 year bond yield DOWN TO 3.565

3j Gold at $3033.50 Silver at: 33.27 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 24 /100 roubles/dollar; ROUBLE AT 84/24

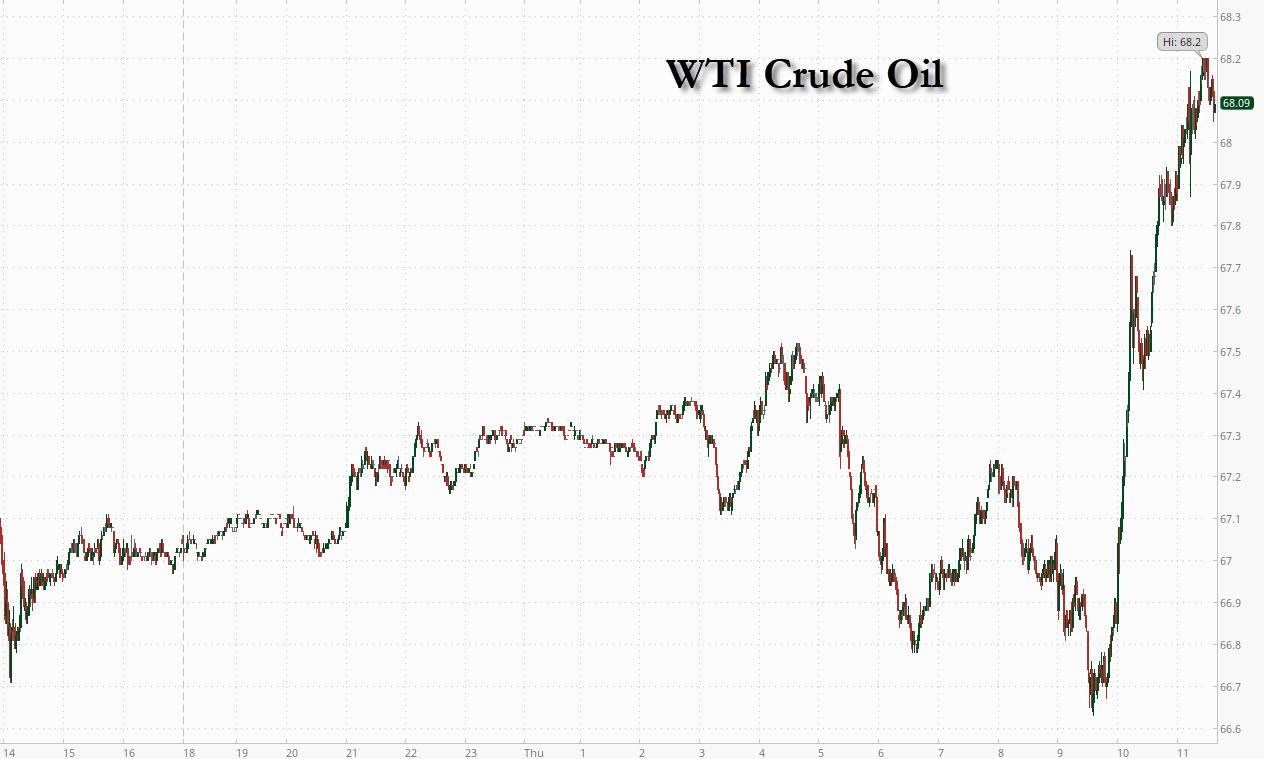

3m oil into the 67 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.44 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.503 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8825 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9735 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.187 DOWN 9 BASIS PTS…

