APRIL 23/GOLD CLOSED DOWN $124.55 TO $3282.20 AS THE FED IS DESPERATE TO CLOSE THEIR HUGE SHORTFALL//SILVER CLOSED UP 65 CENTS TO $33.55/PLATINUM CLOSED UP $10.75 TO $973.65 WHILE PALLADIUM WAS DOWN $4.55 TO $934.50//IN GOLD NEWS SHANGHAI PLANS MULTIPLE WAREHOUSES IN FOREIGN JURISDICTIONS AND THAT WILL BE GOOD FOR OUR PHYSICAL HOLDERS OF GOLD/MORE TROUBLE FOR CHINA AS THEY CANNOT GET THEIR HANDS ON ETHANE AND THIS IS CRIPPLING THEIR PLASTICS INDUSTRY//EUROPEAN PMI’S FLOUNDER!//ISRAEL VS HAMAS UPDATES/HOUTHIS UPDATES//COVID UPDATES/VACCINE INJURY UPDATES/SLAY NEWS/DR PAUL ALEXANDER/MARK CRISPIN MILLER//REUTERS PUTS COLD WATER ON YESTERDAY’S FAKE NEWS ON TRUMP RELAXING CHINA TARIFFS/OTHER USA DATA RELEASES/BESSANT CALLS FOR REMOVAL OF GLOBAL IMBALANCES//SWAMP STORIES FOR YOU TONIGHT//

072 C GOLDMAN 29 190 H BMO CAPITAL MARKETS 1 323 C HSBC 4 363 H WELLS FARGO SECURITI 142 523 H INTERACTIVE BROKERS 2 624 H BOFA SECURITIES 156 661 C JP MORGAN SECURITIES 17 13 686 C STONEX FINANCIAL INC 5 23 690 C ABN AMRO CLR USA LLC 7 700 C UBS SECURITIES LLC 1 726 C PLUS500US FINANCIAL 1 737 C ADVANTAGE FUTURES 1 880 H CITIGROUP 414 905 C ADM 11 991 H CME 129

TOTAL: 478 478 MONTH TO DATE: 64,119

jpmorgan stopped: 13/478

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 478 NOTICES FOR 47,800 OZ 1.4867 TONNES

total notices so far: 64,119 contracts for 6,411,900 OR 199.43 tonnes)

FOR APRIL

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 0 NOTICE(S) FILED FOR 0.00 MILLION OZ/

total number of notices filed so far this month : 3097 CONTRACTS (NOTICES) for 15.485 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $134.55 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 947.70 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.65 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ////A MASSIVE 6.271 MILLION OZ OUT OF THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 447.70 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA HUGE SIZED 2486 CONTRACTS TO 146,923 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL GAIN OF $0.30 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 3236 TOTAL CONTRACTS AS THE CME NOTIFIED US OF A HUGE 750 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD A CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING TUESDAY AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON MONDAY WITH SILVER’S GAIN IN PRICE BUT THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH A HUGE T.A.S. ISSUANCE OF 692 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A HUGE 750 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 692 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY/WEDNESDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 3236 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR SMALL GAIN IN PRICE OF $0.30.

THE CME NOTIFIED US THAT WE HAD 0 CONTRACTS OF THOSE CRAZY EXCHANGE FOR RISK CONTRACTS ISSUED FOR 0 OZ (0 MILLION OZ). THESE EXCHANGE FOR RISKS ARE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THUS FOR THE MONTH OF APRIL WE HAVE A TOTAL OF 4.0 MILLION OZ OF EXCHANGE FOR RISK ISSUED ON TWO OCCASIONS. THE RECIPIENT OF THIS LARGESS IS PROBABLY THE CENTRAL BANK OF INDIA.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT/WEDNESDAY MORNING: A HUGE 692 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.30) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS DESPITE HAVING A SMALL GAIN IN PRICE, WE GAINED A MEGA HUGE 3520 CONTRACTS IN OPEN INTEREST FROM OUR TWO EXCHANGES.

WE HAD A HUGE 750 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.735 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP TO WHICH WE ADD OUR 4.00 MILLION OZ EX FOR RISK

STANDING FOR APRIL INCREASES TO 19.505 MILLION OZ

WE HAD:

/ HUGE COMEX OI GAIN+// A HUGE SIZED EFP ISSUANCE (750 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 692 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 284 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 18 DAYS, total 16,030 contracts: OR 80.150 MILLION OZ (890 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 80.150 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 80.150 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2486 CONTRACTS WITH OUR GAIN IN PRICE OF $0.30 IN SILVER PRICING AT THE COMEX// TUESDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE 750 CONTRACT EFP ISSUANCE CONTRACTS: 750 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A STRONG SILVER OZ STANDING FOR APRIL OF 15.505 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

NEW STANDING APRIL: 19.506 MILLION OZ

THE NEW TAS ISSUANCE MONDAY NIGHT (692 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE WEDNESDAY TRADING.

WE HAD 0 NOTICE(S) FILED TODAY FOR 0.000 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 974 OI CONTRACTS TO 465,351 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1432 CONTRACTS //.

WE HAD A SMALL SIZED DECREASE IN COMEX OI (974 CONTRACTS) . THIS OCCURRED WITH OUR LOSS OF $7.75 IN PRICE TUESDAY. ON WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES (CME CORRECTED// MAYBE?) TO WHICH WE ADD FOR APRIL ITS INITIAL 700 CONTRACT EXCHANGE FOR RISK FOR 70,000 OZ OR 2.177 TONNES AND FRIDAY APRIL 4: 250 CONTRACT ISSUANCE FOR .777 TONNES + MONDAY APRIL 7 NEW ISSUANCE OF .8709 TONNES/ + APRIL 9 ‘S TOTAL OF 484 EX. FOR RISK FOR 48,400 OZ OR 1.5054 TONNES/NEW TOTAL AND FINALLY APRIL 14 EX FOR RISK OF 30,000 OZ OR.6220 TONNES AND THEN TODAY APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES// ;NEW EX FOR RISK 7.776 TONNES TO WHICH WAS ADDED TO OUR NEW QUEUE JUMP OF 56 CONTRACTS OR 5600 OZ (0.1741 TONNES). THUS INITIAL STANDING FOR GOLD/APRIL DELIVERY MONTH IS 199.744 TONNES NORMAL DELIVERY(INCLUDES OF QUEUE JUMP) + 7.776 TONNES EX FOR RISK = 207.520 TONNES

/NEW STANDING FOR APRIL; 199.744 TONNES + 7.776 TONNES EX FOR RISK = 207.520 TONNES

/ ALL OF THIS HAPPENED WITH OUR $7.75 LOSS IN PRICE WITH RESPECT TO TUESDAY’S COMEX ///. WE HAD A STRONG SIZED GAIN OF 4113 OI CONTRACTS (12.793 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AND NOW FOR OUR FRONT MONTH OF APRIL. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS. WE HAVE A MASSIVE AMOUNT OF TONNES STANDING FOR GOLD IN APRIL.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5087 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 465,351

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4113 CONTRACTS WITH 974 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 5087 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4113 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A GOOD SIZED AND CRIMINAL 2079 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5087 CONTRACTS) ACCOMPANYING THE SMALL SIZED DECREASE IN COMEX OI OF 974 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 4113 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING AT THE GOLD COMEX FOR APRIL 199.744 TONNES (WHICH INCLUDES OUR 0.1174 TONNES QUEUE JUMP) AND THIS FOLLOWS TOTAL EXCHANGE FOR RISK ISSUANCE ON 6 OCCASIONS FOR 7.776 TONNES//NEW STANDING ADVANCES TO 207.520 TONNES.

