GOLD CLOSED UP $13.90 TO $3022.00

SILVER CLOSED UP 0.63 TO $33.58

GOLD ACCESS CLOSED 3019.60

Silver ACCESS CLOSED: $33.66

Bitcoin morning price:$87,339 up 3326 DOLLARS.

Bitcoin: afternoon price: $88338 UP 1410 DOLLARS

Platinum price closing UP $7.40 TO $982,00

Palladium price; UP $5.05 TO $961.85

END

*CANADIAN GOLD: $4312.01 UP 3.18 CDN dollars per oz( * NEW ALL TIME HIGH 4361.64- CDN DOLLARS PER OZ//MARCH 19 2025)

*BRITISH GOLD: 2333.35 UP 4.32 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,343.17 BRITISH POUNDS/OZ) MARCH 19/2025

*EURO GOLD: 2,798.34 UP 12.34 Euros per oz //* (ALL TIME CLOSING HIGH: 2,819,78UROS PER OZ/FEB 24 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,013.100000000 USD

INTENT DATE: 03/24/2025 DELIVERY DATE: 03/26/2025

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 1

323 C HSBC 286

363 H WELLS FARGO SEC 59

435 H SCOTIA CAPITAL 112

523 H INTERACTIVE BRO 2

624 H BOFA SECURITIES 60

661 C JP MORGAN 25

686 C STONEX FINANCIA 72 65

709 C BARCLAYS 55

880 H CITIGROUP 26

905 C ADM 5

TOTAL: 384 384

JPMORGAN stopped 25/384 contracts

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2024. CONTRACT: 384 NOTICES FOR 38,400 OZ 1.194 TONNES

total notices so far: 18,731 contracts for 1,873,100 Oz (58.261 tonnes)

FOR MARCH

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 50 NOTICE(S) FILED FOR 0.250 MILLION OZ/

total number of notices filed so far this month : 15,343 for 76.715 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $13.90 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD OUT OF THE GLD//

INVENTORY RESTS AT 929.07 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $.63 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.249 MILLION OZ INTO THE SLV//

THIS IS A MASSIVE FRAUD

CLOSING INVENTORY

CLOSING INVENTORY: 454.883 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 235 CONTRACTS TO 167,074 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY GAIN OF $0,04 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A SMALL LOSS OF 118 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR SMALL GAIN IN PRICE//THURSDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON MONDAY COMEX TRADING / AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED SLIGHTLY ON MONDAY WITH SILVER’S SMALL GAIN IN PRICE. WE HAD A HUGE T.A.S. LIQUIDATION MONDAY. BUT THIS WAS COUPLED WITH A SMALL T.A.S. ISSUANCE OF 310 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS METALS WILL COMMENCE AGAIN! WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND 59 CENTS AND A LEASE RATE OF 7.3%. WE HAD A SMALL 200 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR FAIR 310 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TODAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A TINY 35 CONTRACTS ON OUR TWO EXCHANGES WITH OUR SMALL GAIN IN PRICE. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT MONDAY’S COMEX TRADING SESSION WHICH ACCOUNTS FOR A HUGE PORTION IN THE LOSS OF OI ON OUR TWO EXCHANGES.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.00 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A FAIR 310 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.04 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS DESPITE HAVING A SMALL LOSS IN OUR TWO EXCHANGES OF 35 CONTRACTS WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS TRYING TO CONTAIN SILVER’S PRICE RISE AND THAT ACCOUNTS FOR MOST OF OUR OPEN INTEREST FALL. HOWEVER THE CME NOTIFIED US THAT FOR THE FIRST TIME IN MARCH, WE HAVE BEEN ISSUED 70 CONTRACTS OF EXCHANGE FOR RISK FOR 350,000 OZ. THIS TOTAL WILL BE ADDED TO OUR REGULAR DELIVERY TOTALS FOR MARCH.

WE HAD A 200 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 78.753 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0.185 MILLION OZ EFP TRANSFER TO LONDON TO WHICH WE ADD .350 EXCHANGE FOR RISK

INITIAL STANDING FOR MARCH ADVANCES TO 81.345 MILLION OZ

WE HAD:

/ FAIR COMEX OI LOSS+// A SMALL SIZED EFP ISSUANCE/ VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 310 CONTRACTS)/A 70 CONTRACT EX. FOR RISK FOR 350,000 OZ/SECOND WEEK OF MARCH

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED 35 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR

TOTAL CONTRACTS for 17 DAYS, total 10,491 contracts: OR 52.455 MILLION OZ (617 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 52.455 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 52.455 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 235 CONTRACTS DESPITE OUR GAIN IN PRICE OF 4 CENTS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL 200 CONTRACT EFP ISSUANCE CONTRACTS: 200 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH OF 78.455 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 0.185 MILLION OZ E.F.P. TRANSFER JUMP TO LONDON/

NEW STANDING REDUCES TO 80.995 MILLION OZ + .350 EX. FOR RISK//NEW TOTAL 81.345 MILLION OZ.

