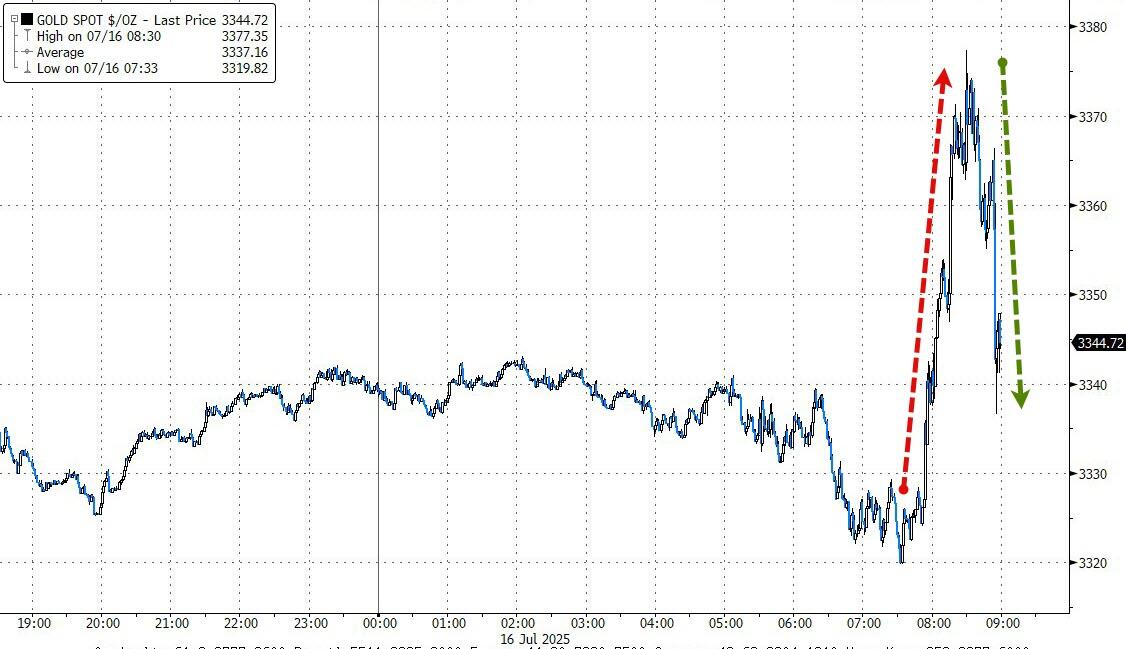

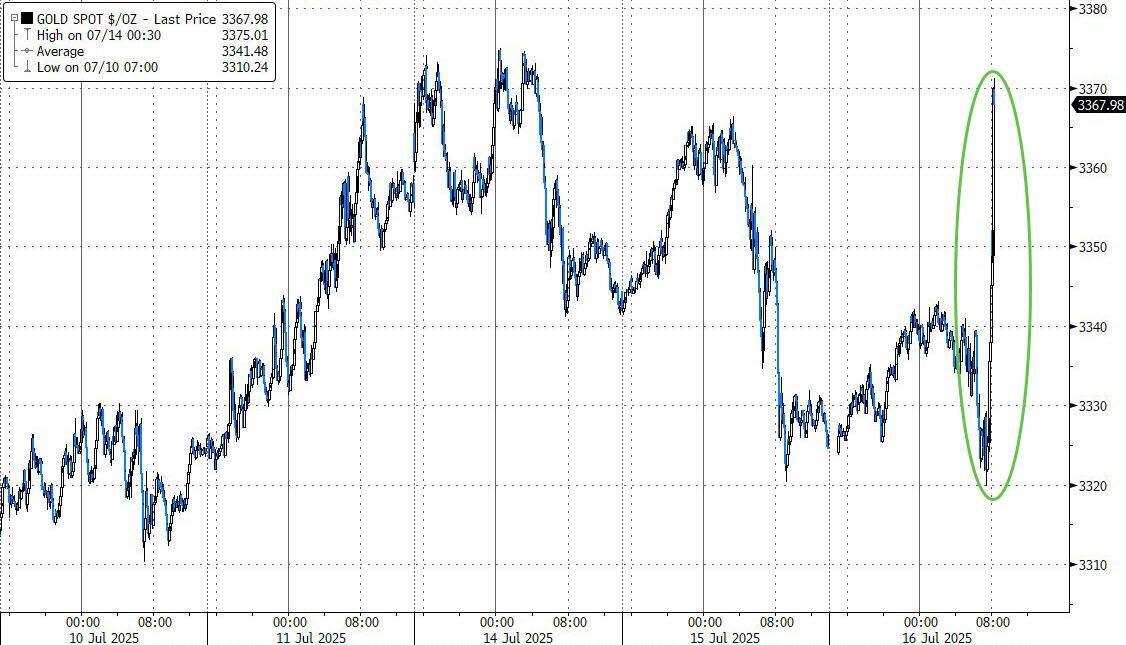

JULY 16/GOLD CLOSED UP $22.20 TO $3351.90 WITH SILVER UP 9 CENTS TO $37.87//PLATINUM WAS UP ANOTHER $38.15 TO $1417.95 AND PALLADIUM WAS UP $26.70//PRECIOUS METALS COMMENTARIES TONIGHT COURTESY OF CHRIS POWELL WITH GATA GOLD DISPATCHES//HOUSE PRICES CONTINUE TO DECLINE IN CHINA CAUSING A MASSIVE HEADACHE FOR THE PBOC//CHINA EXPORTS THE HIGHEST AMOUNT OF RARE EARTHS LAST MONTH/SPAIN UNDERGOES MASSIVE RIOTS AFTER CITIZEN BEATEN BY A MIGRANT//ISRAEL VS IRAN UPDATES/SYRIA UPDATES//COVID UPDATES/VACCINE INJURY UPDATES/MARK CRISPIN MILLER/NEWS ADDICTS/NEWSWIZE ETC//OIL UPDATES//BRICS UPDATES/USA DATA RELEASES/SWAMP STORIES FOR YOU TONIGHT//

332 H STANDARD CHARTERED B 1 661 C JP MORGAN SECURITIES 100 102 686 C STONEX FINANCIAL INC 18 3 709 C BARCLAYS 27 737 C ADVANTAGE FUTURES 3 905 C ADM 12

TOTAL: 133 133 MONTH TO DATE: 9,005

JPMORGTAN STOPPED 102/137

JULY

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 133 CONTRACTs NOTICES FOR 13,300 OZ or 0.4136 TONNES

total notices so far: 9005 contracts for 900,500 OR 28.009 tonnes)

FOR JULY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 192 NOTICE(S) FILED FOR 0.960 million OZ/

total number of notices filed so far this month : 8,691 CONTRACTS (NOTICES) for 43.450 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $22.20 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 947.64 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.09 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ///A FRAUDULENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV///

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 477.632 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA HUGE SIZED 2194 CONTRACTS TO 171,474 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS MEGA HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS OF $0.65 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. WE FINALLY ARE MOVING MUCH HIGHER THAN THE BASE $34.40 SILVER PRICE BARRIER. WE HAD A MEGA HUGE SIZED LOSS OF 1194 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE 1000 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD STRONG LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO TUESDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $36.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON TUESDAY WITH SILVER’S LOSS IN PRICE. THE PRICE FINISHED MILES ABOVE THE MAGIC NUMBER OF $36.00 SILVER SPOT PRICE CLOSING AT $37.78 . WE HAVE ANOTHER MEGA HUGE T.A.S. ISSUANCE AT 1005 CONTRACTS ISSUED BY THE CME AND THAT STILL SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 38.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A HUGE 1000 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 1055 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TODAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A MEGA HUGE SIZED 1194 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.65.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT/WEDNESDAY MORNING: A HUGE SIZED 1055 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.65) BUT WERE UNSUCCESSFUL IN KNOCKING OF ANY NET SILVER LONGS FROM THEIR PERCH AS EVEN THOUGH WE HAD A LOSS OF 1194 CONTRACTS ON OUR TWO EXCHANGES ALL OF THAT LOSS WAS DUE TO T.A.S. SPREADER LIQUIDATION./

WE HAD A 1000 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 34.730 MILLION OZ PLUS TODAY’S STRONG QUEUE JUMP OF 425,000 OZ//NEW STANDING ADVANCES TO 44.530 MILLION OZ

THUS:

INITIAL STANDING FOR JULY: 44.530 MILLION OZ INCLUDING QUEUE JUMPS

WE HAD:

/ MEGA HUGE COMEX OI LOSS+// A HUGE SIZED EFP ISSUANCE 615 CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 1055 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 42 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 11 DAY(S), total 6459contracts: OR 32.295 MILLION OZ (587 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 32.295 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 32.295 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2194 CONTRACTS WITH OUR LOSS IN PRICE OF $0.65 IN SILVER PRICING AT THE COMEX// TUESDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE 1000 CONTRACT EFP ISSUANCE CONTRACTS: 1000 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 4 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 44.530 MILLION OZ//

THE NEW TAS ISSUANCE TUESDAY NIGHT (1055 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE IN WEDNESDAY’S TRADING AND BEYOND!

WE HAD 192 NOTICE(S) FILED TODAY FOR 0.96 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5059 OI CONTRACTS TO 448,531 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 1745 CONTRACTS //.

WE HAD A STRONG SIZED DECREASE IN COMEX OI (5059 CONTRACTS) . THIS OCCURRED WITH OUR LOSS OF $20.80 IN PRICE// TUESDAY///.

LAST THREE MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0.404 TONNES QUEUE JUMP = 29.035 TONNES STANDING

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1523 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 448,531 /NOW STILL AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 171,474 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3536 CONTRACTS WITH 5059 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1523 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3536 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 950 CONTRACTS

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(1523) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 5059 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 3536 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR JULY AT 17.947 TONNES COUPLED WITH TODAY’S 0.404 TONNES QUEUE JUMP//STANDING ADVANCES TO 29.035 TONNES.

NEW STANDING FOR GOLD, JULY CONTRACT AT 29.035 TONNES OF GOLD.

