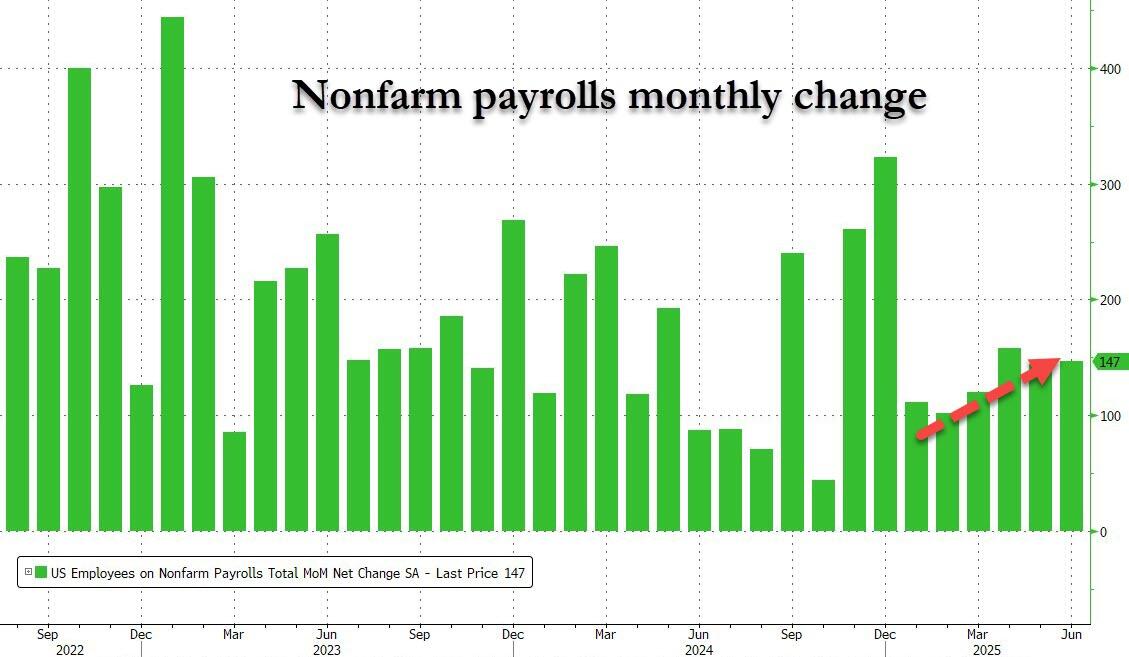

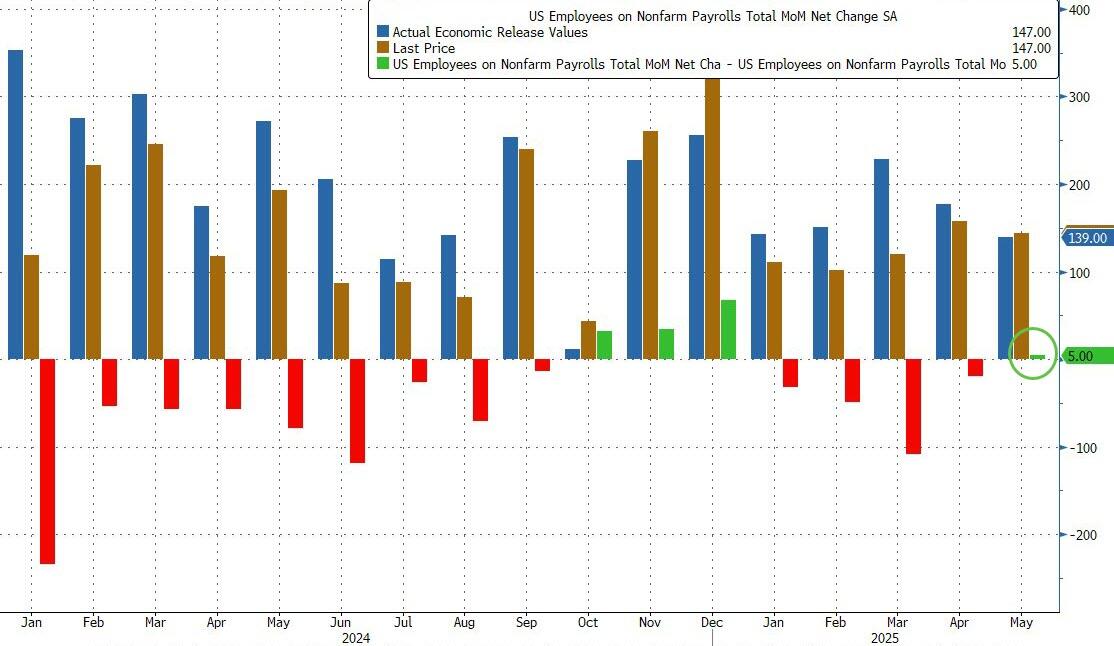

JULY 3/OUR USUAL AND CUSTOMARY RAID ON NON FARM PAYROLL REPORT: SUPPOSEDLY A STRONG REPORT WITH 147,000 JOBS ADDED//GOLD CLOSED DOWN $15.40 TO $3332.60 BUT SILVER REFUSED TO BUCKLE RISING BY 34 CENTS TO $36.86//PLATINUM FELL BY $38.95 WHILE PALLADIUM FELL BY $7.95 T $1148.00//GOLD COMMENTARY TONIGHT FROM PETER REAGAN AND ALASDAIR MACLEOD//FROM GERMANY THE BAN OF AN AfD PARTY GETS CLOSER AND CLOSER!//UPDATES ON THE IRAN VS ISRAEL CONFLICT//WE SEEM TO BE GETTING CLOSER TO A CEASEFIRE BETWEEN ISRAEL AND HAMAS//RELATIONS BETWEEN AZERBAIJAN AND RUSSIA FALLING APART//COVID UPDATES/VACCINE INJURY REPORT//NEWS JUNKIES/NEWSWIZE/EVOL NEWS//THE BIG BEAUTIFUL BILL IN FINAL STAGES BEFORE PASSING//SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 104 323 H HSBC 766 332 H STANDARD CHARTERED B 233 363 H WELLS FARGO SECURITI 245 435 H SCOTIA CAPITAL (USA) 1 624 H BOFA SECURITIES 10 661 C JP MORGAN SECURITIES 77 686 C STONEX FINANCIAL INC 6 20 700 C UBS SECURITIES LLC 7 709 C BARCLAYS 57 737 C ADVANTAGE FUTURES 9 17 880 C CITIGROUP 10

TOTAL: 781 781 MONTH TO DATE: 6,459

JPMORGAN STOPPED 77,781

JULY

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 781 CONTRACTs NOTICES FOR 78,100 OZ or 2.439 TONNES

total notices so far: 6459 contracts for 645,900 OR 20.096 tonnes)

FOR JULY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 195 NOTICE(S) FILED FOR 0.975 million OZ/

total number of notices filed so far this month : 6109 CONTRACTS (NOTICES) for 30.545 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $15.40 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD.

INVENTORY RESTS AT 947.66 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.34 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: /// A WITHDRAWAL OF 0.917 MILLION OZ OUT OF THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 477.313 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A VERY STRONG SIZED 637 CONTRACTS TO 164,204 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0.36 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE FINALLY HAVE THE PIERCING OF $34.40 TO 34.50 SILVER PRICE BARRIER. WE HAD A HUGE SIZED GAIN OF 1113 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A STRONG 476 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO WEDNESDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON TUESDAY WITH SILVER’S GAIN IN PRICE. THE PRICE FINISHED MILES ABOVE THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE CLOSING AT $36.52 . WE HAVE A HUGE T.A.S. ISSUANCE AT 965 CONTRACTS ISSUED BY THE CME AND THAT STILL SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 34.40 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A STRONG 476 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 965 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TODAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 1113 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.36.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A MEGA HUGE 965 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.36) AND WERE UNSUCCESSFUL IN KNOCKING OF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE GAIN OF 1142 CONTRACTS ON OUR TWO EXCHANGES