WE HAVE 1). A SMALL SIZED LOSS OF 35 OI CONTRACTS ON THE TWO EXCHANGES DESPITE OUR LOSS IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR 310 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. SOME NET LONG SPECULATORS WERE BURNED ON FRIDAY WITH OUR LOSS IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (310 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 50 NOTICE(S) FILED TODAY FOR 0.250 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 12,141 OI CONTRACTS TO 506,999 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A LARGE SIZED 644 CONTRACTS//

WE HAD A STRONG SIZED DECREASE IN COMEX OI (12,141 CONTRACTS) OCCURRED WITH OUR STRONG LOSS OF $6.10 IN PRICE MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 31.757 TONNES FOLLOWED BY TODAY’S STRONG 9200 OZ QUEUE JUMP (0.2861 TONNES), ////NEW STANDING ADVANCES TO 58.3017 TONNES + .4655 TONNES EX FOR RISK/PRIOR + .3110 EX FOR RISK TODAY = 59.0792 TONNES

/NEW STANDING FOR MARCH; 58.3017 TONNES + .7775 TONNES EX FOR RISK= 59.0792 TONNES

/ ALL OF THIS HAPPENED WITH OUR $6.10 LOSS IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD A STRONG SIZED LOSS OF 11,261 OI CONTRACTS (35.026 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE FRONT MARCH CONTRACT MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 880 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 536,068

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,261 CONTRACTS WITH 12,141 CONTRACTS DECREASED AT THE COMEX// AND A SMALL SIZED 880 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 11,261 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1394 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (880 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 12,141 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 11,261 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH 31.757 TONNES FOLLOWED BY TODAY’S 0.2861 TONNES QUEUE JUMP. TO WHICH WE MUST ADD OUR NEW .7775 TONNES OF EX FOR RISK ON OUR TWO OCCASION ISSUANCES.

//NEW STANDING ADVANCES TO 58.3017 TONNES + .4655 TONNES EX FOR RISK/PRIOR + .31104 EX FOR RISK TODAY = 59.0792 TONNES

//NEW STANDING MARCH: 59.0792 TONNES

.

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE MONDAY WITH SOME SUCCESS IN REMOVING NET SPECULATOR LONGS, AS WE HAD 1) $6.10 LOSS GAIN AND WE HAD 2) SOME NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG LOSS OF 11,261 CONTRACTS ON OUR TWO EXCHANGES (ALL DUE TO T.A.S. LIQUIDATION ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN MARCH. ALL OF THE GAIN IN OI WAS DUE TO THE HUGE NUMBER OF T.A.S. LIQUIDATION MONDAY.

4) VERY STRONG SIZED COMEX OPEN INTEREST DECREASE 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1394 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH :

TOTAL EFP CONTRACTS ISSUED: 30,148 CONTRACTS OF 3,014,800 OZ OR 93.67 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 1773 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 93.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 93.67 DIVIDED BY 3550 x 100% TONNES = 2.63% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 93.67 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A SMALL SIZED 235 CONTRACTS OI TO 167,074 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1025 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 200 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 318 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A SMALL SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 35 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 0.590

MILLION OZ OCCURRED DESPITE OUR SMALL $0.04 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

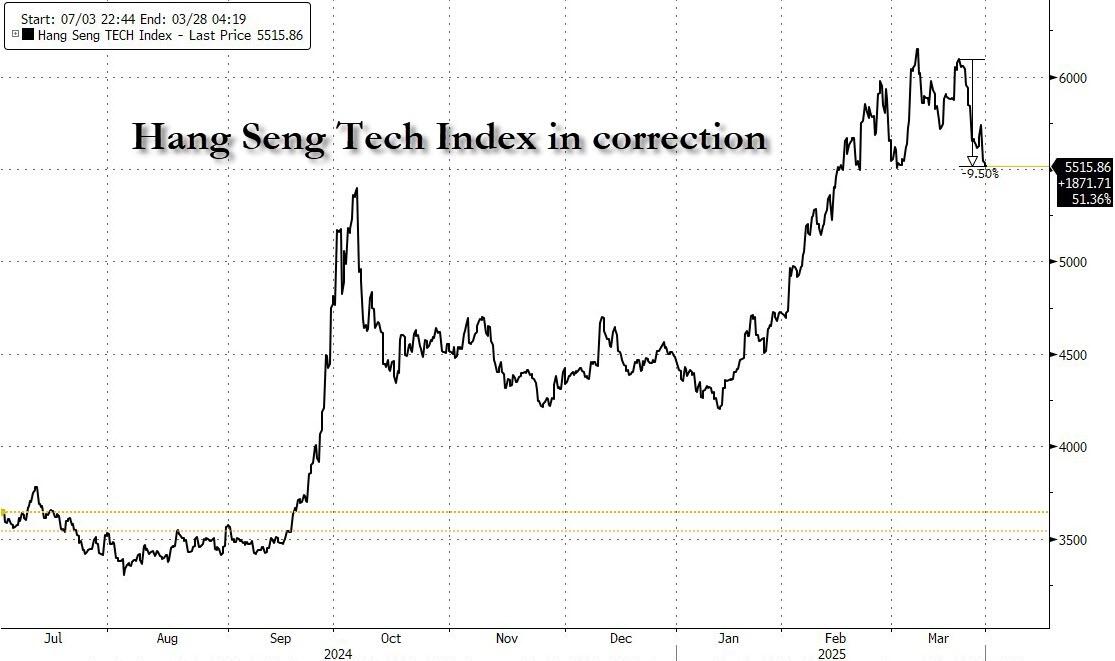

SHANGHAI CLOSED DOWN 0.05 PTS OR 0.00%

//Hang Seng CLOSED DOWN 561.31 PTS OR 2.35%

// Nikkei CLOSED UIP 172.05 OR .46 %//Australia’s all ordinaries CLOSED UP 0.11%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2595 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2613/ Oil UP TO 6944 dollars per barrel for WTI and BRENT UP TO 73.40 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED 12,141 CONTRACTS TO 506,999 WITH OUR LOSS IN PRICE OF $6.10 WITH RESPECT TO MONDAY’S TRADING/. WE LOST SOME NET LONGS WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (800 ).

