SORRY FOR BEING LATE: HAD TO ME MY EYE DR.

we are now beginning to deal with OTC/London LBMA options expiry Friday July 31

as always the crooks raid gold/silver so be careful!!. The reason is suppress the price

due to huge derivative losses endured the banks. Do not fear the raids.

platinum ..OFF THE CHART//29.5%

gold: 6.0%

silver lease rate today//6.5%

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2024: 3549 CONTRACTs NOTICES FOR 354,900 OZ or 15.304 TONNES

total notices so far: 15,304 contracts for 1,530,400 OR 47.601 tonnes)

SILVER NOTICES: 918 NOTICE(S) FILED FOR 4.590 million OZ/

total number of notices filed so far this month : 918 CONTRACTS (NOTICES) for 4/590 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST:

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ

AUGUST: 60.547 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES//STILL QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 4555 CONTRACTS OI TO 165,774 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 760 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 760 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 650 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 4555 CONTRACTS AND ADD TO THE 760 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF 3795 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE LOSS IN PRICE OF $0.54 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 18.975 MILLION PAPER OZ

OCCURRED WITH OUR $0.54 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED DOWN 42.51 PTS OR 1.18%

//Hang Seng CLOSED DOWN 377.91 PTS OR 1.50%

// Nikkei CLOSED UP 415.12 PTS OR 1.02% //Australia’s all ordinaries CLOSED DOWN 0.18%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1927 OFFSHORE CLOSED DOWN AT 7.2004/ Oil UP TO 69.97 dollars per barrel for WTI and BRENT UP TO 72.44 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1927 AND WEAKER//OFF SHORE YUAN TRADING UP TO 7.2004 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3011 CONTRACTS TO 442,248 OI WITH OUR STRONG LOSS IN PRICE OF $27.50 WITH RESPECT TO WEDNESDAY’S // TRADING.. WE LOST ZERO NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2450 ). WE HAD HUGE T.A.S. LIQUIDATION //TUESDAY TRADING AS WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 561 CONTRACTS WITH ALL OF THAT LOSS DUE TO BOTH SPREADERS, THE T.A.S. LIQUIDATION AND MONTHLY SPREADERS.

LAST WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN TUESDAY NIGHT/WEDNESDAY THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. OR IT COULD BE THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY!!.THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY IS NOW 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 0 SO FAR

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS GENERALLY THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE OR FRBNY FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 6TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH JULY WITH A TWO MONTH HIATUS)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A SMALL SIZED LOSS ON OUR TWO EXCHANGES OF 561 CONTRACTS WITH OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN MONDAY THROUGH WEDNESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED ERLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF JUNE AND JULY CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 778 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST FRIDAY’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED YESTERDAY WITH HUGE FURY AS WE APPROACH THE FINAL LONDON/OTC OPTION EXPIRY. (IT ENDS TODAY AT AROUND 11 AM)

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS(ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. NOW IN JULY WE HAVE HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 233 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NONE COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2450 EFP CONTRACT WAS ISSUED: : /AUGUST 2450 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2450 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- HUGE LIQUIDATION OF OUR T.A.S. SPREADERS//WEDNESDAY AND THEY WERE JOINED BY OUR MONTHLY SPREADER LIQUIDATION

- ZERO NET SPEC LIQUIDATION DESPITE OUR STRONG LOSS IN PRICE AS TOTAL LOSS IN OI ON OUR TWO EXCHANGES WAS DUE TO OUR TWO SPREADERS.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY WAS A SMALL SIZED SIZED 778 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS PAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S HUGE LOSS IN PRICE IN GOLD AND SILVER AND A CORRESPONDING LIQUIDATION OF SOME COMEX OI. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH THE RARE TWO ISSUANCES OF EXCHANGE FOR RISK! THE RAIDS THROUGHOUT OPTION EXPIRY WEEK WERE USED TO LOWER THE HUGE DERIVATIVE LOSSES ENDURED BY THE BANKERS.

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A STRONG $27.50/ /) AND BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A SMALL SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION AND MONTH END SPREADER LIQUIDATION ////WEDNESDAY WHICH ACCOUNTS FOR THE LOSS IN TOTAL OI. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE STRONG T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE!

THURSDAYS MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: 0 so far!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE LOST A FAIR SIZED TOTAL OF 1.740 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $27.50

WE HAD A SMALL 297 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 561 CONTRACTS OR 56100 0Z (1.740 TONNES)

