MAY 8/MASSIVE T.A.S. CONTRACTS INITIATED YESTERDAY AND THAT LED TO TODAY’S RAID: GOLD FELL BY $82.60 TO $3301.90 WHILE SILVER WAS DOWN 16 CENTS TO $32.44/PLATINUM WAS DOWN 90 CENTS TO $983.60 WHILE PALLADIUM WAS DOWN $5.70 TO $973.75//BIG NEWS OF THE DAY ANNOUNCED BY TRUMP OF A TRADE DEAL WITH THE UK//MORE UPDATES ISRAEL VS HAMAS//STORIES ON SAUDI ARABIA/ISRAEL VS HEZBOLLAH AND HAMAS//ISRAEL VS HOUTHIS//COVID UPDATES/VACCINE INJURY REPORTS/SLAY NEWS/NEWS ADDICTS//EVOL NEWS/INDIA VS PAKISTAN ENGAGE IN A AIR DOGFIGHT//SWAMP STORIES FOR YOU TONIGHT//

132 C SG AMERICAS 6 190 H BMO CAPITAL MARKETS 947 323 C HSBC 2 363 H WELLS FARGO SECURITI 227 661 C JP MORGAN SECURITIES 558 48 685 C RJ OBRIEN 2 690 C ABN AMRO CLR USA LLC 5 726 C PLUS500US FINANCIAL 1 737 C ADVANTAGE FUTURES 3 1 880 H CITIGROUP 202 905 C ADM 8

TOTAL: 1,005 1,005 MONTH TO DATE: 15,951

JPMORGAN STOPPED 48/1005

MAY

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 1005 NOTICES FOR 100,500 OZ 3.126 TONNES

total notices so far: 15,951 contracts for 1,595,100 OR 49.614 tonnes)

FOR MAY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 230 NOTICE(S) FILED FOR 1.150 MILLION OZ/

total number of notices filed so far this month : 13,581 CONTRACTS (NOTICES) for 69.905 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $82.60 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.23 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 937.67 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.16 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV: //

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 448.783 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1327 CONTRACTS TO 139,208 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS OF $0.54 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A HUGE SIZED LOSS OF 1172 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL 155 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING WEDNESDAY AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON WEDNESDAY WITH SILVER’S HUGE LOSS IN PRICE AND THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH A HUGE T.A.S. ISSUANCE OF 838 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A SMALL 155 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 838 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUGE SIZED 1172 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.54.

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS MUST NOW BE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE 838 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.54) AND WERE SUCCESSFUL IN KNOCKING OFF SOME NET SILVER LONGS FROM THEIR PERCH

WE HAD A SMALL 155 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 67.830 MILLION OZ TO WHICH WE ADD OUR 219 CONTRACT QUEUE JUMP OF 1.095 MILLION OZ AND THEN WE MUST ADD THOSE CRAZY CONTRACT EXCHANGE FOR RISK FOR 12.93 MILLION OZ

INITIAL STANDING FOR MAY: 71.690 MILLION OZ WHICH INCLUDES TODAY’S 1.095 MILLION QUEUE JUMP + 12.93 MILLION OZ (EX FOR RISK) EQUALS 84.62 MILLION OZ./

WE HAD:

/ HUGE COMEX OI LOSS+// A SMALL SIZED EFP ISSUANCE (155 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 838 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 199 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 6 DAYS, total 1849 contracts: OR 9.245 MILLION OZ (370 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 9.245 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 9.245 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1172 CONTRACTS WITH OUR HUGE LOSS IN PRICE OF $0.54 IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. . THE CME NOTIFIED US THAT WE HAD A SMALL 155 CONTRACT EFP ISSUANCE CONTRACTS: 155 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND NOW MAY:

NEW STANDING FOR MAY: 71.690 MILLION OZ. (INCLUDES 1.095 MILLION OZ QUEUE JUMP + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE.//NEW TOTAL STANDING 84.62 MILLION OZ

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (838 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TODAY’S TRADING (THURSDAY TRADING) AND BEYOND.

WE HAD 230 NOTICE(S) FILED TODAY FOR 1.150 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 8582 OI CONTRACTS TO 443,832 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A SMALL 503 CONTRACTS //.

WE HAD A STRONG SIZED DECREASE IN COMEX OI (8582 CONTRACTS) . THIS OCCURRED WITH OUR LOSS OF $30.30 IN PRICE WEDNESDAY. ON WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER..

WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES/) TO WHICH WE ADDED + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

FINAL STANDING FOR APRIL; 201.443 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

INITIAL STANDING FOR MAY: 49.822 TONNES OF GOLD!

/ ALL OF THIS HAPPENED WITH OUR $30.30 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX ///. WE HAD A STRONG SIZED LOSS OF 8167 OI CONTRACTS (25.402 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AS WELL AS THE SAME FOR APRIL AND NOW MAY….. A MONSTROUS 49.822 TONNES DESPITE IT BEING AN OFF MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 415 CONTRACT:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 444,355/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 139,208 CONTRACTS!!

IN ESSENCE WE HAVE A VERY STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8167 CONTRACTS WITH 8582 CONTRACTS DECREASED AT THE COMEX// AND A SMALL SIZED 415 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 8167 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A MEGA MEGA HUGE SIZED AND CRIMINAL 54,145 CONTRACTS ISSUED, THE HIGHEST AMOUNT EVER IN COMEX HISTORY. WE HAD HUGE T.A.S. LIQUIDATION DURING THE COMEX SESSION WEDNESDAY

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (415 CONTRACT) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 8582 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 8167 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING FOR GOLD FOR MAY AT 49.822 TONNES ( WHICH WHICH INCLUDES OUR 3.02628 TONNES QUEUE JUMP)

NEW STANDING FOR GOLD, MAY CONTRACT ADVANCES TO: 49.822 TONNES OF GOLD.

.

/ 3) HUGE T.A.S. LIQUIDATION IN REMOVING SOME NET SPECULATOR LONGS, AS WE HAD 1)A $30.30 COMEX PRICE LOSS.. WE HAD 2) SOME NET LONG SPECS BEING CLIPPED WITH OUR STRONG LOSS OF 7664 CONTRACTS ON OUR TWO EXCHANGES// /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY.