//NEW STANDING APRIL: 199.744 TONNES + 7.776 TONNES EX FOR RISK ON 6 OCCASIONS = 207.520 TONNES

.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION + ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WE HAD: 1)A $7.75 COMEX PRICE LOSS AND WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG GAIN OF 4113 CONTRACTS ON OUR TWO EXCHANGES/./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN APRIL.

4) SMALL SIZED COMEX OI GAIN// 5) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (5087 CONTRACTS)///GOOD T.A.S. ISSUANCE: 2079 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 56,204 CONTRACTS OR 5,620,400 OZ OR 174.818 TONNES IN 18 TRADING DAY(S) AND THUS AVERAGING: 3122 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN18 TRADING DAY(S) IN TONNES 174.818 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 174.818 TONNES DIVIDED BY 3550 x 100% TONNES = 4.92% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 174.818 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 2486 CONTRACTS OI TO 146,923 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 750 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 750 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 750 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2486 CONTRACTS AND ADD TO THE 750 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3520 CONTRACTS WITH THE GAIN IN PRICE OF $0.30 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 16.180 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 3.40 PTS OR 0.10%

//Hang Seng CLOSED UP 510.30 PTS OR 2.37%

// Nikkei CLOSED UP 648.03 OR 1.89%//Australia’s all ordinaries CLOSED UP 1.39%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2893 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2874/ Oil UP TO 64.19 dollars per barrel for WTI and BRENT UP TO 68.02 Stocks in Europe OPENED ALL GREEN.

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED974 CONTRACTS TO 465,351 DESPITE OUR LOSS IN PRICE OF $7.75 WITH RESPECT TO TUESDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (5087 ).

THE CME ANNOUNCED TUESDAY NIGHT, A HUGE 600 EXCHANGE FOR RISK CONTRACTS FOR 60,000 OZ OR 1.866 TONNES. SO FAR THIS MONTH WE HAD RECORDED A NEW RECORD 6 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE FRONT MONTH OF APRIL STANDS AT 7.776 TONNES OF GOLD WHICH MUST BE ADDED TO OUR NORMAL GOLD DELVERIES.

HISTORY: LAST TWO PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.

DETAILS ON APRIL COMEX MONTH

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 4113 CONTRACTS DESPITE OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON WEDNESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF APRIL CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A BIT LARGER THAN FROM THE PAST FEW DAYS AT 2079 CONTRACTS

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 205 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 219 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1.2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF APRIL .… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 5087 EFP CONTRACTS WERE ISSUED: : /APRIL 5087 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5087 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 4113 CONTRACTS IN THAT 5087 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL LOSS OF 974 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $7.75 FOR TUESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. LOOKS LIKE THE SHORT RATS ARE FLEEING THE ARENA AS EVIDENCED BY THE LOWER OPEN INTEREST AT THE COMEX!

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A GOOD SIZED 2079 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S THESE PAST FEW MONTHS,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED NOTHING AS NOBODY LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND ,FOR MARCH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT WEDNESDAY MARCH 17, THE 38,393 T.A.S. CONTRACT ISSUANCE WAS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH AND APRIL.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH. WE HAVE YET TO EXPERIENCE A MEGA CONSECUTIVE 30,000 CONTRACT T.A.S FOR APRIL.

STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (207.520 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 4 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

STANDING FOR GOLD: 199.744 TONNES + 7.776 TONNES EX FOR RISK = 207.520 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 207.520 TONNES (INCLUDES 7.776 TONNES EX FOR RISK)

COMEX GOLD TRADING/APRIL CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A $7.75/ /)/BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION TUESDAY AS THEY WERE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,400 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS THEY SUCCEEDED IN THEIR ATTEMPT TO STOP THE PENETRATION OF OUR $3,400 DOLLAR GOLD BARRIER AS IT IS NOW TRADING WELL BELOW THAT AT $3292 PER OZ AS I WRITE THIS

TUESDAY NIGHT/WEDNESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /APRIL TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCE

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

NOW APRIL, ISSUES ITS 6TH EXCHANGE FOR RISK: 600 CONTRACTS OR 60,000 OZ OR 1.866 TONNES

SUMMARY EXCHANGE FOR RISK/APRIL//TOTAL ISSUANCES 6 FOR 7.776 TONNES OF GOLD!

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES//NEW TOTAL ISSUANCE FOR APRIL: 7.776 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WILL BE ADDED TO OUR NORMAL DELIVERY CYCLE.

STANDING FOR GOLD NOW FOR APRIL:

APRIL: 199.744 TONNES +(7.776 EX FOR RISK// FOR APRIL DELIVERY MONTH =207.525 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS APRIL DELIVERY MONTH AFTER FIRST DAY NOTICE;

WE HAVE GAINED A STRONG SIZED TOTAL OF 17.247 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL FIRST RECORDED AT 166.964 TONNES ON FIRST DAY NOTICE FOLLOWED BY 6 EXCHANGE FOR RISK CONTRACT ISSUANCES FOR 7.776 TONNES.

ALSO TODAY WE RECORD ANOTHER 56 CONTRACT QUEUE JUMP FOR 5600 OZ OR 0.1741 TONNES. WE MUST NOW ADD OUR 7.776 TONNES EXCHANGE FOR RISK TO OUR NEW NORMAL DELIVERY OF 199.744 TONNES AND THUS STANDING FOR GOLD FOR APRIL IS NOW 207.520 TONNES, THE 2ND HIGHEST EVER RECORDED!

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $7.75

WE HAD 1432 CONTRACTS REM,OVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 4113 CONTRACTS OR 411,300 0Z (12.793 TONNES)

3 entries a) Out of Brinks 110,134.684 oz b) Out of JPMorgan: 65,298.681 oz (2031 kilobars) c) Out of Loomis: 25,720.800 oz (800 kilobars)

total withdrawal: 201,154.165 oz or 6.26 tonnes_

Deposit to the Dealer Inventory in oz

0 ENTRIES

Deposits to the Customer Inventory, in oz

we have 1 customer entry

1 ENTRIES: 1 DEPOSIT

I) INTO Ashai 32,016.960 OZ

total weight DEPOSIT: 32,016.960oz or 0.995 tonnes

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

478 notice(s) 47,800 OZ 1.4867 TONNES

No of oz to be served (notices)

99 contracts 9900 OZ 0.3079 TONNES

Total monthly oz gold served (contracts) so far this month

64,119 notices 6,411,900 oz 199.43 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

TOTAL WEIGHT; 0 TONNES

xxxxxxxxxxxxxxxxxxxxx

we have 1 customer entries

we have 1 customer deposit entry

1 ENTRIES: 1 DEPOSIT

I) INTO Ashai 32,016.960 OZ

total weight DEPOSIT: 32,016.960oz or 0.995 tonnes

total deposit 32,016.960 OZ 0.995 tonnes

NIL

xxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:

3 entries a) Out of Brinks 110,134.684 oz b) Out of JPMorgan: 65,298.681 oz (2031 kilobars) c) Out of Loomis: 25,720.800 oz (800 kilobars)

total withdrawal: 201,154.165 oz or 6.26 tonnes_

adjustments: 2 dealer to customer

a) JPMorgan: 13,575.552 oz

ii) Malca: 96,453.000 oz (3,000 kilobars)

xxxxxxxxxxxxxxxxxx

AMOUNT OF GOLD STANDING FOR APRIL

THE FRONT MONTH OF APRIL HAD A LOSS OF 91 CONTRACTS TO STAND AT 577. WE HAD 147 CONTRACTS FILED YESTERDAY. THUS WE GAINED 56 CONTRACTS OR 5,600 OZ (.1741 TONNES) AS WE EXPERIENCED ANOTHER QUEUE JUMP WHERE THESE BOYS DESIRED TO TAKE PHYSICAL DELIVERY OVER HERE. THIS IS CENTRAL BANKERS STANDING FOR PHYSICAL GOLD. LAST FRIDAY’S QUEUE JUMP OF 6.1619 TONNES REPRESENTED THE HIGHEST EVER QUEUE JUMP IN COMEX HISTORY SURPASSING THE PREVIOUS HIGHEST RECORDED WAS AT 5.90 TONNES.

MAY LOST 6 CONTRACTS DOWN TO 6108 CONTRACTS. MAY BECOMES THE FRONT MONTH AND WE WILL ALSO EXPERIENCE A STRONG DELIVERY MONTH EVEN THOUGH IT IS AN OFF MONTH!

JUNE LOST 4313 CONTRACTS TO 350,351. JUNE WILL STILL BE A WHOPPER OF A DELIVERY MONTH

We had 478 contracts filed for today representing 47,800 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 17 notices issued from their client or customer account. The total of all issuance by all participants equate to 478 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 13 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL /2025. contract month, we take the total number of notices filed so far for the month (64,119 X 100 oz ) to which we add the difference between the open interest for the front month of APRIL (577 CONTRACTS) minus the number of notices served upon today (478 x 100 oz per contract) equals 6,421,800 OZ OR 199.744 TONNES

to which we add our 6 exchange for risk issuances for April of 7.776 tonnes

= 207.520 tonnes

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (64,119 x 100 oz +we add the difference for front month of APRIL (577 OI} minus the number of notices served upon today (478 x 100 oz) which equals 6,421,800 OZ OR 199.744 TONNES + 7.776 tonnes ex for risks = 207.520 tonnes

TOTAL COMEX GOLD STANDING FOR APRIL.: 207.520 TONNES WHICH IS HUGE FOR THIS ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL IS FOLLOWING SUIT..

JPMorgan has a total silver weight: 199.954million oz/496.891oz million or 40.22%

TOTAL REGISTERED SILVER: 159.627 MILLION OZ//.TOTAL REG + ELIGIBLE. 496.891Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2025 OI: 4 OPEN INTEREST CONTRACTS FOR A LOSS OF 44 CONTRACTS. WE HAD 45 NOTICES FILED ON TUESDAY SO WE GAINED 1 CONTRACT WHICH UNDERWENT A QUEUE JUMP OF 5,000 OZ AS THESE BOYS WERE NOT WILLING TO WAIT FOR DELIVERY OF SILVER OVER HERE SO THEY ARE TRYING TO TAKE DELIVERY AT ENGLAND .

MAY SAW A LOSS OF 4226 CONTRACTS DOWN TO 46,441 CONTRACTS. MAY BECOMES THE FRONT MONTH AND IT LOOKS LIKE WE WILL HAVE A DANDY AMOUNT OF SILVER STANDING THIS MONTH.

JUNE SAW A GAIN OF 222 CONTRACTS UP TO 2733 CONTRACTS.

JULY GAINED 6137 CONTRACTS UP TO 78,839

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or 0.000 MILLION oz

CONFIRMED volume; ON TUESDAY 122,139 mega t.a.s. release//

AND NOW APRIL DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 3097 X5,000 oz = 15.485 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (4) AND the number of notices served upon today (0 )x (5000 oz)

Thus the standings for silver for the APRIL 2025 contract month: (3097) Notices served so far) x 5000 oz + OI for the front month of APRIL(4) minus number of notices served upon today (0)x 5000 oz equals silver standing for the APRIL contract month equating to 15.505 MILLION OZ . WE MUST NOW ADD OUR 4.0 MILLION OZ EXCHANGE FOR RISK ISSUED ON MONDAY MARCH 31 AND TODAY APRIL 4/NEW STANDING DECREASES TO 19.505 MILLION OZ

New total standing: 19.505 million oz which is huge for this NON active delivery month of APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 159.627million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

GLD INVENTORY: 947.70 TONNES, TONIGHTS TOTAL

SILVER

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

Submitted by admin on Tue, 2025-04-22 16:14 Section: Daily Dispatches

From Reuters Tuesday, April 22, 2025

Canada’s Barrick Gold said today it will exit the Donlin gold Project in Alaska by selling its 50% stake to billionaire John Paulson and NovaGold Resources for up to $1.1 billion.

The Donlin Gold project is a proposed mine that holds roughly 39 million ounces of gold. It was jointly owned by Barrick Gold and NovaGold, holding a 50% stake each.

U.S.-listed shares of Barrick Gold were up 1.7% before the bell, which were also supported by higher prices of the bullion.

Paulson and NovaGold will acquire 80% and 20%, respectively, of Barrick Gold’s interest in the entity, for $1 billion in cash. …

Submitted by admin on Tue, 2025-04-22 14:01 Section: Daily Dispatches

By Amy Lv and Lewis Jackson Reuters Tuesday, April 22, 2025

BEIJING — China is considering setting up overseas warehouses to aid international settlement of specific products on the Shanghai Gold Exchange, its central bank said Monday.

Shanghai Gold Exchange will be supported to conduct cooperation with overseas exchanges to expand use of the yuan benchmark in the international market, the statement said.

The plan to further enhance cross-border financial services in Shanghai was jointly issued by four state agencies including the People’s Bank of China.

Although it did not specify which products would be subject to the plan, the Shanghai Gold Exchange mainly deals with trading of precious metals gold, silver, and platinum.

Beijing has long wanted to step up globalisation of some commodities to enhance its pricing power and international influence. …

Ross Beaty-backed Lumina Gold agrees to $581 million acquisition by China’s CMOC

Submitted by admin on Tue, 2025-04-22 12:45 Section: Daily Dispatches

By Niall McGee The Globe and Mail, Toronto Monday, April 21, 2025

Ross Beaty-backed Lumina Gold Corp. has agreed to be acquired by a subsidiary of China’s CMOC Group Ltd. for $581 million.

Vancouver-based Lumina is developing the Cangrejos gold project in Ecuador. In 2023 the company published an engineering study that showed the potential for a mine to produce 9.8 million ounces of gold, 7.8 million ounces of silver, and 1.1 billion pounds of copper over 26 years. The capital cost for the initial phase of the project was projected at US$925 million.

