GOLD CLOSED UP $19.95 TO $3,244.25

SILVER CLOSED UP $0.44 TO $32.89

GOLD ACCESS CLOSED $3248.95

Silver ACCESS CLOSED: $32.96

Bitcoin morning price:$102,744 UP 1034 DOLLARS.

Bitcoin: afternoon price: $104,670 up 2960 DOLLARS

Platinum price closing DOWN $9.45 TO $991.95

Palladium price; DOWN $9.45 TO $957.25

END

*CANADIAN GOLD: $4,528.98 UP 3.00 CDN dollars per oz( * NEW ALL TIME HIGH $4735.70 CDN DOLLARS PER OZ//APRIL 21 2025)

*BRITISH GOLD: 2442.61 DOWN 13.40 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,566.50 BRITISH POUNDS/OZ) MAY 6/2025

*EURO GOLD: 2928.60 UP 4.65 Euros per oz //* (ALL TIME CLOSING HIGH: 3018.80 EUROS PER OZ/ APRIL 21 //2025)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CONTRACT: MAY 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,220.000000000 USD

INTENT DATE: 05/12/2025 DELIVERY DATE: 05/14/2025

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 144

152 C DORMAN TRADING, LLC 6

323 C HSBC 333

332 H STANDARD CHARTERED B 241

363 H WELLS FARGO SECURITI 349

624 H BOFA SECURITIES 800

661 C JP MORGAN SECURITIES 4 28

737 C ADVANTAGE FUTURES 2 3

905 C ADM 2

TOTAL: 956 956

MONTH TO DATE: 17,081

JPMORGAN STOPPED 21/163

MAY

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 956 NOTICES FOR 95,600 OZ 2.973 TONNES

total notices so far: 17,081 contracts for 1,708,100 OR 53.129 tonnes)

FOR MAY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month : 14,258 CONTRACTS (NOTICES) for 71.290 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $19.85 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 939.09 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.44 AT THE SLV: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: // A DEPOSIT OF 0.273 MILLION OZ INTO THE SL

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 451.057 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 556 CONTRACTS TO 137,944 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS/RAID OF $0.30 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 756 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A GOOD 200 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING MONDAY AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON MONDAY WITH SILVER’S LOSS IN PRICE AND THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH ANOTHER HUGE T.A.S. ISSUANCE OF 627 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A GOOD 200 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 627 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 756 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $0.30.

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS MUST NOW BE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A HUGE 627 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.30) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH

WE HAD A GOOD 200 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 67.830 MILLION OZ TO WHICH WE ADD OUR 5 CONTRACT QUEUE JUMP OF 90,000 OZ AND THEN WE MUST ADD THOSE CRAZY CONTRACT EXCHANGE FOR RISK FOR 12.93 MILLION OZ:

THUS:

INITIAL STANDING FOR MAY: 74.110 MILLION OZ WHICH INCLUDES TODAY’S 90,000 OZ QUEUE JUMP + 12.93 MILLION OZ (EX FOR RISK) EQUALS 87.155 MILLION OZ./

WE HAD:

/ HUGE COMEX OI GAIN+// A GOOD SIZED EFP ISSUANCE (200 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 627 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A SMALL 32 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 9 DAYS, total 2658 contracts: OR 13,290 MILLION OZ (296 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 13.290 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 13.290 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 556 CONTRACTS DESPITE OUR LOSS IN PRICE OF $0.30 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A GOOD 200 CONTRACT EFP ISSUANCE CONTRACTS: 200 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND NOW MAY:

NEW STANDING FOR MAY: 74.225 MILLION OZ. (INCLUDES 90,000 OZ QUEUE JUMP + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 87.155 MILLION OZ

THE NEW TAS ISSUANCE THURSDAY NIGHT (627 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TODAY’S TRADING (MONDAY TRADING) AND BEYOND.

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2289 OI CONTRACTS TO 440,560 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A STRONG 869 CONTRACTS //.

WE HAD A FAIR SIZED INCREASE IN COMEX OI (2,289 CONTRACTS) . THIS OCCURRED DESPITE OUR LOSS OF $115.00 IN PRICE MONDAY. ON WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER..

WE PREVIOUSLY HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES/) TO WHICH WE ADDED + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

FINAL STANDING FOR APRIL; 201.443 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

AND NOW MAY:

INITIAL STANDING FOR MAY: 53.334 TONNES OF GOLD TO WHICH WE ADD TODAY’S EXCHANGE FOR RISK OF 1.55 TONNES//NEW STANDING FOR MAY: 54.884 TONES WHICH IS HUGE!!

/ ALL OF THIS HAPPENED WITH OUR $115.00 LOSS IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD A STRONG SIZED GAIN OF 4514 OI CONTRACTS (14.04 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AS WELL AS THE SAME FOR APRIL AND NOW MAY….. A MONSTROUS 54.884 TONNES DESPITE IT BEING AN OFF MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2225 CONTRACT:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 440,560/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 137,944 CONTRACTS!!

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4514 CONTRACTS WITH 3153 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2225 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4514 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A MEGA MEGA HUGE SIZED AND CRIMINAL 24,745 CONTRACTS ISSUED. THIS REPRESENTS THE 4TH CONSECUTIVE T.A.S ISSUANCED AVERAGING 30,000+ AND THUS WE WILL EXPECT ANOTHER ONE TOMORROW AS THE CROOKS RELOAD THEIR AMMUNITION! SEEMS THAT THEIR RAID WAS A TOTAL FAILURE!!

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2225 CONTRACT) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 3158 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 4514 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING FOR GOLD FOR MAY AT 53.334 TONNES ( WHICH WHICH INCLUDES OUR 2.444 TONNES QUEUE JUMP AND THEN WE ADD OUR MAY 13 ISSUANCE OF 1.55 TONNES EX FOR RISK//NEW TOTAL 54.884

NEW STANDING FOR GOLD, MAY CONTRACT ADVANCES TO: 54.884 TONNES OF GOLD.(INCLUDES QUEUE JUMP AND EX FOR RISK)

.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION BUT, AS WE HAD 1)A $115.00 COMEX PRICE LOSS.. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THAT LOSS AS WE HAD OUR STRONG GAIN OF 5383 CONTRACTS ON OUR TWO EXCHANGES// /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY.

4) FAIR SIZED COMEX OI GAIN// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (2225 CONTRACTS)/// MEGA MEGA HUGE T.A.S. ISSUANCE: 24,745 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAY INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 10,735 CONTRACTS OR 1,073,500 OZ OR 33.390 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 1192 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 33.390 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 33.390 TONNES DIVIDED BY 3550 x 100% TONNES = 0.940% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 33.390 TONNES OF GOLD EFP ISSUANCE

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 556 CONTRACTS OI TO 137,944 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 200 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 309 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 556 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 756 CONTRACTS DESPITE THE LOSS IN PRICE OF $0.30 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 3.940 MILLION PAPER OZ

OCCURRED WITH OUR $0.30 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 5.63 PTS OR 0.17%

//Hang Seng CLOSED DOWN 470.93 PTS OR 2.00%

// Nikkei CLOSED UP 539.00 PTS OR 1.43% //Australia’s all ordinaries CLOSED UP .52%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1991 OFFSHORE CLOSED UP AT 7.1953 / Oil UP TO 62.02 dollars per barrel for WTI and BRENT UP TO 64.98 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1991 AND STRONGER//OFF SHORE YUAN TRADING UP 7.1953 AGAINST US DOLLAR/ AND THUS STRONGER

END

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2289 CONTRACTS TO 440,560 DESPITE OUR STRONG LOSS IN PRICE OF $115.00 WITH RESPECT TO MONDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT, HUGE PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2225 ).

