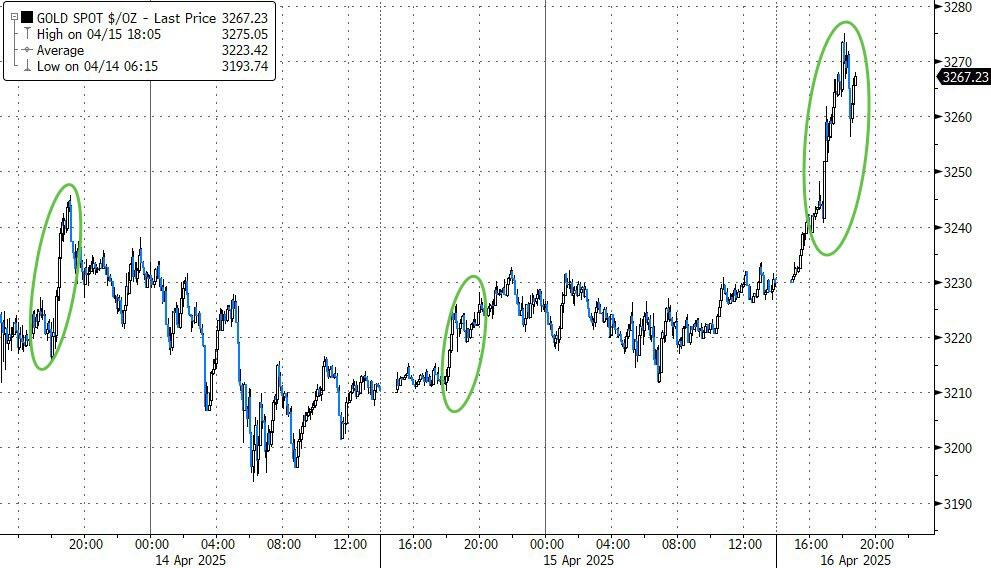

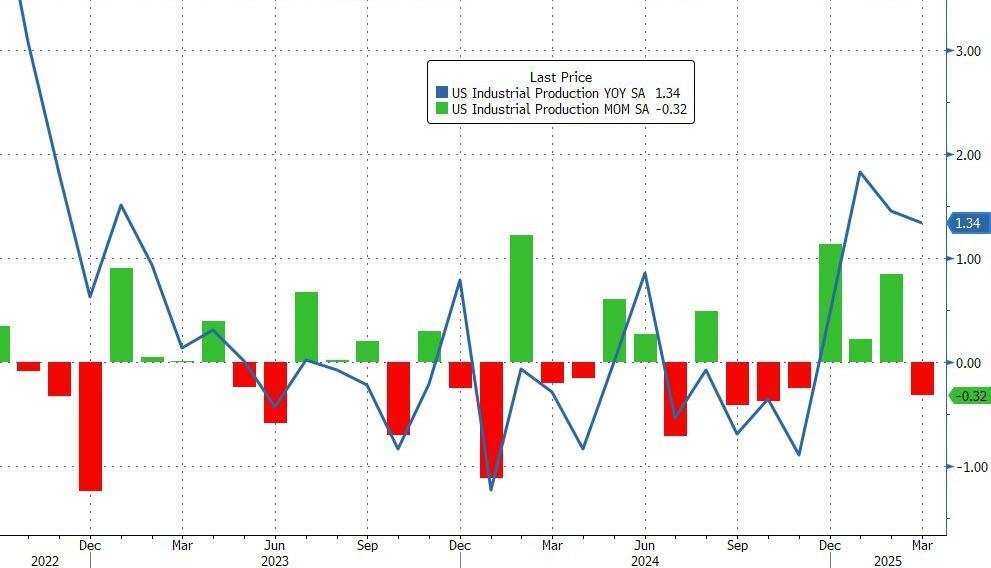

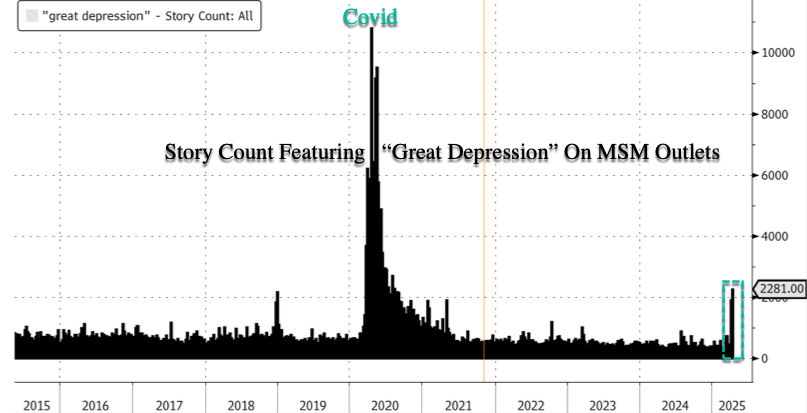

APRIL 16/GOLD FINISHES THE DAY UP BY A RECORD $106.35 TO $3330.15 WITH SILVER TRYING TO JOIN THE PARTY UP $0.70 TO $33.01//PLATINUM AND PALLADIUM ARE STILL CONTROLLED: PLATINUM IS UP $11.25 TO $973.70 WHILE PALLADIUM IS UP ONLY $1.55 TO $978.70//GOLD COMMENTARY TONIGHT FROM PETER SCHIFF//USA MARKETS THE DOW AND NASDAQ HAVE A MISERABLE DAY AS THE FIRST VICTIM OF THE BASIS TRADE APPEARS//CHINA IS STILL AT WAR WITH THE USA ON TARIFFS WITH THE CANADA BENDING THE KNEE AS CANADA WILL NOT TARIFF AUTOS COMING INTO OUR COUNTRY///EUROPE IS STILL IN A MESS AS THEY DO NOT KNOW HOW TO DEAL WITH TRUMP//ISRAEL VS HAMAS//SYRIAN UPDATES//JORDAN GOES TO WAR AGAINST INSURGENT MUSLIM BROTHERHOOD IN THEIR COUNTRY//COVID UPDATES/DR PAUL ALEXANDER/SLAY NEWS ETC//CANADA UPDATES: GOVERNOR OF B. OF CANADA KEEPS RATES UNCHANGED AND YET STATES THAT CANADA WILL HAVE A DEEP RECESSION//USA NEWS; RETAIL SALES SKYROCKET YET INDUSTRIAL PRODUCTION FALTERS//SWAMP STORIES FOR YOU TONIGHT//GREG HUNTER INTERVIEWS DR SHERRY TENPENNY AND IT IS MUST VIEW//

323 C HSBC 3 363 H WELLS FARGO SECURITI 35 686 C STONEX FINANCIAL INC 26 3 690 C ABN AMRO CLR USA LLC 10 2 737 C ADVANTAGE FUTURES 2 905 C ADM 5

