AUGUST 1//POOR JOBS REPORT SENDS ALL PRECIOUS METALS HIGHER: GOLD ROSE BY $51.40 TO $3347.90 WITH SILVER IS UP 19 CENTS TO $36.84//PLATINUM CLOSED DOWN $12.30 TO $1309.25//WHILE PALLDIUM WAS UP $20.55 TO $1210.95//MAJOR PODCAST FROM ANDREW MAGUIRE INTERVIEWING LONDON PAUL: A MUST VIEW//HUGE COMMODITY REPORT ON COPPER//GERMANY AND SPAIN REPORTS ON MIGRANTS AND HOW ITS HAS HURT THEIR ECONOMIES//ISRAEL UPDATES COURTESY OF IBN ISRAEL//ISRAEL VS IRAN/ISRAEL VS HAMAS UPDATES/USA IMPOSES MAJOR SANCTIONS ON IRANIAN SHIPPING MAGNATES AND THAT WILL CRIPPLE THEIR ECONOMY//RUSSIA VS UKRAINE UPDATES/COVID UPDATES/VACCINE INJURY REPORTS/DR PAUL ALEXANDER/MARK CRISPIN MILLER/NEWS ADDICTS/EVOL NEWS/SHALE COSTS RISING OVER THE PAST TWO YEARS. BREAKEVEN IS AROUND $68.00 PER BARREL AND IF THE PRICE DOES NOT IMPROVE THEN RIGS WILL BE TAKEN DOWN//TARIFF DAY ANNOUNCED WITH MAJOR TARIFFS ON A WHOLE HOST OF COUNTRIES: CANADA IS HIT WITH 35% TARIFF/A MUST VIEW COMMENTARY FROM JEFFREY SACHS ON THE TARIFFS//USA MANUFACTURING REPORTS LOWER OUTPUTS/SWAMP STORIES FOR YOU TONIGHT///

118 C MACQUARIE FUTURES US 8 118 H MACQUARIE FUTURES US 223 132 C SG AMERICAS 243 190 H BMO CAPITAL MARKETS 786 285 C NANHUA USA-HK 4 323 C HSBC 722 233 332 H STANDARD CHARTERED B 125 363 H WELLS FARGO SECURITI 74 435 H SCOTIA CAPITAL (USA) 36 555 C BNP PARIBAS SEC CORP 70 657 C MORGAN STANLEY 50 657 H MORGAN STANLEY 416 661 C JP MORGAN SECURITIES 335 530 686 C STONEX FINANCIAL INC 25 15 690 C ABN AMRO CLR USA LLC 49 11 709 C BARCLAYS 19 732 C RBC CAP MARKETS 5 732 H RBC CAP MARKETS 393 800 C MAREX SPEC 1 880 C CITIGROUP 8 905 C ADM 13

TOTAL: 2,197 2,197 MONTH TO DATE: 17,501

JPMORGAN stopped 3549/15,304

AUGUST

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 2197 CONTRACTs NOTICES FOR 219,700 OZ or 6.833 TONNES

total notices so far: 17,501 contracts for 1,750,100 OR 54.435 tonnes)

FOR AUGUST

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 51 NOTICE(S) FILED FOR 0.255 million OZ/

total number of notices filed so far this month : 969 CONTRACTS (NOTICES) for 4.845 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $51.40 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/./

INVENTORY RESTS AT 954.51 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.19 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: //A WITHDRAWAL OF 2.8160 MILLION OUT OF THE SLV/

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 484.266 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA MEGA HUGE SIZED 3820 CONTRACTS TO 161,954 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR CONSIDERABLE LOSS OF $1.00 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. WE FINALLY ARE MOVING MUCH HIGHER THAN THE BASE $34.40 SILVER PRICE BARRIER. WE HAD A MEGA HUGE SIZED LOSS OF 2870 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE 950 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO THURSDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $36.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON THURSDAY WITH SILVER’S CONSIDERABLE LOSS IN PRICE. THE PRICE HOWEVER FINISHED MILES ABOVE THE MAGIC NUMBER OF $36.00 SILVER SPOT PRICE CLOSING AT $36.65 . WE HAVE A MEGA HUGE T.A.S. ISSUANCE AT 972 CONTRACTS ISSUED BY THE CME AND THAT STILL SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING ABOVE THE 38.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A HUGE 950 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 972 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FRIDAY’S// TRADING OR BEYOND/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A MEGA MEGA HUGE SIZED 2870 CONTRACTS ON OUR TWO EXCHANGES WITH OUR HUGE LOSS IN PRICE OF $1.00.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT/FRIDAY MORNING: A STRONG SIZED 972 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.00) AND WERE SUCCESSFUL IN KNOCKING OFF A FEW NET SILVER LONGS FROM THEIR PERCH AS WE HADE A MEGA HUGE LOSS OF 2870 CONTRACTS ON OUR TWO EXCHANGES WITH HUGE T.A.S. SPREADER LIQUIDATION AND HUGE MONTHLY SPREADER LIQUIDATION WITH RESPECT TO THURSDAY’S RAID.. MOST OF THIS LOSS IN OI WAS DUE TO THOSE TWO SPREADER LIQUIDATIONS

WE HAD A 950 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.70 MILLION OZ FOLLOWED BY TODAY’S 72 CONTRACT OR AN ADDITIONAL 360,000 OZ WILL STAND AS THEY UNDERWENT A QUEUE JUMP //NEW STANDING ADVANCES TO 4.995 MILLION OZ.

THUS:

INITIAL STANDING FOR AUGUST: 4.70 MILLION OZ FOLLOWED BY TODAY’S 360,000 OZ QUEUE JUMP//NEW STANDING; 4.995 MILLION OZ

WE HAD:

/ HUGE COMEX OI LOSS+// A HUGE SIZED EFP ISSUANCE 950 CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 972 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED A SMALL 62 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 1 DAY(S), total 950 contracts: OR 4.750 MILLION OZ (950 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 4.750 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 4.750 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3820 CONTRACTS WITH OUR LOSS IN PRICE OF $1.00 IN SILVER PRICING AT THE COMEX// THURSDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE 950 CONTRACT EFP ISSUANCE CONTRACTS: 950 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 5 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ PLUS TODAY;S 360,00 OZ QUEUE JUMP//NEW STANDING 4.995 MILLION OZ

THE NEW TAS ISSUANCE THURSDAY NIGHT (950 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE IN TUESDAY THROUGH THURSDAY TRADING.

WE HAD 51 NOTICE(S) FILED TODAY FOR 0.255 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 14,268 OI CONTRACTS TO 427,980 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 2870 CONTRACTS //.

WE HAD A VERY HUGE DECREASE IN COMEX OI (14,268 CONTRACTS) . THIS OCCURRED WITH OUR LOSS OF $2.65 IN PRICE// THURSDAY///.

LAST FOUR MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

AUGUST: 60.547 TONNES OF GOLD FOLLOWED BY TODAY’S MONSTER 3.477 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 64.074 TONNES OF GOLD/.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1890 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 427,980 /NOW EXTREMELY CLOSE TO ITS NADIR AND WE NOW WITNESS A LOW COMEX OI WITH AN EXTREMELY HIGH PRICE OF GOLD

SILVER ALSO HAS A LOW COMEX OI OF 161,954 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A VERY STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,378 CONTRACTS WITH 14,268 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1890 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 12,378 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 860 CONTRACTS AND THESE ISSUANCES ARE JOINED WITH OUR MONTHLY SPREADER LIQUIDATION TO CREATE OUR RAID IN GOLD/.(LOSS IN PRICE YESTERDAY: $2.65)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(1890) ACCOMPANYING THE HUGE SIZED DECREASE IN COMEX OI OF 14,268 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 12,378 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR AUGUST AT 60.547 TONNES FOLLOWED BY TODAY’S 3.477 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 64.074 TONNES

NEW STANDING FOR GOLD, AUGUST CONTRACT AT 64.074 TONNES OF GOLD

.

