190 H BMO CAPITAL MARKETS 808

332 H STANDARD CHARTERED B 20

363 H WELLS FARGO SECURITI 209

661 C JP MORGAN SECURITIES 144 428

686 C STONEX FINANCIAL INC 2 18

709 C BARCLAYS 265

737 C ADVANTAGE FUTURES 3

905 C ADM 11

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 954 CONTRACTs NOTICES FOR 95,400 OZ or 4.437 TONNES

total notices so far: 8874 contracts for 887,400 OR 27.601 tonnes)

SILVER NOTICES: 270 NOTICE(S) FILED FOR 1.35 million OZ/

total number of notices filed so far this month : 8,499 CONTRACTS (NOTICES) for 42.495 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 27.295 MILLION OZ

AND JULY: 44.105 MILLION OZ//

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 56.681 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 2394 CONTRACTS OI TO 173,668 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 615 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 615 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 220 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2394 CONTRACTS AND ADD TO THE 615 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF 1779 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN IN PRICE OF $0.14 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 8.383 MILLION PAPER OZ

OCCURRED WITH OUR $0.14 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS MONDAY MORNING:

SHANGHAI CLOSED DOWN 14.65 PTS OR 0.42%

//Hang Seng CLOSED UP 315.48 PTS OR 1.30%

// Nikkei CLOSED UP 218.40 PTS OR 0.55% //Australia’s all ordinaries CLOSED UP 0.68%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1736 OFFSHORE CLOSED UP AT 7.1758/ Oil DOWN TO 66.37 dollars per barrel for WTI and BRENT DOWN TO 68.66 Stocks in Europe OPENED MOSTLY ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1736 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1758 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7813 CONTRACTS TO A STILL LOW NUMBER OF 453,590 OI WITH OUR SMALL GAIN IN PRICE OF $0.90 WITH RESPECT TO MONDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2000 ). WE HAD LITTLE T.A.S. LIQUIDATION //MONDAY TRADING.

THE CME ANNOUNCED MONDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES.

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY 0

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 9813 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON FRIDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE IN JANUARY THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND NOW JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS ANOTHER MEGA MEGA HUGE T.A.S. AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A MUCH HIGHER 22,678 T.A.S CONTRACTS THAN MONDAY;’S ISSUANCE. I THOUGHT THAT THE CASINO HAD THROWN IN THE TOWEL WITH MONDAY’S MUCH SMALLER 10,800 T.A.S. ISSUANCE. BUT I WAS WRONG: THE CROOKS DID NOT ABANDON THEIR USUAL AND CUSTOMER 5 MEGA ISSUANCES WITH TODAY’S NO 5 HIGH 22,678 NUMBER. THEY DESPERATELY NEED TO CONTAIN GOLD FROM EXPLODING IN PRICE.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. HOWEVER JULY IS HUGE FOR A NON DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S MAMMOTH QUEUE JUMP OF 1.800 TONNES QUEUE JUMP = 28.637 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 28.637 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 10+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2000 EFP CONTRACT WAS ISSUED: : /AUGUST 2000 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2000 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- LITTLE LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY

- ZERO NET SPEC LIQUIDATION WITH OUR GAIN IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY MORNING/MONDAY NIGHT WAS A HUGE BUT MUCH LARGER 22,678 AND THAT COMPLETES OUR 5 MEGA MEGA T.A.S ISSUANCES. THE CROOKS USE THESE T.A.S. ISSUANCE TO TAME THE PRICE OF GOLD.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE MONDAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.THIS WAS SURELY IN EVIDENCE IN TRADING MONDAY WITH OUR SMALL GAIN IN PRICE!

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S HUGE 1.800 TONNES QUEUE JUMP = 28.637 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 54 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $0.90/ /) AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF SOME NET SPECULATOR LONGS AS WE DID HAVE AN STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD LITTLE T.A.S. SPREADER LIQUIDATION ////MONDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE MEGA MEGA T.A.S. ISSUANCES, TUESDAY MORNING , IN ORDER TO COMMENCE CONTINUAL RAIDS ON OUR PRECIOUS METALS. SO FAR THIS WEEK, THIS EXERCISE HAS BEEN A TOTAL FAILURE…

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; ZERO SO FAR

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE GAINED A STRONG SIZED TOTAL OF 30.52 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S MAMMOTH QUEUE JUMP OF 57,900 OZ OR 1.800 TONNES OF GOLD//NEW STANDING ADVANCES TO 28.637 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $0.90

WE HAD 122 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 9813 CONTRACTS OR 981,300 0Z (30.52 TONNES)

confirmed volume MONDAY 254,763 contracts FAIR

speculators have left the gold arena

END

INITIAL GOLD COMEX

JULY CONTRACT MONTH

JULY 15/2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entries . |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | 0 ENTRIES xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 954 notice(s) 95,400 OZ 4.437 TONNES |

| No of oz to be served (notices) | 333 contracts 33,300 OZ 1.0357 TONNES |

| Total monthly oz gold served (contracts) so far this month | 8874 notices 887,400 oz 27.601 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entry

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entries

adjustments: 1

dealer to customer Brinks 3858.120 oz

(120 kilobars)

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JULY STANDS AT 1287 CONTRACTS FOR A GAIN OF 443 CONTRACTS. ON MONDAY WE HAD 136 NOTICES FILED, SO WE GAINED A STRONG 579 CONTRACTS OR 57900 OZ (1.800 TONNES) ENTERTAINED WITH A MAMMOTH QUEUE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD

AUGUST LOST 12,839 CONTRACTS DOWN TO 241,951 AS AUGUST BECOMES THE FRONT MONTH AND IT’S OI IS VERY HIGH AND NOT CONTRACTING ENOUGH. WE WILL PROBABLY HAVE A HIGH NUMBER OF TONNES STANDING.

SEPT GAINED 82 CONTRACTS TO 1570

We had 954 contracts filed for today representing 95,400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 144 notices issued from their client or customer account. The total of all issuance by all participants equate to 954 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 428 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (8874 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (1287 CONTRACTS) minus the number of notices served upon today (954 x 100 oz per contract) equals 920,700 OZ OR 28.637 TONNES to which we add 0 tonnes of gold issued under exchange for risk// total standing 28.637 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (8874 x 100 oz +we add the difference for front month of JULY (1287 OI} minus the number of notices served upon today (954 x 100 oz) which equals 920,700 OZ OR 28.637 TONNES + 0 tonnes EX FOR RISK = 28.637 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 28.637 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,200,612.131 oz 68.44 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,748,662.049 oz

TOTAL REGISTERED GOLD 20,200,299,.198: or 628.314 tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,548,362.951 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 17,996687 oz (REG GOLD- PLEDGED GOLD)= 559.86 tonnes //

total inventories in gold declining rapidly

SILVER/COMEX

THE JULY 2025 SILVER CONTRACT//INITIAL

JULY 15

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entry 2 ENTRIES i) Out of DELAWARE: 2010.290 OZ 2) out of Loomis: 645,058.060 oz total withdrawal: 645,074.3450 oz |

| Deposits to the Dealer Inventory | 1 ENTRY 1 ENTRY i) Into Stonex: 638,629.010 oz total deposit 638,629.010 oz |

| Deposits to the Customer Inventory | 2 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into CNT 18,018.970 oz ii) Into Stonex 2894.000 oz total deposit 20,913.970 oz |

| No of oz served today (contracts) | 270 CONTRACT(S) (1.35 MILLION OZ |

| No of oz to be served (notices) | 322 contracts (1.610 MILLION oz) |

| Total monthly oz silver served (contracts) | 8499 Contracts (42.495 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposits into dealer accounts

1 ENTRY

i) Into Stonex: 638,629.010 oz

total deposit 638,629.010 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into CNT 18,018.970 oz

ii) Into Stonex 2894.000 oz

total deposit 20,913.970 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

2 ENTRIES

i) Out of DELAWARE: 2010.290 OZ

2) out of Loomis: 645,058.060 oz

total withdrawal: 645,074.3450 oz

ADJUSTMENTs 2 customer to dealer

a) Brinks: 392,491.659 oz

b) CNT 337,099.85 oz

TOTAL REGISTERED SILVER: 195.584 MILLION OZ//.TOTAL REG + ELIGIBLE. 496.635 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 592 OPEN INTEREST CONTRACTS FOR A LOSS OF 360 CONTRACTS. WE HAD 370 CONTRACTS SERVED UPON MONDAY SO WE GAINED 10 CONTRACTS OR 50,000 OZ ENTERTAINED A SMALL QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST GAINED 20 CONTRACTS TO 2592 AS THIS MONTH BECOMES THE FRONT MONTH FOR SILVER

SEPTEMBER LOST 4219 CONTRACTS DOWN TO 131,041 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 270 or 1.350 MILLION oz

CONFIRMED volume; ON MONDAY 88,350 huge//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 8499 X5,000 oz = 42.495 MILLION oz

to which we add the difference between the open interest for the front month of JULY (592) AND the number of notices served upon today (270 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (8499) Notices served so far) x 5000 oz + OI for the front month of JULY(592) minus number of notices served upon today (270)x 5000 oz equals silver standing for the JULY contract month equating to 44.105 MILLION OZ .

