GOLD CLOSED DOWN $7.75 TO $3,406.75

SILVER CLOSED UP $0.30 TO $32.90

GOLD ACCESS CLOSED 3420.70

Silver ACCESS CLOSED: $32.72

Bitcoin morning price:$88,423 UP 1128 DOLLARS.

Bitcoin: afternoon price: $91,650 UP 4355 DOLLARS

Platinum price closing DOWN $3.25 TO $962.90

Palladium price; UP $1.45 TO $939.05

END

*CANADIAN GOLD: $4663.54 DOWN 75.30 CDN dollars per oz( * NEW ALL TIME HIGH $4735.70 CDN DOLLARS PER OZ//APRIL 21 2025)

*BRITISH GOLD: 2529.10 DOWN 37.35 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,559.38 BRITISH POUNDS/OZ) APRIL 21/2025

*EURO GOLD: 2,952.25 DOWN 30.35 Euros per oz //* (ALL TIME CLOSING HIGH: 2,973.82 EUROS PER OZ/ APRIL 21 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,406.200000000 USD

INTENT DATE: 04/21/2025 DELIVERY DATE: 04/23/2025

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 2

363 H WELLS FARGO SECURITI 48

435 H SCOTIA CAPITAL (USA) 96

624 H BOFA SECURITIES 80

661 C JP MORGAN SECURITIES 8

686 C STONEX FINANCIAL INC 13 5

690 C ABN AMRO CLR USA LLC 1

709 C BARCLAYS 25

737 C ADVANTAGE FUTURES 2 1

905 C ADM 9

TOTAL: 145 145

MONTH TO DATE: 63,641

jpmorgan stopped: 0/145

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 145 NOTICES FOR 14500 OZ 0.4510 TONNES

total notices so far: 63,641 contracts for 6,364,100 OR 197.950 tonnes)

FOR APRIL

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 45 NOTICE(S) FILED FOR 0.225 MILLION OZ/

total number of notices filed so far this month : 3097 CONTRACTS (NOTICES) for 15.485 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $7.75 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OUT OF THE GLD

INVENTORY RESTS AT 953.971 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.30 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 453.971 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA HUGE SIZED 2051 CONTRACTS TO 144,437 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL GAIN OF $0.15 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 2256 TOTAL CONTRACTS AS THE CME NOTIFIED US OF A FAIR 205 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD A CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING MONDAY AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON MONDAY WITH SILVER’S GAIN IN PRICE BUT THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH A HUGE T.A.S. ISSUANCE OF 962 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A FAIR 205 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 962 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN MONDAY/TUESDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 2256 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR SMALL GAIN IN PRICE OF $0.15.

THE CME NOTIFIED US THAT WE HAD 0 CONTRACTS OF THOSE CRAZY EXCHANGE FOR RISK CONTRACTS ISSUED FOR 0 OZ (0 MILLION OZ). THESE EXCHANGE FOR RISKS ARE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THUS FOR THE MONTH OF APRIL WE HAVE A TOTAL OF 4.0 MILLION OZ OF EXCHANGE FOR RISK ISSUED ON TWO OCCASIONS. THE RECIPIENT OF THIS LARGESS IS PROBABLY THE CENTRAL BANK OF INDIA.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A HUGE 962 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.15) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS DESPITE HAVING A SMALL GAIN IN PRICE, WE GAINED A MEGA HUGE 2256 CONTRACTS IN OPEN INTEREST FROM OUR TWO EXCHANGES.

WE HAD A FAIR 205 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.735 MILLION OZ FOLLOWED BY TODAY’S 30,000 OZ EFP TRANSFER TO LONDON JUMP TO WHICH WE ADD OUR 4.00 MILLION OZ EX FOR RISK

STANDING FOR APRIL DECREASES TO 19.500 MILLION OZ

WE HAD:

/ HUGE COMEX OI GAIN+// A FAIR SIZED EFP ISSUANCE (205 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 962 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 156 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 17 DAYS, total 15,280 contracts: OR 76.400 MILLION OZ (898 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 76.400- MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 76.400 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2051 CONTRACTS WITH OUR GAIN IN PRICE OF $0.15 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A FAIR 205 CONTRACT EFP ISSUANCE CONTRACTS: 205 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A STRONG SILVER OZ STANDING FOR APRIL OF 15.500 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

NEW STANDING APRIL: 19.500 MILLION OZ

THE NEW TAS ISSUANCE MONDAY NIGHT (962 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND MOST LIKELY TUESDAY TRADING.

WE HAD 45 NOTICE(S) FILED TODAY FOR 0.225 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY STRONG SIZED 7739 OI CONTRACTS TO 466,325 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A MONSTER 2669 CONTRACTS //.

WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI (7739 CONTRACTS) . THIS OCCURRED WITH OUR MONSTER GAIN OF $98.75 IN PRICE MONDAY. ON WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES (CME CORRECTED// MAYBE?) TO WHICH WE ADD FOR APRIL ITS INITIAL 700 CONTRACT EXCHANGE FOR RISK FOR 70,000 OZ OR 2.177 TONNES AND FRIDAY APRIL 4: 250 CONTRACT ISSUANCE FOR .777 TONNES + MONDAY APRIL 7 NEW ISSUANCE OF .8709 TONNES/ + APRIL 9 ‘S TOTAL OF 484 EX. FOR RISK FOR 48,400 OZ OR 1.5054 TONNES/NEW TOTAL AND FINALLY APRIL 14 EX FOR RISK OF 30,000 OZ OR.6220 TONNES// ;NEW EX FOR RISK 5.912 TONNES TO WHICH WAS ADDED TO OUR NEW QUEUE JUMP OF 38 CONTRACTS OR 3800 OZ (0.1182 TONNES). THUS INITIAL STANDING FOR GOLD/APRIL DELIVERY MONTH IS 199.576 TONNES NORMAL DELIVERY(INCLUDES OF QUEUE JUMP) + 5.912 TONNES EX FOR RISK = 205.488 TONNES

/NEW STANDING FOR APRIL; 199.576 TONNES + 5.912 TONNES EX FOR RISK = 205.488 TONNES

/ ALL OF THIS HAPPENED WITH OUR $98.75 GAIN IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD A VERY STRONG SIZED GAIN OF 9169 OI CONTRACTS (28.52 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AND NOW FOR OUR FRONT MONTH OF APRIL. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS. WE HAVE A MASSIVE AMOUNT OF TONNES STANDING FOR GOLD IN APRIL.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1430 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 469.994

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9169 CONTRACTS WITH 7739 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 1430 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 9169 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1517 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1430 CONTRACTS) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 7739 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 9169 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING AT THE GOLD COMEX FOR APRIL 199.576 TONNES (WHICH INCLUDES OUR 0.1182 TONNES QUEUE JUMP) AND THIS FOLLOWS TOTAL EXCHANGE FOR RISK ISSUANCE ON 5 OCCASIONS FOR 5.912 TONNES//NEW STANDING ADVANCES TO 205.488 TONNES.