confirmed volume WEDNESDAY 252,423 contracts// strong

speculators have left the gold arena

END

INITIAL GOLD COMEX

AUGUSST CONTRACT MONTH

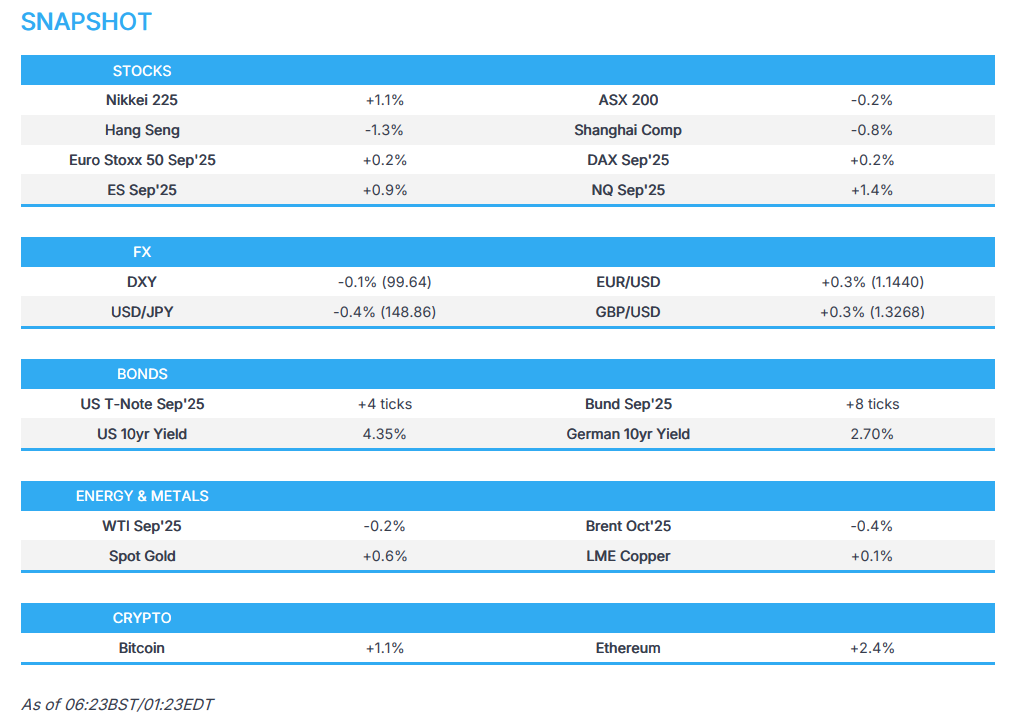

JULY 31/2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entry . |

| Deposit to the Dealer Inventory in oz | 1 ENTRIES i) Into Brinks dealer 124,038.558 oz (3898 kilobars total deposit: 124,03.558 oz 3.898 tonnes |

| Deposits to the Customer Inventory, in oz | 2 ENTRIES i) Into Loomis 4822.65 oz 150 kilobars ii) Into Malca: 32,115.000 oz (1000 kilobars) total deposit: 36,973.650oz or 1.150 tonnes total gold deposit dealer and customer; 5.03 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 15,304 notice(s) 0000 OZ 0.0 TONNES |

| No of oz to be served (notices) | 4162 contracts 416,200 OZ 12.945 TONNES |

| Total monthly oz gold served (contracts) so far this month | 15,304 notices 1,530,400 oz 47.601 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

1 ENTRIES

i) Into Brinks dealer 124,038.558 oz (3898 kilobars

total deposit: 124,03.558 oz

3.898 tonnes

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

2 ENTRIES

i) Into Loomis 4822.65 oz 150 kilobars

ii) Into Malca: 32,115.000 oz (1000 kilobars)

total deposit: 36,973.650oz or 1.150 tonnes

total gold deposit dealer and customer; 5.03 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0

adjustments: 5

first 4 all dealer to customer

a)Asahi: 6088.672 oz

b) Brinks 65,009.322 oz

c) JPMORGAN: 10,995.642 OZ

LAST TWO CUSTOMER TO DEALER

d) Loomis 29,818.549 oz

e) Malca 134,937.747 oz

AMOUNT OF GOLD STANDING FOR JULY

THE FRONT MONTH OF AUGUST STANDS AT 19,466 CONTRACTS FOR A LOSS OF 7031 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF GOLD WILLING TO STAND IN THIS VERY ACTIVE DELIVERY MONTH OF AUGUST IS AS FOLLOWS:

19,466 CONTRACTS X 100 OZ PER CONTRACT

EQUALS

1,946,600 OZ OR 60.547 TONNES.

SEPT GAINED 59 CONTRACTS TO 4627

OCTOBER LOST 256 CONTRACTS DOWN TO 66,721

We had 15,304 contracts filed for today representing 1,530,400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 15,304 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3549 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (47,601 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 19,466CONTRACTS) minus the number of notices served upon today (15,304 x 100 oz per contract) equals 1,946,600 OZ OR 60.547 TONNES

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (15,304 x 100 oz +we add the difference for front month of AUGUST (19,466 OI} minus the number of notices served upon today (15,304 x 100 oz) which equals 1,946,600OZ OR 60.547 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 60.547 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,757,203.840 oz 54.765 tonnes declining rapidly

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,675,473.567 oz

TOTAL REGISTERED GOLD 21,127,636.01 or 657.16 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,547,837.556 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,370,433 oz ((REG GOLD- PLEDGED GOLD)= 602.50tonnes //

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE AUGUST 2025 SILVER CONTRACT//INITIAL

JULY 31

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 ENTRY i) Delaware: 7866.000 oz |

| Deposits to the Dealer Inventory | deposit dealer; one entry i) Into Ashai dealer 589,490.500 oz total deposit 589,490.500 oz |

| Deposits to the Customer Inventory | 2 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into Brinks 225.84.680 oz ii) Into CNT 43,886.120 total deposit: 299,710.800 oz |

| No of oz served today (contracts) | 918 CONTRACT(S) (4.590 MILLION OZ |

| No of oz to be served (notices) | 22 contracts (0.110 MILLION oz) |

| Total monthly oz silver served (contracts) | 918 Contracts (4.590 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

1 ENTRY

i) Into Ashai dealer 589,490.500 oz

total deposit 589,490.500 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into Brinks 225.84.680 oz

ii) Into CNT 43,886.120

total deposit: 299,710.800 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

1 entry

1 ENTRY

i) Delaware: 7866.000 oz

total withdrawal 7866.000 oz

ADJUSTMENTs 1

dealer to customer Brinks

556,882.800 oz

TOTAL REGISTERED SILVER: 191.576 MILLION OZ//.TOTAL REG + ELIGIBLE. 505.219Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 940 OPEN INTEREST CONTRACTS FOR A LOSS OF 91 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER WILLING TO STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST IS AS FOLLOWS:

940 CONTRACTS STANDING X 5000 OZ PER CONTRACT

EQUALS

4.700 MILLION OZ WHICH IS PRETTY GOOD FOR AUGUST.

SEPTEMBER LOST 5498 CONTRACTS DOWN TO 115,827 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 918 or 4.590 MILLION oz

CONFIRMED volume; ON WEDNESDAY 83,381 goood//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 918 X5,000 oz = 4.590 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (940) AND the number of notices served upon today (918 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (918) Notices served so far) x 5000 oz + OI for the front month of AUGUST(940) minus number of notices served upon today (918)x 5000 oz equals silver standing for the AUGUST contract month equating to 4.700 MILLION OZ .

New total standing: 4.70 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 191.576 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/505,219 million. 41.94%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 956.23 TONNES, TONIGHTS TOTAL

SILVER

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 487.852 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

3. CHRIS POWELL AND GATA GOLD DISPATCHES

YPF plaintiffs embark on ‘treasure hunt’ for Argentine central bank’s gold

Submitted by admin on Wed, 2025-07-30 20:33 Section: Daily Dispatches

By Bob Van Voris

Bloomberg News

Wednesday, July 30, 2025

A lawyer representing former YPF SA shareholders told a judge in New York that they’re on a “treasure hunt” for gold bars Argentina’s central bank secretly sent abroad last year.

