APRIL 1/2025/YESTERDAY’S CME REPORT ON GOLD STANDING WAS A HUGE ERROR BY THE CME AND IT HAS BEEN NOW CORRECTED: GOLD CLOSED DOWN $3.55 TO $3114.10/SILVER IS DOWN 36 CENTS TO $$33.62//PLATINUM IS DOWN $9.75 TO $987.20 WHILE PALLADIUM CLOSED DOWN $1.95 TO $986.60//ED STEER GIVES HIS ANALYSIS ON WHAT HAPPENED YESTERDAY WITH THE CME//ISRAEL VS TURKEY UPDATES// ISRAEL VS EGYPT UPDATE//HOUTHIS UPDATES/VACCINE INJURY REPORT/SLAY NEWS ETC//CANADA AND THE TARIFF SITUATION CAUSES LESS TRAVEL TO THE USA////USA DATA RELEASES//SWAMP STORIES FOR YOU TONIGHT//

*CANADIAN GOLD: $4450.46 DOWN 39.40 CDN dollars per oz( * NEW ALL TIME HIGH 4493.62 CDN DOLLARS PER OZ//MARCH 31 2025)

*BRITISH GOLD: 2408.17 DOWN 6.28 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,417.98 BRITISH POUNDS/OZ) MARCH 31/2025

*EURO GOLD: 2,884.26 DOWN 4.20 Euros per oz //* (ALL TIME CLOSING HIGH: 2,888.55 EUROS PER OZ/MARCH 31 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

JPMORGAN stopped 13,023/34,805 contracts

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 34,865 NOTICES FOR 3,486,600 OZ 108.444 TONNES

total notices so far: 37989 contracts for 3,798,900 OR 118.161 tonnes)

FOR APRIL

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 149 NOTICE(S) FILED FOR 0.745 MILLION OZ/

total number of notices filed so far this month : 996 CONTRACTS (NOTICES) for 4.980 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $3.55 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 933,38 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $.36 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV: //

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 448.332 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE3519 CONTRACTS TO 170,975 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0,28 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUGE SIZED LOSS OF 3069 TOTAL CONTRACTS ALL DUE TO CME COLOSSAL ERROR IN REPORTING ON OUR TWO EXCHANGES.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS PLUS SOME MONTH END SPREADER LIQUIDATION ON MONDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED SLIGHTLY ON MONDAY WITH SILVER’S LOSS IN PRICE AS THE PRICE FELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. WE HAD A HUGE T.A.S. LIQUIDATION AND FINALIZATION OF MONTH END SPREADER LIQUIDATION MONDAY. BUT THIS WAS COUPLED WITH A STRONG T.A.S. ISSUANCE OF 847 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS METALS WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAVE A HUGE CONTANGO IN SILVER SPOT VS FRONT FEB OF AROUND $0.99 AND A LEASE RATE OF 7.3%. WE HAD A STRONG 450 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 8477 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUMONGOUS SIZED 3069 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE. WE HAD CONSIDERABLE TAS LIQUIDATION/MONTH END SPREADER LIQUIDATION THROUGHOUT MONDAY’S COMEX TRADING SESSION WHICH ACCOUNTS FOR A HUGE PORTION IN THE NUMBERS OF OI ON OUR TWO EXCHANGES. HOWEVER STRANGELY THE CME NOTIFIED US THAT WE HAD ANOTHER OF THOSE CRAZY EXCHANGE FOR RISK CONTRACTS ISSUED TO TUESDAY AT 400 CONTRACTS FOR 2.0 MILLION OZ. THIS WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A STRONG 847 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.28 BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A SMALL LOSS IN PRICE AND OUR LOSS IN OPEN INTEREST FROM OUR TWO EXCHANGES OF 3069 CONTRACTS WAD DUE TO A COLLOSAL CME REPORTING ERROR. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS//MONTH END SPREADERS TRYING TO CONTAIN SILVER’S PRICE RISE AND THAT ACCOUNTS FOR ALL OF OUR OPEN INTEREST LOSSES AS WELL AS THE REPORTING ERROR

WE HAD A 440 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.155 MILLION OZ (FIRST DAY NOTICE) TO WHICH WE ADD OUR 2.00 MILLION OZ EX FOR RISK

INITIAL STANDING FOR APRIL STANDS AT 12.155 MILLION OZ

WE HAD:

/ MEGA HUGE COMEX OI LOSS+// A STRONG SIZED EFP ISSUANCE (450 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 847 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 519 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 1 DAYS, total 450 contracts: OR 2.25 MILLION OZ (450 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 2,25 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3,519 CONTRACTS WITH OUR LOSS IN PRICE OF 28 CENTS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG 450 CONTRACT EFP ISSUANCE CONTRACTS: 450 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 10.155 MILLION OZ ON FIRST DAY NOTICE, PLUS OUR NEW 2.00 MILLION EX FOR RISK

NEW STANDING APRIL: 12.155 MILLION OZ

WE HAVE 1). A MEGA HUMONGOUS SIZED LOSS OF 3069 OI CONTRACTS ON THE TWO EXCHANGES DESPITE OUR LOSS IN PRICE// 2.THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 847 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//CONSIDERABLE FRONT END OF THE TAS CONTRACTS/MONTH END SPREADERS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. HOWEVER THEY STILL NEED THESE ISSUANCES FOR REPLENISHMENT FOR FUTURE TRADING //3. ZERO NET LONG SPECULATORS WERE BURNED ON MONDAY DESPITE OUR LOSS IN PRICE. ALSO 4. SOME OF OUR LONGS EXERCISED THEIR CONTRACTS AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (847 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 149 NOTICE(S) FILED TODAY FOR 0.745 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY HUGE SIZED 69,052 OI CONTRACTS TO 505,722 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 856 CONTRACTS CONTRACTS//.

WE HAD A MEGA HUMONGOUS SIZED DECREASE IN COMEX OI (69,052 CONTRACTS) ALL DUE TO A COLLOSAL CME REPORTING ERROR. THIS OCCURRED WITH OUR HUGE STRONG GAIN OF $36.70 IN PRICE MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 166.964 TONNES (CME CORRECTED) TO WHICH WE ADD FOR APRIL ITS INITIAL 700 CONTRACT EXCHANGE FOR RISK FOR 70,000 OZ OR 2.177 TONNES. THUS INITIAL STANDING FOR GOLD/APRIL DELIVERY MONTH IS 169.141 TONNES.

