APRIL 3/GLOBAL SHOCK AS TRUMP INITIATES HUGE TARIFFS ON JUST ABOUT EVERY COUNTRY CREATING CHAOS IN THE MARKETS: GOLD CLOSED DOWN $27.85 TO $3101.25 WITH SILVER CLOSING DOWN $1.84 TO $31.95//PLATINUM CLOSED DOWN $21.95 TO $953.85 WHILE PALLADIUM CLOSED DOWN $43.05 TO $931.55//CANADA SEEMS SPARED FROM FURTHER TARIFFS//CANADA CHINA AND THE EU ARE ALREADY PLANNING THEIR OWN TARIFFS ON USA GOODS: THUS WE WILL COMMENCE SHORTLY WITH A TARIFF WAR//GOLD COMMENTARY TONIGHT FROM ALASDAIR MACLEOD//THREE EXCELLENT COMMENTARIES TONIGHT FROM BRANDON SMITH MIKE EVERY AND ANDREW KORYBKO// TARIFF UPDATES FROM THE EU AND CANADA//ISRAEL VS HAMAS/ISRAEL VS LEBANON AND HEZBOLLAH//ISRAEL VS SYRIA: ISRAEL BOMBS MORE AREAS INSIDE SYRIA AND ISSUES A WARNING TO TURKEY/RUSSIA VS UKRAINE UPDATES//IRAN VS USA UPDATES//COVID UPDATES/VACCINE INJURY REPORTS/DR PAUL ALEXANDER/MARK CRISPIN MILLER/SLAY NEWS ETC//CANADA UPDATES ON ITS TARIFF WARS WITH THE USA//USA ECONOMIC DATA RELEASES//SWAMP STORIES FOR YOU TONIGHT

072 C GOLDMAN 706 14 099 H DB AG 333 104 C MIZUHO 2 132 C SG AMERICAS 4667 3 285 C NANHUA USA-HK 24 323 H HSBC 1056 332 H STANDARD CHARTE 747 363 C WELLS FARGO SEC 22 363 H WELLS FARGO SEC 262 435 H SCOTIA CAPITAL 1 624 C BOFA SECURITIES 5 657 C MORGAN STANLEY 261 661 C JP MORGAN 99 2782 661 H JP MORGAN 168 686 C STONEX FINANCIA 26 80 690 C ABN AMRO 311 13 700 C UBS 80 709 C BARCLAYS 20 210 709 H BARCLAYS 96 732 C RBC CAP MARKETS 225 737 C ADVANTAGE 2 13 880 H CITIGROUP 128 905 C ADM 22

TOTAL: 6,189 6,189

MONTH TO DATE:

JPMORGAN stopped 2950 contracts/6189

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 6189 NOTICES FOR 618,900 OZ 19.250 TONNES

total notices so far: 47,704 contracts for 4,770,400 OR 129.129 tonnes)

FOR APRIL

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 730 NOTICE(S) FILED FOR 3.650 MILLION OZ/

total number of notices filed so far this month : 1845 CONTRACTS (NOTICES) for 9.225 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $27.85 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 931.94 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $1.84 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ////A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 446.830 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA HUGE2,093 CONTRACTS TO 172,290 AND CONTINUING ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL GAIN OF $0,15 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A MEGA MEGA HUGE SIZED GAIN OF 2683 TOTAL CONTRACTS.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON WEDNESDAY WITH SILVER’S GAIN IN PRICEBUT THE PRICE IS STILL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. WE HAD A HUGE T.A.S. LIQUIDATION. BUT THIS WAS COUPLED WITH A HUGE T.A.S. ISSUANCE OF 819 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS METALS WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A STRONG 1590 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 819 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUGE SIZED 2683 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE. WE HAD CONSIDERABLE TAS LIQUIDATION/ THROUGHOUT WEDNESDAY’S COMEX TRADING SESSION WHICH ACCOUNTS FOR ALL OF OUR HUGE GAIN IN OI ON OUR TWO EXCHANGES. STRANGELY, ON FIRST DAY NOTICE, THE CME NOTIFIED US THAT WE HAD ANOTHER OF THOSE CRAZY EXCHANGE FOR RISK CONTRACTS ISSUED AT 400 CONTRACTS FOR 2.0 MILLION OZ. THIS WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE 819 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.15 AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A SMALL GAIN IN PRICE AND A HUGE GAIN IN OPEN INTEREST FROM OUR TWO EXCHANGES OF 3927 CONTRACTS.

WE HAD A HUGE 1590 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 12.395 MILLION OZ TO WHICH WE ADD OUR 2.00 MILLION OZ EX FOR RISK

STANDING FOR APRIL INCREASES TO 14.395 MILLION OZ

WE HAD:

/ HUGE COMEX OI GAIN+// A MEGA HUGE SIZED EFP ISSUANCE (1590 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 819 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 244 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 3 DAYS, total 2665 contracts: OR 13.325 MILLION OZ (888 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 13.325 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 13.325 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2093 CONTRACTS WITH OUR GAIN IN PRICE OF 15 CENTS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE 1590 CONTRACT EFP ISSUANCE CONTRACTS: 1590 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A STRONG SILVER OZ STANDING FOR APRIL OF 12.395 MILLION OZ , PLUS OUR NEW 2.00 MILLION EX FOR RISK

NEW STANDING APRIL: 14.395 MILLION OZ

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (819 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 730 NOTICE(S) FILED TODAY FOR 3.650 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5026 OI CONTRACTS TO 493,720 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 536 CONTRACTS CONTRACTS//.

WE HAD A FAIR SIZED DECREASE IN COMEX OI (5026 CONTRACTS) . THIS OCCURRED DESPITE OUR GAIN OF $10.00 IN PRICE WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 160.597 TONNES (CME CORRECTED) TO WHICH WE ADD FOR APRIL ITS INITIAL 700 CONTRACT EXCHANGE FOR RISK FOR 70,000 OZ OR 2.177 TONNES AND OUR NEW EXCHANGE FOR PHYSICAL TRANSFER TO LONDON OF 2753 CONTRACTS OR 275,300 OZ (8.562 TONNES). THUS INITIAL STANDING FOR GOLD/APRIL DELIVERY MONTH IS 160.597 TONNES NORMAL DELIVERY(AFTER REMOVING OUR EXC FOR PHYSICAL TRANSFER + 2.255 TONNES EX FOR RISK = 162.774 TONNES

/NEW STANDING FOR APRIL; 160.597 TONNES + 2.177 TONNES EX FOR RISK = 162.774 TONNES

/ ALL OF THIS HAPPENED WITH OUR $10.00 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX ///. WE HAD A FAIR SIZED LOSS OF 2111 OI CONTRACTS (9.066 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AND NOW FOR OUR FRONT MONTH OF APRIL. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS. WE HAVE A MASSIVE AMOUNT OF TONNES STANDING FOR GOLD IN APRIL.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2915 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 493,720

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2915 CONTRACTS WITH 4490 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 2915 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1575 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 678 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2915 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 5026 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 2111 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING AT THE GOLD COMEX FOR APRIL 160.597 TONNES (WHICH INCLUDES OUR HUGE 8.562 TONNES EFP TRANSFER TO LONDON) AND THIS FOLLOWS FIRST DAY NOTICE INITIAL 2.177 TONNES OF EX. FOR RISK//THUS TOTAL AMOUNT OF GOLD STANDING IN THIS VERY ACTIVE DELIVERY MONTH OF APRIL IS 162.774 TONNES.