//NEW STANDING APRIL: 199.576 TONNES + 5.912 TONNES EX FOR RISK ON 5 OCCASIONS = 205.488 TONNES

.

/ 3) LITTLE IF ANY T.A.S. LIQUIDATION + ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WE HAD: 1)A $98.75 COMEX PRICE GAIN AND WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A HUGE GAIN OF 11,838 CONTRACTS ON OUR TWO EXCHANGES/./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN APRIL.

4) STRONG SIZED COMEX OI GAIN// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (2062 CONTRACTS)///FAIR T.A.S. ISSUANCE: 1517 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 51,117 CONTRACTS OR 5,111,700 OZ OR 158.995 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 3006 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 158.995 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 158.995TONNES DIVIDED BY 3550 x 100% TONNES = 4.47% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 158.995 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 2051 CONTRACTS OI TO 142,386 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 205 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 205 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 205 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2207 CONTRACTS AND ADD TO THE 206 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2256 CONTRACTS WITH THE GAIN IN PRICE OF $0.15 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 11.280 MILLION PAPER OZ

OCCURRED DESPITE OUR SMALL $0.15 IN PRICE GAIN.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 8.32 PTS OR 0.25%

//Hang Seng CLOSED UP 167.18 PTS OR 0.78%

// Nikkei CLOSED DOWN 59.32 OR 0.17%//Australia’s all ordinaries CLOSED UP 0.10%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.3135 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3161/ Oil UP TO 64.14 dollars per barrel for WTI and BRENT DOWN TO 67.06 Stocks in Europe OPENED ALL MIXED.

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7739 CONTRACTS TO 466,325 WITH OUR HUGE GAIN IN PRICE OF $98.75 WITH RESPECT TO MONDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1430 ).

THE CME ANNOUNCED MONDAY NIGHT, 0 EXCHANGE FOR RISK CONTRACTS FOR 0 OZ OR 0.0 TONNES. SO FAR THIS MONTH WE HAD RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE FRONT MONTH OF APRIL STANDS AT 5.912 TONNES OF GOLD WHICH MUST BE ADDED TO OUR NORMAL GOLD DELVERIES.

HISTORY: LAST TWO PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.

DETAILS ON APRIL COMEX MONTH

IN TOTAL WE HAD A VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 11,838 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON WEDNESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF APRIL CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A BIT LARGER THAN FROM THE PAST FEW DAYS AT 1517 CONTRACTS

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 205 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 219 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1.2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF APRIL .… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1517 EFP CONTRACTS WERE ISSUED: : /APRIL 1517 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1517 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 9169 CONTRACTS IN THAT 1430 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG GAIN OF 7739 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR MONSTER GAIN IN PRICE OF $98.75 FOR MONDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. LOOKS LIKE THE SHORT RATS ARE FLEEING THE ARENA AS EVIDENCED BY THE LOWER OPEN INTEREST AT THE COMEX!

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED 1430 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S THESE PAST FEW MONTHS,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED NOTHING AS NOBODY LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND ,FOR MARCH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT WEDNESDAY MARCH 17, THE 38,393 T.A.S. CONTRACT ISSUANCE WAS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH AND APRIL.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH. WE HAVE YET TO EXPERIENCE A MEGA CONSECUTIVE 30,000 CONTRACT T.A.S FOR APRIL.

STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (205.488 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 4 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

STANDING FOR GOLD: 199.576 TONNES + 5.912 TONNES EX FOR RISK = 205.488 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 51 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 205.154 TONNES (INCLUDES 5.912 TONNES EX FOR RISK)

COMEX GOLD TRADING/APRIL CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $98.75/ /)/AND WERE UNSUCCESSFUL IN KNOCKING OFF ANMY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A VERY STRONG SIZED GAIN IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD LITTLE IF ANY T.A.S. SPREADER LIQUIDATION MONDAY AS THEY WERE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,400 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS THEY FAILED IN THEIR ATTEMPT TO STOP THE PENETRATION OUR OUR $3,400 DOLLAR GOLD BARRIER AS IT IS NOW TRADING WELL ABOVE THAT AT $3485 PER OZ AS I WRITE THIS EXPLORING THE IDEA OF BREAKING $3500.

MONDAY NIGHT/TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /APRIL TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCE

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

NOW APRIL, ISSUES ITS 5TH EXCHANGE FOR RISK: 200 CONTRACTS OR 20,000 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK/APRIL//TOTAL ISSUANCES 5 FOR 5.912 TONNES OF GOLD!

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES//NEW TOTAL ISSUANCE FOR APRIL: 5.912 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WILL BE ADDED TO OUR NORMAL DELIVERY CYCLE.

STANDING FOR GOLD NOW FOR APRIL:

APRIL: 199.576 TONNES +(5.912 EX FOR RISK// FOR APRIL DELIVERY MONTH =205.488 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS APRIL DELIVERY MONTH AFTER FIRST DAY NOTICE;

WE HAVE GAINED A STRONG SIZED TOTAL OF 30.82 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL FIRST RECORDED AT 166.964 TONNES ON FIRST DAY NOTICE FOLLOWED BY 5 EXCHANGE FOR RISK CONTRACT ISSUANCES FOR 5.912 TONNES.

