118 C MACQUARIE FUTURES US 5

190 H BMO CAPITAL MARKETS 42

323 C HSBC 206

332 H STANDARD CHARTERED B 112

363 H WELLS FARGO SECURITI 9

661 C JP MORGAN SECURITIES 34

686 C STONEX FINANCIAL INC 14 7

709 C BARCLAYS 8

737 C ADVANTAGE FUTURES 3 3

880 C CITIGROUP 2

905 C ADM 1

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 223 CONTRACTs NOTICES FOR 22,300 OZ or 0.6936 TONNES

total notices so far: 7772 contracts for 777,200 OR 24.174 tonnes)

SILVER NOTICES: 56 NOTICE(S) FILED FOR .280 million OZ/

total number of notices filed so far this month : 7,452 CONTRACTS (NOTICES) for 37.260 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 15.895 MILLION OZ

AND JULY: 40.460 MILLION OZ//

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 22.786 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 627 CONTRACTS OI TO 162,176 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 920 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 920 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 920 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1478 CONTRACTS AND ADD TO THE 920 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF 293 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $0.18 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 1.295 MILLION PAPER OZ

OCCURRED DESPITE OUR TINY $0.18 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED UP 16.04 PTS OR 0.46%

//Hang Seng CLOSED UP 111.16 PTS OR 0.47%

// Nikkei CLOSED DOWN 174.92 PTS OR 0.44% //Australia’s all ordinaries CLOSED UP 0.56%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1771 OFFSHORE CLOSED UP AT 7.1790/ Oil DOWN TO 68.43 dollars per barrel for WTI and BRENT DOWN TO 70.18 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1771 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1790 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3058 CONTRACTS TO A STILL LOW NUMBER OF 440,086 OI DESPITE OUR GAIN IN PRICE OF $4.05 WITH RESPECT TO WEDNESDAY’S // TRADING. WE LOST LITTLE NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1551 ). WE HAD SOME T.A.S. LIQUIDATION //TUESDAY TRADING.

THE CME ANNOUNCED WEDNESDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES.

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY 0

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 1507 CONTRACTS DESPITE OUR SMALL GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE IN JANUARY THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND NOW JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS ANOTHER MEGA MEGA HUGE T.A.S. AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 20,027 T.A.S CONTRACTS. IF HISTORY SERVES US CORRECTLY, WE WILL NOW ENDURE 3 MORE OF THESE MEGA HUGE ISSUANCE OF T.A.S. AS THE CROOKS NEED TO RAID OUR PRECIOUS METALS SOUTHBOND IN PRICE BUT THEY ARE NOT HAVING MUCH LUCK ON THAT SCORE!!!

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. HOWEVER JULY IS HUGE FOR A NON DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 0.3224 TONNES QUEUE JUMP = 24.392 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 24.392 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 10+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 229 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1551 EFP CONTRACT WAS ISSUED: : /AUGUST 1551 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1551 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- SOME LIQUIDATION OF OUR T.A.S. SPREADERS//

- SOME NET SPEC LIQUIDATION DESPITE OUR GAIN IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY MORNING/WEDNESDAY NIGHT WAS A MEGA MEGA AND CRIMINAL SIZED, 20,027 CONTRACTS.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.THIS WAS SURELY IN EVIDENCE IN TRADING WEDNESDAY WITH OUR SMALL GAIN IN PRICE!

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S HUGE 0.3224 TONNES QUEUE JUMP = 24.392 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 54 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $4.05/ /) AND THEY WERE A LITTLE SUCCESSFUL IN KNOCKING OFF SOME NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED LOSS IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD SOME T.A.S. SPREADER LIQUIDATION ////WEDNESDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE MEGA MEGA T.A.S. ISSUANCES, WEDNESDAY MORNING TUESDAY EVENING, IN ORDER TO COMMENCE CONTINUAL RAIDS ON OUR PRECIOUS METALS. SO FAR TODAY, THIS EXERCISE HAS BEEN A TOTAL FAILURE…

THURSDAY MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; ZERO SO FAR

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE LOST A FAIR SIZED TOTAL OF 4.687 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 10,400 OZ OR 0.3224 TONNES OF GOLD//NEW STANDING ADVANCES TO 24.392 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $4.05

WE HAD 226 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 1507 CONTRACTS OR 150,700 0Z (4.687 TONNES)

confirmed volume WEDNESDAY 214,079 contracts FAIR

speculators have left the gold arena

END

INITIAL GOLD COMEX

JULY CONTRACT MONTH

JULY 10/2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRY . 2 ENTRIES i) Out of JPMorgan 96,453.000 oz (3000 kilobars) ii) Out of Loomis 1135.926 oz total withdrawal: 97,588.926 oz or 3.035 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | 0 ENTRY i xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 223 notice(s) 22,300 OZ 0.6936 TONNES |

| No of oz to be served (notices) | 70 contracts 7,000 OZ 0.2177 TONNES |

| Total monthly oz gold served (contracts) so far this month | 7772 notices 777,200 oz 24.174 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

we have 0 customer entry

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

2 ENTRIES

2 ENTRIES

i) Out of JPMorgan 96,453.000 oz

(3000 kilobars)

ii) Out of Loomis 1135.926 oz

total withdrawal: 97,588.926 oz

or 3.035 tonnes

adjustments: 1

Customer to dealer JPMorgan 4071.392 oz

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JULY STANDS AT 293 CONTRACTS FOR A LOSS OF 553 CONTRACTS. ON WEDNESDAY WE HAD 657 NOTICES FILED YESTERDAY SO WE GAINED A 104 CONTRACTS OR 10,400 OZ (0.3234 TONNES) ENTERTAINED WITH A QUEUE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD

AUGUST LOST 17,366 CONTRACTS DOWN TO 275,285

SEPT GAINED 65 CONTRACTS TO 1376

We had 223 contracts filed for today representing 22,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 223 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 34 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (7772 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (293 CONTRACTS) minus the number of notices served upon today (223 x 100 oz per contract) equals 784,200 OZ OR 24.392 TONNES to which we add 0 tonnes of gold issued under exchange for risk// total standing 24.392 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (7772 x 100 oz +we add the difference for front month of JULY (293 OI} minus the number of notices served upon today (223 x 100 oz) which equals 784,200 OZ OR 24.392 TONNES + 0 tonnes EX FOR RISK = 24.392 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 24.392 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,194,511.830 oz 68.258 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,779,205.499 oz

TOTAL REGISTERED GOLD 20,204,157,.318: or 628.434 tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,575,048.181 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 18,009,646 oz (REG GOLD- PLEDGED GOLD)= 560.17 tonnes //

total inventories in gold declining rapidly

SILVER/COMEX

THE JULY 2025 SILVER CONTRACT//INITIAL

JULY 10

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries i) Brinks 1098,087.693 oz ii) Out of JPMorgan: 654,169.900 oz iii) Out of Loomis 3813.880 oz total withdrawal 1,756,071.473 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) into Delaware 2959.903 oz total deposit 2959.903 oz |

| No of oz served today (contracts) | 56 CONTRACT(S) (0.280 MILLION OZ |

| No of oz to be served (notices) | 640contracts (3.20 MILLION oz) |

| Total monthly oz silver served (contracts) | 7452 Contracts (37.260 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposits into dealer accounts

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) into Delaware 2959.903 oz

total deposit 2959.903 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3 entries

i) Brinks 1098,087.693 oz

ii) Out of JPMorgan: 654,169.900 oz

iii) Out of Loomis 3813.880 oz

total withdrawal 1,756,071.473 oz

ADJUSTMENTs 1

a) customer acct to dealer Manfra: 50,900.300 oz

TOTAL REGISTERED SILVER: 191.962 MILLION OZ//.TOTAL REG + ELIGIBLE. 495.535 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 696 OPEN INTEREST CONTRACTS FOR A LOSS OF 435 CONTRACTS. WE HAD 459 CONTRACTS SERVED UPON WEDNESDAY SO WE GAINED 24 CONTRACTS OR 0.120 MILLION OZ ENTERTAINED A MASSIVE QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST GAINED 22 CONTRACTS TO 2344

SEPTEMBER LOST 1159 CONTRACTS DOWN TO 125,701 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 56 or 0.280 MILLION oz

CONFIRMED volume; ON WEDNESDAY 50,874 small//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 7452 X5,000 oz = 37.260 MILLION oz

to which we add the difference between the open interest for the front month of JULY (696) AND the number of notices served upon today (56 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (7452) Notices served so far) x 5000 oz + OI for the front month of JULY(696) minus number of notices served upon today (56)x 5000 oz equals silver standing for the JULY contract month equating to 40.460 MILLION OZ .

New total standing: 40.460 million oz which is huge for this active delivery month of JULY.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 191.962 million oz of registered silver

JPMorgan as a percentage of total silver: 210.929/495.535 million. 42.54%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

JUNE 20 WITH GOLD DOWN $19.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 947.37 TONNES

JUNE 18 WITH GOLD UP $1.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.03 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 945.94 TONNES

JUNE 17 WITH GOLD DOWN $9.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 941.93 TONNES

JUNE 16 WITH GOLD DOWN $33.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.758 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 940.49 TONNES

JUNE 13 WITH GOLD UP $53.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.38 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 932.91 TONNES

JUNE 12 WITH GOLD UP $55.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 934.19 TONNES

JUNE 11 WITH GOLD UP $1.10 TODAY// SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.31 TONNEES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 935.91 TONNES

JUNE 10 WITH GOLD DOWN $11.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.02 TONNEES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 936.22 TONNES

JUNE 9 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.45 TONNEES OF GOLD FROM THE GLD//: /// ///INVENTORY RESTS AT 934.20 TONNES

JUNE 6 WITH GOLD DOWN $28.00 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

JUNE 2 WITH GOLD UP $80.90 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 930.20 TONNES

MAY 30 WITH GOLD DOWN $27.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.59 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 930.20 TONNES

MAY 29 WITH GOLD UP $22.35 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 925.71 TONNES

MAY 28 WITH GOLD DOWN $5.30 TODAY// NO CHANGES IN GOLD AT THE GLD:/ ///INVENTORY RESTS AT 925.61 TONNES

MAY 27 WITH GOLD DOWN $63.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ ///INVENTORY RESTS AT 922.46 TONNES

MAY 23 WITH GOLD UP $69.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD/ ///INVENTORY RESTS AT 923.89TONNES

GLD INVENTORY: 947.37 TONNES, TONIGHTS TOTAL

SILVER

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

JUNE 20 WITH SILVER DOWN $0.83/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.818 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 474.641 MILLION OZ.

JUNE 18 WITH SILVER DOWN $0.20/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 17 WITH SILVER UP $0.67/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 473.096 MILLION OZ.

JUNE 16 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.727 MILLION OZ FROM THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 13 WITH SILVER UP $0.11/NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 473.550 MILLION OZ.

JUNE 12 WITH SILVER UP $0.11/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.276 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 473550 MILLION OZ.

JUNE 11 WITH SILVER DOWN $0.45/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.046 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.274 MILLION OZ.

JUNE 10 WITH SILVER DOWN $0.16/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.232 MILLION OZ.

JUNE 9 WITH SILVER UP $0.69/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.914 MILLION OZ.