//NEW STANDING APRIL: 160.597 TONNES + 2.177 TONNES EX FOR RISK = 162.774 TONNES

.

/ 3) HUGE T.A.S. LIQUIDATION + ZERO SUCCESS IN REMOVING NET SPECULATOR LONGS, AS WE HAD 1) $10.00 COMEX PRICE GAIN AND WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A LOSS OF 2111 CONTRACTS ON OUR TWO EXCHANGES ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN APRIL.

4) STRONG SIZED COMEX OPEN INTEREST DECREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///SMALL T.A.S. ISSUANCE: 678 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 6,525 CONTRACTS OR 652,500 OZ OR 20.295 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 2175 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN3 TRADING DAY(S) IN TONNES 20.295 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 20.295 TONNES DIVIDED BY 3550 x 100% TONNES = 0.571% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 20.295 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE SIZED 2093 CONTRACTS OI TO 172,534 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1590 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1590 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1590 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2093 CONTRACTS AND ADD TO THE 1590 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2683 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 13,42 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 8.12 PTS OR 0.24%

//Hang Seng CLOSED DOWN 362.72 PTS OR 1.52%

// Nikkei CLOSED DOWN 989.94 OR 2.77 %//Australia’s all ordinaries CLOSED DOWN 0.99%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2978 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3006/ Oil DOWN TO 67.58 dollars per barrel for WTI and BRENT DOWN TO 70.57 Stocks in Europe OPENED ALL RED.

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED5026 CONTRACTS TO 493,720 DESPITE OUR GAIN IN PRICE OF $10.00 WITH RESPECT TO WEDNESDAY’S TRADING/. WE LOST ZERO NET LONGS WITH THAT PRICE RISE FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2915 ).

THE CME ANNOUNCED WEDNESDAY NIGHT,A ZERO EXCHANGE FOR RISK CONTRACTS FOR NIL OZ OR 0 TONNES THUS ITS INITIAL ISSUANCE FOR THE FRONT MONTH OF APRIL STANDS AT 2.177 TONNES OF GOLD

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY: WE HAD FIVE EXCHANGE FOR RISKS IN GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.

DETAILS ON APRIL COMEX MONTH

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 2111 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF MARCH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY FRIDAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION// THROUGHOUT THE WEEK.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING A LOWER COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST FRIDAY’S 197 , 199, 2001, , 203 , ,205 , 207 209 AND 211 212 213,215 AND FRIDAY’S 216 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING TODAY’S FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF APRIL .… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2915 EFP CONTRACTS WERE ISSUED: : /APRIL 2915 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2915 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2111 CONTRACTS IN THAT 2915 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A LOSS OF 5026 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $10.00 FOR WEDNESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. MUCH+ OF THE TOTAL LOSS IN OUR TWO EXCHANGES WAS DUE TO THE LIQUIDATION OF T.A.S. CONTRACTS.(GOVERNMENT)

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A SMALL SIZED 678 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S OVER 4 WEEKS AGO AND AGAIN LAST WEEK,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED LITTLE AS FEW LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND NOW ,FOR MARCH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT LAST WEDNESDAY MARCH 17, THE 38,393 T.A.S. CONTRACT ISSUANCE WAS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY DOES TWO IMPORTANT THINGS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH AND APRIL.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH

STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (162.774 TONNES//.CME CORRECTED MAYBE?) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH / FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTHAT 256.607 TONNES

AND NOW LAST 4 MONTHS OF 2025″:

YEAR 2025:

JAN 2025:

113.30 TONNES

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

STANDING FOR GOLD: 160.597 TONNES + 2.177 TONNES EX FOR RISK = 162.774 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 162.774 TONNES (INCLUDES 2.177 TONNES EX FOR RISK)

COMEX GOLD TRADING/APRIL CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $10.00/ /)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED LOSS IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION WEDNESDAY/ AS THEY WERE TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,000 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING AND THEY FAILED MISERABLY AS GOLD IS NOW WELL ABOVE THE $3,000 THRESHOLD AT 3130 PLUS.

LAST NIGHT/THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH MARCH/APRIL TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WILL BE ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND IS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK:

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

NOW APRIL, ISSUES ITS FIRST EXCHANGE FOR RISK:

TOTAL ISSUANCE FOR EXCHANGE FOR RIS ON FIRST DAY NOTICE OF 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD. APRIL ISSUANCE MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK. THESE DELIVERIES WILL BE ADDED TO OUR NORMAL DELIVERY CYCLE. WE HAD 0 NOTICES FOR EXCHANGE FOR RISK FILED FOR TUESDAY.

STANDING NOW FOR APRIL:

APRIL: 160.597 TONNES +(2.177 EX FOR RISK// MARCH 31 FOR APRIL DELIVERY MONTH =162.774TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS APRIL DELIVERY MONTH AFTER FIRST DAY NOTICE;

WE HAVE LOST A STRONG SIZED TOTAL OF 9.066 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL (166.964TONNES) ON FIRST DAY NOTICE FOLLOWED BY OUR INITIAL EXCHANGE FOR RISK ISSUANCE TO THE BANK OF ENGLAND FOR 700 CONTRACTS OR 70,000 OZ (2.177 TONNES) AND TODAY’S HUGE 2,753 CONTRACT EXCHANGE FOR PHYSICAL TRANSFER TO LONDON FOR 275,300 OZ OR 8.562 TONNES. WE MUST NOW ADD OUR 2.177 TONNES EXCHANGE FOR RISK TO OUR NEW NORMAL DELIVERY OF 160.597 TONNES AND THUS STANDING FOR GOLD FOR APRIL IS NOW 162.774 TONNES, THE 2ND HIGHEST EVER RECORDED!

