JULY 24/GOLD DOWN $17.30 TO $3371.50 WITH SILVER DOWN ONLY 11 CENTS TO $39.05//PLATINUM WAS DOWN $14.25 TO $1409.10 AND PALLADIUM WAS DOWN $28.35 TO $1240.95//LEASE RATES CONTINUE TO BE HIGH FOR PLATINUM AND SILVER INDICATING SCARCITY//GOLD COMMENTARIES TONIGHT FROM JOHN RUBINO AND ALASDAIR MACLEOD//GERMAN ECONOMY CONTINUES TO FALTER AND YET BRUSSELS GETS ITS TRIBUTE MONEY//ISRAEL ET AL SUMMARY PROVIDED/ISRAEL VS IRAN: IRAN DROUGHT WORSENS AND THAT WILL BE DANGEROUS TO IT//ISRAEL VS WEST BANK/RUSSIA VS UKRAINE/COVID UPDATES/VACCINE INJURY REPORT//NEWSWIZE AND NEWS ADDICTS/EVOL NEWS/RABOBANK COMMENTS ON THE DAILY EVENTS//OIL IS DISCUSSED//USA DATA RELEASES//TULSI GABBARD RELEASES MORE DOCUMENTS NAILING THE CRIMINAL DEEP STATE OF OBAMA AND COMPANY/SWAMP STORIES FOR YOU TONIGHT//

Here it is… it is the first photograph in history in which man appears in front of the camera.

This photograph is the first in which a person appears in front of the camera and is also the first photo of the city of Paris. The used camera needs about 5 minutes to collect the light and scene. The street was full of people, but as they moved during the shot they failed to impress themselves in the photo except for one person who stopped for a few minutes to shine his shoes and history immortalized him. It was the year 1839.

*CANADIAN GOLD: $4,597.24 DOWN 3.60 CDN dollars per oz( * NEW ALL TIME HIGH $4735.70 CDN DOLLARS PER OZ//APRIL 21 2025)

*BRITISH GOLD: 2494.80 DOWN 1.60 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//2,566.50 BRITISH POUNDS/OZ) MAY 6/2025

*EURO GOLD: 2865.81 DOWN 13.40 Euros per oz //* (ALL TIME CLOSING HIGH: 3018.80 EUROS PER OZ/ APRIL 21 //2025)

EXCHANGE: COMEX

ZERO

JULY

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 0 CONTRACTs NOTICES FOR 0 OZ or 0. TONNES

total notices so far: 10,261 contracts for 1,026,100 OR 31.916 tonnes)

FOR JULY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 25 NOTICE(S) FILED FOR 0.125 million OZ/

total number of notices filed so far this month : 9255 CONTRACTS (NOTICES) for 46.275 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $17.30 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 954.80 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.11 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ///A FRAUDULENT CRIMINAL DEPOSIT OF 1.589 MILLION OZ INTO THE SLV///

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 488.942 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 580 CONTRACTS TO 174,253 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL GAIN OF $0.04 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE FINALLY ARE MOVING MUCH HIGHER THAN THE BASE $34.40 SILVER PRICE BARRIER. WE HAD A STRONG SIZED GAIN OF 680 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL 100 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO WEDNESDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $36.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON WEDNESDAY WITH SILVER’S SMALL GAIN IN PRICE. THE PRICE FINISHED MILES ABOVE THE MAGIC NUMBER OF $36.00 SILVER SPOT PRICE CLOSING AT $39.16 . WE HAVE A STRONG T.A.S. ISSUANCE AT 490 CONTRACTS ISSUED BY THE CME AND THAT STILL SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 38.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A SMALL 100 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR FAIR SIZED 490 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY’S ATTEMPTED RAID// TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A STRONG SIZED 680 CONTRACTS ON OUR TWO EXCHANGES WITH OUR TINY GAIN IN PRICE OF $0.04.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A STRONG SIZED 490 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.04) AND WERE UNSUCCESSFUL IN KNOCKING OF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HADE A STRONG GAIN OF 680 CONTRACTS ON OUR TWO EXCHANGES WITH ZERO T.A.S. SPREADER LIQUIDATION AND ZERO MONTHLY SPREADER LIQUIDATION..

WE HAD A 100 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 34.730 MILLION OZ PLUS TODAY’S GOOD SIZED QUEUE JUMP OF 155,000 OZ//NEW STANDING ADVANCES TO 46.450 MILLION OZ

THUS:

INITIAL STANDING FOR JULY: 46.450 MILLION OZ INCLUDING QUEUE JUMPS

WE HAD:

/ HUGE COMEX OI GAIN+// A SMALL SIZED EFP ISSUANCE 100 CONTRACTS (/ VI) A STRONG NUMBER OF T.A.S. CONTRACT ISSUANCE 490 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 250 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 17 DAY(S), total 7499 contracts: OR 37.495 MILLION OZ (441 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 37.495 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 37.495 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 580 CONTRACTS DESPITE OUR SMALL GAIN IN PRICE OF $0.04 IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. . THE CME NOTIFIED US THAT WE HAD A SMALL 100 CONTRACT EFP ISSUANCE CONTRACTS: 100 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 4 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.450 MILLION OZ//

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (490 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE IN THURSDAY’S RAID/ TRADING.

