WE HAVE NOW ENTERED OPTIONS EXPIRY MONTH WITH THE OTC/LONDON OPTIONS EXPIRY ON MONDAY.

132 C SG AMERICAS 21

624 H BOFA SECURITIES 25

686 C STONEX FINANCIAL INC 1

737 C ADVANTAGE FUTURES 1

905 C ADM 2

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024: 25 CONTRACTs NOTICES FOR 2500 OZ or 0.0777 TONNES

total notices so far: 29,851 contracts for 2,985,100 OR 92.849 tonnes)

SILVER NOTICES: 16 NOTICE(S) FILED FOR 80,000 OZ/

total number of notices filed so far this month : 3387 CONTRACTS (NOTICES) for 16.935 million oz

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

AN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 92.69 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR SIZED 310 CONTRACTS OI TO 168,815 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 740 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 740 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 740 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 310 CONTRACTS AND ADD TO THE 740 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1047 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.48 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 5.235 MILLION PAPER OZ

OCCURRED DESPITE OUR $0.48 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

XXXXX

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 7.52 PTS OR 0.22%

//Hang Seng CLOSED DOWN 149.27 PTS OR 0.61%

// Nikkei CLOSED UP 642.27 PTS OR 0.61% //Australia’s all ordinaries CLOSED UP 0.07%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1700 OFFSHORE CLOSED UP AT 7.1679/ Oil DOWN TO 64.98 dollars per barrel for WTI and BRENT DOWN TO 67.80 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1700 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1679 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST GAINED BY A SMALL SIZED 310 CONTRACTS TO A STILL LOW NUMBER OF 434,448 OI WITH OUR SMALL GAIN IN PRICE OF $4.90 WITH RESPECT TO THURSDAY’S // TRADING. WE GAINED SOME NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1310 ). WE HAD LITTLE T.A.S. LIQUIDATION ALONG AND LITTLE MONTH END CALENDAR SPREADER LIQUIDATION YESTERDAY. THEY WERE SAVING IT UP FOR TODAY!!

THE CME ANNOUNCED THURSDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES. TOTAL ISSUANCE FOR MAY WAS RECORDED AT 9.591 TONNES OF GOLD AND THIS TOTAL WAS ADDED TO OUR NORMAL DELIVERIES. THE BANK OF ENGLAND MUST BE GETTING QUITE ANTSY OF GETTING ITS GOLD BACK.

IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST FIVE MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED SO FAR!!

DETAILS ON JUNE COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1620 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF MAY, AND JUNE CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS SMALL AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 965 T.A.S.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , INITIAL STANDING IS RECORDED AT 62.534 TONNES PLUS TODAY’S 0.1493 TONNES QUEUE JUMP = 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE MONTH FOR THE MONTH: 31.027 TONNES

NEW TOTAL TONNES STANDING JUNE: 94.085 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 32+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 225 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1310 EFP CONTRACT WAS ISSUED: : /AUGUST 1310 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1310 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS

- ZERO NET SPEC LIQUIDATION WITH OUR SMALL GAIN IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY MORNING//THURSDAY NIGHT WAS A SMALL SIZED, 965 CONTRACTS.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL MAY AND JUNE

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.THIS WAS SURELY IN EVIDENCE IN TRADING THURSDAY WITH THE SMALL GAIN IN PRICE!

STANDING LAST 6 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: INITITAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

THIS IS CENTRAL BANKS STANDING FOR PHYSICAL GOLD!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 54 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING/JUNE CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $4.90/ /) AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A SMALL SIZED GAIN IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION + CALENDAR SPREADER LIQUIDATION ////THURSDAY AS THEY SAVING THEM UP FOR TODAY’S RAID. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION TO COMMENCE ON JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JUNE TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: SO FAR ZERO

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS JUNE DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JUNE COMEX CONTRACT

WE HAVE GAINED A FAIR SIZED TOTAL OF 5.038 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE FIRST RECORDED AT 62.534 TONNES ON FIRST DAY NOTICE/MAY 30. TO THIS WE ADD THURSDAY NIGHT’S QUEUE JUMP OF 4800 OZ OR 0.1493 TONNES OF GOLD//NEW STANDING FOR JUNE GOLD ADVANCES TO 93.085

ALL OF THIS QUITE GOOD STANDING FOR JUNE WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $4.90

WE HAD A HUGE 4806 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 1620 CONTRACTS OR 162000 0Z (5.038 TONNES)

confirmed volume THURSDAY 168,212. contracts: awful volume////

//speculators have left the gold arena

END

INITIAL

JUNE CONTRACT MONTH

JUNE 27/2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES . 0 ENTRIES |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | 0 ENTRY xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 25 notice(s) 2500 OZ 0.07777 TONNES |

| No of oz to be served (notices) | 46 contracts 4600 OZ 0.1430 TONNES |

| Total monthly oz gold served (contracts) so far this month | 29,851 notices 2,985,100 oz 92.849 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 0 customer entry

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:

0 ENTRIES

adjustments: 5 (ALL DEALER TO CUSTOMER ACCTS)

a) Brinks 15,818.292 oz (492 kilobars)

b) JPMorgan 52,663.338 oz (1338 kilobars)

c) Loomis 14,467,950 oz (450 kilobars)

d) Malca: 4259.488 oz (285 kilobars)

e) Manfra 4,243.932 oz (132 kilobars)

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JUNE STANDS AT 71 CONTRACTS FOR A LOSS OF 287 CONTRACTS. WE HAD 335 CONTRACTS SERVED ON THURSDAY SO WE GAINED 48 CONTRACTS FOR 4800 OZ OR .1493 TONNES OF GOLD WHICH UNDERWENT A QUEUE JUMP. THIS TOTAL WILL BE ADDED TO OUR INITIAL AMOUNT OF GOLD STANDING AT 62.534 TONNES//NEW STANDING ADVANCES TO 93.085 TONNES

JULY LOST 372 CONTRACTS TO STAND AT 5942

AUGUST LOST 1042 CONTRACTS UP TO 319,534

We had 335 contracts filed for today representing 33,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 25 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JUNE /2025. contract month, we take the total number of notices filed so far for the month (29,851 X 100 oz ) to which we add the difference between the open interest for the front month of JUNE (71 CONTRACTS) minus the number of notices served upon today (25 x 100 oz per contract) equals 2,992,700 OZ OR 93.085 TONNES to which we add 0 tonnes of gold issued under exchange for risk// total standing 93.085 tonnes

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (29,851 x 100 oz +we add the difference for front month of JUNE (71 OI} minus the number of notices served upon today (25 x 100 oz) which equals 2,992,700 OZ OR 93.085 TONNES + 0 tonnes EX FOR RISK = 93.085 tonnes

TOTAL COMEX GOLD STANDING FOR JUNE.: 93.085 TONNES WHICH IS SMALL FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..JUNE DID NOT FOLLOW FEB AND APRIL’S LEAD!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,206,307.064 oz 68.62 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 37,048.334.641 oz

TOTAL REGISTERED GOLD 20,165,828.999: or 627.241 tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,882,505.612 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 17,959,521 oz (REG GOLD- PLEDGED GOLD)= 548.62 tonnes //

total inventories in gold declining rapidly

SILVER/COMEX

THE JUNE 2025 SILVER CONTRACT//INITIAL

JUNE 27

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries i) CNT 29,983.501 oz ii) HSBC 302,806.900 oz iii) Loomis 600,370.600 oz total withdrawal 933,161.001 oz |

| Deposits to the Dealer Inventory | 0 entry |

| Deposits to the Customer Inventory | 1 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into Delaware 2,936.878 oz total deposit 2936.378 oz |

| No of oz served today (contracts) | 16 CONTRACT(S) (80,000 OZ |

| No of oz to be served (notices) | 2contracts (10,000 oz) |

| Total monthly oz silver served (contracts) | 3387 Contracts (16.935 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

0 deposits into dealer accounts

total deposit nil oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into Delaware 2,936.878 oz

total deposit 2936.378 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3 entries

i) CNT 29,983.501 oz

ii) HSBC 302,806.900 oz

iii) Loomis 600,370.600 oz

total withdrawal 933,161.001 oz

ADJUSTMENTs 2/

a) Dealer to customer ASAHI 608,147,700 oz

b) Delaware: dealer to customer: 10,008.45 oz

TOTAL REGISTERED SILVER: 187.681 MILLION OZ//.TOTAL REG + ELIGIBLE. 499.090 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE /2025 OI: 18 OPEN INTEREST CONTRACTS FOR A GAIN OF 16 CONTRACTS. WE HAD 1 CONTRACT SERVED ON THURSDAY SO WE GAINED 17 CONTRACTS OR 85,000 OZ UNDERWENT A QUEUE JUMP IN ORDER TO TAKE DELIVERY OF PHYSICAL SILVER OVER ON THIS SIDE OF THE POND.

