MAY 16/ANOTHER RAID ON OUR PRECIOUS METALS; GOLD CLOSED DOWN $38.90 TO $3184.50 WHILE SILVER WAS DOWN 24 CENTS TO $32.20//PLAITNUM WAS DOWN $4..00 TO $989.95 WHILE PALLADIUM WAS DOWN $47.10 TO $959.95//GOLD COMMENTARY TONIGHT FROM ALASDAIR MACLEOD AND FROM SINGAPORE NEWS//ESSENTIAL GOLD /SILVER PODCAST A MUST VIEW: LIVE FROM THE VAULT ANDREW MAGUIRE PODCAST 223//CHINA DEVELOPS A NEW HYPERSONIC MISSILE//ISRAEL UPDATES;; HOUTHIS FIRE ANOTHER MISSILE WHICH ISRAEL KNOCKS OUT OF THE SKY AND THEN ISRAEL WHACKS YEMEN’S MAJOR PORTS/ISRAEL VS HAMAS//WEST BANK UPDATES//COVID UPDATES/VACCINE INJURY REPORT/NEWS ADDICTS ETC//RABOBANK REPORT ON GLOBAL ECONOMY//BIG NEWS; TRUMP TO SET TARIFFS ON ALL NATIONS IN TWO WEEKS//USA DATA RELEASES//USA ECONOMIC NEWS ON BOEING’S MAX 737 DAMAGES DUE TO THEIR BLOWUPS//SWAMP STORIES FOR YOU TONIGHT//

099 H DEUTSCHE BANK AG 46 118 C MACQUARIE FUTURES US 3 118 H MACQUARIE FUTURES US 500 190 H BMO CAPITAL MARKETS 309 323 C HSBC 75 332 H STANDARD CHARTERED B 6 363 H WELLS FARGO SECURITI 7 555 C BNP PARIBAS SEC CORP 23 661 C JP MORGAN SECURITIES 10 195 737 C ADVANTAGE FUTURES 1 905 C ADM 1

TOTAL: 588 588 MONTH TO DATE: 23,096

MONTH TO DATE: 22,508

JPMORGAN STOPPED 334/3215

MAY

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT NOTICES FOR 588 OZ 58, oz or 1.828 TONNES

total notices so far: 23,096 contracts for 2,309,600 OR 71.838 tonnes)

FOR MAY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month : 14,466 CONTRACTS (NOTICES) for 72.330 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $38.90 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD//

INVENTORY RESTS AT 927.62 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.24 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV: //

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 449.193 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 411 CONTRACTS TO 137,423 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.04 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. WE HAD A FAIR SIZED LOSS OF 286 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A 125 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING THURSDAY AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON THURSDAY WITH SILVER’S SMALL GAIN IN PRICE AND THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH ANOTHER HUGE T.A.S. ISSUANCE OF 463 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A 125 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 463 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FRIDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A SMALL SIZED 286 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR GAIN IN PRICE OF $0.04.

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS MUST NOW BE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT/FRIDAY MORNING: A HUGE 463 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.04) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH

WE HAD A 125 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 67.830 MILLION OZ TO WHICH WE ADD OUR 2 CONTRACT QUEUE JUMP OF 10,000 OZ AND THEN WE MUST ADD THOSE CRAZY CONTRACT EXCHANGE FOR RISK FOR 12.93 MILLION OZ:

THUS:

INITIAL STANDING FOR MAY: 74.530 MILLION OZ WHICH INCLUDES TODAY’S 10,000 OZ QUEUE JUMP + 12.93 MILLION OZ (EX FOR RISK) EQUALS 87.460 MILLION OZ./

WE HAD:

/ FAIR COMEX OI LOSS+// A 125 SIZED EFP ISSUANCE (125 CONTRACTS)/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 463 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A SMALL 130 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 12 DAYS, total 2883 contracts: OR 14,415 MILLION OZ (240 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 14.415 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 14.415 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 411 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.04 IN SILVER PRICING AT THE COMEX// THURSDAY.,. . THE CME NOTIFIED US THAT WE HAD A 100 CONTRACT EFP ISSUANCE CONTRACTS: 125 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND NOW MAY:

NEW STANDING FOR MAY: 74.530 MILLION OZ. (INCLUDES 10,000 OZ QUEUE JUMP + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 87.460 MILLION OZ

THE NEW TAS ISSUANCE FRIDAY NIGHT (463 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TODAY’S TRADING (FRIDAY TRADING) AND BEYOND.

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1373 OI CONTRACTS TO 440,192 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1347 CONTRACTS //.

WE HAD A FAIR SIZED DECREASE IN COMEX OI (1347 CONTRACTS) . THIS OCCURRED DESPITE OUR GAIN OF $38.80 IN PRICE THURSDAY. ON WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER..

FOR THE MONTH OF APRIL WE HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES/) TO WHICH WE ADDED + 8.3571 TONNES EX FOR RISK = 209.953 TONNES STANDING!

