GOLD CLOSED UP $28.75 TO $3,311.30

SILVER CLOSED UP $0.34 TO $33.34

GOLD ACCESS CLOSED $3321.75

Silver ACCESS CLOSED: $33.59

Bitcoin morning price:$106,360 UP 120 DOLLARS.

Bitcoin: afternoon price: $107,570 up 1330 DOLLARS

Platinum price closing UP $26.00 TO $1076.75

Palladium price; UP $15.45 TO $1029.80

END

*CANADIAN GOLD: $4,602.15 UP 25.10 CDN dollars per oz( * NEW ALL TIME HIGH $4735.70 CDN DOLLARS PER OZ//APRIL 21 2025)

*BRITISH GOLD: 2474.376UP 18.36 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,566.50 BRITISH POUNDS/OZ) MAY 6/2025

*EURO GOLD: 2933.64 UP 18.92 Euros per oz //* (ALL TIME CLOSING HIGH: 3018.80 EUROS PER OZ/ APRIL 21 //2025)

DONATE

EXCHANGE: COMEX

CONTRACT: MAY 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,280.300000000 USD

INTENT DATE: 05/20/2025 DELIVERY DATE: 05/22/2025

FIRM ORG FIRM NAME ISSUED STOPPED

118 H MACQUARIE FUTURES US 28

323 C HSBC 53 186

363 H WELLS FARGO SECURITI 178

661 C JP MORGAN SECURITIES 82

686 H STONEX FINANCIAL INC 10

737 C ADVANTAGE FUTURES 1

TOTAL: 269 269

MONTH TO DATE: 23,650

JPMORGAN STOPPED 82/269

MAY

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024: 269 CONTRACTs NOTICES FOR 26,900 OZ or 0.8367 TONNES

total notices so far: 23,650 contracts for 2,365,000 OR 73.5614 tonnes)

FOR MAY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 73 NOTICE(S) FILED FOR 365,000 OZ/

total number of notices filed so far this month : 14,685 CONTRACTS (NOTICES) for 73.425 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $28.75 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 921.60 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.35 AT THE SLV: HJUGE CHANGES IN SILVER INVENTORY AT THE SLV: //A DEPOSIT OF 2.091 MILLION OZ INTO THE SLV

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 451.875 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 3911 CONTRACTS TO 141,451 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0.65 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. WE HAD A MEGA HUMONGOUS SIZED GAIN OF 4161 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A 250 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING WITH RESPECT TO TUESDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON TUESDAY WITH SILVER’S GAIN IN PRICE AS THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH ANOTHER SMALL T.A.S. ISSUANCE OF 218 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A 250 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 450 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUMONGOUS SIZED 4161 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.65.

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS MUST NOW BE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT/WEDNESDAY MORNING: A STRONG 450 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.65) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH

WE HAD A 250 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 67.830 MILLION OZ TO WHICH WE ADD OUR 0 CONTRACT QUEUE JUMP OF 0 OZ AND THEN WE MUST ADD THOSE CRAZY CONTRACT EXCHANGE FOR RISK FOR 12.93 MILLION OZ:

THUS:

INITIAL STANDING FOR MAY: 75.165 MILLION OZ WHICH INCLUDES TODAY’S 425,000 OZ QUEUE JUMP + 12.93 MILLION OZ (EX FOR RISK) EQUALS 88.095 MILLION OZ./

WE HAD:

/ HUMONGOUS COMEX OI GAIN+// A 250 SIZED EFP ISSUANCE (/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 450 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED A SMALL 234 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 15 DAYS, total 3484 contracts: OR 17.420 MILLION OZ (232 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 17.420 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 17.420 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3911 CONTRACTS WITH OUR GAIN IN PRICE OF $0.65 IN SILVER PRICING AT THE COMEX// TUESDAY.,. . THE CME NOTIFIED US THAT WE HAD A 250 CONTRACT EFP ISSUANCE CONTRACTS: 250 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND NOW MAY:

NEW STANDING FOR MAY: 75.165 MILLION OZ. (INCLUDES 0 OZ QUEUE JUMP + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.0951 MILLION OZ

THE NEW TAS ISSUANCE TUESDAY NIGHT (450 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TODAY’S TRADING (TUESDAY TRADING) AND BEYOND.

WE HAD 73 NOTICE(S) FILED TODAY FOR 365,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 5057 OI CONTRACTS TO 448,000 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 688 CONTRACTS //.

WE HAD A STRONG SIZED INCREASE IN COMEX OI (5057 CONTRACTS) . THIS OCCURRED WITH OUR HUGE GAIN OF $51.40 IN PRICE// TUESDAY///.

FOR THE MONTH OF APRIL WE HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES/) TO WHICH WE ADDED + 8.3571 TONNES EX FOR RISK = 209.953 TONNES STANDING!

FINAL STANDING FOR APRIL; 201.443 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

AND NOW MAY: SUMMARY OF EXCHANGE FOR RISKS ADDED

INITIAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 74.214 TONNES. THUS STANDING FOR MAY INCREASES TO 83.805 TONNES OF GOLD

/ ALL OF THIS HAPPENED WITH OUR $51.40 GAIN IN PRICE WITH RESPECT TO TUESDAY’S COMEX ///. WE HAD A STRONG SIZED GAIN OF 5482 OI CONTRACTS (17.05 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE DURING THE FIRST FEW WEEKS OF MAY, AND THROUGHOUT EACH AND EVERY DAY MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MAY CONTRACT MONTH….. A MONSTROUS 83.905 TONNES DESPITE IT BEING AN OFF MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 425 CONTRACT:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 448,000/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 141,451 CONTRACTS!!

