JULY 22/GOLD SKYROCKETS UP ANOTHER $36.60 TO $3428.80//SILVER FINISHES THE DAY UP $0.20 TO $39.20//PLATINUM WAS DOWN $8.30 TO $1441.65 WITH PALLADIUM UP $9.80 TO $1280.60/ISRAEL VS HAMAS; ISRAEL PUSHES INTO THE CENTRAL PART OF THE GAZA STRIP //IRAN: SUPPOSEDLY TO BEGIN NUCLEAR TALKS WITH FRANCE AND GERMANY//RUSSIA VS UKRAINE; RUSSIA DOWNPLAYS 3RD MEETING TO END THE WAR//COVID UPDATES/VACCINE INJURY REPORT/DR PAUL ALEXANDER/MARK CRISPIN MILLER//NEWS ADDICTS ETC//EXCELLENT COMMENTARY TONIGHT FROM DR LACALLE//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUTURES US 16 332 H STANDARD CHARTERED B 1 363 H WELLS FARGO SECURITI 159 435 H SCOTIA CAPITAL (USA) 8 624 H BOFA SECURITIES 63 661 C JP MORGAN SECURITIES 77 686 C STONEX FINANCIAL INC 5 10 686 H STONEX FINANCIAL INC 319 709 C BARCLAYS 9 905 C ADM 22 3

TOTAL: 346 346 MONTH TO DATE: 10,251

JPMORGAN STOPPED 77/340

JULY

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 346 CONTRACTs NOTICES FOR 34,600 OZ or 1.076 TONNES

total notices so far: 10,251 contracts for 1,025,100 OR 31.884 tonnes)

FOR JULY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 59 NOTICE(S) FILED FOR 0.295 million OZ/

total number of notices filed so far this month : 9198 CONTRACTS (NOTICES) for 45.990 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $36.60 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 3.43 TONNES OF GOLD OUT OF THE GLD//

INVENTORY RESTS AT 947.06 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.20 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ///A FRAUDULENT CRINAL OF 11.175 MILLION OZ INTO THE SLV///

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 482.447 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1690 CONTRACTS TO 173,412 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0.78 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE FINALLY ARE MOVING MUCH HIGHER THAN THE BASE $34.40 SILVER PRICE BARRIER. WE HAD A HUGE SIZED GAIN OF 1730 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL 40 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO MONDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $36.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON FRIDAY WITH SILVER’S HUGE GAIN IN PRICE. THE PRICE FINISHED MILES ABOVE THE MAGIC NUMBER OF $36.00 SILVER SPOT PRICE CLOSING AT $39.00 . WE HAVE ANOTHER HUGE T.A.S. ISSUANCE AT 859 CONTRACTS ISSUED BY THE CME AND THAT STILL SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 38.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A SMALL 40 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 859 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUGE SIZED 1730 CONTRACTS ON OUR TWO EXCHANGES WITH OUR STRONG GAIN IN PRICE OF $0.78.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A HUGE SIZED 859 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.78) AND WERE UNSUCCESSFUL IN KNOCKING OF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HADV A HUMONGOUS GAIN OF 1730 CONTRACTS ON OUR TWO EXCHANGES WITH ZERO T.A.S. SPREADER LIQUIDATION.

WE HAD A 40 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 34.730 MILLION OZ PLUS TODAY’S GOOD SIZED QUEUE JUMP OF 300,000 OZ//NEW STANDING ADVANCES TO 46.155 MILLION OZ

THUS:

INITIAL STANDING FOR JULY: 46.155 MILLION OZ INCLUDING QUEUE JUMPS

WE HAD:

/ HUGE COMEX OI GAIN+// A SMALL SIZED EFP ISSUANCE 40 CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 859 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 188 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 15 DAY(S), total 7049 contracts: OR 35.245 MILLION OZ (469 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 35.245 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 35.245 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1730 CONTRACTS WITH OUR GAIN IN PRICE OF $0.78 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A SMALL 40 CONTRACT EFP ISSUANCE CONTRACTS: 40 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 4 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.155 MILLION OZ//

THE NEW TAS ISSUANCE MONDAY NIGHT (959 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE IN TUESDAY’S TRADING OR BEYOND!

WE HAD 59 NOTICE(S) FILED TODAY FOR 0.295 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A MEGA HUMONGOUS SIZED 24,568 OI CONTRACTS TO 477,796 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 6475 CONTRACTS //.

WE HAD A MEGA HUMONGOUS SIZED INCREASE IN COMEX OI (24,568 CONTRACTS) . THIS OCCURRED WITH OUR GAIN OF $40.30 IN PRICE// FRIDAY///.

LAST THREE MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0.1275 TONNES QUEUE JUMP = 32.223 TONNES STANDING

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3751 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 471,321 /NOW STILL AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 173,412 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A MEGA HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 28,319 CONTRACTS WITH 24,568 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 3751 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 28,319 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1696 CONTRACTS

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(3751) ACCOMPANYING THE HUGE SIZED INCREASE IN COMEX OI OF 24,568 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 28,319 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR JULY AT 17.947 TONNES COUPLED WITH TODAY’S 0.1275 TONNES QUEUE JUMP//STANDING ADVANCES TO 32.223 TONNES.

NEW STANDING FOR GOLD, JULY CONTRACT AT 32.223 TONNES OF GOLD.

.