/ 3) HUGE T.A.S. LIQUIDATION AND MONTH END SPREADER LIQUIDATION IN THE COMEX SESSION AS WE HAD 1)A $2.65 COMEX PRICE LOSS. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS DESPITE HAVING A STRONG LOSS OF 12,378 CONTRACTS ON OUR TWO EXCHANGES WE HAD HUGE LIQUIDATION OF OUR TAS SPREADERS AND MONTHLY SPREADERS I.E. MOST OF THE LOSS IN OI WAS DUE TO THE TWO SPREADERS// /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND YOU CAN VISUALIZE THIS BY THE HUGE AMOUNTS OF QUEUE JUMPING WE HAVE BEEN HAVING LATELY

4) VERY STRONG SIZED COMEX OI LOSS// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (1890 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 860 T.A.S.CONTRACTS/

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

TOTAL EFP CONTRACTS ISSUED: 41890 CONTRACTS OR 189,000 OZ OR 5.979 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 1890 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN1 TRADING DAY(S) IN TONNES 5.979 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 5.979 TONNES DIVIDED BY 3550 x 100% TONNES = 0.0166% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

UNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 5.894 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 3820 CONTRACTS OI TO 161,954 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 950 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 950 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 650 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3820 CONTRACTS AND ADD TO THE 950 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF 2870 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE LOSS IN PRICE OF $1.00 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 14.660 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 13.26 PTS OR 0.37%

//Hang Seng CLOSED DOWN 265.52 PTS OR 1.07%

// Nikkei CLOSED DOWN 270.22 PTS OR 0.66% //Australia’s all ordinaries CLOSED DOWN 0.91%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.2118 OFFSHORE CLOSED DOWN AT 7.2204/ Oil DOWN TO 68.96 dollars per barrel for WTI and BRENT DOWN TO 71.23 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.2118 AND WEAKER//OFF SHORE YUAN TRADING UP TO 7.2204 AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED 14,268 CONTRACTS TO 432,354 OI DESPITE OUR SMALL LOSS IN PRICE OF $2.65 WITH RESPECT TO THURSDAY’S // TRADING.. WE LOST SOME NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1890 ). WE HAD HUGE T.A.S. LIQUIDATION //THURSDAY TRADING AS WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 8004 CONTRACTS WITH ALL OF THAT LOSS DUE TO BOTH SPREADERS, THE T.A.S. LIQUIDATION AND MONTHLY SPREADERS.

LAST WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. OR IT COULD BE THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY!!.THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY IS NOW 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

EARLY THIS MORNING THE CME ANNOUNCED A ZERO EXCHANGE FOR RISK ISSUANCE!

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 0 SO FAR

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS GENERALLY THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE OR FRBNY FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 6TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH JULY WITH A TWO MONTH HIATUS)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A VERY STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 12,378 CONTRACTS DESPITE OUR SMALL LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED ERLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST AS IT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 860 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED YESTERDAY WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS TODAY’S MONSTER QUEUE JUMP OF 3.477 TONNES//NEW STANDING 64.074 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 233 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NONE COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST FOLLOWED BY A MONSTER QUEUE JUMP OF 3.477 TONNES/NEW STANDING ADVANCES TO 64.074 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1890 EFP CONTRACT WAS ISSUED: : /AUGUST 1890 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1890 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

HUGE LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY AND THEY WERE JOINED BY OUR MONTHLY SPREADER LIQUIDATION

SOME NET SPEC LIQUIDATION DESPITE OUR SMALL LOSS IN PRICE. HOWEVER MOST OF THAT LOSS IN OI ON OUR TWO EXCHANGES WAS DUE TO OUR TWO SPREADERS.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY WAS A SMALL SIZED SIZED 860 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS PAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S LOSS IN PRICE IN GOLD AND SILVER AND A CORRESPONDING LIQUIDATION OF CONSIDERABLE COMEX OI. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH THE RARE TWO ISSUANCES OF EXCHANGE FOR RISK! THE RAIDS THROUGHOUT OPTION EXPIRY WEEK WERE USED TO LOWER THE HUGE DERIVATIVE LOSSES ENDURED BY THE BANKERS.

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S WHOPPING MONSTER QUEUE JUMP OF 3.477 TONNES//NEW STANDING ADVANCES TO 64.074 TONNES.

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A SMALL $2.65/ /) AND WERE SUCCESSFUL IN KNOCKING OFF A FEW NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION AND MONTH END SPREADER LIQUIDATION ////THURSDAY WHICH ACCOUNTS FOR MOST OF THE LOSS IN TOTAL OI. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE!

FRIDAYS MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE LOST A FAIR SIZED TOTAL OF 38.5 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD TODAY’S MONSTER QUEUE JUMP OF 3..477 TONNES OF GOLD//NEW STANDING ADVANCES TO 64.074 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $2.65

WE HAD A HUGE 4374 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 8004 CONTRACTS OR 800,400 0Z (24.895 TONNES)

1 entry: i) Into the dealer Asahi: 40,,124.45 oz (1248 kilobars)

total deposit 40,124.45 oz (1.248 tonnes)

Deposits to the Customer Inventory, in oz

0 ENTRIES

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

2197 notice(s) 219,700 OZ 6.833 TONNES

No of oz to be served (notices)

3099 contracts 309,900 OZ 9.639 TONNES

Total monthly oz gold served (contracts) so far this month

17,501 notices 1,750,100 oz 54.435 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits:

1 ENTRIES

1 entry: i) Into the dealer Asahi: 40,,124.45 oz (1248 kilobars)

total deposit 40,124.45 oz (1.248 tonnes)

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

ZERO ENTRIES

adjustments: 1

Brinks: deale to customer: 8005.599 oz (249 kilobars)

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 5,296 CONTRACTS FOR A LOSS OF 14,173 CONTRACTS

WE HAD 15,304 CONTRACTS SERVED ON THURSDAY SO WE GAINED A HUGE 1117 CONTRACTS OR A WHOPPING 111700 OZ OF GOLD (3.477 TONNES) EXERCISED A QUEUE JUMP. THIS REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

SEPT GAINED 58 CONTRACTS TO 4685

OCTOBER GAINED 372 CONTRACTS UP TO 67,093

We had 2197 contracts filed for today representing 219,700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 335 notices issued from their client or customer account. The total of all issuance by all participants equate to 2197 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 530 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (17,501 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 5296 CONTRACTS) minus the number of notices served upon today (2197 x 100 oz per contract) equals 2,060,000 OZ OR 64.024 TONNES

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (17,501 x 100 oz +we add the difference for front month of AUGUST (5296 OI} minus the number of notices served upon today (2197 x 100 oz) which equals 2,060,000 OZ OR 64.024 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 64.024 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL REGISTERED SILVER: 191.576 MILLION OZ//.TOTAL REG + ELIGIBLE. 506.661Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 72 OPEN INTEREST CONTRACTS FOR A LOSS OF 868 CONTRACTS. WE HAD 940 CONTRACTS SERVED ON THURSDAY SO WE GAINED 72 CONTRACTS OR AN ADDITIONAL 360,000 OZ WILL STAND AS THEY ENTERTAINED A STRONG QUEUE JUMP

SEPTEMBER LOST 3076 CONTRACTS DOWN TO 112,751 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 51 or 0.255 MILLION oz

CONFIRMED volume; ON THURSDAY 73,928 good//

AND NOW JULY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 969 X5,000 oz = 4.845 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (72) AND the number of notices served upon today (51 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (969) Notices served so far) x 5000 oz + OI for the front month of AUGUST(72) minus number of notices served upon today (51)x 5000 oz equals silver standing for the AUGUST contract month equating to 4.995 MILLION OZ .