/NEW STANDING FOR APRIL; 166.964 TONNES + 2.177 TONNES EX FOR RISK = 169.141 TONNES

/ ALL OF THIS HAPPENED WITH OUR $36.70 GAIN IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD AN ATMOSPHERIC SIZED LOSS OF 67,860 OI CONTRACTS (210.905 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AND NOW FOR OUR FRONT MONTH OF APRIL. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1185 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 506,628

IN ESSENCE WE HAVE A MEGA HUMONGOUS SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 67,860 CONTRACTS WITH 69,052 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1185 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 67,860 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A GOOD SIZED AND CRIMINAL 1645 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1185 CONTRACTS) ACCOMPANYING THE A MEGA HUGE SIZED DECREASE IN COMEX OI OF 68,196 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 69,052 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR APRIL 166.964 TONNES FOLLOWED BY TODAY’S INITIAL 2.177 TONNES OF EX. FOR RISK//THUS INITIAL AMOUNT OF GOLD STANDING IN THIS VERY ACTIVE DELIVERY MONTH OF APRIL IS 169.141 TONNES.

//NEW STANDING APRIL: 166.964 TONNES + 2.177 TONNES EX FOR RISK = 169.141 TONNES

.

/ 3) HUGE T.A.S. LIQUIDATION + MONTH END SPREADERS TRYING TO LOWER GOLD’S PRICE FRIDAY WITH ZERO SUCCESS IN REMOVING NET SPECULATOR LONGS, AS WE HAD 1) $36.70 COMEX PRICE GAIN AND WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD AN ATMOSPHERIC LOSS OF 69,052 CONTRACTS ON OUR TWO EXCHANGES (ALL DUE TO COLLOSAL CME REPORTING ERROR ) ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN APRIL.

4) VERY STRONG SIZED COMEX OPEN INTEREST DECREASE 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///GOOD T.A.S. ISSUANCE: 1645 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 1185 CONTRACTS OR 118,500 OZ OR 3.685 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 1185 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN1 TRADING DAY(S) IN TONNES 3.685 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 3.685 TONNES DIVIDED BY 3550 x 100% TONNES = 0.1030% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 3.685 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 3519 CONTRACTS OI TO 174,494 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 450 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 450 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 450 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3519 CONTRACTS AND ADD TO THE 450 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3069 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 12.70 MILLION OZ

OCCURRED DESPITE OUR $0.28 LOSS IN PRICE. ALL OF THE LOSS IN OI WAS DUE TO COLLOSAL ERROR IN CME REPORTING FINAL NUMBERS YESTERDAY.

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 12.69 PTS OR 0.38%

//Hang Seng CLOSED UP 87.26 PTS OR .38%

// Nikkei CLOSED UP 6.92 OR 0.02 %//Australia’s all ordinaries CLOSED DOWN 1.74%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2697 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2831/ Oil UP TO 71.41 dollars per barrel for WTI and BRENT UP TO 74.76 Stocks in Europe OPENED ALL MOSTLY RED.

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A MEGA HUGE SIZED69,052 CONTRACTS TO 505,772 WITH OUR HUGE GAIN IN PRICE OF $36.70 WITH RESPECT TO MONDAY’S TRADING/. WE LOST ZERO NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1185 ).

THE CME ANNOUNCED MONDAY NIGHT,A ZERO EXCHANGE FOR RISK CONTRACTS FOR NIL OZ OR 0 TONNES THUS ITS INITIAL ISSUANCE FOR THE FRONT MONTH OF APRIL STANDS AT 2.177 TONNES OF GOLD

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY: WE HAD FIVE EXCHANGE FOR RISKS IN GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.

DETAILS ON APRIL COMEX MONTH

IN TOTAL WE HAD A MEGA HUGE SIZED LOSS ON OUR TWO EXCHANGES OF 69,052 CONTRACTS WITH OUR HUGE GAIN IN PRICE. OBVIOUSLY THE HUGE GAIN IN OI YESTERDAY WAS A COLOSSAL ERROR. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON MONDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF MARCH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY FRIDAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION// THROUGHOUT THE WEEK. THEY ISSUED MONDAY NIGHT A GOOD SIZED 1645 CONTRACTS. THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING A LOWER COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, , 203 , ,205 , 207 209 AND 211 212 213,215 AND FRIDAY’S 216 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS TRUMP CAME INTO OFFICE MONDAY NOON JAN 20. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING TODAY’S FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF APRIL .… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1185 EFP CONTRACTS WERE ISSUED: : /APRIL 1185 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1185 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE “LOST” THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A MEGA HUGE SIZED TOTAL OF 69,052 CONTRACTS IN THAT 1185 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUMONGOUS LOSS OF 69,052 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF $36.70 FOR MONDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. MUCH+ OF THE TOTAL GAIN IN OUR TWO EXCHANGES WAS DUE TO THE LIQUIDATION OF T.A.S. CONTRACTS.(GOVERNMENT) AND MONTH END SPREADERS!

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A GOOD SIZED 1645 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER 4 WEEKS AGO AND AGAIN LAST WEEK,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND NOW ,FOR MARCH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT LAST WEDNESDAY MARCH 17, THE 38,393 T.A.S. CONTRACT ISSUANCE WAS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY DOES TWO IMPORTANT THINGS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH AND APRIL.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH

STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (169.141 TONNES//.CME CORRECTED) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH / FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTHAT 256.607 TONNES

AND NOW LAST 4 MONTHS OF 2025″:

YEAR 2025:

JAN 2025: 113.30 TONNES

FEB: 2025: 256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

STANDING FOR GOLD: 166.964 TONNES + 2.177 TONNES EX FOR RISK = 169.141 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 169.141 TONNES (INCLUDES 2.177 TONNES EX FOR RISK)

COMEX GOLD TRADING/APRIL CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $36.70/)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A MEGA HUMONGOUS SIZED LOSS IN OUR TWO EXCHANGES AA DUE TO CME ERROR. AND AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION MONDAY AS WELL AS FINALIZATION OF MONTH END SPREADER LIQUIDATION/ AS THEY WERE TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,000 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING AND THEY FAILED MISERABLY AS GOLD IS NOW WELL ABOVE THE $3,000 THRESHOLD AT 3132 PLUS.

LAST NIGHT/TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH MARCH/APRIL TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND IS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK:

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

NOW APRIL, ISSUES ITS FIRST EXCHANGE FOR RISK:

TOTAL ISSUANCE FOR EXCHANGE FOR RIS ON FIRST DAY NOTICE OF 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD. APRIL ISSUANCE MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK. THESE DELIVERIES WILL BE ADDED TO OUR NORMAL DELIVERY CYCLE. WE HAD 0 NOTICES FOR EXCHANGE FOR RISK FILED FOR TUESDAY.

STANDING NOW FOR APRIL:

APRIL: 166.964 TONNES +(2.177 EX FOR RISK// MARCH 31 FOR APRIL DELIVERY MONTH =169.141 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS APRIL DELIVERY MONTH FIRST DAY NOTICE;

WE HAVE LOST A MEGA HUMONGOUS SIZED TOTAL OF 208.432 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL (166.964TONNES) ON FIRST DAY NOTICE FOLLOWED BY OUR INITIAL EXCHANGE FOR RISK ISSUANCE TO THE BANK OF ENGLAND FOR 700 CONTRACTS OR 70,000 OZ (2.177 TONNES). THIS TOTAL IS NOW ADDED TO OUR NORMAL DELIVERY OF XXXXX TONNES AND THUS INITIAL STANDING FOR GOLD FOR APRIL IS 169.141 TONNES, THE 2ND HIGHEST EVER RECORDED!