TOTAL: 43 43 MONTH TO DATE: 61,463

MONTH TO DATE: 61,420

JPMORGAN STOPPED: 0/43

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 43 NOTICES FOR 4300 OZ 0.1337 TONNES

total notices so far: 61,463 contracts for 6,146,300 OR 191.175 tonnes)

FOR APRIL

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 54 NOTICE(S) FILED FOR 0.270 MILLION OZ/

total number of notices filed so far this month : 2897 CONTRACTS (NOTICES) for 14.485 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $106.35 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 953.15 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.70 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ////A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 452.243 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 845 CONTRACTS TO 144,400 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY GAIN OF $0.07 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. WE HAD A VERY STRONG SIZED LOSS OF 645 TOTAL CONTRACTS AS THE CME NOTIFIED US OF A FAIR 200 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD A CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING TUESDAY AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON TUESDAY WITH SILVER’S GAIN IN PRICE BUT THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH A HUGE T.A.S. ISSUANCE OF 719 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A FAIR 200 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 719 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN WEDNESDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A VERY STRONG SIZED 558 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR GAIN IN PRICE OF $0.07. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT TUESDAY’S COMEX TRADING SESSION. TODAY, THE CME NOTIFIED US THAT WE HAD 0 CONTRACTS OF THOSE CRAZY EXCHANGE FOR RISK CONTRACTS ISSUED FOR 0 OZ (0 MILLION OZ). THESE EXCHANGE FOR RISKS ARE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THUS FOR THE MONTH OF APRIL WE HAVE A TOTAL OF 4.0 MILLION OZ OF EXCHANGE FOR RISK ISSUED ON TWO OCCASIONS. THE RECIPIENT OF THIS LARGESS IS PROBABLY THE CENTRAL BANK OF INDIA.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT/WEDNESDAY MORNING: A HUGE 719 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.07) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A SMALL GAIN IN PRICE BUT WE LOST A VERY STRONG 558 CONTRACTS IN OPEN INTEREST FROM OUR TWO EXCHANGES. ALL OF THE LOSS WAS DUE TO T.A.S. LIQUIDATION, DISTORTING THE COMEX OI STANDING.

WE HAD A FAIR 200 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.735 MILLION OZ FOLLOWED BY TODAY’S 180,000 OZ QUEUE JUMP FOR PHYSICAL TRANSFER TO WHICH WE ADD OUR 4.00 MILLION OZ EX FOR RISK

STANDING FOR APRIL INCREASES TO 18.485 MILLION OZ

WE HAD:

/ HUGE COMEX OI LOSS+// A FAIR SIZED EFP ISSUANCE (200 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 719 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 491 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 12 DAYS, total 14,372 contracts: OR 71.860 MILLION OZ (119 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 71.860 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 71.860 MILLION OZ/// THIS IS HUGE AND THIS MONTH WILL PROBABLY BE A HUMDINGER OF ISSUANCE.

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 845 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.07 IN SILVER PRICING AT THE COMEX// TUESDAY.,. . THE CME NOTIFIED US THAT WE HAD A FAIR 200 CONTRACT EFP ISSUANCE CONTRACTS: 200 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A STRONG SILVER OZ STANDING FOR APRIL OF 14.495 MILLION OZ , PLUS OUR 4.00 MILLION EX FOR RISK

NEW STANDING APRIL: 18.495 MILLION OZ

THE NEW TAS ISSUANCE TUESDAY NIGHT (719 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TODAY.

WE HAD 54 NOTICE(S) FILED TODAY FOR 0.270 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2301 OI CONTRACTS TO 456,628 AND FURTHER FROM TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 946 CONTRACTS CONTRACTS//.

WE HAD A FAIR SIZED INCREASE IN COMEX OI (2301 CONTRACTS) . THIS OCCURRED WITH OUR GAIN OF $12.40 IN PRICE TUESDAY. LAST THURSDAY WAS ALSO THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT EXACLY $100.00 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES (CME CORRECTED// MAYBE?) TO WHICH WE ADD FOR APRIL ITS INITIAL 700 CONTRACT EXCHANGE FOR RISK FOR 70,000 OZ OR 2.177 TONNES AND FRIDAY APRIL 4: 250 CONTRACT ISSUANCE FOR .777 TONNES + MONDAY APRIL 7 NEW ISSUANCE OF .8709 TONNES/ + APRIL 9 ‘S TOTAL OF 484 EX. FOR RISK FOR 48,400 OZ OR 1.5054 TONNES/NEW TOTAL AND FINALLY APRIL 14 EX FOR RISK OF 30,000 OZ OR.6220 TONNES// ;NEW EX FOR RISK 5.912 TONNES TO WHICH WAS ADDED TO OUR NEW QUEUE JUMP OF 341 CONTRACTS OR 34,100 OZ (1.060 TONNES). THUS INITIAL STANDING FOR GOLD/APRIL DELIVERY MONTH IS 193.869 TONNES NORMAL DELIVERY(INCLUDES OF QUEUE JUMP) + 5.912 TONNES EX FOR RISK = 199.779 TONNES

/NEW STANDING FOR APRIL; 193.869 TONNES + 5.912 TONNES EX FOR RISK = 199.779 TONNES

/ ALL OF THIS HAPPENED WITH OUR $12.40 GAIN IN PRICE WITH RESPECT TO TUESDAY’S COMEX ///. WE HAD A STRONG SIZED GAIN OF 4901 OI CONTRACTS (15.24 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AND NOW FOR OUR FRONT MONTH OF APRIL. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS. WE HAVE A MASSIVE AMOUNT OF TONNES STANDING FOR GOLD IN APRIL.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 2600 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 457,574

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4901 CONTRACTS WITH 2301 CONTRACTS INCREASED AT THE COMEX// AND A VERY GOOD SIZED 2600 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4901 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 883 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A VERY GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2600 CONTRACTS) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 2301 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 4901 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING AT THE GOLD COMEX FOR APRIL 193.869 TONNES (WHICH INCLUDES OUR 1.060 TONNES QUEUE JUMP) AND THIS FOLLOWS TOTAL EXCHANGE FOR RISK ISSUANCE ON 5 OCCASIONS FOR 5.912 TONNES//NEW STANDING ADVANCES TO 199.779 TONNES.

//NEW STANDING APRIL: 193.869 TONNES + 5.912 TONNES EX FOR RISK ON 5 OCCASIONS = 199.779 TONNES

.

/ 3) TINY T.A.S. LIQUIDATION + ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WE HAD: 1) $12.40 COMEX PRICE GAIN AND WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG 5847 CONTRACT GAIN ON OUR TWO EXCHANGES ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN APRIL.