JULY LOST 14,625 CONTRACTS DOWN TO 10,163 CONTRACTS WITH ONE DAY LEFT BEFORE FIRST DAY NOTICE. WE WILL HAVE AROUND 30 MILLION OZ OF SILVER STAND FOR JULY DELIVERY.

AUGUST GAINED 435 CONTRACTS TO 2247

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 16 or 80,000 oz

CONFIRMED volume; ON THURSDAY 108,091 huge//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 3387 X5,000 oz = 16.935 MILLION oz

to which we add the difference between the open interest for the front month of JUNE (18) AND the number of notices served upon today (16 )x (5000 oz)

Thus the standings for silver for the JUNE 2025 contract month: (3387) Notices served so far) x 5000 oz + OI for the front month of JUNE(18) minus number of notices served upon today (16)x 5000 oz equals silver standing for the JUNE contract month equating to 16.945 MILLION OZ .

New total standing: 16.945 million oz which is huge for this NON active delivery month of JUNE.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 187.681million oz of registered silver

JPMorgan as a percentage of total silver: 214.820/499/090 million. 42.88%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

JUNE 20 WITH GOLD DOWN $19.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 947.37 TONNES

JUNE 18 WITH GOLD UP $1.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.03 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 945.94 TONNES

JUNE 17 WITH GOLD DOWN $9.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 941.93 TONNES

JUNE 16 WITH GOLD DOWN $33.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.758 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 940.49 TONNES

JUNE 13 WITH GOLD UP $53.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.38 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 932.91 TONNES

JUNE 12 WITH GOLD UP $55.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 934.19 TONNES

JUNE 11 WITH GOLD UP $1.10 TODAY// SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.31 TONNEES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 935.91 TONNES

JUNE 10 WITH GOLD DOWN $11.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.02 TONNEES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 936.22 TONNES

JUNE 9 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.45 TONNEES OF GOLD FROM THE GLD//: /// ///INVENTORY RESTS AT 934.20 TONNES

JUNE 6 WITH GOLD DOWN $28.00 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

JUNE 2 WITH GOLD UP $80.90 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 930.20 TONNES

MAY 30 WITH GOLD DOWN $27.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.59 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 930.20 TONNES

MAY 29 WITH GOLD UP $22.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 925.71 TONNES

MAY 28 WITH GOLD DOWN $5.30 TODAY// NO CHANGES IN GOLD AT THE GLD:/ ///INVENTORY RESTS AT 925.61 TONNES

MAY 27 WITH GOLD DOWN $63.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 922.46 TONNES

MAY 23 WITH GOLD UP $69.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 923.89TONNES

MAY 22 WITH GOLD DOWN $15.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 919.88 TONNES

MAY 21 WITH GOLD UP $28.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.60 TONNES

MAY 20 WITH GOLD UP $51.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.30 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 921.03 TONNES

MAY 19 WITH GOLD UP $46.65 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.89 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 918.73 TONNES

MAY 16 WITH GOLD DOWN $38.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 927.62 TONNES

MAY 15 WITH GOLD UP $38.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.53 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 931.92 TONNES

MAY 14 WITH GOLD DOWN $40.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 936.51 TONNES

GLD INVENTORY: 953.39 TONNES, TONIGHTS TOTAL

SILVER

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

JUNE 20 WITH SILVER DOWN $0.83/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.818 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 474.641 MILLION OZ.

JUNE 18 WITH SILVER DOWN $0.20/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 17 WITH SILVER UP $0.67/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 473.096 MILLION OZ.

JUNE 16 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.727 MILLION OZ FROM THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 13 WITH SILVER UP $0.11/NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 473.550 MILLION OZ.

JUNE 12 WITH SILVER UP $0.11/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.276 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 473550 MILLION OZ.

JUNE 11 WITH SILVER DOWN $0.45/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.046 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.274 MILLION OZ.

JUNE 10 WITH SILVER DOWN $0.16/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.232 MILLION OZ.

JUNE 9 WITH SILVER UP $0.69/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.914 MILLION OZ.

JUNE 6 WITH SILVER UP $0.63/HUGE CHANGES AT THE SLV:A DEPOSIT OF 3.863 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.732 MILLION OZ. (A TOTAL DEPOSIT OF 11.856 MILLION PHANTOM OZ IN THE LAST 4 DAYS)

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

JUNE 2 WITH SILVER UP $1.58/NO CHANGES AT THE SLV: ././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 30 WITH SILVER DOWN $0.36/HUGE CHANGES AT THE SLV: A DEPOSIT OF 2.773 MILLION OZ INTO THE SLV././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 29 WITH SILVER UP $0.29/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 28 WITH SILVER DOWN $0.18/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 27 WITH SILVER DOWN $0.34/HUGE CHANGES AT THE SLV//A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 23 WITH SILVER UP $0.38/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.5 MILLION OZ OF SILVER INTO THE SLV/: //INVENTORY AT SLV RESTS AT 454.375 MILLION OZ

MAY 22 WITH SILVER DOWN $0.27/NO CHANGES IN SILVER INVENTORY AT THE SLV:////: //INVENTORY AT SLV RESTS AT 451.875 MILLION OZ

MAY 21 WITH SILVER UP $0.35/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.091 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 451.875 MILLION OZ

MAY 20 WITH SILVER UP $0.65/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.41 MILLION OZ INTO THE SLV// ////: //INVENTORY AT SLV RESTS AT 449.784 MILLION OZ

MAY 19 WITH SILVER UP $0.17/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.819 MILLION OZ OUT OF THE SLV// ////: //INVENTORY AT SLV RESTS AT 447.193 MILLION OZ

MAY 16 WITH SILVER DOWN $0.24/NO CHANGES IN SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 15 WITH SILVER UP 0.04/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.909 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 449.193 MILLION OZ

MAY 14 WITH SILVER DOWN $0.39/HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.682 MILLION OZ OUT OF SILVER INVENTORY AT THE SLV ////: //INVENTORY AT SLV RESTS AT 450.102 MILLION OZ

CLOSING INVENTORY 477.958 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

MATHEW PIEPENBERG

ALASDAIR MACLEOD…

End-month markdowns

Predictably, futures contract expiry is coinciding with precious metals weakness. But it ignores weakness in the dollar, likely to prompt further dollar selling in favour of gold.

| Alasdair MacleodJun 27∙Paid |

Another week of universal apathy. It is the end of the first half of 2025 with book squaring in mind, and the July futures contract running off the board. In Europe this morning, gold was $3285, down $93 on the week, and silver at $35.85 down 20 cents. Interestingly, price weakness featured during Hong Kong and Shanghai trading hours particularly for gold, a pattern which has been noticeable recently.

Nevertheless, it is noticeable how well gold and silver are holding current price levels when Comex shorts would normally wish to see them much lower. Instead, we can assume that it is punters on the Shanghai Futures Exchange who are in a pickle, with their June contract settlement expiring yesterday.

This week, silver has been notably firm despite Comex open interest declining, shown in the chart below:

Meanwhile, Comex warehouse stocks have held up as the Macromicro chart shows. This is next:

This compares with gold stocks, which have declined sharply:

Silver stand for deliveries continue apace at 3,351 tonnes in Q2. Perhaps the difference between silver and gold is that silver remains in Comex warehouses while gold is being withdrawn.

