AUGUST 4/GOLD CLOSED UP $24.65 TO $3372.55 WITH SILVER UP 50 CENTS TO $37.34//PLATINUM GAINED $40.20 TO $1337.15 WIHT PALLADIUM UP ONLY $1.90 TO $1192.30//GOLD COMMENTARY TONIGHT FROM ALASDAIR MACLEOD/EXCELLENT COMMENTARY TONIGHT ON THE PLIGHT OF THE GERMAN ECONOMY (MIDDLE EAR)//ISRAEL VS HAMAS/HEZBOLLAH ETC SUMMARY BY TBN //OTHER UPDATES ON THIS//RUSSIA VS UKRAINE UPDATES/COVID UPDATES/VACCINE INJURY REPORTS/MARK CRISPIN MILLER/PAUL ALEXANDER//NEWS ADDICTS/EVOL NEWS///OIL REPORTS: OIL RISES ON FURTHER TRUMP TARIFFS ON INDIA//USA TO HAVE A CRIMINAL REFER TO FORMER FBI CHRISTOPHER WRAY//ALSO INVESTIGATION ON JACK SMITH RE HATCH ACT// MARTIN ARMSTRONG ON GREG HUNTER PODCAST//SWAMP STORIES FOR YOU TONIGHT

072 C GOLDMAN 8 104 C MIZUHO SECURITIES US 4 118 C MACQUARIE FUTURES US 534 10 118 H MACQUARIE FUTURES US 256 132 C SG AMERICAS 10 190 H BMO CAPITAL MARKETS 902 285 C NANHUA USA-HK 5 323 C HSBC 320 357 332 H STANDARD CHARTERED B 142 363 H WELLS FARGO SECURITI 581 435 H SCOTIA CAPITAL (USA) 40 523 H INTERACTIVE BROKERS 2 555 C BNP PARIBAS SEC CORP 81 657 C MORGAN STANLEY 58 657 H MORGAN STANLEY 666 661 C JP MORGAN SECURITIES 667 686 C STONEX FINANCIAL INC 31 35 690 C ABN AMRO CLR USA LLC 30 709 C BARCLAYS 22 726 C PLUS500US FINANCIAL 25 732 C RBC CAP MARKETS 6 737 C ADVANTAGE FUTURES 1 880 C CITIGROUP 9 880 H CITIGROUP 404 905 C ADM 37 7

TOTAL: 2,625 2,625 MONTH TO DATE: 20,126

JPMORGAN stopped 667/2698

AUGUST

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 2625 CONTRACTs NOTICES FOR 262,500 OZ or 8.1648 TONNES

total notices so far: 20,126 contracts for 2,012,600 OR 62.600 tonnes)

FOR AUGUST

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 95 NOTICE(S) FILED FOR 0.475 million OZ/

total number of notices filed so far this month : 1064 CONTRACTS (NOTICES) for 5.320 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $24.65 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/./

INVENTORY RESTS AT 953.08 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.50 AT THE SLV: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: //A WITHDRAWAL OF 0.183 MILLION OUT OF THE SLV/

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 484.083 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA HUGE SIZED 1837 CONTRACTS TO 160,117 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.19 IN SILVER PRICING AT THE COMEX WITH RESPECT TO FRIDAY’S TRADING. WE FINALLY ARE MOVING MUCH HIGHER THAN THE BASE $34.40 SILVER PRICE BARRIER. WE HAD A HUGE SIZED LOSS OF 1162 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE 675 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO FRIDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $36.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON FRIDAY WITH SILVER’S GAIN IN PRICE. THE PRICE HOWEVER FINISHED MILES ABOVE THE MAGIC NUMBER OF $36.00 SILVER SPOT PRICE CLOSING AT $36.84 . WE HAVE A MEGA HUGE T.A.S. ISSUANCE AT 814 CONTRACTS ISSUED BY THE CME AND THAT STILL SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING ABOVE THE 38.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A HUGE 675 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 814 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN MONDAY’S// TRADING OR BEYOND/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUGE SIZED 1162 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR GAIN IN PRICE OF $0.19.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT/SATURDAY MORNING: A STRONG SIZED 814 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.19) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY FEW NET SILVER LONGS FROM THEIR PERCH AS WE DESPITE HAVING HUGE LOSS OF 1162 CONTRACTS ON OUR TWO EXCHANGES WE HAD HUGE T.A.S. SPREADER LIQUIDATION

WE HAD A 675 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.70 MILLION OZ FOLLOWED BY TODAY’S 85 CONTRACT QUEUE JUMP OR AN ADDITIONAL 425,000 OZ WILL STAND FOR PHYSICAL ON THIS SIDE OF THE POND //NEW STANDING ADVANCES TO 5.375 MILLION OZ.

THUS:

INITIAL STANDING FOR AUGUST: 4.70 MILLION OZ FOLLOWED BY TODAY’S 425,000 OZ QUEUE JUMP//NEW STANDING; 5.375 MILLION OZ

WE HAD:

/ HUGE COMEX OI LOSS+// A HUGE SIZED EFP ISSUANCE 675 CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 814 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED A SMALL XXX CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 2 DAY(S), total 1625 contracts: OR 8.125 MILLION OZ (812 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 8.125 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 8.125 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1837 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.19 IN SILVER PRICING AT THE COMEX// FRIDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE 675 CONTRACT EFP ISSUANCE CONTRACTS: 675 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 5 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 425,00 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 5.375 MILLION OZ

THE NEW TAS ISSUANCE FRIDAY NIGHT (814 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE IN TUESDAY THROUGH THURSDAY TRADING.

