APRIL 24/GOLD CLOSED UP $54.90 TO $3337.10 WHILE SILVER WAS DOWN A TINY ONE CENT TO $33.54//PLATINUM WAS UP $2.55 TO $976.20 WHILE PPALLADIUMW AS UP $18.10TO $952.60//A GOOD COMMODITY REPORT ON COPPER//BIG TROUBLE AGAIN BETWEEN INDIA AND PAKISTAN AFTER 26 TOURISTS WERE MURDERED: INDIA IS THREATENING TO CUT OFF WATER SUPPLIES TO BADLY NEEDED PAKISTAN//TROUBLES PERSIST BETWEEN CHINA AND USA RE TARIFFS AND WE HAVE A MUST MUST READ ARTICLE ON CHINESE DEMISE WITH THE TARIFFS////ISRAEL VS HAMAS UPDATES/SYRIA VS ISRAEL UPDATES//RUSSIA VS UKRAINE: RUSSIA POUNDS KIEV LAST NIGHT//COVID UPDATES/VACCINE INJURY REPORTS RE ROBT KENNEDY/DR PAUL ALEXANDER/SLAY NEWS, EVOL NEWS/NEWS ADDICTS/ KEY COMMENTARY TONIGHT FROM MICHAEL EVERY//USA DATA RELEASES//SWAMP STORIES FOR YOU TONIGHT//

363 H WELLS FARGO SECURITI 111 435 H SCOTIA CAPITAL (USA) 5 661 C JP MORGAN SECURITIES 100 686 C STONEX FINANCIAL INC 23 20 690 C ABN AMRO CLR USA LLC 7 709 C BARCLAYS 7 905 C ADM 12 991 H CME 13

TOTAL: 149 149 MONTH TO DATE: 64,268

MONTH TO DATE: 64,119

jpmorgan stopped: 0/149

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 149 NOTICES FOR 14,900 OZ 0.4634 TONNES

total notices so far: 64,268 contracts for 6,426,800 OR 199.90 tonnes)

FOR APRIL

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 0 NOTICE(S) FILED FOR 0.00 MILLION OZ/

total number of notices filed so far this month : 3097 CONTRACTS (NOTICES) for 15.485 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $54.90 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 949.14 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.01 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ////A MASSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 452.471 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA MEGA HUGE SIZED 6806 CONTRACTS TO 153,729 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG GAIN OF $0.61 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A MEGA MAMMOTH SIZED GAIN OF 8,479 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE 1673 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD A CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING WEDNESDAY AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON WEDNESDAY WITH SILVER’S GAIN IN PRICE BUT THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH A HUGE T.A.S. ISSUANCE OF 774 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A HUGE 1673 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 774 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUGE SIZED 8479 CONTRACTS ON OUR TWO EXCHANGES WITH OUR STRONG GAIN IN PRICE OF $0.61.

THE CME NOTIFIED US THAT WE HAD 0 CONTRACTS OF THOSE CRAZY EXCHANGE FOR RISK CONTRACTS ISSUED FOR 0 OZ (0 MILLION OZ). THESE EXCHANGE FOR RISKS ARE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THUS FOR THE MONTH OF APRIL WE HAVE A TOTAL OF 4.0 MILLION OZ OF EXCHANGE FOR RISK ISSUED ON TWO OCCASIONS. THE RECIPIENT OF THIS LARGESS IS PROBABLY THE CENTRAL BANK OF INDIA.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE 774 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.65) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A STRONG GAIN IN PRICE, AND WE GAINED A MEGA HUGE 8479 CONTRACTS IN OPEN INTEREST FROM OUR TWO EXCHANGES.

WE HAD A HUGE 1673 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.735 MILLION OZ FOLLOWED BY TODAY’S 170,000 OZ QUEUE JUMP TO WHICH WE ADD OUR 4.00 MILLION OZ EX FOR RISK

STANDING FOR APRIL INCREASES TO 19.655 MILLION OZ

WE HAD:

/ HUGE COMEX OI GAIN+// A HUGE SIZED EFP ISSUANCE (1673 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 774 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 417 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 19 DAYS, total 17,703 contracts: OR 88.515 MILLION OZ (932 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 88.515 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 88.515 MILLION OZ///

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6678 CONTRACTS WITH OUR GAIN IN PRICE OF $0.65 IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE 1673 CONTRACT EFP ISSUANCE CONTRACTS: 1673 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A STRONG SILVER OZ STANDING FOR APRIL OF 15.655 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

NEW STANDING APRIL: 19.655 MILLION OZ

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (774 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE WEDNESDAY TRADING.

WE HAD 32 NOTICE(S) FILED TODAY FOR 0.160 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6678 OI CONTRACTS TO 458,673 AND FURTHER FROM TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 2566 CONTRACTS //.

WE HAD A STRONG SIZED DECREASE IN COMEX OI (6678 CONTRACTS) . THIS OCCURRED WITH OUR HUGE LOSS OF $124.55 IN PRICE WEDNESDAY. LAST WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES (CME CORRECTED// MAYBE?) TO WHICH WE ADD FOR APRIL ITS INITIAL 700 CONTRACT EXCHANGE FOR RISK FOR 70,000 OZ OR 2.177 TONNES AND FRIDAY APRIL 4: 250 CONTRACT ISSUANCE FOR .777 TONNES + MONDAY APRIL 7 NEW ISSUANCE OF .8709 TONNES/ + APRIL 9 ‘S TOTAL OF 484 EX. FOR RISK FOR 48,400 OZ OR 1.5054 TONNES/NEW TOTAL AND FINALLY APRIL 14 EX FOR RISK OF 30,000 OZ OR.6220 TONNES AND THEN TODAY APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES// ;NEW EX FOR RISK 7.776 TONNES TO WHICH WAS ADDED TO OUR NEW QUEUE JUMP OF 131 CONTRACTS OR 13,100 OZ (0.4070 TONNES). THUS STANDING FOR GOLD/APRIL DELIVERY MONTH IS 200.152 TONNES NORMAL DELIVERY(INCLUDES OF QUEUE JUMP) + 7.776 TONNES EX FOR RISK = 207.926 TONNES

/NEW STANDING FOR APRIL; 200.152 TONNES + 7.776 TONNES EX FOR RISK = 207.926 TONNES

/ ALL OF THIS HAPPENED WITH OUR $124.55 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX ///. WE HAD A FAIR SIZED LOSS OF 2549 OI CONTRACTS (7.92 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AND NOW FOR OUR FRONT MONTH OF APRIL. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS. WE HAVE A MASSIVE AMOUNT OF TONNES STANDING FOR GOLD IN APRIL.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4179 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 458,673//NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2549 CONTRACTS WITH 6678 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4129 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2549 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED AND CRIMINAL 2934 CONTRACTS ISSUED.ALL OF THE LOSS IN OI COMEX AND TOTAL WAS DUE TO T.A.S. LIQUIDATION!~

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4179 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 6678 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 2549 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING AT THE GOLD COMEX FOR APRIL 200.152 TONNES (WHICH INCLUDES OUR 0.4070 TONNES QUEUE JUMP) AND THIS FOLLOWS TOTAL EXCHANGE FOR RISK ISSUANCE ON 6 OCCASIONS FOR 7.776 TONNES//NEW STANDING ADVANCES TO 207.926 TONNES.