THE CME ANNOUNCED MONDAY NIGHT, A STRONG 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.55 TONNES. TOTAL ISSUANCE FOR MAY IS NOW 1.55 TONNES OF GOLD. IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST THREE PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

AND NOW WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

MAY: 1 ISSUED SO FAR FOR 500 CONTRACTS OR 50,000 OZ OR 1.55 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!

DETAILS ON MAY COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 4514 CONTRACTS DESPITE OUR HUGE LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF APRIL AND ONTO MAY, CONTINUED TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. HOWEVER TODAY’S NUMBER IS ANOTHER HUMDINGER AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 24,745 T.A.S. FOLLOWING HUGE ISSUANCES DURING OUR LAST 3 TRADING DAYS. . THURSDAY’S ISSUANCE WAS THE HIGHEST NUMBER BY FAR IN COMEX HISTORY WITH FRIDAY’S BEING THE 2ND HIGHEST EVER RECORDED! NATURALLY THAT SIGNALS THAT WE WILL WITNESS CONTINUAL RAIDS AND FOR THE NEXT FEW DAYS, IF HISTORY SERVES US WELL, WE WILL HAVE ANOTHER 1 MEGA MEGA ISSUANCE… (FROM JANUARY 2025 THROUGH TO MARCH 2025 WE HAD THESE 5 MEGA MEGA 30,000+ ISSUANCES WHICH DISTORTED OPEN INTEREST GREATLY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY AS YOU WILL SEE BELOW ANOTHER STRONG QUEUE JUMP OCCURRED ON MAY’S DELIVERY CYCLE// TUESDAY AT 2.444TONNES, THIS MONTH WE HAVE RECORDED THE HIGHEST EVER QUEUE JUMP RECORDED IN COMEX GOLD HISTORY AT 6.4 TONNES.

THE TONNAGE STANDING FOR GOLD FOR MAY IS NOW 54.884 TONNES (WHICH INCLUDES TODAY’S STRONG QUEUE JUMP AND OUR INITIAL 1.55 TONNES EX FOR RISK!)

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 221 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2225 EFP CONTRACT WAS ISSUED: : /JUNE 2225 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2225 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

WE HAD :

- SOME LIQUIDATION OF OUR T.A.S. SPREADERS

- ZERO SPEC LIQUIDATION WITH OUR GAIN IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A MEGA MEGA HUGE SIZED, 24,745 FOLLOWING LAST FRIDAY’S 45,706 CONTRACTS AND AS MENTIONED ABOVE, THE SECOND HIGHEST EVER ISSUANCE IN COMEX HISTORY.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL AND MAY

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE

FINAL STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (209.573 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 5 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY:

INITIAL STANDING AT 28.945 INITAL GOLD TONNES STANDING FIRST DAY NOTICE PLUS 6.4634 TONNES QUEUE JUMP MAY 7 (A RECORD) + ANOTHER HUGE QUEUE JUMP MAY 9 OF 0.534 TONNES + MAY 12 AT .5132 TONNES _ TODAY;S QUEUE JUMP OF 2.444 TONNES PLUS 1.55 TONNES EXCHANGE FOR RISK = 54.884 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 52 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 209.953 TONNES (INCLUDES 8.3571 TONNES EX FOR RISK/AND ALL MONTHLY QUEUE JUMPING)

MAY: STANDING NOW 53.334 TONNES (INCLUDES ALL QUEUE JUMPING) + 1.55 TONNES EX FOR RISK EQUALS 54.884 TONNES!!

COMEX GOLD TRADING/MAY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A MAMMOTH $115.00/ /)BUT THEY WERE A UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION MONDAY AS THEY ARE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE THE MAGIC $3,400 BARRIER AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS IT LOOKS LIKE THEY ARE NOW SUCCEEDING AS GOLD ATTEMPTED TO BREACH THAT 3400 DOLLAR BARRIER AGAIN THURSDAY TRADING. IT IS NOW TRADING EARLY TUESDAY MORNING WELL BELOW TO THAT LEVEL AT $3,227.00

MONDAY NIGHT/TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /MAY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK = 500 CONTRACTS FOR 50,000 OZ OR 1.55 TONNES OF GOLD. WE NOW HAVE 6 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. AND AS ALWAYS THIS WILL BE ADDED TO OUR DAILY DELIVERY SCHEDULE.

HERE IS WHAT HAPPENED LAST MONTH; FINAL GOLD STANDING FOR APRIL:

APRIL: 201.573 TONNES +(8.3571 EX FOR RISK// FOR APRIL DELIVERY MONTH =209.953 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS MAY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// MAY COMEX CONTRACT

WE HAVE GAINED A FAIR SIZED TOTAL OF 14.04 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY FIRST RECORDED AT 28.945 TONNES ON FIRST DAY NOTICE. WE HAD A STRONG 786 CONTRACT QUEUE JUMP FOR 78,600 OZ OR 2.444 TONNES. THIS QUEUE JUMP IS CENTRAL BANKS JUMPING AHEAD OF US SIMPLE MORTALS DEMANDING GOLD FOR THEIR RESERVES. THUS NEW STANDING ADVANCES TO 53.334 TONNES OF GOLD. TO WHICH WE ADD TODAY’S (MAY 13) EXCHANGE FOR RISK ISSUANCE FOR 1.55 TONNES//NEW TOTAL GOLD STANDING FOR MAY INCREASES TO 54.884

THUS MAY STANDING FOR GOLD SO FAR: 54.884 TONNES

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $115.00

WE HAD A HUGE 869 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 4514 CONTRACTS OR 451,400 0Z (14.04 TONNES)

confirmed volume MONDAY 381,812. contracts: strong volume////

//speculators have left the gold arena

END

MAY

// THE MAY 2025 GOLD CONTRACT

MAY 13

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | . withdrawals:2 i) Out of Brinks 4822.65 oz 150 kilobars) ii) Out of JPMorgan 96,453.000 oz (3,000 kilobars) total weight 101,295.650 oz 3.150 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | 2) entries: i) Into Asahia 208,531.466 oz 6486 kilobars) ii) Into JPMorgan: 42,084.218 oz (1309 kilobars) total weight: 254,634.978 oz in tonnes: 7.795 tonnes 7.795 kilobars xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 956 notice(s) 95,600 OZ 2.973 TONNES |

| No of oz to be served (notices) | 66 contracts 6600 OZ 0.2052 TONNES |

| Total monthly oz gold served (contracts) so far this month | 17,081 notices 1,708,100 oz 53.129 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 2 customer entries

2) entries:

i) Into Asahia 208,531.466 oz 6486 kilobars)

ii) Into JPMorgan: 42,084.218 oz (1309 kilobars)

total weight: 254,634.978 oz

in tonnes: 7.795 tonnes

7.795 kilobars

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:2

i) Out of Brinks 4822.65 oz

150 kilobars)

ii) Out of JPMorgan 96,453.000 oz

(3,000 kilobars)

total weight 101,295.650 oz

3.150 tonnes

adjustments: 1//customer to dealer

a) JPMorgan 14,493.693 oz

AMOUNT OF GOLD STANDING FOR MAY

THE FRONT MONTH OF MAY STANDS AT 1016 CONTRACTS FOR A GAIN OF 623 CONTRACTS. WE HAD 163 CONTRACTS SERVED ON MONDAY SO WE GAINED A HUGE 786 CONTRACTS AND THUS WE WITNESS A STRONG 78,600 OZ QUEUE JUMP FOR 2.444 TONNES.

JUNE LOST 22,043 CONTRACTS TO 224,527. JUNE BECOMES OUR NEW FRONT MONTH AND THIS MONTH WILL BE A WHOPPER OF A DELIVERY MONTH. THE FRBNY IS QUITE NERVOUS LOOKING AT JUNE OI.

