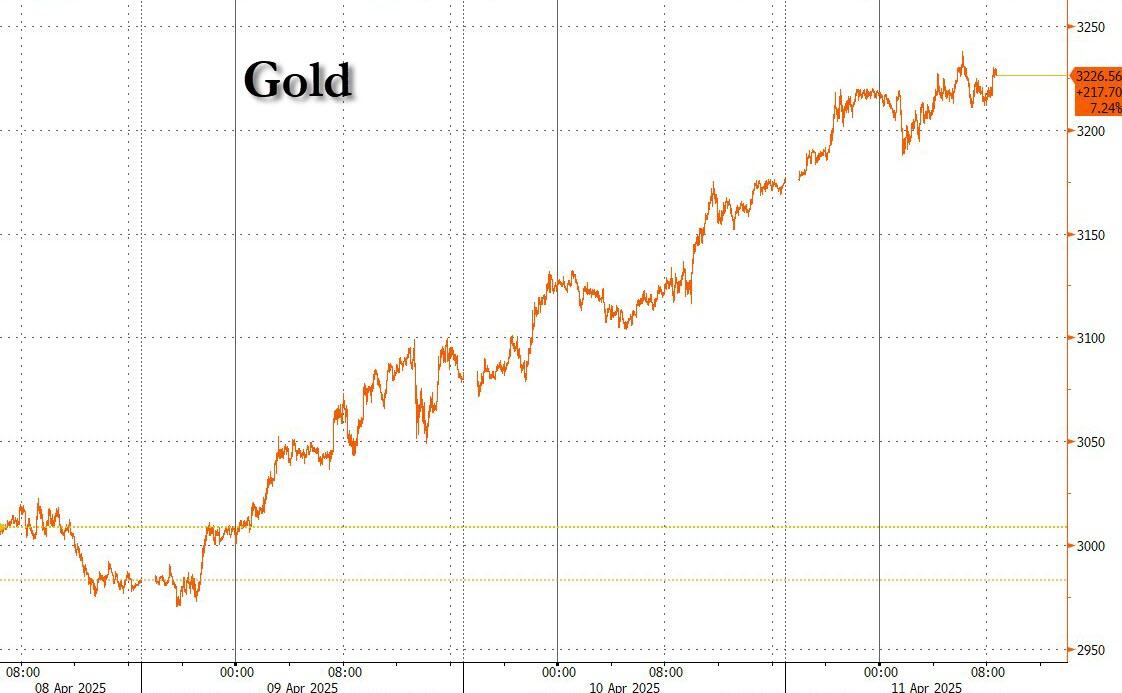

GOLD CLOSED UP $67.70 TO $3,227.30

SILVER CLOSED UP $1.17 TO $32.01

GOLD ACCESS CLOSED 3229.65

Silver ACCESS CLOSED: $32.16

Bitcoin morning price:$82160 UP 2063 DOLLARS.

Bitcoin: afternoon price: $83,177 up 3130 DOLLARS

Platinum price closing UP $3.85 TO $939.90

Palladium price; DOWN $1.20 TO $918.75

END

*CANADIAN GOLD: $4486.20 UP 38.80 CDN dollars per oz( * NEW ALL TIME HIGH 4493.62 CDN DOLLARS PER OZ//MARCH 31 2025)

*BRITISH GOLD: 2471.21 UP 16.96 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,471.21 BRITISH POUNDS/OZ) APRIL 11/2025

*EURO GOLD: 2,849.80 UP 17.47 Euros per oz //* (ALL TIME CLOSING HIGH: 2,888.55 EUROS PER OZ/MARCH 31 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,155.200000000 USD

INTENT DATE: 04/10/2025 DELIVERY DATE: 04/14/2025

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 2

323 C HSBC 85

363 H WELLS FARGO SEC 962

624 H BOFA SECURITIES 100 11

661 C JP MORGAN 29

686 C STONEX FINANCIA 32 18

690 C ABN AMRO 24 14

737 C ADVANTAGE 157

880 H CITIGROUP 793

905 C ADM 15

TOTAL: 1,121 1,121

MONTH TO DATE: 60,722

JPMORGAN stopped 29/1121

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 1121 NOTICES FOR 112,100 OZ 3.486 TONNES

total notices so far: 60,722 contracts for 6,072,200 OR 188.871 tonnes)

FOR APRIL

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 190 NOTICE(S) FILED FOR 0.950 MILLION OZ/

total number of notices filed so far this month : 2710 CONTRACTS (NOTICES) for 13.55 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $67.70 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