//NEW STANDING APRIL: 200.152 TONNES + 7.776 TONNES EX FOR RISK ON 6 OCCASIONS = 207.926 TONNES

.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION + ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS DESPITE HAVING: 1)A $124.55 COMEX PRICE LOSS WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A SMALL LOSS OF 2549 CONTRACTS ON OUR TWO EXCHANGES ALL OF IT DUE TO T.A.S. LIQUIDATION DURING THE RAID/./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN APRIL.

4) STRONG SIZED COMEX OI LOSS// 5) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (4129 CONTRACTS)///GOOD T.A.S. ISSUANCE: 2934 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 60,333 CONTRACTS OR 6,033,300 OZ OR 187.66 TONNES IN 19 TRADING DAY(S) AND THUS AVERAGING: 3175 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN19 TRADING DAY(S) IN TONNES 187.66 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 187.66 TONNES DIVIDED BY 3550 x 100% TONNES = 5.28% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 187.66 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 6806 CONTRACTS OI TO 153,729 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1673 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1673 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1673 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 6806 CONTRACTS AND ADD TO THE 1673 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 8479 CONTRACTS WITH THE GAIN IN PRICE OF $0.61 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 42.395 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 0.93 PTS OR 0.03%

//Hang Seng CLOSED DOWN 162.86 PTS OR 0.74%

// Nikkei CLOSED UP 170.52 OR 0.49%//Australia’s all ordinaries CLOSED UP 0.61%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2895 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2887/ Oil DOWN TO 63.00 dollars per barrel for WTI and BRENT DOWN TO 66.70 Stocks in Europe OPENED MOSTLY ALL RED.

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED6678 CONTRACTS TO 458,673 DESPITE OUR MAMMOTH LOSS IN PRICE OF $124.55 WITH RESPECT TO WEDNESDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4127 ).

THE CME ANNOUNCED WEDNESDAY NIGHT, A ZER0 EXCHANGE FOR RISK CONTRACTS FOR NIL OZ OR NIL TONNES. SO FAR THIS MONTH WE HAD RECORDED A NEW RECORD 6 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE FRONT MONTH OF APRIL STANDS AT 7.776 TONNES OF GOLD WHICH MUST BE ADDED TO OUR NORMAL GOLD DELVERIES.

HISTORY: LAST TWO PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.

DETAILS ON APRIL COMEX MONTH

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 2549 CONTRACTS DESPITE OUR MAMMOTH LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON WEDNESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF APRIL CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A LOT LARGER THAN FROM THE PAST FEW DAYS AT 2934 CONTRACTS

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 207 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 219 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1.2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF APRIL .… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4129 EFP CONTRACTS WERE ISSUED: : /APRIL 4129 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4129 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 17 CONTRACTS IN THAT 4129 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 6678 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR MAMMOTH LOSS IN PRICE OF $124.55 FOR WEDNESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. LOOKS LIKE THE SHORT RATS ARE FLEEING THE ARENA AS EVIDENCED BY THE LOWER OPEN INTEREST AT THE COMEX!

T.A.S. ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A GOOD SIZED 2934 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S THESE PAST FEW MONTHS,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED NOTHING AS NOBODY LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND ,FOR MARCH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT WEDNESDAY MARCH 17, THE 38,393 T.A.S. CONTRACT ISSUANCE WAS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH AND APRIL.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH. WE HAVE YET TO EXPERIENCE A MEGA CONSECUTIVE 30,000 CONTRACT T.A.S FOR APRIL.

STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (207.926 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 4 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

STANDING FOR GOLD: 200.152 TONNES + 7.776 TONNES EX FOR RISK = 207.926 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 207.926 TONNES (INCLUDES 7.776 TONNES EX FOR RISK)

COMEX GOLD TRADING/APRIL CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $124.55/ /)/AND SURPRISINGLY THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A SMALL SIZED LOSS IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION WEDNESDAY AS THEY WERE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,400 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS THEY SUCCEEDED IN THEIR ATTEMPT TO STOP THE PENETRATION OF OUR $3,400 DOLLAR GOLD BARRIER AS IT IS NOW TRADING WELL BELOW THAT AT $3318 PER OZ AS I WRITE THIS. ALL OF THE LOSS IN OI WAS DUE TO T.A.S. LIQUIDATION

WEDNESDAY NIGHT/THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /APRIL TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCE

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

NOW APRIL, ISSUES ITS 6TH EXCHANGE FOR RISK: 600 CONTRACTS OR 60,000 OZ OR 1.866 TONNES

SUMMARY EXCHANGE FOR RISK/APRIL//TOTAL ISSUANCES 6 FOR 7.776 TONNES OF GOLD!

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES//NEW TOTAL ISSUANCE FOR APRIL: 7.776 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WILL BE ADDED TO OUR NORMAL DELIVERY CYCLE.

STANDING FOR GOLD NOW FOR APRIL:

APRIL: 200.152 TONNES +(7.776 EX FOR RISK// FOR APRIL DELIVERY MONTH =207.926 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS APRIL DELIVERY MONTH AFTER FIRST DAY NOTICE;

WE HAVE GAINED A TINY SIZED TOTAL OF 0.05 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL FIRST RECORDED AT 166.964 TONNES ON FIRST DAY NOTICE FOLLOWED BY 6 EXCHANGE FOR RISK CONTRACT ISSUANCES FOR 7.776 TONNES.

ALSO TODAY WE RECORD ANOTHER 131 CONTRACT QUEUE JUMP FOR 13100 OZ OR 0.4070 TONNES. WE MUST NOW ADD OUR 7.776 TONNES EXCHANGE FOR RISK TO OUR NEW NORMAL DELIVERY OF 200.152 TONNES AND THUS STANDING FOR GOLD FOR APRIL IS NOW 207.926 TONNES, THE 2ND HIGHEST EVER RECORDED!

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $124.55

WE HAD 2566 CONTRACTS REM,OVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 2549 CONTRACTS OR 254,900 0Z (7.92 TONNES)

2 entries a) Out of Brinks 546,567.000 oz (17,000 kilobars) b) Out of JPMorgan enhanced: 137,669.900 oz (344 London good delivery bars)

total withdrawal: 684,236.900

Deposit to the Dealer Inventory in oz

0 ENTRIES

Deposits to the Customer Inventory, in oz

we have 0 customer entries

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

149 notice(s) 14900 OZ 0.4634 TONNES

No of oz to be served (notices)

81 contracts 8100 OZ 0.2519 TONNES

Total monthly oz gold served (contracts) so far this month

64,268 notices 6,426,800 oz 199.90 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

TOTAL WEIGHT; 0 TONNES

xxxxxxxxxxxxxxxxxxxxx

we have 0 customer entries

we have 0 customer deposit entry

0 ENTRIES: 0 DEPOSIT

total deposit 0 OZ nil tonnes

NIL

xxxxxxxxxxxxxxxxxxxxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:

