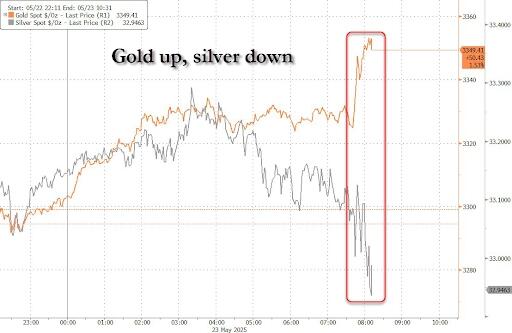

MAY 23/GOLD CLOSED UP A HUGE $69.70 TODAY TO $3365.50// WITH SILVER UP 38 CENTS TO $33.45//PLATINUM UP ANOTHER $18.00 TO $1098.40 WHILE PALLADIUM WENT THE OTHER WAY DOWN $13.90 TO $1003.70//GOLD COMMENTARY TONIGHT FROM ALASDAIR MACLEOD//LIVE FROM THE VAULT PODCAST WITH ANDREW MAGUIRE TALKING TO DR STEPHEN LEEB//COMMODITY COMMENTARY TONIGHT ON STEEL//BIG STORY TONIGHT: TRUMP THREATENS APPLE AND THE EU WITH TARIFFS//UK WELCOMES FAR LEFT ACTIVIST INTO THE COUNTRY//ISRAEL VS HOUTHIS, HAMAS//WEST BANK UPDATES//IRAN VS USA AND ISRAEL UPDATES//VACCINE INJURY REPORT//MARK CRISPIN MILLER/DR PAUL ALEXANDER NEWS ADDICTS/EVOL NEWS//TERROR SUSPECT TODAY CHARGED IN THE MURDER OF TWO ISRAELI STAFF MEMBERS AT WASHINGTON JEWISH MUSEUM//TRUMP BLOCKS ENROLLMENT OF FOREIGN STUDENTS ENTERING HARVARD//MORE SWAMP STORIES FOR YOU TONIGHT//

190 H BMO CAPITAL MARKETS 326 323 C HSBC 61 363 H WELLS FARGO SECURITI 196 624 H BOFA SECURITIES 389 661 C JP MORGAN SECURITIES 456 905 C ADM 2

TOTAL: 715 715 MON

MONTH TO DATE: 23,650

JPMORGAN STOPPED 217/899

MAY

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024: 715 CONTRACTs NOTICES FOR 71,500 OZ or 2.223 TONNES

total notices so far: 25,264 contracts for 2,526,400 OR 78.581 tonnes)

FOR MAY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES:2 NOTICE(S) FILED FOR 10,000 OZ/

total number of notices filed so far this month : 14,798 CONTRACTS (NOTICES) for 73.990 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $67.70 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.01 TONNES OF GOLD OUT OF THE GLD//

INVENTORY RESTS AT 923.89 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.38 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: //A DEPOSIT OF 2.5 MILLION OZ INTO THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 454.375 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 923 CONTRACTS TO 144,831 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUMONGOUS SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS OF $0.27 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. WE HAD A STRONG SIZED LOSS OF 633 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A 290 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD SOME LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING WITH RESPECT TO THURSDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON THURSDAY WITH SILVER’S LOSS IN PRICE AS THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH ANOTHER FAIR T.A.S. ISSUANCE OF 363 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A 290 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 363 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FRIDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A STRONG SIZED 633 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.27.

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS MUST NOW BE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT/FRIDAY MORNING: A FAIR 363 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.27) AND WERE SUCCESSFUL IN KNOCKING OFF SOME NET SILVER LONGS FROM THEIR PERCH

WE HAD A 290 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 67.830 MILLION OZ TO WHICH WE ADD OUR 25,000 CONTRACT E.F.P. TRANSER OF 25,000 OZ AND THEN WE MUST ADD THOSE CRAZY CONTRACT EXCHANGE FOR RISK FOR 12.93 MILLION OZ:

THUS:

INITIAL STANDING FOR MAY: 76.190 MILLION OZ WHICH INCLUDES TODAY’S 25,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ (EX FOR RISK) EQUALS 89.120 MILLION OZ./

WE HAD:

/ HUGE COMEX OI LOSS+// A 290 SIZED EFP ISSUANCE (/ VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 363 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A SMALL 208 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 17 DAYS, total 4424 contracts: OR 22.120 MILLION OZ (260 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 22.120 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 22.12 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 923 CONTRACTS WITH OUR LOSS IN PRICE OF $0.27 IN SILVER PRICING AT THE COMEX// THURSDAY.,. . THE CME NOTIFIED US THAT WE HAD A 290 CONTRACT EFP ISSUANCE CONTRACTS: 290 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND NOW MAY:

NEW STANDING FOR MAY REDUCES TO: 76.190 MILLION OZ. (INCLUDES 25,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING LOWERS TO 89.120 MILLION OZ

THE NEW TAS ISSUANCE THURSDAY NIGHT (363 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TODAY’S TRADING (FRIDAY TRADING) AND BEYOND.

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 776 OI CONTRACTS TO 452,564 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A MONSTER 6789 CONTRACTS //.

WE HAD A SMALL SIZED DECREASE IN COMEX OI (776 CONTRACTS) . THIS OCCURRED DESPITE OUR LOSS OF $15.50 IN PRICE// THURSDAY///.

FOR THE MONTH OF APRIL WE HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES/) TO WHICH WE ADDED + 8.3571 TONNES EX FOR RISK = 209.953 TONNES STANDING!

FINAL STANDING FOR APRIL; 201.443 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

AND NOW MAY: SUMMARY OF EXCHANGE FOR RISKS ADDED

INITIAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.245 TONNES. THUS STANDING FOR MAY INCREASES TO 89.836 TONNES OF GOLD

/ ALL OF THIS HAPPENED WITH OUR $15.50 LOSS IN PRICE WITH RESPECT TO THURSDAY’S COMEX ///. WE HAD A FAIR SIZED GAIN OF 1583 OI CONTRACTS (4.923 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE DURING THE FIRST THREE WEEKS OF MAY, AND THROUGHOUT EACH AND EVERY DAY MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MAY CONTRACT MONTH….. A MONSTROUS 89.836 TONNES DESPITE IT BEING AN OFF MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2359 CONTRACT:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 452,564/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 144,831 CONTRACTS!!