MEGA HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 949.71 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $1.17 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ////A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 449.514 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 512 CONTRACTS TO 150,668 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS GOOD SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.18 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. HOWEVER, WE HAD A SMALL SIZED GAIN OF 288 TOTAL CONTRACTS AS THE CME NOTIFIED US OF A HUGE 800 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD A CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING THURSDAY AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON THURSDAY WITH SILVER’S GAIN IN PRICE BUT THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH A MEGA HUMONGOUS T.A.S. ISSUANCE OF 3527 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS METALS WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A HUGE 800 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUMONGOUS 3527 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 15,061 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.18. WE HAD CONSIDERABLE TAS LIQUIDATION/ THROUGHOUT THURSDAY’S COMEX TRADING SESSION. TODAY, THE CME NOTIFIED US THAT WE HAD 0 CONTRACTS OF THOSE CRAZY EXCHANGE FOR RISK CONTRACTS ISSUED FOR 0 OZ (0 MILLION OZ). THESE EXCHANGE FOR RISKS ARE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THUS FOR THE MONTH OF APRIL WE HAVE A TOTAL OF 4.0 MILLION OZ OF EXCHANGE FOR RISK ISSUED ON TWO OCCASIONS. THE RECIPIENT OF THIS LARGESS IS PROBABLY THE CENTRAL BANK OF INDIA.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT/FRIDAY MORNING: A HUMONGOUS 3527 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.18) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A STRONG GAIN IN PRICE AND WE GAINED A A HUGE 16,061 CONTRACTS IN OPEN INTEREST FROM OUR TWO EXCHANGES.

WE HAD A HUGE 800 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.735 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP FOR PHYSICAL TRANSFER TO WHICH WE ADD OUR 4.00 MILLION OZ EX FOR RISK

STANDING FOR APRIL DECREASES TO 18.150 MILLION OZ

WE HAD:

/ GOOD COMEX OI LOSS+// A HUGE SIZED EFP ISSUANCE (800 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 3527 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A MONSTROUS 7573 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 9 DAYS, total 13,487 contracts: OR 67.435 MILLION OZ (1498 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 67.435 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 67.435 MILLION OZ/// THIS IS HUGE AND THIS MONTH WILL PROBABLY BE A HUMDINGER OF ISSUANCE.

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 7061 CONTRACTS DESPITE OUR SMALL GAIN IN PRICE OF $0.18 IN SILVER PRICING AT THE COMEX// THURSDAY.,. (DUE TO T.A.S. ISSUANCE). THE CME NOTIFIED US THAT WE HAD A HUGE 800 CONTRACT EFP ISSUANCE CONTRACTS: 800 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A STRONG SILVER OZ STANDING FOR APRIL OF 14.150 MILLION OZ , PLUS OUR 4.00 MILLION EX FOR RISK

NEW STANDING APRIL: 18.150 MILLION OZ

THE NEW TAS ISSUANCE THURSDAY NIGHT (3527 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 190 NOTICE(S) FILED TODAY FOR 0.950 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 10,417 OI CONTRACTS TO 459,504 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A MONSTROUS 17,243 CONTRACTS CONTRACTS//.

WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI (10,417 CONTRACTS) . THIS OCCURRED WITH OUR MAMMOTH GAIN OF $100.00 IN PRICE THURSDAY. YESTERDAY WAS ALSO THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES (CME CORRECTED// MAYBE?) TO WHICH WE ADD FOR APRIL ITS INITIAL 700 CONTRACT EXCHANGE FOR RISK FOR 70,000 OZ OR 2.177 TONNES AND FRIDAY APRIL 4: 250 CONTRACT ISSUANCE FOR .777 TONNES + MONDAY APRIL 7 NEW ISSUANCE OF .8709 TONNES/ + APRIL 9 ‘S TOTAL OF 484 EX. FOR RISK FOR 48,400 OZ OR 1.5054 TONNES/NEW TOTAL; EX FOR RISK 5.3304 TONNES TO WHICH WAS ADDED TO OUR NEW RECORD QUEUE JUMP OF 1981 CONTRACTS OR 198,100 OZ (6.1619 TONNES). THUS INITIAL STANDING FOR GOLD/APRIL DELIVERY MONTH IS 192.419 TONNES NORMAL DELIVERY(INCLUDES OF QUEUE JUMP) + 5.3304 TONNES EX FOR RISK = 197.749 TONNES

/NEW STANDING FOR APRIL; 192.419 TONNES + 5.3304 TONNES EX FOR RISK = 197.749 TONNES

/ ALL OF THIS HAPPENED WITH OUR HUMONGOUS $100.00 GAIN IN PRICE WITH RESPECT TO THURSDAY’S COMEX ///. WE HAD ONLY A VERY STRONG SIZED GAIN OF 14,771 OI CONTRACTS (45.94 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AND NOW FOR OUR FRONT MONTH OF APRIL. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS. WE HAVE A MASSIVE AMOUNT OF TONNES STANDING FOR GOLD IN APRIL.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 4354 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 476,747

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 14,771 CONTRACTS WITH 10,417 CONTRACTS INCREASED AT THE COMEX// AND A VERY STRONG SIZED 4354 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 14,771 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED AND CRIMINAL 3071 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A VERY STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4354 CONTRACTS) ACCOMPANYING THE VERY STRONG SIZED INCREASE IN COMEX OI OF 10,417 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 14,771 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING AT THE GOLD COMEX FOR APRIL 192.419 TONNES (WHICH INCLUDES OUR HUGE 6.16 TONNES QUEUE JUMP) AND THIS FOLLOWS TOTAL EXCHANGE FOR RISK ISSUANCE ON 4 OCCASIONS FOR 5.3304 TONNES//NEW STANDING ADVANCES TO 197.749 TONNES.

//NEW STANDING APRIL: 192.419 TONNES + 5.3304 TONNES EX FOR RISK ON 4 OCCASIONS = 197.749 TONNES

.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION + ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WE HAD: 1) $100.00 COMEX PRICE GAIN AND WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A VERY STRONG 14,771 CONTRACT GAIN ON OUR TWO EXCHANGES ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN APRIL.