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $10,00

WE HAD 536 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 2111 CONTRACTS OR 211,100 0Z (9.066 TONNES)

i) Brinks customer acct 95,102.657 oz (2958 kilobars) ii) Brinks enhanced: 95,196.15 oz or 238 London good delivery bars/400 oz each.

total weight; 190,298.800 oz or 5.804 tonnes

Deposit to the Dealer Inventory in oz

1 ENTRIES i) Into ASAHI dealer 450,146.151 oz (14,001 KILOBARS)

TOTAL WEIGHT: 450,146.151 oz or 14.001 tonnes

Deposits to the Customer Inventory, in oz

we have 3 customer entries

we have 3 customer deposits

i) Into Brinks customer acct 64,302.000 oz (2,000 kilobars) ii) Into Loomis customer acct 32,151.000 (1000 kilobars) iii) Into Manfra: 36,060.822 oz

total weight; 132,513.827 oz (4.121 tonnes)

total weight dealer and customer; 18.122 tonnes

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

6,189 notice(s) 618,900 OZ 19.250 TONNES

No of oz to be served (notices)

3928 contracts 392,800 OZ 12.217 TONNES

Total monthly oz gold served (contracts) so far this month

47,704 notices 4,770,400 oz 148.379 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits:

dealer deposits: 1

1 ENTRIES i) Into ASAHI dealer 450,146.151 oz (14,001 KILOBARS)

TOTAL WEIGHT: 450,146.151 oz or 14.001 tonnes

xxxxxxxxxxxxxxxxxxxxx

deposits customer

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 0

0 entry

weight in tonnes: .000 tonnes

xxxxxxxxxxxxxxxxx

we have 3 customer deposits

i) Into Brinks customer acct 64,302.000 oz (2,000 kilobars) ii) Into Loomis customer acct 32,151.000 (1000 kilobars) iii) Into Manfra: 36,060.822 oz

total weight; 132,513.827 oz (4.121 tonnes)

total weight dealer and customer; 18.122 tonnes

adjustments:

i) Brinks /customer to dealer: 160,079.829 oz

ii) customer to dealer Manfra: 192,745.245 oz

xxxxxxxxxxxxxxxxxx

AMOUNT OF GOLD STANDING FOR APRIL

THE FRONT MONTH OF APRIL HAD A LOSS OF 6279 CONTRACTS TO STAND AT 10,117. WE HAD 3526 CONTRACTS FILED YESTERDAY. THUS WE LOST A MAMMOTH 2753 CONTRACTS OR 275,300 OZ AS WE EXPERIENCED A MASSIVE EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE THESE BOYS DESIRED TO TAKE DELIVERY OVER IN LONDON FOR FEAR THAT NO GOLD WOULD BE AVAILABLE FOR THEM OVER HERE!! (DUE TO TARIFF INITIATION).

MAY GAINED 235 CONTRACTS DOWN TO 3949 CONTRACTS

JUNE LOST A SMALL 1012 CONTRACTS TO 401,718 AND JUNE WILL NO DOUBT BE A WHOPPER OF A DELIVERY MONTH

We had 6189 contracts filed for today representing 618,900 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 99 notices issued from their client or customer account. The total of all issuance by all participants equate to 6,189 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2950 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL /2025. contract month, we take the total number of notices filed so far for the month (47,704 X 100 oz ) to which we add the difference between the open interest for the front month of APRIL (10,117 CONTRACTS) minus the number of notices served upon today (6189 x 100 oz per contract) equals 5,163,200 OZ OR 160.597 TONNES

to which we add our initial exchange for risk of 70,000 oz (2.177 tonnes) = 162.774 tonnes

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (47,704 x 100 oz +we add the difference for front month of APRIL (10,117 OI} minus the number of notices served upon today (6189 x 100 oz) which equals 5,163,200 OZ OR 160.597 TONNES + 2.177 tonnes ex for riskprior = 162.774 tonnes

TOTAL COMEX GOLD STANDING FOR APRIL.: 162.774 TONNES WHICH IS HUGE FOR THIS ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL IS FOLLOWING SUIT..

i) Out of Brinks 1175,120.600 oz ii) Out of Delaware 999.900 oz iii) Out of HSBC 594,475.565 oz

total withdrawals 1770,,595.665 oz

ADJUSTMENTs 3 entries// customer to dealer

i) Brinks 419,210.000 oz

ii) CNT 666,601.900 oz

iii) Manfra: 376,255.000 oz

JPMorgan has a total silver weight: 196.297million oz/484.931oz million or 40.55%

TOTAL REGISTERED SILVER: 157.937 MILLION OZ//.TOTAL REG + ELIGIBLE. 484.931Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2025 OI: 1364 OPEN INTEREST CONTRACTS FOR A GAIN OF 329 CONTRACTS. WE HAD 119 NOTICES FILED YESTERDAY SO WE GAINED A MASSIVE 448 CONTRACT QUEUE JUMP FOR 2.240 MILLION OZ//

MAY SAW A LOSS OF 1170 CONTRACTS UP TO 120,134 CONTRACTS

JUNE SAW A LOSS OF 13 CONTRACTS DOWN TO 1315 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 730 or 3.650 MILLION oz

CONFIRMED volume; ON WEDNESDAY 74,361 good//

AND NOW APRIL DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1845 X5,000 oz = 9.225 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (1364) AND the number of notices served upon today (730 )x (5000 oz)

Thus the standings for silver for the APRIL 2025 contract month: (1845) Notices served so far) x 5000 oz + OI for the front month of APRIL(1364) minus number of notices served upon today (730)x 5000 oz equals silver standing for the APRIL contract month equating to 12.395 MILLION OZ . WE MUST NOW ADD OUR 2.0 MILLION OZ EXCHANGE FOR RISK ISSUED ON MONDAY MARCH 31/NEW STANDING INCREASES TO 14.395 MILLION OZ

New total standing: 14.395 million oz which is huge for this NON active delivery month of APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 157.937million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS/

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

MARCH 21 WITH GOLD DOWN $20.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 910.43 TONNES

MARCH 20 WITH GOLD UP $3.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 909.28 TONNES

MARCH 19 WITH GOLD UP $0.45 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 907.27 TONNES

MARCH 18 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 907.27 TONNE

MARCH 17 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.64 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 906.41 TONNES

MARCH 14 WITH GOLD UP $9.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MONSTER DEPOSIT OF 7.17 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 905.81 TONNES

MARCH 13 WITH GOLD UP $42.85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 12 WITH GOLD UP $22.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.90 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 895.20 TONNES

MARCH 11 WITH GOLD UP $21.20 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 891.30 TONNES

MARCH 10 WITH GOLD DOWN $12.45 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 894.317 TONNES

MARCH 7 WITH GOLD DOWN $12.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 6 WITH GOLD UP $2.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 900.30 TONNES

