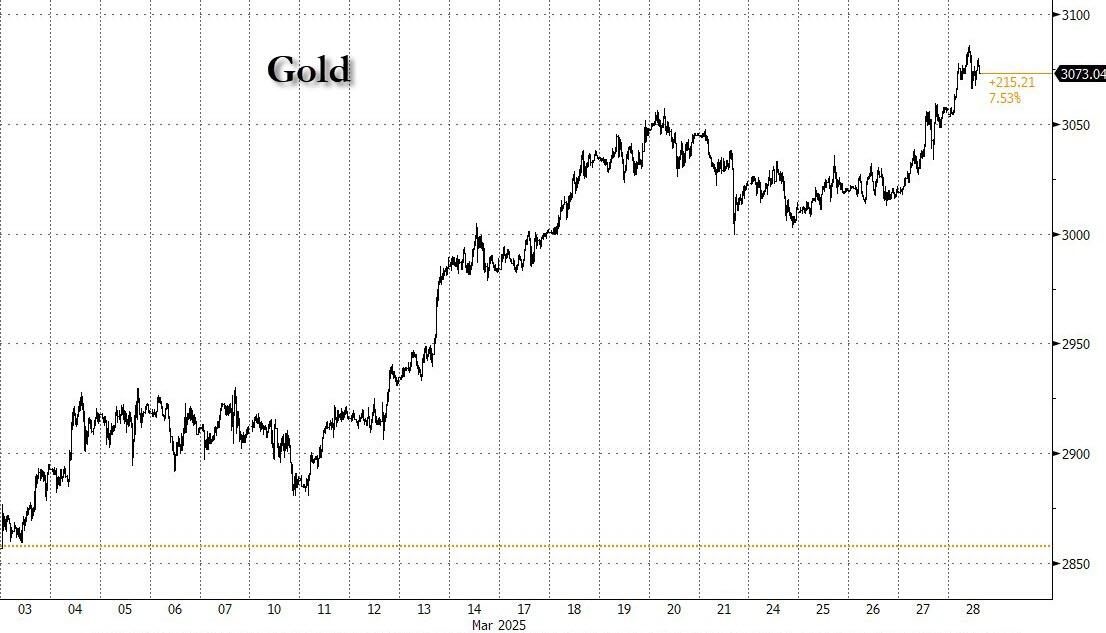

GOLD CLOSED UP $42.45 TO $3080.95

SILVER CLOSED DOWN $0.21 TO $34.24

GOLD ACCESS CLOSED 3080.30

Silver ACCESS CLOSED: $33.98

Bitcoin morning price:$85062 DOWN 2272 DOLLARS.

Bitcoin: afternoon price: $83664 down 3670 DOLLARS

Platinum price closing UP $1.10 TO $984.35

Palladium price; DOWN $1.60 TO $976.30

END

*CANADIAN GOLD: $4412.04 UP 40.54 CDN dollars per oz( * NEW ALL TIME HIGH 4412.04 CDN DOLLARS PER OZ//MARCH 28 2025)

*BRITISH GOLD: 2380.32 UP 21.16 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,380.32 BRITISH POUNDS/OZ) MARCH 28/2025

*EURO GOLD: 2,846.26 UP 17.57 Euros per oz //* (ALL TIME CLOSING HIGH: 2,846.20 EUROS PER OZ/MARCH 28 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,060.200000000 USD

INTENT DATE: 03/27/2025 DELIVERY DATE: 03/31/2025

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 497

624 H BOFA SECURITIES 521

709 C BARCLAYS 18

905 C ADM 6

TOTAL: 521 521

JPMORGAN stopped 0/521 contracts

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2024. CONTRACT: 521 NOTICES FOR 52,100 OZ 1.620 TONNES

total notices so far: 19,149 contracts for 1,939,800 Oz (60.33 tonnes)

FOR MARCH

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 202 NOTICE(S) FILED FOR 1.010 MILLION OZ/

total number of notices filed so far this month : 16,149 for 80.745 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $42.45 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A SMALL DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 929.65 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $.21 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: //A WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 447.422 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA HUGE SIZED 3711 CONTRACTS TO 172,497 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0,60 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. WE HAD A MEGA MEGA HUGE SIZED GAIN OF 5269 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE//THURSDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS PLUS SOME MONTH END SPREADER LIQUIDATION ON THURSDAY COMEX TRADING / AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED HUGELY ON THURSDAY WITH SILVER’S GAIN IN PRICE AND WE ARE RIGHT NOW AT THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. WE HAD A HUGE T.A.S. LIQUIDATION AND COMMENCEMENT OF MONTH END SPREADER LIQUIDATION THURSDAY. BUT THIS WAS COUPLED WITH A STRONG T.A.S. ISSUANCE OF 579 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS METALS WILL COMMENCE AGAIN! WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND $0.99 AND A LEASE RATE OF 7.3%. WE HAD A HUGE 1558 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 579 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TODAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUMONGOUS SIZED 5269 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE. WE HAD CONSIDERABLE TAS LIQUIDATION/MONTH END SPREADER LIQUIDATION THROUGHOUT THURSDAY’S COMEX TRADING SESSION WHICH ACCOUNTS FOR A HUGE PORTION IN THE NUMBERS OF OI ON OUR TWO EXCHANGES.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER. AT 3 AM WE ARE EXACTLY AT $34.40

