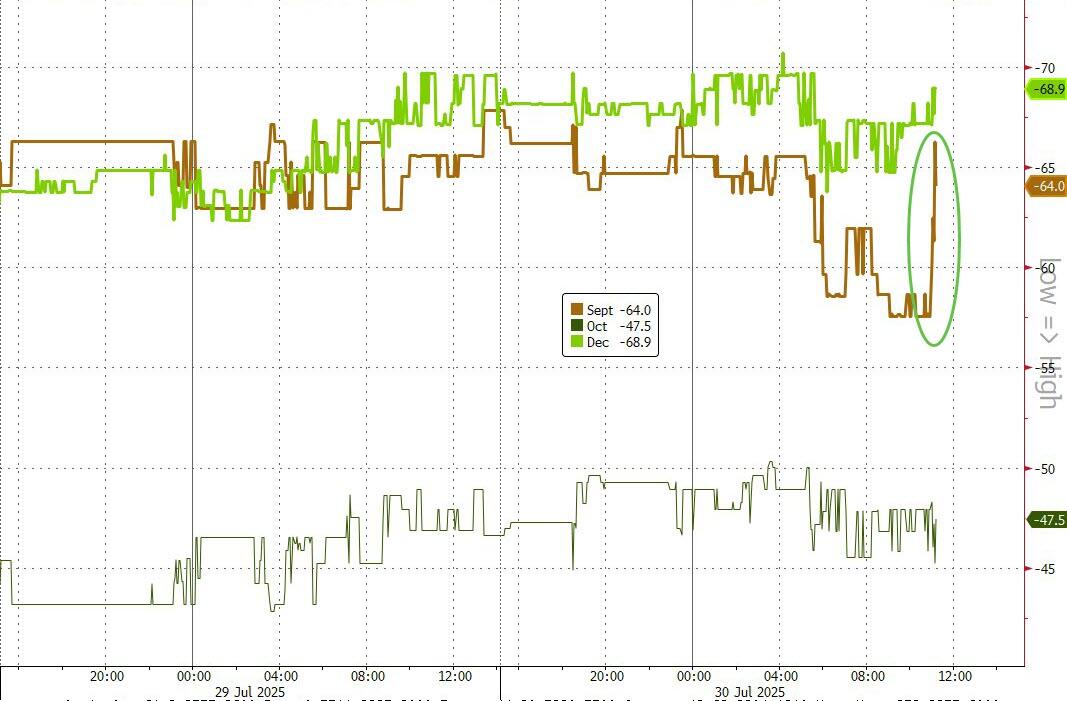

we are now beginning to deal with OTC/London LBMA options expiry Friday July 31

as always the crooks raid gold/silver so be careful!!. The reason is suppress the price

due to huge derivative losses endured the banks. Do not fear the raids.

platinum ..OFF THE CHART//29.5%

gold: 6.0%

silver lease rate today//6.5%

099 H DEUTSCHE BANK AG 13

624 H BOFA SECURITIES 12

661 C JP MORGAN SECURITIES 1

GOLD: NUMBER OF NOTICES FILED FOR JULY/2024: 13 CONTRACTs NOTICES FOR 1300 OZ or 0.0404 TONNES

total notices so far: 12,010 contracts for 1,201,000 OR 37.356 tonnes)

SILVER NOTICES: 9 NOTICE(S) FILED FOR 0.045 million OZ/

total number of notices filed so far this month : 9344 CONTRACTS (NOTICES) for 46.720 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 44.88 MILLION OZ (QUITE SMALL)

AND JULY: 46.720 MILLION OZ//

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 143.256 TONNES//STILL QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A SMALL SIZED 75 CONTRACTS OI TO 170,329 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 650 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 650 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 650 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 75 CONTRACTS AND ADD TO THE 650 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 725 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR SMALL GAIN IN PRICE OF $0.11 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.395 MILLION PAPER OZ

OCCURRED WITH OUR $0.11 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 6.01 PTS OR 0.17%

//Hang Seng CLOSED DOWN 347.52 PTS OR 1.36%

// Nikkei CLOSED DOWN 19.85 PTS OR 0.05% //Australia’s all ordinaries CLOSED UP 0.54%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1813 OFFSHORE CLOSED DOWN AT 7.1876/ Oil UP TO 69.22 dollars per barrel for WTI and BRENT UP TO 72.54 Stocks in Europe OPENED ALL MOSTLY MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1813 AND WEAKER//OFF SHORE YUAN TRADING UP TO 7.1876 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

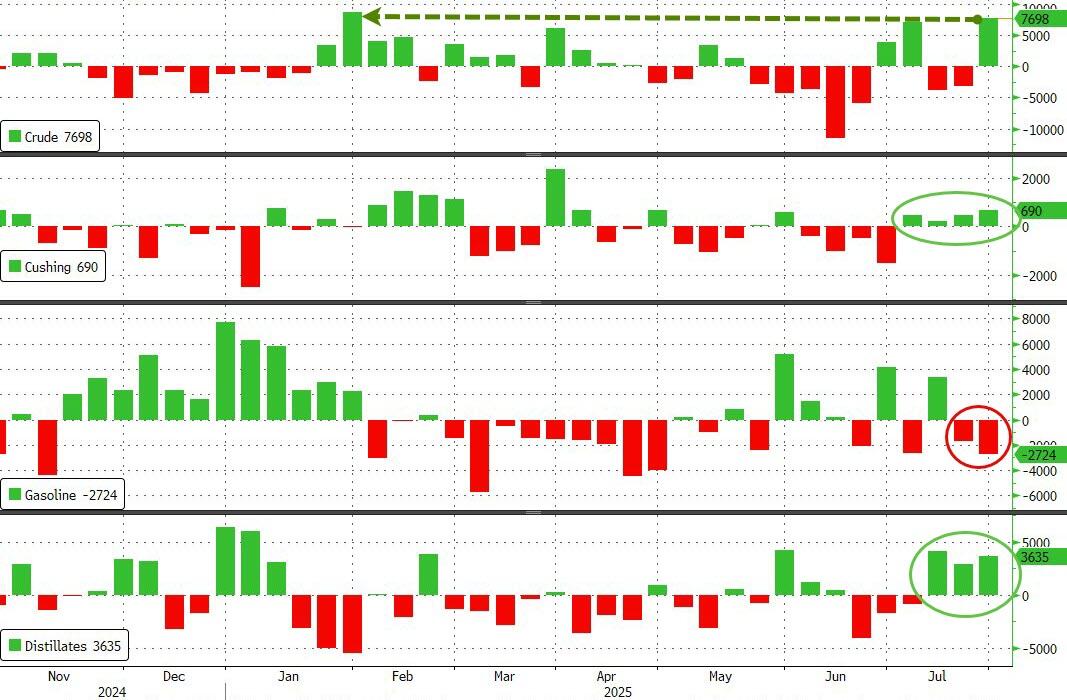

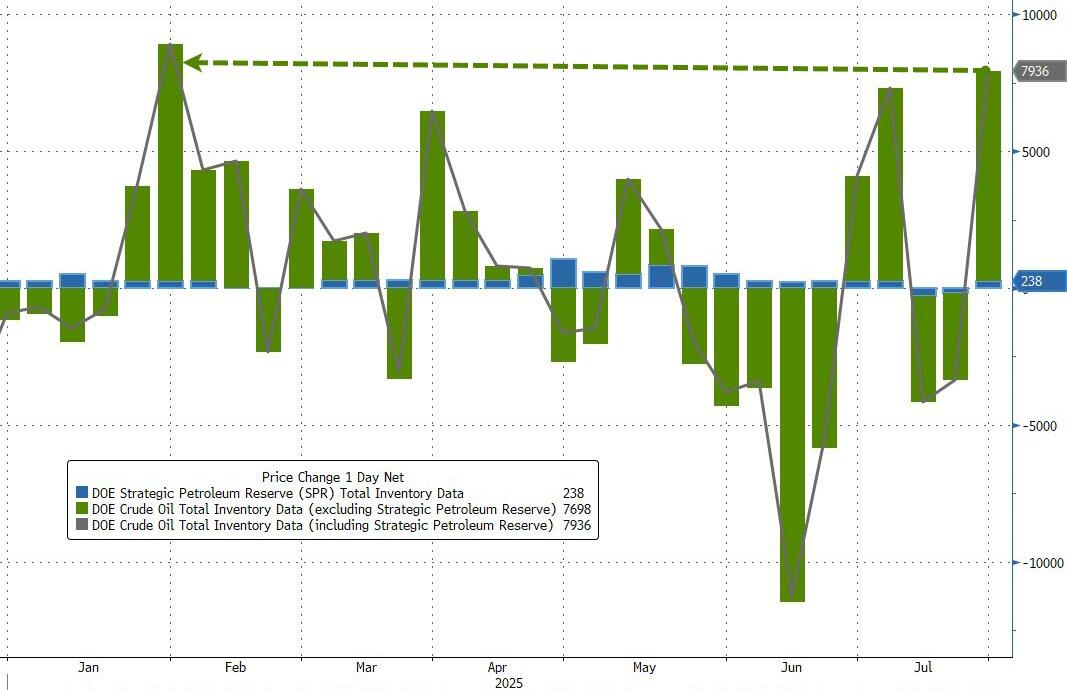

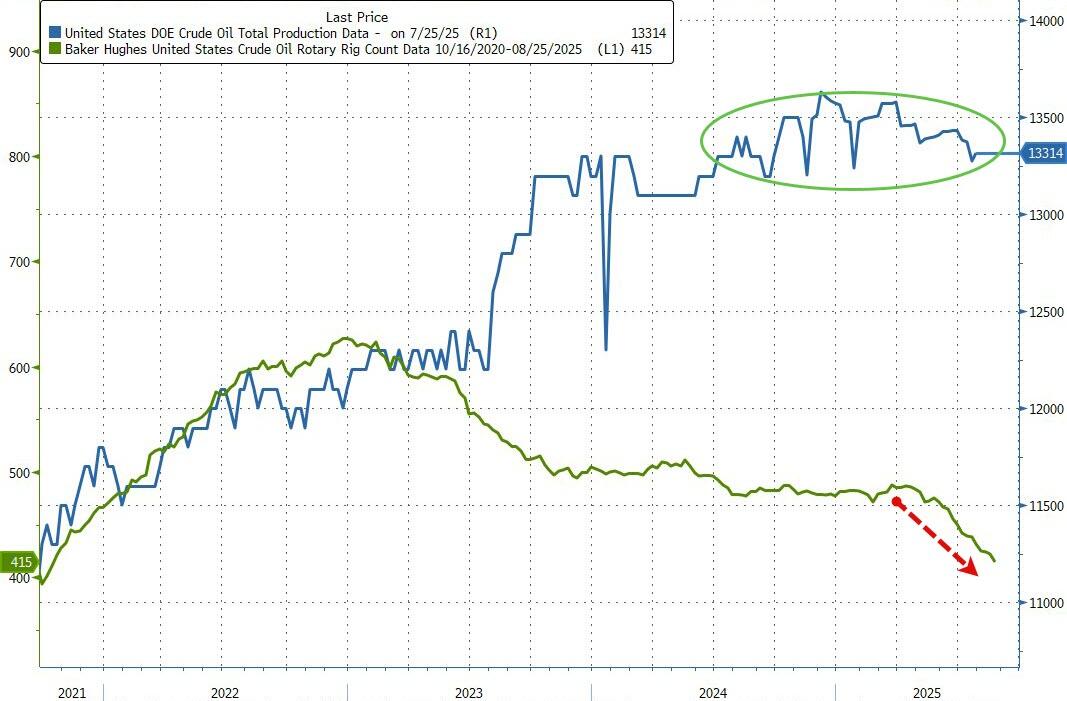

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5,582 CONTRACTS TO 445,257 OI DESPITE OUR STRONG GAIN IN PRICE OF $16.45 WITH RESPECT TO TUESDAY’S // TRADING.. WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3542 ). WE HAD CONSIDERABLE T.A.S. LIQUIDATION //TUESDAY TRADING AS WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 2140 CONTRACTS WITH ALL OF THAT LOSS DUE TO BOTH SPREADERS, THE T.A.S. LIQUIDATION AND MONTHLY SPREADERS.