New total standing: 44.105 million oz which is huge for this active delivery month of JULY. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 195.584 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/496.635 million. 42.33%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

JUNE 20 WITH GOLD DOWN $19.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 947.37 TONNES

JUNE 18 WITH GOLD UP $1.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.03 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 945.94 TONNES

JUNE 17 WITH GOLD DOWN $9.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 941.93 TONNES

JUNE 16 WITH GOLD DOWN $33.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.758 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 940.49 TONNES

JUNE 13 WITH GOLD UP $53.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.38 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 932.91 TONNES

JUNE 12 WITH GOLD UP $55.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 934.19 TONNES

JUNE 11 WITH GOLD UP $1.10 TODAY// SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.31 TONNEES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 935.91 TONNES

JUNE 10 WITH GOLD DOWN $11.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.02 TONNEES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 936.22 TONNES

JUNE 9 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.45 TONNEES OF GOLD FROM THE GLD//: /// ///INVENTORY RESTS AT 934.20 TONNES

JUNE 6 WITH GOLD DOWN $28.00 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

GLD INVENTORY: 947.64 TONNES, TONIGHTS TOTAL

SILVER

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

JUNE 20 WITH SILVER DOWN $0.83/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.818 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 474.641 MILLION OZ.

JUNE 18 WITH SILVER DOWN $0.20/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 17 WITH SILVER UP $0.67/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 473.096 MILLION OZ.

JUNE 16 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.727 MILLION OZ FROM THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 13 WITH SILVER UP $0.11/NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 473.550 MILLION OZ.

JUNE 12 WITH SILVER UP $0.11/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.276 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 473550 MILLION OZ.

JUNE 11 WITH SILVER DOWN $0.45/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.046 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.274 MILLION OZ.

JUNE 10 WITH SILVER DOWN $0.16/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.232 MILLION OZ.

JUNE 9 WITH SILVER UP $0.69/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.914 MILLION OZ.

JUNE 6 WITH SILVER UP $0.63/HUGE CHANGES AT THE SLV:A DEPOSIT OF 3.863 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.732 MILLION OZ. (A TOTAL DEPOSIT OF 11.856 MILLION PHANTOM OZ IN THE LAST 4 DAYS)

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

CLOSING INVENTORY 481.175 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG

Gold Revaluation: Trump’s Red Button Option?

Tuesday, Jul 15, 2025 – 02:00 PM

Authored by Matthew Piepenburg via VonGreyerz.gold,

Could a gold revaluation be on Trump’s mind? Below, we consider the options facing a debt-sick America.

A Bug Racing for a Windshield

As we’ve been warning for years, the US and USD are a bug rapidly seeking a debt-hard windshield.

The trend and speed of this collision (and debt trap) are becoming increasingly more obvious with each passing day and headline.

In simplest terms, as US debt levels soar moon-bound, trust and interest in its IOUs (and the currency/dollar backing those IOUs) are sinking toward the ocean floor.

The evidence of such otherwise “dramatic” statements is literally everywhere.

Hard Questions

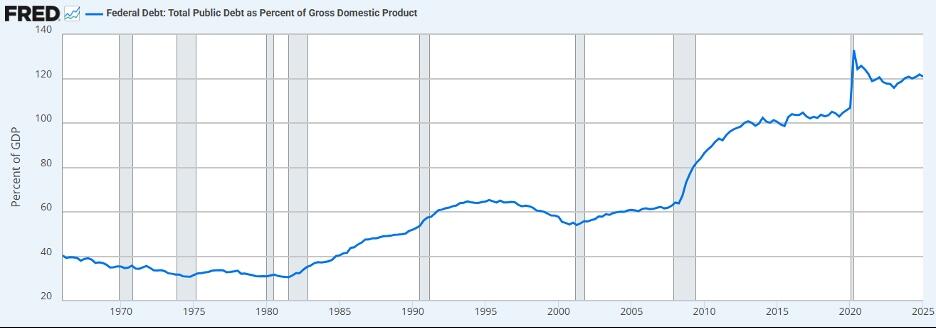

For example, although not at war, the US is running World War 2 debt-to-GDP ratios at the 120% level.

How did this happen? What’s the “emergency” behind this grotesque ratio?

And more importantly, how can Uncle Sam save himself?

Simple Answer

Answering the first question is fairly simple.

We arrived at this appalling turning point because the US has been getting debt drunk for decades.

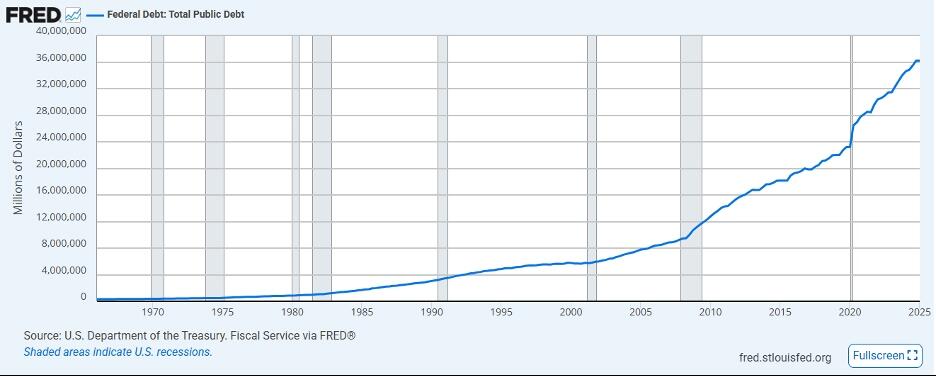

Ever since Nixon took away the gold chaperone from the USD, politicians have been buying temporary prosperity, debt-based “growth” and duped voters by taking US public debt levels from $248B in 1971 to $37T (and counting) today.

This number alone is staggering.

Trillions Matter

The difference between “billions” and “trillions” is not merely alphabetical, it’s brutal.

1 BILLION seconds ago, for example, places us in 1997. Bit 1 TRILLION seconds ago places us at 30,000 BC.

Let that sink in for a moment.

If this shocks or bothers you, well… you’re not alone.

The World Has Called the USA’s Bluff

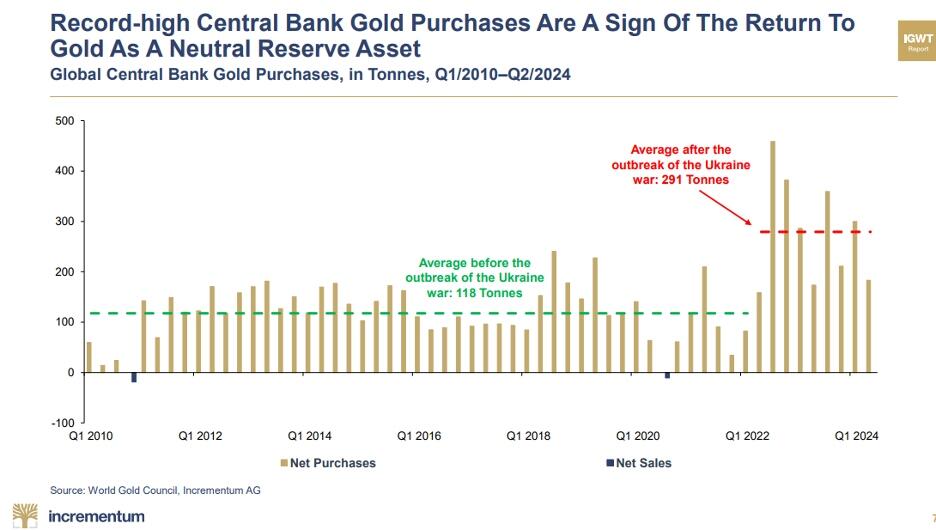

The rest of the world is shocked too, which explains why its central banks have been quietly net-dumping USTs and net-stacking physical gold since 2014.

This further explains why freezing the FX reserves of Russia in 2022 only accelerated the distrust of a now weaponized (and once neutral) world reserve currency.

De-Dollarization…

What followed was a well-telegraphed and carefully forewarned trend of de-dollarization from the BRICS+ coalition.

Tier-1 Status…

This trend took off around the very same time that the BIS, the mother of all central banks, officially classified gold as a Tier-1 reserve asset, making an open mockery of its “sister Tier-1 asset,” the UST.