JUNE 6 WITH SILVER UP $0.63/HUGE CHANGES AT THE SLV:A DEPOSIT OF 3.863 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.732 MILLION OZ. (A TOTAL DEPOSIT OF 11.856 MILLION PHANTOM OZ IN THE LAST 4 DAYS)

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

JUNE 2 WITH SILVER UP $1.58/NO CHANGES AT THE SLV: ././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 30 WITH SILVER DOWN $0.36/HUGE CHANGES AT THE SLV: A DEPOSIT OF 2.773 MILLION OZ INTO THE SLV././///INVENTORY RESTS AT 459.876 MILLION OZ.

MAY 29 WITH SILVER UP $0.29/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 28 WITH SILVER DOWN $0.18/NO CHANGES AT THE SLV////INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 27 WITH SILVER DOWN $0.34/HUGE CHANGES AT THE SLV//A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 457.103 MILLION OZ.

MAY 23 WITH SILVER UP $0.38/HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.5 MILLION OZ OF SILVER INTO THE SLV/: //INVENTORY AT SLV RESTS AT 454.375 MILLION OZ

CLOSING INVENTORY 481.175 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG

ALASDAIR MACLEOD

JOHN RUBINO

A Closer Look At Germany’s Death Spiral

Subscriber Bill G responded to yesterday’s post on Germany’s financial/cultural death spiral by asking:

“And when did debt to GDP cease to be a good measure of economic health? https://countryeconomy.com/countries/compare/germany/usa?sc=XE02”

His point is that if Germany’s government debt is only 65% of GDP, that country is — by definition— in way better shape than the US (debt 120% of GDP).

This is a reasonable question with an interesting answer. So here goes:

Vendor Financing

In the business world, there’s a semi-sleazy practice in which a company lends money to its customers who then use that money to buy the company’s products. This boosts sales and profits, making company managers seem worthy of big year-end bonuses.

Assuming the debtor/customers can pay off their loans, this practice can continue, unbeknownst to outsiders, for a long time. But if customers start defaulting, the “vendor financing” scheme unravels.

Germany has been running the government version of this scam.

With the introduction of the euro as a common currency in 1999, it became clear that eurozone members had wildly differing financial profiles. Greece and Italy, for instance, were bankruptcy candidates who, in a rational world, would have to pay way up to borrow money. But high interest rates would render their debt prohibitively expensive, forcing them out of the eurozone.

So the currency union cooked up the following scheme: The European Central Bank (ECB) would buy non-German government bonds at prices that equated to extremely low interest rates. And Germany would guarantee the solvency of the ECB.

For long stretches, most eurozone countries were able to borrow at lower rates than the US government had to pay, since their bonds were de facto German (i.e., “investment-grade”) paper.

Now here’s where “vendor financing” comes in. Italy, Greece, Spain, et al used some of the money they borrowed to buy German-manufactured goods. As a result, Germany’s economy grew, its trade balance was positive, and its government deficits were modest (when they weren’t actual surpluses).

It’s easy to view the resulting chart as a picture of a financially sound entity.

But remember that Germany, via the ECB, had promised to make good on everyone else’s bonds. Should, say, Italy default, those obligations would in effect become part of Germany’s national debt. So its real obligations are much higher than the official numbers.

And now that Germany is “deindustrializing,” its ability and willingness to cover everyone else’s debts are being called into question, causing peripheral Europe’s interest rates to rise. Note that Spain was able to borrow 10-year money for less than 2% until 2022, when the US ended Germany’s cheap-energy industrial preeminence by blowing up the Nord Stream gas pipeline.

A Eurozone Without Germany Is Toast

So here we are, at a crossroads: Either peripheral Europe starts paying market rates for its ever-increasing government debt, which will force the dissolution of the eurozone and a return to national currencies. Or the ECB — without explicit German guarantees — steps back in and buys huge amounts of low-quality sovereign debt with newly created currency, which will spike inflation and crash the euro.

Either way, Germany’s days as an industrial powerhouse are over, and the eurozone is, as a result, over.

3. CHRIS POWELL OF GATA/DAILY DISPATCHES

Ghana launches task force to curb gold smuggling losses

Submitted by admin on Wed, 2025-07-09 18:51 Section: Daily Dispatches

By Emmanuel Bruce

Reuters

Wednesday, July 9, 2025

ACCRA — Ghana President John Dramani Mahama on Tuesday launched a task force backed by security forces to address illegal gold trading, as Africa’s top producer seeks to recover billions of dollars lost to smuggling.

The task force is Ghana’s first national anti-gold smuggling initiative. The government has previously launched efforts to sanitize artisanal mining, but these were unsuccessful in curbing illegal extraction and preventing revenue losses that plague most African gold producers.

Ghana this year created the new gold board known as GoldBod to centralise gold trading. This has led to record official exports of 55.7 metric tonnes of gold valued at $5 billion in the first five months of 2025, Mahama said at the inauguration of the new task force.

“This is money that would not have come back to Ghana because traders would have taken it and kept the foreign exchange outside,” Mahama said. …

… For remainder of the report:

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 230

WITH CRAIG HEMKE

5. COMMODITY REPORT…COCOA

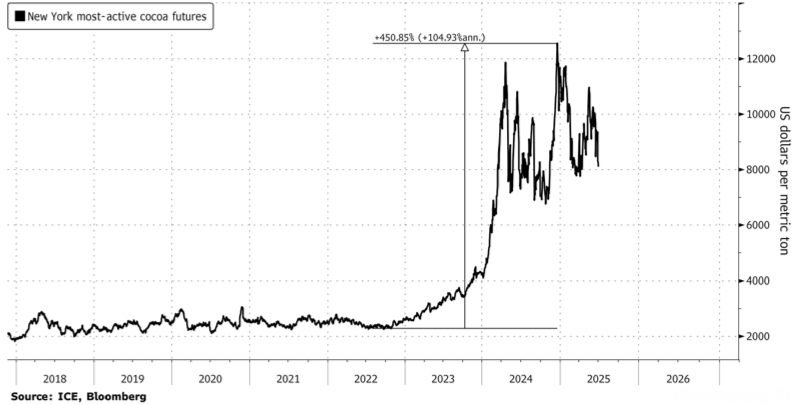

cocoa is still on a tear in price rises!!

