GOLD CLOSED DOWN $13.45 TO $3,323.90

SILVER CLOSED UP $0.30 TO $33.30

OPTION’S EXPIRY/WEDNESDAY APRIL 30 OTC/LONDON OPTIONS EXPIRY

GOLD ACCESS CLOSED $3322.50

Silver ACCESS CLOSED: $32.90

Bitcoin morning price:$95,334 UP 455 DOLLARS.

Bitcoin: afternoon price: $95.290 up 411 DOLLARS

Platinum price closing UP $16.30 TO $987.85

Palladium price; UP $9.65 TO $951.35

END

*CANADIAN GOLD: $4,597.40 DOWN $18.50 CDN dollars per oz( * NEW ALL TIME HIGH $4735.70 CDN DOLLARS PER OZ//APRIL 21 2025)

*BRITISH GOLD: 2478.40 DOWN 5.74 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,559.38 BRITISH POUNDS/OZ) APRIL 21/2025

*EURO GOLD: 2,917.98 DOWN 7.54 Euros per oz //* (ALL TIME CLOSING HIGH: 2,973.82 EUROS PER OZ/ APRIL 21 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

jpmorgan stopped: 0/0

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 0 NOTICES FOR 0 OZ 0.0000 TONNES

total notices so far: 64,754 contracts for 6,475,400 OR 201.412 tonnes)

FOR APRIL

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 0 NOTICE(S) FILED FOR 0.000 MILLION OZ/

total number of notices filed so far this month : 3192 CONTRACTS (NOTICES) for 15.966 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $13.45 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 946.27 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $.30 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ////A MASSIVE DEPOSIT OF 3.229 MILLION OZ INOT THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 451.925 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 373 CONTRACTS TO 154,590 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0.03 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 961 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE 588 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD A CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING MONDAY SPRINKLED WITH SOME MONTH END SPREADERS AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON MONDAY WITH SILVER’S GAIN IN PRICEBUT THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH A HUGE T.A.S. ISSUANCE OF 710 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A HUGE 588 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 710 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY THROUGH WEDNESDAY’S COMEX OPTIONS EXPIRY TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 961 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $0.03.

THE CME NOTIFIED US THAT WE HAD 0 CONTRACTS OF THOSE CRAZY EXCHANGE FOR RISK CONTRACTS ISSUED FOR 0 OZ (0 MILLION OZ). THESE EXCHANGE FOR RISKS ARE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THUS FOR THE MONTH OF APRIL WE HAVE A TOTAL OF 4.0 MILLION OZ OF EXCHANGE FOR RISK ISSUED ON TWO OCCASIONS. THE RECIPIENT OF THIS LARGESS IS PROBABLY THE CENTRAL BANK OF INDIA.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A HUGE 710 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.03) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS DESPITE HAVING A LOSS IN PRICE, WE GAINED A MEGA HUGE 1392 CONTRACTS IN OPEN INTEREST FROM OUR TWO EXCHANGES.

WE HAD A HUGE 588 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.735 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP TO WHICH WE ADD OUR 4.00 MILLION OZ EX FOR RISK

STANDING FOR APRIL REMAINS CONSTANT AT 19.965 MILLION OZ

WE HAD:

/ GOOD COMEX OI GAIN+// A HUGE SIZED EFP ISSUANCE (588 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 710 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 431 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 22 DAYS, total 19,689 contracts: OR 98.445 MILLION OZ (894 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 98.445 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 98.445 MILLION OZ///AVERAGE SIZE ISSUANCE

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 884 CONTRACTS DESPITE OUR LOSS IN PRICE OF $0.03 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE 588 CONTRACT EFP ISSUANCE CONTRACTS: 588 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A STRONG SILVER OZ STANDING FOR APRIL OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

NEW STANDING APRIL: 19.965 MILLION OZ

THE NEW TAS ISSUANCE MONDAY NIGHT (710 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TUESDAY THROUGH WEDNESDAY TRADING.(OPTIONS EXPIRY)

WE HAD 0 NOTICE(S) FILED TODAY FOR 0.00 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2527 OI CONTRACTS TO 448,075 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A 779 CONTRACTS //.

WE HAD A FAIR SIZED INCREASE IN COMEX OI (2527 CONTRACTS) . THIS OCCURRED DESPITE OUR HUGE GAIN OF $50.50 IN PRICE MONDAY. LAST WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES (CME CORRECTED// MAYBE?) TO WHICH WE ADD FOR APRIL ITS INITIAL 700 CONTRACT EXCHANGE FOR RISK FOR 70,000 OZ OR 2.177 TONNES AND FRIDAY APRIL 4: 250 CONTRACT ISSUANCE FOR .777 TONNES + MONDAY APRIL 7 NEW ISSUANCE OF .8709 TONNES/ + APRIL 9 ‘S TOTAL OF 484 EX. FOR RISK FOR 48,400 OZ OR 1.5054 TONNES/NEW TOTAL AND APRIL 14 EX FOR RISK OF 30,000 OZ OR.6220 TONNES AND THEN APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND THEN FINALLY FRIDAY’S 187 CONTRACT EX FOR RISK FOR 18700 OZ OR .5816 TONNES// ;NEW EX FOR RISK 8.3571 TONNES TO WHICH WAS ADDED TO OUR NEW QUEUE JUMP OF 42 CONTRACTS OR 4200 OZ (0.1306 TONNES). THUS STANDING FOR GOLD/APRIL DELIVERY MONTH IS 201.573 TONNES NORMAL DELIVERY(INCLUDES LATEST QUEUE JUMP) + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

/NEW STANDING FOR APRIL; 201.443 TONNES + 8.3571 TONNES EX FOR RISK = 209.800 TONNES

/ ALL OF THIS HAPPENED WITH OUR $50.50 GAIN IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD A FAIR SIZED GAIN OF 2577 OI CONTRACTS (8.015 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AND NOW FOR OUR FRONT MONTH OF APRIL. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS. WE HAVE A MASSIVE AMOUNT OF TONNES STANDING FOR GOLD IN APRIL.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 50 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 448,075//NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2577 CONTRACTS WITH 2527 CONTRACTS INCREASED AT THE COMEX// AND A SMALL SIZED 50 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2577 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1456 CONTRACTS ISSUED. WE HAD CONSIDERABLE T.A.S. LIQUIDATION AND MONTH END SPREADER LIQUIDATION DURING THE COMEX SESSION MONDAY WHICH ACCOUNTS FOR THE LOSS IN PRICE BUT NOTHING ELSE!!

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (50 CONTRACTS) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 2527 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3356 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING AT THE GOLD COMEX FOR APRIL 201.573 TONNES (WHICH INCLUDES OUR 0.1306 TONNES QUEUE JUMP) AND THIS FOLLOWS TOTAL EXCHANGE FOR RISK ISSUANCE ON 7 OCCASIONS FOR 8.3571 TONNES//NEW STANDING ADVANCES TO 209.953 TONNES.