Central Bank Gold Stacking…

Gold stacking by central banks, of course, continued to skyrocket at the same time:

COMEX Panic…

If such signs of US dollar and debt woes/distrust were not obvious enough, the COMEX and LBMA exchanges out of New York and London then began scurrying like headless chickens.

Why?

Because they were trying to find enough physical gold to meet delivery demands to get the gold off of these exchanges, which, since 1974, were once just derivative schemes used to manipulate rather than deliver gold.

But the hidden facts (and implications) were far simpler. Counterparties to this legalized price-fixing scam now wanted their actual gold more than their paper contracts.

Why?

Because they saw physical gold’s growing, inevitable and superior role in a future monetary system moving away from the debt-discredited USD and UST.

Petrodollar Signposts…

To add insult to the USD’s injury, a growing and simultaneous trend away from the petrodollar during the same period was as obvious as it was media-ignored.

But the message was clear: Faith in a USD-driven future was openly in decline.

The Denial Stage?

Defenders of the USD, of course, were quick and right to remind the world that no other nation or currency could beat or replace the mighty Dollar.

After all, it is the world’s reserve currency.

It still holds the majority position in global FX reserves and, let’s be honest, neither China, Russia, nor any other nation has the reputation or bond market to replace the dollar, right?

Right.

Reality Check: Gold’s Future in a Fiat Swamp

But, here’s the kicker.

Nations like China or Russia aren’t trying to replace the USD with their Ruble or Yuan.

They, like the rest of the world, are slowly going to replace the USD with gold.

This doesn’t mean a gold-backed world reserve currency, just a gold-based world settlement system.

China Playing Chess

Take China as an obvious example.

They have no problem de-valuing their fiat currency when measured against gold, an asset they’ve been quietly stacking and misreporting for decades in a chess game of common sense as the USA plays checkers with QE.

Nor does China have much love for USTs…

As I type this, China continues to pair gold to the oil it imports from Russia and Iran (conveniently dubbed “evil” by the weaponized US media).

In just over a decade, China’s gold-to-oil ratio was 8 barrels of oil to one ounce of gold. Today, that same ounce of gold buys China 50 barrels of oil.

Meanwhile, China has no problem seeing its Yuan price of gold rise from 7000/ounce in 2014 to 24,000/ounce today.

In short, the Yuan has collapsed against gold but not against the USD.

But China can live with this for the simple reason that it sees a gold-based new world order, and it has been stacking that gold for years.

Why?

Because the BIS, the IMF, and, of course, the BRICS+ nations see a world in which gold is superior to the debt-discredited USD as a strategic reserve asset.

Gold: Far More than an “Allocation”

Gold is no longer an allocation, hedge or subject of debate—it is the future of global trade and currency settlements. Period.

My colleague, Egon von Greyerz, saw this decades ago.

Of even date, for example, gold is now 20 % of global FX reserves. The USD percentage is falling dramatically to a 46% position, and the Euro holds a 16% slot.

But if central backs and BRICS+ nations continue to stack gold at current levels, gold may not be an official “world reserve currency” in substance or title, but it will be the new leading FX reserve asset in both title and power.

In sum, each of the foregoing themes, of which we have detailed and warned in numerous prior articles, explains the debt “emergency” facing the USD.

The Real Question: What Can the USA Do Now?

But what about the corollary question? That is: What options do the US have left to solve its debt (and hence currency) crisis?

This, too, has been on our minds for years.

More Fantasy Money?

Ultimately, there are no easy solutions or good scenarios left.

The MMT fantasy, for example, of solving a debt crisis with more debt that is paid for with mouse-clicked money has been tried in earnest since the QE guns took the Fed from a pre-08 balance sheet of $800B to a 2022 high of nearly $9T.

As reminded above, that difference between a Billion and Trillion is just plain madness.

The US, faced with solving its debt crisis (and bond market) at the expense of its paper dollar, is running out of time, options and global patience.

So, again—what can the US do today?

More War?

For Hemingway, at least, the most obvious next step is further currency debasement and war, which the past, current and even future headlines seem to confirm, from the Middle East to Eastern Europe:

But with distrust in US politics and foreign policies rising in alternative media platforms highlighting left and right scandals on everything from Russia-Gate laptops to Epstein cover-ups and AIPAC-guided uh-ohs, trust in the left and right stirrups of the DC saddle is tanking at a rapid rate.

Re-sets, DOGE Cuts & Tariff Walls?

Meanwhile, the IMF has been telegraphing a great reset since COVID, and the current Trump administration has been trying to use DOGE cuts and tariff wars to bring debt and spending levels down.

But regardless of one’s political bias, let’s be mathematical: None of these policies is enough, and none of them, as of today, are even working – as the Elon/Trump social media war intensifies in a backdrop of rising rather than falling deficit levels.

More Financial Repression?

I also expect, and have warned of, more financial repression and capital controls around the corner.

But again, not much of a solution given current and future debt levels, debased dollars (worst DXY Q3 in 40 years) and a middle class already on its knees.

The Red Button Option: Gold Revaluation?

But DC has another option, which even the Fed’s recent May 2025 Manual openly hints toward.

I call it the “red-button option” of a radical gold revaluation to effectively use a precious metal (rather than a Fed mouse-click) to achieve QE-like monetization without having to issue more unloved USTs.

One can read the Fed’s lengthy May report on their own, but the Fed-speak boils down to this:

The Fed can add gold certificates to its balance sheet, which can then become assets of the Treasury Department’s TGA account to pay down a sliver of its $37-TRILLION-dollar public debt.

But the trillion-dollar question remains: How will these $42.00 gold certificates be re-valued?

Doing the Math

In a February Forbes article, for example, there was talk of marking these certificates to market.

If that were the case, the 8131 tons of US gold (roughly 260 million ounces) at the current spot price would give Uncle Sam about $850B in instant new money to pay off some debts.

This is nice, but hardly a solution to getting the aforementioned 120% debt-to-GDP figure down to pre-08 levels at a ratio compelling enough to restore trust in—and demand for—Uncle Sam’s unwanted IOUs.

But what if the US government put in a bid for $20,000 gold?

This would create a new price floor for the precious metal while simultaneously placing newly revalued gold certificates ahead of UST’s and mortgage-backed-securities on the Fed’s balance sheet?

Sound crazy?

If you read the May Fed Report, they hint at such a balance sheet “example” but shy away from naming a new price valuation on the gold certificates.

This means we can only guess at what comes next.

Desperate Times, Desperate Measures?

But desperate times require desperate measures, and there is nothing more desperate than the USA (and balance sheet) in its current form.

An emergency gold re-valuation of $20,000, by way of just one example (perhaps lower, perhaps higher?), would create instant trillions in liquidity to address Uncle Sam’s otherwise mathematically unsustainable bar tab.

Such a measure would buy time for US IOUs and votes for a beleaguered White House.

Such considerations, once thought extreme, must now be considered with desperate seriousness in a backdrop of only desperate options.

Nixon made a radical change in 1971. Can a red-button gold revaluation in 2025 or 2026 be equally ignored?

Let’s wait and see.

Be Careful of What You Wish For

And regardless of whether the inflationary red button is pushed or not, gold wins either way, as the dollar’s purchasing power in such a debt landscape has no absolute direction left to it other than downward.

Gold, as the ultimate, most stable, stacked and historically most trusted anti-fiat asset, has no direction left than upward.

Let’s also not forget that if gold is so re-valued, then the nation with the most gold will have the most leverage in this new system.

But as I’ve suggested elsewhere, that nation is more likely to be China than the USA. It has a lot more gold than the World Gold Council reports…

If so, like all empires whose average hegemonic age hovers around 250 years, the era of the American empire is coming to an obvious turning point, no matter how you stack it.