.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION AS WE HAVE 1)A $20.80 COMEX PRICE LOSS. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THE LOSS IN PRICE AS WE HAD A FAIR LOSS OF 3536 CONTRACTS ON OUR TWO EXCHANGES COUPLED WITH CONSIDERABLE LIQUIDATION OF OUR TAS SPREADERS // /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4) FAIR SIZED COMEX OI LOSS// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (1523 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 950 T.A.S.CONTRACTS WHICH COMPLETES OUR 5 DAYS OF MEGA HUGE ISSUANCES ENDING MONDAY.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 19,746 CONTRACTS OR 1,974,600 OZ OR 61.418TONNES IN 11 TRADING DAY(S) AND THUS AVERAGING: 1795 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN11 TRADING DAY(S) IN TONNES 61.418 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 61.418 TONNES DIVIDED BY 3550 x 100% TONNES = 1.74% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 61.418 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 2194 CONTRACTS OI TO 171,516 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1000 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1000 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1000 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2152 CONTRACTS AND ADD TO THE 1000 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF 1194 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $0.65 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 5.97 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED DOWN 1.22 PTS OR 0.03%

//Hang Seng CLOSED DOWN 72.36 PTS OR 0.29%

// Nikkei CLOSED DOWN 14.62 PTS OR 0.04% //Australia’s all ordinaries CLOSED DOWN 0.66%

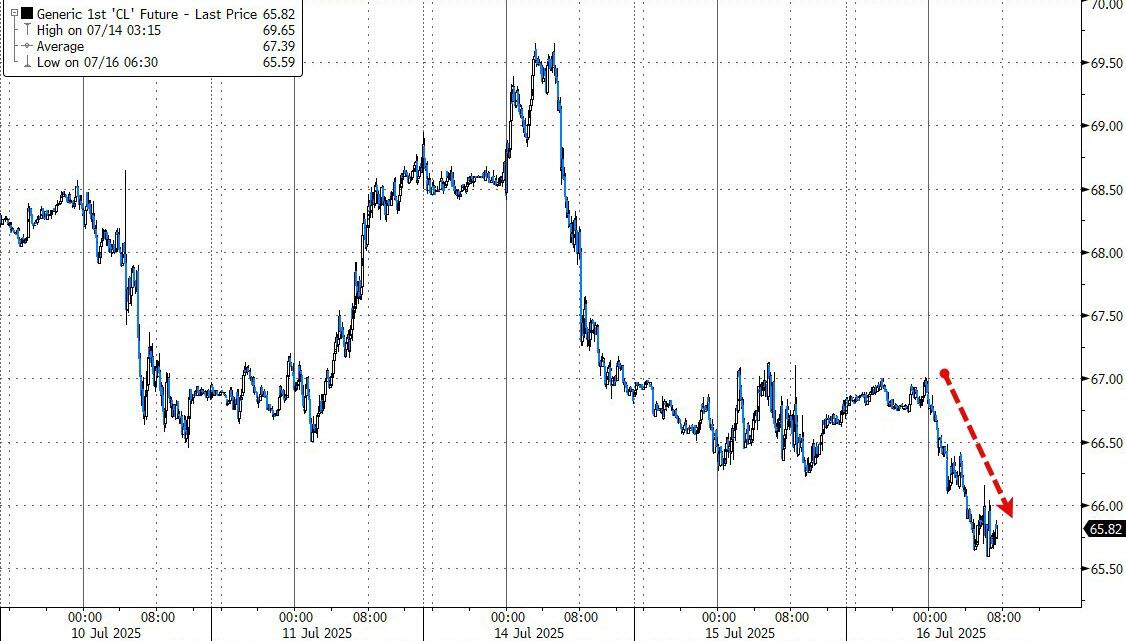

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1780 OFFSHORE CLOSED UP AT 7.1812/ Oil UP TO 66.37 dollars per barrel for WTI and BRENT UP TO 68.49 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1780 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1812 AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 5059 CONTRACTS TO A STILL LOW NUMBER OF 448,531 OI WITH OUR LOSS IN PRICE OF $20.80 WITH RESPECT TO TUESDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1523 ). WE HAD CONSIDERABLE T.A.S. LIQUIDATION //TUESDAY TRADING WHICH ACCOUNTS FOR THE TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL.

THE CME ANNOUNCED TUESDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES.

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY 0

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 3536 CONTRACTS WITH OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE IN JANUARY THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND NOW JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER FINALLY ENDS OUR MEGA MEGA HUGE T.A.S ISSUANCE. AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A MUCH MUCH LOWER 950 T.A.S CONTRACTS THAN MONDAY;’S ISSUANCE OF 22,678. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. HOWEVER JULY IS HUGE FOR A NON DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 0.404 TONNES QUEUE JUMP = 29.035 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 29.035 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 10+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1523 EFP CONTRACT WAS ISSUED: : /AUGUST 2000 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1523 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY

ZERO NET SPEC LIQUIDATION DESPITE OUR LOSS IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY MORNING/MONDAY NIGHT WAS A HUGE BUT MUCH SMALLER 950 CONTRACTS AND THUS OUR 5 MEGA MEGA T.A.S ISSUANCES HAS NOW ENDED.

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE TUESDAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.THIS WAS SURELY IN EVIDENCE IN TRADING TUESDAY WITH OUR LOSS IN PRICE!

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0.404 TONNES QUEUE JUMP = 29/035 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY 20.80/ /) BUT THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE AN FAIR SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION ////TUESDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE MEGA MEGA T.A.S. ISSUANCES, TUESDAY TRADING , IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS. SO FAR FOR THE WEEK, THEY ONLY SUCCEEDED YESTERDAY WITH THE LOWERING OF GOLD’S PRICE ADVANCE.

WEDNESDAY MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE LOST A FAIR SIZED TOTAL OF 10.99 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 13,000 OZ OR 0.404 TONNES OF GOLD//NEW STANDING ADVANCES TO 29.035 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $20.80

WE HAD 1745 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 3536 CONTRACTS OR 353,600 0Z (11.99 TONNES)

Total monthly oz gold served (contracts) so far this month

9005 notices 900,500 oz 28.009 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 entry

i) Into Malca 48,869.520 oz (1520 kilobars)

total deposit 48,869.520 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entries

adjustments: 2 dealer to customer

a)dealer to customer Brinks 289.359 oz( 9 kilobars)

b) dealer to customer Delaware 6,351.559 oz

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JULY STANDS AT 463 CONTRACTS FOR A LOSS OF 824 CONTRACTS. ON TUESDAY WE HAD 954 NOTICES FILED, SO WE GAINED A GOOD SIZED 130 CONTRACTS OR 13,000 OZ (0.404 TONNES) ENTERTAINED WITH A QUEUE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD

AUGUST LOST 11,025 CONTRACTS DOWN TO 230,926 AS AUGUST BECOMES THE FRONT MONTH AND IT’S OI IS VERY HIGH AND NOT CONTRACTING ENOUGH. WE WILL PROBABLY HAVE A HIGH NUMBER OF TONNES STANDING.

SEPT GAINED 49 CONTRACTS TO 1570

We had 133 contracts filed for today representing 13,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 100 notices issued from their client or customer account. The total of all issuance by all participants equate to 133 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 102 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (9005 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (463 CONTRACTS) minus the number of notices served upon today (133 x 100 oz per contract) equals 933,500 OZ OR 29/035 TONNES to which we add 0 tonnes of gold issued under exchange for risk// total standing 29/035 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (9005 x 100 oz +we add the difference for front month of JULY (463 OI} minus the number of notices served upon today (133 x 100 oz) which equals 933,500 OZ OR 29.035 TONNES + 0 tonnes EX FOR RISK = 29.035 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 29.035 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL REGISTERED SILVER: 195.579 MILLION OZ//.TOTAL REG + ELIGIBLE. 497.191 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 407 OPEN INTEREST CONTRACTS FOR A LOSS OF 185 CONTRACTS. WE HAD 270 CONTRACTS SERVED UPON TUESDAY SO WE GAINED A STRONG 85 CONTRACTS OR 425,000 OZ ENTERTAINED A QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST LOST 125 CONTRACTS TO 2467 AS THIS MONTH BECOMES THE FRONT MONTH FOR SILVER

SEPTEMBER LOST 2730 CONTRACTS DOWN TO 128,311 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:192 or 0.960 MILLION oz

CONFIRMED volume; ON TUESDAY 62,265 good//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 8691 X5,000 oz = 43.450 MILLION oz

to which we add the difference between the open interest for the front month of JULY (407) AND the number of notices served upon today (192 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (8691) Notices served so far) x 5000 oz + OI for the front month of JULY(407) minus number of notices served upon today (192)x 5000 oz equals silver standing for the JULY contract month equating to 44.530 MILLION OZ .

New total standing: 44.530 million oz which is huge for this active delivery month of JULY. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 195.579 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/497.181 million. 42.25%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

JUNE 20 WITH GOLD DOWN $19.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 947.37 TONNES

JUNE 18 WITH GOLD UP $1.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.03 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 945.94 TONNES

JUNE 17 WITH GOLD DOWN $9.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 941.93 TONNES

JUNE 16 WITH GOLD DOWN $33.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.758 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 940.49 TONNES

JUNE 13 WITH GOLD UP $53.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.38 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 932.91 TONNES

JUNE 12 WITH GOLD UP $55.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 934.19 TONNES

JUNE 11 WITH GOLD UP $1.10 TODAY// SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.31 TONNEES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 935.91 TONNES

JUNE 10 WITH GOLD DOWN $11.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.02 TONNEES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 936.22 TONNES

JUNE 9 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.45 TONNEES OF GOLD FROM THE GLD//: /// ///INVENTORY RESTS AT 934.20 TONNES

JUNE 6 WITH GOLD DOWN $28.00 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

GLD INVENTORY: 947.64 TONNES, TONIGHTS TOTAL

SILVER

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

JUNE 20 WITH SILVER DOWN $0.83/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.818 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 474.641 MILLION OZ.

JUNE 18 WITH SILVER DOWN $0.20/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 17 WITH SILVER UP $0.67/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 473.096 MILLION OZ.

JUNE 16 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.727 MILLION OZ FROM THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 13 WITH SILVER UP $0.11/NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 473.550 MILLION OZ.