JULY GAINED 1181 CONTRACTS TO STAND AT 1604

We had 163 contracts filed for today representing 16300 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 4 notices issued from their client or customer account. The total of all issuance by all participants equate to 956 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 28 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY /2025. contract month, we take the total number of notices filed so far for the month (17,081 X 100 oz ) to which we add the difference between the open interest for the front month of MAY (1016 CONTRACTS) minus the number of notices served upon today (956 x 100 oz per contract) equals 1,714700 OZ OR 53.334 TONNES

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (17,081 x 100 oz +we add the difference for front month of MAY (1016 OI} minus the number of notices served upon today (956 x 100 oz) which equals 1,714,000 OZ OR 53.334 TONNES

TOTAL COMEX GOLD STANDING FOR MAY.: 53.334 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,197,294.559 oz 68.34 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,270,532.497 oz

TOTAL REGISTERED GOLD 21,676,071.935: or 674.21 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 17,544,460.562 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 19,478,574oz (REG GOLD- PLEDGED GOLD)= 605.86tonnes //

END

SILVER/COMEX

// THE MAY 2025 SILVER CONTRACT//INITIAL

MAY 12

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 withdrawal entries i) Out of CNT 1199,780.669 oz ii) Out of Delaware: 44,489.330 oz iii) Out of Loomis: 600,213.600 oz total withdrawal 1,844,482.998 oz |

| Deposits to the Dealer Inventory | 0 entries/dealer |

| Deposits to the Customer Inventory | 1 deposit entry//customer side/eligible i) Into Asahi: 606,135.200 oz total deposit weight: 606,135.200 oz |

| No of oz served today (contracts) | 1 CONTRACT(S) (5,000 OZ |

| No of oz to be served (notices) | 570 contract (2.860 MILLION oz) |

| Total monthly oz silver served (contracts) | 14,258 Contracts (71.290 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

0 entries/dealer

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1 deposit entry//customer side/eligible

i) Into Asahi: 606,135.200 oz

total deposit weight: 606,135.200 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

3 withdrawal entries

i) Out of CNT 1199,780.669 oz

ii) Out of Delaware: 44,489.330 oz

iii) Out of Loomis: 600,213.600 oz

total withdrawal 1,844,482.998 oz

ADJUSTMENTs 0

JPMorgan has a total silver weight: 217.184million oz/503.481 oz million or 43.09%

TOTAL REGISTERED SILVER: 167.509 MILLION OZ//.TOTAL REG + ELIGIBLE. 503.481Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2025 OI: 580 OPEN INTEREST CONTRACTS FOR A LOSS OF 540 CONTRACTS. WE HAD 558 NOTICES FILED ON MONDAY SO WE GAINED 18 CONTRACTS WHICH UNDERWENT A QUEUE JUMP OF 90,000 OZ WHERE THESE BOYS HAVE DECIDED TO TAKE DELIVERY OVER HERE. I MUST REPORT WE HAD 0 EXCHANGE FOR RISK ISSUANCE FOR TODAY. THUS THE NEW TOTAL REMAINS AT TWO ISSUANCES OF EXCHANGE FOR RISK IS 12.93 MILLION OZ.

JUNE SAW A LOSS OF 26 CONTRACTS DOWN TO 3120 CONTRACTS. JUNE OI REFUSES TO LIQUIDATE

AS IT IS NOW THE FRONT MONTH.

JULY GAINED 237 CONTRACTS UP TO 106,540

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 or 0.005 MILLION oz

CONFIRMED volume; ON MONDAY 66,803 good//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 14,258 X5,000 oz = 71.258 MILLION oz

to which we add the difference between the open interest for the front month of MAY (588) AND the number of notices served upon today (1 )x (5000 oz)

Thus the standings for silver for the MAY 2025 contract month: (14,258) Notices served so far) x 5000 oz + OI for the front month of MAY(588) minus number of notices served upon today (1)x 5000 oz equals silver standing for the MAY contract month equating to 74.225 MILLION OZ . THEN WE MUST ADD OUR NEW 12.93 TONNES OF EXCHANGE FOR RISK. NEW TOTAL STANDING FOR SILVER: 87.155 MILLION OZ

New total standing: 87.155 million oz which is huge for this active delivery month of MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 167.509million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

MAY 13 WITH GOLD UP $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 12 WITH GOLD DOWN $115.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 9 WITH GOLD UP $37.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 939.68 TONNES

MAY 8 WITH GOLD DOWN $82.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.23 TONNES OF GOLD WITHDRAWN FROM THE GLD/ ///INVENTORY RESTS AT 937.67 TONNES

MAY 7 WITH GOLD DOWN $30.30 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 937.96 TONNES

MAY 6 WITH GOLD UP $101.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 937.96 TONNES

MAY 5 WITH GOLD UP $77.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.13 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.28 TONNES

MAY 2 WITH GOLD UP $ 18.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 945.41 TONNES

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

APRIL29 WITH GOLD DOWN $13.45 TODAY// NO CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL28 WITH GOLD UP $50.20 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL25 WITH GOLD DOWN $49.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVEV WITHDRAWAL OF 3.911 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 948.56 TONNES

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

GLD INVENTORY: 937.94 TONNES, TONIGHTS TOTAL

SILVER

MAY 13 WITH SILVER UP $0.44/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 12 WITH SILVER DOWN $0.30/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 9 WITH SILVER UP $0.31/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 8 WITH SILVER DOWN $0.16/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 7 WITH SILVER DOWN $0.54/NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 6 WITH SILVER UP $0.92 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A HUG WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 5 WITH SILVER UP $0.08 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF 0.117 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.602 MILLION OZ

MAY 2 WITH SILVER DOWN $0.19 /MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 4.545 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.424 MILLION OZ

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

APRIL29 WITH SILVER UP $0.30 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.229 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 451.925 MILLION OZ

APRIL28 WITH SILVER DOWN $0.03 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.136 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.696 MILLION OZ

APRIL25 WITH SILVER DOWN $0.44 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 3.639 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.832 MILLION OZ

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

CLOSING INVENTORY 448.783 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2, EGON VON GREYERZ

ALASDAIR MACLEOD

Free trade benefits

On the basis that the consumer is king, free trade is obviously best. But if the producer is king, protectionism is rife. Businesses lobby governments, and the consumer is ill-served.

| Alasdair MacleodMay 13∙Paid |

We should applaud Scott Bessent for returning a sense of perspective to US—Chinese trade relations. An economic crisis, not for China as many think but for the US and its dollar has at least been deferred. The reactions in markets were entirely rational, not least for gold values. The dollar crisis is not over, but Bessent has at least bought some time. The dollar’s sigh of relief measured by gold might be described as being almost audible.

This article explains why US tariff policy is both misguided and dangerous. It debunks the belief that protectionist tariffs are necessary. And the US’s trade deficit is not going to disappear, because it is driven by inflationary funding of the budget deficit.

The theory of comparative advantage

It was economist David Ricardo who originally expressed the benefits of free trade, in his theory of comparative advantage. To illustrate the point, in his Principals of Political Economy he used trade between two countries as an example: Portugal, which produced cloth and wine both exported to England, and England which produced only cloth. He argued that free trade would lead to Portugal increasing its wine production to satisfy English demand and even if it was marginally better at producing cloth than England, assuming that trade between the two balanced, the limitations of capital, labour, and a balance of payments would lead to Portugal’s wine production being enhanced relative to its production of cloth.

Other than the obvious, that Portugal has a better a better climate for wine production than England, there are several suppositions involved with respect to the balance between cloth production which apply to international trade today. As already mentioned, it includes a simplistic trade model where imports and exports between both nations balance. Capital in the form of credit and labour skills in Portugal are assumed to be mobile. There is no subcontracting to other countries. Labour productivity differences is another variable assumed out of the equation. It also includes an assumption that commodity input costs are the same or similar.