WE HAD 95 NOTICE(S) FILED TODAY FOR 0.475 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY STRONG SIZED 9,797 OI CONTRACTS TO 437,777 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 3954 CONTRACTS //.

WE HAD A STRONG INCREASE IN COMEX OI (9,797 CONTRACTS) . THIS OCCURRED WITH OUR GAIN OF $51.40 IN PRICE// FRIDAY///.

LAST FOUR MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

AUGUST: 60.547 TONNES OF GOLD FOLLOWED BY TODAY’S SMALL QUEUE JUMP OF 0.1493 TONNES //NEW STANDING ADVANCES TO 64.221 TONNES OF GOLD/.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2510 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 437,777 /STILL EXTREMELY LOW AND WE NOW WITNESS A LOW COMEX OI WITH AN EXTREMELY HIGH PRICE OF GOLD

SILVER ALSO HAS A LOW COMEX OI OF 160,117 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,307 CONTRACTS WITH 9797 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2510 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 12,307 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 939 CONTRACTS AND THESE ISSUANCES ARE USED TO INITIATE A RAID WHEN CALLED UPON. GOLD PRICE ON FRIDAY ROSE BY $51.40

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(2510) ACCOMPANYING THE LARGE SIZED INCREASE IN COMEX OI OF 9797 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 12,307 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR AUGUST AT 60.547 TONNES FOLLOWED BY TODAY’S 0.1593 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 64.221 TONNES

NEW STANDING FOR GOLD, AUGUST CONTRACT AT 64.221 TONNES OF GOLD

.

/ 3) LITTLE IF ANY T.A.S. LIQUIDATION AND MONTH END SPREADER LIQUIDATION DISAPPEARED FROM THE SCENE AS WE HAD 1)A $51.40 COMEX PRICE GAIN. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG GAIN OF 12,307 CONTRACTS ON OUR TWO EXCHANGES WE HAD BASICALLY ZERO LIQUIDATION OF OUR TAS SPREADERS/ /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED FRIDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND YOU CAN VISUALIZE THIS BY THE HUGE AMOUNTS OF QUEUE JUMPING WE HAVE BEEN HAVING LATELY

4) VERY STRONG SIZED COMEX OI GAIN// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (2510 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 934 T.A.S.CONTRACTS/

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

TOTAL EFP CONTRACTS ISSUED: 4400 CONTRACTS OR 440,000 OZ OR 13.685 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 2200 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN2 TRADING DAY(S) IN TONNES 13.685 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 13.685 TONNES DIVIDED BY 3550 x 100% TONNES = 0.0385% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

UNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 13.685 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1837 CONTRACTS OI TO 160,117 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 675 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 675 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 650 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1837 CONTRACTS AND ADD TO THE 675 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 1162 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.19 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 5.810 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

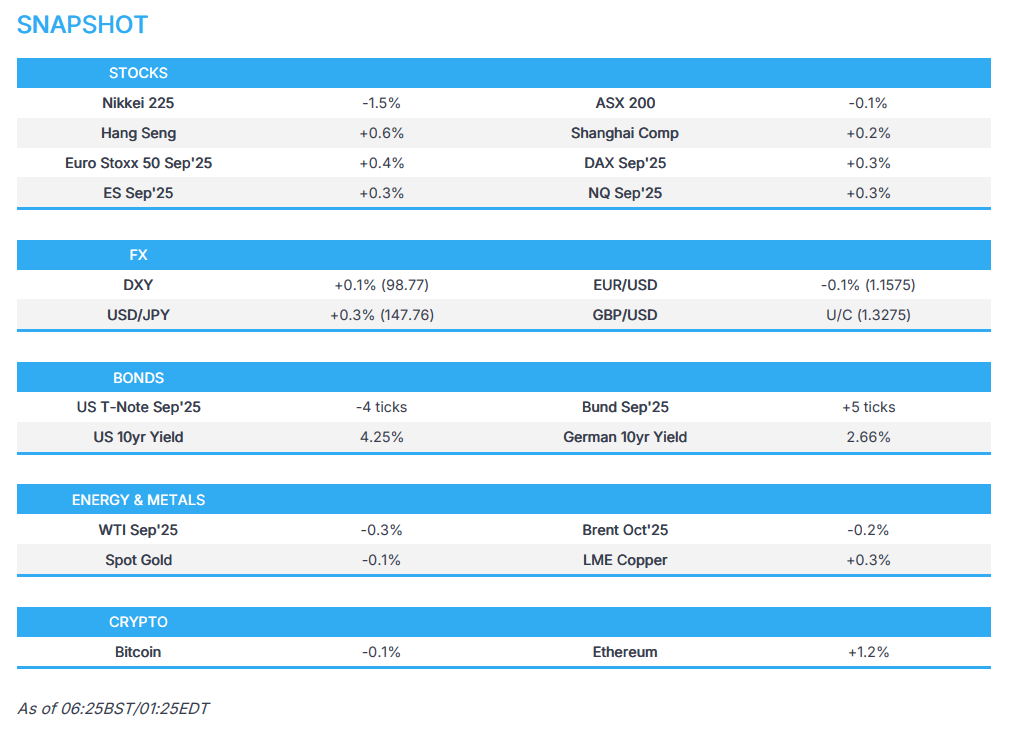

ASIAN MARKETS THIS MONDAY MORNING:

SHANGHAI CLOSED UP 23.36 PTS OR 0.66%

//Hang Seng CLOSED UP 225.64 PTS OR 0.92%

// Nikkei CLOSED DOWN 508.90 PTS OR 1.25% //Australia’s all ordinaries CLOSED UP 0.06%

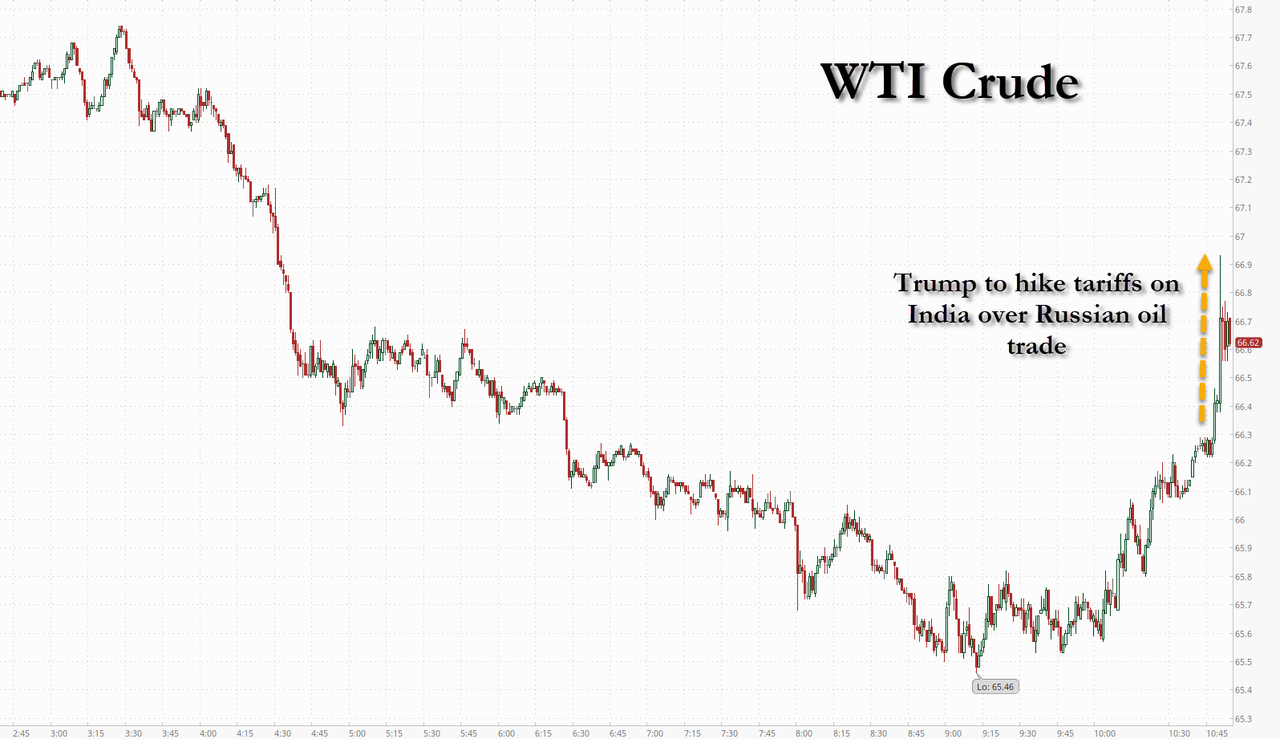

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1766 OFFSHORE CLOSED UP AT 7.1789/ Oil DOWN TO 66.61 dollars per barrel for WTI and BRENT DOWN TO 68.81 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1766 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1789 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY STRONG SIZED 9797 CONTRACTS TO 437,777 OI WITH OUR HUGE GAIN IN PRICE OF $51.40 WITH RESPECT TO FRIDAY’S // TRADING.. WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2510 ). WE HAD LITTLE T.A.S. LIQUIDATION //FRIDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 16,261 CONTRACTS WITH MONTH END SPREADERS DISAPPEARING FROM THE SCENE AND THIS WAS COUPLED WITH MINIMAL T.A.S LIQUIDATION.

LAST WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. OR IT COULD BE THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY!!.THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY IS NOW 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

EARLY THIS SATURDAY MORNING THE CME ANNOUNCED A ZERO EXCHANGE FOR RISK ISSUANCE!

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 0 SO FAR

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS GENERALLY THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE OR FRBNY FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 6TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH JULY WITH A TWO MONTH HIATUS)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 12,307 CONTRACTS WITH OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 934 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED YESTERDAY WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS TODAY’S SMALL QUEUE JUMP OF 0.1493 TONNES//NEW STANDING 64.221 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 234 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NONE COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY A SMALL QUEUE JUMP OF 0.1493 TONNES/NEW STANDING ADVANCES TO 64.221 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2510 EFP CONTRACT WAS ISSUED: : /AUGUST 2510 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2510 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

HUGE LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY BUT LITTLE ON FRIDAY

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT/SATURDAY WAS A SMALL SIZED SIZED 934 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS PAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S HUGE GAIN IN PRICE IN GOLD AND SILVER AND A CORRESPONDING GAIN OF CONSIDERABLE COMEX OI. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH THE RARE TWO ISSUANCES OF EXCHANGE FOR RISK! THE RAIDS THROUGHOUT LAST WEEK’S OPTION EXPIRY WEEK WERE USED TO LOWER THE HUGE DERIVATIVE LOSSES ENDURED BY THE BANKERS.