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

GLD INVENTORY: 931.94 TONNES, TONIGHTS TOTAL

SILVER

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

MARCH 21 WITH SILVER DOWN $0.45 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 442.962 MILLION

MARCH 20 WITH SILVER DOWN $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 19 WITH SILVER DOWN $0.45 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.219 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 18 WITH SILVER UP $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.823 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.373 MILLION

MARCH 17 WITH SILVER UP $0.03 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.096 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 439.550 MILLION

MARCH 14 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.910 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.454 MILLION

MARCH 13 WITH SILVER UP $0.46 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.774 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 434.544 MILLION

MARCH 12 WITH SILVER UP $0.57 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.032 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 435.318 MILLION

MARCH 11 WITH SILVER UP $0.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.816 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 436.410 MILLION

MARCH 10 WITH SILVER DOWN 25 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.276 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.591 MILLION

MARCH 7 WITH SILVER DOWN 40 CENTS/HUGL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.184 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 434.317 MILLION

MARCH 6 WITH SILVER UP 16 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.455 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.046 MILLION

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

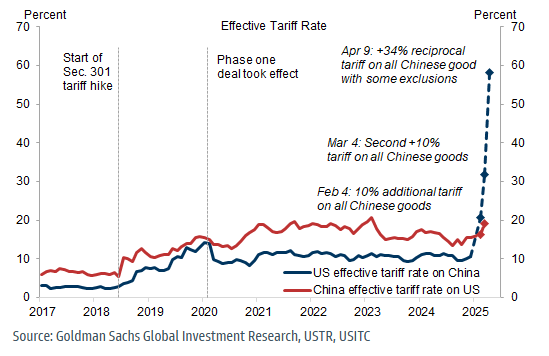

Regular readers of my Substack are aware that I have been warning about the lethal combination of a credit bubble bursting coupled with Smoot-Hawley Tariff Act Mark 2.

Now it’s happening. Trump really meant it when he said he would protect US industry with tariffs, and we knew the answer last night when tariff rates were set out against almost every nation and even one that is not: Two Arctic islands, Svalbard and Jan Mayen were on his list. Some mistake there, surely, other than for US consumers of seal, walrus, and whale meat.

The last time this happened was in 1929-1930, and we know the outcome. The combination of the roaring ’20s bubble and the Smoot Hawley Tariff Act of 1930 resulted in the Wall Street Crash, the subsequent bear market that wiped out about 90% of the Dow, and the depression that led to the failure of about 9,000 banks.

Can it happen again?

You bet. But this time, there are additional factors. Then only about 3% of US GDP was imported consumer goods. Now the figure is considerably greater. The credit bubble is far larger than that of the late ’20s. The financial and monetary consequences promise to be even greater than 1929-1930.

Furthermore, international portfolio diversification has led to foreigners holding over $14 trillion of US equities. They are not going to go down with the sinking ship. They will sell them and dollars, which is why the US dollar’s trade-weighted index has been hit hard, doubtless with more to come.

The impact on both the US and the wider world is going to be extremely serious. This is why equities are falling and bonds are rising (yields falling) in anticipation of portfolios moving out of equities and into the relative safety of government debt. The overvaluation of equities relative to bonds is shown next:

I have used log scales and inverted the US Treasury 10-year note’s yield to show how closely it negatively correlates with the S&P. Everyone understands this relationship. But since Covid, the relationship has broken down, first by zero interest rates driving the yield to under 1% intramonth, and now by equities continuing to rise despite the rise in bond yields. This bubble is twice as extreme as that of the dot-coms in 2000.

The move out of equities into bonds is a temporary portfolio adjustment, because the economic consequences of a collapsing credit bubble drive government finances deep into debt traps. When that happens, bond yields rise to reflect the debt crisis and loss of purchasing power for afflicted currencies. And the pace of economic destruction accelerates.

This brings us to gold, which is legal money (all else being credit in its many forms). The immediate reaction is for market-makers to mark prices down in expectation that profits will be taken to cover losses elsewhere. In fact, gold and gold ETFs are miniscule parts of portfolios and it is more a question of buyers staying away amid the uncertainty. Silver, which is naturally more volatile, is hit even worse.

It is a two-act play. Before the great financial crisis, gold had risen to about $1,000, only to be marked down to under $700. As the inflationary consequences of the Fed’s rescue of the entire banking system sank in, a bullish phase begun taking gold to over $1,900.

My guess is that gold’s markdown this time will be negligible in comparison, because of central bank and Asian demand for physical. Furthermore, the near total lack of exposure to gold and silver along with their derivatives points to portfolio shifts in favour of gold once the initial shock of the bubble being pricked combined with Smoot-Hawley Mark 2 has passed.

end

3. C Powell and Gata dispatches

4. ANDREW MAGUIRE INTERVIEWING PETER GRANDICH

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//COPPER

6 CRYPTOCURRENCY NEWS

ASIA TRADING THURSDAY MORNING WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 8.12 PTS OR 0.24%

//Hang Seng CLOSED DOWN 362.72 PTS OR 1.52%

// Nikkei CLOSED DOWN 989.94 OR 2.77 %//Australia’s all ordinaries CLOSED DOWN 0.99%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2978 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3006/ Oil DOWN TO 67.58 dollars per barrel for WTI and BRENT DOWN TO 70.57 Stocks in Europe OPENED ALL RED.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2978

OFFSHORE YUAN: UP TO 7.3006

SHANGHAI CLOSED CLOSED DOWN 8.12 PTS OR 0.24%

HANG SENG CLOSED CLOSED DOWN 352.72 PTS OR 1.52%

2. Nikkei closed DOWN 989.94 PTS OR 2.77%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 101.37// EURO RISES TO 1.1088 UP 184 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: FALLS TO. +1.340//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.21…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6500/Italian 10 Yr bond yield DOWN to 3.777 SPAIN 10 YR BOND YIELD DOWN TO 3.304

3i Greek 10 year bond yield DOWN TO 3.470

3j Gold at $3094.90 Silver at: 32.37 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 30 /100 roubles/dollar; ROUBLE AT 83.94

3m oil into the 67 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.21// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.340 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8600 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9538 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.080 DOWN 11 BASIS PTS…

USA 30 YR BOND YIELD: 4.480 DOWN 7 BASIS PTS/

USA 2 YR BOND YIELD: 3.809 DOWN 8 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 37.93…