The favourite phrase of economists, that all else being equal, ignores much.

The comparison today is between America or Europe and the Far East, which has led to substantial contracting out of production or elements of it from higher cost centres to lower ones. Time to market from drawing board to final output is also considerably less in the Far East, and time is money. American and European corporations have set up factories in China for this reason. We can see that Ricardo’s theory of comparative advantage might be too simple a model for trade conditions today.

But it is wrong to ditch it entirely. Until relatively recently, Germany and Japan ran export surpluses despite their currencies rising inexorably on the back of export success. The world bought Mercedes and Toyota motor cars, not because they were cheap but because they were and still are very good. They still outcompete American and other European manufacturers, who have failed to innovate their products sufficiently.

The only way to ensure that domestic production is competitive internationally is to produce a better package: in Ricardo’s example, some Portuguese cloth manufacturers could still have sold cloth to England competitively. But an American manufacturer selling product to China has a significant cost hurdle, a huge mountain to climb. But the mountain is huge because American producers have failed to innovate in their own back yard, preferring to invest abroad instead. That is the lesson from Germany’s highly successful mittelstand. That is, before Germany swapped marks for euros.

Let’s imagine for a moment that a US company decides to invest in manufacturing in America. Automation takes differences of human productivity out of the equation, so that manufacturing cost differences can be minimised. There is no reason that distribution costs should be any different for locally manufactured goods compared with imports.

Fixed costs become a problem. Time to market, including planning laws, the cost of land, and time taken to build factories and install plant are considerably greater in America and Europe than elsewhere. But other than this last factor, by manufacturing at scale it should be possible for the US and Europe to enhance exports to global markets.

Some manufacturers have achieved it, mostly smaller niche producers of components and goods. It is the large corporations in the main which have failed to produce goods in their countries of origin. But instead of responding to the production challenge, businesses lobby governments for protection. And governments in Europe and America resort to tariffs and other trade obstacles.

Conclusion: it is wrong to argue that China et al are competing unfairly. It is US and European multinationals that are the problem. Ricardo’s theory of comparative advantage still holds. Therefore, the alliance between big business and government taking anti-competitive measures is the villain.

The balance of trade in Ricardo’s time was settled in gold or acceptable gold substitutes, which ensured that nations did not trade beyond their resources. That is no longer the case. When one nation debauches its currency by running a deficit financed by inflationary means (i.e. not backed by savings), inevitably the budget deficit feeds into a trade deficit.

Therefore, the deficit on trade experienced by America where savings are deteriorating, means that it is joined at the hip to the $2 trillion budget deficit. No number of tariffs and other forms of import controls can change that.

Being a tax on consumers, tariffs tend to raise prices. And when the general level of prices increases, it is the same thing as the purchasing power of the national currency declining. This is why Trump’s tariffs led to the price of gold rising expressed in depreciating dollars. It was entirely rational.

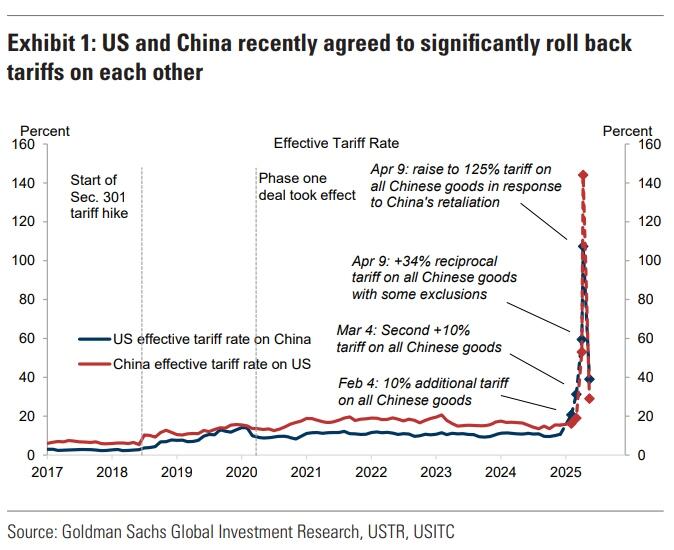

Now that a more sensible approach to imports from China has been negotiated by Scott Bessant, the pressure on a declining dollar has been reduced, and gold backed off nearly $200. Again, this market response is rational. But almost immediately, commentators have assumed that the US might not be heading into a recession after all — a wholly irrational conclusion.

The false input of a budget deficit amounting to 7% of GDP means that private sector GDP is already contracting and has been for several years. A declining private sector leads to falling tax revenues and rising welfare costs, increasing the budget deficit. The relief from outlandish tariffs is temporary. The debt trap is more permanent, which is why the dollar is still in crisis

.

3. CHRIS POWELL AND GATA DISPATCHES

Brien Lundin: China deal creates opportunities for gold shorts and longs

Submitted by admin on Mon, 2025-05-12 13:47 Section: Daily Dispatches

By Brien Lundin

Gold Newsletter / Golden Opportunities

Metairie, Louisiana

Monday, May 12, 2025

I haven’t heard gold mentioned so much in the mainstream financial media at any other point in this new gold bull market.

At every market update on CNBC, for example, it seems the announcer is leading off with a note that gold has posted another $100 day. The metal has never before enjoyed such coverage.

The reason, of course, is because gold is down $100 today, instead of rising that much.

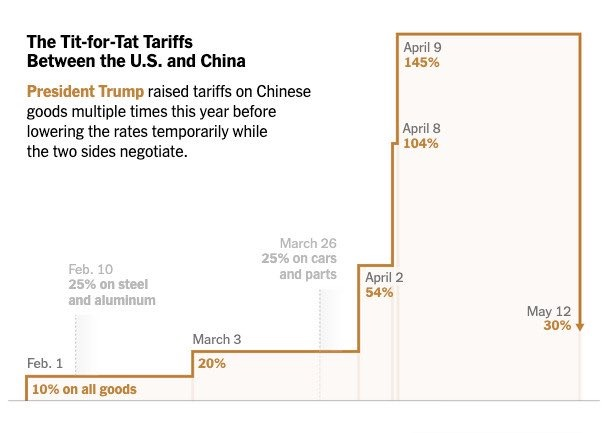

.Maybe I’m an oversensitive gold bug, but it does seem like the Wall Street talking heads are relishing this selloff in gold that’s come immediately in the wake of President Trump’s announced “deal” with China.

This deal, such as it is, essentially postpones for 90 days the most onerous tariff rates that Trump was using as a cudgel to bring China to the table. In the meantime, however, the administration agreed to have U.S. consumers pay 30% more while Chinese buyers pay just 10% in tariffs. …

END

On LFTV, Maguire and Schectman agree that gold is money forever

Submitted by admin on Sun, 2025-05-11 08:39 Section: Daily Dispatches

8:38a ET Sunday, May 11, 2025

Dear Friend of GATA and Gold:

Coin and bullion dealer Miles Franklin’s Andy Schectman is London metals trader Andrew Maguire’s guest on this week’s edition of Kinesis Money’s “Live From the Vault” program, and they discuss how gold has preserved wealth through centuries of monetary and political upheaval.

They also discuss the developing world’s challenge to the pricing of gold by derivatives in Western markets, a challenge that is leading to a worldwide revaluation of gold.

The program is 52 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

U.S. Global’s Frank Holmes: Basel III makes it official that gold is money again

Submitted by admin on Sun, 2025-05-11 08:27 Section: Daily Dispatches

By Frank Holmes

U.S. Global Investors, San Antonio, Texas

Friday, May 9, 2025

For my entire decades-long career in capital markets, I’ve made the case that gold is not just a shiny relic of the past but a serious, strategic asset for modern investors. After years of pounding the table, it feels pretty good to say that the world’s central banks — and now the U.S. banking system — are finally catching up.