JUNE 12 WITH SILVER UP $0.11/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.276 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 473550 MILLION OZ.

JUNE 11 WITH SILVER DOWN $0.45/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.046 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.274 MILLION OZ.

JUNE 10 WITH SILVER DOWN $0.16/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.232 MILLION OZ.

JUNE 9 WITH SILVER UP $0.69/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.914 MILLION OZ.

JUNE 6 WITH SILVER UP $0.63/HUGE CHANGES AT THE SLV:A DEPOSIT OF 3.863 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.732 MILLION OZ. (A TOTAL DEPOSIT OF 11.856 MILLION PHANTOM OZ IN THE LAST 4 DAYS)

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

CLOSING INVENTORY 477.632 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG

ALASDAIR MACLEOD

JOHN RUBINO

CHRIS POWELL AND GATA DISPATCHES

Stupid move!

Ghana moves to hedge gold export prices to protect growth of reserves

Submitted by admin on Tue, 2025-07-15 20:32 Section: Daily Dispatches

By Moses Mozart Dzawu Bloomberg News via Mining Weekly, Bedfordview, South Africa Tuesday, July 15, 2025

Ghana is working on a programme to hedge the price of gold exports as it seeks to shield earnings that have bolstered the central bank’s foreign reserves from future volatility, Bank of Ghana Governor Johnson Asiama said.

Increased production and higher prices have helped Africa’s top gold miner to boost gross international reserves to $11.1-billion, Asiama said today in the capital, Accra. The buffer is enough to cover 4.8 months of imports, he said.

“While beneficial for now, a future correction in prices could quickly narrow our trade surplus,” Asiama said.

Ghana’s gold exports increased by 76% from a year earlier to $5.2 billion in the first four months through April. That has underpinned a widening in the trade surplus to $4.1 billion from $759 million over this period. …

Cyrille Jubert: China and the revaluation of precious metals

Submitted by admin on Mon, 2025-07-14 13:40 Section: Daily Dispatches

By Cyrille Jubert GoldBroker, London Monday, July 14, 2025

Remember the cycles of the mining industry.

For multiple reasons,the price of extracted ore tends to fall, particularly due to competition. Thus, as a mine is operated, the metal content generally decreases, reducing its profitability until the company decides to close it. There are therefore periods during which the extraction of a particular metal is no longer profitable, leading to a sharp drop in production, and then, gradually, a shortage.

For precious metals, to mask the erosion of the purchasing power of currencies, prices were long tightly regulated, first by specialized administrations, then by groups of central banks, such as the London Gold Pool until 1968. Subsequently, a banking cartel continued to manipulate the prices of gold and silver through various means. Among these, Comex futures contracts were a major tool, allowing traders to trade huge volumes of metals without ever demanding delivery.

Since 2004 this cartel has been implementing exchange-traded funds, allowing anyone to buy shares with a simple click, giving investors the false impression of acquiring gold or silver without having to worry about custody or insurance.

But this was merely an illusion. In reality the investor’s cash flow wasn’t necessarily used to acquire physical metal; it could even be used, depending on the cartel’s interests, to bet against the rise of gold or silver.

This type of financial product is collectively referred to as “paper gold” or “paper silver.” These substitutes have grown so widespread that, according to the U.S. Debt Clock, there are approximately 134 ounces of paper gold for every ounce of physical gold, and 364 ounces of paper silver for every ounce of physical silver. …

Barrick may sell its last Canadian gold mine to Discovery Silver

Submitted by admin on Tue, 2025-07-15 20:40 Section: Daily Dispatches

By Jacob Lorinc and Paula Sambo Bloomberg News Tuesday, July 15, 2025

Barrick Mining Corp. is in advanced talks to sell its last Canadian gold mine to Discovery Silver Corp., according to people familiar with the matter, as the firms seek to capitalize on the soaring price of the precious metal.

Discovery Silver is in the final stages of a process Barrick launched in April to sell the Hemlo gold mine in Ontario, according to the people, who asked not to be named.

There’s no certainty the deliberations will lead to a transaction, the people said.

Barrick and Discovery, both based in Toronto, did not immediately respond to requests for comment. …

Mongolia’s central bank joins the international gold price management scheme

Submitted by admin on Mon, 2025-07-14 12:54 Section: Daily Dispatches

12:52p ET Monday, July 14, 2025

Dear Friend of GATA and Gold:

In an essay posted today by the Official Monetary and Financial Institutions Forum, two officials of Mongolia’s central bank report that the bank considers gold to be international money, is managing its gold reserves separately from the rest of its foreign exchange reserves, and admit that the bank is working with other central banks and London Bullion Market Association banks to help manage the gold price.

The officials, bank reserve managers Tuvshingerel Tumenbayar and Azjargal Amarsaikhan, write: “Our trading team closely monitors key macroeconomic and financial market indicators that reflect international policy developments and associated risks. Additionally, we focus on enhancing our capacity to manage gold in both allocated and unallocated forms, working in collaboration with the London Bullion Market Association clearing banks and central banks.”

Of course “unallocated” gold is metal that, in the hands of central banks and their bullion bank agents, tends not to exist and is used to deceive markets into thinking that supply is much greater than it is and that higher prices aren’t warranted.

Tumenbayar and Amarsaikhan conclude: “The Bank of Mongolia is strengthening its commitment to responsible gold reserve management, promoting economic stability, and ensuring that Mongolia’s gold reserves meet the highest global standards for quality, ethics, and transparency.”

As the bank may discover eventually, if it doesn’t already know, those “global standards” for gold are not really very high in regard to ethics and transparency. Maybe the bank can do better over time.

The essay by Tumenbayar and Amarsaikhan is headlined “Gold is Mongolia’s Natural Reserve Strategy” and is posted at OMFIF here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org.

end

Brien Lundin: This is the year for metals, and the New Orleans Investment Conf.

Submitted by admin on Wed, 2025-07-16 13:30 Section: Daily Dispatches

By Brien Lundin Gold Newsletter / Golden Opportunities New Orleans Investment Conference Wednesday, July 16, 2025

This year’s New Orleans Investment Conference is coming up quickly — and the excitement over the metals and mining markets adds more urgency than usual for those hoping to attend.

Our registrations for this year are already well ahead of anything we’ve seen for many years, and I expect a bustling crowd that could eat up our entire hotel room block.

Everyone seems to understand that the most rewarding place to be in a metals and mining bull market is the New Orleans Conference — something that has been driven home time and again over the last five decades.

Adding to the allure of this year’s event is another stellar speaker roster. It’s still evolving, but so far we’ve lined up:

— Matt Taibbi, Rick Rule, Danielle DiMartino Booth, Brent Johnson, George Gammon, Peter Boockvar, Jim Iuorio, Dave Collum, Peter Schiff, Adrian Day, Adam Taggart, Robert Prechter, Robert Helms, and Russ Gray.

Also:

— Mark Skousen, Lobo Tiggre, Nick Hodge, Brent Cook, Chris Powell, Dana Samuelson, Rich Checkan, Thom Calandra, Mary Anne and Pamela Aden, Omar Ayales, Bill Murphy, Gerardo Del Real, Steve Hochberg, Albert Lu, Lindsay Hall, Andy Schectman, and many more, including yours truly.

The New Orleans Conference is always the investment event of the year. But considering that this is a generational opportunity in metals and miners, this is the most exciting moment we have seen for the sector in decades.

New Orleans will be the place to be and, as always, you’ve got our satisfaction guarantee backing up your decision to attend. If you’re not satisfied that the value we offer is worth many times your costs to attend, we’ll refund every cent of your registration fee. No questions asked.

But over the decades that we’ve offered this guarantee, I can count on one hand the number of times we have refunded anyone’s fee.

That’s because we strive to deliver far more value, more bottom-line return on investment than any other event.

And thousands of returning investors over the years attest that we deliver that value.

Again, this is a special year, and registrations could swamp our hotel room block. I strongly recommend that you act now to secure your place by clicking on this link —

// Nikkei CLOSED DOWN 14.62 PTS OR 0.04% //Australia’s all ordinaries CLOSED DOWN 0.66%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1780 OFFSHORE CLOSED UP AT 7.1812/ Oil UP TO 66.37 dollars per barrel for WTI and BRENT UP TO 68.49 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1780 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1812 AGAINST US DOLLAR/ AND THUS WEAKER

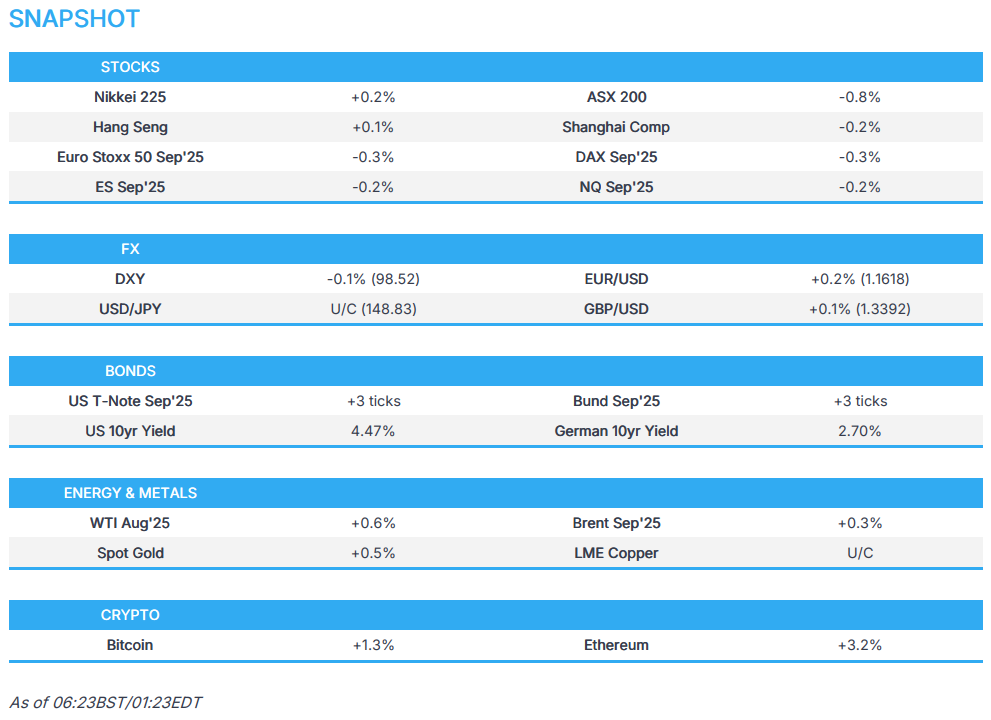

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1780 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1812 (CCP MANIPULATED)