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S SMALL QUEUE JUMP OF 0.1493 TONNES//NEW STANDING ADVANCES TO 64.221 TONNES.

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $51.40/ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD MINOR T.A.S. SPREADER LIQUIDATION AND MONTH END SPREADERS DISAPPEARED FROM THE SCENE ////FRIDAY. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID ON FRIDAY.

SATURDAY MORNING//FRIDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL FRIDAY EVENING/ SATURDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE GAINED A VERY STRONG SIZED TOTAL OF 38.28 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD SATURDAY’S SMALL QUEUE JUMP OF 0.1493 TONNES OF GOLD//NEW STANDING ADVANCES TO 64.221 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $51.40

WE HAD A HUGE 3954 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 16,261 CONTRACTS OR 1,626,100 0Z (50.57 TONNES)

i) Out of JPMorgan 64,302.000 oz (2000 kilobars) ii) Out of Loomis; 2300.290 oz

total withdrawal: 66,602.200 oz

2.07 tonnes)

.

Deposit to the Dealer Inventory in oz

1 ENTRIES

1 entry: i) Into the dealer Asahi: 96,374.518 oz

total deposit 96,374.518 oz (2.99 tonnes)

Deposits to the Customer Inventory, in oz

1 ENTRY i) into Loomis: 48,226.500 oz

(1500 kilobars)

total deposit customer Loomis 48,226.500 oz (1.5 tonnes)

total weight customer and dealer: 4.49 toonnes

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

2625 notice(s) 262500 OZ 8.1648 TONNES

No of oz to be served (notices)

522 contracts 52,200 OZ 1.623 TONNES

Total monthly oz gold served (contracts) so far this month

20,126 notices 2,012,600 oz 62.600 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits:

1 ENTRIES

1 entry: i) Into the dealer Asahi: 96,374.518 oz

total deposit 96,374.518 oz

(2.99 tonnes)

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRY i) into Loomis: 48,226.500 oz

(1500 kilobars)

total deposit customer Loomis 48,226.500 oz (1.5 tonnes)

total weight customer and dealer: 4.49 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

two entries

i) Out of JPMorgan 64,302.000 oz (2000 kilobars) ii) Out of Loomis; 2300.290 oz

total withdrawal: 66,602.200 oz

2.07 tonnes)

adjustments: 1

Malca: customer to dealer; 32,118.849 oz (999 kilobars)

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 3,147 CONTRACTS FOR A LOSS OF 2,149 CONTRACTS

WE HAD 2197 CONTRACTS SERVED ON FRIDAY SO WE GAINED A SMALL 48 CONTRACTS OR A 4800 OZ OF GOLD (0.1493 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND. THIS REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

SEPT GAINED 398 CONTRACTS TO 5083

OCTOBER GAINED 2258 CONTRACTS UP TO 69,351

We had 2625 contracts filed for today representing 262,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and O notices issued from their client or customer account. The total of all issuance by all participants equate to 2625 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 667 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (20,126 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 3147 CONTRACTS) minus the number of notices served upon today (2625 x 100 oz per contract) equals 2,064,700 OZ OR 64.221TONNES

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (20,126 x 100 oz +we add the difference for front month of AUGUST (3147 OI} minus the number of notices served upon today (2625 x 100 oz) which equals 2,064,700 OZ OR 64.221 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 64.221 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL REGISTERED SILVER: 190.743 MILLION OZ//.TOTAL REG + ELIGIBLE. 506.602Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 106 OPEN INTEREST CONTRACTS FOR A GAIN OF 34 CONTRACTS. WE HAD 51 CONTRACTS SERVED ON FRIDAY SO WE GAINED 85 CONTRACTS OR AN ADDITIONAL 425,000 OZ WILL STAND AS THEY ENTERTAINED A STRONG QUEUE JUMP

SEPTEMBER LOST 3067 CONTRACTS DOWN TO 109,684 CONTRACTS.

OCTOBER GAINED 6 CONTRACTS TO 374

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 95 or 0.475 MILLION oz

CONFIRMED volume; ON FRIDAY 75,097 good//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1064 X5,000 oz = 5.320 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (106) AND the number of notices served upon today (95 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1064) Notices served so far) x 5000 oz + OI for the front month of AUGUST(106) minus number of notices served upon today (95)x 5000 oz equals silver standing for the AUGUST contract month equating to 5.375 MILLION OZ .

New total standing: 5.375 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.743 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/506.602 million. 41.65%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 953.08 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

Banks simply lend credit into existence. Ideas that they are simply financial intermediaries, or that they lend deposits are incorrect. This article explains why.

Economists of all disciplines are seemingly unaware of the credit creation process. In their theoretical discourses of money and credit they assume that banks are intermediaries, taking in deposits and lending them out. Consequently, they are seen to have little consequence in economic analysis.

The exception, perhaps, is the Austrian school which posits that bank credit is destabilising. But even there, Ludwig von Mises in his The Theory of Money and Credit appears confused on this issue, writing,

“The activity of banks as negotiators of credit is characterized by the lending of other people’s, i.e. of borrowed money. Banks borrow money in order to lend it; the difference between the rate of interest that is paid to them and the rate that they pay less their working expenses constitutes their profit on this kind of transaction”[i]

In a youtube interview of Richard Werner by Tucker Calson, Werner correctly identified the process of bank credit creation. It was subsequently followed by a commentary on this topic by two senior economists of the Austrian School, Bob Murphy and Jonathan Newman to whom the concept appeared to be new to them, having been schooled in von Mises’s analysis.