FINAL STANDING FOR APRIL; 201.443 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

AND NOW MAY:

INITIAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD YESTERDAY’S EXCHANGE FOR RISK OF 1.633 TONNES TO LAST WEEK”S 1.55 TONNES TO EQUAL 3.183 TONNES// NEW EXCHANGE FOR RISK = 3.183 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 72.006 TONNES. THUS STANDING FOR MAY INCREASES TO 75.189 TONNES OF GOLD

/ ALL OF THIS HAPPENED WITH OUR $38.80 GAIN IN PRICE WITH RESPECT TO THURSDAY’S COMEX ///. WE HAD A SMALL SIZED LOSS OF 286 OI CONTRACTS (1.430 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AS WELL AS THE SAME FOR APRIL AND NOW MAY….. A MONSTROUS 75.189 TONNES DESPITE IT BEING AN OFF MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 700 CONTRACT:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 440,192/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 137,293 CONTRACTS!!

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 673 CONTRACTS WITH 1373 CONTRACTS DECREASED AT THE COMEX// AND A SMALL SIZED 700 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 673 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 581 CONTRACTS ISSUED. THIS ENDS THE 5TH CONSECUTIVE T.A.S ISSUANCED AVERAGING 30,000+ FOR THIS MONTH

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (700 CONTRACT) ACCOMPANYING THE FAIR SIZED DECREASE IN COMEX OI OF 1373 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 673 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING FOR GOLD FOR MAY AT 75.189 TONNES ( WHICH WHICH INCLUDES OUR 3.987 TONNES QUEUE JUMP AND THEN WE ADD OUR MAY 13 AND 15TH ISSUANCE OF 3.183 TONNES EX FOR RISK//NEW TOTAL 75.189 TONNES

NEW STANDING FOR GOLD, MAY CONTRACT ADVANCES TO: 75.189 TONNES OF GOLD.(INCLUDES QUEUE JUMPING AND EX FOR RISK ISSUANCE)

.

/ 3) HUGE T.A.S. LIQUIDATION , AS WE HAD 1)A $38.80 COMEX PRICE GAIN.. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THAT GAIN IN PRICE AS WE HAD OUR FAIR GAIN OF 2299 CONTRACTS ON OUR TWO EXCHANGES// /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY.

4) FAIR SIZED COMEX OI LOSS// 5) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (700 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 581 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAY INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 16,215 CONTRACTS OR 1,621,500 OZ OR 50.435 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 1351 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN12 TRADING DAY(S) IN TONNES 50.435 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 50.435 TONNES DIVIDED BY 3550 x 100% TONNES = 1.42% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 50.435 TONNES OF GOLD EFP ISSUANCE

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A STRONG SIZED 411 CONTRACTS OI TO 137,293 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 125 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 125 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 125 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 281 CONTRACTS AND ADD TO THE 125 E.FP. ISSUED

WE OBTAIN A SMALL SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 286 CONTRACTS WITH THE GAIN IN PRICE OF $0.04 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 0.78 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

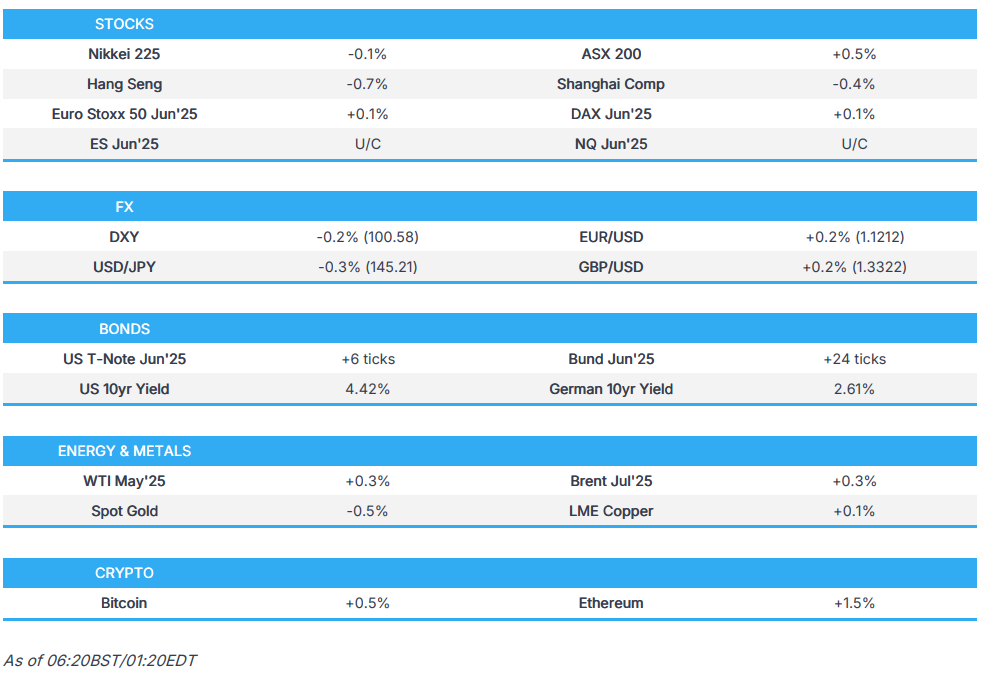

2.ASIAN AFFAIRS FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 13.36 PTS OR 0.40%

//Hang Seng CLOSED DOWN 97.48 PTS OR 0.42%

// Nikkei CLOSED DOWN 1.79 PTS OR 0.00% //Australia’s all ordinaries CLOSED UP .57%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.029 OFFSHORE CLOSED UP AT 7.2033/ Oil UP TO 61.39 dollars per barrel for WTI and BRENT UP TO 64.27 Stocks in Europe OPENED ALL MGREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.2029 AND STRONGER//OFF SHORE YUAN TRADING UP 7.2033 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED1373 CONTRACTS TO 440,192 DESPITE OUR STRONG GAIN IN PRICE OF $38.80 WITH RESPECT TO THURSDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT STRONG PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1700 ).