/ 3) ZERO T.A.S. LIQUIDATION IN THE COMEX SESSION AS WE HAD 1)A $40.30 COMEX PRICE GAIN. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH THE GAIN IN PRICE AS WE HAD A MEGA HUMONGOUS GAIN OF 28,319 CONTRACTS ON OUR TWO EXCHANGES COUPLED WITH ZERO LIQUIDATION OF OUR TAS SPREADERS // /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4) MEGA HUMONGOUS SIZED COMEX OI GAIN// 5) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (3751 CONTRACTS)/// FAIR T.A.S. ISSUANCE: 1696 T.A.S.CONTRACTS

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 25,580 CONTRACTS OR 2,558,000 OZ OR 79.564 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 1705 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN15 TRADING DAY(S) IN TONNES 79.564 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 79.564 TONNES DIVIDED BY 3550 x 100% TONNES = 2.24% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 79.564 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE SIZED 1690 CONTRACTS OI TO 173,600 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 40 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 40 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 40 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1690 CONTRACTS AND ADD TO THE 40 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 1730 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.77 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 8.65 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 22.07 PTS OR 0.62%

//Hang Seng CLOSED UP 97.24 PTS OR 0.39%

// Nikkei CLOSED DOWN 44.19 PTS OR .11% //Australia’s all ordinaries CLOSED UP 0.17%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1741 OFFSHORE CLOSED UP AT 7.1773/ Oil UP TO 66.88 dollars per barrel for WTI and BRENT UP TO 68.24 Stocks in Europe OPENED MOSTLY ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1741 AND STRONG//OFF SHORE YUAN TRADING UP TO 7.1773 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A MEGA MEGA HUMONGOUS SIZED 24,568 CONTRACTS TO 471,321 OI WITH OUR GAIN IN PRICE OF $40.30 WITH RESPECT TO MONDAY’S // TRADING. THIS IS THE HIGHEST GAIN IN COMEX IN QUITE SOME TIME. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3751 ). WE HAD ZERO T.A.S. LIQUIDATION //MONDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 34,794 CONTRACTS.

THE CME ANNOUNCED MONDAY NIGHT, A ZERO EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR NIL TONNES.

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY 0

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A MEGA MEGA HUMONGOUS SIZED GAIN ON OUR TWO EXCHANGES OF 28,319 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON FRIDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE IN JANUARY THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 3.5 TO 5% AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND NOW JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER FINALLY ENDS OUR MEGA MEGA HUGE T.A.S ISSUANCE. AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A MUCH MUCH LOWER 1696 T.A.S CONTRACTS THAN LAST MONDAY’S ISSUANCE OF 22,678. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. HOWEVER JULY IS HUGE FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 1.4618 TONNES QUEUE JUMP = 32.096 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 32.096 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 10+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 232 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3751 EFP CONTRACT WAS ISSUED: : /AUGUST 3751 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3751 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY

ZERO NET SPEC LIQUIDATION WITH OUR STRONG GAIN IN PRICE

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY MORNING/MONDAY NIGHT WAS A FAIR SIZED 1696 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST FRIDAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.THIS WAS SURELY IN EVIDENCE IN TRADING LAST FRIDAY DESPITE OUR SMALL GAIN IN PRICE DURING THE RAID PORTION IN TRADING WHICH ENDED IN TOTAL FAILURE. THAT SET UP YESTERDAY’S (MONDAY) HUMONGOUS GAIN IN PRICE IN GOLD AND SILVER AND A CORRESPONDING MASSIVE BUILDUP OF COMEX OI.

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 1.4618 TONNES QUEUE JUMP = 32.096 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE 40.30/ /) AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A MASSIVE HUMONGOUS SIZED GAIN IN OI FROM TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION ////MONDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE MEGA MEGA T.A.S. ISSUANCES, LAST WEEK , IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS.

TUES MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE GAINED A MEGA HUMONGOUS SIZED TOTAL OF 88.08 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 47,000 OZ OR 1.4618 TONNES OF GOLD//NEW STANDING ADVANCES TO 32.096 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $40.30

WE HAD A MAMMOTH XXXX CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 28319 CONTRACTS OR 2,831,900 0Z (88.08 TONNES)

2 ENTRIES i) Into HSBC 210,624.226 oz ii) Into HSBC enhanced 53,292.125 oz

(133 London good delivery bars)

total deposit: 263,916.35 oz

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

346 notice(s) 34,600 OZ 1.076 TONNES

No of oz to be served (notices)

109 contracts 10,900 OZ 0.3390 TONNES

Total monthly oz gold served (contracts) so far this month

10,251 notices 1,025,100 oz 31.884 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 1 entry

1 ENTRY

Loomis: 32,015.330 oz

total deposit: 32,015.330 oz

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

2 ENTRY

i) Into HSBC 210,624.226 oz ii) Into HSBC enhanced 53,292.125 oz

(133 London good delivery bars)

total deposit: 263,916.35 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entry

adjustments: 1

a) JPMorgan dealer to customer 8069.86 oz (251 kilobars)

AMOUNT OF GOLD STANDING FOR JUNE

THE FRONT MONTH OF JULY STANDS AT 455 CONTRACTS FOR A LOSS OF 351 CONTRACTS. ON MONDAY WE HAD 392 NOTICES FILED, SO WE GAINED A FAIR SIZED 41 CONTRACTS OR 4,100 OZ (0.1275 TONNES) ENTERTAINED WITH A QUEUE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD

AUGUST SHOCKINGLY GAINED 3344 CONTRACTS UP TO 215,738 AS AUGUST BECOMES THE FRONT MONTH AND IT’S OI IS VERY HIGH AND NOT CONTRACTING ENOUGH. WE WILL PROBABLY HAVE A HUGE NUMBER OF TONNES STANDING. WE HAVE ONLY 7 MORE TRADING DAYS BEFORE FIRST DAY NOTICE JULY 31.