10 YR UK BOND YIELD: 4.6220 DOWN 6 PTS

10 YR CANADA BOND YIELD: 2.952 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.570 DOWN 1 PTS.

2a New York OPENING REPORT

Reign Of Tariffs Begins: Futures Crash, Dollar Craters

Thursday, Apr 03, 2025 – 08:21 AM

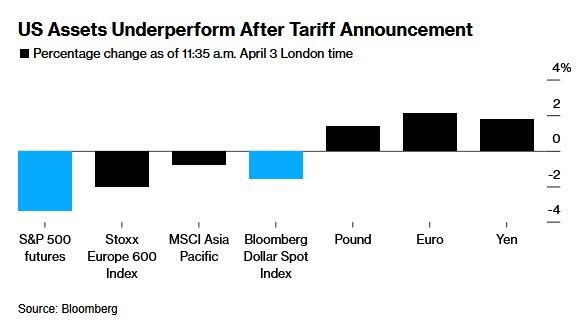

Well, Trump’s “liberation day” is here… and it has liberated countless traders of their net worth and risk assets: the market’s reaction to Trump’s newly-instituted “much worse than expected”reign of tariffs is nothing short of a bloodbath, with a global selloff hitting stock markets everywhere but especially in the US where conventional wisdom, at least early on, is that the recession will be worst. As of 8:00am ET, S&P futures are down 3.5%, while Nasdaq futures tumble 4%, but should really be down more: Pre-market, AAPL (-7.5%), AMZN (-5.6%) and TSLA (-4.6%) are among the worst performing stocks within Mag 7, which is red across the board. As Trump unveiled yesterday (after the close), all US imports will have a minimum 10% tariff, with additional duties for big trading partners. China faces a tariff of well above 50% on many goods; the EU is subjected to a 20% levy. Bond yields crash in anticipation of a looming recession, down 4-10bp lower across the board, the Bloomberg US Dollar index is down -1.6%, set for its biggest drop . Commodities are all also sharply lower: WTI -3.9%, silver -3.4%, even gold is back under $3000. On today’s calendar we get initial and con continuing jobless claims as well as the latest ISM Services data.

Roughly $1.7 trillion is set to be erased from the S&P 500 Index when trading opens Thursday amid worries that the sweeping tariffs could plunge the economy into a recession. The damage was heaviest in companies whose supply chains are most dependent on overseas manufacturing. Apple, which makes the majority of its US-sold devices in China, is on track to open down 7.7%. Lululemon Athletica and Nike among companies with manufacturing ties to Vietnam, are down at least 9%. Walmart Inc. and Dollar Tree Inc., retailers whose stores are filled with products sourced outside of the US, are trading at least 4% lower.

In premarket trading, Apple is the biggest laggard among the Mag7 as the iPhone maker is one of the firms most exposed to tariff risk given China is a key manufacturing hub (Apple -7.2%, Amazon -6.3%, Nvidia -5.5%, Tesla -5.9%, Meta -4.7%, Alphabet -3.0%, Microsoft -2.7%). In general, stocks linked to global trade and the health of the economy are sliding after President Donald Trump announced a minimum 10% tariff on all exporters to the US and additional duties on about 60 nations with large trade imbalances with the US.

Tech: Broadcom (AVGO) -6.2%, Micron (MU) -6.6%, Dell (DELL) -8.4%, HP Inc. (HPQ) -7.0%

Automakers: General Motors (GM) -2.4%, Ford (F) -2.3%, Rivian (RIVN) -5.3%, Lucid (LCID) -5.4%

Financials: JPMorgan (JPM) -3.8%, Bank of America (BAC) -3.9%, Wells Fargo (WFC) -4.5%, Morgan Stanley (MS) -4.8%, Goldman Sachs (GS) -4.6%, Citigroup (C) -4.5%; crypto stocks also slide

Lyft Inc. (LYFT) falls 11% after Bank of America downgraded the ride-sharing company by two notches to underperform, citing reasons that include Waymo’s rapid expansion in San Francisco and Los Angeles.

RH (RH) tumbles 28% after the luxury home furnishing company’s annual revenue growth forecast trailed Wall Street expectations. Analysts note that new round of tariffs add “significantly more uncertainty.”

Here are the key sectors in focus this morning:

Tech and Chips

Apple, which counts China as a key manufacturing hub, led the Mag 7 group lower. Among other Mag 7 movers: Amazon -5.1%, Meta -3.2%

Chipmakers were broadly lower; Nvidia is down 3.2% while Broadcom and Micron also slip.

Automakers, Industrials, Transport

Tariffs threaten to add thousands to car prices, and steep tariffs on the sector are already set to go into effect Thursday morning. EV-makers moving lower: Tesla -3.7%, Rivian -3%

Industrial behemoths slip in postmarket trading as tariff risks may hurt companies with global supply chains. Watch: Caterpillar, Dover, General Electric, Lockheed Martin, Boeing, RTX and Eaton.

Financials

Big banks trade lower and the SPDR S&P Regional Banking ETF falls 4.4%

Consumer

Watch apparel stocks as tariffs on countries like Vietnam and Indonesia are poised to rattle the global shoe and clothing supply chain.

Travel and leisure stocks are down on fears tariffs will raise prices for consumers and curb discretionary spending.

Retailers — many of which source goods from China — are also falling, including Walmart -5.8% and Target -5.2%

Homebuilding

From lumber to steel to building supplies, home construction is highly exposed to tariffs; Watch the ETF (XHB US) that tracks homebuilder and home improvement stocks and its members: Williams-Sonoma, Dream Finders Homes, Builders FirstSource.

Chinese Companies

US-listed shares of Chinese companies decline, including Alibaba -2.7%

Fears about growth and inflation are front of mind, while investors are also dealing with a new level of risk related to volatility and positioning. UBS economists said that real GDP could be hit by 1.5-2 percentage points in 2025, while inflation could rise to close to 5% if tariffs are not reversed soon. RBC strategist Lori Calvasina, meanwhile, cautioned that a “growth scare drawdown” is likely if the S&P falls meaningfully below its mid-March low. In other US assets, Treasury yields slumped while the dollar also fell. Apple and Nike — which rely on global supply chains — are both down more than 6% premarket.

While the jury is still out on the final outcome of Trump’s “reign of tariffs”, which came in far more sever than expected, one thing is emerging: for now, Trump’s shake-up of the global trading system is hurting US assets more than those in many of the big economies he has just slapped with additional tariffs. As noted above, US index futures tumbled as much as 4% after and the dollar cratered, while the impact elsewhere was less extreme. The Stoxx Europe 600 was down 1.9% and a broad gauge of Asian stocks fell as much as 1.7%; while the euro was up 2.2% against the dollar, hitting its highest level since October in what was its biggest one-day jump in a decade. The yen likewise soared.

The tariff announcement has put more pressure on a US stock market that had already floundered this year, as investors braced for Trump’s policies to stir up inflation and raise the odds of a recession in the world’s largest economy. The S&P 500 was down 3.6% this year before the tariff announcement, while the Nasdaq 100 had shed about 7%. The Magnificent Seven tech stocks have also tumbled. By contrast, Germany’s DAX is up 10% in 2025.