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5482 CONTRACTS WITH 5057 CONTRACTS INCREASED AT THE COMEX// AND A SMALL SIZED 425 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5482 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 982 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS 425 CONTRACT) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 5057 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5482 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING FOR GOLD FOR MAY AT 83.805 TONNES ( WHICH WHICH INCLUDES TODAY’S 0.9455 TONNES QUEUE JUMP AND THEN WE ADD OUR MAY 13 , 15TH AND 19TH ISSUANCE OF 9.589 TONNES EX FOR RISK//NEW TOTAL STANDING FOR GOLD: 83.805 TONNES

NEW STANDING FOR GOLD, MAY CONTRACT ADVANCES TO: 83.805 TONNES OF GOLD.(INCLUDES QUEUE JUMPING AND EX FOR RISK ISSUANCE)

.

/ 3) ZERO T.A.S. LIQUIDATION , AS WE HAD 1)A $51.40 COMEX PRICE GAIN.. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THAT GAIN IN PRICE AS WE HAD OUR STRONG GAIN OF 5480 CONTRACTS ON OUR TWO EXCHANGES// /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY.

4) STRONG SIZED COMEX OI GAIN// 5) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (425 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 982 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAY INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 18,755 CONTRACTS OR 1,875,500 OZ OR 58.335 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 1250 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES 58.335 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 58.335 TONNES DIVIDED BY 3550 x 100% TONNES = 1.642% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 58.335 TONNES OF GOLD EFP ISSUANCE

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 3911 CONTRACTS OI TO 141,451 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 250 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3,911 CONTRACTS AND ADD TO THE 250 E.FP. ISSUED

WE OBTAIN A VERY STRONG SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 4161 CONTRACTS WITH THE GAIN IN PRICE OF $0.65 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 20.805 MILLION PAPER OZ

OCCURRED WITH OUR $0.65 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 10.77 PTS OR 0.32%

//Hang Seng CLOSED UP 152.15 PTS OR 0.64%

// Nikkei CLOSED DOWN 37.69 PTS OR 0.10% //Australia’s all ordinaries CLOSED UP 0.61%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.2183 OFFSHORE CLOSED UP AT 7.2060/ Oil UP TO 62.84 dollars per barrel for WTI and BRENT UP TO 66.32 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.2183 AND STRONGER//OFF SHORE YUAN TRADING UP 7.2060 AGAINST US DOLLAR/ AND THUS STRONGER

END

ASIA TRADING WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 10.77 PTS OR 0.32%

//Hang Seng CLOSED UP 152.15 PTS OR 0.64%

// Nikkei CLOSED DOWN 37.69 PTS OR 0.10% //Australia’s all ordinaries CLOSED UP 0.61%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.2183 OFFSHORE CLOSED UP AT 7.2060/ Oil UP TO 62.84 dollars per barrel for WTI and BRENT UP TO 66.32 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.2060 AND STRONGER//OFF SHORE YUAN TRADING UP 7.2060 AGAINST US DOLLAR/ AND THUS STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

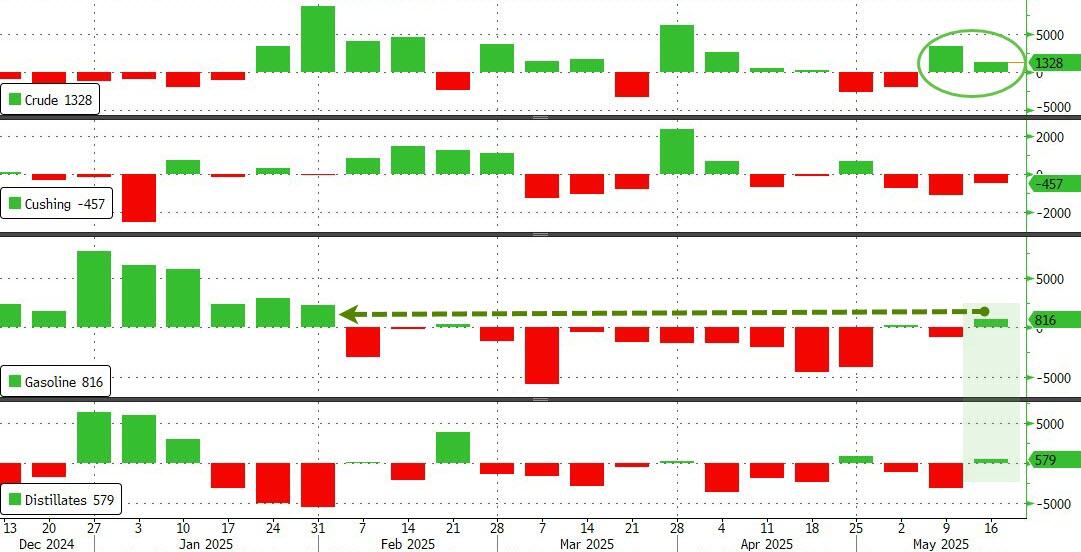

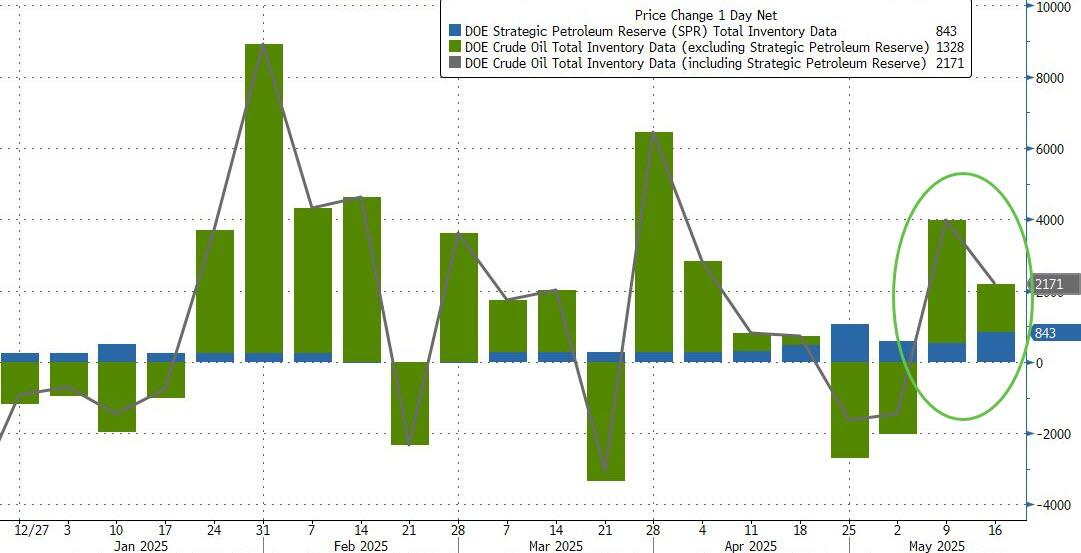

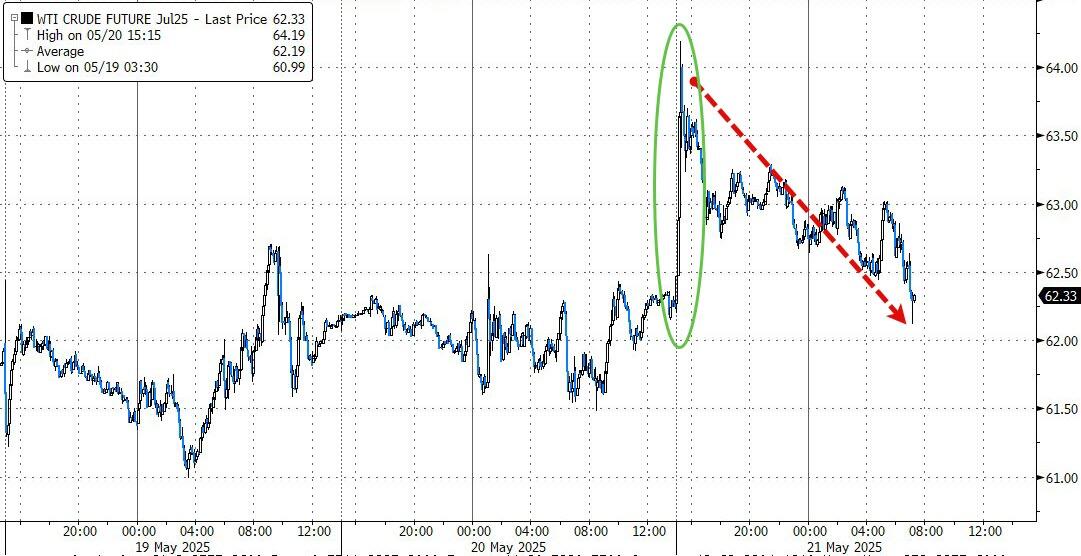

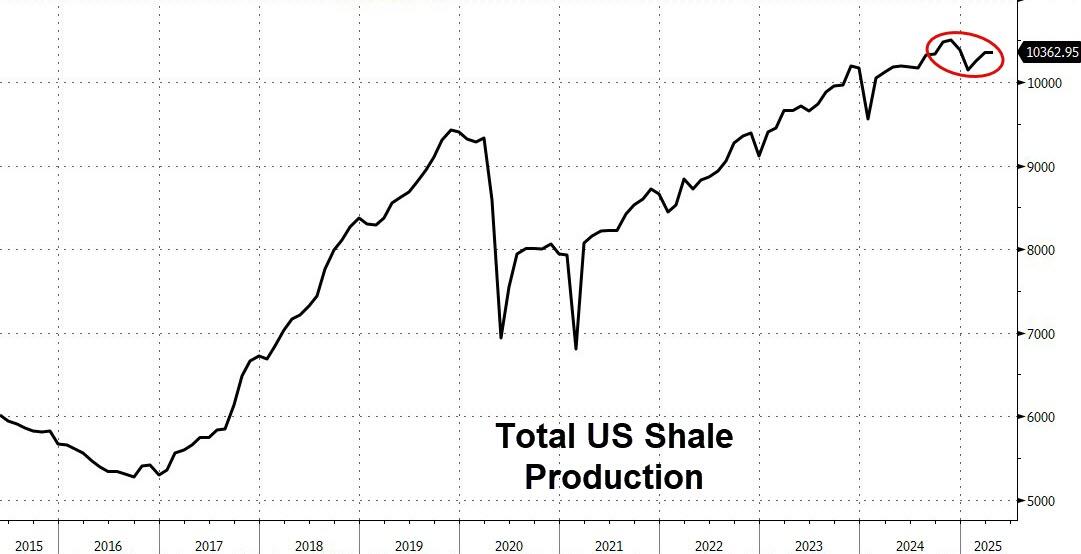

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 5057 CONTRACTS TO 448,000 WITH OUR STRONG GAIN IN PRICE OF $51.40 WITH RESPECT TO TUESDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT STRONG PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (425 ).

THE CME ANNOUNCED TUESDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES. TOTAL ISSUANCE FOR MAY REMAINS AT 9.591 TONNES OF GOLD AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES. THE BANK OF ENGLAND MUST BE GETTING QUITE ANTSY OF GETTING ITS GOLD BACK.

IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST FOUR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK

DETAILS ON MAY COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 5482 CONTRACTS WITH OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON MONDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF APRIL AND ONTO MAY, CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS SMALL AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 982 T.A.S.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY AS YOU WILL SEE BELOW ANOTHER HUMONGOUS QUEUE JUMP OCCURRED ON MAY’S DELIVERY CYCLE (FRIDAY/MAY 16) AT 9.978TONNES, THIS MONTH WE HAVE RECORDED THE HIGHEST EVER QUEUE JUMP RECORDED IN COMEX GOLD HISTORY AT 9.978 TONNES!!! TODAY’S QUEUE JUMP IS A HUGE .6780 TONNES.

THE TONNAGE STANDING FOR GOLD FOR MAY IS NOW 83.805 TONNES (WHICH INCLUDES TODAY’S STRONG QUEUE JUMP OF .9415 TONNES AND TO WHICH WE ADD OUR TOTAL EX FOR RISK: 9.591 TONNES EX FOR RISK!)//

NEW TOTAL TONNES STANDING: 83.805 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 222 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 425 EFP CONTRACT WAS ISSUED: : /JUNE 425 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 425 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

WE HAD :

- HUGE LIQUIDATION OF OUR T.A.S. SPREADERS

- ZERO NET SPEC LIQUIDATION DESPITE OUR LOSS IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A SMALL SIZED, 982 CONTRACTS.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL AND MAY

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE

FINAL STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (209.573 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 5 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY:

INITIAL STANDING AT 28.945 INITAL GOLD TONNES STANDING FIRST DAY NOTICE PLUS 6.4634 TONNES QUEUE JUMP MAY 7 (A RECORD) + ANOTHER HUGE QUEUE JUMP MAY 9 OF 0.534 TONNES + MAY 12 AT .5132 TONNES _ MAY 13; QUEUE JUMP OF 2.444 TONNES AND THEN MAY 14 RECORD 6.8800 TONNES QUEUE JUMP AND THEN (MAY 15) RECORD OF 9.978 TONNES AND THEN FRIDAY’S QUEUE JUMP OF 108,900 OZ/3.387 TONNES (MAY 16) MONDAY’S QUEUE JUMP OF 0.5847 + YESTERDAY’S QUEUE JUMP OF .6780 TONNES + TODAY’S QUEUE JUMP OF .9415 = +EXCHANGE FOR RISK//9.591 TONNES = 83.805 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 52 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 209.953 TONNES (INCLUDES 8.3571 TONNES EX FOR RISK/AND ALL MONTHLY QUEUE JUMPING)

MAY: STANDING NOW 74.214 TONNES (INCLUDES ALL QUEUE JUMPING FOR THE MONTH) + 9.591 TONNES EX FOR RISK EQUALS 83.805 TONNES!!

COMEX GOLD TRADING/MAY CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $51.40/ /)AND THEY WERE A UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION TUESDAY AS THEY ARE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE THE MAGIC $3,400 BARRIER AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING

WEDNESDAY MORNING/TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /MAY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE IS WHAT HAPPENED LAST MONTH; FINAL GOLD STANDING FOR APRIL:

APRIL: 201.573 TONNES +(8.3571 EX FOR RISK// FOR APRIL DELIVERY MONTH =209.953 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS MAY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// MAY COMEX CONTRACT

WE HAVE GAINED A FAIR SIZED TOTAL OF 17.05 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY FIRST RECORDED AT 28.945 TONNES ON FIRST DAY NOTICE/APRIL 30. WE HAD A STRONG 304 CONTRACT QUEUE JUMP WEDNESDAY, FOR 30,400 OZ OR 0.9415 TONNES. THIS QUEUE JUMP IS CENTRAL BANKS JUMPING AHEAD OF US SIMPLE MORTALS DEMANDING GOLD FOR THEIR RESERVES. THUS NEW STANDING ADVANCES TO 74.214 TONNES OF GOLD. TO WHICH WE ADD (MAY 13 MAY 15.MAY 19) EXCHANGE FOR RISK ISSUANCE FOR 9.591 TONNES//NEW TOTAL GOLD STANDING FOR MAY INCREASES TO 83.805 TONNES

THUS MAY STANDING FOR GOLD SO FAR: 83.805 TONNES

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $51.40

WE HAD A SMALL 214 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 5402 CONTRACTS OR 540200 0Z (17.05 TONNES)

confirmed volume TUESDAY 261m793. contracts: fair volume////

//speculators have left the gold arena

END

MAY

// THE MAY 2025 GOLD CONTRACT

MAY 19

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | . 3 ENTRIES i) Out of Brinks 32,954.700 oz (1025 kilobars) ii) Out of JPMorgan enhanced out of London 161,223.600 oz or 403 London good delivery bars iii) Stonex: 2101.440 oz total weight withdrawn: 196,279.400 oz or 6.105 tonnes |

| Deposit to the Dealer Inventory in oz | 1 ENTRIES i) Into ASAHI dealer: 32,118.849 oz (999 kilobars) in tonnes: .999 tonnes |

| Deposits to the Customer Inventory, in oz | 3 ENTRIES i) into HSBC 120,309.042 oz (3742 kilobars) ii) Into Malca: 4340.385oz (135 kilobars) iii) Into Stonex: 4018.875 ( 125 kilobars) total 130,769.742 oz 4,002kilobars or 4.002 tonnes of gold total weight dealer and customer: 5.0 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 269 notice(s) 26900 OZ 0.8367 TONNES |

| No of oz to be served (notices) | 210 contracts 21,000 OZ 0.653 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,650 notices 2,365,000 oz 73.425TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 1 entry

i) Into ASAHI dealer: 32,118.849 oz (999 kilobars)

in tonnes: .999 tonnes

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 3 customer entries

3 ENTRIES

i) into HSBC 120,309.042 oz

(3742 kilobars)

ii) Into Malca: 4340.385oz (135 kilobars)

iii) Into Stonex: 4018.875 ( 125 kilobars)

total 130,769.742 oz 4,002kilobars

or 4.002 tonnes of gold

total weight dealer and customer: 5.0 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 3

3 ENTRIES

i) Out of Brinks 32,954.700 oz

(1025 kilobars)

ii) Out of JPMorgan enhanced out of London

161,223.600 oz or 403 London good delivery bars

iii) Stonex: 2101.440 oz

total weight withdrawn: 196,279.400 oz

or 6.105 tonnes

adjustments: 1//customer to dealer

a) JPMorgan: 675.171 oz (21 kilobars)

AMOUNT OF GOLD STANDING FOR MAY

THE FRONT MONTH OF MAY STANDS AT 479 CONTRACTS FOR A GAIN OF 57 CONTRACTS. WE HAD 247 CONTRACTS SERVED ON TUESDAY SO WE GAINED 304 CONTRACTS AND THUS WE WITNESS A STRONG 30,400 OZ QUEUE JUMP FOR 0.9455 TONNES. THIS FOLLOWS LAST WEEK’S (MAY 15) RECORD BREAKING 9.987 TONNES. FOR THE PAST 7 DAYS WE HAVE RECORDED 24.8212 TONNES OF QUEUE JUMPS. ALL OF THIS IS PHYSICAL GOLD AND ALL GOING TO CENTRAL BANKS. LONDON HAS RECORDED OVER 30 TONNES OF GOLD LEAVING ITS SHORES.

JUNE LOST ONLY 4158 CONTRACTS TO 176,844 JUNE BECOMES OUR NEW FRONT MONTH AND THIS MONTH WILL BE A WHOPPER OF A DELIVERY MONTH. THE FRBNY IS QUITE NERVOUS LOOKING AT JUNE OI.WE HAVE 7 MORE TRADING DAYS BEFORE OUR BIG FIRST DAY NOTICE FRIDAY MAY 30.

JULY GAINED 150 CONTRACTS TO STAND AT 4837

We had 269 contracts filed for today representing 26,900 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 269 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 82 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY /2025. contract month, we take the total number of notices filed so far for the month (23,650 X 100 oz ) to which we add the difference between the open interest for the front month of MAY (479 CONTRACTS) minus the number of notices served upon today (269 x 100 oz per contract) equals 2,386,000 OZ OR 74.214 TONNES to which we add 9.591 tonnes of gold issued under exchange for risk//new totals 83.805 tonnes

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (23,650 x 100 oz +we add the difference for front month of MAY (479 OI} minus the number of notices served upon today (269 x 100 oz) which equals 2,386,000 OZ OR 74.214 TONNES + 9.591 tonnes = 83.805 tonnes

TOTAL COMEX GOLD STANDING FOR MAY.: 83.805 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,216,370.991 oz 68.938 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,951,535.855 oz

TOTAL REGISTERED GOLD 21,325,656.475: or 663.317 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 17,625,879.350 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,070,616oz (REG GOLD- PLEDGED GOLD)= 593.176tonnes //

SILVER/COMEX

// THE MAY 2025 SILVER CONTRACT//INITIAL

MAY 19

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 withdrawal entries i) Out of Brinks 469,508.960 oz ii) Out of Delaware 989.986 oz iii) Out of Loomis 600,962.720 oz total weight withdrawal 1,076,466.666 oz |

| Deposits to the Dealer Inventory | 0 |

| Deposits to the Customer Inventory | 1 DEPOSIT i) Into CNT 600,566.720 oz total deposit: 500,566.720 oz |

| No of oz served today (contracts) | 73 CONTRACT(S) (365,000 OZ |

| No of oz to be served (notices) | 348 contract (1.740 MILLION oz) |

| Total monthly oz silver served (contracts) | 14,685 Contracts (73.425 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

0 deposits into dealer accounts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1 deposit entries//customer side/eligible

1 DEPOSIT

i) Into CNT 600,566.720 oz

total deposit: 500,566.720 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3 withdrawal entries

i) Out of Brinks 469,508.960 oz

ii) Out of Delaware 989.986 oz

iii) Out of Loomis 600,962.720 oz

total weight withdrawal 1,076,466.666 oz

ADJUSTMENTs 0

JPMorgan has a total silver weight: 217.184million oz/500.598 oz million or 43.26%

TOTAL REGISTERED SILVER: 168.457 MILLION OZ//.TOTAL REG + ELIGIBLE. 500.598Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2025 OI: 421 OPEN INTEREST CONTRACTS FOR A LOSS OF 8 CONTRACTS. WE HAD 8 NOTICES FILED ON TUESDAY SO WE GAINED 0 CONTRACTS WHICH UNDERWENT A QUEUE JUMP OF 0 OZ WHERE THESE BOYS HAVE DECIDED TO TAKE DELIVERY OVER HERE. I MUST REPORT WE HAD 0 EXCHANGE FOR RISK ISSUANCE FOR TODAY. THUS THE NEW TOTAL REMAINS AT TWO ISSUANCES OF EXCHANGE FOR RISK IS 12.93 MILLION OZ.

JUNE SAW A LOSS OF 228 CONTRACTS DOWN TO 2669 CONTRACTS. JUNE OI REFUSES TO LIQUIDATE

WE WILL PROBABLY HAVE OVER 14 MILLION OZ STAND FOR JUNE/AN OFF MONTH

AS IT IS NOW THE FRONT MONTH. WE HAVE 6 MORE TRADING DAYS BEFORE FIRST DAY NOTICE, FRIDAY MAY 30.

JULY GAINED 3687 CONTRACTS UP TO 108,510

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 73 or 0.365 MILLION oz

CONFIRMED volume; ON TUESDAY 54,224 pitiful//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 14,685 X5,000 oz = 73.425 MILLION oz

to which we add the difference between the open interest for the front month of MAY (421) AND the number of notices served upon today (73 )x (5000 oz)

Thus the standings for silver for the MAY 2025 contract month: (14,685) Notices served so far) x 5000 oz + OI for the front month of MAY(421) minus number of notices served upon today (73)x 5000 oz equals silver standing for the MAY contract month equating to 75.165 MILLION OZ . THEN WE MUST ADD OUR NEW 12.93 TONNES OF EXCHANGE FOR RISK. NEW TOTAL STANDING FOR SILVER: 88.095 MILLION OZ

New total standing: 88.095 million oz which is huge for this active delivery month of MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 168.457million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

MAY 21 WITH GOLD UP $28.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.60 TONNES