(zerohedge)

Cocoa Supply Crunch Shown In One Chart

Thursday, Jul 10, 2025 – 02:45 AM

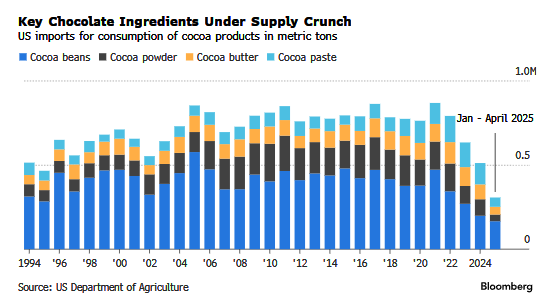

The chocolate industry is facing a new era of chronic shortages and record-high prices across cocoa beans, butter, powder, and paste, sparking structural supply disruptions across North America and Europe. At the heart of the crisis is West Africa, where countries such as Côte d’Ivoire, Ghana, Nigeria, and Cameroon—responsible for 75% of global cocoa production—have been severely impacted by years of adverse weather and crop diseases.

Cocoa bean prices in New York remain near record highs—trading around $8,000 a ton on Tuesday—after skyrocketing over 450% from late 2022 to December 2024, when prices briefly topped $12,000. This surge has driven a 16% increase in key input costs for chocolate makers so far this year, putting additional upward pressure on candy prices at the supermarket.

One of the most striking visualizations of the multi-year cocoa shortage, courtesy of Bloomberg, is the decline in U.S. cocoa imports, which have seen supplies plummet in just a few short years.

In response, major food companies, such as Mars and Hershey, have reduced the sizes of candy bars, added cheaper ingredients e.g., nuts, wheat), or entirely shifted to non-chocolate offerings. Artisan producers like Raaka have reported paying a whopping triple the price for cocoa powder.

This has only kicked off a rise in substitutes for food companies, introducing cocoa powder alternatives, such as:

- Carob blends (Doehler Group, Germany),

- Wheat-based powder (Ardent Mills, U.S.), replacing up to 50% of cocoa powder in some products

- Flavor and color substitutes like vanilla, caramel, coffee, and food coloring are also gaining traction.

“We are in an era where chocolate indulgence will no longer rely solely on cocoa,” Ina Dawer, the global insight manager for ingredients at Euromonitor International, told Bloomberg.

The global cocoa shortage is expected to persist: Cocoa processing in Europe, the largest international market, declined 3.7% in 1Q25 to its lowest level since 2017, while a similar trend has been observed in North America. Coca bean prices are expected to remain elevated through the second half of the year.

END

STUDY ON RARE EARTHS/(ZEROHEDGE)

an in depth study on rare earths: how China has the dominate position and it will take years for western nations to produce these magnets.

(zerohedge)

The Coming Rare Earth Revolution And How To Profit: All You Need To Know About The “Ex-China Supply Chain”

Thursday, Jul 10, 2025 – 03:25 AM

China’s export controls on core rare earth elements (REE) has led to scarcity across the globe and put the spotlight on REE supply chains, especially those which exclude China which is currently the world’s biggest source of raw and refined rare earths, which affords it a unique advantage in the ongoing global trade wars.

In a recent must read report (available to pro subscribers), Morgan Stanley’s metal and mining team published an in-depth look at a number of early-stage REE and magnet projects to map out where Western countries may be able to source these critical minerals, and to find the biggest potential winners from the biggest clash in the ongoing trade war between the US and China.

We excerpt the key highlights below.

1. Mapping a Potential ex-China Rare Earths Supply Chain

Key Takeaways

- REEs and permanent magnets are needed to build cars today and humanoids/robots in the future. Chinese export controls have pressured these supply chains.

- The US has a robust pipeline of ex-China upstream projects, but most are in the engineering and permitting phase, with a limited number under construction.

- Few ex-China permanent magnet projects in pipeline, and capacity of new facilities is <10% of Chinese facilities, in part due to lack of ex-China REE feedstock.

- REE prices to rise as customers & governments diversify ex-China supply. This should lead to premium pricing for existing players and incentivize new supply.

- Morgan Stanley sees MP Materials, Lynas, and ILU as best positioned to capitalize as REE trade flows and pricing adjust.

US reliance on imported critical minerals has increased significantly, with growing implications for national security… In the past 35 years, the US has seen significant growth in both the variety of imported minerals and its dependence on these imports. In 1990, the US was fully reliant on imports for the supply of 9 minerals, and imports exceeded 50% of consumption for 27 minerals (all minerals, not only critical ones). These figures have risen to 15 and 46, respectively, as of 2024. For US policymakers, recent trade tensions highlight the growing vulnerability of the US rare earth supply chain and the urgent need to strengthen domestic supply chains. As the risk of continued export restrictions and geopolitical uncertainty rises, the US and other nations will increasingly prioritize long-term national security over economic concerns.

… and the EU is finding itself in a similar position as it looks to initiate projects both inside and outside the EU… The EU is placing greater focus on incentivizing an ex-China supply of critical minerals. Under the Critical Raw Materials Act (CRMA), the EU has identified 60 projects, 13 of them outside of the EU and 47 inside the EU, to secure critical mineral supply chains for the region. The projects span the full list of critical raw materials and include two rare earth element (REE) extraction projects outside of the EU — Songwe Hill in Malawi and Zandkopsdrift in South Africa — as well as three REE processing projects and two REE recycling projects inside the EU.