New total standing: 4.995 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 191.576 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/506.6612 million. 41.45%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 954.51 TONNES, TONIGHTS TOTAL

SILVER

AUGUST WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

Trump backing off on copper is hitting all metals. US tariffs are in disarray and are backfiring badly on the US economy and the dollar. The case for gold and silver is even stronger.

With Comex’s August contract running off the board and copper’s collapse it is hardly surprising that precious metals traded lower this week. In European trade this morning, gold was $3294, down $43 from Friday’s close, and silver at $36.48 down $1.65. The gold/silver ratio has returned to 90.

Before observing this week’s action in gold and silver, a comment on copper and other base metals is required. President Trump has relented on US import tariffs on copper ore, concentrates, and cathodes leaving 50% tariffs on imports of semi-finished items such as wires and pipes. Consequently, copper futures fell by 25% this week hitting every paper-traded metal, including silver. Copper’s chart is below:

In a longer-term context, this has not damaged copper’s bull market, which remains intact and if nothing else reflects the dollar’s declining purchasing power. More importantly, this episode serves as evidence of the severe damage US trade tariffs are doing to the US economy. Even Paul Krugman, who won his Nobel prize for trade theory opined that “We’re looking at a shock to the economy seven or eight times as big as Smoot-Hawley”.

50% tariffs remain on imported steel and aluminium. Given the climbdown on copper, these are almost certainly next. This is the context in which the dollar is to be valued in future. And given that the dollar’s value is determined by foreign holders owning over 30% more dollars and financial assets than the entire US GDP, this is not a trivial matter. Even against other currencies in their own debt traps and a declining ability to service their ballooning national debts, measured by the trade-weighted index the dollar is falling:

The dollar has rallied into overhead supply, a normal move, but the moving averages still scream bear market.

Krugman’s point will surely become more widely understood. The damage being done to the US economy and therefore the dollar is not yet reflected in headline statistics but is undoubtedly immense. And it is this damage that will determine its future exchange rate not just with other currencies but particularly gold. The next chart shows a very bullish pennant pattern for gold which merits close examination.

The pennant is delineated by the pecked lines. Its flat top suggests that the subsequent move up when the level is broken ($3440) will be the minimum projected by this pattern. That gold has overshot on the downside of the pattern is not unusual and given the disruption from copper is of no concern.

Once the $3440 level is surmounted, the minimum target is determined by the move into the pattern from the last significant consolidation, which is arrowed. This move is worth $900, which added to $3440 gives a minimum target of $4340, taking a similar time to the preceding move which is five months — in other words approximately at the year end.

This outcome might seem fanciful, but in the context of a) a US economy being badly undermined by tariff policies; b) stubborn and rising inflation being driven by the dollar’s falling purchasing power; and c) foreign holders selling dollars to avoid mounting losses it is eminently possible.

In this context, the reaction of silver presents a heaven-sent opportunity for those wishing to hedge this outcome. There is little doubt that silver’s sharp fall has been exacerbated by its role as an industrial metal alongside copper, and that the paper shorts are making hay out of the situation. But this is purely short-term thinking, whipsawing speculative traders.

The silver chart shows a reaction back to the 55-day moving average where it can be expected to find support. This is next:

At a guess, speculation will turn to precious and base metals whose prices may have been buoyed by Trump’s tariffs. But for gold and particularly silver stackers, it represents an opportunity to escape the mounting chaos engulfing the US economy and the dollar.

February 25, 20259:50 PM ESTUpdated February 25, 2025

BEIJING, Feb 26 (Reuters) – U.S. President Donald Trump on Tuesday ordered a probe into possible tariffs on copper imports to rebuild U.S. production of a metal critical to electric vehicles, military hardware, semiconductors and a wide range of consumer goods.

A White House official said the investigation would look at imports of raw mined copper, copper concentrates, copper alloy, scrap copper and derivative products made from the metal. A result is expected quickly.

The Reuters Tariff Watch newsletter is your daily guide to the latest global trade and tariff news. Sign up here.

Here’s what you need to know about U.S. copper imports:

US IMPORTS

The United States produces domestically just over half the refined copper it consumes each year. More than two-thirds of that is mined in Arizona, where the development of a massive new mine has been stalled for more than a decade. The remaining refined copper, just shy of 1 million metric tons annually, is imported.

While the White House framed the new tariffs as a way to counter China’s dominance of the global market, the United States in fact imports most of its refined copper from the Americas.

Chile, Canada and Peru accounted for more than 90% of refined copper imports last year, according to the United States Geological Survey (USGS).

Chart showing US refined copper imports by country

GLOBAL PRODUCTION

China dominates global copper refining, but most of the ore that feeds into its smelters is mined elsewhere, in particular in Latin America. Chile and Peru together mined roughly a third of global copper last year, according to the USGS.

Chart showing global copper mining by country

However, China is expanding its control over world copper mining through its major investments in mines in the Democratic Republic of the Congo (DRC).

The DRC is now the world’s second-largest copper miner after overtaking Peru, due in large part to massive Chinese investment in the African country’s mining sector.

Chart showing global copper refining output by country

The Chinese copper smelting sector dwarfs all others. The country had dozens of copper smelters operating last year. Meanwhile, the United States has only two primary copper smelters, according to the USGS.

Reporting by Lewis Jackson and Amy Lv in Beijing; Editing by Jamie Freed

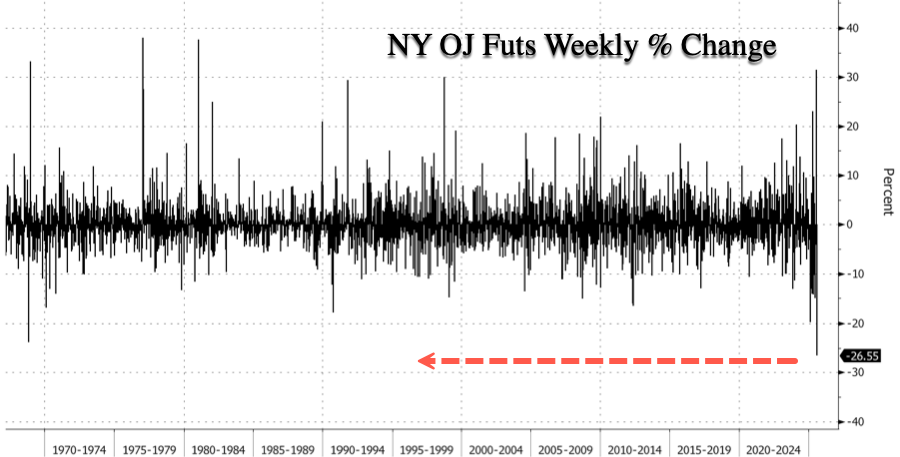

Tariff Exemption Sends Orange Juice Crashing Most On Record

by Tyler Durden

Orange juice futures in New York are on track for the steepest weekly decline on record, with losses exceeding 26%, after the Trump administration formally excluded Brazilian OJ from the newly proposed 50% tariffs on U.S. imports from the South American country. The exemption sparked a sharp reversal in speculative positioning in the contracts, erasing a multi-week rally fueled by trade disruption fears.