LAST WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN LAST NIGHT THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY IS NOW 3.750 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS.

HISTORY: LAST SIX MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 1644 CONTRACTS DESPITE OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN MONDAY AND TUESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE IN JANUARY(AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND NOW JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 1080 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST FRIDAY’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS ARE JOINED WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. NOW IN JULY WE HAVE HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD

NEW TOTAL TONNES STANDING JULY: 41.106 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 233 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NONE COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3542 EFP CONTRACT WAS ISSUED: : /AUGUST 3542 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3542 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY AND THEY WERE JOINED BY OUR MONTHLY SPREADER LIQUIDATION

- ZERO NET SPEC LIQUIDATION WITH OUR STRONG GAIN IN PRICE DESPITE OUR TOTAL LOSS IN OI ON OUR TWO EXCHANGES.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY WAS A FAIR SIZED SIZED 1080 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS PAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S HUGE GAIN IN PRICE IN GOLD AND SILVER AND A CORRESPONDING LIQUIDATION OF SOME COMEX OI. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH THE RARE TWO ISSUANCES OF EXCHANGE FOR RISK! THE UNUSUALLY SMALL RAIDS THROUGHOUT OPTION EXPIRY WEEK USED TO LOWER THE HUGE DERIVATIVE LOSSES ENDURED BY THE BANKERS IS QUITE A SURPRISE.

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

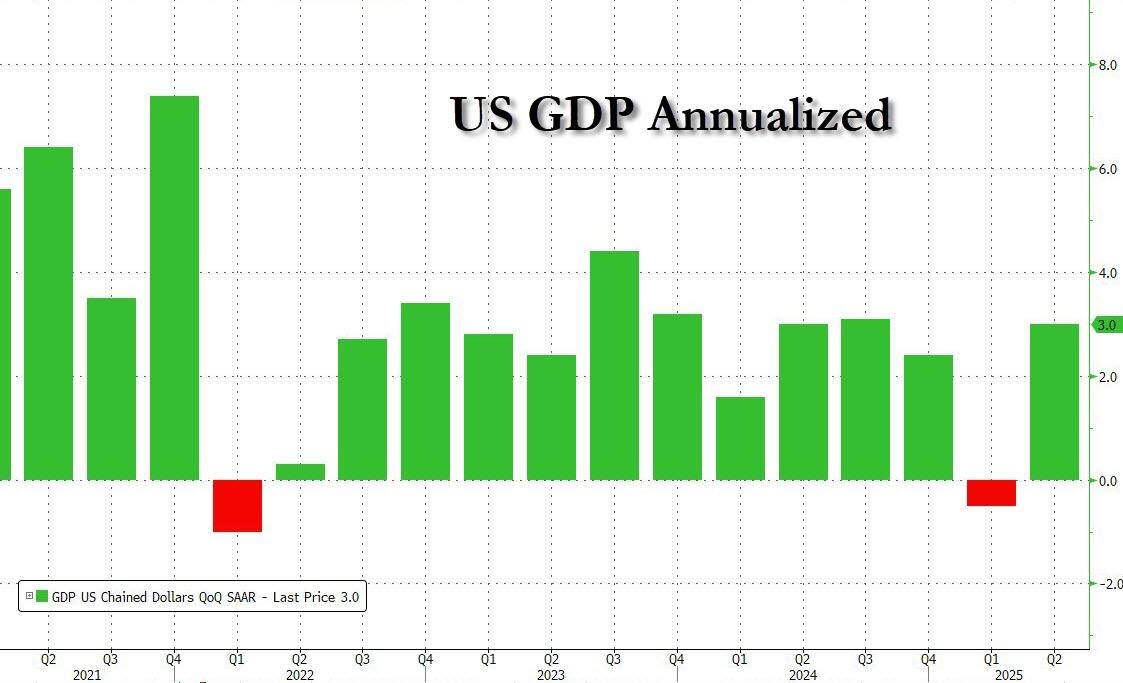

COMEX GOLD TRADING/JULY CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A STRONG $16.45/ /) AND THEY WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION AND MONTH END SPREADER LIQUIDATION ////TUESDAY WHICH ACCOUNTS FOR THE LOSS IN TOTAL OI. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE STRONG T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE!

WEDNESDAYS MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// JULY COMEX CONTRACT

WE HAVE LOST A FAIR SIZED TOTAL OF 6.656 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY FIRST RECORDED AT 17.947 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ OR 0 TONNES OF GOLD TO WHICH WE ADD OUR TWO CRAZY EXCHANGE FOR RISK FOR 3.750//NEW STANDING ADVANCES TO 37.356 TONNES + 3.75 TONNES EX FOR RISK = 41.106 TONNES

ALL OF THIS QUITE GOOD STANDING FOR JULY WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $24.00

WE HAD A SMALL 463 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 2140 CONTRACTS OR 214,000 0Z (6.656 TONNES)

confirmed volume TUESDAY 288,682 contracts// strong

speculators have left the gold arena

END

INITIAL GOLD COMEX

JULY CONTRACT MONTH

JULY 30/2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entry Brinks 1671.852 oz . |

| Deposit to the Dealer Inventory in oz | 2 ENTRIES i) Into Asahi Dealer: 160,621.119 oz (4996 kilobars) ii) Into Brinks dealer 24,884.874 oz (774 kilobars) total deposit 185,505.993 ox (5770 lilobars) or 5.77 tonnes |

| Deposits to the Customer Inventory, in oz | 2 ENTRIES i) Into HSBC enhanced: 160,944.725 oz (402 Good London delivery bars of 400 oz each) ii) Into Manfra: 3150.504 oz (98 kilobars) total deposit: 164,095.229 oz or 5.104 tonnes total gold deposit dealer and customer; 10.874 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 13 notice(s) 1300 OZ 0.0404 TONNES |

| No of oz to be served (notices) | 0 contracts 0 OZ 0.0000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 12,010 notices 1,201,000 oz 37.356 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 2 entries

2 ENTRIES

i) Into Asahi Dealer: 160,621.119 oz (4996 kilobars)

ii) Into Brinks dealer 24,884.874 oz (774 kilobars)

total deposit 185,505.993 ox (5770 lilobars)

or 5.77 tonnes

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

2 ENTRIES

i) Into HSBC enhanced: 160,944.725 oz

(402 Good London delivery bars of 400 oz each)

ii) Into Manfra: 3150.504 oz (98 kilobars)

total deposit: 164,095.229 oz or 5.104 tonnes

total gold deposit dealer and customer; 10.874 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entry

Brinks

1671.852 oz

adjustments: 2

a)JPMorgan: customer to dealer 104,427.482 oz

b) Malca 42,220.901 oz

AMOUNT OF GOLD STANDING FOR JULY

THE FRONT MONTH OF JULY STANDS AT 13 CONTRACTS FOR A LOSS OF 516 CONTRACTS. ON TUESDAY WE HAD 516 NOTICES FILED YESTERDAY, SO WE GAINED 0 CONTRACTS OR NIL OZ (0 TONNES) ENTERTAINED WITH A QUEUE JUMP WHERE THESE BOYS DEMANDED PHYSICAL DELIVERY OVER ON THIS SIDE OF POND UPON EXERCISING AN EFP THROUGH LONDON. THIS IS CENTRAL BANKERS DEMANDING PHYSICAL GOLD AND COMPLETELY GOES AGAINST A NARRATIVE OF A GOLD RAID ON PRICE.

AUGUST LOST 40,296 CONTRACTS DOWN TO 26,497 AS AUGUST BECOMES THE FRONT MONTH AND IT’S OI IS STILL VERY HIGH. WE WILL PROBABLY HAVE A STRONG NUMBER OF TONNES STANDING. WE HAVE ONLY 2 MORE TRADING DAYS BEFORE FIRST DAY NOTICE JULY 31.

SEPT GAINED 433 CONTRACTS TO 4568

We had 13 contracts filed for today representing 1300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 13 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JULY /2025. contract month, we take the total number of notices filed so far for the month (12,010 X 100 oz ) to which we add the difference between the open interest for the front month of JULY (13 CONTRACTS) minus the number of notices served upon today (13 x 100 oz per contract) equals 1,201,000 OZ OR 37.356 TONNES to which we add 1.555 tonnes of gold issued under exchange for risk/PRIOR + 2.195 TONNES TODAY// total standing 41.106 tonnes

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (12,010 x 100 oz +we add the difference for front month of JULY (xxxx OI} minus the number of notices served upon today (13 x 100 oz) which equals 1,201,000OZ OR 37.356 TONNES + 3.75 tonnes EX FOR RISK = 41.106 tonnes

TOTAL COMEX GOLD STANDING FOR JULY.: 41.106 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,884,653.175 oz 58.61 tonnes declining rapidly

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,514,461.359 oz

TOTAL REGISTERED GOLD 20,920,934.783 or 650.72 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,593,526.576 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,036281 oz ((REG GOLD- PLEDGED GOLD)= 592.11tonnes //

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE JULY 2025 SILVER CONTRACT//INITIAL

JULY 30

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 ENTRY |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into Ashai dealer 585,279.220 oz total deposit 585,279.220 oz |

| Deposits to the Customer Inventory | 2 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into Brinks 255,824.679 oz ii) Into Loomis: 1200,645.820 oz oz total deposit: 1,456,470.496 oz |

| No of oz served today (contracts) | 38 CONTRACT(S) (0.190 MILLION OZ |

| No of oz to be served (notices) | 0 contracts (0.000 MILLION oz) |

| Total monthly oz silver served (contracts) | 9344 Contracts (46.720 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

1 ENTRY

i) Into Ashai dealer 585,279.220 oz

total deposit 585,279.220 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into Brinks 255,824.679 oz

ii) Into Loomis: 1200,645.820 oz oz

total deposit: 1,456,470.496 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

0 entry

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 191.541 MILLION OZ//.TOTAL REG + ELIGIBLE. 504.338Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF JULY /2025 OI: 9 OPEN INTEREST CONTRACTS FOR A LOSS OF 32 CONTRACTS. WE HAD 38 CONTRACTS SERVED ON TUESDAY SO WE GAINED 6 CONTRACTS OR 30,000 OZ ENTERTAINED A QUEUE JUMP WHERE THESE BOYS DECIDED TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND.