WE HAD 25 NOTICE(S) FILED TODAY FOR 0.125 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5,311 OI CONTRACTS TO 484,112 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 1664 CONTRACTS //.

WE HAD A STRONG DECREASE IN COMEX OI (5,311 CONTRACTS) . THIS OCCURRED WITH OUR LOSS OF $40.00 IN PRICE// TUESDAY///.

LAST THREE MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0.0342 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK = 33.847 TONNES STANDING

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4175 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 484,112 /NOW STILL AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 174,259 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1136 CONTRACTS WITH 5311 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4175 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1136 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED AND CRIMINAL 3531 CONTRACTS AND THESE ISSUANCES ARE JOINED WITH OUR MONTHLY SPREADER LIQUIDATION TO CREATE OUR RAID IN GOLD/.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(4175) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 5311 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 1136 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR JULY AT 17.947 TONNES COUPLED WITH TODAY’S 0.0342 TONNES QUEUE JUMP + 1.555 TONNES EX. FOR RISK//STANDING ADVANCES TO 33.847 TONNES.

NEW STANDING FOR GOLD, JULY CONTRACT AT 32.258 TONNES OF GOLD + 1.555 TONNES EX FOR RI.SK = 33.847 TONNES

.

/ 3) ZERO T.A.S. LIQUIDATION IN THE COMEX SESSION AS DESPITE HAVING 1)A $40.00 COMEX PRICE LOSS. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A FAIR LOSS OF 1136 CONTRACTS ON OUR TWO EXCHANGES COUPLED WITH CONSIDERABLE LIQUIDATION OF OUR TAS SPREADERS AND MONTHLY SPREADERS // /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4) STRONG SIZED COMEX OI GAIN// 5) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (4175 CONTRACTS)/// STRONG T.A.S. ISSUANCE: 3531 T.A.S.CONTRACTS

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 34,803 CONTRACTS OR 3,480,300 OZ OR 108.25 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 2047 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN17 TRADING DAY(S) IN TONNES 108.25 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 108.25 TONNES DIVIDED BY 3550 x 100% TONNES = 3.04% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

UNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 108.25 TONNES//STILL QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG SIZED 580 CONTRACTS OI TO 174,403 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 100 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 580 CONTRACTS AND ADD TO THE 100 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 680 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR SMALL GAIN IN PRICE OF $0.04 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 3.40 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