The executive order signed by President Trump on Wednesday delayed the implementation of 50% tariffs on Brazilian exports by seven days, while exempting several products, including orange juice, civil aircraft, iron ore, coal, wood pulp, machinery, and fertilizers.

“The tide seems to be turning again for Brazil (more favorably as of Wednesday) with the announcement of a delay (by seven days) in the 50% tariff and the inclusion of some 700 exceptions (or about 45% of exports exempted from the 40pp hike) to the US tariffs on Brazilian imports (crude oil, airplanes and orange juice as the most relevant lines),” UBS analyst Justin Wensek told clients earlier this week.

He noted, “This is a better outcome than the market had been pricing in. However, even if there were no exceptions, as UBS Brazil economists note, the roughly 60% of Brazilian exports to U.S. could be almost immediately re-routed to other countries.”

Craig Elliott, a market analyst at Expana, said Trump’s Brazilian tariffs seem to bring about a “collective sigh of relief.”

“The orange juice market is currently facing challenges even without the threat of tariffs, and there does seem to be a sense of being able to get back to business as usual, and solving the difficulties,” Elliott said.

Orange juice futures in New York declined 9.2% on Friday, pushing them toward a staggering 26.5% weekly decline. This is the largest weekly decline recorded since futures data began in 1967.

The U.S. accounts for 40% of Brazil’s orange juice exports because the greening disease has decimated U.S. supplies in Florida.

OJ prices have been halved since peaking above $5 a pound in late 2024.

Wild week for some commodity markets in the era of Trump tariffs.

END

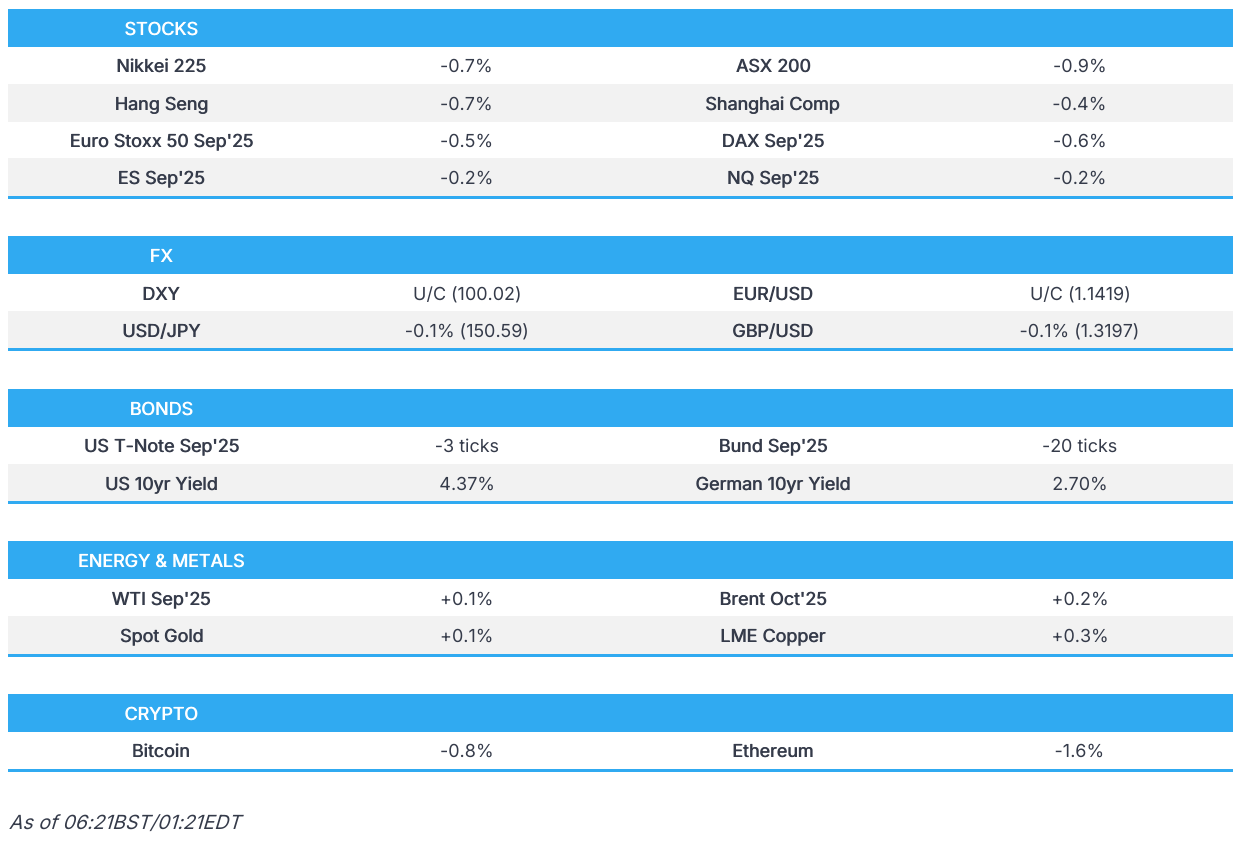

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 13.26 PTS OR 0.37%

//Hang Seng CLOSED DOWN 265.52 PTS OR 1.07%

// Nikkei CLOSED DOWN 270.22 PTS OR 0.66% //Australia’s all ordinaries CLOSED DOWN 0.91%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.2118 OFFSHORE CLOSED DOWN AT 7.2204/ Oil DOWN TO 68.96 dollars per barrel for WTI and BRENT DOWN TO 71.23 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.2118 AND WEAKER//OFF SHORE YUAN TRADING UP TO 7.2204 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2118 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: DOWN TO 7.2204

HANG SENG CLOSED DOWN 265.52 PTS OR 1.07%

2. Nikkei closed UP 270.22 PTS OR 0.66%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 99.83/ EURO FALLS TO 1.1409 DOWN 12 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.551//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.53…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7090/Italian 10 Yr bond yield UP to 3.565 SPAIN 10 YR BOND YIELD UP TO 3.295%

3i Greek 10 year bond yield UP TO 3.410

3j Gold at $3294.00 Silver at: 36.48 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 79 /100 roubles/dollar; ROUBLE AT 80.31

3m oil (WTI) into the 68 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.53// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.551% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8159 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9306 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.380 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.9140 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.941 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.67