ALSO TODAY WE RECORD ANOTHER 38 CONTRACT QUEUE JUMP FOR 3800 OZ OR 0.1182 TONNES. WE MUST NOW ADD OUR 5.912 TONNES EXCHANGE FOR RISK TO OUR NEW NORMAL DELIVERY OF 199.576 TONNES AND THUS STANDING FOR GOLD FOR APRIL IS NOW 205.488 TONNES, THE 2ND HIGHEST EVER RECORDED!

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $98.75

WE HAD 2669 CONTRACTS REM,OVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 9196 CONTRACTS OR 919,600 0Z (28.52 TONNES)

confirmed volume MONDAY 263,293.. contracts: fair///

//speculators have left the gold arena

END

APRIL

// THE APRIL 2025 GOLD CONTRACT

APRIL22

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 4 ENTRIES: 4 withdrawals I) Out of Ashai 247,465.353 oz ii) Out of Brinks 32,118.999 oz (999 kilobars) iii) Out of JPM: 11,381.454 oz (354 kilobars) iv) Out of Loomis: 675.171oz (21 kilobars) total weight withdrawal: 291,640.827oz or 9.071 tonnes . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | we have 0 customer entry xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 145 notice(s) 14500 OZ 0.4510 TONNES |

| No of oz to be served (notices) | 523 contracts 52,300 OZ 1.626 TONNES |

| Total monthly oz gold served (contracts) so far this month | 63,641 notices 6,364,100 oz 197.950 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

TOTAL WEIGHT; 0 TONNES

xxxxxxxxxxxxxxxxxxxxx

we have 0 customer entries

we have 0 customer deposit entry

total deposit

NIL

xxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:

4 ENTRIES: 4 withdrawals

I) Out of Ashai 247,465.353 oz

ii) Out of Brinks 32,118.999 oz (999 kilobars)

iii) Out of JPM: 11,381.454 oz (354 kilobars)

iv) Out of Loomis: 675.171oz (21 kilobars)

total weight withdrawal: 291,640.827oz or 9.071 tonnes

adjustments: 2 dealer to customer

a) Brinks: 107,352.37 oz

ii) Malca: 43,473.774 oz

xxxxxxxxxxxxxxxxxx

AMOUNT OF GOLD STANDING FOR APRIL

THE FRONT MONTH OF APRIL HAD A LOSS OF 465 CONTRACTS TO STAND AT 668. WE HAD 503 CONTRACTS FILED YESTERDAY. THUS WE GAINED 38 CONTRACTS OR 3800 OZ (0.1182 TONNES) AS WE EXPERIENCED ANOTHER QUEUE JUMP WHERE THESE BOYS DESIRED TO TAKE PHYSICAL DELIVERY OVER HERE. THIS IS CENTRAL BANKERS STANDING FOR PHYSICAL GOLD. LAST FRIDAY’S QUEUE JUMP OF 6.1619 TONNES REPRESENTED THE HIGHEST EVER QUEUE JUMP IN COMEX HISTORY SURPASSING THE PREVIOUS HIGHEST RECORDED WAS AT 5.90 TONNES.

MAY GAINED 732 CONTRACTS UP TO 6144 CONTRACTS. MAY BECOMES THE FRONT MONTH AND WE WILL ALSO EXPERIENCE A STRONG DELIVERY MONTH EVEN THOUGH IT IS AN OFF MONTH!

JUNE GAINED 6543CONTRACTS TO 354,684. JUNE WILL STILL BE A WHOPPER OF A DELIVERY MONTH

We had 145 contracts filed for today representing 14,500 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 10 notices issued from their client or customer account. The total of all issuance by all participants equate to 145 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL /2025. contract month, we take the total number of notices filed so far for the month (63,641 X 100 oz ) to which we add the difference between the open interest for the front month of APRIL (668 CONTRACTS) minus the number of notices served upon today (145 x 100 oz per contract) equals 6,416,400 OZ OR 199.576 TONNES

to which we add our 5 exchange for risk issuances for April of 5.912 tonnes

= 205.488 tonnes

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (63,641 x 100 oz +we add the difference for front month of APRIL (668 OI} minus the number of notices served upon today (145 x 100 oz) which equals 6,416,400 OZ OR 199.576 TONNES + 5.912 tonnes ex for risks = 205.488 tonnes

TOTAL COMEX GOLD STANDING FOR APRIL.: 205.488 TONNES WHICH IS HUGE FOR THIS ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL IS FOLLOWING SUIT..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,020,995.744 oz 62.86 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 42,803,280.773 oz

TOTAL REGISTERED GOLD 21,306,726.690 or 662.728 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 21,496.554.083 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 19,285,731oz (REG GOLD- PLEDGED GOLD)= 599.86tonnes //

END

SILVER/COMEX

// THE APRIL 2025 SILVER CONTRACT//INITIAL

APRIL 22

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 withdrawal entries i) out of Brinks: 608,045.090 oz ii) Out of Stonex; 828,680.500 oz total withdrawal: 1,436,725.590 oz |

| Deposits to the Dealer Inventory | 0/ entry |

| Deposits to the Customer Inventory | 0 entries nil |

| No of oz served today (contracts) | 45 CONTRACT(S) (0.225 MILLION OZ |

| No of oz to be served (notices) | 3 contracts (0.015 MILLION oz) |

| Total monthly oz silver served (contracts) | 3097 Contracts (15.485million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

0 entries/dealer

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

0 entries

nil

total deposit nil oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2) withdrawal customer acct

3 withdrawal entries

i) out of Brinks: 599,283.380 oz

ii) Out of Delaware 993.750 oz

iii) Out of Loomis 596,251.700 oz

total withdrawal: 1,196,528.830 oz

ADJUSTMENTs 0

JPMorgan has a total silver weight: 199.954million oz/496.698oz million or 40.27%

TOTAL REGISTERED SILVER: 160.221 MILLION OZ//.TOTAL REG + ELIGIBLE. 496.698Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2025 OI: 48 OPEN INTEREST CONTRACTS FOR A LOSS OF 65 CONTRACTS. WE HAD 59 NOTICES FILED ON MONDAY SO WE LOST 6 CONTRACTS WHICH UNDERWENT AN EFP TRANSFER TO LONDON OF 30,000 OZ AS THESE BOYS WERE NOT WILLING TO WAIT FOR DELIVERY OF SILVER OVER HERE SO THEY ARE TRYING TO TAKE DELIVERY AT ENGLAND .