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT/FRIDAY MORNING: A STRONG 579 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.60 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE GAIN IN PRICE AND A GAIN IN OPEN INTEREST FROM OUR TWO EXCHANGES OF 5269 CONTRACTS. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS//MONTH END SPREADERS TRYING TO CONTAIN SILVER’S PRICE RISE AND THAT ACCOUNTS FOR ALL OF OUR OPEN INTEREST GAINS. HOWEVER THE CME NOTIFIED US THAT FOR THE FIRST TIME IN MARCH, WE HAVE BEEN ISSUED 70 CONTRACTS OF EXCHANGE FOR RISK FOR 350,000 OZ. THIS TOTAL WILL BE ADDED TO OUR REGULAR DELIVERY TOTALS FOR MARCH.

WE HAD A 1558 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 78.753 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0.150 MILLION OZ EFP TRANSFER TO LONDON TO WHICH WE ADD .350 EXCHANGE FOR RISK

INITIAL STANDING FOR MARCH REDUCES TO 81.095 MILLION OZ

WE HAD:

/ HUGE COMEX OI GAIN+// A HUGE SIZED EFP ISSUANCE (1558 CONTRACTS)/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 579 CONTRACTS)/A 70 CONTRACT EX. FOR RISK FOR 350,000 OZ/SECOND WEEK OF MARCH

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED 56 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR

TOTAL CONTRACTS for 20 DAYS, total 13,004 contracts: OR 65.020 MILLION OZ (652 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 65.020 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 65.020 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A MEGA HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3711 CONTRACTS WITH OUR GAIN IN PRICE OF 60 CENTS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE 1558 CONTRACT EFP ISSUANCE CONTRACTS: 1558 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MARCH OF 78.455 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 0.105 MILLION OZ E.F.P. TRANSFER JUMP TO LONDON/

NEW STANDING REDUCES TO 80.745 MILLION OZ + .350 EX. FOR RISK//NEW TOTAL 81.095 MILLION OZ.

WE HAVE 1). A HUMONGOUS SIZED GAIN OF 5269 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR HUGE GAIN IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 579 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//CONSIDERABLE FRONT END OF THE TAS CONTRACTS/MONTH END SPREADERS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION. HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON THURSDAY WITH OUR GAIN IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE THURSDAY NIGHT (579 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 202 NOTICE(S) FILED TODAY FOR 1.010 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 4554 OI CONTRACTS TO 512,637 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A LARGE SIZED 2302 CONTRACTS//

WE HAD A STRONG SIZED INCREASE IN COMEX OI (4554 CONTRACTS) OCCURRED WITH OUR STRONG GAIN OF $31.60 IN PRICE THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 31.757 TONNES FOLLOWED BY TODAY’S STRONG 52,000 OZ QUEUE JUMP (1.6174 TONNES), ////NEW STANDING ADVANCES TO 60.33 TONNES + 6.8429 TONNES EX FOR RISK + ..7775 EX FOR RISK/PRIOR = 67.9479 TONNES

/NEW STANDING FOR MARCH; 60.33 TONNES + 7.6179 TONNES EX FOR RISK= 67.9479 TONNES

/ ALL OF THIS HAPPENED WITH OUR $31.60 GAIN IN PRICE WITH RESPECT TO THURSDAY’S COMEX ///. WE HAD A STRONG SIZED GAIN OF 6754 OI CONTRACTS (21.00 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE FRONT MARCH CONTRACT MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2033 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 512,637

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6754 CONTRACTS WITH 4554 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 2033 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6754 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A GOOD SIZED AND CRIMINAL 1328 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2033 CONTRACTS) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 4554 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 6754 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MARCH 31.757 TONNES FOLLOWED BY TODAY’S 1.6174 TONNES QUEUE JUMP. TO WHICH WE MUST ADD OUR NEW 7.6179 TONNES OF EX FOR RISK ON OUR THREE OCCASION ISSUANCES THIS MONTH.

//NEW STANDING ADVANCES TO 60.33 TONNES + 7.6179 = 67.9479 TONNES

//NEW STANDING MARCH: 67.9479 TONNES

.

/ 3) HUGE T.A.S. LIQUIDATION + MONTH END SPREADERS TRYING TO LOWER GOLD’S PRICE TUESDAY WITH ZERO SUCCESS IN REMOVING NET SPECULATOR LONGS, AS WE HAD 1) $31.60 COMEX PRICE GAIN AND WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG GAIN OF 6754 CONTRACTS ON OUR TWO EXCHANGES (ALL DUE TO T.A.S. LIQUIDATION/MONTH END SPREADERS ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN MARCH. ALL OF THE GAIN IN OI WAS DUE TO THE HUGE NUMBER OF T.A.S. LIQUIDATION/MONTH END SPREADER LIQUIDATION THURSDAY.