//NEW STANDING APRIL: 201.573 TONNES + 8.3571 TONNES EX FOR RISK ON 7 OCCASIONS = 209.953 TONNES

.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION AND MONTH END SPREADER LIQUIDATION+ ZERO SUCCESS IN REMOVING ANY NET SPECULATOR LONGS, AS WE DESPITE HAVING 1)A HUGE $50.50 COMEX PRICE GAIN.. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A FAIR GAIN OF 3356 CONTRACTS ON OUR TWO EXCHANGES ALL OF IT DUE TO T.A.S. LIQUIDATION//MONTH END SPREADER LIQUIDATION /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD IN APRIL. ALSO MAY’S GOLD CONTRACT MONTH REFUSES TO SHED A SINGLE CONTRACT. MAY WILL BE A WHOPPER OF A DELIVERY MONTH.

4) FAIR SIZED COMEX OI GAIN// 5) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (2992 CONTRACTS)///FAIR T.A.S. ISSUANCE: 1456 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 66,406 CONTRACTS OR 6,640,600 OZ OR 206.5505 TONNES IN 22 TRADING DAY(S) AND THUS AVERAGING: 3018 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAY(S) IN TONNES 206.5505 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 206.5505 TONNES DIVIDED BY 3550 x 100% TONNES = 5.81% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 206.5505 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A GOOD SIZED 373 CONTRACTS OI TO 154,590 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 588 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 588 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 750 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 373 CONTRACTS AND ADD TO THE 588 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 961 CONTRACTS DESPITE THE LOSS IN PRICE OF $0.03 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.805 MILLION PAPER OZ

OCCURRED WITH OUR $0.03 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 1.76 PTS OR .05%%

//Hang Seng CLOSED UP 36.15 PTS OR 0.16%

// Nikkei CLOSED //Australia’s all ordinaries CLOSED UP 1.02%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2731 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2738/ Oil UP TO 61.01 dollars per barrel for WTI and BRENT UP TO 64.50 Stocks in Europe OPENED ALL GREEN.

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2527 CONTRACTS TO 448,075 DESPITE OUR MAMMOTH GAIN IN PRICE OF $50.50 WITH RESPECT TO MONDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS DESPITE THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A TINY NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (50 ).

THE CME ANNOUNCED MONDAY NIGHT, A 0 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR 0.0 TONNES. SO FAR THIS MONTH WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE FRONT MONTH OF APRIL STANDS AT 8.3571 TONNES OF GOLD WHICH MUST BE ADDED TO OUR NORMAL GOLD DELVERIES.

HISTORY: LAST TWO PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON APRIL COMEX MONTH

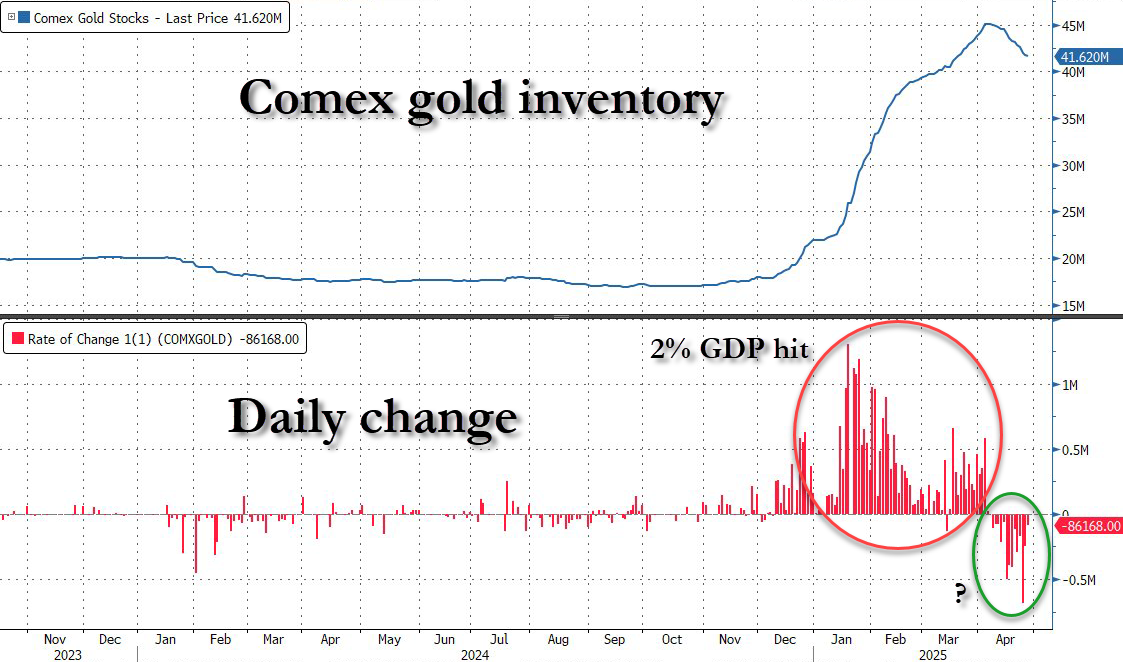

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 2577 CONTRACTS DESPITE OUR MAMMOTH GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON FRIDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH OF APRIL CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A LOT BIGGER THAN FROM OUR PREVIOUS FEW DAYS AT 1456 CONTRACTS

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 219 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1.2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF APRIL .… THE CME REPORTS THAT THE BANKERS ISSUED A TINY SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A TINY SIZED 50 EFP CONTRACTS WERE ISSUED: : /APRIL 50 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 50 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2577 CONTRACTS IN THAT 50 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 2527 COMEX CONTRACTS..AND THIS SMALLISH GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR MAMMOTH GAIN IN PRICE OF $50.50 FOR MONDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. LOOKS LIKE THE SHORT RATS ARE FLEEING THE ARENA AS EVIDENCED BY THE LOWER OPEN INTEREST AT THE COMEX!

THE ENTIRE GAIN IN OI AT THE COMEX WAS DUE TO:

- CONTINUATION OF MONTH END SPREADERS

- LIQUIDATION OF OUR T.A.S. SPREADERS

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED 1456 CONTRACTS, AS AGAIN, ALL OF THE TRADING AND SUPPLY OF CONTRACTS HAVE BEEN ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). AS PER THEIR MEGA 5 DAY ISSUANCE OF T.A.S THESE PAST FEW MONTHS,, THE FED HAS BEEN EXPERIMENTING WITH EINSTEIN’S DEFINITION OF INSANITY….TRYING TO DO THE SAME THING OVER AND OVER AGAIN HOPING FOR A DIFFERENT RESULT. HIS DEFINITION STILL STANDS.. THE CROOKS ACCOMPLISHED NOTHING AS NOBODY LEFT OUR GOLD METAL ARENA. DURING OPTIONS EXPIRY WEEK, A HUGE RAID WAS ORDERED BY THE FED WITH END OF THE MONTH TRADING ( FEB 25 THROUGH FEB 28) AS THE GOLD PRICE GOT HAMMERED A BIT WITH ONLY THE PAPER PRICE OF GOLD LOWERING! . AND ,FOR MARCH, WE HAD+ ANOTHER 5 DAY MEGA ISSUANCE BUT CORRESPONDING MEGA RAIDS FAILED TO MATERIALIZE. I WOULD LIKE TO POINT OUT THAT WEDNESDAY MARCH 17, THE 38,393 T.A.S. CONTRACT ISSUANCE WAS THE HIGHEST ON RECORD!