4) MEGA HUMONGOUS SIZED COMEX OI GAIN// 5) VERY STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (4354 OI GAIN)///STRONG T.A.S. ISSUANCE: 3071 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 35,878 CONTRACTS OR 3,587,800 OZ OR 111.59 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 3986 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 111.59 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 111.59 TONNES DIVIDED BY 3550 x 100% TONNES = 3.14% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 111.59 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A GOOD SIZED 512 CONTRACTS OI TO 150,608 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 800 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 800 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 800 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 512 CONTRACTS AND ADD TO THE 800 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 288 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 1.44 MILLION OZ

OCCURRED WITH OUR $0.18 IN PRICE GAIN

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

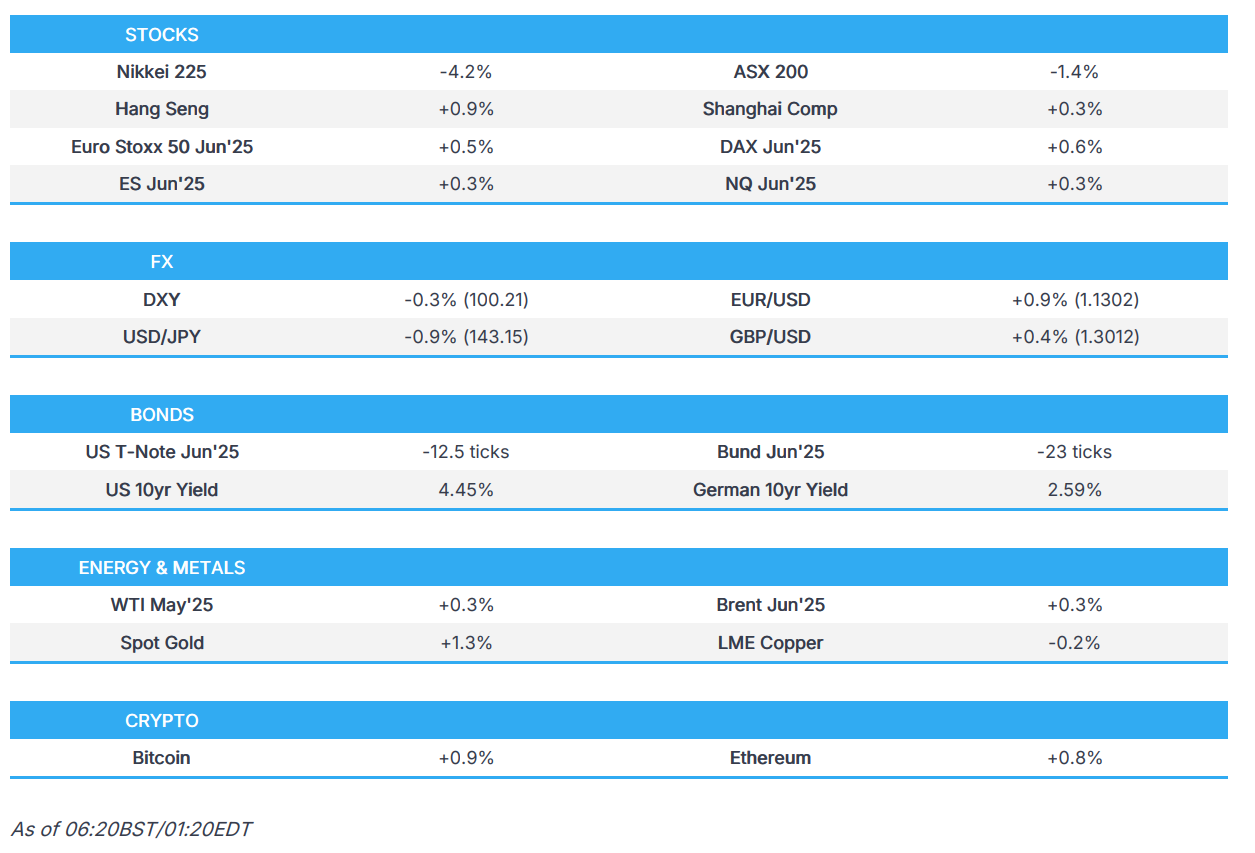

2.ASIAN AFFAIRS FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 14.59 PTS OR 0.45%

//Hang Seng CLOSED UP 232.91 PTS OR 1,13 PTS

// Nikkei CLOSED DOWN 1023.42 OR 2.96%//Australia’s all ordinaries CLOSED DOWN 0.76%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2994 CHINESE YUAN OFFSHORE CLOSED UP TO 7.3050/ Oil DOWN TO 59.93 dollars per barrel for WTI and BRENT DOWN TO 63.47 Stocks in Europe OPENED ALL MOSTLY ALL RED.

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

END

ASIA TRADING FRIDAY MORNING/THURSDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 10,417 CONTRACTS TO 459,504 WITH OUR HUMONGOUS GAIN IN PRICE OF $100.00 WITH RESPECT TO THURSDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT HUGE PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4354 ).