WE HAD A 476 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 34.730 MILLION OZ PLUS TODAY’S HUGE QUEUE JUMP OF 865,000 OZ//NEW STANDING ADVANCES TO 35.695 MILLION OZ

THUS:

INITIAL STANDING FOR JULY: 35.695 MILLION OZ

WE HAD:

/ VERY STRONG COMEX OI GAIN+// A 476 SIZED EFP ISSUANCE (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 965 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 0 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 3 DAY(S), total 1571 contracts: OR 7.855 MILLION OZ (523 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 7.855 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 7.855 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 637 CONTRACTS WITH OUR GAIN IN PRICE OF $0.36 IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. . THE CME NOTIFIED US THAT WE HAD A STRONG 476 CONTRACT EFP ISSUANCE CONTRACTS: 476 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 4 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 35.695 MILLION OZ//

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (965 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE THURSDAY’S TRADING AND BEYOND!

WE HAD 195 NOTICE(S) FILED TODAY FOR 0.975 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1047 OI CONTRACTS TO 438,709 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A MAMMOTH 8843 CONTRACTS //.

WE HAD A FAIR SIZED INCREASE IN COMEX OI (1047 CONTRACTS) . THIS OCCURRED WITH OUR GAIN OF $8.95 IN PRICE// WEDNESDAY///.

LAST THREE MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0.0279 TONNES QUEUE JUMP = 20.348 TONNES STANDING

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 414 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 438,709 /NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 164,204 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1461 CONTRACTS WITH 1047 CONTRACTS INCREASED AT THE COMEX// AND A SMALL SIZED 414 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1461 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 2097 CONTRACTS

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(414) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 1047 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1461 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR JULY AT 17.947 TONNES COUPLED WITH TODAY’S 0.0279 TONNES QUEUE JUMP//STANDING ADVANCES TO 20.348 TONNES.

NEW STANDING FOR GOLD, JULY CONTRACT AT 20.348 TONNES OF GOLD.

.

/ 3) ZERO T.A.S. LIQUIDATION AS WE HAVE 1)A $8.95 COMEX PRICE GAIN. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THE GAIN IN PRICE AS WE HAD A FAIR GAIN OF 1461 CONTRACTS ON OUR TWO EXCHANGES COUPLED WITH ZERO LIQUIDATION OF OUR SPREADERS // /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY BUT SMALLER FOR JUNE!