AUGUST LOST 105 CONTRACTS TO 1,031 AS THIS MONTH BECOMES THE FRONT MONTH FOR SILVER

SEPTEMBER LOST 1652 CONTRACTS DOWN TO 121,325 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 9 or 0.045 MILLION oz

CONFIRMED volume; ON MONDAY 49.378 poor//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 9344 X5,000 oz = 46.720 MILLION oz

to which we add the difference between the open interest for the front month of JULY (9) AND the number of notices served upon today (9 )x (5000 oz)

Thus the standings for silver for the JULY 2025 contract month: (9344) Notices served so far) x 5000 oz + OI for the front month of JULY(9) minus number of notices served upon today (9)x 5000 oz equals silver standing for the JULY contract month equating to 46.720 MILLION OZ .

New total standing: 46.720 million oz which is huge for this active delivery month of JULY. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 191.541 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/504.338 million. 41.94%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 956.23 TONNES, TONIGHTS TOTAL

SILVER

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 487.852 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

Credit collapse and the gold bull

Recession, commodity-driven inflation, and higher interest rates all point to a crisis undermining stocks, bonds, and even currencies. It’s why gold is ready to rise again.

| Alasdair MacleodJul 30∙Paid |

Introduction

Markets are asleep, affected by a general summer torpor. But in the background, there are growing signs that all is not well. Precious metals are in early-stage bull markets for good reasons. CPI price inflation is not going away, and market expectations of lower interest rates are in retreat. It is increasingly evident that bond markets are reluctant to absorb medium and long maturity debt, signalling a destabilising preference for near-cash.

That is the evidence from Wall Street. Anecdotal evidence from Main Street not reflected in official statistics are of small and medium sized businesses struggling outside the major cities, retail outlets closing, and rural communities in trouble. In the shops, food prices and those of other consumer necessities appear to be rising more quickly than government statisticians admit. The term “stagflation” is increasingly used to describe current conditions.

In this article, I examine the common driving forces behind G7 economies and their outlook. The dominant features are a new bull market in commodities, increasing credit risk in bond markets undermining wider financial values, and a deepening recession. I shall consider each in turn.

Commodity outlook

Most important for humanity is energy, and despite the move to more expensive non-fossil fuels crude oil is the basis of all economic activity. Its price matters. Measured in real corporeal money without counterparty risk, which is gold, it is exceptionally cheap.

It is also the most political commodity. In the past the price in dollars has been manipulated by the OPEC cartel, wars, and sanctions against various producers. New technologies such as fracking have contributed to supply, and environmental policies have impacted on demand. But that is just one side of the price equation with gold. Gold itself has been suppressed, firstly by US Treasury sales to keep the Bretton Woods $35 gold standard intact, and subsequently by the creation of gold derivatives to absorb demand which otherwise would have driven gold prices higher relative to dollars. Furthermore, the US treasury’s immense anti-gold propaganda effort all but drove it out of the monetary system.

Much, if not most of the volatility in the oil/gold price is due to these factors rather than supply and demand. But with the fiat currency era ending, gold is beginning to be rehabilitated as the risk-free escape from increasingly dodgy dollars. And we know that while commodities and wholesale goods can and do vary priced in gold, over the long-term gold’s purchasing power is remarkably stable. It is in this context that we note since 1950 WTI crude’s price in gold has fallen by 75%.

Gold’s inherent stability of value means we can expect a rebound towards 1950s gold standard levels, implying up to a 300% increase in the oil/gold ratio. How long it takes depends in turn on the relationship between gold and the dollar along with the other G7 fiat currencies.

We see the same situation in base metals, illustrated next.

In this chart, I include the basket of base metals priced in dollars, illustrating how it increased substantially between 2002—2008, principally due to increasing Chinese manufacturing demand and the expansion of dollar credit, initially under Greenspan and then Bernanke. The subsequent reaction to end-2019 changed with the inflationary covid lockdowns, imparting a new round of price inflation which peaked in 2022. And since last year, base metals priced in dollars have begun to rise again.

Valued in gold, base metals tell a different story. Their most recent value is only 14% of that in 1950, the lowest ever. To an extent, this reflects gold rising against the dollar front-running base metals and commodities generally.

However, as is the case with crude oil, monetary, geopolitical, and economic factors have combined to suppress base metals measured in gold. On the basis that this index can be expected to return towards its gold-standard average, price increases of five or six times in gold alone might reasonably be expected.

Since 2019, food prices have been rising as well, indicated by the chart of Invesco’s DB Agriculture fund — the largest ETF in the sector:

To summarise, irrespective of opinions on the economic outlook, consumer price inflation is going to become a significant problem again sooner rather than later. The implication is that any reduction in interest rates will be short-lived if they occur. Instead, in accordance with their inflation mandates central banks will be forced to raise interest rates unless they are prepared to let their currencies slide. That is, until the debt overload on the private sector leads to or threatens widespread bankruptcies.

Inflation and financial asset values

The correct way to look at price inflation is that it represents loss of a currency’s purchasing power. In order to compensate creditors, the interest on bonds must incorporate compensation for the use of a creditor’s funds and risk to the purchasing power of final repayment. Simplistically, an investor in a currency will require a return which gives him a margin over his expectation of its debasement.

We have seen that commodity prices have only one way to go and that is up. Partly, this may reflect falling fiat currency values, but there is no doubt that the G7 nations have cast themselves away from the new dynamic economies of China, Russia, their Shanghai Cooperation Organisation partners, BRICS members, and the wider global south desperate to move away from US hegemony in favour of the Asian superpowers. In the old dying G7 economies, the public, including the mainstream media upon which they rely for guidance, are hardly aware of this change which is set to energise fully 70% of the world’s population into a new industrial revolution.

Bond yields and interest rates are therefore bound to rise. The importance of this new trend is illustrated in the chart below:

That a 40-year downtrend in bond yields was smashed in 2022 is not trivial. And now we face a new round of commodity price rises and currency debasement. Clearly, bond yields are on a new rising trend of which the last two years merely represent a consolidation. And if economies go into recession, which is almost certainly their trend direction, both private and public sectors will find it increasingly difficult to service their increasing debt as interest rates rise.

The public sector prints, while the private sector goes bust. This brings us to the relationship between long bond yields and equities, which is probably more stretched than it has ever been in history.

In the chart below, I have inverted the yield on the long bond (right hand scale) to illustrate the reverse correlation with the S&P 500 Index (left hand scale), indexing both to 100 in 1985. As one would expect, it confirms that a falling yield normally accompanies an equity bull market, and a rising yield leads to a bear market in equities.

The reason is that investors will increase their bond allocations by selling equities when yields rise and vice-versa. But from time to time, valuation differences can become significant when other factors are present. We saw this in April 2020 at the time of covid, when the long bond yield fell to 1.12% while many businesses effectively ceased trading.

That was an aberration. But note how the bond’s yield rose between October 1998 and January 2000, before bursting the dot-com bubble. The S&P then fell nearly 50%, and the NASDAQ 100 75%. In an effort to stop the slide, the Fed reduced its funds rate from 6.53% in early-2000 to 1% in July 2003 bringing the long bond yield back in line with equities.

The dot-com experience was the top of a credit induced bubble exhibiting speculative behaviour seen during the South Sea Bubble of 1715—1720, and the 1928—1929 period on Wall Street.

This time, the valuation disparity is twice as great as the dot-com bubble, almost certainly the greatest in stock market history. Market expectations are for interest rate cuts which would reduce the overvaluation of equities. But as pointed out above, inflation not only remains above the Fed’s 2% target but will be going higher as commodity prices and Trump’s tariffs bite.

Importantly, there are no offsets to these price pressures this time. Base metals priced in dollars soared between 2002 and 2011, but cheap manufacturing of imported goods from China and East Asian nations absorbed these costs keeping consumer price rises relatively subdued. This time, the one-off effect of cheap Chinese and east Asian production cannot absorb a second commodity shock, and Trump’s tariffs will add to consumer price pressures.

1929—1932 redux

Few investors realise that the reason their portfolios have been doing well is that stock prices have been fuelled by ephemeral credit, which is the other side of debt. Initially, rising bond yields lead to losses in bond portfolios encouraging credit flows into equities, until the valuation disparity described above begins to pop the equity bubble.

We are close to that point, which saw similarities with the US stock market in 1928—1929. Furthermore, the Smoot-Hawley Tariff Act of 1930 became a real risk in September 1929, having been ignored by markets when Congress debated it that summer. President Hoover signed it into law in June1930. The Dow lost 89% of its index value from September 1929 to mid-1932 and 9,000 small and regional banks went bankrupt or closed.

Will September 2025 prove to be a fateful anniversary of events in 1929?

The conditions in today’s credit bubble appear to be more extreme, to which we can add the lack of a gold standard. Not only will the lessons from the Wall Street crash and the thirties depression apply, but we can add a currency collapse into the mix.

Our analysis has rightly focused on the dollar, the King Rat of fiat currencies. Where the dollar goes, the other fiat currencies will get sucked into the same vortex. The other G7 nations share similar debt and overvaluation problems, rendering the entire post-Bretton Woods fiat currency system as unstable as a house of cards.

One puff of wind and it’s all over.

3. CHRIS POWELL AND GATA GOLD DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 233

5. COMMODITY REPORT..COBALT/COPPER/CONGO

“The US Is Catching Up”: Competition With China Over DR Congo Minerals Intensifies

Tuesday, Jul 29, 2025 – 06:50 PM

After years of near-exclusive control over the Democratic Republic of Congo’s (DRC) rich mineral reserves, China now faces growing competition from the United States. Washington is moving aggressively to secure access to cobalt, copper, and lithium—vital for electric vehicles, green energy, and defense technologies, according to the South China Morning Post.

Last year, the US reportedly pressured Kinshasa to block a Chinese acquisition of Chemaf Resources. Now, a US consortium, including firms led by former military executives, has bid for Chemaf’s operations, including the major Mutoshi copper-cobalt project. Bill Gates- and Jeff Bezos-backed KoBold Metals has also signed a deal to explore the Manono lithium deposit, despite a legal dispute with Australia’s AVZ Minerals.