10 YR UK BOND YIELD: 4.6260 UP 6 PTS

10 YR CANADA BOND YIELD: 3.467 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 3.025 DOWN 0 PTS

2a New York OPENING REPORT

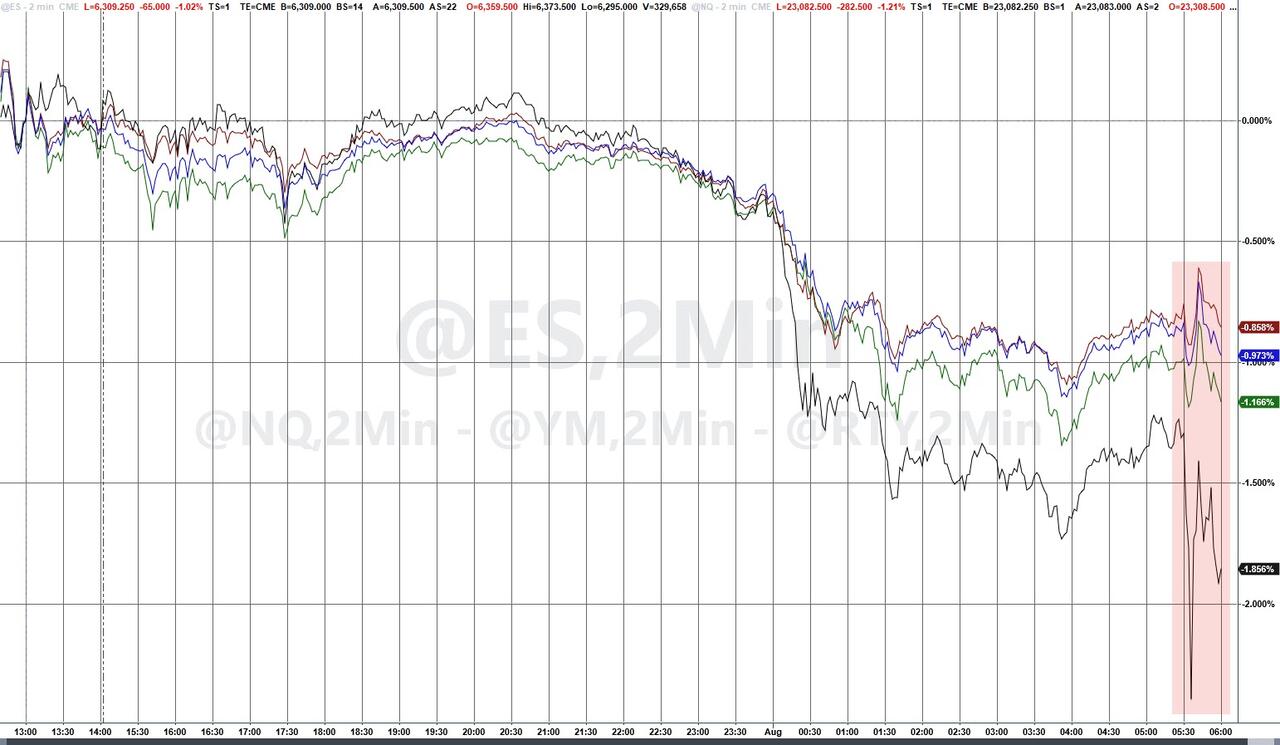

Where’s Your TACO Now: Futures Slide, Global Markets Tumble After Trump Unleashes Harsh Tariffs