2 entries a) Out of Brinks 546,567.000 oz (17,000 kilobars) b) Out of JPMorgan enhanced: 137,669.900 oz (344 London good delivery bars)

total withdrawal: 684,236.900 oz or 21.28 tonnes tonnes_

adjustments: 5 dealer to customer

a)Ashai: 41,673.132 oz

b) Brinks 215,752.355 oz

c) JPMorgan: 675.171 oz

d) Loomis 64,237.698 oz

e) Malca: 3,472.308 oz

total of gold transferred out of dealer to customer: 325,810.664 oz or 10.13 tonnes

xxxxxxxxxxxxxxxxxx

AMOUNT OF GOLD STANDING FOR APRIL

THE FRONT MONTH OF APRIL HAD A LOSS OF 347 CONTRACTS TO STAND AT 230. WE HAD 478 CONTRACTS FILED YESTERDAY. THUS WE GAINED 131 CONTRACTS OR 13,100 OZ (.4070 TONNES) AS WE EXPERIENCED ANOTHER QUEUE JUMP WHERE THESE BOYS DESIRED TO TAKE PHYSICAL DELIVERY OVER HERE. THIS IS CENTRAL BANKERS STANDING FOR PHYSICAL GOLD. LAST FRIDAY’S QUEUE JUMP OF 6.1619 TONNES REPRESENTED THE HIGHEST EVER QUEUE JUMP IN COMEX HISTORY SURPASSING THE PREVIOUS HIGHEST RECORDED WAS AT 5.90 TONNES.

MAY GAINED 295 CONTRACTS UP TO 6403 CONTRACTS WHICH IS A SHOCKER AS NOBODY LEFT THE GOLD ARENA WITH THAT MAMMOTH LOSS???? AND WE ARE LESS THAN A WEEK AWAY FROM FIRST DAY NOTICE???. MAY BECOMES THE FRONT MONTH AND WE WILL ALSO EXPERIENCE A STRONG DELIVERY MONTH EVEN THOUGH IT IS AN OFF MONTH!

JUNE LOST 7912 CONTRACTS TO 342,439. JUNE WILL STILL BE A WHOPPER OF A DELIVERY MONTH

We had 149 contracts filed for today representing 14,900 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 100 notices issued from their client or customer account. The total of all issuance by all participants equate to 149 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL /2025. contract month, we take the total number of notices filed so far for the month (64,268 X 100 oz ) to which we add the difference between the open interest for the front month of APRIL (230 CONTRACTS) minus the number of notices served upon today (149 x 100 oz per contract) equals 6,434,900 OZ OR 200.152 TONNES

to which we add our 6 exchange for risk issuances for April of 7.776 tonnes

= 207.926 tonnes

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (64,268 x 100 oz +we add the difference for front month of APRIL (230 OI} minus the number of notices served upon today (149 x 100 oz) which equals 6,434,900 OZ OR 200.152 TONNES + 7.776 tonnes ex for risks = 207.926 tonnes

TOTAL COMEX GOLD STANDING FOR APRIL.: 207.926 TONNES WHICH IS HUGE FOR THIS ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL IS FOLLOWING SUIT..

i) out of Delaware: 3000.000 oz ii) Out of HSBC 310,124.800 oz iii) Out of Loomis 40,368.440 oz

total withdrawal: 353,493.240 oz

ADJUSTMENTs 0

JPMorgan has a total silver weight: 199.954million oz/497.740oz million or 40.16%

TOTAL REGISTERED SILVER: 159.627 MILLION OZ//.TOTAL REG + ELIGIBLE. 497.740Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2025 OI: 34 OPEN INTEREST CONTRACTS FOR A GAIN OF 30 CONTRACTS. WE HAD 0 NOTICES FILED ON WEDNESDAY SO WE GAINED 34 CONTRACT WHICH UNDERWENT A QUEUE JUMP OF 170,000 OZ AS THESE BOYS WERE WILLING TO WAIT FOR DELIVERY OF SILVER OVER HERE

MAY SAW A LOSS OF 4079 CONTRACTS DOWN TO 42,342 CONTRACTS. MAY BECOMES THE FRONT MONTH AND IT LOOKS LIKE WE WILL HAVE A DANDY AMOUNT OF SILVER STANDING THIS MONTH.

JUNE SAW A GAIN OF 98 CONTRACTS UP TO 2831 CONTRACTS.

JULY GAINED 9682 CONTRACTS UP TO 88,571

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 32 or 0.160 MILLION oz

CONFIRMED volume; ON WEDNESDAY 122,139 mega t.a.s. release//

AND NOW APRIL DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 3129 X5,000 oz = 15.645 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (34) AND the number of notices served upon today (32 )x (5000 oz)

Thus the standings for silver for the APRIL 2025 contract month: (3129) Notices served so far) x 5000 oz + OI for the front month of APRIL(34) minus number of notices served upon today (32)x 5000 oz equals silver standing for the APRIL contract month equating to 15.655 MILLION OZ . WE MUST NOW ADD OUR 4.0 MILLION OZ EXCHANGE FOR RISK ISSUED ON MONDAY MARCH 31 AND TODAY APRIL 4/NEW STANDING INCREASES TO 19.655 MILLION OZ

New total standing: 19.655 million oz which is huge for this NON active delivery month of APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 159.627million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

GLD INVENTORY: 952.471 TONNES, TONIGHTS TOTAL

SILVER

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

CLOSING INVENTORY 452.471 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2, EGON VON GREYERZ

ALASDAIR MACLEOD

3. C Powell and Gata dispatches

4. ANDREW MAGUIRE PODCAST 219

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//COPPER

Breaking Down Copper Trade In Charts Amid Noisy Trade War, IMF Downgrade

Wednesday, Apr 23, 2025 – 05:45 AM

The ongoing trade war is poised to deliver a negative shock to US growth, prompting the International Monetary Fund to slash its 2025 forecast earlier Tuesday. This gloomier outlook has sharpened our focus on the once high-flying industrial metals market—now showing signs of weakness—particularly the copper market.

Goldman analyst Adam Gillard provided clients with a snapshot of current conditions in the copper market, highlighting tight physical supply in China and continued strength in domestic demand.

However, Gillard cautioned that ongoing global industrial production weakness and declining Chinese exports—driven by the deepening trade war—could tip the market into surplus.

The analyst outlined four micro data points on the copper markets for clients to better gauge sentiment:

1. US cathode imports: YTD imports from BL data 408k MT implying an “over-import” of ~100k MT vs market expectations of ~300k MT (by June). If this run rate continues LME should tighten despite the likely tariff related demand shock.

2. Scrap: US scrap spreads remain under pressure as rising discounts erode the CME premium (US scrap is priced off CMX). March exports unchanged sequentially despite ARB strength; we don’t have April export data yet but this will be key given lower US exports (FY production ~542k MT contained) were key to the bull thesis.

3. Chinese demand: Ostensibly strong; YTD demand +10% due to production strength (from increased smelter capacity), seasonally adjusted stock draws (in part due to tariff related tolling exports) and strong net imports (despite deeply negative SHFE / LME import arb). Think this figure inflated by SMM production numbers (base affect) but a strong number nonetheless.

4. Positioning: Although our CTA model is running close to max short LME net spec at 28k is above the Aug24 low of 16k, and China appear to be still be running long on Shanghai (due to strong domestic demand).

The question remains whether copper bulls like Kostas Bintas, Trafigura Group’s former co-head of metals and now with Mercuria Energy Group, and/or Carlyle Group’s Jeff Currie (former Goldman boss of commodities) are still bullish on the industrial metal—or if the trade war has delayed their thesis of much higher prices.