4) STRONG SIZED COMEX OPEN INTEREST INCREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///GOOD T.A.S. ISSUANCE: 1328 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH :

TOTAL EFP CONTRACTS ISSUED: 39,518 CONTRACTS OF 3,951,800 OZ OR 122.917 TONNES IN 20 TRADING DAY(S) AND THUS AVERAGING: 1976 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES 122.917 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 122.917 DIVIDED BY 3550 x 100% TONNES = 3.46% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 122.917 TONNES//QUITE SMALL THIS MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 3711 CONTRACTS OI TO 172,497 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1558 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1558 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1558 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3711 CONTRACTS AND ADD TO THE 1558 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 5269 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 27.135 MILLION OZ

OCCURRED WITH OUR HUGE $0.60 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

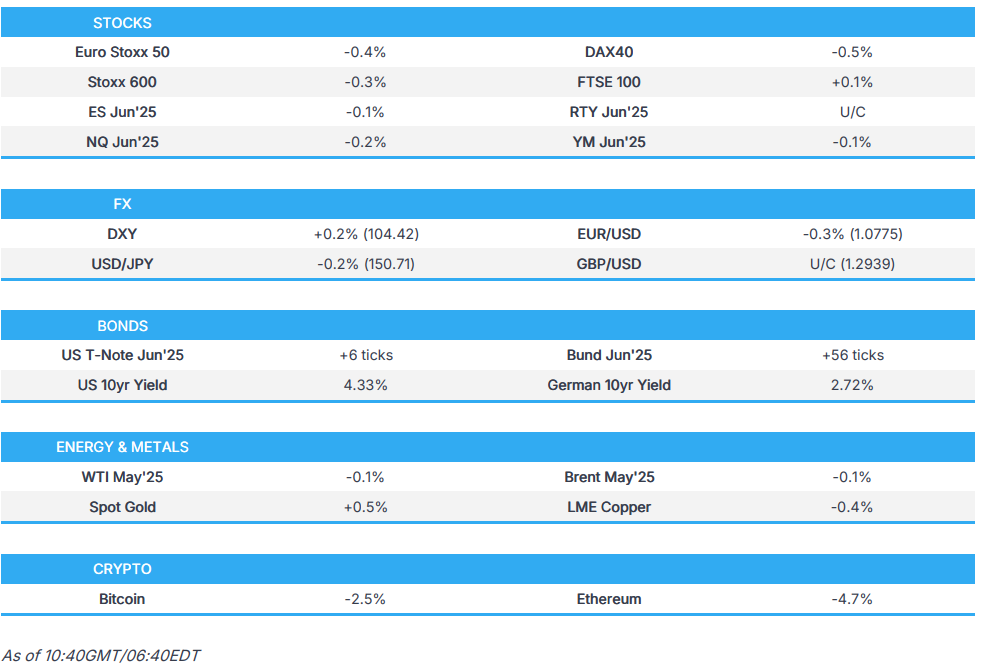

2.ASIAN AFFAIRS FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 22.44 PTS OR 0.67%

//Hang Seng CLOSED DOWN 152.20 PTS OR 0.65%

// Nikkei CLOSED DOWN 679.64 OR 1.80 %//Australia’s all ordinaries CLOSED UP 0.12%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2646 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2758/ Oil UP TO 69.92 dollars per barrel for WTI and BRENT UP TO 73.99 Stocks in Europe OPENED ALL MOSTLY RED.

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAkER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

END

ASIA TRADING FRIDAY MORNING/THURSDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 4554 CONTRACTS TO 512,637 WITH OUR HUGE GAIN IN PRICE OF $31.60 WITH RESPECT TO THURSDAY’S TRADING/. WE LOST ZERO NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2033 ).

THE CME ANNOUNCED THURSDAY NIGHT,A MASSIVE 2200 EXCHANGE FOR RISK CONTRACTS FOR 220,000 OZ OR 6.8429 TONNES. LAST THURSDAY WAS THE FIRST ISSUANCE FOR MARCH FOR .4665 TONNES .ON TUESDAY, MARCH 25 WE HAD OUR 2ND ISSUANCE OF 100 CONTRACTS FOR A TOTAL OF .3110 TONNES. AND NOW WE HAVE OUR 3RD AND FINAL ISSUANCE FOR MARCH. THUS TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH EQUALS: 7.6179 TONNES OF GOLD WHICH WILL BE ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY: WE HAD FIVE EXCHANGE FOR RISKS IN GOLD, TOTALLING 18.4527 TONNES!. THE RECIPIENT OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 4TH CONSECUTIVE ISSUANCE FOR EXCHANGE FOR RISK ISSUANCE!!.

THUS IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 6754 CONTRACTS WITH OUR GAIN IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF MARCH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY TODAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION// THROUGHOUT THE WEEK. THEY ISSUED LAST NIGHT A GOOD SIZED 1328 CONTRACTS. THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING A LOWER COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH YESTERDAY’S TOTALS.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, , 203 , ,205 , 207 209 AND 211 212 213,215 AND FRIDAY’S 216 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF MARCH .… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2033 EFP CONTRACTS WERE ISSUED: : /APRIL 2033 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2033 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6754 CONTRACTS IN THAT 2033 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG GAIN OF 4554 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF $31.60 FOR THURSDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. MUCH+ OF THE TOTAL GAIN IN OUR TWO EXCHANGES WAS DUE TO THE LIQUIDATION OF T.A.S. CONTRACTS.(GOVERNMENT) AND MONTH END SPREADERS!

