GOLD CLOSED UP $37.50 TO $3,339.40

SILVER CLOSED UP $0.31 TO $32.75

GOLD ACCESS CLOSED $3327.00

Silver ACCESS CLOSED: $32.77

Bitcoin morning price:$103,040 UP 1534 DOLLARS.

Bitcoin: afternoon price: $101,146 up 3428 DOLLARS

Platinum price closing UP $17.80 TO $1001.40

Palladium price; UP $4.95 TO $978.70

END

*CANADIAN GOLD: $4,635.83 UP 40.80 CDN dollars per oz( * NEW ALL TIME HIGH $4735.70 CDN DOLLARS PER OZ//APRIL 21 2025)

*BRITISH GOLD: 2500.30 UP 3.00 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,566.50 BRITISH POUNDS/OZ) MAY 6/2025

*EURO GOLD: 2956.55 UP 2.80 Euros per oz //* (ALL TIME CLOSING HIGH: 3018.80 EUROS PER OZ/ APRIL 21 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,296.600000000 USD

INTENT DATE: 05/08/2025 DELIVERY DATE: 05/12/2025

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL MARKETS 7

363 H WELLS FARGO SECURITI 1

661 C JP MORGAN SECURITIES 3

661 H JP MORGAN SECURITIES 1

690 C ABN AMRO CLR USA LLC 5

737 C ADVANTAGE FUTURES 5

TOTAL: 11 11

MONTH TO DATE: 15,962

JPMORGAN STOPPED 3/11

MAY

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 11 NOTICES FOR 1100 OZ 0.0342 TONNES

total notices so far: 15,962 contracts for 1,596,200 OR 49.648 tonnes)

FOR MAY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 118 NOTICE(S) FILED FOR 0.590 MILLION OZ/

total number of notices filed so far this month : 13,699 CONTRACTS (NOTICES) for 68.495 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $37.50 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 939.68 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.31 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV: //

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 448.783 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 2047 CONTRACTS TO 136,887 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL LOSS OF $0.16 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. WE HAD A HUGE SIZED LOSS OF 1747 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A GOOD 300 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING THURSDAY AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON THURSDAY WITH SILVER’S SMALL LOSS IN PRICE AND THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH ANOTHER HUGE T.A.S. ISSUANCE OF 737 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A GOOD 300 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 737 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FRIDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE, SURPRISINGLY WE LOST A A MEGA HUGE SIZED 1747 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $0.16.

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS MUST NOW BE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT/FRIDAY MORNING: A HUGE 737 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.16) AND WERE SUCCESSFUL IN KNOCKING OFF SOME NET SILVER LONGS FROM THEIR PERCH

WE HAD A GOOD 300 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 67.830 MILLION OZ TO WHICH WE ADD OUR 219 CONTRACT QUEUE JUMP OF 2.420 MILLION OZ AND THEN WE MUST ADD THOSE CRAZY CONTRACT EXCHANGE FOR RISK FOR 12.93 MILLION OZ:

THUS:

INITIAL STANDING FOR MAY: 74.110 MILLION OZ WHICH INCLUDES TODAY’S 2.420 MILLION QUEUE JUMP + 12.93 MILLION OZ (EX FOR RISK) EQUALS 87.04 MILLION OZ./

WE HAD:

/ MEGA MEGA COMEX OI LOSS+// A GOOD SIZED EFP ISSUANCE (300 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 737 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A MONSTROUS 2327 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 7 DAYS, total 2149 contracts: OR 10.745 MILLION OZ (307 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 10.745 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 10.745 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1747 CONTRACTS WITH OUR LOSS IN PRICE OF $0.16 IN SILVER PRICING AT THE COMEX// THURSDAY.,. . THE CME NOTIFIED US THAT WE HAD A GOOD 300 CONTRACT EFP ISSUANCE CONTRACTS: 300 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND NOW MAY:

NEW STANDING FOR MAY: 74.110 MILLION OZ. (INCLUDES 2.420 MILLION OZ QUEUE JUMP + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 87.04 MILLION OZ

THE NEW TAS ISSUANCE THURSDAY NIGHT (737 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TODAY’S TRADING (FRIDAY TRADING) AND BEYOND.

WE HAD 118 NOTICE(S) FILED TODAY FOR 0.590 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5401 OI CONTRACTS TO 438,421 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A STRONG 1241 CONTRACTS //.

WE HAD A STRONG SIZED DECREASE IN COMEX OI (5401 CONTRACTS) . THIS OCCURRED DESPITE OUR HUGE LOSS OF $82.50 IN PRICE THURSDAY. ON WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER..

WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES/) TO WHICH WE ADDED + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

FINAL STANDING FOR APRIL; 201.443 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

INITIAL STANDING FOR MAY: 50.358 TONNES OF GOLD!

/ ALL OF THIS HAPPENED WITH OUR $82.50 LOSS IN PRICE WITH RESPECT TO THURSDAY’S COMEX ///. WE HAD A FAIR SIZED LOSS OF 2821 OI CONTRACTS (8.774 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AS WELL AS THE SAME FOR APRIL AND NOW MAY….. A MONSTROUS 50.358 TONNES DESPITE IT BEING AN OFF MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2580 CONTRACT:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 438,431/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 136,887 CONTRACTS!!

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2821 CONTRACTS WITH 5401 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 2580 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2821 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A MEGA MEGA HUGE SIZED AND CRIMINAL 45,706 CONTRACTS ISSUED, THE 2ND HIGHEST AMOUNT EVER IN COMEX HISTORY. WE HAD HUGE T.A.S. LIQUIDATION DURING THE COMEX SESSION THURSDAY

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2580 CONTRACT) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 5401 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 8167 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING FOR GOLD FOR MAY AT 50.358 TONNES ( WHICH WHICH INCLUDES OUR 0.534 TONNES QUEUE JUMP)

NEW STANDING FOR GOLD, MAY CONTRACT ADVANCES TO: 50.358 TONNES OF GOLD.

.

/ 3) HUGE T.A.S. LIQUIDATION IN REMOVING SOME NET SPECULATOR LONGS, AS WE HAD 1)A $82.50 COMEX PRICE LOSS.. WE HAD 2) SOME NET LONG SPECS BEING CLIPPED WITH OUR FAIR LOSS OF 2821 CONTRACTS ON OUR TWO EXCHANGES// /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY.

4) GOOD SIZED COMEX OI LOSS// 5) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (1218 CONTRACTS)/// MEGA MEGA HUGE T.A.S. ISSUANCE: 45,706 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAY INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 7010 CONTRACTS OR 701,000 OZ OR 21.804 TONNES IN 7 TRADING DAY(S) AND THUS AVERAGING: 1001 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES 21.804 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 21.804 TONNES DIVIDED BY 3550 x 100% TONNES = 0.619% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 21.804 TONNES OF GOLD EFP ISSUANCE

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 2047 CONTRACTS OI TO 136,887 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 300 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 300 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 300 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2047 CONTRACTS AND ADD TO THE 300 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1747 CONTRACTS DESPITE THE LOSS IN PRICE OF $0.16 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 8.735 MILLION PAPER OZ

OCCURRED WITH OUR $0.16 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 10.00 PTS OR 0.30%

//Hang Seng CLOSED UP 91.82 PTS OR .43%

// Nikkei CLOSED UP 574.70 PTS OR 1.56% //Australia’s all ordinaries CLOSED UP .49%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.2441 OFFSHORE CLOSED DOWN AT 7.2431 / Oil UP TO 60.74 dollars per barrel for WTI and BRENT UP TO 63.72 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN TRADING AT 7.2441 AND WEAKER//OFF SHORE YUAN TRADING DOWN 7.2431 AGAINST US DOLLAR/ AND THUS WEAKER

END

ASIA TRADING FRIDAY MORNING/THURSDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5401 CONTRACTS TO 438,431 WITH OUR HUGE LOSS IN PRICE OF $82.50 WITH RESPECT TO THURSDAY’S // TRADING. WE LOST SOME NUMBER OF NET LONGS WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2580 ).

THE CME ANNOUNCED THURSDAY NIGHT, A 0 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR 0.0 TONNES. TOTAL ISSUANCE FOR MAY IS ZERO. IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST THREE PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