THE CME ANNOUNCED MONDAY NIGHT, 100 EXCHANGE FOR RISK CONTRACTS FOR 10,000 OZ OR .3110 TONNES. LAST THURSDAY WAS THE FIRST ISSUANCE FOR MARCH FOR .4665 TONNES. THUS TOTAL NO OF EXCHANGE FOR RISK ISSUANCE EQUALS: 7775 TONNES OF GOLD WHICH WILL BE ADDED TO OUR DELIVERY TOTALS.

IN FEBRUARY: WE HAD FIVE EXCHANGE FOR RISKS IN GOLD, TOTALLING 18.4527 TONNES!. THE RECIPIENT OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 4TH CONSECUTIVE ISSUANCE FOR EXCHANGE FOR RISK.

THUS IN TOTAL WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 11,261 CONTRACTS WITH OUR LOSS IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON MONDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF MARCH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY TODAY INCLUDING WITH OUR HUMONGOUS T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION// THROUGHOUT THE WEEK. THEY ISSUED LAST NIGHT A FAIR SIZED 1394 CONTRACTS. THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING A LOWER COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY THURSDAY.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, , 203 , ,205 , 207 209 AND 211 212 213 AND FRIDAY’S 215 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF MARCH .… THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 880 EFP CONTRACTS WERE ISSUED: : /APRIL 880 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 880 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 11,261 CONTRACTS IN THAT 880 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR LOSS OF 12,261 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $6.10 FOR MONDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. ALL OF THE TOTAL LOSS IN OUR TWO EXCHANGES WAS DUE TO THE LIQUIDATION OF T.A.S. CONTRACTS.

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED 1394 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER 4 WEEKS AGO AND AGAIN LAST WEEK,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND NOW ,THIS MONTH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT LAST WEDNESDAY’S 38,393 T.A.S. CONTRACT ISSUANCE IS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY DOES TWO IMPORTANT THINGS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: MARCH (59.0792 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE MARCH DELIVERY MONTH / FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH.

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

AND NOW MARCH:

STANDING FOR GOLD : 58.3017 TONNES + .7775 TONNES EX FOR RISK = 59.0792 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 50 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES.

MARCH: 59.0792 TONNES (INCLUDES .7775 TONNES EX FOR RISK)

COMEX GOLD TRADING/MARCH CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $6.10/)/AND WERE SUCCESSFUL IN KNOCKING OFF CONSIDERABLE APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED LOSS IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION MONDAY/NIGHT AS THEY WERE TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,000 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING AND THEY FAILED MISERABLY AS GOLD IS NOW WELL ABOVE THE $3,000 THRESHOLD AT 3013 PLUS.

LAST NIGHT/TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH MARCH TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND IS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO TODAY’S NORMAL DELIVERY TOTAL.

NOW MARCH ISSUES IT’S SECOND EX FOR RISK:

TOTAL ISSUANCE OF EXCHANGE FOR RISK TODAY EQUALS 100 CONTRACTS FOR .3110 TONNES OF GOLD. PRIOR ISSUANCE: .4665 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH SO FAR: .7775 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

STANDING NOW FOR MARCH:

MARCH: 58.3017 TONNES +3110 EX FOR RISK TODAY+ .46556 TONNES EX FOR RISK = 59.0792 TONNES

WE HAVE LOST A STRONG SIZED TOTAL OF 35.026 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH (31.753TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 9200 OZ OR 0.2861 TONNES: NEW TOTAL STANDING 58.3017 TONNES TO WHICH WE ADD OUR .7775 TONNES OF EXCHANGE FOR RISK//NEW TOTAL: 59.0792 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $6.10

WE HAD 644 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET LOSS ON THE TWO EXCHANGES 11,261 CONTRACTS OR 1,126,100 0Z (35,026 TONNES)

confirmed volume MONDAY 307,601 contracts: fair///

//speculators have left the gold arena

END

MARCH

// THE MARCH 2025 GOLD CONTRACT

MARCH 25

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entry withdrawals: 0 . |

| Deposit to the Dealer Inventory in oz | 1 ENTRY i) Manfra: 28,315.099 oz weight .8807 tonnes |

| Deposits to the Customer Inventory, in oz | we have 2 customer entries we have 2 customer deposits i) Into JPMorgan customer; 64,302.000 oz (2,000 klilobars) iii) Into Malca 96,453.000 oz (5000 kilobars) total weight: 160.755.000 oz (7.000 tonnes) total weight dealer and customer; 7.8807 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 384 notice(s) 38400 OZ 1.194 TONNES |

| No of oz to be served (notices) | 13 contracts 1300 OZ 0.0404 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,731 notices 1,873,100 oz 58.261 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

dealer deposits: 1

1 ENTRY

i) Manfra: 28,315.099 oz

weight .8807 tonnes

xxxxxxxxxxxxxxxxxxxxx

deposits customer

we have 2 customer deposits

i) Into JPMorgan customer; 64,302.000 oz (2,000 klilobars)