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A GOOD SIZED 1328 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER 4 WEEKS AGO AND AGAIN LAST WEEK,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND NOW ,THIS MONTH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT LAST WEDNESDAY MARCH 17, THE 38,393 T.A.S. CONTRACT ISSUANCE WAS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY DOES TWO IMPORTANT THINGS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH

STANDING FOR GOLD FOR THE PAST 4 PLUS YEARS:

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: MARCH (67.9479 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE MARCH DELIVERY MONTH / FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH.

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

AND NOW MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 51 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES.

MARCH: 67.9479 TONNES (INCLUDES .7775 TONNES EX FOR RISK)

COMEX GOLD TRADING/MARCH CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $31.60/)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION THURSDAY AS WELL AS COMMENCEMENT OF MONTH END SPREADER LIQUIDATION/ AS THEY WERE TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,000 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING AND THEY FAILED MISERABLY AS GOLD IS NOW WELL ABOVE THE $3,000 THRESHOLD AT 3,083 PLUS.

LAST NIGHT/FRIDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH MARCH TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND IS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

NOW MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK:

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

STANDING NOW FOR MARCH:

MARCH: 60.33 TONNES +(6.8429 EX FOR RISK MARCH 28+ .7775 TONNES EX FOR RISK/PRIOR TOTAL EX FOR RISK 7.6179) = 67.9479 TONNES

WE HAVE GAINED A FAIR SIZED TOTAL OF 21.00 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MARCH (31.753TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 52,000 OZ OR 1.6174 TONNES: NEW TOTAL STANDING 60.33 TONNES TO WHICH WE ADD OUR 7.6179 TONNES OF EXCHANGE FOR RISK//NEW TOTAL: 67.9479 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $31.60

WE HAD 2302 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL

NET GAIN ON THE TWO EXCHANGES 6754 CONTRACTS OR 675400 0Z (21.00 TONNES)

confirmed volume THURSDAY 327,891 contracts: good///

//speculators have left the gold arena

END

MARCH

// THE MARCH 2025 GOLD CONTRACT

MARCH 28

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entry . zero entry |

| Deposit to the Dealer Inventory in oz | 1 ENTRY i) Into ASAHI dealer 32,118.949 oz (999 kilobars) total weight in tonnes: 0.999 tonnes |

| Deposits to the Customer Inventory, in oz | we have 4 customer entries we have 4 customer deposits i) into JPMorgan customer acct 241.325 oz (75 kilobars) ii) Brinks 16,008.643 oz ii) Malca: 67,002.684 oz (2084 kilobars) iv) Manfra: 61,772.328 oz total customer weight: 147,194.980 oz or 4.578 tonness total weight dealer and customer; 5.577 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 521 notice(s) 52,100 OZ 1.620 TONNES |

| No of oz to be served (notices) | 0 contracts 100 OZ 0.0000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 19,398 notices 1,939,800 oz 60.33 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

dealer deposits: 1

1 ENTRY

i) Into ASAHI dealer 32,118.949 oz

(999 kilobars)

total weight in tonnes: 0.999 tonnes

xxxxxxxxxxxxxxxxxxxxx

deposits customer

we have 4 customer deposits

i) into JPMorgan customer acct 241.325 oz

(75 kilobars)

ii) Brinks 16,008.643 oz

ii) Malca: 67,002.684 oz (2084 kilobars)

iv) Manfra: 61,772.328 oz

total customer weight: 147,194.980 oz

or 4.578 tonness

total weight dealer and customer; 5.577 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 0

xxxxxxxxxxxxxxxxxx

adjustments: customer to dealer: 4 entries

i) Brinks: 12,191.712 oz

ii) Int. Delaware 675.165 oz

iii) JPMorgan 160,690.698 oz

iv) Malca: 163,552.137 oz oz

total weight adjusted 335,759.442 oz or 10.443 tonnes

AMOUNT OF GOLD STANDING FOR MARCH

THE FRONT MONTH OF MARCH HAD A GAIN OF 441 CONTRACTS TO STAND AT 521. WE HAD 79 CONTRACTS SERVED ON THURSDAY SO WE GAINED 520 CONTRACTS FOR 52,000 OZ (1.6174 TONNES AS A PHYSICAL GOLD QUEUE JUMP. THIS IS CENTRAL BANKS LOOKING FOR BADLY NEEDED GOLD

APRIL HAD A LOSS OF ONLY 33,458 CONTRACTS DOWN TO 61,062 CONTRACTS AS THIS MONTH BECOMES THE FRONT MONTH. WE HAVE 1 MORE READING DAY ON FIRST DAY NOTICE, MONDAY MARCH 31.

APRIL WILL BE A DANDY DELIVERY MONTH!!! CERTAINLY OVER 120 TONNES OF GOLD

MAY GAINED 911 CONTRACTS UP TO 3538.