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $36.70

WE HAD 856 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 67,860 CONTRACTS OR 6,786,000 0Z (210.905 TONNES)

i) Brinks customer acct 95,102.657 oz (2958 kilobars) ii) Brinks enhanced: 95,196.15 oz or 238 London good delivery bars/400 oz each.

total weight; 190,298.800 oz or 5.804 tonnes

Deposit to the Dealer Inventory in oz

2 ENTRIES i) Into ASAHI dealer 128,571.849 oz (3999 KILOBARS) ii) Into LOOMIS dealer 12,828.249 oz 399 kilobars)

TOTAL WEIGHT: 141.400.098 oz or 4.398 tonnes

Deposits to the Customer Inventory, in oz

we have 5 customer entries

we have 5 customer deposits

i) into Brinks 32,151.000 oz 1000 kilobars ii) Into JPMorgan: 96,453.000 3,000 kilobars iii) Into Loomis: 32.151 oz (1 kilobar) iv) Into Malca: 192,906.000 oz (6,000 kilobars) v) Into Manfra: 32,151.000 oz (1000 kilobars)

total weight; 353,693.151 oz (11.000 tonnes)

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

3,124 notice(s) 3,124,000 OZ 118.161 TONNES

No of oz to be served (notices)

15,690 contracts 1,569,000 OZ 48.802 TONNES

Total monthly oz gold served (contracts) so far this month

3,798,900 notices 3,486,500 oz 118.161 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits:

dealer deposits: 2

2 ENTRIES i) Into ASAHI dealer 128,571.849 oz (3999 KILOBARS) ii) Into LOOMIS dealer 12,828.249 oz 399 kilobars)

TOTAL WEIGHT: 141.400.098 oz or 4.398 tonnes

xxxxxxxxxxxxxxxxxxxxx

deposits customer

we have 5 customer deposits

we have 5 customer deposits

i) into Brinks 32,151.000 oz 1000 kilobars ii) Into JPMorgan: 96,453.000 3,000 kilobars

iii) Into Loomis: 32.151 oz (1 kilobar)

iv) Into Malca: 192,906.000 oz (6,000 kilobars)

v) Into Manfra: 32,151.000 oz (1000 kilobars)

total weight; 353,693.151 oz (11.000 tonnes)

total dealer and customer weight; 15.398 tonnes

total weight dealer and customer; 12.5543 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 2

2 entries

i) Brinks customer acct 95,102.657 oz (2958 kilobars) ii) Brinks enhanced: 95,196.15 oz or 238 London good delivery bars/400 oz each.

total weight; 190,298.800 oz or 5.804 tonnes

xxxxxxxxxxxxxxxxxx

adjustments: customer to dealer: 3 entries

i) Brinks: 160,781,151 oz

ii) JPMorgan 187,601.085 oz

iii) Manfra; 66,938.382 oz

total weight adjusted 415,326.618 oz or 12.917 tonnes

AMOUNT OF GOLD STANDING FOR APRIL

THE FRONT MONTH OF APRIL HAD A LOSS OF 87,848 CONTRACTS TO STAND AT 18,814.

BECAUSE OF THE CME ERROR IN FINAL REPORTING, I AM CALCULATING THAT THE INITIAL AMOUNT OF GOLD STANDING IS AS FOLLOWS:

18,814 CONTRACTS (OPEN INTEREST FOR APRIL) – 3124 (OI FOR APRIL TODAY)= 15,690 CONTRACTS

(FOR 48.802 TONNES). I THEN TAKE THE TOTAL ISSUANCE FOR APRIL AT 37,989 CONTRACTS AND ADD THE 15,690 CONTRACTS WHICH NOW TOTALS 53,679 CONTRACTS FOR 5,367,900 OZ OR 166.964 TONNES. I WILL NOW STATE THAT THIS IS THE INITIAL AMOUNT OF GOLD STANDING FOR APRIL

THEN WE MUST ADD OUR INITIAL ISSUANCE OF EXCHANGE FOR RISK OF 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES

THUS, OUR INITIAL GOLD STANDING FOR APRIL IS 166.964 + 2.177 TONNES = 169.141 TONNES

MAY GAINED 192 CONTRACTS UP TO 3834.

JUNE GAINED A STRONG 14,198 CONTRACTS AND JUNE WILL NO DOUBT BE A WHOPPER OF A DELIVERY MONTH IF THERE IS GOLD TO BE DELIVERED UPON.

We had 3124 contracts filed for today representing 312,400 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 24 notices issued from their client or customer account. The total of all issuance by all participants equate to 3,124 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1330 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL /2025. contract month, we take the total number of notices filed so far for the month (37,989 X 100 oz ) to which we add the difference between the open interest for the front month of APRIL (18,814 CONTRACTS) minus the number of notices served upon today (3124 x 100 oz per contract) equals 5,367,900 OZ OR 166.964 TONNES

to which we add our initial exchange for risk of 70,000 oz (2.177 tonnes) = 169.141 tonnes

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (37,989 x 100 oz +we add the difference for front month of APRIL (XXXX OI} minus the number of notices served upon today (3124 x 100 oz) which equals 5,3679,000 OZ OR 166.964 TONNES + 2.177 tonnes ex for risk = 169.141 tonnes

TOTAL COMEX GOLD STANDING FOR APRIL.: 169.141 TONNES WHICH IS HUGE FOR THIS ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL IS FOLLOWING SUIT..

JPMorgan has a total silver weight: 192.773million oz/478,455oz million or 40.16%

TOTAL REGISTERED SILVER: 154.588 MILLION OZ//.TOTAL REG + ELIGIBLE. 478.458Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2025 OI: 1184 OPEN INTEREST CONTRACTS FOR A LOSS OF 2319 CONTRACTS. THE CME ADMITS ITS COLOSSAL ERROR IN REPORTING YESTERDAY’S INITIAL AMOUNT OF SILVER WILLING TO STAND. SO I WILL CORRECT IT THE BEST I CAN:

I WILL TAKE THE OPEN INTEREST IN SILVER STANDING TODAY AT 1184 CONTRACTS AND SUBTRACT OUT TODAY’S FILING OF NOTICES AT 149 CONTRACTS. THAT GIVES ME 1035 NOTICES THAT HAVE YET TO BE SERVED UPON. I THEN TAKE THE TOTAL NO. OF NOTICES SERVED ALREADY AT 996 CONTRACTS AND THAT GIVES US 2031 CONTRACTS OR 10.155 MILLION OZ OF SILVER STANDING.