iii) Into Malca 96,453.000 oz (5000 kilobars)

total weight: 160.755.000 oz (7.000 tonnes)

total weight dealer and customer; 7.8807 tonnes

xxxxxxxxxxxxxxxxI

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 0

xxxxxxxxxxxxxxxxxx

adjustments: customer to dealer: 2 entries

i)Brinks 321,477.849 oz

ii) Malca: 108,509.621 oz oz

AMOUNT OF GOLD STANDING FOR MARCH

THE FRONT MONTH OF MARCH HAD A LOSS OF 274 CONTRACTS TO STAND AT 397. WE HAD 366 CONTRACTS SERVED ON MONDAY SO WE GAINED 92 CONTRACTS FOR 9200 OZ (.2861 TONNES AS A PHYSICAL GOLD QUEUE JUMP. THIS IS CENTRAL BANKS LOOKING FOR BADLY NEEDED GOLD

APRIL HAD A LOSS OF 55,799 CONTRACTS DOWN TO 164,807 CONTRACTS AS THIS MONTH BECOMES THE FRONT MONTH. WE HAVE 4 MORE READING DAYS BEFORE FIRST DAY NOTICE, MONDAY MARCH 31.

MAY GAINED 385 CONTRACTS UP TO 1764.

We had 384 contracts filed for today representing 38,400oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 384 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 25 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

T o calculate the INITIAL total number of gold ounces standing for MARCH /2025. contract month, we take the total number of notices filed so far for the month (18,731 X 100 oz ) to which we add the difference between the open interest for the front month of MARCH (397 CONTRACTS) minus the number of notices served upon today (384 x 100 oz per contract) equals 1,874,400 OZ OR 58.3017 TONNES to which we add our .7775 tonnes exchange for risk//new total tonnage standing: 59.0792 tonnes

thus the INITIAL standings for gold for the MARCH contract month: No of notices filed so far (18,731x 100 oz +we add the difference for front month of MARCH (397 OI} minus the number of notices served upon today (384 x 100 oz) which equals 1,874,400 OZ OR 58.3017 TONNES + .7775 ex for risk //new total 59.0792 tonnes

TOTAL COMEX GOLD STANDING FOR MARCH.: 59.0792 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND MARCH IS FOLLOWING SUIT..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,972, 118.482 oz 61.34 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 42,533,452.870 .oz

TOTAL REGISTERED GOLD 21,454,006.855 or 667.309 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 21,099,446.015 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 19,481888oz (REG GOLD- PLEDGED GOLD)= 605.96tonnes //

END

SILVER/COMEX

// THE MARCH 2025 SILVER CONTRACT//INITIAL

MARCH 25

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | withdrawals 1 Loomis: 80,754.940 oz |

| Deposits to the Dealer Inventory | 0 i) 0 entries total dealer 0 oz |

| Deposits to the Customer Inventory | 5 entries i) Into CNT 1,199,531.397 oz ii) Into Delaware 441,701.200 oz iii) Into JPMorgan; 1,177,971.300 oz iv) Into Loomis 322,725.100 oz v) Into Manfra 321,872.912 oz total weight: 3,463.801.709 oz |

| No of oz served today (contracts) | 50 CONTRACT(S) (0.250 MILLION OZ |

| No of oz to be served (notices) | 856 contracts (4.280 MILLION oz) |

| Total monthly oz silver served (contracts) | 15,343 Contracts (76.715 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 entries

total dealer 0 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

5 entries

i) Into CNT 1,199,531.397 oz

ii) Into Delaware 441,701.200 oz

iii) Into JPMorgan; 1,177,971.300 oz

iv) Into Loomis 322,725.100 oz

v) Into Manfra 321,872.912 oz

total weight: 3,463.801.709 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals 1

1 entries

i) Out of Loomis: 80,754.940 oz

total withdrawal 80,754.940 oz

ADJUSTMENTs 8 entries//7 customer to dealer:

a) Brinks 2,174,438.043 oz

b) Out of CNT 1125,604.400 oz

c) Out of Delaware: 145,107.902 oz

d) Out of HSBC 4940.300 oz

e) Out of JPMorgan: 9,449,376.730

f) Out of Malca 2,261,534.4 oz

g) Out of Manfra 3,381,171.856

h) customer to dealer Asahi 15,011.650 oz

total adjustment net out of dealer to customer 13.527 million oz/

JPMorgan has a total silver weight: 185.683million oz/463.574oz million or 39.91%

TOTAL REGISTERED SILVER: 143.061 MILLION OZ//.TOTAL REG + ELIGIBLE. 463.534Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH /2025 OI: 906 OPEN INTEREST CONTRACTS FOR A LOSS OF 143 CONTRACTS.WE HAD 106 CONTRACTS SERVED ON MONDAY SO WE LOST A SMALL 37 CONTRACTS OR 0.185 MILLION OZ UNDERWENT AN EFP TRANSFER TO LONDON LOOKING FOR METAL OVER ON THE LONDON SIDE OF THE POND. WE MUST NOW ADD THAT CRAZY 70 CONTRACT EX FOR RISK/PRIOR FOR 350,000 OZ. THE BANK OF ENGLAND OR ANOTHER OFFICIAL ENTITY IS ASSUMING THE RISK OF DELIVERY AND THE COUNTERPARTY ARE BULLION BANKS WHO CANNOT GUARANTEE DELIVERY.

