we are now near the end of comex expiry: it finishes on Monday

and then we must deal with OTC/London LBMA options expiry Friday July 31

as always; the crooks raid gold/silver. The reason is suppress the price

due to huge derivative losses endured the banks. Do not fear the raids.

platinum ..OFF THE CHART//29%

gold: 3.5%

silver lease rate today//6.0%

118 C MACQUARIE FUTURES US 4

118 H MACQUARIE FUTURES US 62

363 H WELLS FARGO SECURITI 140

435 H SCOTIA CAPITAL (USA) 745

624 H BOFA SECURITIES 926

661 C JP MORGAN SECURITIES 15 17

686 C STONEX FINANCIAL INC 9

709 C BARCLAYS 3

905 C ADM 3

TOTAL: 962 962

MONTH TO DATE: 11,223

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 962 CONTRACTs NOTICES FOR 96,200 OZ or 2.992 TONNES

total notices so far: 11,223 contracts for 1,122,300 OR 34.908 tonnes)

SILVER NOTICES: 37 NOTICE(S) FILED FOR 0.185 million OZ/

total number of notices filed so far this month : 9292 CONTRACTS (NOTICES) for 46.460 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 38.520 MILLION OZ (QUITE SMALL)

AND JULY: 46.575 MILLION OZ//

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 119.626 TONNES//STILL QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A STRONG SIZED 505 CONTRACTS OI TO 173,958 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 205 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 205 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 505 CONTRACTS AND ADD TO THE 205 E.FP. ISSUED

WE OBTAIN A FAIR SIZED LOSS OF 300 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR SMALL LOSS IN PRICE OF $0.11 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 0.480 MILLION PAPER OZ

OCCURRED WITH OUR $0.11 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 0.44 PTS OR 0.01%

//Hang Seng CLOSED UP 358.71 PTS OR 1.43%

// Nikkei CLOSED UP 1396.40 PTS OR 3.51% //Australia’s all ordinaries CLOSED UP 0.67%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1614 OFFSHORE CLOSED UP AT 7.1599/ Oil DOWN TO 65.43 dollars per barrel for WTI and BRENT DOWN TO 68.43 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1614 AND STRONG//OFF SHORE YUAN TRADING UP TO 7.1599 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED 11,968 CONTRACTS TO 472,144 OI WITH OUR LOSS IN PRICE OF $17.30 WITH RESPECT TO THURSDAY’S // TRADING.. WE LOST ZERO NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3655 ). WE HAD CONSIDERABLE T.A.S. LIQUIDATION //THURSDAY TRADING AS WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 8313 CONTRACTS.

ON EARLY WEDNESDAY MORNING, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED TUESDAY NIGHT, A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. HOWEVER LAST NIGHT ZER0 EXCHANGE FOR RISK WAS ISSUED AS THE BANK OF ENGLAND WAS NOW SATISFIED!

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1963 CONTRACTS DESPITE OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN LAST FRIDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE IN JANUARY(AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW DECREASED TO 1% AFTER BEING AS HIGH AT 5% AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND NOW JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER FINALLY ENDS OUR MEGA MEGA HUGE T.A.S ISSUANCE WHICH COMMENCED EARLY LAST WEEK, AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A STRONG BUT MUCH LOWER 2699 T.A.S CONTRACTS THAN MONDAY’S JULY 14, ISSUANCE OF 22,678. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT IS IN FULL FORCE WITH TODAY’S RAID DURING OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATION ARE JOINED WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES TO RAID THE GOLD/SILVER PRICE.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. NOW IN JULY WE HAVE HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 3.334 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK = 37.176 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 37.176 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 32 TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 233 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3655 EFP CONTRACT WAS ISSUED: : /AUGUST 3655 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3655 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY AND THEY WERE JOINED BY OUR MONTHLY SPREADER LIQUIDATION

- ZERO NET SPEC LIQUIDATION DESPITE OUR STRONG LOSS IN PRICE WITH OUR TOTAL GAIN IN OI ON OUR TWO EXCHANGES.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY WAS A FAIR SIZED 2699 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST FRIDAY OR TODAY, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE.. THAT SET UP YESTERDAY’S (WEDNESDAY) HUMONGOUS LOSS IN PRICE IN GOLD AND SILVER AND A CORRESPONDING LIQUIDATION OF SOME COMEX OI. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH THE RARE ISSUANCE OF EXCHANGE FOR RISK!

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 3.334 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK = = 37.176 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $17.30/ /) AND THEY WERE SUCCESSFUL IN KNOCKING OFF ZERO NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED LOSS IN OI FROM TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION AND MONTH END SPREADER LIQUIDATION ////THURSDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE STRONG T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE! LET US SEE WHAT HAPPENS WITH TODAY’S RAID

FRIDAYS MORNING//THURSSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AN ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.55 TONNES EX FOR RISK = 37.176 TONNES OF GOLD STANDING

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE GAINED A FAIR SIZED TOTAL OF 6.105 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 107,200 OZ OR 3.334 TONNES OF GOLD TO WHICH WE ADD THE CRAZY 1.555 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 35.626 TONNES + 1.555 TONNES EX FOR RISK = 37.176 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE TO THE TUNE OF $17.30

WE HAD A MAMMOTH 10,266 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 10,266 CONTRACTS OR 1,026,600 0Z (25.856 TONNES)

confirmed volume THURSDAY 310,286 contracts// very strong

speculators have left the gold arena

END

INITIAL GOLD COMEX

JULY CONTRACT MONTH

JULY 25/2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2 entries i) Out of Brinks 100,600.479 oz (3129 kilobars) ii) Out of Delaware: 6351.559 oz total withdrawal 106,952.038 oz 3.326 tonnes . |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | 2 ENTRIES i) Into Brinks 92,755.635 oz 2885 kilobars 2. HSBC enhanced 159,911.700 oz 400 of 400 oz good London delivery bars. total deposit 252,667.335 oz 7.05 tonnes of gold entered. xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 962 notice(s) 96,200 OZ 2.992 TONNES |

| No of oz to be served (notices) | 231 contracts 23,100 OZ 0.7185 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,223 notices 1,122300 oz 34.908 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entry

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

2 ENTRIES

i) Into Brinks 92,755.635 oz

2885 kilobars

2. HSBC enhanced 159,911.700 oz

400 of 400 oz good London delivery bars.

total deposit 252,667.335 oz

7.05 tonnes of gold entered.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

2 entries

i) Out of Brinks 100,600.479 oz

(3129 kilobars)

ii) Out of Delaware: 6351.559 oz

total withdrawal 106,952.038 oz

3.326 tonnes

adjustments: 1

Brinks; customer account to dealer 289.359 oz (9 kilobars)

AMOUNT OF GOLD STANDING FOR JULY

THE FRONT MONTH OF JULY STANDS AT 1193 CONTRACTS FOR A GAIN OF 1072 CONTRACT. ON THURSDAY WE HAD 0 NOTICES FILED, SO WE GAINED A MASSIVE SIZED 1072 CONTRACTS OR 107,200 OZ (3.334 TONNES) ENTERTAINED WITH A MASSIVE QUEUE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD AND COMPLETELY GOES AGAINST A NARRATIVE OF A GOLD RAID ON PRICE.