LME Copper…

. . .

END

6 CRYPTOCURRENCY NEWS

ASIA TRADING THURSDAY MORNING WEDNESDAY NIGHT

SHANGHAI CLOSED UP 0.93 PTS OR 0.03%

//Hang Seng CLOSED DOWN 162.86 PTS OR 0.74%

// Nikkei CLOSED UP 170.52 OR 0.49%//Australia’s all ordinaries CLOSED UP 0.61%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2895 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2887/ Oil DOWN TO 63.00 dollars per barrel for WTI and BRENT DOWN TO 66.70 Stocks in Europe OPENED MOSTLY ALL RED.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2895 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.2887 (CCP MANIPULATED)

SHANGHAI CLOSED CLOSED UP 0.93 PTS OR 0.03%

HANG SENG CLOSED CLOSED DOWN 162.86 PTS OR 0.74%

2. Nikkei closed UP 170.52 PTS OR 0.49%

3. Europe stocks SO FAR: MOSTLY ALL RED

USA dollar INDEX DOWN TO 99.12// EURO RISES TO 1.1384 UP 55 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.318//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.40…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4680/Italian 10 Yr bond yield DOWN to 3.5885 SPAIN 10 YR BOND YIELD DOWN TO 3.127%

3i Greek 10 year bond yield DOWN TO 3.311

3j Gold at $3338.75 Silver at: 33.48 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 29 /100 roubles/dollar; ROUBLE AT 82.71

3m oil into the 63 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.40// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.318% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8297 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9400 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.348 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.795 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.828 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.32

10 YR UK BOND YIELD: 4.5825 UP 2 PTS

10 YR CANADA BOND YIELD: 3.232 DOWN 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.839 DOWN 1 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

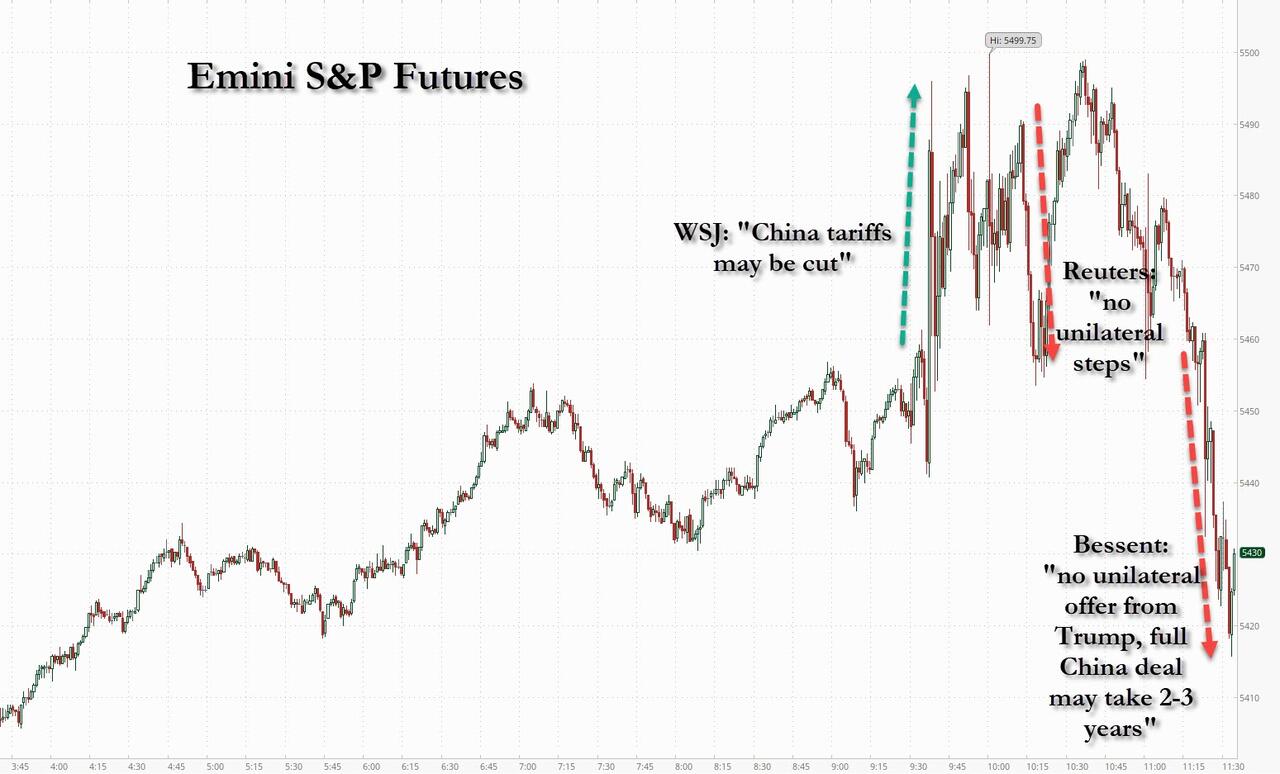

Futures Drop On Tariff Concerns As Dollar Slid

Thursday, Apr 24, 2025 – 08:27 AM

It’s risk-off price action this morning, with US equity futures lower, rates rallying across the curve, macro credit opening softer, while the USD trades broadly lower. The two-day rally in US stocks fizzled amid mixed Trump signals on China tariffs as the president floated a fresh levy timeline while simultaneously denying easing efforts and Beijing called for full rollback of all US duties. As of 8:00am S&P futures slipped -0.3% as China maintained a defiant stance over tariffs imposed by Trump, but were off session lows as investors continue to live headline to headline; Nasdaq futures dropped 0.2% with all Mag7 names in the red; NVDA (-1.5%), TSLA (-1.6%), and AAPL (-1.2%) are leading the losses. With Trump reigniting tariff volatility, IBM warning on federal cuts and China denying trade talks entirely, the rotation out of US risk remains intact. Europe was mixed, Real Estate (+1.16%) and Autos (+0.71%) outperforming but Banks (-0.76%) and Travel (-0.69%) lagged. Overnight, China responded to the recent headlines regarding “US-China talk”: Beijing pointed out that “there are absolutely no negotiation on the economy and trade between China and the US and called to cancel all the unilateral measures on China. Meanwhile Trump downplayed the idea of millionaire tax rate, one that some Republicans sees as a way to pay for the economic package. Bond yields are lower and USD is weaker; 2-, 5-, 10-yr yields are 4.5bp, 4.8bp, 3.3bp lower. The dollar extended its decline (-0.56%), with gold climbing (+1.3%) as investors hedge against prolonged US policy risk. VIX is flat (+0.28%), MOVE dipped (-1.48%) and USYC2Y10 (+1.6%) suggesting caution is returning despite the bounce in crude (+0.74%) copper (+0.57%) and gold (+1.4%). Flows are risk-off: SPY -$1.98B, QQQ -$689M and IWM -$614M, while GLD picked up another +$643M and XLU +$109M. Looking ahead today, we have durable good orders, initial and jobless claims, existing home sales, as well as non-voter Kashkari speaking.