APRIL SAW A LOSS OF 16 CONTRACTS TO STAND AT 2480

MAY SAW A LOSS OF 677 CONTRACTS DOWN TO 124,649 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 50 or 0.250 MILLION oz

CONFIRMED volume; ON MONDAY 36,226 small//

AND NOW MARCH DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 15,343 X5,000 oz = 76.715 MILLION oz

to which we add the difference between the open interest for the front month of MAR (906) AND the number of notices served upon today (50 )x (5000 oz)

Thus the standings for silver for the MARCH 2025 contract month: (15,343) Notices served so far) x 5000 oz + OI for the front month of MAR(906) minus number of notices served upon today (50)x 5000 oz equals silver standing for the MARCH contract month equating to 80.995 MILLION OZ TO WHICH WE ADD .350 MILLION OZ EX FOR RISK//NEW TOTAL 81.345 MILLION OZ//(CME TOTALS CORRECTED FOR TUESDAY)

New total standing: 81.345 million oz which is huge for this very active delivery month of March.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 151.518million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

MARCH 21 WITH GOLD DOWN $20.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 910.43 TONNES

MARCH 20 WITH GOLD UP $3.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 909.28 TONNES

MARCH 19 WITH GOLD UP $0.45 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 907.27 TONNES

MARCH 18 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 907.27 TONNE

MARCH 17 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.64 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 906.41 TONNES

MARCH 14 WITH GOLD UP $9.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MONSTER DEPOSIT OF 7.17 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 905.81 TONNES

MARCH 13 WITH GOLD UP $42.85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 12 WITH GOLD UP $22.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.90 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 895.20 TONNES

MARCH 11 WITH GOLD UP $21.20 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 891.30 TONNES

MARCH 10 WITH GOLD DOWN $12.45 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 894.317 TONNES

MARCH 7 WITH GOLD DOWN $12.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 6 WITH GOLD UP $2.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 900.30 TONNES

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

GLD INVENTORY: 92907 TONNES, TONIGHTS TOTAL

SILVER

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

MARCH 21 WITH SILVER DOWN $0.45 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 442.962 MILLION

MARCH 20 WITH SILVER DOWN $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 19 WITH SILVER DOWN $0.45 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.219 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 18 WITH SILVER UP $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.823 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.373 MILLION

MARCH 17 WITH SILVER UP $0.03 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.096 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 439.550 MILLION

MARCH 14 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.910 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.454 MILLION

MARCH 13 WITH SILVER UP $0.46 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.774 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 434.544 MILLION

MARCH 12 WITH SILVER UP $0.57 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.032 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 435.318 MILLION

MARCH 11 WITH SILVER UP $0.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.816 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 436.410 MILLION

MARCH 10 WITH SILVER DOWN 25 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.276 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.591 MILLION

MARCH 7 WITH SILVER DOWN 40 CENTS/HUGL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.184 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 434.317 MILLION

MARCH 6 WITH SILVER UP 16 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.455 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.046 MILLION

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

CLOSING INVENTORY 454.883 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

Alasdair Macleod..

2. Egon Von Greyerz et al

ALASDAIR MACLEOD….

Gold’s open interest on Comex declines

Preliminary open interest on Comex fell a further 11,497 contracts yesterday, yet the price has held up above $3000 ahead of tomorrow’s option expiry. What does this mean?

| Alasdair MacleodMar 25∙Paid |

Despite gold remaining close to all-time highs, the chart above shows Open Interest falling when reasonably it should be somewhat higher to reflect current bull market conditions. The next chart, which includes the price shows how the price tends to march on regardless of Open Interest on Comex:

The underlying point is that Comex speculators have yet to take a bullish stance. Yet the price is running away.

If it’s not the speculators buying, then it must be a squeeze on the shorts. But normally, in the last week of contract expiry, acting in unison the shorts succeed in marking prices lower, triggering long stops, and making call options expire worthless. We have seen this reflected in the modest price decline since last Thursday’s high. But so far, that decline has been trifling considering the decline in Open Interest.

There may be a final attempt to get gold under $3000 before April options last day trading tomorrow. There are 6,592 option contracts at that exercise price to be made worthless, and a further 3,200+ on exercise prices down to $2975.

Interestingly, the general lack of interest in the futures is also reflected in low option turnover, as the next chart shows:

To summarise, despite the spectacular rise in the gold price in recent months, the undertone remains remarkably firm. Therefore, any dip below $3000 represents an opportunity to buy the June contract before the rest of the investment universe wakes up to the consequences of a continuing bear squeeze in gold futures markets.

3. C Powell and Gata dispatches”

Interviewed by Mike Maharrey, G. Edward Griffin exposes the Federal Reserve

Submitted by admin on Sun, 2025-03-23 19:21 Section: Daily Dispatches

By Mike Maharrey

Money Metals Exchange, Eagle, Idaho

Friday, March 21, 2025

In a riveting and candid conversation on the Money Metals Podcast, host Mike Maharrey sat down with G. Edward Griffin, the prolific author best known for “The Creature from Jekyll Island,” a book that has shaped modern understandings of the Federal Reserve and its shadowy origins.

From secretive meetings among powerful bankers to the implications of programmable digital currencies, Griffin offered insights from decades of research, revealing a system he calls “a legal cartel” and “a criminal organization.