AUGUST LOST 37,897 CONTRACTS DOWN TO 139,241 AS AUGUST BECOMES THE FRONT MONTH AND IT’S OI IS STILL VERY HIGH AND NOT CONTRACTING ENOUGH. WE WILL PROBABLY HAVE A HUGE NUMBER OF TONNES STANDING. WE HAVE ONLY 5 MORE TRADING DAYS BEFORE FIRST DAY NOTICE JULY 31.

SEPT GAINED 667 CONTRACTS TO 3066

We had 962 contracts filed for today representing 96,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 15 notices issued from their client or customer account. The total of all issuance by all participants equate to 962 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 17 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (11,223 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (1193 CONTRACTS) minus the number of notices served upon today (962 x 100 oz per contract) equals 1,145,400 OZ OR 35.626 TONNES to which we add 1.555 tonnes of gold issued under exchange for risk// total standing 37.175 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (11,223 x 100 oz +we add the difference for front month of JULY (1193 OI} minus the number of notices served upon today (962 x 100 oz) which equals 1,145,400OZ OR 35.626 TONNES + 1.555 tonnes EX FOR RISK = 37.176 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 37.176 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,895,972.850 oz 58.97 tonnes declining rapidly

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 37,762,393.929 oz

TOTAL REGISTERED GOLD 20,558,651.558 or 639.469 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,203,732.361 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 18,662.978 oz ((REG GOLD- PLEDGED GOLD)= 580.496tonnes //

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE JULY 2025 SILVER CONTRACT//INITIAL

JULY 25

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 ENTRY i) Out of Delaware: 15,027.740 oz total withdrawal 15,027.740 oz |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into Brinks dealer acct 242,237.220 oz total deposit 242,237.220 oz |

| Deposits to the Customer Inventory | 2 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Int Loomis 596,314.730 oz ii) Into Brinks customer: 1,084,951.100 oz total deposit 1,681,325.830 oz |

| No of oz served today (contracts) | 37 CONTRACT(S) (0.185 MILLION OZ |

| No of oz to be served (notices) | 23 contracts (0.115 MILLION oz) |

| Total monthly oz silver served (contracts) | 9292 Contracts (46.46 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

1 ENTRY

i) Into Brinks dealer acct 242,237.220 oz

total deposit 242,237.220 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Int Loomis 596,314.730 oz

ii) Into Brinks customer: 1,084,951.100 oz

total deposit 1,681,325.830 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

1 ENTRY

i) Out of Delaware: 15,027.740 oz

total withdrawal 15,027.740 oz

ADJUSTMENTs 2

a) strange: Brinks addition customer acct 608,045.090 oz

b) Manfra: customer to dealer: 364,147.500 oz

TOTAL REGISTERED SILVER: 196.470 MILLION OZ//.TOTAL REG + ELIGIBLE. 500.320 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 60 OPEN INTEREST CONTRACTS FOR A LOSS OF 0 CONTRACTS. WE HAD 25 CONTRACTS SERVED ON THURSDAY SO WE GAINED 25 CONTRACTS OR 125,000 OZ ENTERTAINED A QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST LOST 160 CONTRACTS TO 1,400 AS THIS MONTH BECOMES THE FRONT MONTH FOR SILVER

SEPTEMBER LOST 1072 CONTRACTS DOWN TO 128,204 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:37 or 0.185 MILLION oz

CONFIRMED volume; ON THURSDAY 56,012 good//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 9292 X5,000 oz = 46.460 MILLION oz

to which we add the difference between the open interest for the front month of JULY (60) AND the number of notices served upon today (37 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (9292) Notices served so far) x 5000 oz + OI for the front month of JULY(60) minus number of notices served upon today (37)x 5000 oz equals silver standing for the JULY contract month equating to 46.575 MILLION OZ .

New total standing: 46.575 million oz which is huge for this active delivery month of JULY. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 196.470 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/500.320 million. 41.97%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 957.09 TONNES, TONIGHTS TOTAL

SILVER

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 488.942 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG

J0HN RUBINO

ALASDAIR MACLEOD

Gold is set to soar

Technical analysis alone points to gold rising rapidly to at least $4300 by year-end. No wonder platinum, copper, palladium, and silver are front-running gold.

| Alasdair MacleodJul 25∙Paid |

Gold continued its three-month consolidation this week, while silver outperformed. In European morning trade gold was $3348, unchanged from last Friday’s close. And silver was $38.85, up 70 cents on the week. Our headline chart shows silver now outpacing gold so far this year, up 35% and gold up 28%.

Weaking gold since Tuesday’s peak at $3431 has been the impending expiry of the Comex August contract, with last trade for call options on Monday next week.

Gold appears to be nearing the apex of a pennant pattern formation, illustrated next:

This pennant’s shape is immensely bullish. Its flat top and rising bottom reflect a strong fundamental bull which will resolve itself on the upside. Typically, a pennant is a pause in a powerful underlying price direction before its resumption. And when it breaks out of it ($3437) the subsequent move is swift.

Edwards & Magee (the definitive work on Dow Theory) describes a pennant as “These pretty little patterns of consolidation are justly regarded as among the most dependable of chart formations both as to directional and measuring indications”. And “They are half-mast patterns which ordinarily form after a fairly steady and rapid steep price movement”.

Based on this analysis, the minimum price target for gold becomes $4,340, and fairly quickly at that taking about five months, i.e. by the year-end based on the extent and time taken for the move into the pennant from mid-November 2024.

To say the least, the implications are very interesting. From a market perspective, if gold does perform as one of “the most dependable of chart formations both as to directional and measuring indications” indicates, one is left wondering what the market consequences are for the other metals, both precious and base. Look at this Finwiz chart below:

Besides commodity prices measured in declining dollars being generally tilted to the upside, the highest rises are in metals prices: platinum, copper, palladium, silver, and gold. Gold is the least performing of these metals rising only 23% on the chart’s numbers (actually 28% and silver 35%). If gold is targeting a minimum of $4340 in five months it suggests that these other metals are similarly mispriced, potentially more so the way they are jumping the gun.