THE CME ANNOUNCED THURSDAY NIGHT A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR NIL OZ OR 0 TONNES. TOTAL ISSUANCE FOR MAY REMAINS AT 3.184 TONNES OF GOLD AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES.

IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST THREE PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

MAY: 2EX. FOR RISK ISSUED SO FAR FOR 1025 CONTRACTS OR 102500 OZ OR 3.188. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!

DETAILS ON MAY COMEX MONTH//INITIAL

IN TOTAL WE HAD A SMALL SIZED LOSS ON OUR TWO EXCHANGES OF 673 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF APRIL AND ONTO MAY, CONTINUED TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. HOWEVER TODAY’S NUMBER IS SMALL AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 581 T.A.S. FOLLOWING HUGE ISSUANCES DURING OUR LAST 5 TRADING DAYS THIS WEEK. . LAST THURSDAY’S ISSUANCE WAS THE HIGHEST NUMBER BY FAR IN COMEX HISTORY WITH LAST FRIDAY’S BEING THE 2ND HIGHEST EVER RECORDED!THE AVERAGE OF THE 5 ISSUANCES WAS 35,000+. NATURALLY THAT SIGNALS THAT WE WILL WITNESS CONTINUAL RAIDS AND IT CONTINUES TODAY!…

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY AS YOU WILL SEE BELOW ANOTHER HUMONGOUS QUEUE JUMP OCCURRED ON MAY’S DELIVERY CYCLE TODAY (THURSDAY) AT 9.978TONNES, THIS MONTH WE HAVE RECORDED THE HIGHEST EVER QUEUE JUMP RECORDED IN COMEX GOLD HISTORY AT 9.978 TONNES!!!

THE TONNAGE STANDING FOR GOLD FOR MAY IS NOW 75.189 TONNES (WHICH INCLUDES TODAY’S STRONG QUEUE JUMP AND 3.184 TONNES EX FOR RISK!)

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 222 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 700 EFP CONTRACT WAS ISSUED: : /JUNE 700 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 700 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

WE HAD :

HUGE LIQUIDATION OF OUR T.A.S. SPREADERS

ZERO SPEC LIQUIDATION DESPITE OUR LOSS IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A SMALL SIZED, 581 CONTRACTS.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL AND MAY

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE

FINAL STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (209.573 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 5 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY:

INITIAL STANDING AT 28.945 INITAL GOLD TONNES STANDING FIRST DAY NOTICE PLUS 6.4634 TONNES QUEUE JUMP MAY 7 (A RECORD) + ANOTHER HUGE QUEUE JUMP MAY 9 OF 0.534 TONNES + MAY 12 AT .5132 TONNES _ MAY 13; QUEUE JUMP OF 2.444 TONNES AND THEN YESTERDAY’S MAY 14 RECORD 6.8800 TONNES AND THEN TODAY’S (MAY 15) RECORD OF 9.978 PLUS 3.183 TONNES AND FINALLY TODAY’S QUEUE JUMP OF 108,900 OZ/3.387 TONNES (MAY 16) + EXCHANGE FOR RISK = 75.189 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 209.953 TONNES (INCLUDES 8.3571 TONNES EX FOR RISK/AND ALL MONTHLY QUEUE JUMPING)

MAY: STANDING NOW 72.006 TONNES (INCLUDES ALL QUEUE JUMPING FOR THE MONTH) + 3.183 TONNES EX FOR RISK EQUALS 75.189 TONNES!!

COMEX GOLD TRADING/MAY CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $38.80/ /)AND THEY WERE A UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A SMALL SIZED LOSS IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION THURSDAY AS THEY ARE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE THE MAGIC $3,400 BARRIER AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS IT LOOKS LIKE THEY ARE NOW SUCCEEDING AS GOLD ATTEMPTED TO BREACH THAT 3400 DOLLAR BARRIER AGAIN THURSDAY TRADING. IT IS NOW TRADING EARLY FRIDAY MORNING WELL BELOW TO THAT LEVEL AT $3180.00

FRIDAY MORNING/THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /MAY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 2 ISSUANCES FOR 102,500 OZ. THIS TOTALS 3.183 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

HERE IS WHAT HAPPENED LAST MONTH; FINAL GOLD STANDING FOR APRIL:

APRIL: 201.573 TONNES +(8.3571 EX FOR RISK// FOR APRIL DELIVERY MONTH =209.953 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS MAY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// MAY COMEX CONTRACT

WE HAVE LOST A SMALL SIZED TOTAL OF 2.093 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY FIRST RECORDED AT 28.945 TONNES ON FIRST DAY NOTICE/APRIL 30. WE HAD A MONSTER 3208 CONTRACT QUEUE JUMP FOR 108,900 OZ OR 3.987 TONNES. THIS QUEUE JUMP IS CENTRAL BANKS JUMPING AHEAD OF US SIMPLE MORTALS DEMANDING GOLD FOR THEIR RESERVES. THUS NEW STANDING ADVANCES TO 72.006 TONNES OF GOLD. TO WHICH WE ADD (MAY 13 AND MAY 15) EXCHANGE FOR RISK ISSUANCE FOR 3.183 TONNES//NEW TOTAL GOLD STANDING FOR MAY INCREASES TO 75.189 TONNES