THE RAIDS ON OPTIONS EXPIRY ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH AND APRIL. (AND MONTH END SPREADERS)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON FEB 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR//MONTH END SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE JANUARY OPTIONS EXPIRY TRADING AND AGAIN WITH FEBRUARY OPTION EXPIRY MONTH. HALF WAY THROUGH THE JANUARY COMEX MONTH, THE CROOKS ISSUED FIVE CONSECUTIVE 30,000+ CONTRACT ISSUANCE OF T.A.S KNOWING THAT THEY WERE GOING TO INITIATE HUGE RAIDS ON OUR METALS. THEN THEY ISSUED IN LATE FEB, ANOTHER 5 CONSECUTIVE 30,000+ ISSUANCES. AND THEN, FOR THE FIRST TIME IN COMEX HISTORY WE WITNESSED THREE CONSECUTIVE MONTHS OF MEGA HUGE 30,000 + T.A.S CONTRACT ISSUANCES: JANUARY, FEB AND MARCH. WE ARE NOW FACING THIS WEDNESDAY WITH ANOTHER LONDON OTC OPTIONS EXPIRY (APRIL 30) WHERE BOTH SPREADERS WILL BE IN ACTION STOPPING GOLD’S ADVANCE.

STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (209.573 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 4 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 51 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 209.953 TONNES (INCLUDES 8.3571 TONNES EX FOR RISK/AND ALL MONTHLY QUEUE JUMPING)

COMEX GOLD TRADING/APRIL CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $50.50/ /)/AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION MONDAY COUPLED WITH CONTINUATION OF MONTH END SPREADER LIQUIDATION AS THEY WERE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,400 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS THEY SUCCEEDED IN THEIR ATTEMPT TO STOP THE PENETRATION OF OUR $3,400 DOLLAR GOLD BARRIER SO FAR.

MONDAY NIGHT/TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /APRIL TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

NOW APRIL, ISSUES ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK/APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WILL BE ADDED TO OUR NORMAL DELIVERY CYCLE.

STANDING FOR GOLD NOW FOR APRIL:

APRIL: 201.573 TONNES +(8.3571 EX FOR RISK// FOR APRIL DELIVERY MONTH =209.953 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS APRIL DELIVERY MONTH AFTER FIRST DAY NOTICE;

WE HAVE GAINED A STRONG SIZED TOTAL OF 5.919 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL FIRST RECORDED AT 166.964 TONNES ON FIRST DAY NOTICE FOLLOWED BY 7 EXCHANGE FOR RISK CONTRACT ISSUANCES FOR 8.3576 TONNES.

ALSO TODAY WE RECORD ANOTHER 42 CONTRACT QUEUE JUMP FOR 4200 OZ OR 0.1306 TONNES. WE MUST NOW ADD OUR 8.3576 TONNES EXCHANGE FOR RISK TO OUR NEW NORMAL DELIVERY OF 201.573 TONNES AND THUS STANDING FOR GOLD FOR APRIL IS NOW 209.953 TONNES, THE 2ND HIGHEST EVER RECORDED!

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $50.50

WE HAD A MONSTROUS 1808 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 2577 CONTRACTS OR 257700 0Z (8.015 TONNES)

confirmed volume MONDAY 230,204.. contracts: FAIR volume////

//speculators have left the gold arena

END

APRIL

// THE APRIL 2025 GOLD CONTRACT

APRIL29

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | . withdrawals: 1 entries b) Out of Looms: 97,031.718 oz (3018 kilobrs) total withdrawal: 97,031.718 (3.018 tonnes) |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | we have 2 customer entries i) Into HSBC: 38,934.861 oz 1211 kilobars ii) Into Stonex: 16,010.260 oz 498 kilobars total: 1709 kilobars or 1.709 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 0 notice(s) 0 OZ 0.0000 TONNES |

| No of oz to be served (notices) | 52 contracts 4200 OZ 0.16174 TONNES |

| Total monthly oz gold served (contracts) so far this month | 64,754 notices 6,475400 oz 201.412 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

TOTAL WEIGHT; 0 TONNES

xxxxxxxxxxxxxxxxxxxxx

we have 2 customer entries

i) Into HSBC: 38,934.861 oz

1211 kilobars

ii) Into Stonex: 16,010.260 oz

498 kilobars

total: 1709 kilobars or 1.709 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:

1 entries

b) Out of Looms: 97,031.718 oz (3018 kilobrs)

total withdrawal: 97,031.718 (3.018 tonnes)

adjustments: 5//first 4 dealer to customer

a)Loomis: dealer to customer: brinks 23,438.079

b) JPMorgan: 16,397.079 oz

c) Loomis 14,371.497 oz

d) Manfra: 20,833.848 oz

e)Customer to dealer malca: 67,227.741 oz

xxxxxxxxxxxxxxxxxx

AMOUNT OF GOLD STANDING FOR APRIL

THE FRONT MONTH OF APRIL STANDS AT 52 CONTRACTS FOR A LOSS OF 198. WE HAD 240 CONTRACTS FILED ON MONDAY. THUS WE GAINED 42 CONTRACTS OR 4200 OZ (0.1306 TONNES) AS WE EXPERIENCED ANOTHER QUEUE JUMP WHERE THESE BOYS DESIRED TO TAKE PHYSICAL DELIVERY OVER HERE. THIS IS CENTRAL BANKERS STANDING FOR PHYSICAL GOLD. MID APRIL’S QUEUE JUMP OF 6.1619 TONNES REPRESENTED THE HIGHEST EVER QUEUE JUMP IN COMEX HISTORY SURPASSING THE PREVIOUS HIGHEST RECORDED WAS AT 5.90 TONNES.

MAY GAINED 540 CONTRACTS UP TO 8425 CONTRACTS WHICH IS A SHOCKER AS NOBODY LEFT THE GOLD ARENA AND WE ARE 1 DAY AWAY FROM FIRST DAY NOTICE!!!!!. MAY BECOMES THE FRONT MONTH AND WE WILL ALSO EXPERIENCE A MEGA WHOPPER OF A DELIVERY MONTH EVEN THOUGH IT IS AN OFF MONTH!(APPROX 26 TONNES WILL STAND)

JUNE LOST ONLY 735 CONTRACTS TO 323,559. JUNE WILL STILL BE A WHOPPER OF A DELIVERY MONTH.