Friday, Aug 01, 2025 – 08:21 AM

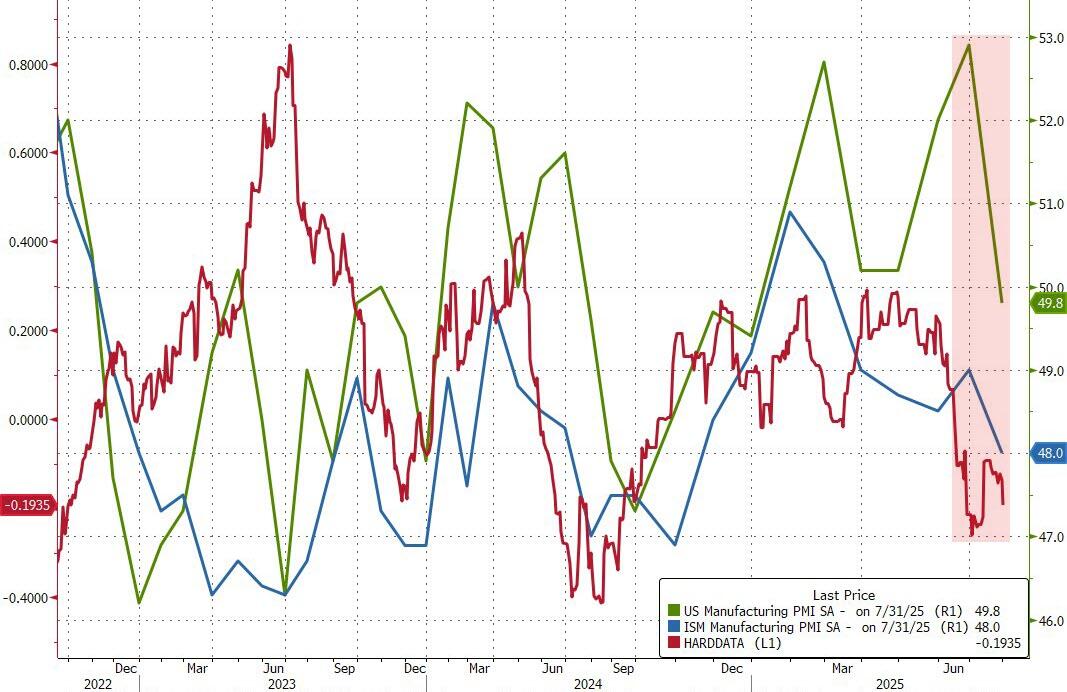

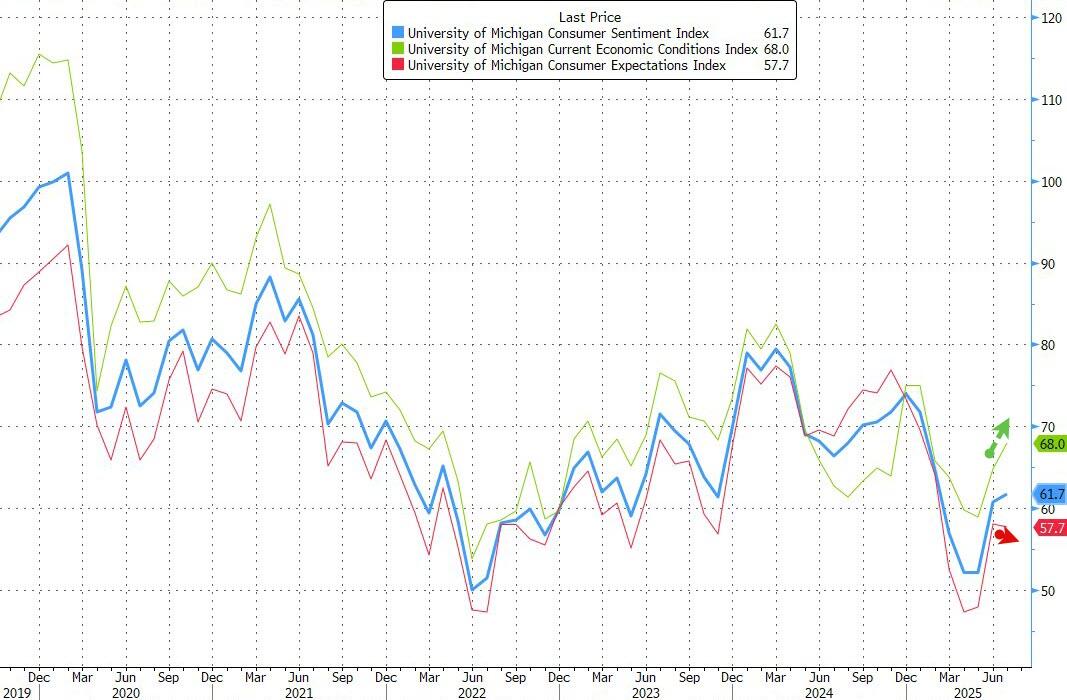

Global markets and US equity futures extended a selloff as Trump’s sweeping import tariffs sparked renewed fears about the outlook for economic growth amid traders. The MSCI All Country World Index fell for a sixth day, the longest streak since September 2023. As of 8:00am ET, S&P futures on the S&P 500 retreated more than 1%, suggesting the index will extend a three-day run of declines. In premarket trading, Amazon.com slumped as much as 8% and weighed on Big Tech after projecting weaker-than-expected operating income, prompting questions about its huge AI spending; Elsewhere AAPL (+1.7%) rallied on iPhone sales growth including while other Mag 7 names are mostly lower NVDA (-.25%), GOOG/L (-2.2%) and META (-1.3%) as Consumer Discretionary and Healthcare underperform. In rates, 30y TSYs added 3.2bps. Commodities are mixed, with precious metals higher and base metals lower. Today’s economic data slate includes July jobs report (8:30am), July final S&P Global US manufacturing PMI (9:45am), and July ISM manufacturing and July final University of Michigan sentiment (10am)

In premarket trading, Mag 7 stocks are mostly lower: Amazon.com slides 7% after projecting weaker-than-expected operating income and trailing the sales growth of its cloud rivals, leaving investors searching for signs that the company’s huge investments in artificial intelligence are paying off. Apple rises 1.8% after the company reported its fastest quarterly revenue growth in more than three years, easily topping Wall Street estimates, after demand picked up for the iPhone and products in China. Others are mostly in the red (Microsoft +0.5%, Meta -1%, Tesla -1.2%, Alphabet -1.8%, Nvidia -2%).

Avantor (AVTR) slumps 10% after the maker of laboratory supplies reported adjusted earnings per share for the second quarter that missed the average analyst estimate.

CCC Intelligent Solutions (CCCS) climbs 15% after the software company reported revenue for the second quarter that exceeded the average analyst estimate.

Coinbase (COIN) falls 11% after the largest US crypto exchange reported revenue for the second quarter that missed the average analyst estimate following a drop in digital-asset market volatility.

Eli Lilly & Co. (LLY) ticks up as much as 2.5% after the Washington Post reported that the US government plans to experiment with covering weight-loss drugs for federal health programs.

First Solar (FSLR) advances 2% after the renewable energy firm boosted its net sales forecast for the full year.

Fluor (FLR) tumbles 17% after the engineering and contracting firm cut its adjusted earnings per share guidance for the full year.

Kimberly-Clark Corp. (KMB) rises 3% after raising its full-year guidance after reporting the strongest volume growth in five years.

Lumen Technologies (LUMN) falls 5% after the telecommunications firm posted 2Q revenue came in just shy of estimates.

Moderna (MRNA) falls 5% after the struggling biotech company narrowed its revenue forecast for the full year.

Reddit (RDDT) rises 16% after the social-networking company forecast revenue for the third quarter that beat the average analyst estimate.

Late on Thursday, Trump announced a slew of new levies, including a 10% global minimum and 15% or higher duties for countries with trade surpluses with America, as he forged ahead with his turbulent effort to reshape international commerce. Questions about the impact on growth and inflation are starting to overshadow the AI-driven optimism that has buoyed megacap technology stocks.

“Next week marks a significant turning point for global trade with the introduction of Trump’s tariffs, creating uncertainty about how these new and historical barriers will affect markets in practice,” said Kim Heuacker, an associate consultant at Camarco. “Current high valuations, particularly among US stocks, are becoming increasingly difficult to justify.”

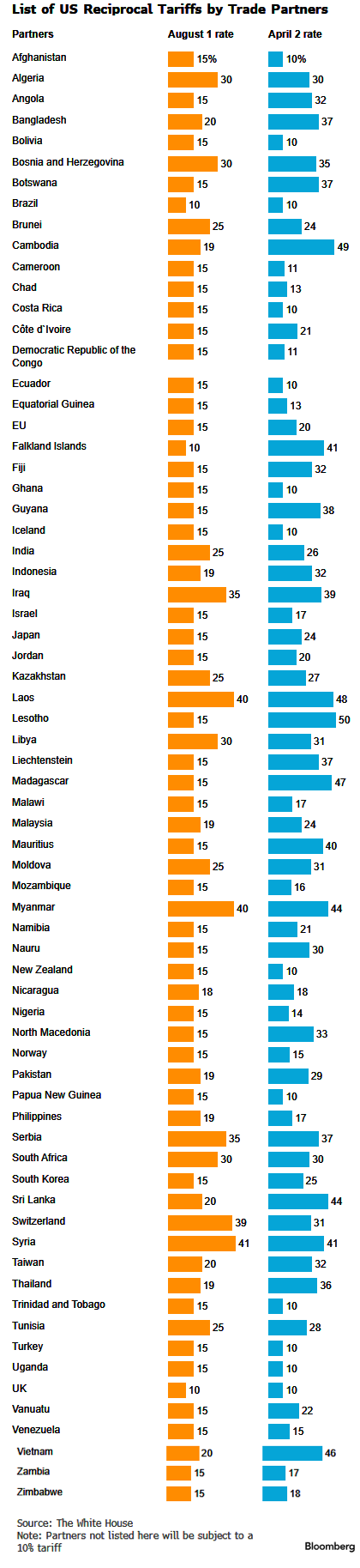

Trump’s baseline rates for many trading partners remain unchanged at 10% from the duties he imposed in April, easing the worst fears of investors after the president had previously said they could double. Yet, his move to raise tariffs on some Canadian goods to 35% threatens to inject fresh tensions into an already strained relationship.

Taken together, the average new tariff rate rises to 15.2% from 13.3% — up significantly from 2.3% in 2024, according to Bloomberg Economics. The biggest losers appear to be China and Switzerland, Bloomberg economist Maeva Cousin says.