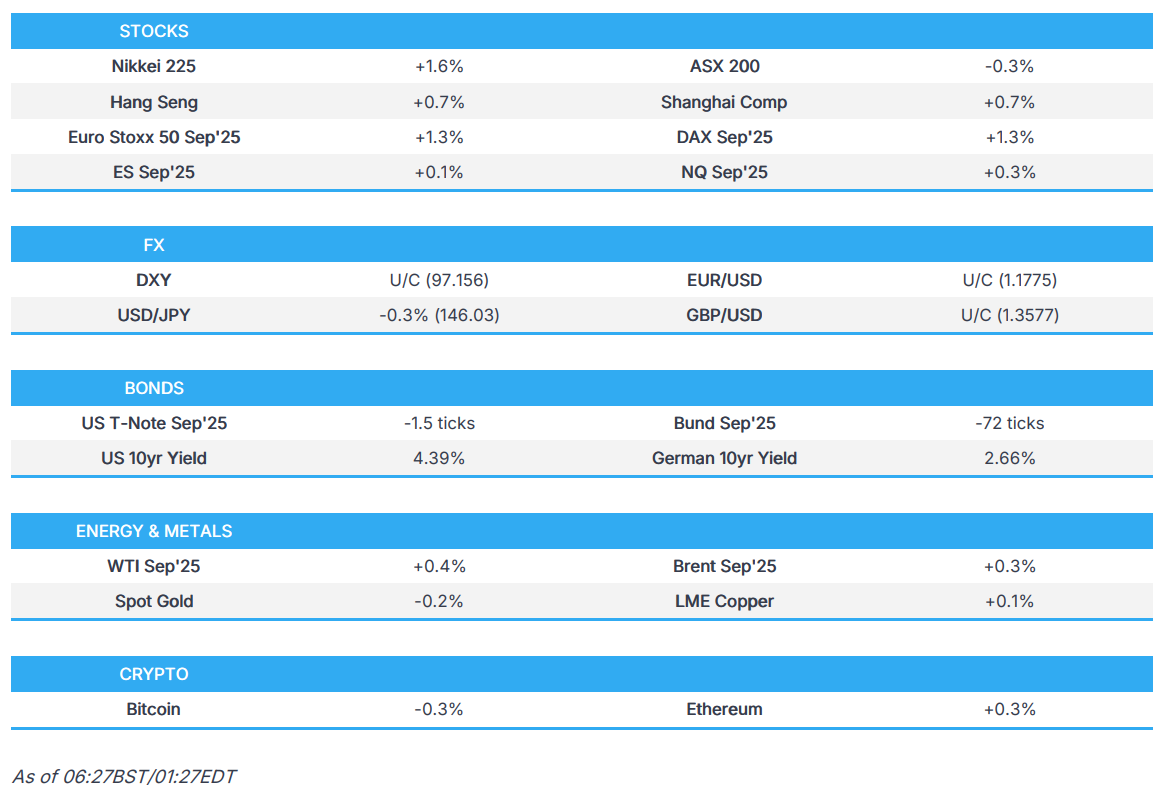

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED UP 0.44 PTS OR 0.01%

//Hang Seng CLOSED UP 358.71 PTS OR 1.43%

// Nikkei CLOSED UP 1396.40 PTS OR 3.51% //Australia’s all ordinaries CLOSED UP 0.67%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1614 OFFSHORE CLOSED UP AT 7.1599/ Oil DOWN TO 65.43 dollars per barrel for WTI and BRENT DOWN TO 68.43 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1614 AND STRONG//OFF SHORE YUAN TRADING UP TO 7.1599 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5,311 CONTRACTS TO 484,112 OI WITH OUR LOSS IN PRICE OF $40.00 WITH RESPECT TO WEDNESDAY’S // TRADING.. WE LOST LITTLE NUMBER OF NET LONGS, IF ANY, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4175 ). WE HAD CONSIDERABLE T.A.S. LIQUIDATION //WEDNESDAY TRADING AS WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1136 CONTRACTS.

YESTERDAY, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED TUESDAY NIGHT, A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. HOWEVER WEDNESDAY NIGHT ZER0 EXCHANGE FOR RISK WAS ISSUED AS THE BANK OF ENGLAND WAS NOW SATISFIED!

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A SMALL SIZED GAIN ON OUR TWO EXCHANGES OF 528 CONTRACTS WITH OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN LAST FRIDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE IN JANUARY(AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 3.5 TO 5% AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND NOW JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER FINALLY ENDS OUR MEGA MEGA HUGE T.A.S ISSUANCE WHICH COMMENCED EARLY LAST WEEK, AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A STRONG BUT MUCH LOWER 3531 T.A.S CONTRACTS THAN LAST MONDAY’S JULY 14, ISSUANCE OF 22,678. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT IS IN FULL FORCE WITH TODAY’S RAID DURING OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATION ARE JOINED WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES TO RAID THE GOLD/SILVER PRICE.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. NOW IN JULY WE HAVE HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 0.0342 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK = 33.842 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 33.842 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 10+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 232 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4175 EFP CONTRACT WAS ISSUED: : /AUGUST 5048 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4175 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS//WEDNESDAY AND THEY WERE JOINED BY OUR MONTHLY SPREADER LIQUIDATION

ZERO NET SPEC LIQUIDATION DESPITE OUR STRONG LOSS IN PRICE WITH OUR TOTAL GAIN IN OI ON OUR TWO EXCHANGES.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY WAS A STRONG SIZED 3531 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST FRIDAY OR TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.. THAT SET UP YESTERDAY’S (WEDNESDAY) HUMONGOUS LOSS IN PRICE IN GOLD AND SILVER AND A CORRESPONDING LIQUIDATION OF SOME COMEX OI. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH THE RARE ISSUANCE OF EXCHANGE FOR RISK!

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0.0342 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK = = 33.842 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $40.00/ /) AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED LOSS IN OI FROM TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION ////WEDNESDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE STRONG T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDED IN TOTAL FAILURE! LET US SEE WHAT HAPPENS WITH TODAY’S RAID

THURDAYS MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AN ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THS 32.096 TONNES + 1.55 TONNES EX FOR RISK = 33,651 TONNES OF GOLD

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE LOST A FAIR SIZED TOTAL OF 3.533 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 1100 OZ OR 0.0342 TONNES OF GOLD TO WHICH WE ADD THE CRAZY 1.555 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 32.292 TONNES + 1.555 TONNES EX FOR RISK = 33.847 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE TO THE TUNE OF $40.00

WE HAD A MAMMOTH 1664 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 1136 CONTRACTS OR 113,600 0Z (3.533 TONNES)

confirmed volume WEDNESDAY 356,044 contracts// very strong

1 ENTRY i) Into Brinks dealer: 96,453.000 oz 3000 kilobars

total dealer deposit 96,453.000 oz

3.00 tonnes

Deposits to the Customer Inventory, in oz

1 ENTRY i) Into Malca: 32,151.000 oz

1000 kilobars

total deposit 32,151.000 oz

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

0 notice(s) 0 OZ 0.0000 TONNES

No of oz to be served (notices)

121 contracts 12,100 OZ 0.3763 TONNES

Total monthly oz gold served (contracts) so far this month

10,261 notices 1,026,100 oz 31.916 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 1 entry

1 ENTRY i) Into Brinks dealer: 96,453.000 oz 3000 kilobars

total dealer deposit 96,453.000 oz

3.00 tonnes

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRY

1 ENTRY i) Into Malca: 32,151.000 oz

1000 kilobars

total deposit 32,151.000 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entry

adjustments: 1

Brinks; customer account to dealer 96,453.000 oz (3000 kilobars)

AMOUNT OF GOLD STANDING FOR JULY

THE FRONT MONTH OF JULY STANDS AT 121 CONTRACTS FOR A GAIN OF 1 CONTRACT. ON WEDNESDAY WE HAD 10 NOTICES FILED, SO WE GAINED A SMALL SIZED 11 CONTRACTS OR 1100 OZ (0.0342 TONNES) ENTERTAINED WITH A QUEUE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD

AUGUST LOST ONLY 30,798 CONTRACTS DOWN TO 177,138 AS AUGUST BECOMES THE FRONT MONTH AND IT’S OI IS VERY HIGH AND NOT CONTRACTING ENOUGH. WE WILL PROBABLY HAVE A HUGE NUMBER OF TONNES STANDING. WE HAVE ONLY 6 MORE TRADING DAYS BEFORE FIRST DAY NOTICE JULY 31.