AND NOW WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

MAY: 0 ISSUED SO FAR…

DETAILS ON MAY COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 2821 CONTRACTS DESPITE OUR HUGE LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF APRIL AND ONTO MAY, CONTINUED TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. HOWEVER TODAY’S NUMBER IS ANOTHER HUMDINGER AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 45,706 T.A.S. FOLLOWING THURSDAY”S HUGE 54,145 CONTRACT ISSUANCE. YESTERDAY’S ISSUANCE WAS THE HIGHEST NUMBER BY FAR IN COMEX HISTORY WITH TODAY’S BEING THE 2ND HIGHEST EVER RECORDED! NATURALLY THAT SIGNALS THAT WE WILL WITNESS CONTINUAL RAIDS AND FOR THE NEXT 4 DAYS IF HISTORY SERVES US WELL ANOTHER 3 MEGA MEGA ISSUANCE… (FROM JANUARY 2025 THROUGH TO MARCH 2025 WE HAD THESE 5 MEGA MEGA 30,000+ ISSUANCES WHICH DISTORTED OPEN INTEREST GREATLY. NOW THE ISSUANCES ARE 40,000+ AS THE CROOKS NEED MORE AMMUNITION TO CARRY OUT THEIR NEFARIOUS DEED RAIDS.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY AS YOU WILL SEE BELOW ANOTHER STRONG QUEUE JUMP OCCURRED ON MAY’S DELIVERY CYCLE// THURSDAY NIGHT AT 0.534 TONNES, THIS MONTH WE HAVE RECORDED THE HIGHEST EVER QUEUE JUMP RECORDED IN COMEX GOLD HISTORY AT 6.4 TONNES.

THE TONNAGE STANDING FOR GOLD FOR MAY IS NOW 50.358 TONNES (WHICH INCLUDES TODAY’S STRONG QUEUE JUMP)

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 221 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2580 EFP CONTRACT WAS ISSUED: : /JUNE 2580 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2580 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2821 CONTRACTS IN THAT 2580 CONTRACT LONG WAS TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 5401 COMEX CONTRACTS..AND THIS FAIR LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUMONGOUS LOSS IN PRICE OF $82.50 /// THURSDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. LOOKS LIKE THE SHORT RATS ARE FLEEING THE ARENA AS EVIDENCED BY THE LOWER OPEN INTEREST AT THE COMEX!

WE HAD :

- HUGE LIQUIDATION OF OUR T.A.S. SPREADERS

- SOME SPEC LIQUIDATION WITH THAT HUGE LOSS IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A MEGA MEGA HUGE SIZED 45,706 CONTRACTS AND AS MENTIONED ABOVE, THE SECOND HIGHEST EVER ISSUANCE IN COMEX HISTORY.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL AND MAY

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE

FINAL STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (209.573 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 5 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY:

INITIAL STANDING AT 28.945 INITAL GOLD TONNES STANDING FIRST DAY NOTICE PLUS 6.4634 TONNES QUEUE JUMP MAY 7 (A RECORD) + ANOTHER HUGE QUEUE JUMP MAY 9 OF 0.534 TONNES = 50.358 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 52 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 209.953 TONNES (INCLUDES 8.3571 TONNES EX FOR RISK/AND ALL MONTHLY QUEUE JUMPING)

MAY: STANDING NOW 50.358 TONNES (INCLUDES ALL QUEUE JUMPING)

COMEX GOLD TRADING/MAY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $82.50/ /)AND THEY WERE A SUCCESSFUL IN KNOCKING OFF SOME APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED LOSS IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION THURSDAY AS THEY ARE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE THE MAGIC $3,400 BARRIER AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS IT LOOKS LIKE THEY ARE NOW SUCCEEDING AS GOLD ATTEMPTED TO BREACH THAT 3400 DOLLAR BARRIER AGAIN THURSDAY TRADING. IT IS NOW TRADING EARLY FRIDAY MORNING WELL BELOW TO THAT LEVEL AT $3,337.00

THURSDAY NIGHT/FRIDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /MAY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK = ZERO SO FAR!

HERE IS WHAT HAPPENED LAST MONTH; FINAL GOLD STANDING FOR APRIL:

APRIL: 201.573 TONNES +(8.3571 EX FOR RISK// FOR APRIL DELIVERY MONTH =209.953 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS MAY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// MAY COMEX CONTRACT

WE HAVE LOST A FAIR SIZED TOTAL OF 8.774 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY FIRST RECORDED AT 28.945 TONNES ON FIRST DAY NOTICE. WE HAD A STRONG 172 CONTRACT QUEUE JUMP FOR 17,200 OZ OR 0.534 TONNES. THIS QUEUE JUMP IS CENTRAL BANKS JUMPING AHEAD OF US SIMPLE MORTALS DEMANDING GOLD FOR THEIR RESERVES. THUS NEW STANDING ADVANCES TO 50.358 TONNES OF GOLD.