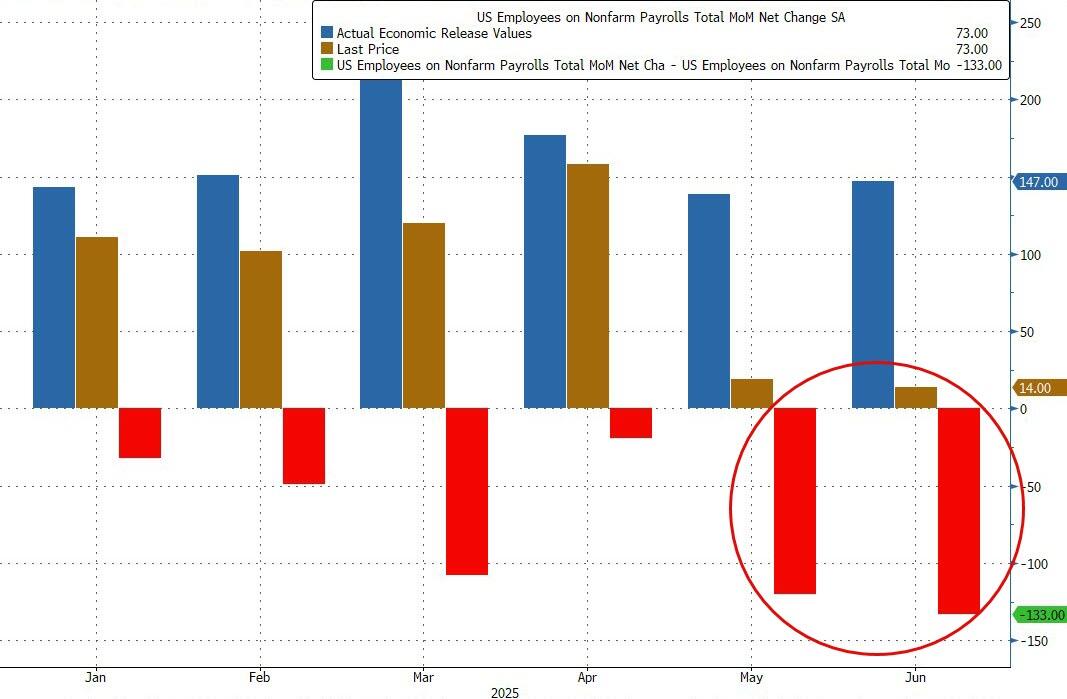

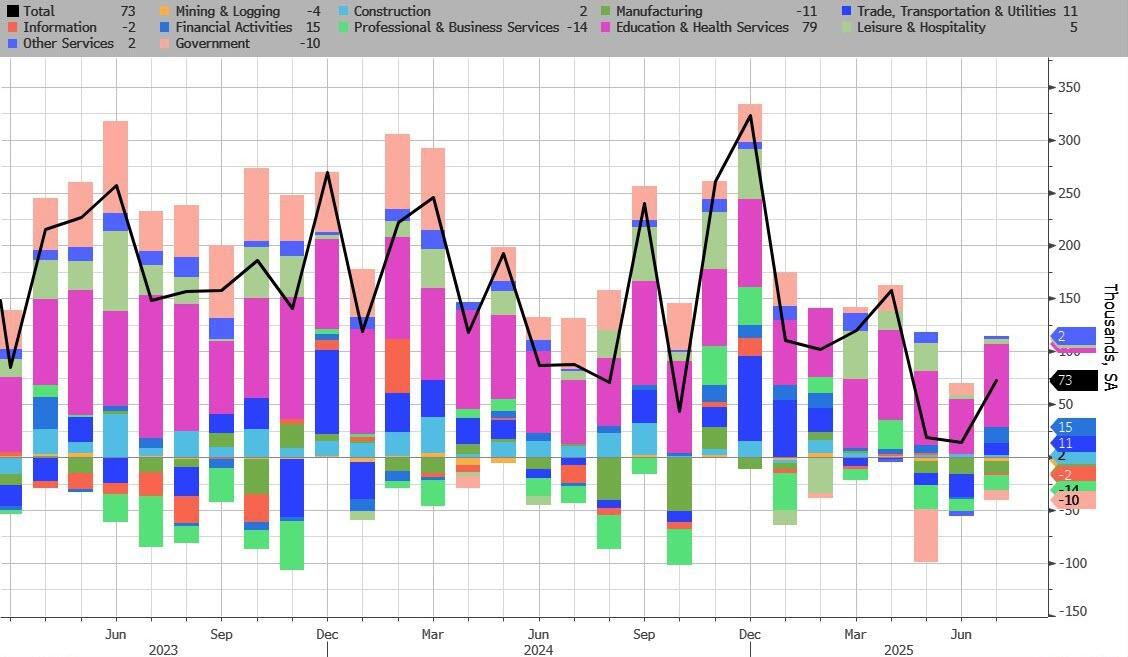

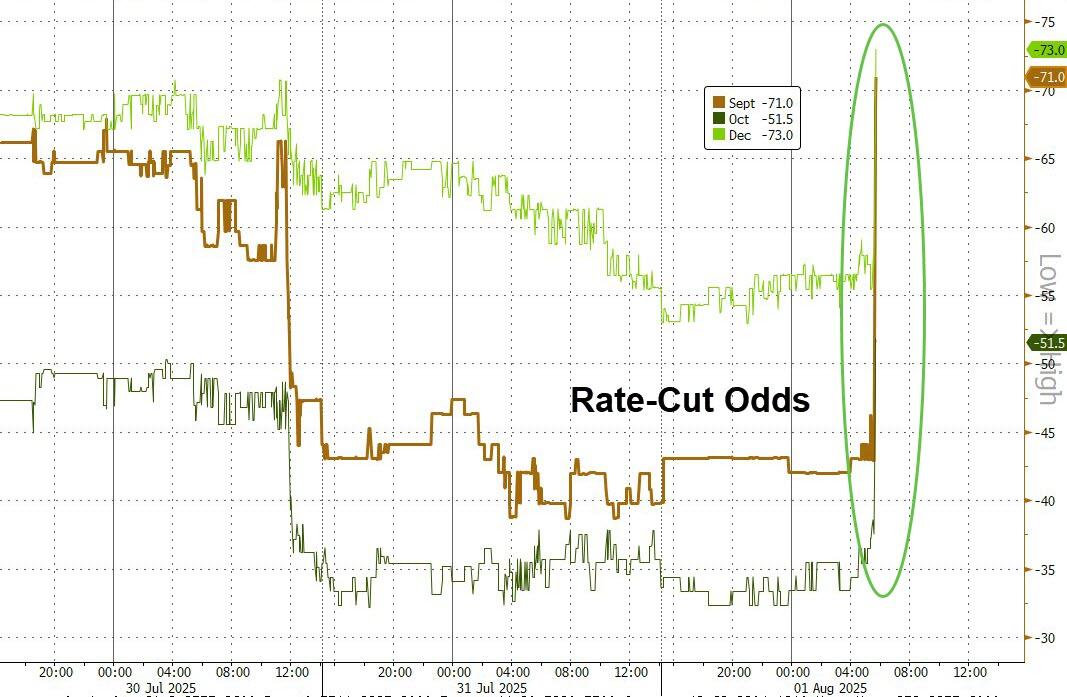

Now that tariff news is in the bag, all eyes turn to today’s jobs report: the US economy is expected to have created 104,000 jobs in July, down from 147,000 a month earlier. The “whisper” is for 120,000. According to JPMorgan, either would be good enough to take the S&P 500 higher (see our full preview here). Today’s closely-watched jobs report may give fresh hope to doves looking to make the case for the Fed to cut interest rates. There are fewer company updates to distract from payrolls, but a slew of new tariffs is dampening the mood.

“Given all the uncertainties, it makes a lot of sense for traders, for dealers to take some money off the table going into nonfarm payrolls today,” said Gareth Nicholson, CIO of Nomura International Wealth Management.

