JULY 18//GOLD CLOSED UP $11.10 TO $3351.90 WITH SILVER ALSO CLOSING HIGHER TO THE TUNE OF 13 CENTS TO $38.22//PLATINUM CLOSED DOWN $32.05 TO $1429.45 WITH PALLADIUM ALSO FALLING BY $25.40 DOWN TO $1259.10//GOLD COMMENTARY TODAY COURTESY OF ALASDAIR MACLEOD//A MUCH WATCH PODCAST TODAY OF ANDREW MAGUIRE TALKING WITH ALASDAIR MACLEOD ON CURRENCIES AND GOLD/SILVER..ROBERT LAMBOURNE PROVIDES FOR US A COMMENTARY FROM CHINA ON THE BULLISHNESS OF SILVER//THE EU PROVIDES ITS BUDGET FOR THE YEAR AND BOTH FRANCE AND GERMANY BLAST THEIR EXTRAVAGANCE//THE EU ROLLS OUT ITS 18TH SANCTIONS AGAINST RUSSIA DUE TO THE UKRAINE/RUSSIA WAR//ISRAEL VS HAMAS UPDATES//THE SITUATION INSIDE SYRIA WITH THE DRUZE HAS MANY UPDATES//RUSSIA VS UKRAINE UPDATES/COVID UPDATES/VACCINE INJURY REPORT/MARK CRISPIN MILLER/DR PAUL ALEXANDER/NEWSWIZE ETC//COMMENTARY TONIGHT ON THE GLOBAL ECONOMY COURTESY OF RABOBANK//USA DATA RELEASES//THERE HAS BEEN A CRIMINAL REFER TO BONDI ON JEROME POWELL RE HIS LAVISH SPENDING FOR THE FED BUILDING AT $2.5 BILLION DOLLARS//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUTURES US 60 332 H STANDARD CHARTERED B 3 363 H WELLS FARGO SECURITI 6 555 H BNP PARIBAS SEC CORP 250 624 H BOFA SECURITIES 251 151 661 C JP MORGAN SECURITIES 147 685 C RJ OBRIEN 1 686 C STONEX FINANCIAL INC 2 709 C BARCLAYS 39 880 H CITIGROUP 93 905 C ADM 1

TOTAL: 502 502 MONTH TO DATE: 9,513

JPMORGAN STOPPED 147/502

JULY

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 502 CONTRACTs NOTICES FOR 50,200 OZ or 1.5614 TONNES

total notices so far: 9513 contracts for 951,300 OR 29.589 tonnes)

FOR JULY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 210 NOTICE(S) FILED FOR 1.050 million OZ/

total number of notices filed so far this month : 9090 CONTRACTS (NOTICES) for 45.450 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $11.10 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//

INVENTORY RESTS AT 948.50 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.13 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ///A FRAUDULENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV///

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 472.453 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1055 CONTRACTS TO 172,865 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR SMALL GAIN OF $0.22 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. WE FINALLY ARE MOVING MUCH HIGHER THAN THE BASE $34.40 SILVER PRICE BARRIER. WE HAD A MEGA HUGE SIZED GAIN OF 1205 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL 150 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD SOME LIQUIDATION OF T.A.S. CONTRACTS EARLY IN COMEX TRADING WITH RESPECT TO THURSDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $36.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON THURSDAY WITH SILVER’S SMALL GAIN IN PRICE. THE PRICE FINISHED MILES ABOVE THE MAGIC NUMBER OF $36.00 SILVER SPOT PRICE CLOSING AT $38.09 . WE HAVE ANOTHER STRONG T.A.S. ISSUANCE AT 393 CONTRACTS ISSUED BY THE CME AND THAT STILL SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 38.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A SMALL 150 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG SIZED 393 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TODAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUGE SIZED 1205 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR SMALL GAIN IN PRICE OF $0.22.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT/FRIDAY MORNING: A STRONG SIZED 393 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.22) AND WERE UNSUCCESSFUL IN KNOCKING OF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A MEGA HUMONGOUS GAIN OF 1205 CONTRACTS ON OUR TWO EXCHANGES

WE HAD A 150 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 34.730 MILLION OZ PLUS TODAY’S STRONG QUEUE JUMP OF 715,000 OZ//NEW STANDING ADVANCES TO 45.805 MILLION OZ

THUS:

INITIAL STANDING FOR JULY: 45.805 MILLION OZ INCLUDING QUEUE JUMPS

WE HAD:

/ HUGE COMEX OI GAIN+// A SMALL SIZED EFP ISSUANCE 150 CONTRACTS (/ VI) A STRONG NUMBER OF T.A.S. CONTRACT ISSUANCE 393 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 141 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 13 DAY(S), total 6709contracts: OR 33.545 MILLION OZ (516 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 33.545 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 33.545 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1075 CONTRACTS DESPITE OUR SMALL GAIN IN PRICE OF $0.22 IN SILVER PRICING AT THE COMEX// THURSDAY.,. . THE CME NOTIFIED US THAT WE HAD A SMALL 150 CONTRACT EFP ISSUANCE CONTRACTS: 150 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 4 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 45.805 MILLION OZ//

THE NEW TAS ISSUANCE THURSDAY NIGHT (393 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE IN FRIDAY’S TRADING OR BEYOND!

WE HAD 210 NOTICE(S) FILED TODAY FOR 1.050 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6341 OI CONTRACTS TO 444,521 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 7952 CONTRACTS //.

WE HAD A STRONG SIZED DECREASE IN COMEX OI (6341 CONTRACTS) . THIS OCCURRED DESPITE OUR LOSS OF $11.10 IN PRICE// THURSDAY///.

