MAY 1/THE RAID ON OUR PRECIOUS METALS CONTINUES WITH CHINA OFF ON MAY DAY HOLIDAY: GOLD CLOSED DOWN $92.45 TO $3216.90//SILVER WAS DOWN 43 CENTS TO $32.22/PLATINUM WAS DOWN $4.60 TO $965.15 WHEREAS PALLADIUM WAS DOWN ONLY 5 CENTS TO $944.25/GOLD COMMENTARY TONIGHT FROM PETER SCHIFF//ISRAEL VS HAMAS UPDATES; MAJOR STORY THE HUGE FIRES BURNING SURROUNDING JERUSALEM AND THE WEST BANK//UKRAINE SIGNS THE DEAL WITH THE USA FOR RARE EARTHS AND THUS A DEPARTURE AS UKRAINE MUST PAY THE USA FOR THEIR AID//COIVD UPDATES/MARK CRISPIN MILLER/SLAY NEWS/PMI’S IN THE USA DISAPPOINT, YET ISM MANUFACTURING BEATS EXPECTATIONS//SWAMP NEWS FOR YOU TONIGHT//

190 H BMO CAPITAL MARKETS 32 323 C HSBC 14 332 H STANDARD CHARTERED B 32 435 H SCOTIA CAPITAL (USA) 2 624 H BOFA SECURITIES 2 661 C JP MORGAN SECURITIES 10 686 C STONEX FINANCIAL INC 53 6 709 C BARCLAYS 4 726 C PLUS500US FINANCIAL 1 737 C ADVANTAGE FUTURES 18 11 880 H CITIGROUP 62 905 C ADM 23

TOTAL: 135 135 MONTH TO DATE: 9,278

jpmorgan stopped: 10/135

MAY

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 135 NOTICES FOR 13,500 OZ 0.4197 TONNES

total notices so far: 9278 contracts for 927,800 OR 28.358 tonnes)

FOR MAY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 925 NOTICE(S) FILED FOR 4.625 MILLION OZ/

total number of notices filed so far this month : 12,617 CONTRACTS (NOTICES) for 63.085 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $92.45 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 944.26 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $.43 AT THE SLV: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: ////A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 454.972 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA HUGE SIZED 14,813 CONTRACTS TO 137,856 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS OF $0.65 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A HUGE SIZED LOSS OF 14,365 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A GOOD 341 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD A HUGE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING WEDNESDAY SPRINKLED WITH FINALIZATION OF MONTH END SPREADERS AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 4 WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON WEDNESDAY WITH SILVER’S LOSS IN PRICE BUT THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH A STRONG T.A.S. ISSUANCE OF 545 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A GOOD 341 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 545 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY’S LONDON/.OTC OPTIONS EXPIRY TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUGE SIZED 14,472 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.65.

THE CME NOTIFIED US THAT TODAY WE HAD A MEGA HUGE 2439 CONTRACTS OF THOSE CRAZY EXCHANGE FOR RISK CONTRACTS ISSUED FOR 12,195,000 OZ. THESE EXCHANGE FOR RISKS MUST NOW BE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THUS FOR THE MONTH OF MAY WE HAVE A TOTAL OF 12.195 MILLION OZ OF EXCHANGE FOR RISK ISSUED ON OUR FIRST OCCASION. THE RECIPIENT OF THIS LARGESS IS PROBABLY THE CENTRAL BANK OF INDIA.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A GOOD 363 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.65) AND WERE UNSUCCESSFUL IN KNOCKING OFF CONSIDERABLE NET SILVER LONGS FROM THEIR PERCH AS DESPITE HAVING A LOSS IN PRICE, WE LOST A MEGA HUGE 14,365 CONTRACTS IN OPEN INTEREST FROM OUR TWO EXCHANGES.

WE HAD A GOOD 341 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 67.830 MILLION OZ TO WHICH WE ADD OUR 219 CONTRACT QUEUE JUMP OF 1.095 MILLION OZ AND THEN WE MUST ADD THAT CRAZY 2,459 CONTRACT EXCHANGE FOR RISK FOR 12.195 MILLION OZ

INITIAL STANDING FOR MAY: 67.830 MILLION OZ PLUS 1.095 MILLION OZ (QUEUE JUMP) + 12.195 MILLION OZ (EX FOR RISK) EQUALS 81.11 MILLION OZ./

WE HAD:

/ MEGA HUGE COMEX OI LOSS+// A GOOD SIZED EFP ISSUANCE (341 CONTRACTS)/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 545 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 107 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 1 DAY, total 341 contracts: OR 1.705 MILLION OZ (341 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 1.705 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 1.705 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 14,813 CONTRACTS WITH OUR LOSS IN PRICE OF $0.65 IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. . THE CME NOTIFIED US THAT WE HAD A GOOD 341 CONTRACT EFP ISSUANCE CONTRACTS: 341 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

NEW INITITAL STANDING FOR MAY: 67.830 MILLION OZ. PLUD 1.095 MILLION OZ QUEUE JUMP + 12.195 MILLION OZ EXCHANGE FOR RISK ISSUANCE.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (545 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE THURSDAY TRADING.

WE HAD 925 NOTICE(S) FILED TODAY FOR 4.625 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 9017 OI CONTRACTS TO 442,851 AND FURTHER FROM TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A SMALL 83 CONTRACTS //.

WE HAD A STRONG SIZED DECREASE IN COMEX OI (9017 CONTRACTS) . THIS OCCURRED DESPITE OUR LOSS OF $14.05 IN PRICE WEDNESDAY. ON WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES (CME CORRECTED//) TO WHICH WE ADDED

+ 8.3571 TONNES EX FOR RISK = 209.953 TONNES

FINAL STANDING FOR APRIL; 201.443 TONNES + 8.3571 TONNES EX FOR RISK = 209.800 TONNES

INITIAL STANDING FOR MAY: 29.135 TONNES OF GOLD!