Copper’s rise can be partially explained by Trump’s tariff policies, which are currently threats rather than eventual outcomes. But a paper-driven crisis in one or more of these metals due to derivative leverages entering a delivery shortage becomes a real danger. But of these metals, silver must be our focus.

Silver’s performance illustrates a catch up from severe under-pricing, which other than a few speculative episodes is decades old. For much of the time, while demand for silver for photovoltaics and other electric/electronic applications has soared the price remained depressed. That is now correcting, and for investors who have missed the gold story, which is nearly everyone, silver is the obvious route to acquiring a stake in monetary metals.

Meanwhile, silver is making up for lost time and its bull appears to be unstoppable. This is next:

While we can point to statistics and stories about supply and demand, the common factor is a decline in the dollar, whose trade weighted index still points lower:

This fits in with gold going higher. But if gold does rise to targets based on technical patterns, it is unlikely to be just a dollar crisis. Time to batten down the hatches!

end

3. CHRIS POWELL AND GATA DISPATCHES

Serbia will hold all its gold at home, shunning global hubs

Submitted by admin on Thu, 2025-07-24 09:31 Section: Daily Dispatches

By Misha Savic and Jack Ryan

Bloomberg News

Thursday, July 24, 2025

Serbia’s central bank plans to bring all of its roughly $6 billion worth of gold reserves onto its own soil to ensure the security of the hoard in periods of crisis.

That will make Serbia the first eastern European country not to hold any of its bullion in traditional hubs like Switzerland, the United Kingdom, and the United States

“By returning gold to the country, the National Bank of Serbia sought to increase the availability and security of gold reserves in periods of crisis and uncertainty,” the central bank said in response to questions, adding that the repatriation efforts began in 2021 amid “an environment of increased global uncertainty.” …

Serbia bought 17 tons abroad from 2019 through last year, in addition to at least 19 tons from Zijin Mining Group Co.’s local unit. That brought total reserves to 50.5 tons, all stashed in Belgrade except five tons bought in 2024 and still stored in Switzerland for now. That amount of gold is worth about $6 billion at current spot gold prices.

The remaining five tons will be brought home “as soon as possible,” Governor Jorgovanka Tabakovic said last week. …

… For the remainder of the report:

Jesse Colombo: How the gold-silver ratio predicted silver’s surge

Submitted by admin on Thu, 2025-07-24 17:26 Section: Daily Dispatches

By Jesse Colombo

TheBubbleBubble.Substack.com

Thursday, July 24, 2025

I wanted to share an update highlighting a fascinating development — and the successful confirmation of a theory I proposed during the bleak days of early April:

That was when silver, along with most financial markets, plunged following President Trump’s surprising “Liberation Day” tariff announcement.

Silver sank a staggering 21% in just three trading sessions — a move that was both shocking and disheartening for precious metals investors. Yet even then I saw a glimmer of hope in the parallels with the early 2020 Covid lockdowns, which initially caused panic but ultimately sparked a powerful silver rally to seven-year highs.

In this update, I’ll walk through how that theory played out—and what it still indicates for silver’s path ahead. …

… For the remainder of the analysis:

end

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 233

5. COMMODITY REPORT..sugar

we will certainly be more healthy but it could cause a strain on USA cane sugar supplies

(zerohedge)

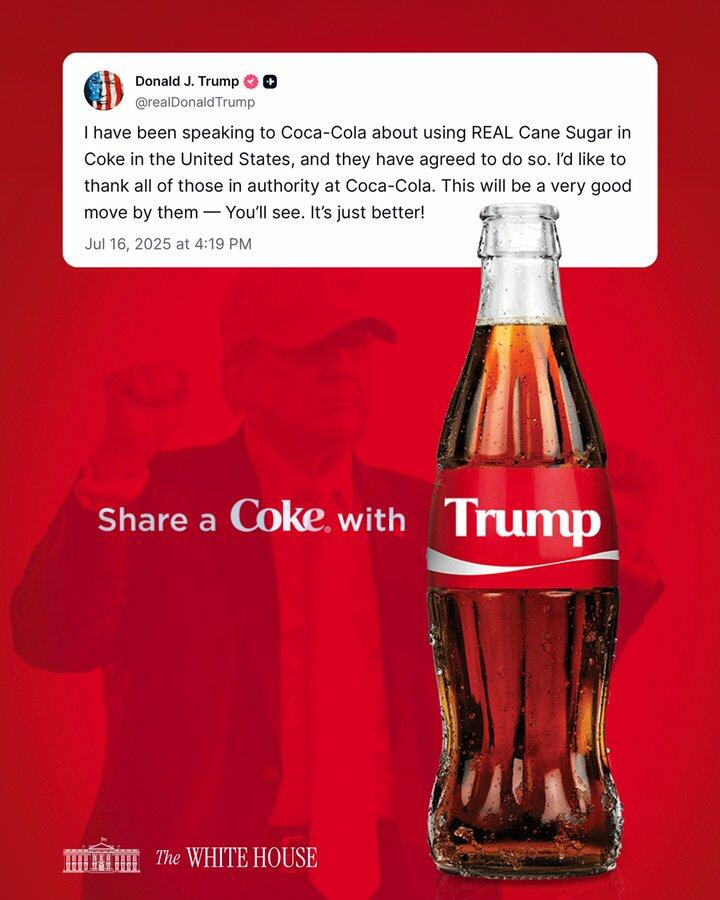

Coke’s Cane-Sweetened Soda Launch This Fall Could Strain US Sugar Supplies

Friday, Jul 25, 2025 – 04:15 AM

President Donald Trump and Health and Human Services Secretary Robert F. Kennedy Jr.’s crackdown on the ultra-processed food industrial complex has triggered a seismic shift in the beverage world. Coca-Cola is reformulating select sodas with cane sugar, and PepsiCo’s CEO has indicated similar moves. The pivot away from high-fructose corn syrup (HFCS-55), a sweetener long associated with America’s obesity and metabolic health crisis, marks a major victory for the “Make America Healthy Again” movement.

Bloomberg points out that the move to shift soda products via various top brands from HFCS-55 to cane sugar could strain the nation’s sugar supply chain…

The push means the U.S. may need to import more expensive sweetener from Mexico and Brazil — particularly if other companies follow suit.

The move threatens to worsen an already stressed supply chain, exposing American companies and consumers to higher prices just as they are facing market upheaval from Trump’s tariffs.

U.S. raw cane sugar futures are trading at record highs, with U.S. contracts now more than double the price of global benchmarks, widening the cost gap to an all-time record.

Coke plans to release the soda offering infused with cane sugar in the next several months. This could be a boon for U.S. farmers who grow the crop across Louisiana and Florida at a time when demand has been sluggish.