Well-known Canadian mining financier and philanthropist Beaty is Lumina’s biggest shareholder.

CMOC Singapore Pte. Ltd. is offering to pay $1.27 a share in cash to Lumina shareholders, a 41% premium to the stock’s closing price on Thursday. CMOC Group is a major global producer of molybdenum and tungsten in China, of copper and cobalt in the Democratic Republic of Congo, and of niobium and phosphate in Brazil.

CMOC is publicly traded, but one of its largest shareholders is Luoyang Mining Group, a state-controlled entity in China. …

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//COPPER

Breaking Down Copper Trade In Charts Amid Noisy Trade War, IMF Downgrade

Wednesday, Apr 23, 2025 – 05:45 AM

The ongoing trade war is poised to deliver a negative shock to US growth, prompting the International Monetary Fund to slash its 2025 forecast earlier Tuesday. This gloomier outlook has sharpened our focus on the once high-flying industrial metals market—now showing signs of weakness—particularly the copper market.

Goldman analyst Adam Gillard provided clients with a snapshot of current conditions in the copper market, highlighting tight physical supply in China and continued strength in domestic demand.

However, Gillard cautioned that ongoing global industrial production weakness and declining Chinese exports—driven by the deepening trade war—could tip the market into surplus.

The analyst outlined four micro data points on the copper markets for clients to better gauge sentiment:

1. US cathode imports: YTD imports from BL data 408k MT implying an “over-import” of ~100k MT vs market expectations of ~300k MT (by June). If this run rate continues LME should tighten despite the likely tariff related demand shock.

2. Scrap: US scrap spreads remain under pressure as rising discounts erode the CME premium (US scrap is priced off CMX). March exports unchanged sequentially despite ARB strength; we don’t have April export data yet but this will be key given lower US exports (FY production ~542k MT contained) were key to the bull thesis.

3. Chinese demand: Ostensibly strong; YTD demand +10% due to production strength (from increased smelter capacity), seasonally adjusted stock draws (in part due to tariff related tolling exports) and strong net imports (despite deeply negative SHFE / LME import arb). Think this figure inflated by SMM production numbers (base affect) but a strong number nonetheless.

4. Positioning: Although our CTA model is running close to max short LME net spec at 28k is above the Aug24 low of 16k, and China appear to be still be running long on Shanghai (due to strong domestic demand).

The question remains whether copper bulls like Kostas Bintas, Trafigura Group’s former co-head of metals and now with Mercuria Energy Group, and/or Carlyle Group’s Jeff Currie (former Goldman boss of commodities) are still bullish on the industrial metal—or if the trade war has delayed their thesis of much higher prices.

LME Copper…

. . .

END

6 CRYPTOCURRENCY NEWS

ASIA TRADING WEDNESDAY MORNING TUESDAY NIGHT

SHANGHAI CLOSED DOWN 3.40 PTS OR 0.10%

//Hang Seng CLOSED UP 510.30 PTS OR 2.37%

// Nikkei CLOSED UP 648.03 OR 1.89%//Australia’s all ordinaries CLOSED UP 1.39%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2893 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2874/ Oil UP TO 64.19 dollars per barrel for WTI and BRENT UP TO 68.02 Stocks in Europe OPENED ALL GREEN.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2894 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.2873 (CCP MANIPULATED)

SHANGHAI CLOSED CLOSED DOWN 3.40 PTS OR 0.10%

HANG SENG CLOSED CLOSED UP 510.30 PTS OR 2.37%

2. Nikkei closed UP 648.03 PTS OR 1.89%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 98.93// EURO RISES TO 1.1389 UP 35 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.331//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.01…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4660/Italian 10 Yr bond yield DOWN to 3.5696 SPAIN 10 YR BOND YIELD DOWN TO 3.160%

3i Greek 10 year bond yield DOWN TO 3.3229

3j Gold at $3335/35 Silver at: 32.97 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 46 /100 roubles/dollar; ROUBLE AT 82.97

3m oil into the 64 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.01// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.331% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8241 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9387 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.304 DOWN 8 BASIS PTS…

USA 30 YR BOND YIELD: 4.844 DOWN 14 BASIS PTS/

USA 2 YR BOND YIELD: 3.816 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.29

10 YR UK BOND YIELD: 4.537 DOWN 9 PTS

10 YR CANADA BOND YIELD: 3.155 DOWN 8 BASIS PTS

5 YR CANADA BOND YIELD: 2.754 DOWN 4 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

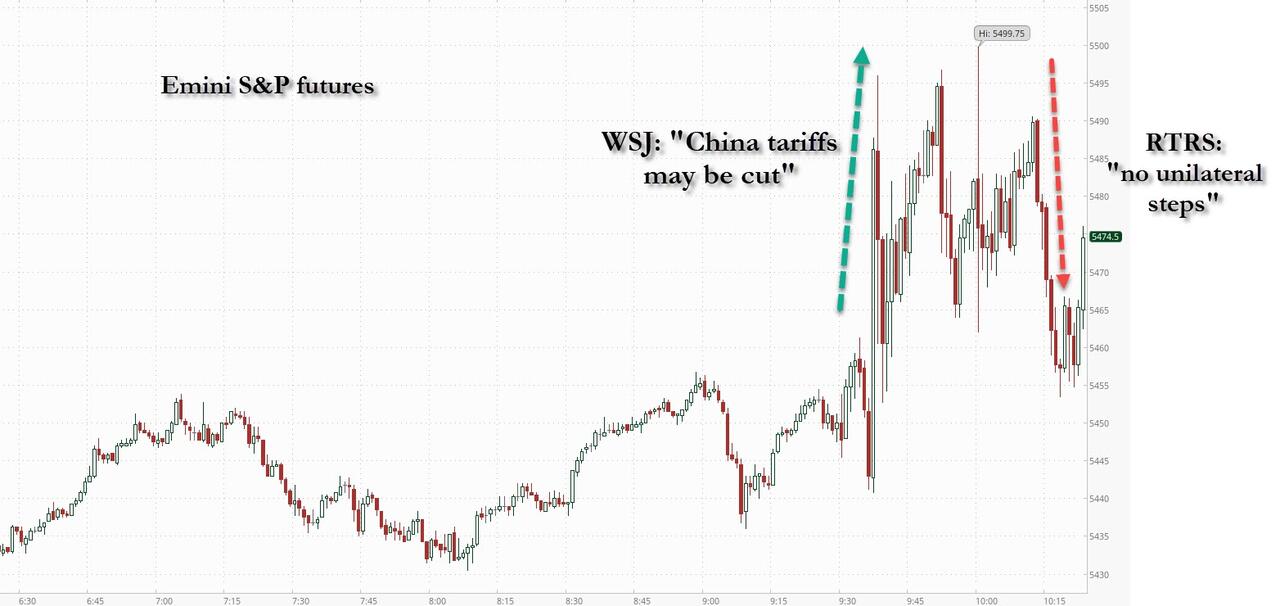

2a New York OPENING REPORT

Futures Surge After Trump Tones Down Rhetoric On China, POWELL

Wednesday, Apr 23, 2025 – 08:26 AM

US futures jumped and the dollar stabilized after president Trump said he has no intention of firing Powell, easing some fears on the Fed’s independence, while he also plans to be “very nice” to China in trade talks and sees China tariff coming down substantially which hinted a potential pivot in trade policy. As of 8:00am ET, S&P futures are up 2.3%, with Nasdaq futures surging 2.7%. Pre-market, Mag 7 names are all higher led by TSLA (+6.4%, after Musk said that his time on DOGE will significantly drop next month), NVDA (+4.9%), AMZN (+4.1%) and META (+3.7%). Intel rose 3% on reports it will cut more than 20% of its staff, a move aimed at eliminating bureaucracy. 10y TSY yields are down 10bps to 4.30% as longer-dated Treasuries rally, recovering from selling on concerns about the Fed’s continued independence; the USD reversed earlier gains. Commodities are mostly higher led by oil (+1.6%) and base metals; gold is 1.3% lower.