4) STRONG SIZED COMEX OI GAIN// 5) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (414 CONTRACTS)/// FAIR T.A.S. ISSUANCE: 2097 T.A.S.CONTRACTS//

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 1404 CONTRACTS OR 140,400 OZ OR 4.367 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 468 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN3 TRADING DAY(S) IN TONNES 4.367 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 4.367 TONNES DIVIDED BY 3550 x 100% TONNES = 0.113% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

AN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 4.367 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG SIZED 637 CONTRACTS OI TO 164,204 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 476 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 476 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 476 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 666 CONTRACTS AND ADD TO THE 476 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1113 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.21 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 5.710 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED UP 6.36 PTS OR 0.18%

//Hang Seng CLOSED DOWN 182.64 PTS OR 0.75%

// Nikkei CLOSED UP 23.42 PTS OR 0.06% //Australia’s all ordinaries CLOSED UP 0.06%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1625 OFFSHORE CLOSED UP AT 7.1584/ Oil UP TO 66.79 dollars per barrel for WTI and BRENT DOWN TO 68.46 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN TRADING AT 7.1625 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1584 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1047 CONTRACTS TO A STILL LOW NUMBER OF 438,709 OI WITH OUR SMALL GAIN IN PRICE OF $8.95 WITH RESPECT TO WEDNESDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (414 ). WE HAD ZERO T.A.S. LIQUIDATION //TUESDAY TRADING.

THE CME ANNOUNCED WEDNESDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES.

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY 0

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1461 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON WEDNESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE IN JANUARY THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND NOW JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS FAIR AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 2097 T.A.S.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

HOWEVER JULY IS HUGE FOR A NON DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S MASSIVE QUEUE JUMP OF 0.027 TONNES QUEUE JUMP = 20.348 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 20.348 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 10+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 229 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 414 EFP CONTRACT WAS ISSUED: : /AUGUST 414 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 414 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//

ZERO NET SPEC LIQUIDATION WITH OUR HUGE GAIN IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY MORNING//WEDNESDAY NIGHT WAS A FAIR SIZED, 2097 CONTRACTS.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.THIS WAS SURELY IN EVIDENCE IN TRADING THURSDAY WITH THE SMALL GAIN IN PRICE!

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0.027 QUEUE JUMP = 20.348 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $8.95/ /) AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD LITTLE T.A.S. SPREADER LIQUIDATION ////WEDNESDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING YESTERDAY. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS

THURSDAY MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OFAPRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE GAINED A STRONG SIZED TOTAL OF 4.54 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S SMALL QUEUE JUMP OF 900 OZ OR 0.027 TONNES OF GOLD//NEW STANDING ADVANCES TO 20.348 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $8.95

WE HAD A HUGE 8843 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 1461 CONTRACTS OR 146,100 0Z (4.54 TONNES)

or 801 withdrawal of 801 London good delivery bars.

ii) Out of Loomis: 15,753.990 oz (490 kilobars)

total withdrawal 336,500.315 oz

10.435 tonnes

Deposit to the Dealer Inventory in oz

1 ENTRY i) Into Brinks: 73,882.998 oz

(2298 kilobars)

Deposits to the Customer Inventory, in oz

0 ENTRY

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

781 notice(s) 78,100 OZ 2.429 TONNES

No of oz to be served (notices)

83 contracts 8300 OZ 0.2581 TONNES

Total monthly oz gold served (contracts) so far this month

6459 notices 645900 oz 20.096 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 1 entry

1 ENTRY i) Into Brinks: 73,882.998 oz

(2298 kilobars)

total deposit 73,882.998 oz

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 2 customer entry

2 ENTRIES

i) Out of JPMorgan enhanced 320,746.325 oz

or 801 withdrawal of 801 London good delivery bars.

ii) Out of Loomis: 15,753.990 oz (490 kilobars)

total withdrawal 336,500.315 oz

10.435 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

adjustments: 0

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JULY STANDS AT 864 CONTRACTS FOR A LOSS OF 362 CONTRACTS. ON WEDNESDAY WE HAD 371 NOTICES FILED SO WE GAINED A SMALL 9 CONTRACTS OR 900 OZ (0.027 TONNES) ENTERTAINED WITH A QUEUE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD

AUGUST LOST 2183 CONTRACTS DOWN TO 314,846

SEPT GAINED 91 CONTRACTS TO 1227

We had 781 contracts filed for today representing 78,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 781 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 77 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (6459 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (864 CONTRACTS) minus the number of notices served upon today (781 x 100 oz per contract) equals 654,200 OZ OR 20.348 TONNES to which we add 0 tonnes of gold issued under exchange for risk// total standing 20.348 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (6459 x 100 oz +we add the difference for front month of JULY (864 OI} minus the number of notices served upon today (781 x 100 oz) which equals 654,200 OZ OR 20.348 TONNES + 0 tonnes EX FOR RISK = 20.348 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 20.338 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

i) Out of CNT 598,176.745 oz ii) Out of HSBC 304,243.610 oz

total withdrawal 902,370.355 oz

ADJUSTMENTs 2

a) dealer to customer Brinks 365,774.582 oz oz

ii) customer to dealer Stonex 600,569.400 oz

TOTAL REGISTERED SILVER: 192.681 MILLION OZ//.TOTAL REG + ELIGIBLE. 499.281 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 1225 OPEN INTEREST CONTRACTS FOR A LOSS OF 327 CONTRACTS. WE HAD 500 CONTRACTS SERVED UPON YESTERDAY SO WE GAINED 173 CONTRACTS OR 865,000 OZ ENTERTAINED A QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST GAINED 8 CONTRACTS TO 2400

SEPTEMBER GAINED 458 CONTRACTS UP TO 131,773 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 196 or 975,000 oz

CONFIRMED volume; ON WEDNESDAY 44,855 small//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 6109 X5,000 oz = 30.545 MILLION oz

to which we add the difference between the open interest for the front month of JULY (1225) AND the number of notices served upon today (195 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (6109) Notices served so far) x 5000 oz + OI for the front month of JULY(1225) minus number of notices served upon today (195)x 5000 oz equals silver standing for the JULY contract month equating to 35.695 MILLION OZ .