4) FAIR SIZED COMEX OI GAIN// 5) VERY GOOD SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (2600 CONTRACTS)///SMALL T.A.S. ISSUANCE: 883 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 44,895 CONTRACTS OR 4,489,500 OZ OR 139.64 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 3741 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN12 TRADING DAY(S) IN TONNES 139.64 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 139.64 TONNES DIVIDED BY 3550 x 100% TONNES = 3.93% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 139.64 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A STRONG SIZED 845 CONTRACTS OI TO 144,400 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 200 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 845 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A VERY STRONG SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 645 CONTRACTS DESPITE THE GAIN IN PRICE OF $0.07 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 3.225 MILLION PAPER OZ

OCCURRED WITH OUR $0.07 IN PRICE GAIN. ALL OF THE LOSS WAS DUE TO T.A.S. LIQUIDATION.

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED UP 8.34 PTS OR 0.20%

//Hang Seng CLOSED DOWN 409.29 PTS OR 1.91 PTS

// Nikkei CLOSED DOWN 347.14 OR 1.01%//Australia’s all ordinaries CLOSED DOWN 0.10%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.3082 CHINESE YUAN OFFSHORE CLOSED UP TO 7.3089/ Oil UP TO 61.89 dollars per barrel for WTI and BRENT UP TO 65.15 Stocks in Europe OPENED ALL RED.

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED2301 CONTRACTS TO 456,625 WITH OUR STRONG GAIN IN PRICE OF $12.40 WITH RESPECT TO TUESDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A GOOD NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2600 ).

THE CME ANNOUNCED TUESDAY NIGHT, 0 EXCHANGE FOR RISK CONTRACTS FOR 0 OZ OR 0.0 TONNES. SO FAR THIS MONTH WE HAD RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE FRONT MONTH OF APRIL STANDS AT 5.912 TONNES OF GOLD WHICH MUST BE ADDED TO OUR NORMAL GOLD DELVERIES.

HISTORY: LAST TWO PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.

DETAILS ON APRIL COMEX MONTH

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 4901 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF APRIL CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY FRIDAY INCLUDING WITH OUR STRONG T.A.S. ISSUANCES AND HUGE T.A.S. LIQUIDATION THROUGHOUT THE WEEK.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 198 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 217 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1.2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF APRIL .… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A GOOD SIZED 2600 EFP CONTRACTS WERE ISSUED: : /APRIL 2600 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2600 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 4901 CONTRACTS IN THAT 2600 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GAIN OF A FAIR 2301 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $12.40 FOR TUESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. LOOKS LIKE THE SHORT RATS ARE FLEEING THE ARENA!

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A SMALL SIZED 833 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S THESE PAST FEW MONTHS,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED NOTHING AS NOBODY LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND ,FOR MARCH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT WEDNESDAY MARCH 17, THE 38,393 T.A.S. CONTRACT ISSUANCE WAS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH AND APRIL.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH. WE HAVE YET TO EXPERIENCE A MEGA CONSECUTIVE 30,000 CONTRACT T.A.S FOR APRIL.

STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (199.779 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 4 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

STANDING FOR GOLD: 193.869 TONNES + 5.912 TONNES EX FOR RISK = 199.779 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 199.779 TONNES (INCLUDES 5.912 TONNES EX FOR RISK)

COMEX GOLD TRADING/APRIL CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $12.90/ /)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION TUESDAY AS THEY WERE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,200 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM ALSO RISING AS THEY FAILED MISERABLY IN THEIR ATTEMPT TO HOLD THE $3,200 DOLLAR BARRIER AS THEY ARE NOW TRYING TO PROTECT THE 3300 DOLLAR POSITION AS WE ARE TRADING AT $3294 AS I WRITE THIS AT 4: 44 AM. EUROPEANS BROKE THE BARRIER EARLIER AT 4:20 AM ONLY TO BE REPELLED BACK BELOW THE 3300 DOLLAR LEVEL. SINCE THEN IT CLIMBED ABOVE THE 3300 LEVEL AND IT WILL CLOSE SIGNIFICANTLY ABOVE THIS LINE IN THE SAND.

TUESDAY NIGHT/WEDNESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH MARCH/APRIL TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCE

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

NOW APRIL, ISSUES ITS 5TH EXCHANGE FOR RISK: 200 CONTRACTS OR 20,000 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK/APRIL

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES//NEW TOTAL ISSUANCE FOR APRIL: 5.912 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WILL BE ADDED TO OUR NORMAL DELIVERY CYCLE.

STANDING NOW FOR APRIL:

APRIL: 192.802 TONNES +(5.912 EX FOR RISK// FOR APRIL DELIVERY MONTH =198.714 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS APRIL DELIVERY MONTH AFTER FIRST DAY NOTICE;

WE HAVE GAINED A STRONG SIZED TOTAL OF 15.244 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL FIRST RECORDED AT 166.964 TONNES ON FIRST DAY NOTICE FOLLOWED BY 5 CONSECUTIVE EXCHANGE FOR RISK CONTRACT ISSUANCES FOR 5.912 TONNES.

ALSO TODAY WE RECORD ANOTHER 341 CONTRACT QUEUE JUMP FOR 34,100 OZ OR 1.060 TONNES. WE MUST NOW ADD OUR 5.912 TONNES EXCHANGE FOR RISK TO OUR NEW NORMAL DELIVERY OF 193.869 TONNES AND THUS STANDING FOR GOLD FOR APRIL IS NOW 199.779 TONNES, THE 2ND HIGHEST EVER RECORDED!

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $12.90,

WE HAD 946 CONTRACTS REM,OVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 4901 CONTRACTS OR 490,100 0Z (15.244 TONNES)

SEEMS THAT THE RATS ARE LEAVING THE DERIVATIVE SHIP AS FAST AS THEIR FEET CAN CARRY THEM!!!

i) Ashai: 57,407.932 oz ii) Brinks customer: 341,475.771 oz (10,621 kilobars)

total weight withdrawal: 398,883.703 oz or 12.406 tonnes

.