“We aren’t buying the dip in the US,” said Aneeka Gupta, head of macroeconomic research at Wisdom Tree UK Ltd. “Investors are turning toward income as a source of refuge in these times of uncertainty as they wait and watch how countries essentially come back with their countermeasures.”

The widespread selloff in global markets makes clear that investors don’t expect any winners from the latest – and by the far the largest – salvo in a growing trade war. But they also suggest the US itself might be one of the biggest victims of Trump’s protectionist policies.

“Global asset allocators will be looking at the US in a very different way,” Neil Birrell, chief investment officer at Premier Miton Investors, said by phone. “Would international investors sell the US as a result of this and start moving money? Yes, they probably will.”

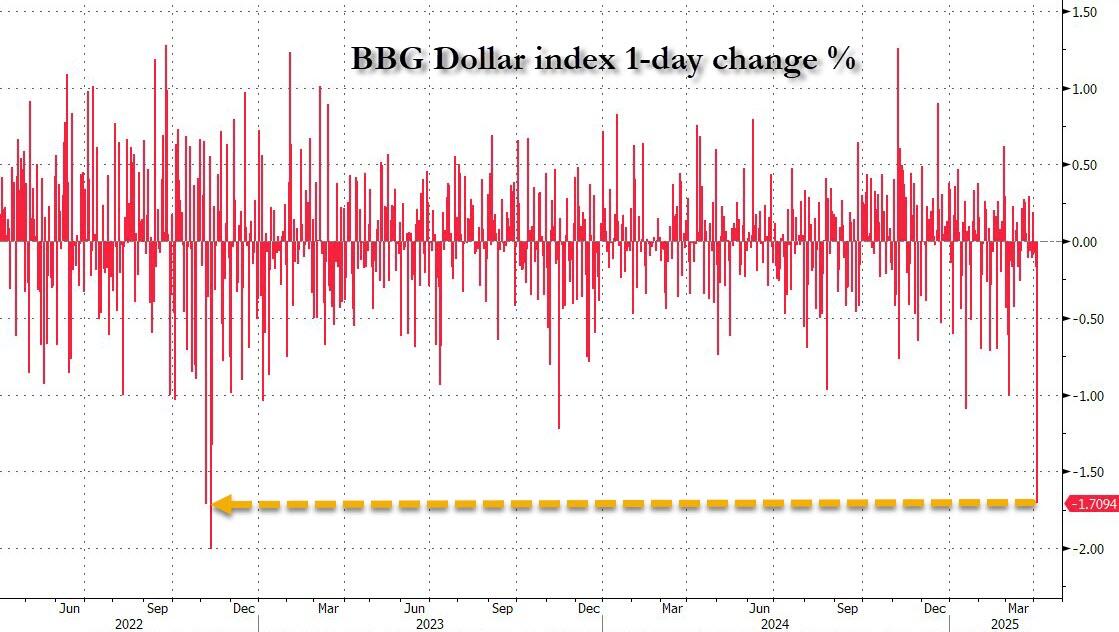

Meanwhile, the dollar headed for its worst day in over two years…

… as traders prepared for the economic impact. The Japanese yen gained 1.9% against the greenback, and Treasury 10-year yields hit their lowest level since October, further weighing on the greenback. The Euro meanwhile enjoyed its best 1 day against the dollar in the last decade: only the 3.1% surge in Dec 2015 was bigger.

“The aggravation of US growth concerns on the tariff news and related further falls in US stocks has meant that the dollar isn’t enjoying its traditional safe-haven, reserve currency status support,” said Ray Attrill, head of foreign-exchange strategy at National Australia Bank Ltd.

The Stoxx 600 falls 1.6% to the lowest since the end of January after Trump announced the steepest American tariffs in a century, including a 20% rate for the European Union, which said it will retaliate. Most sectors are sliding, with real estate and utilities among the rare gainers. Consumer products, banks and technology are the worst hit sectors. Here are the biggest movers Thursday:

Most European sectors are under pressure following Trump’s tariff announcement. Banks, tech, industrials and commodity-linked sectors are the worst performers, while those that offer defensive charecteristics, such as utilities and real estate, are outperforming

European medical technology and healthcare services stocks drop after Trump said he will apply at least a 10% tariff on all exporters to the US, with even higher duties on some 60 nations

European luxury stocks slide after Trump unveiled a 20% tariff on EU imports and a 31% rate on Switzerland. Companies that make goods in the US and EU, like LVMH, could see less of an earnings hit, according to analysts

Logitech shares sink as much as 12%, the most in over a year, hit by escalating trade tensions from the US. The computer peripherals firm is seen more sensitive to higher tariffs as it generates bulk of sales from the US and owns production facilities in China

Diageo shares rise as much as 3.1%, leading gains for European distillers, as analysts say the US tariffs announcement avoided the worst-case scenario for the sector

South Africa’s key stock index drops as much as 2.6%, the most since August, as new US tarrifs weigh on global markets. A deepening dispute in the nation’s ruling coalition over proposed tax increases also hit the sentiment

Roche shares drop as much as 2.9%, lagging behind European pharma peers, after the company said a high-dose version of its best-selling multiple sclerosis drug Ocrevus failed to outperform the original in a large study

LPP drops as much as 7.7% after Poland’s biggest fashion retailer reported 4Q earnings missing estimates and confirmed an ambitious store opening plan that is seen by analysts as a profitability risk.

Earlier in the session, Asian stocks also tumbled:

Japan’s Nikkei 225 suffered heavy losses with the index firmly beneath the 35,000 level after the US announced 24% tariffs for Japan, while notable losses were seen in the financial sector and automakers were also hit by the 25% auto tariffs.

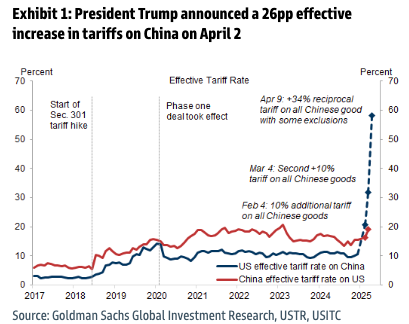

Hang Seng and Shanghai Comp were pressured after US President Trump imposed a 34% tariff on China, on top of the existing 20% tariffs, for a total 54% tariff rate which saw the Hong Kong benchmark conform to the broad selling in the Asia-Pac region although the mainland initially showed some resilience with downside somewhat cushioned after stronger-than-expected Chinese Caixin Services PMI data.