ALASDAIR MACLEOD

JOHN RUBINO

CHRIS POWELL AND GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 231

5. COMMODITY REPORT…ORANGE JUICE

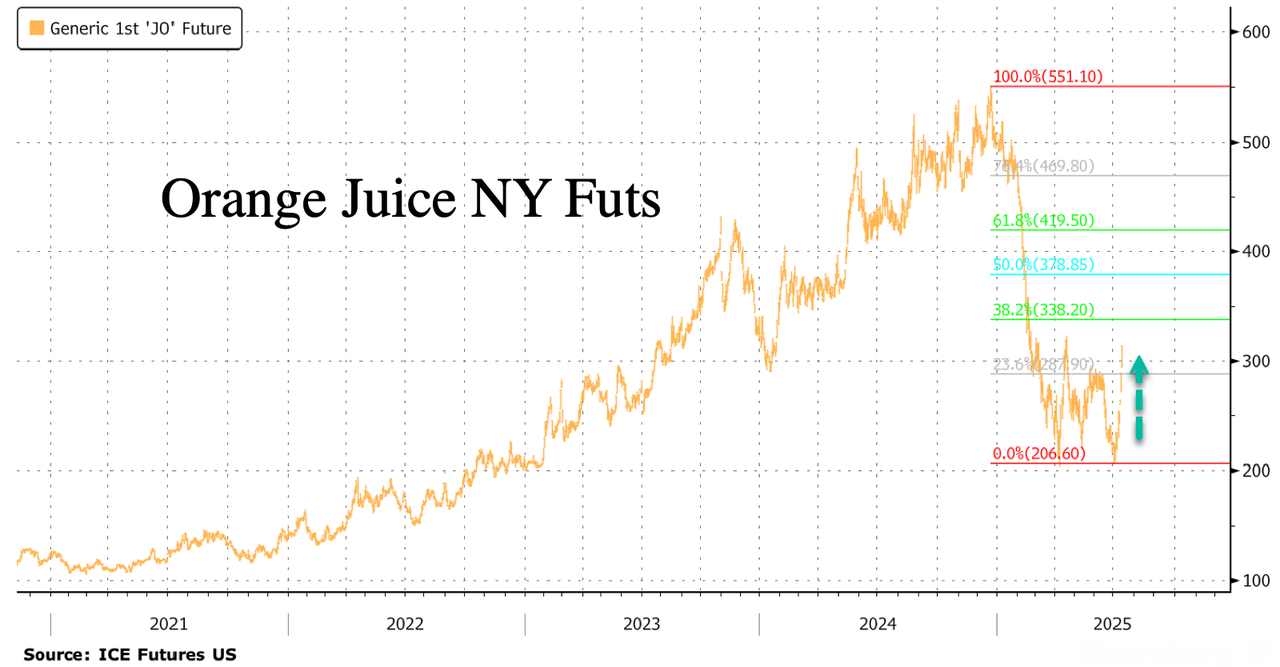

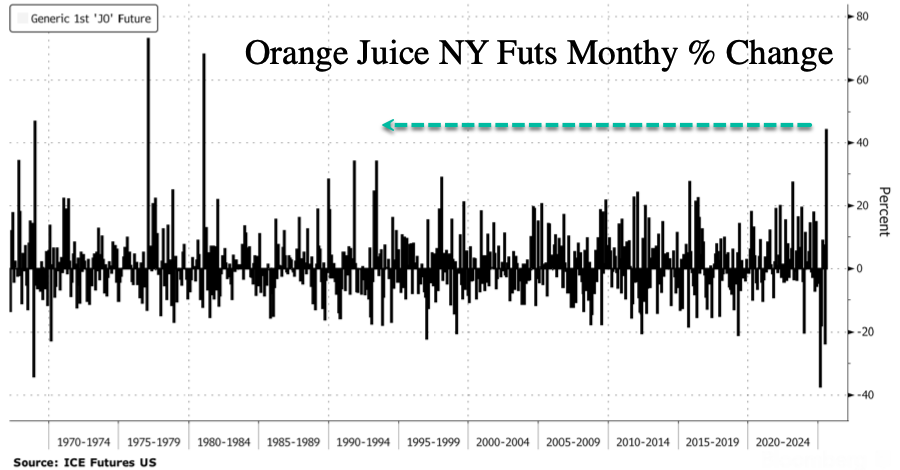

Orange Juice Futures Squeeze On Trump’s Brazil Tariff Threat

Monday, Jul 14, 2025 – 11:00 PM

President Trump fired off a flurry of trade warning letters last week to countries including South Korea, Brazil, Europe, Mexico, and Canada. In one letter to Brazilian President Luiz Inácio “Lula” da Silva, Trump announced the potential for a new 50% tariff on imports from Brazil. The move has since sparked fears of supply disruptions and sent orange juice futures in New York soaring to a four-month high.

The most active contract jumped 8.655% to $3.1385 a pound on Monday, the highest since early March. Orange juice futures have been rallying since Trump’s trade warning letter to the South American country last week, stoking fears of renewed supply disruptions. Prices previously surged as high as $5 a pound in late 2024, as U.S. orange juice production fell to decade lows. Prices then crashed earlier this year.

OJ is on track for the largest monthly gain since January 1981.

The threat of disrupted OJ supplies comes as the U.S. has ramped up imports from Brazil in recent years, with Florida production in disarray due to greening disease and hurricanes that have devastated large swaths of groves, according to Craig Elliott, a market analyst at Expana, as cited by Bloomberg. He noted that while the full impact of the proposed tariff remains uncertain, the volume of trade at risk is substantial and could further undermine Brazil’s competitiveness.

Tariffs risk upending Brazil–U.S. ag trade across a wide range of goods (much more than just OJ) — from coffee and red meat to poultry, pork, and more.

END

RARE EARTHS/MP MATERIALS

MP Materials Surges 10%, Apple To Announce $500 Million Partnership, Joining Pentagon As Investors

Tuesday, Jul 15, 2025 – 06:55 AM

Apple is reportedly set to join the Pentagon as an investor in MP Materials and announce a $500 million partnership with the company, according to a Fox Business report citing individuals familiar with the matter this morning.

MP shares surged more than 10% on the news in a move that comes after a more than 100% gain over the last several months for the critical U.S. rare Earth mineral company.

The deal includes a commitment from Apple to purchase rare earth magnets produced at MP’s facility in Texas, using domestically sourced materials. As part of the agreement, the two companies are also expected to develop a new recycling facility in Mountain Pass, California, to recover and repurpose rare earth elements from used electronics.

In addition, Apple and MP plan to build a second manufacturing plant in Fort Worth, Texas, further solidifying a U.S.-based supply chain for these critical materials.

Over a month ago, we flagged MP and USA Rare Earth as two companies likely to be major winners from Washington’s rare earth reshoring push—particularly under policies aimed at reducing reliance on China. Since we first mentioned it more than a month ago, the stock is up more than 100%.

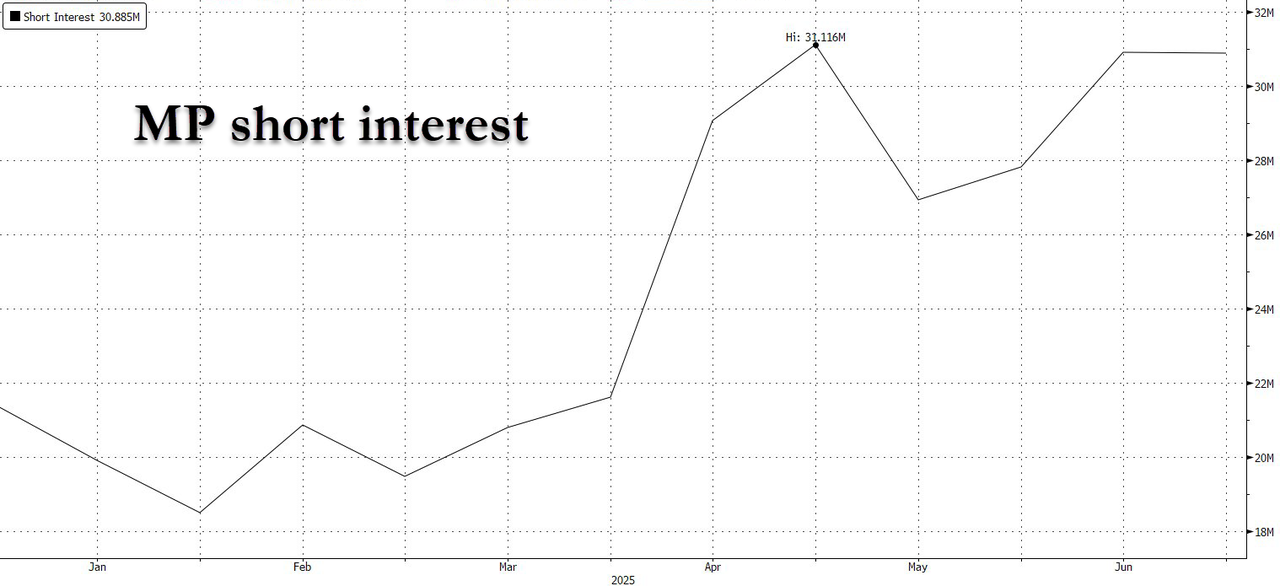

We noted at the time that MP’s uniquely central role in the domestic rare earth supply chain positioned it for outperformance, and we pointed out that the stock had an enormous 21% short interest, making it ripe for a squeeze.