MAY 20 WITH GOLD UP $51.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.30 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.03 TONNES

MAY 19 WITH GOLD UP $46.65 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.89 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 918.73 TONNES

MAY 16 WITH GOLD DOWN $38.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 927.62 TONNES

MAY 15 WITH GOLD UP $38.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.53 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 931.92 TONNES

MAY 14 WITH GOLD DOWN $40.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 936.51 TONNES

MAY 13 WITH GOLD UP $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 12 WITH GOLD DOWN $115.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 9 WITH GOLD UP $37.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 939.68 TONNES

MAY 8 WITH GOLD DOWN $82.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.23 TONNES OF GOLD WITHDRAWN FROM THE GLD/ ///INVENTORY RESTS AT 937.67 TONNES

MAY 7 WITH GOLD DOWN $30.30 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 937.96 TONNES

MAY 6 WITH GOLD UP $101.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 937.96 TONNES

MAY 5 WITH GOLD UP $77.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.13 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.28 TONNES

MAY 2 WITH GOLD UP $ 18.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 945.41 TONNES

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

APRIL29 WITH GOLD DOWN $13.45 TODAY// NO CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL28 WITH GOLD UP $50.20 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL25 WITH GOLD DOWN $49.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVEV WITHDRAWAL OF 3.911 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 948.56 TONNES

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

GLD INVENTORY: 921.60 TONNES, TONIGHTS TOTAL

SILVER

MAY 21 WITH SILVER UP $0.35/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.091 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 451.875 MILLION OZ

MAY 20 WITH SILVER UP $0.65/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.41 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 449.784 MILLION OZ

MAY 19 WITH SILVER UP $0.17/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHTDRAWAL OF 1.819 MILLION OZ OUT OF THE SLV// ////: //INVENTORY AT SLV RESTS AT 447.193 MILLION OZ

MAY 16 WITH SILVER DOWN $0.24/NO CHANGES IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 15 WITH SILVER UP 0.04/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.909 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 14 WITH SILVER DOWN $0.39/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.682 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.102 MILLION OZ

MAY 13 WITH SILVER UP $0.44/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 12 WITH SILVER DOWN $0.30/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 9 WITH SILVER UP $0.31/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 8 WITH SILVER DOWN $0.16/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 7 WITH SILVER DOWN $0.54/NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 6 WITH SILVER UP $0.92 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A HUG WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 5 WITH SILVER UP $0.08 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF 0.117 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.602 MILLION OZ

MAY 2 WITH SILVER DOWN $0.19 /MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 4.545 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.424 MILLION OZ

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

APRIL29 WITH SILVER UP $0.30 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.229 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 451.925 MILLION OZ

APRIL28 WITH SILVER DOWN $0.03 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.136 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.696 MILLION OZ

APRIL25 WITH SILVER DOWN $0.44 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 3.639 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.832 MILLION OZ

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

CLOSING INVENTORY 441.875 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

Schiff: Strong Dollar Or Exports? Pick One…

Wednesday, May 21, 2025 – 03:45 PM

Last week, Peter joined Glenn Diesen for an interview on the post-trade deal economy. Peter takes on the myths surrounding Trump’s trade war with China, the real impact of tariffs on Americans, and where he sees the dollar heading as the world’s reserve currency. He explains why the perceived victories of protectionist trade policy are little more than marketing stunts, and warns about the risks of continued US borrowing and a potential dollar crisis.

Peter opens with his signature candor, cutting through the narratives around Trump’s approach to China and the broader trade war. He stresses that Americans have been misled about the true causes of trade deficits and the effectiveness of tariffs:

Well, first of all, Trump declared war and then surrendered and called it a victory. You know, the victory is that he saved us from ourselves, although it’s not a complete save. I don’t think we’re out of the woods. But, you know, Trump never had the cards to win the war in the first place. In the first place, I think he assessed the situation backwards. The whole trade war was misguided anyway, because the trade deficits are not the result of foreigners cheating us or ripping us off or bad trade deals.

He explains how the president’s business acumen translated into a branding exercise in the White House, rather than substantive reform:

I know he’s a great promoter. He’s a great marketer. That I’ll give him. I mean, he won the White House twice, right, so he sold the country on himself as the product. So he did a great job. And, you know, he’s a showman. He had The Apprentice, he had his hotels, his golf courses, you know, some of his other businesses. It’s all about branding, right? He brands the Trump brand. He puts the big Trump on everything, right?… I was curious – what are the lessons for China? Was anything achieved?

Dispelling a common misconception, Peter clearly lays out the economic reality of tariffs—contrary to claims made by several politicians, these taxes are paid by Americans, not by foreign exporters:

But again, the tariffs weren’t even on China. They were an inconvenience for Chinese companies. But the tariffs were on Americans. You know, the Chinese tariffs were on the Chinese. I mean, Trump can only tax Americans, and tariffs are an indirect tax that consumers pay when they buy products that are subject to the tariff. The actual tariff is paid by the importer, which is an American company. Now, if you import directly, right, if you decide to go on some Chinese site and order a product and they mail it directly to you, then, you know, when the package comes through customs, they add the tariff and you’ve got to pay it. The Chinese don’t pay it. The tariffs are paid by Americans. So it’s always been a lie. I pointed that out during the campaign.

When it comes to reducing trade deficits, Peter argues that policy makers want to have their cake and eat it too— pushing for a strong dollar and lower trade deficits at the same time, despite the fact that these aims are fundamentally at odds:

They want both. But of course, you can’t have both. The reason our trade deficits are so big is because the dollar is so overvalued. And so the only real way to make a big dent in the trade deficit is to have a much weaker dollar. I mean, that’ll do it. That’ll just make imports so expensive that Americans won’t be able to afford them, and so the imports will come down. And it will make our stuff a lot cheaper, whatever we got, and so we’ll export more of it. So a weaker dollar would do the trick, but of course the weaker dollar means much higher inflation in the US, which is why they don’t want a weak dollar.