USA 30 YR BOND YIELD: 4.502 DOWN 9 BASIS PTS/

USA 2 YR BOND YIELD: 4.054 UP 1 BASIS PTS

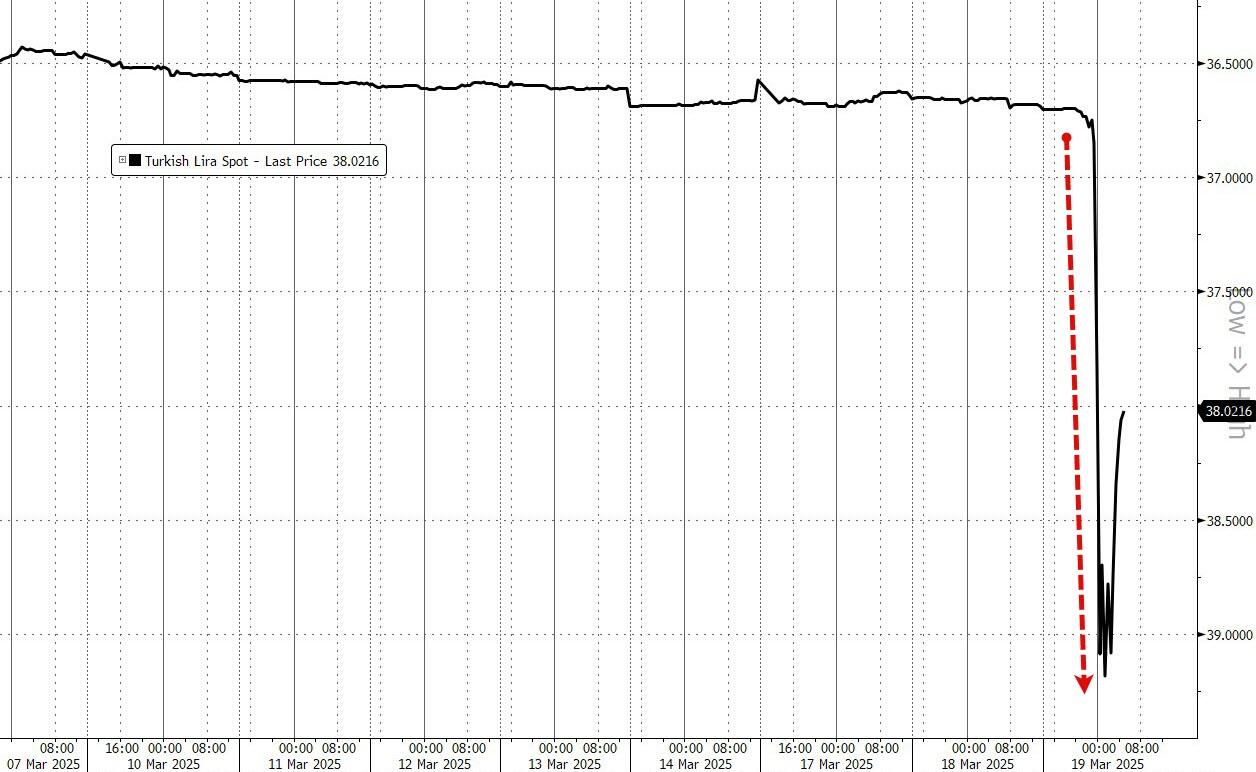

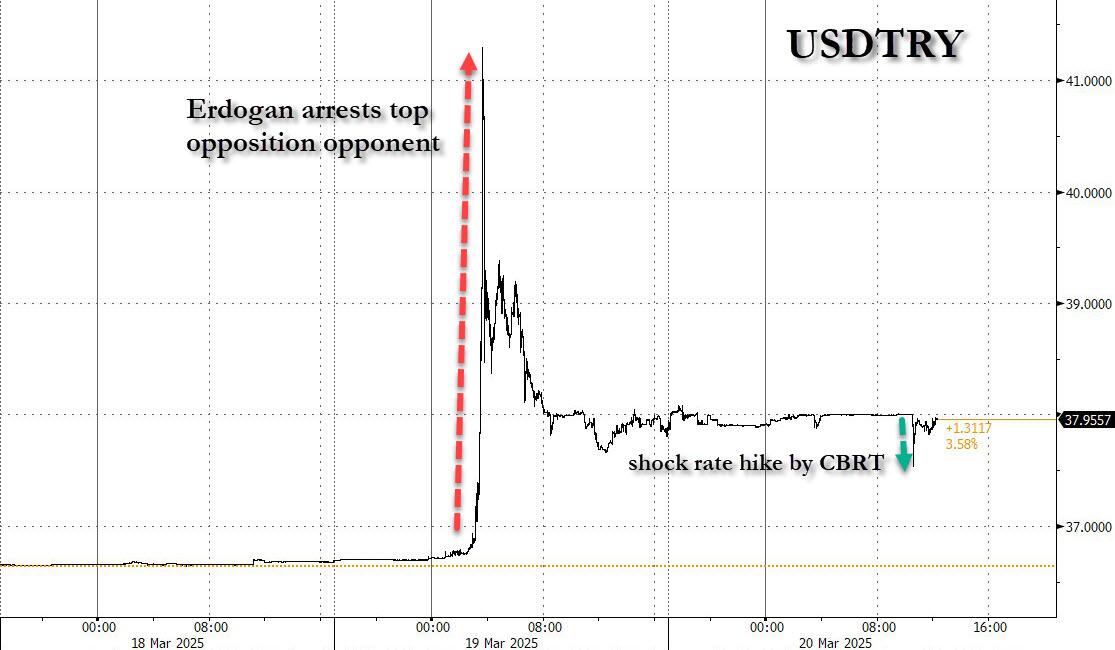

USA DOLLAR VS TURKISH LIRA: 38.00…

10 YR UK BOND YIELD: 4.6395 DOWN 5 PTS

10 YR CANADA BOND YIELD: 2.974 DOWN 7 BASIS PTS

5 YR CANADA BOND YIELD: 2.488 DOWN 12 PTS.

2a New York OPENING REPORT

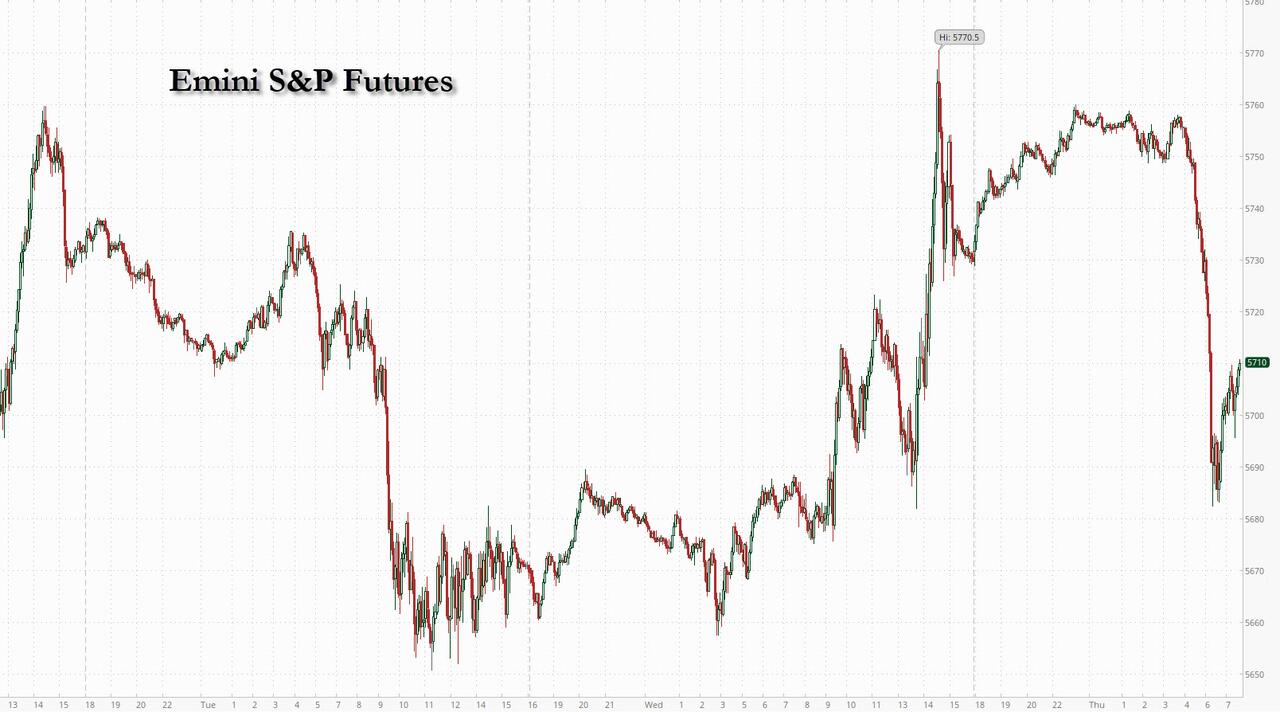

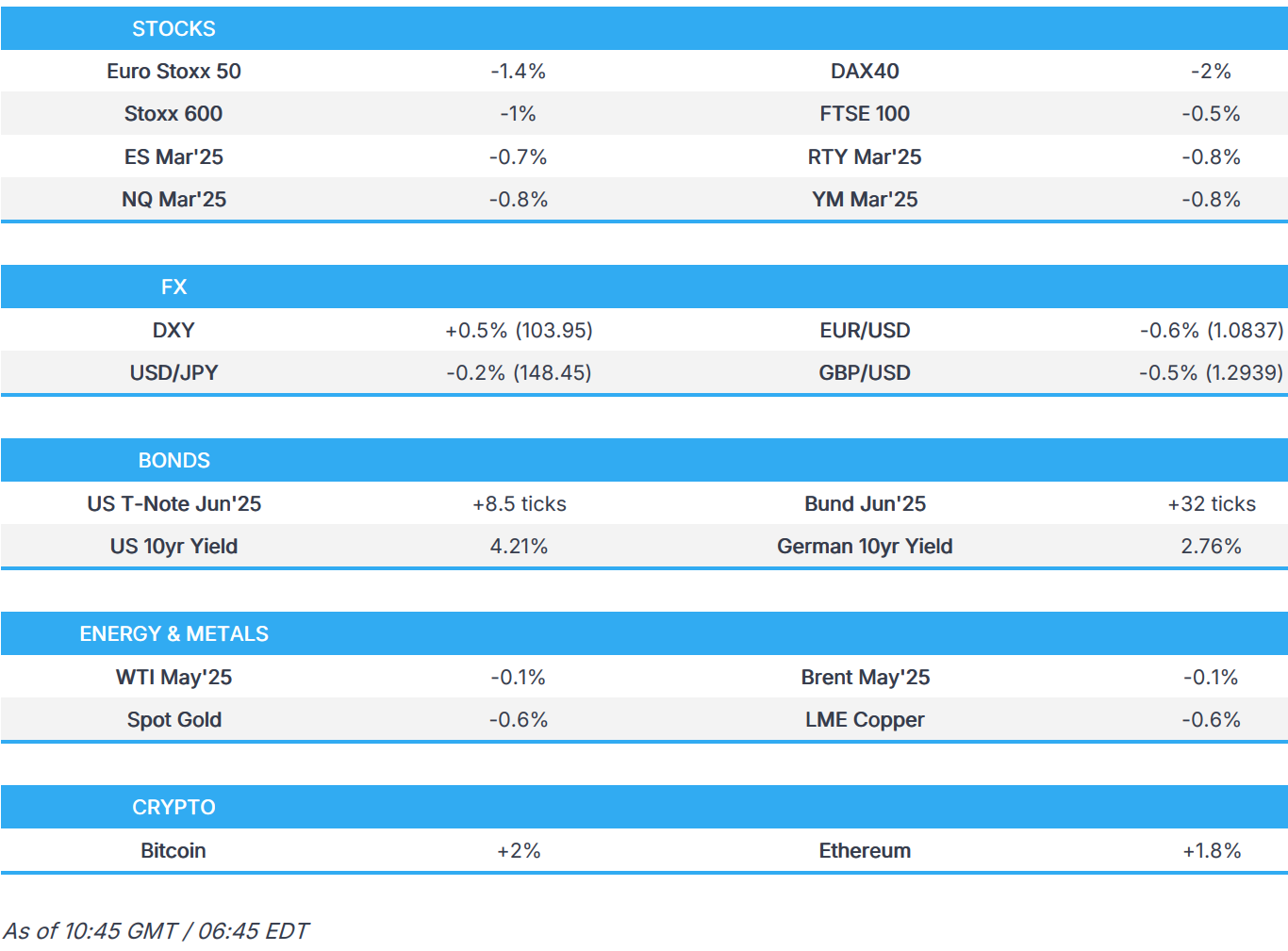

Futures Slump, Erasing Most Post-Fed Gains

Thursday, Mar 20, 2025 – 08:09 AM

US equity futures swooned shortly after 5am ET, erasing all post-FOMC gains, as doubts grew that the Fed can significantly cut interest rates in the face of potentially inflationary trade tariffs and sentiment was weighed down by comments from ECB President Lagarde, who said that US tariffs could hit growth in the region, and couldn’t make firm commitments on interest rates. As of 8:00am S&P futures dropped 0.4% a day after Wall Street rallied on the Fed’s signal that it still sees room to ease policy this year; Nasdaq futures lost 0.6%, paring much of the earlier advance seen after Fed Chair Powell offered reassuring comments about the outlook for US growth and inflation. European stocks also dropped with the Stoxx 600 down 0.9% and are set to snap a four-day winning streak. JPM warned earlier that yesterday’s rally