/ ALL OF THIS HAPPENED WITH OUR $14.05 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX ///. WE HAD A STRONG SIZED LOSS OF 7388 OI CONTRACTS (22.97 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AND THE SAME FOR APRIL AND NOW MAY. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS. WE HAVE A MASSIVE AMOUNT OF TONNES STANDING FOR GOLD IN MAY.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1629 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 442,851/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 137,856 CONTRACTS!!

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7388 CONTRACTS WITH 9017 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1629 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 7388 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1607 CONTRACTS ISSUED. WE HAD CONSIDERABLE T.A.S. LIQUIDATION AND MONTH END SPREADER LIQUIDATION DURING THE COMEX SESSION WEDNESDAY WHICH ACCOUNTS FOR SOME OF THE LOSS IN PRICE

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1629 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 9017 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 7388 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING FOR GOLD FOR MAY AT 29.135 TONNES ( WHICH WHICH INCLUDES OUR .6967 TONNES QUEUE JUMP)

NEW STANDING FOR GOLD, MAY CONTRACT: 29.135 TONNES OF GOLD.

.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION AND MONTH END SPREADER LIQUIDATION+ CONSIDERABLE SUCCESS IN REMOVING SOME NET SPECULATOR LONGS, AS WE HAD 1)A $14.05 COMEX PRICE LOSS.. WE HAD 2) CONSIDERABLE NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG LOSS OF 7308 CONTRACTS ON OUR TWO EXCHANGES MUCH OF IT DUE TO T.A.S. LIQUIDATION//MONTH END SPREADER LIQUIDATION /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY.

4) STRONG SIZED COMEX OI LOSS// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (1629 CONTRACTS)///STRONG T.A.S. ISSUANCE: 545 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAY INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 1629 CONTRACTS OR 162,900 OZ OR 5.066 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 1629 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN1 TRADING DAY(S) IN TONNES 5.066 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 5.066 TONNES DIVIDED BY 3550 x 100% TONNES = 0.149% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 5.066 TONES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 14,813 CONTRACTS OI TO 137,963 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 341 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 341 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 341 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 14,706 CONTRACTS AND ADD TO THE 341 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 14,472 CONTRACTS DESPITE THE LOSS IN PRICE OF $0.65 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 72.360 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED

//Hang Seng CLOSED

// Nikkei CLOSED UP 406.92 PTS OR 1.13% //Australia’s all ordinaries CLOSED UP 0.30%

//Chinese yuan (ONSHORE) CLOSED OFFSHORE CLOSED DOWN TO 7.2735/ Oil UP TO 57.31 dollars per barrel for WTI and BRENT UP TO 59.97 Stocks in Europe OPENED ALL MIXED.

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED9017 CONTRACTS TO 442,851 WITH OUR LOSS IN PRICE OF $14.05 WITH RESPECT TO WEDNESDAY’S // TRADING. WE LOST CONSIDERABLE NUMBER OF NET LONGS WITH THAT PRICE LOSSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1629 ).

THE CME ANNOUNCED WEDNESDAY NIGHT, A 0 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR 0.0 TONNES. IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST THREE PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

AND NOW WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

MAY: 0 ISSUED SO FAR…

DETAILS ON MAY COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 7388 CONTRACTS WITH OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF APRIL CONTINUED TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A LOT LARGER THAN FROM OUR PREVIOUS FEW DAYS AT 1607 CONTRACTS

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS. THE TONNAGE STANDING FOR GOLD FOR MAY IS 29 PLUS TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 219 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1.2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1629 EFP CONTRACTS WERE ISSUED: : /JUNE 1629 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1629 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7388 CONTRACTS IN THAT 1629 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 9034 COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $14.05 FOR WEDNESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. LOOKS LIKE THE SHORT RATS ARE FLEEING THE ARENA AS EVIDENCED BY THE LOWER OPEN INTEREST AT THE COMEX!

THE ENTIRE LOSS IN OI AT THE COMEX WAS DUE TO:

FINALIZATION OF MONTH END SPREADERS

LIQUIDATION OF OUR T.A.S. SPREADERS

CONSIDERABLE SPEC LIQUIDATION

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A FAIR SIZED 1607 CONTRACTS,

THE RAIDS ON OPTIONS EXPIRY ACCOMPLISHED TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL. (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE

FINAL STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (209.573 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 5 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: INITIAL STANDING AT 28.945 TONNES OF GOLD PLUS .6767 TONNES QUEUE JUMP = 29.135 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 209.953 TONNES (INCLUDES 8.3571 TONNES EX FOR RISK/AND ALL MONTHLY QUEUE JUMPING)

MAY: STANDING NOW 29.135 TONNES

COMEX GOLD TRADING/MAY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A $14.05/ /)/BUT THEY WERE SUCCESSFUL IN KNOCKING OFF CONSIDERABLE APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED LOSS IN OUR TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION WEDNESDAY COUPLED WITH FINALIZATION OF MONTH END SPREADER LIQUIDATION AS THEY WERE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,400 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS THEY SUCCEEDED IN THEIR ATTEMPT TO STOP THE PENETRATION OF OUR $3,400 DOLLAR GOLD BARRIER SO FAR.

WEDNESDAY NIGHT/THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER AND THUS THE REASON FOR THE HUGE LEASE RATE AT 10% (SCARCITY OF GOLD) THIS PAST MONTH.