The shareholders, backed by litigation funding firm Burford Capital, are trying to collect on a $16 billion court judgment resulting from the nation’s 2012 nationalization of YPF. U.S. District Judge Loretta Preska ruled Tuesday that Argentina needed to turn over relevant text messages and emails from Economy Minister Luis Caputo and others.

Seth Levine, a lawyer for the plaintiffs, said at the hearing before Preska that locating the gold was one reason they needed the messages. …

… For the remainder of the report:

end

Play silver’s breakout by donating to GATA

Submitted by admin on Wed, 2025-07-30 20:30 Section: Daily Dispatches

8:28p ET Wednesday, July 30, 2025

Dear Friend of GATA and Gold:

Like gold, silver now seems to be breaking out of its longstanding derivatives clutches engineered by the U.S. government and its investment bank agents. But this largely surreptitious manipulation of the monetary metals markets hasn’t been overthrown yet.

Indeed, it probably won’t be overthrown until the public is invited to attend every proceeding of the Federal Reserve Board, the U.S. Treasury Department, and the Bank for International Settlements. So GATA’s work is unfinished, and free and transparent markes for the monetary metals are not yet secured.

But with silver’s price rising, there’s an especially good way for advocates of the monetary metals to help keep GATA in the fight. That’s by making a donation to GATA of $250 or more, which will entitle the donor to a beautiful 1-ounce silver round commemorating GATA’ work.

Our friends at Money Metals Exchange in Eagle, Idaho, support our struggle so much that they have minted the silver round honoring GATA.

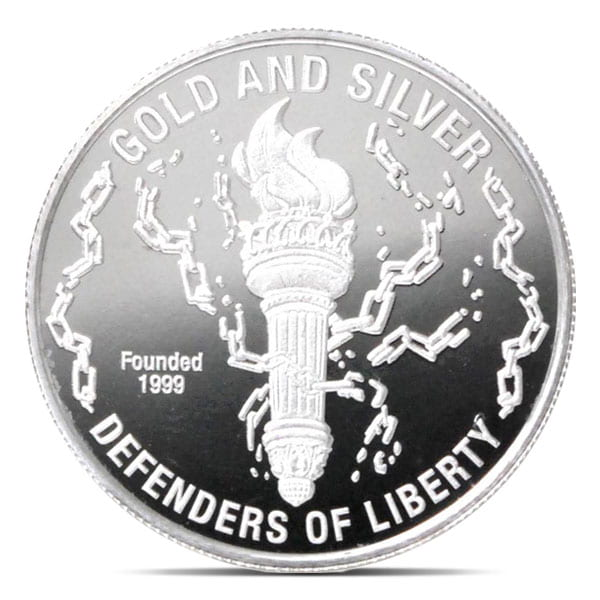

On the front of the round is an engraving copied from the GATA painting by Alain Despert, depicting GATA as a modern-day Don Quixote leading a march of gold and silver advocates on the U.S. Treasury Department building in Washington:

The back of the round shows the torch of liberty breaking the chains of price suppression and recognizing gold and silver as the crucial defenders of liberty:

You can purchase the GATA commemorative silver round directly from Money Metals Exchange for around $41 here:

But if you’d like to help GATA as well, please donate $250 or more and we’ll arrange to have your silver round shipped to you from Money Metals Exchange, which is now the operator of the largest precious metals depository in the United States west of New York, a depository larger than Fort Knox. (By the way — whatever happened to the Trump administration’s planned inspection of Fort Knox to see if the gold it is said to contain is secure? Was the president dissuaded by a confidential warning that the gold is encumbered by some of those derivatives?)

Your gift in any amount will fuel GATA’s important work.

Since GATA is a federally recognized tax-exempt educational and civil rights organization, donations are federally tax-deductible. If you receive a silver round for your donation, the metal value of the round must be subtracted from the federal tax-deductibility of your donation. For example, with the silver round priced at $42, a $250 donation made to GATA would be federally tax-deductible for $208.

To donate, please mail a check payable to GATA to:

Gold Anti-Trust Action Committee Inc.

c/o Chris Powell, Secretary/Treasurer

7 Villa Louisa Road

Manchester, Conn. 06043-7541 USA

Or visit GATA’s internet site here:

Please make sure to let us know your shipping address as well as your e-mail address so we can speed your silver round to you and thank you promptly without incurring the time and expense of surface mail.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Adrian Ash: China ‘buys the dip’ in gold after record ETF outflows

Submitted by admin on Wed, 2025-07-30 20:19 Section: Daily Dispatches

By Adrian Ash

Bullion Vault, London

Wednesday, July 30, 2025

Gold fell again today against a surging U.S. follar, setting its lowest London price in three weeks as headlines proclaiming a sudden flight out of Chinese bullion-backed exchange-traded trust funds preceded the U.S. Federal Reserve’s July interest-rate decision.

After spring 2025 saw record trading into China gold ETFs, “Some investors are taking profits from gold and rotating into equities to chase stronger momentum,” Bloomberg quotes analyst Steve Zhou at Huaan Fund Management Co., issuer of the largest gold ETF available to Chinese investors.

“Retail investors have been the main drivers of the outflows,” Zhou says, highlighting the attraction of swapping into this month’s 5.5% jump in the CSI300 index of Chinese corporate equities.

Mid-month, Asian-listed gold ETFs as a group grew to need the most bullion backing ever, peaking above 324 tonnes according to data compiled and published by the mining industry’s World Gold Council. …

… For the remainder of the analysis:

end

Mike Maharrey: 2021 meme reveals the relentless devaluation of our money

Submitted by admin on Wed, 2025-07-30 09:22 Section: Daily Dispatches

By Mike Maharrey

Money Metals Exchange, Eagle, Idaho

Tuesday, July 29, 2025

I ran across a 2021 meme the other day that vividly illustrates just how quickly the government is destroying your money.

The meme points out that in 1964 the minimum wage was $1.25, or five quarters. That sounds really low, but keep in mind that before 1965, quarters were 90% silver. In 2021 the melt value of those five quarters was $23.34.

In other words the five quarters a minimum-wage worker earned in an hour in 1964 had $23.34 in purchasing power in 2021. There’s your “living wage.”