We had 0 contracts filed for today representing 0 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL /2025. contract month, we take the total number of notices filed so far for the month (64,754 X 100 oz ) to which we add the difference between the open interest for the front month of APRIL (52 CONTRACTS) minus the number of notices served upon today (0 x 100 oz per contract) equals 6,480,600 OZ OR 201.573 TONNES

to which we add our 7 exchange for risk issuances for April of 8.3576 tonnes

= 209.953 tonnes

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (64,754 x 100 oz +we add the difference for front month of APRIL (52 OI} minus the number of notices served upon today (0 x 100 oz) which equals 6,480,600 OZ OR 201.573 TONNES + 8.3576 tonnes ex for risks = 209.953 tonnes

TOTAL COMEX GOLD STANDING FOR APRIL.: 209.953 TONNES WHICH IS HUGE FOR THIS ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL IS FOLLOWING SUIT..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,770,025.821 oz 55.06 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 41,577,603.790 oz

TOTAL REGISTERED GOLD 20,715,556.875 or 644.34 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 20,862,046.915 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 18,945,531oz (REG GOLD- PLEDGED GOLD)= 589.28tonnes //

END

SILVER/COMEX

// THE APRIL 2025 SILVER CONTRACT//INITIAL

APRIL 29

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 withdrawal entry i) Loomis 1,210,923.420 oz total withdrawal: 1,210,923.420 oz |

| Deposits to the Dealer Inventory | 0/ entry |

| Deposits to the Customer Inventory | 3) entries deposits customer side i)Into ASAHI: 439,253.400 oz ii) Into JPMorgan: 1,771,853.920 oz iii) Into CNT 351,932.676 oz total deposit 2,563,039.976 oz |

| No of oz served today (contracts) | 0 CONTRACT(S) (0.000 MILLION OZ |

| No of oz to be served (notices) | 1 contract (5000 oz) |

| Total monthly oz silver served (contracts) | 3192 Contracts (15.966million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

0 entries/dealer

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

deposits customer side

3 entries

i)Into ASAHI: 439,253.400 oz

ii) Into JPMorgan: 1,771,853.920 oz

iii) Into CNT 351,932.676 oz

total deposit: 2,563,039.976 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx) withdrawal customer acct

1 withdrawal entry

i) Loomis

1,210,923.420 oz

total withdrawal: 1,210,923.420 oz

ADJUSTMENTs 0

JPMorgan has a total silver weight: 200.593million oz/497.746 oz million or 40.16%

TOTAL REGISTERED SILVER: 163.205 MILLION OZ//.TOTAL REG + ELIGIBLE. 499.098Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2025 OI: 1 OPEN INTEREST CONTRACTS FOR A GAIN OF 1 CONTRACT. WE HAD 0 NOTICES FILED ON MONDAY SO WE GAINED 1 CONTRACTS WHICH UNDERWENT A QUEUE JUMP OF 5,000 OZ

MAY SAW A LOSS OF 9761 CONTRACTS DOWN TO 17,643 CONTRACTS. MAY BECOMES THE FRONT MONTH AND IT LOOKS LIKE WE WILL HAVE A DANDY AMOUNT OF SILVER STANDING THIS MONTH.

(PROBABLY NORTH OF 12,000 CONTRACTS OR 60 MILLION OZ)

JUNE SAW A GAIN OF 34 CONTRACTS UP TO 3054 CONTRACTS.

JULY GAINED 9857 CONTRACTS UP TO 113,079

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or 0.000 MILLION oz

CONFIRMED volume; ON MONDAY 93,412 strong//

AND NOW APRIL DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 3192 X5,000 oz = 15.960 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (1) AND the number of notices served upon today (0 )x (5000 oz)

Thus the standings for silver for the APRIL 2025 contract month: (3192) Notices served so far) x 5000 oz + OI for the front month of APRIL(1) minus number of notices served upon today (0)x 5000 oz equals silver standing for the APRIL contract month equating to 15.965 MILLION OZ . WE MUST NOW ADD OUR 4.0 MILLION OZ EXCHANGE FOR RISK ISSUED ON MONDAY MARCH 31 AND APRIL 4/NEW STANDING INCREASES TO 19.965 MILLION OZ

New total standing: 19.965 million oz which is huge for this NON active delivery month of APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 163.205million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

APRIL29 WITH GOLD DOWN $13.45 TODAY// NO CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL28 WITH GOLD UP $50.20 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL25 WITH GOLD DOWN $49.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVEV WITHDRAWAL OF 3.911 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 948.56 TONNES

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

GLD INVENTORY: 946.27 TONNES, TONIGHTS TOTAL

SILVER

APRIL29 WITH SILVER UP $0.30 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.229 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 451.925 MILLION OZ

APRIL28 WITH SILVER DOWN $0.03 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.136 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.696 MILLION OZ

APRIL25 WITH SILVER DOWN $0.44 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 3.639 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.832 MILLION OZ

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

CLOSING INVENTORY 451.925 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2, EGON VON GREYERZ

ALASDAIR MACLEOD

3. C Powell and Gata dispatches

4. ANDREW MAGUIRE PODCAST 220

END

END

The Parable Of Goldfinger

Tuesday, Apr 29, 2025 – 06:30 AM

Authored by Alexander Zemek-Parkinson via BondVigiliantes.com,

Is there a relationship between the price of gold and bonds? Most vigilantes would agree that there is some correlation based on inflation, with bond yields and the price of gold rising when inflation is on the way up, and vice versa. Most “goldbugs” would probably agree with this assessment. They would say that the metal was a repository of long-term value and was an effective medium for protecting purchasing power. The late Julian Baring was the man with the golden fund1. He presented the relative purchasing power of gold in terms of fixed-price menus at the Savoy, an exercise he frequently undertook with M&G’s former CEO Paddy Lineker. Baring’s results were somewhat mixed, but there can be no doubt of his conclusion that, over time, the gold price not only equalled but outpaced the rate of inflation. It would be easy to conclude, in today’s world of rising bond yields and a historically high gold price, that there is a correlation, and that it is still valid.

But is it? An answer to this can be found in Ian Fleming’s novel, Goldfinger.

Before we turn our attention to Bond, Treasury Bond… Let me enlighten you on the secret life of Ian Fleming. He worked at (but not for) the Bank of England, and in both the film and the novel, he stages a well-crafted scene in one of its palatial offices. He introduces us to a fictional Colonel Smithers, whose job it was to monitor the quantity of gold in the vaults and to stem any bullion ‘leakage’ (smuggling to you and me). Enter the evil Auric Goldfinger, who leads Bond on a merry chase across Europe and the US.

Part of that chase takes Bond to Geneva, where Fleming attended university. Here’s where things get interesting. Goldfinger’s lair where he melts down his gold Rolls-Royce, is on the outskirts of a small village called Coppet4. Fleming gives a detailed description of the village’s ancient chateau, the small forest behind it and the position of a building which houses his foundry. This all exists in real life, except that the foundry is actually the tomb of one of the earliest Bond Vigilantes: the banker Jacques Necker, who was a finance minister under Louis XVI. Necker was popular because he thought debt finance was preferable to placing a heavier tax burden on the public.

Central to Necker’s concept of debt finance was the establishment of a central bank along British principles and a beneficial partnership between sovereign and private investors. System and laws were all-important. He succeeded in raising substantial loans for the beleaguered King as the nation’s political scene deteriorated. His scheme worked for a while, but the debt he created expired worthless. Necker got the sack, the King met the guillotine and a popular government was installed. In its place came the revolutionary interest-free fiat currency called the Assignat. These bills came with a dark warning on their borders5: “Death to counterfeiters, and rewards to denouncers”.