Deposit to the Dealer Inventory in oz

0 ENTRIES

Deposits to the Customer Inventory, in oz

we have 1 customer entry

i) Into Loomis customer account; 3999.940 oz

total deposit 3999.940 oz (.1244 tonnes)

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

43 notice(s) 4300 OZ 0.1337 TONNES

No of oz to be served (notices)

866 contracts 86,600 OZ 2.693 TONNES

Total monthly oz gold served (contracts) so far this month

61,463 notices 6,146,300 oz 191.175 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

TOTAL WEIGHT; 0 TONNES

xxxxxxxxxxxxxxxxxxxxx

we have 1 customer entries

we have 1 customer entry

i) Into Loomis customer account; 3999.940 oz

total deposit 3999.940 oz (.1244 tonnes)

xxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 2//customer account

2 ENTRIES: 2 withdrawals

i) Ashai: 57,407.932 oz

ii) Brinks customer: 341,475.771 oz (10,621 kilobars)

total weight withdrawal: 398,883.703 oz or 12.406 tonnes

adjustments: 1 dealer brinks to customer Brinks

375,587.982 oz (Brinks)

xxxxxxxxxxxxxxxxxx

AMOUNT OF GOLD STANDING FOR APRIL

THE FRONT MONTH OF APRIL HAD A LOSS OF 170 CONTRACTS TO STAND AT 909. WE HAD 511 CONTRACTS FILED TUESDAY. THUS WE GAINED A HUGE 341 CONTRACTS OR 34,100 OZ (1.060 TONNES) AS WE EXPERIENCED ANOTHER QUEUE JUMP WHERE THESE BOYS DESIRED TO TAKE PHYSICAL DELIVERY OVER HERE. THIS IS CENTRAL BANKERS STANDING FOR PHYSICAL GOLD. LAST FRIDAY’S QUEUE JUMP OF 6.1619 TONNES REPRESENTED THE HIGHEST EVER QUEUE JUMP IN COMEX HISTORY SURPASSING THE PREVIOUS HIGHEST RECORDED YESTERDAY AT 5.90 TONNES.

MAY GAINED 35 CONTRACTS UP TO 5240 CONTRACTS

JUNE GAINED 2211 CONTRACTS TO 348,201. JUNE WILL STILL BE A WHOPPER OF A DELIVERY MONTH

We had 43 contracts filed for today representing 4300 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 43 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL /2025. contract month, we take the total number of notices filed so far for the month (61,463 X 100 oz ) to which we add the difference between the open interest for the front month of APRIL (909 CONTRACTS) minus the number of notices served upon today (43 x 100 oz per contract) equals 6,232,900 OZ OR 193.869 TONNES

to which we add our 5 exchange for risk issuances for April of 5.910 tonnes

= 199.779 tonnes

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (61,463 x 100 oz +we add the difference for front month of APRIL (909 OI} minus the number of notices served upon today (43 x 100 oz) which equals 6,232,900 OZ OR 193.869 TONNES + 5.912 tonnes ex for risks = 199.779 tonnes

TOTAL COMEX GOLD STANDING FOR APRIL.: 199.779 TONNES WHICH IS HUGE FOR THIS ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL IS FOLLOWING SUIT..

JPMorgan has a total silver weight: 199.954million oz/498.568oz million or 40.27%

TOTAL REGISTERED SILVER: 160.344 MILLION OZ//.TOTAL REG + ELIGIBLE. 498.568Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2025 OI: 56 OPEN INTEREST CONTRACTS FOR A LOSS OF 74 CONTRACTS. WE HAD 110 NOTICES FILED ON TUESDAY SO WE GAINED 36 CONTRACTS WHICH UNDERWENT A STRONG QUEUE JUMP OF 180,000 OZ AS THESE BOYS WERE WILLING TO WAIT FOR DELIVERY OF SILVER OVER ON THIS SIDE OF THE POND.

MAY SAW A LOSS OF 2651 CONTRACTS DOWN TO 60,254 CONTRACTS. MAY BECOMES THE FRONT MONTH AND IT LOOKS LIKE WE WILL HAVE A DANDY AMOUNT OF SILVER STANDING THIS MONTH.

JUNE SAW A GAIN OF 1 CONTRACTS UP TO 1595 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 54 or 0.270 MILLION oz

CONFIRMED volume; ON TUESDAY 50,179 weak//

AND NOW APRIL DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 2897 X5,000 oz = 14.485 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (56) AND the number of notices served upon today (54 )x (5000 oz)

Thus the standings for silver for the APRIL 2025 contract month: (2897) Notices served so far) x 5000 oz + OI for the front month of APRIL(56) minus number of notices served upon today (54)x 5000 oz equals silver standing for the APRIL contract month equating to 14.485 MILLION OZ . WE MUST NOW ADD OUR 4.0 MILLION OZ EXCHANGE FOR RISK ISSUED ON MONDAY MARCH 31 AND TODAY APRIL 4/NEW STANDING INCREASES TO 18.495 MILLION OZ

New total standing: 18.495 million oz which is huge for this NON active delivery month of APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 159.954million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

0 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

MARCH 21 WITH GOLD DOWN $20.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 910.43 TONNES

MARCH 20 WITH GOLD UP $3.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 909.28 TONNES

MARCH 19 WITH GOLD UP $0.45 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 907.27 TONNES

MARCH 18 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 907.27 TONNE

MARCH 17 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.64 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 906.41 TONNES

MARCH 14 WITH GOLD UP $9.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MONSTER DEPOSIT OF 7.17 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 905.81 TONNES

MARCH 13 WITH GOLD UP $42.85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 12 WITH GOLD UP $22.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.90 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 895.20 TONNES

MARCH 11 WITH GOLD UP $21.20 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 891.30 TONNES

MARCH 10 WITH GOLD DOWN $12.45 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 894.317 TONNES

MARCH 7 WITH GOLD DOWN $12.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 6 WITH GOLD UP $2.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 900.30 TONNES

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

GLD INVENTORY: 953.15 TONNES, TONIGHTS TOTAL

SILVER

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

MARCH 21 WITH SILVER DOWN $0.45 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 442.962 MILLION

MARCH 20 WITH SILVER DOWN $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 19 WITH SILVER DOWN $0.45 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.219 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 18 WITH SILVER UP $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.823 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.373 MILLION

MARCH 17 WITH SILVER UP $0.03 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.096 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 439.550 MILLION

MARCH 14 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.910 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.454 MILLION

MARCH 13 WITH SILVER UP $0.46 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.774 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 434.544 MILLION

MARCH 12 WITH SILVER UP $0.57 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.032 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 435.318 MILLION

MARCH 11 WITH SILVER UP $0.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.816 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 436.410 MILLION

MARCH 10 WITH SILVER DOWN 25 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.276 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.591 MILLION

MARCH 7 WITH SILVER DOWN 40 CENTS/HUGL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.184 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 434.317 MILLION

MARCH 6 WITH SILVER UP 16 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.455 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.046 MILLION

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

CLOSING INVENTORY 442.243 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

The Dollar Bubble Just Burst: Peter Schiff Warns “This Is The Collapse I’ve Warned About For Years”

In an interview last week on Kitco News, Peter joined Jeremy Szafron to offer his latest insights into the unraveling U.S. economy, surging gold prices, and rapid inflationary pressures. Peter explains the Fed’s precarious position, the imminent threat of a U.S.-centric financial crisis, and why he thinks we’ve already entered serious economic decline, despite the government’s denials.