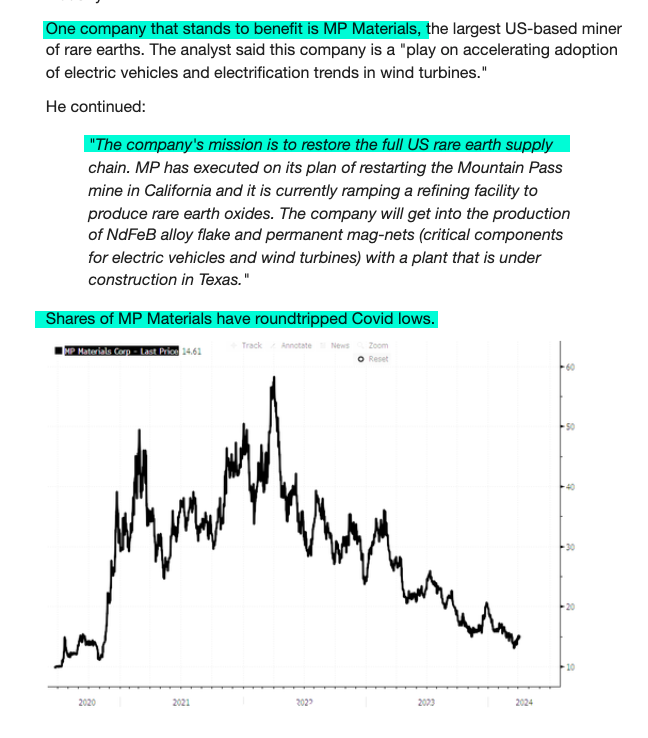

Recall that one year ago, in our April 2024 note titled “Next Big Mineral Trade Revealed by Morgan Stanley,” we identified MP Materials as “one company that stands to benefit” from the restoration of America’s rare earth supply chain.

Further, our most recent report for subscribers “The Coming Rare Earth Revolution And How To Profit: All You Need To Know About The “Ex-China Supply Chain“ detailed why MP stood to substantially outperform in the coming months and years as the critical rare earth supply chain was shifted domestically to exclude China, and to benefit domestic miners and producers such as MP.

Our conviction was promptly validated days ago when the U.S. government—via the State Department and the Pentagon—took a 15% stake in MP, an exceedingly rare move that made the U.S. the company’s largest shareholder.

The investment marked a “transformational” public-private partnership by the Trump admin, aimed at building a domestic rare earth element supply chain. As part of the deal, the Pentagon will receive convertible preferred shares and warrants equal to a 15% stake—surpassing stakes held by CEO James Litinsky and BlackRock. The shares convert at $30.03 each and carry no cash dividend.

MP stock surged over 50% on the news, becoming the top performer in the mining sector this year and more than covering the cost of our premium subscription for readers who acted quickly.

That was great news. But it was even better news that among the biggest shorts were Goldman’s hedge fund clients who, for months, had plotted and schemed how to unobtrusively short the name during the bank’s various idea dinner events.

Here is an excerpt from the latest note by Goldman energy and natural resources specialist Adam Wijaya out days ago:

Rare Earths… how high… biggest move in the space yesterday came from Rare Earths complex… led by MP +51%… have hosted several Metals idea dinners over the last few weeks and this name has been a consensus short… pain yesterday was real…

Now, that pain is very likely going to continue today. Thanks, “Tim Apple”.

END

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 14.65 PTS OR 0.42%

//Hang Seng CLOSED UP 315.48 PTS OR 1.30%

// Nikkei CLOSED UP 218.40 PTS OR 0.55% //Australia’s all ordinaries CLOSED UP 0.68%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1736 OFFSHORE CLOSED DOWN AT 7.1758/ Oil DOWN TO 66.37 dollars per barrel for WTI and BRENT DOWN TO 68.66 Stocks in Europe OPENED MOSTLY ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN TRADING AT 7.1736 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1758 AGAINST US DOLLAR/ AND THUS WEAKER

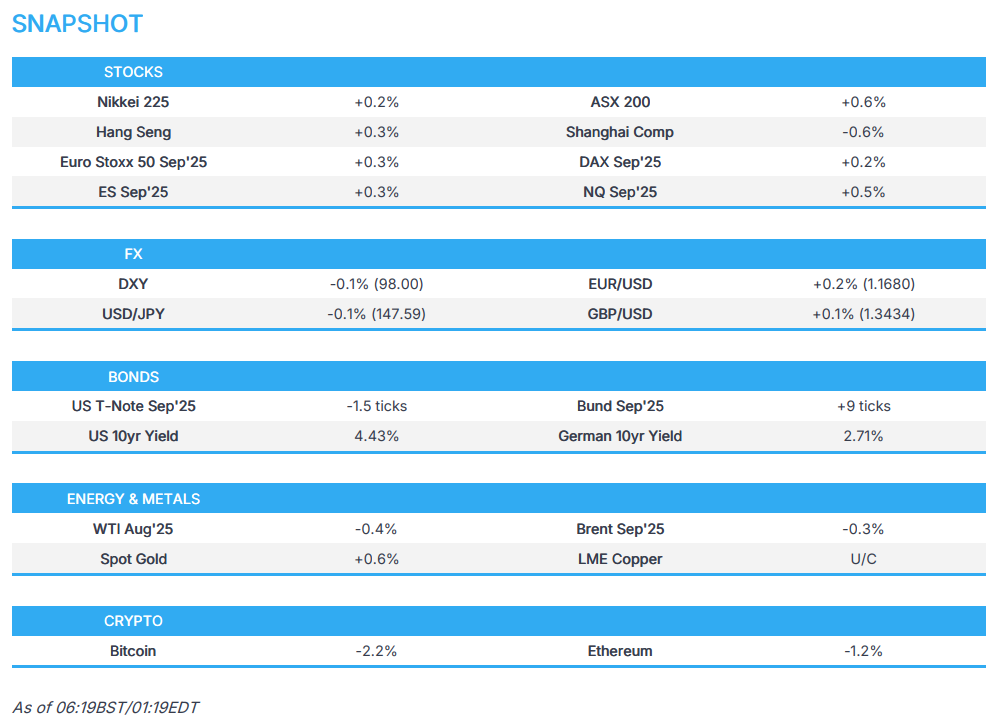

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1736 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1758 (CCP MANIPULATED)

SHANGHAI CLOSED DOWN 14.65 PTS OR 0.42%

HANG SENG CLOSED UP 315.58 PTS OR 1.30%

2. Nikkei closed UP 218.40 PTS OR 0.55%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 97.65/ EURO RISES TO 1.1659 UP 24 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.577//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.66…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6940/Italian 10 Yr bond yield DOWN to 3.578 SPAIN 10 YR BOND YIELD DOWN TO 3.304%

3i Greek 10 year bond yield DOWN TO 3.401

3j Gold at $3364.25 Silver at: 38.33 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 19 /100 roubles/dollar; ROUBLE AT 77.91

3m oil (WTI) into the 66 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.66// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.577% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7956 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9300 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.418 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.957 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.898 DOWN 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.22

10 YR UK BOND YIELD: 4.5740 DOWN 3 PTS

10 YR CANADA BOND YIELD: 3.519 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 3.048 UP 0 PTS

2a New York OPENING REPORT

Futures Rise, Nvidia Spikes After Trump Greenlights Selling Some Chips To China

Tuesday, Jul 15, 2025 – 08:26 AM

US equity futures are higher, led by Tech with the biggest overnight news being that Trump is allowing NVDA to resume its (less advanced) H2O chip sales to China; there had been chatter of a chips-for-rare earths pact to thaw US/China trade relations. As of 8:00am ET, S&P futures rose 0.3%, while Nasdaq futures rose 0.5%, with NVDA jumping another +5.3% in pre-market trading, while AMD +3.5%, MRVL +2.85, AVGO +1.4% also gained. The balance of Mag7 is mostly higher; semis are poised to be the best sub-group, and cyclicals are higher with banks with a mild bid into earnings this morning. Bond yields are lower as the curve bull flattens into CPI with JPM noting that some FICC client convos are pointing to a dovish CPI print. The USD is weaker and commodities are declining across all 3 complexes though precious, crude, and sugar remain bid. Today’s focus is the unofficial kick off 25Q2 earnings and Banks have a low bar to cross and CPI is not yet expected to reflect the expected inflation from the trade war.

In premarket trading, Mag 7 stocks were higher: Nvidia rose 4.4% as the company planned to resume sales of its H20 AI chip in China after securing Washington’s assurances that such shipments would get approved (Meta +0.6%, Apple +0.3%, Alphabet +0.2%, Amazon +0.2%, Tesla +0.2%, Microsoft -0.1%).

- Semiconductor firms also gain alongside Nvidia, including AMD (AMD) +5% and Broadcom (AVGO) +1.5%.

- Makers of wound-care products are falling after the US government proposed to change how skin substitutes are paid for.

- MiMedx (MDXG) tumbles 17% while Organogenesis (ORGO) sinks 25%

- BlackRock (BLK) falls 1.9% after the investment firm’s net inflows missed analyst estimates in the second quarter. The company’s reported assets under management beat the average analyst estimate.

- MP Materials (MP) gains 7% after Fox Business reported that Apple is set to announce a $500 million deal with the company for rare earths produced in the US, citing people familiar with the matter.