These moves follow a US-brokered “minerals-for-security” agreement between the DRC and Rwanda aimed at stabilizing eastern Congo. In return, American companies gain mineral access.

Joseph Cihunda, a law professor at the University of Kinshasa, said the Congolese government is trying to avoid becoming a battleground between global powers. “Even in Congolese public opinion, they do not want such a confrontation,” he noted. President Félix Tshisekedi recently met with Chinese officials to reassure them of continued cooperation.

“Minerals are abundant in the DR Congo and there is room for everyone, American, European and Chinese,” Cihunda added.

SCMP writes that China remains deeply embedded in the DRC mining sector. Its ambassador to Kinshasa, Zhao Bin, rejected claims Beijing had neglected Congo, saying: “We have neither treated the DR Congo as a bargaining chip nor imposed any discriminatory measures against it.” Zhao emphasized China’s “non-interference” policy and its practical support, from military aid to economic assistance.

Analysts say the US is now trying to catch up. Sun Yun of the Stimson Center said, “The US is catching up on its critical mineral vulnerability and it will have to vigorously push for more assets and security in its supply chain.”

Much of the competition centers on cobalt—of which the DRC supplies roughly 70% of the global total—as well as copper, lithium, and other key metals. Western companies ceded many assets to Chinese control in past years, including Freeport-McMoRan’s sale of Tenke Fungurume and Kisanfu to China Molybdenum in 2016 and 2020.

Chris Berry of House Mountain Partners said US policy on minerals has shifted from environmental goals to security priorities: “Rather than a focus on ESG or ‘green growth’ the focus is now on national defence and self-sufficiency in critical mineral access.” He expects US companies to be “much more aggressive in deal making” as they compete with China.

END

COPPER

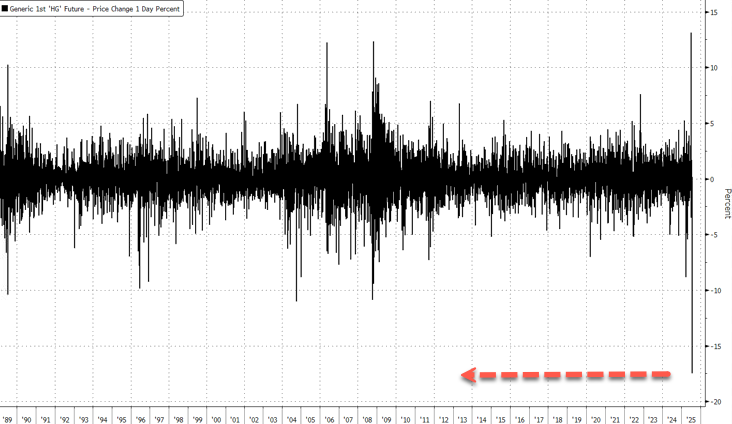

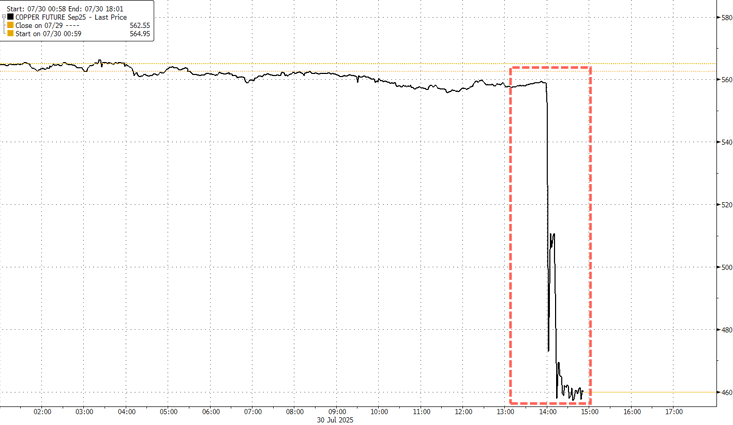

US Copper Prices Crash Most On Record After Trump Confirms 50% Tariff Excludes Refined Products

Wednesday, Jul 30, 2025 – 03:41 PM

U.S. copper futures crashed over 19% within minutes around 2:00 p.m. ET, marking the largest intraday drop on record, after the White House announced a 50% tariff on all semi-finished copper imports starting August 1.

Largest daily decline on record!

Traders were stunned when copper cathodes, the most widely imported and traded form of refined copper, were exempted from the new duties, triggering a vicious unwinding of bullish bets. The initial expectation had been that the tariffs would apply to all refined imports.

Pre-2:00 p.m. ET, U.S. copper prices were trading at record highs.

President Trump invoked the Defense Production Act, which allows his administration to direct industries to boost production of copper critical to national security. This means 25% of high-quality copper scrap and forms of raw copper must be made in the U.S. and sold domestically in 2027. That percentage would rise to 40% by the end of the decade. This move should be enough to boost domestic refining capacity while supporting U.S. refiners.

Trump wrote in the order that the Commerce Secretary concluded copper imports threaten U.S. national security, citing overreliance on foreign sources, weakened domestic capacity, and global overproduction.

The metal is critical to defense systems, infrastructure, and the broader industrial base, with no adequate substitutes.

“Today, a single foreign country dominates global copper smelting and refining, controlling over 50 percent of global smelting capacity and holding four of the top five largest refining facilities,” the order said, stopping short of naming China.

Trump’s actions:

- Effective August 1, 2025, Trump imposed a 50% tariff on semi-finished copper products and intensive copper derivatives.

- Refined copper (cathodes) was excluded for now, but a phased tariff of 15% in 2027 and 30% in 2028 is under consideration.

- The tariff is in addition to any existing duties from other executive actions, such as those targeting drug trafficking or trade imbalances.

- The proclamation includes a mechanism to add further copper derivatives to the tariff list.

- Strict customs enforcement is ordered, including criminal penalties for underreporting copper content.

Trump’s order seeks to rebuild America’s copper industrial base, strengthen supply chain resilience, accelerate domestic production and investment, and reduce the alarming dependence on China for base metals and rare earths (think magnets). It’s a strategic move to prepare for the volatile 2030s, as the global order fractures into a dangerous bipolar world. Securing critical supply chains now is essential to safeguarding the nation’s future.

END

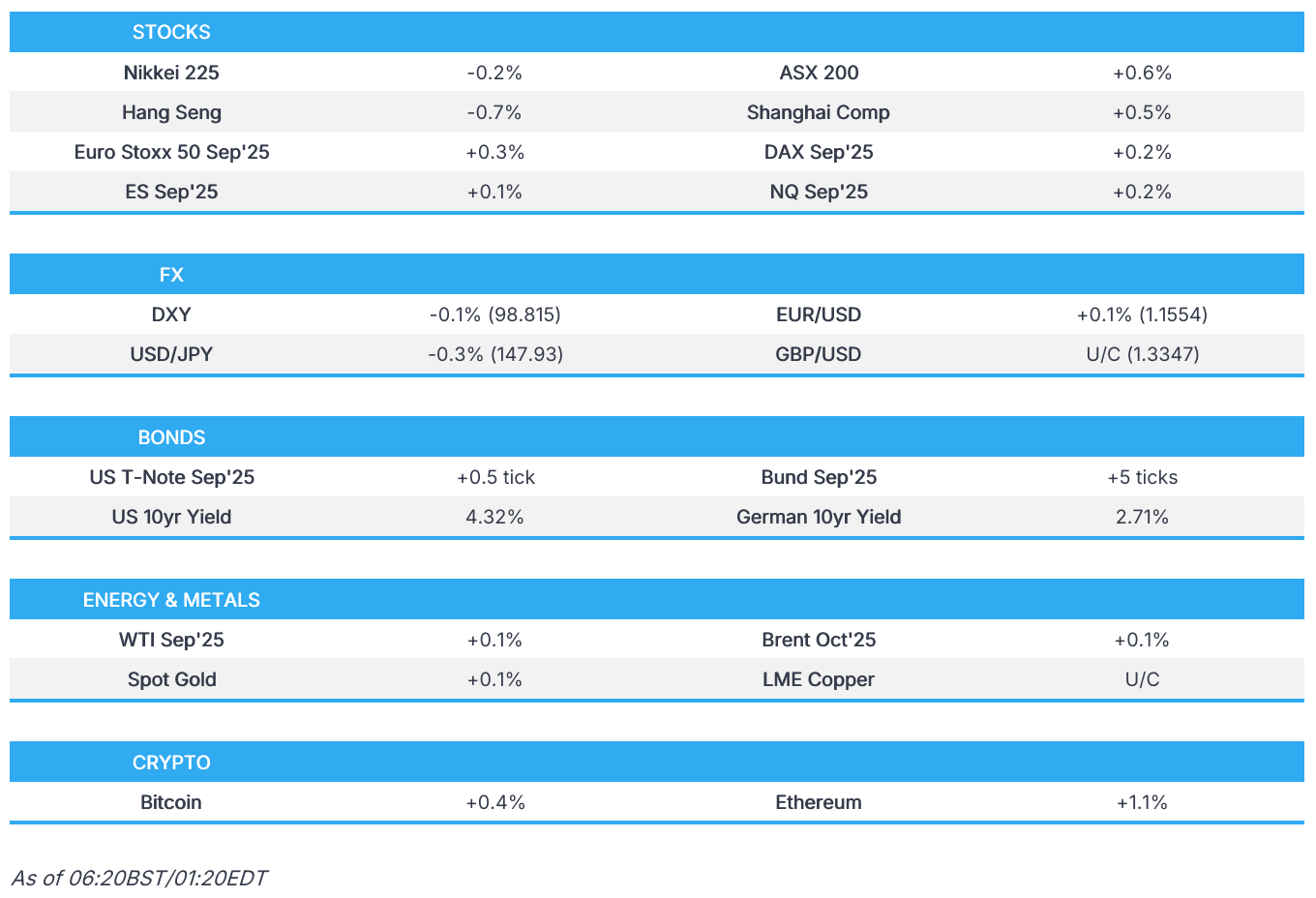

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 6.01 PTS OR 0.17%

//Hang Seng CLOSED DOWN 347.52 PTS OR 1.36%

// Nikkei CLOSED DOWN 19.85 PTS OR 0.05% //Australia’s all ordinaries CLOSED UP 0.54%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1813 OFFSHORE CLOSED DOWN AT 7.1876/ Oil UP TO 69.22 dollars per barrel for WTI and BRENT UP TO 72.54 Stocks in Europe OPENED ALL MOSTLY MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1813 AND WEAKER//OFF SHORE YUAN TRADING UP TO 7.1876 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1813 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.1876