Wrapping up, Peter warns that the current trajectory is unsustainable. With continued deficits, reliance on foreign creditors, and a dollar whose status as the world’s reserve currency is under threat, a reckoning is likely around the corner:

No, I think we’re going to have a dollar crisis and a sovereign debt crisis. I mean, that’s just how it’s going to end. We’re going to keep on living beyond our means until we can’t do it anymore. We’re going to keep on borrowing until the lenders stop lending to us. And I think we’re already on that path. The question is, how long does it take to really completely de-dollarize, to kind of sever this lifeline that we have? I don’t know. But, I mean, the process has started. And at some point, the pace is going to accelerate.

For more of Peter’s analysis on the US-China tariff deal, check out Peter’s latest podcast!

MATHEW PIEPENBERG

2.ALASDAIR MACLEOD

3. CHRIS POWELL AND GATA DISPATCHES

4/On LFTV, Andrew Maguire LIVE FROM THE VAULT 223

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//CATTLE

6 CRYPTOCURRENCY NEWS

ASIAN MARKETS THIS MORNING:

SHANGHAI CLOSED UP 10.77 PTS OR 0.32%

//Hang Seng CLOSED UP 152.15 PTS OR 0.64%

// Nikkei CLOSED DOWN 37.69 PTS OR 0.10% //Australia’s all ordinaries CLOSED UP 0.61%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.2183 OFFSHORE CLOSED UP AT 7.2060/ Oil UP TO 62.84 dollars per barrel for WTI and BRENT UP TO 66.32 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.2183 AND STRONGER//OFF SHORE YUAN TRADING UP 7.2060 AGAINST US DOLLAR/ AND THUS STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2183 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.2060 (CCP MANIPULATED)

SHANGHAI CLOSED UP 10.77 PTS OR 0.32%

HANG SENG CLOSED UP 348.76 PTS OR 1.49%

2. Nikkei closed DOWN 37.60 PTS OR 0.10%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 99.59// EURO RISES TO 1.1319 UP 31 BASIS PTS

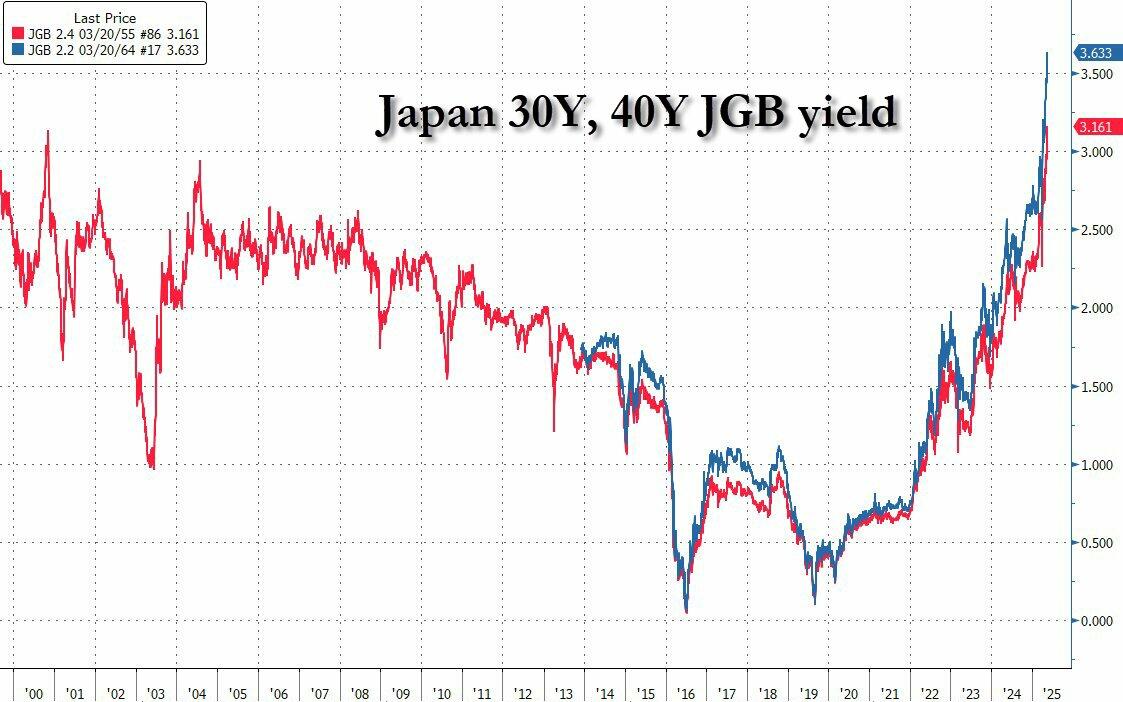

3b Japan 10 YR bond yield: RISES TO. +1.517//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 144.10…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6570/Italian 10 Yr bond yield UP to 3.676 SPAIN 10 YR BOND YIELD UP TO 3.283%

3i Greek 10 year bond yield UP TO 3.312

3j Gold at $3309.40. Silver at: 33.15 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 6 /100 roubles/dollar; ROUBLE AT 80.25

3m oil into the 62 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 144.10// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.517% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8254 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9345 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.537 UP 6 BASIS PTS…

USA 30 YR BOND YIELD: 5.027 UP 6 BASIS PTS/

USA 2 YR BOND YIELD: 3.994 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.84