Bloomberg expanded more about the potential of strained cane sugar supply chains…

The problem is that the U.S. doesn’t grow a great deal of cane, making up about 30% of overall American sugar supplies, according to the U.S. Department of Agriculture. The rest comes from imports — about 2.2 million metric tons for the 2025-26 season — or American-grown sugar beets that perform better in colder climates.

If Coke’s cane-sweetened version is a success, if would likely put a dent in those U.S. supplies. The higher demand could require more imports, especially from Mexico, which has historically been the U.S.’s biggest sugar supplier, and top sugar producer Brazil.

The other challenge with using healthier ingredients is the increased cost. USDA data shows that refined cane sugar costs more than 52 cents per pound in June, or about 12% more than high-fructose corn syrup.

Related:

- White House Unveils Sweeping MAHA Changes In Nation’s Food Supply Chain

- Trump Says Coca-Cola Agreed On Major Reformulation To Use Real Cane Sugar

- Pepsi Exec Floats Switch To Sugar After Trump Coca-Cola Announcement

MAHA must sharpen its messaging to consumers by making one thing clear: healthier food will cost more than the garbage on store shelves today, but not nearly as much as a cancer treatment later in life. After all, what’s the actual price you put on your health?

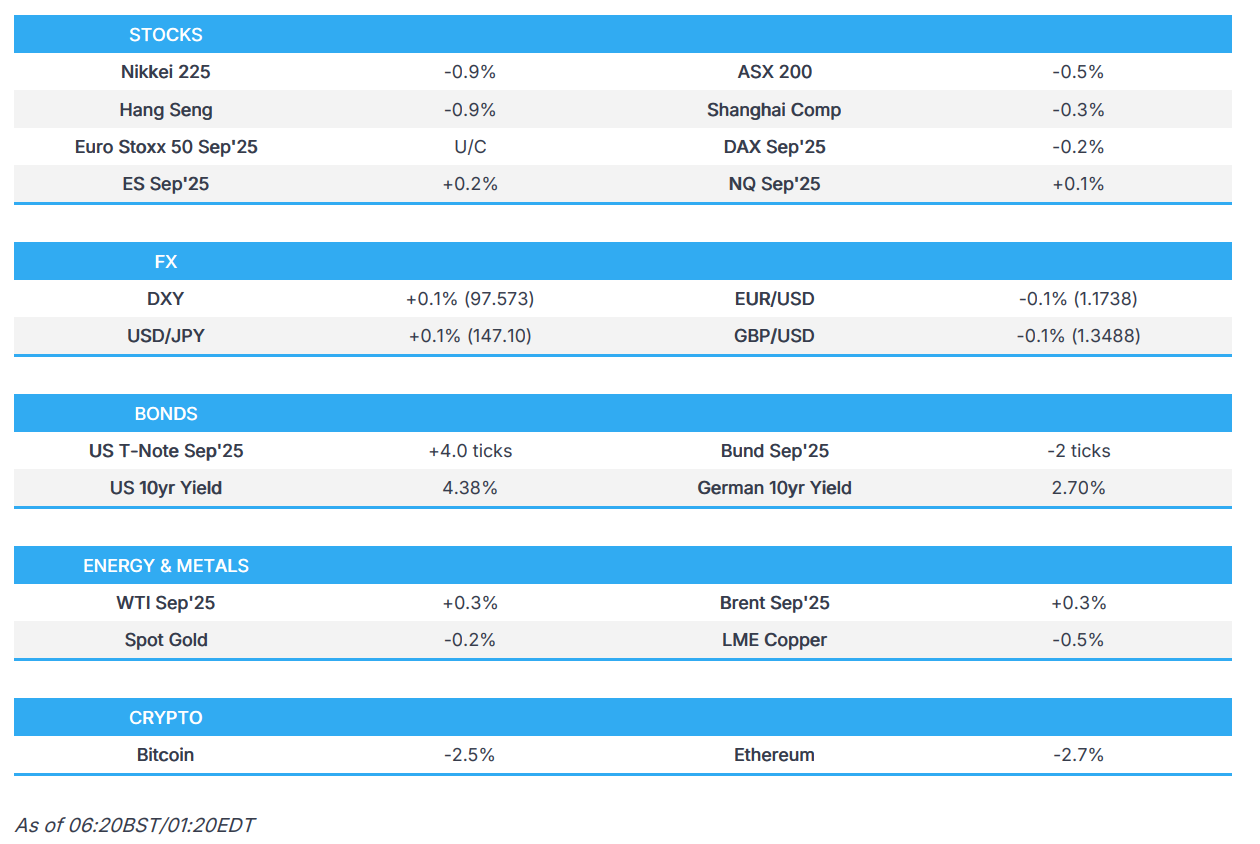

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 12.07 PTS OR 0.33%

//Hang Seng CLOSED DOWN 270.71 PTS OR 1.01%

// Nikkei CLOSED DOWN 370.11 PTS OR 0.88% //Australia’s all ordinaries CLOSED DOWN 0.50%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1668 OFFSHORE CLOSED DOWN AT 7.1671/ Oil UP TO 66.47 dollars per barrel for WTI and BRENT UP TO 69.50 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP TRADING AT 7.1668 AND WEAKER//OFF SHORE YUAN TRADING UP TO 7.1671 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1668 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1671

HANG SENG CLOSED DOWN 270.71 PTS OR 1.01%

2. Nikkei closed DOWN 370.11 PTS OR 0.88%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 97.26/ EURO RISES TO 1.1756 UP 2 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.602//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.33…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7620/Italian 10 Yr bond yield UP to 3.644 SPAIN 10 YR BOND YIELD UP TO 3.368%

3i Greek 10 year bond yield UP TO 3.486

3j Gold at $3354.90 Silver at: 39.03 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 21 /100 roubles/dollar; ROUBLE AT 79.46

3m oil (WTI) into the 66 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.33// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.602% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7954 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9350 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.413 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.954 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.923 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.55

10 YR UK BOND YIELD: 4.6490 UP 3 PTS

10 YR CANADA BOND YIELD: 3.556 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.100 DOWN 0 PTS

2a New York OPENING REPORT

Stocks Ease Back From Record High Ahead Of Tariff Deadline, Earnings Flood

by Tyler Durden

Friday, Jul 25, 2025 – 08:29 AM

US equity futures are flat at the end of a hectic earnings week and the return of meme traders in force. The market is waiting for next week’s trading deluge when nearly 30% of the S&P reports, as well as additional trade deal headlines ahead of the Aug 1 tariff deadline, with focus on a potential 15% tariff rate deal with the EU. As of 8:00am ET S&P and Nasdaq futures are unchanged. Pre-market, megacap tech stocks are mixed with AAPL (+0.4%) leading gains and TSLA lagging (-0.9%); Energy is outperforming. Yields are higher as is the USD; 2-, 5-, 10-, 30-yr yields are 0.49bp, 1.25bp, 1.81bp, 2.69bp higher, with the 10Y tradinbg at 4.41%. Commodities are mixed with oil higher, while base and precious metals are lower. On today’s calendar we get the June preliminary durable goods orders (8:30am) and July Kansas City Fed services activity (11am).