THUS MAY STANDING FOR GOLD SO FAR: 75.189 TONNES

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $38.80

WE HAD A STRONG 1347 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 673 CONTRACTS OR 67,300 0Z (2.093 TONNES)

Total monthly oz gold served (contracts) so far this month

23,096 notices 2,309,600 oz 71,838 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 0 customer entry

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:0

adjustments: 4 all dealer to customer

a) JPmorgan: 32.151 oe kilobar

b) Malca: 37,616.670 oz (1170 kilobars)

c) Manfra 137,801.588 oz

d) Stonex 2101.44 oz

removal: from customer account JPMorgan 32.15 oz (1 kilobarts)

AMOUNT OF GOLD STANDING FOR MAY

THE FRONT MONTH OF MAY STANDS AT 642 CONTRACTS FOR A LOSS OF 2126 CONTRACTS. WE HAD 3215 CONTRACTS SERVED ON THURSDAY SO WE GAINED 1089 CONTRACTS AND THUS WE WITNESS A MONSTER 108,900 OZ QUEUE JUMP FOR 3.387 TONNES. THIS FOLLOWS YESTERDAY’S RECORD BREAKING 9.987 TONNES. FOR THE PAST 4 DAYS WE HAVE RECORDED 22.605 TONNES OF QUEUE JUMPS. ALL OF THIS IS PHYSICAL GOLD AND ALL GOING TO CENTRAL BANKS.

JUNE LOST 7226 CONTRACTS TO 189,555. JUNE BECOMES OUR NEW FRONT MONTH AND THIS MONTH WILL BE A WHOPPER OF A DELIVERY MONTH. THE FRBNY IS QUITE NERVOUS LOOKING AT JUNE OI.

JULY GAINED 392 CONTRACTS TO STAND AT 3622

We had 588 contracts filed for today representing 58,800 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 10 notices issued from their client or customer account. The total of all issuance by all participants equate to 588 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 198 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY /2025. contract month, we take the total number of notices filed so far for the month (23,096 X 100 oz ) to which we add the difference between the open interest for the front month of MAY (642 CONTRACTS) minus the number of notices served upon today (588 x 100 oz per contract) equals 2,315,000 OZ OR 72.006 TONNES to which we add 3.183 tonnes of gold issued under exchange for risk//new totals 75.189 tonnes

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (23,096 x 100 oz +we add the difference for front month of MAY (642 OI} minus the number of notices served upon today (588 x 100 oz) which equals 2,315,000 OZ OR 72.006 TONNES + 3.183 tonnes = 75.189 tonnes

TOTAL COMEX GOLD STANDING FOR MAY.: 75.189 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..

JPMorgan has a total silver weight: 217.184million oz/502 oz million or 43.22%

TOTAL REGISTERED SILVER: 168.084 MILLION OZ//.TOTAL REG + ELIGIBLE. 502.162Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2025 OI: 441 OPEN INTEREST CONTRACTS FOR A LOSS OF 166 CONTRACTS. WE HAD 168 NOTICES FILED ON THURSDAY SO WE GAINED 2 CONTRACTS WHICH UNDERWENT A QUEUE JUMP OF 10,000 OZ WHERE THESE BOYS HAVE DECIDED TO TAKE DELIVERY OVER HERE. I MUST REPORT WE HAD 0 EXCHANGE FOR RISK ISSUANCE FOR TODAY. THUS THE NEW TOTAL REMAINS AT TWO ISSUANCES OF EXCHANGE FOR RISK IS 12.93 MILLION OZ.

JUNE SAW A LOSS OF 12 CONTRACTS DOWN TO 2954 CONTRACTS. JUNE OI REFUSES TO LIQUIDATE

WE WILL PROBABLY HAVE OVER 14 MILLION OZ STAND FOR JUNE/AN OFF MONTH

AS IT IS NOW THE FRONT MONTH.

JULY LOST 264 CONTRACTS DOWN TO 104,831

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 or 0.005 MILLION oz

CONFIRMED volume; ON THURSDAY 48,007poor//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 14,466 X5,000 oz = 72.330 MILLION oz

to which we add the difference between the open interest for the front month of MAY (441) AND the number of notices served upon today (1 )x (5000 oz)

Thus the standings for silver for the MAY 2025 contract month: (14,466) Notices served so far) x 5000 oz + OI for the front month of MAY(441) minus number of notices served upon today (1)x 5000 oz equals silver standing for the MAY contract month equating to 74.530 MILLION OZ . THEN WE MUST ADD OUR NEW 12.93 TONNES OF EXCHANGE FOR RISK. NEW TOTAL STANDING FOR SILVER: 87.460 MILLION OZ

New total standing: 87.460 million oz which is huge for this active delivery month of MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 168.094million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

MAY 16 WITH GOLD DOWN $38.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 927.62 TONNES

MAY 15 WITH GOLD UP $38.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.53 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 931.92 TONNES

MAY 14 WITH GOLD DOWN $40.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 936.51 TONNES

MAY 13 WITH GOLD UP $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 12 WITH GOLD DOWN $115.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 9 WITH GOLD UP $37.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 939.68 TONNES

MAY 8 WITH GOLD DOWN $82.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.23 TONNES OF GOLD WITHDRAWN FROM THE GLD/ ///INVENTORY RESTS AT 937.67 TONNES