MAY SAW A LOSS OF 823 CONTRACTS DOWN TO 50,667 CONTRACTS. MAY BECOMES THE FRONT MONTH AND IT LOOKS LIKE WE WILL HAVE A DANDY AMOUNT OF SILVER STANDING THIS MONTH.

JUNE SAW A GAIN OF 591 CONTRACTS UP TO 2511 CONTRACTS.

JULY GAINED 2254 CONTRACTS UP TO 72,752

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 45 or 0.225 MILLION oz

CONFIRMED volume; ON MONDAY 67,955 fair//

AND NOW APRIL DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 3097 X5,000 oz = 15.485 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (48) AND the number of notices served upon today (45 )x (5000 oz)

Thus the standings for silver for the APRIL 2025 contract month: (3097) Notices served so far) x 5000 oz + OI for the front month of APRIL(48) minus number of notices served upon today (45)x 5000 oz equals silver standing for the APRIL contract month equating to 15.500 MILLION OZ . WE MUST NOW ADD OUR 4.0 MILLION OZ EXCHANGE FOR RISK ISSUED ON MONDAY MARCH 31 AND TODAY APRIL 4/NEW STANDING DECREASES TO 19.500 MILLION OZ

New total standing: 19.500 million oz which is huge for this NON active delivery month of APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 160.221million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

MARCH 21 WITH GOLD DOWN $20.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 910.43 TONNES

MARCH 20 WITH GOLD UP $3.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 909.28 TONNES

MARCH 19 WITH GOLD UP $0.45 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 907.27 TONNES

MARCH 18 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 907.27 TONNE

MARCH 17 WITH GOLD UP $34.05 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.64 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 906.41 TONNES

MARCH 14 WITH GOLD UP $9.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MONSTER DEPOSIT OF 7.17 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 905.81 TONNES

MARCH 13 WITH GOLD UP $42.85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 12 WITH GOLD UP $22.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.90 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 895.20 TONNES

MARCH 11 WITH GOLD UP $21.20 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 891.30 TONNES

MARCH 10 WITH GOLD DOWN $12.45 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 894.317 TONNES

MARCH 7 WITH GOLD DOWN $12.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 898.64 TONNES

MARCH 6 WITH GOLD UP $2.10 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.44 TONNES TONNES OUT OF THE GLD ///INVENTORY RESTS AT 900.30 TONNES

MARCH 5 WITH GOLD UP $6.75 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.87 TONNES INTO THE GLD ///INVENTORY RESTS AT 901.80 TONNES

MARCH 4 WITH GOLD UP $19.05 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 900.93 TONNES

MARCH 3 WITH GOLD UP $50.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 28 WITH GOLD DOWN $44.70 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 1.72 TONNES INTO THE GLD ///INVENTORY RESTS AT 904.38 TONNES

FEB 26 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 25 WITH GOLD DOWN $40,85 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 3.45 TONNES INTO THE GLD ///INVENTORY RESTS AT 907.83 TONNES

FEB 24 WITH GOLD UP 7,65 TODAY HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 20.66 TONNES FROM THE GLD ///INVENTORY RESTS AT 904.38TONNES

FEB 21 WITH GOLD DOWN $1.35 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 5.77ONNES FROM THE GLD ///INVENTORY RESTS AT 883.72TONNES

FEB 20 WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 8.51TONNES FROM THE GLD ///INVENTORY RESTS AT 877,95TONNES

FEB 19/ WITH GOLD DOWN $10.40 TODAY HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 6.38TONNES FROM THE GLD ///INVENTORY RESTS AT 869.44TONNES

FEB 18/ WITH GOLD UP $43.00 TODAY HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.14TONNES FROM THE GLD ///INVENTORY RESTS AT 863.06TONNES

GLD INVENTORY: 959.17 TONNES, TONIGHTS TOTAL

SILVER

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

MARCH 21 WITH SILVER DOWN $0.45 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 442.962 MILLION

MARCH 20 WITH SILVER DOWN $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 19 WITH SILVER DOWN $0.45 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.219 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.054 MILLION

MARCH 18 WITH SILVER UP $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.823 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 444.373 MILLION

MARCH 17 WITH SILVER UP $0.03 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.096 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 439.550 MILLION

MARCH 14 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.910 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.454 MILLION

MARCH 13 WITH SILVER UP $0.46 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.774 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 434.544 MILLION

MARCH 12 WITH SILVER UP $0.57 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.032 MILLION OZ OUT OF THE THE SLV. //INVENTORY AT SLV RESTS AT 435.318 MILLION

MARCH 11 WITH SILVER UP $0.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.816 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 436.410 MILLION

MARCH 10 WITH SILVER DOWN 25 CENTS/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.276 MILLION OZ INTO THE THE SLV. //INVENTORY AT SLV RESTS AT 435.591 MILLION

MARCH 7 WITH SILVER DOWN 40 CENTS/HUGL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.184 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 434.317 MILLION

MARCH 6 WITH SILVER UP 16 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.455 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.046 MILLION

MARCH 5 WITH SILVER UP 82 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.172 MILLION OZ OUT OF THE SLV. //INVENTORY AT SLV RESTS AT 436.501 MILLION OZ

MARCH 4 WITH SILVER UP 9 CENTS//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.82 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 436.673 MILLION OZ

MARCH 3 WITH SILVER UP $0.78//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 28 WITH SILVER DOWN 0.56//SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.819 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 438.493 MILLION OZ

FEB 26 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 25 WITH SILVER DOWN $0.90//HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6,245 MILLION OZ INTO THE SLV. //INVENTORY AT SLV RESTS AT 441.4061MILLION OZ

FEB 24WITH SILVER DOWN $0.15//NO CHANGES IN SILVER INVENTORY AT THE SLV. //INVENTORY AT SLV RESTS AT 435.171MILLION OZ

FEB 21WITH SILVER DOWN $0.40//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.456MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 20WITH SILVER UP $0.29//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 1.547 MILLION OZ/. //INVENTORY AT SLV RESTS AT 435,171MILLION OZ