Griffin explained that the Federal Reserve is not a government agency, as most Americans believe, but a private banking cartel formed under the Federal Reserve Act of 1913. It was designed to appear governmental — complete with a name implying federal oversight — but, in practice, is independent from Congress and operates in the interest of its member banks.

The Fed’s inception was cloaked in secrecy. Griffin recounted how, in 1910, powerful bankers including Paul Warburg, and Sen. Nelson Aldrich boarded a private railcar under strict secrecy protocols and traveled to Jekyll Island, Georgia.

There, at a private resort owned by some of the richest industrialists of the era, they drafted what would become the blueprint for the Federal Reserve System. …

… For the remainder of the report and the podcast:

end

Robert Lambourne: After hedge funds and Treasury’s dealers, who’s left to buy U.S. debt?

Submitted by admin on Sat, 2025-03-22 14:34 Section: Daily Dispatches

By Robert Lambourne

Saturday, March 22, 2025

The U.S. Treasuries market today is evoking a maxed-out credit card.

The end of “quantitative tightening” by the Federal Reserve seems imminent, apparently to be rapidly replaced by another round of “quantitative easing.”

Hedge funds have continued to be buyers of Treasuries and apparently have been incentivized to hold them. In particular as we covered in late 2023, some of these funds have been able to set up profitable and essentially risk-free basis trades by simultaneously holding Treasury bonds and a short position in Treasury futures to offset their exposure.

Both the Bank for International Settlements and the International Monetary Fund have issued reports on these hedge fund holdings, long and short, and the basis trades.

Given the current chaos in U.S. capital markets, it seems hard to expect overseas investors to hold U.S. Treasuries other than short-term ones.

That hedge funds were recently reported by the International Monetary Fund to be holding 11% of Treasuries highlights how important hedge funds have become as investors. This raises suspicion that the hedge funds have been offered incentives to buy Treasuries and that they may be the buyers of last resort apart from the Federal Reserve.

Understanding this situation is important for investors in gold since it seems that a tipping point is near. Either the U.S. federal government debt is funded by way of “quantitative easing” or some sort of gold price reset is engineered to enable enough repayment of debt to return it to a more normal level.

Either course seems likely to result in much higher gold prices, and it is possible that prices could rise far higher than ordinarily might seem plausible. Years of official gold price suppression policy are behind this.

… Hedge fund buying in 2022 as QT commenced …

A GATA dispatch on October 22, 2023 –

— considered whether the commencement of QT in June 2022 was driven by hedge funds using a basis trade whereby they acquired not only Treasuries but also equivalent short positions in them.

This chart –

— is from that dispatch and tracked on a weekly basis the level of net short positions in U.S. Treasury futures (in blue) and the decline in the holdings of U.S. Treasuries held by the Federal Reserve from the peak holding on June 8, 2022 — $5,771.4 billion (in green). The starting date for both lines is the week commencing March 20, 2022, when the Fed’s assets were reported to be at the highest in total, at $9,012 billion on March 23, 2022.

Visually there appears to be a strong correlation between the two and suggests that hedge fund involvement was important to allow QT to proceed smoothly.

The dispatch concludes:

“The possibility that U.S. monetary authorities have tacitly engineered and supported a policy of encouraging what regulators, including the Fed itself, consider to be a risky trade, with hedge funds holding highly leveraged short positions in Treasury futures, is perhaps a reason to query whether U.S. Treasury bonds represent the safest investment category globally. The answer perhaps depends on whether the chart reveals a strange coincidence or is a sign of an effort to ease the passage of QT.”

Another GATA dispatch on this topic was issued on December 23, 2023:

This dispatch considers the substantial profits made by the hedge funds as a reward for assisting QT and concludes:

“If, as seems very possible, the fantastic profits made by the hedge funds involved in the basis trade arose largely from explicit or tacit cooperation with the Federal Reserve or the Treasury Department or both to get QT done, the U.S. financial system and the government agencies running it would be rigging markets and corrupt and deceptive in still another way.”

… More recent updates from the IMF on hedge fund buying of Treasuries …

The IMF Global Financial Stability report from April 2024 notes that hedge funds held more than 7% of outstanding Treasuries and that leveraged fund positions had been increased.

Two charts from the IMF report highlight the importance of hedge fund buying of Treasuries from Q3 2022 to Q4 2023, with hedge funds buying accounting for more than the total sales by the Federal Reserve —

— and hedge fund ownership of the Treasuries market exceeding 7%:

The topic of basis trades was clearly of interest to the IMF, and its report notes that “Federal Reserve Board staff, using proprietary data sets, find that the volume of the basis trade is likely significantly lower than that implied by leveraged funds’ Treasury futures positions alone, and estimate that hedge funds have increased basis trade activities by at least $317 billion since Q1 2022.”

This appears to be a tepid point and it seems clear that hedge funds very much became the major buyer of Treasuries when QT was underway. So the suspicion remains that hedge funds were prepared to undertake these purchases because of the opportunity to engage in a profitable basis trade. Whether this trade was created for them remains an open question.

The next edition of the IMF Global Financial Report, issued in October 2024, has the following chart:

It highlights that hedge funds had risen to holding 11% of the Treasuries market and furthermore that primary dealers in Treasury securities were also holding a further 5% of the market. Hence, approximately one sixth of the Treasury securities that have been issued are owned by these two groups.