SHANGHAI CLOSED DOWN 1.22 PTS OR 0.03%

HANG SENG CLOSED DOWN 72.36 PTS OR 0.29%

2. Nikkei closed DOWN 14.62 PTS OR 0.04%

3. Europe stocks SO FAR: MOSTLY ALL GREEN

USA dollar INDEX DOWN TO 98.21/ EURO RISES TO 1.1621 UP 14 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.571//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.80…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7170/Italian 10 Yr bond yield UP to 3.604 SPAIN 10 YR BOND YIELD UP TO 3.332%

3i Greek 10 year bond yield UP TO 3.428

3j Gold at $3340.25 Silver at: 37.97 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 6 /100 roubles/dollar; ROUBLE AT 78.01

3m oil (WTI) into the 66 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.66// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.571% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8013 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9314 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

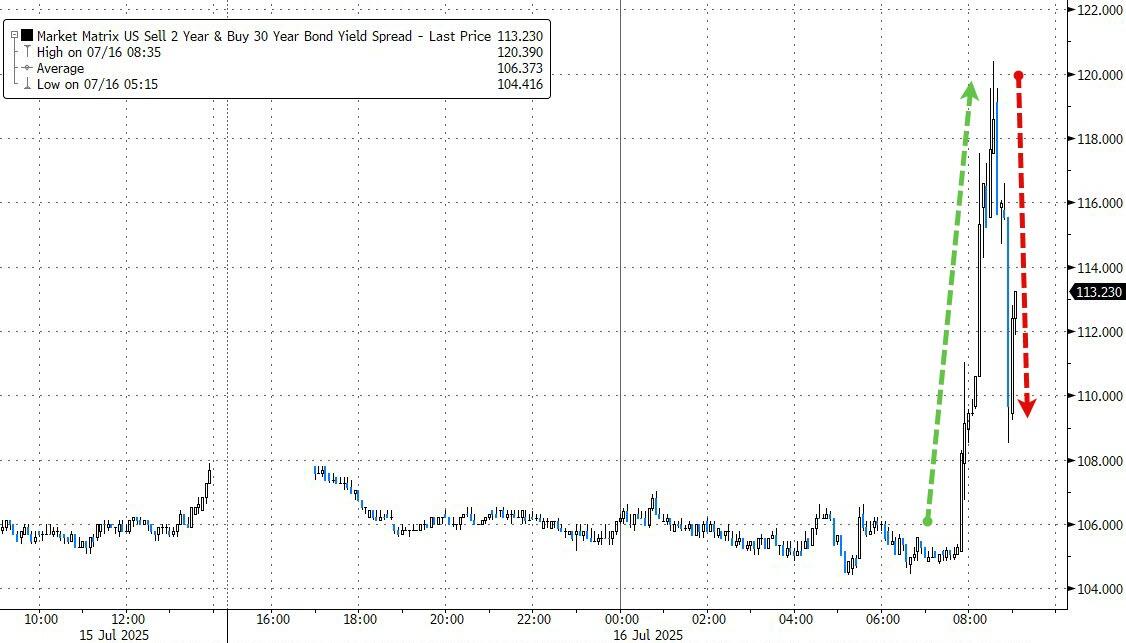

USA 10 YR BOND YIELD: 4.488 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 5.015 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.953 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.26