That’s pretty staggering in and of itself, but now fast-forward a few years. As of today the melt value of those five quarters is $34.45.

In other words, the value (purchasing power) of those five quarters has increased by another 47.6% in just 3 1/2 years!

This reflects the relentless devaluation of U.S. money. …

… For the remainder of the commentary:

Craig Hemke: A lesson in open interest

Submitted by admin on Tue, 2025-07-29 18:34 Section: Daily Dispatches

By Craig Hemke

Sprott Money, Toronto

Tuesday, July 29, 2025

I’ve learned a few things while watching the Comrc precious metals every day for the past 15 years. One lesson involves the timing and scale of new contract issuance during price rallies, and all of us just got reminder of this last week.

Let’s start with a matrix of sorts. What you see below isn’t universally true, but if you watch and record the daily price and open interest (OI) changes for Comex gold and silver, you’ll soon see that it’s about 90% accurate.

Price up, OI up: Speculators are adding longs, while commercials are adding shorts.

Price up, OI down: A short squeeze is likely underway.

Price down, OI down: Speculators are being flushed out, and commercials are covering shorts.

Price down, OI up: Someone is aggressively shorting, driving prices lower. …

… For the remainder of the analysis:

end

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 233

5. COMMODITY REPORT..RARE EARTHS

/Myanmar’s Kachin State Is At The Center Of The Sino-US Scramble For Rare Earths

this area is loaded with rare earths. the USA seeks influence in this area over the dominance of China

(Korybko)

Wednesday, Jul 30, 2025 – 11:25 PM

Authored by Andrew Korybko via Substack,

The US seeks influence over this region that supplies much of neighboring China’s rare earth industry…

Western media has published a spree of articles raising awareness of the important role that Myanmar’s Kachin State plays in the global rare earth minerals industry.

The latest phase of that country’s long-running civil war, which is more complex than most Western and non-Western accounts alike make it seem as explained here in February 2024, has seen regional separatists take control of sites that produce roughly half of the world’s heavy rare earths.

Here are five of those aforementioned reports about this:

* 28 March: “Insight: Myanmar rebels disrupt China rare earth trade, sparking regional scramble”

* 23 June: “How war-torn Myanmar plays a critical role in China’s rare earth dominance”

* 8 July: “Exclusive: Why China’s ultimatum to Myanmar rebels threatens global supply of heavy rare earths”

* 11 July: “What to Know About the Rush for Rare Earth Metals in War-Torn Myanmar”

* 18 July: “A Rebel Army Is Building a Rare-Earth Empire on China’s Border”

To summarize, the Kachin Independence Army (KIA) is trying to expand control over its eponymous state, which threatens the ruling military authorities with whom they’ve been at war for decades. China has reportedly demanded that they halt their offensive otherwise it’ll curtail imports of their rare earths. This could in turn destabilize global supply chains if the KIA doesn’t comply and China carries through on its ultimatum since China has a near-monopoly on processing these resources.

It’s within this context that the US just lifted sanctions on some of the ruling junta’s allies. By alleviating some of the pressure that it placed upon them since they reassumed power over the country in early 2021 following disputed parliamentary elections several months prior, which sparked the latest round of what’s by far the world’s longest-running civil war, the US seems to be signaling interest in a deal. All pressure could possibly be removed if Myanmar (con)federalizes and gives the US influence over Kachin.

Myanmar might be tempted to consider this seeing as how the armed forces have been on the backfoot for nearly the past two years. It’s also so concerned about becoming disproportionately dependent on China that it comprehensively expanded ties with Russia as a means of hedging against that scenario. An American-brokered political-resource deal might therefore keep the generals in power and lead to Myanmar diversifying its Chinese balancing act by having the US complement Russia’s role in this regard.

The Sino-US scramble for rare earths, which Russian Foreign Ministry spokeswoman Maria Zakharova assessed to be part of the AI-driven ‘tech race’, is a top US foreign policy priority. It’s accordingly more important for the US to obtain control over these resources or at least influence over China’s suppliers, such as what it’s seeking to do through the peace deal that it recently brokered between the Democratic Republic of the Congo and Rwanda as explained here, than to “spread democracy” in Myanmar.

This grand strategic imperative accounts for the US’ unexpected lifting of sanctions on some of the ruling junta’s allies, which comes amidst Western media’s spree of articles raising wider awareness of the important role that Myanmar’s Kachin State plays in the global rare earth minerals industry. Those reports help precondition the Western public to understand why the US might soon sacrifice the prior administration’s “democracy” goals in Myanmar by cutting a political-resource deal with the generals.

end

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED DOWN 42.51 PTS OR 1.18%

//Hang Seng CLOSED DOWN 377.91 PTS OR 1.50%

// Nikkei CLOSED UP 415.12 PTS OR 1.02% //Australia’s all ordinaries CLOSED DOWN 0.18%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1927 OFFSHORE CLOSED DOWN AT 7.2004/ Oil UP TO 69.97 dollars per barrel for WTI and BRENT UP TO 72.44 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1927 AND WEAKER//OFF SHORE YUAN TRADING UP TO 7.2004 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1927 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.2004

HANG SENG CLOSED DOWN 377.91 PTS OR 1.50%

2. Nikkei closed UP 415.12 PTS OR 1.02%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 98.54/ EURO RISES TO 1.1438 UP 2 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.558//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 149.45…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6890/Italian 10 Yr bond yield DOWN to 3.527 SPAIN 10 YR BOND YIELD DOWN TO 3.269%

3i Greek 10 year bond yield DOWN TO 3.382

3j Gold at $3305.70 Silver at: 36.95 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 39 /100 roubles/dollar; ROUBLE AT 81.61

3m oil (WTI) into the 69 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149.45// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.558% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8129 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9299 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.346 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.871 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.930 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.59