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /MAY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

NOW APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK/APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

FINAL STANDING FOR GOLD NOW FOR APRIL:

APRIL: 201.573 TONNES +(8.3571 EX FOR RISK// FOR APRIL DELIVERY MONTH =209.953 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS MAY DELIVERY MONTH GOING INTO FIRST DAY NOTICE;

WE HAVE LOST A STRONG SIZED TOTAL OF 22.97 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY FIRST RECORDED AT 28.945 TONNES ON FIRST DAY NOTICE. WE HAD A HUGE 224 CONTRACT QUEUE JUMP FOR 22,400 OZ OR .6767 TONNES. THUS NEW STANDING ADVANCES TO 29.135 TONNES OF GOLD.

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $14.05

WE HAD A SMALL 83 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 7388 CONTRACTS OR 738,800 0Z (22.97 TONNES)

confirmed volume WEDNESDAY 220,999.. contracts: small volume////

a)) Out of Loomis: 64,302.000 oz (2000 kilobars) b) Out of Asahi 50,047.222 oz

c) Out of JPMorgan 675.171 oz 21 kilobars d) Out of Brinks 63,999.687 oz e) Out of Malca 139,926.774 oz f) out of HSBC enhanced: 11,791.625 oz or 21 London good delivery bars of 400 oz each.

total withdrawal: 367,419.489 (11,42 tonnes)

Deposit to the Dealer Inventory in oz

0 ENTRIES

Deposits to the Customer Inventory, in oz

we have 1 customer entries

we have 1 customer entry deposits i) Into Brinks: 400,663.901 oz 12462 kilobars

12.46 tonnes

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

135 notice(s) 13,500 OZ 0.4197 TONNES

No of oz to be served (notices)

89 contracts 8900 OZ 0.2768 TONNES

Total monthly oz gold served (contracts) so far this month

9278 notices 927800 oz 28.858 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

we have 1 customer entry deposits

i) Into Brinks: 400,663.901 oz

12462 kilobars

12.46 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:

withdrawals: 6 entries

a)) Out of Loomis: 64,302.000 oz (2000 kilobars) b) Out of Asahi 50,047.222 oz

c) Out of JPMorgan 675.171 oz 21 kilobars d) Out of Brinks 63,999.687 oz e) Out of Malca 139,926.774 oz f) out of HSBC enhanced: 11,791.625 oz or 21 London good delivery bars of 400 oz each.

total withdrawal: 367,419.489 (11,42 tonnes)

adjustments: 1//customer to dealer account Brinks

a)1,354,184.980 oz (42.12 tonnes

xxxxxxxxxxxxxxxxxx

AMOUNT OF GOLD STANDING FOR MAY

THE FRONT MONTH OF MAY STANDS AT 224 CONTRACTS FOR A LOSS OF 9082 CONTRACTS. WE HAD 9306 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 224 CONTRACTS OR 22,400 OZ FOR .6967 TONNES

JUNE LOST 654 CONTRACTS TO 322,708. JUNE BECOMES OUR NEW FRONT MONTH AND THIS MONTH WILL BE A WHOPPER OF A DELIVERY MONTH.

We had 135 contracts filed for today representing 13500 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 135 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 10 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY /2025. contract month, we take the total number of notices filed so far for the month (9278 X 100 oz ) to which we add the difference between the open interest for the front month of MAY (224 CONTRACTS) minus the number of notices served upon today (135 x 100 oz per contract) equals 936700 OZ OR 29.135 TONNES

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (9278 x 100 oz +we add the difference for front month of MAY (224 OI} minus the number of notices served upon today (135 x 100 oz) which equals 936,700 OZ OR 29.135 TONNES

TOTAL COMEX GOLD STANDING FOR MAY.: 29.135 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..

JPMorgan has a total silver weight: 205.915million oz/500.128 oz million or 41.2%

TOTAL REGISTERED SILVER: 165.721 MILLION OZ//.TOTAL REG + ELIGIBLE. 500.128Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF MAY /2025 OI: 2093 OPEN INTEREST CONTRACTS FOR A LOSS OF 11,473 CONTRACTS. WE HAD 11,692 NOTICES FILED YESTERDAY SO WE GAINED 219 CONTRACTS WHICH UNDERWENT A STORNG QUEUE JUMP OF 1.095 MILLION OZ. HOWEVER SADLY I MUST REPORT OUR MASSIVE 2419 CONTRACT ISSUANCE FOR EXCHANGE FOR RISK FOR 12.195 MILLION OZ. THE RECIPIENT OF THAT LARGESS WAS THE CENTRAL BANK OF INDIA.

JUNE SAW A GAIN OF 92 CONTRACTS UP TO 3318 CONTRACTS.

JULY LOST 3680 CONTRACTS DOWN TO 110,922

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 925 or 4.625 MILLION oz

CONFIRMED volume; ON WEDNESDAY 58.177 fair//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 12,617 X5,000 oz = 63,085 MILLION oz

to which we add the difference between the open interest for the front month of MAY (2093) AND the number of notices served upon today (925 )x (5000 oz)

Thus the standings for silver for the MAY 2025 contract month: (12,617) Notices served so far) x 5000 oz + OI for the front month of MAY(2093) minus number of notices served upon today (925)x 5000 oz equals silver standing for the MAY contract month equating to 68.925 MILLION OZ . THEN WE MUST ADD OUR NEW 12.195 TONNES OF EXCHANGE FOR RISK. NEW TOTAL STANDING FOR SILVER: 81.11 MILLION OZ

New total standing: 81.11 million oz which is huge for this NON active delivery month of MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 163.205million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

APRIL29 WITH GOLD DOWN $13.45 TODAY// NO CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL28 WITH GOLD UP $50.20 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL25 WITH GOLD DOWN $49.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVEV WITHDRAWAL OF 3.911 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 948.56 TONNES

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

GLD INVENTORY: 944.26 TONNES, TONIGHTS TOTAL

SILVER

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

APRIL29 WITH SILVER UP $0.30 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.229 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 451.925 MILLION OZ

APRIL28 WITH SILVER DOWN $0.03 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.136 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.696 MILLION OZ

APRIL25 WITH SILVER DOWN $0.44 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 3.639 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.832 MILLION OZ

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

Peter returned to the mic to analyze a volatile week on Wall Street. He unpacks the market’s recent surge, the political pressures buffeting the Federal Reserve, and the deeper consequences of unsound economic policy. From the opaque motives driving central bankers to the misleading optimism embedded in public statements about tariffs and trade, Peter reveals why investors should remain cautious, not complacent.