MAY 7 WITH GOLD DOWN $30.30 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 937.96 TONNES

MAY 6 WITH GOLD UP $101.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 937.96 TONNES

MAY 5 WITH GOLD UP $77.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.13 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.28 TONNES

MAY 2 WITH GOLD UP $ 18.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 945.41 TONNES

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

APRIL29 WITH GOLD DOWN $13.45 TODAY// NO CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL28 WITH GOLD UP $50.20 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL25 WITH GOLD DOWN $49.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVEV WITHDRAWAL OF 3.911 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 948.56 TONNES

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

GLD INVENTORY: 927.62 TONNES, TONIGHTS TOTAL

SILVER

MAY 16 WITH SILVER DOWN $0.24/NO CHANGES IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 15 WITH SILVER UP 0.04/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.909 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 14 WITH SILVER DOWN $0.39/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.682 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.102 MILLION OZ

MAY 13 WITH SILVER UP $0.44/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 12 WITH SILVER DOWN $0.30/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 9 WITH SILVER UP $0.31/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 8 WITH SILVER DOWN $0.16/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 7 WITH SILVER DOWN $0.54/NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 6 WITH SILVER UP $0.92 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A HUG WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 5 WITH SILVER UP $0.08 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF 0.117 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.602 MILLION OZ

MAY 2 WITH SILVER DOWN $0.19 /MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 4.545 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.424 MILLION OZ

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

APRIL29 WITH SILVER UP $0.30 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.229 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 451.925 MILLION OZ

APRIL28 WITH SILVER DOWN $0.03 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.136 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.696 MILLION OZ

APRIL25 WITH SILVER DOWN $0.44 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 3.639 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.832 MILLION OZ

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

Our friend and colleague Jim Rickards was on Steve Bannon’s War Room show Tuesday, and it may be the most important interview Jim has done this year.

In this fascinating discussion, Jim starts with the history of the original petrodollar system. And he knows the subject well, having helped create it.

The premise of the 1974 petrodollar agreement was that Saudi Arabia would only sell oil in dollars, which would stimulate demand for greenbacks as a reserve currency.

Here’s Jim explaining the basics to Steve Bannon’s audience:

“We had a carrot and stick approach. Bill Simon, who was Secretary of the Treasury, went to the Saudis and said ‘everybody in the world needs oil, and if you price oil in dollars, then everybody needs dollars.’

And that basically underpins the role of the dollar today as the world’s reserve currency.

The stick was, if you don’t do it we’re going to invade Saudi Arabia and take over oil production.

The carrot was, if you price oil in dollars, we’ll give you a security umbrella.

It’s rare to hear such candor coming from someone who was directly involved in the formation of the petrodollar system.

Needless to say, the petrodollar system was successful and led to a resurgence in the American dollar as the world’s key reserve currency (despite Nixon ditching the gold standard just 3 years earlier).

At this point, Steve Bannon interrupted with an insightful question (paraphrased):

“Wait, you say the petrodollar system is still in place, but the Saudis are now selling oil to China for yuan. Aren’t cracks showing in the petrodollar system?”

Jim responded that yes, cracks are starting to show in the system, and that’s why Trump was in Saudi Arabia, to seal a “Petrodollar 2.0” agreement. Jim also points out that, at least for now, the amount of oil Saudi Arabia is selling for yuan and other currencies is miniscule compared to dollar-based sales.

Jim proceeds to lay out the purpose of Petrodollar 2.0:

“The U.S., by strengthening its relationship with Saudi Arabia, and creating Petrodollar 2.0, puts the pressure on China to reduce their tariffs and meet Trump’s requirements. Otherwise they don’t have a source of dollars.”

This time around, Trump is using a strictly carrot-based approach. He’s on a charm offensive and looking to build strong, lasting ties with Saudi Arabia and the broader Middle East. This is a smart approach and we expect it will bear fruit in the near future.

Had President Trump taken a threatening approach to Saudi Arabia, it almost certainly would have driven the country into China’s waiting arms. And America can’t afford to let that happen.

It’s an excellent interview, and you can watch the entire thing here (free) on Rumble. Jim also gets into Russia vs. Ukraine with Steve, and brings an insightful and unique perspective as always.

Perhaps global economic ills will be put on pause for the summer. But the entire investment world will be looking for the dip to buy the best performing asset of recent months — GOLD

In a continuing consolidation, gold and silver sold off this week. In European trading hours this morning, gold was $3206, down $74 from last Friday’s close and silver at $32.25 was down only 43 cents. The gold/silver ratio is back under 100 at 99.4.

As proof that Western capital markets no longer determine gold and silver prices, declines this week have been during Far East trading hours. While trading on the Globex facility by Westerners cannot be ruled out, the fact that moves happen during Shanghai trading hours should be noted. And while SGE physical deliveries have increased (153.05 tonnes in April v. 120.16 in March) it would appear that leveraged futures in Shanghai are causing some market indigestion.

Meanwhile, attempts by the swaps on Comex to take prices meet resistance. For example, yesterday gold was hit down to $3124 before rallying to close at $3240, a $116 turnaround.

Stand-for deliveries on Comex continue apace. So far this month, we’ve seen 13,265 gold contracts stood for delivery, which is 41.2 tonnes. And 3,484 silver contracts, which represents 541.8 tonnes.