… leaving China in a powerful position to influence global rare earth markets, primarily via mineral export restrictions. China dominates the global REE processing/refining industry, accounting for an estimated 65% of mined NdPr supply, 88% of refined NdPr supply, and >90% of downstream NdFeB permanent magnet supply in 2025, according to Woodmac. China has not hesitated to use its dominance of this critical supply chain as a geopolitical tool, dating back to 2010, when the country halted exports to Japan amid an escalating diplomatic crisis, a move that sent REE prices soaring. In 2019 and 2021 (here and here), China floated REE export controls amid rising trade tensions, which, according to The Financial Times, aimed to test how much defense contractors in the US and Europe would be affected. China has since banned the export of rare earth processing technology; most recently, in early April, it placed export controls on the export of heavy rare earth elements (HREE) and permanent magnets to all countries (i.e., not just the US). Because virtually all separated HREE production comes from China, this has led to distortions in market prices outside of China as companies scramble to secure supply (Exhibit 5 and Exhibit 6).

Rare earths are critical to many current applications… The US Department of Defense (DoD) deems rare earths as critical minerals because they are required (and difficult to substitute) in national security applications. While the DoD is estimated to be only ~5% of US demand, rare earths are used in essential military equipment such as motors in aircraft and tanks, missile guidance systems, and radar/sonar for submarines and surface ships (Exhibit 1 and Exhibit 2). The remaining ~95% of demand is primarily used in permanent magnets that go into autos (~40%); electronics & mechanical components, including speakers (~20%); HVAC systems (8%); wind energy (~8%); and others (~19%).

… and are key to future humanoid development. As governments vie for the pole position in humanoid development, China is off to a strong start given its advanced rare earth and permanent magnet supply chains. Morgan Stanley’s Metals and Mining team’s work suggests NdPr will enter deficit by 2037 as a result of incremental demand from humanoids; however, this analysis includes Chinese supply of NdPr oxides, which we know has been exploited in the past to adversely affect foreign markets. Put plainly, the world is quickly realizing it is reliant on China’s REE and permanent magnet supply chain to build cars today and humanoids/robots tomorrow. This uncomfortable realization may drive a meaningful uptick in mining investment in the US and other developed countries after decades of underinvestment.

So, where will the ex-China supply come from in a multipolar world? While MP Materials (MP) and Lynas (LYC.AU) have championed non-Chinese rare earth and permanent magnet supply chains (with ILU.AU currently building a refinery, with first production expected in CY27), China remains in control with ~88% of global refined NdPr supply, an even higher portion of permanent magnet capacity, and >99% of refined HREE supply. As a result, the rest of the world will need to develop not only upstream REE deposits but midstream separating/refining and downstream permanent magnet capabilities. This report highlights over 30 projects across the supply chain, many of which have received some form of government assistance. In the case of upstream and midstream projects, these are categorized based on their exposure to either light or heavy rare earths (Exhibit 7 and Exhibit 8). Based on the data provided by companies regarding their individual projects, the identified projects (mining, refining/separating, and magnet-making) will require $10-12 billion of initial capital investment. However, there are currently very few permanent magnet projects outside China and true level of capital investment needed to break China’s grip on the permanent magnet market is likely much higher.

2. Story in Charts

Exhibit 1: Rare Earths and permanent magnets are required for key defense applications…

Exhibit 2: …which can use 920-9,200lbs of rare earths, raising national security concerns given the world’s reliance on imports from China for these materials

Exhibit 3: Moreover, MS forecasts the growth in humanoids will push NdPr into deficit by 2037…

Exhibit 4:… however, this is inclusive of China supply, which is estimated to account for >70% refined NdPr through the forecast period…

Exhibit 5: …but China’s weaponization of REEs via export restrictions have led to scarcity in Dysprosium…

Exhibit 6: …and Terbium outside of China

Exhibit 7: … suggesting supply chains will need to look elsewhere and incentivize rest of world upstream REE…

Exhibit 8: …and downstream permanent magnet projects to come online…

Exhibit 9: …which will require higher incentive prices according to Woodmac…

Exhibit 10: …underpinning forecasts for increasing NdPr prices through the decade

Exhibit 11: Projects across the Rare Earth + Permanent Magnet Supply Chain located outside China

3. The Upstream: Where Will ex-China Mined Rare Earths Come From?

The pipeline of ex-China projects seems robust, but most projects remain in trial phases, with few companies having published preliminary economic assessments (PEAs) for their respective projects. Moreover, some of the most advanced projects, such as VHM’s Goschen and Lindian’s Kangankunde, both targeting initial production by YE26, are not currently looking to move downstream into separated oxide production. China controls 85-90% of refined production, and essentially all refined heavy rare earth element (HREE) production. Therefore, these projects are unlikely to make a dent in China’s dominance as they will need to ship the concentrate they produce to the customers that can currently process it: Chinese REE refiners.

This list of projects is by no means intended to be exhaustive, and we will continue to monitor for additional developments.

Light REE Upstream Projects

Eneabba Project — Iluka Resources (ILU.AX; Market Cap: US$974m): Iluka Resources is advancing on a rare earth refinery to be located in Western Australia. The facility will have capacity to take ~55kt of concentrate and is expected to produce ~5.5ktpa of NdPr and ~0.75ktpa of DyTb. The project is expected to cost a total of $1.7-1.8bn, of which $680m has been sunk/committed to date, with commissioning of the site expected to begin in 2027. Once complete, Eneabba will represent Australia’s first fully integrated refinery for the production of separated light and heavy rare earths oxides. The refinery will use monazite stockpiles at Eneabba as initial feedstock, along with material from the company’s Balranald mine that will be commissioned in 2H25. Moreover, the facility will have the ability to take 3rd party concentrate as feedstock, though management will pursue these opportunities once closer to start-up.