10 YR UK BOND YIELD: 4.6650 UP 6 PTS

10 YR CANADA BOND YIELD: 3.604 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.140 UP 1/2 PTS

2a New York OPENING REPORT

Futures Drop As Tariffs, Earnings And Rising Yields Dent Sentiment

Wednesday, Jul 16, 2025 – 07:34 AM

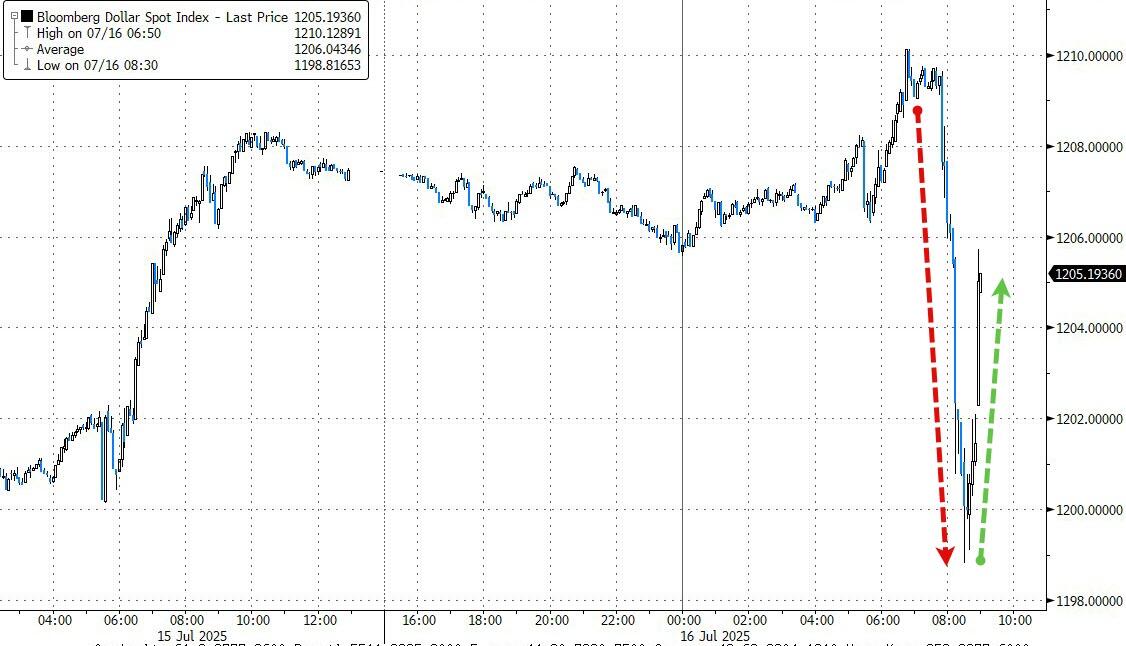

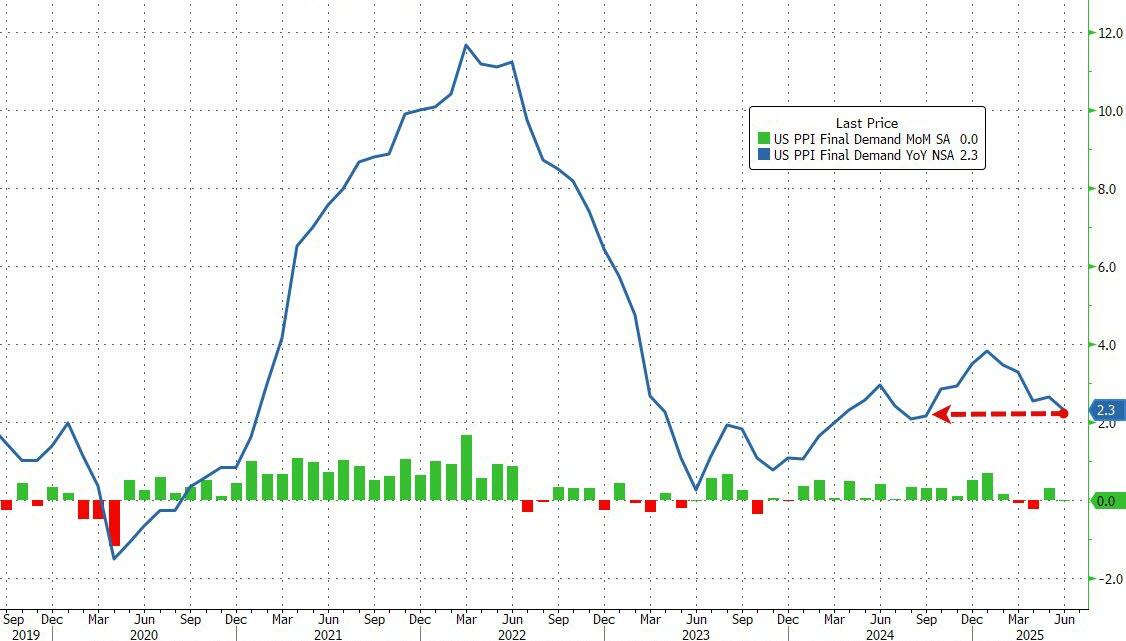

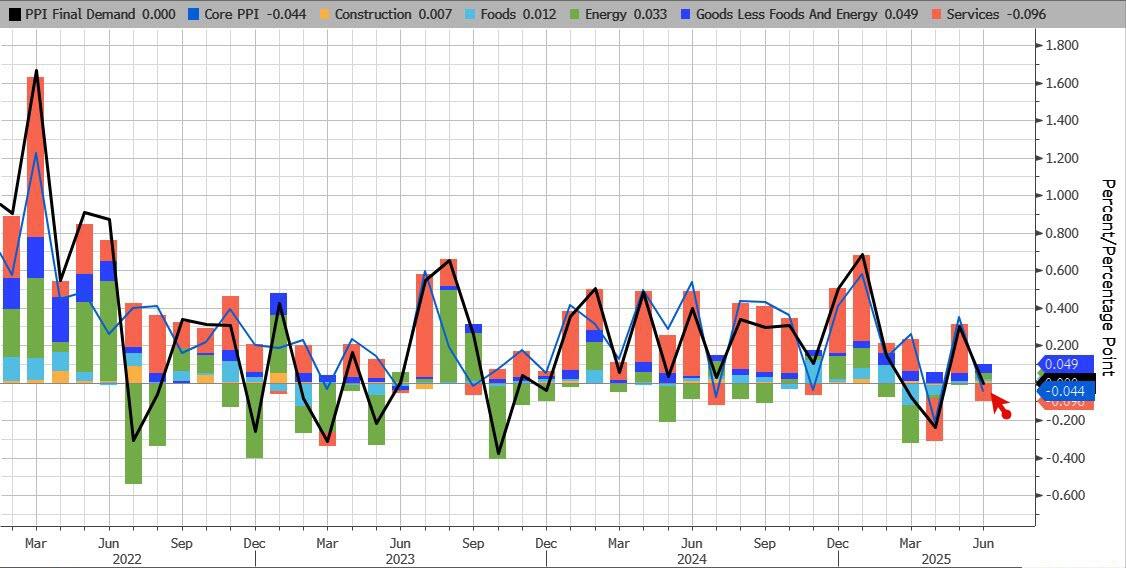

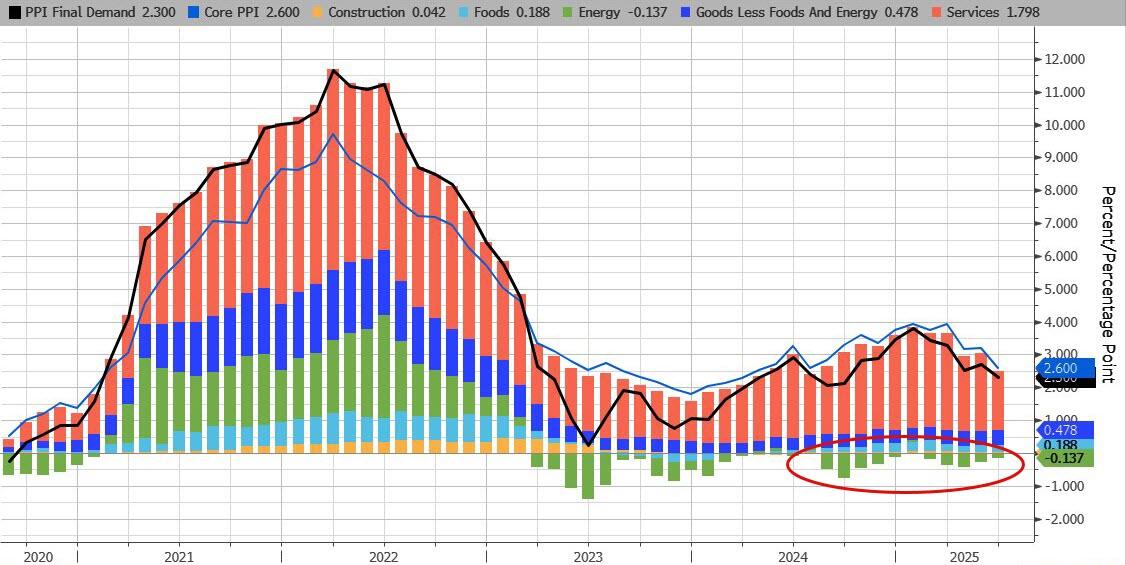

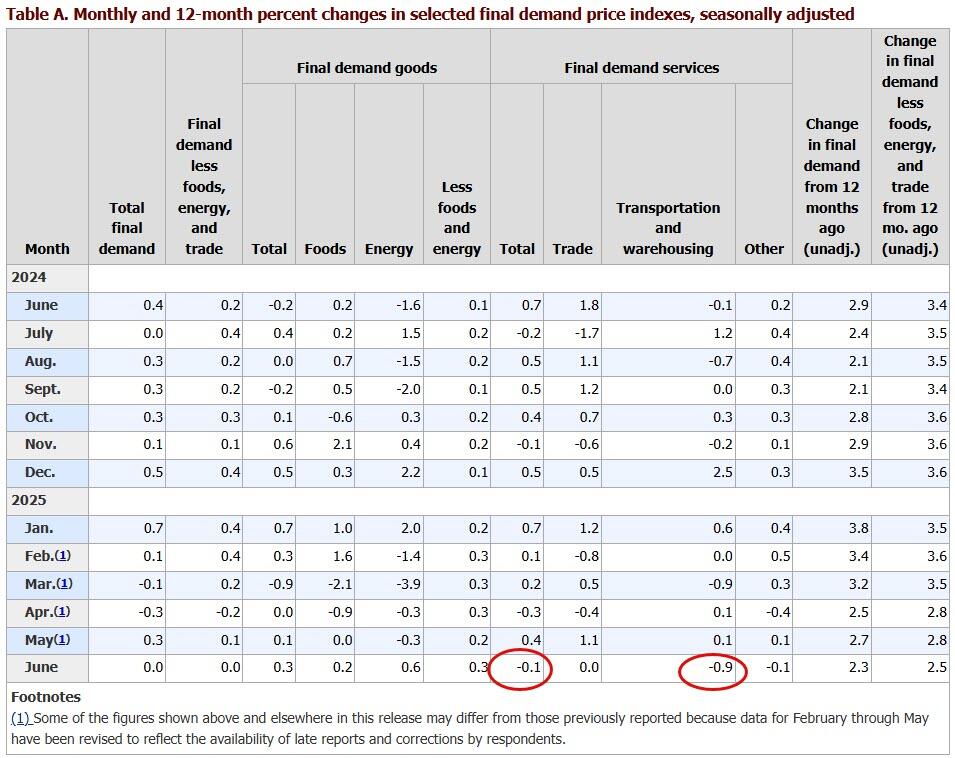

US equity futures and global stocks dropped, but were well off session lows, as a stream of negative tariff headlines and dialed-back expectations for interest-rate cuts prompted doubts about the market’s ability to sustain recent highs and sent 30Y yields above 5%, a level seen as a redline for further stock appreciation. As of 7:00am, the S&P 500 was on track for a second straight decline, with futures down 0.1% after , while Nasdaq futures were 0.3% lower after closing at a record; the small-caps Russell 2000 is seeing an early outperformance bid. Pre-mkt, Mag7/semis are mixed as are Cyclicals with Banks seeing an offer into the next batch of earnings. In Europe, the Stoxx 600 slipped 0.2%, weighed down by technology shares as ASML Holding NV trimmed its growth outlook for next year, citing trade tensions; French car giant Renault slumped 16% after slashing its profit guidance. Treasury yields are flat as is the USD. Commodities are mostly higher with Ags leading, precious metals following while energy is modestly weaker. Today’s macro data focus is the PPI data which will give more clues about how tariffs are affecting companies after mixed CPI numbers. We have another batch of Fedspeakers who will say nothing of importance.

In premarket trading, Mag 7 stocks are mixed (Apple +0.3%, Alphabet +0.2%, Meta +0.3%, Microsoft little changed, Tesla -0.4%, Amazon -0.5%, Nvidia -0.6%). Here are some other notable premarket movers:

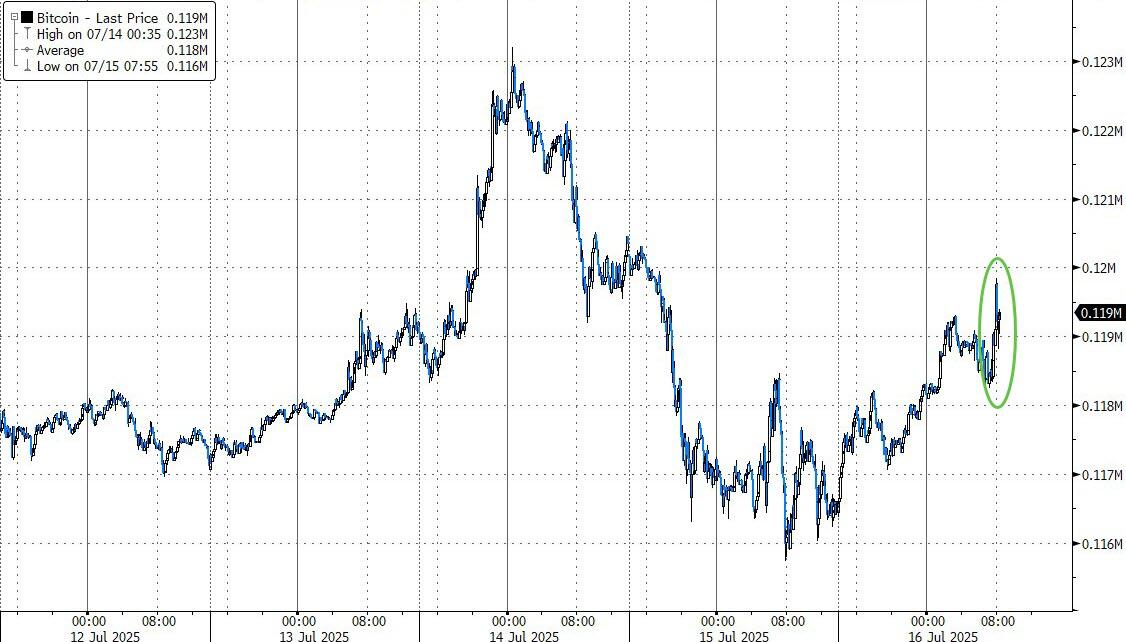

Crypto-linked stocks rose with Bitcoin prices in premarket trading Wednesday as President Donald Trump said the House will pass the GENIUS Act stablecoin bill on Wednesday after a procedural vote Tuesday failed (Among gainers Strategy +1.5%, Circle Internet Group +1.6%, Coinbase +0.8%, Galaxy Digital +4.1%, Hut 8 +2.3%, Hive Digital Technologies +0.7%, MARA Holdings +1.8%, Cleanspark +1.8%, Riot Platforms +2.1%, Cipher Mining +0.5%, Bitfarms +2.9%, Terawulf +1.6%, Bit Digital +6.4%, SharpLink Gaming +13%, and Bitdeer Technologies +2.6%).

ASML ADRs (ASML) fall 8.4% after the chip equipment maker struck a more cautious tone about growth outlook next year.

JB Hunt reported 2Q earnings that beat estimates, but flagged “higher professional driver wages and equipment-related costs.”

Brighthouse Financial (BHF) is up 7.4% on light volume after the Wall Street Journal said Aquarian is in exclusive talks to buy the provider of annuities and life insurance, citing people familiar.