LAST THREE MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 1.576 TONNES QUEUE JUMP = 30.634 TONNES STANDING

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 500 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 444,521 /NOW STILL AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 172,865 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5841 CONTRACTS WITH 6341 CONTRACTS DECREASED AT THE COMEX// AND A SMALL SIZED 500 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5841 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1202 CONTRACTS

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(500) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 6341 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 5841 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR JULY AT 17.947 TONNES COUPLED WITH TODAY’S 1.576 TONNES QUEUE JUMP//STANDING ADVANCES TO 30.634 TONNES.

NEW STANDING FOR GOLD, JULY CONTRACT AT 30.634 TONNES OF GOLD.

.

/ 3) SOME T.A.S. LIQUIDATION EARLY IN THE COMEX SESSION AS WE HAD 1)A $11.10 COMEX PRICE LOSS. HOWEVER WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THE LOSS IN PRICE AS WE HAD A STRONG LOSS OF 5841 CONTRACTS ON OUR TWO EXCHANGES COUPLED WITH SOME EARLY LIQUIDATION OF OUR TAS SPREADERS // /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4) STRONG SIZED COMEX OI LOSS// 5) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (500 CONTRACTS)/// FAIR T.A.S. ISSUANCE: 1202 T.A.S.CONTRACTS

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 20,734 CONTRACTS OR 2,073,400 OZ OR 64.49 TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 1594 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN13 TRADING DAY(S) IN TONNES 64.49 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 64.49 TONNES DIVIDED BY 3550 x 100% TONNES = 1.83% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 64.49 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1055 CONTRACTS OI TO 172,865 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 150 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1000 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1055 CONTRACTS AND ADD TO THE 150 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF 1205 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR SMALL GAIN IN PRICE OF $0.22 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 6.730 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 17.66 PTS OR 0.50%

//Hang Seng CLOSED UP 326.71 PTS OR 1.33%

// Nikkei CLOSED DOWN 82.08 PTS OR 0.21% //Australia’s all ordinaries CLOSED UP 1.30%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1767 OFFSHORE CLOSED DOWN AT 7.1805/ Oil UP TO 66.45 dollars per barrel for WTI and BRENT UP TO 68.34 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1767 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1805 AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6341 CONTRACTS TO A STILL LOW NUMBER OF 444,521 OI DESPITE OUR LOSS IN PRICE OF $11.10 WITH RESPECT TO THURSDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (500 ). WE HAD LITTLE T.A.S. LIQUIDATION //THURSDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICALEQUATING 2111 CONTRACTS.

THE CME ANNOUNCED THURSDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES.

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY 0

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 5841 CONTRACTS DESPITE OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON THURSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE IN JANUARY THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND NOW JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER FINALLY ENDS OUR MEGA MEGA HUGE T.A.S ISSUANCE. AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A MUCH MUCH LOWER 1202 T.A.S CONTRACTS THAN MONDAY’S ISSUANCE OF 22,678. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. HOWEVER JULY IS HUGE FOR A NON DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 1.576 TONNES QUEUE JUMP = 30.634 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 30.634 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 10+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 232 EPISODE AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 500 EFP CONTRACT WAS ISSUED: : /AUGUST 500 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 500 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

LITTLE LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY (EARLY IN THE COMEX SESSION)

ZERO NET SPEC LIQUIDATION DESPITE OUR LOSS IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY MORNING/THURSDAY NIGHT WAS A FAIR 1202 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THURSDAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.THIS WAS SURELY IN EVIDENCE IN TRADING THURSDAY WITH OUR LOSS IN PRICE DURING THE RAID WHICH ENDED IN TOTAL FAILURE

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 1.576 TONNES QUEUE JUMP = 30.634 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY 11.10/ /) BUT THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE AN FAIR SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION ////THURSDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE MEGA MEGA T.A.S. ISSUANCES, LAST WEEK , IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS. SO FAR FOR THE WEEK, THEY ONLY SUCCEEDED ON TUESDAY WITH THURSDAY’S RAID A TOTAL BUST.

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE GAINED A FAIR SIZED TOTAL OF 6.566 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 50700 OZ OR 1.576 TONNES OF GOLD//NEW STANDING ADVANCES TO 30.634 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $11.10

WE HAD A MAMMOTH 7952 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 5841 CONTRACTS OR 584,100 0Z (18.16 TONNES)

total deposit 48,258.651 oz (1.501 tonnes of gold)

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

502 notice(s) 50200 OZ 1.5614 TONNES

No of oz to be served (notices)

336 contracts 33,600 OZ 1.045 TONNES

Total monthly oz gold served (contracts) so far this month

9513 notices 951,300 oz 29.589 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRY

i) Into JPMORGAN 48,258.651 oz (1501 kilobars)

total deposit 48,258.651 oz (1.501 tonnes of gold)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entries

adjustments: 0

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JULY STANDS AT 838 CONTRACTS FOR A GAIN OF 501 CONTRACTS. ON THURSDAY WE HAD 6 NOTICES FILED, SO WE GAINED A HUGE SIZED 507 CONTRACTS OR 50,700 OZ (1.576 TONNES) ENTERTAINED WITH A QUEUE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD

AUGUST LOST 13,583 CONTRACTS DOWN TO 213,303 AS AUGUST BECOMES THE FRONT MONTH AND IT’S OI IS VERY HIGH AND NOT CONTRACTING ENOUGH. WE WILL PROBABLY HAVE A HIGH NUMBER OF TONNES STANDING.

