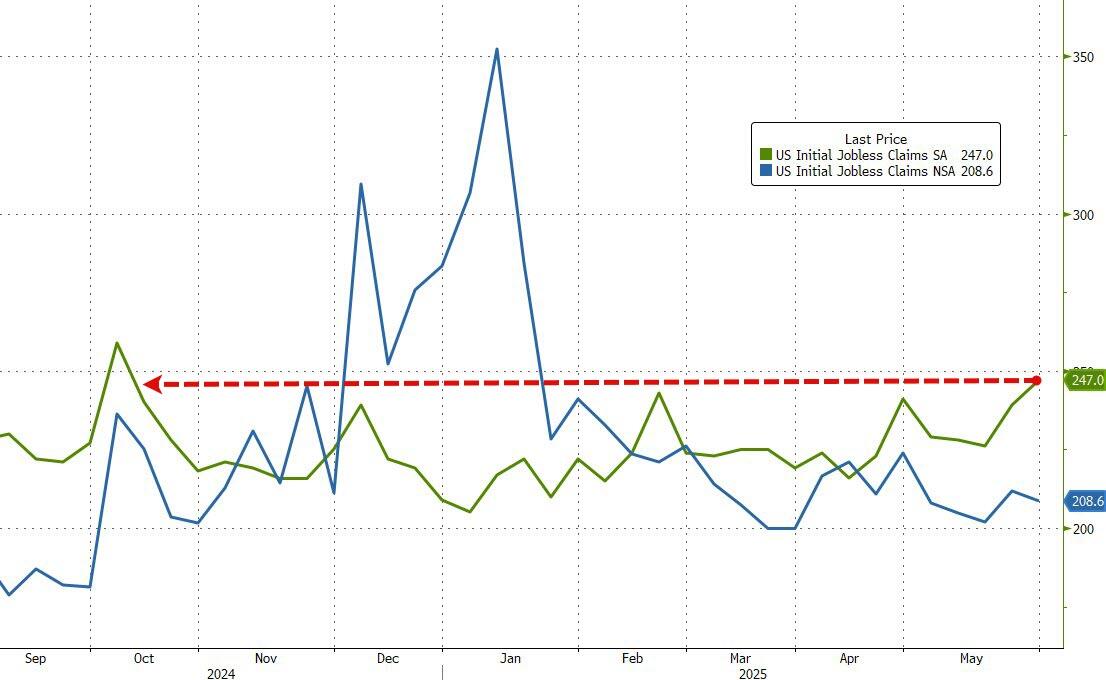

JUNE 5/SILVER FINALLY BREAKS OUT OF ITS SHACKLES RISING $1.14 AFTER FINALLY PIERCING THROUGH THE $34.40-$34.50 BARRIER//GOLD HOWEVER FALLS VICTIM TO ANOTHER ATTACK BY OUR BANKER FRIENDS SETTLING DOWN $23.10 TO $3352.20//PLATINUM CONTINUES TO HAVE STELLAR DAYS RISING ANOTHER $43.80 TO $1140.03 WHILE PALLADIUM ROSE ONLY %5.45 TO $1009.05//GOLD COMMENTARY TONIGHT FROM NICK GIAMBRUNO//TRUMP HAS A PHONE CALL FROM XI AND THAT IGNITES ALL MARKETS//CHINA CONTINUES TO BLOCK ALL EXPORTS OF RARE EARTHS TO EUROPE AND THE USA//GERMAN ECONOMY CONTINUES TO FALTER//ECB LOWERS ITS INTEREST RATE BY 25 BASIS POINTS///ISRAEL VS HAMAS UPDATES //RUSSIA VS UKRAINE UPDATES/COVID UPDATES/COVID VACCINE INJURY REPORTS//NEWS ADDICTS/EVOL NEWS/MARK CRISPIN MILLER/ PAUL ALEXANDER//USA DEFICIT SHRINKS BY THE GREATEST AMOUNT SINCE 2008 DUE TO LOWER IMPORTS//JOBLESS CLAIMS RISE//MUSK GOES BALLISTIC ON TRUMPS BBB BILL//OTHER IMPORTANT USA NEWS//SWAMP STORIES FOR YOU TONIGHT//

072 C GOLDMAN 4 099 H DEUTSCHE BANK AG 545 104 C MIZUHO SECURITIES US 2 118 C MACQUARIE FUTURES US 243 132 C SG AMERICAS 13 190 H BMO CAPITAL MARKETS 73 323 C HSBC 170 332 H STANDARD CHARTERED B 172 363 H WELLS FARGO SECURITI 151 435 H SCOTIA CAPITAL (USA) 32 555 C BNP PARIBAS SEC CORP 28 624 H BOFA SECURITIES 1565 661 C JP MORGAN SECURITIES 372 1037 690 C ABN AMRO CLR USA LLC 5 12 709 C BARCLAYS 41 905 C ADM 24 11

TOTAL: 2,250 2,250 MONTH TO DATE: 21,411

JPMORGAN STOPPED 1037//2250

JUNE

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024: 2250 CONTRACTs NOTICES FOR 225,000 OZ or 6.998 TONNES

total notices so far: 21,411 contracts for 2141,100 OR 66.597 tonnes)

FOR JUNE

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 120 NOTICE(S) FILED FOR 600,000 OZ/

total number of notices filed so far this month : 2415 CONTRACTS (NOTICES) for 12.075 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $23.10 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 935.65 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $1.14 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: //A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV// THIS WILL BE A HUGE DERIVATIVE MESS

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 467.869 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 2705 CONTRACTS TO 166,052 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0.01 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A MEGA HUGE SIZED GAIN OF 2,955 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A 250 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD SOME LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING WITH RESPECT TO WEDNESDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON WEDNESDAY WITH SILVER’S SLIGHT LOSS IN PRICE YESTERDAY, TODAY THE PRICE IS NOW MILES ABOVE THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE TRADING AT 35.68. . BUT THIS WAS COUPLED WITH ANOTHER HUGE T.A.S. ISSUANCE OF 684 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING WELL OVER THE 34.40 DOLLAR MARK!!. WE HAD A FAIR 250 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE 684 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUGE SIZED 2955 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $0.01.

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 AND FAILED . THE PRICE IS NOW $35.67 AS WE HEAD FOR THE ALL TIME HIGH OF $50.00

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE 684 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.01) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE GAIN OF 3090 CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A 250 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 9.90 MILLION OZ FOLLOWED BY TODAY’S 750,000 OZ QUEUE JUMP//NEW TOTAL STANDING 12.985 MILLION OZ!!

THUS:

INITIAL STANDING FOR JUNE: 9.90 MILLION OZ PLUS TODAY’S 750,000 OZ QUEUE JUMP = 12.985 MILLION OZ.

WE HAD:

/ HUGE COMEX OI GAIN+// A 250 SIZED EFP ISSUANCE (/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 684 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A SMALL 136 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 4 DAY(S), total 3070 contracts: OR 15.35 MILLION OZ (830 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 15.35 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 15.35 MILLION OZ (NOTICE EFP ISSUANCE GETTING SMALLER AND SMALLER AS CENTRAL BANKS EXERCISE THESE AND TAKE DELIVERY)

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2955 CONTRACTS DESPITE OUR LOSS IN PRICE OF $0.01 IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. . THE CME NOTIFIED US THAT WE HAD A 250 CONTRACT EFP ISSUANCE CONTRACTS: 250 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY REDUCES TO: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND NOW JUNE: INITIAL 9.90 MILLION OZ PLUS 750,000 OZ EFP TRANSFER TO LONDON = 12.985 MILLION OZ

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (684 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TODAY’S TRADING (THURSDAY TRADING) AND BEYOND.

WE HAD 120 NOTICE(S) FILED TODAY FOR 600,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1313 OI CONTRACTS TO 417,254 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE AN EXTREMELY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A MONSTER 3964 CONTRACTS //.

WE HAD A FAIR SIZED INCREASE IN COMEX OI (1313 CONTRACTS) . THIS OCCURRED WITH OUR HUGE GAIN OF $22.30 IN PRICE// WEDNESDAY///.

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH

/ WE HAD A $22.30 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX ///. WE HAD A FAIR SIZED GAIN OF 2443 OI CONTRACTS (7.98 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE DURING THE FIRST THREE WEEKS OF MAY, AND THROUGHOUT EACH AND EVERY DAY MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A SMALLER THAN EXPECTED INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE JUNE CONTRACT MONTH….. A SMALLISH 62.534 TONNES TO WHICH WE SUBTRACT TODAY’S SMALL .1241 TONNES OF EFP TRANSFER TO LONDON //NEW STANDING LOWERS TO 72.712 TONNES!!. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1130 CONTRACT:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 417,254/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 166,052 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2443 CONTRACTS WITH 1313 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 1130 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2443 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 399 CONTRACTS

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS 1130 CONTRACT) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 1313 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2443 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) WEAK INITIAL STANDING FOR GOLD FOR JUNE AT 62.524TONNES FOLLOWED BY TODAY’S SMALL 0.1241 TONNES EXCHANGE FOR PHYSICAL JUMPING TO LONDON//NEW STANDING REDUCES TO 72.712 TONNES./

NEW STANDING FOR GOLD, JUNE CONTRACT AT 72.839 TONNES OF GOLD.

.

/ 3) LITTLE T.A.S. LIQUIDATION , AS WE HAD 1)A $22.30 COMEX PRICE GAIN.. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THAT HUGE GAIN IN PRICE AS WE HAD A STRONG GAIN OF 5937 CONTRACTS ON OUR TWO EXCHANGES // /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY BUT SMALLER FOR JUNE!

4) FAIR SIZED COMEX OI GAIN// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (1130 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 399 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

JUNE INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 8593 CONTRACTS OR 859,300 OZ OR 26.72 TONNES IN 4 TRADING DAY(S) AND THUS AVERAGING: 2148 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN4 TRADING DAY(S) IN TONNES 26.72 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 26.72 TONNES DIVIDED BY 3550 x 100% TONNES = 0.760% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 26.72 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

SPREADING OPERATIONS

/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 2705 CONTRACTS OI TO 166,052 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 250 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2841 CONTRACTS AND ADD TO THE 250 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2955 CONTRACTS DESPITE THE LOSS IN PRICE OF $0.01 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 15.45 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS MORNING:

SHANGHAI CLOSED UP 7.90 PTS OR 0.23%

//Hang Seng CLOSED UP 252,94 PTS OR 1.07%

// Nikkei CLOSED DOWN 192.96 PTS OR 0.51% //Australia’s all ordinaries CLOSED DOWN 0.02%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1799 OFFSHORE CLOSED UP AT 7.1754/ Oil DOWN TO 63.02 dollars per barrel for WTI and BRENT UP TO 65,11 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1788 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1754 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1313 CONTRACTS TO A STILL LOW NUMBER OF 417,254 OI WITH OUR STRONG GAIN IN PRICE OF $22.30 WITH RESPECT TO WEDNESDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1130 ). WE HAD CONSIDERABLE T.A.S. LIQUIDATION WHICH ACCOUNTS FOR THE PRICE LOSS.

THE CME ANNOUNCED WEDNESDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES. TOTAL ISSUANCE FOR MAY WAS RECORDED AT 9.591 TONNES OF GOLD AND THIS TOTAL WAS ADDED TO OUR NORMAL DELIVERIES. THE BANK OF ENGLAND MUST BE GETTING QUITE ANTSY OF GETTING ITS GOLD BACK.

IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST FIVE MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED SO FAR!!

DETAILS ON JUNE COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 2445 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF MAY, AND JUNE CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS SMALL AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 339 T.A.S.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , INITIAL STANDING IS RECORDED AT 62.534 TONNES PLUS TODAY’S 0.1241 TONNES EXCHANGE FOR PHYSICAL TRANSFER TO LONDON = 72.712 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL QUEUE JUMPING FOR THE MONTH LOWERS TO: 10.1809 TONNES.

NEW TOTAL TONNES STANDING JUNE: 72.712 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 5+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 225 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1130 EFP CONTRACT WAS ISSUED: : /AUGUST 1130 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1130 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

WE HAD :

CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS

ZERO NET SPEC LIQUIDATION DESPITE OUR HUGE LOSS IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY MORNING//WEDNESDAY NIGHT WAS A SMALL SIZED, 399 CONTRACTS.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL MAY AND JUNE

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.THIS WAS SURELY IN EVIDENCE IN TRADING TUESDAY WITH THE LOSS IN OI

STANDING LAST 6 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: INITITAL STANDING 62.534 TONNES MINUS .1241 TONNES EFP TRANSFER TO LONDON/TODAY = 72.712 TONNES (0 EX FOR RISK) TOTAL QUEUE JUMPS FOR THE MONTH OF JUNE EQUALS 10.1809 TONNES. THIS IS CENTRAL BANKS STANDING FOR PHYSICAL GOLD!!

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING/JUNE CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $22.30/ /) AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD LITTLE T.A.S. SPREADER LIQUIDATION ////WEDNESDAY AS THEY ARE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE THE MAGIC $3,400 BARRIER AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING

THURSDAY MORNING/WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JUNE TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

ANALYSIS JUNE DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JUNE COMEX CONTRACT

WE HAVE GAINED A STRONG SIZED TOTAL OF 7.598 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE FIRST RECORDED AT 62.534 TONNES ON FIRST DAY NOTICE/MAY 30. TO THIS WE SUBTRACT WEDNESDAY NIGHT’S SMALL EFP TRANSFER OF 4100 OZ OR 0.1275 TONNES OF GOLD//NEW STANDING FOR JUNE GOLD LOWERS TO 72.712.

ALL OF THIS QUITE SMALL STANDING FOR JUNE WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $22.30

WE HAD A MONSTER 3964 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 2443 CONTRACTS OR 244300 0Z (7.598 TONNES)

confirmed volume WEDNESDAY 175,434. contracts: small volume////

Total monthly oz gold served (contracts) so far this month

21,411 notices 2,141,100 oz 66.597 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 0 customer entries

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: 0 entry

adjustments: 3//

a) Brinks 53,208.910 OZ (1655 kilobars) totally removed from brinks customer

b) Out of JPMorgan: 23,789.378 oz (dealer to customer)

c) out of Manfra: 45,332.330 oz 1410 kilobars (dealer to customer)

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JUNE STANDS AT 4216 CONTRACTS FOR A LOSS OF 1018 CONTRACTS. WE HAD 977 CONTRACTS SERVED ON WEDNESDAY SO WE LOST 41 CONTRACTS FOR 4100 OZ OR 0.1275 TONNES OF GOLD UNDERWENT A EXCHANGE FOR PHYSICAL TRANSFER WHERE THESE BOYS DECIDED TO TAKE IMMEDIATE DELIVERY OVER IN LONDON THIS TOTAL WILL BE SUBTRACTED TO OUR INITIAL AMOUNT OF GOLD STANDING AT 62.534 TONNES//NEW STANDING LOWERS TO 72.712 TONNES

JULY LOST 13 CONTRACTS TO STAND AT 6799

AUGUST GAINED 1524 CONTRACTS UP TO 322,266

We had 2250 contracts filed for today representing 225,000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 372 notices issued from their client or customer account. The total of all issuance by all participants equate to 2250 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1037 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE /2025. contract month, we take the total number of notices filed so far for the month (21,411 X 100 oz ) to which we add the difference between the open interest for the front month of JUNE (4216 CONTRACTS) minus the number of notices served upon today (2250 x 100 oz per contract) equals 2,337,700 OZ OR 72.712 TONNES to which we add 0 tonnes of gold issued under exchange for risk// total standing 72.712 tonnes

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (21,411 x 100 oz +we add the difference for front month of JUNE (4216 OI} minus the number of notices served upon today (2250 x 100 oz) which equals 2,337,700 OZ OR 72.712 TONNES + 0 tonnes EX FOR RISK = 72.712 tonnes

TOTAL COMEX GOLD STANDING FOR JUNE.: 72.712 TONNES WHICH IS SMALL FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..JUNE DID NOT FOLLOW FEB AND APRIL’S LEAD!!

i) Out of CNT 59,957.366 oz ii) Out of HSBC 370,426.280 oz

total withdrawal 430,383.646 oz

ADJUSTMENTs 0

JPMorgan has a total silver weight: 214.825million oz/495.544 oz million or 43.23%

TOTAL REGISTERED SILVER: 158.995 MILLION OZ//.TOTAL REG + ELIGIBLE. 495.544 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2025 OI: 302 OPEN INTEREST CONTRACTS FOR A GAIN OF 147 CONTRACTS. WE HAD 3 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 150 CONTRACTS OR 750,000 OZ UNDERWENT A HUGE QUEUE JUMP IN ORDER TO TAKE DELIVERY OF PHYSICAL SILVER OVER ON THIS SIDE OF THE POND.

JULY LOST 711 CONTRACTS DOWN TO 117,515

AUGUST GAINED 37 CONTRACTS TO 482

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 120 or 600,000 oz

CONFIRMED volume; ON WEDNESDAY 59,710 good//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 2415 X5,000 oz = 12.075 MILLION oz

to which we add the difference between the open interest for the front month of JUNE (302) AND the number of notices served upon today (120 )x (5000 oz)

Thus the standings for silver for the JUNE 2025 contract month: (2415) Notices served so far) x 5000 oz + OI for the front month of JUNE(302) minus number of notices served upon today (120)x 5000 oz equals silver standing for the JUNE contract month equating to 12.985 MILLION OZ .

New total standing: 12.985 million oz which is huge for this NON active delivery month of JUNE.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 158.995million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

JUNE 2 WITH GOLD UP $80.90 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 930.20 TONNES

MAY 30 WITH GOLD DOWN $27.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.59 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 930.20 TONNES

MAY 29 WITH GOLD UP $22.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 925.71 TONNES

MAY 28 WITH GOLD DOWN $5.30 TODAY// NO CHANGES IN GOLD AT THE GLD:/ ///INVENTORY RESTS AT 925.61 TONNES

MAY 27 WITH GOLD DOWN $63.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 922.46 TONNES

MAY 23 WITH GOLD UP $69.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 923.89TONNES

MAY 22 WITH GOLD DOWN $15.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 919.88 TONNES

MAY 21 WITH GOLD UP $28.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.60 TONNES

MAY 20 WITH GOLD UP $51.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.30 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.03 TONNES

MAY 19 WITH GOLD UP $46.65 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.89 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 918.73 TONNES

MAY 16 WITH GOLD DOWN $38.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 927.62 TONNES

MAY 15 WITH GOLD UP $38.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.53 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 931.92 TONNES

MAY 14 WITH GOLD DOWN $40.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 936.51 TONNES

MAY 13 WITH GOLD UP $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 12 WITH GOLD DOWN $115.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 937.94 TONNES

MAY 9 WITH GOLD UP $37.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 939.68 TONNES

MAY 8 WITH GOLD DOWN $82.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.23 TONNES OF GOLD WITHDRAWN FROM THE GLD/ ///INVENTORY RESTS AT 937.67 TONNES

MAY 7 WITH GOLD DOWN $30.30 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 937.96 TONNES

MAY 6 WITH GOLD UP $101.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 937.96 TONNES

MAY 5 WITH GOLD UP $77.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.13 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.28 TONNES

MAY 2 WITH GOLD UP $ 18.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 945.41 TONNES

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

GLD INVENTORY: 935.65 TONNES, TONIGHTS TOTAL

SILVER

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

JUNE 2 WITH SILVER UP $1.58/NO CHANGES AT THE SLV: ././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 30 WITH SILVER DOWN $0.36/HUGE CHANGES AT THE SLV: A DEPOSIT OF 2.773 MILLION OZ INTO THE SLV././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 29 WITH SILVER UP $0.29/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 28 WITH SILVER DOWN $0.18/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 27 WITH SILVER DOWN $0.34/HUGE CHANGES AT THE SLV//A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 23 WITH SILVER UP $0.38/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.5 MILLION OZ OF SILVER INTO THE SLV/: //INVENTORY AT SLV RESTS AT 454.375 MILLION OZ

MAY 22 WITH SILVER DOWN $0.27/NO CHANGES IN SILVER INVENTORY AT THE SLV:////: //INVENTORY AT SLV RESTS AT 451.875 MILLION OZ

MAY 21 WITH SILVER UP $0.35/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.091 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 451.875 MILLION OZ

MAY 20 WITH SILVER UP $0.65/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.41 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 449.784 MILLION OZ

MAY 19 WITH SILVER UP $0.17/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.819 MILLION OZ OUT OF THE SLV// ////: //INVENTORY AT SLV RESTS AT 447.193 MILLION OZ

MAY 16 WITH SILVER DOWN $0.24/NO CHANGES IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 15 WITH SILVER UP 0.04/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.909 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 14 WITH SILVER DOWN $0.39/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.682 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.102 MILLION OZ

MAY 13 WITH SILVER UP $0.44/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 12 WITH SILVER DOWN $0.30/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.001 MILLION OZ INTO SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.7845 MILLION OZ

MAY 9 WITH SILVER UP $0.31/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 8 WITH SILVER DOWN $0.16/NO CHANGES IN SILVER INVENTORY AT THE SLV:NO CHANGE IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 7 WITH SILVER DOWN $0.54/NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 6 WITH SILVER UP $0.92 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A HUG WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 5 WITH SILVER UP $0.08 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF 0.117 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.602 MILLION OZ

MAY 2 WITH SILVER DOWN $0.19 /MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 4.545 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.424 MILLION OZ

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

CLOSING INVENTORY 467.869 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

MATHEW PIEPENBERG

2.ALASDAIR MACLEOD

NICK GIAMBRUNO

The Next Gold Confiscation: What It Could Look Like… And How To Avoid It

On April 5, 1933, under the pretext of a national emergency, President Franklin D. Roosevelt issued Executive Order 6102, making it illegal for US citizens to own gold.

The decree forced Americans to sell their gold to the government at an artificially low “official price.” If they refused, they faced harsh penalties: a $10,000 fine (over $200,000 in today’s debased dollars) and/or up to 10 years in prison.

It was blatant theft—a sweeping confiscation of wealth from the American people.

Today, many fear the US government could resort to gold confiscation again if it becomes desperate enough.

And honestly, those fears aren’t misplaced.

The government’s financial situation is rapidly deteriorating.

But would it really attempt another 1933-style gold grab?

I don’t think so.

What’s More Likely Than Outright Confiscation

Here’s the reality: only a tiny fraction of Americans own gold today.

I’d wager most have never even seen a gold coin, let alone understand its value.

Back in 1933, things were different. The US was still operating under a version of the gold standard, and gold was much more widely held. Today, a repeat of that playbook just isn’t worth the effort.

If the government wants to steal wealth, it doesn’t need to knock on your door. It can do it quietly and continuously—by printing money and debasing the currency. It’s the stealthy way to confiscate from savers.

But gold owners shouldn’t feel too comfortable.

I believe the next threat will come in a new form—not outright confiscation, but through a punitive windfall-profits tax on gold. And that could be even more dangerous.

The Coming “Fair Share” Gold Tax

There’s precedent for this. In 1980, Congress passed the Crude Oil Windfall Profit Tax Act, which levied up to 70% on so-called “windfall profits” from domestic oil producers.

And what exactly is a “windfall profit”?

As far as I can tell, it’s whatever politicians say it is. There’s no real definition—just a politically convenient excuse for legalized plunder.

In essence, a windfall profit is simply a profit the government doesn’t like.

So imagine this: gold explodes in price due to a currency crisis. Congress rushes in to “protect the people” and passes something like the Fair Share Gold Windfall Profit Tax Act, slapping on a tax of 70% or more on any gold profits.

How to Protect Yourself

The good news? There are practical steps you can take to avoid this kind of expropriation.

Sure, you could renounce your US citizenship. But let’s be honest—that’s a drastic move and not realistic for most people.

Thankfully, there’s a far more practical solution. You can do it right from your living room.

Own gold in a Roth IRA.

A Roth IRA is a tax-free zone. You contribute with after-tax dollars, and any future capital gains or income from your investments grow tax-free. Best of all, withdrawals in retirement are tax-free, too.

And while there are no guarantees when it comes to future legislation, investments held in a Roth IRA are far less likely to be targeted by a windfall-profits tax—especially one aimed at gold.

It’s a simple move that makes you a hard target.

So how do you actually do this—and protect your gold from the threats ahead?

That’s exactly why I just released a brand-new video with legendary gold investor Doug Casey. In it, he reveals his time-tested strategies for safeguarding your gold from inflation, bank failures, capital controls—and even government confiscation. Doug Casey Reveals the Best Way to Store Your Gold Click here to watch it and protect your savings before it’s too late.

end

Precious Metals Go Vertical: Silver Leads, Platinum Awakens

Massive break out in the weekly silver chart. Do not forget to roll those SLV call spreads (outlined here) dynamically in order to capture max optionality.

Source: LSEG Workspace

Precious gap

As we pointed out earlier this week: imagine silver closes just a little part of that gap…

Source: LSEG Workspace

Room to chase

Silver net non commercials have missed the last move higher in silver. Chase set up is big.

Source: LSEG Workspace

CTAs in silver

Room to chase…

Source: Mentor Q

S(A)ilver

The AI narrative has made a strong comeback, and you need silver to run those AI machines…

Source: LSEG Workspace

Silver seasonality

Maybe silver is just front running the seasonality chart by a few weeks…

Source: Equity Clock

More precious

Beyond the silver break out…Platinum awakening big time. A close slightly higher and things could get very dynamic to the upside. Recall what GS pointed out in late May: “…slowing electric vehicle adoption could keep diesel car usage higher, spurring demand for Platinum in catalytic converters”.

Congratulations, gold bugs, your long, painful wait is ending. The following chart shows the three-year rolling average annualized returns for stocks, bonds, and gold, with the latter now winning.

Gold is holding its gains even as it moves into its seasonally weakest stretch. No “sell and May and go away” so far.

This is great news for gold miners, which are seeing their revenues outpace their costs, dramatically widening their profit margins. Note that the next chart is a bit outdated. With gold at $3,300/oz, current margins are actually a lot wider.

Wider margins mean more cash flow, which in turn means higher capital spending. The miners underinvested during gold’s long doldrums, and now have to catch up by finding and/or buying more ounces in the ground.

A growing share of this capex will be in the form of M&A, as big miners buy smaller ones at ever-more-favorable premiums. Check out the recent gains seen by our Portfolio stocks.

What About Silver?

The gold/silver ratio (the number of silver ounces required to buy one ounce of gold) peaked recently at a historically crazy-high 105. Normally, a reading above 90 is a sign that silver is about to outperform gold (i.e., the gold/silver ratio declines). And that’s starting to happen, as silver tests resistance at $35/oz.

What’s Driving the Precious Metals Bull Market?

Central banks have been aggressive buyers of gold for the past few years, which accounts for the steady price increase.

Wall Street, meanwhile, has suddenly discovered precious metals. From Katusa Research:

Wall Street Just Placed a Massive Gold Bet—And Retail Has No Idea.

$75 BILLION just flooded into gold funds—that’s 3X higher than any crisis before. When institutional money moves this fast, this violently, they’re not speculating. They’re positioning.

This run, in short, compares favorably with the previous two precious metals bull markets (in the 1970s and 2000s), when the well-positioned made life-changing money.

end

4/On LFTV, Andrew Maguire LIVE FROM THE VAULT 225

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:ALUMINIUM AND STEEL

6 CRYPTOCURRENCY NEWS

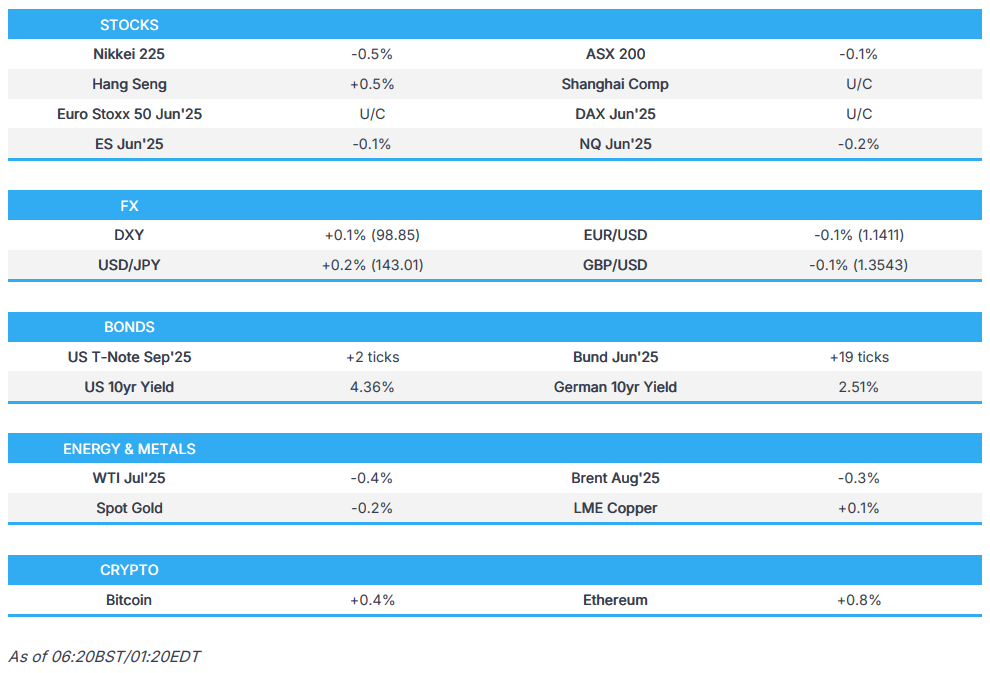

ASIAN MARKETS THIS MORNING:

SHANGHAI CLOSED UP 7.90 PTS OR 0.23%

//Hang Seng CLOSED UP 252,94 PTS OR 1.07%

// Nikkei CLOSED DOWN 192.96 PTS OR 0.51% //Australia’s all ordinaries CLOSED DOWN 0.02%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1799 OFFSHORE CLOSED UP AT 7.1754/ Oil DOWN TO 63.02 dollars per barrel for WTI and BRENT UP TO 65,11 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1788 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1754 AGAINST US DOLLAR/ AND THUS STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1799 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.1954 (CCP MANIPULATED)

SHANGHAI CLOSED UP 7.90 PTS OR 0.23%

HANG SENG CLOSED UP 252.94 PTS OR 1.07%

2. Nikkei closed DOWN 192.96 PTS OR 0.51%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 98,72// EURO RISES TO 1.1424 UP 4 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.472//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 144.15…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4890/Italian 10 Yr bond yield DOWN to 3.456 SPAIN 10 YR BOND YIELD DOWN TO 3.083%

3i Greek 10 year bond yield DOWN TO 3.241

3j Gold at $3394.00 Silver at: 35.69 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 33 /100 roubles/dollar; ROUBLE AT 78.91

3m oil into the 63 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.15// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.472% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8195 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9362 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.351 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.863 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.883 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 39.35

10 YR UK BOND YIELD: 4.5910 DOWN 7 PTS

10 YR CANADA BOND YIELD: 3.236 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.860 UP 1 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

US Equity Futures Unchanged Ahead Of ECB As Jobs Data Looms

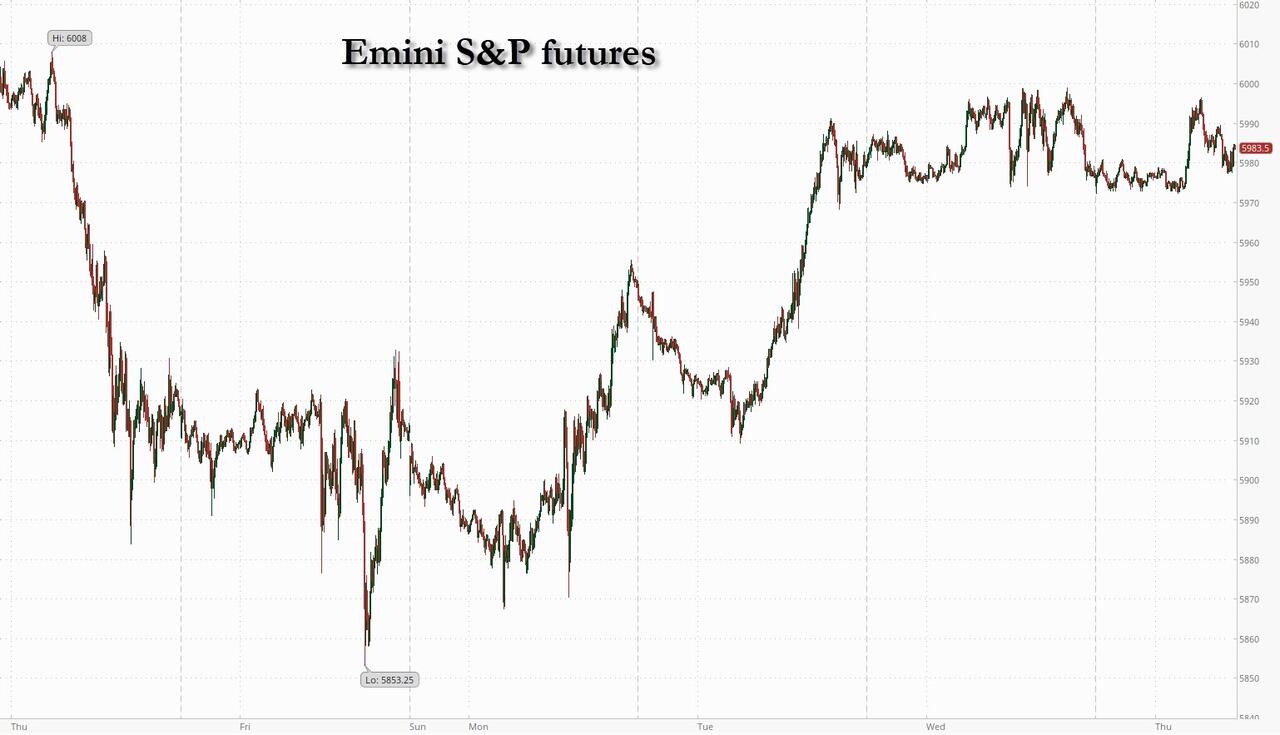

Thursday, Jun 05, 2025 – 08:15 AM

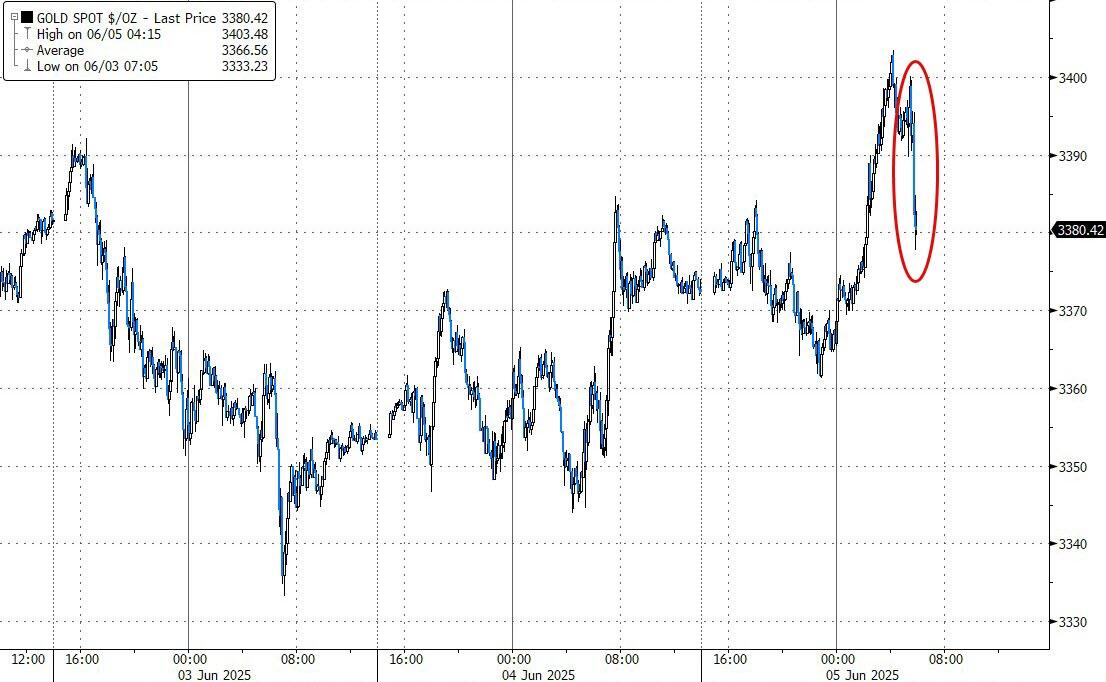

US equity futures are unchanged, as they struggle for direction ahead of Friday’s payrolls report, following a series of data releases that offered mixed signals on the health of the economy. As of 8:00am, S&P futures are flat, having traded on either side of the unchanged line during the overnight session and followed a slurry of weak macro data releases which saw Wednesday’s gains erase and recover, with the S&P ultimately ending the day flat. Nasdaq 100 futs are down 0.1% with Mag 7 stocks mostly higher except for TSLA (-1.6%). Stocks and bonds in Europe gained ahead of the ECB’s expected 8th consecutive interest rate cut. The yield on 10-year US Treasuries steadied as Wednesday’s bond rally faded. The dollar reversed earlier losses even as gold surged to briefly top $3400. Commodities are mostly mixed with notable outperformance in silver (+3.1%). News flow since yesterday’s close has been largely muted: headlines continue to focus on trade negotiation development, particularly implication on rare earth curbs (BBG and CNBC) and upcoming Trump-Xi call.

In premarket trading, the Mag 7 stocks are mixed (Alphabet +1.3%, Amazon +0.7%, Meta +0.2%, Microsoft 0%, Tesla -2.6%, Nvidia -0.5%, Apple -0.3%). Broadcom shares rise 1% in premarket ahead of earnings due after the bell. Chewy shares (CHWY) are down 2.4% premarket after Jefferies analyst Kaumil Gajrawala cut the recommendation on the online retailer of pet products to hold from buy, writing that valuation appears “primed” for a first-quarter beat and raise that’s unlikely to happen. Dollar Tree Inc. shares (DLTR) are up 1.6% in premarket trading, after JPMorgan upgraded the discount retailer to overweight from neutral. Here are some other notable movers:

Five Below (FIVE) gains 6% in premarket trading after the discount stores company reported first-quarter results that beat expectations and guided for net sales in the second quarter that are above estimates.

Nebius shares (NBIS) gain 5.6% in US premarket trading after the AI infrastructure software provider is initiated with a buy rating at Arete Research, while peer CoreWeave declines 2% after getting new neutral rating.

PVH shares (PVH) drop 7.9% in premarket trading after the Calvin Klein owner cut its full-year adjusted earnings guidance, and noted that the outlook reflects an estimated net negative impact in relation to tariffs placed on goods coming into the US.

Planet Labs shares (PL) jump 20% in premarket trading after first-quarter revenue beat estimates. Analysts at Citizens said the satellite data provider had a “stellar quarter” and the stock remains an opportunity for long-term capital appreciation.

Visa shares (V) rise 1% in premarket trading on Thursday as Mizuho Securities raises the stock to outperform from neutral, saying the cash-to-card runway in the US still has room to grow.

The wild swings in stocks that were sparked by the Trump administration’s tariff announcements in April — and subsequent rebound — have given way to more subdued daily moves in recent weeks. The US benchmark has remained largely flat since mid-May as traders assess the impact of the trade war on economic activity.

Friday’s jobs report is expected to show that growth in nonfarm payrolls slowed and the unemployment rate remained steady. While the figures would chime with Wednesday data that showed a contraction in US services and a deceleration in private hiring, separate data earlier in the week unexpectedly showed a fairly broad advance in US job openings.

“Consensus is for lower job creation,” said Ulrich Urbahn, head of multi-asset strategy and research at Berenberg. “I think there must be a big surprise to the downside for volatility to increase.”

Some investors are warning that the current period of relative market calm could once again give way to volatility, as uncertainty lingers over the outcome of trade negotiations between the US and its biggest trading partners — and the full economic impact remains unclear.

“Our bias remains to sell any rallies” in US bonds, said Mohit Kumar, chief European strategist at Jefferies International. “We are concerned over the fiscal deficits and the willingness of the rest of the world to continue financing US fiscal deficits.”

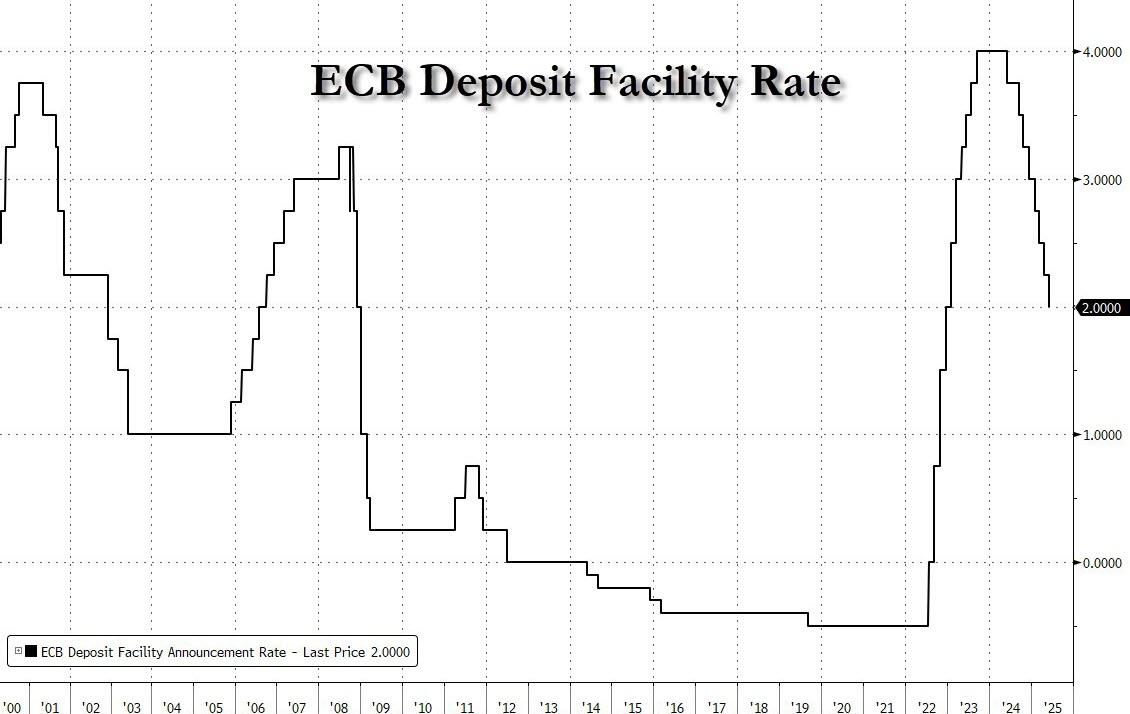

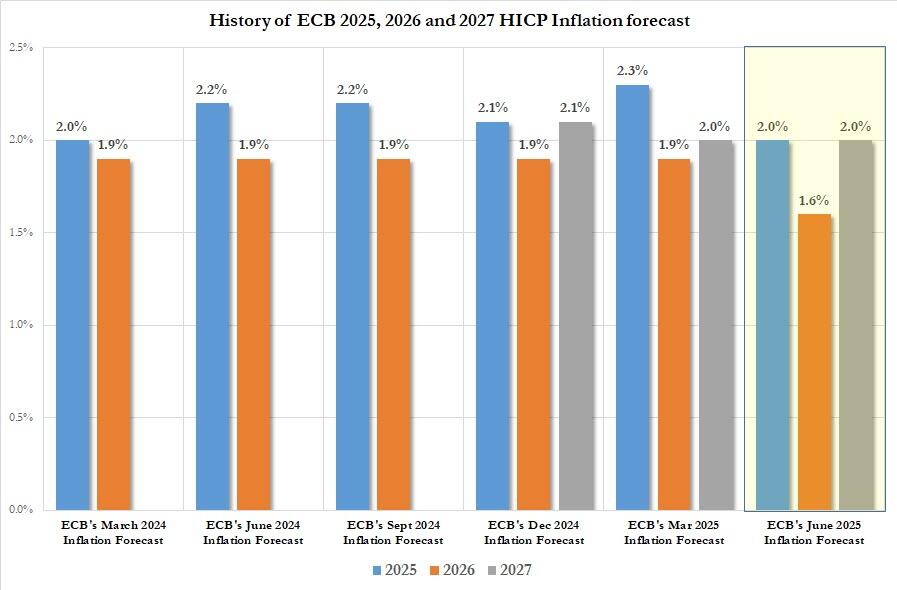

The European Central Bank is set to cut rates for an eighth time later on Thursday. Another reduction is expected in September, when trade talks with the US should have concluded and fresh forecasts will reveal the full implications of the tariffs. And speaking of Europe, the Stoxx 600 is up 0.4%, rising for a third day ahead of a widely anticipated interest-rate cut by the European Central Bank. European stocks were on track for the highest close in more than two weeks. Technology, construction and health care stocks are leading gains while travel and retail provide a drag. Here are the biggest European movers:

Bayer shares rise as much as 5.1% after Goldman Sachs upgrades the German chemicals and pharmaceutical company to buy from neutral, saying it sees earnings as having bottomed out and thinks risks around litigation and pharma data are overdone.

Dr. Martens surges as much as 17%, the most since November, after the UK bootmaker releases its full-year results and outlines its new ‘Levers For Growth’ strategy update.

Redcare shares rise as much as 2.3%, paring some of Wednesday’s 14% drop that was spurred by a rating downgrade at Kepler Cheuvreux. Concerns about structural challenges related to the anticipated phaseout of the CardLink system are “unwarranted and lack concrete support,” according to Deutsche Bank analysts.

Wise shares rise as much as 9% to a record high after the money-transfer firm said it intends to seek a primary listing in the US to enhance visibility to the investment community and the stock’s trading.

Burckhardt shares gain as much as 6%, to the highest level since February, with Vontobel analysts saying the Swiss compressors manufacturer delivered significant margin progress compared to last year, driven by a good product mix.

Wizz Air shares fall as much as 27%, the steepest drop since the early days of the pandemic, after the airline’s cost guidance and fourth-quarter results disappointed analysts.

CMC Markets shares tank as much as 18% after reporting annual pretax profit below expectations after disappointing investors on costs, according to analysts at Shore Capital, while the dividend was also lower than hoped.

Akzo Nobel falls as much as 2.5% as UBS cuts the recommendation on the coatings and Dulux paint maker to neutral from buy.

Avolta shares drop as much as 7.9% after one of its investors sold shares at a discount to Wednesday’s close.

Hemnet falls as much as 8.4% to its lowest since Jan. 31 after Nordea double-downgraded its view on the Swedish real estate listings platform to sell from buy, saying recent monetization pushes for premium offerings “may have crossed a line where user price elasticity begins to invite disruption.”

Earlier in the session, Asian stocks edged higher, as South Korean shares extended a rally on hopes of improved corporate governance under the new president. The MSCI Asia Pacific Index rose as much as 0.4%, heading for its highest level in more than three years. Korea’s Kospi Index jumped 1.5% after the ruling party said it will propose a revision to Commercial Act again, a key step in improving corporate governance. Benchmarks in Hong Kong and Taiwan also gained, with US economic data starting to soften and supporting the case for an interest-rate cut by the Federal Reserve. Japanese shares fell. Demand at the country’s 30-year bond auction was weaker than the average over the past year. The regional benchmark’s gain in recent weeks is in tandem with global peers, which closed at a record high Wednesday on expectations that the worst of higher tariffs may be over. Still, uncertainty remains high around the progress of US-China trade talks, with Chinese leader Xi Jinping making clear that a phone call doesn’t come without a price. That’s even as Trump is seeking a personal discussion with Beijing to prevent further escalation in trade tensions.

In FX, the Bloomberg Dollar Spot Index is unchanged. The Japanese yen is the weakest of the G-10 currencies, falling 0.3% against the greenback. The kiwi tops the leader board with a 0.4% gain. The euro traded steady after advancing more than 10% against the dollar year-to-date.

In rates, treasuries are mixed with gains only seen at the longer end of the curve. US 30-year yields fall 2 bps to 4.86%. European government bonds advance across all maturities, with UK and German 10-year yields falling 3-4 bps each. Japanese government bonds rose after an auction of 30-year debt was better than many investors had feared. Still, a bid-to-cover ratio of 2.92 at the offering pointed to a general lack of appetite for longer-maturity debt. Markets

In commodities, oil prices are steady with WTI near $63 a barrel. Spot gold rises $12 to around $3,385/oz. Silver rises 3% and above $35/oz for the time since 2012.

Looking to the day ahead, and the main highlight will be the ECB’s latest policy decision and President Lagarde’s subsequent press conference. Otherwise, we’ll hear from the Fed’s Kugler, Harker and Schmid, BoE Deputy Governor Breeden, and the BoE’s Greene. Data releases from the UK include the weekly initial jobless claims and the April trade balance. Meanwhile in Europe, there’s German factory orders for April, and the May construction PMIs for Germany and the UK.

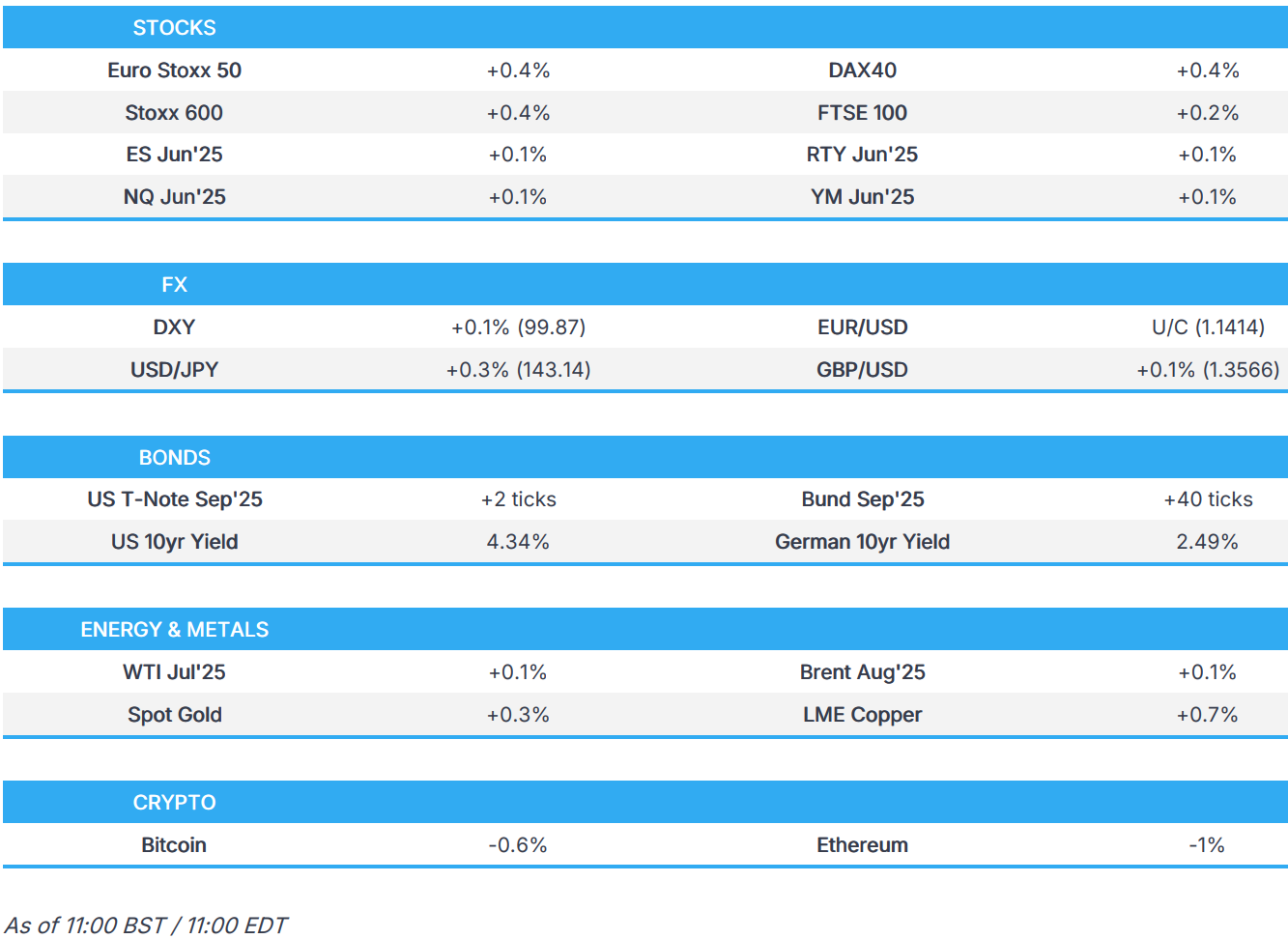

Market Snapshot

S&P 500 mini little changed

Nasdaq 100 mini little changed

Russell 2000 mini +0.1%

Stoxx Europe 600 +0.4%

DAX +0.4%

CAC 40 +0.4%

10-year Treasury yield -1 basis point at 4.35%

VIX little changed at 17.58

Bloomberg Dollar Index little changed at 1208.49

euro little changed at $1.142

WTI crude +0.1% at $62.94/barrel

Top Overnight News

White House official said Elon Musk’s opposition is one disagreement in an otherwise harmonious relationship and it will not consult every policy decision with Elon Musk, while the official added that President Trump is committed to getting the bill passed, despite opposition from Musk.

The ECB looks all but certain to cut rates by 25 bps to 2% today. Another reduction is expected in September, but constantly changing US trade threats will cloud new economic projections and President Christine Lagarde’s press conference. BBG

Donald Trump and Republican senators discussed ways to scale back the $40,000 state and local tax deduction cap in the House version of the president’s tax-cut bill, Senate Majority Leader John Thune said. BBG

Treasuries edged higher as traders got a boost from Japan, where government bonds rose after a 30-year auction was better than feared. BBG

“There’s no resolution yet on SALT, which Senate Republicans want to change significantly. We’re told Trump didn’t object when GOP senators reiterated their desire to water down the House’s USD 40,000 deduction cap.”: Punchbowl

Senate Republicans on Wednesday discussed the need to cut out waste, fraud and abuse in Medicare to achieve more deficit reduction in President Trump’s landmark bill to extend the 2017 tax cuts, provide new tax relief, secure the border and boost defense spending. The Hill

US Senate Majority Leader Thune said Senate Republicans had a positive budget bill talk with President Trump and feel good about where they are on the Trump tax bill, while GOP Senator Crapo said Republicans have very strong support and unity on the Trump tax bill.

OMB chief Vought said the White House doesn’t support the debt ceiling being removed from the reconciliation bill and that the Trump spending bill will improve the deficit, while he added they are having very good conversations with the Senate on the Trump spending bill and opposing views from outside aren’t hurting bill’s prospects.

Trump signed a proclamation to ban travel from certain countries whereby the proclamation fully restricts and limits the entry of nationals from 12 countries, including Afghanistan, Burma, Chad, Republic of Congo, Equatorial Guinea, Eritrea, Haiti, Iran, Libya, Somalia, Sudan, and Yemen, while Trump said travel ban list is subject to revision and new countries could be added as threats emerge around the world. Furthermore, President Trump signed a proclamation to restrict foreign student visas at Harvard University.

Wall Street’s top regulator took a step toward toughening rules for foreign companies listed on American stock markets on Wednesday, saying many Chinese firms in particular unduly benefited from having to make fewer regular disclosures to investors. The regulator warned that foreign firms, especially ones from China, could face stricter disclosure rules. SCMP

US business optimism moved sharply lower, with only 27% of executives polled in May by the AICPA confident about the economic outlook for the 12 months ahead. BBG

A private gauge of China’s services sector signaled that activity picked up in May, despite a renewed fall in new export orders. The Caixin services purchasing managers index rose to 51.1 last month from 50.7 in April, Caixin Media and S&P Global said Thursday. That marked the 29th month above the 50-mark separating expansion from contraction. WSJ

China warned major EV makers including BYD, Geely and Xiaomi to stop unsustainable price wars, people familiar said. Officials urged self-regulation but gave no formal orders. They also raised concerns over unpaid supplier bills. BBG

German factory orders unexpectedly kept rising in April after Trump’s announcement of US reciprocal tariffs, defying expectations for a setback. BBG

Tariffs/Trade

US President Trump is to meet with German Chancellor Merz at 11:45EDT/16:45BST today.

US auto supplier group said immediate and decisive action is needed to prevent widespread disruption and economic fallout across the vehicle supplier sector on the Chinese rare earth issue.

Vietnam sent a document with replies to US requests on trade and the Trade Minister met with USTR Greer to discuss the main points in Vietnam’s replies to the US’s requests on trade.

Chinese Foreign Ministry says there is no information to share on a US President Trump/Chinese President Xi call, via Bloomberg.

EU Trade Commissioner Sefcovic says China’s “impressive” rise must not come at the expense of the European economy “Our objective is straightforward, to identify real and highest vulnerability across political areas. I am talking about advanced semiconductors, AI and quantum tech”.

EU Businesses are lobbying Beijing to set up a “special channel” to fast track Chinese approval of rare earth export licenses for “reliable” companies, according to FT sources; proposal was made at a meeting with European companies and MOFCOM officials.

A more detailed look at global markets courtesy of Newsquawk