The initial migration of gold into Comex from London, Switzerland, and elsewhere is now being reversed, mainly through stand for deliveries. Since warehouse stocks peaked in early-April, 245.5 tonnes have been stood for delivery while stocks declined a similar 249.3 tonnes. While it cannot be totally ruled out, we can be certain that the bulk of these deliveries are not returning to the arbitrageurs who flew bullion from Europe to trade futures premiums.

It leaves the question hanging as to how they will find the bullion to close the arbitrage. Some of it is due to be returned to leasing central banks in London, and we can also surmise that some of it was raided from ETF holdings. An assumption in London is that higher prices will produce the sellers to close these arbitrages out, which is presumably why major bullion banks are forecasting higher prices.

But this does not account for the mismatch in ownership. Those standing for deliveries appear to be hoarding gold instead of trading it. And this rationale was justified by the dollar’s weakness in the last few weeks. The dollar’s trade weighted index chart is truly awful:

Pressure is mounting on the Fed to cut interest rates, with President Trump publicly criticising Jay Powell for not doing so. With Powell’s term due to end in 11 months, Trump could announce a dovish successor in September creating a shadow Fed chief, according to the Wall Street Journal. Ramming Trump’s point home was a decline in US GDP of 0.5% in Q1 2025, significantly worse than expected. But price inflation is still well above the 2% target, and the tariff truce ends on 8 July, creating further price uncertainty.

The sharp decline in the dollar’s TWI is bound to bring additional price inflation from imported consumer goods. With these uncertainties, Powell’s caution is understandable. But with Trump seemingly determined to force the pace on monetary policy it is hardly surprising that gold is holding close to its highs. But it is the fiat dollar that’s declining, and that decline is accelerating as our last chart illustrates:

Foreign holders of an estimated $39.6 trillion dollars and underlying financial assets are staring at significant losses as Trump squabbles with the Fed. Their selling is set to weaken the dollar even more, and therefore gold higher

END

3. CHRIS POWELL AND GATA DISPATCHES

4. ANDRE MAGUIRE/LIVE FROM THE VAULT KINESIS 229

5. COMMODITY REPORT…COPPER

Goldman Sees Copper Peaking In August Amid Ex-US Supply Squeeze

Thursday, Jun 26, 2025 – 10:50 PM

Goldman Sachs analysts have released a new note this morning, raising their price forecast for 2H25 copper. The upgrade stems from tightening global supplies, as the ongoing US Section 232 investigation into the industrial metal drives massive inflows into the domestic market.

“The ex-US copper market has tightened, causing fears of a regional copper shortage despite the global market currently being in surplus,” a team of Goldman analysts, led by Eoin Dinsmore, wrote in a note to institutional clients.

As a result of the ongoing US Section 232 copper investigation, Dinsmore told clients this “continues to drive an unusually wide gap between COMEX (US) and LME (UK) prices, resulting in the US over-importing ~400kt of copper so far this year. US inventory has risen to over 100 days worth of consumption, up from just 33 days at the beginning of the year.”

Prices are expected to keep rising and peak in August…

We upgrade our 2H 2025 LME copper price forecast to $9,890/t from $9,140 previously, meaning that we expect the LME price to continue rising over the next two months, peaking for the year at $10,050 in August, before falling to $9,700 by December. With a 25% tariff on US copper imports by September remaining our base case, we reiterate our copper tariff trade of long Dec-25 COMEX-LME copper arbitrage.

Despite low inventories in China and the rest of the world, the global copper market remains in a modest surplus—estimated at ~280kt built in H1 2025 and ending the year with a 105kt surplus. However, this surplus is entirely concentrated in the US, with an expected 400kt post-trade surplus, while China and the rest of the world face regional deficits of ~100kt and ~200kt, respectively—creating significant regional supply imbalances.

The outcome of the ongoing Section 232 tariff investigation by the Trump administration will determine how oversupplied the US copper market becomes—and how tight the ex-US market remains. Dinsmore expects continued US inflows until a decision is made, with a base case 80% probability of a 25% tariff by September.

More color here from the analysts:

The timing of the ongoing S232 tariff investigation is crucial to how oversupplied the US copper market becomes, and how tight the rest of world market becomes. Because of how wide LME timespreads would need to get in order to close the import arbitrage, we expect copper to continue to flow into the US until the outcome of the investigation is announced – albeit at a slower pace as the import arbitrage narrows. Our base case (80% probability) of a 25% tariff being put in place on copper imports by September (Exhibit 5) means that we expect US inventories (including unreported) to increase by 150kt in Q3, before drawing by 120kt in Q4 after the tariff is imposed and imports fall close to zero. Conversely, we expect rest of world (ex-US and China) stocks to continue drawing in Q3 before turning to a build in Q4. However, a later than anticipated tariff announcement would mean that US importing continues into Q4, tightening the ex-US market even further.

The analysts noted that while it’s highly unlikely, if no tariff is announced, COMEX prices would likely fall below LME prices due to elevated US inventories. As a result, LME forward spreads would ease, with surplus US copper either exported or delivered into domestic LME warehouses.

The analysts stated: “We remain bullish copper prices in 2027 as a growing deficit, driven by strong electrification demand and limited mine supply growth, likely pushes prices to an annual average of $10,750 – the price level needed to incentivise investment in brownfield Chilean mine supply.”

Other key themes copper bulls have pumped in recent years include the AI boom and data center buildout, along with the broader “Powering Up America” narrative—focused on rebuilding the nation’s aging power grid to support the electrification wave of the 2030s.

More from Goldman Sachs research here available to pro subs.

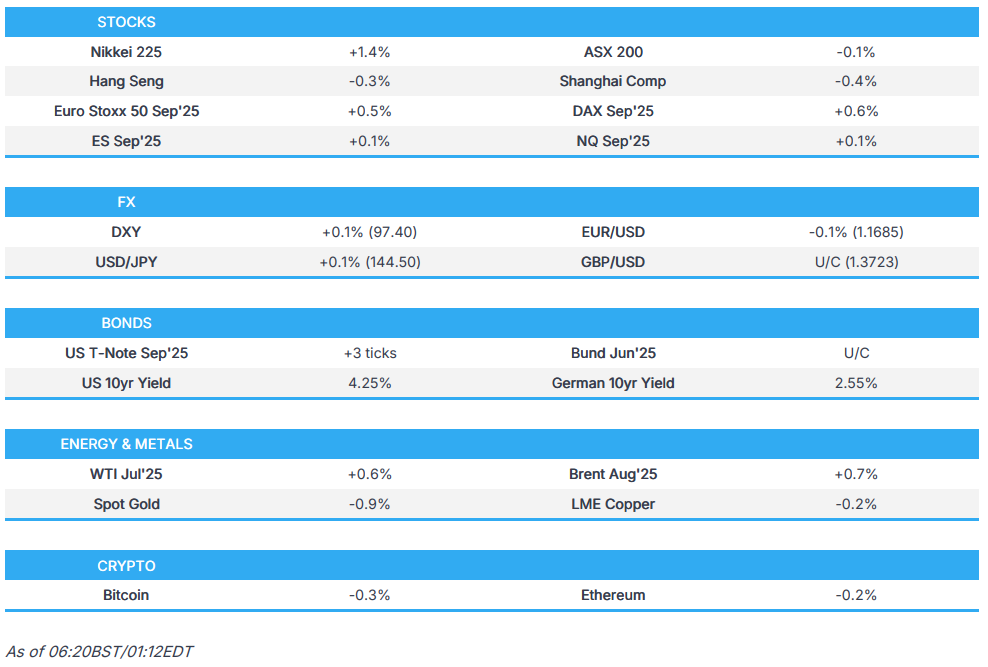

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 24.23 PTS OR 0.70%

//Hang Seng CLOSED DOWN 41.09 PTS OR 0.17%

// Nikkei CLOSED UP 566.21 PTS OR 1.43% //Australia’s all ordinaries CLOSED DOWN 0.34%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1684 OFFSHORE CLOSED DOWN AT 7.1676/ Oil UP TO 65.71 dollars per barrel for WTI and BRENT DOWN TO 68.23 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1684 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1676 AGAINST US DOLLAR/ AND THUS STRONGER

END

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1684 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.1676 (CCP MANIPULATED)