SEPT GAINED 137 CONTRACTS TO 1729

We had 6 contracts filed for today representing 600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 502 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 147 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (9513 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (838 CONTRACTS) minus the number of notices served upon today (502 x 100 oz per contract) equals 984,900 OZ OR 30.634 TONNES to which we add 0 tonnes of gold issued under exchange for risk// total standing 30.634 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (9513 x 100 oz +we add the difference for front month of JULY (838 OI} minus the number of notices served upon today (502 x 100 oz) which equals 984,900 OZ OR 30.634 TONNES + 0 tonnes EX FOR RISK = 30.634 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 30.634 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

2 ENTRIES i) Out of Brinks 40,243.700 oz ii) Out of Stonex 614,449.500 oz

total withdrawal: 654,693.200 oz

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 195.913 MILLION OZ//.TOTAL REG + ELIGIBLE. 497.243 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 281 OPEN INTEREST CONTRACTS FOR A LOSS OF 46 CONTRACTS. WE HAD 189 CONTRACTS SERVED UPON THURSDAY SO WE GAINED A STRONG 143 CONTRACTS OR 715,000 OZ ENTERTAINED A QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST LOST 42 CONTRACTS TO 2,362 AS THIS MONTH BECOMES THE FRONT MONTH FOR SILVER

SEPTEMBER GAINED 1165 CONTRACTS UP TO 129,798 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:210 or 1.050 MILLION oz

CONFIRMED volume; ON THURSDAY 47,017 poor//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 9090 X5,000 oz = 45.450 MILLION oz

to which we add the difference between the open interest for the front month of JULY (281) AND the number of notices served upon today (210 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (9090) Notices served so far) x 5000 oz + OI for the front month of JULY(281) minus number of notices served upon today (210)x 5000 oz equals silver standing for the JULY contract month equating to 45.805 MILLION OZ .

New total standing: 45.805 million oz which is huge for this active delivery month of JULY. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 195.913 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/497.243 million. 42.25%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

JUNE 20 WITH GOLD DOWN $19.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 947.37 TONNES

JUNE 18 WITH GOLD UP $1.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.03 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 945.94 TONNES

JUNE 17 WITH GOLD DOWN $9.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 941.93 TONNES

JUNE 16 WITH GOLD DOWN $33.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.758 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 940.49 TONNES

JUNE 13 WITH GOLD UP $53.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.38 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 932.91 TONNES

JUNE 12 WITH GOLD UP $55.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 934.19 TONNES

JUNE 11 WITH GOLD UP $1.10 TODAY// SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.31 TONNEES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 935.91 TONNES

JUNE 10 WITH GOLD DOWN $11.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.02 TONNEES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 936.22 TONNES

JUNE 9 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.45 TONNEES OF GOLD FROM THE GLD//: /// ///INVENTORY RESTS AT 934.20 TONNES

JUNE 6 WITH GOLD DOWN $28.00 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

GLD INVENTORY: 948.50 TONNES, TONIGHTS TOTAL

SILVER

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

JUNE 20 WITH SILVER DOWN $0.83/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.818 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 474.641 MILLION OZ.

JUNE 18 WITH SILVER DOWN $0.20/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 17 WITH SILVER UP $0.67/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 473.096 MILLION OZ.

JUNE 16 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.727 MILLION OZ FROM THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 13 WITH SILVER UP $0.11/NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 473.550 MILLION OZ.

JUNE 12 WITH SILVER UP $0.11/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.276 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 473550 MILLION OZ.

JUNE 11 WITH SILVER DOWN $0.45/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.046 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.274 MILLION OZ.

JUNE 10 WITH SILVER DOWN $0.16/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.232 MILLION OZ.

JUNE 9 WITH SILVER UP $0.69/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.914 MILLION OZ.

JUNE 6 WITH SILVER UP $0.63/HUGE CHANGES AT THE SLV:A DEPOSIT OF 3.863 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.732 MILLION OZ. (A TOTAL DEPOSIT OF 11.856 MILLION PHANTOM OZ IN THE LAST 4 DAYS)

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

Silver swaps are facing a short squeeze in poor liquidity, with lease rates on the September Comex contract at over 5%. Gold continues to consolidate in a bullish pennant formation.

This week, gold continued its consolidation, while silver squeezed higher from Wednesday onwards. In European trade this morning, gold was $3350, down a paltry $5 from last Friday’s close. Silver was $38.35, barely changed on balance.

As our headline chart shows, silver is now outperforming gold, up 32% v gold up 27% this year so far. Will it continue?

I think the answer is yes. Silver has underperformed gold over the last decade, culminating in a gold/silver ratio of 121 in March 2021. That has come down substantially, but at 87 is still too high for a metal which is in growing supply deficit. Furthermore, future mine supply in the longer term is hampered by the lack of new discoveries for both silver and other metals where silver is a byproduct, and environmental and planning restrictions resulting in substantial lead times for new mine development.

The chart also remains positive:

Silver appears to be in runaway mode, perhaps needing some consolidation in the $40 region. That would make sense, with the short side in paper markets is being badly squeezed, reflected in the relationship between Comex’s open interest and the price:

Note how the price continued rising after the decline in open interest following its peak on 17 June (arrowed). This is evidence of a vicious bear squeeze, whereby liquidation of long positions failed to result in lower prices. And now open interest is rising, piling further pressure on the shorts, particularly in the swap category.

The record net short position is comprised of 27,804 long contracts as well as 80,128 shorts, the latter representing 400,640,000 ounces (update due tonight). The shorts are held by 24 traders, giving an average financial exposure of $634m per trader in illiquid conditions.

This is against a background of record Comex warehouse stocks, as the MacroMicro chart shows:

Comex warehouse stocks are the equivalent of 60% of mined supply. Commercial users appear to be treating Comex as the largest supply source of above-ground silver. In other words, silver is accumulating, with its new owners happy to store it in Comex vaults until they need it.

A factor driving the paper shortage is high lease rates, at over 5% today on the September contract confirming the liquidity shortage despite high warehouse stocks. The latter appears to incorporate a fear factor, reflecting Trump’s proposed blanket tariffs on Mexican imports, with the swaps being squeezed by poor liquidity.

In conclusion, it appears sensible to own physical silver in these conditions, because this squeeze looks like it has further to go, despite warehouse stock levels.

Silver’s potential is against a background for gold. Gold has been consolidating nicely in a bullish pennant formation which is now three months old.