Peter opens the show with his signature skepticism toward market mood swings, reminding listeners that bear markets are notorious for sharp, misleading rallies:

This is another Sunday night podcast following what was a big turnaround week for the markets. It really started on turnaround Tuesday, but it lasted the entire week. Now, I don’t think it’s a permanent turnaround. I think it’s a bear market rally, a counter trend move in pretty much all of the markets. This is how bear markets work. You get some pretty big short-term counter movements that serve the purpose of creating a false sense of hope that the market is bottomed out.

He critiques Trump’s approach to monetary policy, noting that Trump only wants lower rates for political reasons:

He basically started calling Jerome Powell names, you know, like they’re at a playground, calling him ‘too late Powell.’And he said that Powell needs to cut rates and he can’t go soon enough. We got to get rid of Powell. He’s screwing up by not cutting rates. And so the markets didn’t like that type of pressure on Powell from the White House to not only cut rates but risk being fired if he didn’t.

Peter compares the post-2008 Fed policy to today. He argues that Janet Yellen, who led the Federal Reserve under President Obama, was motivated by politics rather than economics, just like Powell:

I’m sure that he’s not the only one. I’m sure Yellen was very much a team player for Obama. That’s why she never even raised rates once when Obama was president. She kept them at zero the whole time. She didn’t start hiking rates until Trump won. And then she started hiking rates. So she kept rates at zero. That was very political. And Trump was right when he ran against Hillary Clinton back in 2016 for pointing out that the Fed was political.

Turning to the week’s market rally, Peter calls out the engineered optimism around the trade war, warning listeners that it’s built on hollow promises rather than substantive breakthroughs:

But the big movers were in the stock market, and it wasn’t just because of the damage control that was done on Tuesday. We got more crafted statements from the Trump administration, especially, I think, from Scott Bessent, about the trade war and the tariffs, and some positive statements that I think the tariffs will come down soon. Things are going well, the negotiations are going good, so a lot of positive comments that I think were all a bunch of BS. I think these comments were deliberately floated out there to get the markets to rise, to get them to think, oh, okay, it’s almost over, we’re going to know the war is going to be over. And we got this big relief rally really on nothing.

Finally, Peter contends that China might ultimately benefit from disentangling itself from the U.S. financially, a view that breaks sharply with conventional wisdom on global trade. He argues China’s ongoing export relationship is propping up a debtor—one that pays with increasingly dubious U.S. IOUs:

And as far as I’m concerned, in the long run, it’s the best thing that could happen to China. Because China needs to stop trading with the United States to the degree that it does, because we’re screwing them over. Because we’re not paying; we’re just giving them IOUs that are basically not going to be worth anything. So their economy is getting all screwed up, maintaining this vendor financing of a customer that’s never going to pay. And it’s doing real damage to their economy, and the sooner they can repair that damage, the better for them.

If you missed it, make sure you check out Peter’s latest interview on the Young & Profiting podcast!