10 YR UK BOND YIELD: 4.5740 DOWN 4 PTS

10 YR CANADA BOND YIELD: 3.489 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 3.043 DOWN 0 PTS

2a New York OPENING REPORT

Futures Storm To Another Record High After Blowout Tech Earnings

Thursday, Jul 31, 2025 – 08:24 AM

“Powell hawkish, QRA a damp squib. Just when it felt darkest, MSFT and META came to the rescue.” That’s how Goldman Delta-1 head Rich Privorotsky summarized overnight events in his overnight wrap and boy was he right: US equity futures are soaring deep into record territory following blowout earnings from META and MSFT, which are +11.8% and +8.4% pre-mkt, and traders are asking if AAPL and AMZN – which report after the close – can provide an encore performance? As of 8:00am, S&P futures are 0.9% higher, having risen more than 1% earlier, while Nasdaq futures are surging as much as 1.3% after results and spending plans from Meta and Microsoft confirmed the AI trade is here to stay. That’s helping traders overlook Trump’s last-minute tariff curveballs and a more hawkish tone from Fed Chair Powell. Yields are 1-2bp lower as USD is flat. Commodities are mixed with Energy somehow weaker even though it appears that the world’s entire future is based on data center construction for the next several decades; Ags are stronger, gold is up/silver down, and base metals weaker with copper down more than 20% on adjustments to copper tariff policy. Overnight, US/S.Korea reached a deal for 15% plus $350bn in investments and $100bn in energy purchases. Brazil stays at 50% but delayed start with some exemptions (commodities, aircraft, orange juice). US says India to have 25% tariff plus penalty but negotiations to continue. This leaves Canada (call later today), Mexico, China, and Australia as major partners without an updated deal. Today’s macro data focus is on monthly PCE, Jobless Claims, Personal Income/Spending.

In premarket trading, most Mag7 stocks are flying: Meta surges 11% after Facebook’s parent company gave a strong revenue forecast and reported second-quarter results that beat analysts’ expectations. While it also raised its full-year forecast for capital expenditures, analysts said the company’s spending was justified by its growth. Microsoft shares rally 8% after the software giant reported very strong results, with notable strength in its cloud business and Azure product (Amazon +3%, Nvidia +2%, Apple -0.1%, , Tesla -0.2%, Alphabet -0.4%).

- Software, cloud-computing and semiconductor companies are rising as Meta and Microsoft raise capital expenditure plans.

- Alignment Healthcare (ALHC) rises 21% after the Medicare Advantage company said 2Q health plan memberships increased 28% from a year ago, topping estimates. The company also raised some year forecasts.

- Apellis Pharma (APLS) climbs 11% after reporting revenue for the second quarter that missed the average analyst estimate.

- Applied Digital (APLD) rallies 21% as the digital infrastructure company reports better-than-expected quarterly revenue, and says cloud infrastructure provider CoreWeave to lease an additional 150MW of capacity at the North Dakota data center campus. CoreWeave (CRWV) shares jump 10%.

- Arm Holdings Plc (ARM) falls 6% after the company gave a lower-than-expected profit forecast for the current period after ramping up spending on new products.

- Carvana (CVNA) soars 15% after the online car retailer reported revenue during the second quarter that exceeded the average analyst estimate.

- Confluent (CFLT) falls 29% as analysts, including at Stifel, downgrade the application software company’s stock, citing a tough outlook for revenue growth amid cloud usage optimization and lackluster customer additions.

- CVS Health (CVS) rises 7% after the company boosted its adjusted earnings-per-share guidance for the full year, following second-quarter results that also topped expectations.

- Datadog Inc. (DDOG) is down 3% as a filing showed Chief Executive Officer Olivier Pomel sold shares of the software company.

- EBay (EBAY) jumps 14% after the online auction company reported second-quarter results that beat expectations and gave an outlook seen as positive.

- PTC Inc. (PTC) rises 7% after the software company reported third-quarter results that beat expectations and raised its full-year forecast.

- Norwegian Cruise (NCLH) jumps 8% after the cruise operator reported adjusted Ebitda for the second quarter that beat the average analyst estimate. The firm also boosted its outlook for occupancy rates for the full year, topping Wall Street’s expectations.

- Qualcomm (QCOM) falls 6% after the chipmaker reported its third-quarter results and gave an outlook. Analysts say the report disappointed with the company’s handset market.

- Shake Shack (SHAK) falls 8% after the burger chain providing a 3Q revenue outlook that disappointed.

- TransMedics (TMDX) rises 17% after the biotechnology company reported diluted EPS for the second quarter that beat the average analyst estimate.

- Tronox Holdings (TROX) drops 11% after the chemical company cut its year forecast for revenue and adj. Ebitda as management sees lower pigment and zircon volumes and price than previously anticipated. Management also cut the dividend

- Western Digital (WDC) jumps 8% after the computer-storage company beat fourth quarter estimates and provided first quarter forecasts above estimates. Analysts note potential gross margin upside and favorable supply/demand drivers.

Brace for another busy session, with Apple and Amazon reporting and core PCE data for June due. S&P 500 futures surge after blowout earnings from MSFT and META put the index on track for another record. Analysts said that Meta capex may reach $100b next year – an eye-popping 45% increase on this year’s projected figure. Microsoft is also spending big on AI. Along with better-than-expected growth in its cloud business, that’s set to help it become the second company ever to reach a $4 trillion market cap. If even a portion of Microsoft’s 8% premarket gain holds through the start of cash trading, the tech giant is set to match the feat of Nvidia, which hit the $4 trillion milestone earlier this month. Apple and Amazon.com are due to report later Thursday.

Headline-grabbing earnings are helping to allay fears about a tariff-driven slowdown in the world’s biggest economy and justifying high stock valuations. Investors are also navigating trade tensions and central bank decisions.

“It’s really the good results in the US which are providing a tailwind for markets,” said Karen Georges, a fund manager at Ecofi. “We needed the Mag 7 to deliver this quarter for the rally to continue throughout the summer.”

The deluge of data continues Thursday, with reports on jobless claims and monthly core inflation due before the open of trading. The PCE deflator, the Federal Reserve’s preferred inflation gauge, is likely to show a quicker rate of price growth than the CPI index has revealed, bolstering the Fed’s go-slow approach, according to Bloomberg Intelligence.

Treasuries rose across the curve, helping to reverse some of their pullback Wednesday after Powell said no decision had been made about easing policy in September. The dollar traded at its highest levels since May. “Our base case remains that the Fed will begin cutting rates in the second half of this year as we expect the economy to continue to slow,” Richard Clarida, global economic advisor at PIMCO wrote in a note after the meeting. “However, uncertainty remains high and data will continue to drive the Fed.”