Probably the most important news in recent weeks is Trump’s frustration that the Fed won’t reduce interest rates. Sensibly, Powell is keeping his head down and not being dragged into commenting. He surely knows that inflationary pressures are mounting, in part due to Trump’s tariff policies. He also knows that the Fed has a funding problem with a lack of demand along the treasury yield curve to absorb new debt and the refunding of maturing debt. To reduce interest rates goes against the inflation mandate and would make debt funding more difficult, other than by escalating T-bill issuance.

Meanwhile, the dollar’s trade-weighted index has stabilised — for the moment. But the chart says it is still going lower. The Powell/Trump issue could determine the timing of the next move

.

JOHN RUBINO

The next two commentaries provided to us from Robert Lambourne:

Since the beginning of this year, silver prices have surged by over 30%, outperforming gold, as investors have sought to expand their exposure to safe-haven assets amid the backdrop of the global trade war.

Since the beginning of this year, silver prices have surged by over 30%, outperforming gold, as investors have sought to expand their exposure to safe-haven assets amid the backdrop of the global trade war.

However, analysts believe that there is still room for silver prices to rise, driven by tight physical supply and growing investment demand. Citi Group forecast in a report on Wednesday that silver prices would rise to $40 per ounce in the next three months, further adjusting upward from the previous target price of $38.

Citi analysts pointed out that the rise in silver prices is not just a catch-up with gold prices but also a reflection of strong silver fundamentals. Additionally, silver prices are expected to benefit from expectations for US Fed interest rate cuts.

Tim Treadgold, a senior mining journalist in Australia, revealed another factor, stating that there are signs that the Russian Central Bank is buying silver in large quantities, which will affect silver prices. He did not provide evidence of the Russian Central Bank’s purchases but noted that since the bank announced its purchase of silver as reserves in September last year, silver prices have consistently outperformed gold.

Has a big buyer emerged? Treadgold said that gold has been the star of the commodity sector over the past three years. However, there are also signs that investors have paused their gold investments. Since 2022, gold prices have more than doubled, initially driven by central bank purchases and later joined by private investors entering the market.

He added that the rise in silver prices has been relatively slow, mainly due to the lack of big buyers like central banks. However, if the Russian Central Bank is quietly building up its silver reserves, other central banks in countries with good relations with Russia may follow suit.

On September 30, 2024, the Russian government revealed plans to invest up to 51 billion rubles ($535.5 million) over the next three years to increase its precious metal reserves. According to its draft federal budget, in addition to gold, Russia also seeks to expand the scope of its precious metal reserves to include silver and platinum group metals.

The draft budget does not include details about potential purchase plans, but some analysts believe that including silver in central bank foreign exchange reserves may attract new investor interest and re-establish it as an official monetary metal.

Willem Middelkoop, founder of the Commodity Discovery Fund, is one of the first to pay attention to the Russian Central Bank’s move. He said that although 60% of silver demand comes from industrial applications, investors should not completely overlook silver’s role as a monetary asset.

Meanwhile, Citi also predicts that gold will enter a plateau phase relative to silver. Analysts said that the market may have already seen the peak in gold prices, which was $3,500 per ounce set in April. The reason for the pullback in gold prices is weakening investment demand and an improved economic outlook.

Inflows into Silver-Backed Exchange-Traded Products Already Surpass 2024 Totals

(Washington, DC – July 9, 2025) Heightened geopolitical and economic uncertainties, along with positive price expectations, spurred silver investment in the first half of 2025. This action primarily drove the precious metal’s price in June to its highest level in 13 years.

Silver Price

The average annual silver price rose 25% through the first six months of 2025, only marginally lower than the average gold price, which increased by 26% during the same period.

The elevated gold:silver ratio in April and May also made silver appear undervalued from a long-term perspective. Meanwhile, improving sentiment in the industrial metals sector, following the start of trade talks between China and the US, provided additional price support.

Silver-Backed Exchange-Traded Products (ETPs)

With net inflows of 95 million ounces (Moz) in the first half of 2025, silver ETP investment has already surpassed the total for all of last year. This surge reflects increasingly bullish price expectations.

By June 30, global silver ETP holdings reached 1.13 billion ounces (Boz), just 7% below their highest level since the peak of 1.21 Boz in February 2021. Thanks to firmer silver prices, the value of these holdings hit a series of all-time highs in June, exceeding US$40 billion for the first time. Growth was relatively consistent over the first five months of 2025, before buying surged in June, which alone accounted for nearly half of the gains. As such, this marked the most significant monthly increase since the Reddit-driven silver squeeze in early 2021.

Futures Trading

On the CME, net managed money positions strengthened this year. As of June 24 (the latest available data at the time of writing), the net long position was up a staggering 163% from end-2024 levels. Notably, institutional investors have demonstrated a strong commitment to silver as a store of value for much of this year. This is reflected in the average net longs over the first six months of 2025, which achieved their highest level since the first half of 2021.

Retail Silver Investment

Retail investment in silver has experienced contrasting fortunes so far this year. In Europe, the recovery that began in late 2024 has continued into 2025. However, this growth stems from a relatively low base, and retail investment (in volume terms) still lags behind the elevated levels seen during 2020–2022. Nevertheless, the market has benefited from a slowdown in secondary market liquidations, which has lifted demand for newly minted bars and coins.

Indian retail investment demand remains strong, posting a 7% year-over-year gain over the first six months of 2025. This partly reflects ongoing strong price expectations.

This contrasts with the US, where selling back by retail investors remains high. This dynamic, along with weak retail purchases, has weighed heavily on new bar and coin sales as some US investors have been encouraged by multi-year high prices to book profits. Furthermore, the absence of a crisis in the US (like the collapse of Silicon Valley Bank in 2023) has reduced safe-haven purchases. Overall, US retail demand for silver is estimated to have fallen by at least 30% so far this year.