In premarket trading, magnificent Seven stocks are mixed (Apple +0.3%, Meta +0.3%, Microsoft +0.3%, Amazon +0.4%, Alphabet +0.3%, Nvidia -0.2%, Tesla -0.3%).

- AST SpaceMobile (ASTS) falls 8% after offering convertible notes as well as common stock in a separate, registered direct offering.

- Booz Allen Hamilton (BAH) climbs about 1% after the after the defense contractor posted 1Q profit that beat the average analyst estimate.

- Charter Communications (CHTR) falls 6% after the cable company reported second-quarter earnings that missed expectations.

- Centene (CNC) tumbles 12% after the health insurer reported adjusted loss per share for the second quarter, surprising analysts who’d forecasted a profit.

- Comfort Systems (FIX) is up 14% after the HVAC company reported revenue for the second quarter that beat the average analyst estimate.

- Coursera (COUR) jumps 28% after the online education company reported second-quarter results that beat expectations.

- Deckers Outdoor (DECK) rises 11% after the company reported net sales for the first quarter that beat the average analyst estimate.

- Edwards Life (EW) shares are up 7% after the medical devices company raised the low end of its sales forecast range for the year.

- Intel Corp. (INTC) falls 8% after Chief Executive Officer Lip-Bu Tan sparked concerns that he was more focused on cost cutting than restoring the chipmaker’s technological edge.

- Newmont Corp (NEM) advances 2% after the precious metals miner reported adjusted earnings per share for the second quarter that beat the average analyst estimate.

- Synovus Financial Corp. (SNV) falls 9% after Pinnacle Financial Partners Inc. (PNFP) agreed to acquire the company in an all-stock transaction valued at $8.6 billion. Pinnacle (PNFP) shares are down 5%.

- Sarepta (SRPT) tumbles 11% after an evaluating committee of the European Medicines Agency recommended against the approval of the company’s gene therapy Elevidys.

Traders have eased back on a rally that took the S&P 500 to its 10th record high in 19 days amid optimism around trade deals and corporate earnings. Next week is the busiest of the earnings season and investors are looking to the Federal Reserve’s interest-rate meeting on July 30 after data reduced the case for further cuts.

“Markets now see a greater chance that the Fed Chair will maintain a hawkish tone at the upcoming meeting” said Hebe Chen, an analyst at Vantage Markets in Sydney. “Political dynamics and economic indicators reinforce a more cautious Fed stance.”

Bubbly valuations are also giving BofA’s Michael Hartnett pause, although there are no signs of a reversal yet and the S&P 500 is set to notch a third month of solid gains. Hartnett warned of a “bigger retail, bigger liquidity, bigger volatility, bigger bubble” as global central banks ease policy and governments loosen financial regulation. US margin debt is starting to run too hot — a potentially concerning sign for the credit market, according to Deutsche Bank credit strategists. As shown below, brokerages have extended a record $1 trillion in margin credit to clients in June.

Europe’s Stoxx 600 falls 0.3% as disappointing earnings fueled worries about the impact of tariffs. The financial services and telecommunications sectors were the biggest laggards, while consumer products and automobile stocks outperformed. Here are the biggest movers Friday:

- Remy Cointreau shares rose as much as 5.5% after the French group raised its operating profit target and reported higher than expected revenues for the first quarter

- Nexity shares jump as much as 16%, the most since 2009, after the French real estate firm reported first half-year results which CIC Market Solutions said reflect “tangible operational improvement in a still challenging real estate environment”

- Close Brothers shares gain as much as 13%, after the financial services group agreed to sell its execution and securities business Winterflood Securities to Marex Group in an attempt to pare its footprint ahead of a court verdict over UK motor lending

- European mining stocks are among the worst-performers in the Stoxx 600 benchmark on Friday, after iron ore futures dropped as much as 2.5% in Singapore, the most since April 9, pressured by signs of rising supply

- Puma shares fall as much as 19% after the German sportswear maker issued what Jefferies analysts described as a “major profit warning”

- Signify shares plunge as much as 13%, the most since March 2020, after the Dutch light and lamps manufacturer reported adjusted Ebita for the second quarter that missed expectations

- Valeo shares fall as much as 16%, the most since March 2020, after a sales guidance cut as analysts note broad underperformance across all regions in the French firm’s results

- Michelin shares fall as much as 4.5% after the French car parts firm’s earnings missed expectations, with analysts noting concerns around FX and weaker volumes

- Vallourec falls as much as 4.5%, the most since May 26, after the steel producer reported net income for the second quarter that missed the average analyst estimate

Earlier in the session, Asian stocks fell, ending a six-day rally, as investors braced for the US tariff deadline and a Federal Reserve policy decision due next week. The MSCI Asia Pacific Index dropped as much as 1.2%, set for its worst loss since June 19. Tencent and Alibaba were among the biggest drags, while Shin-Etsu Chemical shares sank in Tokyo on weak guidance. Hong Kong led declines among regional gauges, with notable losses also in Japan, mainland China and India. Japanese stocks slipped as investors took profits from this week’s strong rally, while disappointing earnings from some manufacturers hurt sentiment. The Nikkei gauge fell 0.9%. Elsewhere, Vietnamese shares rose to a record high, aided by the return of foreign fund inflows amid optimism about a trade deal with the US. The benchmark VN Index rose 0.7% at the close, surpassing its last high in January 2022.

In FX, the Bloomberg Dollar Spot Index is up 0.3%, rising for a second day after US President Trump downplayed his clash with Fed Chair Jerome Powell during a tour of the central bank’s renovation project on Thursday. The yen is the weakest of the G-10 currencies, falling 0.6% against the greenback having only found a modicum of support after Bloomberg reported Bank of Japan officials see the possibility of mulling another interest-rate hike this year. The pound also underperforms after UK retail sales rose less than forecast.

In rates, ten-year US Treasury yields rose two basis points to 4.42%. Euro-area government bonds extended their post-ECB selloff as traders continue to reduce their bets on a final interest-rate cut by the central bank this year this year. German 10-year yields rise another 5 bps to 2.76%. Gilts also decline, albeit to a lesser extent.