As of July 1, 2025, gold will officially be classified as a Tier 1, high-quality liquid asset under the Basel III banking regulations. That means U.S. banks can count physical gold at 100% of its market value toward their core capital reserves.

No longer will gold be marked down by 50% as a “Tier 3” asset, as it was under the old rules.

This is a seismic shift in how regulators perceive gold, and it’s a long-overdue recognition of what many of us have known for decades: Gold is money. And it’s the kind of money you want to own when the world is on fire. …

… For the remainder of the commentary:

* * *

4. ANDREW MAGUIRE PODCAST 222

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//CATTLE

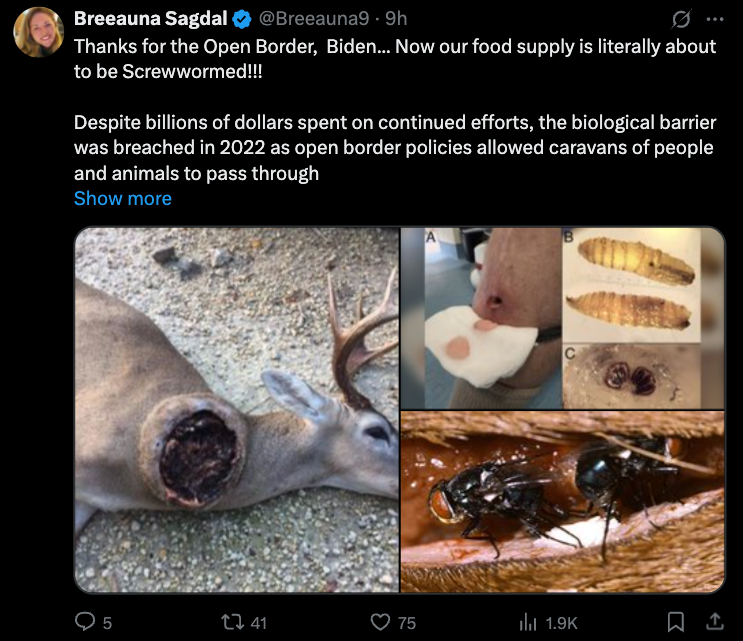

US Cattle Futures Hit New Highs After Mexican Beef Imports Halted To Stop “Pest Invasion”

Monday, May 12, 2025 – 04:40 PM

Feeder cattle futures in Chicago surged to a record high on Monday after U.S. Agriculture Secretary Brooke Rollins announced an immediate suspension of live cattle, horse, and bison imports from southern border land ports. The move comes in response to the spread of the flesh-eating New World Screwworm (NWS) in Mexico—a parasitic threat deemed a national security risk due to its potential to devastate already tight U.S. cattle supplies.

“Due to the threat of New World Screwworm I am announcing the suspension of live cattle, horse, & bison imports through U.S. southern border ports of entry effective immediately,” Rollins wrote on X.

She warned: “The last time this devastating pest invaded America, it took 30 years for our cattle industry to recover. This cannot happen again.”

.com/SecRollins/status/1921637437362811164?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E1921637437362811164%7Ctwgr%5E61d2018aa9

“The protection of our animals and safety of our nation’s food supply is a national security issue of the utmost importance. Once we see increased surveillance and eradication efforts, and the positive results of those actions, we remain committed to opening the border for livestock trade. This is not about politics or punishment of Mexico, rather it is about food and animal safety,” Rollins wrote in a press release.

She said NWS has been detected in remote farms with minimal cattle movement around Oaxaca and Veracruz—about 700 miles away from the U.S.-Mexico border.

Via Breeauna Sagdal, Senior Writer and Research Fellow at The Beef Initiative…

Import restrictions sent feeder cattle futures to a record high of $3.05 per pound in Chicago. Contracts are up more than 15% this year.

“Futures markets are likely to begin pricing in greater supply risk for later in the year,” analysts from Steiner Consulting Group wrote in a note to clients.

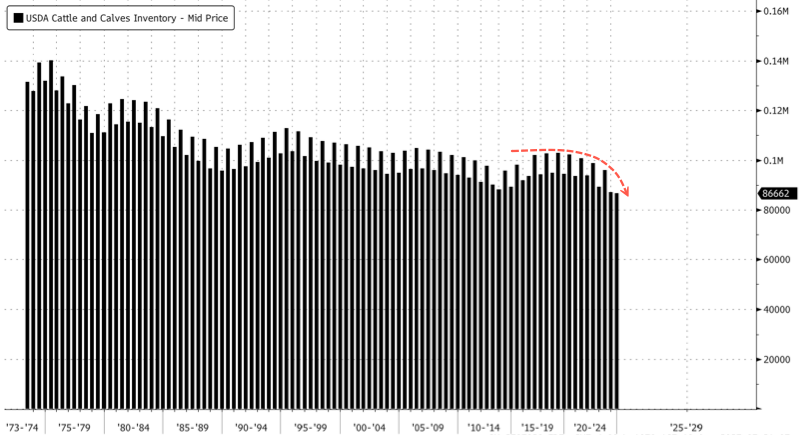

At the start of the year, the U.S. Department of Agriculture’s (USDA) annual Cattle Inventory report revealed that the nation’s cattle supply had fallen to a 73-year low, totaling about 86.6 million head.

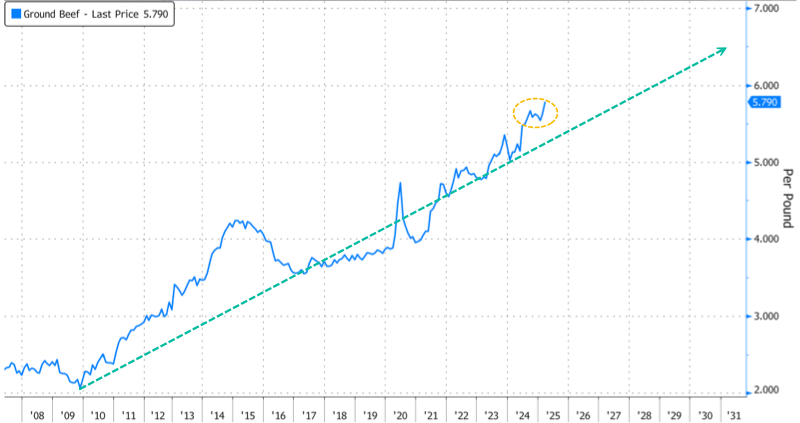

At the supermarket, USDA data from the end of March showed that the average price for a pound of ground beef reached another record high of $5.79.

During last week’s earnings call, Tyson Foods executive Brady Stewart, who oversees the company’s beef and pork supply chains, suggested the U.S. cattle herd may be nearing a bottom—potentially signaling the start of a rebuilding cycle. However, Tyson has not yet updated its guidance following the import restrictions imposed on Sunday.

Support your local ranchers and break free from the industrial food complex. Don’t be fooled by “Product of USA” labels stamped on imported beef from overseas. It’s time to buy American-raised meat and know exactly where your food comes from. Learn more here.