THEN I MUST ADD OUR NEW ISSUANCE OF 2.0 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL STANDING 12.155 MILLION OZ//

MAY SAW A LOSS OF 2368 CONTRACTS DOWN TO 123,769 CONTRACTS

JUNE SAW A GAIN OF 49 CONTRACTS UP TO 1323 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 149 or 0.745 MILLION oz

CONFIRMED volume; ON MONDAY 73,661 huge//

AND NOW APRIL DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 996 X5,000 oz = 4.980 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (1184) AND the number of notices served upon today (149 )x (5000 oz)

Thus the standings for silver for the APRIL 2025 contract month: (996) Notices served so far) x 5000 oz + OI for the front month of APRIL(1184) minus number of notices served upon today (149)x 5000 oz equals silver standing for the APRIL contract month equating to 10.155 MILLION OZ

New total standing: 10.155 million oz which is huge for this NON active delivery month of APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 154.588million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

MARCH 21 WITH GOLD DOWN $20.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 910.43 TONNES

MARCH 20 WITH GOLD UP $3.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 909.28 TONNES

MARCH 19 WITH GOLD UP $0.45 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 907.27 TONNES

MARCH 18 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 907.27 TONNE

MARCH 17 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.64 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 906.41 TONNES

MARCH 14 WITH GOLD UP $9.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MONSTER DEPOSIT OF 7.17 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 905.81 TONNES

MARCH 13 WITH GOLD UP $42.85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 12 WITH GOLD UP $22.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.90 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 895.20 TONNES

MARCH 11 WITH GOLD UP $21.20 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 891.30 TONNES

MARCH 10 WITH GOLD DOWN $12.45 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 894.317 TONNES

MARCH 7 WITH GOLD DOWN $12.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 6 WITH GOLD UP $2.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 900.30 TONNES

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

GLD INVENTORY: 933.38 TONNES, TONIGHTS TOTAL

SILVER

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: / //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

MARCH 21 WITH SILVER DOWN $0.45 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 442.962 MILLION

MARCH 20 WITH SILVER DOWN $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 19 WITH SILVER DOWN $0.45 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.219 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 18 WITH SILVER UP $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.823 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.373 MILLION

MARCH 17 WITH SILVER UP $0.03 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.096 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 439.550 MILLION

MARCH 14 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.910 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.454 MILLION

MARCH 13 WITH SILVER UP $0.46 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.774 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 434.544 MILLION

MARCH 12 WITH SILVER UP $0.57 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.032 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 435.318 MILLION

MARCH 11 WITH SILVER UP $0.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.816 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 436.410 MILLION

MARCH 10 WITH SILVER DOWN 25 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.276 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.591 MILLION

MARCH 7 WITH SILVER DOWN 40 CENTS/HUGL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.184 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 434.317 MILLION

MARCH 6 WITH SILVER UP 16 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.455 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.046 MILLION

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

CLOSING INVENTORY 448.332 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2. Egon Von Greyerz et al

3. C Powell and Gata dispatches

Ed Steer: A huge reporting error at CME Group’s Comex

Submitted by admin on Tue, 2025-04-01 12:27 Section: Daily Dispatches

Excerpted from Ed Steer’s Gold and Silver Digest Tuesday, April 1, 2025

I checked Friday’s final total open interest numbers on the Comex, and the change from the preliminary report in gold was absolutely incomprehensible, as it rose from +13,558 contracts up to a mind-blowing +62,187 contracts. That was the result of gold open interest in April blowing out by +45,420 Comex contracts, and June open interest by +16,556 contracts.

… Dispatch continues below …

That number would also be net of the record gold deliveries on first day notice. Whether that’s an error remains to be seen, but I’ve never seen anything like it before, and I await developments.

The final change in total silver contracts rose by a decent amount, from +780 contracts up to 1,997 contracts — and, like gold, this number was wrong as well.

But the preliminary report that came out at 1:30 a.m. ET this morning for the Monday trading session took all of that away, plus a bunch more, as it showed that gold open interest in April fell by 87,848 Comex contracts, leaving 18,814 still around, minus the 3,124 contracts out for delivery on Wednesday. …

Friday’s daily delivery report showed that 34,865 contracts were actually posted for delivery today, so that means that 87,848 minus 34,865 equals 52,983 Comex gold contracts vanished from the April delivery month.

Silver open interest in April cratered by 2,319 Comex contracts, leaving 1,184 contracts still open, minus the 149 contracts that are out for delivery on Wednesday. …

Friday’s daily delivery deport showed that 847 silver contracts were actually posted for delivery today, so that means that 1,184 minus 847 equals 337 more silver contracts were added to April deliveries yesterday, which is preposterous, since only 97 April silver contracts were traded yesterday.

Total gold open interest on Monday cratered by a net 68,196 Comex contracts, and total silver open interest by 3,000 contracts.

So there was a screw-up of biblical proportions in the CME Group’s open interest numbers for both silver and gold on Friday, something I’ve not seen before. Let’s hope this is the end of it.

* * *

4. ANDREW MAGUIRE INTERVIEWING PETER GRANDICH

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//COPPER

6 CRYPTOCURRENCY NEWS

ASIA TRADING TUESDAY MORNING MONDAY NIGHT

SHANGHAI CLOSED UP 12.69 PTS OR 0.38%

//Hang Seng CLOSED UP 87.26 PTS OR .38%

// Nikkei CLOSED UP 6.92 OR 0.02 %//Australia’s all ordinaries CLOSED DOWN 1.74%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2697 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2831/ Oil UP TO 71.41 dollars per barrel for WTI and BRENT UP TO 74.76 Stocks in Europe OPENED ALL MOSTLY RED.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2697

OFFSHORE YUAN: DOWN TO 7.2831

SHANGHAI CLOSED CLOSED UP 12.69 PTS OR 0.38%

HANG SENG CLOSED CLOSED UP 87.26 PTS OR 0.38%

2. Nikkei closed UP 6.92 PTS OR 0.02%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103.96// EURO RISES TO 1.0823 UP 5 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: RISES TO. +1.481//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 149.18…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6610/Italian 10 Yr bond yield DOWN to 3.773 SPAIN 10 YR BOND YIELD DOWN TO 3.293

3i Greek 10 year bond yield DOWN TO 3.467

3j Gold at $3130.00 Silver at: 33.81 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 5 /100 roubles/dollar; ROUBLE AT 84.84

3m oil into the 71 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149.18// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.481 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8824 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9518 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.158 DOWN 9 BASIS PTS…

USA 30 YR BOND YIELD: 4.523 DOWN 9 BASIS PTS/

USA 2 YR BOND YIELD: 3.848 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 37.93…