Well, I mean, this is something that I’ve been predicting for quite some time now. It was inevitable. I always thought it would be an external dollar crisis that would set these events in motion. I didn’t realize that we would do it to ourselves, but we have. We’ve pricked our own bubble and there’s a lot of air that’s going to come out of it. You know, Donald Trump looked at our huge trade deficits and just concluded that the trade deficits themselves were the problem and that they must be the result of foreigners cheating us and ripping us off.

As economic uncertainty has grown, gold prices have surged significantly. Peter emphasizes gold’s recent notable momentum, a rally that many investors overlooked due to their fixation with cryptocurrencies like Bitcoin:

Well, gold’s up over $250 in the last three days. So we’re accelerating. Two days, the last couple of days, we were $100 a day, and maybe we’ll be up again. Maybe we’ll be up another 100 by the time they close today’s trading. But what’s happening, and what I’ve been telling people was happening all last year as the price of gold went from 2000 to 3000 and nobody cared and nobody was buying it because everybody was sidetracked by Bitcoin and all the talk about digital gold.

Turning to the inflation outlook, Peter sharply criticizes the Fed’s claims that inflation expectations remain anchored at their so-called 2% target. He argues that the actual inflation outlook is far worse than the Fed admits and set to climb higher:

Yeah, well, the year ahead inflation expectations now are 6.7%. I mean, the Fed keeps saying that long-term expectations remain anchored at 2%. What are they talking about? Nothing is anchored at 2%. We’ve been adrift for a long time and now we’re at 6.7%. And you know what? It’s going to be a lot higher than that. The Fed is completely wrong.

Peter believes the Federal Reserve will eventually be forced to reverse rate hikes and resume quantitative easing (QE), but only after recognizing clear systemic deterioration. He foresees a painful and widespread economic contraction, particularly affecting employment within the service sector:

I think the Fed is eventually going to cut rates and go back to QE, but they’re waiting for everything to collapse. Because they don’t even know that it’s going to collapse. But they’re waiting for some signs that the financial system is buckled. Maybe they want to see big layoffs, which are coming. We’re going to have widespread layoffs in the United States because the whole service sector economy is going to shut down because all the imports are going to be cut off.

Finally, Peter cautions listeners that the U.S. economy is heading toward a severe crisis—one he considers far worse than the global financial crisis of 2008. Crucially, he points out that the brunt of the damage will impact America specifically, emphasizing the international shift away from reliance on the U.S. dollar and American markets:

Well, I think that there is going to be a massive loss of confidence because it’s been a confidence game the entire time. But look, this is going to be a financial crisis much worse than 2008, but it’s not going to be global. It is a U.S. crisis. It’s not a global crisis. It’s actually liberation for the rest of the world because they’re going to be liberated from the burden of supporting the U.S. economy. That means more for them.

On LFTV, Alasdair Macleod explains why China may be behind silver price suppression

Submitted by admin on Sat, 2025-04-12 22:42 Section: Daily Dispatches

10:43p ET Saturday, August 31, 2024

Dear Friend of GATA and Gold (and Silver):

Market analyst and economist Alasdair Macleod, this week’s guest with London metals trader Andrew Maguire on Kinesis Money’s “Live from the Vault” program, explains why he believes that China has been the instigator of silver price suppression and will terminate the scheme soon.

Macleod adds that markets and governments around the world are losing faith in the dollar and U.S. assets and that the only refuge is gold

Gold leasing by central banks, Macleod says, long has enabled multiple counting of world gold reserves, and the closing of those leases is reducing liquidity for paper gold and constricting the financial derivatives system.

The program is 57 minutes long and can be seen at YouTube here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

* * *

4. ANDREW MAGUIRE PODCAST

LIVE FROM THE VAULT/ANDREW MAGUIRE WITH ALASDAIR MACLEOD

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//ROLEX

END

6 CRYPTOCURRENCY NEWS

ASIA TRADING WEDNESDAY MORNING TUESDAY NIGHT

SHANGHAI CLOSED UP 8.34 PTS OR 0.20%

//Hang Seng CLOSED DOWN 409.29 PTS OR 1.91 PTS

// Nikkei CLOSED DOWN 347.14 OR 1.01%//Australia’s all ordinaries CLOSED DOWN 0.10%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.3082 CHINESE YUAN OFFSHORE CLOSED UP TO 7.3089/ Oil UP TO 61.89 dollars per barrel for WTI and BRENT UP TO 65.15 Stocks in Europe OPENED ALL RED.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.3082 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.3089 (CCP MANIPULATED)

SHANGHAI CLOSED CLOSED DOWN 8.34 PTS OR 0.20%

HANG SENG CLOSED CLOSED DOWN 409.29 OR 1.91%

2. Nikkei closed DOWN 347.14 PTS OR 1.01%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 99.38// EURO RISES TO 1.1358 UP 65 BASIS PT HEADING TO PARITY WITH USA

3b Japan 10 YR bond yield: FALLS TO. +1.282//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.84…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5200/Italian 10 Yr bond yield DOWN to 3.716 SPAIN 10 YR BOND YIELD DOWN TO 3.226

3i Greek 10 year bond yield DOWN TO 3.436

3j Gold at $3300.25 Silver at: 32.93 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 40 /100 roubles/dollar; ROUBLE AT 82.63

3m oil into the 61 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.84// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.282% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8176 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9287 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.310 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.797 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.822 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.13

10 YR UK BOND YIELD: 4.676 UP 3 PTS

10 YR CANADA BOND YIELD: 3.110 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.723 DOWN 2 PTS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