In this article I shall explain why the fractional reserve theory is incorrect, and Werner’s explanation of credit creation is what actually happens. For the avoidance of doubt and to clarify the position, we must make two important definitions at the outset:

· Gold is money, and everything else is credit. Gold has no counterparty risk and is final settlement, extinguishing credit. Credit is always on the other side of a balance sheet to a debt obligation.

· Banks are dealers in credit.

Defining credit

When both Werner and the Austrians talk of credit as money, they are factually incorrect. The difference was set out in Justinian’s Pandects in Roman law, which is the basis of common law in all the empire’s successor nations, their colonies, and dominions including the USA. No amount of gold ownership bans, executive orders, or confiscation alters this fact. Technically, gold is corporeal money, and credit which has no physical existence is incorporeal.

Gold needs no further definition. Credit exists in many forms, but it is always an obligation for future settlement. It is ubiquitous and governs all our business relationships, gold rarely being used in settlement. A tradesman will be employed in his work, extending credit to his customer until the work is completed satisfactorily when he expects payment to be made. Unless he is paid in advance, an employee will provide his skills extending credit to his employer until the end of the week, or month, when he also expects to be paid.

Bonds are an obligation to pay interest and repay the principal under the terms of a loan agreement or prospectus. Even shares in a company are credit, because they represent a commitment by the company’s management to deliver an income stream or to accumulate value in the company in trust for the shareholder. Everything works on credit, where payment is a promised obligation.

All financial instruments are credit. That they have value is again down to Justinian’s Pandects, which incorporated the findings of two Roman jurors, Ulpian and Julius Paulus in the second and third centuries AD. These two jurors ruled that a credit could be exchanged without a debtor’s agreement. No transfer, no value: even bad debts are bought and sold, and modern capital markets could not exist without their rulings.

It is vital to understand the all-embracing role of credit in an economy. It goes far beyond banking. Anyone can and does create credit, subject to his or her credibility.

Credit is wrongly termed money by economists and statisticians alike. A national currency is a promise to pay in gold and appears as such on the issuing central bank’s balance sheet as a liability. The best it ever was was a money substitute; today it is only fiat. Checking and deposit accounts with commercial banks are credit denominated in a national currency, representing a bank’s promise to pay its customers.

In practice, money in the form of gold coin or bars is almost never used as circulating media. When you pay someone with a bank deposit, it is either in cash which is a central bank’s liability, or by cheque or deposit-transfer from your bank to your creditor’s bank. In days of gold standards, nations and traders would settle trade imbalances in gold particularly when there was credit risk perceived in holding a foreign currency. But that finally ceased in 1971 when the Bretton Woods agreement was “suspended”.

How banks create credit

Werner referred to the Goldsmiths in London as the originators of modern banking. In fact, banking was invented by the Romans, but the basis of credit creation today was in London in the seventeenth century during the civil war (1642—1651). Goldsmiths routinely stored gold and silver for customers, issuing receipts as evidence of ownership. and they soon discovered that these receipts changed hands as a more convenient form of payment than gold itself.

The goldsmiths then found that they themselves could issue credit based on customers’ gold so long as the customer was prepared to relinquish ownership in return for interest at 6% before ownership was returned on demand.

It should be noted that the interest paid by a goldsmith to a customer came from the goldsmith’s general profits and was by way of a dividend and not interest earned on his deposit by lending it out. Presumably, it was this error in understanding which led economists to incorrectly believe that deposit-taking was the basis of fractional reserve banking.

The goldsmiths soon found that they could safely issue more loans than they had gold to back them, based on a calculation of the likelihood of depositing customers demanding the return of their gold. It was from this practice that modern banking evolved, with bank credit extended to merchants and businesses being entirely responsible for financing the rapid development of Britain’s industrial revolution.

As dealers in credit, banks were doing what we all do by creating credit and obligations in our day-to-day business activities. They would simply offer credit at interest to a customer they deemed creditworthy , crediting his account to enable him to draw down the loan. The simplified illustration below shows how this works in practice, starting with the bank’s own capital:

The bank creates the loan and, in its books, a matching deposit. Notice how the bank does not use its own capital. By creating the loan, the bank doubles its own capital from interest earned in this example.

Importantly, as the customer draws down on the loan, the balance on his deposit reduces by the same amount exactly. The loan is drawn down in order to pay the customer’s own creditors who may or may not bank with the same bank. This creates deposits in other names some elsewhere, leading to an imbalance between the bank’s liabilities and assets. When this imbalance is not offset by other customer’s movements, the bank either has a surplus on its assets to lend to other banks, or a surplus on its liabilities which it has to fund from other banks. This is the purpose of bank clearing facilities and the function of the interbank market.

“The vast majority of money held by the public takes the form of bank deposits. But where the stock of bank deposits comes from is often misunderstood. One common misconception is that banks act simply as intermediaries, lending out the deposits that savers place with them. In this view deposits are typically ‘created’ by the saving decisions of households, and banks then ‘lend out’ those existing deposits to borrowers, for example to companies looking to finance investment or individuals wanting to purchase houses.

“In fact, when households choose to save more money in bank accounts, those deposits come simply at the expense of deposits that would have otherwise gone to companies in payment for goods and services. Saving does not by itself increase the deposits or ‘funds available’ for banks to lend. Indeed, viewing banks simply as intermediaries ignores the fact that, in reality in the modern economy, commercial banks are the creators of deposit money. This article explains how, rather than banks lending out deposits that are placed with them, the act of lending creates deposits — the reverse of the sequence typically described in textbooks.”