In commodities, gold extended a decline on Friday as the dollar rose after Donald Trump downplayed his clash with Federal Reserve Chairman Jerome Powell. Oil was steady on optimism over US trade talks ahead of a key deadline next week, and as tightness in diesel markets boosts sentiment. WTI rises 0.2% to near $66.19 a barrel. Spot gold falls $21 to near $3,347/oz. Bitcoin drops 3% and below $116,000.

On today’s calendar, we have only the June preliminary durable goods orders (8:30am) and July Kansas City Fed services activity (11am). Fed officials remain in a communications blackout ahead of their July 30 rate decision.

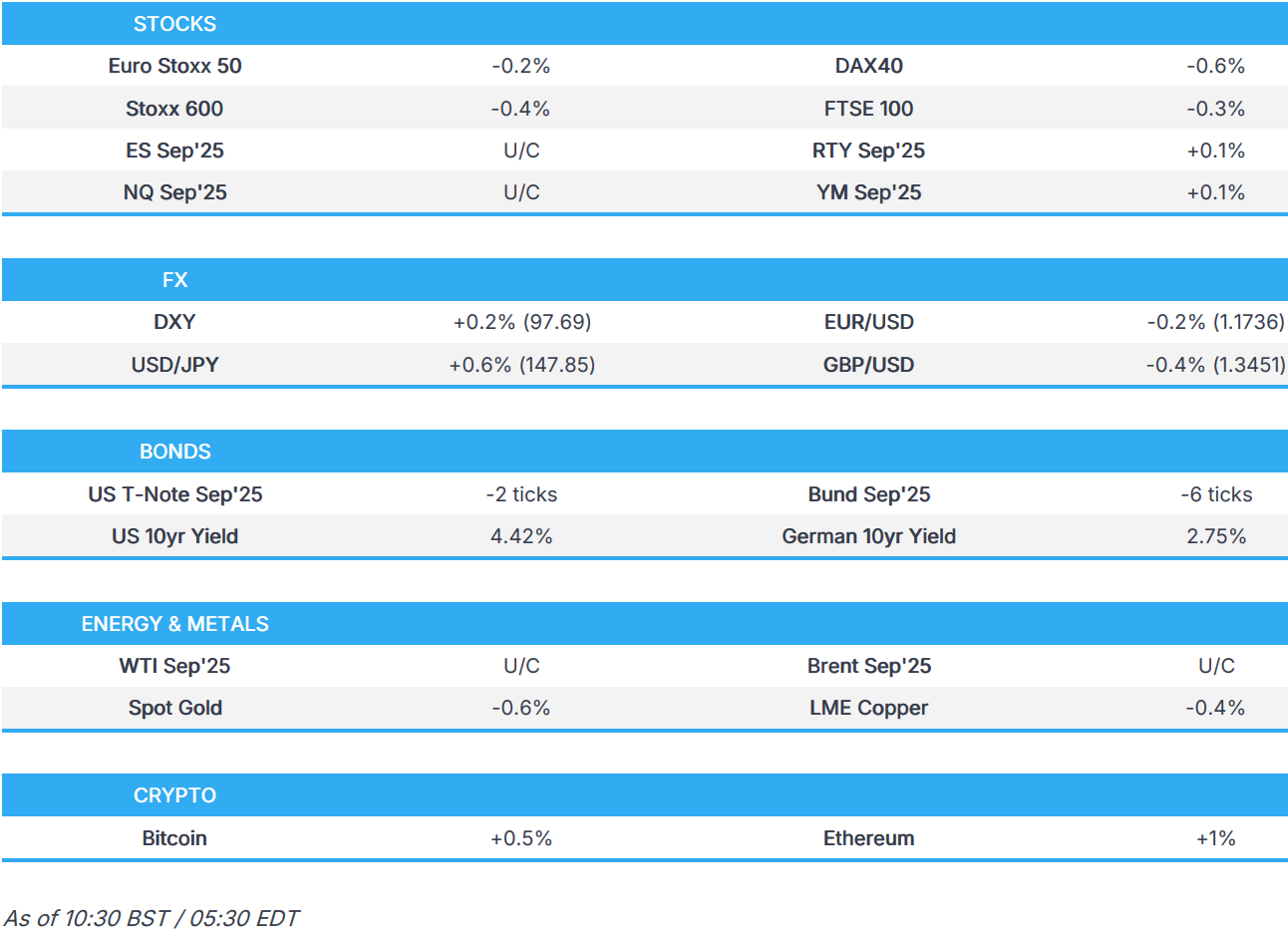

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini little changed

- Russell 2000 mini +0.1%

- Stoxx Europe 600 -0.3%

- DAX -0.5%

- CAC 40 +0.1%

- 10-year Treasury yield +2 basis points at 4.42%

- VIX little changed at 15.38

- Bloomberg Dollar Index +0.3% at 1198.84

- euro -0.1% at $1.1737

- WTI crude +0.5% at $66.35/barrel

Top Overnight News

- The dollar gained after Donald Trump downplayed his clash with Jerome Powell over the Fed’s renovation costs, saying it wasn’t reason enough to fire him. Trump said during his visit to the Federal Reserve that it is a tough construction job, while Trump and Powell briefly voiced disagreement over renovation figures and he reiterated that he wants Powell to lower interest rates. Trump later commented that he talked with Fed Chair Powell on rates and the meeting was productive, and noted that there was no tension, while he repeated several times that he believes Powell will do the right thing. Trump also said he has maybe three names in mind for Powell’s replacement but stated it is not necessary to fire Powell which would be a big move. BBG

- China’s budget deficit reached a record 5.25 trillion yuan ($733 billion) in the first half, as the government boosts domestic demand amid reduced US exports. BBG

- Boeing has been a big winner of Trump’s tariff wars as the firm sees a spike in int’l orders in conjunction w/White House trade deals. NYT

- Trump’s trade deal with Tokyo opens scope for the Bank of Japan to raise interest rates again this year, sources say, a prospect the central bank may start to telegraph by offering a less gloomy view on the economic outlook. RTRS

- Consumer inflation in Tokyo eased slightly in July, suggesting that the BOJ can take more time to gauge the economic impact of U.S. tariffs before raising interest rates. Headline number came in at +2.9% (down from +3.1% in June and below the Street’s +3% forecast) while core came in at +3.2% (inline with the Street, but down from +3.4% in June). WSJ

- Japan’s right-wing populists are gaining influence as voters rebel against rising prices and foreigners. The shift is fueling calls for tax cuts or more spending, and threatening Japan’s status as a global haven. BBG

- The ECB’s Martins Kazaks said in an interview that there’s “no urgent need” to move on rates, adding to expectations for a hold at the September meeting. BBG

- The U.S. has collected an additional $55 billion in tariffs this year. Corporate America has largely shouldered the bill for now, but that could change as firms gradually adjust prices to account for the new tariffs that are the highest level we have seen in decades. WSJ

- INTC (Intel) -8% in the pre on eps last night, concern the chipmaker is more focused on cutting costs than restoring its technological edge. CEO Lip-Bu Tan called investments begun under his predecessor excessive and unwise. BBG

Tariffs/Trade

- US Treasury Secretary Bessent said the US is in a pretty good place with China on trade and he will talk to China about them buying sanctioned oil from Russia and Iran, while Bessent separately commented that he met with Singapore’s Trade Minister.