Global Payments (GPN) is up 6.4%; activist investor Elliott Investment Management has amassed a sizable position in payments services company, according to a person with knowledge of the matter.

Renault SA shares sank 16% after the automaker lowered its profitability outlook for the year and named company veteran Duncan Minto interim chief executive officer.

Nvidia Corp. boss Jensen Huang anticipates getting the first batch of US licenses to export H20 AI chips to China soon.

Barclays Plc was fined £42 million ($56 million) over failures to properly identify financial crime risks with two clients.

Huawei Technologies Co. took the top spot in China’s smartphone market for the first time in more than four years.

Among trade headlines, Trump said he was likely to impose tariffs on pharmaceuticals as soon as the end of the month and that levies on chips could come soon as well. Traders further pared bets to their lowest level in a month for two Federal Reserve interest rate cuts this year on anticipation that tariff-related costs are increasingly being passed on to consumers (a continuation of a bet that has so far been dead wrong). Elsewhere, EU’s McGrath says a trade deal between the EU and US can be done by Aug. 1 and expects two weeks of “intense negotiations.” Meanwhile, UBS strategists said US equity investors are complacent in their view that tariffs are predominantly a negotiation tool. They put their S&P 500 year-end target of 5,300 – some 1000 lower than where the S&P is trading now – under review.

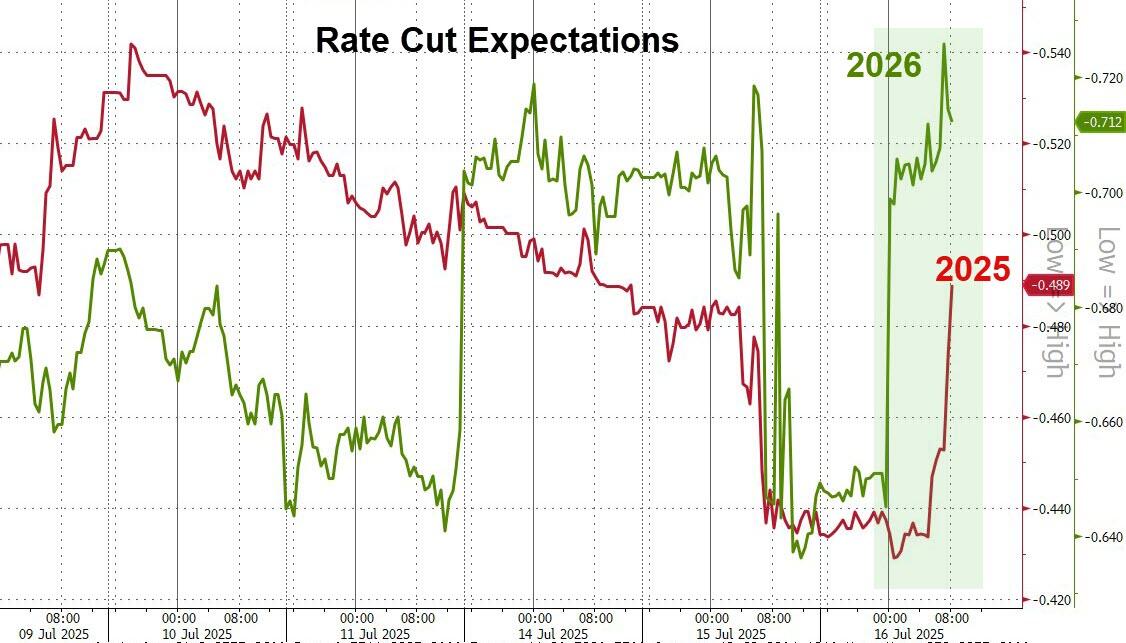

Traders trimmed expectations for Fed rate cuts after the CPI data, but the main Fed focus today is on who may replace Powell. Kevin Hassett is the early frontrunner, Bloomberg reported, with Kevin Warsh also in the top two. The Trump administration is also said to be finalizing an executive order that would pave the way for 401(k) retirement savings plans to invest in private equity.

After big bank earnings got off to an underwhelming start on Tuesday, investors will be looking at the next flurry of results with Bank of American Corp., Goldman Sachs and Morgan Stanley reporting today. “We have toned down our risk by a notch,” said Mohit Kumar, chief European strategist at Jefferies International. “However, technicals are still supportive and news flow of more deals being struck over the coming weeks should offset some of the negative trade rhetoric.”

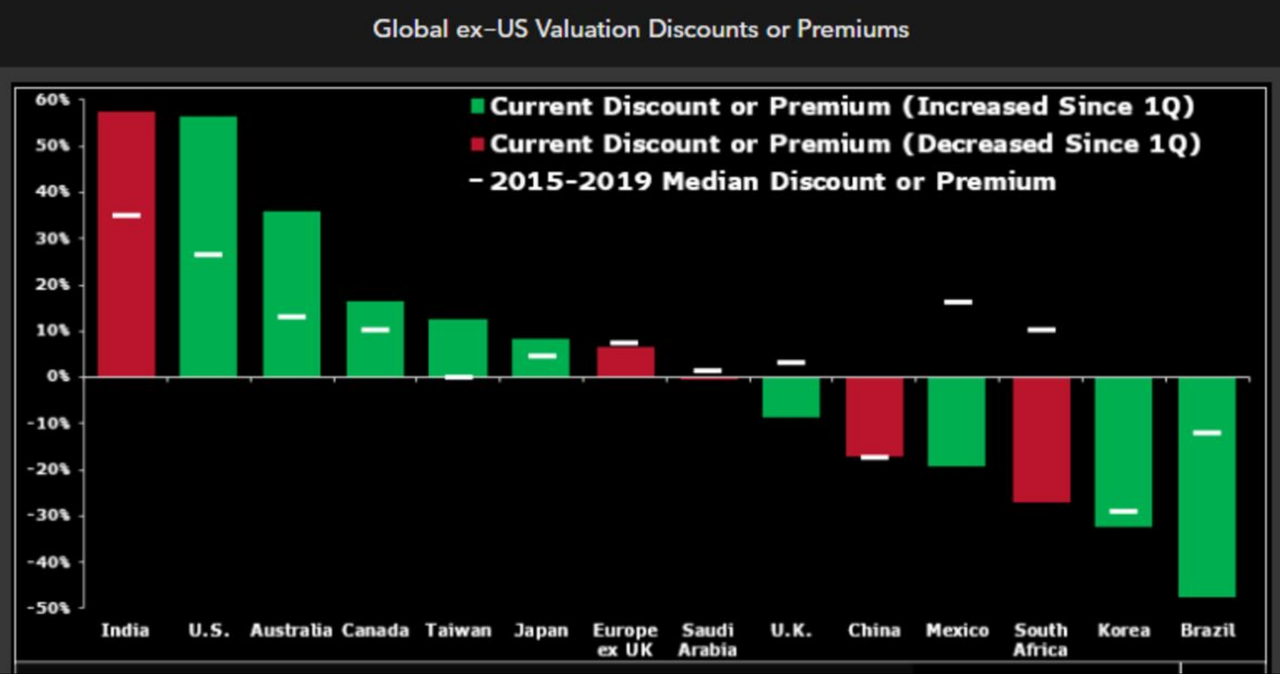

US stocks are back to near-historic premiums over global peers, but bargain hunters must also work harder to find options outside the world’s biggest market, according to Bloomberg Intelligence. The S&P 500 now trades at a 55% forward P/E premium to the Bloomberg Global ex-US Index, more than double the roughly 25% median from 2015-19.

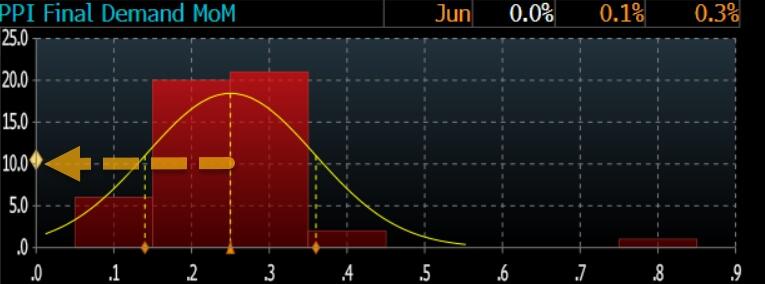

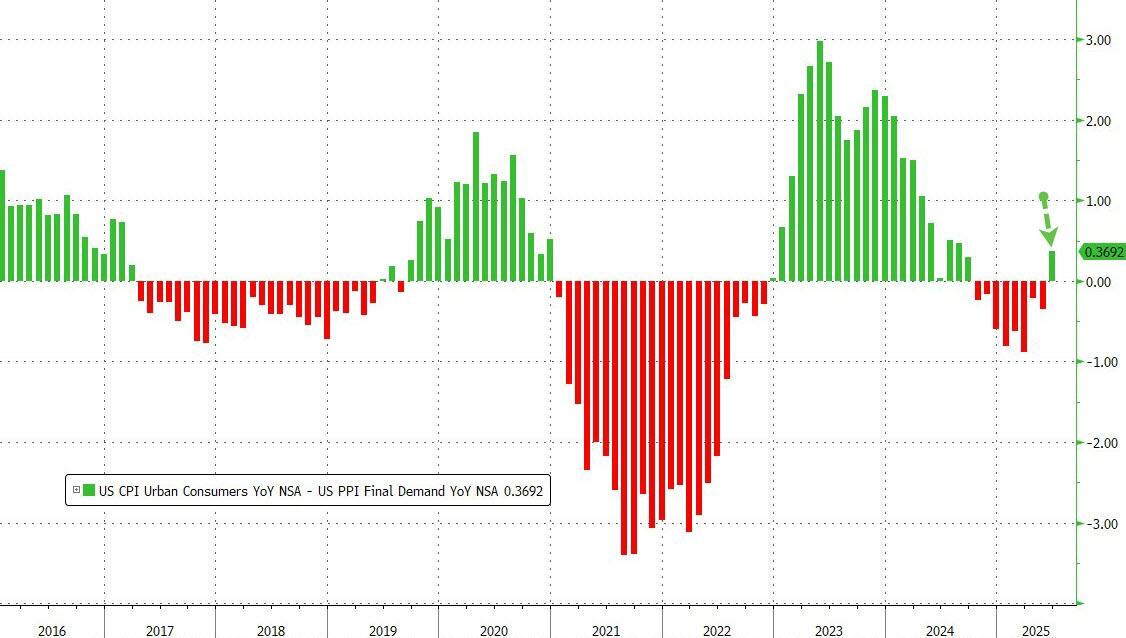

Economic data due later Wednesday is expected to show a similar trend for producer goods. “The tariff inflation shock starts to hit,” wrote Robin Brooks, a senior fellow at the Brookings Institution and former chief currency strategist at Goldman Sachs Group Inc. “This effect will keep building in intensity as pre-tariff inventories are depleted.”