In premarket trading, Tesla led the Mag 7 stocks higher as CEO Elon Musk pledged to pull back from his work with the US government to concentrate on the electric-vehicle company (Tesla +7.4%, Alphabet +2.4%, Nvidia +5.7%, Amazon +5%, Apple +3.3%, Microsoft +2.6%, Meta +4.7%). Chip, cryptocurrency-linked stocks and US-listed Chinese companies rally after Trump said China tariffs will drop if the two countries can reach a deal. The president also said he had no intention of firing Powell. Semiconductors gained (SMCI +6.7%, Nvidia +5.7%, Dell +5.5%) as did Apple suppliers: (Qualcomm +2.6%, Broadcom +4.6%, Cirrus Logic +4.3%). Crypto-linked stocks jumped after bitcoin surged above $94,000 (Robinhood +8.1%, Coinbase +4.2%, MicroStrategy +3.4%). Here are some other notable movers:

AT&T gains 4% after adding 324,000 mobile-phone customers in the first quarter, beating Wall Street projections for 254,000.

Boston Scientific rises 6% after the medical device firm boosted its net sales and adjusted profit forecast for the full year.

Bristol-Myers Squibb falls 4.7% after the company’s treatment for schizophrenia failed in a study designed to expand its use, denting the company’s ambitions to turn it into a blockbuster.

Enphase Energy drops 11% after the solar equipment maker’s revenue forecast missed analyst estimates at the midpoint. Morgan Stanley downgrades the stock to underweight from equal-weight.

Intel rises 4% as the company is poised to announce plans this week to cut more than 20% of its staff, according to a person with knowledge of the matter.

Packaging drops 4.5% after the containerboard producer p gave a second-quarter earnings per share forecast that was below the average analyst estimate.

Pegasystems soars 26% after the customer relationship management software company reported first-quarter results that beat expectations.

Philip Morris climbs 3% after the tobacco company boosted its adjusted earnings per share guidance for the full year; the guidance beat the average analyst estimate.

Sportradar slips 3.6% after shareholders including an affiliate of the Canada Pension Plan Investment Board, an affiliate of Technology Crossover Ventures, and Sportradar CEO Carsten Koerl offered 23 million class A shares via Goldman Sachs, JPMorgan.

Vertiv Holdings advances 18% after the company boosted its net sales guidance for the full year.

XPeng ADRs jumps 8% after the Chinese electric vehicle maker unveiled a fast-charging variant of its P7+ sedan model at the 2025 Shanghai auto show.

Wall Street is set to build on the biggest equity gains in two weeks, with S&P 500 futures climbing 2.3% after Trump allayed fears that he plans to fire Federal Reserve Chair Jerome Powell. Optimism of easing US-China trade tensions added to the risk-on mood. Treasuries also rallied as worries about threats to Powell’s position faded: 10-year yields dropped ten basis points to 4.30%. A gauge of dollar strength steadied after rallying from a 16-month low. Bitcoin stormed above $90,000 for the first time since early March. Gold fell as demand for havens cooled. Oil extended its rebound.

Trump said Tuesday he had no intention of firing Powell, despite his frustration with the Fed not moving more quickly to lower borrowing costs. The president posted on social media last week that the Fed chair’s “termination cannot come fast enough!” His rebuke of the Fed and comments from officials that Trump was studying whether he could replace its chief had sent the dollar to the lowest level since December 2023.

Trump’s comments on the Fed chief late Tuesday are a walk-back from opinions expressed in the past week that sparked concerns about the US central bank’s independence. On the trade front, Trump and Treasury Secretary Scott Bessent said that a standoff with China can be de-escalated. On trade, Trump said he plans to be “very nice” to China in any talks and that tariffs will drop if the two countries can reach a deal. The US president also said that final tariffs on China wouldn’t be “anywhere near” the 145% level set.

Still, gains come with a warning from some on Wall Street of possible “head fakes,” given Trump’s unpredictability. Stock trading volumes were light on Tuesday, while the S&P 500 remains down about 7% since Trump’s “Liberation Day” tariffs. Some money managers, like Janus Henderson, are looking to cut exposure to the US.

“I took the view that the actual probability of Powell getting sacked was close to zero, but the tuning down of the rhetoric on China is clearly a relief,” said Francois Rimeu, a strategist at La Francaise AM in Paris.

“It’s really hard to see the endgame on trade,” said Rimeu at La Francaise AM. “Investors need to prepare in the event that say, in three months, we land with US tariffs that are manageable for the global economy.”

“If one is optimistic, one can take the view that Trump is slowly backing down on trade and on firing Powell,” said Gillles Guibout, head of European equities at AXA IM. “But he has a structural tendency to create uncertainty and now there’s a real defiance among international investors, and that’s palpable in the dollar.”

It’s also a busy day for earnings, with Boeing rising in premarket after first-quarter sales topped estimates. AT&T climbed after a strong first-quarter report. Philip Morris gained as its earnings forecast beat estimates. SAP soared the most in six years after profit at Europe’s most valuable company exceeded expectations.

In Europe, the Stoxx 600 rose 1.8%, led by gains in mining and technology shares. SAP soared as much as 11% after the German software firm reported profit and free cash flow that topped estimates; Reckitt Benckiser was the biggest laggard. Here are the biggest movers Wednesday:

SAP shares surge as much as 11% after the German software company reported a 29% growth in current cloud backlog on constant-currency terms, indicating resilient demand for its cloud-based software

BE Semiconductor soars as much as 10% after the Dutch firm said two leading memory chipmakers placed orders for its hybrid bonders, a chip-packaging technology used to connect chips and enhance their performance

Croda shares rise as much as 10%, their best one-day gain in 14 years, after the chemicals maker reported earnings and analysts pointed to a strong performance across divisions

Valmet shares rise as much as 9.6% after the supplier of tech and services to the pulp and paper industries reported higher order numbers than anticipated and reiterated its annual outlook

Babcock International shares rise as much as 6%, in sixth straight day of gains and hitting the highest level since July 2018, after the support services company released a pre-close update

Randstad shares rise as much as 6.2% after the Dutch staffing firm’s earnings beat estimates with a smaller-than-expected contraction in first-quarter organic revenue, with analysts pointing to stable trends