SEPT GAINED 255 CONTRACTS TO 399

We had 0 contracts filed for today representing 0 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (10,261 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (121 CONTRACTS) minus the number of notices served upon today (0 x 100 oz per contract) equals 1,038,200 OZ OR 32.292 TONNES to which we add 1.555 tonnes of gold issued under exchange for risk// total standing 33.847 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (10,251 x 100 oz +we add the difference for front month of JULY (121 OI} minus the number of notices served upon today (0 x 100 oz) which equals 1,038,200 OZ OR 32.292 TONNES + 1.555 tonnes EX FOR RISK = 33.847 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 33.847 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

i) out of Delaware 1018.050 oz ii) Out of Loomis 600,007.480 oz

total withdrawal: 601,025.53 oz

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 195.863 MILLION OZ//.TOTAL REG + ELIGIBLE. 497.804 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 60 OPEN INTEREST CONTRACTS FOR A LOSS OF 1 CONTRACTS. WE HAD 32 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 31 CONTRACTS OR 155,000 OZ ENTERTAINED A QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST LOST 244 CONTRACTS TO 1,640 AS THIS MONTH BECOMES THE FRONT MONTH FOR SILVER

SEPTEMBER LOST 272 CONTRACTS DOWN TO 129,276 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:25 or 0.125 MILLION oz

CONFIRMED volume; ON WEDNESDAY 69,719 good//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 9255 X5,000 oz = 46.275 MILLION oz

to which we add the difference between the open interest for the front month of JULY (60) AND the number of notices served upon today (25 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (9255) Notices served so far) x 5000 oz + OI for the front month of JULY(60) minus number of notices served upon today (25)x 5000 oz equals silver standing for the JULY contract month equating to 46.450 MILLION OZ .

New total standing: 46.450 million oz which is huge for this active delivery month of JULY. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 195.863 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/497.804 million. 42.45%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

JUNE 20 WITH GOLD DOWN $19.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 947.37 TONNES

JUNE 18 WITH GOLD UP $1.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.03 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 945.94 TONNES

JUNE 17 WITH GOLD DOWN $9.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 941.93 TONNES

JUNE 16 WITH GOLD DOWN $33.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.758 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 940.49 TONNES

JUNE 13 WITH GOLD UP $53.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.38 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 932.91 TONNES

JUNE 12 WITH GOLD UP $55.75 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 934.19 TONNES

JUNE 11 WITH GOLD UP $1.10 TODAY// SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.31 TONNEES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 935.91 TONNES

JUNE 10 WITH GOLD DOWN $11.80 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.02 TONNEES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 936.22 TONNES

JUNE 9 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.45 TONNEES OF GOLD FROM THE GLD//: /// ///INVENTORY RESTS AT 934.20 TONNES

JUNE 6 WITH GOLD DOWN $28.00 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 5 WITH GOLD DOWN $23.10 TODAY// NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 4 WITH GOLD UP $22.30 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 935.65 TONNES

JUNE 3 WITH GOLD DOWN $19.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD. /// ///INVENTORY RESTS AT 933.07 TONNES

GLD INVENTORY: 954.80 TONNES, TONIGHTS TOTAL

SILVER

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

JUNE 20 WITH SILVER DOWN $0.83/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.818 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 474.641 MILLION OZ.

JUNE 18 WITH SILVER DOWN $0.20/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 17 WITH SILVER UP $0.67/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 1.273 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 473.096 MILLION OZ.

JUNE 16 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.727 MILLION OZ FROM THE SLV..////INVENTORY RESTS AT 471.823 MILLION OZ.

JUNE 13 WITH SILVER UP $0.11/NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 473.550 MILLION OZ.

JUNE 12 WITH SILVER UP $0.11/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.276 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 473550 MILLION OZ.

JUNE 11 WITH SILVER DOWN $0.45/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.046 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.274 MILLION OZ.

JUNE 10 WITH SILVER DOWN $0.16/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.232 MILLION OZ.

JUNE 9 WITH SILVER UP $0.69/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.182 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 472.914 MILLION OZ.

JUNE 6 WITH SILVER UP $0.63/HUGE CHANGES AT THE SLV:A DEPOSIT OF 3.863 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 471.732 MILLION OZ. (A TOTAL DEPOSIT OF 11.856 MILLION PHANTOM OZ IN THE LAST 4 DAYS)

JUNE 5 WITH SILVER UP $1.14/HUGE CHANGES AT THE SLV:A DEPOSIT OF 4.364 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 467.869 MILLION OZ.