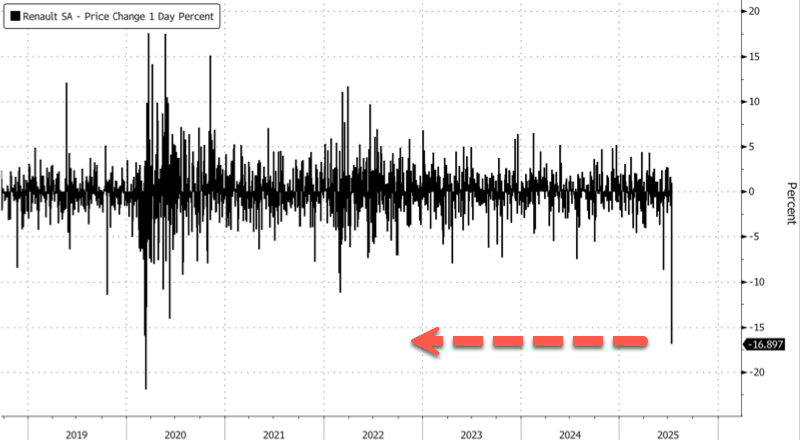

In Europe, the Stoxx 600 is down 0.2%, falling for a fourth straight session after some disappointing corporate updates from the region. Autos are leading declines as Renault shares fall 17% after the French carmaker issued a profit warning. Technology stocks also underperform as ASML shares fall 8% in Amsterdam after the CEO walked back the company’s growth forecast for next year due to trade disputes and global tensions. Equities have struggled to hit new highs in recent weeks amid lingering uncertainty around the US trade war. Among notable moves, Richemont rises on better-than-expected sales, defying a wider downturn for luxury goods. Renault shares tumble after a profit warning. Here are some of the more notable equity movers:

Richemont shares rise as much as 2.4% after the Cartier-owner reported surging sales at its jewelry division despite a tough backdrop for the luxury goods industry.

Partners Group climbs as much as 7.3%, after the Swiss private equity company delivers a beat on assets under management in the first half and reiterates its outlook for the full year.

Barco shares surge as much as 17%, hitting the highest since April 2024, following the visualization specialist’s first-half Ebitda beat.

ASML shares fall as much as 7.3%, the most in three months, after the chip equipment maker cautioned about growth next year.

Renault shares fall as much as 17%, the steepest drop since March 2020, after the French carmaker issued a profit warning on Tuesday evening, lowering operating margin guidance for this year and also trimming its free cash flow expectations.

AstraZeneca shares drop as much as 1.6%, after its experimental drug for a rare plasma cell disorder failed to delay death or reduce the number of hospitalizations for heart problems.

Ontex shares plunge as much as 12%, after the maker of disposable personal hygiene products delivered quarterly results below expectations and cut its full-year earnings outlook.

Bakkafrost falls as much as 14%, the most since July 2023, after the seafood group issued a profit warning.

Nel falls as much as 8.1%, the most since May, after the hydrogen technology supplier reported a sharp fall in new orders in the second quarter. Citi said weak order intake is a continued concern.

Fuchs shares plunge as much as 16%, the biggest drop since 2011, as the lubricant maker cut its annual guidance after second-quarter profit came in lower than expected.

DNO shares drop as much as 8.1% after the oil producer said it has temporarily suspended operations at its Tawke license in the Kurdistan region of Iraq following three explosions early this morning.

Svenska Handelsbanken declines as much as 8%, the worst performer on the Stoxx 600 Banks Index, after net interest income at the Nordic lender missed analysts estimates for the second quarter.

Earlier in the session, Asian stocks were mixed, as gains in Hong Kong and optimism over the tech sector were countered by dimming prospects for Federal Reserve easing. The MSCI Asia Pacific Index dipped 0.1%. Key gauges declined in Australia and South Korea, while shares rose in Taiwan as well as Hong Kong. TSMC and Alibaba climbed for a second day after news that the US would allow resumption of some AI chip shipments to China. The regional benchmark has traded sideways in July after a three-month rally. Broader sentiment took a hit Wednesday after US consumer price data indicated companies are beginning to pass through some tariff-related costs, with Fed Dallas President Lorie Logan saying. Hong Kong stocks advanced meanwhile, with the Hang Seng Index heading for its highest close since February 2022 on a rebound in risk appetite amid signs of easing US-China tensions. Still, upcoming Chinese corporate results are expected to show weak earnings growth.

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The euro outperforms its G-10 peers slightly with a 0.2% gain. The pound fades post-CPI gains, trading flat versus the greenback just below $1.34.

In rates, Treasuries are steady ahead of more US inflation data later on Wednesday in the form of producer prices. US 10-year yields are flat at 4.48%. Japan’s super-long bonds rebounded following a sharp selloff earlier in the week, as investors weighed the potential for increased fiscal spending after this weekend’s upper house election. Gilts fall along the curve after UK inflation unexpectedly rose to its highest level since January 2024, prompting traders to trim bets on easing by the Bank of England this year. UK 10-year yields rise 3 bps to 4.65%. Bunds are little changed.

In commodities, spot gold rises $16 to around $3,340/oz. Bitcoin climbs 2% and back above $119,000. WTI falls 0.5% to near $66.20 a barrel.

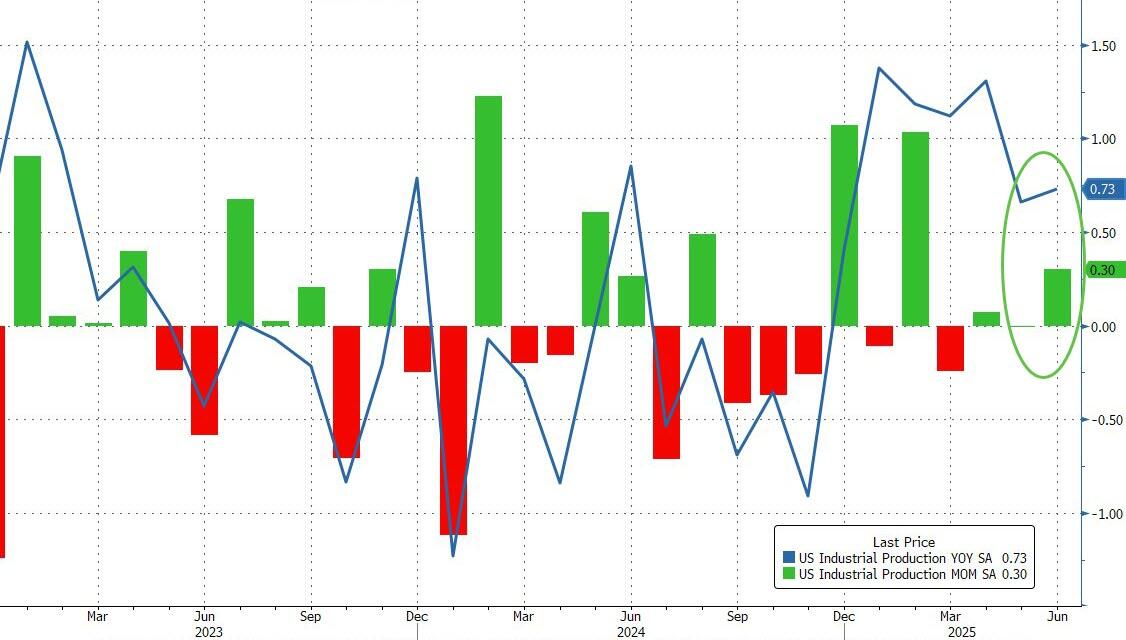

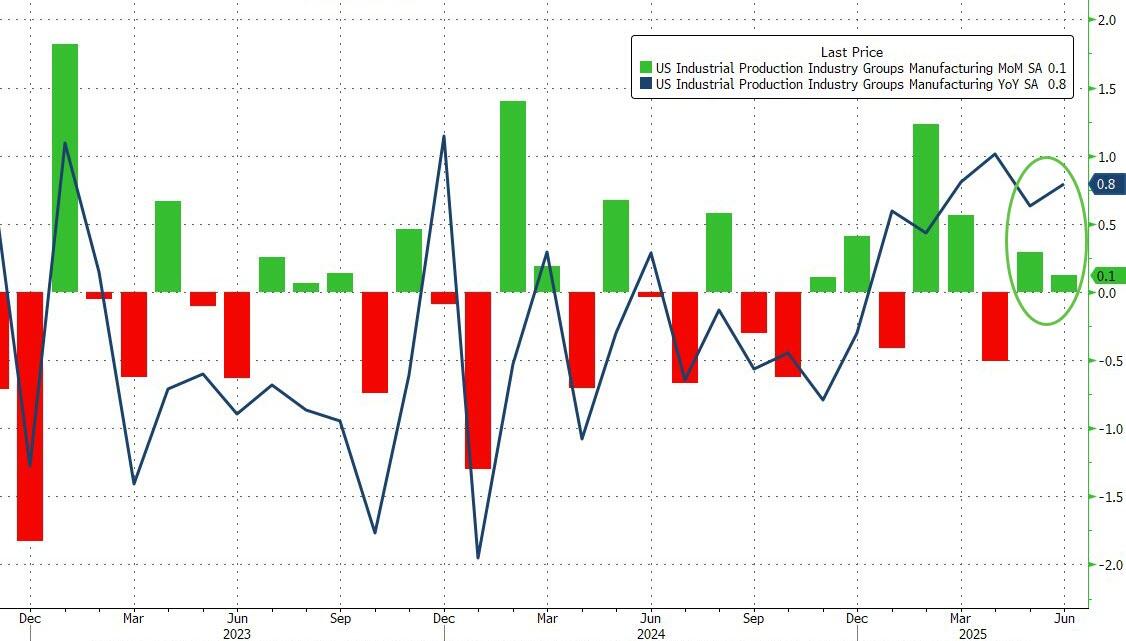

Today’s US economic data slate includes June PPI and July New York Fed services business activity (8:30am) and June industrial production (9:15am). Fed speaker slate includes Barkin (8am), Hammack (9:15am), Barr (10am), Bostic (3:30pm) and Williams (6:30pm), and Fed releases Beige book at 2pm