New total standing: 35.695 million oz which is huge for this active delivery month of JULY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 192.681 million oz of registered silver

JPMorgan as a percentage of total silver: 214.173/499.281 million. 42.88%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

JUNE 20 WITH GOLD DOWN $19.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 947.37 TONNES

JUNE 18 WITH GOLD UP $1.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.03 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 945.94 TONNES

JUNE 17 WITH GOLD DOWN $9.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 941.93 TONNES

JUNE 16 WITH GOLD DOWN $33.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.758 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 940.49 TONNES

JUNE 13 WITH GOLD UP $53.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.38 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 932.91 TONNES

JUNE 12 WITH GOLD UP $55.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 934.19 TONNES

JUNE 11 WITH GOLD UP $1.10 TODAY// SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.31 TONNEES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 935.91 TONNES

JUNE 10 WITH GOLD DOWN $11.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.02 TONNEES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 936.22 TONNES

JUNE 9 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.45 TONNEES OF GOLD FROM THE GLD//: /// ///INVENTORY RESTS AT 934.20 TONNES

JUNE 6 WITH GOLD DOWN $28.00 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

JUNE 2 WITH GOLD UP $80.90 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 930.20 TONNES

MAY 30 WITH GOLD DOWN $27.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.59 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 930.20 TONNES

MAY 29 WITH GOLD UP $22.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 925.71 TONNES

MAY 28 WITH GOLD DOWN $5.30 TODAY// NO CHANGES IN GOLD AT THE GLD:/ ///INVENTORY RESTS AT 925.61 TONNES

MAY 27 WITH GOLD DOWN $63.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 922.46 TONNES

MAY 23 WITH GOLD UP $69.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 923.89TONNES

GLD INVENTORY: 947.66 TONNES, TONIGHTS TOTAL

SILVER

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

JUNE 20 WITH SILVER DOWN $0.83/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.818 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 474.641 MILLION OZ.

JUNE 18 WITH SILVER DOWN $0.20/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 17 WITH SILVER UP $0.67/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 473.096 MILLION OZ.

JUNE 16 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.727 MILLION OZ FROM THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 13 WITH SILVER UP $0.11/NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 473.550 MILLION OZ.

JUNE 12 WITH SILVER UP $0.11/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.276 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 473550 MILLION OZ.

JUNE 11 WITH SILVER DOWN $0.45/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.046 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.274 MILLION OZ.

JUNE 10 WITH SILVER DOWN $0.16/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.232 MILLION OZ.

JUNE 9 WITH SILVER UP $0.69/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.914 MILLION OZ.

JUNE 6 WITH SILVER UP $0.63/HUGE CHANGES AT THE SLV:A DEPOSIT OF 3.863 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.732 MILLION OZ. (A TOTAL DEPOSIT OF 11.856 MILLION PHANTOM OZ IN THE LAST 4 DAYS)

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

JUNE 2 WITH SILVER UP $1.58/NO CHANGES AT THE SLV: ././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 30 WITH SILVER DOWN $0.36/HUGE CHANGES AT THE SLV: A DEPOSIT OF 2.773 MILLION OZ INTO THE SLV././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 29 WITH SILVER UP $0.29/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 28 WITH SILVER DOWN $0.18/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 27 WITH SILVER DOWN $0.34/HUGE CHANGES AT THE SLV//A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 23 WITH SILVER UP $0.38/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.5 MILLION OZ OF SILVER INTO THE SLV/: //INVENTORY AT SLV RESTS AT 454.375 MILLION OZ

Speaking on the Money Sense podcast, Alasdair Macleod chimed in on why he believes we are in an environment similar to 1929, or the start of the Great Depression.

In recent times, we have seen things compared often to infamous economic downturns, like the inflation and recession of the 1970s. We have also seen invocations of the Great Depression when the lockdowns happened, and gold accordingly leapt in massive bounds back then.

But these days, the price of gold is nearly doubled since the start of the lockdowns, so there might very well be something to MacLeod’s idea. Rather than buying into the narrative that reopenings prevented a 1929-style economic environment, Macleod thinks we are merely in the opening acts of a new global economic depression.

Macleod calls it the U.S. debt trap, mentioning how gold might have already overtaken U.S. dollars in terms of central bank reserves. As I’ve mentioned frequently since 2022, appetite for long-term U.S. government debt is hitting historical lows. Very few entities are willing to wager that the U.S. dollar, in 20-30 years, will still be a desirable asset.

The economy isn’t growing anymore (and there are questions of whether it can), and an annual budget deficit of 6%+ means stagnation is a serious concern.