European stocks are down, having given up earlier gains. Losses in mining and travel shares have weighed on the Stoxx 600. Rolls-Royce shares soar to a record after the aircraft-engine maker raised its outlook for the year, while AB InBev plunges on its latest results. Here are the biggest movers Thursday:

- Rolls-Royce rises as much as 12% after the aero engine maker increased guidance for the year by more than analysts expected. Strong margin performances in the civil aerospace and power systems divisions drew particular attention

- BBVA jumps 9.1% after the Spanish lender beat estimates, improved its guidance and vowed to step up investor payouts. Shares have underperformed so far this year as the bank pursues a takeover bid of Banco Sabadell

- Safran raised its full-year guidance for free cash flow, revenue growth and operating income well above analysts expectations, sending its shares up 4.3% to a record high

- Argenx surges as much as 16%, the most in two years, after the biotech company reported Vyvgart sales for the second quarter that JPMorgan analysts called a “significant beat.” Barclays said a high bar for success has been met

- Societe Generale shares jumped as much as 8.5% to the highest level since Oct. 2008 after the French lender reported an upbeat 2Q set of earnings. The bank surpassed estimates and increased its profitability target for 2025

- Shell rises as much as 3.5% after the oil company reported adjusted profit for the second quarter that beat the average analyst estimate, and announced a $3.5 billion share buyback. Analysts at RBC note strong marketing result

- Rentokil jumps as much as 12%, the most in over a year, after the pest controller confirmed its full-year guidance and posted results in line with expectations. Analysts note encouraging trends in the firm’s growth initiatives

- AB InBev falls as much as 11%, the steepest decline since 2020, after second-quarter volumes missed estimates. All regions missed expectations barring North America, with Latin America a particular area of weakness, analysts says

- Mining shares are the worst-performing sub-index in the Stoxx 600 on Thursday after US President Donald Trump imposed a 50% tariff on some copper imports, but excluded the most widely imported form of the metal

- Sanofi shares drop as much as 3.7%, the most in two months, after the French drugmaker reported weaker-than-expected earnings for the second quarter, overshadowing a sales beat

- Accor shares fall as much as 13% in brisk volumes, their biggest one-day plunge since the Covid-19 drop of March 2020, after the hotel operator unveiled disappointing guidance

- Eramet shares drop as much as 9.8%, the most in nine months. The mining and metallurgy firm reported weaker-than-expected results in the first half, driven by production and logistical issues, mainly in lithium

- Straumann falls as much as 6.6%, the most since April 7, after US peer Align Technology — which makes clear dental braces — reported weaker-than-expected second-quarter results and provided an outlook which also missed estimates

Earlier in the session, Asian equities were set for their longest losing streak since December, as economic gloom and disappointment over outcomes from a key political meeting swamped shares in China. The MSCI Asia Pacific Index fell as much as 0.4%, poised for a fifth-straight daily decline. Samsung Electronics was among the biggest drags after disappointing earnings. Stocks in Tokyo bucked the regional drop, maintaining gains after the Bank of Japan kept policy rate unchanged. Equity benchmarks in Hong Kong and mainland China declined more than 1% amid weak economic data and little positive surprise from a key government meeting. Some negative sentiment also carried over to the region from US trading overnight after Federal Reserve Chair Jerome Powell said there’s been no decision on easing policy in September. Indian shares erased earlier losses as President Donald Trump said both sides were still in discussions on trade after he threatened at least 25% tariff on imports from the South Asian nation. Meanwhile, stocks in Seoul swung from a gain to a loss as investors shrugged off a relatively light 15% US tariff.

In FX, the Japanese yen is now about 0.2% weaker against the dollar, having erased an earlier gain after BOJ Governor Ueda reduced expectations of a near-term rate increase. The yen weakened to 150 against the dollar for the first time since April 2 as investors took comments from Bank of Japan Governor Kazuo Ueda to be less hawkish than expected. The Bloomberg Dollar Spot Index rose, and traded at its highest levels since May. The euro climbs 0.3% after showing little reaction to regional euro-area inflation data that was largely in line with estimates.

Treasuries rose across the curve, helping to reverse some of their pullback Wednesday after Fed Chair Jerome Powell said no decision had been made about easing policy in September. US yields are mostly richer by 1bp-3bp with 2-year little changed, flattening 2s10s curve by 1.5bp, 5s30s by less than 1bp; 10-year lower by 3bp near 4.34%, outperforming Germany’s by about 1.5bp while UK 10-year keeps pace. European government bonds are mixed. Both the UK and German yields curves flatten with the short-end underperforming.

In commodities, US crude futures fall 0.8% to near $69.50 a barrel. Spot gold rises $32 to around $3,307/oz. Copper prices slipped 0.7% on the London Metal Exchange Thursday — following a collapse in New York — after US President Donald Trump shocked the metals world by exempting the most widely traded forms of copper from his hotly anticipated import tariffs.

Bitcoin rises 1.2% and above $118,000.

To the day ahead now, for the data releases in the US, the focus will be on June personal income/spending (includes PCE price indexes), 2Q employment cost index and weekly jobless claims (8:30am) and July Chicago PMI (9:45am, several minutes earlier to subscribers). The earnings calendar will remain busy with Apple and Amazon being the main highlight, while in Europe we have Rolls-Royce and BMW.