SEPT GAINED 170 CONTRACTS TO 1755

We had 346 contracts filed for today representing 34,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 346 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 77 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (10,251 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (455 CONTRACTS) minus the number of notices served upon today (346 x 100 oz per contract) equals 1,036,000 OZ OR 32.223 TONNES to which we add 0 tonnes of gold issued under exchange for risk// total standing 32.223 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (10,251 x 100 oz +we add the difference for front month of JULY (455 OI} minus the number of notices served upon today (346 x 100 oz) which equals 1,036,900 OZ OR 32.223 TONNES + 0 tonnes EX FOR RISK = 32.223 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 32.223 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

i) out of De;aware 1997.844 oz ii) Out of Loomis 599,960.200 oz

total withdrawal: 609,958.046 oz

ADJUSTMENTs 1

customer to dealer; Brinks

49,373.400 oz

TOTAL REGISTERED SILVER: 195.863 MILLION OZ//.TOTAL REG + ELIGIBLE. 497.984 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 92 OPEN INTEREST CONTRACTS FOR A GAIN OF 11 CONTRACTS. WE HAD 49 CONTRACTS SERVED ON MONDAY SO WE GAINED 60 CONTRACTS OR 300,000 OZ ENTERTAINED A QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST LOST 161 CONTRACTS TO 2,191 AS THIS MONTH BECOMES THE FRONT MONTH FOR SILVER

SEPTEMBER GAINED 1371 CONTRACTS UP TO 129,717 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:59 or 0.295 MILLION oz

CONFIRMED volume; ON MONDAY 54,553 poor//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 9198 X5,000 oz = 45.990 MILLION oz

to which we add the difference between the open interest for the front month of JULY (92) AND the number of notices served upon today (59 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (9198) Notices served so far) x 5000 oz + OI for the front month of JULY(92) minus number of notices served upon today (59)x 5000 oz equals silver standing for the JULY contract month equating to 46.155 MILLION OZ .

New total standing: 46.155 million oz which is huge for this active delivery month of JULY. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 195.863 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/497.984 million. 42.25%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

JUNE 20 WITH GOLD DOWN $19.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 947.37 TONNES

JUNE 18 WITH GOLD UP $1.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.03 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 945.94 TONNES

JUNE 17 WITH GOLD DOWN $9.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 941.93 TONNES

JUNE 16 WITH GOLD DOWN $33.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.758 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 940.49 TONNES

JUNE 13 WITH GOLD UP $53.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.38 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 932.91 TONNES

JUNE 12 WITH GOLD UP $55.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 934.19 TONNES

JUNE 11 WITH GOLD UP $1.10 TODAY// SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.31 TONNEES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 935.91 TONNES

JUNE 10 WITH GOLD DOWN $11.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.02 TONNEES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 936.22 TONNES

JUNE 9 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.45 TONNEES OF GOLD FROM THE GLD//: /// ///INVENTORY RESTS AT 934.20 TONNES

JUNE 6 WITH GOLD DOWN $28.00 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

GLD INVENTORY: 943.63 TONNES, TONIGHTS TOTAL

SILVER

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

JUNE 20 WITH SILVER DOWN $0.83/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.818 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 474.641 MILLION OZ.

JUNE 18 WITH SILVER DOWN $0.20/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 17 WITH SILVER UP $0.67/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 473.096 MILLION OZ.

JUNE 16 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.727 MILLION OZ FROM THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 13 WITH SILVER UP $0.11/NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 473.550 MILLION OZ.

JUNE 12 WITH SILVER UP $0.11/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.276 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 473550 MILLION OZ.

JUNE 11 WITH SILVER DOWN $0.45/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.046 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.274 MILLION OZ.

JUNE 10 WITH SILVER DOWN $0.16/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.232 MILLION OZ.

JUNE 9 WITH SILVER UP $0.69/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.914 MILLION OZ.

JUNE 6 WITH SILVER UP $0.63/HUGE CHANGES AT THE SLV:A DEPOSIT OF 3.863 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.732 MILLION OZ. (A TOTAL DEPOSIT OF 11.856 MILLION PHANTOM OZ IN THE LAST 4 DAYS)

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

If Donald Trump has his way and recent reports are accurate, Federal Reserve Chair Jerome Powell is considering stepping down from his position. While extremely rare, Fed Chairs resigning before the end of their term isn’t entirely unheard of. Powell’s obligations would ordinarily extend to May 2026.

But if he abdicates, Trump would replace him with an ultra-dove who is committed to aggressively cutting short-term interest rates, delivering the cheap money he craves. This new dove will crush the dollar, eviscerate savers, and send long-term interest rates soaring much higher.

Markets are watching Powell closely, and pundits are speculating on who might replace him in the extraordinary event that he decides to leave the Fed. But even if he doesn’t resign, the end result of central bankers tinkering with the economy is always net inflationary. Whether you’re talking about the Fed or the Bank of Japan, the end result on a long enough timeline is always an expanded money supply, a currency crisis, and a reset driven by economic catastrophe.

The Fed Funds rate is 4.25%–4.5%. Trump said it should be 1.25%–1.5%. Rumors are that Powell may resign by Monday, so his replacement can slash rates to that level. This would put the nail in the dollar's coffin, sending long-term interest rates, consumer prices, & gold soaring.

In today’s low rate-addicted economy, 5% and up is considered being on the “high” end. In a self-correcting free market, they would be drastically higher. Forcing low interest rates on the economy is like trying to keep a greased beach ball underwater, pushing it deeper and deeper as it continues inflating with even more air.

You’re not in control, and you never were. When you finally lose your grip, it rockets out of the surface of the pool even harder and faster.

What makes the dollar different is its exorbitant privilege as the world reserve currency, and our ability to force that reality economically and geopolitically. But that privilege has been ending for many years in slow motion, and now, economic policies like capricious tariffs and “Big, Beautiful Bills” are accelerating its demise. Touted as a form of economic stimulus, Trump’s economic policies mean higher deficits.