THUS MAY STANDING FOR GOLD SO FAR: 50.358 TONNES

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $82.50

WE HAD A HUGE 1241 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 2821 CONTRACTS OR 282100 0Z (8.774 TONNES)

confirmed volume THURSDAY 405,478. contracts: huge volume////t.a.s. induced

//speculators have left the gold arena

END

MAY

// THE MAY 2025 GOLD CONTRACT

MAY 9

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | . withdrawals:0 |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER we have 1 customer entry i)Into JPMorgan: 22,864.132 oz weight in tonnes: .711 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 11 notice(s) 1100 OZ 0.0342 TONNES |

| No of oz to be served (notices) | 228 contracts 22,800 OZ 0.7091 TONNES |

| Total monthly oz gold served (contracts) so far this month | 15,962 notices 1,596,200 oz 49.648 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 1 customer entry

i)Into JPMorgan: 22,864.132 oz

weight in tonnes: .711 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals/ customer (eligible category)

withdrawals: 0

adjustments: 3//

a) Brinks dealer to customer: 7137.522 oz 222 kilopbars

b) JPMorgan: 289.35 oz dealer to customer 9 kilobars

c) Malca; dealer to customer 13,050.653 oz

AMOUNT OF GOLD STANDING FOR MAY

THE FRONT MONTH OF MAY STANDS AT 239 CONTRACTS FOR A LOSS OF 833 CONTRACTS. WE HAD 1005 CONTRACTS SERVED ON THURSDAY SO WE GAINED A HUGE 172 CONTRACTS AND THUS WE WITNESS A STRONG 17,200 OZ QUEUE JUMP FOR 0.5340 TONNES.

JUNE LOST A HUMDINGER OF 22,398 CONTRACTS TO 261,155. JUNE BECOMES OUR NEW FRONT MONTH AND THIS MONTH WILL BE A WHOPPER OF A DELIVERY MONTH. THE FRBNY IS QUITE NERVOUS LOOKING AT JUNE OI.

JULY GAINED 176 CONTRACTS TO STAND AT 1376

We had 1005 contracts filed for today representing 100,500 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 1 notices issued from their client or customer account. The total of all issuance by all participants equate to 11 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY /2025. contract month, we take the total number of notices filed so far for the month (15,962 X 100 oz ) to which we add the difference between the open interest for the front month of MAY (239 CONTRACTS) minus the number of notices served upon today (11 x 100 oz per contract) equals 1,619,000 OZ OR 50.358 TONNES

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (15,962 x 100 oz +we add the difference for front month of MAY (239 OI} minus the number of notices served upon today (11 x 100 oz) which equals 1,619,000 OZ OR 50.358 TONNES

TOTAL COMEX GOLD STANDING FOR MAY.: 50.358 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,183,199.736 oz 67.90 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,154,146.819 oz

TOTAL REGISTERED GOLD 21,699,737.264: or 674.01 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 17,484,409.555 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 18,516.538oz (REG GOLD- PLEDGED GOLD)= 607.04tonnes //

END

SILVER/COMEX

// THE APRIL 2025 SILVER CONTRACT//INITIAL

MAY 9

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 withdrawal entries i) Brinks 238,831.400 oz ii) CNT 600,214.633 oz iii)Delaware 994.900 oz iv) Loomis: 617,124.550 oz total withdrawal 1,457,165.513 oz |

| Deposits to the Dealer Inventory | 1 entries/dealer i) Into Stonex: 248,701.10 oz total dealer deposit: 248,701.10 oz |

| Deposits to the Customer Inventory | 3 deposit entry//customer side/eligible i) Into HSBC 38,745.150 oz ii)Into JPMorgan 1942,330.600 oz iii) Into Stonex 8639.000 oz total deposit weight: 1,939,714.0000 oz |

| No of oz served today (contracts) | 118 CONTRACT(S) (0.590 MILLION OZ |

| No of oz to be served (notices) | 1123 contract (5.615 MILLION oz) |

| Total monthly oz silver served (contracts) | 13,699 Contracts (68.495million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 entries/dealer

i) Into Stonex: 248,701.10 oz

total dealer deposit: 248,701.10 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

3 deposit entry//customer side/eligible

i) Into HSBC 38,745.150 oz

ii)Into JPMorgan 1942,330.600 oz

iii) Into Stonex 8,639.000 oz

total deposit weight: 1,939,714.0000 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

4 withdrawal entries

i) Brinks 238,831.400 oz

ii) CNT 600,214.633 oz

iii)Delaware 994.900 oz

iv) Loomis: 617,124.550 oz

total withdrawal 1,457,165.513 oz

ADJUSTMENTs 2

a) JPMorgan: 315,293.310 oz

b) CNT 594,572,808 oz

JPMorgan has a total silver weight: 215.960million oz/503.581 oz million or 42.74%

TOTAL REGISTERED SILVER: 167.509 MILLION OZ//.TOTAL REG + ELIGIBLE. 503,581Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2025 OI: 1241 OPEN INTEREST CONTRACTS FOR A GAIN OF 254 CONTRACTS. WE HAD 230 NOTICES FILED ON THURSDAY SO WE GAINED 484 CONTRACTS WHICH UNDERWENT A MASSIVE QUEUE JUMP OF 2.420 MILLION OZ WHERE THESE BOYS HAVE DECIDED TO TAKE DELIVERY OVER HERE. I MUST REPORT WE HAD 0 EXCHANGE FOR RISK ISSUANCE. THUS THE NEW TOTAL REMAINS AT TWO ISSUANCES OF EXCHANGE FOR RISK IS 12.93 MILLION OZ.

JUNE SAW A GAIN OF 13 CONTRACTS UP TO 3196 CONTRACTS. JUNE OI REFUSES TO LIQUIDATE

AS IT IS NOW THE FRONT MONTH.

JULY LOST 2991 CONTRACTS DOWN TO 106,229

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 118 or 0.590 MILLION oz

CONFIRMED volume; ON THURSDAY 54,023 fair//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 13,699 X5,000 oz = 68.495 MILLION oz

to which we add the difference between the open interest for the front month of MAY (1241) AND the number of notices served upon today (118 )x (5000 oz)

Thus the standings for silver for the MAY 2025 contract month: (13,699) Notices served so far) x 5000 oz + OI for the front month of MAY(1241) minus number of notices served upon today (118)x 5000 oz equals silver standing for the MAY contract month equating to 74.110 MILLION OZ . THEN WE MUST ADD OUR NEW 12.93 TONNES OF EXCHANGE FOR RISK. NEW TOTAL STANDING FOR SILVER: 87.04 MILLION OZ

New total standing: 87.04 million oz which is huge for this active delivery month of MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 167.609million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

MAY 9 WITH GOLD UP $37.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 939.68 TONNES

MAY 8 WITH GOLD DOWN $82.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.23 TONNES OF GOLD WITHDRAWN FROM THE GLD/ ///INVENTORY RESTS AT 937.67 TONNES

MAY 7 WITH GOLD DOWN $30.30 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 937.96 TONNES

MAY 6 WITH GOLD UP $101.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 937.96 TONNES

MAY 5 WITH GOLD UP $77.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.13 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.28 TONNES

MAY 2 WITH GOLD UP $ 18.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 945.41 TONNES

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

APRIL29 WITH GOLD DOWN $13.45 TODAY// NO CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL28 WITH GOLD UP $50.20 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL25 WITH GOLD DOWN $49.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVEV WITHDRAWAL OF 3.911 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 948.56 TONNES

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

GLD INVENTORY: 939.68 TONNES, TONIGHTS TOTAL

SILVER

MAY 9 WITH SILVER DOWN $0.16/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 8 WITH SILVER DOWN $0.16/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 7 WITH SILVER DOWN $0.54/NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 6 WITH SILVER UP $0.92 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A HUG WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 5 WITH SILVER UP $0.08 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF 0.117 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.602 MILLION OZ

MAY 2 WITH SILVER DOWN $0.19 /MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 4.545 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.424 MILLION OZ

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

APRIL29 WITH SILVER UP $0.30 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.229 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 451.925 MILLION OZ

APRIL28 WITH SILVER DOWN $0.03 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.136 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.696 MILLION OZ

APRIL25 WITH SILVER DOWN $0.44 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 3.639 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.832 MILLION OZ

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

CLOSING INVENTORY 448.783 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

VINCE LANCI

Gold Reconsidered: A Strategy To Facilitate 21st Century United States Excellence

Thursday, May 08, 2025 – 10:35 PM

By Vincent Lanci

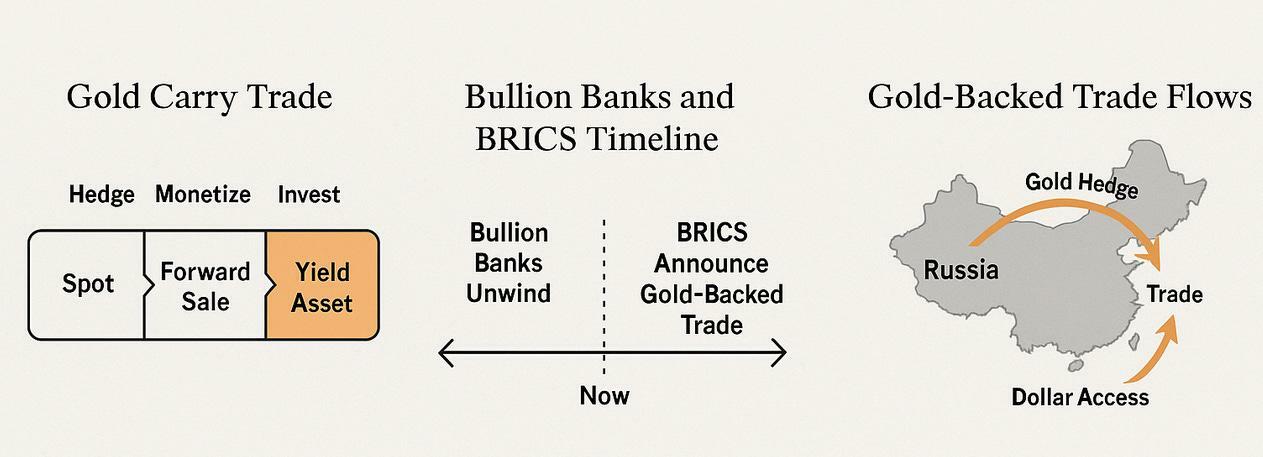

Summary: This report explores gold’s reemergence not merely as a store of value, but as a strategic monetary tool for circumventing sanctions, supporting trade diplomacy, and conducting debt management. Drawing upon historical precedent, contemporary developments, and theoretical frameworks such as Stephen Miran’s Mar-a-Lago Accord, this essay proposes that the United States is positioned to reengage in a sovereign-level gold trading for purposes of reducing debt, rewarding trade partners, and restoring the US manufacture-export base. This mechanism, once dominated by bullion banks and now emulated by sanctioned states, enables the monetization of gold without outright liquidation. Gold-forward hedges provide the United States with an opportunity to strategically weaken the dollar as a component of its need to remain competitive in export driven global economies, reduce debt obligations, and support trade-partner allies through targeted currency support. This report argues that gold’s transformation under Basel III, coupled with a shift in U.S. monetary strategy, marks a return to gold’s core geopolitical function.

I. Introduction. Gold is a store of value; it is money. With its immutable physical properties, universal recognition, and lack of counterparty risk, gold serves as a uniquely effective asset in sovereign monetary operations. This paper explores how the U.S. can operationalize gold as a monetary instrument to manage debt, influence foreign exchange dynamics, and pursue geopolitical leverage in a deglobalizing world.

II. Historical Foundation: The Bullion Bank Carry Trade. Beginning in the 1990s, bullion banks employed a gold carry trade model that enabled monetization without sale. This involved:

- Holding physical gold owned or on loan from another party (spot position)

- Selling that gold forward (creating a future potential liability)

- Investing the proceeds in higher-yielding assets (e.g., Treasuries, stocks, or foreign bonds)

This trade structure provided income while keeping physical reserves intact and suppressed upward pressure on gold prices. It became a cornerstone of central bank expectation management strategy and a projection tool of a stable, reliable USD.

III. The Mar-a-Lago Accord. Stephen Miran’s Mar-a-Lago Accord offered a blueprint for leveraging gold to manage U.S. debt and trade imbalances. That proposal involved:

- Selling U.S. gold reserves

- Using proceeds to purchase foreign currencies with higher yields

- Reducing the effective interest burden on U.S. liabilities

Though politically toxic, the ESF and similar tools had already historically been used in currency stabilization crises. While Miran’s Accord was publicly shelved, some of its core mechanisms remain feasible.

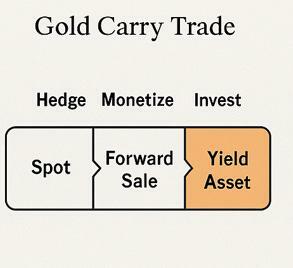

IV. Gold and Sanctions Evasion. The Russia-Iran Model Sanctioned states such as Russia and Iran have leveraged gold to access dollar liquidity via trusted counterparties. By holding and hedging gold through countries like China, they generate liquid proceeds in local or global currencies that are ultimately converted to dollars. This allows them to fund operations while avoiding SWIFT and U.S. financial enforcement.

The oil-for-gold arrangement between Russia and China first described by this paper’s author in 2017. set a precedent. Initially dismissed as rumor, it gained traction when later acknowledged by credible banking analysts. Most recently, an offshoot of its success was announced between China and Saudi Arabia in which the Saudis would receive payment for their oil in RMB with gold optionality attached. The gold would be held by China as it had been for Russian deals. This shows that gold can function as a sanctions-neutral reserve and transfer mechanism while simultaneously being a monetary bridge (mBridge) to the USD or other currencies if needed.

V. Structural Shifts in the Gold Market: The macro and regulatory backdrop has shifted:

- Basel III reclassifies gold as a Tier 1 asset

- Recent OCC Gold derivative reclassification at Banks

- These banks held over 90% of U.S. gold derivative exposure

- BRICS countries now prioritize gold over Treasuries for trade reserves

Together, these changes signal a revaluation of gold within both private and sovereign balance sheets.

VI. A New U.S. Strategy: Gold-Backed Trade Diplomacy. The U.S. can now pursue a sovereign gold carry trade:

- Forward-sale gold to trusted banks

- Use proceeds to buy foreign currencies or EM debt

- Prop up allied currencies, reduce dollar strength

- Execute monetary stimulus while avoiding inflation mismanagement

This framework allows integration of trade and monetary policy. As part of bilateral trade negotiations, the U.S. can offer to stabilize emerging-market currencies, reducing resistance to tariff reform and strengthening political ties.

VII. Conclusion. Gold is returning to center stage as a versatile tool for 21st-century financial statecraft. By adopting carry trade mechanisms pioneered by bullion banks and mirrored by adversarial regimes, the U.S. has the opportunity to align debt management, currency strategy, and trade diplomacy. The convergence of regulatory changes, gold repatriation, and geopolitical fragmentation makes this moment uniquely ripe for gold’s strategic reintegration.

2, EGON VON GREYERZ

ALASDAIR MACLEOD

Healthy consolidation in gold and silver

After the post-liberation day volatility, all markets seek direction. However, the signs are that the negative trend for equities and bonds, and positive trend for PMs will continue in time.

| Alasdair MacleodMay 9∙Paid |

This week, consolidation has continued for gold and silver. In early European trading this morning, gold was $2321, up $83 from last Friday’s close after hitting a high of $3438 on Tuesday. Silver was $32.58, up 60 cents over the same timescale. Trade on Comex was light to moderate, with the price action being increasingly driven in Shanghai.

Gold having risen strongly this year so far (up 26%) and particularly over the last month, it appears that Chinese speculators on the Shanghai Futures Exchange are suffering mild market indigestion. This sets the scene for Comex shorts, still trying to close their positions encouraging the longs to sell by marking down prices to trigger stop-losses.

But Open Interest in both contracts is at the low end, indicating that weak holders have already left the Comex scene. This is shown in the next chart for gold:

Note how open interest is now below 450,000 contracts — on preliminary figures last night they were 439,672. Despite the collapse in this metric, the price remains close to all-time highs. Call this the China effect: it illustrates that the influence brought to bear on gold in Western paper markets is now not the real game.

So we must look to China. And here, a pause in gold’s upwards momentum is justified by confirmation that Trump’s tariffs are being eroded, in China’s case through back-channel negotiations. Yesterday, new tariffs were agreed between the UK and the US, confirming that the US is tending to back down. It gives comfort to US investors as well, who believe that the Art of the Deal is alive and well. The dollar’s trade-weighted index reflects this accordingly:

Currently at 100.5, the $TWI has rallied into overhead supply. This is likely to be seen by foreign holders as an opportunity to reduce their exposure. By way of confirmation, the Fed kept its funds rate unchanged, as expected. The Fed will be very much aware that to have trimmed the rate would have increased selling pressure, not just on the dollar, but on Treasuries as well.

Meanwhile, China is still easing its monetary policy, which can only stimulate household demand for gold accumulation accounts, with some $2.5 trillion equivalent of new money to invest annually. That’s what tells us gold’s consolidation is just that, prior to new Chinese investing in physical set to push prices significantly higher.

Silver is also showing a steadier tone. Again, Comex open interest is at the low end, illustrated next.

Open interest (arrowed) shows that all else being equal it could go slightly lower. Ideally one would like to see it below 130,000 contracts (139,214 preliminary numbers yesterday). But does this really matter?

The technical chart suggests not. This is next.

This is very bullish, which suggests that Comex Open Interest should be on a rising trend: that is to say selloffs become less extreme as time goes on. Undoubtedly, it is this chart and similar technical representations which make the silver bugs so bullish. Bear in mind that silver bugs are far from being the mainstream opinion, vociferous though they may be.

The mainstream dismisses reports of excess demand over supply, pointing out that there are large stocks of silver classified as “investment”. In the past, this has often been the source of marginal supply.