Australia’s ASX 200 declined with the index dragged lower by underperformance in tech and energy, while there were comments from Australian PM Albanese who said they will not impose reciprocal tariffs and will continue to make the case for these unjustified tariffs to be removed from exporters.

In FX, the Bloomberg Dollar Spot Index drops 1.7%, on course for its largest intraday fall since November 2022. The Swedish krona is leading gains against the greenback, rising 2.4%. The Japanese yen and Swiss franc are not far behind.

In rates, treasuries rally, pushing US 10-year yields down 7 bps to 4.06%. European bonds also gain, led by the short-end as traders boost bets on interest rate cuts by both the European Central Bank and Bank of England.

In commodities, WTI drops 3.9% to below $69 a barrel. Spot gold declines 50 to around $3,091/oz. Bitcoin falls 3% to below $83,000

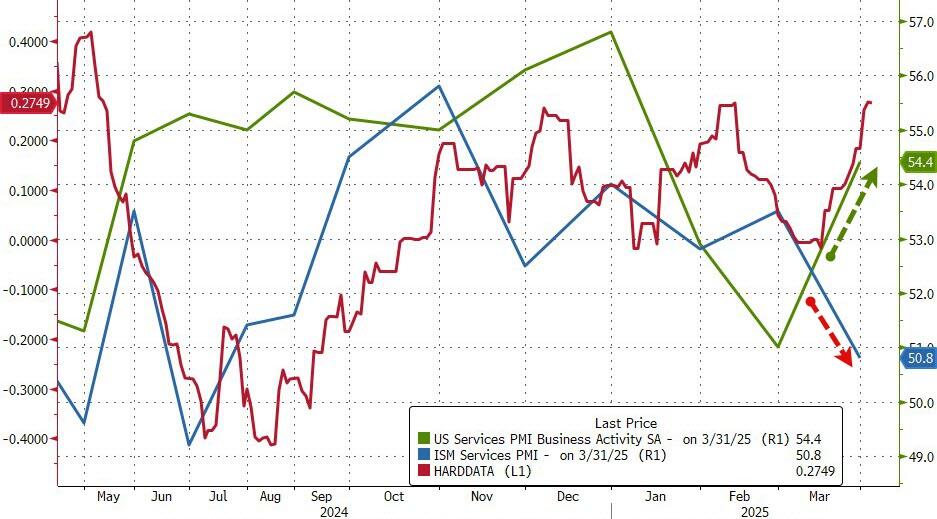

Looking to the day ahead now, focus within a busy economic release schedule will likely center on March ISM Services at 10am ET, seen easing to 52.9, from 53.5. Other releases include Challenger job cuts report for March at 7.30am ET, Trade balance for Feb. at 8.30am ET and US weekly jobless claims at 8.30am ET. Central bank speakers include Fed’s Jefferson and Cook’s speech and the ECB’s account of the March meeting. NATO’s foreign ministers are also set to meet today until April 4.