10 YR UK BOND YIELD: 4.6620 DOWN 4 PTS

10 YR CANADA BOND YIELD: 2.931 DOWN 4 BASIS PTS

5 YR CANADA BOND YIELD: 2.575 DOWN 8 PTS.

2a New York OPENING REPORT

Futures Slide After WaPo Report Trump Seeks 20% Tariffs On Most Imports

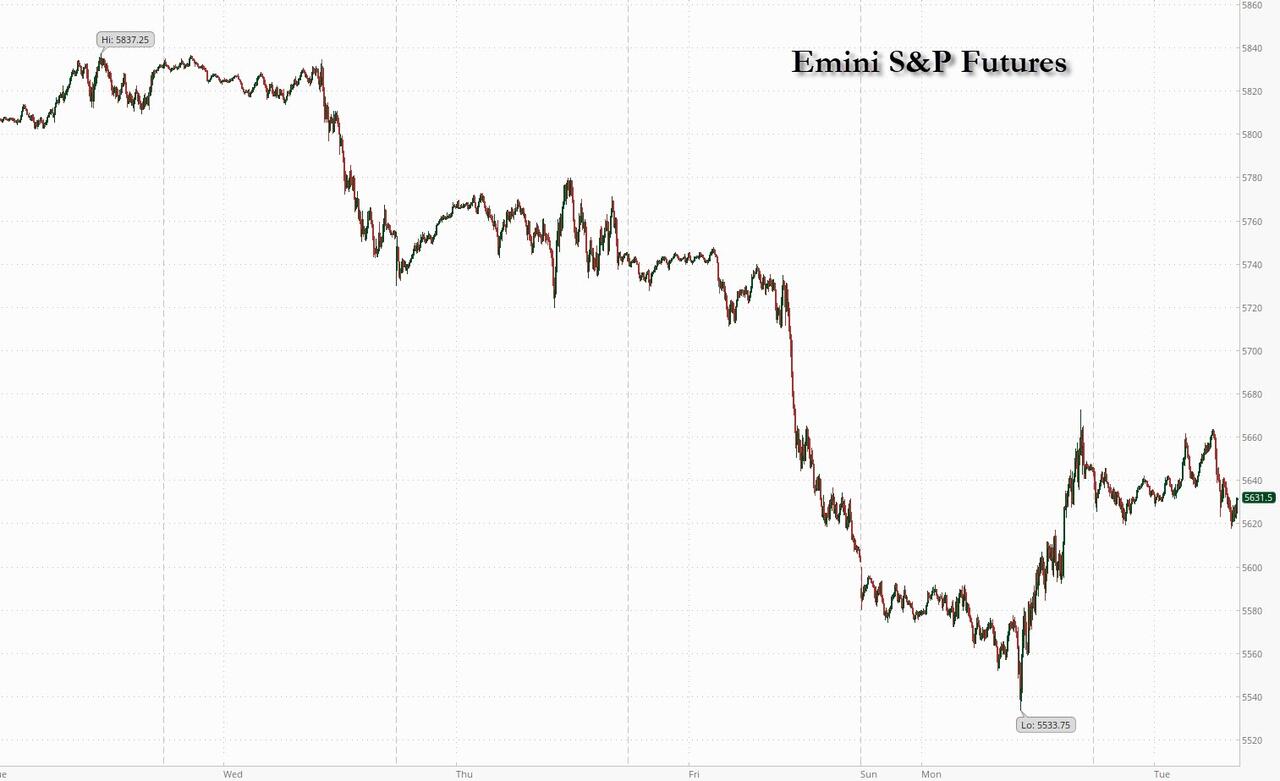

Tuesday, Apr 01, 2025 – 08:26 AM

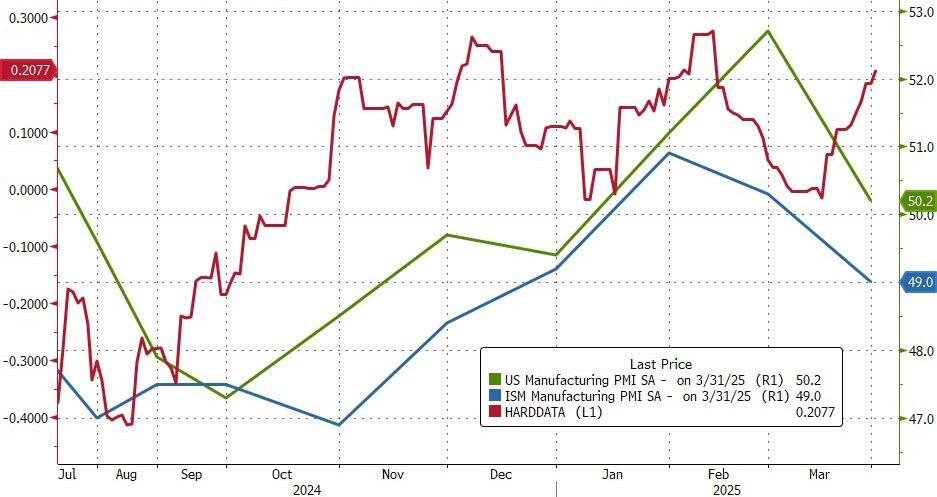

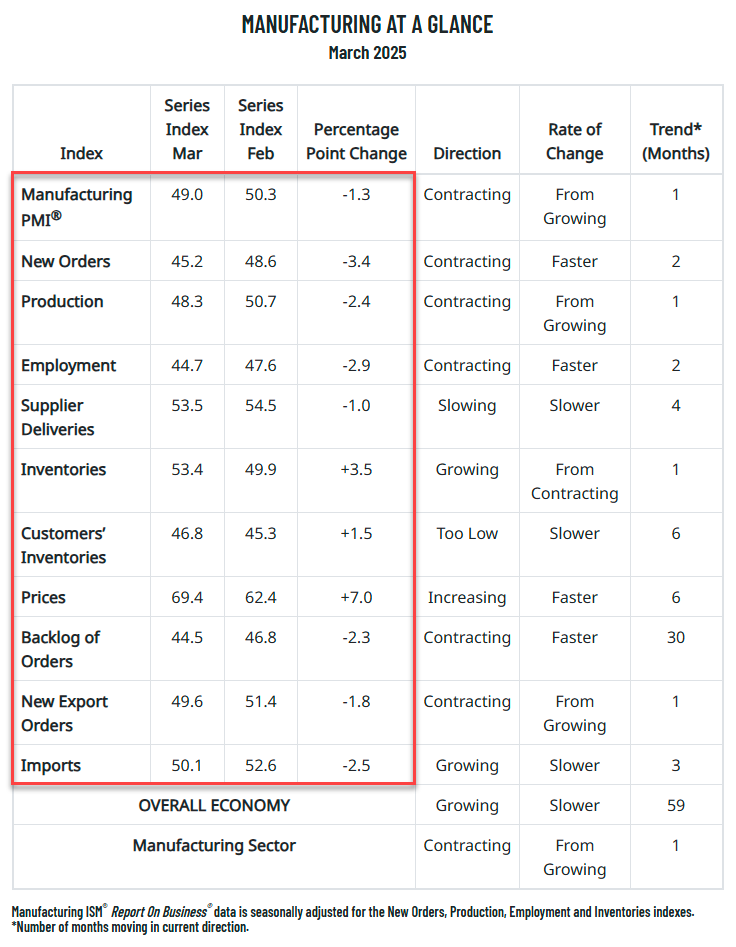

US equity futures fell abruptly just around 6am ET, reversing earlier gains and unable to benefit from the positive risk tone in European trade, hinting at another very volatile session on Wall Street, as tomorrow’s tariffs “liberation day” loomed over markets. Gold extended its winning streak, rising to another record high. As of 8:00am ET, S&P futures were down 0.5%, reversing an earlier gain of 0.2%, after the Washington Post reported a White House proposal to impose tariffs of around 20% on most imports. Nasdaq futures slid 0.6% as Tesla rose modestly but other Mag 7 stocks were in the red. European and Asian markets both rose. Bond yields slid 4bps, pushing the 10Y yield to 4.16% while the USD traded higher on the back of Euro weakness. Commodities are mostly flat this morning with base metals declining (copper -0.9%). Overnight, headlines were largely light, with geopolitical tension and trade policy remaining uncertain. Trump seems to dial back his criticism on Putin, per BBG article (here). We will get the Final March ISM-Mfg this morning: consensus expects the Index to print 49.5 survey vs. 50.3 prior; we also get the latest JOLTS report.

In US premarket trading, Tesla rose while fellow Magnificent Seven stocks edge lower (Tesla +3.1%, Nvidia +0.6%, Alphabet +0.5%, Meta +0.2%, Amazon +0.3%, Microsoft +0.2%, Apple -1%). Johnson & Johnson slid 3.5% in premarket trading after a judge rejected its third attempt to use bankruptcy of one of its units to end baby powder cancer claims. Delta Airlines Inc. and Southwest Airlines Co. fell after Jefferies analysts cut their ratings on concern about consumer spending. Here are some other notable premarket movers:

Newsmax shares jump 11%, putting the conservative media outlet’s stock on track to extend gains after it jumped 735% in its debut Monday.

Live Nation slip 1.5% after President Donald Trump said he will sign an executive order aimed at tackling ticket scalping, saying that it is a “big step” in dealing with an issue that “bothers” a lot of artists

Microvast shares surge 26% after the lithium-ion battery maker reported 2024 revenue that beat its guidance thanks to growing demand for its technology.

Gorilla Technology shares drop 6.4% after the analytics technology firm reported full-year results and reiterated its revenue forecast for 2025.

Intel slid after new CEO Lip-Bu Tan said the chipmaker will spin off assets that aren’t central to its mission and create new products including custom semiconductors to try to better align itself with customers

President Donald Trump will announce his reciprocal tariff plan at 3 p.m. on Wednesday at an event in the White House Rose Garden, but the extent of his levies remain unclear. There’s also confusion around whether the US president will take a lenient or harder tack, making investors wary of risky stock bets.

“Investors are grappling with what could be announced this week,” said Laura Cooper, global investment strategist at Nuveen. “The range of outcomes is so wide that traders are struggling with how to price in that potential outcome.”