Warehouse statistics show silver stocks close to all-time highs at 501,750,232 ounces, but gold stocks have definitely peaked.

It’s difficult to assess at this point whether the consolidation in gold and silver prices has further to go. The technical chart suggests that gold would look healthier if the long-term moving average was allowed to catch up with the price:

Gold has found support consistently at the 55-day moving average, but it is still far above the 1-year MA currently at 2,701 but rising strongly. Technical analysts would argue that a dip to $3000 over the summer would probably find firm support while allowing the 1-year MA to catch up. However, the outcome is likely to be driven by currency and economic events.

Technically, silver looks more promising, being less extended in its bull market:

This chart is just looking for an excuse to go much higher. So, what are the economic developments likely to cause silver to outperform gold?

Perhaps the clue is to be found in President Trump being increasingly sidelined with respect to tariffs. Scott Bessent, the Treasury Secretary reassured capital markets by negotiating more reasonable tariffs with China, if only for 90 days. That takes us into August, during which time a longer-term agreement might be negotiated.

In other words, it is a case of wait and see, likely to be reflected in the dollar/gold exchange rate. With this pause probably comes a deferment of recessionary fears, which would justify silver’s stronger technicals.

That said, the investment world has been alerted to the prospects for gold. And while equities could continue to rally — depending on bond markets — severely underweight investors will be looking to buy into gold’s dip. Surely, they will be praying for a pullback to $3000…

A stronger technical base would support a move to the $4000 level, being touted by some of the large banks — JPMorgan sees that by Q2 2026. But there are some signs that bond yields are increasing. The 40-year JGB is particularly striking:

So is the long end of the UK gilt market

Others, such as German bunds and US Treasuries show similar patterns, which analysts are ignoring. But they are the sown-seeds of the next credit crisis, crashing equities and likely fiat currencies with them.

other major gold stories:

Singapore news

Kiss of death to NY and London

Singapore’s Abaxx Exchange to launch new gold contract

SINGAPORE-based startup Abaxx Exchange is launching a new physical gold contract next month, seeking to challenge London and New York’s grip on the global bullion market following gold’s record price rally this year, said the Financial Times on Tuesday.

The bourse, which has secured over £77m from investors including BlackRock and CBOE Global Markets, will offer a physical one kilogram gold contract denominated in US dollars and deliverable in Singapore, the paper said.

Abaxx CEO Josh Crumb described the current gold market structure as “dysfunctional”, arguing that infrastructure hasn’t kept pace with trading practices. “Our view is that Asia ex-China needs a gold market, to manage physical gold, that is not reliant on New York and London,” said Crumb, citing “geopolitical” risks in these traditional centres.

The contract will be Singapore’s only physical gold futures offering, potentially meeting regional demand from jewellery manufacturers and investors, said the Financial Times. “In Singapore, people feel like they are not well served by the existing market,” Crumb said. “The actual real physical demand is kilo bars going into Asia.”

Albert Cheng, head of the Singapore Bullion Market Association, commented: “We have the potential to compete with London, but we need the infrastructure to bring in more flows.”

Abaxx eventually aims to offer 24/7 trading, pending regulatory approval. The company, majority-owned by Toronto-listed Abaxx Technologies (market cap £180m), expects to reach break-even during 2026.

Former Goldman Sachs commodities research head Jeff Currie, an Abaxx board member, told the newspaper the gold contract will gain traction quickly: “It’s going to be the most versatile contract out there.”

3. CHRIS POWELL AND GATA DISPATCHES

4/On LFTV, Andrew Maguire LIVE FROM THE VAULT 223

B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//COPPER

6 CRYPTOCURRENCY NEWS

ASIAN MARKETS THIS MORNING:

SHANGHAI CLOSED DOWN 13.36 PTS OR 0.40%

//Hang Seng CLOSED DOWN 97.48 PTS OR 0.42%

// Nikkei CLOSED DOWN 1.79 PTS OR 0.00% //Australia’s all ordinaries CLOSED UP .57%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.029 OFFSHORE CLOSED UP AT 7.2033/ Oil UP TO 61.39 dollars per barrel for WTI and BRENT UP TO 64.27 Stocks in Europe OPENED ALL MGREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.2029 AND STRONGER//OFF SHORE YUAN TRADING UP 7.2033 AGAINST US DOLLAR/ AND THUS STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2029 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.2033 (CCP MANIPULATED)

SHANGHAI CLOSED DOWN 13.36 PTS OR 0.40%

HANG SENG CLOSED DOWN 97.48 PTS OR 0.42%

2. Nikkei closed DOWN 1.79 PTS OR 0.00%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 100.56// EURO RISES TO 1.1202 UP 9 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.452//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 145.27…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and UP FOR DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5844/Italian 10 Yr bond yield DOWN to 3.589 SPAIN 10 YR BOND YIELD DOWN TO 3.202%

3i Greek 10 year bond yield DOWN TO 3.362

3j Gold at $3205.80 Silver at: 32.27 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 54 /100 roubles/dollar; ROUBLE AT 80.54

3m oil into the 61 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 145.27// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.452% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8347 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9357 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.411 DOWN 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.878 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.945 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.82