SHANGHAI CLOSED DOWN 24.23 PTS OR 0.70%

HANG SENG CLOSED DOWN 41.09 PTS OR 0.17%

2. Nikkei closed UP 566.21 PTS OR 1.43%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 96.88/ EURO RISES TO 1.1711 UP 18 BASIS PTS

3b Japan 10 YR bond yield: RISE TO. +1.440//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 144.51…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.5870/Italian 10 Yr bond yield UP to 3.505 SPAIN 10 YR BOND YIELD UP TO 3.234%

3i Greek 10 year bond yield UP TO 3.306

3j Gold at $3288.20 Silver at: 36.24 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 28 /100 roubles/dollar; ROUBLE AT 78.46

3m oil (WTI) into the 65 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 144.51// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.440% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8002 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9372 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.267 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.821 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.745 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 39.89

10 YR UK BOND YIELD: 4.470 DOWN 0 PTS

10 YR CANADA BOND YIELD: 3.3380 UP 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.882 DOWN 3 PTS

2a New York OPENING REPORT

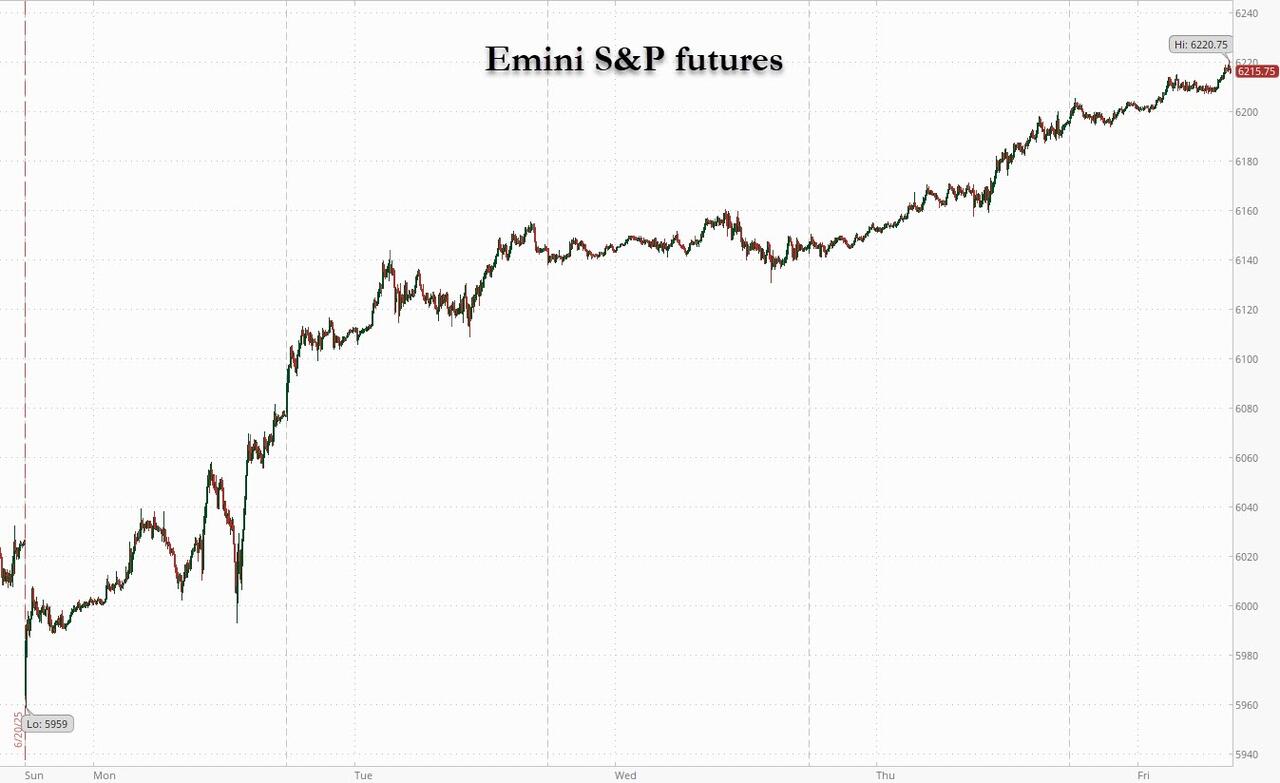

S&P Futures Trade At All Time High Boosted By Trade Talks, Nike Results

Friday, Jun 27, 2025 – 08:28 AM

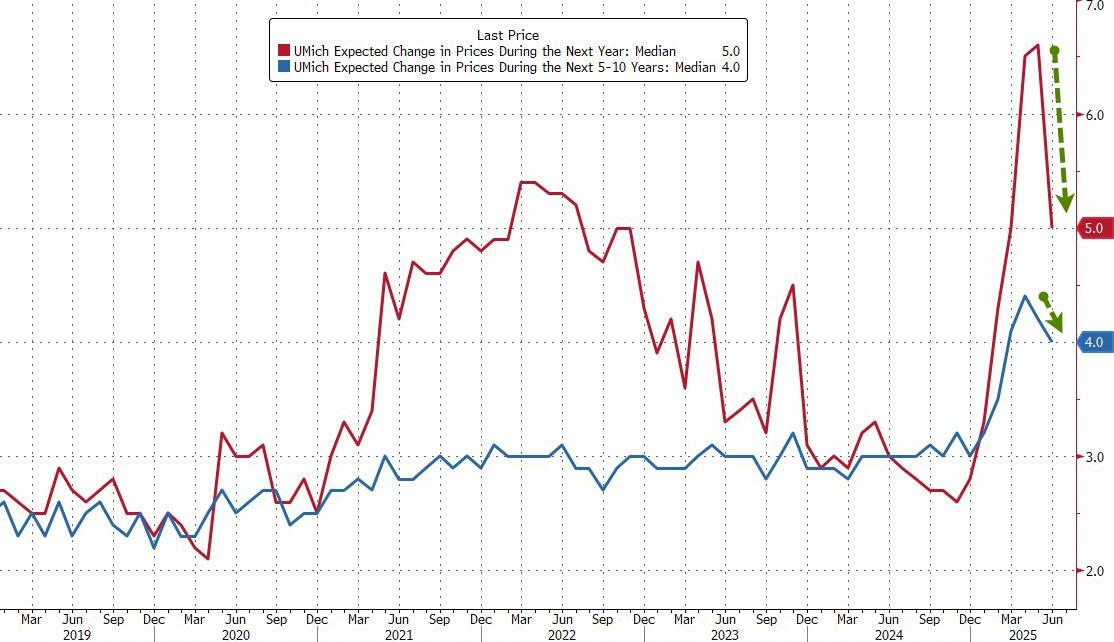

US equity futures are higher, buoyed by the (non) news that the US and China have signed a trade truce (which they first signed three weeks ago but nobody complied with it, so may as well push stocks up on the exact same headline again). The positive mood has also been helped by expectations of Fed rate cuts, a better-than-feared outlook from Nike and equity flow data. As JPM recaps, since yesterday’s close, there have been three major market focuses: (i) Lutnick said that US and China have already signed their trade deal; (ii) Nike’s guidance beats expectation; (iii) the removal of Section 899 yesterday afternoon. As of 8:00am ET, S&P futures are 0.3% higher and currently trading in record territory after Howard Lutnick indicated the US has plans to reach agreements with 10 major trading partners, while Nasdaq futures continued their panic FOMO meltup, rising another 0.5%, and set to rise every day this week. Pre-Market, Mag 7 are all higher; NKE shares are the outlier surging 10% after earnings. 2y fell -3bp, while 10y added 1bp; USD is higher. Commodities are mixed: Oil added +1.9%, while Ags are mostly lower. US economic data slate includes May personal income and spending (8:30am), June final University of Michigan sentiment (10am) and Kansas City Fed services activity (11am).

In premarket trading, Mag 7 stocks are higher alongside futures (AMZN +1.2%, Nvidia +0.9%, Meta +0.8%, Tesla +0.5%, Apple +0.5%, Alphabet +0.4%, Microsoft 0%).

- Amazon (AMZN) leads gains in the Magnificent Seven cohort of US tech stocks, rising 1.2%, after receiving an upgrade from BNP Paribas Exane.

- Atlantic Union Bankshares Corp. shares (AUB) are up 9.3% after the bank said it sold about $2 billion of its performing commercial real estate loans to Blackstone.