We had 521 contracts filed for today representing 52,100 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 521 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MARCH /2025. contract month, we take the total number of notices filed so far for the month (19,398 X 100 oz ) to which we add the difference between the open interest for the front month of MARCH (521 CONTRACTS) minus the number of notices served upon today (521 x 100 oz per contract) equals 1,939,800 OZ OR 60.330 TONNES to which we add our 7.6179 tonnes exchange for risk//new total tonnage standing: 67.9479 tonnes

thus the INITIAL standings for gold for the MARCH contract month: No of notices filed so far (19,398 x 100 oz +we add the difference for front month of MARCH (521 OI} minus the number of notices served upon today (521 x 100 oz) which equals 1,939,800 OZ OR 60.33 TONNES + .7.6179 ex for risk //new total 67.9479 tonnes

TOTAL COMEX GOLD STANDING FOR MARCH.: 67.9479 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND MARCH IS FOLLOWING SUIT..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,972, 118.482 oz 61.34 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 43,347,625.918 .oz

TOTAL REGISTERED GOLD 22,752,455.145 or 707.696 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 20,595,170.773 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 20,780.337oz (REG GOLD- PLEDGED GOLD)= 646.355tonnes //

END

SILVER/COMEX

// THE MARCH 2025 SILVER CONTRACT//INITIAL

MARCH 27

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | withdrawals 1 Brinks 50,890.100 oz |

| Deposits to the Dealer Inventory | 2 entries i) Into Brinks dealer acct 622,091.830 oz ii) Into ASAHI: 1,228,631.320 oz total 1850,723.15 oz total dealer 312,701.477 oz |

| Deposits to the Customer Inventory | 4 entries i) Into Brinks customer acct 2018.195 oz ii) Into CNT 13,832.790 oz iii) Into JPMorgan 1,833,748.900 oz iv) Into Manfra; 323.336.912 oz total 2172,936.802 oz |

| No of oz served today (contracts) | 202 CONTRACT(S) (1.010 MILLION OZ |

| No of oz to be served (notices) | 0 contracts (0 MILLION oz) |

| Total monthly oz silver served (contracts) | 16,149 Contracts (80.745 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

2 entries

i) Into Brinks dealer acct 622,091.830 oz

ii) Into ASAHI: 1,228,631.320 oz

total 1850,723.15 oz

total dealer 312,701.477 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

4 entries

i) Into Brinks customer acct 2018.195 oz

ii) Into CNT 13,832.790 oz

iii) Into JPMorgan 1,833,748.900 oz

iv) Into Manfra; 323.336.912 oz

total 2172,936.802 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1 entries

withdrawals 1

Brinks

50,890.100 oz

ADJUSTMENTs 1 entries// customer to dealer:

Brinks: 971,162.280 oz

JPMorgan has a total silver weight: 190,478million oz/472.420oz million or 40.32%

TOTAL REGISTERED SILVER: 152.514 MILLION OZ//.TOTAL REG + ELIGIBLE. 472.420Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH /2025 OI: 202 OPEN INTEREST CONTRACTS FOR A LOSS OF 388 CONTRACTS.WE HAD 367 CONTRACTS SERVED ON THURSDAY SO WE LOST ANOTHER 21 CONTRACTS OR 0.105 MILLION OZ UNDERWENT AN EFP TRANSFER TO LONDON LOOKING FOR METAL OVER ON THE LONDON SIDE OF THE POND THIS IS THE 4TH CONSECUTIVE EFP TRANSFER THIS MONTH. WE MUST NOW ADD THAT CRAZY 70 CONTRACT EX FOR RISK/PRIOR FOR 350,000 OZ. THE BANK OF ENGLAND OR ANOTHER OFFICIAL ENTITY IS ASSUMING THE RISK OF DELIVERY AND THE COUNTERPARTY ARE BULLION BANKS WHO CANNOT GUARANTEE DELIVERY.

APRIL SAW A LOSS OF 132 CONTRACTS TO STAND AT 2172. APRIL IS NOW THE NEW FRONT MONTH

AND PROBABLY AROUND 10 MILLION OZ WILL STAND FOR DELIVERY AT THE COMEX.

MAY SAW A GAIN OF 2586 CONTRACTS UP TO 126,596 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 202 or 1.010 MILLION oz

CONFIRMED volume; ON THURSDAY 88,860 huge//

AND NOW MARCH DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 16,,149 X5,000 oz = 80.745 MILLION oz

to which we add the difference between the open interest for the front month of MAR (202) AND the number of notices served upon today (202 )x (5000 oz)

Thus the standings for silver for the MARCH 2025 contract month: (16,149) Notices served so far) x 5000 oz + OI for the front month of MAR(202) minus number of notices served upon today (202)x 5000 oz equals silver standing for the MARCH contract month equating to 80.745 MILLION OZ TO WHICH WE ADD .350 MILLION OZ EX FOR RISK//NEW TOTAL 81.095 MILLION OZ//

New total standing: 81.095 million oz which is huge for this very active delivery month of March.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 152.514million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

MARCH 26 WITH GOLD UP $42.45 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

MARCH 21 WITH GOLD DOWN $20.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 910.43 TONNES

MARCH 20 WITH GOLD UP $3.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 909.28 TONNES

MARCH 19 WITH GOLD UP $0.45 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 907.27 TONNES

MARCH 18 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 907.27 TONNE

MARCH 17 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.64 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 906.41 TONNES

MARCH 14 WITH GOLD UP $9.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MONSTER DEPOSIT OF 7.17 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 905.81 TONNES

MARCH 13 WITH GOLD UP $42.85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 12 WITH GOLD UP $22.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.90 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 895.20 TONNES

MARCH 11 WITH GOLD UP $21.20 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 891.30 TONNES