Debt skyrockets, interest rates remain too low, deficits remain sky-high, growth remains low, and the cycle receives more and more fuel until something inevitably finally breaks the market’s trust. That’s when it all falls apart. Both Trump’s fiscal policy and Federal Reserve monetary policy, with or without Powell, are partners in crime for an economic crash.

“We are not changing course, we are headed on a course to a fiscal disaster. And we’re not veering from that course…we’re just stepping on the gas.”

Claims that the BBB’s spending will be magically funded by tariff revenues are nonsense. Tariffs will reduce demand for those goods, meaning the real revenue collected is always drastically lower than what hopeful projections like to pretend. Companies aren’t all going to pack up and move their manufacturing to the US, they’ll just stop selling to Americans. At absolute best, any companies that do move their manufacturing will take years, compromising Trump’s political dependence on instant results.

Despite a surprisingly good fiscal quarter for the US Government, the BBB makes it unlikely to last. We can rely on both Republican and Democrat administrations to be much better spenders than savers. When the government spends, it’s always with someone else’s money, and over 14% of that spending is just interest on the debt.

The Big, Beautiful Bill contains 1,116 pages, yet not a single page reduces future deficits. In fact, they make them larger. Only two House Republicans had the courage to vote against this monstrosity, @RepThomasMassie and @Rep_Davidson. The bill is a total fraud and a betrayal.

With or without the fiscal policies, inflation is all central bankers really know how to do. Sometimes they inflate slowly, at what they claim is the ideal 2% level, and sometimes they inflate a lot all at once, like in response to the 2008 financial crisis and COVID. The impact of monetary policy on ordinary Americans isn’t apparent right away. But eventually, the devastating effects of inflation are felt in the form of higher prices for everything people need to survive.

In the meantime we’re left with a boom and bust cycle where central bankers decide the “right time” to engineer a recession to try and stave off an all-out collapse. They always return to low interest rates and money printing because without them, the easy money-addicted system would collapse.

If Powell remains the Fed Chair, rate cuts will still come. It’s a matter of If, not When. But if he resigns, and is replaced with a dove hand-picked by Trump, inflation won’t just start to boil over —it will rocket into the stratosphere.

2. MATHEW PIEPENBERG

ALASDAIR MACLEOD

3. CHRIS POWELL AND GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 232

5. COMMODITY REPORT…gold

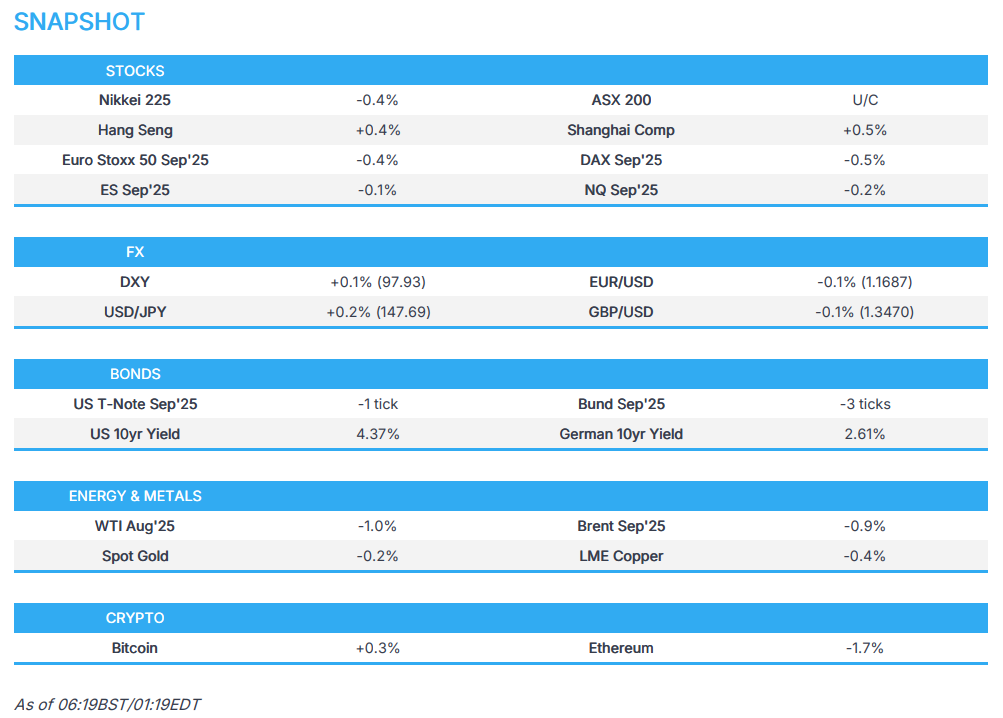

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 22.07 PTS OR 0.62%

//Hang Seng CLOSED UP 97.24 PTS OR 0.39%

// Nikkei CLOSED DOWN 44.19 PTS OR .11% //Australia’s all ordinaries CLOSED UP 0.17%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1741 OFFSHORE CLOSED UP AT 7.1773/ Oil UP TO 66.88 dollars per barrel for WTI and BRENT UP TO 68.24 Stocks in Europe OPENED MOSTLY ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1741 AND STRONG//OFF SHORE YUAN TRADING UP TO 7.1773 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1741 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1773 (CCP MANIPULATED)

SHANGHAI CLOSED UP 22.07 PTS OR 0.62%

HANG SENG CLOSED DOWN 97.24 PTS OR 0.39%

2. Nikkei closed DOWN 44.19 PTS OR .11%

3. Europe stocks SO FAR: MOSTLY ALL RED

USA dollar INDEX UP TO 97.71/ EURO RISES TO 1.1685 DOWN 9 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.504//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.84…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6200/Italian 10 Yr bond yield UP to 3.494 SPAIN 10 YR BOND YIELD UP TO 3.229%