- Estee Lauder Cos. (EL) up 2.9% after HSBC raised its recommendation to buy from hold and increased its price target to $99 from $80 as it sees the cosmetics company at the end of a downgrade cycle.

- Li Auto ADRs (LI) drop 2.7% after the Chinese EV maker reduced its vehicle deliveries target for the second quarter, citing a sales system upgrade.

- Nike shares (NKE) rise 10% after forecasting a smaller-than-expected drop in revenue for the current quarter, a sign that the sportswear company’s earnings trend may have hit an inflection point, analysts say.

- WR Berkley Corp. (WRB) edges down 0.7% after a TD Cowen analyst cut its recommendation to hold from buy, citing outperformance following news Mitsui Sumitomo Insurance was buying a 15% equity stake.

- Trade Desk (TTD) gained 3.9% in premarket trading after being upgraded to outperform at Evercore ISI, while Baidu fell 0.8%.

- CorMedix (CRMD) falls 11% after launching an $85 million share offering via RBC.

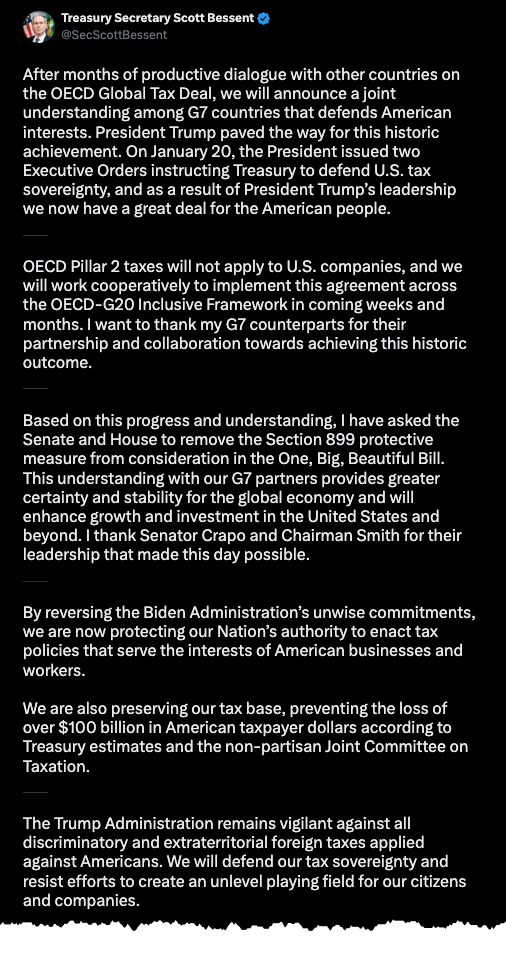

Commerce Secretary Howard Lutnick said that the US and China had finalized an understanding, and added the White House is nearing agreements with 10 major trading partners ahead of a July 9 deadline for reciprocal tariffs.

Meanwhile, the Treasury Department announced a deal with G-7 allies that will exclude US companies from some taxes imposed by other countries in exchange for removing the “revenge tax” proposal from President Donald Trump’s tax bill.

“There were fears that the revenge tax would make it much harder for companies and individuals to invest in the US, since it would increase their tax rates,” said Kathleen Brooks, research director at Xtb Ltd. “There are still more trade agreements to be done, for example with the European Union, but things are moving in the right direction.”

The Thursday moves were driven by US economic data that supported the case for policy easing. The swaps market has fully priced two further rate reductions this year and increased bets on a third.

A flurry of Fed officials this week made clear they’ll need a few more months to gain confidence that tariff-driven price hikes won’t raise inflation in a persistent way. Economists see the personal consumption expenditures price index excluding food and energy marking the tamest three-month stretch since the pandemic five years ago.

Copper rose as Goldman analysts warned that shortages will get worse before levies come into effect. A key one-day copper price spread surged to the highest level in four years on the London Metal Exchange, placing fresh strains on buyers contending with a rapid decline in inventories fueled by US plans to impose tariffs on the metal.

European stocks also gain with the Stoxx 600 climbing almost 1% and set for its first weekly advance in three. Data Friday showed inflation inched up in France and Spain, but not enough to concern European Central Bank officials who are optimistic that their 2% target will be met sustainably this year. Most sectors are in the green with auto, media and consumer products leading while miners lag. Here are some of the biggest movers on Friday:

- Adidas, Puma and JD Sports are rising after US giant Nike said its yearlong sales decline is starting to ease, with a smaller sales drop seen in the current quarter than earlier anticipated.

- Schneider Electric shares gain as much as 4.8% after electrical power equipment manufacturer reiterated its full-year guidance on a pre-close analyst call, which Oddo BHF said is “reassuring.”

- Pearson shares rise as much as 3.8% as analysts at BNP Paribas Exane upgraded the education-focused company and flagged a buying opportunity following recent weakness in the share price.

- Knorr-Bremse falls as much as 5.8%, the most since April, as shares in the German maker of brakes for trains and commercial vehicles were downgraded to neutral by both Citi and JPMorgan due to US truck data weakness and FX.

- Babcock shares drop as much as 4.1% after Deutsche Bank downgraded the stock.

Earlier in the session, Asian stocks rose, on track to cap their best week in nearly two months, helped by positive developments on US-China trade and bets on Federal Reserve interest-rate cuts. The MSCI Asia Pacific Index rose as much as 0.7% Friday, with Xiaomi providing a boost as the release of its electric SUV saw strong demand. Japanese stocks led gains, with the blue-chip Nikkei 225 topping 40,000. The regional gauge is poised for a weekly gain of more than 3% as risk-on sentiment returns after a cooling of Israel-Iran tensions. Next week’s key focal points include inflation data in South Korea, Indonesia and the Philippines as well as a US jobs report. Asean is holding a bond market forum in Kyoto while the ECB holds an annual forum in Portugal.

“Easing tariff concerns, lower geopolitical risks especially in the Middle East, rising hopes of Fed cuts, higher confidence on AI demand” are all contributing to gains in Asian stocks, said Vey-Sern Ling, a managing director at Union Bancaire Privee. “Asia markets are in a good position especially with a potentially weaker dollar,” he said.