FEB 19WITH SILVER DOWN $0.16//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : HUGE CHANGES AT THE SLV A WITHDRAWAL OF 2.276 MILLION OZ/. //INVENTORY AT SLV RESTS AT 436.717MILLION OZ

FEB 18WITH SILVER UP $.56//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : NO CHANGES AT THE SLX/. //INVENTORY AT SLV RESTS AT 438.994MILLION OZ

FEB 14WITH SILVER UP $.01//HUGE CHANGES IN SILVER INVENTORY AT THE SLV : A DEPOSIT OF 1.593 MILLION OZ INTO THE SLV./. //INVENTORY AT SLV RESTS AT 437.401 MILLION OZ

CLOSING INVENTORY 453.971 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2, EGON VON GREYERZ

ALASDAIR MACLEOD

A sober look at America’s decline

This article by Patrick Barron was posted at Going Postal last week. I have his permission

David Hume’s Insight Explains America’s Economic Decline

Only Sound Money Will Clear International Settlement Accounts

16th April 2025 Patrick Barron America, Economics, Finance, Markets, Trade

Since he was a young up-and-coming property magnate in New York City, Donald Trump has been fixated on what he believes to be foreigners’ cheating on international trading terms to the detriment of the US. He believes, along with many Americans, that foreigners have stolen all our good, high paying jobs by manipulating their own currencies, subsidizing their home industries, and erecting protective trade barriers–in the form of tariffs and quotas–that make American goods uncompetitive. He believes that erecting high tariffs against foreign goods will level the playing field, so to speak, and restore American industry and high paying jobs. In summary, Donald Trump is a firm believer in Autarky and Mercantilism, discredited economic theories that tout national self-sufficiency on the one hand and exporting more than one imports on the other.

MacleodFinance Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.Subscribed

Foreigners Are Not to Blame for America’s Economic Woes

Whatever one may think about America’s economic progress or lack thereof and about whether or not America is losing good paying jobs, foreigners are not to blame. We ourselves are to blame, and there are several ways in which we “do it to ourselves”. The first and most important occurred at Bretton Woods in 1944 when the dollar was granted international reserve currency standing as the equivalent of gold at thirty-five dollars per ounce. The thinking, which was challenged at the time in a series of articles by New York Times columnist Henry Hazlitt, was that as long as the US had enough gold to completely back its currency at that price, the international trade clearing system would function just as well and with less cost than the cumbersome system, as it was described, of shipping gold back and forth among nations. For example, if England imported more goods from France than vice versa, then England would owe France money. It would “clear” its shortfall by shipping gold to France. Under the Bretton Woods system, England would send American dollars to France or ask an American bank to pay France dollars held in its account in New York. Much easier, or so almost everyone thought at the time. Although he spoke in more diplomatic terms, Henry Hazlitt felt that the temptation to print money without gold backing was too tempting even for Americans. He was right.

De Gaulle and Rueff Suspected American Cheating

The problems arose when the US started printing more money than it could back with gold at thirty-five dollars an ounce, just as Hazlitt feared. Charles De Gaulle, president of France in the 1960’s, and Jacques Rueff, his long time chief financial advisor, were both economic scholars of the “old school” who suspected that Americans were cheating; i.e., printing dollars without sufficient gold backing. De Gaulle ordered the Bank of France to exchange eighty percent of its dollar holdings for gold specie at the set price. The race, as they say, was on. There ensued the equivalent of an old-fashioned bank run on the US gold supply by foreign central banks. When America’s gold supply became dangerously low and demand for gold redemption had not slowed, President Nixon suspended gold redemption. Because of its post WWII economic position and its critical defense support of NATO against an aggressive Soviet Union, America’s major trading partners acquiesced in the gold suspension and the world went on a dollar reserve system unbacked by anything other than faith in the US.

This was the beginning of an explosion in fiat money and American budget deficits. This lethal combination of fiat dollars becoming the world’s premier reserve currency meant that the US never really “cleared” its international trading account again in real money; i.e., gold. Today America is the largest debtor nation in the history of the world.

The Consequences to America for Violating David Hume’s “Price Specie Flow Mechanism”

In a recent interview on Liberty and Finance Jeffrey Tucker explained the importance of clearing international trade in sound money, namely gold, which was the well accepted doctrine of the world for centuries. Born over three hundred years ago Scottish philosopher David Hume explained why nations that settle international trade in gold will always tend toward price equilibrium. No nation needs to manipulate its trading terms out of fear that it will run out of gold or import so much gold that its price level will rise so high that its products will become uncompetitive in the world market. Hume termed his discovery the ”Price Specie Flow Mechanism”. If a country sells much more in the world market than it buys, which is the Mercantilists’ desire, the price level will rise so high that its products will become uncompetitive, ending the importation of gold for goods and services. Likewise, if a country imports more than it sells, its price level will fall; making its products more competitive and the flow will reverse. This was the accepted theory for centuries, during which international trade and living standards expanded to reach new historical heights.

The Consequences of the Failure of Bretton Woods

But, Jeffrey Tucker explains, what happens when gold, the “specie” in Hume’s theory, is no longer used for settlement? What happens when fiat money, which can and was manufactured in vast quantities out of thin air, becomes the settlement medium? Enter the failure of Bretton Woods, which resulted in the rise of the fiat dollar reserve system. Tucker explains that America became corrupted by its newly found money spigot. It no longer had to compete with the world, because it could always simply print more money. And print more money it did! In spades!

Now let’s see how this played out in Austrian economic terms. Austrian economics explains that all economic life is conducted at the individual level, what Austrians call Methodological Individualism. The ability of America to import ‘til the cows come home and settle with dollars printed out of thin air meant that it really did not have to compete in worldwide markets anymore. The main thing that America exported was dollars! At the individual level, this meant that America could accede to just about all welfare lobbies. Americans no longer really had to worry about getting a good education, working hard, etc. in order to get good jobs. Its radicalized labor unions could strike for above world labor rates. As Tucker explains, a half a century later American workers are overpaid in international markets. Its goods are shoddily produced. Industry after industry has failed. Government schools turn out students who rank very far down world survey results. America has been covering up this scandal with fiat money, which is just more of the same old snake oil that got it there.