10 YR UK BOND YIELD: 4.664 DOWN 4 PTS

10 YR CANADA BOND YIELD: 3.146 DOWN 11 BASIS PTS

5 YR CANADA BOND YIELD: 2.747 DOWN 10 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

US Futures Rise For Fifth Day In A Row As S&P 6000 Looms

by Tyler Durden

Friday, May 16, 2025 – 08:23 AM

US stock futures are set for a fifth straight session in the green, as US equity funds benefited from their first inflows since the Liberation Day shock, and with 6000 in the S&P now less than a 100 points away. As of 8:00am, S&P 500 futures were up 0.3% after the index closed up 4.5% for the week on Thursday as the latest economic data spurred speculation the Fed will cut interest rates twice this year. Nasdaq futures gained 0.4% with Mag 7 leading (TSLA (+1.1%), GOOGL (+0.9%), and NVDA (+0.7%) are outperforming). The powerful rally this week has pushed the tech-heavy equity benchmark into overbought territory, while the S&P closed Thursday at the highest level since February. Europe’s benchmark Stoxx 600 gauge also gained, heading for a fifth weekly advance. The dollar weakened for a second session against major peers, while the yen and Swiss franc gained, and the 10-year Treasury yield was lower after declining 10 basis points Thursday as traders priced in more Fed cuts: bond yields are lower, with 2-, 5-, 10-, and 30-year yields down by 3.09bp, 3.7bp, 3.5bp, and 2.6bp respectively. Commodities are mostly lower, led by gold while oil reversed earlier losses. Overnight headlines were largely quiet. Today, we will receive University of Michigan Sentiment survey data, where consensus expects a modest bounce (to 53.5 vs. 52.2 prior).

In premarket trading, Mag 7 stocks are mostly higher with the exception of Meta after an equal-weighted gauge of the group fell over 1% on Thursday (Alphabet +1.5%, Tesla +1.1%, Nvidia +0.9%, Amazon +0.4%, Microsoft little changed, Apple +0.1%, Meta Platforms -0.1%). Charter Communications (CHTR) gains 9.4% after agreeing to merge with Cox Communications in a deal that values Cox at an enterprise value of about $34.5 billion. Vistra (VST) is up 5.1% after it said it executed a definitive agreement to acquire seven modern natural gas generation facilities from Lotus Infrastructure Partners for $1.9 billion. Here are some other notable premarket movers:

Archer Aviation (ACHR) shares rise 5.7%, adding to gains from Thursday following its announcement that the electric vertical take-off and landing aircraft company had been selected as the ‘Official Air Taxi Provider’ for the LA28 Olympic and Paralympic Games.

Doximity (DOCS) drops 18% after the healthcare-software company’s full-year forecast disappointed, with analysts pointing to a cautious tone from the management team on the call regarding the outlook for market growth.

Globant (GLOB) shares sink 28% after the technology services provider cut full-year revenue guidance for 2025 to a level that undershot analysts’ expectations.

Pentair (PNR) shares rise 2.2% after JPMorgan upgrades the water-treatment company to overweight from neutral on expectations of potential guidance upside.

Quantum Computing (QUBT) shares are up 9.7% after the quantum optics technology company reported its first-quarter results.

Rocket Cos. (RKT) gains 4.4% after ValueAct Capital Management LLC reported a 9.9% holding in the mortgage finance company, according to a new 13D filing with the US Securities & Exchange Commission.

Take-Two (TTWO) falls 2% as the video-game publisher’s full-year forecast for revenue came up short.

Travere Therapeutics (TVTX) shares drop 17% after the biotech’s application for its kidney disease treatment Filspari (sparsentan) failed to get priority review status from the US FDA and is set to face an advisory panel.

One month after the nevertrump media hyperventilated about the “US exceptionalism” trade dying, US equities are back in favor following the de-escalation of trade tensions between the US and China. Stocks are now trading like last month’s rout never happened, even though uncertainty remains about the effect of tariffs on the US economy and the direction that the global trade war will take in the coming months. Bank of America’s Michael Hartnett said weekly US equity inflows resumed at $19.8 billion for the first time since Liberation Day. Meanwhile, stocks haven’t been getting rewarded for earnings beats: firms that topped expectations in the first quarter reports saw their share prices rise by less than usual, according to JPMorgan strategists. Meanwhile, Federal Reserve Bank of Atlanta President Raphael Bostic said he expects the US economy to slow this year but not fall into recession.

“For now, we believe that the path of least resistance is still higher for risky assets,” said Mohit Kumar, chief economist and strategist at Jefferies International. “We would start turning a bit more cautious around June/July when we expect the hard data start weakening.”

Thursday afternoon brought a deluge of 13F filings, which showed hedge funds adding healthcare exposure and cutting tech over the first three months of the year. Michael Burry’s Scion Asset Management liquidated almost its entire listed equity portfolio in the first quarter. Meanwhile, Warren Buffett’s Berkshire Hathaway trimmed its holdings of financials stocks.

Traders are also watching negotiations around the US budget with its promise of large tax cuts and the potential impact that will have on the fiscal deficit.

Elsewhere, Japan’s economy shrank for the first time in a year as the surging yen crushed exports, illustrating its vulnerability even before sustaining the impact of Trump’s tariff measures. Paradoxically, the yen gained 0.2% on Friday to trade around 145 per dollar even as Bank of Japan official Toyoaki Nakamura, the most dovish board member, warned against hurrying to raise the benchmark interest rate.