- UK PM Starmer is to press US President Trump over a deal to cut tariffs on UK steel imports, according to FT.

- India’s Commerce Minister said he was optimistic that India could reach an agreement with the US ahead of the August 1st deadline and he had some wonderful engagement with his “friend and colleague from the US”. Furthermore, he said they are making fantastic progress with the US on a trade deal and hopes they’ll be able to conclude a “very consequential partnership”.

- Chinese Foreign Ministry says China is willing to import more marketable high-quality European products; says EU should relax restrictions on exports of high-tech products to China.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were lower after the mixed performance in the US and with light catalysts for markets outside of earnings. ASX 200 mildly retreated with the downside led by underperformance in key industries including mining, materials, resources and financials, while Whitehaven Coal failed to benefit despite posting higher quarterly output and sales. Nikkei 225 gave back some of this week’s gains amid profit taking despite a weaker currency and mostly softer Tokyo CPI. Hang Seng and Shanghai Comp conformed to the downbeat mood but with the downside in the mainland cushioned after a firm PBoC liquidity effort which resulted in a net daily injection of around CNY 602bln via 7-day reverse repos, while participants await next week’s US-China trade discussions in Sweden.

Top Asian News

- PBoC Deputy Governor Zou Lan wrote that the PBoC will promote the Treasury’s role in cash and liquidity management, according to PBoC-backed Financial News.

- Japanese PM Ishiba held meetings with party leaders, although Japan’s CDP leader Noda said PM Ishiba did not mention his future in talks with party leaders, while Japan Innovation Party co-Leader Maehara said he is not considering joining PM Ishiba’s coalition.

- BoJ reportedly sees a potential rate hike environment this year, via Bloomberg citing sources; expects to have enough data by end-2025 to consider a move. No requirement to make a significant change to the outlook. US deal reduces uncertainty.

- China will implement proactive fiscal policy to promote economic recovery.

European bourses (STOXX 600 -0.4%) opened lower across the board, continuing the downbeat mood seen in the APAC session. Downside which extended in the morning, but more recently a slight bounce has been seen across a few major indices such as the Euro Stoxx 50 and STOXX 600. European sectors hold a strong negative bias, with only a couple of industries holding afloat. Autos were initially the underperformer, but then flicked into the green as Volkswagen (+4%) pared initial losses, as traders fully digested the results and CEO commentary. Though its not all good for the sector, with Traton firmly in the red after it slashed its 2025 outlook amid US tariff uncertainty. LVMH (+4.5%) also bounced off lows seen at the open, to currently trade higher – the Co. reported a deeper than expected sales decline but its commentary on China was a little more upbeat.

European Earnings

- Volkswagen (VOW3 GY) – Headline metrics missed and cut guidance. Q2 (EUR): Revenue 80.8bln (exp. 82.19bln), -3% Y/Y. Op. Margin 4-5% (prev. guided 5.5-6.5%)

- Puma (PUM GY) – Co. cut its FY outlook, and now expects a loss in adj. EBIT terms, citing weak demand and tariff concerns.

- NatWest (NWG LN) – Strong NII and NII. Raises FY Income guidance and starts a GBP 750mln share buyback programme.

Top European News

- UK and Australia are to sign a GBP 20bln nuclear-powered submarine deal, according to The Times.

- ECB’s Villeroy says the increases in US tariffs and the extent of which is still uncertain, are not expected to cause inflation to rise, it is important to remain completely open about future monetary policy decisions.

- ECB’s Rehn says ECB will base policy decisions on a meeting-specific assessment of the inflation outlook and the risks surrounding it.

- ECB’s Kazaks says no urgent need to move rates and noted value holding rates at the current level.

- ECB’s Rehn says ECB will base policy decisions on a meeting-specific assessment of the inflation outlook and the risks surrounding it.

- ECB Survey of Professional Forecasters (Q3): Headline inflation expectations revised down for 2025-26 but unchanged for 2027 and the longer term

- UK Chancellor Reeves is reportedly considering overruling the Supreme Court in the scenario that they uphold all of the appeal court ruling that customers could be entitled to billions in compensation, via Guardian citing sources.

FX

- DXY is a touch higher, in an extension of yesterday’s upside, which was brought about by upside in US yields in the wake of weekly claims and PMI metrics. That being said, DXY is still down by the best part of 1% on the week alongside the flattening of the US yield curve and a pick-up in the JPY earlier in the week. Focus today will be on US Durable Goods and Atlanta Fed GDPNow. DXY briefly eclipsed yesterday’s best at 97.55 before topping out at 97.63.

- EUR remains more resilient than peers vs. the USD in the wake of Thursday’s “hawkish” ECB policy announcement. To recap, the GC stood pat on policy as expected given the current uncertainties surrounding the trade outlook. The greatest source of traction came after Lagarde reiterated that policy remains in a good place, suggesting that policymakers are not in a rush to adjust policy. Elsewhere, German IFO metrics came in a touch below expected but failed to engineer any traction in EUR. EUR/USD remains within Thursday’s 1.1731-88 range.

- JPY is continuing to give back some of its gains vs. the USD seen earlier in the week on account of the US-Japan trade deal. Today’s price action has been aided by softer-than-expected Tokyo CPI data, which showed the headline and core readings retreated beneath the 3% level for the first time since March. Attention is now pivoting to next week’s BoJ policy announcement, which is widely-expected to see policymakers stand pat on rates. Source reporting today via Bloomberg noted that the BoJ sees a potential rate hike environment this year and expects to have enough data by end-2025 to consider a move.

- GBP is pressured vs. the USD in the wake of softer-than-expected June retail sales metrics. M/M retail sales printed at 0.9% vs. Exp. 1.2% (prev. -2.8%), Y/Y came in at 1.7% vs. Exp. 1.8% (prev. -1.1%). Nonetheless, GBP was sent lower vs. both the USD and EUR with markets despondent regarding the current UK macro environment, which is one characterised by slowing growth, a loosening labour market and stubborn inflation. Cable has delved as low as 1.3460 but still holding comfortably above the weekly trough from Monday at 1.3402.

- Antipodeans are both softer vs. the USD alongside this morning’s soft risk tone and a lack of pertinent antipode-specific drivers.