Somewhat touching upon our own idea of a disassociation between gold and armed conflict, Macleod says that U.S. dollar and debt are actually the preferred safe haven during such times. This, in turn, makes the U.S. economy even more vulnerable if or when the threat of that military conflict subsides, as investors then start moving out of U.S. assets.

Looking back on it now, Macleod believes that the narrative of China dedollarizing to boost the yuan was just a way of making the dollar look better in comparison.

We are seeing that unfold month after month, as a recent report detailed how 32% of central banks are expected to buy gold just in the short-term.

As both the report and Macleod note, the situation is so bad that central banks are even taking on other currencies as reserves, so long as it means less exposure to the dollar.

Besides being under-owned, Macleod’s analysis of COMEX open interest suggests that gold might still be underbought, making the climb to $3,500 all the more remarkable. This is the first time since 1977 that U.S. assets have all broadly fallen in conjunction while gold has gone up, but, as said, 1929 might be a closer comparison.

Central banks are buying gold because they have a vision of the future, and this vision doesn’t appear to involve the currencies they print having any real money.

Macleod is also one of the many analysts convinced that China’s gold heap exceeds 30,000 tons, and he also says that silver is not to be overlooked here.

He says that informed accusations of silver price suppression go back more than two decades, with JPMorgan being consistently listed as a key culprit.

The idea, he notes, is to artificially deflate silver’s spot price to sell massive amounts of the physical variety.

But to whom?

China is again pointed to, with Macleod saying that China’s silver reserves might be even more stupefying than their gold stockpile.

He reminds us that the Shanghai Gold Exchange is wholly owned by the PBoC and appears to exist primarily as an instrument for the state to acquire more bullion while suppressing reports of purchases.

Although he says gold might be starting its summer doldrums, it’s interesting to note that it’s double the price of its summer doldrums from two years back.

Not much has changed in terms of fundamentals since then, so we have to ask what investors can expect over the next two years.

And, if we are indeed in a not-so-hidden 1929-style environment, what can gold investors in turn expect over the coming decade?

Submitted by admin on Wed, 2025-07-02 21:08 Section: Daily Dispatches

By James Bickerton Newsweek, New York Wednesday, July 2, 2025

Texans are to be allowed to pay with with gold and silver for everyday transactions after Gov. Greg Abbott signed House Bill 1056 into law. The law, which was championed by Republican state Rep. Mark Dorazio, designates the precious metals as legal tender in the state.

Texans will be able to use their gold and silver holdings, stored in the state’s bullion depository, for payments through electronic systems such as mobile apps or debit cards.

The provision comes after legislative debate, and takes effect on May 1, 2027, enabling transactions based on the state comptroller’s valuation of the metals at the time of sale. …

Guess who is urging central banks to sell their gold reserves

Submitted by admin on Wed, 2025-07-02 14:37 Section: Daily Dispatches

He’s no independent analyst.

* * *

2:49p ET Wednesday, July 2, 2025

Dear Friend of GATA and Gold:

If there was a monthly award for celebrating the obvious, or one for deceitful propaganda, they well might go to Mark Sobel, U.S. chairman of the Official Monetary and Financial Institutions Forum, purportedly a research group that occasionally enables favored people to rub shoulders with central bankers. (People critical of central banking are carefully excluded from OMFIF functions.)

OMFIF today published an essay by Sobel deploring the increasing acquisition of gold by central banks and noting that “monetizing” central bank gold reserves — that is, selling them — “could generate resources for good use

In the essay, headlined “Financial Authorities Should Responsibly Sell Their Gold Stocks” —

— Sobel writes: “Gold no longer has an official role in the international monetary system. It generates no interest, is costly to store, and is less liquid and harder to sell than securities, for example. Even if one argues that holding gold stocks results in an appreciation for the national balance sheet, that is generating no flow of resources to officialdom.”

Sobel seems to think that central bankers haven’t heard all this before and have no knowledge of history — that they don’t know that their institutions were major sellers of gold a few decades ago.

He doesn’t address that selling or its objective — to drive the ancient and independent form of money out of the world financial system, increasing the power of central banks and the power of one particular country, leaving the world defenseless.

Even more remarkably, Sobel doesn’t address why central banks lately have grown enthusiastic about gold — their fear of continued subservience to the imperial power whose currency they long have accepted for reserve purposes, their fear of becoming subservient to some other potential imperial power seeking to “internationalize” its currency, and their resentment of the market rigging undertaken by an imperial power, rigging long documented by GATA:

Maybe it’s because — surprise! — Sobel has spent most of his life as an employee of the U.S. Treasury Department, during which he was manager of the department’s Exchange Stabilization Fund, a primary instrument of market rigging by the U.S. government. Indeed, keeping the world enslaved to the U.S. dollar has been the great purpose of Sobel’s career:

Not surprisingly, Sobel’s essay and the biographical tagline appended to it by OMFIF make no reference to his background. OMFIF would have the world believe that the essay is independent expert analysis when it is actually U.S. government propaganda.

Sobel concludes: “If authorities were to responsibly sell gold stocks, it might quickly become evident that frothy headlines about gold and official reserve diversification were built on sand.”

Or it might quickly become evident that without gold reserves many countries were forfeiting their chance for regaining independence in monetary and international affairs.

As for gold reserves being built on sand, what does Sobel think government currencies often have been built on, and, indeed, what some are built on even now?