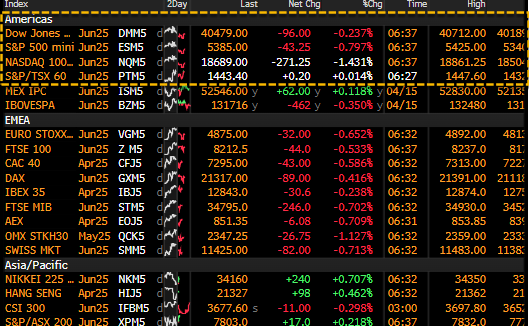

2a New York OPENING REPORT

Futures Slide After Nvidia Chip Export Curbs Slam Tech Stocks

Wednesday, Apr 16, 2025 – 08:34 AM

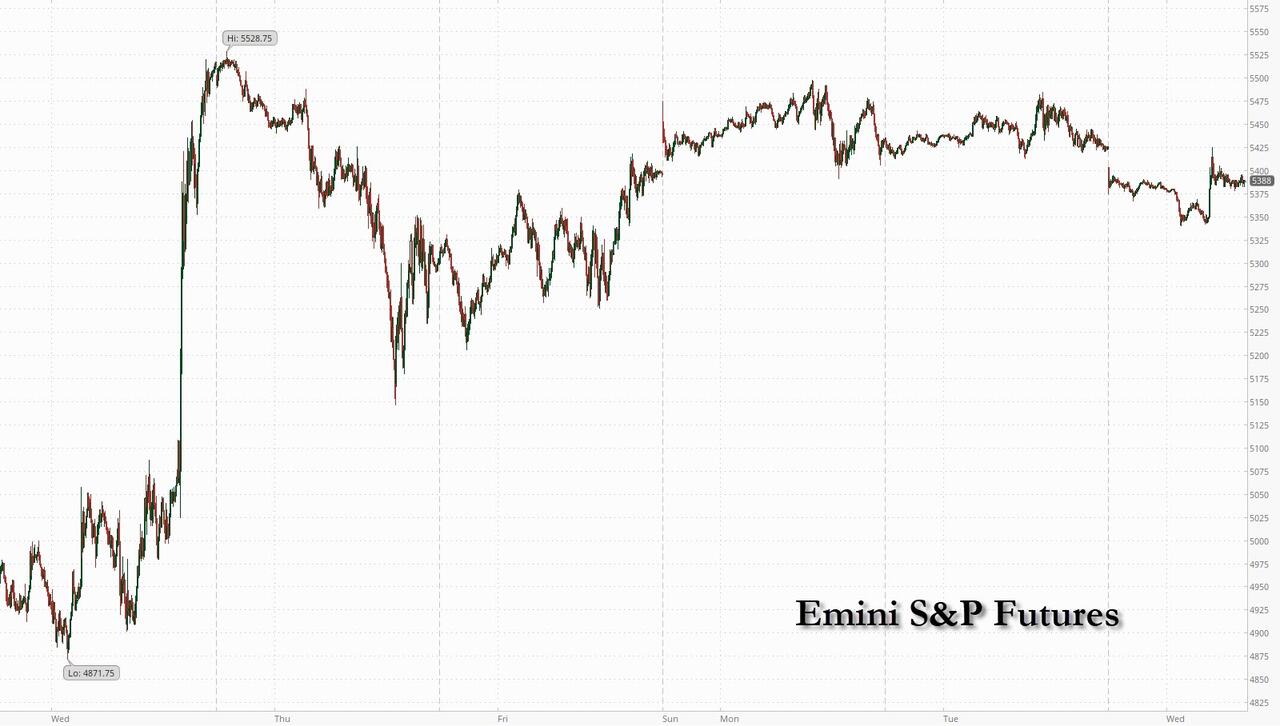

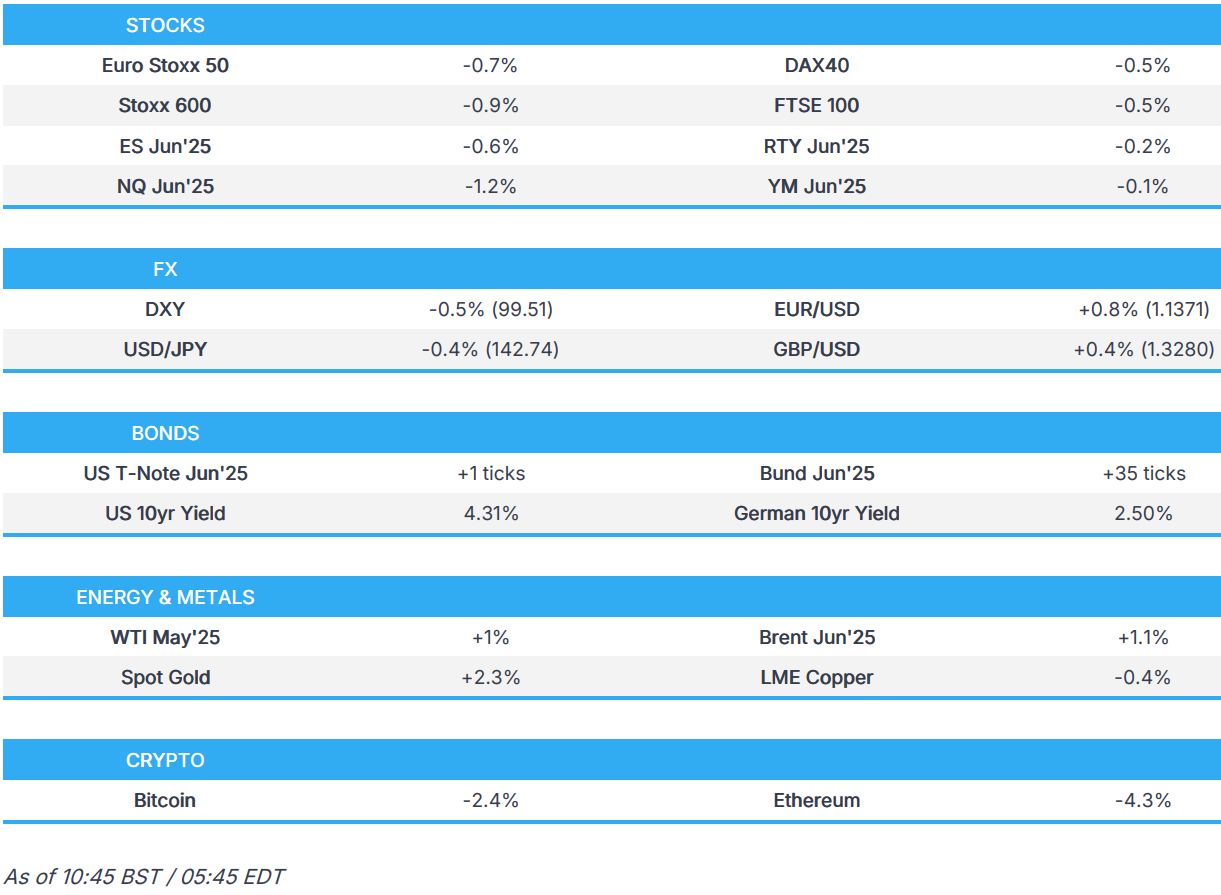

US equity futures are lower after NVDA unveiled the US government restricted export of its H2) chips to China, sending the stock -6% lower pre-market and dragging the broader market lower; Europe chip giant ASML Holding NV reported disappointing results further denting the semi space. As of 8:00am, S&P futures are down 0.7%, and Nasdaq futures slide 1.5%, with the balance of Mag7 and Semis, all weaker (AMD -6.2%, AVGO -3.3%). Futures had been even lower overnight but bounced shortly after 4am ET after China said to be open to trade talks with some preconditions, including (i) consistency of message and respectful approach; (ii) one person to negotiate that is not Trump but has his authority; with the goal of having a signable agreement before the leaders meet in person. Bond yields are mixed as the curve twists steeper while USD weakness continues, sending the Bloomberg dollar index to a 6 month low. Commodities are rallying today with all 3 complexes higher; WTI crude oil futures are up about 1%, gold futures more than 2%, extending their recent advance. Precious is standing out to the upside, with gold hitting a new record high above $3300. Today’s macro data focus is on Retail Sales.