Akzo Nobel shares rise as much as 8.2% after the specialty chemicals firm posted first-quarter Ebitda that was ahead of consensus and reaffirmed its adjusted Ebitda forecast for the full year

Reckitt Benckiser shares drop as much as 4.7% after the personal care and homecare product maker delivered like-for-like growth below expectations following a miss in North America and Europe

European defense shares fall, with traders pointing to a Financial Times report that said Russian President Vladimir Putin has offered to halt his country’s invasion of Ukraine across the current front line

Temenos shares drop as much as 8.3%, the most since October, after reporting results that reflect a difficult start to the year and add risk to the company’s reiterated full-year forecasts

Hochschild Mining shares plunge as much as 17%, the most in over three months, after first-quarter production fell short of expectations. Analysts point to poor weather and challenges at the Mara Rosa mine

OVH Groupe slides as much as 11%, following two sessions of strong gains, after Morgan Stanley downgraded to underweight and said the cloud computing company’s valuation appears stretched

Earlier in the session, Asian stocks rallied after President Donald Trump’s administration indicated softer stances on trade with China and Jerome Powell’s tenure as Federal Reserve chair. The MSCI Asia Pacific Index rose as much as 1.9%, with TSMC and Alibaba among the biggest contributors. Benchmarks in Taiwan, Hong Kong and Japan led gains in the region. One by one, equity benchmarks in Asia are recouping losses suffered since Trump’s announcement of inceased tariffs on April 2. India, which has emerged as a relative safe haven amid the tariff war, was the first major global market to wipe out such declines last week. South Korea and Australia stock gauges did so on Wednesday, after Indonesia on Tuesday.

In FX, the Bloomberg Dollar Spot Index slipped 0.1%, wiping out an earlier 0.6% gain; the US currency fell versus all G-10 currencies bar the safe-haven yen and Swiss franc; the higher-risk Australian dollar rose, gained amid hopes of easing trade tensions between China and the US. The Swiss franc falls 0.2% and to the bottom of the G-10 FX pile while the yen weakens 0.1% against the greenback.

In rates, treasuries rose with 30-year yield falling nearly 15bp to week’s low 4.73%; 10-year yields declined 10bp to 4.30% while short-end tenors were little changed, leaving curve spreads dramatically flatter. US session includes 5-year note auction and several Fed speakers. German bonds drop, led by short-term debt, despite downbeat euro-area PMI data. The UK gilt curve flattens as long-end bonds rally following the DMO’s shift in bond sales further away from long maturities, narrowing the 2s30s spread by 12bps. while 2-year yields was little changed, leaving 2s10s and 5s30s curves nearly 10bp flatter on the day. Treasury auction cycle continues with $70 billion 5-year notes sale at 1pm New York time; Tuesday’s 2-year tailed by 0.6bp. WI 5-year yield near 3.955% is about 14.5bp richer than last month’s auction, which tailed by 0.5bp. This week’s cycle concludes Thursday with $44 billion 7-year note sale

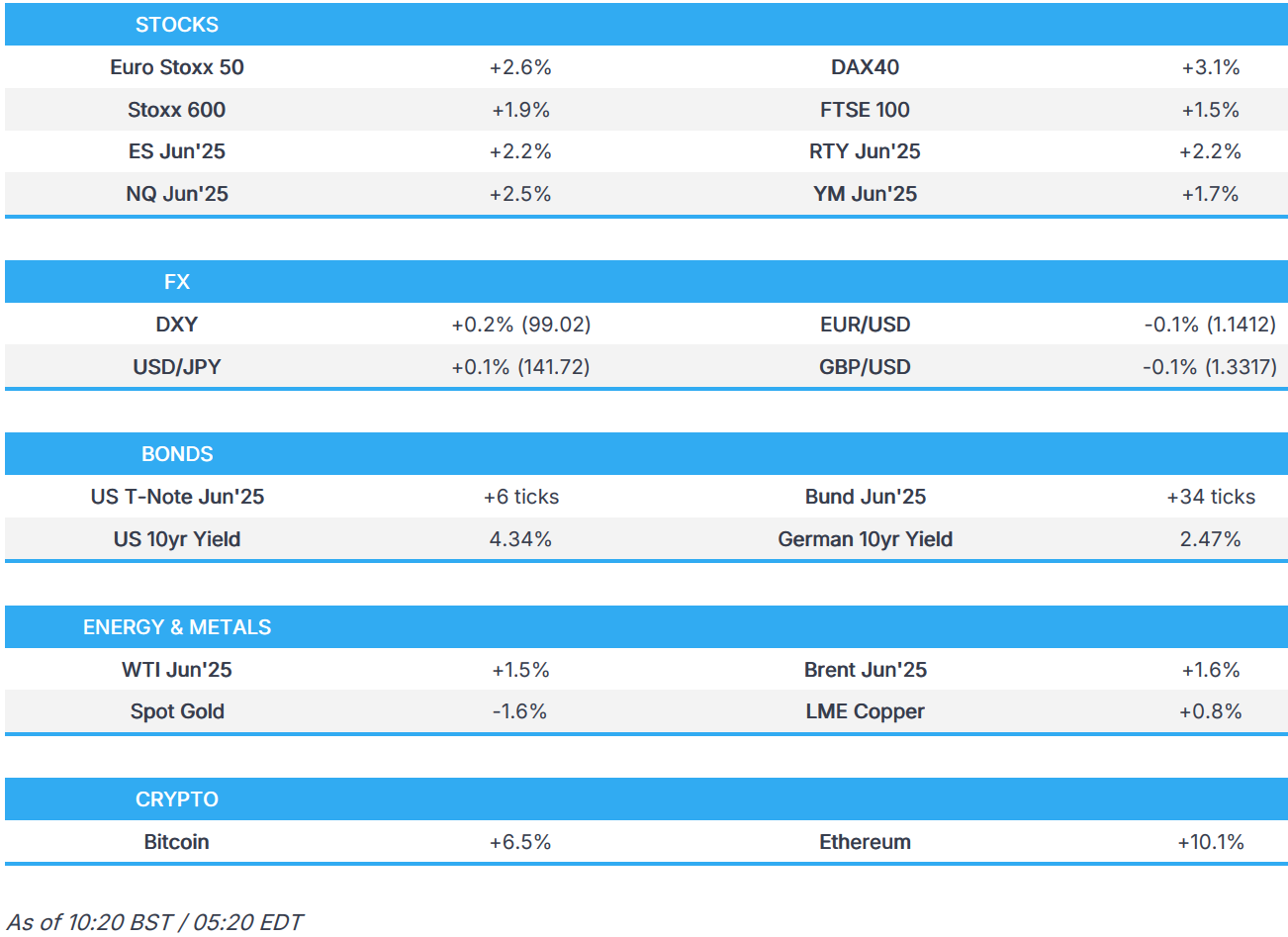

In commodities, spot gold tumbles $47 to $3,334/oz as haven demand ebbs. Oil prices advance, with WTI rising 1.6% to $64.70 a barrel. Bitcoin jumps over 3% and above $94,000.