HANG SENG CLOSED DOWN 347.52 PTS OR 1.36%

2. Nikkei closed DOWN 19.85 PTS OR 0.05%

3. Europe stocks SO FAR: ALL MOSTLY MIXED

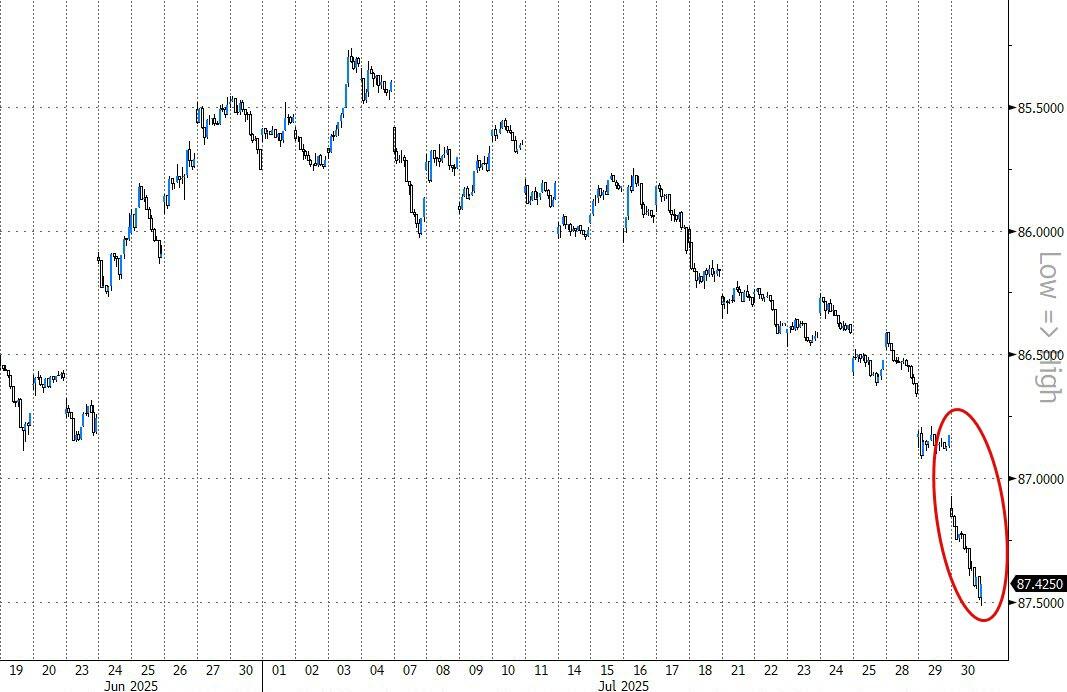

USA dollar INDEX DOWN TO 98.63/ EURO RISES TO 1.15562 UP 2 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.553//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.08…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6750/Italian 10 Yr bond yield DOWN to 3.520 SPAIN 10 YR BOND YIELD DOWN TO 3.257%

3i Greek 10 year bond yield DOWN TO 3.377

3j Gold at $3331.70 Silver at: 38.10 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 27 /100 roubles/dollar; ROUBLE AT 82.37

3m oil (WTI) into the 69 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.08// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.553% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8045 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9293 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.326 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.867 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 3.873 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.58