JUNE 4 WITH SILVER DOWN $0.01/HUGE CHANGES AT THE SLV:A DEPOSIT OF 2.084 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 463.505 MILLION OZ.

JUNE 3 WITH SILVER DOWN $0.02/HUGE CHANGES AT THE SLV:A DEPOSIT OF 1.545 MILLION OZ INTO THE SLV/ ././///INVENTORY RESTS AT 461.421 MILLION OZ.

Japan, with its highest in human history per capita government debt, has been an accident waiting to happen for a long time. But somehow, it has always managed to slip out of whatever trap the financial markets set for it.

Until now?

Japanese interest rates have been rising, increasing government interest costs and leading traders to wonder if the Bank of Japan has lost control of the narrative:

Some headlines from just the past couple of weeks:

(Financial Post) – In 2008, Japan was the quiet stabilizer in an unravelling world. Its central bank was passive, its interest rates were near zero and its bond market quietly absorbed global capital. Fast forward to 2025, and Japan is no longer the ballast, it’s the epicentre of a potential sovereign debt crisis. And what’s happening there could soon ripple across the globe, especially into the U.S. Treasury market.

The quiet anchor is slipping

Japan’s government bond yields are rising at a pace not seen in decades. The 30-year Japanese Government Bond (JGB) recently breached 3.2 per cent, the highest level on record. The 10-year yield is now above 1.58 per cent, a level that would have been unthinkable just a few years ago.

But this isn’t a healthy normalization. It’s a structural repricing driven by a collapsing yen, rising energy costs, and a growing loss of confidence in the Bank of Japan (BOJ). The central bank’s long-standing policy of yield curve control is being overwhelmed by market forces. Investors are no longer waiting for the BOJ to lead; they’re setting the terms themselves.

Japan now faces a brutal policy bind: Defend the bond market and the yen collapses, or defend the yen and bond yields spike.

With a debt-to-GDP ratio exceeding 260 per cent, Japan’s fiscal math is already fragile. At the same time, as of mid-July 2025, the yen is trading near 150 yen to the U.S. dollar, its lowest level in more than 30 years. The most likely path forward is quiet intervention: stealth bond purchases, liquidity injections and vague reassurances. But the core issue remains: The BOJ no longer commands the market narrative.

Why this matters for the U.S.

Japan isn’t just another economy. It’s the largest foreign holder of U.S. Treasuries, with more than US$1.13 trillion in holdings. For decades, Japanese investors have been reliable buyers of U.S. debt, helping to keep American borrowing costs low. But that may be changing.

As yields rise at home and the yen weakens, Japanese investors are under pressure to repatriate capital and sell foreign bonds, including U.S. Treasuries, to invest domestically. This shift could have serious consequences:

Reduced demand for U.S. debt, especially at the long end of the curve.

Higher yields, as the Treasury struggles to attract buyers.

Increased volatility, as global capital flows realign.

In short, if Japan steps back from the U.S. bond market, America’s borrowing costs could rise sharply, just as its own fiscal challenges are mounting.

The end of the MMT era

This moment also marks a turning point for central banks more broadly. The era of Modern Monetary Theory (MMT) — the idea that governments can print money to fund spending without consequence — is effectively over. The Federal Reserve can no longer rely on unlimited bond buying to stabilize markets. The risks of inflation, currency devaluation, and loss of investor confidence are now too great. And Japan is giving the world a glimpse of what happens when debt levels become unsustainable and central banks lose control. The U.S. may not be far behind.

The GENIUS Act could be very good for gold, as I explain. And the anti-CBDC bill making its way through Congress will kill off the entire CBDC movement, not just in the US.

The GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins) establishes a legal framework for regulating stablecoins. Currently valued at a $240bn total, stablecoins are used in crypto payments, remittances, and cross-border payment solutions. Other uses are expected to evolve.

Let us be clear: with regulation comes respectability. The financial community will embrace GENIUS as a marketing opportunity, but perhaps not in a way you might think.

Clearly, the crypto market has grown rapidly, and nothing worries a government more than having an unregulated payment system. Having been in denial over crypto and CBDCs, the USG is now embracing reality, and the GENIUS act will be followed by further legislation; the Clarity Act (moving regulatory oversight of crypto away from the SEC and toward the Commodity Future Trading Commission [CTFC], and the Anti-CBDC Surveillance State Act which will ban the Fed from issuing its own CBDC.

It was only a matter of time before the USG legislated to bring cryptocurrencies under its control. And it is doing this by regulating payments.

Will GENIUS lead to more stablecoins?

We can also be sure that commercial banks support GENIUS, which can be expected to expand significantly in the coming years. The great thing, from both the banks and the government’s point of view, is that by legislating that a US$ stablecoin is fully backed by dollar cash and near-cash such as T-bills, minimal bank capital is required and US$ stablecoins could evolve into a significant source of short-term funding for the US treasury if future demand for stablecoins grows.

A bank can issue its own stablecoins alongside normal checking accounts, and delight of delights for the bank that is, GENIUS prohibits the payment of interest. By backing its stablecoins with T-bills, it creates a return currently of 4.35% on 3-month T-bills, with almost no expense. Instead of creating credit by lending money into existence, the bank acts as a bank of deposit.