3i Greek 10 year bond yield UP TO 3.329

3j Gold at $3384.70 Silver at: 38.88 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 24 /100 roubles/dollar; ROUBLE AT 77.95

3m oil (WTI) into the 66 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.84// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.504% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7980 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9326 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.385 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.958 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.863 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.42

10 YR UK BOND YIELD: 4.6290 UP 1 PTS

10 YR CANADA BOND YIELD: 3.519 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 3.041 DOWN 0 PTS

2a New York OPENING REPORT

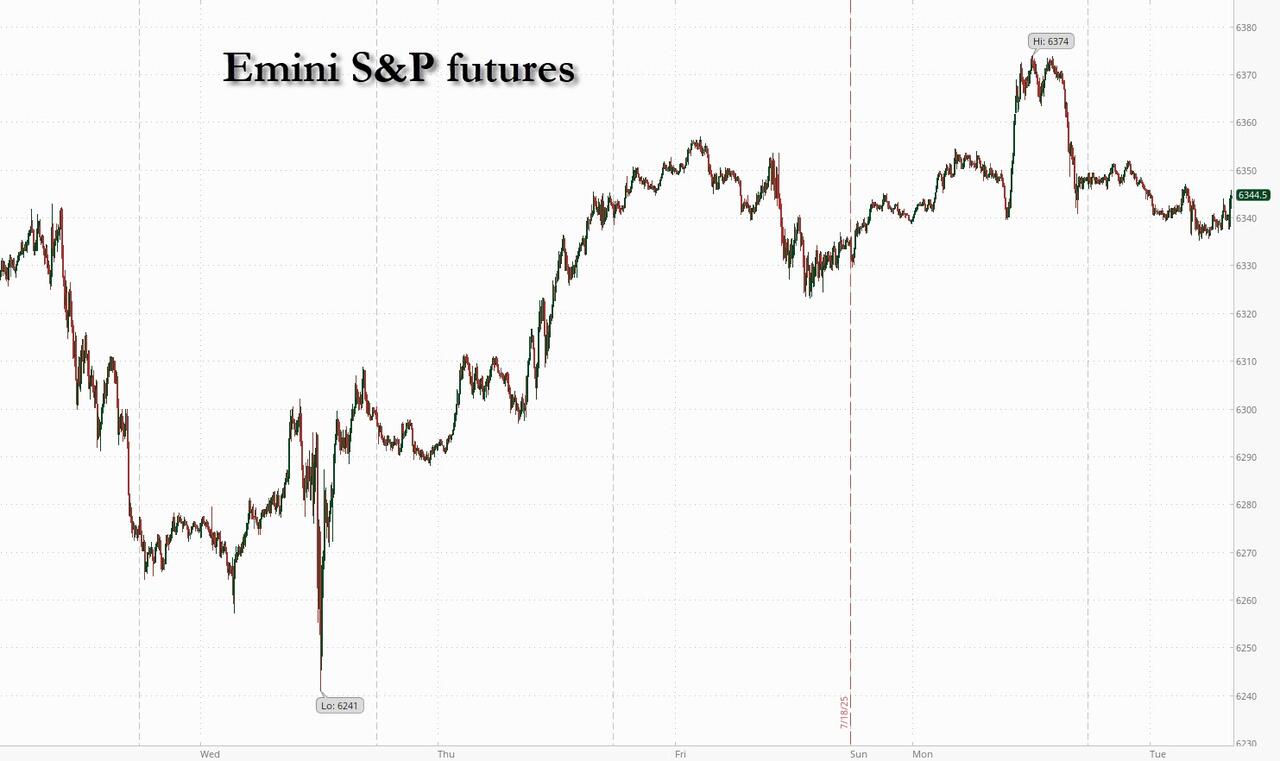

Futures Rally Pauses At All Time High With Mag7 Earnings On Deck

Tuesday, Jul 22, 2025 – 08:29 AM

US equity futures are trading flat, erasing an earlier loss following record highs in both the S&P and Nasdaq while the small cap Russell 2000 sits 8.5% below its ATH. As of 8:00am ET, S&P futures are unchanged while Nasdaq futures are down 0.1% as investors brace for corporate news on how tariffs are filtering through to their earnings. In pre-market trading Mag7 names are mixed with AAPL, GOOG, and META higher and NVDA pulling semis lower. Cyclicals are weaker with Industrials outperforming. Treasuries and the dollar steadied before an 830am speech from Fed Chair Jerome Powell in which he is not expected to discuss monetary policy. Powell has faced relentless criticism from the Trump administration, mostly over decisions to hold interest rates steady so far in 2025. The yield curve is seeing a slight twist steeper with 10s and 30s +1bp; USD is modestly lower after yesterday seeing its largest daily decline since June 12. Commodities are weaker with Energy/precious lower, base metals higher, and Ags mixed. Today’s macro data focus is on regional Fed activity indicators.

In premarket trading, Mag7 stocks are mixed (Alphabet +0.4%, Meta +0.3%, Apple +0.2%, Amazon +0.09%, Microsoft is little changed, Tesla -0.2%, Nvidia -0.6%). Here are some other notable premarket movers:

Calix (CALX) rises 3% after the communication software company reported second-quarter results that beat expectations and gave an outlook that is seen as strong.

Circle Internet Group (CRCL) falls 2% after the stablecoin issuer was downgraded to sell from neutral at Compass Point Research & Trading LLC as it sees more competition for Circle now that the US stablecoin bill has passed.