Looking ahead, in the coin and bar market, there is potential for strong two-way activity in the months ahead, although demand for newly struck products may remain subdued. One area of uncertainty, however, is how investors will react should the silver price eclipse US$40. The market could see a mixture of profit-taking by some, while other investors jump in, expecting further price gains.

CHRIS POWELL AND GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 232

5. COMMODITY REPORT…URANIUM

For National Security, We Need Uranium Mined In America

Perhaps it’s too soon to mark nuclear power’s revival in the U.S. but there is a burst of activity that should ultimately yield a new generation of advanced nuclear plants and small modular reactors.

This is especially true for major industrial energy consumers—which now also includes data centers—where there is a strong economic incentive to use more nuclear power instead of natural gas and intermittent renewables.

In Illinois, Meta recently signed a long-term agreement to buy nuclear power from Constellation’s Clinton nuclear plant, the latest in a slew of deals between big tech and the nuclear industry. Constellation also said it would restart Three Mile Island Unit One in Pennsylvania and sell the power to Microsoft under a 20-year agreement. Google, too, has agreed to fund the development of small modular reactors, or SMRs, at three new nuclear sites in Oregon. TVA plans to build SMRs at its Clinch River site and Kairos Power has a blueprint for an advanced molten salt reactor. Moreover, Amazon, Google and Meta signed a pledge in March calling for nuclear energy worldwide to triple by 2050.

Elevating nuclear power on our list of energy options makes sense because it is the only way to generate large amounts of emission-free electricity reliably for AI-powered data centers, electric vehicles and industries. But surging demand for electricity and nuclear power underscores a serious issue: Who will provide the huge amounts of uranium needed to fuel nuclear plants?

Currently, 95 percent of the uranium used at US nuclear plants is imported from other countries, with Russia and former Soviet States flooding the global market and driving free-market companies out of business. China is also rapidly expanding its influence in the global uranium supply chain. But our dependence on uranium imports is not for lack of domestic resources.

In fact, in the mid-1970s the U.S. was the sole supplier of enriched uranium in the West, and business boomed. Since then, artificially low prices—and policy antagonism to domestic production—have forced U.S. customers into the hands of foreign competitors. Currently, there are only five uranium mines operating in the U.S. in contrast to several dozen in the 1970s and 20 as recently as 2009.

A uranium crisis may not be imminent, but the long-term implications of buying cheap foreign uranium instead of from US mining companies are ominous, particularly for national defense, including the Navy’s fleet of nuclear-powered aircraft carriers and nuclear submarines. Our nation’s fleet of 94 nuclear power plants also requires a dependable supply of uranium.

American industries, including our defense industrial base, are currently under immense pressure from China’s export restrictions on mineral exports—including rare earth metals. We know too well that the era of overreliance on mineral imports must come to an end. This is an economic, energy and national security vulnerability that has become untenable.

Given the risk of a cutoff of uranium imports or a huge spike in the price of uranium, we need a government policy to counter the threat to our national security and economy. President Trump recently said the Administration will draw up recommendations for reviving and expanding U.S. uranium production. That’s a good first step but we must match intent with action.

Our dependence on imported minerals, particularly from adversaries, poses a grave threat to national security. And it will cause serious trouble for key sectors of our economy if something isn’t done soon to boost domestic production. For these reasons, the U.S. now faces a monumental challenge: scaling up production of uranium, diversifying supply chains to protect national security and doing so in ways that are sustainable.

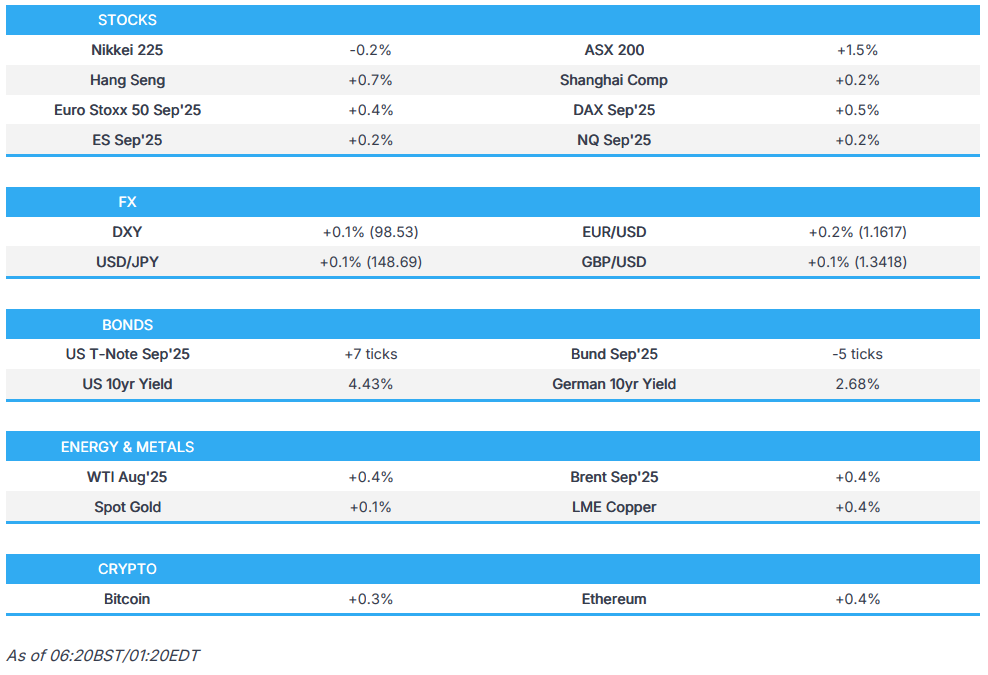

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 17.66 PTS OR 0.50%

//Hang Seng CLOSED UP 326.71 PTS OR 1.33%

// Nikkei CLOSED DOWN 82.08 PTS OR 0.21% //Australia’s all ordinaries CLOSED UP 1.30%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1767 OFFSHORE CLOSED DOWN AT 7.1805/ Oil UP TO 66.45 dollars per barrel for WTI and BRENT UP TO 68.34 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1767 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1805 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1767 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.1805 (CCP MANIPULATED)