may not be indicative of near-term direction as the Fed’s forecast shifted to support the Stagflation narrative and Powell reintroduced transitory inflation, neither are likely to give confidence to investors. Mag7 names are all loower with TSLA leading losses, while Energy and Financials are higher but Chinese ADRs under pressure. The yield curve is bull flattening after steepening yesterday; the market is still placing its heaviest bets on June and/or Sept rate cuts. USD is poised to have its strongest day in 3 weeks, which is weighing on Emerging markets. Commodities are weaker ex-WTI and Softs; gold dips below its all time high of $3,050. Today’s macro data focus is on Jobless Claims, Regional Fed activity indicators, and Housing data.

In premarket trading, Tesla slipped the most among the Magnificent Seven stocks after the electric-vehicle maker recalled all the Cybertrucks it produced and sold in the first 15 months it was on the market in the US (Alphabet -0.4%, Amazon -0.2%, Apple -0.2%, Microsoft -0.3%, Meta -0.09%, Nvidia -0.4% and Tesla -1.1%). Microchip Technology was undermined by its plan to sell depositary shares to repay debt., while US-listed shares in PDD Holdings Inc. slid as the Chinese budget-shopping site’s sales missed estimates for a third straight quarter. Here are the most notable US premarket movers:

- Akebia Therapeutics (AKBA) slumps 28% after the drugmaker launched a secondary offering of shares, with the size to be determined, via Leerink Partners and Piper Sandler.

- Aramark (ARMK) falls 2% after peer Sodexo lowered its revenue guidance, citing slower growth at its US university business.

- Cava Group (CAVA) gains 3% after an upgrade to overweight at JPMorgan.

- Celldex Therapeutics (CLDX) rises 2% after Morgan Stanley initiated coverage of the drug developer with an overweight rating, citing the firm’s compelling approach to treating a number of inflammatory conditions.

- Coty (COTY) gains 3% after Citi raised the cosmetics company to buy, saying the weakness in its consumer-beauty segment and normalization in prestige are largely reflected in the stock.

- Five Below (FIVE) jumps 9% after the discount retailer reported fourth-quarter results that beat expectations.

- PDD (PDD) ADRs fall 6% after the Chinese budget-shopping site reported sales that missed estimates for a third consecutive quarter, showing a further slowdown in growth amid pressures from domestic rivals and trade uncertainties in global markets.

- ProAssurance (PRA) surges 49% after the specialty insurer agreed to be bought by the Doctors Co., the largest US physician-owned medical malpractice insurer.

- Microchip Technology (MCHP) falls 6% after the company offered $1.35 billion in depositary shares. The group will use part of the proceeds to repay debt.

- Rivian (RIVN) slips 2% as Piper downgrades the stock to neutral, with analysts saying automakers, except for Tesla, should be avoided.

- QXO (QXO) rises 3% after the building products distributor struck a deal to buy Beacon Roofing Supply.

US markets have just endured a bruising four-week stretch in which the S&P 500 slid into a correction, but relief from assurances offered by Powell after the Fed meeting is already dissipating. Powell downplayed the economic impact of President Donald Trump’s tariff policies and said any resulting inflation bump could be transitory. The central bank also dialed back its growth forecasts for this year, while investors remain concerned about Trump’s plans to unleash a fresh tariff wave on April 2.

“The fact that the Fed Chair didn’t play to recessionary fear helped sentiment, but I am a bit bothered by his characterization of the impact of tariffs on inflation as one-off,” Wei Li, global chief investment strategist at BlackRock said on Bloomberg TV. Traders pricing as many as three Fed cuts this year could end up disappointed, Li said, adding that “markets are still expecting the Fed to be able to come to the rescue of the economy if the economy slows down, but the growth-inflation trade-off is becoming very tough indeed.”