10 YR UK BOND YIELD: 4.5940 DOWN 6 PTS

10 YR CANADA BOND YIELD: 3.473 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 3.037 DOWN 0 PTS

2a New York OPENING REPORT

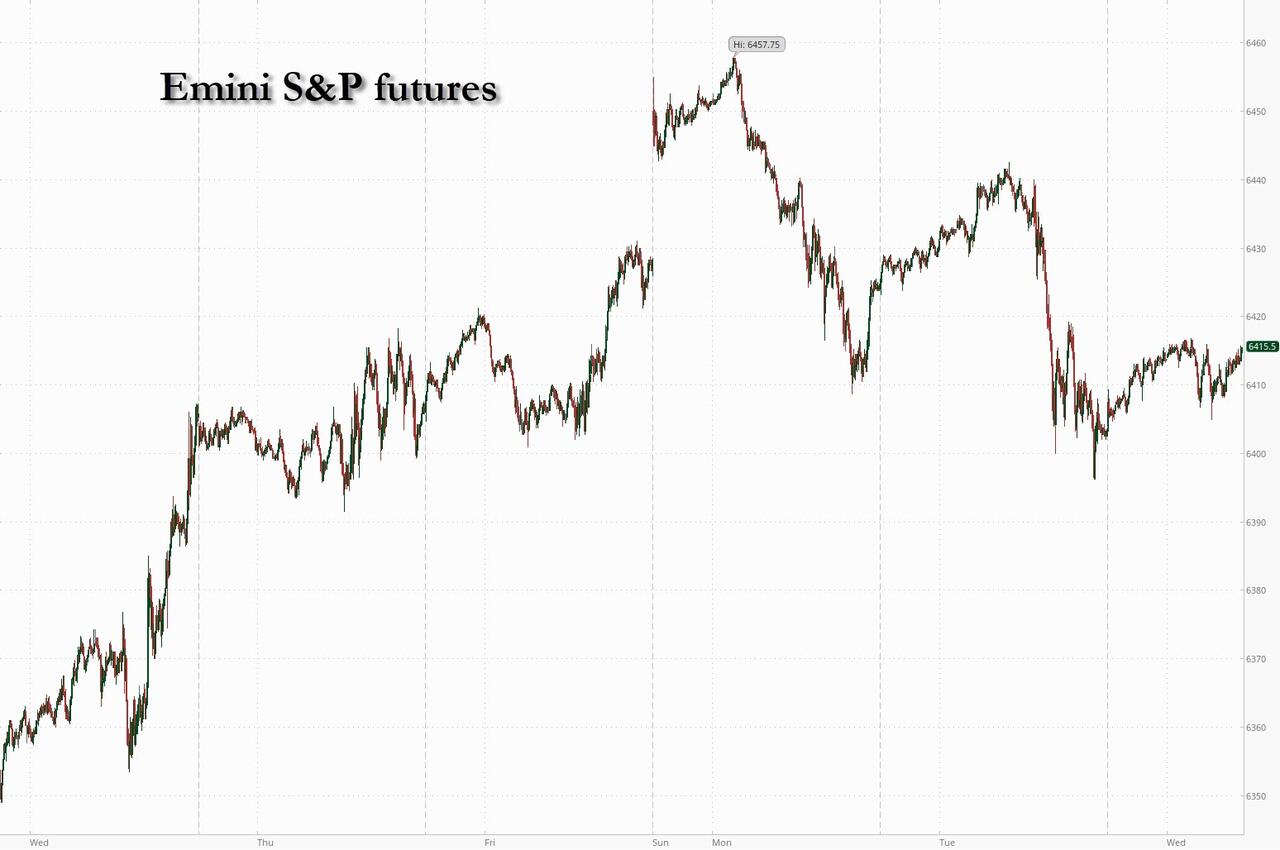

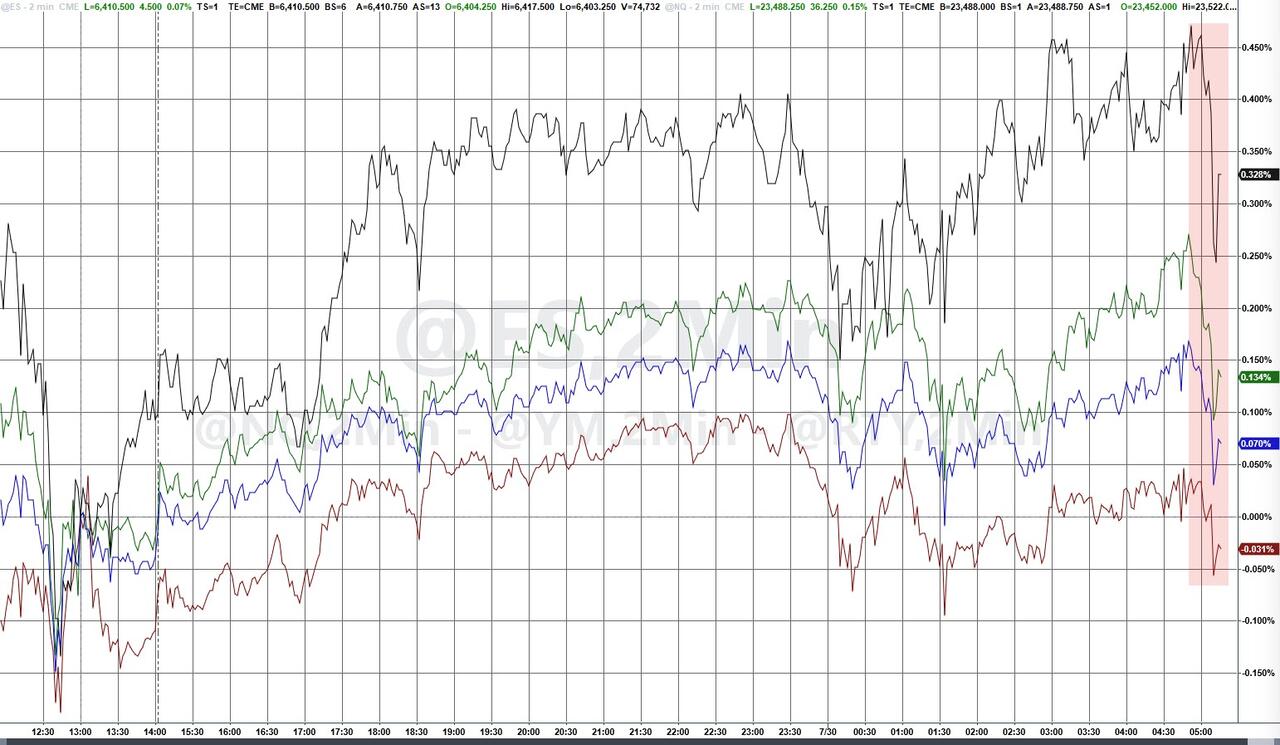

Futures Rise Ahead Of Huge Day: Fed, Mag7 Earnings, Refunding, GDP And More

Wednesday, Jul 30, 2025 – 07:52 AM

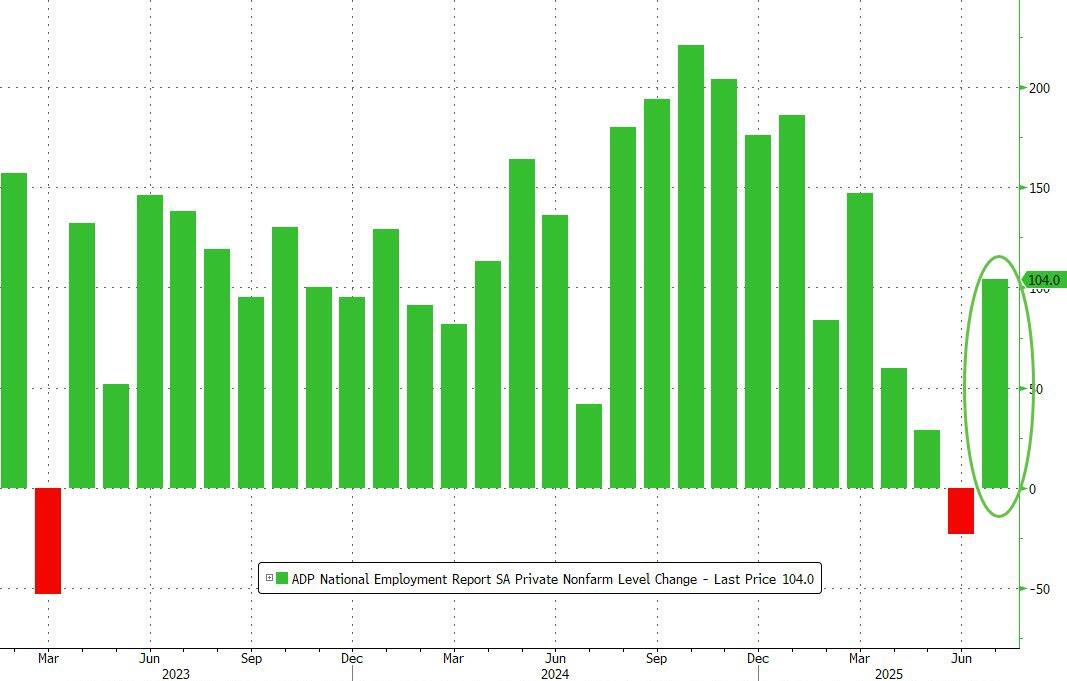

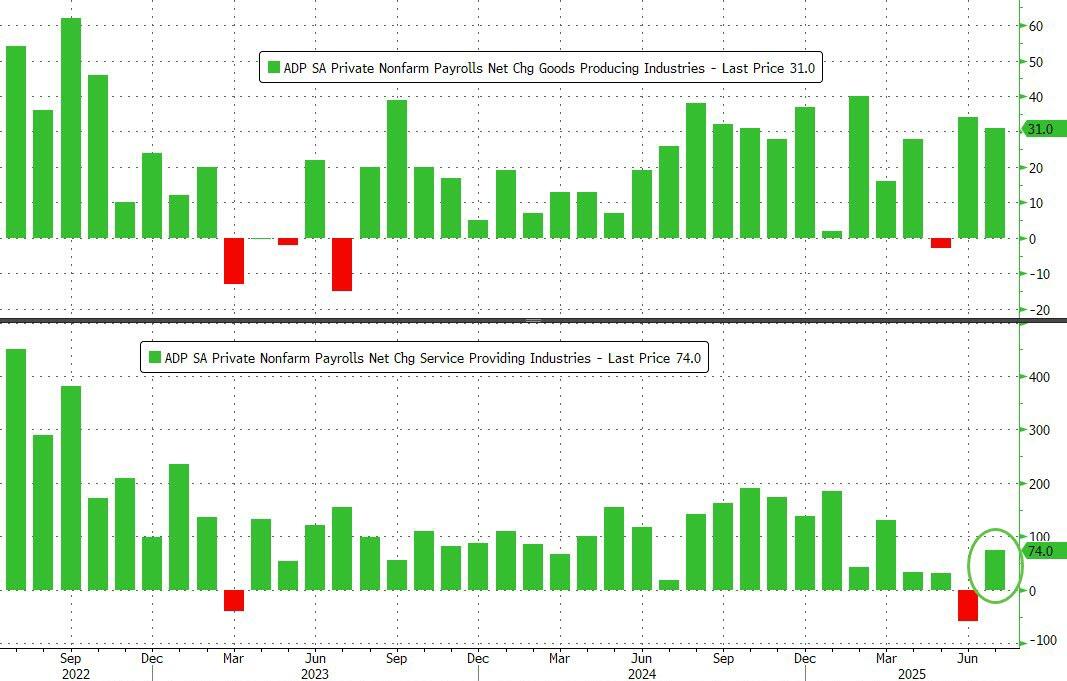

US equity futures were modestly higher in the hours before Wednesday’s Fed rate decision (where Powell is expected to keep rates unchanged) as traders also braced for the restart of Mag7 earnings with META and MSFT reporting after the close, while also bracing for an avalanche of macro news. As of 7:45am, S&P 500 futures rose 0.1% and Nasdaq 100 contracts add 0.2%, with all Mag7 names (ex-GOOG) higher premarket with Semis also bid up.Expectations are for the Fed to hold rates steady, with as much as 2 governor dissents (for the first time since 1993), with a focus on the Powell press conference for any hints of what the Fed will do in Sept. The Treasury’s refunding announcement is today which may add some bond vol. The yield curve is seeing bear steeping (10Y trading 4.33%, up 1bps) with the Bloomberg Dollar Index snapping a 4-day rally that followed trade pacts with the European Union and Japan. Commodities are mixed with profit-taking in Energy, Ags/Base higher, and gold up but silver down. There is a flood of data: first at 8:30am, we get US GDP (Q2 advance; consensus +2.4%, last -0.5), ADP employment (GS +90k, consensus +80k, last -33k), and Treasury QRA (GIR sees a 50–100% increase in buybacks. The key: a) Will coupon sizes be reduced? (low chance) b) How much of the buyback is aimed at long-dated paper? This afternoon, all eyes are on FOMC decision (no change expected // watch for 2 dissenters in Bowman + Waller // mkt pricing in 1.86 cuts through YE). Tonight, watching MSFT + META earnings (positioning in both remains elevated).

In premarket trading, Meta leads gains among Mag 7 ahead of its earnings report. Microsoft is also slated to report after the market closes (Meta +1.%, Nvidia +0.5%, Tesla +0.2%, Microsoft +0.3%, Apple +0.2%, Amazon +0.1%, Alphabet -0.1%). Here are some other notable premarket movers:

- AtriCure (ATRC) jump 10% after the medical-device firm forecast full-year adjusted Ebitda and revenue ahead of Wall Street’s expectations.

- Etsy (ETSY) climbs 6% after the online marketplace for crafts and vintage items posted 2Q gross merchandise sales that beat the average analyst estimate.

- Harley-Davidson (HOG) rises 8% after the motorcycle company also confirmed a deal where HDFS agreed to sell a 4.9% interest to KKR and PIMCO.

- Humana (HUM) rises 7% after the health insurer raised its profit guidance for the year, bucking a trend in the US health-insurance industry after most other companies cut their forecasts in recent months.

- LendingClub (LC) soars 24% after the financial services company forecast new originations for the third quarter, and its guidance beat the average analyst estimate. JPMorgan and Piper Sandler raise their price targets for the stock.

- Mondelez International Inc. (MDLZ) slips 1% after management said unease around the economy drove a bigger-than-expected decline in North American sales in the second quarter.

- Peloton Interactive (PTON) shares rise 7% after UBS upgraded to buy, citing upside to full-year 2026 Ebitda expectation supported by top line growth and further cost cuts.

- Qorvo (QRVO) rises 9% after the Apple supplier reported stronger-than-expected earnings and gave an upbeat forecast.

- Seagate Technology (STX) falls 6% after the computer-hardware manufacturer gave an outlook that was described as disappointing. It also reported fourth-quarter results that beat expectations.

- SoFi Technologies Inc. (SOFI) drops 8% after the provider of consumer financial services said it’s selling $1.5 billion of stock.

- Starbucks (SBUX) is up 4% after the coffee chain reported net revenue for the third quarter that beat the average analyst estimate. The report also showed that comparable sales came in better-than-expected in China and North America, two of the company’s key markets.

- Teradyne (TER) rises 6% after the chip manufacturer reported adjusted earnings per share for the second quarter that beat the average analyst estimate. Analysts noted that management now sees greater visibility into the second half of the year.

- VF Corp. (VFC) soars 15% after the the apparel and shoe company reported fiscal first-quarter earnings that beat Wall Street expectations, signaling that turnaround efforts are beginning to show results.

- Visa Inc. (V) is down 1.5% after the world’s biggest payments network left its earning outlook unchanged for the rest of the fiscal year.

In other corporate news, Tesla is said to have signed a $4.3 billion agreement to source lithium iron phosphate batteries from LG Energy in the second tie-up for the EV maker in South Korea this month. Anthropic is said to be nearing a deal to raise as much as $5 billion in a new round of funding that would value the AI startup at $170 billion.