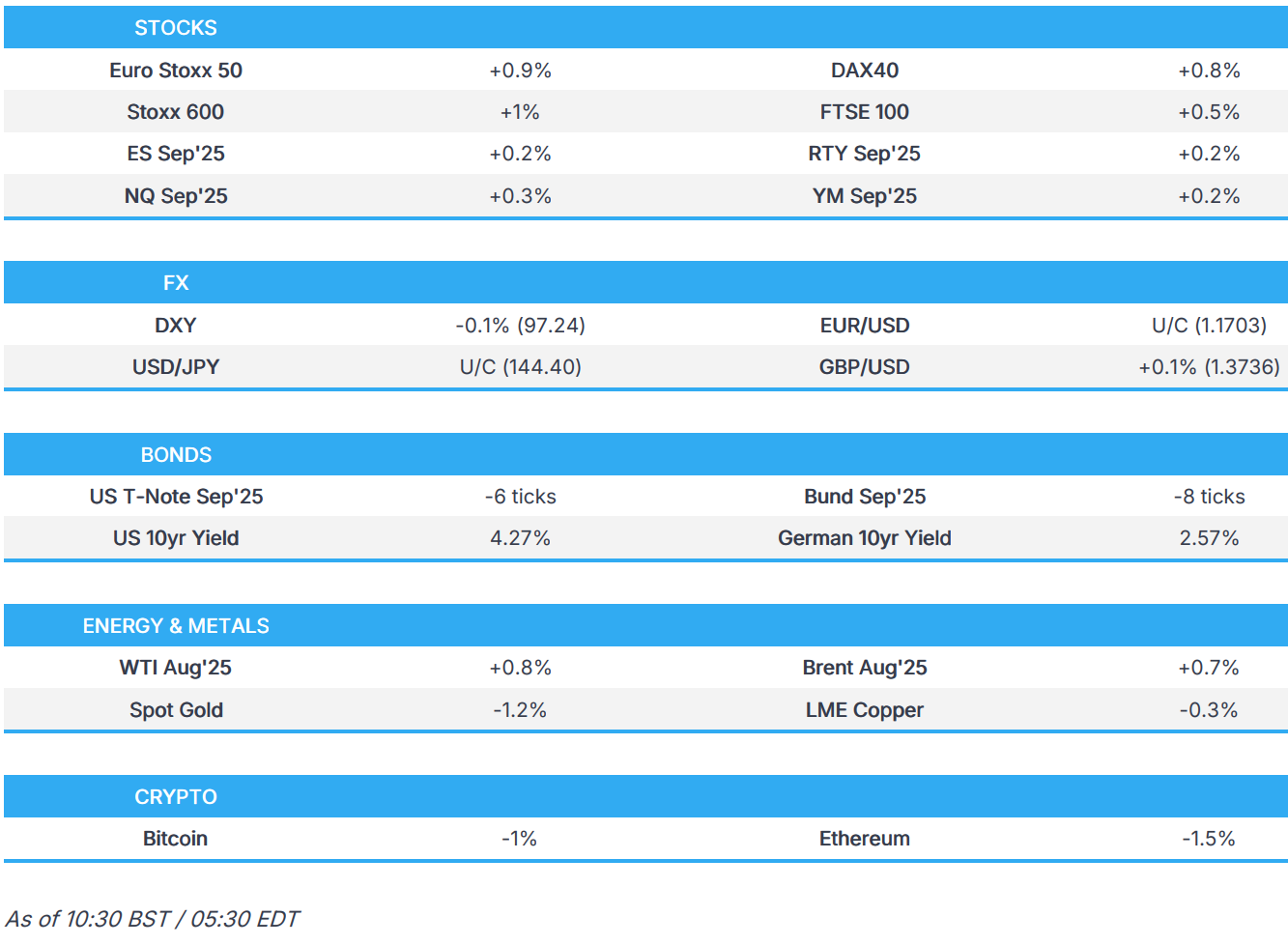

In FX, the Bloomberg Dollar Spot Index is flat. The Swedish krona is leading gains against the greenback among the G-10’s, rising 0.4%. EURUSD is up a seventh day, longest winning streak in a year; euro is up 1.6% on a weekly basis, the most in a month. GBPUSD up 0.1% at 1.3745; the pair is up 2.2% this week, best performance since early March. USD/JPY little changed at 144.39.

In rates, treasures fall for the first time this week; Yields are 1bp-3bp cheaper with front-end and belly lagging slightly, flattening 2s10s spread by about 0.5bp, 5s30s by 1.5bp; 10-year near 4.27% is 2bp cheaper on the day, slightly underperforming bunds and gilts in the sector. European government bonds are little changed.

In commodities, oil pared some of the biggest weekly decline in two years after a ceasefire between Israel and Iran, with the market’s focus shifting from the conflict in the Middle East to US trade negotiations. Spot copper contracts continued to trade at huge premiums to later-dated futures on the London Metal Exchange, after key price spreads this week hit the highest levels since an historic short squeeze in 2021. Gold falls $40 and below $3,300/oz as demand for haven assets dwindles; the precious metal heads for its second consecutive weekly loss, after a ceasefire between Israel and Iran dented demand for havens.

Looking to the day ahead, the key release will be today’s May PCE in the US, closely watched following the weaker-than-expected CPI print earlier this month. Other data releases include US personal income, personal spending, June Kansas City Fed services activity, We’ll also get Fed’s Williams, Hammack and Cook speak, ECB’s Rehn speaks

Market snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.3%

- Russell 2000 mini +0.3%

- Stoxx Europe 600 +0.9%

- DAX +0.8%, CAC 40 +1.4%

- 10-year Treasury yield +3 basis points at 4.27%

- VIX -0.4 points at 16.2

- Bloomberg Dollar Index little changed at 1194.19

- euro little changed at $1.1709

- WTI crude +0.9% at $65.8/barrel

Top Overnight News

- Lutnick said the US will imminently announce trade deals with 10 major trading partners while Trump hinted at an agreement arriving soon with India. BBG

- Equities momentum continuing this morning after the US and China finalized an understanding on trade. The deal includes a commitment from China to deliver rare earths. BBG

- US lawmakers said they would remove Section 899 from the tax bill: Reuters.

- On whether the US Reconcilliation Bill can be sent to President Trump by the July 4th deadline, Punchbowl says that it is possible, but is becoming increasingly difficult; Senators say voting will not being until Saturday at the absolute earliest. “…one key holdout said they’re far from the point when Trump will be needed to help close a deal.” Senators say voting will not being until Saturday at the absolute earliest, with that viewed as optimistic. Senate parliamentarian ruling focused on “the provider tax freeze in the bill rather than the Senate’s more drastic constraints for Medicaid expansion states, according to two sources with knowledge of the decision”. Republicans believe they can come up with a fix. President Trump has reportedly told multiple GOP senators privately that he prefers the House’s provider tax framework, which is much less drastic than the Senate’s version.

- US DOGE Service has sent staff to the Bureau of Alcohol, Tobacco, Firearms and Explosives with the goal of revising or eliminating dozens of rules and gun restrictions by July 4th: WaPo

- Europe considers a range of concessions to the White House in an effort to strike a trade deal in the near-term, including lowering tariffs on a range of imports, removing certain non-tariff barriers, buying more American products, and taking steps to address concerns about China. WSJ

- A flurry of Federal Reserve officials this week made clear they’ll need a few more months to gain confidence that tariff-driven price hikes won’t raise inflation in a persistent way. After Waller and Bowman’s dovish commentary on lowering rates as soon as July, nearly a dozen policymakers have dumped cold water on that idea since then. BBG

- China’s industrial profits slumped 9.1% in May, the biggest drop since October, under the weight of higher US tariffs and deflationary pressure. The decline adds urgency for more stimulus to meet growth goals. BBG

- Japan’s Tokyo CPI for June cools by more than anticipated, coming in at +3.1% Y/Y on a core basis (down from +3.3% in May and below the Street’s +3.3% forecast). WSJ

- Individual investors in Japan are boosting their purchases of government bonds at the fastest pace in 18 years as a rise in yields enhances the asset’s appeal. BBG

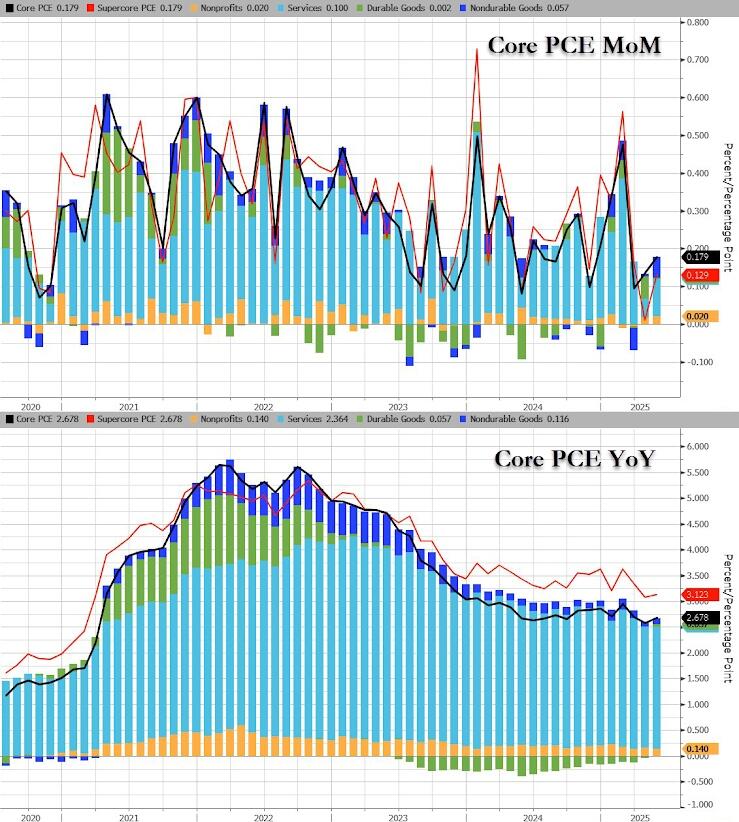

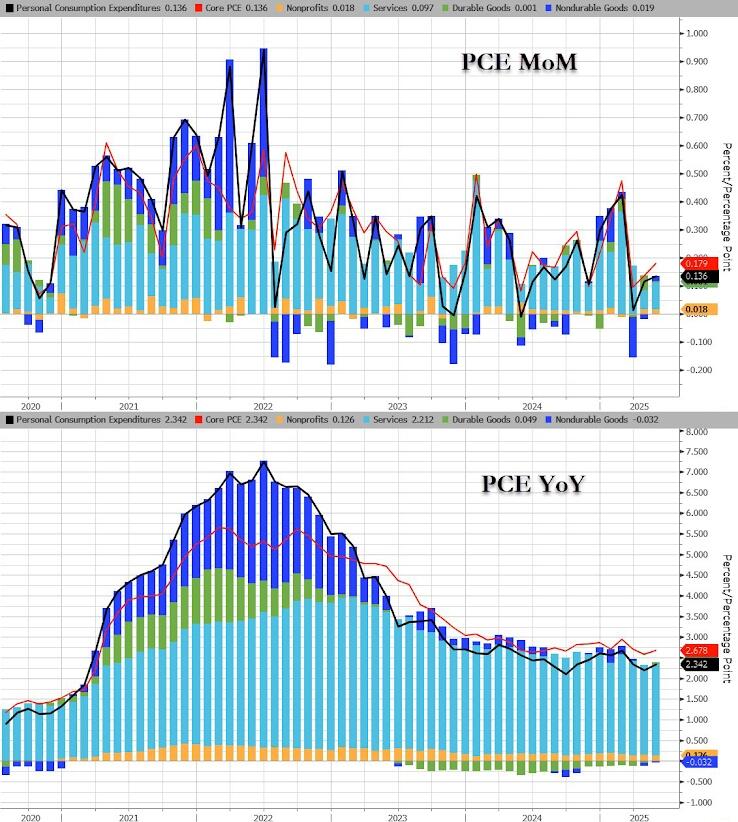

- Goldman forecast that core PCE prices rose 0.18% in May and 2.63% over the last year. Data from the CPI, PPI, and import prices suggest a modest tariff effect and a soft core print this month. Headline PCE prices rose 0.14% in May and 2.29% over the last year. GS expects the largest tariff effects on monthly inflation to show up from June through August. GIR

- NKE +9% pre mkt…after mgmt reaffirmed that 4Q will be peak pressure on call keeping turnaround story intact; That overshadows the weaker quarter last night (EPS $0.14 vs bogey of $0.20+).

Trade/Tariffs

- US President Trump said he just signed a deal with China on Wednesday, and says he has one maybe coming up with India. Trump added that China is starting to open up. It was later clarified that the US and China have agreed to an additional understanding to implement the Geneva agreement, according to a White House official cited by Fox’s Lawrence. A second Administration official confirmed that the framework finalises what was agreed in London and also addresses Chinese export controls, according to a source familiar with the agreement.

- China issues a statement on trade framework with US; two sides confirmed details on framework China will approve export applications for controlled items in accordance with the law. Both sides maintained close communications after meetings in London. The US side will accordingly lift a series of restrictive measures taken against China.

- European Commission President von der Leyen said the EU received the latest US proposal today and is prepared for both a deal and a no-deal outcome, stating all options remain on the table.

- French President Macron said he favours a speedy and fair EU–US trade deal, but warned that if the US maintains a 10% tariff, Europe would have to apply equivalent compensatory measures.

- US chip export curbs may slow China’s adoption of DeepSeek’s next model, R2, via The Information.

- US Commerce Secretary Lutnick said tax bill passage is expected within the next week or two, adding that the China deal was “signed and sealed” two days ago. Lutnick stated that several deals will be announced in the coming week, with the Europe deal expected at the end. He noted that although Europe had a sluggish start, it is now performing excellently and there is optimism about a deal with the EU. Countries seeking further negotiations are welcome, and all nations will be categorised into appropriate tariff groups by the 9 July deadline for reciprocal tariff agreements. He added that the US is close to finalising a deal with India and that the tariff programme will not need to change if the bill is adjusted.

- German Chancellor Merz said von der Leyen proposed the creation of a new European trade organisation, and added that EU leaders are largely united on finalising the Mercosur trade deal.

- Chinese Foreign Ministry says Yi will travel to EU headquarters June 30th for China-EU high-level strategic dialogue; will also visit Germany and France.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly firmer for a bulk of the session following gains on Wall Street amid expectations of a future Fed Chair more aligned with the President. Sentiment was further supported after US President Trump announced he had signed a deal with China on Wednesday. Although initial reports were unclear and caused some confusion, White House officials later clarified that the signing finalised what had previously been agreed upon in Geneva and London. China has not yet confirmed the signing of the deal. APAC stocks later waned off best levels to trade mixed. ASX 200 was supported by the broader mood, with the rise in copper keeping miners propped up before paring back. Nikkei 225 outperformed across the region, buoyed by recent JPY weakness and a softer-than-expected Tokyo Core CPI reading, which could temper some of the recent hawkish rhetoric from BoJ’s Tamura. Hang Seng and Shanghai Comp opened with modest gains, drawing some support from US President Trump’s announcement of a signed deal with China. It was later clarified the deal finalised prior agreements made in Geneva and London, though China has yet to confirm the signing. Chinese bourses later turned flat.

Top Asian News

- The PBoC injected CNY 525.9bln via 7-day reverse repos, maintaining the rate at 1.40%.

- Japanese Finance Minister Kato said they will continue cautious consideration of potential buybacks of previously issued bonds, according to local Reuters.

- The South Korean government held an emergency meeting on household debt, and plans to strengthen measures to control it, according to the financial regulator.

- Li Auto (2015 HK) expects to deliver circa 108k vehicles in Q2 (vs. May 29th guidance of 123-128k).

European bourses (STOXX 600 +1%) opened with a strong positive bias and continued to trudge higher as the morning progressed – currently trading at session highs. Sentiment over the past couple of days has been boosted by; 1) Thursday’s report that Trump is looking to announce Powell’s replacement early, 2) WSJ reports that the EU is considering lowering tariffs on US imports in a bid to woo US President Trump, 3) von der Leyen suggesting the EU had received the latest US trade proposal – stressing that whilst they are ready for a deal, they have made preparations for no deal. European sectors are entirely in the green. Autos leads, followed by Consumer Products as the likes of Adidas (+4%) and Puma (+5%) benefit from Nike’s post-earning strength.

Top European News

- ECB’s Knot, when asked about market expectations of one more 25bps cut by the end of the year, Knot said that possibility was “difficult for me to exclude”, via FT.

- German minimum wage to increase to EUR 14.60/hr by 2027; will take place via two steps from current level of EUR 12.82.

- ECB’s de Guindos says the ECB is on track to meet its 2% inflation target

FX

- DXY has extended its losing streak to a fifth session as a combination of geopolitical tensions easing, declining yields, concerns over Fed independence and ongoing fiscal concerns act as a drag on the greenback. Over the past 24 hours, the trade agenda has reasserted itself on the market narrative after US President Trump said he signed a deal with China on Wednesday; it was later clarified that the US and China have agreed to an additional understanding to implement the Geneva agreement. DXY is currently contained within Thursday’s 96.99-97.60 range, into US PCE and a couple of Fed speakers.

- EUR is firmer vs. the USD amid some encouragement on the trade front for the EU. This comes after the WSJ reported that the EU is reportedly considering lowering tariffs on US imports in a bid to woo US President Trump. Furthermore, US Commerce Secretary Lutnick said that although Europe had a sluggish start, it is now performing excellently and there is optimism about a deal with the EU. That being said, European Commission President von der Leyen said the EU is prepared for both a deal and a no-deal outcome, stating all options remain on the table. EUR/USD currently trading around 1.1715.

- JPY is still struggling to make much headway vs. the USD relative to other peers with Japanese data overnight acting as a headwind for the Yen. National inflation data for June came in soft on a headline and core basis (retail sales were also weak). USD/JPY is currently tucked within Thursday’s 143.75-145.26 range and sat just above its 50DMA at 144.32.

- GBP is a touch firmer vs. the USD and steady on a 1.37 handle. It has been a week lacking in fresh macro drivers for the UK and that remains the case. There has been some attention on the political scene with UK PM Starmer facing a possible rebellion from his own MPs over proposed welfare cuts. Cable is currently tucked below Thursday’s multi-year high at 1.3770.

- Antipodeans are both marginally stronger vs. the USD alongside the positive risk tone and subsequently shrugging off a contraction in Chinese Industrial Profits. Both currencies are also likely being underpinned by the aforementioned developments between the US and China on the trade front. Albeit, details remain light at this stage.

Fixed Income

- A contained/slightly softer start to the day for USTs. Benchmark pulling back from Thursday’s 112-03 MTD high, but only marginally with the current trough at 111-26+, comfortably clear of Thursday’s 111-21 base. Focus overnight has been on the latest US-China framework agreement, but essentially just firming the prior Geneva/London talks. Focus today now turns to US PCE and a couple of Fed speakers.

- Bunds are in-fitting with the above. Under modest pressure in the European morning into the region’s first inflation figures for June. Before those, no reaction to ECB’s Knot who said to the FT that the possibility of a 25bps cut by end-2025 was “difficult for me to exclude”. To recap those HICP metrics, French figures were hotter-than-expected across the board sparking a modest hawkish reaction. Specifically, this sent Bunds down from near the 130.66 high to around 130.44. Spanish figures were a little more mixed, but also held a hawkish skew, taking Bunds to a fresh low of 130.20.

- Gilts opened higher by a few ticks and then extended a handful more to 93.36, catching up to the late-Thursday performance for USTs/Bunds, before conforming to the broader bias and slipping slightly. However, action has been minimal with Gilts comfortably above the 93.00 mark and shy of today and Thursday’s open at 93.32.

- Italy sells EUR 6.5bln vs exp. EUR 5.5-6.5bln 2.70% 2030, 2.95% 2030 & 3.60% 2035 BTP and EUR vs exp. EUR 1.5-2.0bln 2034 CCTeu.

Commodities

- Crude is on a firmer footing today, in what has been a session lacking of pertinent geopolitical updates; more focus on US-China / US-EU trade updates, but details are light at the moment. Price action has been relatively steady throughout the morning, awaiting US PCE later. Brent Aug’25 currently trading around USD 67.20/bbl.

- Spot gold trades with a downward bias, and fails to benefit from the slightly softer Dollar and seemingly continuing to be weighed upon by the relatively calm in the Middle East; currently sits below USD 3.3k/oz.

- 3M LME Copper is unable to benefit from the risk tone. However, while softer, 3M LME Copper is holding onto essentially all of the upside it derived on Monday when it rose by near USD 200 to a USD 9.91k peak. As it stands, the base metal has slipped just below the USD 9.9k mark, but remains on track to close out the week with strong gains after opening it at USD 9.65k.

- The US Energy Department announced that scheduled oil deliveries into the Strategic Petroleum Reserve will be delayed until December, due to maintenance at SPR sites. Of the 15.8mln barrels originally planned through May, only 8.8mln have been delivered so far.

- Goldman Sachs said Brent crude could reach USD 90/bbl by year-end in a Strait of Hormuz disruption scenario, while options markets see a 60% chance Brent stays in the USD 60s in 3 months and a 28% chance it exceeds USD 70.

- Shanghai Warehouse Stocks: Copper -19.26k/T (prev. -1.1k).

Geopolitics

- Iranian Foreign Minister Araqchi said Tehran is assessing whether diplomacy with the US is in its interest, adding that there is currently no understanding for renewed talks with the US. Araqchi dismissed speculation about the resumption of negotiations with the US, saying it should not be taken seriously. There are no plans to receive IAEA Chief Grossi in Tehran, according to Reuters.

- Iran’s representative to the UN said Tehran is open to forming a regional nuclear consortium and exchanging uranium in the event of an agreement with Washington, via Sky News Arabia.

- An explosion occurred at the “Aluf” plant within a complex belonging to the Iranian defence industries in the Republic of Azerbaijan, according to Al Hadath.

- Israeli Prime Minister Netanyahu agreed with US President Trump to end the Gaza war within two weeks, according to Al Arabiya citing Israeli press.

- Israeli Defence Minister warned of further strikes on Iran if it resumes nuclear development, according to Al Arabiya.

- EU leaders agreed to renew existing Russia sanctions for another six months, according to Reuters

US Event Calendar

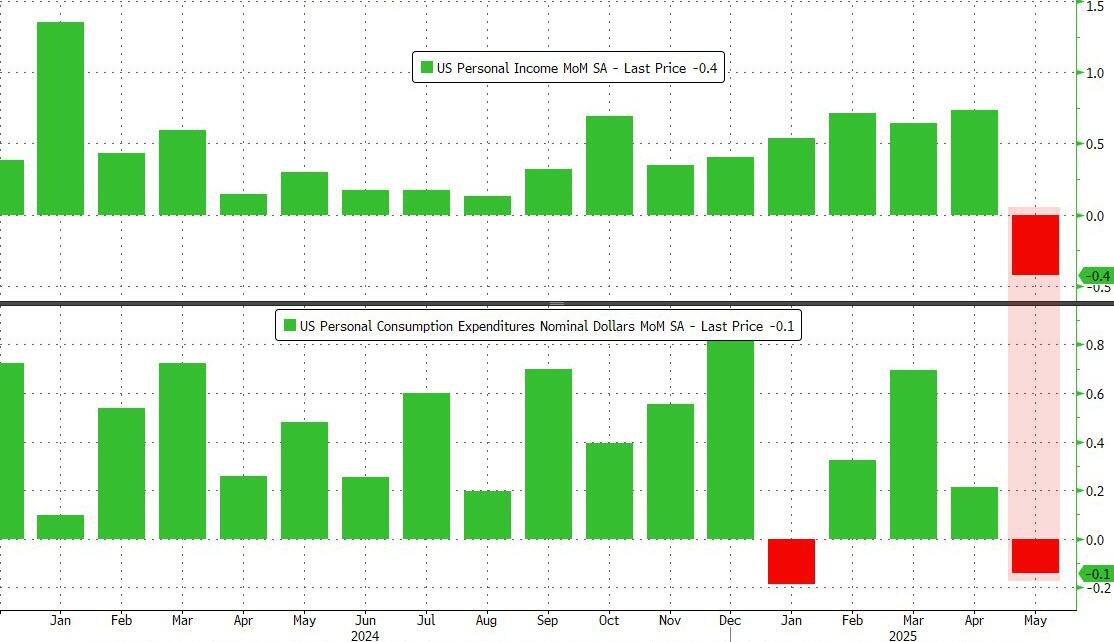

- 8:30am: U.S. Personal Income, May, est. 0.3%, prior 0.8%

- 8:30am: U.S. Personal Spending, May, est. 0.1%, prior 0.2%

- 8:30am: U.S. Core PCE Price Index MoM, May, est. 0.1%, prior 0.1%

- 8:30am: U.S. Core PCE Price Index YoY, May, est. 2.6%, prior 2.5%

- 8:30am: U.S. PCE Price Index MoM, May, est. 0.1%, prior 0.1%

- 8:30am: U.S. PCE Price Index YoY, May, est. 2.3%, prior 2.1%

- 10am: U.S. U. of Mich. Sentiment, June F, est. 60.5, prior 60.5

DB’s Jim Reid concludes the overnight wrap

A rare period of 2025 calm seems to have broken out for now. It may be that we’re in the eye of the storm that was the Middle East, and later to become tariffs again. However for now markets are not thinking about, or are not particularly concerned about, the upcoming July 9th tariff deadline. However after the bell we got some more positive headlines on trade which we’ll detail below. However, even before that, US markets steamed ahead with the first S&P 500 (+0.80%) closing just shy of a new all-time high as investors have again begun to anticipate further rate cuts this year. The optimism for lower borrowing costs in the near term was helped by Tuesday night’s news that Trump is considering naming his pick for the Fed’s next chair early. Even as the White House yesterday suggested that such a nomination was not “imminent”, markets are getting themselves used to the prospect over lower rates going forward. Whether this will prove to be yet another false dawn only time will tell.