It really is that simple.

Why fractional reserve banking is incorrect

Fractional reserve banking assumes that a customer first deposits currency or payment from another bank into his bank. The bank then lends most of it, typically assumed to be 90% of the deposit, keeping a reserve of 10% against the possibility of default. Hence the term, fractional reserve.

This begs the question as to where the first deposit comes from. It can’t come from another bank. Presumably, it is currency in the form of notes issued by the central bank.

The story then goes that the 90% is loaned out to be spent by the borrower, ending up as deposits in other banks. Other banks then lend out 90% of that. By a series of loans through the banking system, the original deposit is said to end up being multiplied nearly nine times through this iterative process.

A moment’s thought will dismiss the multiplier argument, because the closest the banking system can get to lending the entire deposit is only 90% of it, however many banks are involved. But it doesn’t stop claims that a money multiplier effect inflates bank credit, as the screenshot below from an article by Princeton University demonstrates:

The error is to not recognise that it is the same credit leant out by banks A to K. By the same token, you would say that a $100 banknote circulating from hand to hand increases the money supply by much more than its notional value. Obviously, it does not.

In any event, the fractional reserve banking theory is incorrect, as the Bank of England article and its extract above makes clear. I covered this point in a film for The Cobden Centre which was premiered at the House of Lords in 2023. My contribution starts at 9 minutes, and is confirmed at 8 minutes in by William White, who was an economic advisor to the Bank for International Settlements, having started his career at the Bank of England and spent 22 years at the Bank of Canada.

Richard Werner’s interview by Tucker Carlson threw up other insights in the world of bank credit which are derived from a proper understanding of bank credit creation, but these are beyond the scope of this article.

[i] See The Theory of Money and Credit, Part 3, Chapter 1, section 2.

3. CHRIS POWELL AND GATA GOLD DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 234

ANDREW INTERVIEWS: LONDON PAUL:

5. COMMODITY REPORT..COPPER

ASIAN MARKETS THIS MONDAY MORNING:

SHANGHAI CLOSED UP 23.36 PTS OR 0.66%

//Hang Seng CLOSED UP 225.64 PTS OR 0.92%

// Nikkei CLOSED DOWN 508.90 PTS OR 1.25% //Australia’s all ordinaries CLOSED UP 0.06%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1766 OFFSHORE CLOSED UP AT 7.1789/ Oil DOWN TO 66.61 dollars per barrel for WTI and BRENT DOWN TO 68.81 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1766 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1789 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1766 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1789

HANG SENG CLOSED UP 225.64 PTS OR 0.92%

2. Nikkei closed DOWN 508.90 PTS OR 1/25%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 99.62/ EURO FALLS TO 1.1571 DOWN 15 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.503//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.74…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6718/Italian 10 Yr bond yield DOWN to 3.512 SPAIN 10 YR BOND YIELD DOWN TO 3.247%

3i Greek 10 year bond yield DOWN TO 3.369

3j Gold at $3259.00 Silver at: 37.22 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 21 /100 roubles/dollar; ROUBLE AT 79/71

3m oil (WTI) into the 66 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147/74// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.503% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8083 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9353 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.246 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.847 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.714 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.68

10 YR UK BOND YIELD: 4.586 UP 0 PTS

10 YR CANADA BOND YIELD: 3.385 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.942 DOWN 0 PTS

2a New York OPENING REPORT

Futures Rise, Recovering From Friday’s Dump On Rising Rate Cut Expectations

Monday, Aug 04, 2025 – 08:06 AM

Futures are higher as markets rebound from last week’s sell-off amid increased expectations the Fed will ride to the rescue with rate cuts following Friday’s dismal US jobs data. As of 7:45am ET, S&P 500 and Nasdaq futures climbed 0.7% after the index had its biggest decline since May on Friday. Pre-market, Mag7 and Semis are outperforming with Cyclicals over Defensives. Bond yields are 2-3bp higher as the USD falls again. Commodities are weaker with Energy underperforming as OPEC+ approves another supply hike. This is a catalyst-light week with tomorrow’s ISM the most important and heightened focus on weekly claims with the Fed spotlighting the unemployment rate.

In premarket trading, all Magnificent Seven stocks are higher alongside index futures (Amazon +1.8% after a Friday selloff, Nvidia +1.2%, Meta Platforms +1.1%, Tesla +1%, Alphabet +0.8%, Microsoft +0.8%, Apple +0.8%). here are the other notable premarket movers:

Berkshire Hathaway (BRK/B) is down 0.6% after Warren Buffett’s company took a $3.8 billion impairment on its Kraft Heinz stake.

Boeing (BA) falls 0.3% as workers at its St. Louis-area defense factories strike for the first time in almost three decades.

Blade Air Mobility Inc. (BLDE) is up 16% after Bloomberg reported that Joby Aviation Inc. (JOBY) is exploring an acquisition of the helicopter ride-share operator. Joby shares are up 5%.

CommScope (COMM) shares climbed 42% before being halted after reaching a deal to sell its broadband connectivity arm for about $10.5 billion in cash to Amphenol Corp. as it seeks to cut its debt. Amphenol (APH) gains 4%.

Kodiak Gas (KGS) rises 5% after the announcement that the provider of natural gas compression services will join the S&P Small Cap 600 Index.

Opendoor (OPEN) climbs 14% as much as 20% after the company regained compliance with the Nasdaq exchange.