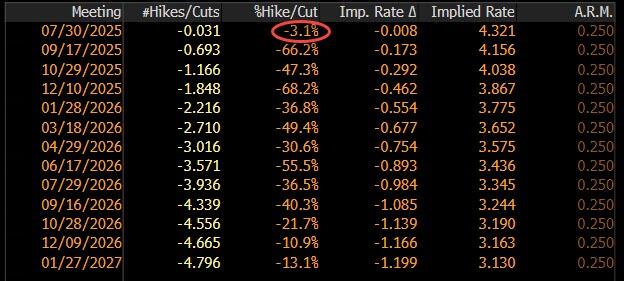

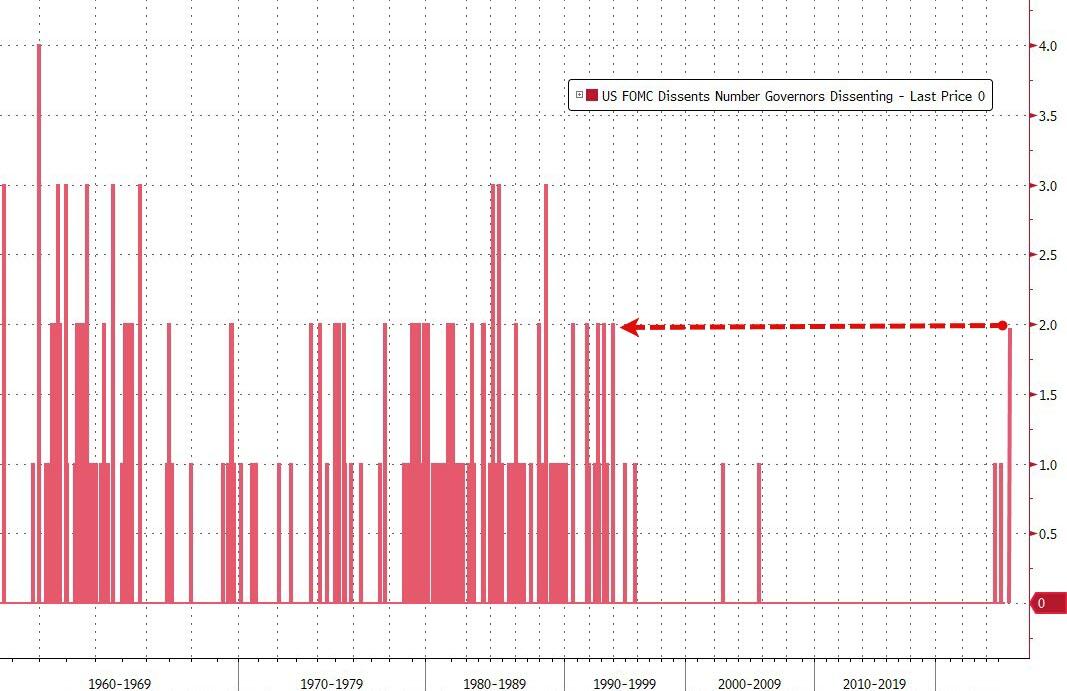

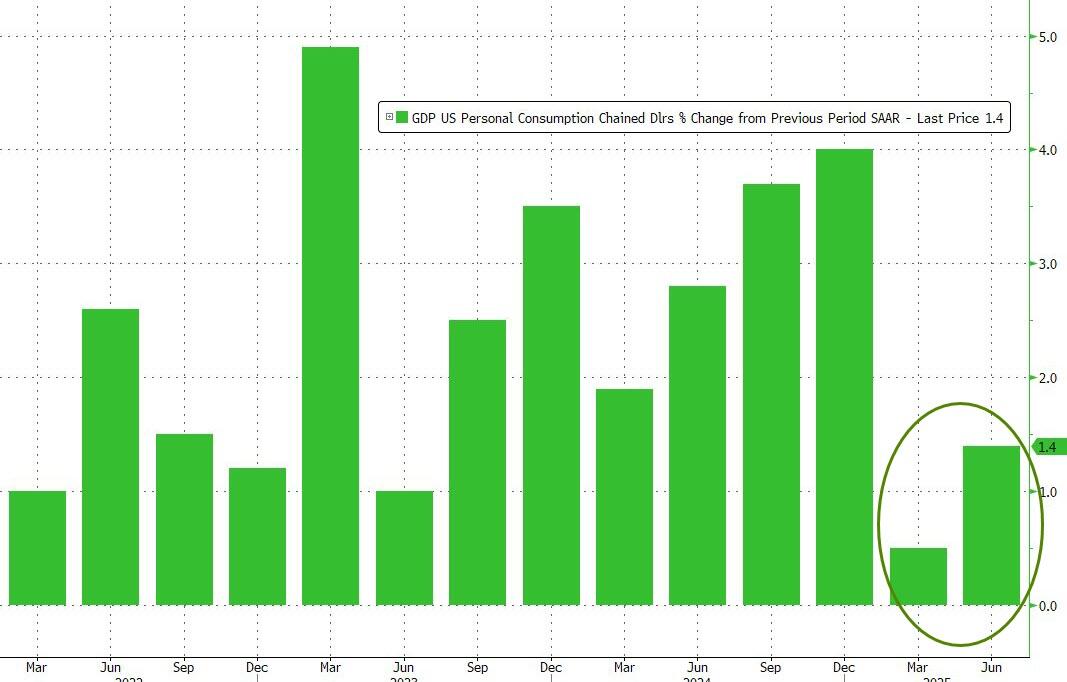

The Fed is almost unanimously expected to hold rates steady for a fifth consecutive meeting in the face of sustained pressure from President Donald Trump on Powell to lower borrowing costs, but watch out for the number of dissenting rate-setters and Chair Jerome Powell’s commentary, as well as Trump’s undoubtedly angry response to it all. There is just a 3% market implied chance of a 25 rate cut today (our full preview is here).

Investors will watch for any signs of a greater openness from the Fed to easing when it next gathers in September as they take stock of the number of dissenting policymakers. Swap markets have priced around 100 basis points of easing over the next 12 months.

“They’ll want to see what happens on the inflation side, so the speed of those cuts may not be as much as risk assets might want,” Priya Misra, portfolio manager at J.P. Morgan Asset Management, told Bloomberg TV. “Interest rates are still restrictive. How much do they need to cut to get into accomodative territory? They have to cut a lot.”

Inflation and jobs data since the Fed’s June meeting, as well as trade-policy developments, haven’t moved the Fed any closer to a cut, according to Bloomberg Economics’ Anna Wong, “If anything, the core PCE inflation data release due July 31 — which we expect to be a hot print – and July’s nonfarm payrolls, due Aug. 1 and also likely to be strong — may divide the committee even further,” she wrote.

Before the Fed, GDP figures will offer an update on the health of the American economy in the buildup to Friday’s key payrolls report. The relentless rush of big earnings continues in the US later, with Microsoft and Meta both reporting. Theire results will be a crucial barometer for growth stocks — which have supercharged gains for US equities this year. Meta’s ad impressions and pricing could see some pressure amid a spending pullback among Chinese advertisers, according to Bloomberg Intelligence. Microsoft is expected to post a 14% rise in sales when it reports results Wednesday, driven by growth in its Azure cloud-computing unit.

“Earnings and data matter more than Wednesday’s Fed meeting, and that’s why stocks will likely nudge higher again this week, despite any possible short-term disruption from the central bank decision” said BBG macro strategist Mark Cudmore. “This year is primarily about trade policy, and the most important issue for markets and consumers is, when will the impact of tariffs show up in prices and profits? It’s the answer to that question that will dictate the future US rate path more than any sell-side generated excitement over the number of dissents.”

On the trade front, there were signs of rapprochement between the US and China. Trump is set to make the final call on maintaining their tariff truce before it expires in two weeks, an extension that would mark a continued stabilization in ties between the world’s two biggest economies. Chinese trade negotiator Li Chenggang told reporters in Stockholm the two sides had agreed to prolong the pause, without providing further details.

“It’s clear both sides want to do a deal,” said Justin Onuekwusi, chief investment officer at St James’s Place in London. “That willingness at the moment is enough to appease markets.”

Elsewhere, the US West Coast and countries in the Pacific braced for tsunamis in the wake of a powerful earthquake in Russia’s Far East, although the initial waves to hit Japan were small. The yen gained 0.4% against the dollar after a tsunami warning for areas including the Tokyo Bay.

According to Barclays strateeegists, the US stock rally has been fueled by retail traders, while institutional buying has been more measured. CTA and vol target funds’ exposure has increased only modestly, suggesting more room for upside, while hedge funds trimmed long bets.

In Europe, the Euro Stoxx 600 edges higher, reversing earlier losses after data showed the euro-area economy unexpectedly grew in the second quarter. Gains in consumer goods, food, and construction offset losses in chemicals and retail. Mercedes-Benz and Porsche fall after cutting profit forecasts, citing tariff pressure, while HSBC drags on banks after missing estimates. Luxury group Kering and food giant Danone jumped following their respective earnings, while HSBC and Adidas fell on theirs. Amplifon plunges most on record after posting weak results and cutting its full-year outlook. Here are the biggest movers Wednesday:

- Danone rises 7.3% after the packaged food company reported recurring operating income for the first half-year that met the average analyst estimate. Analysts view outperformance in Specialized Nutrition as key to strong results

- Kering shares jumped as much as 4.8% after the luxury-goods maker reported better-than-expected operating profit. Sales however plunged at its key unit Gucci which is undergoing a second design revamp in three years

- JDE Peet’s shares gained as much as 13%, the most since October, after the coffee company reported revenue for the first half-year that beat the average analyst estimate and raised its outlook

- Grifols shares jumped as much as 10% as the Spanish blood plasma company resumed dividend payment after four years and beat 2Q estimates; Renta 4 says company continues to demonstrate strength in underlying business

- Porsche shares rise as much as 4.1% as analysts highlight free cash flow and revenue strength in second-quarter results, despite another outlook cut. Shares are still down more than 20% so far this year

- L’Oreal shares rise as much as 2.9% to the highest in almost eight weeks, reversing a fall in early trading. Analysts note significant phasing effects which impacted the cosmetics company’s second quarter results

- Nexans shares gained as much as 6.2% to highest level since November, after cable manufacturer reported earnings that analysts say are strong and boosted its adjusted Ebitda guidance for the full year

- Amplifon plunges as much as 27%, their biggest drop on record, after the hearing care specialist posted results significantly below expectations and cut its FY outlook. Banca Akros and Mediobanca both downgraded the stock

- Adidas plunges as much as 8.6% after the footwear giant reported weaker than expected revenue growth which offset a margin beat. The lack of guidance upgrade is said to be driven by increased tariff uncertainty

- HSBC slumps 5.1% in London trading, the worst performing stock among Stoxx 600 banks, after its 2Q pretax profit missed the consensus analyst estimate. The lender reported an increase in expenses and took a $2.1b impairment

- Inficon shares fall as much as 10% after the Swiss vacuum instruments maker reported second-quarter earnings that missed estimates, and cut its operating margin forecast for the year

- AUTO1 shares fall as much as 4.8% as the firm’s guidance raise failed to enthuse the market, with the stock already up over 50% this year, with UBS noting the company’s investments in Autohero, though Ebitda still beat estimates

Earlier in the session, Asian stocks eked out small gains as investors looked past some tariff developments and turned their focus to key monetary policy decisions from Japan and the US. The MSCI Asia Pacific Index gained as much as 0.6%, poised to snap a three-day decline, with chipmakers TSMC and Samsung Electronics among the top contributors. Equities advanced in tech-heavy South Korea and Taiwan. The regional benchmark has slipped slightly after climbing to a four-year high last week. Markets in Hong Kong traded lower as trade talks between Beijing and Washington were set to continue ahead of the expiry of a tariff truce in two weeks. Adding an extra 90 days is one option, Treasury Secretary Scott Bessent said, while President Donald Trump will make the final call. Separately, the US also said that India may be hit with a tariff rate of 20% to 25%. Stocks were mixed in Tokyo ahead of Bank of Japan’s policy decision Thursday. The central bank is expected to keep rates unchanged this time, while the market gauges prospects for another hike this year. Investors have also moved to the sidelines as they await the August 1 tariff deadline after Japan forged a trade deal with the US last week.

In FX, the Bloomberg Dollar Spot Index slips 0.1%. The yen leads G-10 FX, up 0.3% against the dollar, while the Aussie lags, down 0.2% after softer-than-expected inflation.

In rates, treasuries dip ahead of the quarterly refunding and Fed decision, with US 10-year yields up 1bp to 4.33%.

Bunds hold gains, with German 10-year yields down 2bps to 2.69%. Gilts outperform, pushing UK 10-year yields 4bps lower.

In commodities, oil falls 0.6%, with WTI near $68.80, while spot gold gains $6 to around $3,332/oz.

Bitcoin is a little lower and trades just above the USD 118k mark; Ethereum posts deeper losses and holds just above USD 3.8k.