SHANGHAI CLOSED UP 17.66 PTS OR 0.50%

HANG SENG CLOSED DOWN 18.81 PTS OR 0.08%

2. Nikkei closed DOWN 82.08 PTS OR 0.21%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 98.07/ EURO RISES TO 1.1643 UP 28 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.525//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.60…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6970/Italian 10 Yr bond yield UP to 3.589 SPAIN 10 YR BOND YIELD UP TO 3.316%

3i Greek 10 year bond yield UP TO 3.422

3j Gold at $3347.70 Silver at: 38.30 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 33 /100 roubles/dollar; ROUBLE AT 78.46

3m oil (WTI) into the 67 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.60// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.525% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8016 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9333 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.438 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.991 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.894 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.38

10 YR UK BOND YIELD: 4.6640 UP 1 PTS

10 YR CANADA BOND YIELD: 3.574 DOWN 2 BASIS PTS

5 YR CANADA BOND YIELD: 3.105 DOWN 2 PTS

2a New York OPENING REPORT

Futures Flat With $2.8 Trillion In Options Set To Expire

Friday, Jul 18, 2025 – 08:21 AM

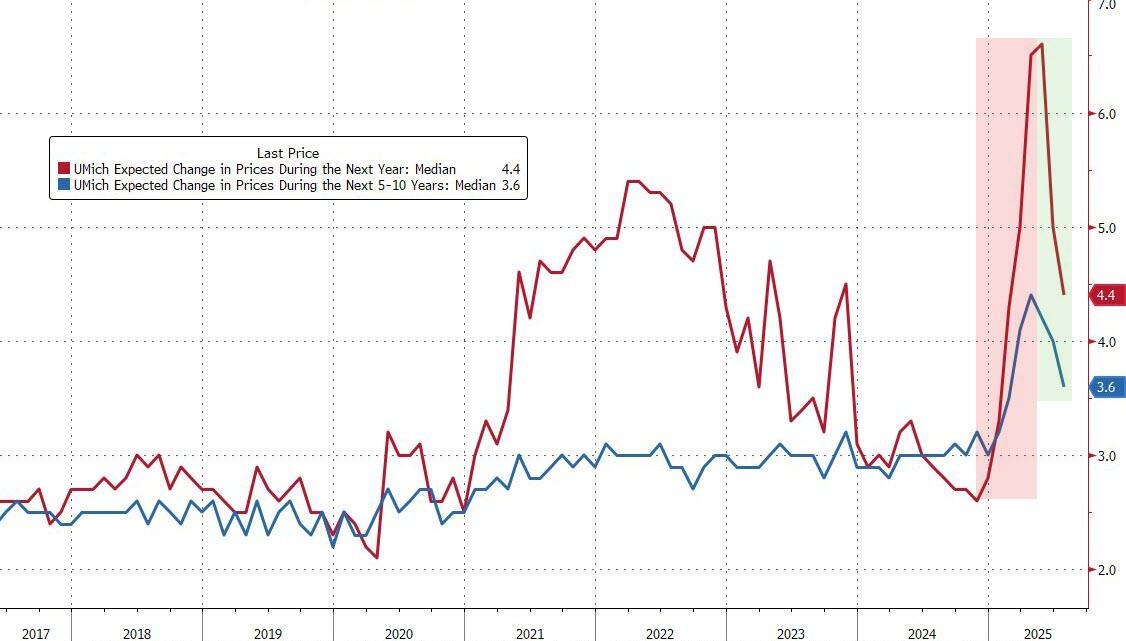

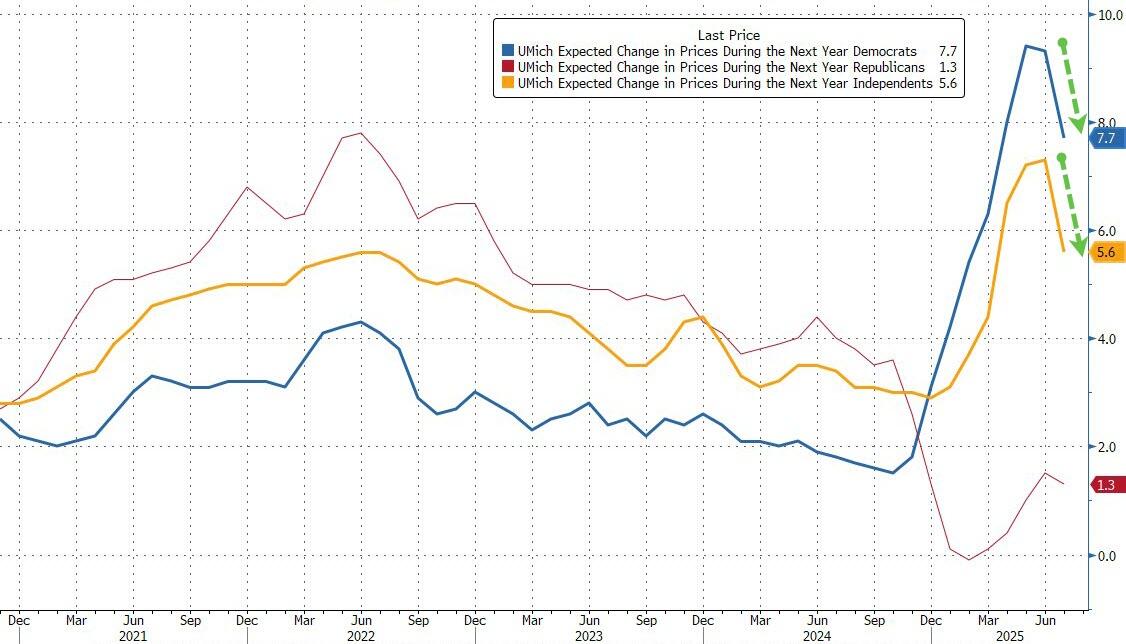

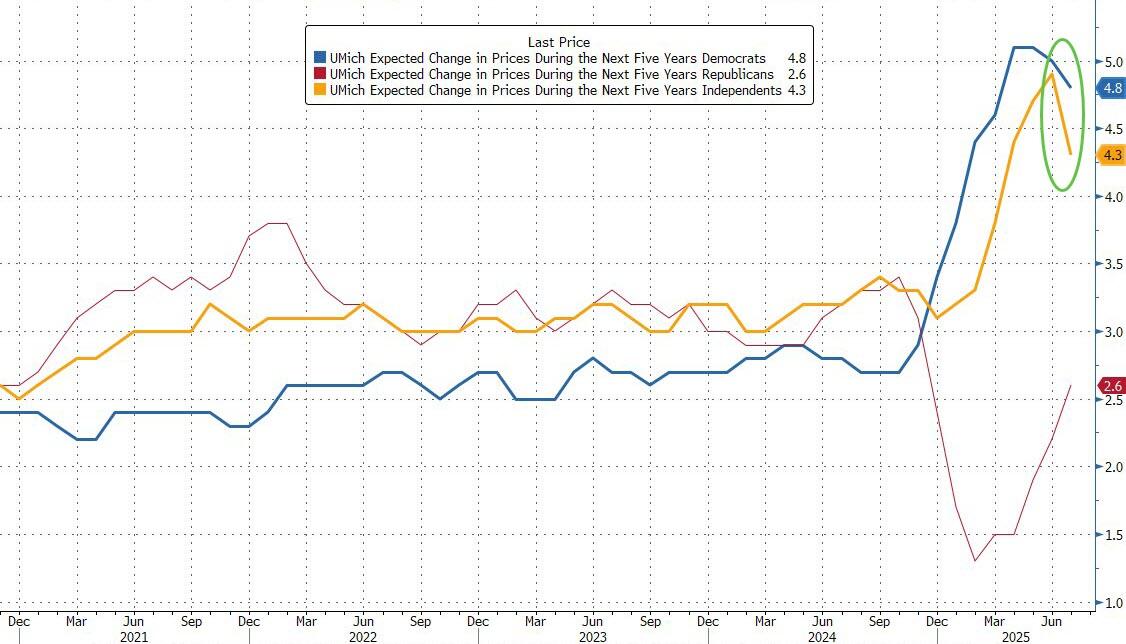

US equity futures are flat even as the global equity rally extended into Europe, following Friday’s gains in Asia and Thursday’s record close on Wall Street. As of 8:00am, S&P futures are unchanged while Nasdaq 100 futures rise 0.1% after NFLX had a solid report, but market reactions were muted amid high expectations. Europe’s Stoxx 600 initially rose 0.4% but has since erased gains, with Energy stocks outperforming and tracking a two-day advance in oil prices as Brent crude futures climb 1.2% to above $70 per barrel. Pre-market in the US, megacap tech sees NVDA up modestly (+0.4%), followed by AAPL and GOOGL. Consumer Staples and Financials are outperforming. The dollar and 2Y rates dropped after Fed Governor Christopher Waller repeated his recent view that the Fed should cut 25bps this month. Yields are lower and USD is weaker; 2-, 5-, 10-, and 30-year yields are down by 1-2bps. Commodities are