THE CME ANNOUNCED THURSDAY NIGHT, 0 EXCHANGE FOR RISK CONTRACTS FOR 0 OZ OR 0 TONNES. SO FAR THIS MONTH WE HAD RECORDED 4 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTALEXCHANGE FOR RISK FOR THE FRONT MONTH OF APRIL STANDS AT 5.3304 TONNES OF GOLD WHICH MUST BE ADDED TO OUR NORMAL GOLD DELVERIES.

HISTORY: LAST TWO PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.

DETAILS ON APRIL COMEX MONTH

IN TOTAL WE HAD A MEGA HUMONGOUS SIZED GAIN ON OUR TWO EXCHANGES OF 32,014 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF APRIL CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY TODAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION// THROUGHOUT THE WEEK.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 186 + TONNES.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 217 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1.2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING. IT IS SURELY ON DISPLAY TODAY AND DURING THIS MONTH OF APRIL.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF APRIL .… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4354 EFP CONTRACTS WERE ISSUED: : /APRIL 4354 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4354 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 14,771 CONTRACTS IN THAT 4354 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GAIN OF A HUGE 10,,417 COMEX CONTRACTS..AND THIS HUGE GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GIGANTIC GAIN IN PRICE OF $100.00 FOR THURSDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. SEEMS THAT EVERYBODY PILED INTO THE COMEX AS THE GOLD PRICE WAS RISING EXPONENTIALLY.

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A VERY STRONG SIZED 3071 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S THESE PAST FEW MONTHS,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED NOTHING AS NOBODY LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND ,FOR MARCH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT WEDNESDAY MARCH 17, THE 38,393 T.A.S. CONTRACT ISSUANCE WAS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH AND APRIL.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH. WE HAVE YET TO EXPERIENCE A MEGA CONSECUTIVE 30,000 CONTRACT T.A.S FOR APRIL.

STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (197.749 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 4 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

STANDING FOR GOLD: 192,419 TONNES + 5.3304 TONNES EX FOR RISK = 197.749 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 51 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 197.749 TONNES (INCLUDES 5.3304 TONNES EX FOR RISK)

COMEX GOLD TRADING/APRIL CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $100.00/ /)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A VERY STRONG SIZED GAIN IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD LITTLE T.A.S. SPREADER LIQUIDATION THURSDAY AS THEY WERE TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,200 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING AS THEY FAILED MISERABLY IN THEIR ATTEMPT TO HOLD THE $3,200 DOLLAR BARRIER AS IT IS NOW TRADING AT 3243.

THURSDAY NIGHT/FRIDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH MARCH/APRIL TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY:

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN A FEW NIGHTS AGO,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK:

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

NOW APRIL, ISSUES ITS 4TH EXCHANGE FOR RISK: 484 CONTRACTS OR 48,400 OZ OR 1.5054 TONNES

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES AND NOW 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES//NEW TOTAL ISSUANCE FOR APRIL: 5.3304 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WILL BE ADDED TO OUR NORMAL DELIVERY CYCLE.

STANDING NOW FOR APRIL:

APRIL: 192.419 TONNES +(5.3304 EX FOR RISK// FOR APRIL DELIVERY MONTH =197.749 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS APRIL DELIVERY MONTH AFTER FIRST DAY NOTICE;

WE HAVE GAINED A STRONG SIZED TOTAL OF 45.94 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL FIRST RECORDED AT 166.964 TONNES ON FIRST DAY NOTICE FOLLOWED BY 4 CONSECUTIVE EXCHANGE FOR RISK CONTRACT ISSUANCES FOR 5.3304 TONNES.

ALSO TODAY WE RECORD ANOTHER HUGE 1981 CONTRACT QUEUE JUMP FOR 198,100 OZ OR 6.1619 TONNES. WE MUST NOW ADD OUR 5.3304 TONNES EXCHANGE FOR RISK TO OUR NEW NORMAL DELIVERY OF 192.419 TONNES AND THUS STANDING FOR GOLD FOR APRIL IS NOW 197.749 TONNES, THE 2ND HIGHEST EVER RECORDED!

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $100.00, THE HIGHEST NOMINAL GAIN IN COMEX HISTORY.

WE HAD A MONSTROUS 17,243 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 14,771 CONTRACTS OR 1,477,100 0Z (45.94 TONNES)

SEEMS THAT THE RATS ARE LEAVING THE DERIVATIVE SHIP!!

confirmed volume THURSDAY 259,651.. contracts: GOOD///

//speculators have left the gold arena

END

APRIL

// THE APRIL 2025 GOLD CONTRACT

APRIL11

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2 ENTRIES: i) Out of jpm enhanced: 152,532.225 oz or 381 London good delivery bars/400 oz each ii) Out of Int. Delaware 64,302.000 oz (2000 kilobars) total weight 216,834.225 OZ (6,744.44 OZ) 6.744 TONNES . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | we have 1 customer entries TOTAL CUSTOMER DEPOSITS: 1 ENTRY i) Into Brinks enhanced; 42,778.100 oz 106 London good delivery bars of 400 oz each total weight deposit 42,778.100 oz or 1.33 tonnes total weight of customer and dealer; 1.33 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1121 notice(s) 112100 OZ 3.486 TONNES |

| No of oz to be served (notices) | 1141 contracts 114,100 OZ 3.548 TONNES |

| Total monthly oz gold served (contracts) so far this month | 60,722 notices 6,072,200 oz 188.871 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

we have 0 customer entries

TOTAL CUSTOMER DEPOSITS: 0 ENTRY

TOTAL CUSTOMER AND DELIVERY WEIGHT ENTRY ZERO TONNES

xxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 2//customer account

2 ENTRIES:

i) Out of jpm enhanced: 152,532.225 oz

or 381 London good delivery bars/400 oz each

ii) Out of Int. Delaware 64,302.000 oz (2000 kilobars)

total weight 216,834.225 OZ (6,744.44 OZ)