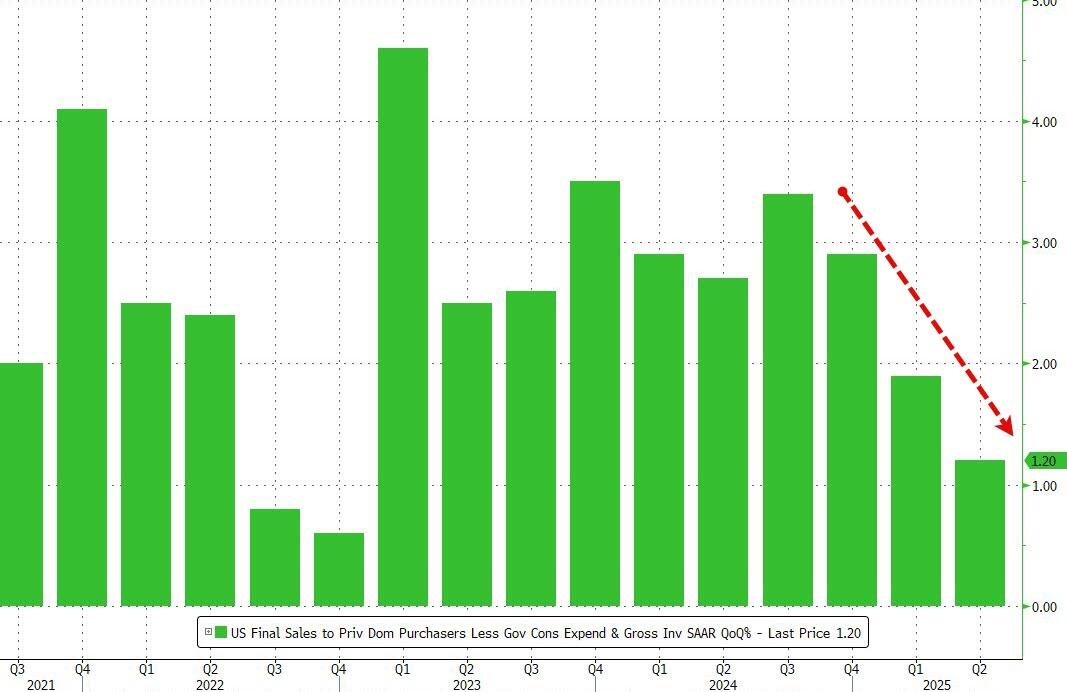

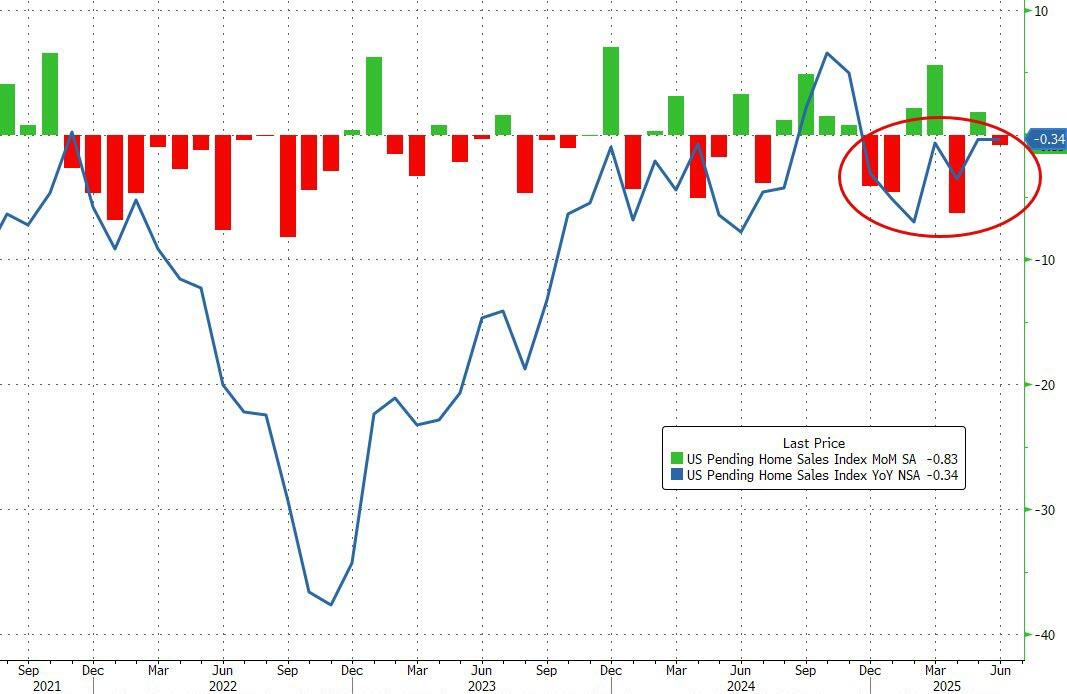

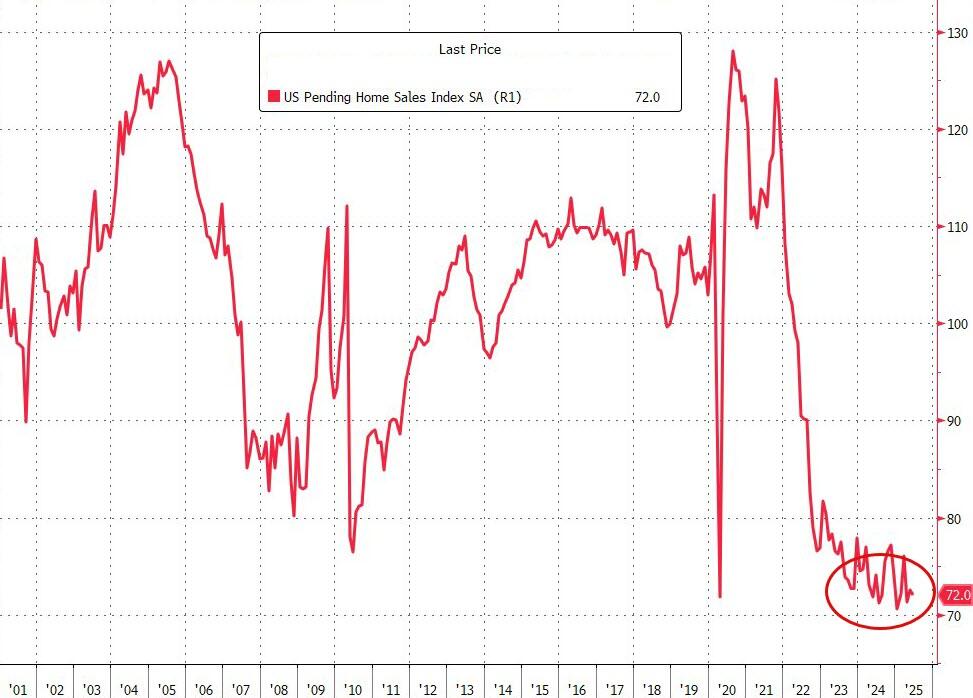

Looking ahead to today, the main event will be the Fed rate decision at 2pm ET. Before the decision, the main data releases will be the ADP’s employment change data for July at 8:15am. At 8:30am, markets will pay close attention to readings of GDP, personal consumption and core personal consumption expenditures prices for the second quarter. Pending home sales for June are due at 10am, before the day’s main event — the Fed’s latest policy decision at 2pm. On the earnings side, we will hear from two of the Mag-7 with Microsoft and Meta reporting after the US close. Other US results include Qualcomm and Ford, while in Europe the highlights include Airbus, BAE, Mercedes-Benz and Porsche

Market Snapshot

- S&P 500 mini +0.1%,

- Nasdaq 100 mini +0.2%,

- Russell 2000 mini +0.4%

- Stoxx Europe 600 little changed,

- DAX little changed

- CAC 40 +0.5%

- 10-year Treasury yield +1 basis point at 4.33%

- VIX -0.1 points at 15.88

- Bloomberg Dollar Index little changed at 1209.31

- euro little changed at $1.1552

- WTI crude -0.5% at $68.89/barrel

Top Overnight News

- Tsunami waves of 3.6ft seen at Crescent City in California, according to NTWC.

- The Fed is expected to hold rates, despite Donald Trump’s calls for cuts. Any policymaker dissent may send the message that some prefer to cut sooner rather than later, but with an onslaught of data due before their next meeting, Jerome Powell will probably keep his options open. BBG

- Chinese leaders signaled they would refrain from rolling out more major stimulus for now, as authorities pivot to addressing excess capacity in the economy. Instead of announcing more policy support to bolster growth, the ruling Communist Party’s Politburo, pledged Wednesday to better execute policies that are already in place. WSJ

- Trump’s recent trade deals with Japan and the EU boast big investment numbers, but lack crucial details, raising questions about the deals’ true impact. BBG

- L/S hedge funds have made a comeback during this year’s market turbulence, with sizeable gains helping attract fresh cash from investors after nearly a decade of outflows. These funds took in $10bn from investors in the first half of the year, following more than $120bn of withdrawals since 2016. FT

- China’s gold-backed ETFs are seeing record outflows this month as investors shift into local equities. BBG

- Australia’s inflation continued to ease in the second quarter, raising bets that the central bank will deliver its third interest rate cut next month. WSJ

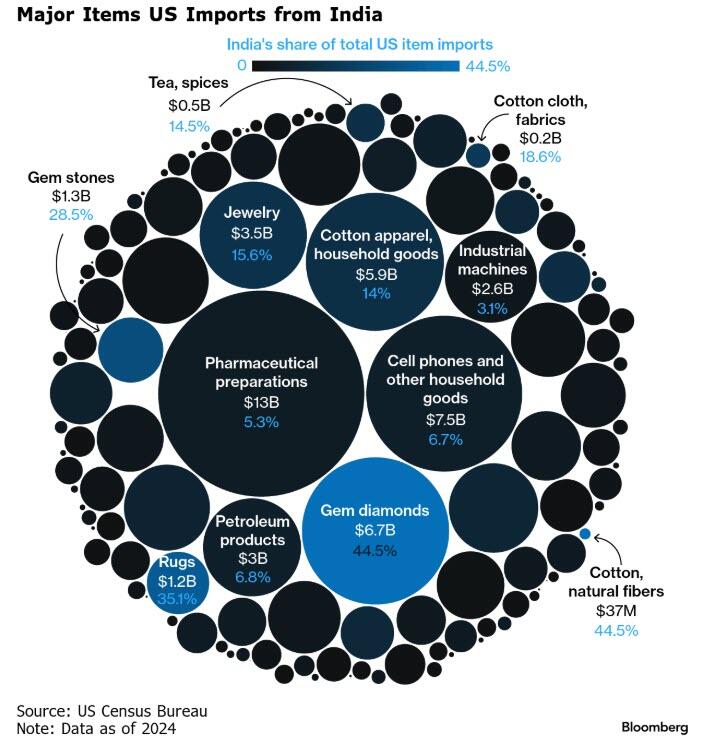

- India is skeptical it can reach a deal w/the US by the 8/1 deadline and plans to continue negotiating even if its hit w/higher tariffs for a period of time. BBG