mixed, with Oil and Precious Metals higher, while Base Metals are flat. The combined value of cryptoassets soared beyond $4 trillion for the first time, fueled by a surge in Ethereum and momentum from a legislative push to regulate the sector. Looking at today’s calendar, the US economic data slate includes June housing starts (8:30am) and July preliminary University of Michigan sentiment (10am). Fed speaker slate includes only Waller, and Fed officials’ external communications blackout ahead of their July 30 decision starts Saturday

In premarket trading, Mag 7 stocks are higher (Nvidia +0.4%, Tesla +0.3%, Alphabet +0.4%, Microsoft +0.2%, Apple +0.1%, Amazon +0.1%, Meta Platforms +0.2%). Here are some other notable premarket movers:

American Express Co. (AXP) rises 1.7% after the company’s billed business on its cards and other products outperformed expectations in the second quarter as its affluent customers continued to spend.

Blaize (BZAI) surges 100% after the company secured a contract to deploy its hybrid AI platform across Asia in collaboration with Starshine Computing Power Technology.

Hess Corp. (HES) rises 7% after winning its arbitration battle with Exxon Mobil Corp., clearing the way for it to be bought by Chevron Corp. more than 20 months after the $53 billion deal was announced. Chevron (CVX) shares are up 3%

Interactive Brokers (IBKR) rises 5% after reporting total net interest income for the second quarter that beat the average analyst estimate

Netflix (NFLX) falls 1.7% after the streaming-video company’s strong second-quarter results clashed against high expectations. The stock has been a strong performer this year, up nearly 50% off an April low.

Sable Offshore (SOC) rises 6% after a Santa Barbara judge issued a preliminary ruling on the oil and gas company’s Las Flores Pipelines.

Sarepta (SRPT) sinks 31% after the gene therapy maker said another patient has died from acute liver failure after receiving one of its experimental gene therapies for a muscle disease.

Symbotic (SYM) slips 1.8% after Deutsche Bank cut the automation technology company to hold, citing that much of the stock’s growth is already priced in at the current valuation.

Viatris (VTRS) falls 3% after saying its Phase 3 trial of pimecrolimus 0.3% ophthalmic ointment for blepharitis did not meet the primary endpoint, prompting the company to review its development plans.