4) STRONG SIZED COMEX OI LOSS// 5) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (1218 CONTRACTS)/// MEGA MEGA HUGE T.A.S. ISSUANCE: 54,145 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAY INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 4438 CONTRACTS OR 443,800 OZ OR 13.804 TONNES IN 6 TRADING DAY(S) AND THUS AVERAGING: 739 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN6 TRADING DAY(S) IN TONNES 13.804 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 13.804 TONNES DIVIDED BY 3550 x 100% TONNES = 0.388% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 13.804 TONNES OF GOLD EFP ISSUANCE

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1327 CONTRACTS OI TO 138,934 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 155 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 155 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 155 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1327 CONTRACTS AND ADD TO THE 155 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1172 CONTRACTS WITH THE HUGE LOSS IN PRICE OF $0.54 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 5.860 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 9.33 PTS OR 0.280%

//Hang Seng CLOSED UP 84.04 PTS OR .37%

// Nikkei CLOSED UP 84.04 PTS OR .37% //Australia’s all ordinaries CLOSED UP .26%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.2367 OFFSHORE CLOSED DOWN AT 7.2379 / Oil UP TO 58.66 dollars per barrel for WTI and BRENT UP TO 61.60 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN TRADING AT 7.2367 AND WEAKER//OFF SHORE YUAN TRADING DOWN 7.2378 AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED8582 CONTRACTS TO 443,832 WITH OUR HUGE LOSS IN PRICE OF $30.30 WITH RESPECT TO WEDNESDAY’S // TRADING. WE LOST SOME NUMBER OF NET LONGS WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (415 ).

THE CME ANNOUNCED WEDNESDAY NIGHT, A 0 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR 0.0 TONNES. TOTAL ISSUANCE FOR MAY IS ZERO. IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST THREE PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

AND NOW WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

MAY: 0 ISSUED SO FAR…

DETAILS ON MAY COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 8582 CONTRACTS WITH OUR HUGE LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON WEDNESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF APRIL AND ONTO MAY, CONTINUED TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. HOWEVER TODAY’S NUMBER IS A HUMDINGER AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 54,145 CONTRACTS, THE HIGHEST NUMBER BY FAR IN COMEX HISTORY. NATURALLY THAT SIGNALS THAT WE WILL WITNESS CONTINUAL RAIDS AND FOR THE NEXT 4 DAYS IF HISTORY SERVES US WELL ANOTHER 4 MEGA MEGA ISSUANCE… (FROM JANUARY 2025 THROUGH TO MARCH 2025 WE HAD THESE 5 MEGA MEGA 30,000+ ISSUANCES WHICH DISTORTED OPEN INTEREST GREATLY

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY AS YOU WILL SEE BELOW ANOTHER MASSIVE QUEUE JUMP OCCURRED ON MAY’S DELIVERY CYCLE WITH ANOTHER HUGE QUEUE JUMP RECORDED WEDNESDAY NIGHT AT 6.4634 TONNES, THE HIGHEST EVER QUEUE JUMP RECORDED IN COMEX GOLD HISTORY. TODAY’S QUEUE JUMP IS ALSO HUGE AT.3.2628 TONNES

THE TONNAGE STANDING FOR GOLD FOR MAY IS NOW 49.822 TONNES (WHICH INCLUDES TODAY’S MASSIVE QUEUE JUMP)

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 221 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 415 EFP CONTRACT WAS ISSUED: : /JUNE 415 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 415 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 8167 CONTRACTS IN THAT 415 CONTRACT LONG WAS TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 8582COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR HUMONGOUS LOSS IN PRICE OF $30.30 /// WEDNESDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. LOOKS LIKE THE SHORT RATS ARE FLEEING THE ARENA AS EVIDENCED BY THE LOWER OPEN INTEREST AT THE COMEX!

WE HAD :

HUGE LIQUIDATION OF OUR T.A.S. SPREADERS

SOME SPEC LIQUIDATION

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A MEGA MEGA HUGE SIZED 54,145 CONTRACTS AND AS MENTIONED ABOVE, THE HIGHEST EVER ISSUANCE IN COMEX HISTORY.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL AND MAY

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE

FINAL STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (209.573 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 5 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY:

INITIAL STANDING AT 28.945 INITAL GOLD TONNES STANDING FIRST DAY NOTICE PLUS 6.4634 TONNES QUEUE JUMP MAY 7 (A RECORD) + ANOTHER HUGE QUEUE JUMP MAY 8 OF 3.2628 TONNES = 49.822 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 209.953 TONNES (INCLUDES 8.3571 TONNES EX FOR RISK/AND ALL MONTHLY QUEUE JUMPING)

MAY: STANDING NOW 49.822 TONNES (INCLUDES ALL QUEUE JUMPING)

COMEX GOLD TRADING/MAY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $30.30/ /)AND THEY WERE A SUCCESSFUL IN KNOCKING OFF SOME APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A VERY STRONG SIZED LOSS IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION WEDNESDAY BUT THEY ARE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,400 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS IT LOOKS LIKE THEY ARE NOW SUCCEEDING AS GOLD ATTEMPTS TO BREACH THAT 3400 DOLLAR BARRIER AGAIN AS IT IS NOW TRADING EARLY MORNING WELL BELOW TO THAT LEVEL AT $3,353.00 DOWN $12 DOLLARS ON THE DAY.

WEDNESDAY NIGHT/THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /MAY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK = ZERO SO FAR!

HERE IS WHAT HAPPENED LAST MONTH; FINAL GOLD STANDING FOR APRIL:

APRIL: 201.573 TONNES +(8.3571 EX FOR RISK// FOR APRIL DELIVERY MONTH =209.953 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS MAY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// MAY COMEX CONTRACT

WE HAVE LOST A STRONG SIZED TOTAL OF 23.838 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY FIRST RECORDED AT 28.945 TONNES ON FIRST DAY NOTICE. WE HAD A MASSIVE 1049 CONTRACT QUEUE JUMP FOR 104,900 OZ OR 3.2628 TONNES. THIS QUEUE JUMP IS CENTRAL BANKS JUMPING AHEAD OF US MORTALS DEMANDING GOLD FOR THEIR RESERVES. THUS NEW STANDING ADVANCES TO 49.822 TONNES OF GOLD.

THUS MAY STANDING FOR GOLD SO FAR: 46.687 TONNES

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $30.30

WE HAD A SMALL 503 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 8167 CONTRACTS OR 816.700 0Z (25.402 TONNES)

confirmed volume WEDNESDAY 389,124.. contracts: GOOD volume////

a)) out of ASAHI 32,016.960 oz b) Out of Brinks: 341,925.880 oz (10,635 kilobars) c) Out of HSVC enhanced: 95,796.750 oz (239 London good delivery bars) d) Out of JPMorgan: 482.265 oz (15 kilobars) e) Out of JPMorgan enhanced: 133,827.320 oz (334 London good delivery bars)

total weight/withdrawal: 604,049.155 oz (18.788 tonnes of gold) absolutely huge

Deposit to the Dealer Inventory in oz

0 ENTRIES

Deposits to the Customer Inventory, in oz

we have 1 customer entry

i)Into Stonex enhanced: 3981.000 oz

10 London good delivery bars.

weight:.1238 tonnes

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

1005 notice(s) 100,500 OZ 3.126 TONNES

No of oz to be served (notices)

67 contracts 6700 OZ 0.2083 TONNES

Total monthly oz gold served (contracts) so far this month

15,951 notices 1,595,100 oz 49.614 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

we have 1 customer entry

i)Into Stonex enhanced: 3981.000 oz

10 London good delivery bars.

weight:.1238 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals/ customer (eligible category)

withdrawals:

4 entries

a) out of Brinks 96,453.000 oz (3000 kilobars)

b) Out of HSBC enhanced: 72,613.125 oz (181 London good delivery bars)

c) Out of JPMorgan: 241,549.015 oz

d) Out of Manfra: 144,030.830 oz (4480 kilobars)

total weight/withdrawal: 554,645.970 oz (17,25 tonnes of gold) absolutely huge

adjustments: 0//

AMOUNT OF GOLD STANDING FOR MAY

THE FRONT MONTH OF MAY STANDS AT 1072 CONTRACTS FOR A LOSS OF 1117 CONTRACTS. WE HAD 2121 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED A HUGE 1049 CONTRACTS AND THUS WE WITNESS A MASSIVE 104,900 OZ QUEUE JUMP FOR 3.2628 TONNES.

JUNE LOST A HUMDINGER OF 22,250 CONTRACTS TO 283,553. JUNE BECOMES OUR NEW FRONT MONTH AND THIS MONTH WILL BE A WHOPPER OF A DELIVERY MONTH. THE FRBNY IS QUITE NERVOUS LOOKING AT JUNE OI.

JULY GAINED 597 CONTRACTS TO STAND AT 1200

We had 1005 contracts filed for today representing 100,500 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 558 notices issued from their client or customer account. The total of all issuance by all participants equate to 1005 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 48 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY /2025. contract month, we take the total number of notices filed so far for the month (15,951 X 100 oz ) to which we add the difference between the open interest for the front month of MAY (x1072 CONTRACTS) minus the number of notices served upon today (1005 x 100 oz per contract) equals 1,601,800 OZ OR 49.822 TONNES

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (15,951 x 100 oz +we add the difference for front month of MAY (1072 OI} minus the number of notices served upon today (1005 x 100 oz) which equals 1,601,800 OZ OR 49.822 TONNES

TOTAL COMEX GOLD STANDING FOR MAY.: 49.822 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..

JPMorgan has a total silver weight: 214.018million oz/502.80 oz million or 42.56%

TOTAL REGISTERED SILVER: 166.981 MILLION OZ//.TOTAL REG + ELIGIBLE. 502.800Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2025 OI: 987 OPEN INTEREST CONTRACTS FOR A GAIN OF 73 CONTRACTS. WE HAD 146 NOTICES FILED ON WEDNESDAY SO WE GAINED 219 CONTRACTS WHICH UNDERWENT A STRONG QUEUE JUMP OF 1.095 MILLION OZ WHERE THESE BOYS HAVE DECIDED TO TAKE DELIVERY OVER HERE. I MUST REPORT WE HAD 0 EXCHANGE FOR RISK ISSUANCE. THUS THE NEW TOTAL REMAINS AT TWO ISSUANCES OF EXCHANGE FOR RISK IS 12.93 MILLION OZ.

JUNE SAW A LOSS OF 54 CONTRACTS DOWN TO 3183 CONTRACTS.

JULY LOST 2144 CONTRACTS DOWN TO 109,220

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 230 or 1.150 MILLION oz

CONFIRMED volume; ON WEDNESDAY 140,261 monstrous//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 13,581 X5,000 oz = 67.905 MILLION oz

to which we add the difference between the open interest for the front month of MAY (987) AND the number of notices served upon today (230 )x (5000 oz)

Thus the standings for silver for the MAY 2025 contract month: (13,581) Notices served so far) x 5000 oz + OI for the front month of MAY(987) minus number of notices served upon today (230)x 5000 oz equals silver standing for the MAY contract month equating to 71.690 MILLION OZ . THEN WE MUST ADD OUR NEW 12.93 TONNES OF EXCHANGE FOR RISK. NEW TOTAL STANDING FOR SILVER: 84.62 MILLION OZ

New total standing: 54.830 million oz which is huge for this active delivery month of MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 166.981million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

MAY 8 WITH GOLD DOWN $82.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.23 TONNES OF GOLD WITHDRAWN FROM THE GLD/ ///INVENTORY RESTS AT 937.67 TONNES

MAY 7 WITH GOLD DOWN $30.30 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 937.96 TONNES

MAY 6 WITH GOLD UP $101.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 937.96 TONNES

MAY 5 WITH GOLD UP $77.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.13 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.28 TONNES

MAY 2 WITH GOLD UP $ 18.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 945.41 TONNES

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

APRIL29 WITH GOLD DOWN $13.45 TODAY// NO CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL28 WITH GOLD UP $50.20 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL25 WITH GOLD DOWN $49.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVEV WITHDRAWAL OF 3.911 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 948.56 TONNES

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

GLD INVENTORY: 937.67 TONNES, TONIGHTS TOTAL

SILVER

MAY 8 WITH SILVER DOWN $0.16/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 7 WITH SILVER DOWN $0.54/NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 6 WITH SILVER UP $0.92 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A HUG WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 5 WITH SILVER UP $0.08 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF 0.117 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.602 MILLION OZ

MAY 2 WITH SILVER DOWN $0.19 /MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 4.545 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.424 MILLION OZ

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

APRIL29 WITH SILVER UP $0.30 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.229 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 451.925 MILLION OZ

APRIL28 WITH SILVER DOWN $0.03 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.136 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.696 MILLION OZ

APRIL25 WITH SILVER DOWN $0.44 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 3.639 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.832 MILLION OZ

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

CLOSING INVENTORY 448.783 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

MISH SHEDLOCK

2, EGON VON GREYERZ

ALASDAIR MACLEOD

3. C Powell and Gata dispatches

4. ANDREW MAGUIRE PODCAST 221

LIVE FROM THE VAULT NO 221 WITH ANDREW MAGUIRE

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//RARE EARTHS

6 CRYPTOCURRENCY NEWS

ASIA TRADING THURSDAY MORNING WEDNESDAY NIGHT

SHANGHAI CLOSED UP 9.33 PTS OR 0.280%

//Hang Seng CLOSED UP 84.04 PTS OR .37%

// Nikkei CLOSED UP 84.04 PTS OR .37% //Australia’s all ordinaries CLOSED UP .26%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.2367 OFFSHORE CLOSED DOWN AT 7.2379 / Oil UP TO 58.66 dollars per barrel for WTI and BRENT UP TO 61.60 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN TRADING AT 7.2367 AND WEAKER//OFF SHORE YUAN TRADING DOWN 7.2378 AGAINST US DOLLAR/ AND THUS WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2367 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.2379 (CCP MANIPULATED)

SHANGHAI CLOSED UP 9.33 PTS OR 0.28%

HANG SENG CLOSED UP 84.04 PTS OR .37%

2. Nikkei closed UP 148.97 PTS OR .41%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 99.99// EURO RISES TO 1.1287 DOWN 16 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.337//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 144.95…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5075/Italian 10 Yr bond yield DOWN to 3.576 SPAIN 10 YR BOND YIELD DOWN TO 3.158%

3i Greek 10 year bond yield DOWN TO 3.331

3j Gold at $3344.65 Silver at: 32.33 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 72 /100 roubles/dollar; ROUBLE AT 82.25

3m oil into the 58 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 144.95// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.337% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8263 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9327 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.313 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.807 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.8223 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.64

10 YR UK BOND YIELD: 4.5080 UP 5 PTS

10 YR CANADA BOND YIELD: 3.098 DOWN 5 BASIS PTS

5 YR CANADA BOND YIELD: 2.707 DOWN 4 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

Futures, Global Markets Jump On Trump Trade Deal With UK

Thursday, May 08, 2025 – 08:24 AM

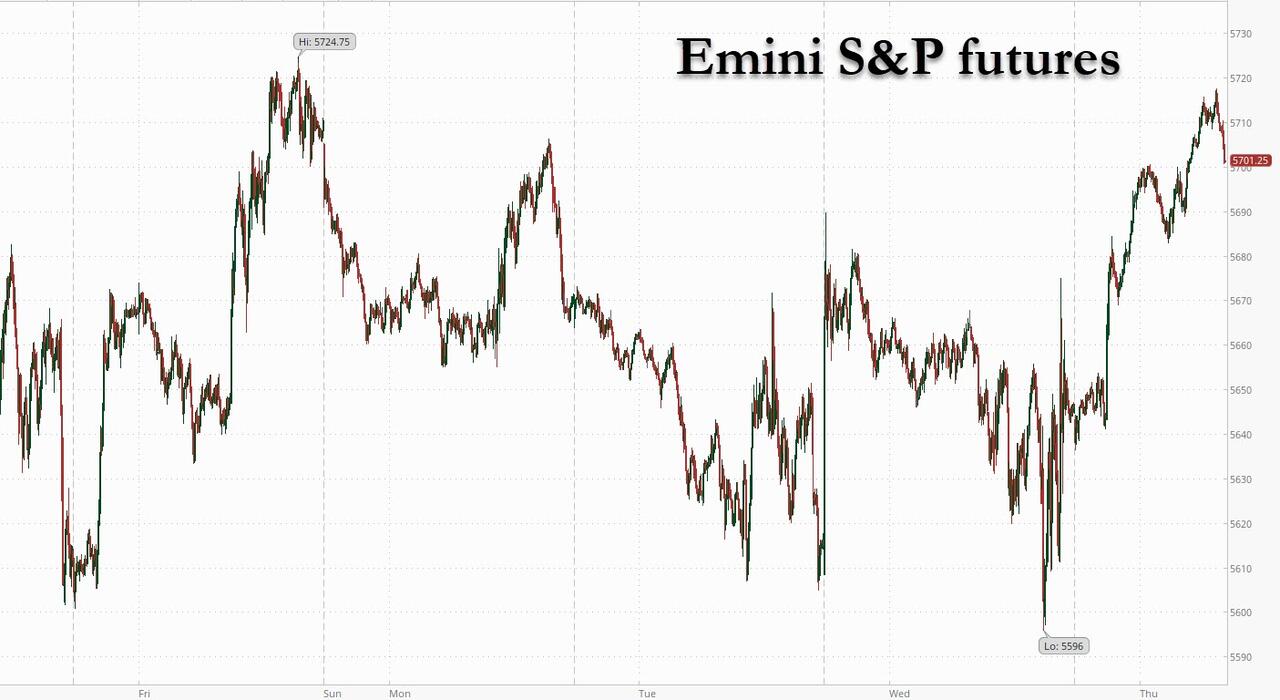

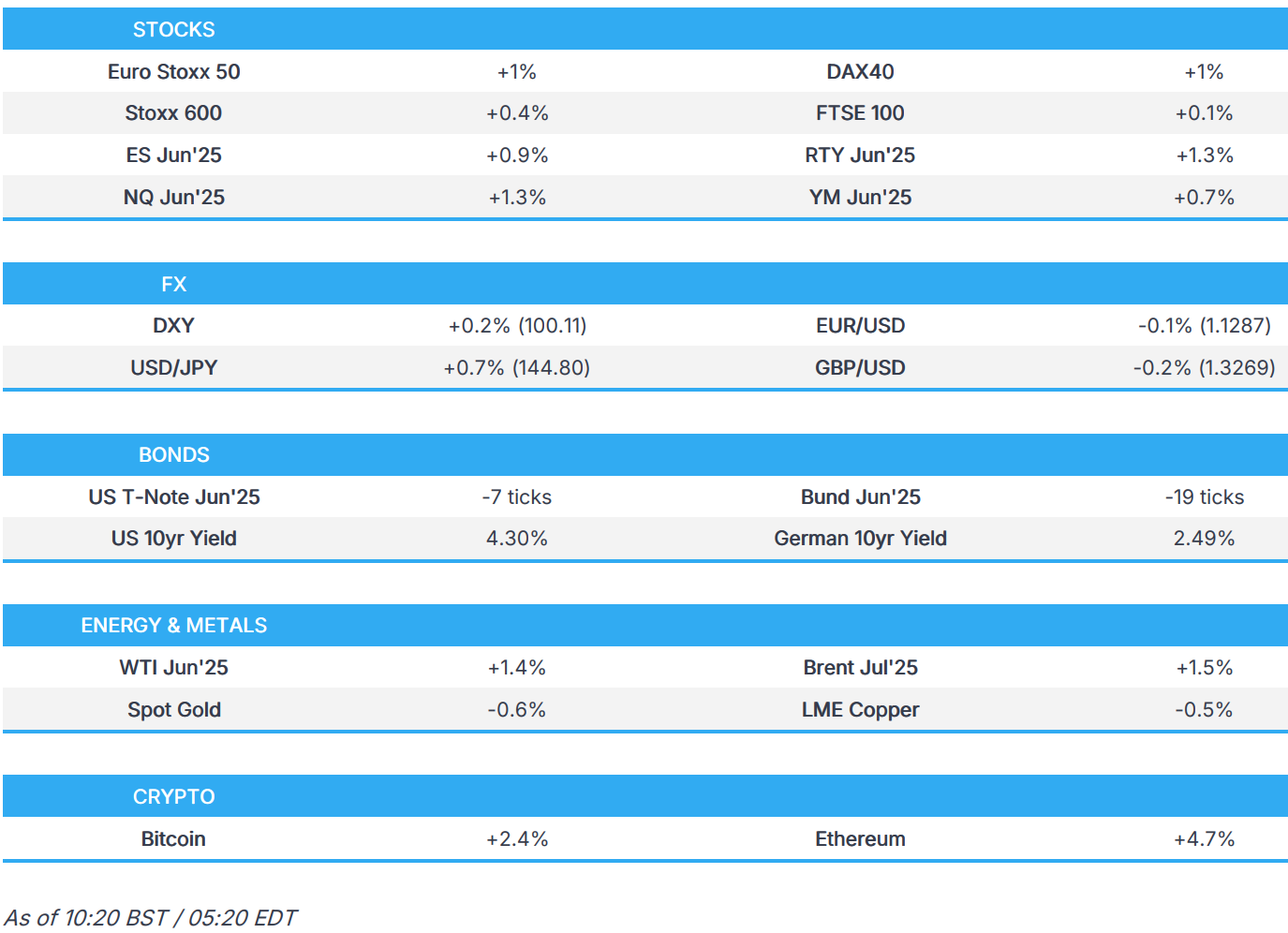

US equity futures storm higher, and are back to their post-Liberation Day highs on positive trade news (Imminent “comprehensive” trade agreement with UK the first of his promised deals; removal of chip export restrictions) and a neutral Fed (economy has strength to wait to see trade war impact hit hard data) even as China again reiterated that the US should cancel unilateral tariffs ahead the first official meeting between the countries this weekend amid reports the US is considering exempting child-related goods from its 145% tariffs on China. As of 8:00am ET, S&P futures rose 0.9% while Nasdaq futures are 1.2% higher, both near session highs. Elsewhere FTSE +40bps, DAX +1.2%, CAC +1%, Shanghai +28bps, Hang Seng +37bps, Nikkei +41bps. Intel rose more than 3% in premarket trading, while peers such as Nvidia and Micron also gained on news Trump will rescind restrictions regulating the export of semiconductors to various countries. Outside of tariffs, Norway and Sweden central banks left rates unch (expected) while we get the BoE this morning (25bps cut expected). US Bond yields are 4-5bp higher across the curve and USD is poised to have its best day 6 sessions with DXY +50bp. Today’s macro data focus is on jobless claims, NY Fed 1-year inflation expectations, and labor costs.

In premarket trading, Mag 7 stocks climb as the Trump administration plans to rescind some Biden-era AI chip curbs as part of a broader effort to revise global semiconductor trade restrictions (Nvidia +1.6%, Alphabet +1.9%, Meta +2%, Tesla +1.3%, Apple +1%, Amazon +1.6%, Microsoft +0.9%). Cryptocurrency-exposed stocks rise as Bitcoin approaches the $100,000 mark for the first time since February as global trade tensions show signs of easing. AppLovin climbs 14% after the AI-powered advertisement platform reported first-quarter results that beat expectations. Arm Holdings tumbled 9% after giving a disappointing sales forecast for the current quarter, stoking concerns about a tariff-fueled slowdown for the chip industry. Here are some other notable premarket movers:

Carvana (CVNA) rises 4% after the online used-car retailer doubled its profits in the first quarter with record vehicle volume.

Coherent (COHR) gains 6% after the semiconductor device company reported third-quarter results that beat expectations

Dave Inc. (DAVE) rises 28% after the digital banking services company boosted its revenue and adjusted Ebitda forecast for the full year, surpassing expectations.

Eli Lilly (LLY) drops 1.5% and AbbVie (ABBV) dips 1.7% following a Politico report that President Donald Trump plans to revive an effort to dramatically slash drug costs by tying the amount the government pays for some medicines to lower prices abroad.

Fortinet (FTNT) tumbles 8% after the security software company reported its first-quarter results and gave an outlook

Fluence Energy Inc. (FLNC) falls 15% after the provider of energy storage systems cut its total revenue guidance range for the full year, a reduction of $700m at the midpoint.

Fortinet (FTNT) tumbles 14% after the security software company reported its first-quarter results that Jefferies says missed “elevated investor expectations.”

Krispy Kreme Inc. (DNUT) falls 19% after saying the company will no longer pay quarterly cash dividends in order to pay down its debt and focus on growth.

Magnite Inc. (MGNI) rises 11% after the advertising technology company reported first-quarter results that beat expectations on profitability metrics. It also said it was taking a cautious approach in its outlook given tariff-related uncertainty, a move analysts support.

MercadoLibre (MELI) climbs 8% after the e-commerce and fintech giant beat analysts’ expectations in the first quarter of the year, delivering strong growth in its credit portfolio.

Peloton Interactive Inc. (PTON) falls 4% after reporting that revenue sank 13% last quarter, marking the third straight year-on-year decline in sales.

Shopify Inc. (SHOP) slips 8% after projected sales in the current quarter that just met expectations, suggesting steep tariffs on goods from China present a challenge.

Tapestry Inc. (TPR) gains 9% after the handbag maker raised its annual outlook, shrugging off broader concerns about worsening consumer sentiment and the trade war.

Tutor Perini Corp. (TPC) climbs 15% after the construction company boosted its year profit outlook. First quarter revenue increased 19% from the year-ago period and beat estimates.

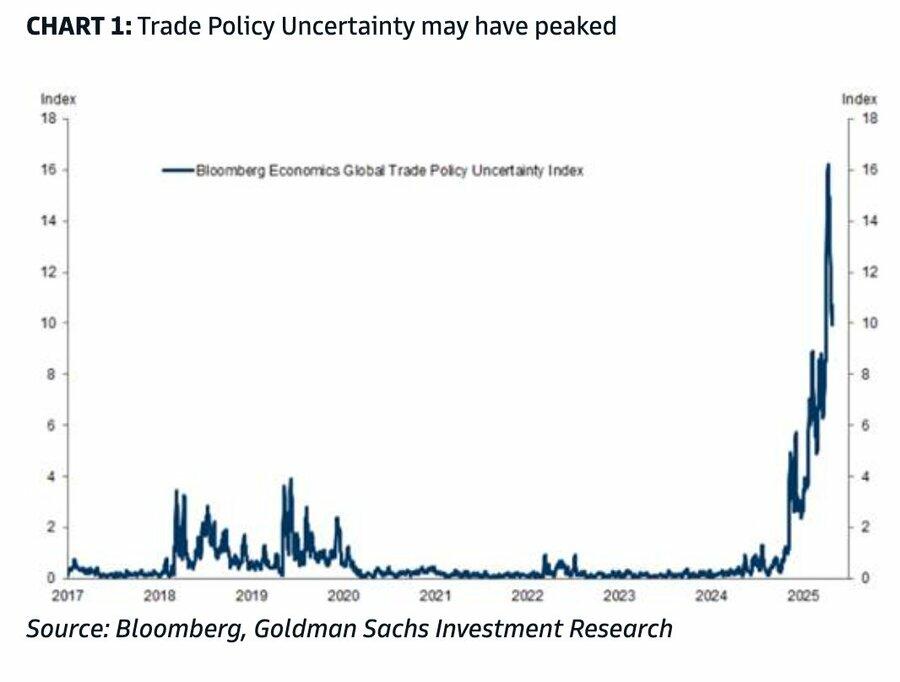

Global markets were lifted after Trump administration’s plan to rescind some Biden-era curbs on chipmakers and news of a trade agreement with Britain, which followed news that US and Chinese officials will meet this weekend to discuss trade. Investors are waiting to see if crippling levies mooted by Trump will be negotiated down, averting lasting damage to economic growth and corporate profits.

“The fear has been of higher prices, company profit margins being squeezed, and the economy going into recession as a result of higher tariffs,” said Kenneth Broux, a strategist at Societe Generale. “If you start unwinding all of that, it’s got to be bullish for risk assets.”

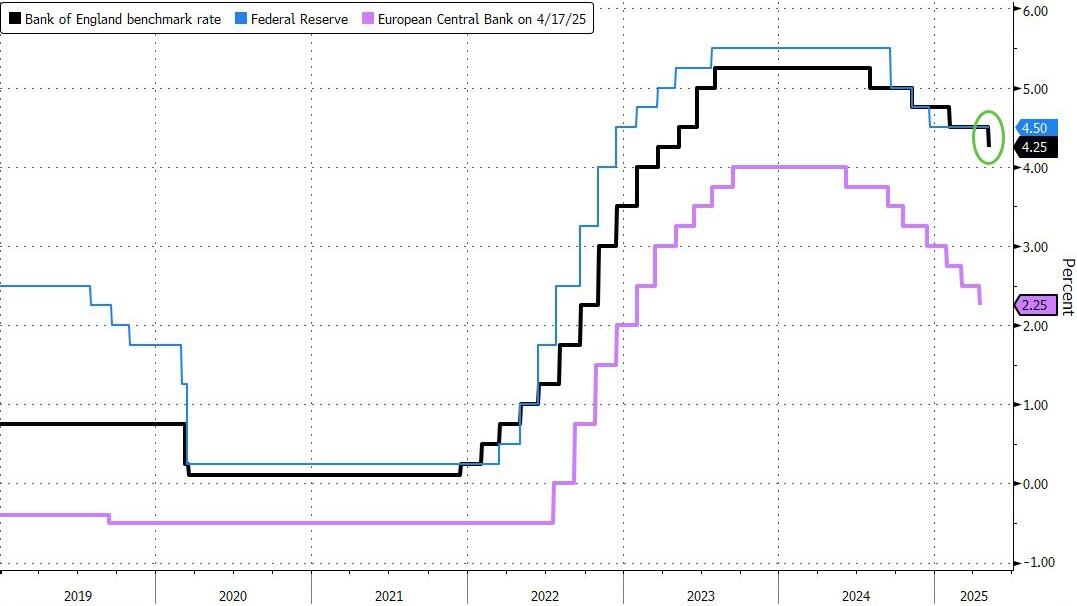

In the UK, gilt yields rose about five basis points, reversing an earlier slide, after the BOE reduced interest rates to 4.25% in a decision made before the US trade deal was announced. However, the BOE upgraded its annual growth forecast for 2025 while two officials voted not to cut rates this time due to inflation risks and a recent easing in financial conditions.

For Neil Birrell, chief investment officer at Premier Miton Investors, the split BOE vote “goes to show the scale of the uncertainty that exists amongst a key group, namely the actual setters of policy. It’s going to be difficult to make a call on future policy on the back of that.”

Meanwhile, while there was little international fallout from the conflict between India and Pakistan, investors were monitoring signs of escalation. Pakistan’s main equity index shed as much as 8.8%, while India’s Nifty 50 Index lost as much as 01.1%. The Indian rupee slid over 1% against the dollar.

The trade headlines also lifted Europe’s Stoxx 600 index by about 0.9%, as tech, industrials and travel are the best-performing European sectors. Chip stocks including ASML were among the top gainers. Siemens Energy rose after it said the impact of tariffs was going to be limited, while Danish container giant Maersk declines after cutting its forecast amid trade war. Britain’s domestically focused FTSE 250 index rose to a two-month high. Here are the biggest winners:

Siemens Energy shares gain as much as 4.1%, touching a record high, shrugging off US tariff chaos and saying the effect of import duties on its bottom line will be small.

Adecco shares gain as much as 4.3% after the Swiss staffing company posts a top line beat in a mixed set of first-quarter results.

Puma shares jump as much as 6%, hitting their highest level in almost two months, after the sportswear retailer delivered a small sales beat and reiterated its guidance for the year.

Rheinmetall shares rise as much as 2% to a new record after the German firm’s weapon and ammunition sales for the first quarter beat the average analyst estimate.

Novonesis shares rise as much as 4.3% after the Danish biotechnology firm reported strong results for the first quarter, including a small beat on organic sales growth.

J. Martins shares advance as much as 6.3% after retailer maintained Ebitda margin for 1Q even as an unfavorable calendar with a late Easter slowed same-store sales in Poland.

Argenx shares drop as much as 9.5% after the biotech firm reported Vyvgart sales for the first quarter that were slightly weaker than JPMorgan analysts had been expecting.

Maersk shares fall 2.2% after the Danish container giant’s earnings beat was overshadowed by it cutting its forecast for the global transport market rattled by trade war.

Zurich Insurance shares slip as much as 1.4% as Switzerland’s largest insurer cautioned that prices are moderating in Europe, the Middle East and Africa and North America even as it reported solid results for the first quarter.

Amadeus shares fall as much as 3.6% after the travel IT services provider reported sales and Ebitda that missed estimates.

Centrica shares drop as much as 8%, the most since last July, after analysts warned the British Gas-owner’s AGM update suggests there is downside risks to consensus numbers for this year.

Zealand Pharma shares fall as much as 5.9% after the Danish drug developer released results for the first quarter which Van Lanschot Kempen analysts said were “uneventful.”

Earlier in the session, stocks in Asia declined, on course to end a four-day run of gains, as earnings caution in Japan outweighed optimism over signs of easing trade tensions. The MSCI Asia Pacific Index fell 0.6%, reversing an earlier 0.3% gain. Japanese firms Nintendo Co. and Toyota Motor Corp. were among the biggest drags, with the carmaker expecting a $1.3 billion profit hit in just two months on tariffs. Nintendo projected weaker-than-expected initial sales of the Switch 2. Trading was halted in Pakistan after its benchmark KSE-30 Index slumped on intensifying military conflict with India. Indian stocks were slightly lower. Markets were in the green in Hong Kong, China and South Korea as signs of progress in trade negotiations supported sentiment. The confirmation of US-China trade talks starting this weekend, and Thursday’s report that the US is about to announce a deal with the United Kingdom, boosted optimism that the global tariff war has entered a de-escalation stage. Foreign investor flows into Asian stocks excluding China and Japan reached $3 billion so far this week, according to Bloomberg-compiled data.

In FX, the dollar was 0.2% higher against a basket of peers, benefiting also from the Federal Reserve’s signal that it’s in no hurry to ease monetary policy. The Fed held interest rates steady as expected on Wednesday, and warned that higher tariffs could raise inflation and unemployment. The pound climbed after the Bank of England cut interest rates as expected, but stuck to signaling “gradual and careful” moves in the coming months.

In rates, treasuries are cheaper across the curve as US stock futures rally; rate-sensitive two-year Treasury yields rose about five basis points as traders trimmed the odds of a July cut to around 80%. US yields are 3bp-4bp higher across maturities with intermediate tenors leading losses, flattening 5s30s spread by 1.5bp and unwinding a portion of Wednesday’s steepening move. 10-year at 4.30%, just off day’s high. Supply also a factor, with an auction of 30-year bonds ahead at 1pm New York time. Gilt futures fell to session lows after Bank of England cut rates to 4.25% as expected in a three-way split. UK front-end yields cheaper by about 5bp, flattening the gilt curve after the BOE rate decision. The week’s Treasury auction cycle concludes with $25 billion 30-year new issue, following strong demand for 10-year notes Tuesday. WI 30-year yield near ~4.795% is about 2bp richer than last month’s, which stopped through by 2.6bp. Investors will now monitor weekly jobless data, which is expected to show claims slipped marginally in the latest week to 230,000.

In commodities, oil climbs 1.4% higher to near $58.86. Bitcoin rose toward the $100,000 mark for the first time since February. Spot gold falls about $10 to near $3,350/oz.

Looking ahead, the US economic calendar includes 1Q nonfarm productivity and weekly jobless claims (8:30am), March wholesale inventories (10am) and April New York Fed 1-year inflation expectations (11am)

Market Snapshot

S&P 500 mini +1%

Nasdaq 100 mini +1.4%

Russell 2000 mini +1.3%

Stoxx Europe 600 +0.5%

DAX +1.2%

CAC 40 +0.8%

10-year Treasury yield +4 basis points at 4.31%

VIX -1 points at 22.52

Bloomberg Dollar Index +0.3% at 1225.78

euro little changed at $1.129

WTI crude +1% at $58.67/barrel

Top Overnight News

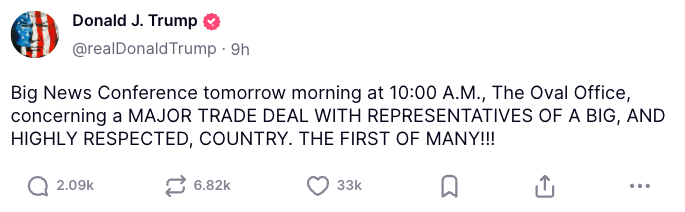

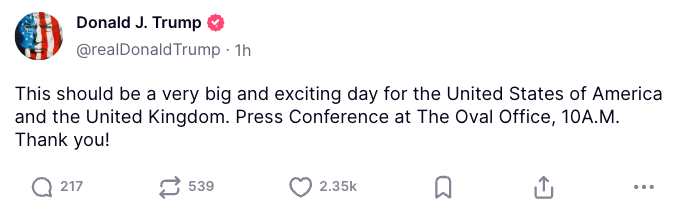

President Trump is expected to announce a framework of a trade deal with the U.K. on Thursday, the first in what the White House hopes is a series of trade agreements since it imposed tariffs against allies and adversaries. Trump said there would be a press conference in the Oval Office at 10 a.m. WSJ

Pakistan said it shot down 12 drones from India that had killed one civilian and injured four soldiers. India’s rupee weakened 1%. BBG

Ukraine has discussed ways to pressure Russia into agreeing to a 30-day ceasefire with U.S., French, British and German senior officials, President Volodymyr Zelenskiy’s top aide said on Thursday, part of a flurry of diplomacy to try to end the war. RTRS

US President Trump’s big announcement is regarding a Medicare drug plan, according to Politico.

US President Trump posted “We are making great progress on “The One, Big, Beautiful Bill.” Our Economy is doing well, but it’s going to BOOM in a way never seen before. We are going to do NO TAX ON TIPS, NO TAX ON SENIORS’ SOCIAL SECURITY, NO TAX ON OVERTIME, and much more. It will be the biggest Tax Cut for Middle and Working Class Americans by far, and it is time for Main Street to WIN. MAKE AMERICA GREAT AGAIN!”

White House said the Treasury and Commerce departments have formulated plans for a sovereign wealth fund, but no final decisions have yet been made.

China is considering largely scrapping its pre-sales model for homes, people familiar said. The move aims to address the country’s housing crisis, but may exacerbate cash flow pressure on developers. BBG

The BOJ can’t ignore the potential downside risks to prices stemming from US tariffs, Kazuo Ueda said. BBG

The Bank of England cut interest rates by a quarter point to 4.25% as Donald Trump’s global trade war weighs on UK growth, in a decision that split senior officials into three groups and was made before the US President hinted at an imminent deal to lower tariffs on British exports. BBG

Brazil’s central bank raised its interest rate by a half-point to 14.75%, the highest level since 2006. Policymakers kept their options open for either another hike or a pause at its next decision. BBG

GOOGL +2% … Google issued statement overnight, responding to AAPL’s intraday comments on search traffic: We continue to see overall query growth in Search. That includes an increase in total queries coming from Apple’s devices and platforms. More generally, as we enhance Search with new features, people are seeing that Google Search is more useful for more of their queries — and they’re accessing it for new things and in new ways, whether from browsers or the Google app, using their voice or Google Lens. We’re excited to continue this innovation and look forward to sharing more at Google I/O.”

Trump tapped Casey Means to be the next US surgeon general after his prior nominee was withdrawn. The health app founder is a vocal critic of the pharmaceutical industry and Big Food. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher amid some trade optimism and following the mildly positive handover from Wall St where price action was choppy in the aftermath of the FOMC meeting as the Fed kept the FFR at 4.25-4.50%, as expected, and noted that risks to the economic outlook increased further, while Fed Chair Powell reiterated a wait-and-see approach and ruled out a pre-emptive cut during the presser. ASX 200 marginally gained amid strength in gold miners, industrials and tech but with the upside capped by weakness in the top-weighted financial sector after Big 4 bank ANZ’s earnings. Nikkei 225 was underpinned by recent currency weakness and trade deal optimism, although a return to the 37,000 level remained elusive. Hang Seng and Shanghai Comp remained positive following the previous day’s PBoC’s policy loosening, but with further upside in the mainland limited after recent comments from US President Trump, who was unwilling to lower tariffs to get China to the table.

Top Asian News

HKMA maintained its base rate at 4.75%, as expected, in lockstep with the Fed.

BoJ Minutes from the March 18th-19th Meeting reiterated they are to raise rates if the economic outlook is realised and a member said it’s appropriate to pay close attention to the new US policies and their impact on the global economy. Furthermore, a member said the BoJ would need to be particularly cautious when considering the timing of the next rate hike as downside risks stemming from US policies had rapidly heightened, while a member said that even with heightened uncertainties, it did not warrant BoJ to be always cautious and the BoJ may face a situation where it should act decisively.

China is weighing housing market overhaul to curb pre-sales, via Bloomberg

European bourses (STOXX 600 +0.3%) opened mostly firmer and have traded with an upward bias throughout the European morning. European sectors are mixed; Tech takes the top spot, joined closely by Industrials whilst Healthcare lags. Tech benefits from post-earning strength in Infineon (+3%) – despite missing on headline metrics and highlighting that it sees 2025 rev. slightly lower Y/Y due to tariff impact. US equity futures (ES +0.8%, NQ +1%) are broadly in the green, in-fitting with the broader risk tone as markets await Trump’s trade announcement.

Top European News

UK PM Starmer is expected to promise on Thursday that his government will deliver a defence dividend for voters, framing an increase in military spending forced by a US shift away from underwriting Europe’s security, as an economic opportunity, according to Reuters.

Sky’s Coates says his sources are confirming that the US-UK trade deal claims are correct. Will be a “heads of terms” agreement, rather than a full deal, but substantive.

NIESR lowered its UK 2025 GDP growth forecast to 1.2% from 1.5%, while it said Chancellor Reeves looks set to miss her budget targets again, partly due to the economic impact from her tax increase on employers, which raises the prospect of more tax hikes.