- Trade Desk (TTD) rallies 14% after S&P Dow Jones Indices said the advertising technology company will join the S&P 500 Index before trading opens on July 18.

- Wells Fargo & Co. (WFC) falls about 2% after lowering its full-year guidance for net interest income, after another quarter of tepid growth amid the ongoing trade war.

Outside of earnings, micro focus this am is on NVDA (+5%) with the company planning to resume H20 chip sales to China after assurances from Washington that shipments will be approved. After the White House banned exports in April, it’s a surprise reversal that may add billions to Nvidia’s revenue this year. The move may help spur easing tensions between US-China trade negotiations/furthers the “TACO” trade. TTD (+15%) set to replace ANSS in S&P 500.

For Nvidia, the approval of export licenses for the H20 chip not only boosts its earnings prospects but also bodes well for progress in trade talks between the White House and key partners. With stocks trading near record highs, investors will also gain a clearer read on corporate health as major banks mark the unofficial start of earnings season.

“The US policy reversal on selling AI chips to China clearly constitutes good news for the industry,” said David Kruk, head of trading at La Financiere de L’Echiquier. “Other than that, the upward trend is still being fueled by investors riding the TACO trade — there are threats but they have yet to materialize.”

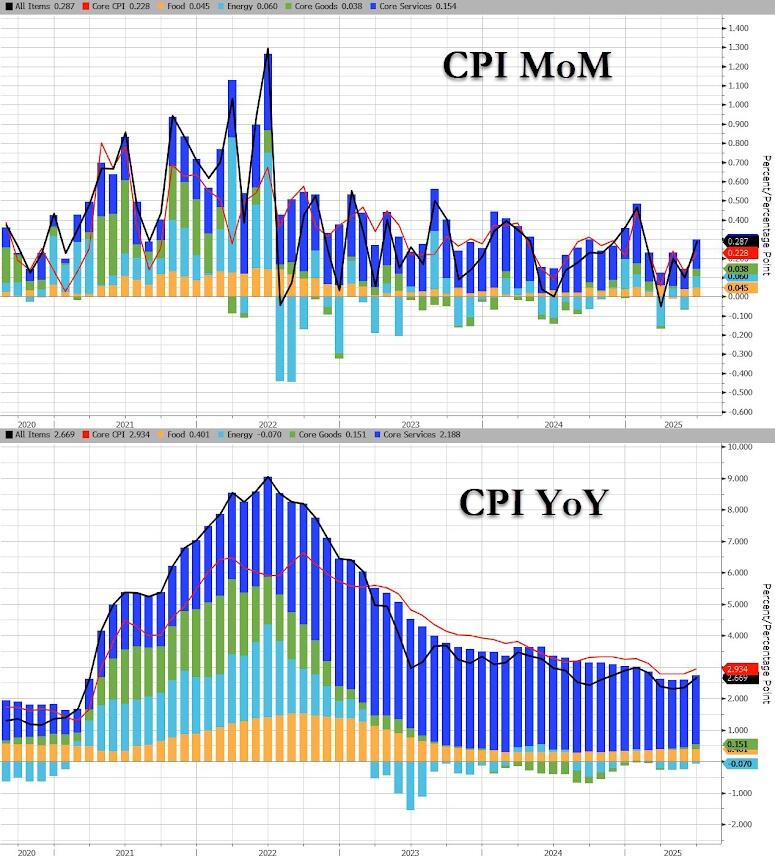

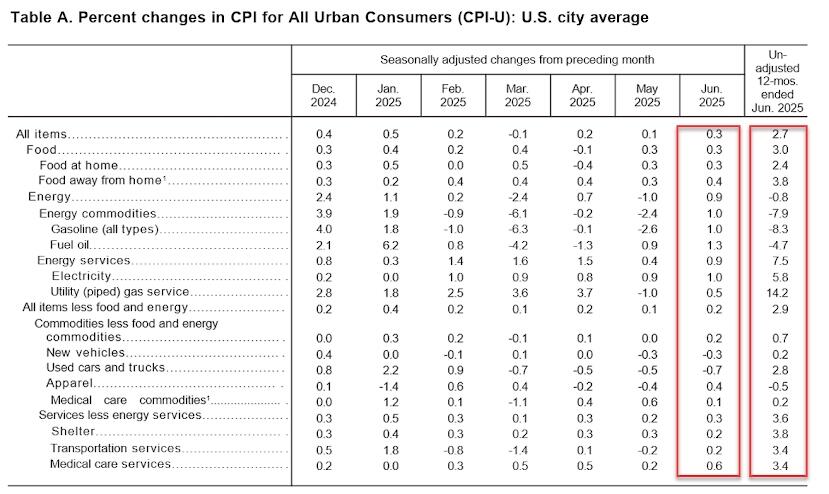

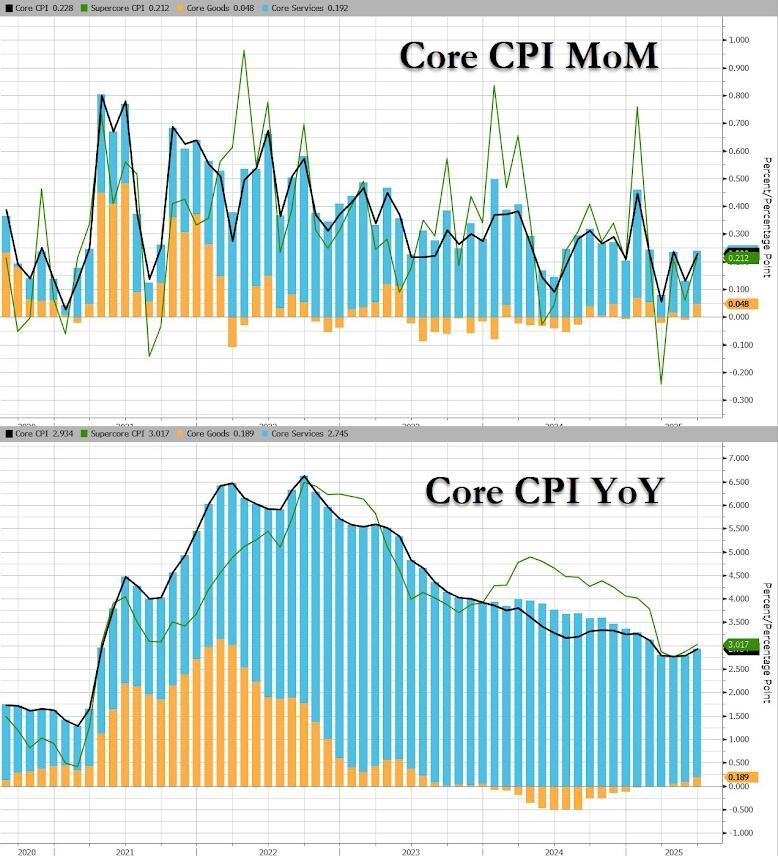

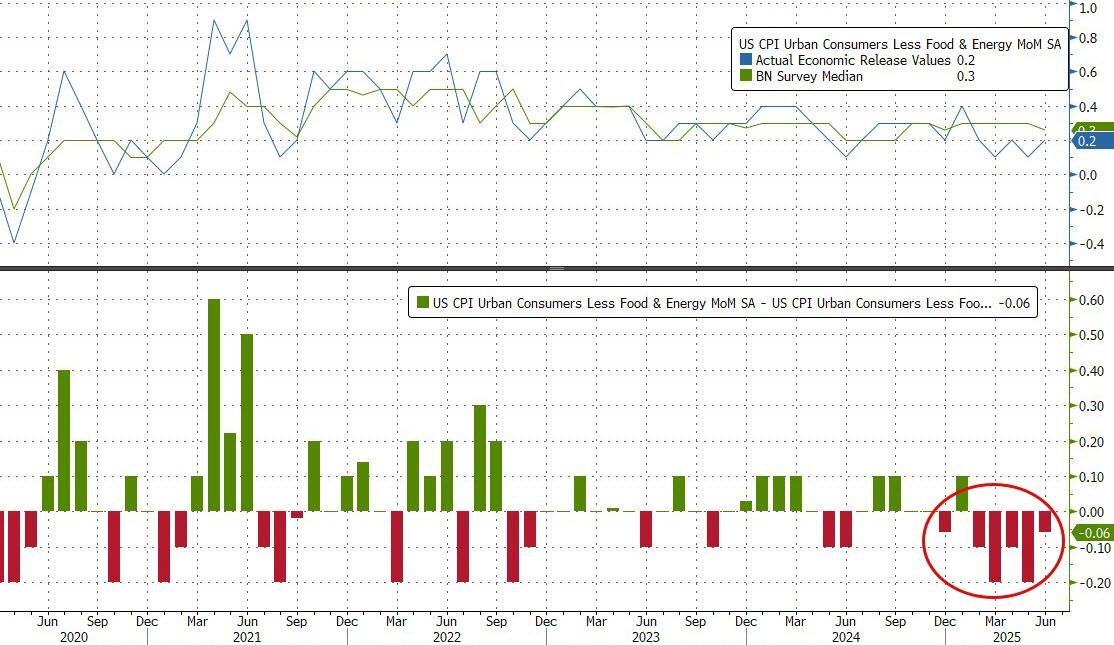

CPI is the big macro event for today: economist estimates for m/m change range from 0.1% to 0.4%, with the median 0.3%. June report is first of three to be released before Fed’s September meeting, for which traders have priced in 15bp of easing (see our CPI preview here). Goldman warns to watch for: 1) weakness in used cars, 2) modest increase in car insurance, 3) modest rebound in airfare, 4) +0.08pp increase on core inflation from tariff pressures. After months of seeing little inflation, CPI probably experienced slightly faster growth in June as companies started to pass along higher costs of imported merchandise associated with tariffs. The options market is betting the S&P 500 will swing 0.6% in either direction after the release.