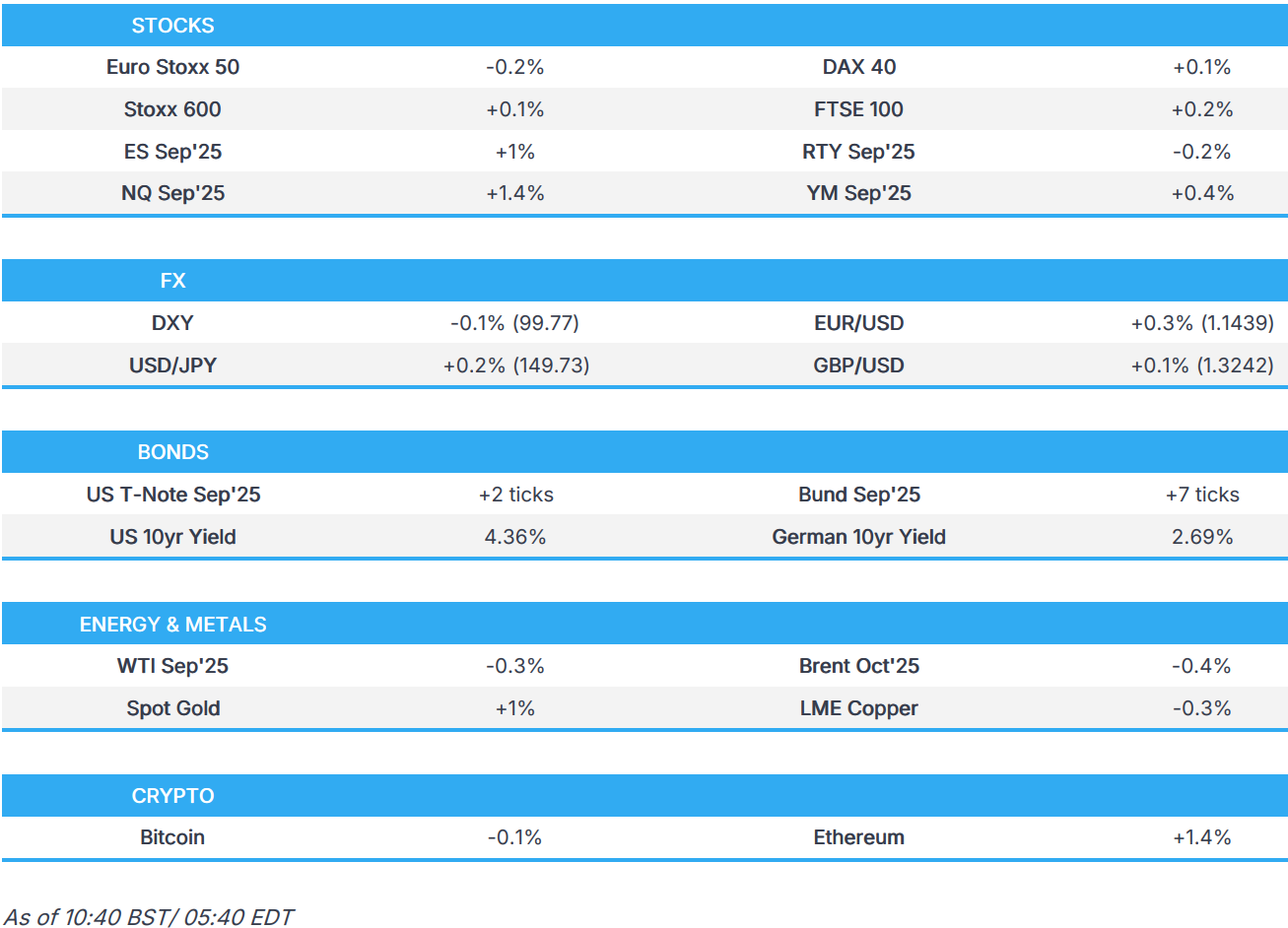

Market Snapshot

- S&P 500 mini +1%

- Nasdaq 100 mini +1.4%

- Russell 2000 mini -0.2%

- Stoxx Europe 600 little changed

- DAX +0.1%

- CAC 40 -0.2%

- 10-year Treasury yield -1 basis point at 4.36%

- VIX -0.6 points at 14.9

- Bloomberg Dollar Index little changed at 1218.53

- euro +0.4% at $1.1445

- WTI crude -0.2% at $69.84/barrel

Top Overnight News

- Trump announced a trade agreement at 6:15pmET Wed night with South Korea – South Korea will be charged a tariff of 15% (consistent w/Japan and the EU) and has pledged to provide $350B for investment in the US w/another $100B intended for energy purchases. Politico

- China reportedly summons NVIDIA (NVDA) on H20 chip backdoor security risk: Bloomberg.

- US Senator Warren (D) sent a letter to Commerce Secretary Lutnick asking that new rules developed by the Ministry maintain incentives for companies to keep computing infrastructure in the US: Punchbowl

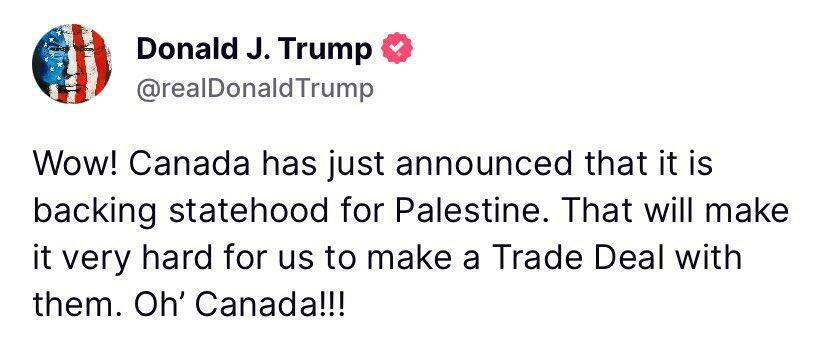

- Trump once again threatened to suspend trade talks with Canada, this time over Carney’s promise to recognize Palestinian statehood. Politico

- BOJ left rates unchanged, as expected, but raised its inflation forecasts, spurring speculation that it could resume policy tightening later this year, although Ueda’s language in the presser cooled speculation of an imminent hike. FT

- Trump is set to hold a phone call w/Mexico’s president Thurs morning as the two countries search for a trade agreement ahead of the 8/1 deadline. BBG

- Top officials from big US trading partners have rushed to Washington in a bid to strike last-ditch trade dela with Trump less than 24 hrs before being hit again with the president’s highest levels of tariffs. Canada and Mexico sent delegations and were locked in intense talks with the Trump admin on Wednesday. FT

- AAPL iPhone exports to the US from India will remain untouched by President Donald Trump’s latest 25% tariffs on the South Asian nation, for now. BBG

- China’s NBS PMIs cool in Jul, with manufacturing coming in at 49.3 (down from 49.7 in June and below the Street’s 49.7 forecast) and non-manufacturing at 50.1 (down from 50.5 in June and below the Street’s 50.2 forecast) WSJ

- French inflation was stable in July at a level well below the ECB’s 2% target, supporting the case for more interest-rate cuts. BBG