… Outlook for the Treasuries market …

This reliance on hedge funds and primary dealers seems to imply that the Fed and the Treasury Department have run out of new investor groups to buy Treasuries.

It is hard to envisage any increase in purchases by foreign investors, especially given the alarm over tariffs and the recently published document from the White House on inward investment –

— which makes clear that investment from China is not welcome.

In this context last week’s Federal Reserve meeting indicates that changes are coming. This report from Reuters sets out that QT seems to be shutting down and that QE, as far as the Treasuries market is concerned, may be about to restart:

Hence it seems that there is now a general recognition in the Fed and the Treasury Department that the only way to increase federal government borrowing henceforth is for the Fed to buy bonds.

So the time may have arrived for the authorities to consider whether a gold price reset is a better way forward.

For gold investors it seems that whatever path is chosen, gold is likely to rise in price.

The risks of gold confiscation need to be considered, along with whether there are multiple claims on gold held in exchange-traded funds and other funds. These risks argue for a cautious approach to investment in gold, with a clear preference for holding actual metal.

Also needing to be considered is the possibility that China — which appears to be in a depression, weighed down by high debt, especially in the property sector — may decide to reset the gold price. China might act without warning as a counter to what its leadership sees as hostile acts from abroad.

—-

Robert Lambourne is a retired business executive in the United Kingdom who consults for GATA about the involvement of the Bank for International Settlements in the gold market and about U.S. government debt.

* * *

* * *

4. ANDREW MAGUIRE PODCAST

a must view…

Episode 215

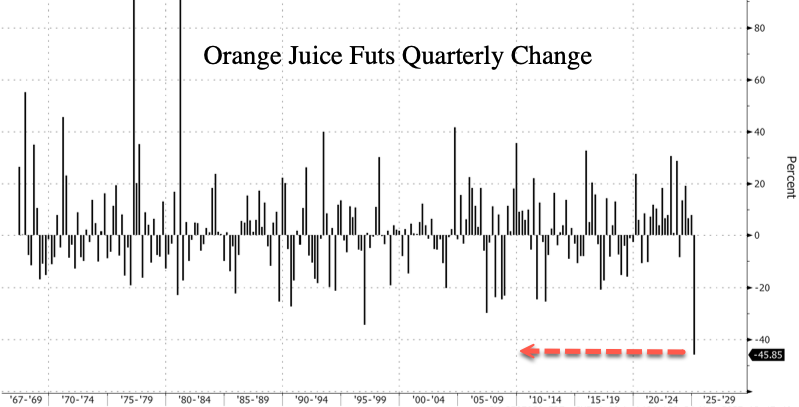

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY//ORANGE JUICE

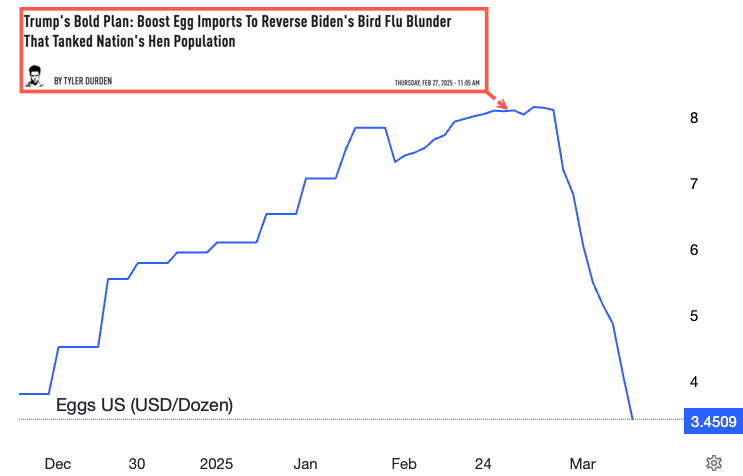

First Eggs, Now Orange Prices Crash Most In Half Century

Monday, Mar 24, 2025 – 08:30 PM

Prices for some of the most common breakfast staples have fallen over the past month. While attention has primarily focused on President Trump’s countermeasures — which have helped arrest the rise in egg prices and send them tumbling in recent weeks — orange juice prices are now on track to post their sharpest quarterly decline in over 50 years.

Bloomberg data shows that if losses of 45% persist through the end of the month, the first quarter would mark the largest quarterly decline since the second quarter of 1967.

Prices have been halved from $5 a pound in mid-December to around $2.50.

As we previously mentioned in December, prices hovered over $5 on production figures in Florida, sliding to 1930 levels. There are shifting consumer behavior trends of falling demand for the sugary citrus drink usually paired with eggs and bacon.

Data from Nielsen and the Florida Department of Citrus show a 7% drop in juice volumes sold this season through February. The latest drop adds to the ongoing trend of shifting consumer habits, with orange juice consumption halved since the DotCom peak.

In addition to plunging OJ prices, egg prices have been more than halved in just a few weeks after President Trump announced a plan to offset a loss of domestic production following Biden-Harris’ reckless culling of 150 million egg-laying hens.

Breakfast is about to become cheaper in the weeks ahead.