The dollars dipped and treasuries advanced, with the 10-year yield down two basis points to 4.43%, after Fed governor Waller again backed a July interest-rate cut to support a softening labor market. The message failed to catch on in money markets, with swaps pricing less than a 60% chance of a quarter-point cut in September and assign no probability to easing this month. The cross-asset moves come at the end of a week marked by market jitters over speculation that President Donald Trump might fire Fed Chair Jerome Powell. And sure enough, Trump continued his Fed attacks on Friday, saying policymakers “are choking out the housing market with their high rate.”

Meanwhile, the week’s market gains reflected strong economic data and optimism that US companies will post robust second-quarter figures, helping to soothe uncertainty stirred by Trump’s tariff war. Early results show S&P 500 earnings are on track to rise 3.2% for the second quarter, slightly ahead of pre-season expectations of 2.8%, according to data compiled by Bloomberg Intelligence.

And speaking of earnings, on Friday, 3M raised its profit forecast and beat Wall Street’s estimates as CEO William Brown’s effort to reinvigorate the company gained momentum. American Express’s billed business on its cards and other products also beat forecasts. On Thursday, Netflix’s results surpassed expectations across all key metrics and raised its full-year outlook for both revenue and profit margins. The stock slipped in premarket trading after a near 50% rally from its April low.

“All that helps to reinforce the bull case for equities, with this solid underlying economic momentum likely to see earnings growth remain healthy,” said Michael Brown, senior research strategist at Pepperstone.

In trade, EU purposed scrapping 10% duty on US cars if Trump lowers 25% tariff below 20%, crude is bid as the EU adopted its 18th sanction package against Russia capping oil price at $47 per barrel, and the US House passed the GENIUS ACT to regulate stablecoins which now heads to the President to sign.

Elsewhere, the share of global equity flows heading to the US has plunged in 2025, BofA’s Michael Hartnett wrote, as the trade war raises doubts about so-called American exceptionalism. US stock funds attracted just under half of total flows so far this year, compared with 72% in 2024. For Mohit Kumar, chief European strategist at Jefferies International, risk assets are likely to remain well supported until next month, when US employment data may start to show some weakness.

“We remain positive on risky assets over the coming weeks, though we have taken some chips off the table,” Kumar noted. “Technicals will start to shift in August.”

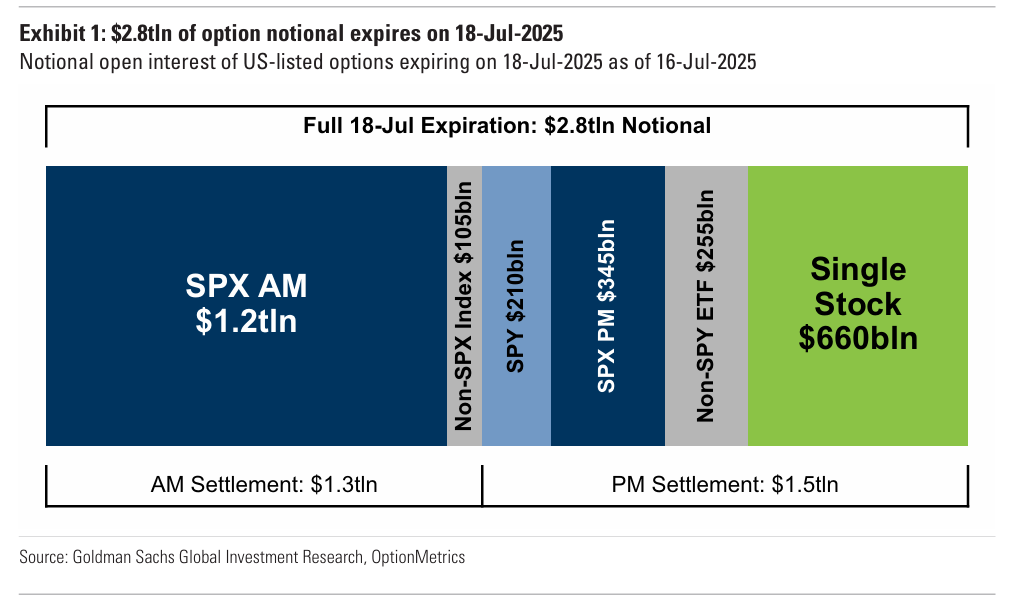

Also don’t forget that today is a big option expiration Friday with over $2.8 trillion of notional options exposure will expire including $1.5 trillion of SPX options and $660 billion notional of single stock options. The notional open interest for this expiration is similar to that of last July. Next week we get ~23% of SPX mkt cap reporting and Powell speaking at a conference on Tuesday.

Europe’s Stoxx 600 initially rose 0.4% but has since erased gains, with Energy stocks outperforming and tracking a two-day advance in oil prices as Brent crude futures climb 1.2% to above $70 per barrel. Mining stocks also outperform after BHP delivered an upbeat assessment of Chinese demand. US equity futures edged higher. Here are the biggest European movers:

Saab shares soar as much as 13% to hit an all-time high after the defense technology business posted sales above expectations in the second quarter and raised its growth outlook for the full year.

Reckitt Benckiser shares rise as much as 2.2% after the UK consumer goods company agreed to sell most of its homecare business to Advent International for an enterprise value of up to $4.8 billion.

Vestas shares rise as much as 12%, hitting the highest level since May, after the wind turbine company announced a large order in the US amid a paucity of order activity in the region.

SKF advances as much as 5.5%, the most since May, after the Swedish ball-bearings giant reported a strong set of 2Q results, with analysts positively noting the company’s resilient sales and margins.

Senior shares jump as much as 19%, soaring to a 2019-high, after the company struck a deal to offload its Aerostructures business.

Getinge shares rise as much as 7.2%, the most since April 10, after the Swedish health-care equipment firm reported adjusted operating profit for the second quarter that beat the average analyst estimate.