No wonder banks like it. And no wonder the US treasury loves it too, given that selling long maturity bonds is challenging. But unlike expanding credit by lending it into existence, it is difficult to see who would take up a bank’s stablecoins, when perfectly good ones such as tether already exist.

In short, the theory is fine, but the reality is likely to disappoint. The prospects for pure currency stablecoins are tied to those of cryptos. Otherwise, they compete with conventional deposits. If JPMorgan issued its own $ stablecoins, this new activity would have to compete with JPMorgan’s dollar deposit accounts. And since its premium dollar-deposit offers 3.6% for a $50,000 minimum, why buy JPM stablecoins?

Perhaps more interesting could be the issue of hybrids comprised of gold and stablecoins.

For example, say an investment package consists of stablecoin and gold on a 50-50 basis. It could be promoted as a hedge against having a pure dollar deposit account as part of a depositor’s asset diversification. The promoting bank keeps the T-bill interest on half the stablecoins it issues, which pays for the bullion storage fees and gives the issuer a tidy profit.

In this way, GENIUS opens up the possibility of innovative marketing techniques by banks and other financial institutions.

Probably more important than GENIUS is the Anti-CBDC Surveillance State Act which prevents the Fed from issuing a CBDC.

I have long held the view that commercial banks do not want to see central banks competing with them by issuing CBDCs directly to the public. In the US’s political system many congressmen and senators benefit from their election expenses being funded by banks, which are sure to take the view that a good politician is one who when bought stays bought. Therefore, this bill is sure to be enacted.

Given the dollar’s status as the King Rat of fiat currencies, this anti-CBDC act is likely to become a mortal blow for the global CBDC movement. And surely, that is a very good thing.

END

not good for Newmont;

(zerohedge)

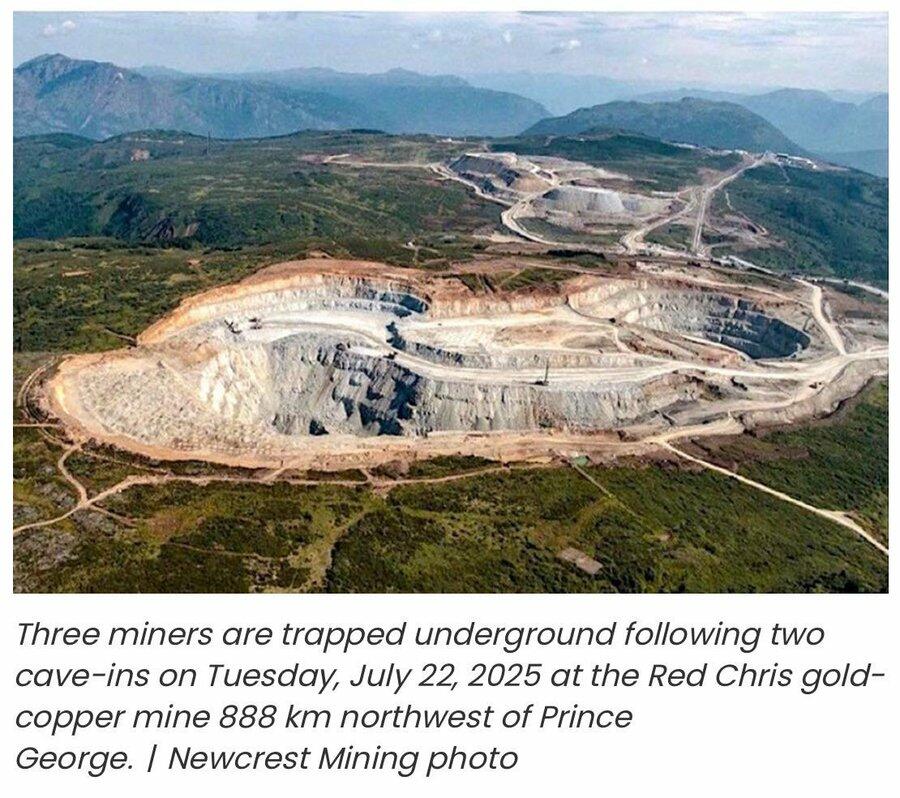

Gold Miners Trapped 500 Meters Underground In British Columbia

Thursday, Jul 24, 2025 – 11:25 AM

Three miners have been trapped 500 meters underground at Newmont Corp.’s Red Chris mine in northwest British Columbia since Tuesday after part of a non-producing area of the mine collapsed.

“At the time of the initial incident, three business partner employees were working more than 500 meters beyond the affected zone and were asked to relocate to a designated refuge station before a subsequent fall of ground blocked the access way,” Newmont wrote in a statement published on its website.

Newmont stated that the refuge station is “equipped with adequate food, water, and ventilation” to support the three miners during an “extended stay.”

A second collapse blocked access and restricted communication, Newmont said, adding that operations at the gold and copper mine have been suspended to focus resources on the rescue effort.

According to British Columbia’s mining database, Red Chris received Mines Act and Environmental Management approvals in May 2012 and began regular production in mid-2015. The mine’s current projected operational timeline is expected to continue through 2043.

What you should know about Red Chris:

Strategic mine for Newmont: While not among Newmont’s largest operations, Red Chris is part of its global portfolio and represents a foothold in Canada’s mineral-rich British Columbia region.