MARCH 10 WITH GOLD DOWN $12.45 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 894.317 TONNES

MARCH 7 WITH GOLD DOWN $12.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 6 WITH GOLD UP $2.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 900.30 TONNES

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

GLD INVENTORY: 929.65 TONNES, TONIGHTS TOTAL

SILVER

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

MARCH 21 WITH SILVER DOWN $0.45 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 442.962 MILLION

MARCH 20 WITH SILVER DOWN $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 19 WITH SILVER DOWN $0.45 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.219 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 18 WITH SILVER UP $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.823 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.373 MILLION

MARCH 17 WITH SILVER UP $0.03 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.096 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 439.550 MILLION

MARCH 14 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.910 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.454 MILLION

MARCH 13 WITH SILVER UP $0.46 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.774 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 434.544 MILLION

MARCH 12 WITH SILVER UP $0.57 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.032 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 435.318 MILLION

MARCH 11 WITH SILVER UP $0.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.816 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 436.410 MILLION

MARCH 10 WITH SILVER DOWN 25 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.276 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.591 MILLION

MARCH 7 WITH SILVER DOWN 40 CENTS/HUGL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.184 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 434.317 MILLION

MARCH 6 WITH SILVER UP 16 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.455 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.046 MILLION

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

CLOSING INVENTORY 447.422 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

JAMES RICKARDS….

Rickards: Trump & The Fate Of The Dollar

Friday, Mar 28, 2025 – 02:40 PM

Authored by James Rickards via DailyReckoning.com,

What is the Mar-a-Lago Accord? And what would a Mar-a-Lago Accord mean for the value of the U.S. dollar?

We begin our analysis with the name itself. Mar-a-Lago Accord is an echo of the three major international currency accords since the original Bretton Woods Agreements reached in 1944.

Accords Through The Years

The first was the Smithsonian Agreement in December 1971. This came in the aftermath of President Nixon’s decision on August 15, 1971, to end the convertibility of U.S. dollars into physical gold by U.S. trading partners at the fixed rate of $35.00 per ounce. The major countries in the global system (U.S., UK, France, Germany, Italy, Japan, Netherlands, Sweden, Switzerland, Canada, Belgium, and Netherlands) met at the Smithsonian Institution in Washington DC to decide how to reopen the gold window.

The main U.S. goal was to devalue the dollar. In the end, the price of gold was increased by 8.5% to $38.00 per ounce (revalued to $42.22 per ounce in 1973), which equaled a 7.9% dollar devaluation. Other currencies were revalued against the dollar, including a 16.9% upward revaluation of the Japanese yen.

The effort to reopen the gold window failed. Instead, major countries moved to floating exchange rates, which remains the norm to this day. Gold moved to free market trading and is currently about $3,050 per ounce. That gold price represents a 98.8% devaluation of the dollar measured by weight of gold since 1971.

The period from 1971 to 1985 was tumultuous in foreign exchange markets including the Petrodollar agreement (1974), the Herstatt Bank collapse (1974), the sterling crisis (1976), U.S. hyperinflation (50% from 1977-1981), a gold price super-spike (1980), and a major global recession (1981-1982). By 1983, inflation was subdued, the dollar was gaining strength, and strong economic growth was achieved in the U.S. under Ronald Reagan.

The next major economic gathering on foreign exchange was the Plaza Accord in September 1985. This was convened by U.S. Treasury Secretary James Baker at the Plaza Hotel in New York and included the U.S., Germany, the UK, Japan and France. At the time, the dollar was at an all-time high relative to other currencies. The dollar had even strengthened against gold, which had dropped in price from $800.00 per ounce in January 1980 to around $320.00 per ounce in 1985.

The purpose of the meeting was to devalue the dollar in stages. In this respect, the meeting was a success. Importantly, the method of devaluation was to be gradual and it was to be accomplished by central bank and finance ministry interventions in the foreign exchange markets. It was not a fiat devaluation; it was a finesse.

In practice, the market interventions were quite few. Once foreign exchange traders got the message, they took the dollar where it needed to go on their own. No foreign exchange dealer wanted to be on the wrong side of the trade if the central banks decided to intervene on any particular day.

The Louvre Accord, signed on February 22, 1987, among the U.S., UK, Canada, France, Japan and Germany was, in effect, a victory lap following the Plaza Accord. Between 1985 and 1987, the dollar did devalue against other currencies. The dollar also fell against gold, which rose from $320 per ounce to $445 per ounce by the time of the meeting. It was mission accomplished for Treasury Secretary James Baker. The purpose of the Louvre Accord was to lock down the accomplishments of the Plaza Accord, stop further dollar depreciation, and return to a period of relative stability in foreign exchange markets.

This accord was also a success. The dollar was mostly stable after 1987, despite the introduction of the euro in 2000 (the euro bounced between $0.80 and $1.60 in the early 2000s. Today it’s $1.09, which is not far from its original valuation of $1.16).

The other wild card was gold. After hitting bottom at around $250 per ounce in 1999, gold surged to $1,900 per ounce in 2011, a 670% gain for gold and a de facto devaluation of the dollar when measured by weight of gold. The period of relative stability in foreign exchange markets lasted until 2010 when a new currency war was unleashed by President Obama.