GATA would welcome a chance to discuss these issues at a function of the Official Monetary and Financial Institutions Forum if the organization ever permits such a discussion. But so far the organization has refused even to acknowledge GATA’s mail.

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

Submitted by admin on Wed, 2025-07-02 10:10 Section: Daily Dispatches

From the Sound Money Defense League, Eagle, Idaho Wednesday, June 2, 2025

By signing sound money legislation this week, Florida Governor Ron DeSantis has ended Florida’s discriminatory practice of assessing sales taxes on small purchases of gold, silver, or platinum bullion and coins.

Florida’s House Bill 7031, a bill by the House Ways and Means committee, was considered by multiple House and Senate committees before passing overwhelmingly out of both chambers and reaching the governor’s desk

This bill removes the arbitrary $500 minimum purchase size for citizens to qualify for any sales tax exemptions on precious metals as of August 1, 2025. …

BIS annual report again verifies GATA’s calculations of the bank’s gold swaps

Submitted by admin on Tue, 2025-07-01 14:02 Section: Daily Dispatches

As usual Lambourne is too modest to note that BIS annual reports REPEATEDLY have confirmed his calculations of the totals of the bank’s secret gold swaps.

* * *

By Robert Lambourne July 1, 2025

Last weekend the Bank for International Settlements published its annual report for the year ending March 31, 2025:

It includes some detail on the gold transactions carried out by the bank and in particular at the bottom of Page 195 it confirms that the gold swaps outstanding on March 31 were 10 tonnes, reasonably close to the estimate published by GATA on May 23, 9.5 tonnes:

This table summarizes the level of gold swaps since the BIS began reporting them in its annual report as of March 31, 2010.

March 2010: 346 tonnes. March 2011: 409 tonnes. March 2012: 355 tonnes. March 2013: 404 tonnes. March 2014: 236 tonnes. March 2015: 47 tonnes. March 2016: 0 tonnes. March 2017: 438 tonnes. March 2018: 361 tonnes. March 2019: 175 tonnes March 2020: 326 tonnes March 2021: 490 tonnes March 2022: 358 tonnes March 2023: 77 tonnes March 2024: 72 tonnes March 2025: 10 tonnes

The monthly estimates of the swaps published by GATA reveal a pattern of regular gold trading that is often substantial. This indicates a much closer official interest and involvement in the gold market by the BIS and its central bank members than they generally admit.

The BIS has given no explanation for its gold swaps since their existence was disclosed in the bank’s 2009-10 annual report. Regular questions are asked of GATA about the purpose of the swaps, and as far as GATA is aware no further disclosures have been made since an article was published in the Financial Times on July 29, 2010.

Below are that article and an article from Business Insider following up on that article.

BIS Gold Swaps Mystery Is Unraveled

By Jack Farchy and Javier Blas Financial Times, London July 29, 2010

Three big banks — HSBC, Societe Generale, and BNP Paribas — were among more than 10 based in Europe that swapped gold with the Bank for International Settlements in a series of unusual deals that caused confusion in the gold market and left traders scratching their heads.

The mystery of who was involved in deals with the BIS, the bank for central banks, and what they were doing, has become clearer.

The Financial Times has learnt that the swaps, which were initiated by the BIS, came as the so-called “central banks’ bank” sought to obtain a return on its huge U.S. dollar-denominated holdings. The BIS asked the commercial banks to pledge a gold swap as guarantee for the dollar deposits they were taking from the Basel-based institution.

When news of the swaps, which were disclosed in a note to the BIS’ latest annual report, circulated among traders this month, it caused a sharp fall in the gold price, sending bullion to what was then six-week lows. Gold has since fallen further: it was trading at $1,164 an ounce on Thursday.

Some analysts speculated that the swap deals were a surreptitious bailout of the European banking system ahead of last week’s publication of stress tests. But bankers and officials have described the transactions as “mutually beneficial.”

“The client approached us with the idea of buying some gold with the option to sell it back,” said one European banker, referring to the BIS.

Another banker said: “From time to time central banks or the BIS want to optimize the return on their currency holdings.”

Nonetheless, two central bank officials said some of the commercial banks also needed the U.S. dollar funding and were keen to act as a counterparty with the BIS. The gold swaps began in December and surged in January, when the Greek debt crisis erupted and European commercial banks were facing funding problems.

Jaime Caruana, head of the BIS, told the FT the swaps were “regular commercial activities” for the bank.

In a short note in its annual report, published at the end of June, the BIS said it had taken 346 tonnes of gold in exchange for foreign currency in “swap operations” in the financial year to March 31.

In the same fiscal year, the BIS took three times the amount of currency deposits it had taken the previous year as central banks around the world became concerned about using commercial banks for their deposits and turned to the Basel institution.

In a gold swap, one counterparty, in this case a bank, sells its gold to the other, in this case the BIS, with an agreement to buy it back at a later date.

The gold swaps were, in effect, a form of collateral against the U.S.-dollar deposits placed by the BIS with commercial banks. Gold is widely regarded as one of the safest assets but has not been widely used as collateral in the past. Mr. Caruana described the transactions as “loans with a guarantee.”

Investors have bought physical gold in record amounts during the past two years and deposited it in commercial banks. European financial institutions are awash with bullion and some are trying to pledge gold as a guarantee.