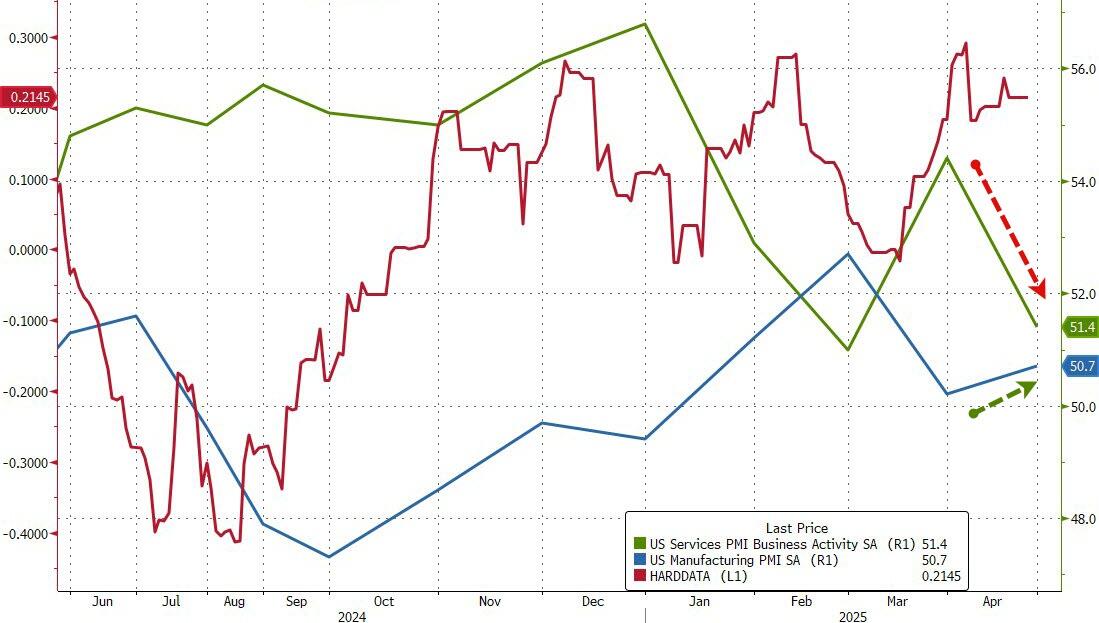

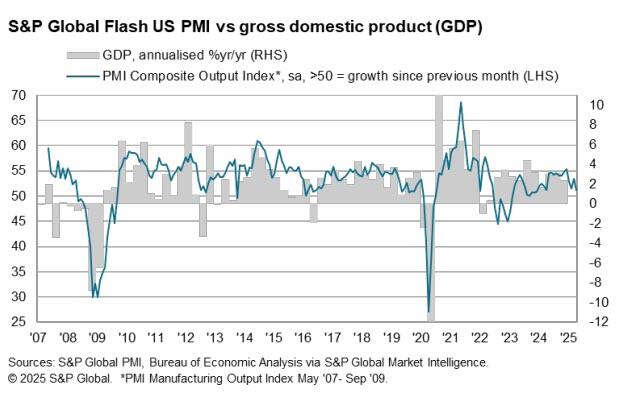

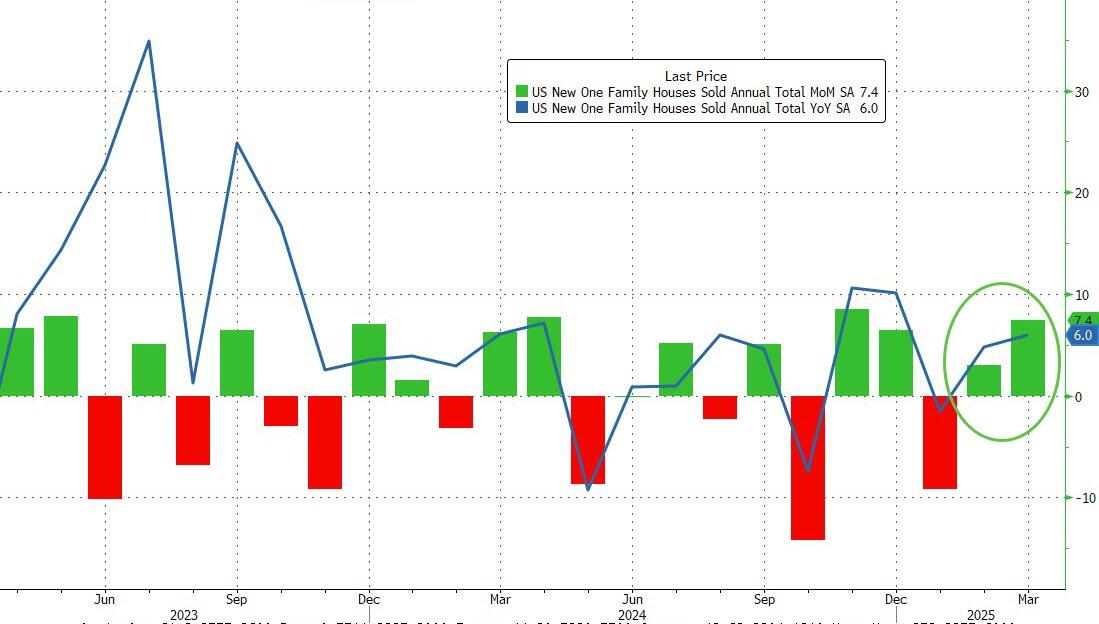

Today’s econ calendar includes April S&P Global manufacturing PMI (9:45am) and March new home sales (10am). Fed releases latest Beige book at 2pm. Fed speaker slate includes Goolsbee (9am), Musalem (9:30am, 2:35pm), Waller (9:35am) and Hammack (6:30pm)

Market Snapshot

S&P 500 mini +2.1%

Nasdaq 100 mini +2.5%

Russell 2000 mini +2.1%

Stoxx Europe 600 +1.8%

DAX +2.9%, CAC 40 +2.4%

10-year Treasury yield -6 basis points at 4.34%

VIX -2.3 points at 28.31

Bloomberg Dollar Index little changed at 1221.89

euro -0.2% at $1.14

WTI crude +1.8% at $64.8/barrel

Top Overnight News

President Trump said he is not planning to fire Federal Reserve Chairman Jerome Powell prompting some relief from investors who had been spooked by the White House’s commentary towards the Fed in recent weeks. WSJ

Trump suggested tariffs on China may be “substantially” cut if a deal is reached. China said the door was “wide open” for talks. BBG

Tesla shares climbed (+6% premkt) premarket despite an earnings miss after Elon Musk said he’ll pull back “significantly” from DOGE in May. BBG

JD Vance said the US has issued a “very explicit proposal” to Russia and Ukraine on a path forward to a peace deal and that territory concessions are needed.

Fed’s Kugler (voter) said tariff increases are significantly larger than previously expected and economic effects of tariffs and uncertainty will likely be larger than anticipated. Kugler added that Fed policy is well-positioned for macroeconomic changes and she supports holding the policy rate steady as long as upside risks to inflation continue, whilst economic activity and employment remain stable.