Europe’s benchmark Stoxx 600 gauge also gained, heading for a fifth weekly advance as cooling global trade tensions improve investor sentiment and corporate earnings season comes in better than expected. Health care and food and beverage sectors outperform. Among single stocks Richemont rises after reporting a rise in full year sales. Here are the most notable European movers:

Richemont shares rise as much as 5.5% after the Swiss firm’s jewelry division saw strong growth thanks to demand for its high-end Cartier and Van Cleef & Arpels brands.

Orsted shares rise as much as 2.1%, snapping three days of declines, after UBS analysts say the stock is pricing in a “close to worst case” scenario when it comes to a potential halt order on the Danish company’s two US offshore projects.

1&1 shares soar after its parent United Internet submitted a partial offer to acquire as much as 9.19% of 1&1 shares, for a cash consideration of €18.5 apiece.

Tate & Lyle shares gain as much as 3.1%, among the best performers in the Stoxx 600’s food, beverage and tobacco subgroup, after Citi upgrades the stock to buy from neutral, saying the risk/reward “looks attractive.”

CVC Capital shares climb as much as 5.4%, to the highest in six weeks, after Morgan Stanley upgrades its recommendation on the alternative investment manager to overweight, seeing scope for recovery after recent underperformance.

Nibe falls as much as 4.1% after Handelsbanken cut its recommendation on the Swedish heat-pump manufacturer to sell from hold, quoting recent strong share performance.

Eutelsat shares drop as much as 11% after the satellite operator said on earnings call that it’s “far too early” to discuss the European Union’s revenue commitment to its next-generation low-earth orbit satellites, dampening hope of enhanced government support in the near term.

Rubis shares fall as much as 3.7% after the French energy solutions firm said Nils Christian Bergene will step down as chairman and a member of the supervisory board, a departure that CIC analysts called a surprise.

Workspace Group shares fall as much as 11% after the landlord to mostly small- and medium-sized London businesses warned rising vacancies in its portfolio will dent profits.

Future shares decline as much as 9.2% after the UK specialist publisher said its FY25 organic revenue will face a low-single-digit decline, below estimates.

Tokmanni falls as much as 14%, the most since last July, after the Finnish retail group missed expectations in its first-quarter report.

Dino Polska drops as much as 7.5%, most since August, as Poland’s food retailer reported slowing like-for-like sales in 1Q, raising concerns about its business model and triggering profit taking after 42% rally YTD.

Earlier in the session, Asian stocks traded in a narrow range as the rally sparked by US-China trade talks continued to cool and earnings from Chinese e-commerce giant Alibaba underwhelmed. The MSCI Asia Pacific Index swung between a gain of as much as 0.3% and loss of 0.2%. NetEase was the biggest contributor to the gains, after the China-based video-game company reported first-quarter results that beat expectations. Meanwhile, Alibaba was among the major drags, after its quarterly revenue missed estimates and cloud business disappointed. Key indexes dropped in mainland China, Hong Kong and India, while benchmarks rose in Australia and Taiwan. Goldman Sachs strategists raised their 3-month and 12-month targets for the MSCI Asia Pacific ex-Japan Index to 610 and 660, respectively, from 570 and 620, expecting “moderately higher” returns for the region thanks to improved earnings growth amid a better-than-expected outcome to US-China trade talks.

In FX, the Bloomberg Dollar Spot Index fell as much as 0.2%, declining for the second straight day; it is on track to end the week 0.1% higher; the yen and Swiss franc among the beneficiaries.

In rates, the 10-year Treasury yield was lower after declining 10 basis points Thursday as traders added bets on Fed rate cuts; treasuries are richer across the curve with futures adding to Thursday’s gains and 10-year yields dropping back to 4.405% and near 100-DMA. US yields richer by 2bp to 3bp across the curve with spreads broadly within a basis point of Thursday close; in the 10-year sector bunds and gilts outperform Treasuries by 2.5bp and 1.5bp so far on the day.

In commodities, gold fell to extend its weekly loss as demand for haven assets waned. Oil prices declined after Iran’s foreign minister cast doubts on the status of US-Iran nuclear talks.

Looking at today’s US data calendar, key events includes April housing starts/building permits, import/export price index, May New York services business activity (8:30am), University of Michigan sentiment (10am) and March TIC flows (4pm). Fed speaker slate includes Daly at 9:40pm

Market Snapshot

S&P 500 mini +0.3%

Nasdaq 100 mini +0.3%

Russell 2000 mini +0.4%

Stoxx Europe 600 +0.6%

DAX +0.7%, CAC 40 +0.6%

10-year Treasury yield -3 basis points at 4.4%

VIX -0.2 points at 17.66

Bloomberg Dollar Index -0.1% at 1228.52

euro +0.2% at $1.1208

WTI crude -0.3% at $61.45/barrel

Top Overnight News

Donald Trump said he’d set tariff rates for US trading partners “over the next two to three weeks.” BBG

US Deputy Treasury Secretary Faulkender said he is not concerned about persistent increases in prices, while he added that inflation will return to target levels and they are setting the foundation for the US economy to take off in H2.

The Trump administration plans to put a number of Chinese chipmaking companies (including memory chipmaker ChangXin Memory) on an export blacklist, but some officials want to delay the move to avoid hurting efforts to strike a long-term trade agreement with China. FT

Hopes faded for Russia-Ukraine talks set to take place today in Istanbul. The focus now shifts to when Trump may meet Vladimir Putin.