George Milling-Stanley, managing director for government affairs at the industry-backed World Gold Council, said: “The gold swaps commercial banks carried out with the BIS demonstrate the effectiveness of gold as an asset class, because even in the depths of the worst liquidity crisis in living memory, institutions with access to gold were able to make use of it to generate dollar liquidity.

“The issue also feeds right into the current debate among Asian central banks about the lack of assets suitable for use as cross-border collateral.”

Last year, CME Group, the world’s largest derivatives exchange, allowed investors to use gold futures as collateral for some operations. Other institutions, such as central banks, had begun using and requesting gold as collateral in the past two years as perceptions of counterparty risk have risen, bankers and officials said.

The gold used in the swaps came mainly from investors’ deposit accounts at the European commercial banks. Some investors prefer to deposit their gold in so-called “allocated accounts,” which restrict the custodian banks’ ability to use the gold in their market operations by assigning them specific bullion bars. But other investors prefer cheaper “unallocated accounts,” which give banks access to their bullion for their day-to-day operations.

Officials said other commercial banks obtained the gold from the lending market, borrowing bullion from emerging countries’ central banks.

European Banks Lent Their Customers’ Gold to the BIS

— the source of the gold provided in the dollar swaps with the BIS is coming from customers of about 10 European banks that are holding their gold at the banks in “unallocated accounts.”

“The gold used in the swaps came mainly from investors’ deposit accounts at the European commercial banks. Some investors prefer to deposit their gold in so-called ‘allocated accounts,’ which restrict the custodian banks’ ability to use the gold in their market operations by assigning them specific bullion bars. But other investors prefer cheaper ‘unallocated accounts,’ which give banks access to their bullion for their day-to-day operations.”

The European Banks, including HSBC, Societe Generale, and BNP Paribas, were desperately in need of dollars because of a repeat of the short squeeze we had previously identified. Their customers were withdrawing dollars previously on deposit at the banks, which were unable to meet the demand because of the deterioration of the dollar assets they held, and because of the fractional-reserve nature of their operations.

So the BIS stepped in and swapped its dollar holdings for the some of the banks’ customer’s gold. Let us be clear about this. The gold is on deposit at the banks, in the same way that customer dollars had been on deposit.

In lending the gold to BIS, they were relieved of their dollar short squeeze and were able to supply their customer demands. The BIS obtained a fee of some sort in the swap, and so it is happy, although it is foolish to think of the BIS as a primarily profit-motivated organization. It is more like the Federal Reserve than Goldman Sachs.

The question remains unanswered, though. What is the duration of the swap, and does the BIS intend to hold the gold or use it in other interbank operations?

Yes, the nice high-level chart the FT includes shows the spike in gold holdings at the BIS, but does this mean that it is sitting there in their reserves unencumbered, or are they leasing any or all of it out, “putting it to work,” as they say? Central banks are notorious for making little distinction between unencumbered gold assets and real assets in the vault.

But it is nice to see verification in the mighty Financial Times that if you hold your bullion gold in an “unallocated account,” even with a prestigious bank, it may very well not be there when you wish to have it, and the prices will soar as the banks scurry to cover, just as has happened twice of late with their U.S. dollar assets.

Or you may be asked to settle in cash if there is some clause in the contract, as in the case of the exchange-traded funds or the Comex.

Robert Lambourne is a retired business executive in the United Kingdom who consults for GATA about the involvement of the Bank for International Settlements in the gold market and about U.S. government debt.

end

Ambrose Evans-Pritchard: Fed independence is already dead, and Trump will get his monetary bailout

Submitted by admin on Tue, 2025-07-01 11:06 Section: Daily Dispatches

By Ambrose Evans-Pritchard The Telegraph, London Tuesday, July 1, 2025

Central banks have no God-given right to independence. Nothing in the US constitution authorises the US Federal Reserve to act as a shadow government, and nor should it have such powers under any theory of accountable democracy.

One can admire the gentlemanly altruism of Fed chairman Jerome Powell, and one can deplore the motives and methods of Donald Trump, while also conceding that Trump is accidentally right on the perils of overmighty technocrats. The Fed has slipped its leash.

It is not alone in that. Central bankers have been calling the shots across the advanced democracies over the last 30 years, elevating this priesthood to the status of Nietzschean rock stars.

Sir Paul Tucker argues in his expose, “Unelected Power: The Quest For Legitimacy in Central Banking,” that they have become the “third great pillar of unelected power,” akin to the judiciary but without the constraints.

The Bank of England veteran says the fraternity has strayed a very long way into “quasi-fiscal” intervention, picking winners and losers in what amounts to a revolution in the system of government.

There is a case for zero rates and quantitative easing in a crisis, but these policies were pursued for too long and have led to a vast transfer of wealth from wage workers to the owners of capital. The central banks unwittingly became agents of extreme inequality.

Trump has purged the top echelons of the US military, the CIA, the NSA, the FBI, the justice department and every agency that stands in his way. It would be out of character if he spared the Fed.

His war of words against Powell is in full flight: “Low IQ … a very stupid person, actually … terrible … a major loser … Mister Too Late … a total and complete moron.”

Needless to say, Trump’s determination to get his hands on the machinery of interest rates and bond purchases is an admission that his “big, beautiful bill” is pushing the limits of US debt sustainability.