2, EGON VON GREYERZ

ALASDAIR MACLEOD

3. C Powell and Gata dispatches

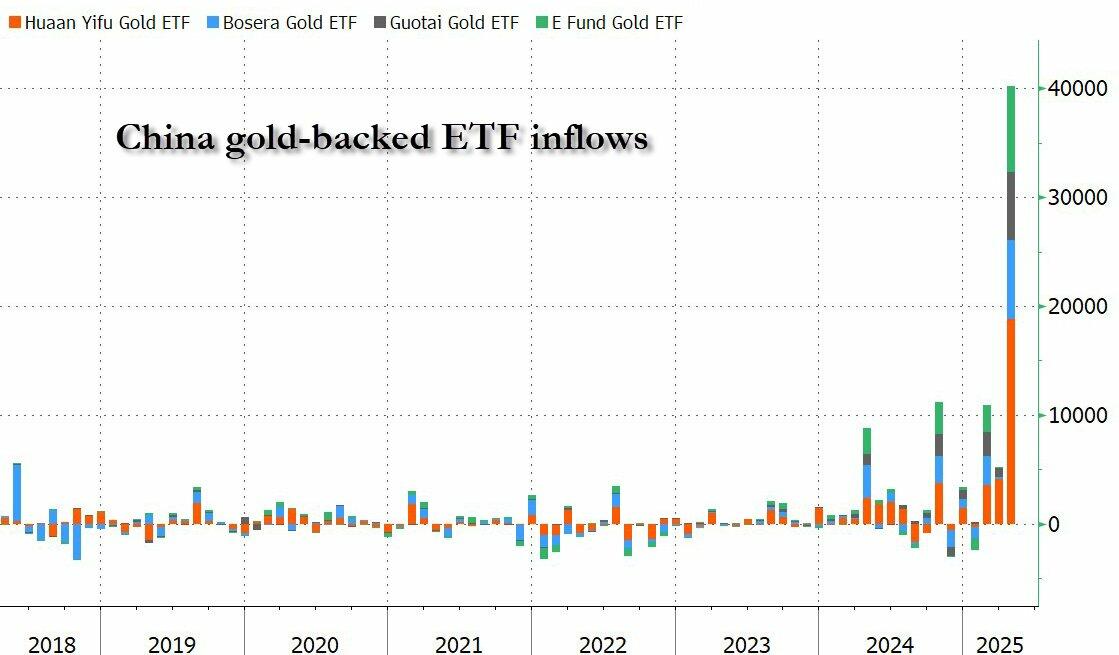

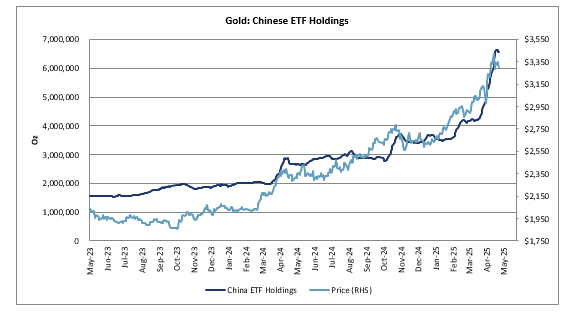

Chinese investors pile into gold funds at record pace

Submitted by admin on Wed, 2025-04-30 02:12 Section: Daily Dispatches

By Leslie Hook and Cheng Leng Financial Times, London Wednesday, April 30, 2025

Chinese investors are piling into gold funds at a record rate, as Donald Trump’s trade war and fears over a U.S. recession and inflation drive a hunt for haven assets.

Inflows into gold exchange traded funds in China total 70 tonnes — or about $7.4 billion — so far this month, more than double the previous monthly record, according to the World Gold Council, an industry body

“Whilst we have seen ETF demand from other regions, China is really in the lead now,” said John Reade, senior market strategist at the WGC, adding that Chinese investment demand for the precious metal had risen “dramatically” this month.

The country’s share of global gold exchange-traded fund holdings has jumped to 6%, up from 3% at the start of this year, while over the past four weeks Chinese demand accounted for more than half of global gold ETF inflows. …

Submitted by admin on Mon, 2025-04-28 17:39 Section: Daily Dispatches

By Jan Nieuwenhuijs Money Metals Exchange, Eagle, Idaho Monday, April 28, 2025

As we are in the final stages of a debt cycle that is causing gold to skyrocket, the question arises: How high can gold go?

Comparing the current bull run to the previous two points to a gold run as high as $16,000 per ounce.

I typically analyze the gold price through a framework of how gold relates to “credit assets” (national currencies, debt securities, equity, etc.). Simplified, trends in the ratio between gold and credit assets tell us where we are in a debt cycle, and where we are in a debt cycle reveals in what direction the gold price is heading.

In an economic boom, capital flows into credit assets (debt), and the gold price stalls. When markets exhibit excessive confidence in credit, financial bubbles tend to form.

When the bubbles pop, investors flock to gold until a new equilibrium is established in the financial system between money without counterparty risk (gold) and assets with counterparty risk (credit). …

Submitted by admin on Sun, 2025-04-27 13:34 Section: Daily Dispatches

By Caitlin McCabe and Joe Wallace The Wall Street Journal via MSN, Redmond, Washington Sunday, April 27, 2025

John Paulson made a vast fortune betting against the U.S. housing market in what was dubbed “the greatest trade ever.” And his next act — a years-long wager on gold — is finally turning out to be a another great trade.

More than a decade and a half after Paulson went big on gold, the billionaire investor has emerged as one of the winners from the record-setting surge in the price of the precious metal.

President Trump’s trade war and threats to fire the head of the Federal Reserve shook confidence in the dollar and propelled gold prices above $3,500 a troy ounce last week. Gold rose this year even as stocks and bonds floundered.

Rather than cashing out, Paulson is doubling down, tossing in $800 million to buy a big stake in a remote gold mine in a rugged region of southwestern Alaska.

“There’s only one reserve that in physical form will protect you against all these things for literally millennia,” said Paulson, rattling off a list of scenarios ranging from inflation to the confiscation of assets by governments. …

Swiss franc’s surge sparks bets for return to negative interest rates

Submitted by admin on Sun, 2025-04-27 10:30 Section: Daily Dispatches

By Emily Herbert, Ian Smith, and Mercedes Ruehl Financial Times, London Sunday, April 27, 2025

The Swiss franc has soared to a decade high against the dollar as investors rush for shelter from the global trade turmoil, sparking bets that the country’s central bank will have to lower interest rates to zero or below to curb the currency’s rise

The currency, historically a financial market haven because of the Alpine country’s political and economic stability, reached near-record strength against the dollar this week, with the greenback sinking close to SFr 0.80 for the first time since the franc’s shock appreciation in 2015.

That has put policymakers in a bind, as they seek to restrain the currency to support the export-heavy economy without provoking a backlash from the United States, which has already threatened Switzerland with high tariffs. …

Former Fed governor Warsh blasts U.S. central bank for leaving its lane

Submitted by admin on Sat, 2025-04-26 10:36 Section: Daily Dispatches

By Francesco Canepa Reuters via Yahoo News, Sunnyvale, California Friday, April 25, 2025

WASHINGTON — Former Federal Reserve Governor Kevin Warsh, with whom President Donald Trump is reported to have discussed firing U.S. central bank chief Jerome Powell and installing him in his place, today unleashed a barrage of criticism of the Fed and argued for fundamental changes to how it operates.

In a speech full of long-standing criticisms but short on specifics for what he would do differently, Warsh said he believes in the Fed’s “operational independence” but argued it has gone beyond its remit and undermined its claims to independence.

“Independence is reflexively declared, all too often in my view, when the Fed is criticized,” he told a conference in Washington organized by the Group of Thirty, an international body of financiers and academics.

He urged the Fed to stop relying on “stale” government data, subject to revision, to guide its decisions, and on letting the public know policymakers’ economic forecasts and where they believe interest rates may be headed. …

Silver supply deficit will break price suppression, First Majestic’s Keith Neumeyer says

Submitted by admin on Fri, 2025-04-25 20:42 Section: Daily Dispatches

8:43p ET Friday, April 25, 2025

Dear Friend of GATA and Gold:

Gold isn’t the only monetary metals market heavily manipulated by bullion banks, First Majestic Silver CEO Keith Neumeyer tells Mike Maharrey on Money Metals Exchange’s weekly market review. Neumeyer says about 300 ounces of “paper” silver — imaginary silver — trade for every ounce of real metal.

But the resulting supply deficit will defeat the manipulation eventually, Neumeyer says, and First Majestic believes in its product’s monetary component, holding silver as a financial asset on the company’s books.

The interview is 42 minutes long and begins at the 7:14 mark at YouTube here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

4. ANDREW MAGUIRE PODCAST 220

END

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//RARE EARTHS

6 CRYPTOCURRENCY NEWS

ASIA TRADING THURSDAY MORNING WEDNESDAY NIGHT

SHANGHAI CLOSED

//Hang Seng CLOSED

// Nikkei CLOSED UP 406.92 PTS OR 1.13% //Australia’s all ordinaries CLOSED UP 0.30%

//Chinese yuan (ONSHORE) CLOSED OFFSHORE CLOSED DOWN TO 7.2735/ Oil UP TO 57.31 dollars per barrel for WTI and BRENT UP TO 59.97 Stocks in Europe OPENED ALL MIXED.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED XXXX (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.2735 (CCP MANIPULATED)

SHANGHAI CLOSED C

HANG SENG CLOSED

2. Nikkei closed UP 406.92 PTS OR 1.13

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 99.61// EURO FALLS TO 1.1325 DOWN 3 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.269//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 144.28…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: XX OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR DOWN this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4470/Italian 10 Yr bond yield U to 3.583 SPAIN 10 YR BOND YIELD DOWN TO 3.111%

3i Greek 10 year bond yield UP TO 3.310

3j Gold at $3230.10 Silver at: 32.10 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 35 /100 roubles/dollar; ROUBLE AT 81.64

3m oil into the 57 dollar handle for WTI and 59 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 144.28// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.269% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8263 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9357 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.147 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.667 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.603 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.46

10 YR UK BOND YIELD: 4.4730 DOWN 2 PTS

10 YR CANADA BOND YIELD: 3.089 DOWN 4 BASIS PTS

5 YR CANADA BOND YIELD: 2.679 DOWN 6 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

US Futures Surge On Blowout Tech Earnings, Erasing April’s Losses

by Tyler Durden

Thursday, May 01, 2025 – 08:26 AM

US equity futures are sharply higher, erasing all of April’s losses on blowout earnings from MSFT and META, and relief over signs the Trump administration is stepping back from its harshest tariff threats. As of 8:00am ET, S&P futures rose 1.2% to 5655, the highest level since before Trump’s Liberation Day announcement and pointing to an eighth consecutive session of gains for the cash index; Nasdaq futures gained 1.7%, as META and MSFT added +6.3% and +7.8%, respectively; most Mag 7 names, NVDA (3.7%) and semis are higher given META’s CapEx increase and MSFT’s reiteration on CapEx guidance. The dollar is higher after the BOJ finally flipped dovish and slashed its growth target pushing USDJPY to 144.5 this morning. It’s light on overnight news as most of Europe is closed today ex-UK along with China; US/Ukraine signed an agreement over the country’s natural resources, UK Manf PMI printed better but remained in contraction, and Trump reiterated that there is a “very good chance” of a deal with China on NewsNation last night. Commodities are mostly lower: WTI -1.2%; Gold -1.7%. The US economic calendar includes weekly jobless claims (8:30am), April manufacturing PMI (9:45am), ISM manufacturing and March construction spending (10am). Fed’s external communications blackout ahead of the May 7 FOMC meeting. Apple and Amazon results are due after the market close.

In premarket trading, the Magnificent Seven are mostly higher: Microsoft (MSFT) gains 8% after the company reported stronger-than-expected quarterly sales and profit growth. Meta (META) jumps 6% after the company’s advertising sales quelled Wall Street concerns about the impact of the Trump administration’s trade war. Apple was the only tech giant in the red, falling 1.4% after a federal judge said in a ruling that it violated a court order requiring it to open up the App Store to third-party payment options (other Mag7s are up Nvidia +4.6%, Amazon +3.7%, Alphabet +1%, Tesla +0.7%). McDonald’s Corp. (MCD) declines 1.4% as sales fell in the first quarter, reflecting a deterioration in consumer sentiment that’s making it harder for restaurants to lure in diners. Eli Lilly & Co. (LLY) drops 5% after the company cut its earnings outlook. Here are some other notable premarket movers:

Align Technology rises 10% after the Invisalign company reported quarterly shipments that beat the average analyst estimate.

Confluent Inc. falls 10% after the provider of a streaming platform gave an outlook for second-quarter subscription revenue that fell shy of expectations. First quarter results showed a slowdown in additions of customers with $100,000 in annual recurring revenue.

CVS Health rises 8% after the company boosted its adjusted earnings per-share-guidance for the full year and reported better-than-expected results for the first quarter

E2open shares are up 34% after WiseTech Global, in response to media reports about its being in discussions to acquire E2open, said it was participating in a strategic review process.

KKR & Co. rises 2% after the investment firm reported assets under management that beat the average analyst estimate. Fee-related earnings also came in above analysts’ expectations.

Qualcomm falls 5% as the biggest maker of chips that run smartphones gave a tepid revenue prediction for the current quarter, underscoring concerns that tariffs will hurt demand for its products.

Robinhood gains 4% after the trading platform’s earnings largely beat expectations, with analysts highlighting positive trends in April amid market volatility and a boost from a lower tax rate.

Shake Shack falls 3% after posting first-quarter results.

Wayfair gains 5% after posting adjusted earnings per share for the first quarter that beat the average analyst estimate.

Tech giants added to investor optimism that deals between the US and its partners would limit the damage from Trump’s trade war. Wall Street ended a tumultuous month on a day in which the S&P 500 erased an intraday drop of more than 2% to close 0.2% higher. Traders sought reassurance in bets on Federal Reserve easing after the US economy contracted for the first time since 2022.

“So far we’re seeing big tech companies deliver on earnings, which is reassuring, and it’s this reassurance which is supporting equity market futures,” said Georgios Leontaris, chief investment officer for EMEA at HSBC Global Private Banking. “The other element of the story beyond earnings is obviously the ongoing debate as to whether we’ve seen peak tariff noise or not.”

Apple results are due after the market close. Analysts will be listening closely for any further detail on how the company, whose supply chain is reliant on China, Vietnam, and India, views the impact of tariffs

The White House said it was nearing an announcement of a first tranche of trade deals with partners that would reduce planned tariffs. Sentiment was also helped by a report that the US has been proactively reaching out to China through various channels. At the same time, Trump said he would not rush deals to appease nervous investors.

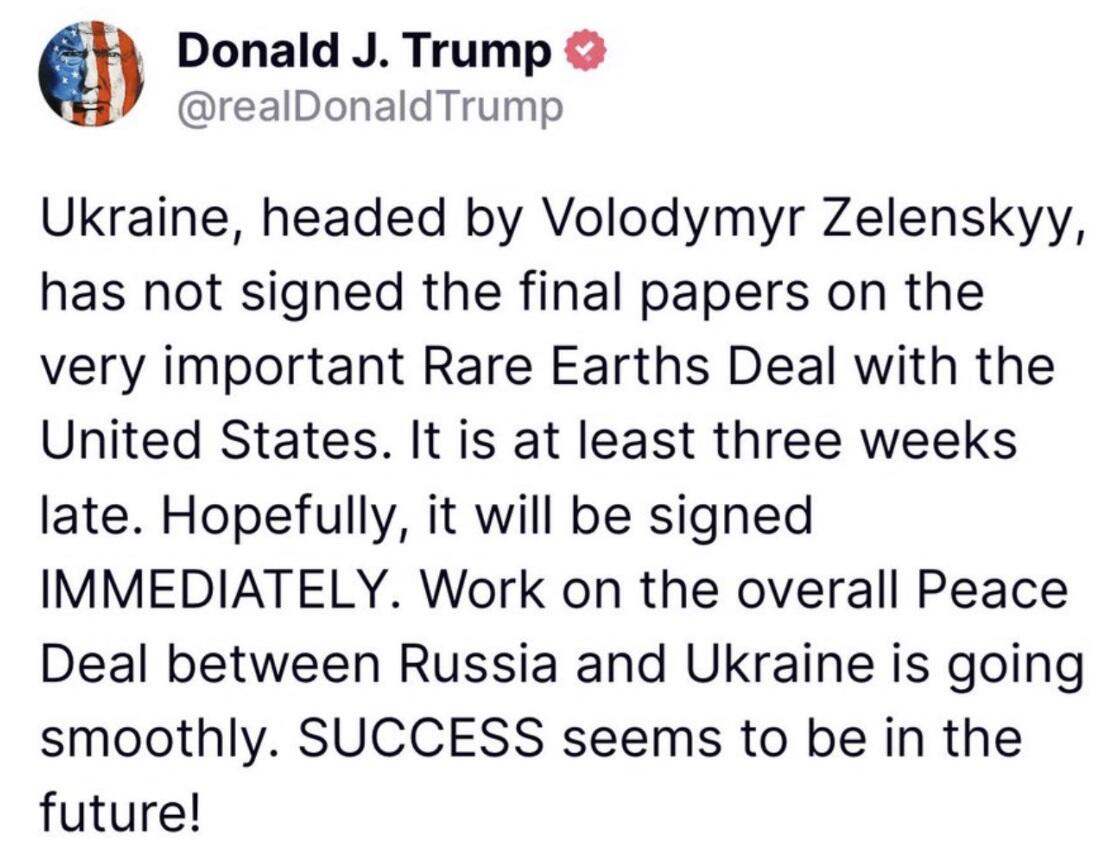

The US and Ukraine reached a deal over access to the country’s natural resources, offering a measure of assurance to officials in Kyiv who had feared Trump would pull back his support in peace talks with Russia.

Elsewhere, most markets in Europe and many in Asia are shut for holidays. The UK’s FTSE 100 index was steady, following 13 days of gains, the longest winning streak since 2017. Gains in material and industrial names are offset by losses in energy and health care.

In FX, the Bloomberg Dollar Spot Index rises 0.3%. the yen is the weakest of the G-10 currencies, falling 0.9% against the greenback after the Bank of Japan pushed back the timing for when it expects to reach its inflation target and slashed its growth forecasts. The pound and euro are little changed.

In rates, treasuries climb, pushing US 10-year yields down 2 bp to 4.14%. Treasury spreads remain within a basis point of Wednesday’s close, as gains remain broad-based across the curve. Gilts are steady, with UK 10-year borrowing costs flat at 4.44%. Treasury futures edge higher into the early US session, on the day’s highs with yields lower by 1bp to 2bp across the curve. US session focus includes weekly jobless claims along with both ISM and PMI manufacturing reports.

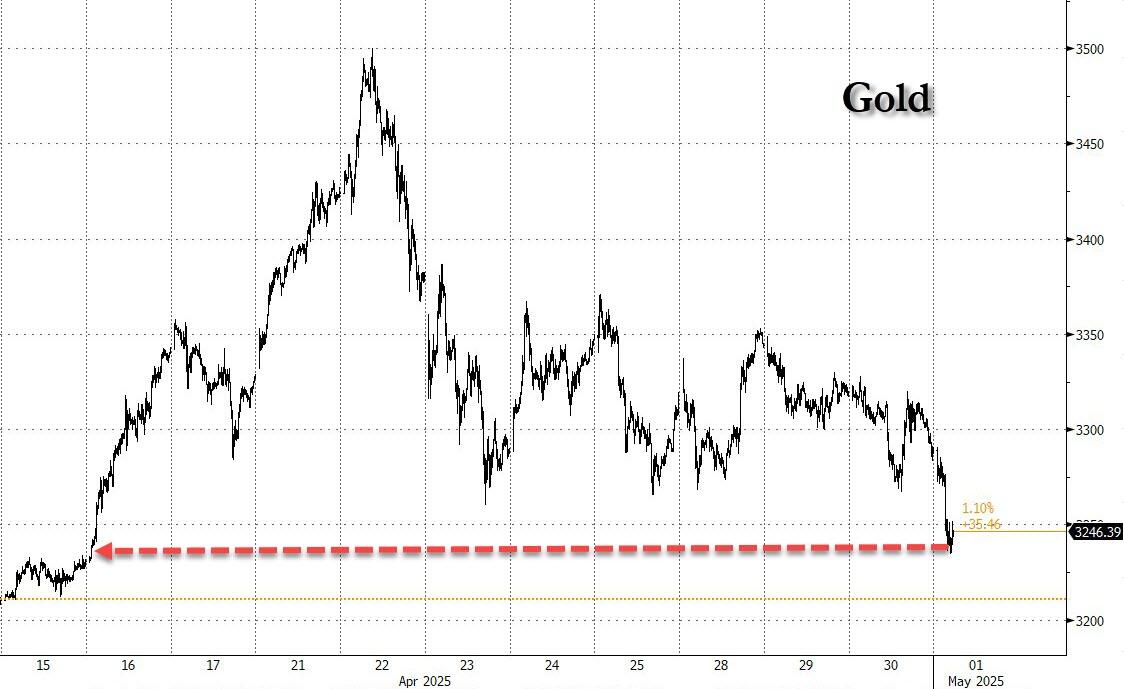

In commodities, oil prices decline, with WTI falling 2.3% to below $57 a barrel; the drop followed the biggest monthly drop since 2021, as signs that the Saudi-led OPEC+ alliance may be entering a prolonged period of higher output added to concerns the trade war will hurt demand. Spot gold is down $65 at $3,223/oz, falling for a third day on signs of potential trade-talk progress between the US and several other nations, quelling demand for havens even as signs of slowdowns have emerged in the largest economies. Bitcoin rises 1% and above $95,000.

Looking at today’s calendar, we get the April Challenger job cuts (7:30am), weekly jobless claims (8:30am), April manufacturing PMI (9:45am), ISM manufacturing and March construction spending (10am). Fed’s external communications blackout ahead of the May 7 FOMC meeting

Market Snapshot

S&P 500 mini +1.2%

Nasdaq 100 mini +1.6%

Russell 2000 mini +0.3%

Stoxx Europe 600 little changed

DAX +0.3%

CAC 40 +0.5%

10-year Treasury yield -2 basis points at 4.15%

VIX -0.9 points at 23.85

Bloomberg Dollar Index +0.2% at 1226.38

euro little changed at $1.1324

WTI crude -2% at $57.02/barrel

Top Overnight news

The US and Ukraine signed an agreement over access to the country’s natural resources. The deal will see the US will get first claim on profits transferred into a jointly managed investment fund that’s intended in part to reimburse the US for future military assistance. BBG

House Republicans are seriously considering proposals to further limit tax deductions that companies can take for their highest-paid workers’ compensation, expanding restrictions that now apply only to a handful of current or former executives making more than $1 million, according to people familiar with the discussions. WSJ

US President Trump said we are going to have ‘Made in the USA’ like never before and he stated give us a little time to get moving regarding the economy. Furthermore, Trump said interest rates should go down and reiterated that “he (Powell) should reduce interest rates, I understand them better than him”, as well as noted it would be nice for people wanting to buy homes and things.

There was some chatter that the House Ways and Means Committee is going to mark up their tax package on May 8th: Punchbowl.

Elon Musk said he’s considering sending DOGE to the Fed, citing a costly renovation of its headquarters as an example of potential government waste. BBG

The yen dropped as much as 1.2% after the BOJ pushed back the timing for when it expects to reach its inflation target and Governor Kazuo Ueda spoke of uncertainties due to tariffs. For now, policymakers kept rates at 0.5%. BBG

China feels the white house is “too divided” on trade policy and will hold off on entering serious trade talks with the US while it waits to see which of Trump’s advisors will have his ear and how other countries respond to the 90 day pause on tariffs. SCMP

Saudi Arabian officials are briefing allies and industry experts to say the kingdom is unwilling to prop up the oil market with further supply cuts and can handle a prolonged period of low prices, five sources with knowledge of the talks said. This possible shift in Saudi policy could suggest a move toward producing more and expanding its market share, a major change after five years spent balancing the market through deep output as a leader of the OPEC+ group of oil producers. RTRS

The EU is planning to share a paper with the US next week that will set out a package of proposals to kick-start trade negotiations with the Trump administration. The paper will propose lowering trade and non-tariff barriers, boosting European investments in the US, cooperating on global challenges such as tackling China’s steel overcapacity and purchasing US goods like liquefied natural gas and technologies. BBG

Janet Yellen has warned that Trump’s tariffs will have a “tremendously adverse” impact on the US economy as they “hobble” companies that rely on critical mineral supplies from China. She added: “I’m not yet ready to say that I’m forecasting a recession, but certainly the odds have gone way up. FT

Microsoft beat estimates and showed strong growth in its key Azure cloud business, while Meta also topped estimates and raised its full-year capex forecast as it continues to invest in AI. With first-quarter earnings in full swing the scorecard so far has shown resilience amid Trump’s trade war. The next big test comes after the close, when Apple and Amazon report. BBG

Tariffs/Trade