Gold and Copper Production: The mine produces both gold and copper, which are critical metals in demand for both industrial and investment purposes. It produced nearly 40,000 ounces of gold in 2023.

Joint Venture Model: Newmont owns a 70% stake and operates the mine in partnership with Imperial Metals Corp.

Specialist teams from nearby mines are being assembled. Newmont has not provided a rescue timeline or indicated how long the refuge station can sustain the three miners.

Submitted by admin on Thu, 2025-07-24 08:12 Section: Daily Dispatches

By Maxwell Akalaare Adombila Reuters Wednesday, July 23, 2025

DAKAR, Senegal — China’s Zijin Mining is the front-runner to acquire Barrick Mining’s Tongon gold mine in northern Ivory Coast for up to $500 million, two sources close to the matter told Reuters.

Barrick, the world’s third largest gold producer, is pivoting toward high-margin, long-life assets, with a growing focus on copper and strategic operations in Africa and the Middle East.

It suspended activity at its flagship Loulo-Gounkoto complex in neighbouring Mali after the country’s military government blocked exports, detained staff, and seized three tons of gold in a dispute over its new mining code. …

Submitted by admin on Wed, 2025-07-23 12:48 Section: Daily Dispatches

By Jp Cortez Money Metals Exchange, Eagle, Idaho Tuesday, July 22, 2025

On Monday, Treasury Secretary Scott Bessent called for a full review of the Federal Reserve system. He said on CNBC’s “Squawk Box,” “I think what we need to do is examine the entire Federal Reserve institution and whether they have been successful.”

It’s a completely legitimate statement, but Bessent is a bizarre messenger for it.

To be sure, the treasury secretary is no Ron Paul. The Trump administration calling for a review of the Federal Reserve is more likely to result in findings that the Fed’s power should be transferred to an official government department so the secretary can play God with the monetary levers.

That said, Secretary Bessent made an interesting comment that harkens back to a day of simpler monetary policy. He quipped, “All these PhDs over there — I don’t know what they do. This is like universal basic income for academic economists.”

Is Secretary Bessent right? Centrally planned monetary policy today is astoundingly complex, supposedly requiring a team of hundreds of professional economists to manage.

Alternatively, under a gold standard, money is tied to a consistent, trusted asset.

Was the old way better? Does money need “interesting features” or esoteric, in-depth explanations from experts using jargon that alienates the average person?

Gold outperformed every major asset class in first half of this year

Submitted by admin on Tue, 2025-07-22 10:04 Section: Daily Dispatches

By Mike Maharrey Money Metals Exchange, Eagle, Idaho Tuesday, July 21, 2025

Gold was up nearly 26% through the first six months of 2025, ranking as the top-performing asset class.

This booming performance continued the momentum built in 2024 when gold surged by 26.5%.

After recording 40 all-time highs in 2024, gold set another 26 all-time highs through the first six months of this year. In April gold cracked the $3,500 level for the first time. It also set a record in inflation-adjusted terms.

Gold outperformed every other major asset class. Developed market stocks (excluding the U.S.) came in second place, rising by about 19%. …

Paul Brownstein: Silver is the financial system’s canary

Submitted by admin on Mon, 2025-07-21 21:20 Section: Daily Dispatches

By Paul Brownstein ChartsAndParts.Substack.com Monday, July 21, 2025

Everything in silver is getting so, so stretched. It’s hard to imagine this game going on much longer. Harder still to imagine what happens when it ends.

This isn’t just about silver. It’s about fragility, exposure, and cracks in a system designed to hold — until it can’t.

In the past few weeks a rare alignment hit the silver market:

— Record short positions by swap dealers, offsetting natural demand.

— SLV borrow rates spike with shorts scrambling.

— Silver lease rates spike with users paying up for physical

— Comex warehouse stock explodes by more than 200 million ounces, with futures buyers taking delivery.

Submitted by admin on Mon, 2025-07-21 21:12 Section: Daily Dispatches

By Adam Sharp Daily Reckoning, Baltimore Monday, July 21, 2025

In 1970 silver traded at around $1.60 per ounce. By its peak in 1980, it reached $49.45. A handsome 30x return.

The story of how it got there is full of intrigue and conspiracy. We’ll get to that. But first, a little background is in order.

Monetary demand for silver had collapsed after the U.S. and other countries stopped using it in coins in 1965. Before that, America’s dimes and quarters were 90% silver. Other countries soon followed suit.

After governments ended their silver coinage, the market was flooded with stockpiles of the metal. Savvy collectors also bought up silver coins and melted them down. This temporarily boosted supply and depressed the price.

But inflation, and demand for hard money, were quietly building. In 1971 Nixon terminated the gold standard. From that point on, fiat money was completely free from the restraints of hard assets.

The dollar was no longer convertible to gold by foreign governments, and our coins were now made of copper and nickel rather than valuable silver.