In premarket trading, Mag 7 stocks fall (Tesla -0.6%, Nvidia -0.3%, Meta -0.5%, Apple -0.2%, Amazon -0.3%, Alphabet -0.2%, Microsoft -0.06%). IBM slumped 6.8% after 1Q results failed ease investor concerns. Chipotle fell 3.6% after the Mexican restaurant chain lowered its full-year outlook after quarterly sales declined for the first time in almost five years. Comcast fell 3% after reporting first-quarter losses of pay-TV and broadband customers that exceeded analysts’ estimates, a reflection of the growing competition from streaming companies and wireless providers. Here are some other notable premarket movers:

Alaska Air (ALK) tumbles 6.5% after the carrier’s 2Q forecast for adjusted earnings per share trailed the average analyst estimate.

Edwards Lifesciences (EW) climbs 3% after the medical device maker boosted its sales forecast for the full year.

Hasbro (HAS) gains 6% after the toymaker posted 1Q profit that beat estimates.

Impinj (PI) climbs 17% after the semiconductor device company reported first-quarter results that beat expectations and gave a positive revenue forecast.

Procter & Gamble (PG) falls 1.8% after the consumer products company cut its core earnings per share growth forecast for the full year.

Robert Half (RHI) tumbles 15% after the staffing services company reported first-quarter EPS that missed the average analyst estimate and noted that US trade policy is weighing on business confidence.

ServiceNow (NOW) rallies 8% after the software company reported first-quarter results that beat expectations and gave an outlook that is seen as strong.

Southwest Air (LUV) drops 4% after the carrier said it is not reiterating its 2025 or 2026 Ebit guidance as a result of weakening consumer spending and “macroeconomic uncertainty.”

Texas Instruments (TXN) rises 9% after the chipmaker reported first-quarter results that beat expectations and gave an outlook that is seen as strong.

Tractor Supply (TSCO) falls 4% after the farm-store chain reported sales for the first quarter that missed the average analyst estimate.

Stocks are struggling to extend Wednesday’s global rally, which was spurred by signs Trump is rethinking the most aggressive elements of his stances on trade and the Federal Reserve. The market moves underscore how investors are grappling to keep up with pronouncements from officials in the administration and frequent back-and-forth by Trump on his tariffs. Bessent tempered some of the optimism over that development, as he said the US was not looking to unilaterally lower tariffs and that a full trade deal could take two to three years. China, in turn, said Thursday that the US should revoke all unilateral tariffs and that Washington needs to show sincerity if it wants to hold trade negotiations.

“In terms of geopolitical risk, there’s a chance that we have reached a bottom, even if that’s not necessarily the case for markets,” said Francois Antomarchi, a fund manager at Degroof Petercam asset management. “Trump has touched the limits of what he can inflict on corporate America. That being said, there’s always a possibility he starts acting on another political front and triggers more volatility.”

Overnight, we continued to see mixed messages on trade negotiations, with President Trump saying last night that China may receive a new levy rate in two to three weeks, while China’s Foreign Ministry denied both countries are in talks and said the US should revoke all unilateral tariffs. Also had reports that the US is considering reducing certain tariffs targeting the auto industry although Trump said he wasn’t. CNBC reported that EU officials have warned that there’s still a lot of work that needs to get done before a trade deal can be reached with the US. Japan is hoping to finalize an agreement around the Group of Seven summit in June, however, they are likely going to resist Trump efforts to form trade bloc against China.

“You’re just seeing conflicting statements and noise coming from the US, where the overall narrative is just all over the place,” said Peter Kinsella, head of foreign-currency strategy at Union Bancaire Privee Ubp SA in London. “It’s impossible to trade.”

Deutsche Bank strategists were the latest to slash their year-end S&P 500 target by 12%, citing the blow to US companies from tariffs. While the new target of 6,150 points leaves 14% upside from Wednesday’s close, it means the index will only recover losses sustained since its February peak. Up until this change, the Deutsche Bank team had one of the most bullish views for the benchmark.

“With the potential impact of the announced tariffs large and likely to fall disproportionately on US companies, we lower our S&P 500 EPS estimate for 2025 from $282 to $240,” the strategists wrote in a note, adding that the consensus view is at risk of further downgrades.

Europe’s Stoxx 600 is down 0.4% with bank, retail and technology shares posting the largest declines.Real Estate (+1.16%) and Autos (+0.71%) outperform but Banks (-0.76%) and Travel (-0.69%) lag. Germany’s IFO Survey was better (for both current and expectations) helping push the euro higher. Here are the biggest movers on Thursday:

Galderma shares climb as much as 7.9% after the Swiss dermatology company reaffirms its core Ebitda margin forecast for the full year, which RBC flags as positive given it includes the impact of US tariffs

Beijer Ref shares gain as much as 9.8% to touch a one-month high, after the Swedish industrial cooling and ventilation firm posted strong earnings. Analysts praised the company’s solid organic growth

Indivior shares gain as much as 8.1% after the UK drugmaker posted earnings. Jefferies welcomed the 1Q beat and reiterated guidance, with expectations for a second-half rebound driven by Sublocade support

Belimo rises as much as 10% after the Swiss manufacturer of heating, ventilation and air conditioning upwardly revises its guidance for the full year. Analysts note particular strength in US data center demand

Inchcape shares plummet as much as 17%, marking their worst drop since 2008, after the automotive distributor posted a drop in organic sales and added a caveat to its guidance as tariffs inject more uncertainty

Kering shares fall as much as 6.9% following a sales miss which analysts said showed that its key Gucci brand continues to struggle. The update raised doubts that the French luxury group can bounce back in 2H

BNP Paribas shares dropped 2.2%, making it one of the worst performing banks in Europe, after the French lender reported a drop in first-quarter net income despite record result from equities trading

Nokia shares fall as much as 5.8% after the telecom equipment firm reported weaker-than-expected 1Q earnings and said reaching the top end of its guidance now appears more challenging

Dassault Systemes shares slide as much as 9.7%, to the lowest intraday since 2020. The software company issued a mixed first-quarter report, as softness in licenses driven by broader macro uncertaint

Worldline shares slide as much as 8.8% after the payments firm removed its previous full-year guidance, citing management’s limited tenure and macro-related uncertainty

Husqvarna shares fall as much as 7.7%, the most since April 7, after the Swedish garden and outdoor equipment firm reported weak earnings and announced its CEO would depart

Thales shares fall as much as 6.1% after the French defense company’s orders were softer than expected in the first quarter — according to Jefferies. JPMorgan highlights some weakness in non-defense divisions

EssilorLuxottica shares fall as much as 3% after the Ray-Ban maker’s earnings fell in line with expectations, not enough to push the outperforming stock any higher as macro headwinds marred the update

Earlier in the session, Asian stock rally took a breather on Thursday as investors digested the latest commentary from the Trump administration on its tariff plan. The MSCI Asia Pacific Index edged lower after a five-day run of gains. Shares in Taiwan, South Korea and Hong Kong fell. Stock benchmarks in Japan bucked the trend to gain about 1%, buoyed by carmakers on news that the US is considering whether to reduce certain tariffs targeting the auto industry. While signs that President Donald Trump is easing up on his tough stance against China and the Federal Reserve drove a relief rally globally on Wednesday, the momentum cooled after Treasury Secretary Scott Bessent cast doubt on a timely resolution to the US-China trade war. A reduction in US import tariffs is “conditional on China coming to the table and perhaps then after a two to three-year period we could see a bilateral trade deal in the works,” said Chris Weston, head of research at Pepperstone. “For now, the collective takes the news flow to mean that we’ve seen the worst of tariff policy.”