The Congressional Budget Office (CBO) says the draft will add $3.3 trillion (£2.4 trillion) to deficits by 2034, mostly from rolling over the Trump 1.0 tax cuts that were never affordable in the first place.

The US is in a runaway debt compound trap. The budget deficit is 6.7% of GDP at full employment. The next recession will push it into double digits.

Interest costs were 1.6% of GDP in 2018, during those halcyon days of free global money. They are 3.2% this year and rising fast. “The federal budget has become highly sensitive to interest rate dynamics,” said James Knightley, from ING.

The US is also about to breach the Niall Ferguson rule: that great powers go into terminal decline once interest costs exceed military spending as a share of GDP.

Net public debt was 54% of GDP at the turn of the century. It is now 121pc, rising by two points a year even in good times, and heading for 140% in short order.

This is partly because US demographics have turned bad and middle-class welfare is out of control. But it is no coincidence that this drastic deterioration has happened during the era of independent central banks.

These econometric presbyters have made grave and repeated monetary errors, in thrall to a “dynamic stochastic general equilibrium” model with a bias towards debt creation and a refusal to let Schumpeterian creative destruction run its course.

They targeted consumer price inflation — just as China was jamming the signal by flooding the world with cheap goods — and let asset inflation and debt bubbles run rampant instead, until the experiment blew up in their faces in 2008.

The European Central Bank is in a class of its own, a sort of Vatican City answerable to no one, in the words of Lord Skidelsky. It pushed half the eurozone into an avoidable debt crisis by overtightening into the downturn, causing Europe’s lost decade.

It used instruments of financial torture to topple two elected governments — Greece (2010) and Italy (2011) — parachuting in nomenklatura stalwarts to take over. It forced Greece’s Syriza government to its knees in 2015 by pre-emptively draining bank liquidity. It issued secret letters ordering Spain to change its constitution, and Italy to change its labour laws.

The Fed, the ECB and the Bank of England all made a hash of Covid inflation by pushing QE after recovery was under way. It is not clear to me that this credentialed elite have made a better fist of matters than the lesser mortals before them.

The Fed has not been independent for most of its 111-year history. It met in a borrowed room in Alexander Hamilton’s treasury building until 1937, and not much changed after that. Former chairman Marriner Eccles bemoaned that he was a cypher who “merely executed treasury decisions”.

President Harry Truman harassed Eccles’ successor for refusing to soak up federal debt and hold down bond yields, ultimately forcing him into the Fed-treasury accord, i.e. into total subjugation. This accord wiped out much of America’s war debt by means of financial repression and double-digit inflation. It expropriated creditors.

Truman ultimately forced the poor wretch to resign, saying “his services were no longer satisfactory”. First he accused him of serving Stalin’s interests, a trick that Trump might find irresistible. Just replace Stalin with Xi Jinping.

Even Paul Volcker, slayer of the great inflation, was bullied shamelessly, writing in his memoirs that Ronald Reagan’s chief of staff ordered him in 1984 “not to raise rates before the election”.

Edoardo Campanella, director of Unicredit’s Investment Institute, says Trump is merely “turning back the clock” to the historical norm. Furthermore, the Democrats are complicit in eroding Fed autonomy since many have been trying to draft it to curb CO2 emissions and fight social injustice.

Legally, the president can terminate the 14-year term of the Fed’s seven board members only “for cause”, usually malfeasance or neglect. But Trump has fired a dozen top officials at federal agencies with the same protection.

Powell’s term ends in May 2026. Trump can either sack him before that by conjuring a fictitious emergency or emasculate him by appointing a “shadow chairman”, a rate-cutter waiting in the wings.

Trump would also have to purge the board one by one. A team of his loyalists have already thought of that. They drew up a secretive 10-page report before the election proposing a series of radical steps to break all resistance.

It is an open question whether Fed capture would deliver the benefits Trump craves. Bond vigilantes rebelled when he talked of firing Powell in April. It was his Truss moment, pushing up the long-term yields that set US mortgage rates and corporate borrowing costs.

A global “deep state” trumped Trump himself, demonstrating that a collective force of global wealth funds is more powerful even than an American president.

Yields on 10-year treasuries have since settled down to 4.26% and are 50 points lower than in April. Either investors have been lulled by the lack of inflation so far or this may be the calm before the next storm.

The tariff price shock hits with a lag. Importers are exhausting the large inventories built up to beat deadlines.

Berenberg Bank says shipments from China take 30 days to reach Los Angeles, 45 days to reach Chicago, and 55 days to reach New York. It then takes weeks before they end up on the market. Some companies have swallowed the initial cost of the import taxes, hoping that there will be trade deals.

They will not endure losses for long.

The Fed is right to delay cuts until it can see through the tariff fog and make a judgment on the stagflationary costs of mass deportation. There may yet be a global exodus from US debt markets if Trump forces through Turkish-style monetary expansion against fundamentals.

Trump has an answer for that, too: he will in the end compel the Fed to buy debt and suppress yields. But that way lies a collapse of the dollar and the path to perdition.

Remember the Rudi Dornbusch rule: “Crises take longer to arrive than you can possibly imagine, but when they do come, they happen faster than you can possibly imagine.”

end

4. ANDRE MAGUIRE/LIVE FROM THE VAULT KINESIS 229

5. COMMODITY REPORT…PLATINUM