- MSFT +8.5% in the pre mkt, Azure growth +39% cc vs. expectations for +35%, Total Revs $76.4% (+17% y/y) vs cons $73.8bn and EPS $3.65 or ~8% beat vs cons ~$3.38. META +11.8% pre mkt and new ATHs. Handily beat every line with less capex/opex pressure than expected … Ad revs ACCEL to +22% y/y cc, 2Q Revs $47.52bn (+22% y/y cc) vs guide $42.5-45.5bn vs cons $44.8bn (+15% y/y) vs +19% y/y cc last qtr: Goldman Sachs

Trade/Tariffs

- US President Trump announced that the US has agreed to a “Full and Complete Trade Deal” with South Korea in which South Korea will give the United States USD 350bln for investments owned and controlled by the US, and selected by Trump, while South Korea will also purchase USD 100bln of LNG, or other energy products and South Korea has also agreed to invest a large sum of money for their Investment purposes with this sum to be announced within the next two weeks when the President Lee comes to the White House for a bilateral meeting. Trump added “It is also agreed that South Korea will be completely OPEN TO TRADE with the United States, and that they will accept American product including Cars and Trucks, Agriculture, etc. We have agreed to a Tariff for South Korea of 15%. America will not be charged a Tariff.”

- South Korean Presidential Office confirmed US lowered tariffs on South Korean autos to 15% from 25%, while it added that chips and drug tariffs will not be worse than those applied to other countries and stated that USD 200bln of funds are allocated for chips, nuclear power, batteries, and bio sectors. Furthermore, it stated that the rice and beef market will not be opened and that South Korea demanded 12.5% auto tariffs but President Trump insisted on 15%.

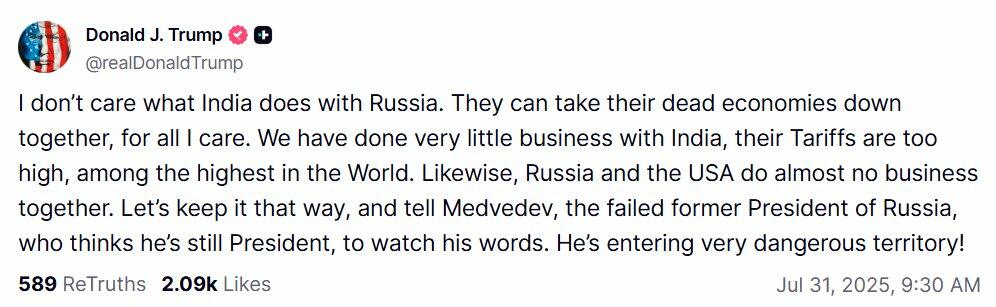

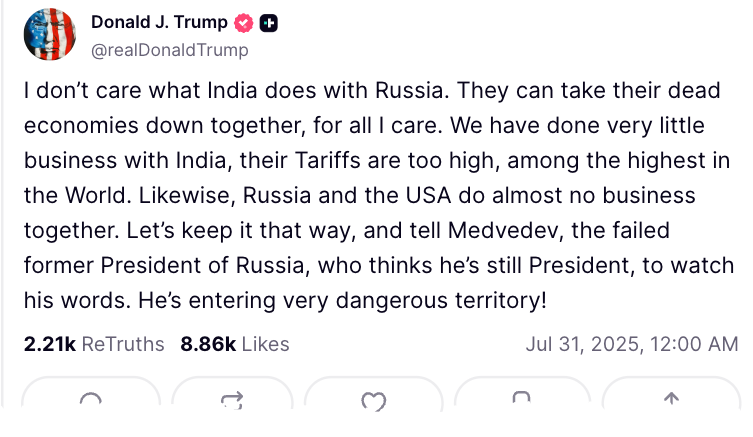

- US President Trump posted “I don’t care what India does with Russia. They can take their dead economies down together, for all I care. We have done very little business with India, their Tariffs are too high, among the highest in the World. Likewise, Russia and the USA do almost no business together. Let’s keep it that way, and tell Medvedev, the failed former President of Russia, who thinks he’s still President, to watch his words. He’s entering very dangerous territory!”

- US President Trump will discuss Mexico’s plan to cut trade deficit with Mexican President Sheinbaum on Thursday ahead of the August 1st deadline.

- US President Trump plans to sign new executive orders on Thursday, imposing higher tariff rates on several countries that have been unable to reach negotiated trade agreements by Friday deadline, while this could include a number of America’s biggest trading partners, including Canada, Mexico and Taiwan, according to POLITICO.

- Pakistan’s government said the trade agreement with the US will result in a reduction in reciprocal tariffs, especially on Pakistani exports to the US, and is expected to spur increased US investment in Pakistan’s infrastructure and development projects. Furthermore, it stated that the US–Pakistan deal marks the beginning of economic collaboration in energy, mines and minerals, IT, cryptocurrency, and other sectors.

- US Commerce Secretary Lutnick announced trade deals were made with Cambodia and Thailand. However, the Thai Finance Minister later said they are still working a bit more on the trade proposal to the US and he expects to receive info on US tariffs within 24 hours.

- EU is to give 0% tariff for export quota of 1mln metrics tons of Indonesian crude palm oil a year under free trade agreement, according to an Indonesia official.

Earnings

- Meta Platforms Inc (META) Q2 2025 (USD): EPS 7.14 (exp. 5.85), Revenue 47.52bln (exp. 44.87bln); +12% shares pre-market.

- Microsoft Corp (MSFT) Q2 2025 (USD): EPS 3.65 (exp. 3.35), Revenue 76.44bln (exp. 73.76bln); +8% shares pre-market.

- Arm Holdings (ARM) Q1 2026 (USD): Adj. EPS 0.35 (exp. 0.35), Revenue 1.05bln (exp. 1.05bln); -7% shares pre-market.

- Qualcomm Inc (QCOM) Q3 2025 (USD): Adj. EPS 2.77 (exp. 2.70), Revenue 10.37bln (exp. 10.30bln); -6% shares pre-market.

- eBay Inc (EBAY) Q2 2025 (USD): Adj. EPS 1.37 (exp. 1.30), Revenue 2.7bln (exp. 2.64bln); +13% shares pre-market.

- Western Digital Corp (WDC) Q4 2025 (USD): Adj. EPS 1.66 (exp. 1.46), Revenue 2.605bln (exp. 2.46bln); +9% shares pre-market.

A more detailed look at global markets courtesy of Newsquawk