6.744 TONNES

adjustments: 4 all dealer to customer

a) Ashai: 407,995.296oz

ii) Brinks 87,968.362 oz

iii) JPMorgan 15,432.480 oz

iv) Manfra 10,906.022 oz

total weight adjusted a whopping 16.24 tonnes tonnes

(522,302.16 oz)

xxxxxxxxxxxxxxxxxx

AMOUNT OF GOLD STANDING FOR APRIL

THE FRONT MONTH OF APRIL HAD A GAIN OF 362 CONTRACTS TO STAND AT 2262. WE HAD 1619 CONTRACTS FILED THURSDAY. THUS WE GAINED A HUMONGOUS 1981 CONTRACTS OR 198,100 OZ (6.1619TONNES) AS WE EXPERIENCED ANOTHER MASSIVE QUEUE JUMP WHERE THESE BOYS DESIRED TO TAKE PHYSICAL DELIVERY OVER HERE. THIS IS CENTRAL BANKERS STANDING FOR PHYSICAL GOLD. THIS QUEUE JUMP OF 6.1619 TONNES REPRESENTED THE HIGHEST EVER QUEUE JUMP IN COMEX HISTORY SURPASSING THE PREVIOUS HIGHEST RECORDED YESTERDAY AT 5.90 TONNES. TODAY REPRESENTS THE FIRST EVER 4 IN A ROW OF MASSIVE 5 + TONNES OF QUEUE JUMPING IN COMEX HISTORY!!

MAY GAINED 292 CONTRACTS UP TO 5128 CONTRACTS

JUNE GAINED 6086 CONTRACTS TO 351,390. JUNE WILL STILL BE A WHOPPER OF A DELIVERY MONTH

We had 1121 contracts filed for today representing 112,100 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1121 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 29 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL /2025. contract month, we take the total number of notices filed so far for the month (60,722 X 100 oz ) to which we add the difference between the open interest for the front month of APRIL (2262 CONTRACTS) minus the number of notices served upon today (1121 x 100 oz per contract) equals 6,186,300 OZ OR 192.419 TONNES

to which we add our 4 exchange for risk issuances for April of 5.3304 tonnes

= 197.749 tonnes

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (60,722 x 100 oz +we add the difference for front month of APRIL (2262 OI} minus the number of notices served upon today (1121 x 100 oz) which equals 6,186,300 OZ OR 192.419 TONNES + 5.3304 tonnes ex for risks = 197.742 tonnes

TOTAL COMEX GOLD STANDING FOR APRIL.: 197.743 TONNES WHICH IS HUGE FOR THIS ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL IS FOLLOWING SUIT..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,055,639.792 oz 63.93 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 44,575,964.165 oz

TOTAL REGISTERED GOLD 22,310,273.870 or 693.94 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 22,265,,690.295 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 20,254,634oz (REG GOLD- PLEDGED GOLD)= 630.00tonnes //

END

SILVER/COMEX

// THE APRIL 2025 SILVER CONTRACT//INITIAL

APRIL 11

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | withdrawals 2 2 entries: i) Loomis: 537,432.500 oz ii) Delaware 57,318.414 oz total withdrawal 594,750.904 oz |

| Deposits to the Dealer Inventory | |

| Deposits to the Customer Inventory | deposits customer side 2 entries i) Into CNT customer 1,199,143.2709 oz ii) Into Loomis 634,944.000 total weight 1,834,087.270 oz |

| No of oz served today (contracts) | 190 CONTRACT(S) (0.950 MILLION OZ |

| No of oz to be served (notices) | 309 contracts (1.545 MILLION oz) |

| Total monthly oz silver served (contracts) | 2710 Contracts (13.55million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

0 entries/dealer

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

2 entries

i) Into CNT customer 1,199,143.2709 oz

ii) Into Loomis 634,944.000

total weight 1,834,087.270 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 entries//customer withdrawals

withdrawals 2

2 entries:

i) Loomis: 537,432.500 oz

ii) Delaware 57,318.414 oz

total withdrawal 594,750.904 oz

total withdrawals 594,750.914 oz

ADJUSTMENTs 1 entries//

dealer to customer CNT

41,275.45 oz

JPMorgan has a total silver weight: 199.954million oz/497.475oz million or 40.27%

TOTAL REGISTERED SILVER: 159.602 MILLION OZ//.TOTAL REG + ELIGIBLE. 497.465Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2025 OI: 310 OPEN INTEREST CONTRACTS FOR A LOSS OF 95 CONTRACTS. WE HAD 96 NOTICES FILED THURSDAY SO WE GAINED 1 CONTRACTS WHICH UNDERWENT A SMALL QUEUE JUMP OF 5,000 OZ AS THESE BOYS WERE WILLING TO WAIT FOR DELIVERY OF SILVER OVER ON THIS SIDE OF THE POND.