A New Mar-A-Lago Accord

Which brings us to discussion of a possible new international monetary conference in the chain of conferences from the Smithsonian Agreement to the Plaza Accord to the Louvre Accord. Given Donald Trump’s dominance on the world economic scene today and his love of ornate architecture of the kind seen at the Plaza Hotel and the Louvre (Trump owned the Plaza Hotel from 1988 to 1995),it’s not a stretch to expect that Trump would convene any new world monetary conference at his equally ornate Mar-a-Lago club in Palm Beach, Florida.

The first discussion of a Mar-a-Lago Accord appears in Chapter Six of my book Aftermath (2019), published six years ahead of current attention to the topic. That chapter is titled “The Mar-a-Lago Accord” and contains extensive discussion of the evolution of the international monetary system starting in 1870, including the more recent accords noted above.

It then moves through my private meetings with IMF head John Lipsky and Treasury Secretary Tim Geithner with a focus on a possible new gold standard and the attempted replacement of gold by the Special Drawing Right (SDR), created in 1969 and used among IMF members ever since. It ends with the classic 1912 quote from Pierpont Morgan that, “Money is gold, and nothing else.” and recommends that investors acquire physical gold for their portfolios. The dollar price of gold has risen 120% since that recommendation.

Today’s vogue in Mar-a-Lago Accord research began with a November 2024 paper written by Stephan Miran titled “A User’s Guide to Restructuring the Global Trading System”, published by Hudson Bay Capital. Although the title refers to the trading system, it explains how currency devaluation can be used to offset the impact of tariffs and refers to “persistent dollar overvaluation.”

From there, it’s a short leap to the ghost of the Plaza Accord and the need for a new Mar-a-Lago Accord. (Shortly after the paper was published, Trump appointed Miran as Chair of his Council of Economic Advisors, which gives his views added weight).

Issuance of 100-Year Bonds

In the currency section of the paper (pages 27-34), Miran not only suggests a devaluation of the dollar; he proposes that the U.S. issue 100-year bonds. In Miran’s view, 100-year bonds will be attractive to foreign reserve managers and will reduce any dollar selling needed to prop up their own currencies. Those long-term dollar holdings will mitigate short-term dollar devaluation in a way that moves the entire international monetary system toward a desirable equilibrium. Miran specifically uses the term Mar-a-Lago Accord to describe his proposed system.

There are many more technical details in Miran’s plan that we don’t have room to discuss in this article. These include use of the Treasury’s Exchange Stabilization Fund, the Fed’s Bank Term Funding Program, and Fed currency swap lines. Miran also suggests using the International Emergency Economic Powers Act of 1977 (IEEPA) to impose withholding taxes on interest payments to foreign holders of Treasury securities (a form of capital controls) as a way to discourage trading partners from holding Treasuries and therefore a way to devalue the dollar.

Trading partners would be evaluated using a traffic-light system. Countries would be ranked green (friendly), yellow (neutral) and red (adversary). Green countries would get U.S. military protection and the most favorable tariffs, yellow would get reciprocal tariffs, and red countries would get no security help, punitive tariffs and possible capital controls.

A Financial Catastrophe in the Making

In effect, Miran is trying to have it both ways. He wants to devalue the dollar and at the same time keep the dollar at the center of the International Monetary System. Nixon did this in 1971 and Baker did it in 1985. With regard to Miran, one cannot resist a paraphrase of Lloyd Bensen – “Stephan, you’re no Jim Baker.” The success of the Plaza Accord depended entirely on close cooperation of the major country finance ministries. No such cooperation exists today given sanctions on Russia, tariffs on China and the U.S. isolation of the EU with respect to the War in Ukraine.

Since Miran’s paper, the topic has spun completely out of control. A recent MarketWatch headline says “Wall Street can’t stop talking about the ‘Mar-a-Lago Accord.’”Some analysts propose that gold on the Federal Reserve’s balance sheet (actually a gold certificate) would be revalued from $42.22 per ounce to the market price (now $3,050 per ounce) with the “profit” added to the Treasury General Account. Another idea is to use U.S. assets such as land and mineral rights to collateralize U.S. debt.

As of now, no one knows what a Mar-a-Lago Accord would actually be or whether it will even happen, so it’s impossible to describe the impact. Still, the best-known version of the plan would have unintended consequences that could lead to a global financial catastrophe.

There’s no need to force holders to swap short-term debt for long-term debt. You simply let the short-term debt mature and replace it with new 100-year bond issues through the existing primary dealer underwriting system. No coercion is needed; there would be huge demand for 100-year debt.

Dollar devaluation does not fight potential inflation from tariffs (there isn’t any). It actually causes inflation by increasing the cost of imported goods. Any gold price mark-up on the Fed’s books is simply an accounting entry. The suggested “audit” of Fort Knox by Trump and Elon Musk (if it happens) will be nothing more than a staged photo-op. Gold has a world price entirely unaffected by accounting games between the Treasury and the Fed.

Again, the Mar-a-Lago Accord as it’s envisioned today would cause a global financial crisis. That’s because it fails to understand the importance of short-term Treasury debt as collateral for inter-bank lending and derivatives. Substituting 100-year Treasury debt for short-term Treasury bills would make those bills scarce. Treasury bills are the most liquid collateral in the world and are at the root of the Eurodollar system and the $1 quadrillion derivatives market. Scarcity of Treasury bills would implode bank balance sheets and lead to the greatest banking crisis in history.