Futures were hit shortly after 6am after the WaPo reported that White House aides have drafted a proposal to impose tariffs of around 20% on most imports to the United States. In a hitpiece that appears intended to spark panic and restart the selloff, the authors write that “if implemented, the plan is likely to send shock waves through the stock market and global economy. Assuming that permanent tariffs took effect in the current quarter and triggered robust retaliation by U.S. trading partners, the economy would almost immediately tumble into a recession that would last for more than a year, sending the jobless rate above 7 percent, according to Mark Zandi, chief economist for Moody’s, who described the results as a worst-case scenario.”

Trump has touted his April 2 announcement as a “Liberation Day,” heralding the start of a more protectionist policy meant as retribution against trading partners he has long accused of “ripping off” the US. He has already placed levies on Canada, Mexico and China — the US’s three largest trading partners — as well as automobiles, steel and aluminum. Import taxes on copper could come within several weeks. He has also threatened duties on pharmaceutical, semiconductor and lumber imports.

Many fear Trump’s announcement will mark the start of lengthy and fractious negotiations with trade partners, pressuring the economy and keeping market volatility elevated. On Tuesday, European Commission President Ursula von der Leyen said the bloc is prepared to retaliate if reciprocal tariffs are imposed.

“We could get another period of potential negotiations which is just going to prolong this uncertainty and underpin further choppy price action,” Nuveen’s Cooper said.

As tariffs loom, US carmakers are lobbying the administration to exclude certain low-cost car components, Bloomberg reported. The EU said it will use a broad range of options to retaliate. An analysis by Bloomberg Economics found that a maximalist approach could add up to 28 percentage points to the average US tariff rate — resulting in a hit of 4% to US GDP.

Strategists at Citigroup said that a surge in short flows pushed net positioning for the Nasdaq back to neutral ahead of tariff announcements. Barclays strategists, meanwhile, said that hedge funds and CTAs turned short US equities and long Treasuries last month, likely improving the risk-reward outlook into April 2.

Chip stocks could be in focus after Commerce chief Lutnick signaled he could withhold promised Chips Act grants as he pushes companies in line for subsidies to expand their US projects.

Europe’s Stoxx 600 rose 1.2% and is on course to snap a four-day losing streak as concerns regarding imminent US trade tariffs appear to have subsided. All 20 sectors are in the green, with auto, industrial and technology names leading gains. Goldman Sachs strategists cited a weaker growth outlook as a reason to cut their forecast for Europe’s Stoxx 600, following a similar move from the US team. The team led by Sharon Bell trimmed the 12-month target on the index to 570 points from 580. Here are the biggest movers Tuesday:

Europe’s biggest pharmaceutical companies advance, making healthcare the best performing Stoxx 600 subgroup, after JPMorgan analysts say potential US tariffs are expected to have a “manageable impact” on the sector

Gubra shares jump as much as 19% after the Danish drugmaker said interim phase 1 results for its obesity treatment candidate GUBamy were “positive.” Shares trim some gains to rise 12% at 10.27am CET

Greencore Group shares rise as much as 11% after the food producer said better-than-expected profit conversion means its FY25 adjusted operating profit will be ahead of current consensus. Analysts at Jefferies said the positive update

Enav shares jump after results met estimates and the air navigation services firm said it sees an annual revenue growth of 4.3% by 2029; Banca Akros’ Francesco Sala says the results were in line with estimates

UK supermarket stocks fall as a Kantar report adds to concern over increasing competitive pressures across the industry. Separately, BNPP Exane cuts earnings estimates for Tesco and Sainsbury, while downgrading the latter