There Is a Solution

The only solution is to go back on the gold standard. As long as America can print fiat money to pay for imports it will print fiat money. But under the discipline of the gold standard, Americans will have to produce good quality products at world market prices in order to earn the foreign exchange (gold) needed to settle international trade. It’s the only way. Erecting tariffs, as desired by President Trump, solves nothing and merely exacerbates the situation. America must learn to compete in the world on equal terms; i.e., it cannot simply print fiat dollars. It must produce goods that foreigners wish to buy at prices that foreigners are willing to pay. Becoming an autarkic nation, a la North Korea, will condemn Americans to poverty. America needs to become an honest, commercially oriented nation. If not, the world will pass it by just as has happened to other great nations in the past.

© Patrick Barron 2025 Website

3. C Powell and Gata dispatches

As the dollar falters, central banks tread a tightrope: Devalue their currency or not?

Submitted by admin on Tue, 2025-04-22 08:51 Section: Daily Dispatches

By Lee Ying Shan

CNBC, New York

Monday, April 21, 2025

The dollar has been sliding and the ripple effect on other currencies has brought a mix of relief and headache to central banks around the world.

Uncertainty about U.S. policymaking has led to a flight out of the U.S. dollar and Treasurys in recent weeks, with the dollar index weakening more than 9% so far this year. Market watchers see further declines.

According to Bank of America’s most recent Global Fund Manager Survey, a net 61% of participants anticipate a decline in the dollar’s value over the next 12 months — the most pessimistic outlook of major investors in almost 20 years. …

… For the remainder of the report:

4. ANDREW MAGUIRE PODCAST 219

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//ROLEX

END

6 CRYPTOCURRENCY NEWS

ASIA TRADING TUESDAY MORNING MONDAY NIGHT

SHANGHAI CLOSED UP 8.32 PTS OR 0.25%

//Hang Seng CLOSED UP 167.18 PTS OR 0.78%

// Nikkei CLOSED DOWN 59.32 OR 0.17%//Australia’s all ordinaries CLOSED UP 0.10%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.3135 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3161/ Oil UP TO 64.14 dollars per barrel for WTI and BRENT DOWN TO 67.06 Stocks in Europe OPENED ALL MIXED.

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

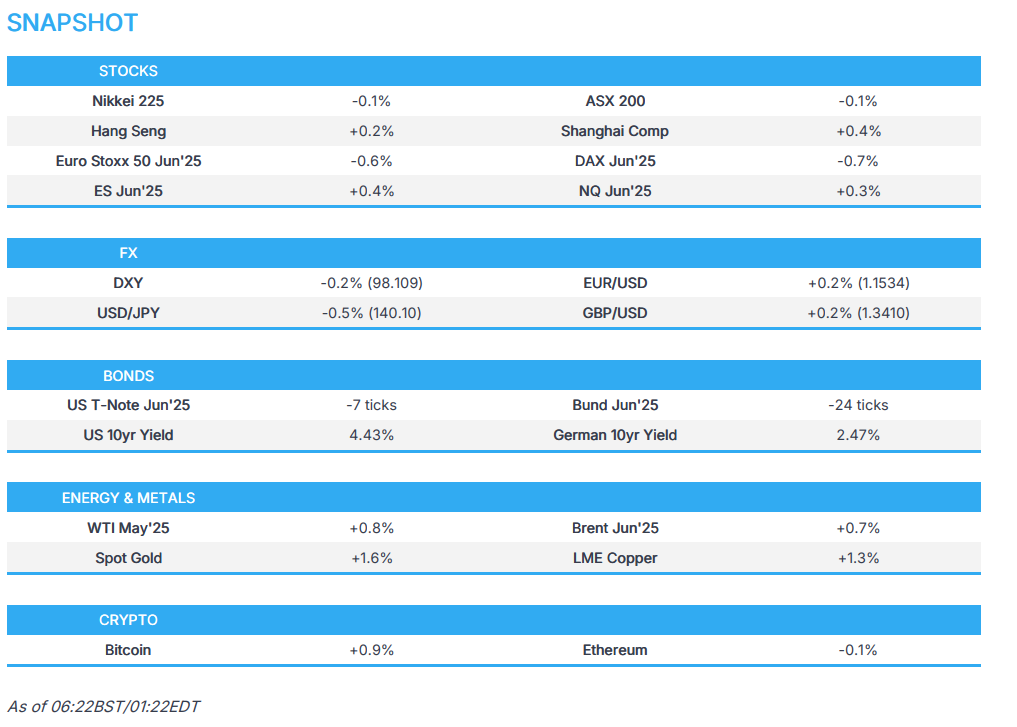

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.3135 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.3161 (CCP MANIPULATED)

SHANGHAI CLOSED CLOSED UP 8.32 PTS OR 0.25%

HANG SENG CLOSED CLOSED UP 167.18 PTS OR 0.78%

2. Nikkei closed DOWN 59.32 PTS OR 0.17%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 98.24// EURO FALLS TO 1.1491 DOWN 23 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.3135//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 140.33…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4560/Italian 10 Yr bond yield DOWN to 3.636 SPAIN 10 YR BOND YIELD DOWN TO 3.160

3i Greek 10 year bond yield DOWN TO 3.349

3j Gold at $3456.60 Silver at: 32.66 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN AND 28 /100 roubles/dollar; ROUBLE AT 81.31

3m oil into the 64 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 140.94// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.312% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8122 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9333 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.421 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.904 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.802 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.26

10 YR UK BOND YIELD: 4.6295 UP 6 PTS

10 YR CANADA BOND YIELD: 3.237 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.799 DOWN 1 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