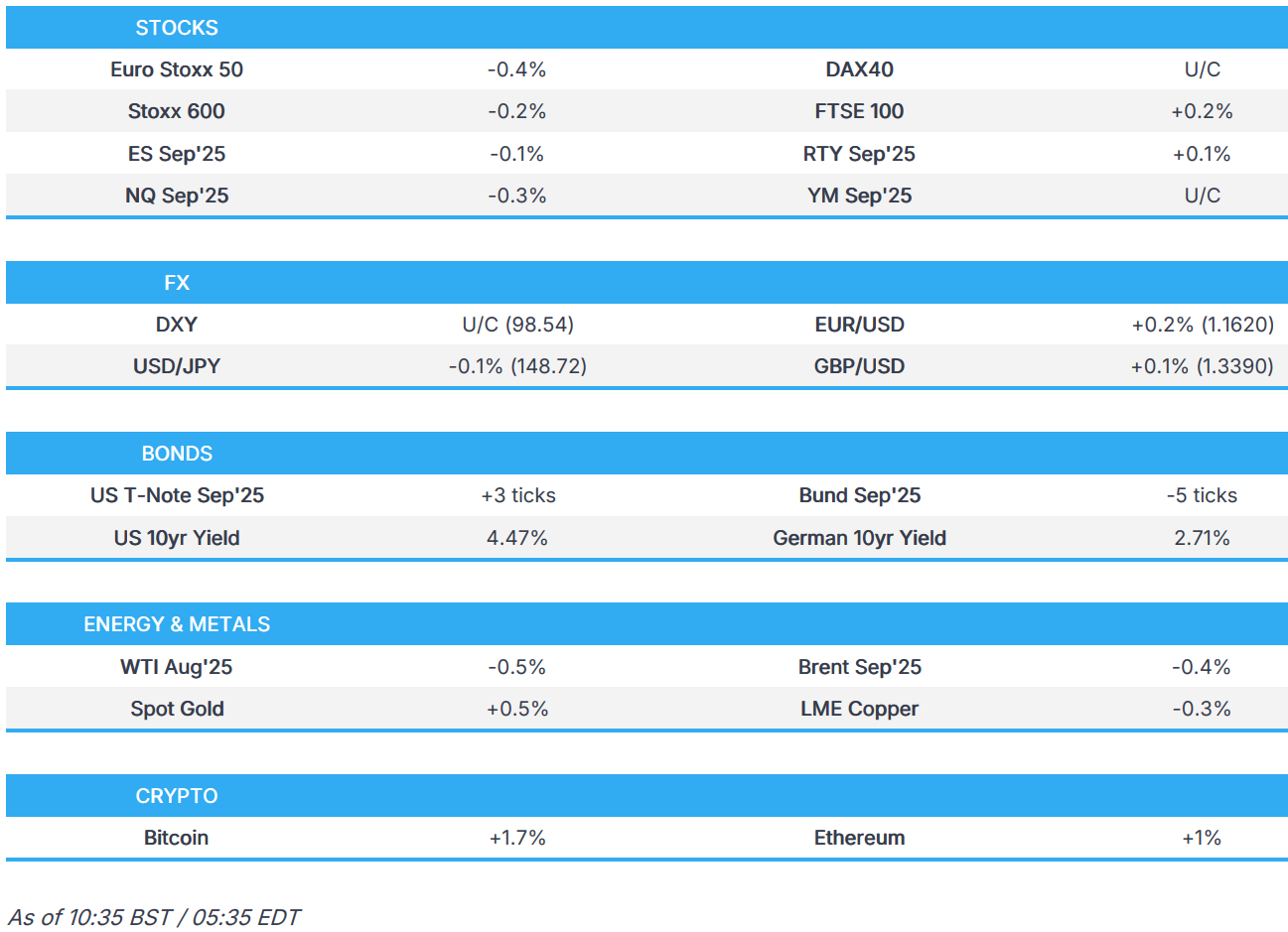

Market Snapshot

S&P 500 mini -0.1%

Nasdaq 100 mini -0.3%

Russell 2000 mini little changed

Stoxx Europe 600 -0.1%

DAX +0.2%

CAC 40 little changed

10-year Treasury yield -1 basis point at 4.48%

VIX unchanged at 17.38

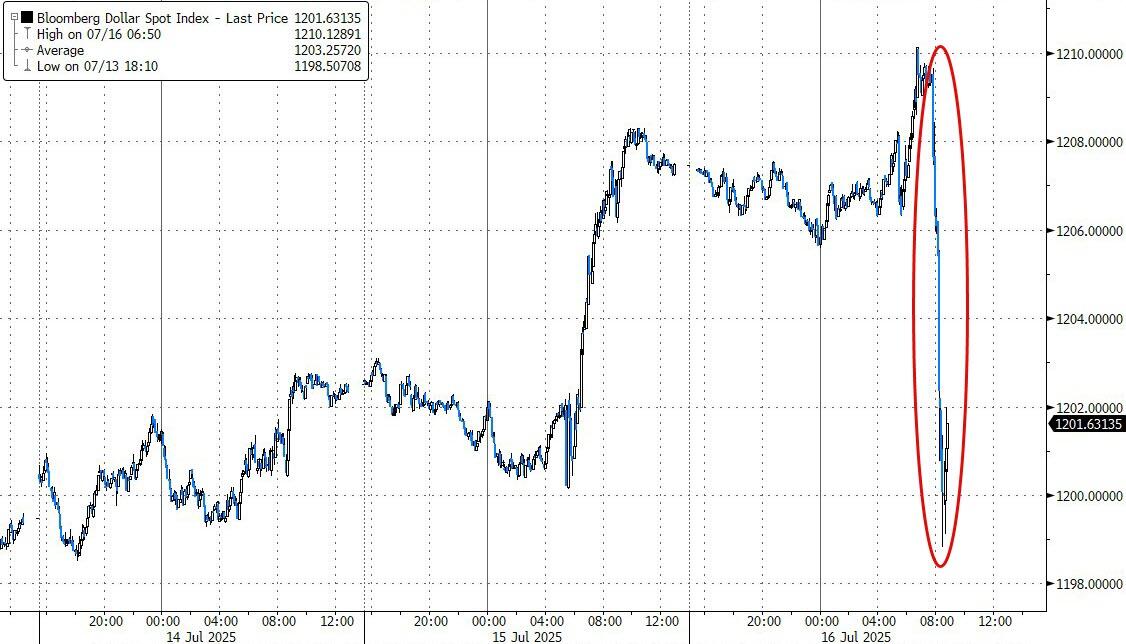

Bloomberg Dollar Index little changed at 1206.71

euro +0.2% at $1.162

WTI crude -0.3% at $66.32/barrel

Top Overnight News

Trump said on Tuesday that Treasury Secretary Scott Bessent could be a candidate to replace Federal Reserve Chairman Jerome Powell, but suggested that might not happen. When asked if Powell’s renovation cost overrun were a fire able offense, Trump said “I think it sort of is.” RTRS

President Donald Trump said he was likely to impose tariffs on pharmaceuticals as soon as the end of the month and that levies on semiconductors could come soon as well, suggesting that those import taxes could hit alongside broad “reciprocal” rates set for implementation on Aug. 1. BBG

Kevin Hassett, one of President Donald Trump’s longest-serving economic aides, is the early frontrunner to replace Jerome Powell as Federal Reserve chief next year, followed by Kevin Warsh. BBG

Trump is expected to sign an executive order in the coming days designed to help open up 401(k)s to private-market investments, according to WSJ.

Senator Cassidy said President Trump is to sign Fentanyl Act into law on Wednesday.

Defense Secretary Hegseth ordered the release of 2000 National Guard troops from the federal protection mission in LA.

Japan’s super-long bonds rose, reversing course after a rout earlier in the week over concern that this weekend’s election will result in higher government spending. BBG

Rio Tinto’s macro commentary on the Chinese economy – “industrial activity and net exports grew strongly during the quarter on the back of China’s highly competitive manufacturing sector. Trade diversification continued as the decline in exports to the US was more than offset by shipments to other regions. Retail sales growth was supported by ongoing stimulus measures while the government remains committed to infrastructure investment. However, headwinds such as trade tensions and a soft property market continue to pose challenges.”

Indonesia’s central bank cut its policy rate by 25bp to 5.25% (analysts were split on the outcome of this meeting, with some anticipating a cut while others felt rates would stay unchanged). WSJ

ASML (-7.3% in pre) walked back growth forecasts for next year due to the trade uncertainty, even as its second-quarter orders beat estimates. The stock slumped. BBG

Inflation unexpectedly rose in the U.K., likely keeping policymakers at the BOE cautious despite a limping economy. Headline, core, and services CPI all were higher than anticipated. WSJ

Taiwan, Switzerland and India, none of which received letters letters from Trump last week, are all potentially closing in on deals that could be announced in the coming weeks. Politico

Fed’s Logan (2026 voter) said the base case is that monetary policy needs to hold tight for a while longer to bring inflation down and she wants to see low inflation continue longer to be convinced, while she added that June CPI data suggests PCE inflation, which the Fed targets at 2%, will rise. Logan also commented that softer inflation and a weakening labor market could call for lower rates fairly soon and under the base case, the Fed can sustain maximum employment even with modestly restrictive policy.

Trade/Tariffs

US President Trump they are working on five to six trade deals and there will probably be two to three deals by August 1st.