Meanwhile, bond investors seized on the Fed’s lower growth forecasts, as well as rate-setters’ indications for a half percentage point of policy easing this year. ECB President Christine Lagarde added to the worries about the economic outlook, saying Thursday that the brewing trade war could hit growth.

European equities slipped, halting a four-day winning streak, on concern that tariffs could undercut the region’s economies. The Stoxx Europe 600 Index was down 1% by 10:40 a.m. in London, with investors taking profits on top-performing sectors including defense, banks and industrials. Sentiment was weighed down by comments from European Central Bank President Christine Lagarde, who said that US tariffs could hit growth in the region, and couldn’t make firm commitments on interest rates. Meanwhile the Swiss National Bank cut its interest rate to deter investors from pushing money into the franc. Meanwhile the Swiss National Bank cut its interest rate to deter investors from pushing money into the franc. Here are the biggest movers Thursday:

- Shaftesbury Capital gains as much as 18%, the most since 2020, after the company announced it has partnered with Norges Bank Investment Management in a deal that values the Covent Garden estate at £2.7 billion

- Eurofins shares advance as much as 6.2%, the most since June 25, after the laboratory-testing company started a new buyback program

- CVC Capital shares rise as much as 4.8%, the biggest jump since Dec. 12, after full-year earnings beat expectations, though analysts say weaker-than-expected guidance on performance-related earnings could drive downgrades

- Nexi rose as much as 5.8% in Milan trading after Corriere della Sera daily reported that US fund TPG made an offer for about EU850m for Nexi’s Digital Banking Solutions division

- Jeronimo Martins shares rise as much as 3.2% as retailer reported 4Q Ebitda beat thanks to better performance of Portuguese and Colombian chains

- Sodexo slumps as much as 18%, the most since September 2002, after the food services company issued a profit warning due to challenges including weaker growth in North America in both health care and education

- Lanxess drops as much as 9.4%, largest decline in a month, after the German chemicals company’s 2025 adjusted Ebitda guidance missed estimates. That was mostly due to prebuying in 4Q, Citi says

- 3i Group shares fall as much as 8.3%, the steepest decline since May 2022, after the private equity firm gave an update on its biggest portfolio company that analysts said was disappointing

- Investec falls as much as 4.6% in Johannesburg, the most since December, after the bank said it expects its basic earnings per share for the full year to fall by as much as 36% compared to the prior year

- Husqvarna falls as much as 4.5% as SEB Equities lowers its price target to a new Street-low and trims 2025-27 EPS estimates by 11%-12%, citing soft sentiment in Europe and a “clearly weakening” US environment

Earlier in the session, Asian stocks were mixed as investors sold Chinese shares, offsetting optimism elsewhere after the Federal Reserve signaled there’s still room to ease policy later this year. The MSCI Asia Pacific ex-Japan Index was little changed. Shares advanced in Taiwan, South Korea and Australia, while Indonesian stocks extended a rebound for a second day. Japanese markets were shut for a holiday. A gauge of Chinese shares listed in Hong Kong posted its biggest drop in three weeks, with some market participants attributing the losses to profit taking and waning earnings catalysts. Onshore Chinese shares also fell. Investors are taking stock as they await additional market catalysts, said David Chao, global market strategist, Asia Pacific ex-Japan at Invesco. “We are also moving through peak tariff uncertainty, and these risks could be amplified in the coming weeks.”