Phalaborwa Project — Rainbow Rare Earths (RBW.L | Market Cap: US$99m): The Phalaborwa project is located in South Africa and is 85% owned by Rainbow Rare Earths, with option to acquire remaining 15% from Bosveld. The company also sold a 0.85% revenue royalty to Ecora Resources for $8.5m in cash in 2024. The project has a mineral resource of 35.0Mt at 0.44% TREO contained within two phosphogypsum stacks derived from historic phosphate hard rock mining (Exhibit 13). Phalaborwa’s operating cost is expected to be considerably lower than traditional rare earth projects as the phosphogypsum material is already sitting at surface in a chemically cracked form, which eliminates the cost and risk of mining, hauling, crushing, grinding, flotation, and cracking; thus allowing the company to overcome the relatively low grades at Phalaborwa.

The project has a 16-year mine life and expects to process 2.2Mtpa (of the 35.0Mt total resource). Using the 0.44% grades and ~65% recoveries in Phalaborwa’s economic assessment, the company expects to produce ~1,900tpa of rare earth oxides, which includes ~1,820t of NdPr, ~60t of Dysprosium (Dy) and ~20t of Terbium (Tb). The company expects operating costs of $40.83/kg of magnet REO produced, which, based on spot prices for NdPr ($60/kg), Dy ($225/kg) and Tb ($1,000/kg), suggests operating margin of ~46%. Rainbow Rare Earths is targeting initial production in 2027 and is currently in process of preparing a definitive feasibility study for the project, after which financing and construction will begin. The project is expected to integrate midstream operations producing separated oxides of >99% purity.

Bear Lodge — Rare Element Resources (REEMF.OTC; Market Cap: US$374m): Rare Element Resources (RER) is a Colorado based company with 100% ownership of the Bear Lodge asset located in northeastern Wyoming as well as a midstream processing facility located nearby in Upton, Wyoming, where the company is currently finishing construction of a Demonstration Plant that has received ~$24m in funding from the DoE. The company is ~65% owned by a subsidiary of General Atomics who is working with RER to advance the company’s proprietary extraction/separation technology. The Demonstration Plant, which will be using the aforementioned proprietary tech, is expected to begin operations in late 2025 and operate for up to 10 months and produce 10 tons of separated NdPr oxide, which will inform later feasibility studies. The Demonstration Plant will use stockpiled sample materials from the Bear Lodge REE project.

Bear Lodge has a total resource (measured, indicated and inferred) of 7.92Mt at a TREO grade of 3.97%, which implies total contained RE 314kt. Based on a 2014 technical report, the TREO grade of 3.97% has ~23% NdPr content, 0.5% Dysprosium and 0.1% Terbium. The company plans to conduct further economic assessments following completion of the 10 month production period at the Demonstration Plant.

Longonjo — Pensana (PRE.L; Market Cap: US$259m): The Longonjo project is located in Angola and will produce a mixed RE concentrate to export via the Lobito Corridor to a downstream separation plant in the UK that would produce separated oxides. The site has a total Mineral Reserves of 21.5Mt at a TREO grade of 3.04%, which includes ~21.5% NdPr. The current mine plan, based on Mineral Reserves only, has a 20+ year life of mine and expects to produced 20,000t/yr of a mixed rare earth concentrate (MREC). This would be sent to the downstream separation facility that is expected to produce 12,500tpa of separated rare earth oxides, including 4,400tpa of NdPr. The company announced that construction at the site began as of May 2025 and expects the construction and commissioning process to take ~22 months.

Songwe Hill Mine + Pulawy REE Separation Plant — Mkango Resources (LSE: MKA.L; Market Cap: US$81m): Mkango Resources is currently pursuing the development of an REE mine in the East African country of Malawi, the Songwe Hill REE project, that will produce a mixed rare earth carbonate (MREC) to feed a processing/separation facility to be built in Poland. Both the mine and separation facility have been deemed startegic projects by the EU’s Critical Raw Materials Act. Songwe Hill is one of the few rare earth projects to have completed a definitive feasibility study and the mine is expected to have an 18 year life of mine, averaging 5,964tpa of TREO, which includes 1,953tpa of NdPr and 56tpa of Dy and Tb oxide. The MREC will be shipped to the separation facility in Poland, which is currently advancing a feasibility study, that is expected to produce 1,018tpa of NdPr oxide. Both sites have an estimated starting date of production in 2027.

Zandkopsdrift — Frontier Rare Earths (private): The Zandkopsdrift deposit is located in South Africa and has been deemed a strategic project by the EU’s Critical Raw Materials Act (CRMA). Frontier Rare Earths completed a prefeasibility study and began the definitive feasibility study (expected to last 18-24 months) in 2H2023. Upon completion of the DFS, the company will complete front end engineering and construction financing works before commencing a 24 month construction period with first production expected in 1H28. The site plans to process 1Mt of ore each year, which would produce ~4,000tpa of magnet rare earths over a 45+ year life of mine based on current proven and probable reserves. The production will be heavily weighted toward NdPr, which will account for 3,800 of the 4,000t, with Dy at ~143tpa and Tb at 32tpa. Zandopsdrift is currently only focused on extraction of these minerals and producing a TREO concentrate.