In FX, the Bloomberg Dollar Spot Index fell 0.4%, snapping a two-day winning streak after China also demanded that the US revoke all unilateral tariffs; ongoing tensions underscored the risks stemming from aggressive US tariffs. The euro rises 0.6%, helped by stronger-than-expected German IFO data although Rehn’s comments saw it pullback from the highs. The Norwegian krone is leading G-10 currency gains against the dollar, rising 1.2%. The Canadian dollar underperforms, albeit still up 0.3%. USD/JPY fell as much as 0.8% to 142.31.

“The dollar rebound this week doesn’t represent much more than a squeeze on speculative short dollar positions generated by the ‘no intention to fire Powell’ headlines and signs of back peddling on some of the tariff items,” said Ray Attrill, head of foreign-exchange strategy at National Australia Bank Ltd. “It doesn’t change the negative big picture view of the dollar”

In rates, the 10-year Treasury yield fell 3bps to 4.35%, sliding back toward a 4.24% touched on Wednesday, its lowest since April 8. Treasuries hold modest curve-steepening gains in early US trading, led by German government bonds which are also higher, having extended gains after ECB’s Rehn said they shouldn’t rule out a larger interest-rate cut. German 10-year borrowing costs fall 3 bps. Gilts are also higher, albeit lagging peers. Bund curve steepened as traders priced in additional ECB easing. The US session includes a 7-year note auction, last coupon sale until May 5, following good demand for Wednesday’s 5-year offering.

In commodities, oil prices advance, with WTI rising 0.6% to $62.60 a barrel. Gold jumps $50 to around $3,336/oz. Bitcoin falls 1% to below $93,000.