6 CRYPTOCURRENCY NEWS

ASIA TRADING TUESDAY MORNING MONDAY NIGHT

SHANGHAI CLOSED DOWN 0.05 PTS OR 0.00%

//Hang Seng CLOSED DOWN 561.31 PTS OR 2.35%

// Nikkei CLOSED UIP 172.05 OR .46 %//Australia’s all ordinaries CLOSED UP 0.11%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2595 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2613/ Oil UP TO 6944 dollars per barrel for WTI and BRENT UP TO 73.40 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAkER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TYUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2595

OFFSHORE YUAN: DOWN TO 7.2616

SHANGHAI CLOSED CLOSED DOWN 0.05 PTS OR 0.00%

HANG SENG CLOSED CLOSED DOWN 561.31 PTS OR 2.35%

2. Nikkei closed

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 103.72// EURO RISES TO 1.0823 UP 26 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: RISES TO. +1.558//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.10…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP[ TO +2.8285/Italian 10 Yr bond yield UP to 3.920 SPAIN 10 YR BOND YIELD UP TO 3.424

3i Greek 10 year bond yield UP TO 3.620

3j Gold at $3023.00 Silver at: 33.47 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 50 /100 roubles/dollar; ROUBLE AT 84.37

3m oil into the 69 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.10 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.558 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8817 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9547 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.358 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.6960 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.043 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 37.99…

10 YR UK BOND YIELD: 4.7990 UP 8 PTS

10 YR CANADA BOND YIELD: 3.097 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.729 UP 2 PTS.

2a New York OPENING REPORT

Futures Rise As Global Markets Extend Monday’s Torrid Rally

Tuesday, Mar 25, 2025 – 08:21 AM

US equity futs are little changed, erasing a modest loss earlier in the session when investors took some profits from yesterday’s torrid rally which pushed the S&P 1.8% higher. As of 8:00am ET, S&P and Nasdaq futures are both up 0.2%, with Mag 7 stocks all higher pre-market, led by TSLA (+1.4%). European stocks gained as the Estoxx 50 rises 1.1% led by energy and financials, although Asian stocks dropped for a third straight day of losses, driven by Chinese tech shares trading in Hong Kong slid 2.6%, weighed down by a drop in Xiaomi after its $5.5 billion share sale. Investors were also rattled by Trump’s new threat of “secondary tariffs” on countries that buy oil from Venezuela. Bond yields are 1-3bp higher. Commodities are mostly higher led by precious metals (silver) and oil. WTI crude oil futures add about 0.5% to Monday’s 1.2% gain. Today, we will receive consumer confidence at 10am ET (est 94.0 survey vs. 98.3 prior).

In premarket trading, Tesla whipsawed, first sliding as data showed fresh sales declines in Europe, only to rebound 1.4% higher making it the top gainer among the Mag7 stocks (Alphabet +0.3%, Amazon +0.1%, Apple +0.05%, Microsoft +0.1%, Meta +0.5%, Nvidia -0.4% and Tesla +1.4%). Ally Financial declines 2% after BTIG downgraded the auto-lender to sell, projecting that the company won’t meet its net interest margin and return on equity targets in the near term due to macroeconomic headwinds and increased competition. Carvana rises 4% after Morgan Stanley raised the used-car retailer to overweight, saying the pullback in shares creates an attractive entry point for the used-car retailer. Here are some other notable premarket movers:

- Cloudflare (NET) climbs 6% as BofA double-upgrades the software company to buy on improving fundamentals, saying it’s set to be an “AI winner.”

- Faraday Future (FFAI) climbs 13% after the mobility ecosystem company secured $41m in new cash financing commitments.

- KB Home (KBH) falls 9% after the homebuilder cut its fiscal 2025 revenue guidance amid a soft start to the spring selling season.

- McCormick (MKC) slips 3% as the maker of spices posted 1Q profit that missed expectations.

- Mobileye Global (MBLY) gains 9% after Volkswagen Group said it is working with the maker of software and hardware technologies for automobiles to enhance driver assistance in future MQB vehicles.

- Oklo (OKLO) slides 7% after the nuclear fission reactors firm reported disappointing quarterly results.

- Smithfield Foods Inc. (SFD) rises 3% after the world’s largest pork producer said it expects 2025 sales growth in the “low-to-mid-single-digit percent range”.

- Trump Media (DJT) jumps 7% after signing a non-binding agreement to partner with Crypto.com for a series of ETFs through its Truth.Fi brand.

- UniFirst (UNF) drops 10% after Cintas (CTAS) terminated discussions to acquire the workplace uniform rental company.

Markets have been unnerved by a fresh tariff salvo from Trump, who threatened a 25% levy on any nation purchasing crude from Venezuela. Brent crude rose 0.5%, adding to Monday’s gain. Trump also said he will announce tariffs on automobile imports in the coming days — and indicated nations will receive breaks from next week’s “reciprocal” tariffs, further adding to confusion about the plan for sweeping levies to kick in on April 2.

“Between now and the 2nd of April, it’s just a phase of wait and see,” said Michael Nizard, head of multi-asset at Edmond de Rothschild Asset Management. “If Trump is doing exactly what he’s saying in terms of reciprocal tariffs, it should be negative both for Wall Street and Main Street.”

Investors also remain unclear on how tariffs might impact inflation and economic growth, with most recent data hinting at softer economic momentum alongside still-elevated price pressures. While swaps still price the Federal Reserve to cut rates twice this year, Atlanta Fed chief Raphael Bostic said Tuesday he sees just one 25 basis-point reduction, due to “very bumpy” inflation.