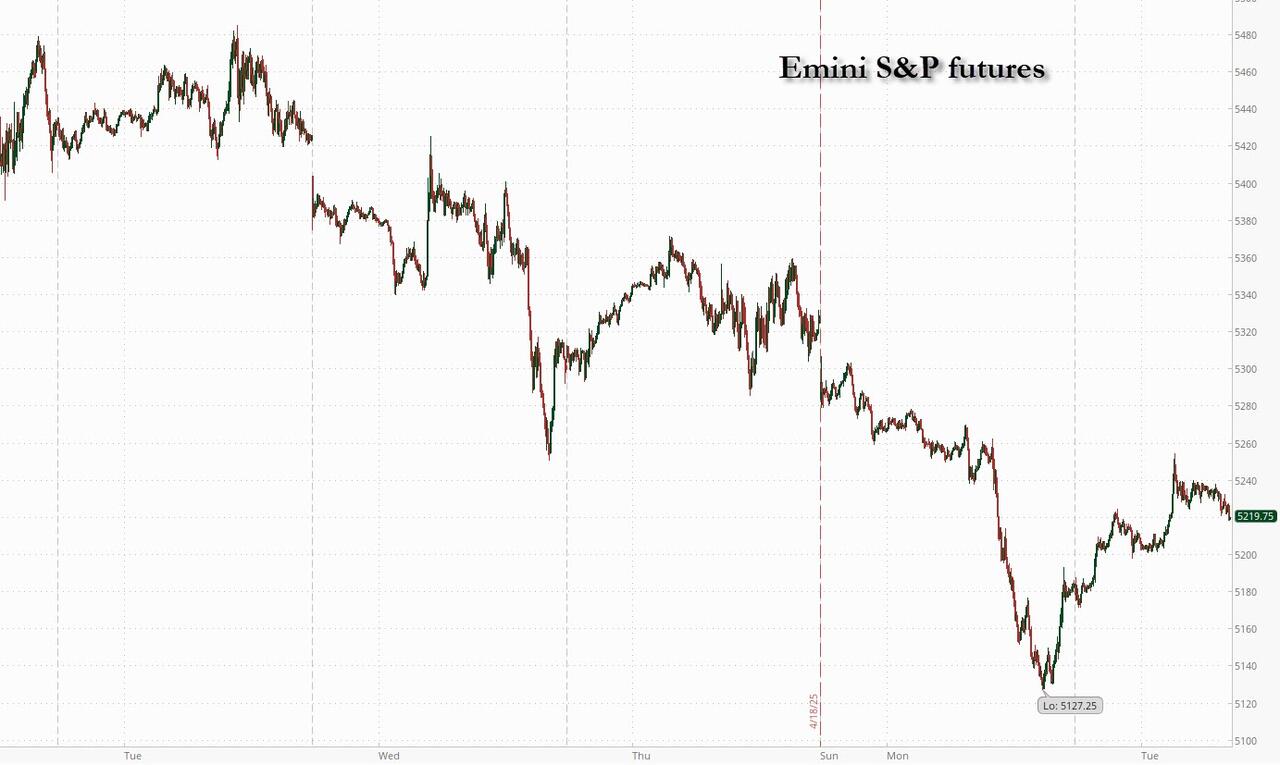

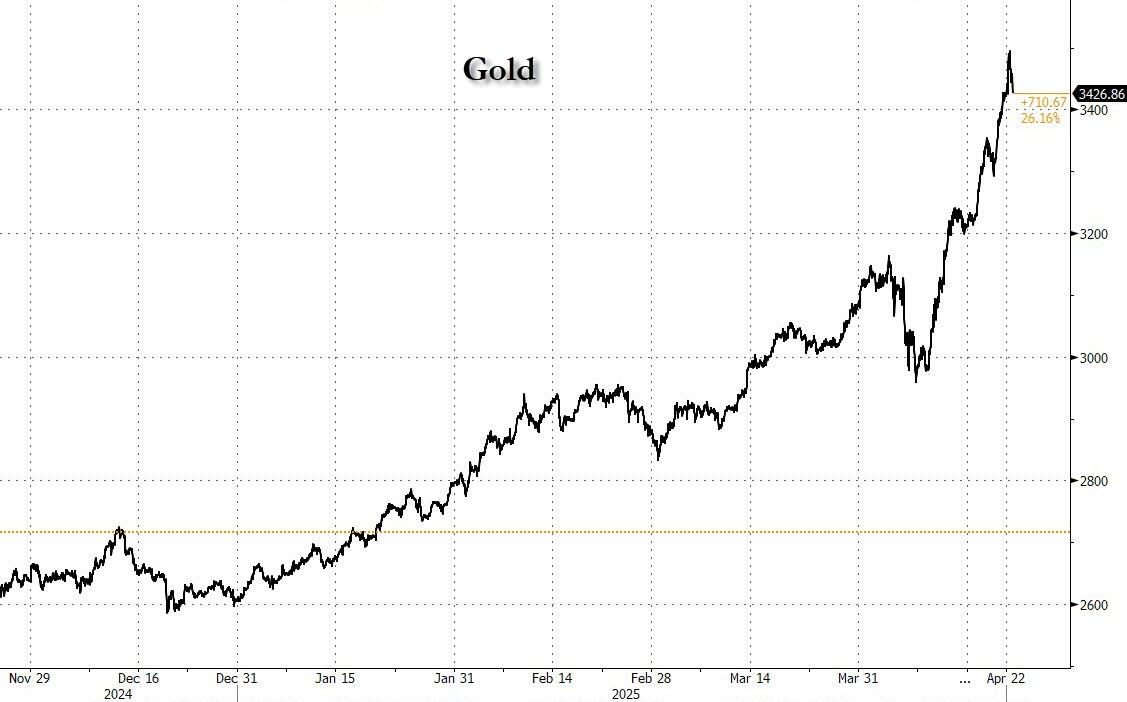

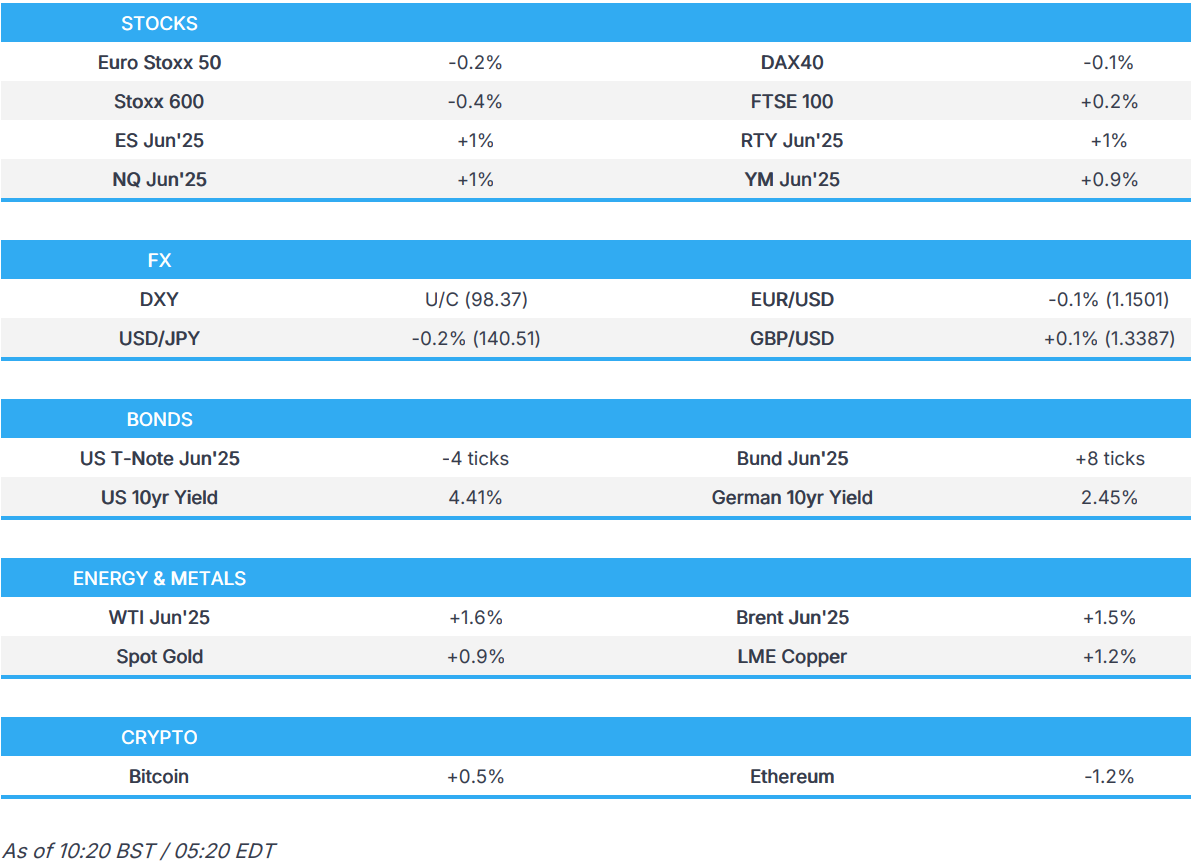