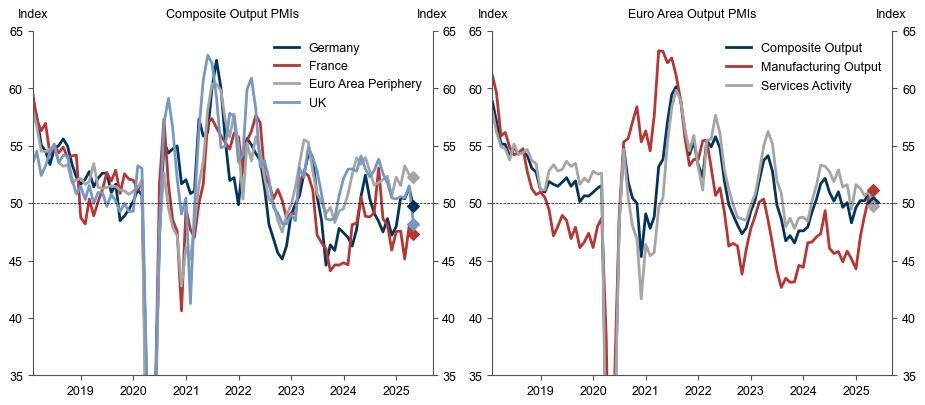

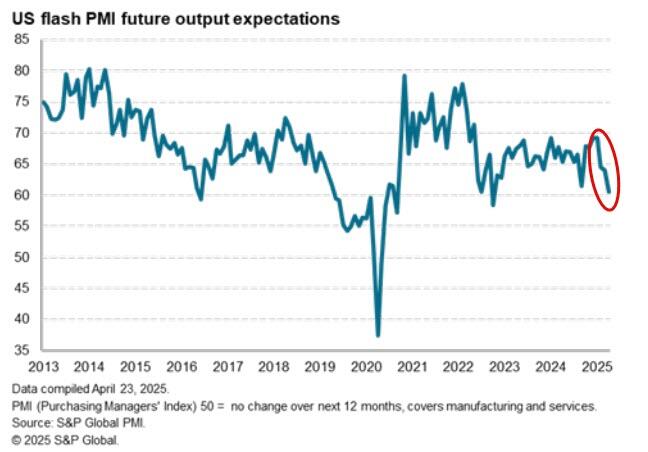

Trade war is starting to slam Europe’s economy. The euro-area’s flash composite PMI gauge fell more than expected this month to 50.1, as both the German and French measures missed. The UK gauge also fell more than estimated. BBG

Talks between the U.S., Ukraine and European officials to discuss ending Russia’s war in Ukraine faltered on Wednesday as U.S. Secretary of State Marco Rubio abruptly cancelled his trip to London and negotiations were downgraded. Rubio’s no show prompted a broader meeting of foreign ministers from Ukraine, Britain, France and Germany to be cancelled, although talks continued at a lower level. RTRS

UK government borrowing exceeded official forecasts made just last month. The budget deficit in the full fiscal year through March was £151.9 billion, above the OBR’s £137.3 billion projection. BBG

The US wants the UK to lower levies and other non-tariff barriers on a variety of US goods, including a reduction in its automotive tariff from 10% to 2.5%, the WSJ reported. Chancellor Rachel Reeves will meet Treasury Secretary Scott Bessent this week. BBG

Tariffs/Trade

“China: Door wide open for trade talks with US”, according to Sky News Arabia

US President Trump said they are doing fine with China and are going to be very nice with China, while he added that they have to make a deal and if they don’t, the US will set a deal. Trump also stated the tariff on China will not be as high as 145% and will not be anywhere near that level but it won’t be zero.

US is preparing negotiating terms for UK trade talks and will aim for the UK to reduce its automotive tariff from 10% to 2.5%, while the US will also push the UK to relax rules on agricultural imports from the US, including beef and revise rules of origin for goods from each nation, according to Wall Street Journal citing sources.

A more detailed look at global markets courtesy of Newsquawk

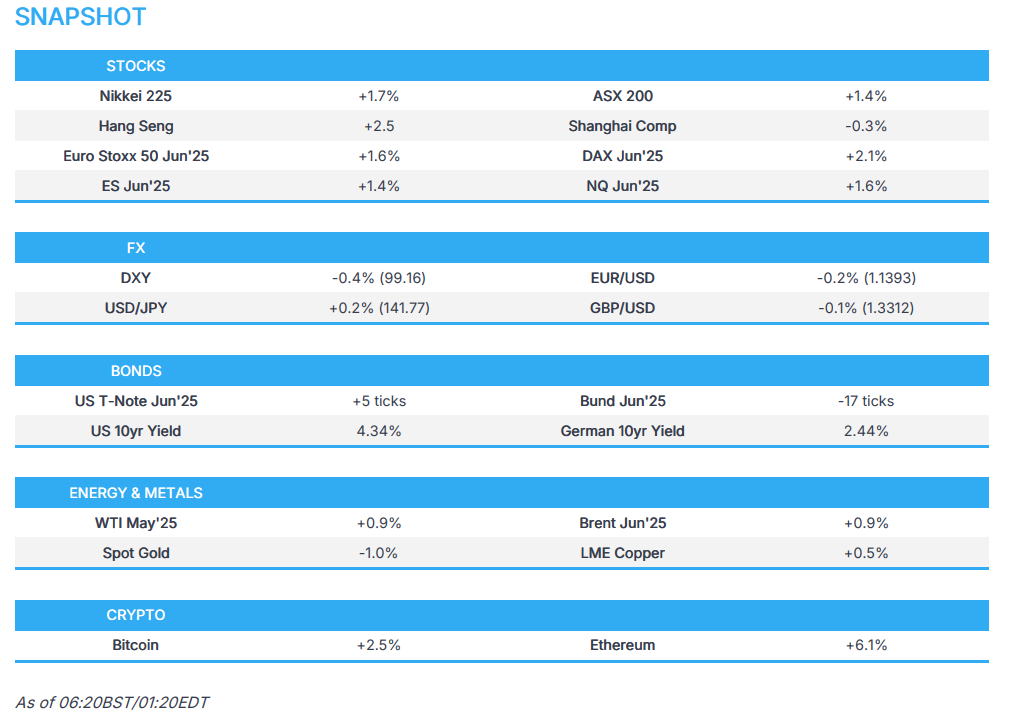

APAC stocks rallied amid tailwinds from the US owing to trade deal hopes and after US President Trump softened his rhetoric on Fed Chair Powell in which he stated he has no intention of firing the Fed chair. ASX 200 was led higher by outperformance in energy and tech with the former supported by a rebound in oil prices and after a quarterly production update from Woodside Energy, while gold miners suffered after the precious metal dropped as the risk-on mood sapped haven demand. Nikkei 225 benefitted from initial currency weakness and briefly surged to above the 35,000 level shortly after the open before fading some of its advances. Hang Seng and Shanghai Comp were varied as the Hong Kong benchmark joined in on the broad rally and the mainland was contained despite the encouraging comments from Treasury Secretary Bessent who noted the tariff standoff with China is unsustainable and expects the situation to de-escalate, while President Trump said they are going to be very nice with China and that the tariff on China will not be anywhere near the 145% level.

Top Asian News

Chinese Foreign Ministry said the US cannot say that it wishes to reach an agreement whilst on the other hand maintaining extreme pressure; this is not the correct way to deal with China.