MAY SAW A GAIN OF 4662 CONTRACTS DOWN TO 75.429 CONTRACTS.

JUNE SAW A LOSS OF 56 CONTRACTS DOWN TO 1413 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 190 or 0.950 MILLION oz

CONFIRMED volume; ON THURSDAY 103,519 mega huge//

AND NOW APRIL DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 2710 X5,000 oz = 13.55 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (310) AND the number of notices served upon today (190 )x (5000 oz)

Thus the standings for silver for the APRIL 2025 contract month: (2710) Notices served so far) x 5000 oz + OI for the front month of APRIL(310) minus number of notices served upon today (190)x 5000 oz equals silver standing for the APRIL contract month equating to 14.150 MILLION OZ . WE MUST NOW ADD OUR 4.0 MILLION OZ EXCHANGE FOR RISK ISSUED ON MONDAY MARCH 31 AND TODY APRIL 4/NEW STANDING INCREASES TO 18.150 MILLION OZ

New total standing: 18.150 million oz which is huge for this NON active delivery month of APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 159.602million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

MARCH 21 WITH GOLD DOWN $20.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 910.43 TONNES

MARCH 20 WITH GOLD UP $3.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 909.28 TONNES

MARCH 19 WITH GOLD UP $0.45 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 907.27 TONNES

MARCH 18 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 907.27 TONNE

MARCH 17 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.64 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 906.41 TONNES

MARCH 14 WITH GOLD UP $9.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MONSTER DEPOSIT OF 7.17 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 905.81 TONNES

MARCH 13 WITH GOLD UP $42.85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 12 WITH GOLD UP $22.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.90 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 895.20 TONNES

MARCH 11 WITH GOLD UP $21.20 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 891.30 TONNES

MARCH 10 WITH GOLD DOWN $12.45 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 894.317 TONNES

MARCH 7 WITH GOLD DOWN $12.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 6 WITH GOLD UP $2.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 900.30 TONNES

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

GLD INVENTORY: 937.09 TONNES, TONIGHTS TOTAL

SILVER

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

MARCH 21 WITH SILVER DOWN $0.45 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 442.962 MILLION

MARCH 20 WITH SILVER DOWN $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 19 WITH SILVER DOWN $0.45 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.219 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 18 WITH SILVER UP $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.823 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.373 MILLION

MARCH 17 WITH SILVER UP $0.03 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.096 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 439.550 MILLION

MARCH 14 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.910 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.454 MILLION

MARCH 13 WITH SILVER UP $0.46 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.774 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 434.544 MILLION

MARCH 12 WITH SILVER UP $0.57 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.032 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 435.318 MILLION

MARCH 11 WITH SILVER UP $0.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.816 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 436.410 MILLION

MARCH 10 WITH SILVER DOWN 25 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.276 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.591 MILLION

MARCH 7 WITH SILVER DOWN 40 CENTS/HUGL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.184 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 434.317 MILLION

MARCH 6 WITH SILVER UP 16 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.455 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.046 MILLION

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

CLOSING INVENTORY 449.71 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2, EGON VON GREYERZ

ALASDAIR MACLEOD

Donald’s $ ducks

Measured in gold, the dollar’s decline is accelerating as foreigners bail out and gold is the go-to refuge. It is a panic on a global scale that looks like it is only just starting.

| Alasdair MacleodApr 11∙Paid |

Donald’s $ ducks

After last week’s dramatic selloff, gold and silver rallied this week, spectacularly in the case of gold. In early morning European trade today, gold was $3,219, up $180 from last Friday’s close — a new record level. Silver was $31.36, up $1.78. But since last week’s dramatic selloff, silver has been left way behind gold, reflected in our headline chart.

So what’s driving these two metals?

Part of the reason for this disparity is that Comex dealers have a better understanding of industrial demand factors than of money. This has led them into the wrong contract, which is illustrated in the chart below of price and open interests.

Open interest in gold recently collapsed from 574,824 to 449,087 contracts on Wednesday or 125,737 contracts (equivalent of 391 tonnes) taking it toward oversold territory, while on balance the price barely moved. In silver, the decline in open interest was more modest, while the price fell heavily. Previously, open interest and the price had been moving together in normal bullish fashion, suggesting the price was more vulnerable to unexpected shocks.

When silver is valued as an industrial metal, its price corelates with copper. Both metals initially soared on tariff fears, then fell back heavily when markets became scared of the recessionary consequences. Gold, however, reflects fears for the dollar and has caught paper markets on the hop.

Other than the gold price itself, the best illustration of the dollar’s plight is its trade weighted index:

Ouch! This is a collapse against other currencies that are hardly paragons of virtue themselves. Not only is this a classic dollar bear market, but the momentum to the downside is consistent with becoming self-feeding.

What gold and the TWI chart are telling us is that taking everything into account markets now expect the dollar to lose purchasing power at an alarming rate. Consequently, we can kiss goodbye any prospect for interest rate cuts and lower bond yields. Instead, they will have to rise in the coming months, which is bound to be a nasty systemic shock.

Let that sink in for a moment.

We can now sense the future direction of bond yields, and our next chart is of the 10-year UST note confirming worst fears:

It is being sensed already, but when the pecked line is broken all dollar credit values will slide. Equity and bond values are bound to fall heavily, and foreign holders of some $32 trillion of onshore dollar assets including $14 trillion of equities will flee from not only the assets, but the dollar as well.