Genmab falls as much as 5.4% after Bernstein cut its rating on the biotechnology company to underperform, saying the share price is far from fully discounting the loss of exclusivity for its Darzalex blood cancer treatment

Zealand Pharma shares drop as much as 6.3%, worst performer in the Stoxx 600 Health Care Index, after smaller Danish drug developer Gubra said interim early-stage results for its experimental obesity treatment were positive

Travis Perkins shares fall as much as 13% to their lowest since June 2009 after the wholesaler said there was uncertainty regarding recovery in UK construction activity and challenging market conditions have continued

Interroll shares drop as much as 2.6% after Kepler Cheuvreux cut the recommendation on the Swiss industrial equipment firm to reduce from hold, citing limited near-term catalysts and high valuation

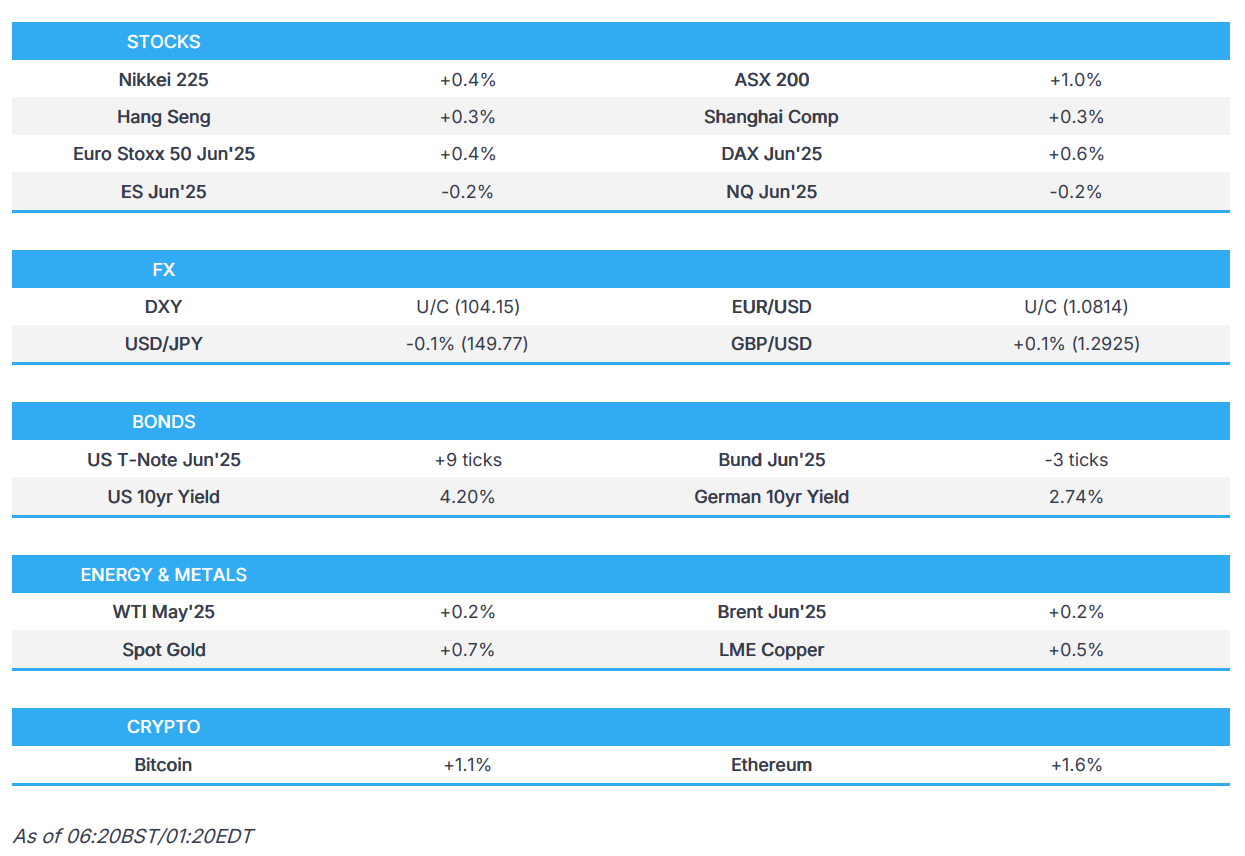

Earlier in the session, Asian equities also rose, poised to snap a three-day selloff as traders reassessed positions ahead of the planned imposition of more US tariffs. The MSCI Asia Pacific Index advanced as much as 1.1%, led by gains in Taiwan, South Korea and Hong Kong. TSMC, Tencent and Samsung Electronics were among the biggest boosts. Traders remained on edge, however, with 30-day volatility on the gauge trading around the highest level since October. Most key Asian benchmarks were in the green on Tuesday. India was an exception, with tech heavyweights sliding on concern that slower growth in the US may hurt spending by their clients. Markets in Indonesia, Malaysia and the Philippines were shut for holidays.

The rebound doesn’t signal “much about the overall market’s direction in next 6 to 12 months,” said Homin Lee, senior macro strategist at Lombard Odier Singapore. “It will still be important to get the details of Trump’s announcements tomorrow given the significant – and potentially market-negative – complexities implied in the tariff framework Trump appears to be considering.”

In FX, the Bloomberg Dollar Spot Index is little changed. The Aussie dollar pared gains seen after the RBA stood pat on rates with a slight hawkish tinge to the statement. The Swedish krona takes top spot with a 0.5% gain.

In rates, treasuries continue to benefit from haven demand, with futures reaching session highs after the Washington Post reported a White House proposal to impose tariffs of around 20% on most imports. Additional support comes from steeper gains for bunds after euro-area inflation eased further toward the European Central Bank’s 2% target, and declines for S&P 500 futures. US yields are 2bp-4bp richer across maturities with gains led by intermediates, flattening 2s10s spread by around 2bp; 10-year is on session lows around 4.165% with bunds and gilts outperforming by 3bp and 2.5bp in the sector. European government bonds are broadly higher with UK and German 10-year borrowing costs falling 6 bps each. Traders have added to their ECB and BOE interest-rate cut bets, although there was little reaction to euro-area CPI data – the headline matched forecasts while the core rate slowed slightly more than expected. US session includes March US manufacturing PMIs from S&P Global and ISM.