Enter three brothers: William, Lamar, and Nelson Hunt. The three were sons of oil tycoon H.L. Hunt. …

// Nikkei CLOSED UP 655.01 PTS OR 1.59% //Australia’s all ordinaries CLOSED DOWN 0.24%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1536 OFFSHORE CLOSED UP AT 7.1513/ Oil UP TO 65.84 dollars per barrel for WTI and BRENT UP TO 69.04 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1536 AND STRONG//OFF SHORE YUAN TRADING UP TO 7.1513 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1536 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1513 (CCP MANIPULATED)

SHANGHAI CLOSED UP 23.43 PTS OR 0.65%

HANG SENG CLOSED UP 104.78 PTS OR 0.41%

2. Nikkei closed UP 655.01 PTS OR 1.59%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 97.04/ EURO RISES TO 1.1741 UP 9 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.602//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.38…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6810/Italian 10 Yr bond yield UP to 3.542 SPAIN 10 YR BOND YIELD UP TO 3.271%

3i Greek 10 year bond yield UP TO 3.388

3j Gold at $3366.90 Silver at: 39.10 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 41 /100 roubles/dollar; ROUBLE AT 78.81

3m oil (WTI) into the 65 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.38// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.602% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7935 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9332 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.403 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.960 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.893 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.48

10 YR UK BOND YIELD: 4.6540 UP 3 PTS

10 YR CANADA BOND YIELD: 3.563 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 3.098 DOWN 1 PTS

2a New York OPENING REPORT

Global Stocks, US Futures Hit New Record Highs As Google Earnings Boost AI Theme

Thursday, Jul 24, 2025 – 08:21 AM

Global stocks extended their rally to fresh record highs on the prospect of more trade deals with the US, easing fears of a drawn-out tariff war while US equity futures are also higher led by Tech with small caps lower after yesterday’s outperformance, as sentiment was boosted by Alphabet signaling strong demand for its AI products, while Tesla posted the biggest revenue decline in at least a decade. As of 8:00am, S&P futures are 0.1% higher and Nasdaq futs gain 0.3% with the AI theme driving Tech following GOOG earnings with $10 billlion capex boost helping lift other AI infrastructure stocks in premarket trading, including NVDA and AVGO. Tesla slumped 6% after Elon Musk warned of difficult times ahead after losing electric vehicle incentives in the US. Cyclicals are stronger pre-market led by Industrials. Bond yields are 1bp from 2s to 30s with USD seeing its first bid in 5 sessions. Commodities are also higher led by Ags/Energy with weakness in both Base and Precious metals. Today’s macro data focus is on Flash PMIs, Jobless Claims, Home Sales, and regional Fed activity indicators.

In premarket trading, Mag 7 stocks were mostly higher: Alphabet (GOOGL) rose 3.6% after after the Google parent reported second-quarter results that beat expectations. Tesla (TSLA) fell 6% after Elon Musk warned of a hard year ahead for the electric-vehicle maker. Elsewhere, Nvidia +1.1%, Amazon +0.7%, Meta +0.02%, Microsoft -0.02%, Apple -0.1%). Here are the other notable premarket movers:

American Airlines Group Inc. (AAL) falls 4% after the carrier reinstated its forecast this year, providing a wide range of possible outcomes.

American Eagle (AEO) is up 16%, putting the stock on track to extend gains, after the apparel retailer announced a campaign headlined by actress Sydney Sweeney. Also, the stock was mentioned on the WallStreetBets page of Reddit, which has been known for sparking bouts of meme-stock activity.

ASGN (ASGN) rises 8% after the IT services company reported second-quarter results that beat expectations.

Blackstone Inc. (BX) rises 2% after reporting a 25% jump in distributable earnings for the second quarter, buoyed by profits from its retail and evergreen funds.

Community Health Systems Inc. (CYH) sinks 29% after the owner and operator of hospitals cut the top end of its year forecast range for adjusted Ebitda and announced the retirement of CEO Tim Hingtgen.

Dow (DOW) slumps 9% after the chemicals producer reported adjusted operating loss per share for the second quarter that missed estimates. The company also cut it’s quarterly dividend.

International Business Machines (IBM) falls 6% after the IT services company reported second-quarter results that featured a disappointing read on its software business.

Las Vegas Sands (LVS) climbs 6% after the casino and resorts operator reported adjusted earnings per share for the second quarter that beat the average analyst estimate.

MaxLinear (MXL) soars 25% after the semiconductor device company reported second-quarter results that beat expectations and gave a forecast.

Mobileye Global (MBLY) gains 4% after the maker of software and hardware technology for automobiles boosted its revenue forecast for the full year.

ServiceNow (NOW) advances 6% after the software company reported second-quarter results that beat expectations and raised its full-year forecast for subscription revenue.

T-Mobile (TMUS) gains 4% after the nation’s second largest wireless provider boosted its postpaid net customers guidance for the full year.

Tractor Supply (TSCO) rises 3% after reporting comparable sales for the second quarter that beat the average analyst estimate.

Viking Therapeutics (VKTX) drops 8% after the obesity drug developer reported second-quarter loss per share that was wider than the average analyst estimate.

West Pharmaceutical Services (WST) gains 23% after the company boosted its adjusted earnings per share guidance for the full year.

As earnings season picks up pace, investors are keen for reassurance that the record-breaking US rally can continue and that lofty valuations are justified. Europe’s stocks climbed following reports the US is closing in on an agreement with the European Union to set a 15% tariff for most products.