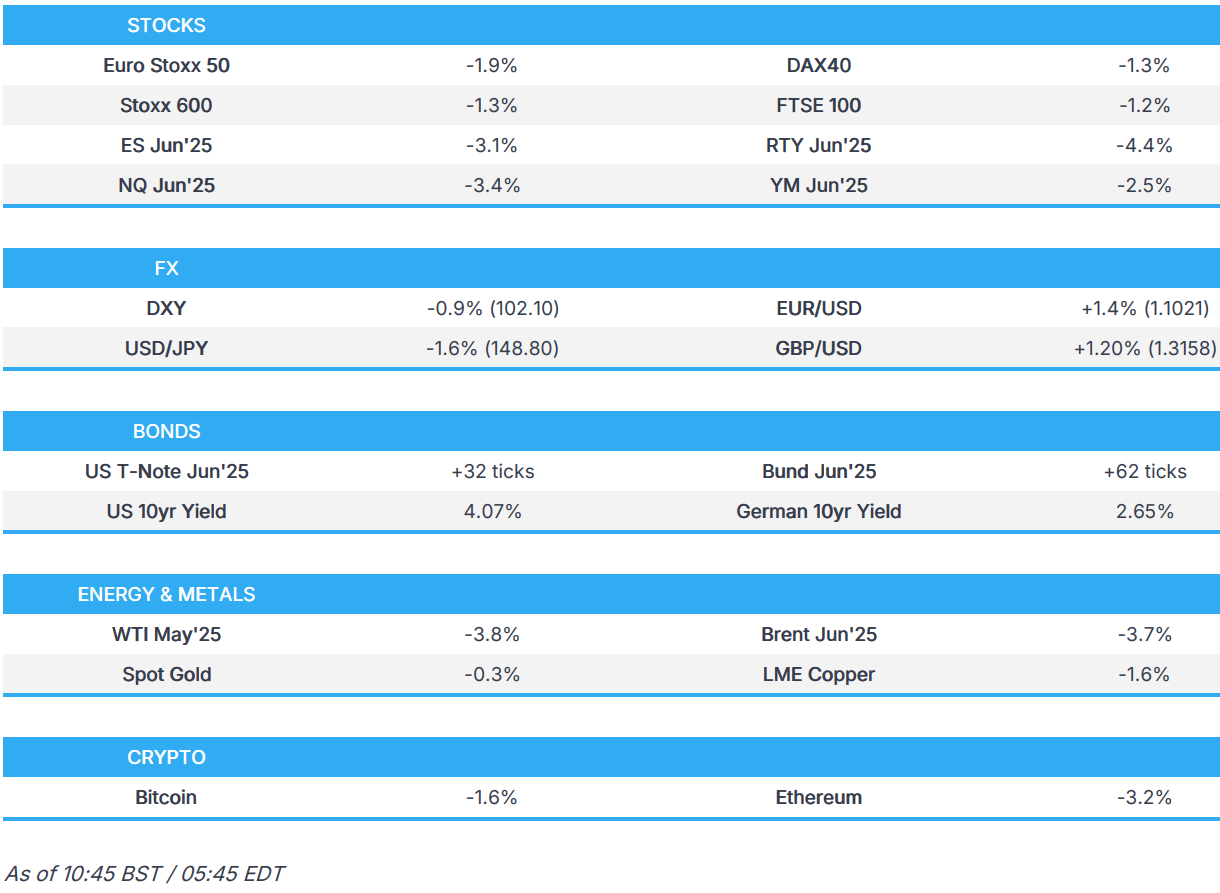

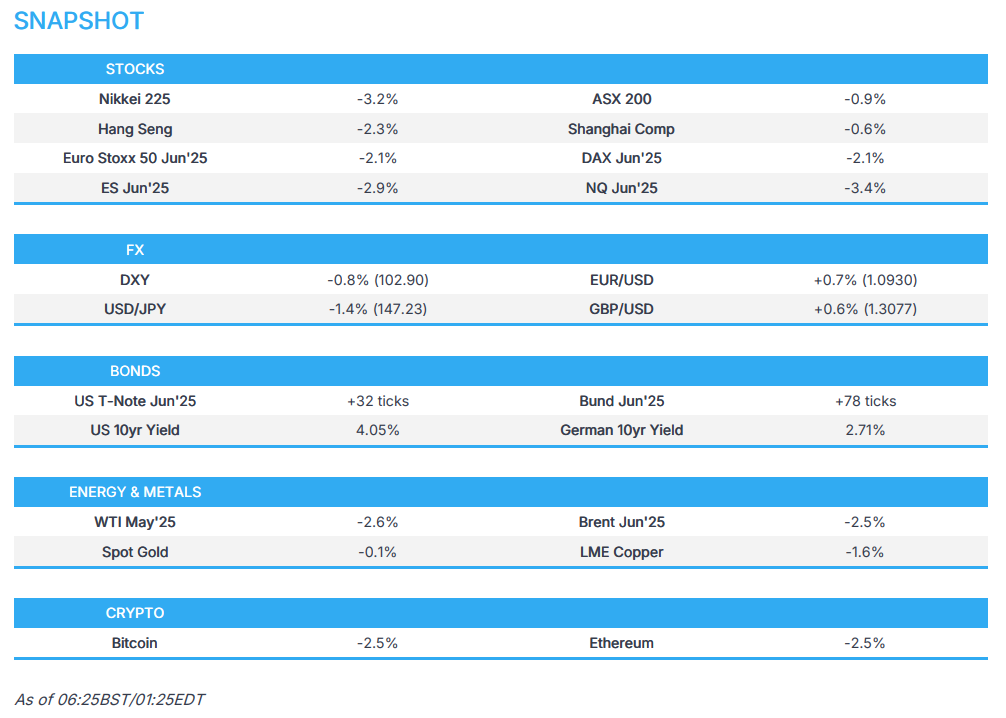

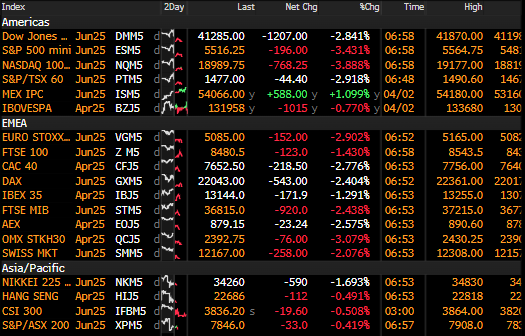

Market Snapshot

S&P 500 mini -3.2%

Nasdaq 100 mini -3.8%

Russell 2000 mini -4.4%

Stoxx Europe 600 -1.5%

DAX -1.7%

CAC 40 -2.1%

10-year Treasury yield -5 basis points at 4.08%

VIX +3.9 points at 25.45

Bloomberg Dollar Index -1.3% at 1254.51

euro +1.5% at $1.1018

WTI crude -3.3% at $69.35/barrel

Top Overnight News

Apple shares slumped premarket on the tariffs announcement despite efforts to insulate its supply chains. Other major tech stocks including Nvidia, Meta, Tesla and Alphabet also declined. Nike, Adidas and Puma plunged given their reliance on Vietnamese manufacturing. BBG

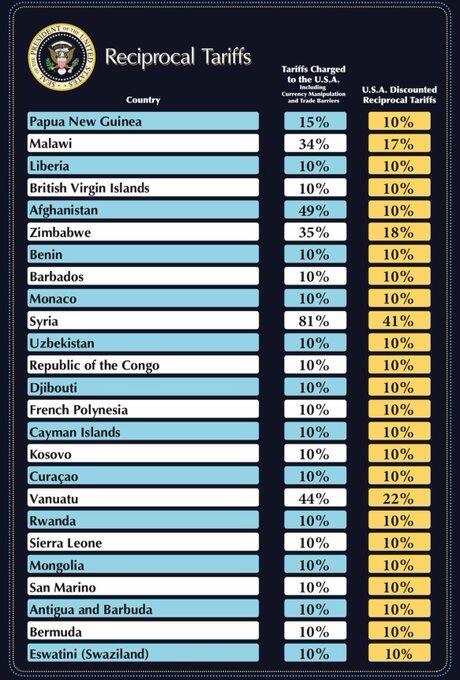

Here’s what the White House and its crack team of trade investigators seems to have done: Take the US’s goods trade deficit with any particular country, and divide it by the total amount of goods imported from that country. Cut that percentage in half, and there’s the US’s “reciprocal” tariff rate. FT

US President Trump reiterated that tax cuts will be passed in one big beautiful bill in Congress, while he added they need to get permanent tax cuts.

US President Trump posted on Truth Social that “Speaker of the House Mike Johnson and Senate Majority Leader John Thune have been working tirelessly on taking the next step to pass the plan for our ONE, BIG, BEAUTIFUL BILL, as it is known, as well as getting us closer to the Debt Extension necessary to continue our great work. The Senate Budget plan gives us the tools that we need to get our shared priorities done, including certain PERMANENT Tax Cuts, Spending Cuts, Energy, Historic Investments in Defense, Border, and much more. We are going to cut Spending, and right-size the Budget back to where it should be. The Senate Plan has my Complete and Total Support. Likewise, the House is working along the same lines. Every Republican, House and Senate, must UNIFY. We need to pass it IMMEDIATELY!”

In the immediate aftermath of Trump’s tariff announcement, confusion reigned even among some White House officials about what rate the approximately $440 billion in Chinese imports would face. Policy experts were perplexed, too. Barron’s

Fed Governor Kugler said the latest data indicates progress towards the 2% inflation target may have stalled and she supports keeping the current policy rate in place as long as upside risks to inflation continue, given stable activity and employment. Furthermore, she stated that inflation expectations have risen and upcoming policy changes hold upside risk, as well as noted that there may be reasons why tariffs have more prolonged effects.

Goldman’s bottom line on Tariff Announcements: The “reciprocal” tariff policy President Trump announced would impose a weighted average tariff rate of 18.3%, around 3pp higher than we expected. However, roughly 1/3 of total imports would be exempt, which reduces the impact to a 12.6pp increase in the effective tariff rate. We estimate this and other tariffs announced year-to-date would raise the US effective tariff rate by 18.8pp. While we assume that negotiations with trading partners will lead to somewhat lower “reciprocal” rates than announced today, the prospect for escalation following retaliatory tariffs and a high probability of further sectoral tariffs suggests a risk that the US effective tariff rate rises more than the 15pp increase we assume in our economic forecast. GIR