In premarket trading, Nvidia was the biggest drag for Magnificent Seven stocks after Trump’s administration banned the chip giant from selling its H20 chip in China (Nvidia -6.3%, Tesla -2%, Meta 1.9%, Apple -0.8%, Amazon -1%, Alphabet -2.1% and Microsoft -0.9%). Semiconductor stocks are weighed down after ASML reported quarterly bookings well below estimates (AMD -6.8%, Broadcom -3.8%, Micron -3.7%, Marvell Technology -3.6%, ASML ADRs -4.5%). United Airlines (UAL) climbs 7% after the carrier Tuesday said it expects an adjusted profit of $11.50 to $13.50 a share if the current environment remains stable; But full-year earnings would drop to as little as $7 a share if the US economy enters a recession (peers rise: Delta Air Lines (DAL) +3.2%, American Airlines (AAL) +2.8%). Here are some other notable movers:

Interactive Brokers (IBKR) drops 8% after the broker’s first-quarter earnings fell short of expectations, with analysts attributing the EPS miss to a slide in net interest income and higher expenses. Peer Robinhood (HOOD) declines 4%

JB Hunt (JBHT) falls 6% after the trucker reported revenue in multiple segments that fell short of consensus estimates.

MP Materials (MP) rises 2.9% and TMC the Metals Co. (TMC) gains 3% after President Trump launched a probe into the need for tariffs on critical minerals, the latest action in an expanding trade war that has targeted key sectors of the global economy.

Omnicom (OMC) slips 2.4% after the advertising company reported quarterly revenue that came in slightly under expectations.

REV Group (REVG) falls 3% after Morgan Stanley downgraded the manufacturer of specialty vehicles on tariff risk

Hertz (HTZ) jumps 21% after Pershing Square Capital Management disclosed a 12.7 million share stake in Hertz. Stake value amounts to about $46.5 million

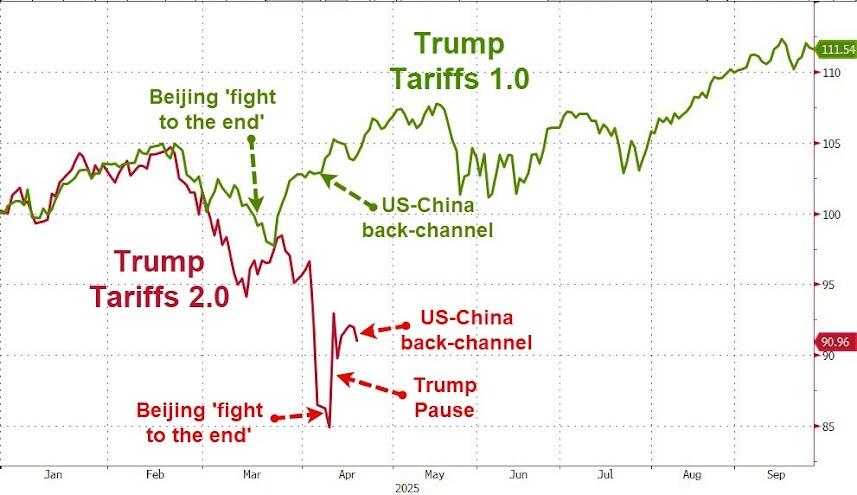

Markets were setting up for another overnight rout after the US government informed Nvidia on Monday that its H20 chip would require a license to export to China “for the indefinite future.” The new rules address Washington’s concerns that “the covered products may be used in, or diverted to, a supercomputer in China,” the company said in a filing. Nvidia warned it will report about $5.5 billion in writedowns during the current quarter, tied to inventory and commitments for the chip.

“This move is unnerving for two reasons,” said Vishnu Varathan, Singapore-based head of economics and strategy at Mizuho Bank, referring to the Nvidia curbs. “First, it conveys the mercurial nature of Trump tariffs in so far that it has revoked earlier concessions extended to Nvidia. Second, this also suggests that the US-China undercurrents are rather abusive, even as there appears to be some calm on the surface.”

However, stocks pared some of the losses in the morning session on signs China may be open to negotiations with the US, sparking some optimism over the possibility of easing trade tensions. China said it wants a number of steps from President Donald Trump’s administration before it will agree to talks, including showing more respect by reining in disparaging remarks by members of his cabinet, according to a person familiar with the Chinese government’s thinking.

“We’re keeping a defensive stance during this period of uncertainty while being increasingly cautious on tech stocks and industries which have a high share of their value chain exposed to China,” said Francois Antomarchi, a fund manager at Degroof Petercam Asset Management. “There’s the question of knowing when we hit the bottom, geopolitically speaking, of the trade war, and I’m not sure we’re there yet.”

The US government informed Nvidia on Monday that its H20 chip would require a license to export to China “for the indefinite future.” The new rules address Washington’s concerns that “the covered products may be used in, or diverted to, a supercomputer in China,” the company said in a filing. Nvidia warned it will report about $5.5 billion in writedowns during the current quarter, tied to inventory and commitments for the chip. “This move is unnerving for two reasons,” said Vishnu Varathan, Singapore-based head of economics and strategy at Mizuho Bank, referring to the Nvidia curbs. “First, it conveys the mercurial nature of Trump tariffs in so far that it has revoked earlier concessions extended to Nvidia. Second, this also suggests that the US-China undercurrents are rather abusive, even as there appears to be some calm on the surface.”

Meanwhile, UK bonds rallied after inflation eased more than expected in March, spurring increased bets from traders on Bank of England interest rates.