The question then arises as to the consequences for other currencies, which are likely to be damaged by the lethal combination of higher US bond yields, their own debt traps, and severe equity bear markets.

This is painting a very dark picture, but it is getting difficult to see how this deterioration in US and global credit values can be avoided. For now, it is only a matter of Trump’s administration undermining the dollar’s credibility. We need to monitor how market opinions elsewhere reflect these fears.

Finally, a few words on silver. While investors have been badly whipsawed in the last two weeks, it has left silver grossly undervalued. We can cite the gold-silver ratio at 103, which is an aberration. And the chart looks good as well:

All that has happened is that the price has successfully back-tested the breakout level of the previous four-year consolidation. Rising moving averages in correct sequence tell us that the bull is intact. Silver should now be ready to break the $35 level and move on rapidly higher. Losing faith is not a sensible option in what is still a monetary metal.

3. C Powell and Gata dispatches

4. ANDREW MAGUIRE PODCAST

LIVE FROM THE VAULT/ANDREW MAGUIRE WITH ALASDAIR MACLEOD

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//ROLEX

END

6 CRYPTOCURRENCY NEWS

ASIA TRADING FRIDAY MORNING THURSDAY NIGHT

SHANGHAI CLOSED UP 14.59 PTS OR 0.45%

//Hang Seng CLOSED UP 232.91 PTS OR 1,13 PTS

// Nikkei CLOSED DOWN 1023.42 OR 2.96%//Australia’s all ordinaries CLOSED DOWN 0.76%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2994 CHINESE YUAN OFFSHORE CLOSED UP TO 7.3050/ Oil DOWN TO 59.93 dollars per barrel for WTI and BRENT DOWN TO 63.47 Stocks in Europe OPENED ALL MOSTLY ALL RED.

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2994

OFFSHORE YUAN: UP TO 7.3050

SHANGHAI CLOSED CLOSED UP 14.59 PTS OR 0.45%

HANG SENG CLOSED CLOSED UP 232.91 OR 1.13%

2. Nikkei closed DOWN 1023.42 PTS OR 2.96%

3. Europe stocks SO FAR: MOSTLY ALL RED

USA dollar INDEX DOWN TO 99.53// EURO RISES TO 1.1342 UP 84 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: FALLS TO. +1.288//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.72…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

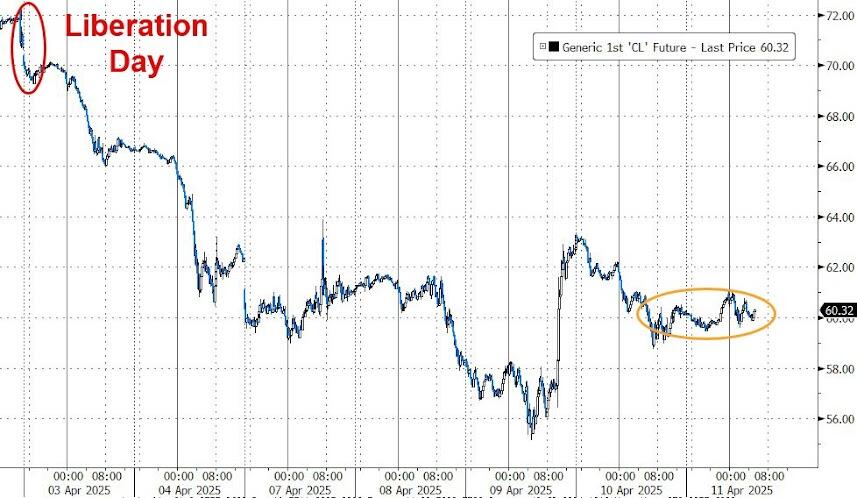

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5235/Italian 10 Yr bond yield DOWN to 3.794 SPAIN 10 YR BOND YIELD DOWN TO 3.280

3i Greek 10 year bond yield DOWN TO 3.495

3j Gold at $3235.00 Silver at: 31.62 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 13 /100 roubles/dollar; ROUBLE AT 83.36

3m oil into the 59 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.72// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.288% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8160 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9255 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.434 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.866 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.835 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.06

10 YR UK BOND YIELD: 4.7405 UP 5 PTS

10 YR CANADA BOND YIELD: 3.237 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.821 DOWN 2 PTS.

2a New York OPENING REPORT

Futures Flat, Gold Soars, Dollar Crashes After China Hikes US Tariffs To 125%

by Tyler Durden

Friday, Apr 11, 2025 – 09:21 AM

Things are moving so fast it’s becoming pointless to do static market wraps like this one, but may as well try even if it will be completely irrelevant the minute we publish this.

US equity futures are slightly higher, having reversed steep overnight losses. What is remarkable however is that even after China announced a decision to raise tariffs on all US goods from 84% to 125%, stocks initially dippped by have since recovered. As of 8:40am, S&P futures are up 0.6% helped by solid earnings from JPM and Morgan Stanley, while Nasdaq futures gained 0.8%, lifted by solid Mag7 performance.