The Euro Stoxx 600 falls 1.2% to around a one-month low, tracking declines in Asia with pharmaceutical stocks including Novo Nordisk A/S, GSK Plc and AstraZeneca Plc leading declines after Trump demanded drug companies lower US prices. Travel, industrial and technology shares are also leading declines. The tariffs are “really bad for Europe,” said Ludovic Subran, chief investment officer at Allianz SE. “The cost for companies will be huge, as the US is the biggest market by far.” These are the biggest movers Friday:

Campari gains as much as 8.8%, the most since April, after the Italian spirits maker reported 1H results. Adjusted Ebitda and sales for the period beat consensus estimates and the company left its full-year guidance unchanged

Melrose Industries gains as much as 7.9%, the most in almost four months, after the aerospace company reported earnings ahead of expectations in the first half, which analysts at RBC say helps de-risk its full-year guidance

Erste shares rise as much as 3.1% to a fresh all-time high after the bank raised its forecast for return on tangible equity and net interest income. Analysts at Morgan Stanley note strong capital position

UMG shares fall as much as 8.9% after the music label reported Ebitda margin that expanded more slowly than expected during 2Q, with its merchandising unit being hit by higher tariffs and freight costs

European pharmaceutical stocks drop after US President Donald Trump demanded drug companies lower US prices, and Novo Nordisk loses its spot among Europe’s 10 most valuable companies after nearly a weeklong slump

Daimler Truck falls as much as 5.5% in early trade after the truckmaker lowered its outlook, citing the impact on sales from ongoing tariffs in North America. Order weakness in North America stood out, Citi says

Saint-Gobain shares fall as much as 5%, the most in almost four months, after results from the French construction materials producer showed a slowing volume trend into the second-quarter

J. Martins falls as much as 4.6% in early trading as 2Q earnings beat driven by rebound of like-for-like sales in Poland and better cost control is clouded by erosion of Portuguese retailer’s gross margin

Engie falls as much as 8.3%, before trimming losses, after the French energy group said most earnings metrics fell year on year, with Jefferies seeing a 24% miss on Ebit ex-nuclear. Shares are down 3.1% as of 10.29am in Paris

Cancom shares drop as much as 21%, the most since 2008, after the IT services provider cut its outlook for the full year, citing challenges in its core German market

Mutares shares fall as much as 22% after the German Financial Supervisory Authority (BaFin) says in statement that there are concrete indications the investment firm has violated accounting regulations

Earlier in the session, Asian stocks were set to record their biggest weekly decline since April as Washington’s tariffs damped the outlook for the export-dependent region. The MSCI Asia Pacific Index dropped as much as 1% on Friday, with South Korean equities leading declines after authorities unveiled plans to raise taxes on corporations and investors. Tech shares weighed on the regional gauge as Tokyo Electron dropped the most in nearly a year following a move by the chip tool maker to lower its full-year earnings outlook. The retreat in the Asian index marks a reversal of the back-to-back weekly gains that helped propel it to the highest level since March 2021. Investors are watching the parameters and impact of trade deals, as well as factors such as central bank policy direction to plot their next move.

In FX, the Bloomberg Dollar Spot Index rises 0.2%, trading at the highest in two months after Trump fired his latest salvo at the Federal Reserve, saying in a social-media post the institution’s board should “assume control” if Chair Jerome Powell doesn’t lower interest rates. Traders are also bracing for key US jobs data later Friday. The Swiss franc is among the weakest G-10 currencies, falling 0.5% against the greenback after Switzerland was hit with a 39% levy by Trump. The yen outperforms, rising 0.2% after some modest jawboning from the Japanese Finance Minister.

In rates, treasuries are mixed, with outperformance at the short-end pushing 2-year yields down 2 bps. Gilts lead a selloff in European government bonds, with UK 10-year yields rising 5 bps.

In commodities, WTI crude futures fall 0.7% to $68.80 a barrel. Gold rises $5. Bitcoin falls 1%. Bitcoin is on the backfoot, and trades back below the USD 115k mark – downside which is in-fitting with the broader risk tone.

Looking at today’s US economic data calendar we get the July jobs report (8:30am), July final S&P Global US manufacturing PMI (9:45am), and July ISM manufacturing and July final University of Michigan sentiment (10am). Fed speaker slate includes Hammack (9:10am) and Bostic (10:30am)

Market Snapshot

S&P 500 mini -1%

Nasdaq 100 mini -1.1%

Russell 2000 mini -1.5%

Stoxx Europe 600 -1.3%

DAX -1.8%

CAC 40 -1.9%

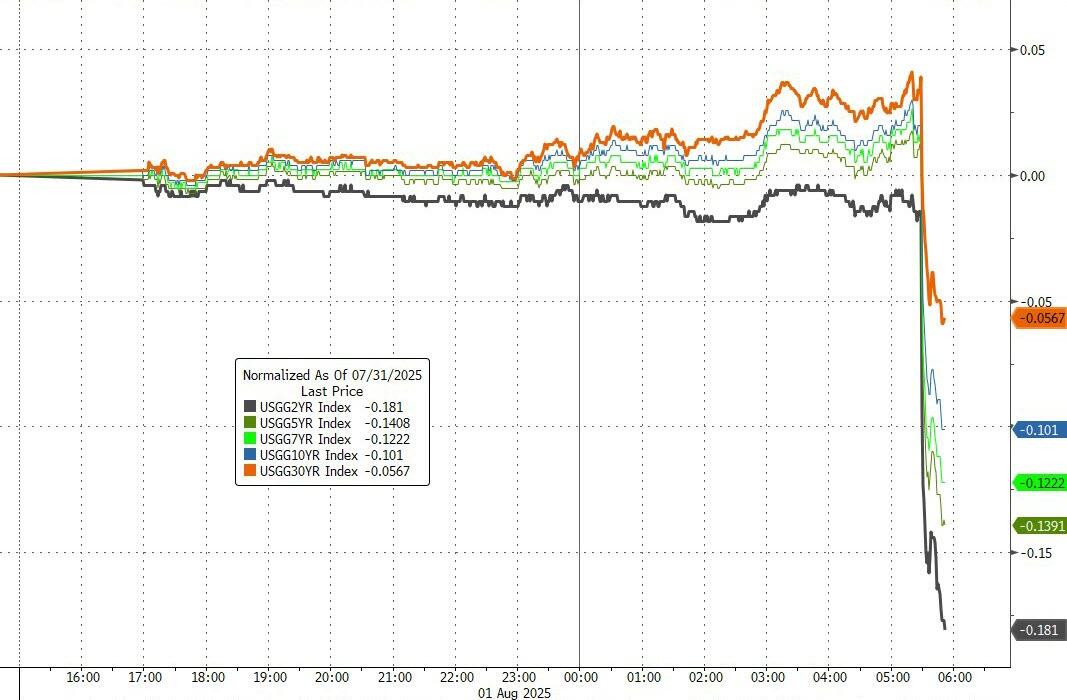

10-year Treasury yield +1 basis point at 4.38%

VIX +2 points at 18.69

Bloomberg Dollar Index +0.2% at 1224.03

euro -0.1% at $1.1402

WTI crude -0.6% at $68.86/barrel

Top Overnight News

Donald Trump set a 10% global minimum tariff, with rates of 15% and higher for countries with significant trade surpluses with the US. BBG

Trump says he remains open to trade deals, and negotiations are set to continue despite the new tariff rates going into effect. NBC News

Donald Trump will impose a 39% tariff on imports from Switzerland, one of the steepest levies globally which threaten to leave the country’s key exports reeling: BBG

Trump again criticized Powell in which he called him ‘Too late’ and said he is a terrible Fed Chair.

US held secret talks w/Moscow this week but failed to make progress on a ceasefire, and there isn’t much hope for Witkoff’s upcoming trip to Russia to change the situation. NYT

Asia’s factory activity deteriorated in July as soft global demand and lingering uncertainty over U.S. tariffs weighed on business morale, private sector surveys showed on Friday, clouding the outlook for the region’s fragile recovery. Reuters