CSX (CSX) rises 4% after Semafor reported that Berkshire Hathaway-owned BNSF is working with Goldman Sachs to explore a takeover of a rival. It wasn’t immediately clear whether BNSF has its eye on Norfolk Southern or CSX, report says.

Danaher (DHR) slips 1% after the company reported operating loss in its life sciences unit for the second quarter, surprising analysts who’d forecasted a profit.

D.R. Horton (DHI) gains 6% after the homebuilder narrowed its revenue forecast for the full year.

General Motors Co. (GM) falls 3% after second-quarter profit fell as President Donald Trump’s tariffs on foreign-made vehicles and parts chopped $1.1 billion from adjusted earnings.

Medpace (MEDP) gains 44% after the clinical research company raised its sales and profit guidance.

Norwegian Cruise Line Holdings Ltd. (NCLH) climbs 1% after receiving a bullish initiation from TD Cowen, which added the cruise operator to its top picks ahead of the the Florida-based company’s earnings next week.

NXP Semiconductors (NXPI) falls 6% after the chipmaker issued a third-quarter revenue forecast that missed some bullish analysts’ estimates.

Sarepta Therapeutics (SRPT) falls 2%, on course to extend losses into a third session, as Barclays downgrades the stock to equal-weight from overweight. Separately, the drugmaker said it will temporarily pause shipments of Elevidys, its gene therapy to treat Duchenne muscular dystrophy, reversing its prior stance.

Sherwin-Williams (SHW) drops 3% after the paint company cut its adjusted earnings per share guidance for the full year.

Shopify’s US-listed shares (SHOP) fall 2.7% after Loop Capital Markets cut its recommendation on the stock to hold from buy, citing valuation concerns.

In earnings, NXP Semiconductors gave a less bullish third-quarter forecast than some investors had anticipated, while Steel Dynamics second-quarter adjusted EPS missed.

A record-breaking stock rally has powered on in the face of growing uncertainty over trade negotiations ahead of the Aug 1 tariff deadline. But with valuations stretched, the strong second-quarter earnings season is failing to illicit much of a reaction from investors so far, as they wait for more concrete information on the tariff fallout.

“Of course we see beats, but that won’t tell us a huge amount about where we are going forward,” JP Morgan Asset Management Global Market Strategist Hugh Gimber told Bloomberg TV. “That’s where we are spending our energy on this earnings season, trying to gauge where the hit from tariffs will come through.”

After hitting a series of all-time highs, the S&P 500 is trading around 22 times expected 12-month profits. The S&P 500 hasn’t posted a 1% up or down day since late June. Reports from megacaps Tesla Inc. and Alphabet Inc. are due Wednesday.

Wall Street giants such as Invesco, Fidelity and JPMorgan Asset Management are leaning harder into the rally in risk assets. The high-octane wager is that while Trump is threatening to disrupt the economic order anew, he will step back from the brink.

The 50 global companies with the highest US sales exposure are now expected to post average earnings growth of 10% this year, down nearly 400 basis points from estimates at the start of the year, according to BI strategists. The 50 firms with the least US exposure have seen upward estimate revisions. Elsewhere, Goldman Sachs traders said chip stocks are the most crowded pocket of tech, if not the market, on AI enthusiasm.

On the trade front, President Donald Trump may issue more unilateral tariff letters before the tariff deadline, White House Press Secretary Karoline Leavitt said. More trade deals may also be reached before the deadline, she added. Philippine President Ferdinand Marcos Jr. will be the latest foreign leader eager to make a deal before the deadline when he visits Trump in the Oval Office later Tuesday. A team of US officials will visit India in the second half of August to hold talks on a bilateral trade deal, the Financial Express reported Tuesday.

Firms such as Invesco Ltd., Fidelity International Ltd. and JPMorgan Asset Management are leaning harder into the rally in risk assets. The high-octane wager is that while Trump is threatening to disrupt the economic order anew, he will step back from the brink.

European stocks are in the red amid a mixed batch of earnings as investors await the results of trade negotiations between Brussels and Washington. The Stoxx 600 is down 0.5%. Chemical and tech shares are lagging, while utilities and miners are gaining. Among individual stocks, Akzo Nobel falls after cutting its profit forecast for the year. Here are the biggest movers:

Norsk Hydro gains as much as 4.3%, the most since April, after reporting a solid set of second-quarter figures, according to analysts, with weakness in the Aluminum Metal arm offset by strength elsewhere, with a significant beat in its Energy division.

Compass Group gains as much as 8.9% after the catering and support services company lifted its full-year guidance and announced the acquisition of Dutch caterer Vermaat.

Centrica shares gain as much as 6.8%, most in five months, after the energy company agreed to take a 15% stake in the UK’s Sizewell C nuclear power plant.

GB Group shares rise as much as 4.8%, after the cybersecurity company reassured investors with in-line trading during the first quarter following disappointing annual results back in June.

Greencore Group shares jump as much as 9.3%, trading at their highest level since January 2020, after the food manufacturer lifted its profit outlook for the year.

Akzo Nobel shares fall as much as 5.3%, the most since early April, with Morgan Stanley analysts calling it a “disappointing set of results” with pricing/mix coming in below their expectations.

Lindt & Spruengli shares fall as much as 5.8%, after the chocolate maker reported weaker-than-expected volume growth and first-half earnings missed estimates amid soaring cocoa prices.

Givaudan shares drop as much as 7.2%, the most in over three months, after like-for like sales missed in the second quarter.

Sartorius shares drop as much as 7.9%, the most since April 7, after the German lab equipment maker reported results for the second quarter.

Kier drops as much as 8.6%, snapping a run of four straight gains, after the UK construction company announced that CEO Andrew Davies will retire at the end of October.

Asker Healthcare falls as much as 6.4%, the most since April, after reporting its first earnings since its listing on Stockholm in March.