More importantly, the dollar (DXY index) plunged below 100 for the first time since 2023 on concerns its status as the world’s reserve currency is being eroded as the US-China trade war intensifies (spoiler alert: it’s not, because very soon we are about to see China, Japan and Europe unleashing a monetary bazooka to preserve their export industries (i.e. economy) pushing the euro topped to a 3 year high much to the horror of Europe’s exporters while the yen also exploded higher, sending the country’s exporting industries in a crisis.

And amid this fiat carnage, gold soared to a fresh record high and even bitcoin is starting to catch a bid as algos slowly but surely realize that if the dollar is no longer the world’s reserve currency, and every other fiat currency is worse than the dollar, then… yeah.

In premarket trading, Mag 7 stocks were mixed after China’s decision to raise tariffs on all US goods from 84% to 125%.

Tesla -0.3%, Amazon +0.2%, Meta +0.7%, Apple +0.06%, Alphabet +0.6%, Microsoft +0.3%, Nvidia +1%). Shares in companies working on biotech AI models gain after the FDA said it plans to phase out animal testing requirements for monoclonal antibodies and other drugs (Recursion Pharmaceuticals +14%, Absci +15%, Certara +20%, Schrodinger +14%, Nuvation Bio +2.9%). US-listed Chinese stocks are holding onto their gains after the latest escalation in trade tensions that saw China raising levies on US goods to 125%, but saying it won’t match further US tariff hikes (Alibaba + 2.2%, Baidu 3.6% +4.1%, NetEase +2.1%). Here are some other notable premarket movers:

- American Express (AXP) climbs 2.6% as BofA turns bullish, seeing the credit card provider as recession resilient.

- Cinemark Holdings (CNK) rises 3% as JPMorgan upgrades to overweight, saying the cinema company is one of the least economically exposed firms in the current volatile environment.

- EQT (EQT US) shares slip 1.6%. The gas producer expects to report a total derivatives loss of $679 million for the three months ended March 31, according to a statement.

- JPMorgan (JPM) rises 1% as the bank’s stock traders took in a record haul in the first quarter but its FICC and iBanking revenues missed.

- Morgan Stanley (MS) rises 3% as 1Q net revenue tops estimates.

- Stellantis (STLA) shares fall 2.8% after the carmaker said shipments dropped 9% in the latest three month period.

- Verve Therapeutics (VERV) gains 6.6% after saying that the FDA granted fast track designation for VERVE-102.

- Wells Fargo (WFC) gains 1.7% after posting quarterly results.

As Bloomberg notes, in a week that’s seen the biggest swings in decades erupt across stock and bond markets, currency moves took the spotlight on Friday. In the latest tit-for-tat move, China announced it would raise tariffs on all US goods from 84% to 125% and warned that it plans to “resolutely counterattack and fight to the end” if the US continues to infringe on its rights and interests. The Ministry of Finance also called the Trump administration’s actions a “joke” and said it no longer considers them worth matching.

“The question of a potential dollar confidence crisis has now been definitively answered – we are experiencing one in full force,” ING Bank NV strategists including Francesco Pesole wrote in a note. “The dollar collapse is working as a barometer of ‘sell America’ at the moment.”

JPM shares rose as much as 4% in US premarket trading before fading all gains, after the bank boosted loan-loss provisions and bolstered its reserves. Rival Morgan Stanley also climbed after reporting soaring trading revenue amid market volatility.

“The economy is facing considerable turbulence,” JPMorgan CEO Jamie Dimon said in commentary accompanying the results. “Clients have become more cautious amid an increase in market volatility driven by geopolitical and trade-related tensions.”

BlackRock Inc. reported lower-than-expected net inflows in the quarter with CEO Larry Fink likening current conditions to the “structural shifts” seen during the global financial crisis and the Covid pandemic. “Uncertainty and anxiety about the future of markets and the economy are dominating client conversations,” Fink said in a statement.

Earlier, Bank of America’s Michael Hartnett said President Donald Trump’s tariffs and the resulting market turmoil were turning US exceptionalism into “US repudiation.” He advised investors sell any rallies until the Federal Reserve steps in and the US and China de-escalate, recommending a short position on stocks — until the S&P 500 hits 4,800 points — and a long bet on two-year Treasuries. Higher bond yields, lower stocks and a weaker dollar are “driving global asset liquidation, will likely force policymakers to act,” Hartnett wrote in a note. But investors should “sell the rips in risk assets.”

A Citi index shows analysts are slashing estimates at a pace that is generally seen during growth shocks, such as the pandemic. Meanwhile, Bank of America data shows massive inflows to passive equity funds, while Treasuries had their biggest weekly inflow ever.

Meanwhile, Trump’s second term is now off to one of the worst starts for the stock market since the Herbert Hoover era in 1929, tying with George W. Bush. Other assets also faced more turbulence, with the dollar extending losses after its biggest plunge in three years, gold hitting a new high and oil prices on track for a second straight weekly decline.

In Europe, the Stoxx 600 is down 1.5% with industrial goods and travel and leisure stocks were the biggest laggards, while the utilities and food and beverage sectors performed better than the wider benchmark. Here are the biggest movers on Friday:

- Argenx shares gain as much as 4.3%, after the US Food and Drug Administration approved a new option for patients to self-inject Vyvgart Hytrulo with a prefilled syringe

- Schott Pharma shares jump as much as 13%, after the German healthcare supplier released preliminary figures for the second quarter that were ahead of market estimates