Kangankunde REE Project — Lindian Resources (LIN.AX; Market Cap: US$80m): The Kangankunde project is located in Malawi and is fully permitted to commence construction and operations. The company completed a feasibility study in June 2024 that covers “Stage 1” operations, which includes mining operations and a mineral processing plant to produce monazite concentrate. The current operational plan is focused on concentrate production and there are currently no plans to produce separated rare earths. Lindian resources has begun preconstruction activities and is nearing completion of a further optimized feasibility study. The company is targeting initial production in 2026. The asset is expected to produce ~8,250t of TREO each year, which includes ~1,600tpa of NdPr.

Halleck Creek — American Rare Earths (ARR.AX; Market Cap: US$90m): The Halleck Creek project has one of the largest REE resources in North America at 2.63 billion tonnes, however the site has relatively low TREO grades of ~0.33%. The project is located on state and federal land and the company plans to move forward with the Cowboy State Mine, located within Halleck Creek, as it is entirely on state land which can speed up the permitting process by 5-10 years. Based on an updated scoping study in Feb 2025, the company expects to mine 3Mtpa over a ~20 year life of mine and plans to have onsite mineral processing and separation facilities. The company’s scoping study suggests ~1,800tpa of NdPr oxide, 24tpa of Tb oxide and 98tpa of Dysprosium; a pre-feasibility study is expected to be published in 4Q25. In addition, the company is progressing on state permitting and environmental baseline studies, and ARR’s scoping study envisions a 2.5-year construction period. As a result, initial production is not expected until 2029/2030.

Sheep Creek Deposit — US Critical Materials Corp (private): The Sheep Creek Deposit is located in southwest Montana and the land claims owned by US Critical Materials are located on multi-use land administered by the US Forest Service. The site was previously mined in the 1960s, which has allowed US Critical Materials the ability to access significant mineralization and underground samples via pre-existing mine workings that were reopened in 2023 providing access to the property 150-400 feet below the surface. Early stage exploration efforts continue at the site and initial results suggest potential for one of the highest grade deposits in North America at ~9% TREO, of which ~27% is NdPr. The company is partnering with Idaho National Laboratory (INL) on developing a process to handle, separate, and extract metals from the carbonatite ore located at Sheep Creek. The project is still in the very early stages and US Critical Materials in conjunction with INL expect to provide updates on progress made with extraction and purification testing along with a draft flowsheet update in summer 2025.

Lulea Industrial Park + Malmberget and Per Geijer Mines — LKAB (private): LKAB is advancing on development of two iron ore mines with REE byproducts and an industrial processing facility all located in Sweden. The project has been deemed a strategic project by the EU’s Critical Raw Materials Act (CRMA). The company is currently constructing a demonstration plant at Lulea to verify the process to produce critical minerals. The company is still in the permitting phase for the 3 aspects of this strategic project and does not expect to reach full-scale commercial operations at the industrial park until the 2030s.

Brook Mine — Ramaco Resources (METC.O; Market Cap: US$616m): The Brook Mine is located in the Sheridan Coal Field in northern Wyoming and consists of approximately 15,800 acres, of which 4,600 acres are already permitted. The land was originally acquired to be converted into a coal mine in 2012, but Ramaco pivoted and began REE exploration in 2021 and 2022. TREO content is estimated at 1.1-1.4mt at a grade of between 0.0375% and 0.0469%. That said, the companies current tonnage estimates are not considered mineral resources nor mineral reserves as no cut-off grade was applied in preparing the estimated tonnage and grades (i.e., it represents a comprehensive estimate of all in-place minerals, regardless of grade). The company, in conjunction with the Flour corporation, which has been assisting with testing and engineering for the project, plans to release a preliminary economic assessment by the end of 2Q25. Under Ramaco’s commercial development timeframe, the company plans to have pilot operations producing rare earth concentrate in 2026 and also begin production on a full-scale plant to produce commercial oxides by 2028.

Woods Creek — Integral Metals (INTG.CN; Market Cap: US$20m): Located near the Sheep Creek Deposit, in southwest Montana, the site is part of a similar mineralization and targets REE within carbonatite ore. The site is located on federal lands, which face longer permitting timelines, and is currently in early stage exploration/drilling. Initial grab samples of carbonatite collected in 2024 returned a total rare earth oxide (TREO) of 7.08% containing ~14% NdPr. Given the need for further permitting and the long-lead times for permitting on federal land (10+ years in some cases) this project is unlikely to begin production until mid-next decade, barring any changes to the Federal permitting process.

INSPIREE Project — Itelyum (private): The INSPIREE project is located in northern Italy and has been deemed a strategic project by the EU’s Critical Raw Materials Act (CRMA). The site will be a small-scale magnet recycling facility that produces REE oxalates from end of life magnets. The site will have a two-step process with Level I involving the disassembly of magnets and Level II consisting of the recovery of REE oxalates from said magnets at Itelyum’s hydrometallurgical plant. The Level I plant will have dismantling capacity of 1,000 tons/year and the Level II plant will treat 2,000 tons/year of permanent magnets, resulting in the recovery of 700 tons/year of REE oxalates.

Upstream — Heavy REE Projects

Lynas HREE Separation Facility — Lynas Rare Earths (LYC.AX; Market Cap: US$5.6bn): Lynas is currently ramping up operations at its Malaysia separation facility, which according to the company will have separating capacity of 1,500 tonnes of heavy rare earths per year. The company installed the Dy and Tb separation circuits in February of this year and announced first production dysprosium oxides in May, 2025 followed by first production of terbium oxides in June, 2025. Achieving production of separated Dy and Tb has made Lynas the only commercial producer of HREE products outside of China, at a crucial time given China’s recent placement of export controls on these materials. Plans are also underway to construct Light Rare Earth (1.25ktpa NdPr) and Heavy Rare Earth (2.5-3ktpa HRE) separation plants in the US, in partnership with the US Government through the US Department of Defense which were previously expected online in FY26. However there have been some project delays due to wastewater management plan challenges, with LYC in discussions with the US DoD around extra capex required for plan changes underway currently.