Spotify (SPOT) gains 3% after the audio-streaming company said it will increase the monthly cost of premium subscriptions in some markets.

Steelcase Inc. (SCS) soars 45 % after HNI (HNI) agreed to buy the company. HNI shares are down 20%.

Tyson Foods (TSN) rises 4% as management raised its earnings forecast after quarterly profit unexpectedly rose as a boom in US chicken continues to offset losses in the beef business.

Wayfair rises 11% after the e-commerce firm posted second quarter profit that sailed past estimates.

Friday’s tumble on Wall Street, which was sparked by rising US unemployment and slower job creation, boosted bets for a Fed rate cut to prop up the market economy. Traders rushed into Treasuries despite worries about the inflationary effect of Trump’s tariffs, which have kept policy makers in hawkish mode.

“We’re buyers of pullbacks and bullish the next 12 months,” Morgan Stanley equity strategists led by Michael Wilson wrote in a note. “We think the Fed will eventually transition to cuts. Friday may be all we get to the downside for now; that is, until the next payroll number or other weaker, lagging growth data is potentially revealed.”

Overnight-indexed swaps signaled more than 80% odds of a reduction next month while fully pricing in one more cut by year-end. Some market-watchers are even anticipating the Fed may cut rates by 50 basis points, twice the regular amount. That may be too optimistic, given the outlook for inflation and growth, according to Pictet Wealth Management.