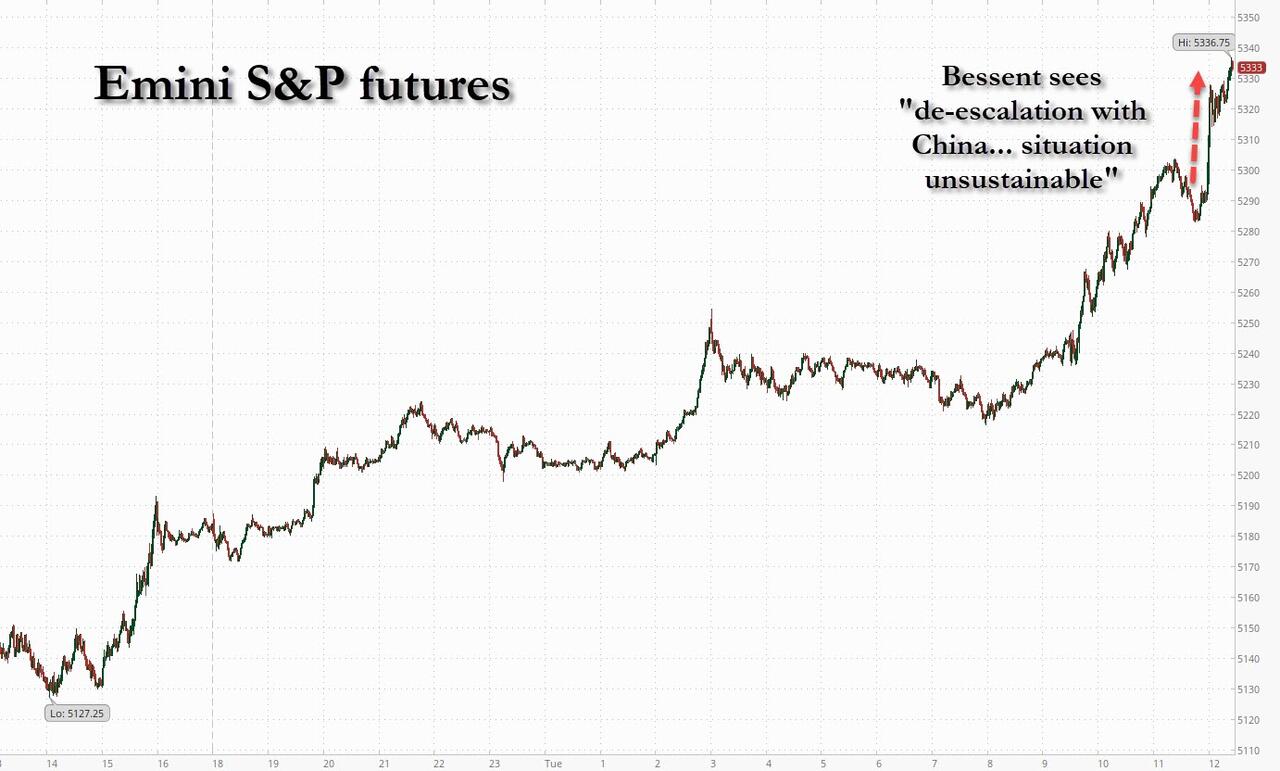

Futures Rebound On Trade Deal Optimism, Gold Hits Another Record

Tuesday, Apr 22, 2025 – 08:28 AM