6 CRYPTOCURRENCY NEWS

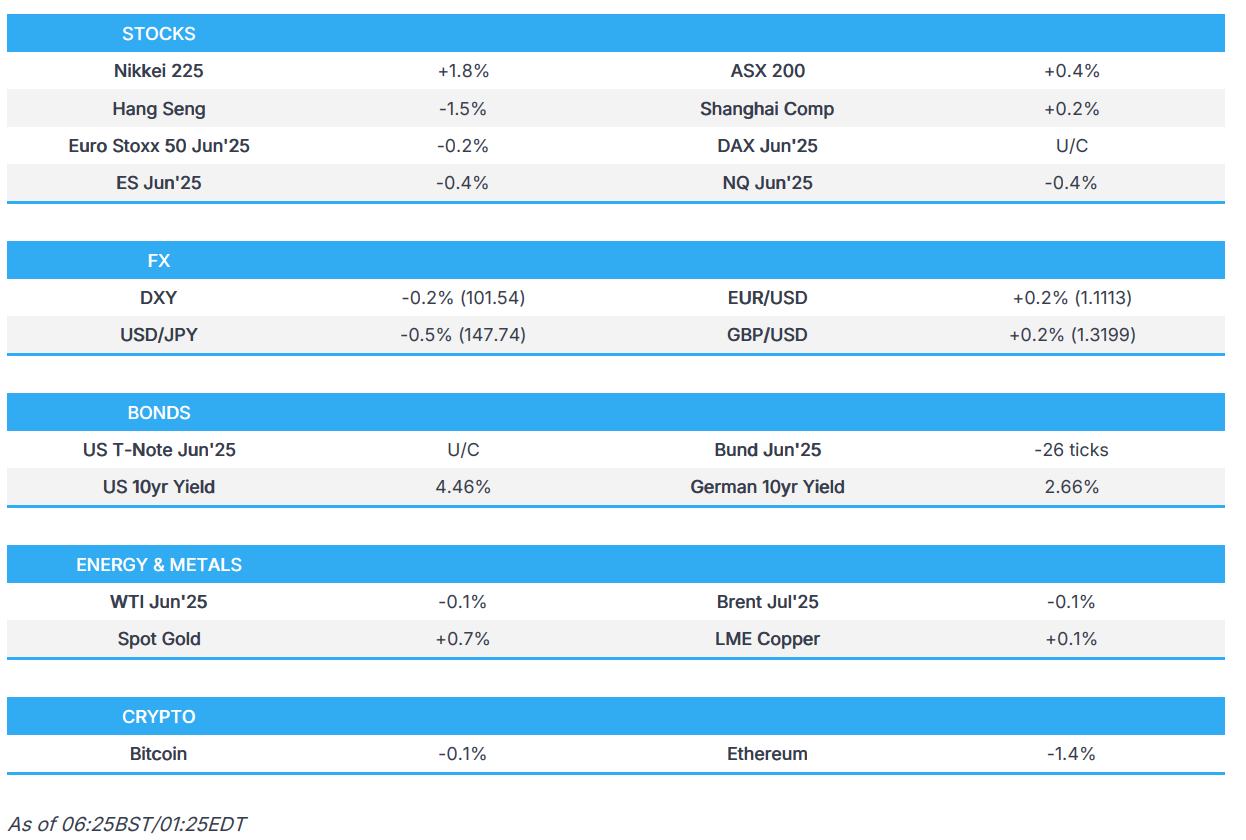

ASIA TRADING TUESDAY MORNING MONDAY NIGHT

SHANGHAI CLOSED UP 5.63 PTS OR 0.17%

//Hang Seng CLOSED DOWN 470.93 PTS OR 2.00%

// Nikkei CLOSED UP 539.00 PTS OR 1.43% //Australia’s all ordinaries CLOSED UP .52%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1991 OFFSHORE CLOSED UP AT 7.1953 / Oil UP TO 62.02 dollars per barrel for WTI and BRENT UP TO 64.98 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1991 AND STRONGER//OFF SHORE YUAN TRADING UP 7.1953 AGAINST US DOLLAR/ AND THUS STRONGER

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1991 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.1953 (CCP MANIPULATED)

SHANGHAI CLOSED UP 5.63 PTS OR 0.17%

HANG SENG CLOSED DOWN 539.00 PTS OR 2.00%

2. Nikkei closed UP 539.00 PTS OR 1.49%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 101.34// EURO RISES TO 1.1114 UP 19 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.449//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.56…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6685/Italian 10 Yr bond yield UP to 3.690 SPAIN 10 YR BOND YIELD UP TO 3.297%

3i Greek 10 year bond yield UP TO 3.448

3j Gold at $3257.65 Silver at: 33.15 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 20 /100 roubles/dollar; ROUBLE AT 80.50

3m oil into the 62 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.12// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.454% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8449 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9371 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.460 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.901 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.983 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.80

10 YR UK BOND YIELD: 4.7285 UP 3 PTS

10 YR CANADA BOND YIELD: 3.207 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.809 DOWN 6 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