Maybe. But silver investors are unlikely to let their silver go if they see prices rising. And that’s what the technical chart is screaming at us.

end

3. C Powell and Gata dispatches

4. ANDREW MAGUIRE PODCAST 222

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//RARE EARTHS

6 CRYPTOCURRENCY NEWS

ASIA TRADING FRIDAY MORNING THURSDAY NIGHT

SHANGHAI CLOSED DOWN 10.00 PTS OR 0.30%

//Hang Seng CLOSED UP 91.82 PTS OR .43%

// Nikkei CLOSED UP 574.70 PTS OR 1.56% //Australia’s all ordinaries CLOSED UP .49%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.2441 OFFSHORE CLOSED DOWN AT 7.2431 / Oil UP TO 60.74 dollars per barrel for WTI and BRENT UP TO 63.72 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN TRADING AT 7.2441 AND WEAKER//OFF SHORE YUAN TRADING DOWN 7.2431 AGAINST US DOLLAR/ AND THUS WEAKER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2441 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.2431 (CCP MANIPULATED)

SHANGHAI CLOSED DOWN 10.00 PTS OR 0.30%

HANG SENG CLOSED UP 91.82 PTS OR .43%

2. Nikkei closed UP 574.70 PTS OR 1.56%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 100.24// EURO RISES TO 1.1252 UP 25 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.364//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 145.23…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.5820/Italian 10 Yr bond yield UP to 3.646 SPAIN 10 YR BOND YIELD UP TO 3.230%

3i Greek 10 year bond yield UP TO 3.395

3j Gold at $3326.65 Silver at: 32.57 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 36 /100 roubles/dollar; ROUBLE AT 83.75

3m oil into the 60 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 145.23// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.364% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8309 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9349 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.374 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.844 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.860 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.61

10 YR UK BOND YIELD: 4.6410 UP 10 PTS

10 YR CANADA BOND YIELD: 3.202 UP 4 BASIS PTS

5 YR CANADA BOND YIELD: 2.804 UP 4 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

Futures Gain Ahead Of US-China Trade Talks

Friday, May 09, 2025 – 08:32 AM

US equity futures traded modestly higher pointing to a third day of gains, until just before 730am ET when Trump decided to play bad cop to Scott Bessent’s good cop and posted on Truth Social that “80% Tariff on China seems right!” but then added that the final tariff rate is “Up to Scott B.”

That comment promptly hit futures, erasing the market’s modest gains, but upon reflection and realization that Trump was probably just in one of his moods, futures resumed their ascent after yesterday’s trade deal with the UK and Trump’s comments to buy the market. The focus is on the start of China trade talks this weekend, but if we use the US/UK deal as a template, it is light on details with a seemingly minimal economic impact. As of 8:00am ET, S&P futures are up 0.2% and Nasdaq futures gain 0.3%. Pre-market, all Mag7 names are higher with cyclicals mixed but with a bias to Quality names. Markets also benefited from a slew of positive earnings, with Microchip Technology, Lyft, and Pinterest surging while Expedia plunged after it cut bookings growth forecasts. Bond yields are flat as the yield curve bull steepens and the USD sells off after its strongest day since Nov 6 (day after the US Pres. Election). In commodities, energy continues to see a bid with WTI now above $60/bbl, Ags are higher, and precious metals are outperforming base. There is nothing on the macro data calendar, and earnings are light today so today’s session will likely be investors trying to position for outcomes after this weekend’s US/China summit.

In premarket trading, most Mag 7 stocks were green (Tesla +0.75%, Apple +0.2%, Amazon +0.03%, Meta +0.8%, Nvidia +0.1%, Alphabet +0.07%, Microsoft +0.03%). Affirm Holdings fell 6% after the buy-now-pay-later company gave a revenue forecast for the current quarter with the midpoint trailing the avearge analyst estimate. Expedia tumbled 9% after the travel services company cut its gross bookings growth forecast for 2025.

- Figs Inc. (FIGS) drops 16% postmarket after the seller of medical scrubs reduced its year outlook for adjusted Ebitda margin.

- Globus Medical (GMED) drops 14% after the medical device company’s earnings missed estimates, with analysts pointing to weakness in its US spine business and the challenges of integrating recent deals.

- Gogo (GOGO) soars 21% after the in-flight broadband company reaffirmed its adjusted Ebitda guidance for the full year.

- Green Dot (GDOT) rises 18% after the payments companyboosted its adjusted earnings per share forecast for the full year.

- HubSpot (HUBS) declines 4% after the software company gave an outlook for adjusted earnings that is weaker than expected and said Brian Halligan resigned as executive chairperson.

- Iovance Biotherapeutics (IOVA) plunges 34% after the biotech’s first-quarter revenue fell short of estimates and the company cut its full-year forecast.