I’ve decided that none of this is a coincidence (or I wouldn’t have an article). What is Fleming actually trying to tell us? The message is clear that there is a link between debt and the value of gold. But does it hold true for inflation?

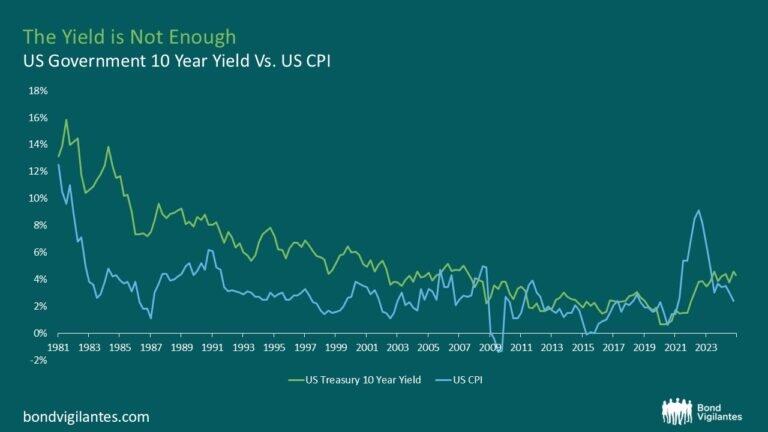

Below is a graph that is going to come as no surprise to the contemporary Bond Vigilante. It shows an observable correlation between bond yields and CPI. When inflation goes up, bond yields go up. When it comes down, bond yields come down. Nothing exciting.

Source: Bloomberg

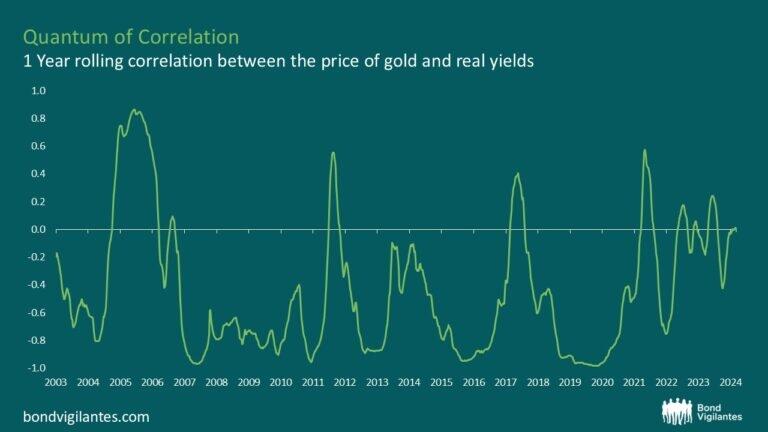

Now, let’s look at that again with the same bonds but set against the price of gold instead. We are looking for moments where the yield on the bonds fall and the gold price goes up to seek out some form of correlation between the two asset classes that we are told by textbooks exists.

Source: Bloomberg

Admittedly, a tricky graph there but there are a couple of times where we can see this in action. We see in ’82, ’87 and ’07 clear points where the yields fell and the gold price went up reflecting the ‘flight to safety’ that these trades tend to represent. So we are seeing a negative correlation in action. This sort of thing happens at times of market distress and when things in global markets look dicey.

Of late though, once you dial in on the rolling correlation between the price of gold and the real yield of US Treasuries over the last 20 years, that relationship has begun to break down. In the last 5 years, the correlation has hovered around zero thanks to the recent rise in the gold price. So quite literally there is no correlation between the two assets (and we know there has certainly been market distress recently).

Source: https://www.longtermtrends.net/gold-vs-real-yields/

So what then should we make of gold recently breaking the $3,000 mark? Is this significant for bond markets? Yes.

Things become clearer when we start considering broader macroeconomic movements over the last 50 years. From the 1980s onward, global market dynamics started to change with the introduction of Reaganomics, the Cold War summit and the widespread acceptance of globalisation. The world got smaller and the peace dividend grew, and with it came the development of broad mechanisms for an international system of freer trade. To the astonishment of Julian Baring, bond prices flew as global inflation fell and international cooperation improved. Bond risk premia dwindled.

Then, with the credit crisis of 2007 and the sovereign debt crisis of 2009, gold got moving again and made up for lost time. Why? Fear and uncertainty needled their way back into the bond markets and to gold’s residual value. In both government and commercial bond markets, investors began to demand higher yields8 because the benefits of globalisation seemed to be fast-disappearing9. We now appear to face a more uncertain macroeconomic environment, and quantitative easing, which eventually supported bond prices at artificially high levels, has gone into reverse. Just as the peace dividend now seems to be on the wane, the risk vectors have begun to rise.

Fleming, at the time of Goldfinger, was facing another series of global transformations: the wane of the Bretton Woods system, the possible change of the pound to a fiat currency and their effect upon the fabric of British social and political constructs10.

Gold has begun to behave like wampum, tulip bulbs and beanie babies11, bubble assets whose unexplained residual value eclipsed their intrinsic value and whose price reflects something other than the commodity it represents. To return to Mr. Baring, the Savoy index would now tell us that a single gold sovereign could buy you roughly 15 meals (a historic high). But where exactly is gold’s additional residual value coming from? I’d return to our friend Colonel Smithers, who supplied the moral to this, our Goldfinger parable.

Whilst bonds are the barometer of trust and faith in a system, Smithers maintains that…

“Gold is the talisman of fear”.

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//RARE EARTHS

6 CRYPTOCURRENCY NEWS

ASIA TRADING TUESDAY MORNING MONDAY NIGHT

SHANGHAI CLOSED DOWN 1.76 PTS OR .05%%

//Hang Seng CLOSED UP 36.15 PTS OR 0.16%

// Nikkei CLOSED //Australia’s all ordinaries CLOSED UP 1.02%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.2731 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2738/ Oil UP TO 61.01 dollars per barrel for WTI and BRENT UP TO 64.50 Stocks in Europe OPENED ALL GREEN.

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING

STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2731 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.2738 (CCP MANIPULATED)

SHANGHAI CLOSED CLOSED DOWN 1.76 PTS OR 0.05%

HANG SENG CLOSED CLOSED UP 36.15 PTS OR 0.16%

2. Nikkei closed

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 99.09// EURO FALLS TO 1.1382 DOWN 26 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.325//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.59…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR DOWN this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.5040/Italian 10 Yr bond yield UP to 3.625 SPAIN 10 YR BOND YIELD UP TO 3.173%

3i Greek 10 year bond yield UP TO 3.343

3j Gold at $3310.70 Silver at: 33.22 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 99 /100 roubles/dollar; ROUBLE AT 81.76

3m oil into the 61 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.59// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.325% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8253 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9392 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.252 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.704 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.709 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.45

10 YR UK BOND YIELD: 4.530 UP 2 PTS

10 YR CANADA BOND YIELD: 3.211 UP 5 BASIS PTS

5 YR CANADA BOND YIELD: 2.801 UP 5 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

Futures Flat As Markets Brace For Earnings Tsunami

Tuesday, Apr 29, 2025 – 08:29 AM

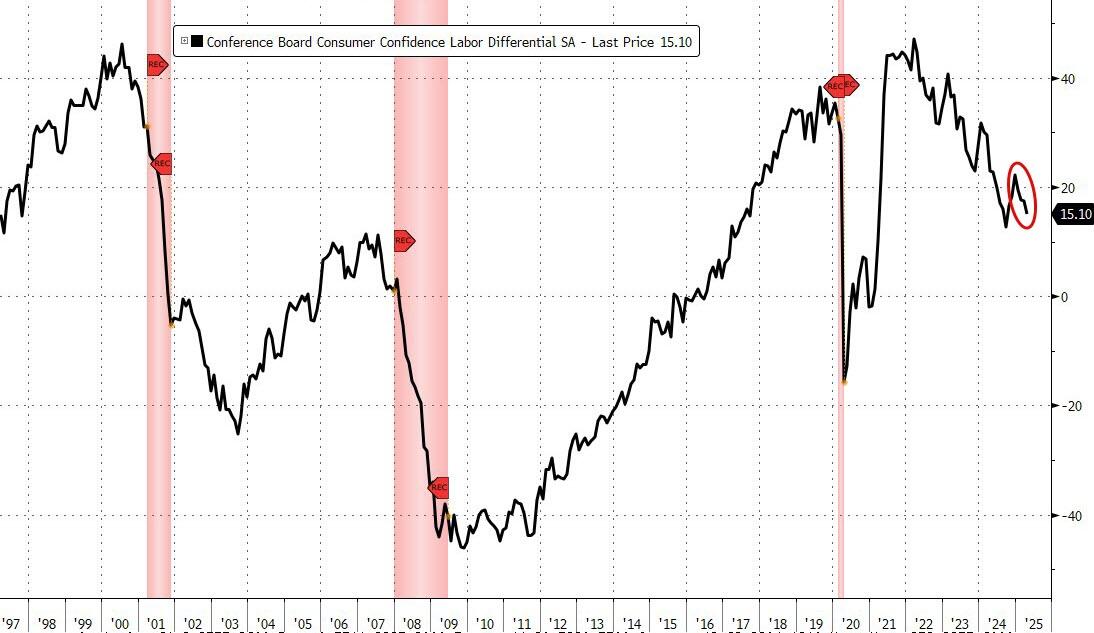

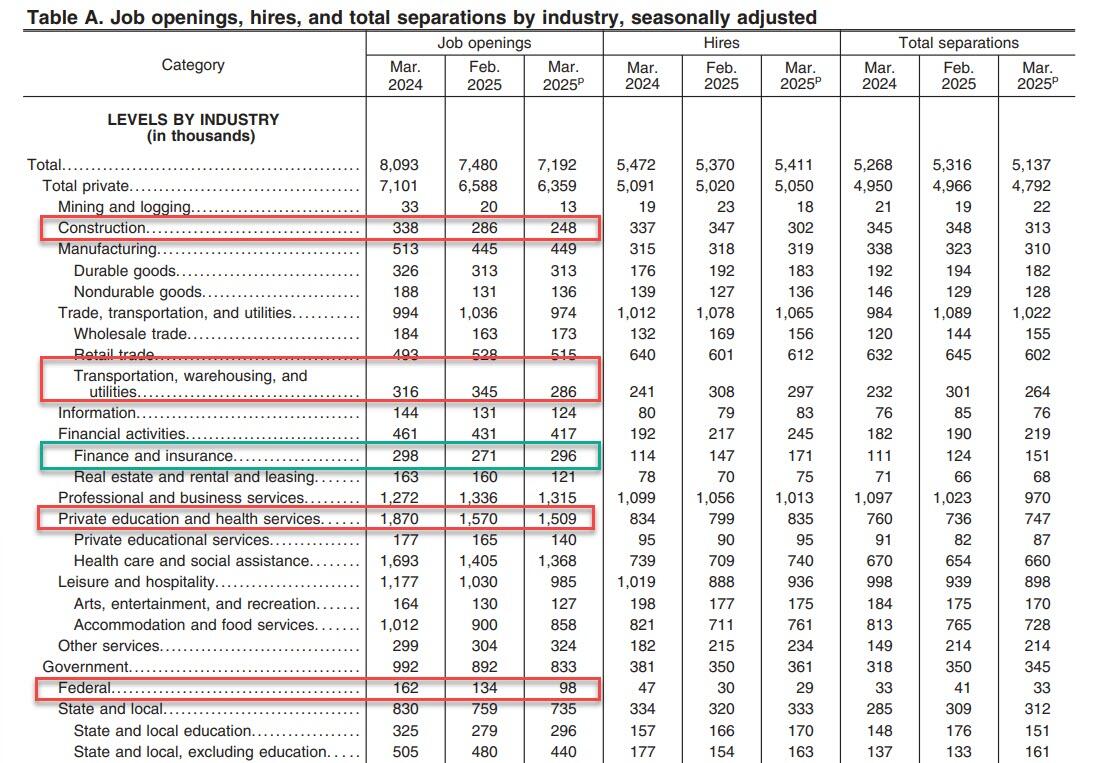

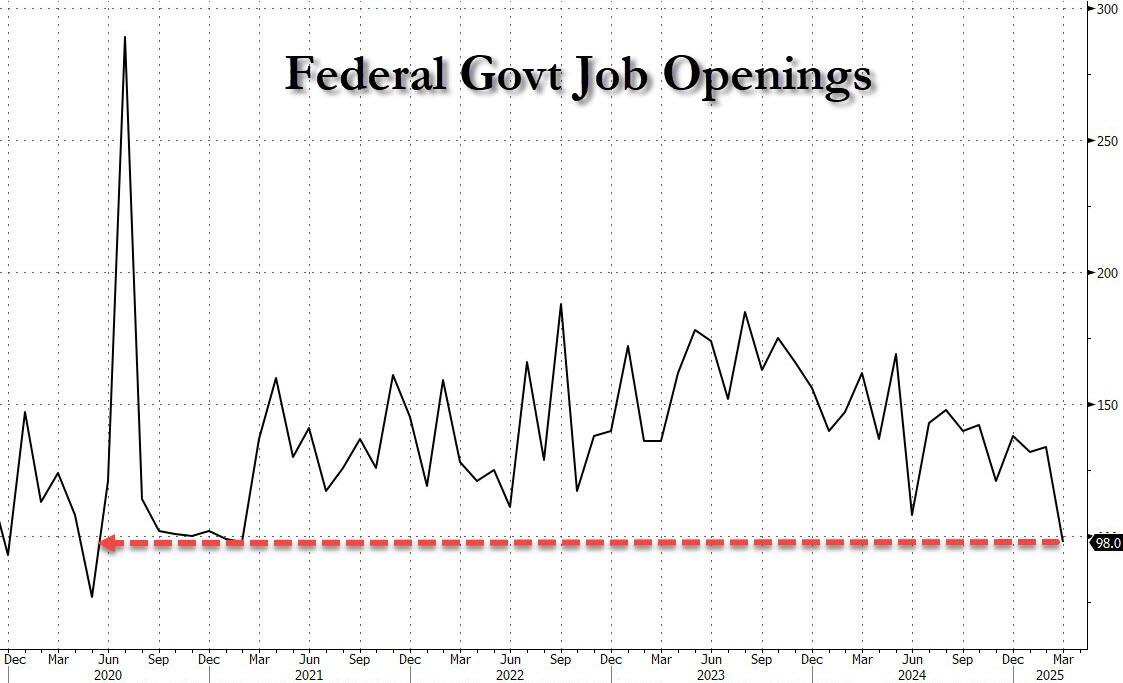

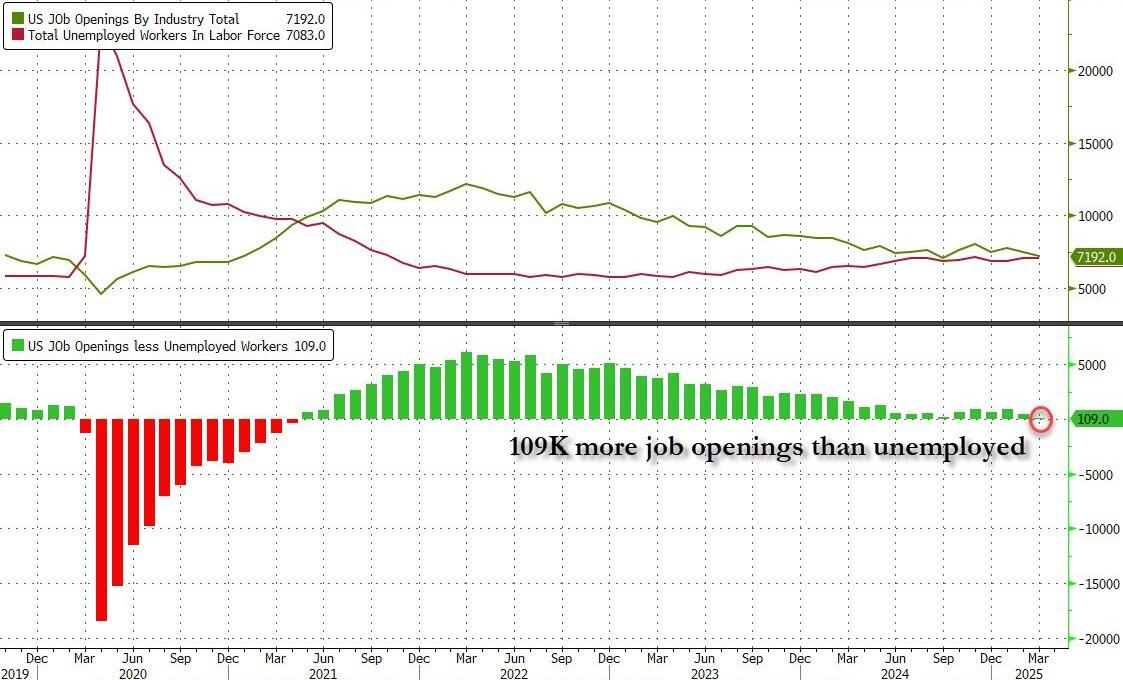

US equity futures were unchanged, erasing a modest gain and loss earlier, after General Motors pulled earnings guidance for 2025 and put share buybacks on hold until it has more clarity on the impact of US tariffs. As of 8:15am, S&P futures were flat, while Nasdaq futures were down 0.2% as TSLA rose +1.0% pre-mkt, followed by MSFT +0.5% and AMZN +0.5%. GM dropped in premarket trading, reversing an earlier gain, as it said it would suspend $4 billion of share repurchases. Bond yields and USD are higher (2-, 5-, 10-yr yields are 1.6bp, 2.9bp, 2.7bp higher). Commodities are mixed with WTI futures dropping 1.7%, adding to sharp losses seen Monday, Base Metals higher, and Precious Metals mixed. WSJ repeated a report from last week that Trump may ease his auto tariffs today; Elsewhere, Scott Bessent set July 4 as the goal to pass Trump’s tax cut package; he will announce the debt-ceiling X-date this week or next. Today, the key macro focus will be JOLTS Job Openings and Conf. Board Consumer Confidence.

In premarket trading, Magnificent Seven stocks are mixed as futures whipsaw )Amazon +0.2%, Alphabet +0.2%, Microsoft +0.1%, Apple +0.1%, Tesla -0.1%, Meta -0.1%, Nvidia -0.7%). General Motors (GM) shares fall 2.4% premarket after the automaker withdrew 2025 earnings guidance and paused $4 billion in share repurchases until it has more clarity on tariff impacts. Hims & Hers Health Inc. (HIMS) shares soared as much as 46% as it’s among companies Novo Nordisk A/S is partnering with to offer its popular weight-loss drug Wegovy to more US patients at a reduced price. Here are some other notable premarket movers:

- Crown Holdings (CCK) shares rise 3.3% after the beverage can maker reported adjusted earnings per share for the first quarter that beat the average analyst estimate. Analysts note strong volumes in Europe and Brazil

- Honeywell International Inc. (HON) shares gain 4.7% after the company raised its full-year guidance for earnings per share.

- PayPal (PYPL) shares are down 4.1% in premarket trading after the company reported fewer payment transactions in the first quarter than analysts expected.

- Okta (OKTA) shares rise 3.8% after S&P Dow Jones Indices announced that the stock will replace Berry Global in the S&P MidCap 400 before trading opens May 1.

- Regeneron (REGN) shares fall 7.5% after the drugmaker reported profit and sales for the first quarter that fell short of expectations.

- Ultra Clean (UCTT) shares are down 10% after the semiconductor manufacturing company reported first-quarter results that missed expectations and gave an outlook that is below the analyst consensus.

- UPS (UPS) shares are up 2% after the company reported adjusted earnings per share in the first quarter above what analysts expected

- Waste Management (WM) shares fall 1.7% after the firm’s first-quarter update missed revenue expectations and free cash flow dropped, with analysts saying that investors could have been hoping for more in order to support the stock’s year-to-date rally

- Wolfspeed (WOLF) shares are up 10% as the chipmaker is set for its sixth session of straight gains to match February’s winning streak

As Bloomberg notes, after weeks of intense volatility, markets now seem to be in a holding pattern. Gold is consolidating after hitting record highs, the DXY dollar index remains below its key 100 level, and oil is drifting lower. For investors, it’s difficult to find consensus, with risk management, confidence, and the guiding narrative on US exceptionalism upended by tariffs.

“With the uncertainty created by the tariffs we need to start pricing at least a probability of a US recession,” Johanna Kyrklund, chief investment officer at Schroders Plc, told Bloomberg TV. “As we analyze each company stock-by-stock, we’re looking for that risk to growth.”

Tariff sentiment continues to drive price action, with investors weighing plans by the Trump administration to ease the impact of auto tariffs by lifting some levies on foreign parts for cars and trucks made inside the US. However, it doesn’t look like a trade resolution is coming anytime soon. China’s top diplomat warned countries against caving in to US tariff threats, and Trump’s tactics are only serving to make China’s Xi Jinping more popular. At home, Treasury Secretary Bessent set a July 4 goal to pass a multi-trillion dollar tax cut package to appease voters getting fed up of Trump’s handling of the economy.

Still, with just over a third of S&P 500 companies reporting quarterly results, of those, 75% have beat estimates, according to data compiled by Bloomberg. S&P 500-listed companies worth $20 trillion are set to deliver results this week in one of the heaviest for 2025 earnings seasons. But the next few days are key: companies worth $20 trillion are set to deliver results this week in one of the heaviest for 2025 earnings seasons.

Beyond the plethora of earnings, investors will be tracking data for clues on economic resilience in the face of tariffs. Prospects for Federal Reserve interest-rate cuts will be guided by Friday’s US non-farm payrolls figures. Sentiment earlier was boosted by signs of easing trade tensions after a White House official said imported automobiles would be given a reprieve from separate tariffs on aluminum and steel.

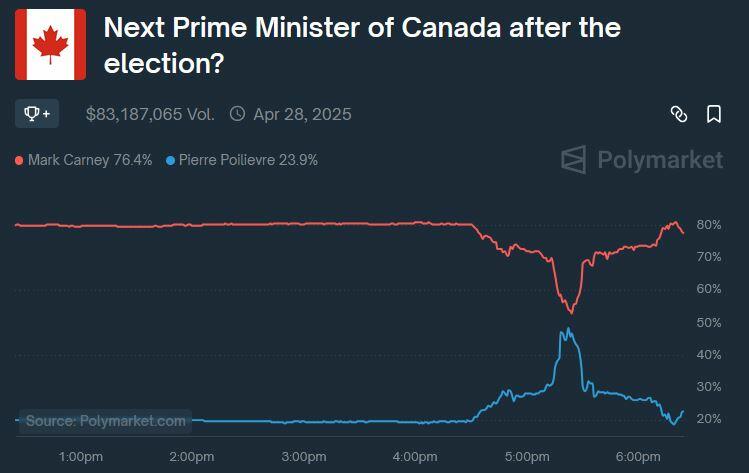

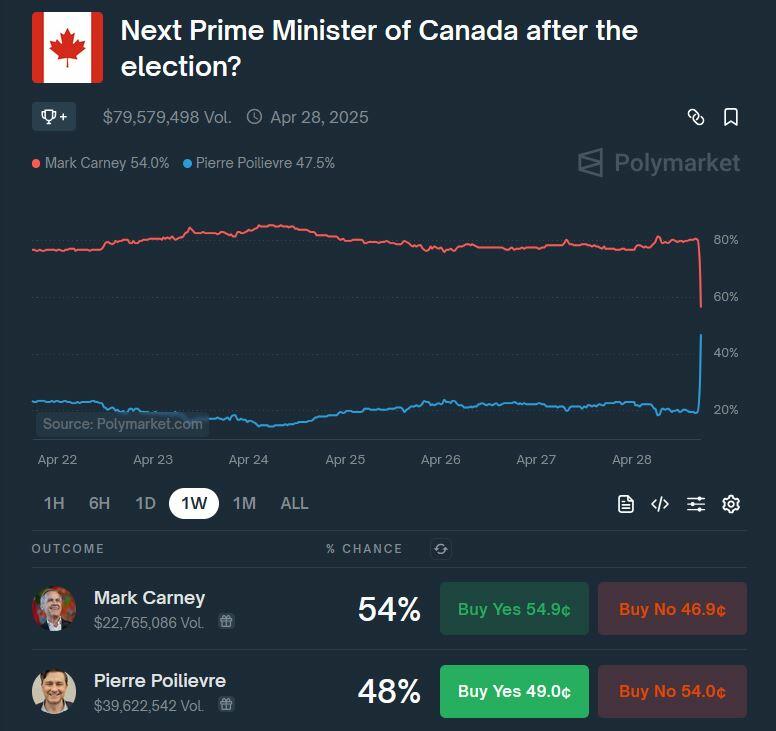

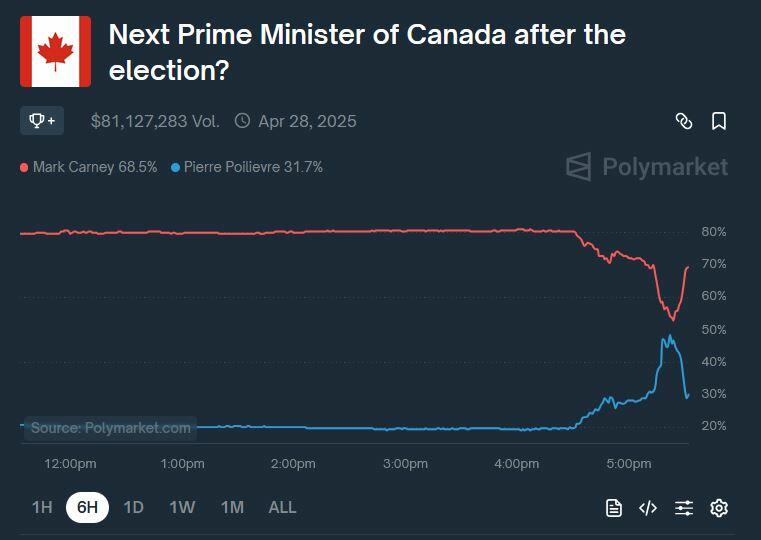

In Canada, the Liberal Party is projected to win a fourth consecutive election, giving a mandate to former central banker Mark Carney.

European stocks rise 0.4%, with risk sentiment improving after the US said imported autos would be given a reprieve from separate tariffs on aluminum and steel. Miners, travel and banks are the strongest-performing European sectors, while the IBEX lags peers, dropping 0.5%, as Spain deals with the fallout of a massive blackout. In earnings, Deutsche Bank shares rise after its trading unit hit a record. HSBC climbs after announcing a fresh share buyback. BP shares fall after the oil major cut its buyback as profit missed forecasts. Here are some of the biggest movers on Tuesday:

- Rheinmetall shares rise as much as 7.3% after smashing expectations across the board with analysts praising a blowout quarter.

- Deutsche Bank shares gain as much as 4.6% after the lender posted a strong set of results, led by its trading unit hitting a record in the first quarter amid high market volatility.

- Neste shares gain as much as 13% after the Finnish refiner posted an increase in margins within its renewable product unit in the first quarter results.

- HelloFresh shares jump as much as 12% after the meal-kit company reported first-quarter adjusted Ebitda that beat estimates by roughly 30%, a sign that the firm is hastening its pivot to profitability as it cuts fulfillment and marketing expenses.

- Amundi shares slide as much as 2.4% after the investment manager’s first-quarter earnings showed a mixed performance that could weigh on consensus estimates, according to analysts.

- Porsche shares fall as much as 7.6%, their steepest drop since early February, after the luxury carmaker issued another profit warning.