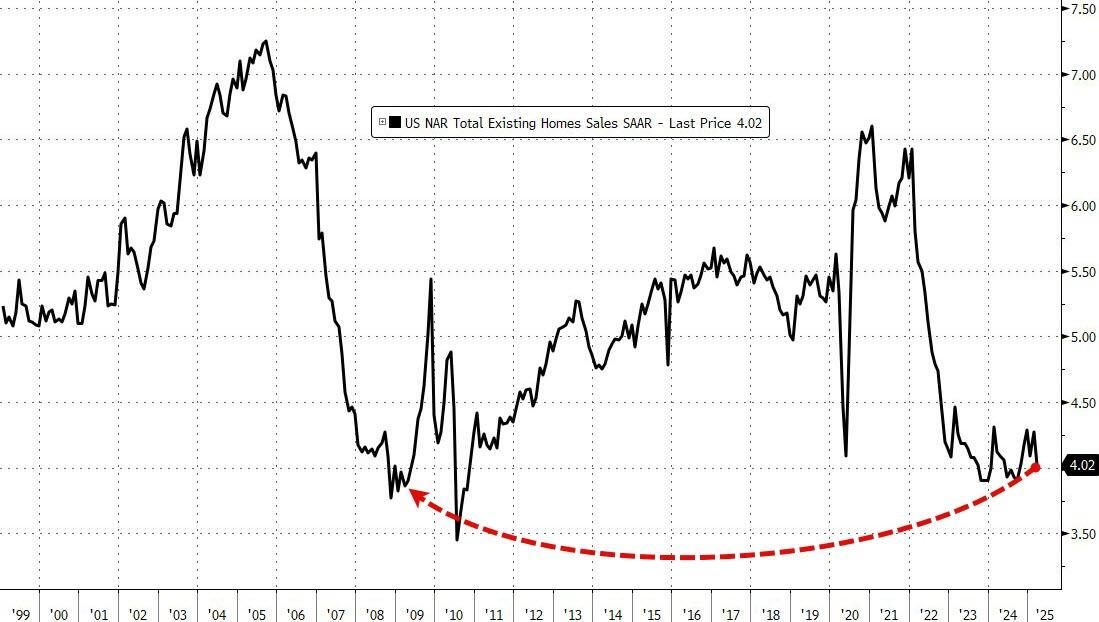

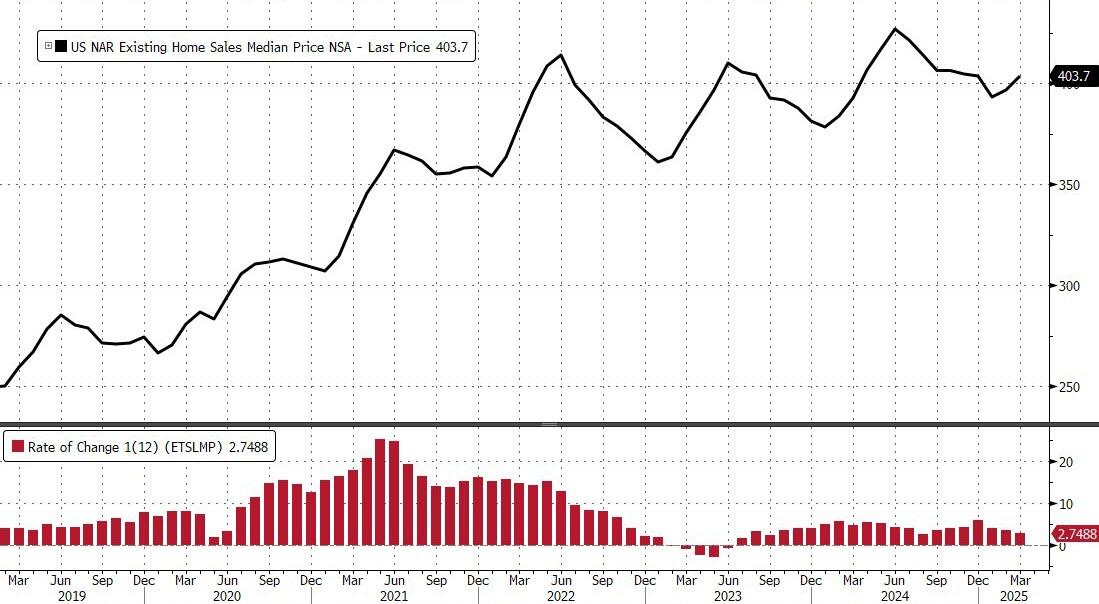

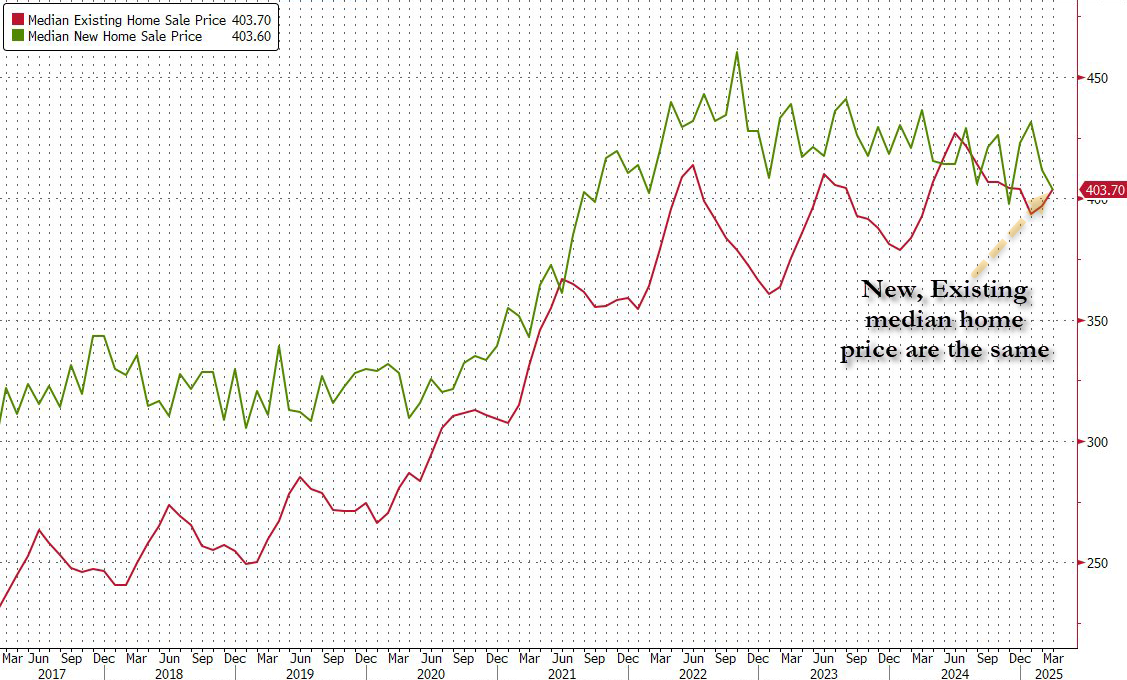

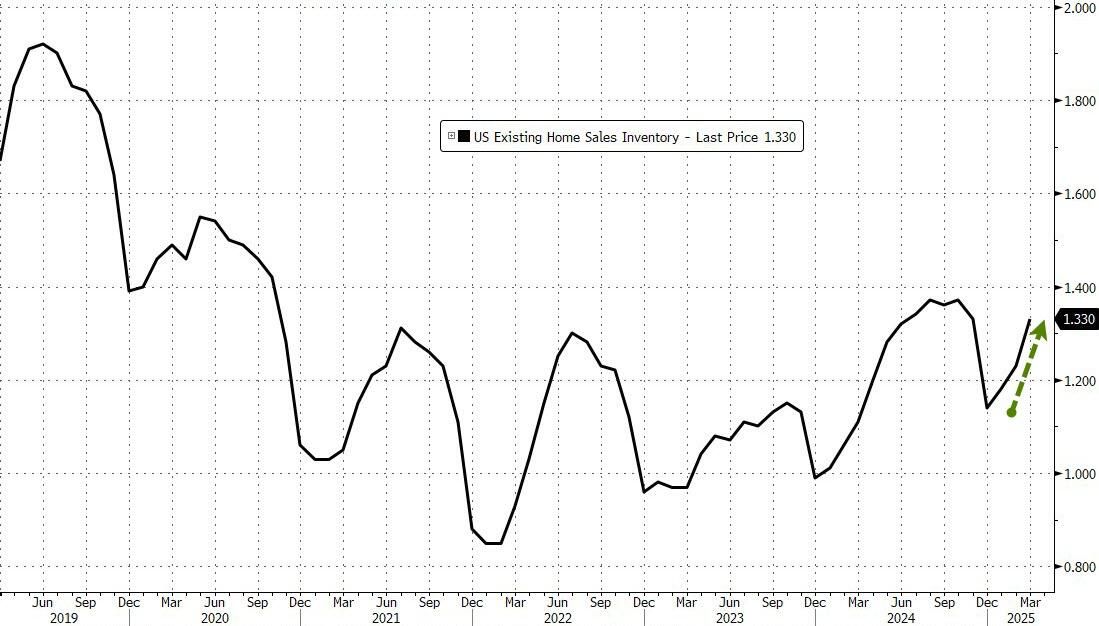

On today’s calendar, we have Initial Jobless Claims and Durable Goods at 8:30am, Existing Home Sales at 10am, and Kansas City Fed Manf at 11am. Fed’s Kashkari speaks at 5pm. We get another slew of EPS and $44bn 7yr UST auction at 1pm.