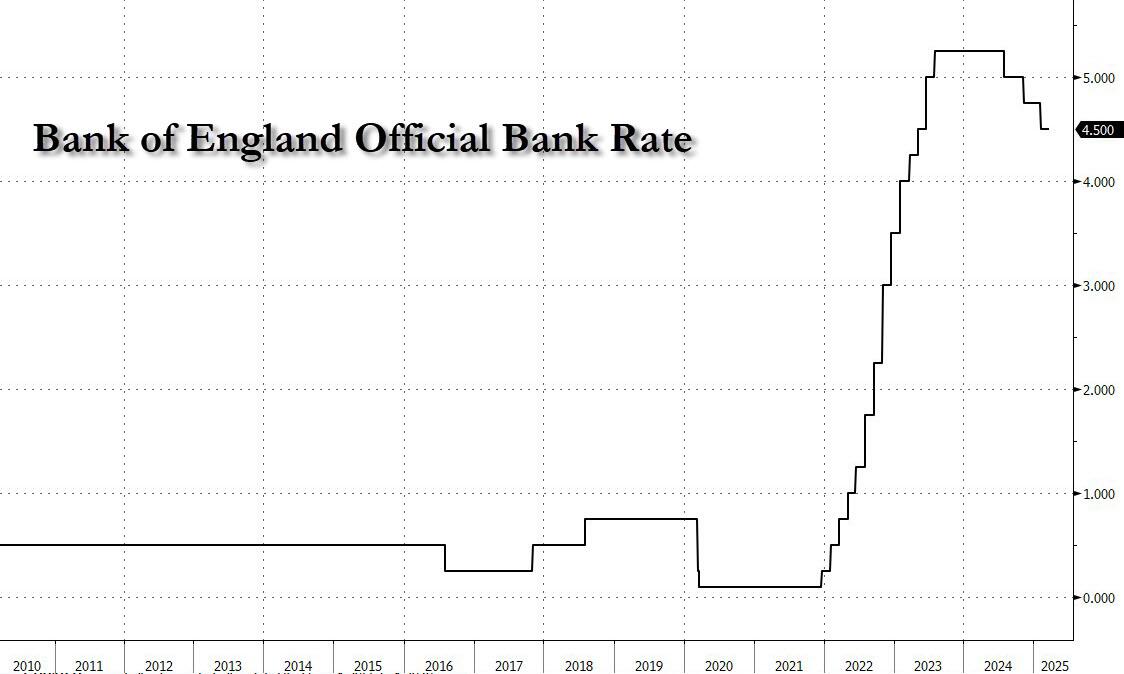

In FX, the Bloomberg Dollar Spot Index rose 0.3% and above levels seen before Wednesday’s Federal Reserve decision after US equity futures abruptly turned lower. The pound slipped 0.3%, having risen earlier this week to the highest since November. The Bank of England is expected to leave its benchmark rate unchanged later, with fresh data showing that UK wage growth held at its highest level in nine months.

- EUR/USD drops as much as 0.6% to 1.0839, lowest in nearly a week

- GBP/USD down 0.3% to 1.2962; the Bank of England is likely to turn less dovish on Thursday as officials start to fret about the fallout from Donald Trump’s tariff wars and a renewed bout of domestic inflation

- EUR/CHF falls as much as 0.4% to 0.9531 before briefly reversing losses after the Swiss National Bank cut its interest rate to the lowest since September 2022 and declared another reduction is less likely for now

- EUR/SEK rallies by 0.4% to 11.0589, highest since March 14; Sweden’s central bank kept its benchmark rate unchanged at a two-year low and reiterated it’s finished with the easing cycle

- AUD/USD plummets by 1.1% to 0.6287; Australian employment surprisingly dropped in February, sending the currency and government bond yields lower as traders boosted bets on further interest-rate cuts this year

- USD/CAD up a third day, gains 0.4% to 1.4385; Canadian Prime Minister Mark Carney is poised to call a snap federal election on Sunday for an expected vote on April 28, the Globe and Mail reports

In rates, treasury futures push higher into early US session with yields falling across the curve. 10-year yields, lower by around 5bps at 4.19%, remain near richest levels of the session with bunds and gilts in the sector outperforming slightly, catching up with Wednesday’s post-FOMC moves in US rates. Investors continue to digest Wednesday’s Fed meeting, where Chair Powell said the inflationary impact of tariffs is likely to be transitory. US session features weekly jobless claims data at 8:30am New York time and a 10-year TIPS reopening at 1pm. Treasuries have added to their post-Fed gains, with US 10-year yields falling another ~3 bps to 4.21%. Gilts lead a rally in European government bonds ahead of the Bank of England decision, with UK 10-year borrowing costs falling nearly 6 bps to 4.57%. The pound falls 0.5%.

In commodities, Oil prices turn lower with Brent down 0.1% to $70.75 a barrel. Spot gold drops $19 to around $3,028/oz. Bitcoin inches lower toward $85,000.