The big winner in this context is gold. The BRICS are moving toward gold as fast as they can. Investors can do the same. Don’t be left behind.

2. Egon Von Greyerz et al

ALASDAIR MACLEOD….

Gold and silver outperform

In generally lacklustre financial markets, the standout winners have been gold and silver. This report looks at the consequences for portfolio reallocations in Q2 2025 and beyond.

| Alasdair MacleodMar 28∙Paid |

Gold and silver rose strongly this week on Far East demand. In European early morning trade, gold was $3072, up $50 from last Friday’s close after hitting the $3085 level during Asian trading hours — a new record. Silver stirred at $34.38, up $1.36 on the same time scale. Comex volumes in gold were healthy, while they still remain subdued in silver except for yesterday when silver rose by 2%.

Later today, a dip in gold and silver cannot be ruled out because with Asian trading closed for the weekend, any pause in futures’ demand for gold and silver is likely to be pounced on by the swaps selling to drive prices lower. This is entirely predictable. But it’s the prospect for prices in the following weeks, being the start of a new investment performance quarter and beyond that should concern us.

Gold’s remarkable performance, up 17.3% in the first quarter of 2025 along with silver (+19%) is the best performing asset class compared with other investment media. Yet gold and gold substitutes such as ETFs and mines are unbelievably under-owned in investment portfolios. In a March 17 article for my paid Substack subscribers, I revealed that in the entire portfolio universe of MSCI’s $217.1 trillion value of US and other developed-nation portfolios, the entire gold mining universe (bullion, ETFs and gold mines) represents only 0.21% of that total.

The following table shows relative performances of principal asset classes to date:

Already, this dichotomy is leading to ETF demand, as the following chart from the World Gold Council revealed:

The dark blue is North America, which in February added 72.2 tonnes equivalent, while Europe (light blue) having added 39 tonnes in January only added 2 tonnes in February. Asia added 24.4 tonnes in February. This tells us that it was only last month that investment managers in the US began the process of reweighting their portfolios in favour of gold.

Asian demand this week appears to reflect major Chinese insurance companies buying gold, having been authorised to do so by the Chinese regulators in a “pilot programme” limited to about $27 billion (280 tonnes). This is a significant amount in global bullion markets already drained of liquidity by the Comex futures market. Given it is only a pilot, future authorisations leading to further relaxing of restrictions will mean larger tonnages being purchased.

Gold is still being delivered into Comex, draining foreign trading centres of their liquidity as MacroMicro’s chart shows:

The same is true for silver:

The economic background is very favourable for gold and silver as well. Trump continues with his aggressive tariffs, due to bring in a new round on 2 April. This will kill both global and US economies, raising prices in America in particular. Interest rates and bond yields will have to accommodate this fact, along with economic damage leading to soaring budget deficits and springing debt traps on the US, UK, Japan, and various EU governments. The deterioration of their finances is bound to weaken their currencies valued in real money, which is gold and to a lesser extent silver.

Clearly, investors are badly wrongfooted for these developments and will have to rethink portfolio allocations. The bull market in gold for them is only just starting.

3. C Powell and Gata dispatches

4. ANDREW MAGUIRE PODCAST

a must view…live from the vault 216

youtube.com/watch?v=7pNluNn187Q&list=PLE1y8hGSqr8ar1gKUdfqFDK5ygLIlrdmz&index=1

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//COPPER

6 CRYPTOCURRENCY NEWS

ASIA TRADING FRIDAY MORNING THURSDAY NIGHT

SHANGHAI CLOSED DOWN 22.44 PTS OR 0.67%

//Hang Seng CLOSED DOWN 152.20 PTS OR 0.65%

// Nikkei CLOSED DOWN 679.64 OR 1.80 %//Australia’s all ordinaries CLOSED UP 0.12%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2646 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2758/ Oil UP TO 69.92 dollars per barrel for WTI and BRENT UP TO 73.99 Stocks in Europe OPENED ALL MOSTLY RED.

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2646

OFFSHORE YUAN: DOWN TO 7.2758

SHANGHAI CLOSED CLOSED DOWN 22.44 PTS OR 0.67%

HANG SENG CLOSED CLOSED DOWN 679.64 PTS OR 1.80%

2. Nikkei closed DOWN 679.64 PTS OR 1.80%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 104.13// EURO RISES TO 1.07720 DOWN 29 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: FALLS TO. +1.527//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.83…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7280/Italian 10 Yr bond yield DOWN to 3.840 SPAIN 10 YR BOND YIELD DOWN TO 3.350

3i Greek 10 year bond yield DOWN TO 3.548

3j Gold at $3074.50 Silver at: 34.38 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 55 /100 roubles/dollar; ROUBLE AT 83.95

3m oil into the 69 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.83 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.527 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8829 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9511 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.330 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.682 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.988 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.01…

10 YR UK BOND YIELD: 4.7750 DOWN 11 PTS

10 YR CANADA BOND YIELD: 3.081 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.713 DOWN 3 PTS.

2a New York OPENING REPORT

Futures Slide, Gold Soars Ahead Of Inflation Data Amid Tariff Turmoil

Friday, Mar 28, 2025 – 08:26 AM