Alfa Laval shares fall as much as 5.3%, the most since April, after the Swedish industrial group reported earnings.

TietoEVRY falls as much as 8.4%, the most since February, after the Finnish software and services firm reported “another soft quarter,” according to Morgan Stanley.

A key Asian stock benchmark erased a gain and dipped, weighed down by losses in South Korean and Taiwanese chipmaker shares. The MSCI Asia Pacific Index fell as much as 0.5%, set for its first decline in four sessions. Taiwan Semiconductor Manufacturing and Samsung Electronics were the biggest drags. Lenders in Australia weighed down the index further ahead of the earnings season. South Korean stocks retreated from near an all-time high ahead of this week’s tariff talks with the US and upcoming earnings releases. Japanese shares had a volatile session as investors weighed policy implications from the ruling Liberal Democratic Party’s historic setback in Sunday’s elections. Prime Minister Shigeru Ishiba’s plan to remain in his role alleviated some worry of a sudden upheaval, though uncertainty has risen over the stability of his government. Among other nations hoping for positive trade talks, Malaysia is said to be seeking a milder US tariff rate of 20%, while Philippine President Ferdinand Marcos Jr. plans to meet with President Donald Trump later Tuesday. Elsewhere, Thailand is set to name its new central bank chief on Tuesday, ending a months-long search.

In FX, the dollar kicked off the day stronger but has seen that fade. The Bloomberg Dollar Spot Index is now down for the day after having yesterday seeing its largest daily decline since June 12. The New Zealand dollar is the worst G-10 performer after seeing first quarterly decline in exports for two years, and the yen continues its wild gyrations as markets are in denial over the coming fiscal easing tsunami that will send the currency tumbling.

In rates, Treasuries are under slight pressure as US trading day begins, after Monday’s rally sent yields across tenors to lowest levels in more than a week. 10- to 30-year yields are higher by 1bp-2bp with shorter-maturity tenors little changed; the 10-year near 4.39% is back above the 200-day moving average level it dipped below Monday and hasn’t closed below since July 2. Potential catalysts are in short supply as the US economic calendar is light and Fed policymakers are in self-imposed external communications blackout ahead of their July 29-30 meeting, however Chair Powell is slated to give welcoming remarks at a regulatory conference in Washington at 8:30am, and Governor Michelle Bowman, the Fed’s vice chair for supervision, is slated to appear on CNBC at 7:30am. UK bonds are falling after the country’s budget deficit hit the highest since April 2021. The yield on 10-year gilt bonds is up four basis points, lagging comparable Treasuries and bunds, where their respective yields are each up by a basis points.

Oil is falling, with tariff worries and supply concerns the culprits. Brent futures down 1.1% and below $69/barrel. Gold weaker, down around $8 to about $3,388/oz.

In commodities, oil fell for a third session, and gold slipped. Iron ore headed toward the highest in nearly five months as traders eyed China’s prospective supply-side reforms for the steel industry and plans for a massive dam project

The US economic data calendar includes July Philadelphia Fed non-manufacturing activity (8:30am) and July Richmond Fed manufacturing index and business conditions (10am). Fed officials are in external communications blackout ahead of their July 30 rate decision, anticipated to be no change in the fed funds target range of 4.25%-4.5%