10 YR UK BOND YIELD: 4.8235 UP 12 PTS

10 YR CANADA BOND YIELD: 3.296 UP 12 BASIS PTS

5 YR CANADA BOND YIELD: 2.886 UP 11 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

Futures Slide As 30Y Yield Rises Above 5%, Oil Jumps On Iran War Fears

Wednesday, May 21, 2025 – 08:27 AM

US equity futures and global markets are weaker with both tech and small caps underperforming as yields rise (10Y TSY at 4.53% last) and the curve bear steepens. As of 8:00am ET, S&P futures are down 0.5% with sentiment hit by a CNN report that Israel may be preparing to strike Iranian nuclear facilities. That sent oil higher, while haven assets outperformed; Nasdaq futures also drop 0.6%, with Mag7 names mostly lower and Semis/Cyclicals underperforming. In Europe major markets are mostly lower with the UK leading and France lagging. UK inflation his a 15-month high. Treasury yields ticked above key psychological levels, with the 30-year above 5%. The dollar lost ground against all major currencies pushing the DXY index back below 100 as the yen continues its relentless ascent while Japanese long bonds crater. Commodities are higher this morning, benefiting from the lower dollar and led higher by energy and precious metals with the former higher on elevated geopolitical risk. Oil climbed about 0.7% on a report that Israel could be gearing up for a possible strike on Iran’s nuclear facilities. It is another light macro data day with no macro news but with multiple Fed speakers. Earnings from big retailers will be in focus for clues on the impact of tariffs.

In premarket trading, Mag 7 stocks are mixed (Alphabet +0.5%, Tesla +0.5%, Apple -0.4%, Microsoft -0.5%, Nvidia -0.7%, Amazon -0.8%, Meta -0.6%). Canada Goose rose 9% after the coat manufacturer posted fourth-quarter revenue that beat estimates. Lowe’s (LOW) climbs 2% after comparable sales beat expectations during the latest quarter as shoppers maintained home spending despite weakening consumer sentiment and economic turbulence.

- Moderna (MRNA) slips 1.3% after the biotechnology company voluntarily withdrew its pending biologics license application for its flu, Covid combination vaccine for adults 50 years and older.

- Target (TGT) slumped 4% after the beleaguered company cut its FY sales outlook, and now sees full year sales declining by single digits after previously seeing growth

- NU Holdings (NU) falls 2.6% after saying said Chief Operating Officer Youssef Lahrech is stepping down, adding to a string of management changes in the upper ranks of Latin America’s standout financial technology firm.

- Palo Alto Networks (PANW) slips 3% after the cybersecurity provider posted quarterly results and gave an outlook. Analysts note subscription and support revenue slightly missed expectations and JPMorgan reduced its price target.

- Take-Two Interactive (TTWO) declines 4% after the video-game publisher announced plans to sell $1 billion of new stock to investors. The offering range is $225 to $232 per share, according to people familiar with the matter.

- Toll Brothers (TOL) gains 3% after the company reaffirmed its expectations for home sales in its full fiscal year, citing resilience among its affluent buyers.

- UnitedHealth (UNH) tumbles 5% after the Guardian reported that the health insurer secretly paid nursing homes to reduce hospital transfers for ailing residents.

- VF Corp. (VFC) falls 12% after the owner of apparel and footwear brands forecast a wider-than-expected adjusted operating loss from continuing operations for the first quarter.

Target, Lowe’s, Marshalls-owner TJX and Timberland maker VF Corp are all set to report this morning. Any comments on post-tariff pricing adjustments will be key after Walmart warned of price hikes last month, with Trump retorting that the retailer should “eat the tariffs.”

Overnight, republicans said they reached an agreement on state and local tax deductions for President Donald Trump’s economic bill after negotiating through the night. While investors have rushed back into stocks on hopes that the US is easing off its tariff threats, there are questions about whether gains can be sustained as concerns about fiscal deficits and mounting debt drive bond yields higher.

“There’s a lot of optimism that has been discounted in markets and it seems that many investors believe that the trade war is over,” said Frederique Carrier, head of investment strategy for RBC Wealth Management in the British Isles and Asia. “However, the underlying issues which have been at the root of tensions for decades have not been tackled.”

Equity trading volumes were light across the board. The UK and European Union extended the bidding window for debt auctions on Wednesday in response to Bloomberg LP technical issues. Globally, the yield-curve for government debt steepened across most markets as worries mount around swelling debt and deficits. The rate for 10-year US Treasuries advanced four basis points to 4.53%, while the yield for gilts with a similar tenure rose six basis points to 4.76%.

“The direction of travel is obviously higher,” Lindsay Rosner, head of multi-sector fixed income investing at Goldman Sachs Asset Management, told Bloomberg TV. “At the core of it, fiscal is in question, and it’s not just a US problem, it’s a global problem.”

Meanwhile, Morgan Stanley raised its call on US stocks and Treasuries on expectations that interest-rate cuts will support bonds and boost company earnings. The S&P 500 Index will reach 6,500 by the second quarter of 2026, they wrote. They also see the dollar continuing to weaken as the US’s economic growth premium relative to peers fades.

“The US dollar has of course lost its luster as the undisputed safe reserve asset,” said Richard Franulovich, head of FX strategy at Westpac Banking Corp.

In Europe the Stoxx 600 is on course to snap a four-day win streak as it falls 0.6%. Retail, auto, and travel shares are leading declines while utilities outperform as the only sector up in Europe. major markets are mostly lower with the UK leading and France lagging. UK inflation his a 15-month high. Here are the biggest European movers:

- Genfit shares climb as much as 7.6% after the French biotech company said it will receive a €26.5 million milestone payment from Ipsen.

- SSE rises as much as 1.9% after the UK utility company cut its five-year spending plan by £3 billion as projects slow amid planning delays, while also releasing full-year results.

- Electrolux Professional rallies as much as 8.5% to its highest level since March 26 after Handelsbanken upgraded its view on the Swedish professional appliances maker to buy from hold, projecting the company will gain market share in the US.

- Infineon shares rise as much as 1.8% after the chipmaker said it’s collaborating with Nvidia on a new power delivery infrastructure for AI data centers.

- Orion gains as much as 4.9%, hitting a record high after the Finnish drug company says its partner MSD has expanded the development program for opevesostat to now include women’s cancers.