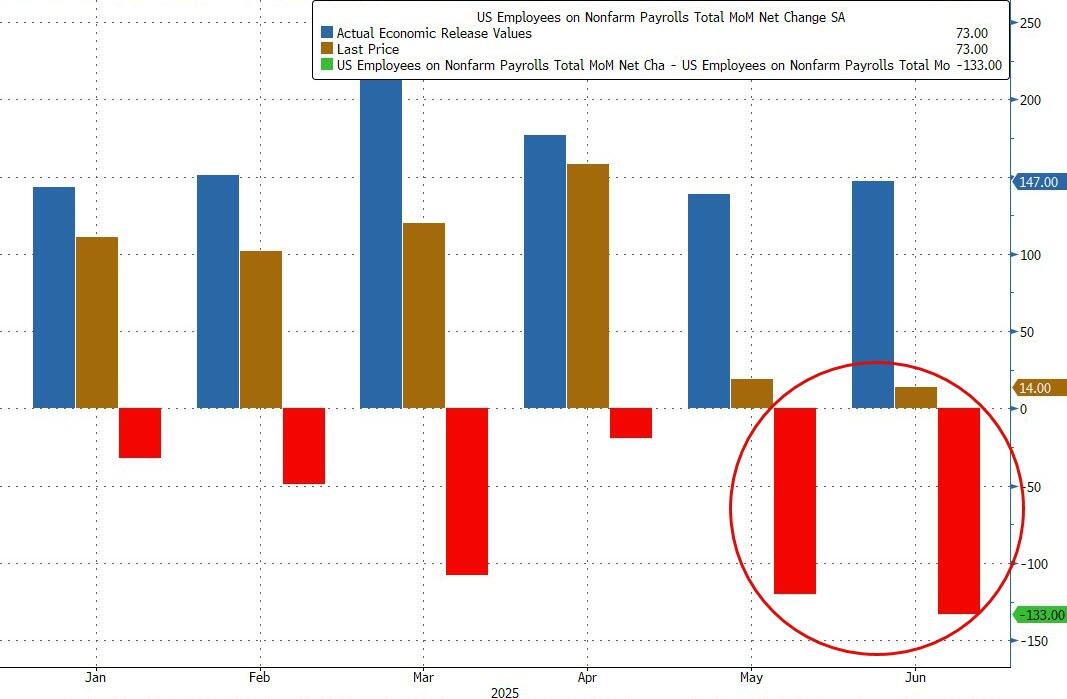

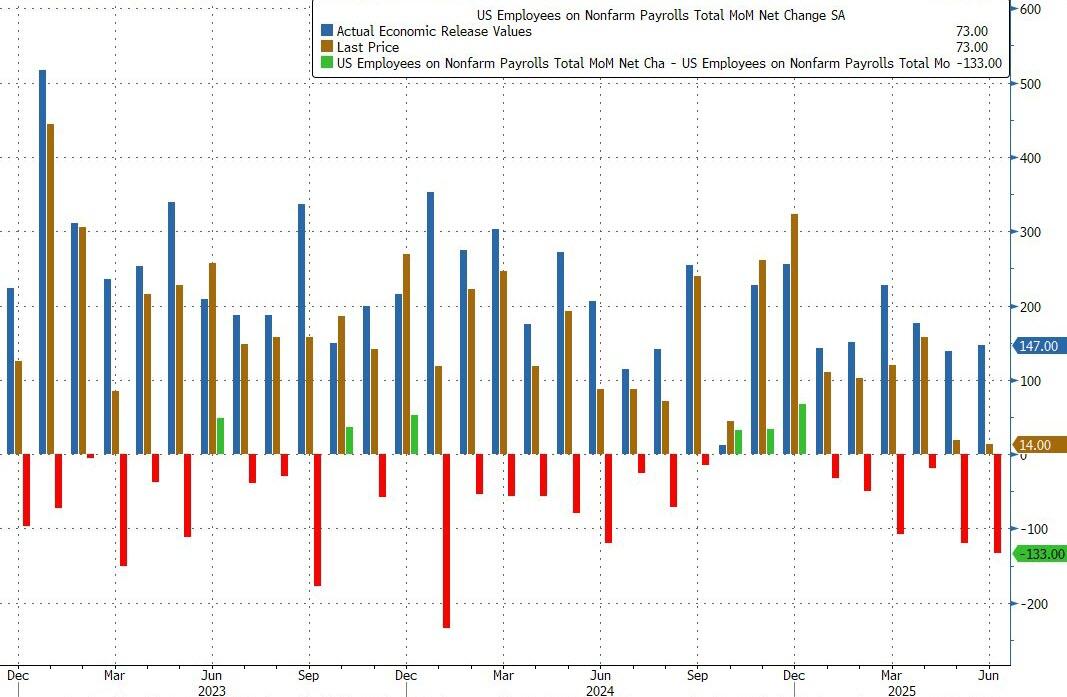

Separately, Trump said he will announce a new Fed governor and jobs data statistician in the coming days, two appointments that could shape his economic agenda. The Fed announced Friday that Adriana Kugler will step down from her position as a governor, giving Trump an opportunity to install a policymaker who aligns with his demands for lower interest rates. Also on Friday, Trump fired chief labor statistician Erika McEntarfer hours after labor market data showed weak jobs growth based in part on steep downward revisions for May and June.

Meanwhile, the US Trade Representative Jamieson Greer sounded a cautiously optimistic note on discussions with China on rare earth flows, following trade talks that further steadied ties between the economies. “Things have changed dramatically in the trade environment globally, not only the US,” veteran investor Mark Mobius said in a Bloomberg TV interview. “People are looking at this much more realistically. There’s going to be a lot of thinking about how to make things fairer for all countries involved.”

Europe’s Stoxx 600 index rose about 0.6%. Banks led the advance after UK lenders won a major reprieve in a pivotal UK car finance case, with Lloyds Banking Group Plc surging more than 7%. As noted above, the Swiss stocks benchmark, meanwhile, fell as the market reopened after a holiday, on worries about the impact from US President Donald Trump’s punitive 39% export tariff and a push for drugmakers to lower prices. Here are the biggest movers Monday:

UK lenders including Lloyds and Barclays advance after they won a major reprieve in a pivotal UK car finance case; Jefferies analyst Jonathan Pierce says the ruling is a “huge win for industry” that shows “common sense”

Clarkson shares rise as much as 6.4% to the highest level since March after the shipping-services company posted results ahead of expectations and reiterated its guidance, which analysts at Panmure Liberum say is reassuring

Novo Nordisk shares rise as much as 2.9%, paring some of last week’s record 32% drop. Goldman Sachs analysts say bull/bear scenarios for the Danish drugmaker “suggest upside risk”

TeamViewer shares rise as much as 3.5% as Kepler Cheuvreux upgrades the German software company to buy as it sees momentum improving in the coming quarters and says this isn’t factored into the valuation

Metlen Energy and Metals’ shares rose in its debut on the London Stock Exchange on Monday after moving its primary listing from Athens, although the trading in the stock was relatively thin

Swiss stocks are down as the market resumes trading for the first time since President Trump unexpectedly slapped punitive 39% tariffs on the country. Roche, ABB and UBS are among the biggest decliners in the SMI Index

Stabilus shares fall as much as 12% after the German machinery and equipment maker’s 3Q earnings missed expectations, according to Bernstein, while it narrowed its full-year adjusted Ebit margin and revenue forecast

Auction Technology Group drops as much as 22%, the most since 2023, after the online marketplace operator downgraded its margin guidance for the full year, which analysts at Panmure Liberum said will pressure consensus

Swiss stocks slumped as the market reopened after a holiday, on worries about the impact from US President Donald Trump’s punitive 39% export tariff and a push for drugmakers to lower prices.

Earlier in the session, Asian equities traded in a narrow range, with Japanese stocks leading declines while South Korean shares rose after growing optimism a controversial tax plan may be revised. The MSCI Asia Pacific Index gained slightly, erasing an earlier loss of as much as 0.5%. Advances in Tencent and Nintendo helped boost the regional benchmark. MUFG was among the biggest drags along with other Japanese large caps including Recruit and Hitachi. Key equity indexes fell more than 1% in Tokyo while the yen climbed, as Friday’s weak US payrolls data raised expectations for Federal Reserve interest-rate cuts. Korean benchmarks rebounded as a petition to withdraw planned corporate and capital-gains tax hikes drew strong support. The regional MSCI Asia gauge was set to snap a six-day decline, as investors digested a slew of new US tariffs. Shares rose in Hong Kong as investors looked beyond the Politburo meeting, seeking fresh catalysts amid ongoing tariff negotiations between US and China. Mainland investors also poured a record amount of money into exchange-traded funds that track the market in the Asian financial hub.

In FX, the dollar was steady after a gauge of the greenback’s strength plunged 0.9% on Friday. The Swiss franc underperforms, falling 0.5% against the greenback having only derived brief support from a larger-than-expected rise in CPI.

In rates, treasuries pared last week’s gains as traders braced for a hefty slate of bond sales this week. Yields on the 10-year notes climbed 1 basis point to 4.23% after dropping 16 basis points Friday. Gilts dip but German government bonds are steady. Treasury new-issue auctions this week begin Tuesday with $58 billion 3-year notes, followed by $42 billion 10-year notes and $25 billion 30-year bonds Wednesday and Thursday

In commodities, WTI crude futures slide 1.3% to near $66.50 a barrel after OPEC+’s latest supply increase. Spot gold is steady near $3,360/oz.