It’s still too early to gauge the impact of the Trump administration’s tariff agenda on inflation, said Arend Kapteyn, UBS Group AG’s global head of economic and strategy research. He noted that July’s data, set to be released next month, would likely provide the earliest indication of any clear effect. The lag is helping to underpin the Federal Reserve’s wait-and-see approach to cutting interest rates, with swaps pricing in less than two quarter-points of monetary easing this year.

“We’re about to go into a five- to six-month period of accelerating inflation,” Kapteyn told Bloomberg TV. “It’s a trade-off between when does the labor market starts to ease, starts to crack — and we’re already seeing some signs of that — versus how quickly is the inflation data increasing.”

The latgest Fund Managers Survey by Bank of America showed that fund managers are rushing back into risky assets at a record pace on optimism over economic growth and strong corporate profits. The share of investors taking a higher-than-normal risk level in their portfolios registered the biggest increase over a three-month span going back to 2001, the poll showed. It also pointed to strong increases in allocations to US and European stocks, as well as tech shares.

“We are still far from levels where we would advocate a short, but given valuation and positioning, it makes sense to take some chips off the table,” he said.

European stocks advance with the Stoxx 600 up 0.2%. Technology, media and auto shares are leading gains as Nvidia plans to resume sales of its H20 AI chip to China. Among individual stocks, B&M sinks to a record low following a weak first quarter. Here are the biggest European movers:

- European semiconductor stocks are gaining ground on Tuesday as Nvidia plans to resume sales of its H20 AI chip to China.

- Experian shares advance as much as 5.2%, touching a new record high, after the UK credit services firm reported first-quarter organic revenue growth that beat estimates.

- Orsted climbs as much as 6.4% after Morgan Stanley upgrades the Danish offshore wind developer to overweight from equal-weight, saying in note that an improving risk/reward makes it “worth a fresh look.”

- Accelleron shares jump as much as 13% to a record high after the Swiss engine parts maker raised its guidance.

- Trustpilot Group shares rise 12% to the highest since March after the British holding company’s preliminary first-half revenue beat the average analyst estimate.

- TomTom shares rise as much as 11% on Tuesday after the GPS-maker narrowed its revenue forecast for the full year by lifting the bottom rung of the range.

- Ericsson shares fall as much as 4.4% after the telecom equipment maker said sales growth in 3Q is expected to be below average seasonality over the past three years.

- B&M shares plunge as much as 14%, hitting their lowest level on record, after posting weaker topline growth than anticipated in the first quarter despite weak comparatives and favorable weather.

- Barratt Redrow shares plummet as much as 13%, after the property developer said it built fewer houses than hoped in FY25 and posted disappointing guidance for FY26.

- Solvay falls as much as 4.2% as JPMorgan says it “joins the profit warning party,” with the Belgian firm becoming the latest in the European chemicals space to cut its guidance.

- AFRY slumps as much as 9.2% after its second-quarter results, the Swedish engineering consultancy’s biggest decline since its previous quarterly statement in late April.

- Azoty shares drop 3.1% to the lowest since June 24 after Orlen indicated it’s not interested in buying the Polish chemicals producer’s polymers project.

Earlier in the session, Asian stocks also advanced as Nvidia’s plan to resume some chip sales to China stoked optimism over geopolitics. Chinese shares were mixed as the latest economic data raised concerns over pressure on domestic consumption. The MSCI Asia Pacific Index gained as much as 0.7% after Nvidia said it plans to restart sales of its H20 AI accelerator to China. Alibaba, Tencent and TSMC were the biggest boosts to the gauge. Benchmarks in Hong Kong, Taiwan and South Korea advanced. Mainland Chinese shares fluctuated after macro numbers showed an uneven recovery. While economic growth exceeded expectations in the second quarter thanks to strong exports to markets outside the US, consumer demand at home remained weak. That’s bound to keep investors cautious after a recent equity rally. Elsewhere, traders are positioning for the weekend upper house election in Japan. Sentiment is cautious, as a surge in bond yields underscored mounting worries about the nation’s fiscal situation. Markets are watching the JGB yield breakout ahead of upper house elections & potential pressure on US rates.

In FX, the Bloomberg Dollar Spot Index falls 0.2% ahead of US inflation data that is forecast to show an acceleration in CPI for June. The euro and pound both add 0.2%.

In rates, Treasuries climb, pushing US 10-year yields down 2 bps to 4.41% ahead of June CPI data, supported by bigger gains in European bond markets, where curves are similarly flatter. European government bonds rise with little reaction seen in bunds to stronger-than-expected German ZEW data and a beat for euro-area industrial production. Short-dated US government bond yields rose after Treasury Secretary Scott Bessent said it would be confusing for Federal Reserve Chair Jerome Powell to remain at the central bank after his term ends, adding that a “formal process” has already begun to identify a potential successor.

In commodities, oil prices are little changed, paring earlier losses with WTI near $67 a barrel. Spot gold climbs $18 to around $3,362/oz. Bitcoin retreats 3% to near $117,000.

Looking at today’s calendar, US economic data slate includes July Empire manufacturing and June CPI (8:30am). Fed speaker slate includes Bowman (9:15am), Barr (12:45pm), Barkin (1pm), Collins (2:45pm) and Logan (7:45pm).