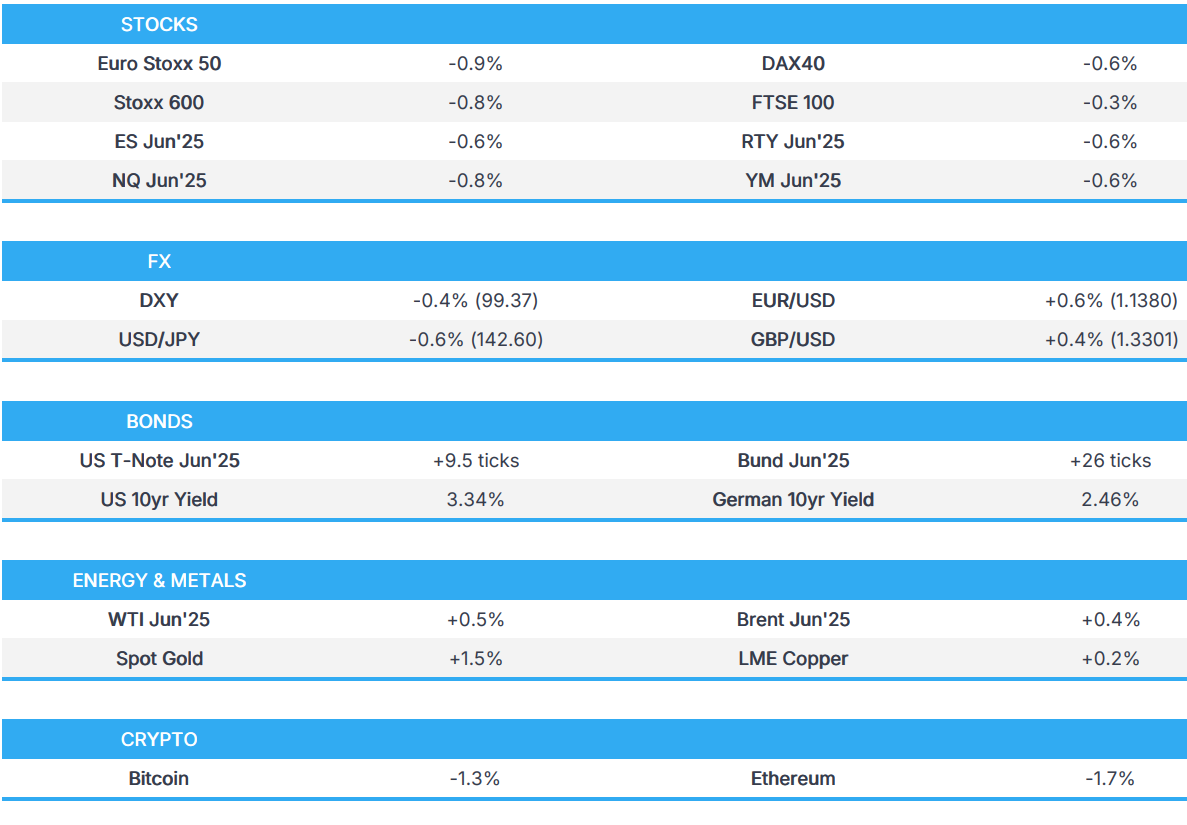

Market Snapshot

S&P 500 mini -0.3%

Nasdaq 100 mini -0.3%

Russell 2000 mini -0.2%

Stoxx Europe 600 -0.3%

DAX -0.5%

CAC 40 -0.6%

10-year Treasury yield -3 basis points at 4.35%

VIX +1 points at 29.49

Bloomberg Dollar Index -0.3% at 1225.41

euro +0.5% at $1.137

WTI crude +0.8% at $62.74/barrel

Top Overnight News

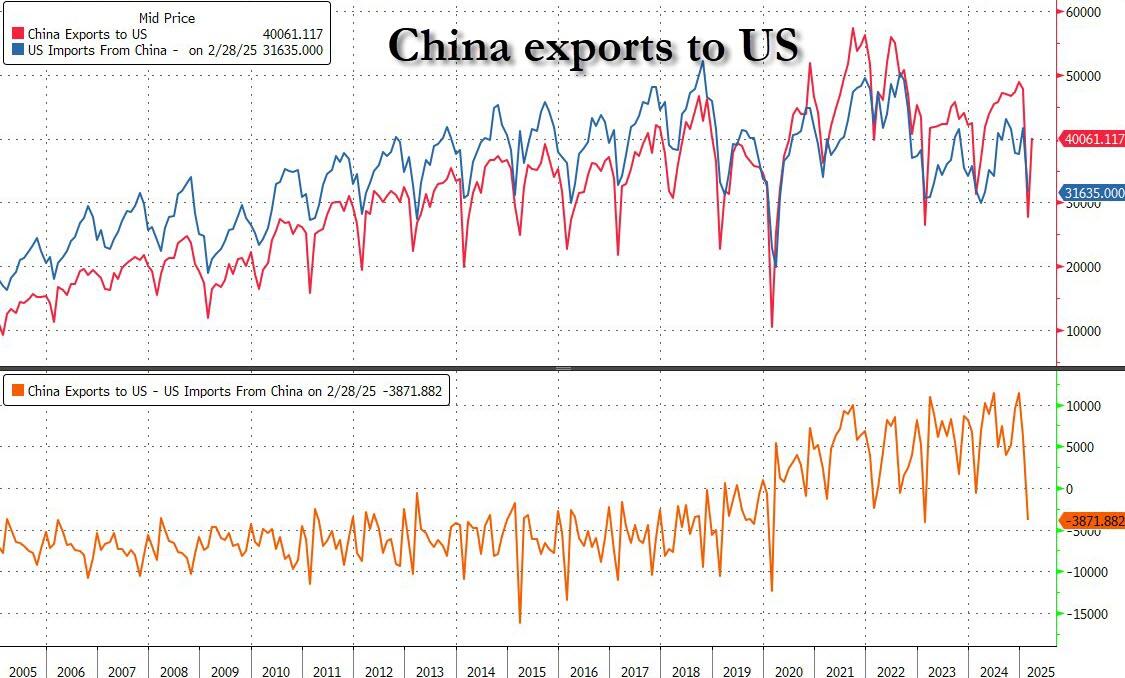

Factories in China have begun slowing production and furloughing some workers as the trade war unleashed by Trump dries up orders for products ranging from jeans to home appliances. With most Chinese goods now facing US Duties of at least 145%, some factory owners say American customers have cancelled or suspended orders, forcing them to cut production. FT

US House Republicans will seek a $150bln Pentagon spending hike as part of their party-line mega bill: Politico.

Trump said he might call Jerome Powell and reiterated the Fed chair is making a mistake by not lowering rates. Cleveland President Beth Hammack said slowing the pace of the Fed’s balance-sheet runoff may let it continue for longer. BBG

Trump and House Speaker Mike Johnson signal opposition to a new 40% tax bracket for those earning $1M+, likely putting a “nail in the coffin of the idea.” Politico

BofA Institute Total Card Spending (Week-to-Apr-19th): +3.1% (Y/Y) (prev. 2.3%); said easter continues to be a major retail event for the US

Trump is planning to spare carmakers from some of his most onerous tariffs, on another trade war climbdown. The move would exempt car parts from the tariffs that Trump is imposing on imports from China. Exemptions would leave in place a 25% tariff Trump imposed on all imports of foreign made cars and a separate 25% levy on parts would also remain and is due to take effect from May 3. FT

Marco Rubio refuted a Politico story that reported the White House may lift sanctions on Russian energy assets as part of a Ukraine peace deal. Overnight, Russia hit Kyiv with one of the heaviest aerial strikes this year. BBG

China on Thursday said that there were no ongoing discussions with the U.S. on tariffs, despite indications from the White House this week that there would be some easing in tensions with Beijing. “If the U.S. really wants to resolve the problem … it should cancel all the unilateral measures on China,” Ministry of Commerce Spokesperson He Yadong told reporters. CNBC

Japanese bonds and stocks are set to draw the biggest combined monthly foreign inflows on record, adding to signs global funds are seeking alternatives to US assets. BBG

EU officials warn that there’s still a lot of work that needs to get done before a trade deal can be reached with the US. CNBC

The ECB will probably have to cut rates further and shouldn’t exclude a larger reduction, Governing Council member Olli Rehn said. BBG

Fed’s Hammack (2026 voter) said uncertainty is a big issue in the economy and is causing businesses to pause, while she added that an incredibly high bar exists for the Fed to step in and they have not seen the need for Fed market intervention. Hammack also commented that recent market troubles were a risk transfer and that markets were functioning, as well as noted it is not a good time to be pre-emptive amid policy uncertainty and reiterated now is a good time for monetary policy to take its time.

Tariffs/Trade

China’s Vice Premier He Lifeng said the nation must face up to the new situation of the US tariff increase on China; need to increase policy supply and solve practical problems.

China’s Foreign Ministry spokesperson, on US trade talks, said “As far as I know, China and the US have not consulted or negotiated on the issue of tariffs, let alone reached an agreement,” via Global Times.

China’s MOFCOM said any content about China-US economic and trade talks is “groundless and has no factual basis” If US really wants to resolve the issue, it should life all unilateral tariff measures against China.

China Foreign Ministry spokesperson Gou said China and the US are not yet in talks on tariffs; will fight tariff war “if we have to” Respect is condition for any talks to happen. Tariffs disrupt TWO rules, and harm people of all countries.

China’s MOFCOM held a meeting with foreign firms to discuss the impact of US tariff increases on the investment and operations of foreign enterprises in China; committed to further opening-up, with policies that are stable, consistent, and predictable.

US President Trump said it depends on China how soon tariffs can come down and they have spoken to 90 countries regarding tariffs already. Trump said if they don’t have a deal, they will set tariffs and could set the tariff for China over the next two or three weeks, while he suggested that there is daily direct contact between US and China. Furthermore, Trump commented that they don’t want cars from Canada and that car tariffs from Canada could go up, as well as noted that they are working on a deal with Canada and will see what happens.

It was earlier reported that US President Trump is to exempt carmakers from some US tariffs in which he was said to be planning to spare carmakers from some of his most onerous tariffs, in another trade war climbdown following intense lobbying by industry executives over recent weeks, according to FT.

White House Economic Advisor Hassett said the USTR has 14 meetings scheduled this week with foreign trade ministers and there are 18 written offers from trade ministers, while he stated China is open to talks.