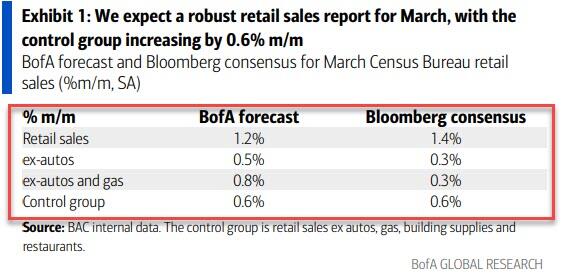

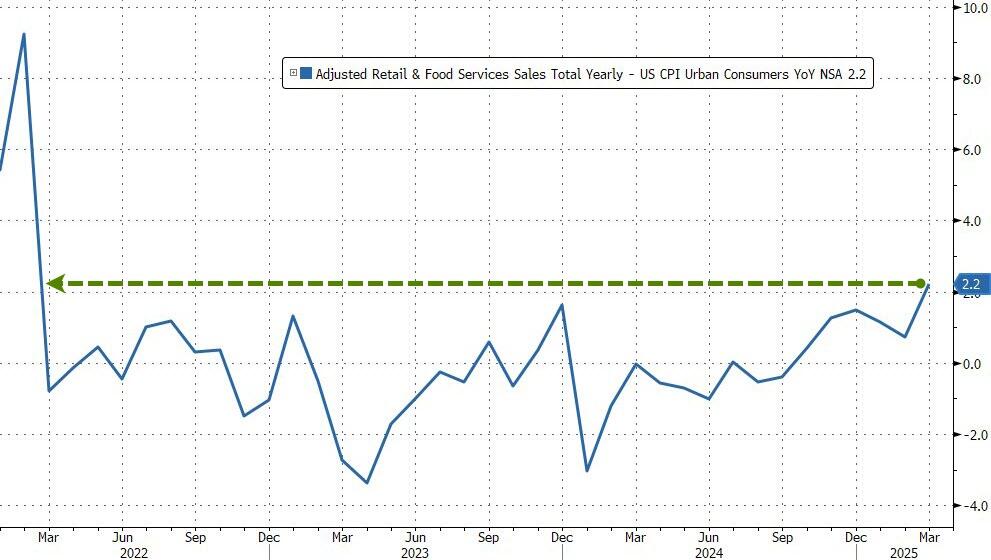

Federal Reserve Chair Jerome Powell is expected to give a speech later in the day, and investors will be watching March retail sales data for a reading of consumer sentiment before the tariff turmoil.

In Europe, the Stoxx 600 pares its drop to 0.9%, technology and financial services shares are the worst-performers, while utilities and telecommunications stocks are the biggest gainers. Tech sentiment was further dented by ASML, whose first-quarter orders missed estimates. Here are the biggest movers Wednesday:

Sartorius shares rise as much as 9.4% after the German lab equipment maker reported better-than-expected results for the first quarter

Heineken shares gain as much as 3.5%, the most since April 10, after the Dutch brewer’s earnings. Analysts see a beat on Q1 volumes and sales, solid delivery in key markets, and guidance that helped offset FX concerns

European oil and gas producers drop as much as 1.4%, snapping a two-day winning streak, as crude prices extend their decline

Bunzl shares plunge as much as 27%, marking a record drop, after the value-added distributor cut its annual guidance due to challenges in North America and paused its share buyback

EQT shares slide as much as 8.5% as the Swedish investment firm’s cautious guidance on exits and valuations tempers enthusiasm despite a generally solid first-quarter earnings update

ASML shares drop as much as 7.6% after the chip-equipment maker reported quarterly bookings well below estimates, a sign of weakness in customer demand

Straumann shares fall as much as 5.3%, worst performer in the Stoxx 600 Health Care Index on Wednesday, after UBS cut its price target on the stock to a Street-low, citing the recent strengthening of the Swiss franc

Antofagasta falls as much as 2.7% in London after the miner reported copper production for the first quarter 2025 that was 23% lower versus prior comparable period

WH Smith shares drop as much as 3.3% after UBS said the retailer is closing far more stores than previously expected this year, while others warned a foreign-exchange headwind could also hit consensus estimates

XPS Pensions shares fall as much as 5.2%, the most since April 7, after the UK benefits consultaning firm issued a trading update which Shore Capital says slightly beat expectations but leaves little room for upward revisions

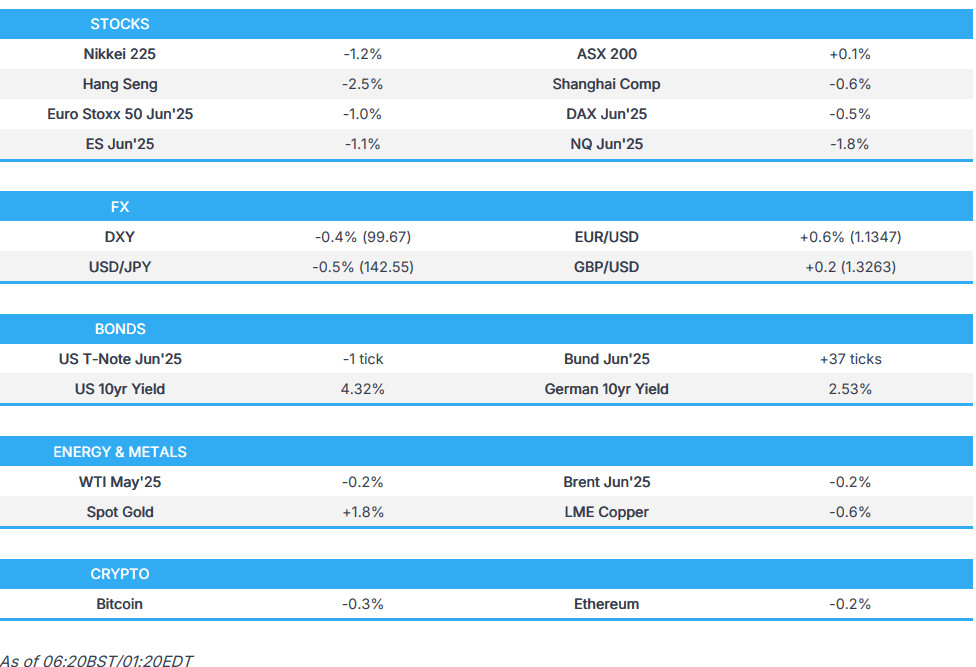

Earlier in the session, Asian stocks dropped, driven by technology shares following new restrictions on exports of Nvidia’s H20 chips to China. The MSCI Asia Pacific Index declined as much as 1.4%, with TSMC, Alibaba and Tencent among the major drags. The Hang Seng China Enterprises Index led losses among major regional gauges, falling 2.6% on worries around escalation of US-China tensions. Benchmarks in Taiwan, Japan and South Korea also fell. The latest Nvidia curbs shook investor confidence again after recent signs of stabilization around President Donald Trump’s tariff war. Sentiment was also hurt by disappointing results from Dutch chip-equipment maker ASML and a US probe into the need for levies on critical minerals. Chinese onshore shares eked out small gains toward the end of the day. Some investors remain optimistic on the nation’s efforts to bolster its economy and tech industry. China earlier reported a set of upbeat economic data. Investors will be also be watching for any signs of a cooling in US-Sino tensions.

“Asian stocks found it hard to muster much in the way of forward progress today with the Nvidia news,” said Tim Waterer, chief market analyst at KCM Trade in Sydney. “There is a reliance on the H20 chip from big name players in the Asian tech space, so any moves which could impact supply will be a drag on the broader sector.”

In FX, the Bloomberg Dollar Spot Index is down 0.5% having earlier fell to a six-month low. The Swiss franc outperforms on haven demand although has pared gains to 0.8% amid the bounce in stocks. The euro also adds 0.8% against the greenback. The pound adds 0.3% to around $1.327.