GOLD CLOSED DOWN $27.10 TO $3,291.95

SILVER CLOSED DOWN $0.36 TO $32.95

GOLD ACCESS CLOSED $3293.00

Silver ACCESS CLOSED: $32.97

TONIGHT FINISHES OPTION EXPIRY FOR THE COMEX//AND THUS THE REASON FOR THE RAID//FRIDAY IS OPTIONS EXPIRY FOR THE LONDON/OTC OPTIONS

Bitcoin morning price:$105,320 DOWN 620 DOLLARS.

Bitcoin: afternoon price: $104,760 DOWN 1180 DOLLARS

Platinum price closing DOWN $20.15 TO $1059.20

Palladium price; DOWN $7.20 TO $969.50

END

*CANADIAN GOLD: $4,519.76 DOWN 57.70 CDN dollars per oz( * NEW ALL TIME HIGH $4735.70 CDN DOLLARS PER OZ//APRIL 21 2025)

*BRITISH GOLD: 2445.33 DOWN 10.66 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,566.50 BRITISH POUNDS/OZ) MAY 6/2025

*EURO GOLD: 2901.40 DOWN 12.93 Euros per oz //* (ALL TIME CLOSING HIGH: 3018.80 EUROS PER OZ/ APRIL 21 //2025)

DONATE

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,317.100000000 USD

INTENT DATE: 05/29/2025 DELIVERY DATE: 06/02/2025

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 257 8

072 H GOLDMAN 7

099 H DEUTSCHE BANK AG 3780

104 C MIZUHO SECURITIES US 87

118 C MACQUARIE FUTURES US 36

118 H MACQUARIE FUTURES US 1061

132 C SG AMERICAS 425

167 C MAREX 35

190 H BMO CAPITAL MARKETS 1182

285 C NANHUA USA-HK 38

323 C HSBC 320 676

332 H STANDARD CHARTERED B 428

357 C WEDBUSH SECURITIES 4

363 H WELLS FARGO SECURITI 141 11

555 C BNP PARIBAS SEC CORP 417

555 H BNP PARIBAS SEC CORP 942

624 H BOFA SECURITIES 713

657 C MORGAN STANLEY 947

657 H MORGAN STANLEY 333

661 C JP MORGAN SECURITIES 5586 8394

686 C STONEX FINANCIAL INC 333 2

690 C ABN AMRO CLR USA LLC 4

709 C BARCLAYS 1389

709 H BARCLAYS 113

732 C RBC CAP MARKETS 500

880 C CITIGROUP 50

880 H CITIGROUP 2315

905 C ADM 8 4

TOTAL: 15,273 15,273

MONTH TO DATE: 15,273

JPMORGAN STOPPED 8394/15,273

MAY

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024: 15,273 CONTRACTs NOTICES FOR 1,527,300 OZ or 47.505 TONNES

total notices so far: 15,273 contracts for 1,527,300 OR 47.505 tonnes)

FOR JUNE

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 1817 NOTICE(S) FILED FOR 9.085 MILLION OZ/

total number of notices filed so far this month : 1817 CONTRACTS (NOTICES) for 9.085 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $27.10 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.59 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 930.20 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $.36 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: //A DEPOSIT OF 2.773 MILLION OZ INTO THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 459.103 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 1297 CONTRACTS TO 149,317 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.29 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 1472 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A 175 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD SOME LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING WITH RESPECT TO THURSDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON THURSDAY WITH SILVER’S GAIN IN PRICE AS THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH ANOTHER FAIR T.A.S. ISSUANCE OF 239 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A 175 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR SMALL 239 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FRIDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 1472 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.29.

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS MUST NOW BE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT/FRIDAY MORNING: A SMALL 239 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.29) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH

WE HAD A 175 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 9.90 MILLION OZ

THUS:

INITIAL STANDING FOR JUNE: 9.90 MILLION OZ

WE HAD:

/ HUGE COMEX OI GAIN+// A 175 SIZED EFP ISSUANCE (/ VI) SMALL SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 239 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A SMALL 120 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 21 DAYS, total 5795 contracts: OR 28.975 MILLION OZ (275 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 28.975 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1297 CONTRACTS WITH OUR GAIN IN PRICE OF $0.29 IN SILVER PRICING AT THE COMEX// THURSDAY.,. . THE CME NOTIFIED US THAT WE HAD A 175 CONTRACT EFP ISSUANCE CONTRACTS: 175 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY REDUCES TO: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND NOW JUNE: 9.90 MILLION OZ

THE NEW TAS ISSUANCE THURSDAY NIGHT (239 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TODAY’S TRADING (FRIDAY TRADING) AND BEYOND.

WE HAD 1817 NOTICE(S) FILED TODAY FOR 9.085 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST BY A STRONG SIZED 6937 OI CONTRACTS TO 422,605 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A MONSTER 3966 CONTRACTS //.

WE HAD A STRONG SIZED DECREASE IN COMEX OI (6937 CONTRACTS) . THIS OCCURRED DESPITE OUR GAIN OF $22.35 IN PRICE// THURSDAY///.

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

INITIAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH

/ WE HAD A $22.35 GAIN IN PRICE WITH RESPECT TO THURSDAY’S COMEX ///. WE HAD A STRONG SIZED LOSS OF 4083 OI CONTRACTS (12.69 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE DURING THE FIRST THREE WEEKS OF MAY, AND THROUGHOUT EACH AND EVERY DAY MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A SMALLER THAN EXPECTED AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE JUNE CONTRACT MONTH….. A SMALLISH 62.534 TONNES. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2854 CONTRACT:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 422,605/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 149,317 CONTRACTS!!

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4083 CONTRACTS WITH 6937 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 2854 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 4083 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 418 CONTRACTS

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS 2854 CONTRACT) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 6937 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 4083 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) WEAK STANDING FOR GOLD FOR JUNE AT 62.524TONNES

NEW STANDING FOR GOLD, JUNE CONTRACT INITIALLY AT 62.534 TONNES OF GOLD.

.

/ 3) ZERO T.A.S. LIQUIDATION , AS WE HAD 1)A $22.35 COMEX PRICE GAIN.. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THAT GAIN IN PRICE AS WE HAD A TINY LOSS OF 117 CONTRACTS ON OUR TWO EXCHANGES// /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY.

4) FAIR SIZED COMEX OI LOSS// 5) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (6071 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 418 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAY INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 36,490 CONTRACTS OR 3,649,000 OZ OR 113.499 TONNES IN 21 TRADING DAY(S) AND THUS AVERAGING: 1737 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES 113.499 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 113.499 TONNES DIVIDED BY 3550 x 100% TONNES = 3.21% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1297 CONTRACTS OI TO 149,317 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 175 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 175 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 175 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1297 CONTRACTS AND ADD TO THE 175 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1472 CONTRACTS WITH THE GAIN IN PRICE OF $0.29 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 7.360 MILLION PAPER OZ

OCCURRED WITH OUR $0.29 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS FRIDAY MORNING//THURSDAY NIGHT

ASIAN MARKETS THIS MORNING:

SHANGHAI CLOSED DOWN 15.96 PTS OR 0.47%

//Hang Seng CLOSED DOWN 283.61 PTS OR 1.62%

// Nikkei CLOSED DOWN 467.88 PTS OR 1.22% //Australia’s all ordinaries CLOSED UP 0.26%

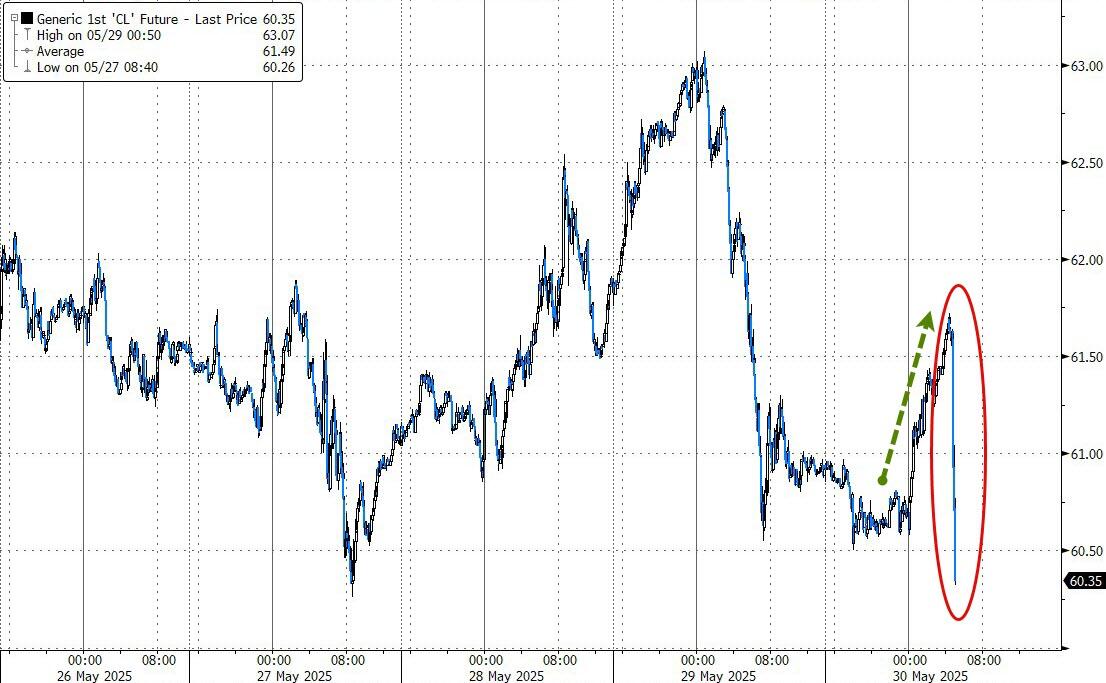

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1960 OFFSHORE CLOSED DOWN AT 7.1990/ Oil DOWN TO 61.37 dollars per barrel for WTI and BRENT DOWN TO 63.71 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1960 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1990 AGAINST US DOLLAR/ AND THUS WEAKER

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6937 CONTRACTS TO 422,605 DESPITE OUR GAIN IN PRICE OF $22.35 WITH RESPECT TO THURSDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2854 ).

THE CME ANNOUNCED THURSDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES. TOTAL ISSUANCE FOR MAY REMAINS AT 9.591 TONNES OF GOLD AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES. THE BANK OF ENGLAND MUST BE GETTING QUITE ANTSY OF GETTING ITS GOLD BACK.

IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST FIVE MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

JUNE: ZERO ISSUED SO FAR!!

DETAILS ON JUNE COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 4083 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF MAY, CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS SMALL AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A SMALL 418 T.A.S.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , INITIAL STANDING IS RECORDED AT 62.534 TONNES.

NEW TOTAL TONNES STANDING: 62.534 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 5+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 223 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2854 EFP CONTRACT WAS ISSUED: : /AUGUST 2854 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2854 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS

- ZERO NET SPEC LIQUIDATION WITH OUR HUGE GAIN IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY MORNING/WEDNESDAY NIGHT WAS A SMALL SIZED, 418 CONTRACTS.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL AND MAY

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE

STANDING LAST 6 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: INITITAL STANDING 62.534 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 52 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING/JUNE CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $22.35/ /) AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A TINY SIZED LOSS IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD LITTLE IF ANY T.A.S. SPREADER LIQUIDATION THURSDAY AS THEY ARE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE THE MAGIC $3,400 BARRIER AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING (AS WE NOW ENTER LONDON/OTC OPTION EXPIRY WEEK WHICH WILL CONCLUDE THIS FRIDAY, MAY 30)

FRIDAY MORNING/THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JUNE TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: SO FAR ZERO

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS JUNE DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JUNE COMEX CONTRACT

WE HAVE LOST A STRONG SIZED TOTAL OF 12.69 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE FIRST RECORDED AT 62.534 TONNES ON FIRST DAY NOTICE/MAY 30.

ALL OF THIS QUITE SMALL STANDING FOR JUNE AND THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $22.35

WE HAD A MONSTER 3966 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 4083 CONTRACTS OR 408,300 0Z (12.69 TONNES)

confirmed volume THURSDAY 264,492. contracts: fair volume////

//speculators have left the gold arena

END

MAY 30

INITIAL

JUNE CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | NIL xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 15,273 notice(s) 1,527,300 OZ 47.505 TONNES |

| No of oz to be served (notices) | 4832 contracts 483,200 OZ 15.029 TONNES |

| Total monthly oz gold served (contracts) so far this month | 15,273 notices 1,527,300 oz 47.505 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 0 customer entries

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 0

adjustments: 4//

the first two are customer to dealer

a) Asahi: 32,015.018 oz

b) Brinks 32,118.849 oz (999 kilobars)

Next two//dealer to customer

c) Malca: 1543.248 oz 48 kilobars

d) 580.232 oz

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JUNE STANDS AT 20,105 CONTRACTS FOR A LOSS OF 14,674 CONTRACTS.

THUS BY DEFINITION, THE INITAL AMOUNT OF GOLD STANDING FOR THIS STRONG DELIVERY MONTH OF JUNE IS AS FOLLOWS:

20,105 CONTRACTS X 100 OZ PER CONTRACT

EQUALS

2,010,500 OZ OR 62.534 TONNES

JULY GAINED 194 CONTRACTS TO STAND AT 7230

AUGUST GAINED 6154 CONTRACTS UP TO 317,115

We had 15,273 contracts filed for today representing 1,527,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and5585 notices issued from their client or customer account. The total of all issuance by all participants equate to 15,273 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 8394 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE /2025. contract month, we take the total number of notices filed so far for the month (15,273 X 100 oz ) to which we add the difference between the open interest for the front month of JUNE (20,105 CONTRACTS) minus the number of notices served upon today (15,273 x 100 oz per contract) equals 2,010,500 OZ OR 62.534 TONNES to which we add 0 tonnes of gold issued under exchange for risk// totals 62.534 tonnes

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (15,273 x 100 oz +we add the difference for front month of JUNE (20,105 OI} minus the number of notices served upon today (15,273 x 100 oz) which equals 2,010,500 OZ OR 62.534 TONNES + 0 tonnes EX FOR RISK = 62.534 tonnes

TOTAL COMEX GOLD STANDING FOR JUNE.: 62.534 TONNES WHICH IS SMALL FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..JUNE DID NOT FOLLOW FEB AND APRIL’S LEAD!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,193,240.283 oz 68.218 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,789,194.161 oz

TOTAL REGISTERED GOLD 21,319,411.780: or 663.122 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,469,782.381 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,126,171 oz (REG GOLD- PLEDGED GOLD)= 594.90 tonnes //

SILVER/COMEX

THE JUNE 2025 SILVER CONTRACT//INITIAL

MAY 30

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 withdrawal entries i) Out of Brinks 2,376,557.120 oz ii Out of Delaware 9739.712 oz iii) Out of HSBC 919,,783.910 oz total withdrawal 3,306,080.732 oz |

| Deposits to the Dealer Inventory | 1 entry i) into Stonex: 580,254.700 oz total deposit: 580,254.700 oz |

| Deposits to the Customer Inventory | 2 DEPOSIT ENTRIES i) Into CNT 4990.01 oz ii) Into Int. Delaware 600,962.720 oz total deposit 605,952.730 oz |

| No of oz served today (contracts) | 1817 CONTRACT(S) (9.095 OZ |

| No of oz to be served (notices) | 163 contract (0.815 MILLION oz) |

| Total monthly oz silver served (contracts) | 1817 Contracts (9.085 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposits into dealer accounts

1 entry

i) into Stonex: 580,254.700 oz

total deposit: 580,254.700 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 deposit entries//customer side/eligible

2 DEPOSIT ENTRIES

i) Into CNT 4990.01 oz

ii) Into Int. Delaware 600,962.720 oz

total deposit 605,952.730 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3 withdrawal entries

i) Out of Brinks 2,376,557.120 oz

ii Out of Delaware 9739.712 oz

iii) Out of HSBC 919,,783.910 oz

total withdrawal 3,306,080.732 oz

ADJUSTMENTs 2//customer to dealer

i) Out of CNT 765,818.38 oz

ii) Out of Delaware 182,117.879 oz

JPMorgan has a total silver weight: 214.825million oz/496.007 oz million or 43.34%

TOTAL REGISTERED SILVER: 158.100 MILLION OZ//.TOTAL REG + ELIGIBLE. 496.007Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2025 OI: 1980 OPEN INTEREST CONTRACTS FOR A LOSS OF 236 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING FOR THIS NON ACTIVE DELIVERY MONTH OF JUNE IS AS FOLLOWS

1980 CONTRACTS STANDING X 5000 OZ PER CONTRACT

EQUALS

9.90 MILLION OZ

WHICH IS PRETTY GOOD !

JULY GAINED 810 CONTRACTS UP TO 111,156

AUGUST LOST 20 CONTRACTS TO 459

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1817 or 9.085 MILLION oz

CONFIRMED volume; ON THURSDAY 55,084 fair//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 1817 X5,000 oz = 9.085 MILLION oz

to which we add the difference between the open interest for the front month of JUNE (1980) AND the number of notices served upon today (1817 )x (5000 oz)

Thus the standings for silver for the JUNE 2025 contract month: (1817) Notices served so far) x 5000 oz + OI for the front month of JUNE(1980) minus number of notices served upon today (1817)x 5000 oz equals silver standing for the JUNE contract month equating to 9.900 MILLION OZ .

New total standing: 9.900 million oz which is huge for this NON active delivery month of MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 156.572million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

MAY 30 WITH GOLD DOWN $27.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.59 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 930.20 TONNES

MAY 29 WITH GOLD UP $22.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 925.71 TONNES

MAY 28 WITH GOLD DOWN $5.30 TODAY// NO CHANGES IN GOLD AT THE GLD:/ ///INVENTORY RESTS AT 925.61 TONNES

MAY 27 WITH GOLD DOWN $63.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 922.46 TONNES

MAY 23 WITH GOLD UP $69.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 923.89TONNES

MAY 22 WITH GOLD DOWN $15.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 919.88 TONNES

MAY 21 WITH GOLD UP $28.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.60 TONNES

MAY 20 WITH GOLD UP $51.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.30 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.03 TONNES

MAY 19 WITH GOLD UP $46.65 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.89 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 918.73 TONNES

MAY 16 WITH GOLD DOWN $38.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 927.62 TONNES

MAY 15 WITH GOLD UP $38.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.53 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 931.92 TONNES

MAY 14 WITH GOLD DOWN $40.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 936.51 TONNES

MAY 13 WITH GOLD UP $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 12 WITH GOLD DOWN $115.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 9 WITH GOLD UP $37.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 939.68 TONNES

MAY 8 WITH GOLD DOWN $82.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.23 TONNES OF GOLD WITHDRAWN FROM THE GLD/ ///INVENTORY RESTS AT 937.67 TONNES

MAY 7 WITH GOLD DOWN $30.30 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 937.96 TONNES

MAY 6 WITH GOLD UP $101.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 937.96 TONNES

MAY 5 WITH GOLD UP $77.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.13 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.28 TONNES

MAY 2 WITH GOLD UP $ 18.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 945.41 TONNES

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

GLD INVENTORY: 930.20 TONNES, TONIGHTS TOTAL

SILVER

MAY 30 WITH SILVER DOWN $0.36/HUGE CHANGES AT THE SLV: A DEPOSIT OF 2.773 MILLION OZ INTO THE SLV././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 29 WITH SILVER UP $0.29/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 28 WITH SILVER DOWN $0.18/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 27 WITH SILVER DOWN $0.34/HUGE CHANGES AT THE SLV//A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 23 WITH SILVER UP $0.38/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.5 MILLION OZ OF SILVER INTO THE SLV/: //INVENTORY AT SLV RESTS AT 454.375 MILLION OZ

MAY 22 WITH SILVER DOWN $0.27/NO CHANGES IN SILVER INVENTORY AT THE SLV:////: //INVENTORY AT SLV RESTS AT 451.875 MILLION OZ

MAY 21 WITH SILVER UP $0.35/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.091 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 451.875 MILLION OZ

MAY 20 WITH SILVER UP $0.65/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.41 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 449.784 MILLION OZ

MAY 19 WITH SILVER UP $0.17/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.819 MILLION OZ OUT OF THE SLV// ////: //INVENTORY AT SLV RESTS AT 447.193 MILLION OZ

MAY 16 WITH SILVER DOWN $0.24/NO CHANGES IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 15 WITH SILVER UP 0.04/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.909 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 14 WITH SILVER DOWN $0.39/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.682 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.102 MILLION OZ

MAY 13 WITH SILVER UP $0.44/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 12 WITH SILVER DOWN $0.30/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 9 WITH SILVER UP $0.31/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 8 WITH SILVER DOWN $0.16/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 7 WITH SILVER DOWN $0.54/NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 6 WITH SILVER UP $0.92 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A HUG WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 5 WITH SILVER UP $0.08 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF 0.117 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.602 MILLION OZ

MAY 2 WITH SILVER DOWN $0.19 /MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 4.545 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.424 MILLION OZ

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

CLOSING INVENTORY 459.876 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

Peter Schiff: Traders Are “Selling America”

Friday, May 30, 2025 – 02:25 PM

Via SchiffGold.com,

During his latest podcast, Peter dissects another rough stretch for American financial markets, spotlighting mounting selloffs across sectors and another breakout moment for gold. He breaks down why US treasuries are now riskier than ever, the structural problems with fiscal and monetary policy, and how tariffs are hitting American consumers harder than politicians care to admit.

The week’s headlines were dominated by red ink, but Peter points out that there’s still one clear winner:

Anyway, it was a big week in the markets and it was a bad week for US financial markets across the board. It was another ‘sell America’ week, and I think we’re going to have a lot more weeks like this one. In fact, if you remember when Trump first won and everybody was talking about the Trump trade being ‘buy America,’ I was one of the few people that said, ‘No, the Trump trade was sell America’ because I understood the ramifications of the policies that Trump would be pursuing, and the markets are reacting exactly as I had expected them to react. The star of the week was gold. Gold rose more than 5% on the week.

Peter doesn’t mince words when discussing the supposed safety of US government bonds. He urges investors to stop pretending that treasuries are a safe haven, especially given America’s ballooning obligations:

Again, as far as I’m concerned, it’s all junk bonds. If you buy U.S. treasuries, you have no chance of making any money; you will lose for sure. The only question is how you’re going to lose. You’re either going to lose because the Treasury defaults and that is a real possibility. I’d say it’s a lower possibility, although if you happen to be in China and you own U.S. treasuries, I’d say it’s a pretty high possibility. … But either the government defaults and they don’t pay you, or they pay you by printing a lot of money.

This shift in perception, from risk-free to risky, marks a fundamental change in global markets. Peter revisits how even after major geopolitical shocks, what used to be the “go-to” assets are looking shaky:

One of the most significant developments really this year is that treasuries have moved from a safe haven to a risk asset. That was evident after the Liberation Day announcement when treasuries got killed along with stocks. I’ve said this for a long time that eventually the only safe haven left standing was going to be gold. Gold is the only thing that really rallied during that initial week or so of collapse. Investors went into gold.

On the policy front, Peter calls out both major parties, arguing that regardless of who’s steering the ship, America’s debt trajectory is accelerating:

But so this big, beautiful bill not only doesn’t put us on a different course when it comes to the debt. We stay on the same course: we’ve just stepped on the gas. So we were on a path to a debt crisis and a dollar crisis. We’re staying on that path. We’re just driving faster, so we’re just going to get to that destination quicker because we elected Trump. Now, of course, had we elected Kamala Harris, I’m sure that whatever budget they’d have come up with– assuming the Democrats came in with her and she had both houses of Congress– I’m sure their deficits might have been even bigger.

The real-world impact hits consumers hardest, Peter explains, especially as tariffs bite and the dollar’s weakness amplifies the pain at the checkout counter:

Anyway, the bottom line is Walmart’s got to raise prices. Everybody’s got to raise prices. And as Trump realizes this, maybe that’s what’s happening; he realizes that it’s not external revenue. It’s internal revenue– that the people who pay the tariffs are the American consumers, especially with the weakness of the dollar. Because remember, one of the things that a lot of these so-called experts were saying was that the tariffs were going to strengthen the dollar and the stronger dollar was going to help offset the tariffs because we were going to import cheaper because of the strong dollar. Well, it has actually had the opposite effect.

For more of Peter’s analysis last week, check out the second episode of the revamped Friday Gold Wrap podcast!

MATHEW PIEPENBERG

2.ALASDAIR MACLEOD

Gold and silver remain firm

Wholesale market operators who rely on being able to roll leases on maturity face the prospect of having to buy back bullion which has simply vanished.

| Alasdair MacleodMay 30∙Paid |

In a week when the US Court of International Trade ruled that the constitution gave Congress the power to levy tariffs and not the president, gold and silver sailed on more or less regardless. In European trade this morning, gold was $3,295, unchanged from last Friday’s close. Silver was $33.17, up 12 cents. Trade was quiet in a short week due to public holidays on Monday in London and the US.

Furthermore, this week Comex June contracts were running off the board, which together with option expiry is usually a time of price weakness as traders with long positions and call options sell or abandon them respectively, resulting in sell-offs. They didn’t happen.

Judging by Comex data, gold is actually oversold with open interest the lowest it has been since February 2024.

Attempts by the shorts to shake out weak longs were futile because there aren’t any. And the stands-for-delivery continue at pace at 640.5 tonnes this year so far, an annual rate of 1,540 tonnes. It is beginning to eat into Comex stocks which have declined by over 195 tonnes since the all-time peak on 3 April — the day after Trump’s so-called liberation day:

Recall that some of that gold was extracted from the Bank of England’s vault, whose bullion stocks since October declined by 437 tonnes to end-April. We can be certain that much of this gold was leased by bullion banks from BoE central bank customers. And that this gold has been delivered into unknown hands through Comex stand-for-deliveries.

This is a radical departure from the Bank’s ledger transfer system, whereby gold remains stored at the Bank irrespective of ownership. Central banks leasing gold are now aware that gold which they have leased out has effectively disappeared with no firm guarantee that it will be replaced by the lessors when leases end.

The scale of the problem, real or imagined, is enough to persuade central banks with earmarked gold in London and New York to withdraw from all gold leasing activities. This gives both forward and futures markets a problem, because gold leasing is a major source of market liquidity.

Instead, wholesale market operators who rely on being able to roll leases on maturity face the prospect of having to buy back bullion that has simply vanished.

Doubtless, when the super-premiums on Comex triggered an arbitrage flow of over 870 tonnes into Comex warehouses from last October to April from London, Switzerland, and elsewhere the arbitrageurs thought only of the profits without the final transaction of buying back gold for paper. It really was a sucker’s trade of “you have the paper and we have the gold” variety.

Meanwhile, with no flaky longs on Comex, if that’s any guide to other markets as leases expire and the scramble to buy bullion gets underway, the backstop must be to bail out the bullion banks. The chart below illustrates the technical background, which offers no comfort to the shorts:

The chart suggests a liquidity crisis that is ongoing. And with the gold/silver ratio at 99, speculators are likely to chase silver to maximise profits as a crisis in gold paper markets unfolds. Silver’s chart is below

:

3. CHRIS POWELL AND GATA DISPATCHES

end

4/On LFTV, Andrew Maguire LIVE FROM THE VAULT 225

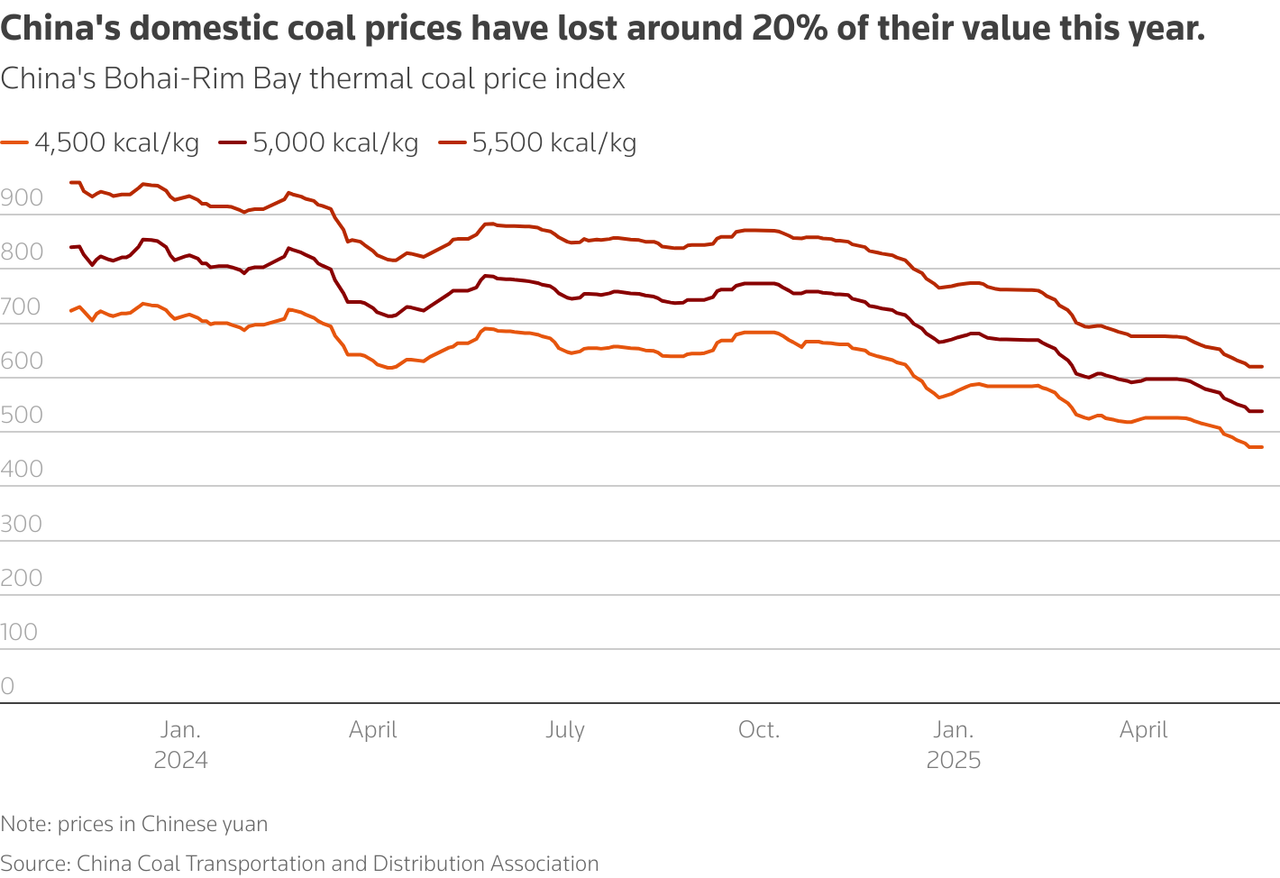

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:coal

China Drowning In Soaring Coal Inventories Amid Sinking Power Demand, Crashing Coal Pr

Thursday, May 29, 2025 – 08:30 PM

China’s overarching central planning model, meant to keep the economy from keeling over, has become so tangled up it is next to impossible to keep track of fake supply and even faker demand. It is also starting to dangerously resemble late stage USSR, when supply-side economics covered up the rot in the economy until the absolute end.

According to Reuters, with its economy slowing, if not contracting, China is pressing its coal-fired power plants to stockpile more of the fuel and import less in an effort to shore up domestic prices, but traders are skeptical the measures will help to stop the slide.

The coal industry in China faces rising coal stockpiles after a massive expansion of output following shortages and blackouts in 2021 is churning out more coal than even the world’s largest thermal power fleet can consume.

To support money-losing miners whose profits are under growing pressure, the state planner has asked power plants to prioritize domestic coal and increase thermal coal stockpiles by 10%, setting an overall target of 215 million metric tons by June 10, the sources said. However, with inventories piling up along the supply chain, the guidelines would be unlikely to spur much buying or support prices.

Mine stockpiles are up 42% from a year ago, while northern Bohai area port inventories are up 25% annually, the state-run China Energy Daily has said. Buyers are also being asked to procure coal from northern ports to chip away at high port stockpiles, three Reuters sources said.

The NDRC’s moves follow months of calls from industry groups and companies to curb coal imports and output. Chinese coal prices have marched steadily downwards, however. Prices for medium-grade coal with a heat value of 5,500 kilocalories per kilogram stood at 620 yuan ($86) per metric ton on Tuesday, the lowest since March 2021.

Prices have fallen so far that some buyers have tried to wiggle out of long-term contracts in favor of spot sales.

China imported a record 542.7 million tons of coal in 2024, but the total is expected to fall this year. Coal imports slid 16% in April on the year.

Chinese mine production continues to grow despite the collapse in prices, with a government haunted by the shortages and blackouts of 2021 and 2022 unlikely to consider output cuts.

“I think they’re very mindful to avoid a repeat of that,” said LSEG lead coal analyst Toby Hassall. “They will tolerate a period where some domestic production is really struggling.”

China’s coal production rose 6.6% on the year during the period from January to April, to stand at 1.58 billion tons. At the same time, industry profits fell 48.9% year-on-year for the same period, official data showed on Tuesday.

end

6 CRYPTOCURRENCY NEWS

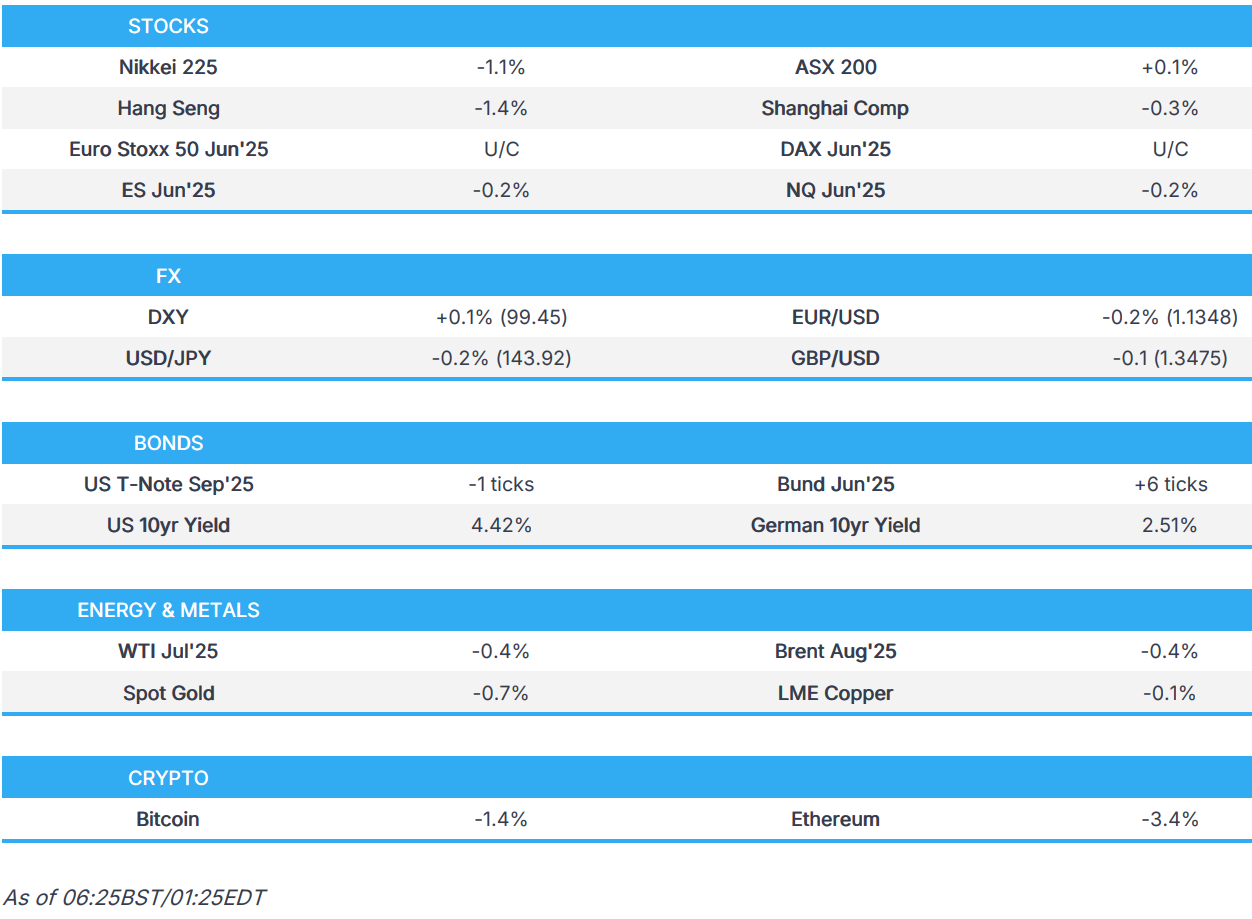

ASIAN MARKETS THIS MORNING:

SHANGHAI CLOSED DOWN 15.96 PTS OR 0.47%

//Hang Seng CLOSED DOWN 283.61 PTS OR 1.62%

// Nikkei CLOSED DOWN 467.88 PTS OR 1.22% //Australia’s all ordinaries CLOSED UP 0.26%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1960 OFFSHORE CLOSED DOWN AT 7.1990/ Oil DOWN TO 61.37 dollars per barrel for WTI and BRENT DOWN TO 63.71 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1960 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1990 AGAINST US DOLLAR/ AND THUS WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1960 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.1990 (CCP MANIPULATED)

SHANGHAI CLOSED DOWN 15.86 PTS OR 0.47%

HANG SENG CLOSED UP 296.23 PTS OR 1.27%

2. Nikkei closed DOWN 467.88 PTS OR 1.22%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 99.53// EURO RISES TO 1.1331 UP 38 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.500//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 144.09…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5260/Italian 10 Yr bond yield DOWN to 3.519 SPAIN 10 YR BOND YIELD DOWN TO 3.125%

3i Greek 10 year bond yield DOWN TO 3.276

3j Gold at $3297.50 Silver at: 33.13 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 76 /100 roubles/dollar; ROUBLE AT 78.66

3m oil into the 61 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 144.05// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.500% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8234 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9329 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.436 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.934 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.941 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 39.24

10 YR UK BOND YIELD: 4.663 DOWN 5 PTS

10 YR CANADA BOND YIELD: 3.205 DOWN 4 BASIS PTS

5 YR CANADA BOND YIELD: 2.816 DOWN 3 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

Futures Drop As Trade Pessimism Returns

Friday, May 30, 2025 – 08:22 AM

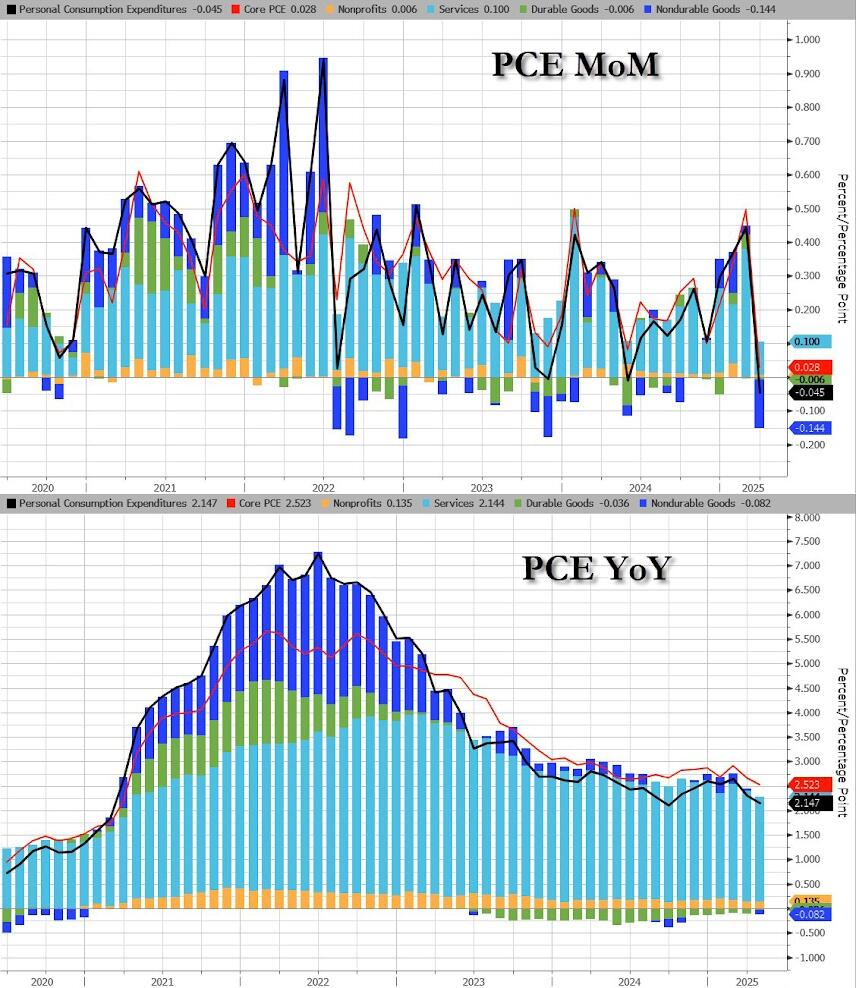

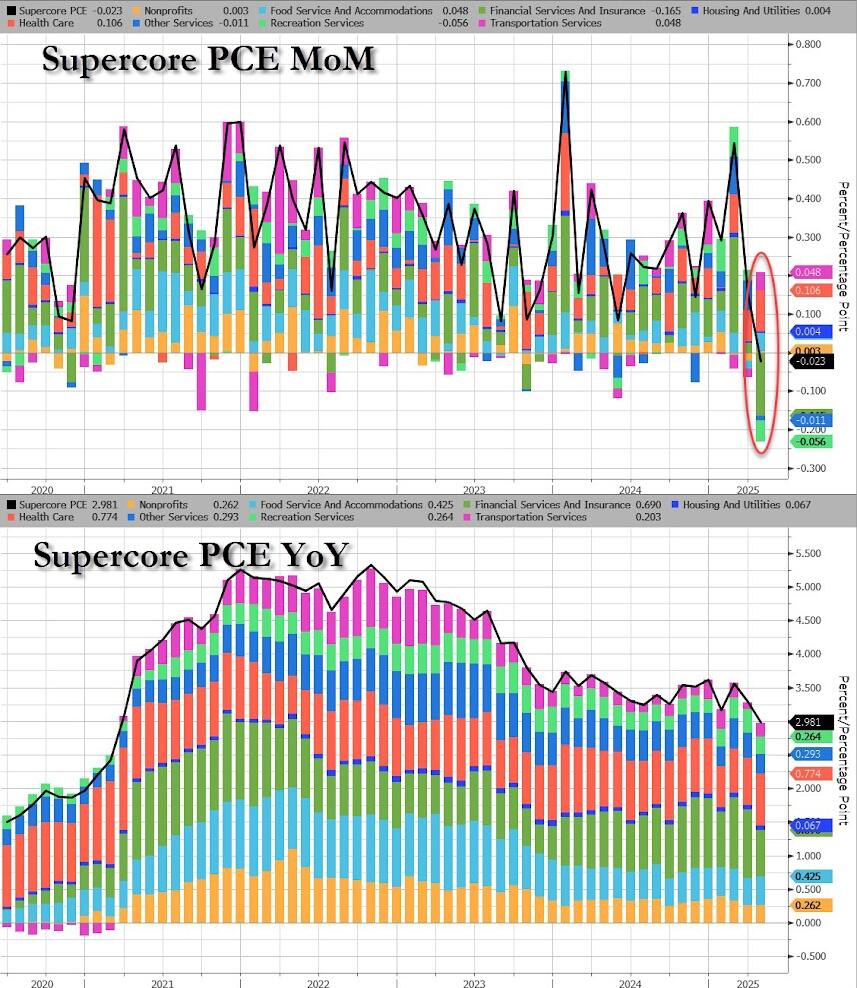

US equity futures are in the red but well off session lows, with tech leading and small caps lagging. As of 8:00am S&P futures are down -0.1% at 5,917 having earlier dropped as much as 0.5%; according to Goldman, US equities are “not reacting well” to i) “Plan B” article from the WSJ (which recaps what we said here) that “the administration is considering a stopgap effort to impose tariffs on swaths of the global economy under a never-before-used provision of the Trade Act of 1974, which includes language allowing for tariffs of up to 15% for 150 days to address trade imbalances with other countries”, and 2) a Reuters article quoting Bessent that US-China tariff talks are “a bit stalled.” Pre-market Mag 7 are mostly lower with TSLA -1.4%, NVDA -0.6% and META -0.4%. Bond yields are largely unchanged with the 10Y trading at 4.42%; the USD is modestly higher against G7 peers. Commodities are mixed with oil higher and metals lower. Today, macro focus will be on the April PCE and the final Michigan survey; tomorrow, OPEC+ will meet to decide on July output.

In premarket trading, Mag 7 stocks are flat to lower (Apple +0.1%, Alphabet +0.2%, Microsoft +0.07%, Amazon is flat, Meta -0.01%, Nvidia -0.2%, Tesla -0.8%). Gap sinks 15% after the company predicted a tariff impact of up to $300 million and revealed weakness at Banana Republic and Athleta. Here are some other notable premarket movers:

- Marvell Technology (MRVL) slips 3% after the chipmaker posted quarterly results and provided an outlook. While analysts are generally positive, they said more may have been expected given AI enthusiasm.

- NetApp (NTAP) falls 5% after the data storage provider forecast 1Q profit that missed the average analyst estimate. Bloomberg Intelligence writes that the “enterprise IT-spending environment for NetApp is proving more tepid than expected.”

- PagerDuty Inc. (PD) declines 6.2% after the software company cut its full-year revenue forecast and reported its first-quarter results. Analysts noted some execution issues in the quarter.

- Park Hotels & Resorts Inc. (PK) inches 1% lower after Truist cut its recommendation to hold, anticipating weaker tourism in Hawaii.

- UiPath (PATH) rises 13% after the automation software company provided a 2Q revenue outlook that beat estimates.

- Ulta Beauty (ULTA) jumps 8% after the cosmetics retailer boosted its earnings per share forecast for the full year.

- Zscaler (ZS) gains 3% after the software company reported third-quarter results that beat expectations and raised its full-year forecast.

Tariff headlines are once again shaping markets as unpredictability about the impact and scope of Trump’s trade agenda pushes investors to re-assess their appetite for risk. It follows a rebound in US stocks that had set the S&P 500 on track for its biggest monthly gain since 2023 before momentum began to fade on fiscal and growth concerns.

Late on Thursday, Treasury Secretary Scott Bessent said that trade talks with China were “a bit stalled.” Earlier, a federal appeals court offered Trump a temporary reprieve from a ruling that threatened to throw out the bulk of his agenda. Trump aides have insisted that the president will not be denied his tariff push and that the policies will remain, one way or another.

“The setup is quite pessimistic, whether you look at trade, fiscal outlooks, inflation, valuations, you name it,” said Dan Boardman-Weston, chief investment officer at BRI Wealth Management. “We’re keeping some cash on the sidelines as I expect volatility is here to stay for much longer.”

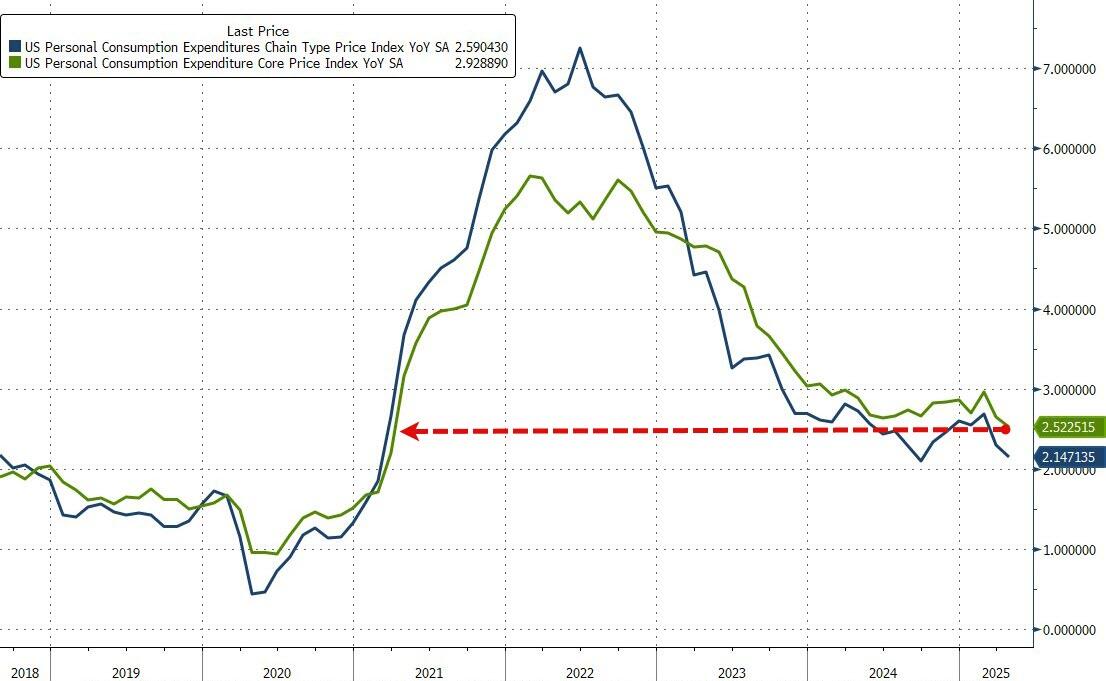

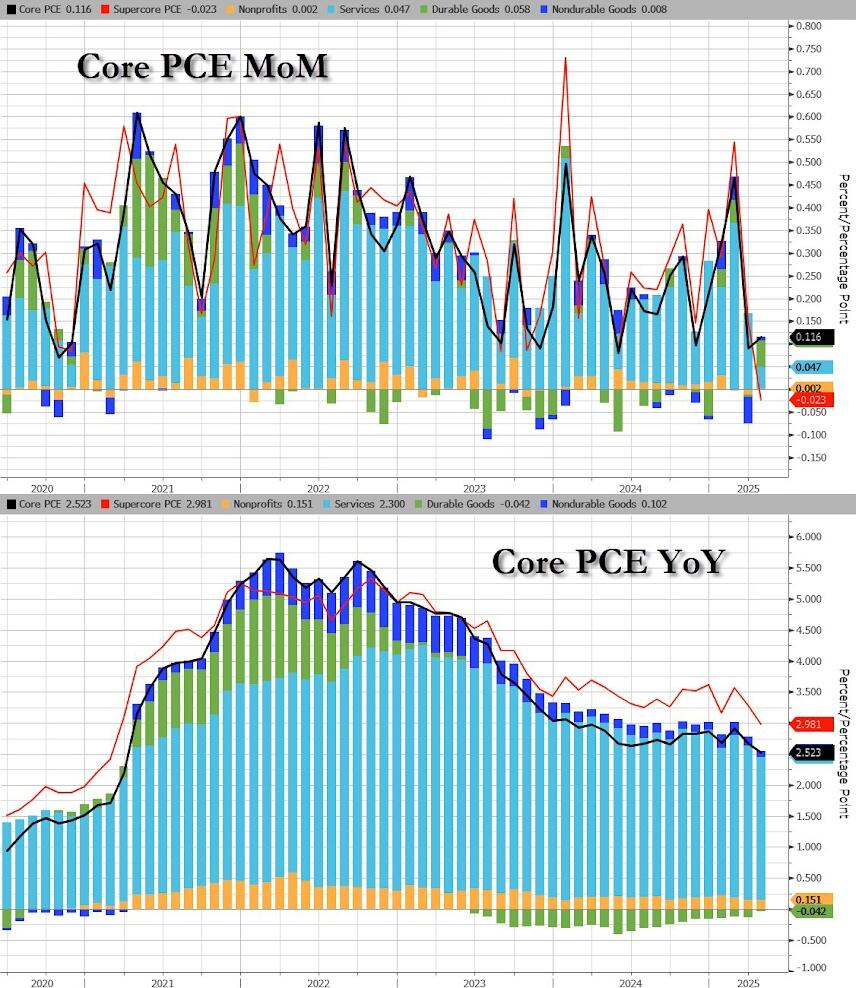

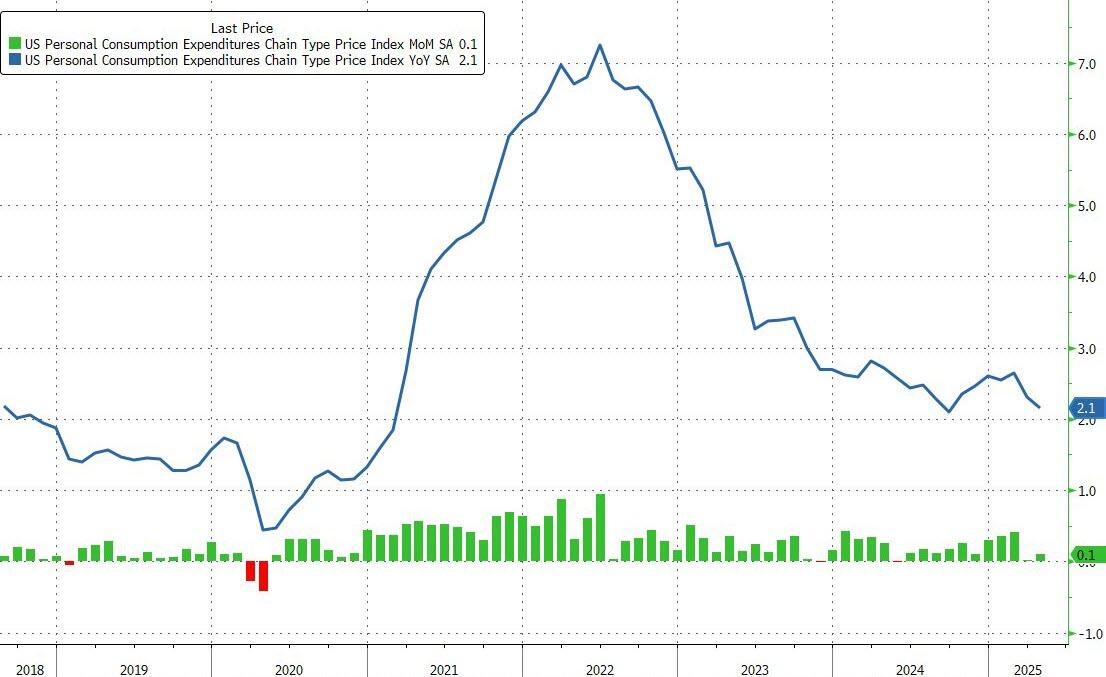

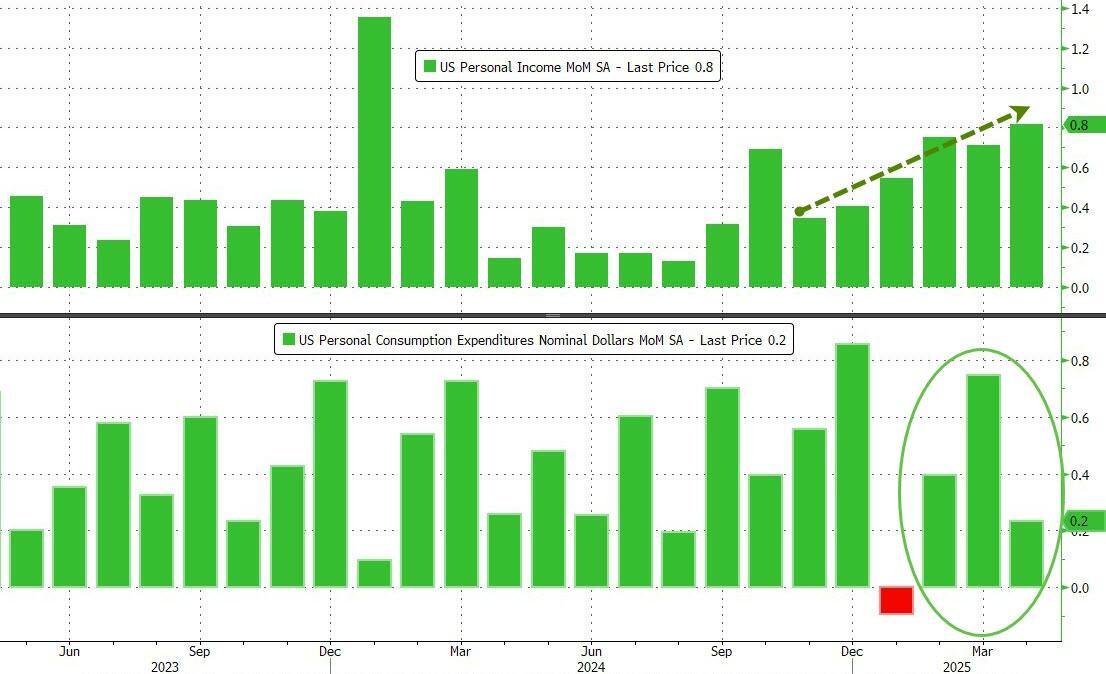

Later on Friday, traders’ focus will turn to the US core PCE, the Fed’s preferred infaltion gauge, for signals about the health of the economy and the outlook for interest-rate cuts. While the impact of Trump’s tariffs on April price data is expected to be modest, the trade-policy influence is likely to become more apparent as soon as next month. On Thursday, a report showed the US economy shrank at the start of the year due to weaker consumer spending and an even bigger impact from trade than initially reported.

Meanwhile, European stocks continued to benefit from weaker sentiment toward the US. The Stoxx 600 rose 0.6% and is on course for its best month since January as traders look past ongoing trade-related uncertainty. Financial services and utility shares are leading gains. Here are the most notable movers:

- M&G shares gain as much as 8.6% to reach the highest since June 2021, after Dai-ichi Life Holdings said it will acquire a 15% stake in the UK life insurer.

- Ovzon shares surge as much as 49% to their highest intraday level since February 2023, after the Swedish satellite communications services firm got a 1.04 billion Swedish Kroner (around €95.6 million) order from the country’s Defense Materiel Administration.

- Lindt rises as much as 1.7% as its price target was lifted to a street-high at Morgan Stanley, which says the Swiss chocolate maker’s premium valuation multiple can be supported at current levels.

- Beazley and Hiscox shares edge higher after Berenberg re-initiated coverage on the UK insurers with buy ratings and new Street-high price targets, describing the firms as a “compelling investment case.”

- Sanofi shares drop as much as 6.1%, after just one of two late-stage studies evaluating the experimental drug itepekimab in former smokers with inadequately controlled chronic obstructive pulmonary disease (COPD) met the primary endpoint.

- hVIVO shares plummet as much as 58%, slumping to a five-year low, after the company warned a significant contract has been canceled due to uncertainties in the pharmaceutical industry.

- Elekta shares fall as much as 5.3% after Morgan Stanley cut its price target on the Swedish medical equipment firm, noting that weak orders growth “cancelled out” better-than-expected earnings.

Earlier in the session, Asian stocks declined, though are still on track for its best month since November 2023, led by losses in Hong Kong after Donald Trump’s tariff agenda received a temporary reprieve. The MSCI Asia Pacific Index fell as much as 0.7%, paring its gain for May to 4.7%. Alibaba and Tencent were among the biggest drags Friday, as US Treasury Secretary Scott Bessent’s comment on “stalled” trade talks with China also weighed on the market. The measure is set for its first weekly loss since early April as the Trump administration’s back-and-forth moves fan uncertainty. Despite the weakness, the key Asian stock gauge was set to cap its first set of back-to-back monthly gains of the year on continued inflows from global funds as they trade on the “sell America” theme.

In FX, the Bloomberg Dollar Spot Index rose 0.2% but remained on track for its longest streak of monthly losses in five years. Traders’ concern that Trump’s trade policies could undermine the economy is adding to the greenback’s weakness and eroding its appeal as a traditional haven. The yen is the best performing G-10 currency, rising 0.1% against the greenback after prices in Tokyo jumped the most in two years.

“No matter what happens, markets realize that we are facing a long period of uncertainty,” said Win Thin, global head of markets strategy at Brown Brothers Harriman & Co. “Allowing tariffs to remain in place raises risks of stagflation and is both dollar and equity negative.”