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1583 CONTRACTS WITH 776 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2359 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1583 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 950 CONTRACTS ISSUED.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS 2359 CONTRACT) ACCOMPANYING THE FAIR SIZED DECREASE IN COMEX OI OF 776 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1583 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING FOR GOLD FOR MAY AT 80.245 TONNES ( WHICH WHICH INCLUDES TODAY’S 3.259 TONNES QUEUE JUMP AND THEN WE ADD OUR MAY 13 , 15TH AND 19TH ISSUANCE OF 9.589 TONNES EX FOR RISK//NEW TOTAL STANDING FOR GOLD INCREASES TO: 89.836 TONNES

NEW STANDING FOR GOLD, MAY CONTRACT ADVANCES TO: 89.836 TONNES OF GOLD.(INCLUDES QUEUE JUMPING AND EX FOR RISK ISSUANCE)

.

/ 3) ZERO T.A.S. LIQUIDATION , AS WE HAD 1)A $15.50 COMEX PRICE LOSS.. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED DESPITE THAT LOSS IN PRICE AS WE HAD OUR STRONG GAIN OF 8113 CONTRACTS ON OUR TWO EXCHANGES// /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY.

4) SMALL SIZED COMEX OI LOSS// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (23598 CONTRACTS)/// FAIR T.A.S. ISSUANCE: 950 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAY INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 23,414 CONTRACTS OR 2,341,400 OZ OR 72.827 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 1377 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN17 TRADING DAY(S) IN TONNES 72.827 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 72.827 TONNES DIVIDED BY 3550 x 100% TONNES = 2.056% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 72.827 TONNES OF GOLD EFP ISSUANCE

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUMONGOUS SIZED 923 CONTRACTS OI TO 144,831 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 290 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 290 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 290 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 923 CONTRACTS AND ADD TO THE 290 E.FP. ISSUED

WE OBTAIN A STRONG SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 633 CONTRACTS WITH THE LOSS IN PRICE OF $0.27 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 3.165 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 31.82 PTS OR 0.94%

//Hang Seng CLOSED UP 56.44 PTS OR 0.24%

// Nikkei CLOSED UP 174.60 PTS OR 0.47% //Australia’s all ordinaries CLOSED UP 0.18%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1906 OFFSHORE CLOSED UP AT 7.1872/ Oil DOWN TO 60.70 dollars per barrel for WTI and BRENT DOWN TO 63.99 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1906 AND STRONGER//OFF SHORE YUAN TRADING UP 7.1872 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED776 CONTRACTS TO 452,564 WITH OUR LOSS IN PRICE OF $15.50 WITH RESPECT TO THURSDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT STRONG PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2359 ).

THE CME ANNOUNCED THURSDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES. TOTAL ISSUANCE FOR MAY REMAINS AT 9.591 TONNES OF GOLD AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES. THE BANK OF ENGLAND MUST BE GETTING QUITE ANTSY OF GETTING ITS GOLD BACK.

IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST FOUR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK

DETAILS ON MAY COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1383 CONTRACTS DESPITE OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF APRIL AND ONTO MAY, CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS FAIR AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 950 T.A.S.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY AS YOU WILL SEE BELOW ANOTHER HUMONGOUS QUEUE JUMP OCCURRED ON MAY’S DELIVERY CYCLE (FRIDAY/MAY 16) AT 9.978TONNES, THIS MONTH WE HAVE RECORDED THE HIGHEST EVER QUEUE JUMP RECORDED IN COMEX GOLD HISTORY AT 9.978 TONNES!!! TODAY’S QUEUE JUMP IS A HUGE 3.259 TONNES.

THE TONNAGE STANDING FOR GOLD FOR MAY IS NOW 80.245 TONNES (WHICH INCLUDES TODAY’S STRONG QUEUE JUMP OF 3.259 TONNES AND TO WHICH WE ADD OUR TOTAL EX FOR RISK: 9.591 TONNES EX FOR RISK!)//

NEW TOTAL TONNES STANDING: 89.836 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 5+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 222 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2359 EFP CONTRACT WAS ISSUED: : /JUNE 2369 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2359 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

WE HAD :

ZERO LIQUIDATION OF OUR T.A.S. SPREADERS

ZERO NET SPEC LIQUIDATION WITH OUR HUGE GAIN IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY MORNING/THURSDAY NIGHT WAS A FAIR SIZED, 950 CONTRACTS.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL AND MAY

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE

FINAL STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (209.573 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 5 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY:

INITIAL STANDING AT 28.945 INITAL GOLD TONNES STANDING FIRST DAY NOTICE PLUS 6.4634 TONNES QUEUE JUMP MAY 7 (A RECORD) + ANOTHER HUGE QUEUE JUMP MAY 9 OF 0.534 TONNES + MAY 12 AT .5132 TONNES _ MAY 13; QUEUE JUMP OF 2.444 TONNES AND THEN MAY 14 RECORD 6.8800 TONNES QUEUE JUMP AND THEN (MAY 15) RECORD OF 9.978 TONNES AND THEN FRIDAY’S QUEUE JUMP OF 108,900 OZ/3.387 TONNES (MAY 16) MONDAY’S QUEUE JUMP OF 0.5847 + TUESDAY’S QUEUE JUMP OF .6780 TONNES + WEDNESDAY’S QUEUE JUMP OF .9415 AND THEN THURSDAY;S QUEUE JUMP OF 2.7402 TONNES AND FINALLY TODAY’S AT 3.259 TONNES: +EXCHANGE FOR RISK//9.591 TONNES = 89.836 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 209.953 TONNES (INCLUDES 8.3571 TONNES EX FOR RISK/AND ALL MONTHLY QUEUE JUMPING)

MAY: STANDING NOW 80.245 TONNES (INCLUDES ALL QUEUE JUMPING FOR THE MONTH) + 9.591 TONNES EX FOR RISK EQUALS 89.836 TONNES!!

COMEX GOLD TRADING/MAY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $15.50/ /) BUT THEY WERE A UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD SOME T.A.S. SPREADER LIQUIDATION THURSDAY AS THEY ARE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE THE MAGIC $3,400 BARRIER AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING

FRIDAY MORNING/THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /MAY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

HERE IS WHAT HAPPENED LAST MONTH; FINAL GOLD STANDING FOR APRIL:

APRIL: 201.573 TONNES +(8.3571 EX FOR RISK// FOR APRIL DELIVERY MONTH =209.953 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS MAY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// MAY COMEX CONTRACT

WE HAVE GAINED A STRONG SIZED TOTAL OF 26.040 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY FIRST RECORDED AT 28.945 TONNES ON FIRST DAY NOTICE/APRIL 30. WE HAD A STRONG 1048 CONTRACT QUEUE JUMP THURSDAY, FOR 104,800 OZ OR 3.259 TONNES. THIS QUEUE JUMP IS CENTRAL BANKS JUMPING AHEAD OF US SIMPLE MORTALS DEMANDING GOLD FOR THEIR RESERVES. THUS NEW STANDING ADVANCES TO 76.955 TONNES OF GOLD. TO WHICH WE ADD (MAY 13 MAY 15.MAY 19) EXCHANGE FOR RISK ISSUANCE FOR 9.591 TONNES//NEW TOTAL GOLD STANDING FOR MAY INCREASES TO 89.836 TONNES

THUS MAY STANDING FOR GOLD SO FAR: 89.836 TONNES

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $15.50

WE HAD A MONSTER 6789 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 1583 CONTRACTS OR 158300 0Z (4.923 TONNES)

Total monthly oz gold served (contracts) so far this month

25,264 notices 2,526,400 oz 78.581 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 0 customer entries

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 0

adjustments: 2//

a) Malca 36,459.224 oz (1134 kilobars)

b) Manfra: removal dealer Manfra 5,401.368 oz (or 168 kilobars)

AMOUNT OF GOLD STANDING FOR MAY

THE FRONT MONTH OF MAY STANDS AT 1250 CONTRACTS FOR A GAIN OF 159 CONTRACTS. WE HAD 889 CONTRACTS SERVED ON THURSDAY SO WE GAINED A HUGE 1048 CONTRACTS AND THUS WE WITNESS A HUGE 104,800 OZ QUEUE JUMP FOR 3.259 TONNES. THIS FOLLOWS LAST WEEK’S (MAY 15) RECORD BREAKING 9.987 TONNES. FOR THE PAST 9 DAYS WE HAVE RECORDED 30.8204 TONNES OF QUEUE JUMPS. ALL OF THIS IS PHYSICAL GOLD AND ALL GOING TO CENTRAL BANKS. LONDON HAS RECORDED OVER 30 TONNES OF GOLD LEAVING ITS SHORES THIS MONTH

JUNE LOST 17,081 CONTRACTS TO 143,847 JUNE BECOMES OUR NEW FRONT MONTH AND THIS MONTH WILL BE A MEGA WHOPPER OF A DELIVERY MONTH. THE FRBNY IS QUITE NERVOUS LOOKING AT JUNE OI.WE HAVE 4 MORE TRADING DAYS BEFORE OUR BIG FIRST DAY NOTICE FRIDAY MAY 30. (MONDAY IS A HOLIDAY/MEMORIAL DAY)

JULY GAINED 87 CONTRACTS TO STAND AT 5402

We had 715 contracts filed for today representing 71,500 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 715 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 456 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY /2025. contract month, we take the total number of notices filed so far for the month (25,264 X 100 oz ) to which we add the difference between the open interest for the front month of MAY (1250 CONTRACTS) minus the number of notices served upon today (715 x 100 oz per contract) equals 2,579,900 OZ OR 80.245 TONNES to which we add 9.591 tonnes of gold issued under exchange for risk//new totals 89.836 tonnes

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (25,264 x 100 oz +we add the difference for front month of MAY (1250 OI} minus the number of notices served upon today (715 x 100 oz) which equals 2,579,900 OZ OR 80.245 TONNES + 9.591 tonnes = 89.836 tonnes

TOTAL COMEX GOLD STANDING FOR MAY.: 89.836 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..

i) Out of HSBC 610,424.100 oz ii) Out of JPMorgan 1198,893.500 oz iii) Out of loomis 600,113.200 oz

total withdrawal: 2409.436.800 oz

ADJUSTMENTs 0

JPMorgan has a total silver weight: 214.825million oz/496.694 oz million or 43.14%

TOTAL REGISTERED SILVER: 168.457 MILLION OZ//.TOTAL REG + ELIGIBLE. 496.694Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2025 OI: 442 OPEN INTEREST CONTRACTS FOR A LOSS OF 116 CONTRACTS. WE HAD 111 NOTICES FILED ON THURSDAY SO WE LOST 5 CONTRACTS WHICH UNDERWENT AN EFP TRANSER TO LONDON OF 25,000 OZ WHERE THESE BOYS HAVE DECIDED TO TAKE DELIVERY OVER THERE. I MUST REPORT WE HAD 0 EXCHANGE FOR RISK ISSUANCE FOR TODAY. THUS THE NEW TOTAL REMAINS AT TWO ISSUANCES OF EXCHANGE FOR RISK IS 12.93 MILLION OZ.

JUNE SAW A LOSS OF 48 CONTRACTS DOWN TO 2558 CONTRACTS. JUNE OI REFUSES TO LIQUIDATE

WE WILL PROBABLY HAVE OVER 12 TO 13 MILLION OZ STAND FOR JUNE/AN OFF MONTH

AS IT IS NOW THE FRONT MONTH. WE HAVE 4 MORE TRADING DAYS BEFORE FIRST DAY NOTICE, FRIDAY MAY 30.

JULY LOST 1444 CONTRACTS DOWN TO 110,427

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 or 10,000 oz

CONFIRMED volume; ON THURSDAY 71,300 FAIR//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 14,798 X5,000 oz = 73.990 MILLION oz

to which we add the difference between the open interest for the front month of MAY (442) AND the number of notices served upon today (2 )x (5000 oz)

Thus the standings for silver for the MAY 2025 contract month: (14,798) Notices served so far) x 5000 oz + OI for the front month of MAY(442) minus number of notices served upon today (2)x 5000 oz equals silver standing for the MAY contract month equating to 76.190 MILLION OZ . THEN WE MUST ADD OUR NEW 12.93 TONNES OF EXCHANGE FOR RISK. NEW TOTAL STANDING FOR SILVER: 89.120 MILLION OZ

New total standing: 89.120 million oz which is huge for this active delivery month of MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 168.457million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

MAY 23 WITH GOLD UP $69.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 919.88 TONNES

MAY 22 WITH GOLD DOWN $15.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 919.88 TONNES

MAY 21 WITH GOLD UP $28.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.60 TONNES

MAY 20 WITH GOLD UP $51.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.30 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.03 TONNES

MAY 19 WITH GOLD UP $46.65 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.89 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 918.73 TONNES

MAY 16 WITH GOLD DOWN $38.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 927.62 TONNES

MAY 15 WITH GOLD UP $38.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.53 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 931.92 TONNES

MAY 14 WITH GOLD DOWN $40.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 936.51 TONNES

MAY 13 WITH GOLD UP $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 12 WITH GOLD DOWN $115.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 9 WITH GOLD UP $37.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 939.68 TONNES

MAY 8 WITH GOLD DOWN $82.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.23 TONNES OF GOLD WITHDRAWN FROM THE GLD/ ///INVENTORY RESTS AT 937.67 TONNES

MAY 7 WITH GOLD DOWN $30.30 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 937.96 TONNES

MAY 6 WITH GOLD UP $101.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 937.96 TONNES

MAY 5 WITH GOLD UP $77.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.13 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.28 TONNES

MAY 2 WITH GOLD UP $ 18.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 945.41 TONNES

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

APRIL29 WITH GOLD DOWN $13.45 TODAY// NO CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL28 WITH GOLD UP $50.20 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL25 WITH GOLD DOWN $49.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVEV WITHDRAWAL OF 3.911 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 948.56 TONNES

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

GLD INVENTORY: 923.89 TONNES, TONIGHTS TOTAL

SILVER

MAY 23 WITH SILVER UP $0.38/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.5 MILLION OZ OF SILVER INTO THE SLV/: //INVENTORY AT SLV RESTS AT 454.375 MILLION OZ

MAY 22 WITH SILVER DOWN $0.27/NO CHANGES IN SILVER INVENTORY AT THE SLV:////: //INVENTORY AT SLV RESTS AT 451.875 MILLION OZ

MAY 21 WITH SILVER UP $0.35/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.091 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 451.875 MILLION OZ

MAY 20 WITH SILVER UP $0.65/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.41 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 449.784 MILLION OZ

MAY 19 WITH SILVER UP $0.17/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHTDRAWAL OF 1.819 MILLION OZ OUT OF THE SLV// ////: //INVENTORY AT SLV RESTS AT 447.193 MILLION OZ

MAY 16 WITH SILVER DOWN $0.24/NO CHANGES IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 15 WITH SILVER UP 0.04/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.909 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 14 WITH SILVER DOWN $0.39/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.682 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.102 MILLION OZ

MAY 13 WITH SILVER UP $0.44/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 12 WITH SILVER DOWN $0.30/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 9 WITH SILVER UP $0.31/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 8 WITH SILVER DOWN $0.16/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 7 WITH SILVER DOWN $0.54/NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 6 WITH SILVER UP $0.92 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A HUG WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 5 WITH SILVER UP $0.08 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF 0.117 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.602 MILLION OZ

MAY 2 WITH SILVER DOWN $0.19 /MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 4.545 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.424 MILLION OZ

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

APRIL29 WITH SILVER UP $0.30 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.229 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 451.925 MILLION OZ

APRIL28 WITH SILVER DOWN $0.03 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.136 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.696 MILLION OZ

APRIL25 WITH SILVER DOWN $0.44 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 3.639 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.832 MILLION OZ

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

It’s the best of times for gold; the worst of times for dollars. Led by long-dated JGBs, global government bond markets are wobbling. We can see where this is going…

This week saw moderately firmer prices for gold and silver following a near-four-week consolidation. In European trade this morning, gold was $3328, up $27 from last Friday’s close. And silver was $33.20, up 93 cents. Futures volumes on Comex remained low-to-moderate, though picking up slightly as the week progressed.

It is worth bearing in mind that measured by open interest, both contracts are still in oversold territory, a technical positive factor limiting the ability of the swaps to shake out longs:

Traders and stackers alike will be wondering whether the consolidation timed from 22 April is over. While gold’s bullish outlook is undoubted, a look at the technical chart is not clear.

While support at the 55-day moving average has held, it could be argued that more time for the 12-month MA to catch up would provide a better platform for gold to climb towards $4000. But with gold’s Comex open interest low, does this really matter?

Probably not, given that this week has seen a developing crisis in government bond markets, with long-dated JGB yields soaring:

It matters because of the signal being sent about the future of the second largest debt market in the world and its short-term interest rates, and also because the yen carry-trade plays a major part in funding US government debt. Contagion into US Treasuries is pretty much certain.

Additionally, this was the week when the US House of Representatives passed Trump’s “big, beautiful spending bill” adding trillions of debt which has to be funded with foreign investors acting as the marginal players. With his tariff policies, Trump has almost certainly alienated this cohort, making funding more difficult. And so far, market consensus over the economic outlook is probably too optimistic: a recession is almost certain blowing budget deficit estimates out of the water. And the implications for dollar interest rates are that they could rise rather than fall.

The long bond chart appears to confirm this danger:

It will take very little to drive the long bond yield to 20-year highs above 5.2%, and a crisis in JGBs doesn’t help.

Monday is Memorial Day in the US, so its markets will be closed, thinning out trade and making them less predictable. Will this be an opportunity for the Japanese and US governments to collude in a bond market support operation? It would be wrong to rule it out. But looking through next week, we can see the consequences of alienating foreigners from US debt markets in the next chart:

Before 2 April when Trump announced his new tariffs, the US$ trade-weighted index correlated nicely with the 10-year UST-note yield, as one would expect. That date is marked by the pecked line. From then on, the correlation broke down with the dollar collapsing and the T-bond yield soaring. There has been no clearer indication of the loss of foreign confidence in the dollar and US debt.

We have looked at the prospect for higher bond yields and concluded that despite possible government intervention next week while the US is on holiday, they are going higher. The blue line in the chart above is almost certainly heading to over 5%. Now we shall look at the chart for the TWI:

Ouch! This one is heading significantly lower. So, the bond crisis is also a dollar crisis likely to develop over the next few weeks. It answers the question posed earlier in this article about whether gold spends more time consolidating before going higher. Other than the manipulation over Comex contract expiry next week, it is hard to see any reason why gold should not go considerably higher sooner rather than later.

3. CHRIS POWELL AND GATA DISPATCHES

BIS gold swaps have collapsed 99% in four years

Submitted by admin on Fri, 2025-05-23 12:59 Section: Daily Dispatches

GATA’s Robert Lambourne long has provided the most contemporaneous proof of official intervention against gold — and the proof that gold is winning.

* * *

1:07p ET Friday, May 23, 2025

Dear Friend of GATA and Gold:

For 26 years GATA has documented extensively the efforts of Western central banks and especially the U.S. government to suppress and manipulate the price of gold to protect the U.S. dollar against competition as the world reserve currency and to control interest rates:

But for the last six years the most contemporaneous proof of surreptitious central bank intervention in the gold market has come from GATA’s consultant about the Bank for International Settlements, Robert Lambourne, who has analyzed the BIS’ monthly statements of account to discern the volume of gold swaps undertaken by the bank on its own behalf and on the behalf of its central bank members.

The bank has never challenged Lambourne’s calculations, just as it has refused to explain publicly the objectives of the gold swaps and identify their participants, but its annual reports have confirmed the accuracy of Lambourne’s reports.

Since surreptitious intervention in the gold market by the U.S. government and its closest allies is a prohibited subject in Western financial journalism, Lambourne’s reports have been essential to anyone outside government and central banking who sought to understand the monetary metals markets — and for years now Lambourne’s work about the BIS has shown that Western central bank policy on gold was changing dramatically.

That is, four years ago, in February 2021, Lambourne showed that the BIS had undertaken 552 tones in gold swaps. Since then the BIS’ gold swaps have declined fairly steadily, and according to the BIS’ March and April statements of account, published this week —

— the BIS reduced its gold swaps to 9.5 tonnes in March and to a mere 5 tonnes in April.

If the BIS’ reports are honest, as of April its gold swaps are now less than 1% of what they were four years ago.

The decline in the bank’s gold swaps has coincided with a steady rise in the gold price, with frequent announcements by certain central banks of gold acquisitions, and with a growing impression that something very big is going on behind the scenes with gold.

Eventually maybe people in the West will see gold’s resurrection, the debasement of their government currencies, and the refusal of their governments to acknowledge and explain their market interventions as evidence that their democracies are largely an illusion.

In the meantime, month by month Lambourne has frightened away the shills who used to deny that the gold market was manipulated or who dismissed manipulation as the ordinary and inconsequential tricks of traders having no connection with government.

Thanks in large part to GATA and a few other independent researchers and analysts, nearly everyone involved with the monetary metals knows now that governments long have waged a largely secret war against them, a war that is also aimed against their own people. Lambourne’s surveillance of the BIS has produced the crucial signs that governments are retreating and gold, the ancient defender of individual liberty, is winning.

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

Fort Knox episode of ‘America’s Book of Secrets’ featuring GATA reaches YouTube

Submitted by admin on Wed, 2025-05-21 11:45 Section: Daily Dispatches

11:45a ET Wednesday, May 21, 2025

Dear Friend of GATA and Gold:

The History channel at YouTube yesterday posted the entirety of the “America’s Book of Secrets” episode from 2012 about the U.S. gold reserve at Fort Knox, an episode in which GATA has a prominent part.

The program has been rebroadcast in syndication on cable television networks many times in the last 13 years, but it may be of interest to those who haven’t seen it already.

At least it shows that GATA has been working on the gold price manipulation issue for a long time, and that your secretary/treasurer was young once.

The episode is 43 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

China’s gold imports surge to 11-month high despite record prices

Submitted by admin on Wed, 2025-05-21 11:11 Section: Daily Dispatches

By Yihui Xie Bloomberg News Tuesday, May 20, 2025

China imported the most gold in nearly a year last month despite record prices, after heightened demand for the precious metal prompted the central bank to ease restrictions on bullion inflows.

Total gold imports to the country reached 127.5 metric tons, a 11-month high, according to customs data released today. This represents a 73% jump from a month earlier, even after gold hit successive all-time highs, at once point touching $3,500 an ounce.

The rise in imports is likely due to the People’s Bank of China allocating fresh quotas to some commercial banks in April, as the authority responds to strong demand from institutional and retail investors at the height of the trade war. The central bank controls physical bullion flows, typically granting import licenses and quotas only to select banks. …

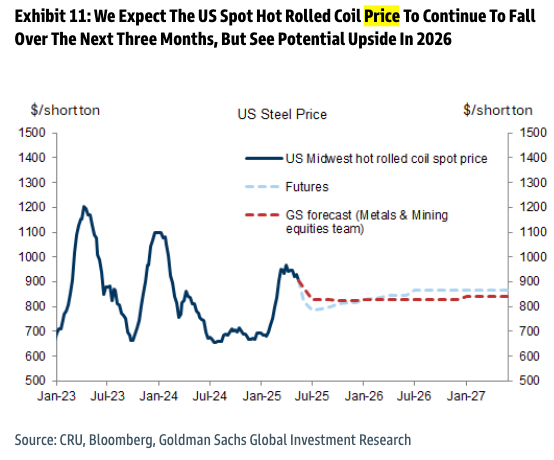

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:STEEL

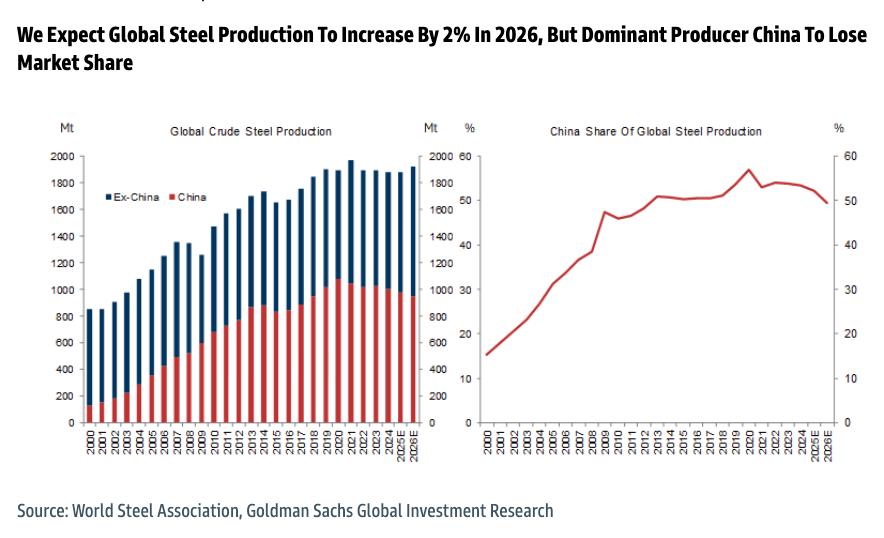

China’s Two-Decade Global Steel Expansion “Has Now Ended”

Friday, May 23, 2025 – 10:45 AM

In Goldman’s latest global steel outlook, analysts Aurelia Waltham, Eoin Dinsmore, and others highlight a key inflection point: China’s share of global steel production has declined for the first time in over two decades, reversing a multi-decade expansion period.

“After more than two decades of China increasing its share of global steel production, we believe this structural trend has now come to an end as China’s domestic demand continues to falter and barriers to steel exports intensify,” Waltham and her team wrote in a note published on Friday morning.

The analysts noted that their global steel supply and demand model forecasted a 3% and 4% year-over-year increase in ex-China steel demand for 2025 and 2026, respectively. As Chinese steel exports are expected to decline, ex-China crude steel production is projected to rise by 3% in 2025 and 8% in 2026.

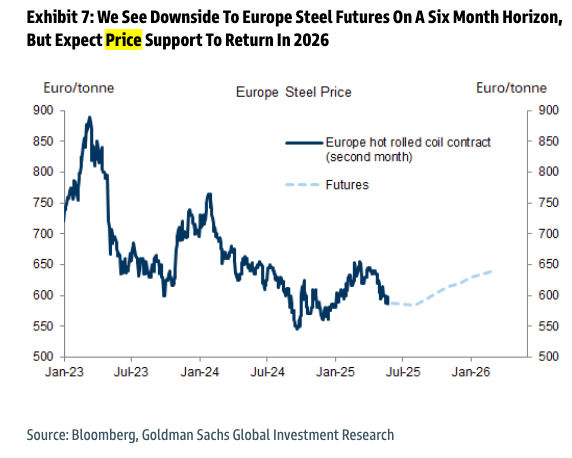

“While we are bearish on US and European steel prices on the three-to-six month horizon, we expect a re-acceleration in demand growth and lower Chinese steel exports to provide price upside in 2026,” Waltham said.

They outlined the biggest risk to their forecast of China losing global market share:

We see the biggest risk to our call that China will start to lose market share of global steel production to the rest of the world over the next two years being indirect[1] Chinese steel exports continuing to climb, pushing down rest of world apparent steel demand. This would likely see China steel demand from the manufacturing sector exceeding our current expectations, preventing a decline in Chinese steel output and apparent domestic demand, while at the same time meaning rest of world steel production growth would fall below end use consumption growth. However, this would be at odds with China’s policy to reduce steel output.

Following a 25-year expansion that saw China increase its share of global steel production from approximately 15% in 2000 to about 55% by 2020, analysts now forecast a decline to about 50% by 2026.

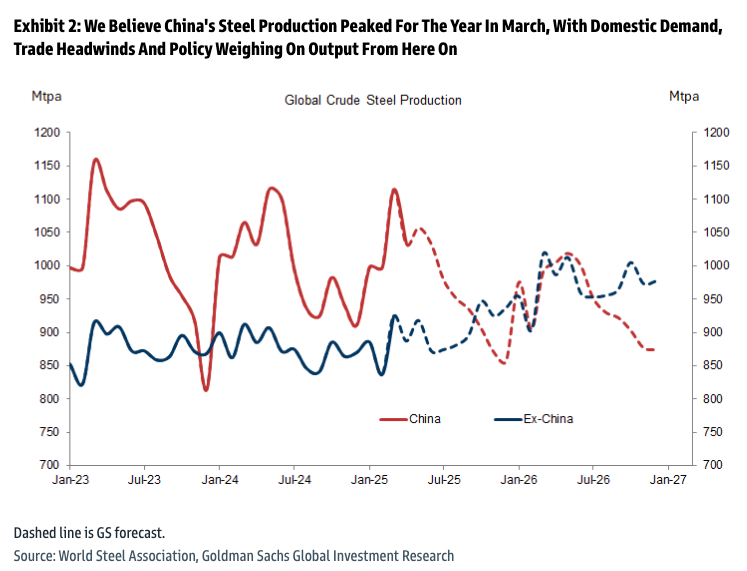

China’s steel production for 2025 already peaked in March.

Key takeaways about China’s declining influence in global steel markets:

Peak Reached: China’s steel production likely peaked in March 2025 and is expected to decline by 2–3% YoY through 2026.

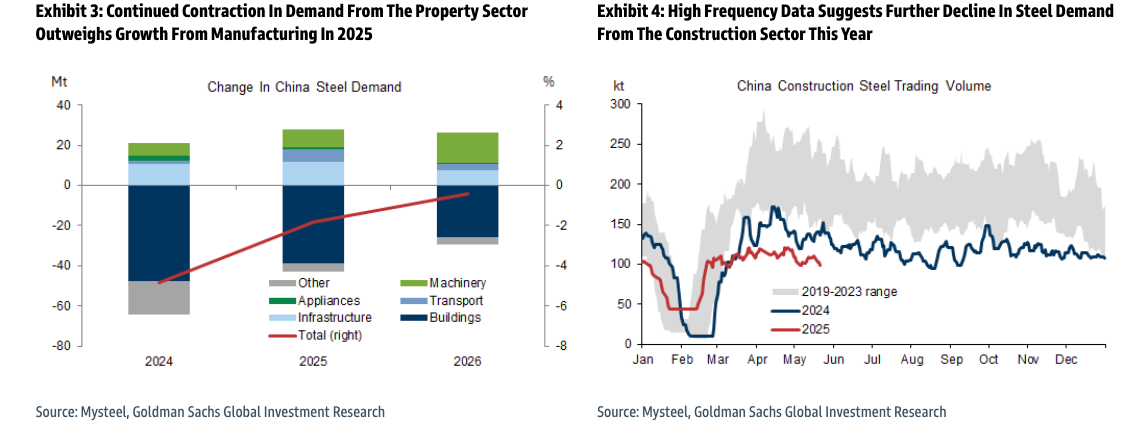

Domestic demand slowdown: A continued decline in construction activity, especially new housing starts (forecasted to drop 24% in 2025), will more than offset gains from manufacturing (e.g., autos and appliances).

Export headwinds: Chinese finished and semi-finished steel exports are forecast to drop 33% YoY in 2026, from 12% to under 8% of ex-China steel consumption.

Policy risk: If exports or output stay elevated, the Chinese government may impose mandated production cuts (likely via emissions controls) in Q4 2025 to meet policy targets.

China’s economy is still a mess. Property sector will continue to weigh on steel demand.

However, the analysts view a rebound in ex-China steel:

Ex-China growth: Production outside China is expected to rise 3% in 2025 and 8% in 2026, helped by recovering demand and lower competition from Chinese exports.

Regional demand: Demand in the U.S., EU, and India will gradually improve. Apparent demand outside China is forecast to rise 3–4% annually into 2026.

Global Steel Price Outlook:

Near-term weakness: U.S. and European prices face further downside in the next 3–6 months due to lackluster demand and high inventories.

2026 upside: Prices are forecast to rise in 2026 as Chinese exports fall and global demand picks up, particularly in Asia and the EU. Anti-dumping measures and trade friction will help contain Chinese supply abroad.

European Steel Price Forcast

US Hot Rolled Coil Price Forecast

The long-standing concern over China flooding global markets with steel may finally be easing—a shift that could pave the way for Western producers to ramp up output. We anticipate this trend will be evident in the U.S amid President Trump’s ‘America First’ era.

6 CRYPTOCURRENCY NEWS

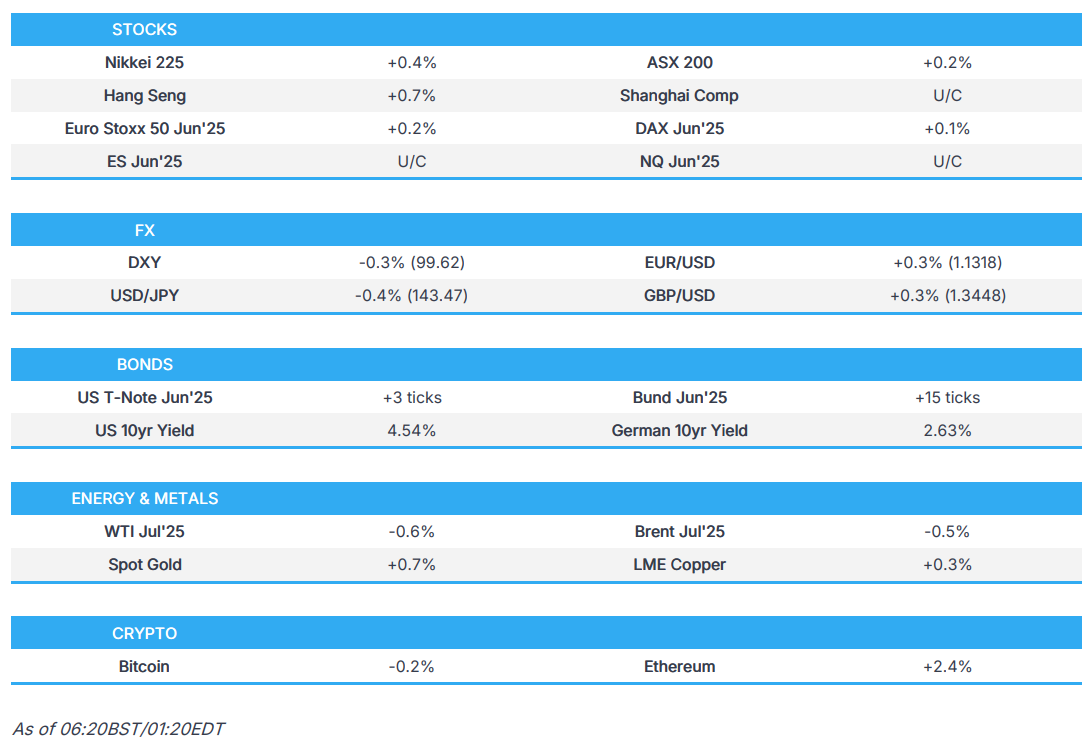

ASIAN MARKETS THIS MORNING:

SHANGHAI CLOSED DOWN 31.82 PTS OR 0.94%

//Hang Seng CLOSED UP 56.44 PTS OR 0.24%

// Nikkei CLOSED UP 174.60 PTS OR 0.47% //Australia’s all ordinaries CLOSED UP 0.18%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1906 OFFSHORE CLOSED UP AT 7.1872/ Oil DOWN TO 60.70 dollars per barrel for WTI and BRENT DOWN TO 63.99 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1906 AND STRONGER//OFF SHORE YUAN TRADING UP 7.1872 AGAINST US DOLLAR/ AND THUS STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1906 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1872 (CCP MANIPULATED)

SHANGHAI CLOSED DOWN 31.82 PTS OR 0.94%

HANG SENG CLOSED UP 56.95 PTS OR 0.24%

2. Nikkei closed UP 174.60 PTS OR 0.47%

3. Europe stocks SO FAR: ALL GREEN

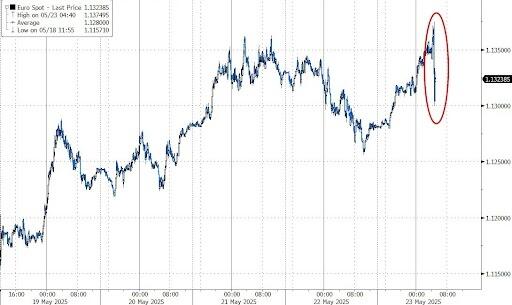

USA dollar INDEX DOWN TO 99.35// EURO RISES TO 1.1339 UP 57 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.546//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 143.38…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

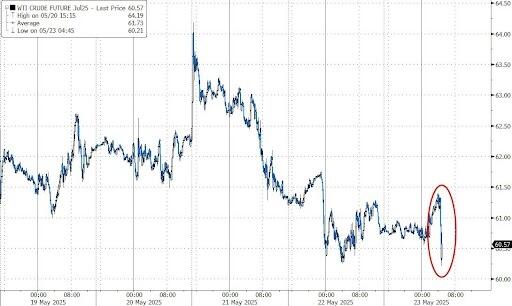

3g Oil DOWN for WTI and DOWN FOR UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6240/Italian 10 Yr bond yield DOWN to 3.640 SPAIN 10 YR BOND YIELD DOWN TO 3.232%

3i Greek 10 year bond yield DOWN TO 3.382

3j Gold at $3326.45. Silver at: 33.24 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 50 /100 roubles/dollar; ROUBLE AT 79.24

3m oil into the 60 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.19// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.546% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8267 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9373 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

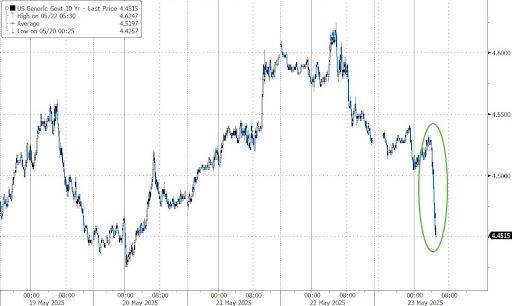

USA 10 YR BOND YIELD: 4.517 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 5.020 DOWN 5 BASIS PTS/

USA 2 YR BOND YIELD: 3.987 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 39.03

10 YR UK BOND YIELD: 4.7350 DOWN 9 PTS

10 YR CANADA BOND YIELD: 3.373 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.965 DOWN 1 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

2b European Opening report

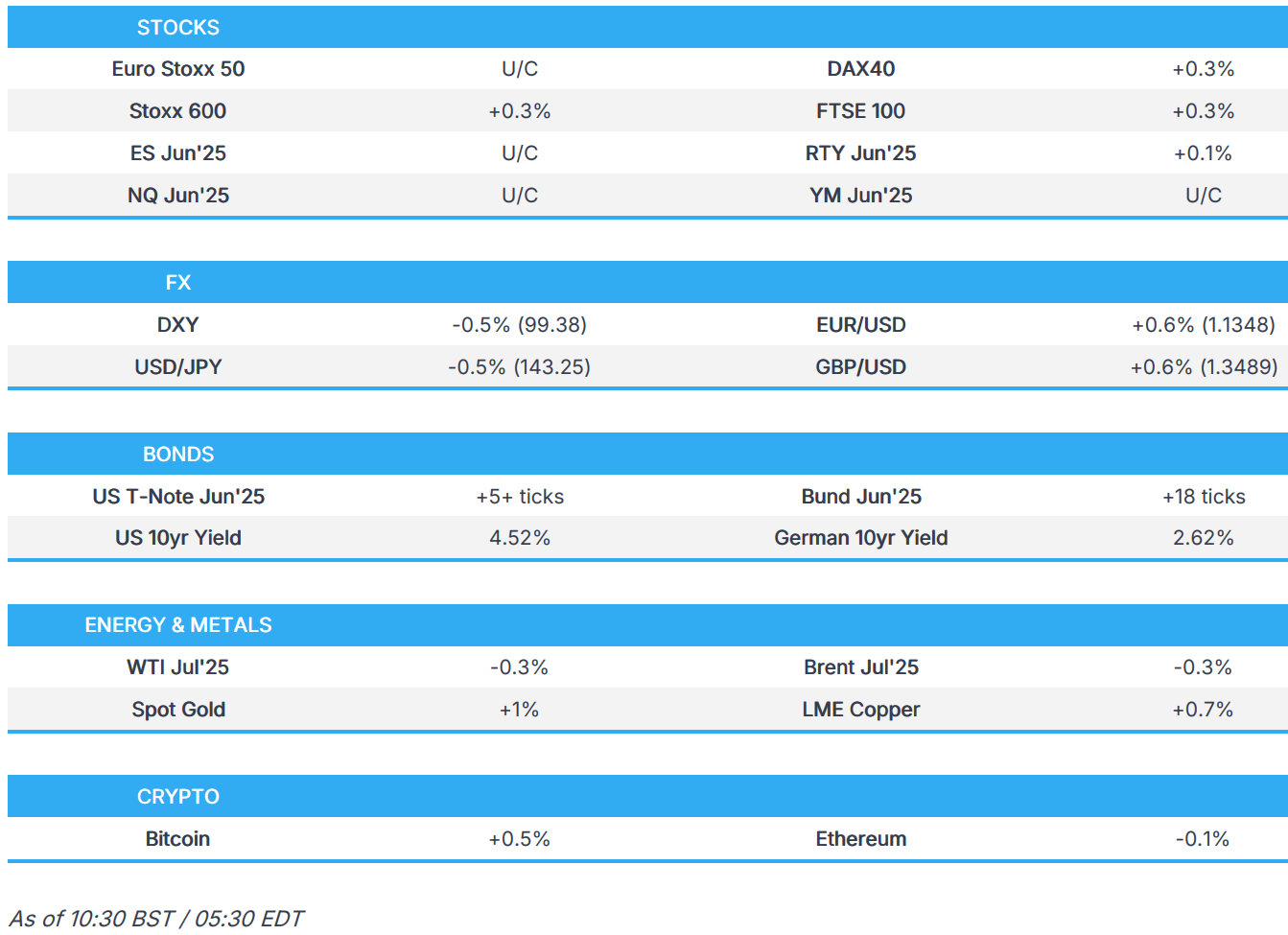

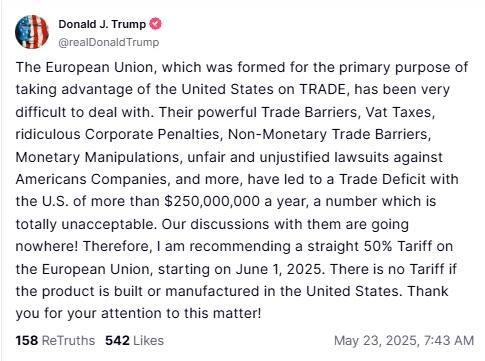

USD continues to slip while Bonds edge higher awaiting Fed speak; Trump is pushing the EU to cut tariffs or face extra duties – Newsquawk US Market Open

Friday, May 23, 2025 – 05:44 AM

US President Trump is pushing the EU to cut tariffs or face extra duties with US negotiators to tell Brussels they expect unilateral concessions, according to FT.

European and US equity futures are trading mixed and generally reside on either side of the unchanged mark.

USD shunned once again after Thursday’s attempted bounce; JPY benefits from hot core inflation data overnight; GBP little moved to firmer-than-expected Retail Sales.

Bonds are higher as USTs look to claw back recent losses; some downside in Bunds following German GDP but proved fleeting.

Crude remains subdued whilst metals benefit from the softer Dollar ahead of US-Iran talks at 12:00 BST / 07:00 EDT.

Looking ahead, Canadian Retail Sales, Speakers including ECB’s Schnabel, BoE’s Pill, Fed’s Musalem & Cook.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

TARIFFS/TRADE

US Deputy Secretary of State Landau spoke with Chinese Vice Foreign Minister Ma on Thursday and acknowledged the importance of the bilateral relationship to the people of both countries, while they discussed a wide range of issues of mutual interest and agreed on the importance of keeping open lines of communication.

US President Trump is pushing the EU to cut tariffs or face extra duties with US negotiators to tell Brussels they expect unilateral concessions, while USTR Greer is preparing to tell EU counterpart Sefcovic that recent “explanatory note” falls short of US expectations, according to FT.

Japanese PM Ishiba said he held a call with US President Trump in which they discussed tariffs, diplomacy and security, while there might be an occasion where he visits the US for in-person talks with Trump. Furthermore, Ishiba said there are no changes to Japan’s stance on US tariffs and demand for the elimination of tariffs, nor to Japan’s policy of talking with the US on creating US jobs.

Japan’s chief tariff negotiator Akazawa reiterated there is no change to stance on requesting elimination of US tariffs, but noted they aim to reach an agreement, while he plans to visit the US around May 30th for the fourth round of trade talks, according to sources cited by Reuters.

Japan is to reportedly propose investments by Nippon Steel (5401 JT) in tariff talks with the US, according to NHK.

EUROPEAN TRADE

EQUITIES

European bourses opened incrementally firmer and trudged higher throughout the morning – though more recently, some downside has been seen to display a mixed picture in Europe.

European sectors opened without a clear bias, but have since moved to a strong positive direction. Basic Resources tops the pile, joined closely by Travel & Leisure and then Healthcare. Retail lags.

US equity futures are flat/modestly firmer, following similar price action seen in Europe. Docket ahead is lacking in terms of Tier 1 data, but the focus will be on Fed speak from Musalem and Cook.

This week’s downtrend for the USD has resumed. For today’s session, the calendar is light in terms of tier 1 data but Fed’s Goolsbee, Musalem, Schmid and Cook are all due on the speaker slate. DXY has just slipped below the bottom end of Thursday’s 99.44-100.11 range.

EUR is capitalising on the softer USD with EUR/USD back on a 1.13 handle. Today’s detailed release of Q1 German GDP exceeded expectations but failed to engineer much in the way of additional support from the EUR given that the beat was attributed to front-loading ahead of expected tariff actions by the Trump admin. On the trade front, the FT has reported that US President Trump is pushing the EU to lower tariffs or face additional duties with US negotiators to tell Brussels they expect unilateral concessions. On the speaker front, ECB dove Stournaras has stated that he sees a June rate cut and then a pause, whilst Rehn has backed a June rate reduction, data permitting. The pair was little moved to the latest ECB Wage Tracker. EUR/USD currently around 1.1337.

JPY is out-muscling the USD in the wake of hot Japanese core inflation data overnight. ING writes that “Excluding both fresh food and energy, core-core inflation rose to 3.0%, suggesting that underlying inflation will remain above the BoJ’s target of 2.0%”. On the trade front, Japan’s chief tariff negotiator Akazawa reiterated there is no change to the stance on requesting the elimination of US tariffs. However, he noted they aim to reach an agreement and plans to visit the US around May 30th for the fourth round of trade talks. USD/JPY currently sits within Thursday’s 142.80-144.40 range.