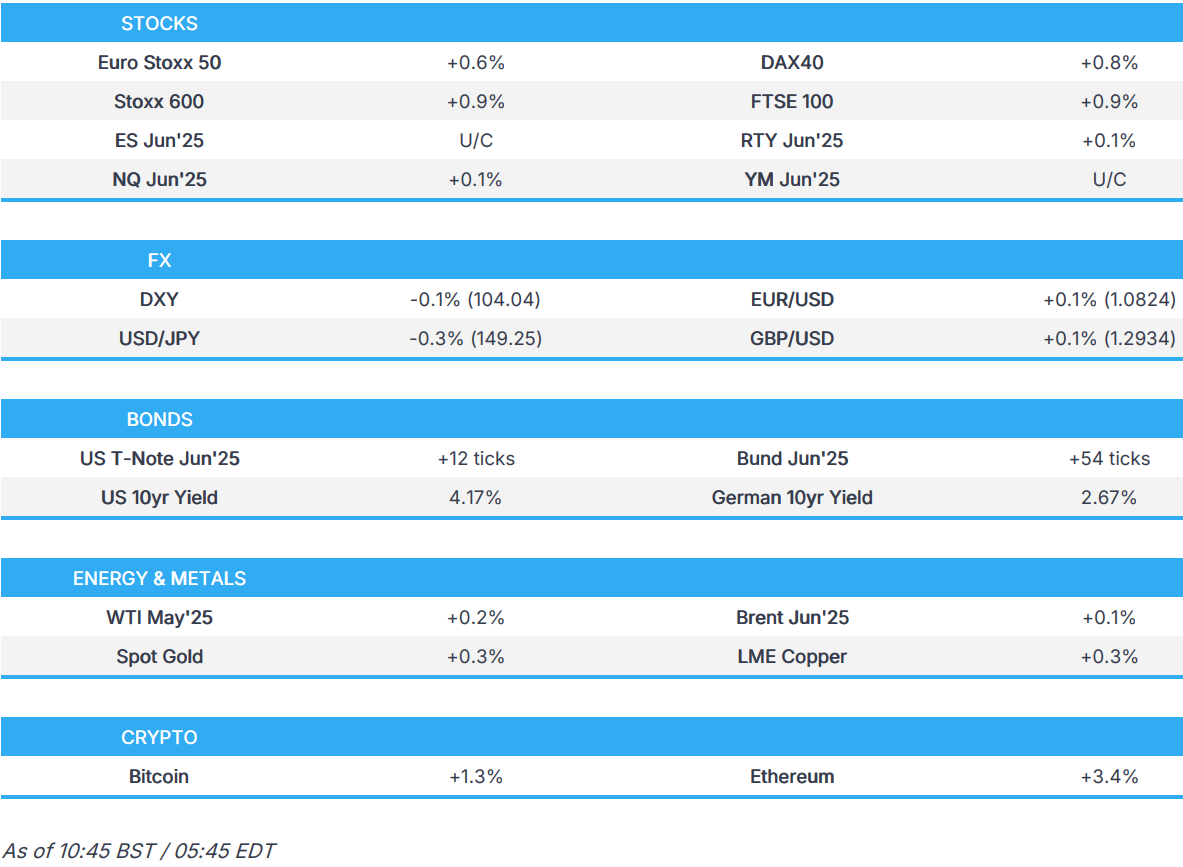

In commodities, spot gold adds $10 to $3,133 having notched another record high earlier near $3,150. WTI is steady near $71.50 a barrel. Bitcoin rises over 2% to above $84,000.

Today’s US economic calendar includes March final S&P Global US manufacturing PMI (9:45am), February construction spending, JOLTS job openings and March ISM manufacturing (10am) and Dallas Fed services activity (10:30am). ed speaker slate includes Richmond Fed’s Barkin discussing monetary policy and the economic outlook (9am).

Market Snapshot

S&P 500 mini -0.5%

Nasdaq 100 mini -0.4%

Russell 2000 mini +0.1%

Stoxx Europe 600 +1.2%, DAX +1.5%, CAC 40 +0.9%

10-year Treasury yield -3 basis points at 4.18%

VIX +0.1 points at 22.39

Bloomberg Dollar Index little changed at 1274.63

euro little changed at $1.0806

WTI crude -0.3% at $71.23/barrel

Top Overnight News

The US plans to extend the 2017 tax cuts, making them permanent and adding Trump’s campaign promises like eliminating taxes on tips, overtime pay and Social Security, Treasury Secretary Scott Bessent told Fox News. BBG

Howard Lutnick may withhold Chips Act grants to push companies to expand their US projects, people familiar said. Lutnick aims to generate tens of billions of dollars in additional investment commitments without increasing the size of federal grants. Donald Trump created a new office to manage the Chips Act’s funds and speed up some investments in the US. BBG

President Trump signed an executive order establishing the United States Investment Accelerator which establishes an office within the Department of Commerce meant to facilitate and accelerate investments above USD 1bln in the US, while the White House said the Investment Accelerator is to administer the CHIPS program office.

Trump signed an executive order aimed at protecting fans from ‘exploitative ticket scalping’ and reforming the US live entertainment ticketing industry, according to Reuters.

Republicans could be poised to deal a symbolic blow to President Donald Trump’s trade policy, with several GOP senators indicating they planned to join Democrats in a Tuesday vote to block blanket tariffs on Canada (although the bill will probably never become law). Politico

President Trump said that he had settled on a plan for his latest batch of tariffs expected this week but didn’t reveal what he had decided, after his economic team struggled to coalesce around a remade U.S. trade strategy. He wants to both raise revenue with tariffs and use them as leverage to get other nations to lower their own duties, or make other policy changes.

Boeing (BA) slows the production of 737 Max to 31 craft per month (current 38) to keep from derailing the assembly line, via Air Current; further slowing wing production.

Eurozone CPI for Mar comes in a bit cooler than anticipated on a core basis (+2.4% vs. the Street +2.4% and down from +2.6% in Feb) while headline was inline at +2.2% (down from +2.3% in Feb). BBG

The European Union said it will use a broad range of options to retaliate against the US if President Donald Trump follows through on his threat to impose so-called reciprocal tariffs on the bloc this week. “We do not necessarily want to retaliate,” European Commission President Ursula von der Leyen said on Tuesday. “If necessary we have a strong plan to retaliate and will use it.” BBG

China’s factory activity expanded at its fastest pace in four months in March, buoyed by stronger demand and robust export orders, a private-sector survey showed on Tuesday. The Caixin/S&P Global manufacturing PMI climbed to 51.2 in March from 50.8 in the previous month, surpassing analyst expectations of 51.1. The 50-mark separates growth from contraction. RTRS

China has kicked off large-scale military and coastguard exercises around Taiwan, the latest round in Beijing’s escalating campaign to assert its claims of sovereignty and suppress the island nation’s efforts to preserve its de facto independence. The drills on Tuesday came as Taiwan’s President Lai Ching-te seeks to improve military and civilian preparedness for a potential Chinese attach and strengthen society to defend against espionage and other infiltration from China, which last month he called a “hostile foreign force.” FT

China, Japan and South Korea agreed to jointly respond to U.S. tariffs, a social media account affiliated with Chinese state media said on Monday, an assertion Seoul called “somewhat exaggerated”, while Tokyo said there was no such discussion. The state media comments came after the three countries held their first economic dialogue in five years on Sunday, seeking to facilitate regional trade as the Asian export powers brace against U.S. President Donald Trump’s tariffs. RTRS

Tariffs/Trade