Futures Dip As Torrid Squeeze Pauses Ahead Of CPI Report

Tuesday, May 13, 2025 – 08:24 AM

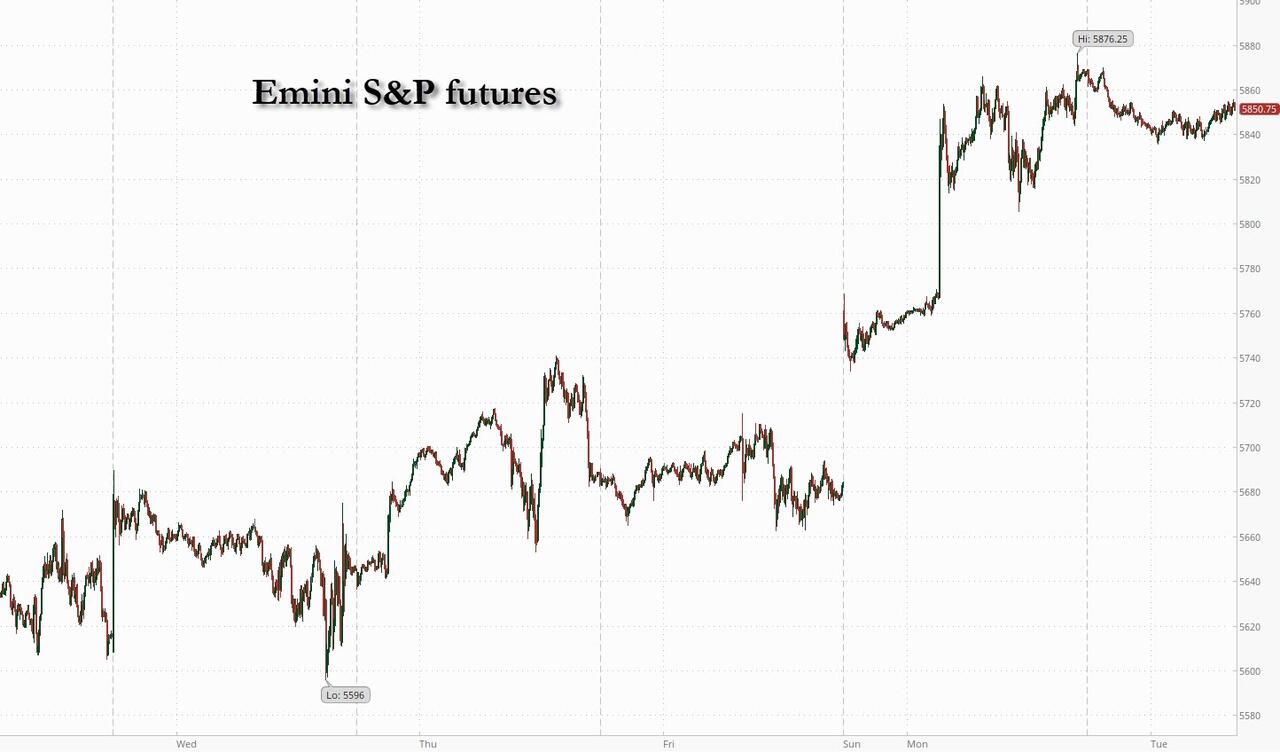

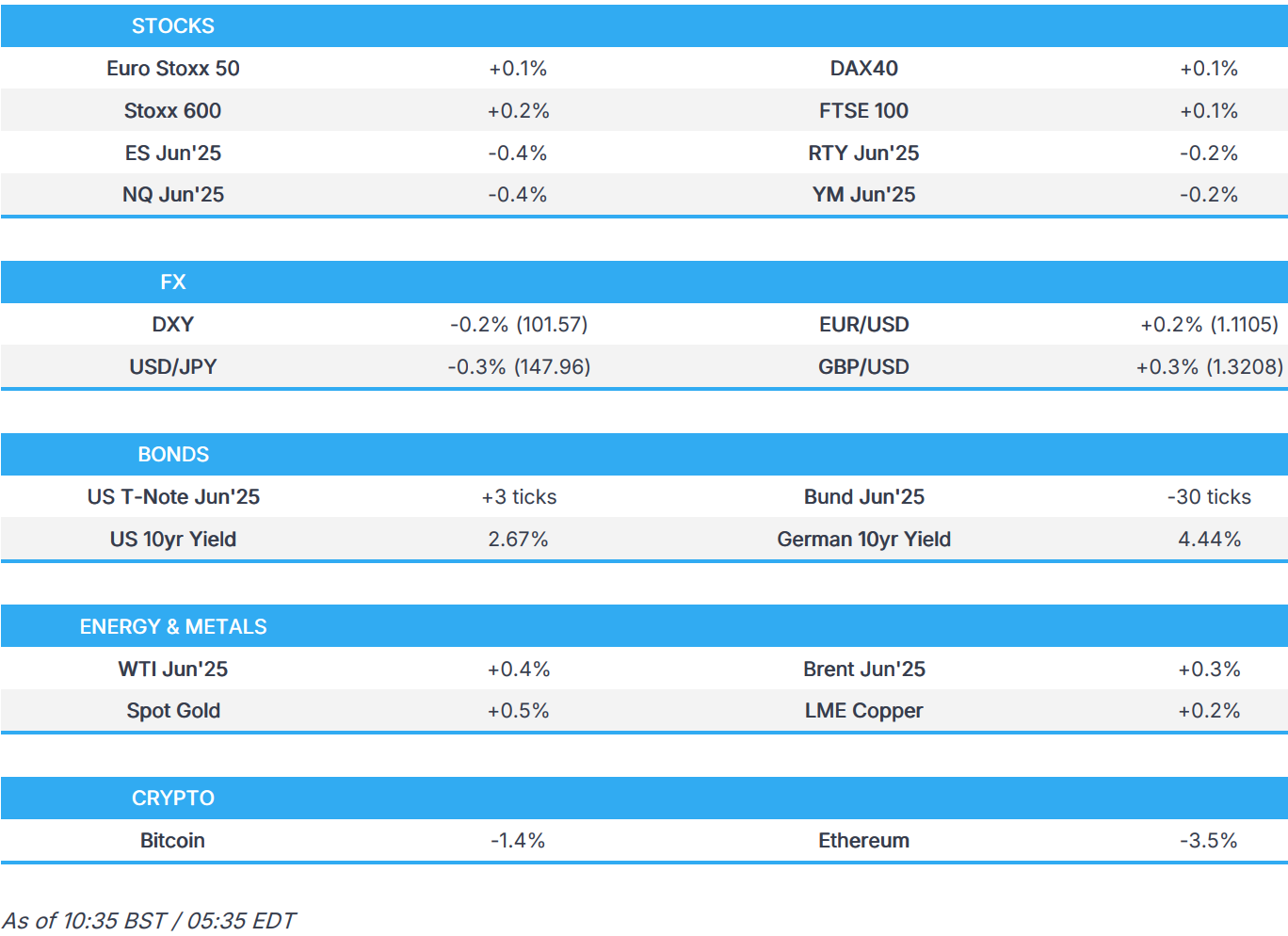

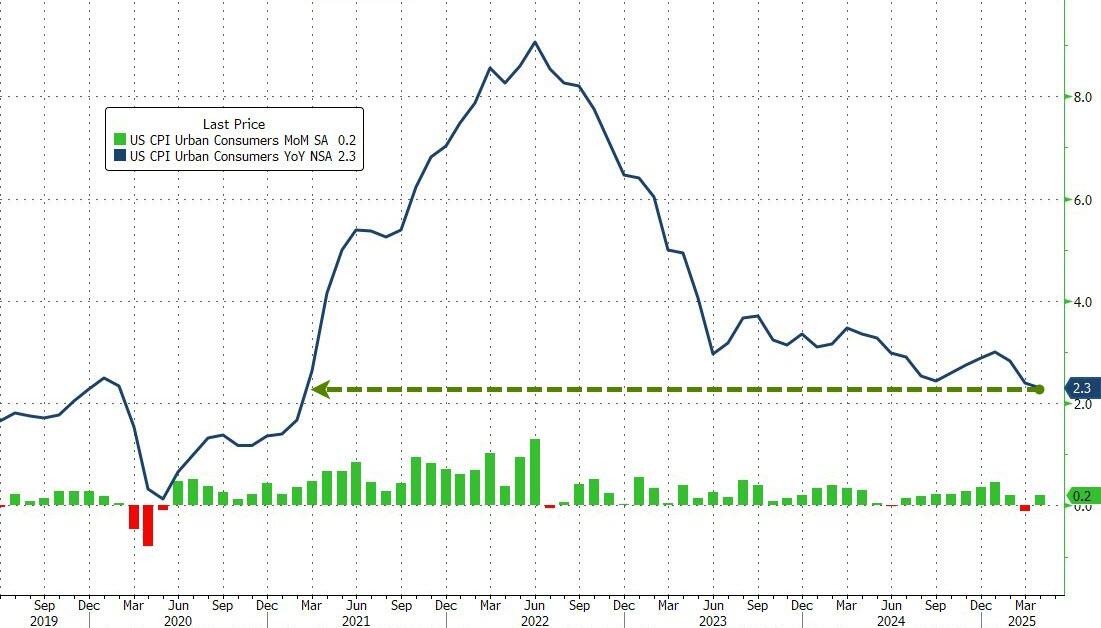

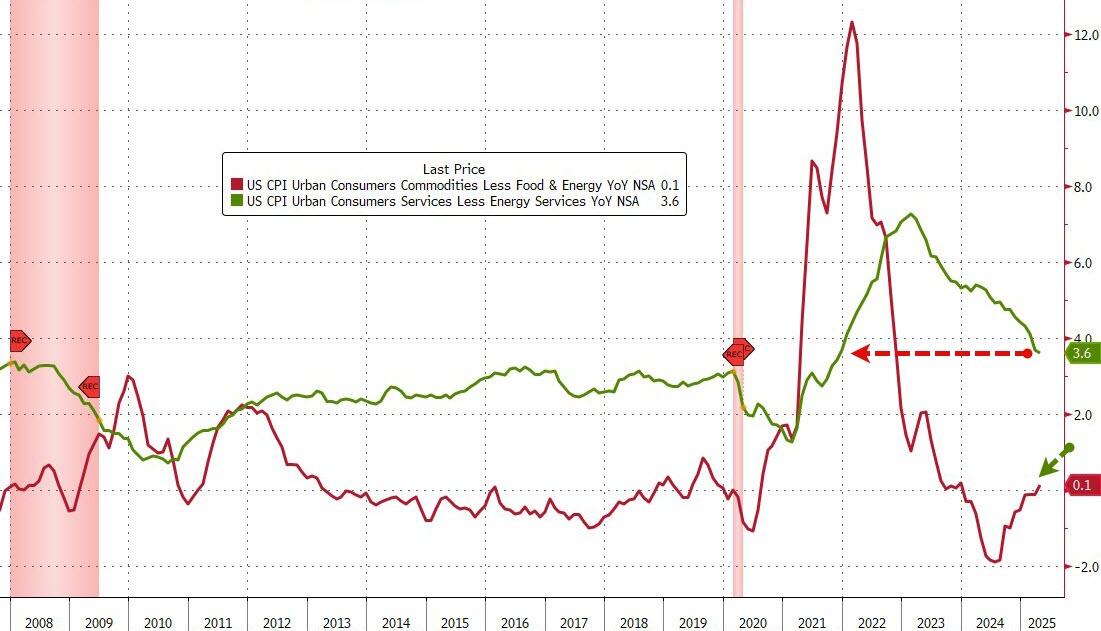

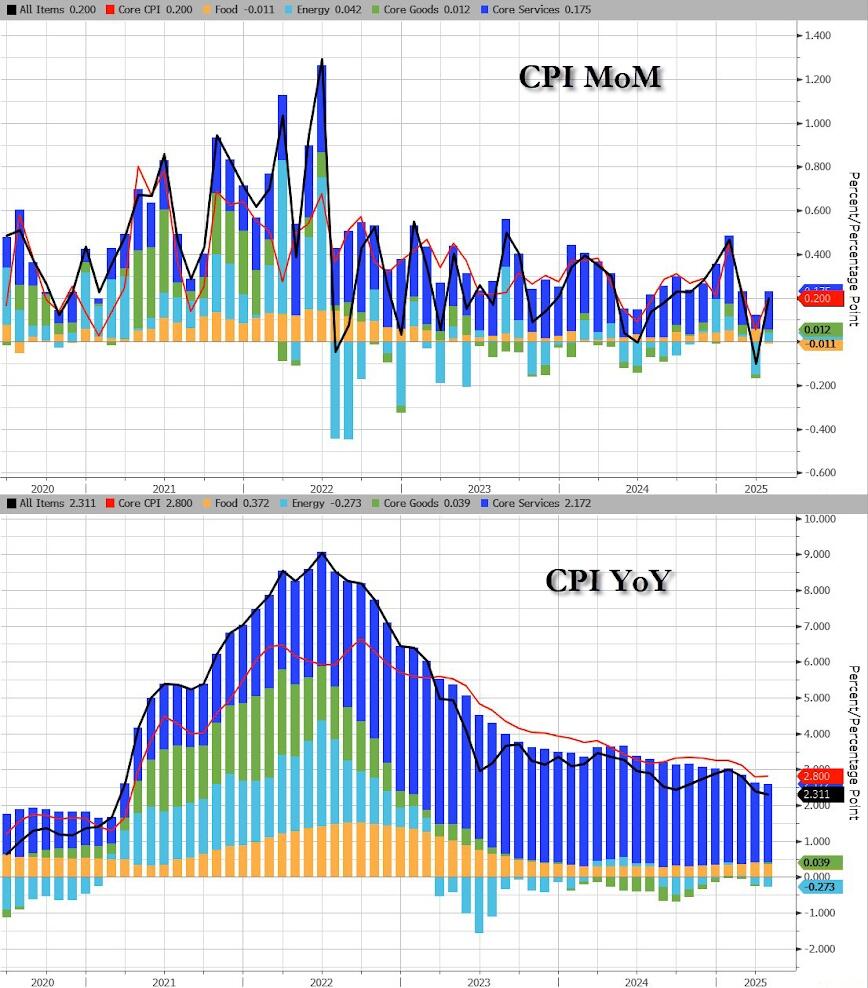

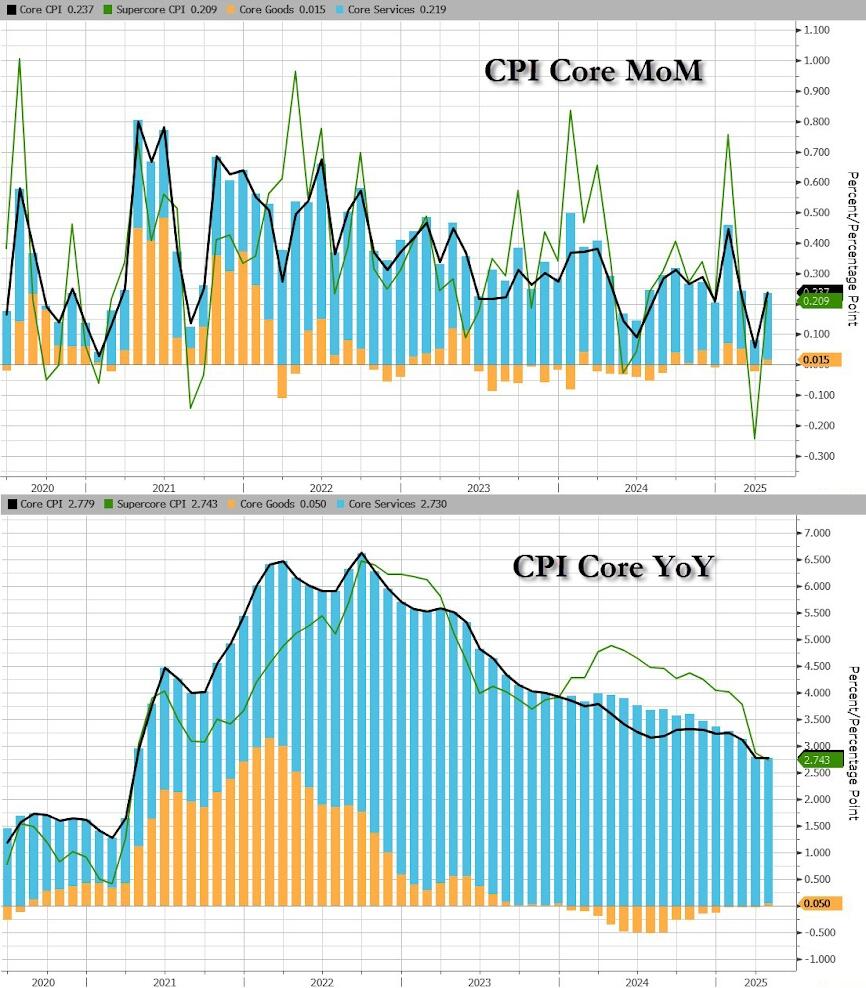

US equity futures are modestly lower ahead of today’s CPI report, but well off session lows, as markets take a slight pause following yesterday’s surge and as trade war truce euphoria gives way to lingering concerns about inflation and economic growth. As of 8:00am ET, S&P and Nasdaq 100 futures were down 0.2% with Mag7 and Semis names weaker pre-mkt, pulling the index lower. UnitedHealth Group sank 10% in pre-market trading after suspending its 2025 outlook. In the latest trade war news, US reduced the tariff on ‘de minimis’ shipments from China, per Reuters, from 120% to 54%, while China reversed its ban on Boeing jets. Appetite for safer assets picked up again, with Treasury yields falling and gold prices on the rise. The dollar slipped after gaining more than 1.4% yesterday, its strongest day since Nov 6, 2024, the day after the election. Today’s macro data focus is on CPI where the YoY numbers are expected to remain flat MoM despite an acceleration in the MoM prints. Earnings prints are not expected to be market moving today.

In premarket trading, Magnificent Seven stocks were mostly lower with the exception of NVDA (Tesla -0.3%, Meta Platforms -0.2%, Microsoft -0.3%, Apple -0.3%, Alphabet -0.2%, Amazon +0.02%, Nvidia +0.2%). Coinbase Global (COIN) climbs 9% after S&P Dow Jones Indices said the company will join the S&P 500 Index before trading opens May 19. UnitedHealth Group shares drop 10% after the health insurer suspended its 2025 outlook and said CEO Andrew Witty is stepping down for personal reasons, effective immediately. Here are some more notable premarket movers: