JULY 1/FIRST DAY FOR BASEL III RULES: GOLD CLOSED UP $43.85 TO $3339.05 WHILE SILVER ROSE BY $0.21 TO $36.16//PLATINUM ROSE BY $6.75 TO $1346.85 WITH PALLADIUM SHOWING NO GAIN REMAINING AT $1099.60//GOLD COMMENTARY TONIGHT FROM MATHEW PIEPENBERG//IRAN NEWS UPDATES/ISRAEL VS HAMAS UPDATES/WEST BANK UPDATES/RUSSIA VS UKRAINE UPDATES//USA NEWS: A MASSIVE 30 BILLION DOLLAR HEALTH CARE FRAUD EXPOSED//COVID INJURY UPDATES/NEWS ADDICTS//USA MANUFACTURING SURVEYS SOAR//LABOUR ADVANCES AS JOB OPENINGS IN USA SOAR//USA SENATE PASSES THE BIG BEAUTIFUL BILL AND NOW THIS GOES ONTO THE HOUSE//

323 C HSBC 54 332 H STANDARD CHARTERED B 372 363 H WELLS FARGO SECURITI 421 435 H SCOTIA CAPITAL (USA) 1 624 H BOFA SECURITIES 16 661 C JP MORGAN SECURITIES 1058 124 686 C STONEX FINANCIAL INC 7 8 690 C ABN AMRO CLR USA LLC 3 709 C BARCLAYS 91 737 C ADVANTAGE FUTURES 18 8 905 C ADM 9

TOTAL: 1,095 1,095 MONTH TO DATE: 5,307

JPMORGAN STOPPED 124/1095

JULY

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 1095 CONTRACTs NOTICES FOR 109,500 OZ or 3.405 TONNES

total notices so far: 5307 contracts for 530,700 OR 16.506 tonnes)

FOR JULY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 275 NOTICE(S) FILED FOR 1.375 OZ/

total number of notices filed so far this month : 5414 CONTRACTS (NOTICES) for 27.070 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $43.85 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD INTO THE GLD.

INVENTORY RESTS AT 952.53 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.21 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: /// A WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 476.686 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA HUGE SIZED 4126 CONTRACTS TO 162,359 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR SMALL LOSS OF $0.20 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE FINALLY HAVE THE PIERCING OF $34.40 TO 34.50 SILVER PRICE BARRIER. WE HAD A HUGE SIZED LOSS OF 3626 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A STRONG 500 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS AND MONTH END SPREADERS IN COMEX TRADING WITH RESPECT TO MONDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON MONDAY WITH SILVER’S LOSS IN PRICE. THE PRICE FINISHED MILES ABOVE THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE CLOSING AT $35.95 . WE HAVE A HUGE T.A.S. ISSUANCE AT 995 CONTRACTS ISSUED BY THE CME AND THAT STILL SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 34.40 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A HUGE 500 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 995 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TODAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUGE SIZED 3626 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.20. WITH ALL OF THE LOSS DUE TO OUR TWO SPREADER LIQUIDATIONS

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A MEGA HUGE 995 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.20) BUT WERE A LITTLE SUCCESSFUL IN KNOCKING OF SOME NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE LOSS OF 3594 CONTRACTS ON OUR TWO EXCHANGES WITH MOST OF THE LOSS DUE TO OUR 2 SPREADERS.

WE HAD A 500 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 34.730 MILLION OZ PLUS TODAY’S HUGE QUEUE JUMP OF 250,000 OZ//NEW STANDING 34.985 MILLION OZ

THUS:

INITIAL STANDING FOR JULY: 34.985 MILLION OZ

WE HAD:

/ MEGA HUGE COMEX OI LOSS+// A 500 SIZED EFP ISSUANCE (/ VI) A MEGA HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 995 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A TINY 32 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 1 DAY(S), total 500 contracts: OR 2.5 MILLION OZ (500 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 2.5 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 2.50 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4126 CONTRACTS WITH OUR LOSS IN PRICE OF $0.20 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A STRONG 500 CONTRACT EFP ISSUANCE CONTRACTS: 500 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 4 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 34.985 MILLION OZ//

THE NEW TAS ISSUANCE MONDAY NIGHT (995 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE TUESDAY’S TRADING AND BEYOND!

WE HAD 275 NOTICE(S) FILED TODAY FOR 1.375 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1308 OI CONTRACTS TO 434,714 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 395 CONTRACTS //.

WE HAD A FAIR SIZED DECREASE IN COMEX OI (1308 CONTRACTS) . THIS OCCURRED DESPITE OUR GAIN OF $20.00 IN PRICE// MONDAY///.

LAST THREE MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL: 17.847 TONNES. PLUS TODAY’S 1.965 TONNES QUEUE JUMP = 19.888 TONNES STANDING

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 240 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 434,714 /NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 162,359 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1068 CONTRACTS WITH 1308 CONTRACTS DECREASED AT THE COMEX// AND A SMALL SIZED 240 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1068 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1459 CONTRACTS

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(240) ACCOMPANYING THE FAIR SIZED DECREASE IN COMEX OI OF 1308 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 1068 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR JULY AT 17.947 TONNES COUPLED WITH TODAY’S 1.965 TONNES QUEUE JUMP//STANDING ADVANCES TO 19.888 TONNES.

NEW STANDING FOR GOLD, JULY CONTRACT AT 19.888 TONNES OF GOLD.

.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION AS DESPITE HAVING 1)A $20.00 COMEX PRICE GAIN. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THE GAIN IN PRICE AS WE HAD A FAIR LOSS OF 1308 CONTRACTS ON OUR TWO EXCHANGES COUPLED WITH HUGE LIQUIDATION OF OUR TWO SPREADERS // /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY BUT SMALLER FOR JUNE!

4) FAIR SIZED COMEX OI LOSS// 5) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (500 CONTRACTS)/// FAIR T.A.S. ISSUANCE: 1459 T.A.S.CONTRACTS//

JUNE INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 240 CONTRACTS OR 24,000 OZ OR 0.746 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 240 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN1 TRADING DAY(S) IN TONNES 0.746 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS .746 TONNES DIVIDED BY 3550 x 100% TONNES = 0.021% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

AN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 746 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 4126 CONTRACTS OI TO 162,359 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 500 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 500 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 500 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 4126 CONTRACTS AND ADD TO THE 500 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 3636 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.20 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 18.13 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

XXXXX

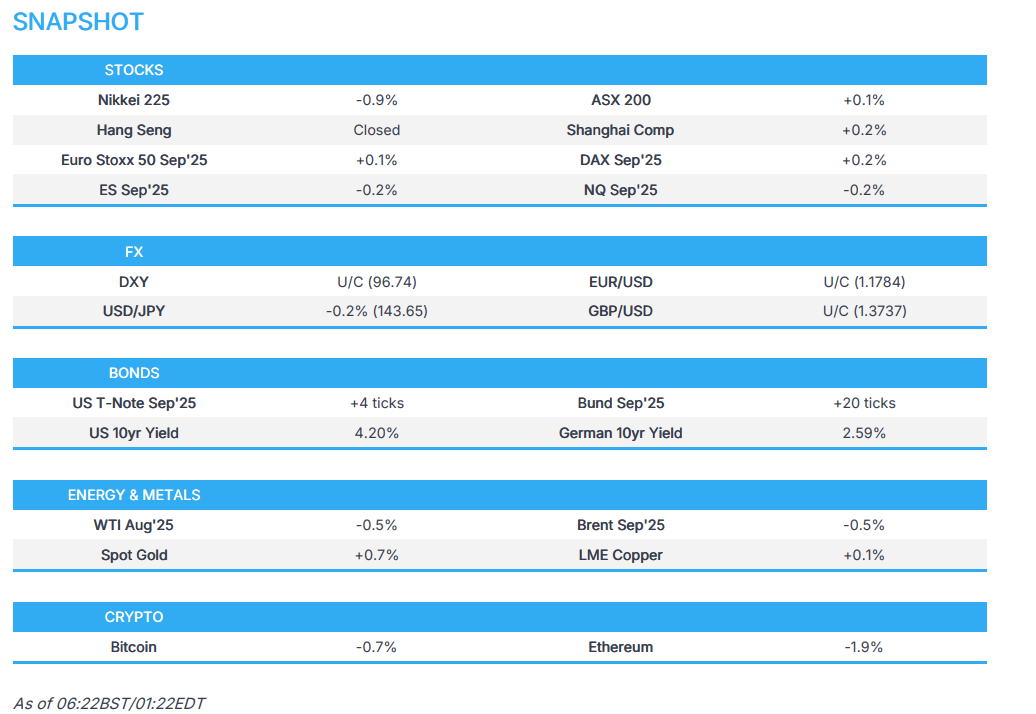

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 13.32 PTS OR 0.39%

//Hang Seng CLOSED

// Nikkei CLOSED DOWN 501.06 PTS OR 0.87% //Australia’s all ordinaries CLOSED DOWN 0.01%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1624 OFFSHORE CLOSED UP AT 7.1605/ Oil UP TO 65.52 dollars per barrel for WTI and BRENT UP TO 67.20 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1624 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1605 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1308 CONTRACTS TO A STILL LOW NUMBER OF 434,714 OI DESPITE OUR GAIN IN PRICE OF $20.00 WITH RESPECT TO MONDAY’S // TRADING. WE LOST MINIMAL NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (240 ). WE HAD HUGE T.A.S. LIQUIDATION ALONG AND HUGE FINALIZATION OF MONTH END CALENDAR SPREADER LIQUIDATION //MONDAY TRADING.

THE CME ANNOUNCED M0NDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES.

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY 0

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 1308 CONTRACTS DESPITE OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF MAY, JUNE AND JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS FAIR AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1459 T.A.S.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING IS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

HOWEVER JULY IS HUGE FOR A NON DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S MASSIVE QUEUE JUMP OF 1.965 TONNES QUEUE JUMP = 19.988 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 19.988 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 32+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 225 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 240 EFP CONTRACT WAS ISSUED: : /AUGUST 2400 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2400 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

HUGE LIQUIDATION OF OUR T.A.S. SPREADERS//HUGE MONTH END SPREADER LIQUIDATION AS WELL

ZERO NET SPEC LIQUIDATION WITH OUR HUGE GAIN IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY MORNING//MONDAY NIGHT WAS A FAIR SIZED, 1459 CONTRACTS.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.THIS WAS SURELY IN EVIDENCE IN TRADING THURSDAY WITH THE SMALL GAIN IN PRICE!

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $20.00/ /) AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED LOSS IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION + CALENDAR SPREADER LIQUIDATION ////MONDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING TODAY. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE LOST A FAIR SIZED TOTAL OF 3.321 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 63,200 OZ OR 1.965 TONNES OF GOLD//NEW STANDING ADVANCES TO 19.888 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $20.00

WE HAD A HUGE 965 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 1068 CONTRACTS OR 106,800 0Z (3.321 TONNES)

Total monthly oz gold served (contracts) so far this month

5307 notices 530,700 oz 16.506TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 0 customer entry

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:

0 ENTRIES

total withdrawal NIL oz

adjustments: 1 ( DEALER TO CUSTOMER ACCTS)

a)BRINKS //dealer to customer acct

96,453.000 oz (3000 kilobars)

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JULY STANDS AT 2182 CONTRACTS FOR A LOSS OF 3580 CONTRACTS. ON MONDAY WE HAD 4212 NOTICES FILED SO WE GAINED A HUGE 632 CONTRACTS OR 63,200 OZ (1.965 TONNES) ENTERTAINED WITH MUCH JOY A HUGE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD

AUGUST GAINED 623 CONTRACTS UP TO 317,771

SEPT LOST 3 CONTRACTS TO 1097

We had 4212 contracts filed for today representing 421,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 1058 notices issued from their client or customer account. The total of all issuance by all participants equate to 1095 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 124 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (5307 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (2182 CONTRACTS) minus the number of notices served upon today (1095 x 100 oz per contract) equals 639,400 OZ OR 19.888 TONNES to which we add 0 tonnes of gold issued under exchange for risk// total standing 19.888 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (5307 x 100 oz +we add the difference for front month of JULY (2182 OI} minus the number of notices served upon today (1095 x 100 oz) which equals 639,400 OZ OR 19.888 TONNES + 0 tonnes EX FOR RISK = 19.888 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 19.888 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

i) Out of Asahi 608,147.700 oz ii) Our of HSBC 308,705/100 oz

total withdrawal 916,852.800 oz

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 190.021 MILLION OZ//.TOTAL REG + ELIGIBLE. 499.695 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 1858 OPEN INTEREST CONTRACTS FOR A LOSS OF 5089 CONTRACTS. WE HAD 5139 CONTRACTS SERVED UPON YESTERDAY SO WE GAINED 50 CONTRACTS OR 250,000 OZ ENTERTAINED A QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST LOST 4 CONTRACTS TO 2369

SEPTEMBER GAINED 737 CONTRACTS UP TO 130,370 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 275 or 1,375,000 oz

CONFIRMED volume; ON MONDAY 47,114 small//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 5414 X5,000 oz = 27.070 MILLION oz

to which we add the difference between the open interest for the front month of JULY (1858) AND the number of notices served upon today (275 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (5414) Notices served so far) x 5000 oz + OI for the front month of JULY(1858) minus number of notices served upon today (275)x 5000 oz equals silver standing for the JULY contract month equating to 34.985 MILLION OZ .

New total standing: 34.985 million oz which is huge for this active delivery month of JULY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.628 million oz of registered silver

JPMorgan as a percentage of total silver: 214.820/501.210 million. 42.71%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

JUNE 20 WITH GOLD DOWN $19.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 947.37 TONNES

JUNE 18 WITH GOLD UP $1.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.03 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 945.94 TONNES

JUNE 17 WITH GOLD DOWN $9.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 941.93 TONNES

JUNE 16 WITH GOLD DOWN $33.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.758 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 940.49 TONNES

JUNE 13 WITH GOLD UP $53.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.38 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 932.91 TONNES

JUNE 12 WITH GOLD UP $55.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 934.19 TONNES

JUNE 11 WITH GOLD UP $1.10 TODAY// SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.31 TONNEES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 935.91 TONNES

JUNE 10 WITH GOLD DOWN $11.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.02 TONNEES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 936.22 TONNES

JUNE 9 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.45 TONNEES OF GOLD FROM THE GLD//: /// ///INVENTORY RESTS AT 934.20 TONNES

JUNE 6 WITH GOLD DOWN $28.00 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

JUNE 2 WITH GOLD UP $80.90 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 930.20 TONNES

MAY 30 WITH GOLD DOWN $27.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.59 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 930.20 TONNES

MAY 29 WITH GOLD UP $22.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 925.71 TONNES

MAY 28 WITH GOLD DOWN $5.30 TODAY// NO CHANGES IN GOLD AT THE GLD:/ ///INVENTORY RESTS AT 925.61 TONNES

MAY 27 WITH GOLD DOWN $63.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 922.46 TONNES

MAY 23 WITH GOLD UP $69.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 923.89TONNES

GLD INVENTORY: 952.53 TONNES, TONIGHTS TOTAL

SILVER

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

JUNE 20 WITH SILVER DOWN $0.83/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.818 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 474.641 MILLION OZ.

JUNE 18 WITH SILVER DOWN $0.20/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 17 WITH SILVER UP $0.67/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 473.096 MILLION OZ.

JUNE 16 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.727 MILLION OZ FROM THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 13 WITH SILVER UP $0.11/NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 473.550 MILLION OZ.

JUNE 12 WITH SILVER UP $0.11/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.276 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 473550 MILLION OZ.

JUNE 11 WITH SILVER DOWN $0.45/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.046 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.274 MILLION OZ.

JUNE 10 WITH SILVER DOWN $0.16/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.232 MILLION OZ.

JUNE 9 WITH SILVER UP $0.69/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.914 MILLION OZ.

JUNE 6 WITH SILVER UP $0.63/HUGE CHANGES AT THE SLV:A DEPOSIT OF 3.863 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.732 MILLION OZ. (A TOTAL DEPOSIT OF 11.856 MILLION PHANTOM OZ IN THE LAST 4 DAYS)

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

JUNE 2 WITH SILVER UP $1.58/NO CHANGES AT THE SLV: ././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 30 WITH SILVER DOWN $0.36/HUGE CHANGES AT THE SLV: A DEPOSIT OF 2.773 MILLION OZ INTO THE SLV././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 29 WITH SILVER UP $0.29/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 28 WITH SILVER DOWN $0.18/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 27 WITH SILVER DOWN $0.34/HUGE CHANGES AT THE SLV//A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 23 WITH SILVER UP $0.38/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.5 MILLION OZ OF SILVER INTO THE SLV/: //INVENTORY AT SLV RESTS AT 454.375 MILLION OZ

Many are wondering if it’s too late to buy gold, that gold has peaked and they have missed their opportunity.

We hope the below series of facts, figures and common-sense reality-checks will put such fears squarely to rest, as gold’s role, price direction and days are only just beginning.

A Light House in the Fog

In a world of geopolitical tensions, can-kicking monetary fantasies, falling bombs, rising debt, discredited leadership, impotent summits, weaponized trade and a comically discredited media narrative, it’s hard to find a lighthouse in such fog.

Even with the world closest to the brink of nuclear war since the Cuban missile crisis, the markets, forever certain that a life-boat of mega liquidity is just one crisis away, churned Titanically forward with no ice berg fears.

VON GREYERZ advisor, Ronnie Stoeferle, sarcastically described the recent S&P, NASDAQ and NIVIDIA behavior as being almost like that of a Zen monk.

But there’s nothing “Zen” about these markets, times, currencies or financial systems. And there’s certainly nothing “Zen” about the once-sacred 10Y UST…

How do we know this? How have we always known this?

In short, what has been our lighthouse?

The answer is as simple as it timeless, indestructible, and honest: Gold.

The Quiet Accumulation Phase

Unlike politicians scrambling for power like donkeys fighting for hay (Chamfort) and squawking threats, promises and miracle solutions for one more X follower, vote or concession, sophisticated gold investors—from generational family offices, portfolio managers and sovereign wealth funds to eastern central banks and even the IMF and BIS—have been quietly accumulating gold at unprecedented levels.

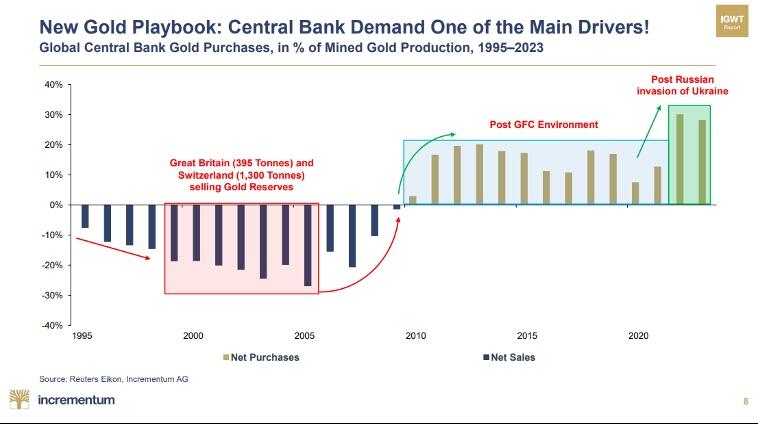

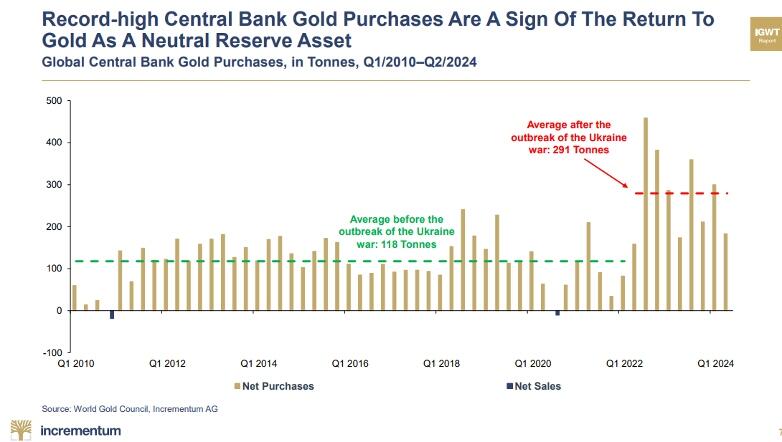

For the last 3 years (since the US foolishly weaponized the world reserve currency), central banks have been annually accumulating over 1000 tons of gold.

Average central bank gold stacking has skyrocketed from 118 tons (pre-2022), to over 290 tons per/bank/year post weaponization.

In short, despite all the fog, squawking, speculating and debating, precious metal investors have been watching what gold does rather than listening to what failed policy makers and systems are saying.

The Unofficial Reserve Currency

Nassim Taleb bluntly said the quiet part out loud in a recent Bloomberg interview, namely that gold is effectively becoming the unofficial global reserve currency.

We have been saying the same for years, not because we fawn on every empty phrase of every empty politico or market pundit, but because we have been watching what gold does.

And let’s look at what gold has been quietly, calmly and historically doing—and SIGNALING—for years.

Signals Rather than Words

In 1971, when the USD lost its golden chaperone, money supply expansion, inflation and hence a gold price explosion followed, held in check only by Volcker’s aggressive, post-1980 rate hikes.

Even the Great Financial Crisis of 2008, in which gold ultimately out-hedged a perfect market storm, the only thing to “save” that not-so-Zen equity market was Bernanke’s money printing to the moon.

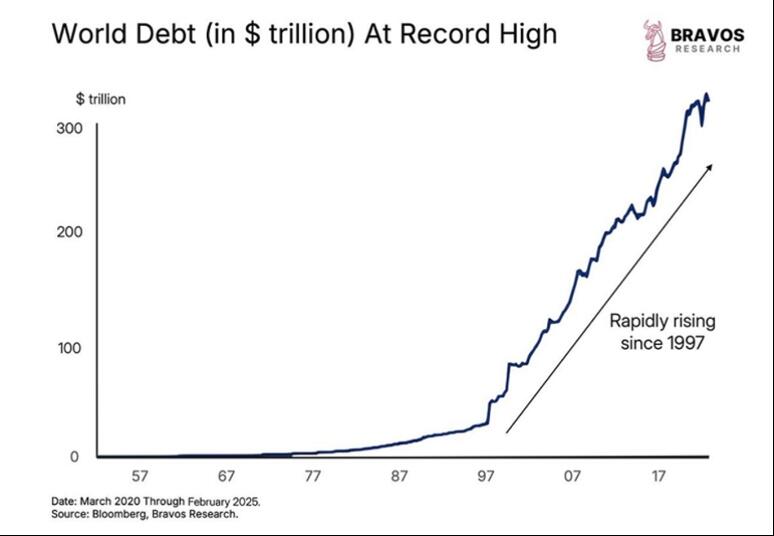

But as US public debt levels crawl toward $37T, we objectively know (and knew from day-one) that raising rates wouldn’t work for Powell as they did for Volcker, and hence Powell’s “higher-for-longer” policies were doomed from the onset by the hard math of fiscal dominance.

Or stated more simply, America was too far in debt to afford its own so-called “inflation killing” rate hikes.

We also know that QE to the moon is another useless option, and that Bernanke’s Nobel Prize for such a “temporary” solution has since devolved into a currency destroying nightmare.

In short, the Fed is Trapped. Cornered. Out of good options.

Period.

More Recent Signs of Golden Power

But there are far more current yet ignored signals from that modest pet rock, which has been quietly getting the last laugh on a global system that is loudly getting more desperate and hence more centralized.

From Day-One of the Putin sanctions, we said that trust in, and hence demand for, the dollar and UST would fall as gold slowly rose to replace this mistrust.

We also carefully tracked the critically important move by the BIS to rate physical gold as a Tier-One, global reserve asset.

This was another quiet, yet media-ignored BIS signal, that gold was becoming a far more trusted and objectively superior store of value that an over-issued and increasingly weaponized/unloved UST.

This was neon-flashing evidence that nations preferred physical gold to paper money or unloved US IOUs.

The Old System Nearing Its Gettysburg Moment

Such signals from the BIS, the COMEX, and the BRICS de-dollarization policies were analogous to armies slowly preparing their financial cannons for a massive shift in a global monetary and financial system.

Sadly, yet objectively, this very system– unknown to most participants and trend speculators—was already reaching a clear Gettysburg Moment in which the fight to save it may continue, but the war is already lost.

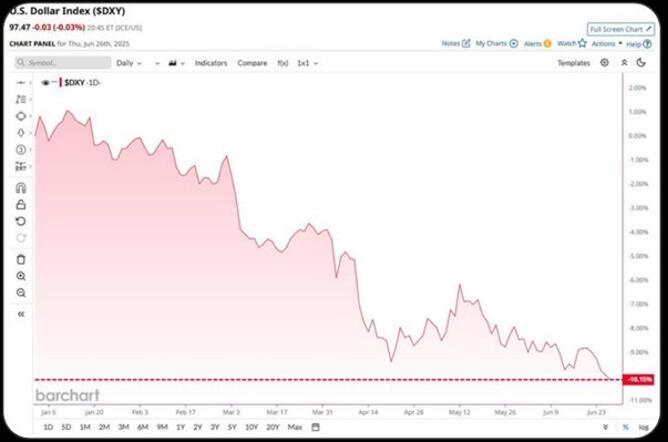

The Biggest Casualty? The USD…

Today we see the desperate signs of this losing war in the desperate measures to give credit to an otherwise discredited and debased world reserve currency which even JP Morgan confesses is 15% over-valued based on long-term real exchange rates.

This year alone, the USD has lost 10% of its power and is seeing its worst first-half performance in nearly 40 years.

Meanwhile the EUR-USD is nearing 1.17 and gold is consolidating.

Too Late for Gold?

But despite all these signals of gold rising (more than 75 All-Time-Highs in 2025 alone and outperforming the S&P total return for two decades), there are those who would say gold is too volatile or that it peaked at $3500.00.

In other words, there are those who think it’s too late to catch “the gold bubble”?

Oh dear… what a complete misunderstanding of reality, markets, gold and broken financial systems such a view embodies.

Gold: No Mania, just a Sober Culmination

Gold is not in a bubble.

Gold is not to be compared to a tech stock or a speculation craze, and gold is no longer even a volatility “hedge” or “allocation.”

Rather, gold is becoming the base money for a system that is openly denying its own slow death and losing war.

In other words, gold’s exponential growth and role are not peaking, they are only just beginning.

But let’s show rather than say that, as words have become just as cheap as dollars in a system terrified of its own unravelling.

Gold is not spiking because the future of the global financial system and paper currencies is looking brighter.

Instead, and based on the string cite of signals above, gold is rising because that very debt-based, MMT-fantasy pushing addiction to mouse-clicked money and debt-based (currency-destroying) “growth” is failing.

Trust: Hard to Quantify but Easy to Own

The recent and extraordinary (but entirely inevitable) “rally” in the gold price had nothing to with its yields or earnings (it offers none), but everything to do with its trust.

Or stated otherwise, Gold is not changing, but trust in the global financial and currency system is.

Gold is doing nothing other than what it has done for millennia when debt levels unmask the sins and addictions of its fiat money comptrollers: It is signaling a slow reset toward real money from paper currencies.

In such moments of dramatic global change, looming resets and embarrassing policy failures, the old correlations break down.

Strong dollar or weak dollar, low inflation or high inflation, positive real yields (2023,24 & 25) or negative real yields—gold is rising in all scenarios because gold is breaking away from a broken system that has printed, borrowed, taxed and even traded itself into debt trap.

Who Is Afraid?

Yes, gold loves chaos, but today it’s not Main Street that is running to gold, it is the very central bankers who are terrified of the chaotic system they alone created and broke which are running to this metal.

In short, it’s not the people who are scared—it’s their governments.

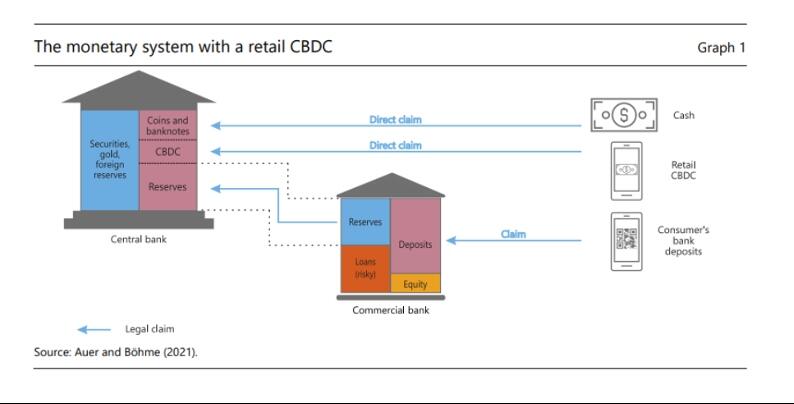

Even the IMF, which has recently admitted that it doesn’t fully know what is coming, at least knows that whatever (even horrific CBDC) reset arises, it will have gold (the last truly politically neutral asset in a global financial war) as its anchor rather than a hitherto chastised “pet rock.”

And so, in this backdrop of reality rather than spin, we ask again, is it too late to buy gold?

Silver Speaks

In addition to the foregoing reality checks and answers, let us not forget what silver is saying to us.

Those familiar with long-term, sophisticated precious metal investing are well aware that rising silver (and mining stocks) confirm a bull market in gold, which we argue has not yet even begun despite gold’s recent record highs.

As of this writing, the gold/silver ratio still hovers in the 100:1 area and silver ETF inflows are yawning.

In short, silver, despite its steady movements North, is still greatly lagging the gold moves of late, suggesting that gold has yet to make its true move in price, role and use.

Today silver lags, but when it moves, its move will be explosive.

For us, the current silver lag is a sign that gold is still early rather than too late in its secular direction.

Peak Distrust, Not Peak Gold

The recent gold price tops at $3500 were not a sign of mania or peak gold, but simply an early indicator (and reflection) of the rotten debt foundations beneath a global credit and currency system slowly teetering toward a massive shift.

In such a setting/shift, gold’s value today is merely a fraction of what is to come.

For those thinking beyond the next equity trend or miracle stock toward protecting and growing their wealth, they are not even close to “too late,” but rather right on time.

END

ALASDAIR MACLEOD…

3. CHRIS POWELL AND GATA DISPATCHES

4. ANDRE MAGUIRE/LIVE FROM THE VAULT KINESIS 229

5. COMMODITY REPORT…COPPER

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 13.32 PTS OR 0.39%

//Hang Seng CLOSED

// Nikkei CLOSED DOWN 501.06 PTS OR 0.87% //Australia’s all ordinaries CLOSED DOWN 0.01%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1624 OFFSHORE CLOSED UP AT 7.1605/ Oil UP TO 65.52 dollars per barrel for WTI and BRENT UP TO 67.20 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1624 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1605 AGAINST US DOLLAR/ AND THUS STRONGER

END

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1624 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1605 (CCP MANIPULATED)

SHANGHAI CLOSED UP 13.32 PTS OR 0.39%

HANG SENG CLOSED

2. Nikkei closed UP 501.06 PTS OR 1.24%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 96.20/ EURO RISES TO 1.1809 UP 23 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.391//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.98…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5510/Italian 10 Yr bond yield DOWN to 3.458 SPAIN 10 YR BOND YIELD DOWN TO 3.198%

3i Greek 10 year bond yield DOWN TO 3.285

3j Gold at $3352.25 Silver at: 36.42 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 31 /100 roubles/dollar; ROUBLE AT 78.61

3m oil (WTI) into the 65 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.98// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.391% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7897 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9366 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.266 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.757 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.727 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 39.85

10 YR UK BOND YIELD: 4.4310 DOWN 6 PTS

10 YR CANADA BOND YIELD: 3.272 DOWN 4 BASIS PTS

5 YR CANADA BOND YIELD: 2.824 DOWN 3 PTS

2a New York OPENING REPORT

Futures Drop As Trade Concerns, Trump-Musk Feud Returns

Tuesday, Jul 01, 2025 – 08:36 AM

US equity futures – which closed at a fresh all time high after the best quarter since 2023 put them in extremely overbought territory – are weaker, dragged by Tech as TSLA is -5% pre-mkt on Musk vs Trump part 2. Pre-mkt, the balance of Mag7 is mixed with Staples outperforming. As of 8:00am, S&P futures are down 0.2% following two successive closes at all-time highs as sentiment remains linked to progress of trade negotiations and the fate of President Trump’s tax and spending bill, which the Senate has failed to pass. Nasdaq futures also drop 0.3% while European stocks also fell. Bond yields are lower as the curve flattens with USD continuing to decline, setting another 52-wk low. As discussed yesterday, the dollar had its worst H1 since 1973 while SPX has its best quarter since 23Q1. Commodities are weaker although gold is soaring. Today is the first piece of the labor market puzzle with JOLTS but we also receive ISM-MFG and vehicle sales. Powell speaks at 9.30am. The voting process on the tax/budget bill continues.

In premarket trading, Tesla falls 5% after President Donald Trump lashed out at Elon Musk, accusing the Tesla and SpaceX chief executive officer of benefiting excessively from government subsidies for electric vehicles.Other Mag7 stocks are mixe ( Apple +0.4%, Amazon +0.05%, Alphabet -0.03%, Meta -0.01%, Microsoft +0.07%, Nvidia -0.7%). Here are some other notable premarket movers:

US-listed Macau casino operators are trading higher premarket Tuesday, after monthly gaming revenue for the world’s biggest gambling hub exceeded analyst expectations in June. Wynn Resorts (WYNN) +3.9%, Las Vegas Sands (LVS) +4%

AeroVironment Inc. (AVAV) falls 5% after the defense company announced proposed underwritten public offerings of $750m worth of shares of its common stock and $600m aggregate principal amount of its convertible senior notes due 2030.

Dyne Therapeutics (DYN) drops 11% after the company offered around 24.2 million shares, raising around $200 million. The offering was priced at $8.25 per share, representing a discount of around 13.3% vs. Monday’s closing price of $9.52.

Greif (GEF) climbs 1.6% after agreeing to sell its containerboard business to Packaging Corporation of America (PKG) for $1.8b in cash.

MSC Industrial (MSM) rises 3% after the distributor of metalworking products posted adjusted earnings per share for the third quarter that beat the average analyst estimate.

Sweetgreen (SG) drops 3% as TD Cowen downgrades to hold, saying the salad restaurant chain’s key urban footprint “appears to be under extreme pressure.”

Wolfspeed (WOLF) surges 73% after the chipmaker said it would file for bankruptcy to enact a creditor-backed plan to slash $4.6 billion in debt. The company filed for reorganization under Chapter 11 and expects to emerge out of bankruptcy by the end of the third quarter.

Until this morning, stock bulls had seized control of a market that was rattled by Trump’s trade overhaul, a war in the Middle East and persistent uncertainty over growth and inflation. Yet unpredictability persists, with US trade talks racing toward a July 9 deadline and Trump pushing to finalize a budget that’s projected to add more than $3 trillion to the US deficit over the next decade.

“We’ve had a strong quarter, but there’s still too much on the table,” said Haris Khurshid, chief investment officer at Karobaar Capital. “If the trade talks drag or the tax bill stalls, we’ll see how much conviction these bulls really have.”

Trade talks hit a snag after Japan said it would not sacrifice its agricultural sector as part of its tariff talks with the United States, after President Donald Trump complained that the key Asian ally was not buying American rice. That won’t help Japan’s auto sector which is already reeling amid widespread cost cuts to remain competitive in the US market.

As discussed yesterday, Goldman’s flow gurus noted the S&P 500 will add to its rally this month before losing steam into August. “We are entering the strongest month for the S&P historically,” they said, noting that the first two weeks of the months are traditionally the best span of the year for stocks.

While economists are widely expecting Trump’s tariffs to drive inflation higher, subdued price growth so far has cast doubt on that view, emboldening the White House and increasing its pressure on Jerome Powell. Although the Fed has so far held off on cutting interest rates, two governors have recently publicly diverged from Powell, suggesting a reduction could be appropriate as early as July. Swaps imply at least two quarter-points of monetary easing by the end of the year, with an about 65% chance of a third cut by December.

“The bulk of the market sees July as a live meeting, that’s limiting the dollar,” Geoffrey Yu, a strategist at Bank of New York Mellon Corp., told Bloomberg TV. “Going back to the other asset classes, the fact that July is live and we may get two cuts at least this year, that is underpinning risk sentiment as well.”

Powell and other top central bankers are set to discuss monetary policy at the European Central Bank’s annual retreat later on Tuesday in Portugal. Also on investors’ radar is a slew of economic data, including a wave of PMI readings and the US job openings report ahead of Thursday’s nonfarm payrolls.

“On balance, we see the environment as constructive for risky assets,” noted Mohit Kumar, chief European strategist at Jefferies International. “But with positioning moving to the long side, we do not see a sharp rally but a slow grind higher in risky assets.”

Europe’s Stoxx 600 falls 0.3%, with media and auto shares among the biggest laggards. In individual stocks, Umicore shares rise after the firm boosted its Ebitda guidance. Here are the most notable European movers:

Umicore gains as much as 12%, hitting the highest since late-July 2024, after the materials technology company lifted its adjusted Ebitda guidance for the full year to a range of €790m to €840m.

Zealand Pharma shares rise as much as 5.1%, the most in six weeks, after BNP Paribas Exane analysts initiated coverage on the stock with an outperform recommendation, saying the “attractive” risk-reward at current levels is “difficult to ignore.”

Jeronimo Martins shares surge as much as 5.7%, most since May 8, after Citi upgraded the retailer to buy, citing expectations of a rebound in the Polish food market.

Elixirr shares rise as much as 6.5% after the business management consulting firm completed its move to the London Stock Exchange’s Main Market from AIM.

Baloise and Helvetia gain after UBS lifted recommendations on both stocks to buy from neutral, citing a potential 20% uplift in cash generation from the proposed merger.

Mpac Group plunges as much as 34%, after the packaging and support services company warned annual revenue will be significantly below expectations because tariff uncertainty is causing US customers to defer orders.

InPost drops as much as 6.1% to lowest since April 17 as Advent International sold a 3.5% stake in company via accelerated book-building at a discount to Monday’s closing price.

VusionGroup shares fall as much as 7.9% to €252.6 after the French consumer electronics firm’s offering of 650,000 shares by holder Walmart priced at a discount.

UK homebuilders underperform after data showed house prices fell the most in more than two years in June, in a sign buyers are under pressure after an increase in transaction taxes in April.

Earlier in the session, Asian equities advanced, after halting a four-day rally Monday, as Taiwan saw a strong rebound and South Korean stocks climbed. The MSCI Asia Pacific Index rose 0.4%, putting the index on pace for its highest close since September 2021. Shares of TSMC, Hon Hai and Reliance Industries contributed the most the benchmark’s gains. Taiwanese stocks jumped on a tech rally and bounce in the local currency. Singapore’s Straits Times Index was on pace for a record high. Holding companies helped drive gains in Korea on optimism that legal revisions will be approved this week to help speed corporate reforms.

In FX, the Bloomberg Dollar Spot Index falls 0.4% to the lowest since March 2022 while perceived safe-haven assets outperform, as investors monitor progress on trade talks and wrangling in Washington over President Donald Trump’s tax bill. The yen is leading gains against the greenback in the G-10 sphere, rising 0.8% with the Swiss franc not far behind. The euro is on the verge of its longest winning streak against the greenback in more two decades. The common currency gained as much as 0.4% to $1.1829, and a higher close would extend its rally to a ninth straight day, the longest stretch since 2004.

In rates, treasuries extend Monday’s advance, with yields falling by 2bp to 4bp across tenors, led by euro-zone bonds after ECB’s Martins Kazaks said significant gains for the currency could warrant another rate cut. US yields are lowest since early May, the 10-year under 4.19% for the first time since May 1 but trailing steeper drops for UK and German counterparts. European bonds also advance, led by longer-dated maturities. UK and German 30-year yields fall 6-7 bps each. Gilts got a boost after Bank of England Governor Andrew Bailey said they are looking at the possibility of offloading fewer government bonds over the coming year. A long list of ECB speakers provided few surprises while euro-area inflation rose as expected and was also largely ignored. Among Tuesday’s events are a global monetary policy panel in Sintra that includes Fed Chair Jerome Powell.

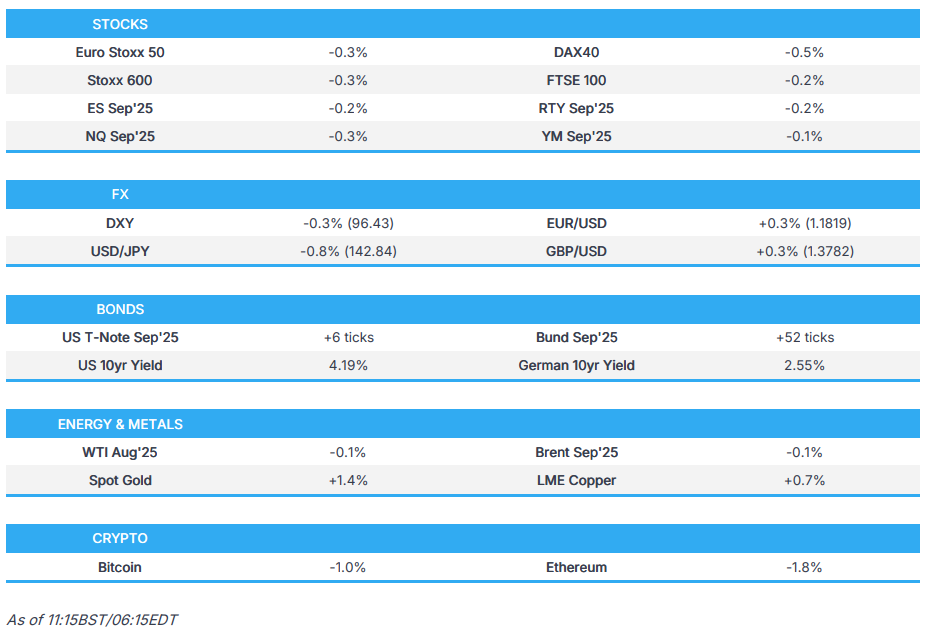

In commodities, oil prices are steady with WTI near $65 a barrel; spot gold climbs $40 to around $3,344/oz.

Looking at today’s calendar, US economic data slate includes June final S&P Global US manufacturing PMI (9:45am), June ISM manufacturing, May construction spending and May JOLTS job openings (10am) and June Dallas Fed services activity (10:30am). Fed speakers are limited to Powell’s Sintra panel (9:30am), which also includes BOE Governor Andrew Bailey, ECB President Christine Lagarde, BOJ Governor Kazuo Ueda and Bank of Korea Governor Chang Yong Rhee

Market Snapshot

S&P 500 mini -0.2%

Nasdaq 100 mini -0.2%

Russell 2000 mini -0.2%

Stoxx Europe 600 -0.2%

DAX -0.3%, CAC 40 -0.3%

10-year Treasury yield -3 basis points at 4.19%

VIX +0.3 points at 17.06

Bloomberg Dollar Index -0.3% at 1186.29

euro +0.2% at $1.1816

WTI crude little changed at $65.16/barrel

Top Overnight News

Musk resumes his campaign against the reconciliation bill, vowing to start a third party and launch primary campaigns against Republicans who vote for it. Tesla shares (-4%) slid premarket after Donald Trump accused Elon Musk of benefiting excessively from EV subsidies, suggesting the Department of Government Efficiency should take a look at his companies. NYT, BBG

Moderate Republicans and hard-line conservatives in the House are expressing increasing opposition to the Senate’s version of the “big, beautiful bill” just days before the lower chamber is set to consider the legislation, a daunting dynamic for GOP leaders as they race to meet their self-imposed Friday deadline. The Hill

US Senate parliamentarian has ruled that Sen. Murkowski’s Alaska carve-out for SNAP is compliant with the Byrd Rule, but the Medicaid one is not compliant, via Punchbowl’s Desiderio.

US Senate votes 99-1 to remove the AI state regulation moratorium from the Reconciliation Bill (i.e. Senate adopts Blackburn’s amendment).

Punchbowl reports US Senate Majority leader Thune said, “We’re getting to the end here.”, adds It’s unclear if Thune has the votes necessary for passage, or if he’s prepared to plow ahead with a final vote anyway.

Punchbowl reports the House Rules Committee is “slated to come at noon to begin to prepare the bill for floor consideration. The full House is expected back Wednesday.”

Trump’s top trade officials are scaling back their ambitions for comprehensive reciprocal deals with foreign countries, seeking narrower agreements to avert the looking reimposition of US tariffs. People familiar wit the talks said US officials were seeking phased deals with most engaged countries as they race to find agreements by July 9 deadline. FT

A private gauge of China’s manufacturing activity bounced back into expansionary territory in June, as a temporary trade truce between Beijing and Washington eased some pressures on Chinese factories. The Caixin manufacturing purchasing managers index rose to 50.4 in June from 48.3 in May. WSJ

UK house prices fell the most in more than two years in June, Nationwide said, as an increase in transaction taxes piled pressure on buyers. It leaves prices just 2.1% above the level seen a year ago, a fall in real terms. WSJ

Japan will not sacrifice the agricultural sector as part of its tariff talks with the United States, its top negotiator said on Tuesday, after President Donald Trump complained that the key Asian ally was not buying American rice. RTRS

Eurozone inflation expectations cool, with 12-months falling to +2.8% (down 30bp) and 36-months easing to +2.4% (down 10bp). ECB’s Lane says the battle to bring Eurozone inflation back to the 2% target is complete. BBG

UK house prices fell the most in more than two years in June, Nationwide said, as an increase in transaction taxes piled pressure on buyers. It leaves prices just 2.1% above the level seen a year ago, a fall in real terms.

DOGE officials at the SEC have in recent weeks sought meetings with staff to explore loosening regulations on SPACs and reporting requirements for private investment advisers, Reuters reported. BBG

Trade/Tariffs

US narrows trade focus to secure deals, while officials were seeking phased deals with the most engaged countries as they race to find agreements by July 9th, according to FT.

Japan’s Chief Cabinet Secretary Hayashi said Japan won’t do anything to sacrifice the agricultural sector in US trade talks, while Farm Minister Koizumi said he won’t comment on US President Trump’s posts regarding Japan’s rice imports.

EU is to accept Trump’s universal tariff but seeks key exemptions and it wants the US to commit to lower rates on key sectors such as pharmaceuticals, alcohol, semiconductors and commercial aircraft, while it is pushing for quotas and exemptions to effectively lower a 25% tariff on automobiles and car parts as well as a 50% tariff on steel and aluminium, according to Bloomberg.