Mountain Pass HREE Separation Facility — MP Materials (MP.N; Market Cap: US$7.1bn): MP was awarded $35m in 2022 from the DoD to design and build a facility to process HREE at its Mountain Pass mine. The company is currently mining the Mountain Pass deposit producing ~45kt of TREO in 2024 and is ramping production of its light REE separation facility where it’s producing ~550t per quarter (vs. nameplate capacity of ~1,500t per quarter). MP is currently advancing detailed engineering work and equipment procurement for the project. Based on recent commentary from the company, they expect to bring heavy rare earth separation production at scale starting in 2026. The HREE facility is expected to produce separated Dy and Tb to be used as feedstock for MP’s magnetics facility in Texas.

White Mesa Mill — Energy Fuels (UUUU.A; Market Cap: US$1.2bn): Energy Fuels, traditionally focused on uranium, has been operating the White Mesa processing facility in Utah, the largest uranium processing facility in the US, for 40+ years. Given the sites history processing uranium, the company has expanded its capabilities to process monazite ores, traditionally high in radioactive content, to produce high-purity REE oxides and achieved initial NdPr oxide production in 2024. The material is being validated by customers for potential offtake. The company currently processes monazite sand byproducts from Chemours heavy mineral sands (HMS) mines in the Southeast US. The company plans to import monazite sands from other mining projects they are developing in Australia, Madagascar, and Brazil in the coming years.

The White Mesa mill has installed capacity to process up to 10ktpa of monazite and produce up to 1ktpa of NdPr oxide. However, the current offtake agreement is for 1-2ktpa of monazite sands from Chemours. The company is currently piloting REE oxide separations of heavy REEs such as Dy and Tb while also advancing engineering work on a Phase 2 REE expansion to bring total capacity to 6ktpa of NdPr, 225tpa of Dy and 75tpa of Tb oxides, the Phase 2 expansion is not expected to come online until 2028. The company is simultaneously advancing on HMS mining projects to increase monazite sands production, the mining projects are not expected to come online until 2H27.

Caremag Processing Facility — Carester (private): The Caremag facility, which was deemed a strategic project by the EU’s Critical Raw Materials Act (CRMA), will be based in Lacq, in southern France, and will be a large-scale REE recycling and refining facility. The plant is expected to be operational by late 2026 and will recycle 2,000 tonnes of rare earth magnets and refine 5,000 tonnes of mining concentrate annually. The plant is expected to produce 600 tonnes per year of dysprosium and terbium oxides, as well as 800 tonnes per year of Nd and Pr oxides. The company has raised €216m to build the facility, which includes €110m from Japan Organization for Metals and Energy Security (JOGMEC) and private-sector Iwatani corporation as well as €106m from from various subsidies and advances provided by the French government. The company has already entered into a long-term agreement with Stellantis in September 2024 to supply over 3,400 tonnes of Nd, Pr, Dy and Tb oxides over the next 10 years.

Carina Project — Aclara Resources (ARA.TO; Market Cap: US$157m): The Carina Project is Aclara’s flagship REE project. It is an ionic clay deposit, historically the source for most of the world’s supply of HREE, located in Goias, Brazil. The company is testing operations from a pilot plant to process ionic clays and recently announced the successful production of HREE concentrate (here). Moreover, the company recently submitted its Environmental Impact Assessment to the Brazilian government (here) and is simultaneously advancing on a pre-feasibility study and feasibility study, which are expected to be released in 3Q25 and 1Q26, respectively.

The site has a total Mineral Resource of 297.6Mt at a TREO grade of 1.45% (~19.5% NdPr, 2.7% Dy and 0.4% Tb). Annual production is expected to be ~1,350t of NdPr, 163t of Dy and 28t of Tb. Mining operations are expected to begin in 2028 and concentrate will be sent to a separation facility to produce oxides. The separation facility will be located in the US and Aclara is working with the US Department of Commerce to identify the most strategic site for the facility. The company expects to progress on laboratory test work and integrated pilot scale testing for its separation plant in 2025.

Penco Module — Aclara Resources (ARA.TO; Market Cap: US$157m): The Penco Module is Aclara’s second REE project, is located near Concepcion, Chile, and is expected to start operations in 2027. The site has a relatively small Mineral Resource of 29.2Mt at a TREO grade of 2.28% (19.4% NdPr, 2.9% Dy and 0.4% Tb). Annual production is expected to be ~126t of NdPr, 45t of Dy and 6t of Tb. The company’s pilot plant ran in 2023 and confirmed the processing parameters and process flowsheet design for a future full-scale plant design. In addition, it produced high purity HREE concentrate to feed separation trials. The company applied for its environmental permits in 2024, received a response from the relevant Chilean Environmental agency in September 2024, and submitted a comprehensive report in March 2025 addressing technical observations that were raised.

Goschen Rare Earth Project — VHM (VHM.AX; Market Cap US$34m): The Goschen project is located in Victoria, Australia. The project is one of the only REE projects in development with proven and probable reserves along with its larger mineral resource. The project has total reserves of 98.8Mt at TREO grades of 2.45% with NdPr as ~18.5%, Dy at 2.5% and Tb at 0.4%. The total Mineral Resource is 491.8Mt at TREO grades of 2.14% with NdPr at 19.2%, Dy at 2.3% and Tb at 0.5%. The company has already received its mining license and expects to receive its environmental and workplan approvals within the 2Q25-3Q25 timeframe, with a final investment decision expected to be announced by YE25. Construction and commissioning are expected to begin soon thereafter with initial production slated for 4Q26, pending permit approvals.