- Barclays month-end rebalancing: weak USD selling against all majors.

- PBoC set USD/CNY mid-point at 7.1419 vs exp. 7.1609 (Prev. 7.1385).

Fixed Income

- A softer start to the session for USTs. However, once again, the magnitude of price action is relatively modest for USTs at this point in time. Some focus on Trump’s meeting with Fed Chair Powell, where the President called for cuts but said it is not necessary to fire him and doing so would be a big move. Attention now turns to US Durable goods & Atlanta Fed’s GDPNow tracker. Thus far, USTs are at the low-end of a 110-24+ to 110-31 band, entirely within Thursday’s 110-19+ to 111-02 parameter.

- Bunds are also in the red but under much more pressure than USTs. At most, lower by over 70 ticks to a 128.84 trough and a fresh low for the week. Overnight action was contained, in-fitting with peers, with selling emerging in the early-European morning, gradually at first but then intensifying into the cash equity open despite the weaker start there – no real driver for the move. As such, it appears the move is a continued repricing of the ECB after the meeting yesterday where Lagarde said they are in a good policy place. Since, source reports via Bloomberg and Reuters outline that the baseline for September is for rates to be maintained. No move to Ifo this morning, the series printed softer than forecast across the board.

- Gilts are softer, between USTs and Bunds in terms of magnitude. Lower by 20 ticks at most in a 91.32-55 band and entirely within Thursday’s 91.18-69 parameters. The only update of note so far has been Retail Sales, which saw a bounce in-line with the direction of analyst expectations, though disappointing the strong consensus view. Nonetheless, Pantheon Macro maintains their Q2 GDP growth view of 0.2% Q/Q.

Commodities

- WTI and Brent held an upward bias following Thursday’s gains on the back of trade optimism, with desks pointing out that Chevron’s resumption of operations in Venezuela overlooked against the backdrop of trade developments. More recently some pressure has been seen across the crude complex, to take WTI and Brent towards the unchanged mark. Today’s session has been lacking on pertinent updates, still awaiting the readout of the Iran/E3 meeting. WTI resides in a USD 66.05-66.74/bbl range with its Brent counterpart in a USD 69.21-69.86/bbl range at the time of writing.

- Precious metals are lower despite the cautious risk tone but amid a firmer Dollar as assets are seemingly sold in favour of cash heading into the weekend. Spot gold dipped under yesterday’s low (USD 3,351.46/oz) as it eyes the 50 DMA to the downside (USD 3,341.27/oz) as it trades in a USD 3,344.64-3,373.50/oz parameter.

- Mixed trade across base metals in line with the broader tentativeness across the markets amid a lack of fresh catalysts. 3M LME copper resides in a narrow USD 9,821.45-9,887.75/t range at the time of writing.

US Event Calendar

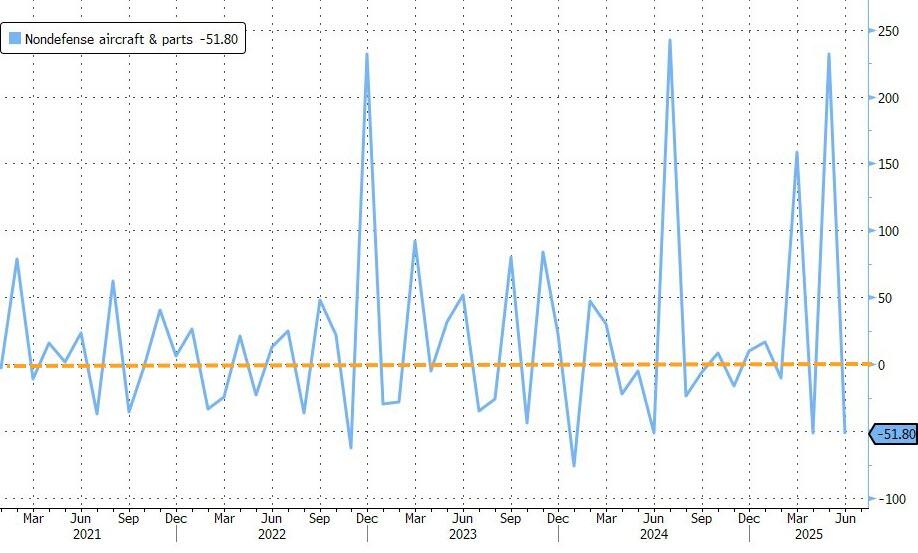

- 8:30 am: Jun P Durable Goods Orders, est. -10.71%, prior 16.4%

- 8:30 am: Jun P Durables Ex Transportation, est. 0.1%, prior 0.5%

- 8:30 am: Jun P Cap Goods Orders Nondef Ex Air, est. 0.1%, prior 1.7%

- 8:30 am: Jun P Cap Goods Ship Nondef Ex Air, est. 0.2%, prior 0.4%

DB’s Jim Reid concludes the overnight wrap

The risk-on tone just about continued yesterday, as another batch of strong US data supported investor optimism, with the S&P 500 (+0.07%) ending a quiet session at a 4th consecutive all-time high. But whilst equities were rallying, sovereign bonds struggled across the board, as the latest data and a hawkish-leaning ECB decision saw investors dial back the likelihood of near-term rate cuts, particularly in Europe. So the 2yr yield in Germany (+9.1bps) and France (+9.0bps) both posted their biggest jump since May, and US Treasuries lost ground across the curve.

In terms of that ECB decision, the main headline was much as expected, with rates being left unchanged for the first time in a year. However, there were several aspects that leant in a more hawkish direction, which led to growing doubts about whether they’d deliver another cut anytime soon. The statement kept their options open with the ECB “not pre-committing to a particular rate path.”, while Lagarde said that they were “in a good place now to hold and to watch how these risks develop over the course of the next few months.” Moreover, Lagarde did not rule out the possibility of the next move being a hike when asked.

That meeting led to a clear reaction among European sovereign bonds, with yields on 10yr bunds (+6.3bps), OATs (+7.9bps) and BTPs (+8.9bps) all ending the day higher. That came as investors grew more sceptical that the ECB would cut again this year, and there was additional momentum after the flash PMIs for July were a bit stronger than expected. For instance, the Euro Area composite PMI rose to an 11-month high of 51.0 (vs. 50.7 expected), so it added to the sense that the European economy had held up after Liberation Day.

Later in the session, there was then a Bloomberg article which said that those pushing for another cut “face an uphill battle”, and that another hold “looks like the baseline for September”. So that fit into the message from the press conference, and meant that yields got a fresh push higher into the close. Our own European economists see the ECB as signaling an extended pause and while another rate cut is possible, it may not be immediate. They also think the first hike could come sooner than most assume. See their full reaction here.