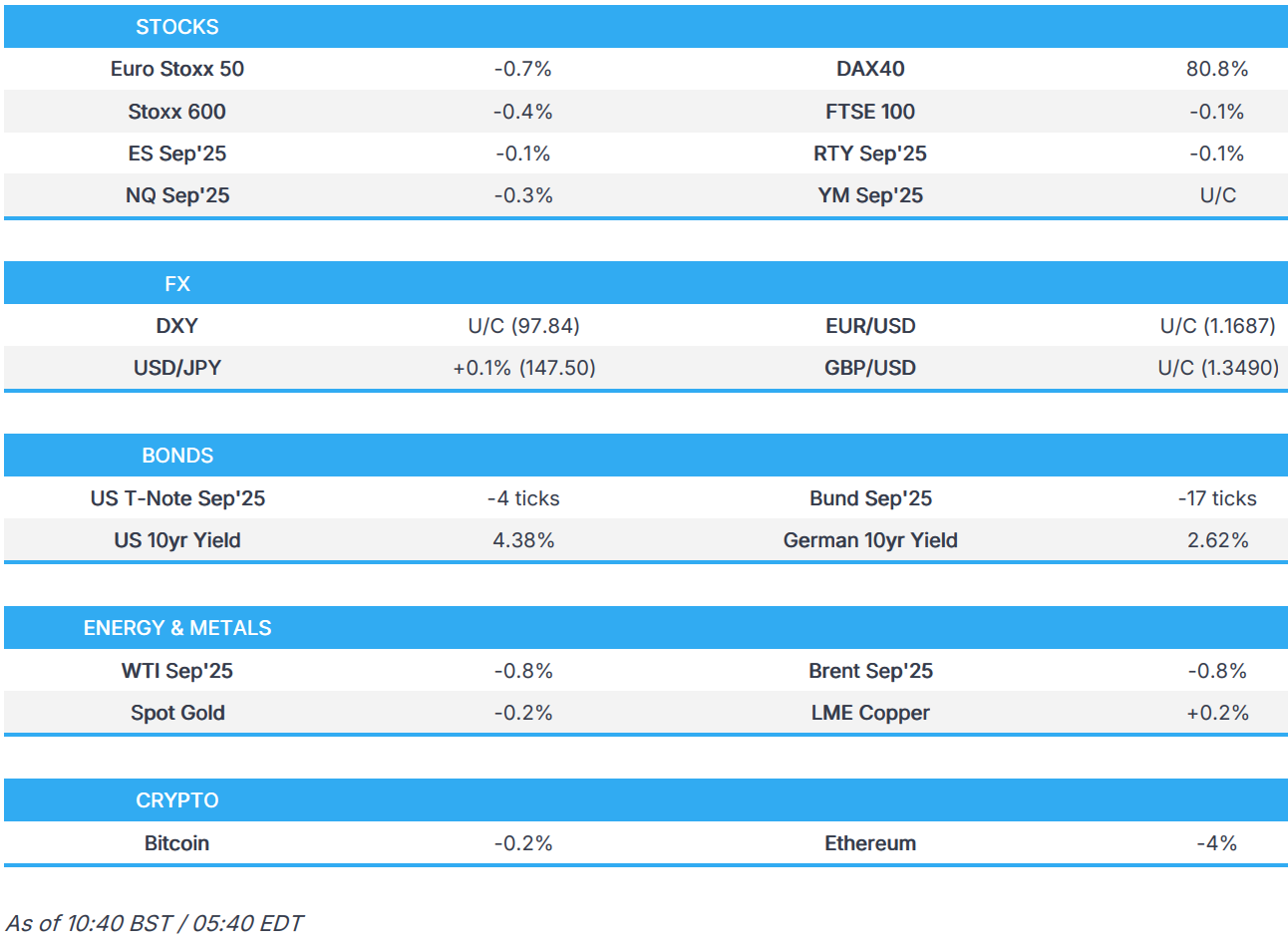

Market Snapshot

S&P 500 mini -0.1%

Nasdaq 100 mini -0.3%

Russell 2000 mini -0.1%

Stoxx Europe 600 -0.4%

DAX -0.8%, CAC 40 -0.5%

10-year Treasury yield +1 basis point at 4.39%

VIX +0.3 points at 16.95

Bloomberg Dollar Index little changed at 1200.52

euro little changed at $1.1701

WTI crude -1.1% at $66.47/barrel

Top Overnight News

Scott Bessent called for a review of the Fed’s HQ renovation, urging the central bank to also scrutinize its non-monetary policy operations. He warned of “significant mission creep.” BBG

SoftBank and OpenAI’s $500bln AI project struggles to get off the ground with the Stargate venture, introduced at a White House event earlier this year, now setting a more modest goal of building a small data centre by year-end: WSJ.

Trump’s targeting of trade loopholes would threaten 70% of China’s US exports and more than 2.1% of GDP. BBG

The prospects of an interim trade deal between India and the United States before Washington’s August 1 deadline have dimmed, as talks remain deadlocked over tariff cuts on key agricultural and dairy products. RTRS

A growing number of European Union member states, including Germany, are considering using wide-ranging “anti-coercion” measures targeting U.S. services if the EU cannot reach a trade deal with U.S. President Donald Trump

Japan’s chief trade negotiator Ryosei Akazawa spoke with Howard Lutnick for two hours yesterday to discuss a tariff agreement. BBG

Bank of Japan officials see little need to shift their policy stance of gradually raising interest rates in the wake of Prime Minister Shigeru Ishiba’s latest election setback. BBG

France urges Brussels to take a more confrontational approach to trade talks w/Washington. Politico

The UK borrowed billions more than forecast in June as a surge in debt-interest payments sent the budget deficit to £20.7 billion. BBG

GM’s second-quarter profit fell as Trump’s tariffs chopped $1.1 billion from earnings. Shares retreated -285 bps premarket. Goldman thinks positioning was longer and thinks expectations were for lower tariff impact. Details: EPS beat ($2.53x vs. $2.34 cons) on Q2 net sales of $47bn (slightly above $46bn cons). BBG

Trade/Tariffs

Canadian PM Carney issued a statement following a meeting with US Senators and stated they discussed work to strengthen continental defence and security, as well as Canada’s successes in dismantling illegal drug smuggling and securing the border.

Canada’s Minister of Intergovernmental Affairs Leblanc will be in Washington this week for trade discussions.

Japan’s tariff negotiator Akazawa and US Commerce Secretary Lutnick met for over two hours in Washington on Monday and held frank talks to seek agreement benefiting both Japan and the US, while Japan will continue to seek common ground on tariff issues with the US, according to the Japanese government.

South Korean Finance Minister Koo said he will hold trade talks with his US counterpart on July 25th, while Koo added that the Foreign Minister and Industry Minister will conduct meetings with US counterparts as soon as possible.

India and US mini trade deal is ruled out before August 1st, according to CNBC TV18, citing sources.

India-US trade deal prospects are dim ahead of the August 1st deadline, sides remain deadlocked over ags and dairy products, according to Reuters sources.

Malaysia has been asked by the US to extend tax exemptions for US EVs, while Malaysia is seeking a 20% US levy, but is said to be resisting EV and ownership demands, according to Bloomberg.

“Chinese experts warned that if the US attempts to weaponize trade talks and tariffs…Beijing will not yield to the pressure. Such moves would also risk undermining the trade negotiation mechanism between the two countries”, via Global Times.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed after failing to sustain the early upward momentum seen at the open following the fresh record intraday highs on Wall St and with two-way price action seen in Japan following the ruling coalition’s upper house election loss. ASX 200 was rangebound as strength in the mining, materials, resources and healthcare sectors offset the losses in financials, energy and industrials, while the RBA Minutes from the July meeting provided very little to shift the dial but continued to signal future cuts ahead. Nikkei 225 initially surged to above the 40,000 level as participants returned from the long weekend, but then wiped out its gains and then some, as participants second-guessed the ramifications of the ruling coalition’s upper house election setback. Hang Seng and Shanghai Comp kept afloat in rangebound trade amid a lack of major fresh catalysts and after the Hong Kong benchmark breached the 25,000 level.

Top Asian News