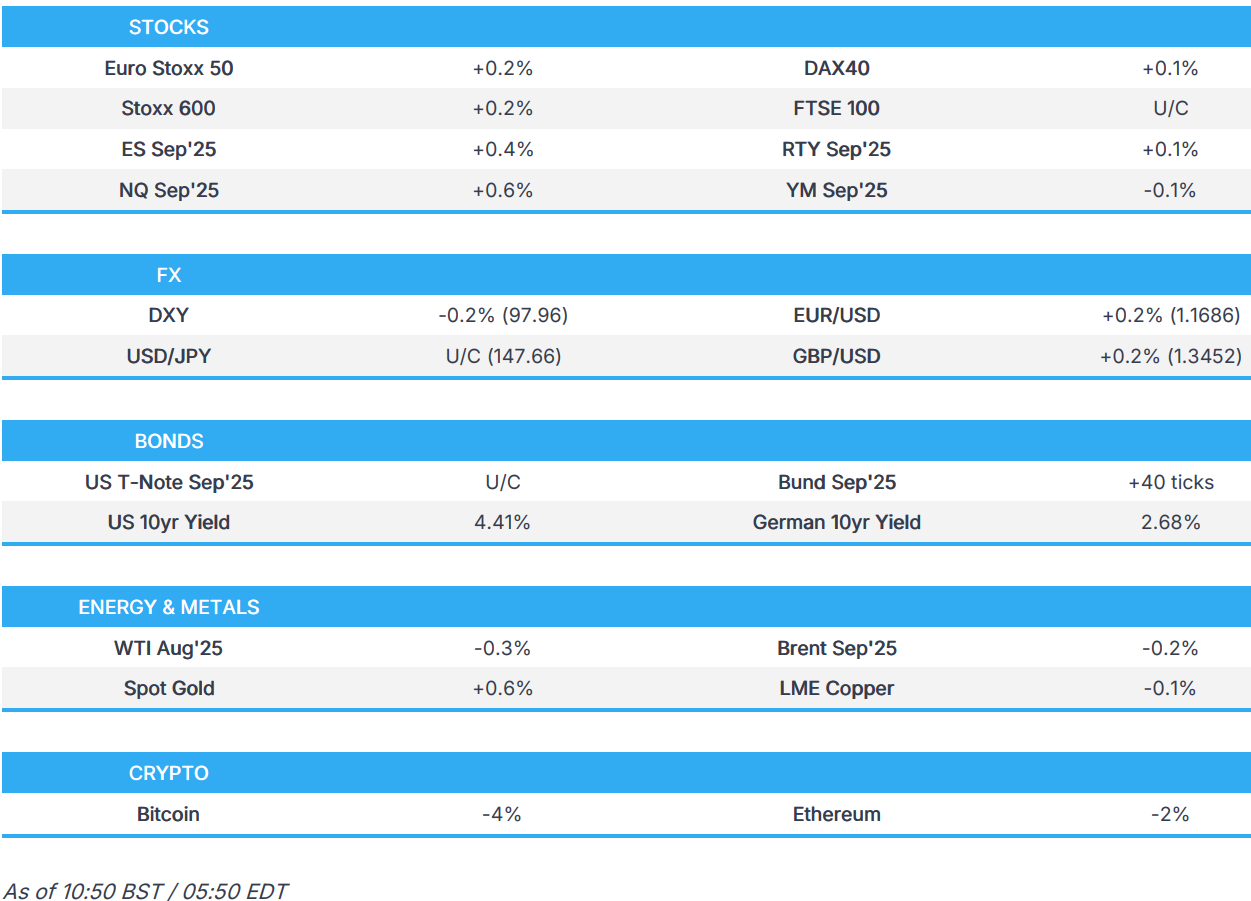

Market Snapshot

- S&P 500 mini +0.3%

- Nasdaq 100 mini +0.6%

- Russell 2000 mini little changed

- Stoxx Europe 600 +0.2%

- DAX +0.1%, CAC 40 little changed

- 10-year Treasury yield -2 basis points at 4.41%

- VIX -0.4 points at 16.8

- Bloomberg Dollar Index -0.1% at 1200.91

- euro +0.2% at $1.1682

- WTI crude little changed at $67.03/barrel

Top Overnight News

- Fed Chair Powell responded to Senate Banking Chair Scott and Senator Warren regarding building renovations in which he stated the inspector general had full access to project information and receives monthly reports, while he has asked the board’s inspector general to take a fresh look at the project, according to Politico and Reuters

- Stocks advanced after Nvidia Corp. secured US assurances to resume sales of some artificial intelligence chips to China, lifting sentiment on a busy day that also features inflation data and big bank earnings.

- Gold advanced, recovering from Monday’s modest drop, as investors digested mixed messages from the US regarding the progress of trade negotiations.

- Japan’s long-term government debt yield touched the highest level since 2008, as a raft of election tax-cut pledges puts investors on edge and risks higher costs all around in the country.

- Liquidity in sovereign bond markets is falling and term premium is rising. With little sign of budgetary restraint almost anywhere, a fiscal crisis in a developed bond market is not inconceivable.

- Euro hedging costs are subdued ahead of key US inflation data, as summer trading conditions and a shift in market focus toward labor metrics dampen demand for short-dated gamma.

- Stocks traders appear to be looking past the possibility of a stronger-than-expected inflation reading on Tuesday, putting them in a vulnerable position if President Donald Trump’s trade war leaves its mark on US consumer prices.

- US President Donald Trump’s latest threat of 100% tariffs on Russia would risk complicating relations with two nations crucial to his economic and strategic goals: China and India.

- Kevin Warsh, a top contender to replace Jerome Powell as chair of the Federal Reserve, is finally ready to cut interest rates. As a governor at the US central bank from 2006 to 2011, Warsh called for higher rates even in the depths of the financial crisis, warning often of impending inflation. That’s a concern he’s reiterated as recently as last year. But this year, Warsh has become an enthusiastic supporter of lower borrowing costs.

Trade/Tariffs

- US Department of Commerce announced it is withdrawing from and terminating the 2019 agreement suspending anti-dumping duty investigation on fresh tomatoes from Mexico, while it is issuing an anti-dumping duty order, resulting in duties of 17.09% on most imports of tomatoes from Mexico.

- Mexico’s Economy Ministry rejected the US decision on tomato duties which it considered unfair and against the interests of both Mexican producers and US industry, while it will support local tomato producers to seek a deal under which the duty is suspended.

- EU draws up retaliatory tariffs for US goods in case a trade deal is not reached with aircraft and booze among imports targeted as EU debates how to respond to Trump’s latest trade threats, according to WSJ.

- Japanese PM Ishiba and trade negotiator Akazawa are to meet with US Treasury Secretary Bessent during his trip to Japan, while the meeting is being considered for July 18th in Tokyo, according to Yomiuri.

- Japan’s Economy Minister and trade negotiator Akazawa said Japan is still arranging the makeup of attendees for the US National Day at Osaka Expo, while he added they will continue dialogue through various channels to seek an agreement with the US on tariffs.

A more detailed look at global markets courtesy of Newsquawk

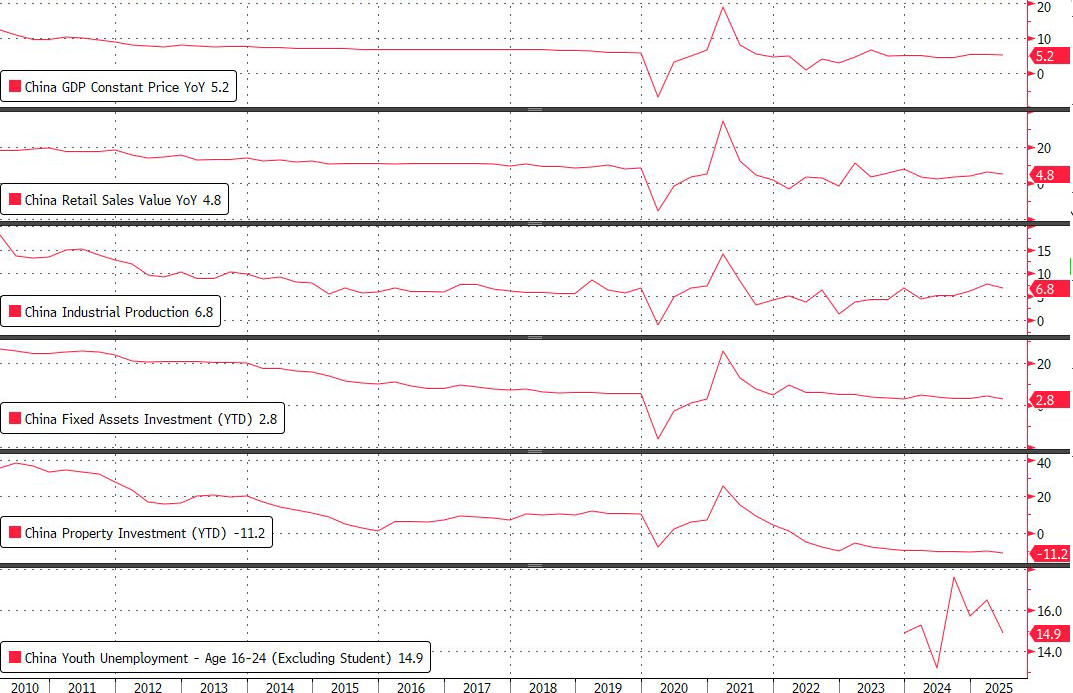

APAC stocks were ultimately mixed with the region indecisive in the aftermath of the latest Chinese GDP and activity data, while participants also awaited CPI data and the start of earnings season stateside. ASX 200 gained with strength in tech and some defensive sectors, while the positive sentiment was also facilitated by an increase in Consumer Confidence and as Australian PM Albanese met with Chinese President Xi. Nikkei 225 traded indecisively following recent currency weakness and rising JGB yields. Hang Seng and Shanghai Comp diverged following the somewhat mixed tier-1 data releases from China in which GDP figures for Q2 and Industrial Production in June topped forecasts but Retail Sales and Fixed Assets Investments disappointed, while House Prices were varied and continued to contract.

Top Asian News

- Chinese President Xi met with Australian PM Albanese and said it is most important to seek common ground while sharing differences and that China is ready to work with the Australian side to push bilateral ties further and make great progress. Furthermore, Australian PM Albanese said in the meeting with Chinese President Xi that they welcome progress on cooperation on free trade and value their relationship with China, while he added they will continue to approach the relationship in a calm and consistent manner guided by their national interest.

- China’s stats bureau spokesperson reiterated that the economic foundation needs to be consolidated and stated that overall economic performance in H1 was stable with steady progress, although structural contradictions within the economy have not been fundamentally alleviated. The stats bureau official stated that domestic demand as a contribution to economic growth has been a driving force for GDP but noted that they need to improve investment structure and environment, while the real estate market is heading towards stabilisation and policy support to boost consumption in H1 should sustain spending in H2. Furthermore, it was stated that China is at a critical moment in improving consumption structure and it will supplement policy support with measures to ensure a stable operation of the economy.

- China held its urban work conference and will vigorously promote the optimisation of urban structure, while it will pay more attention to overall urban planning and make efforts to build innovative cities with vitality, according to Xinhua.