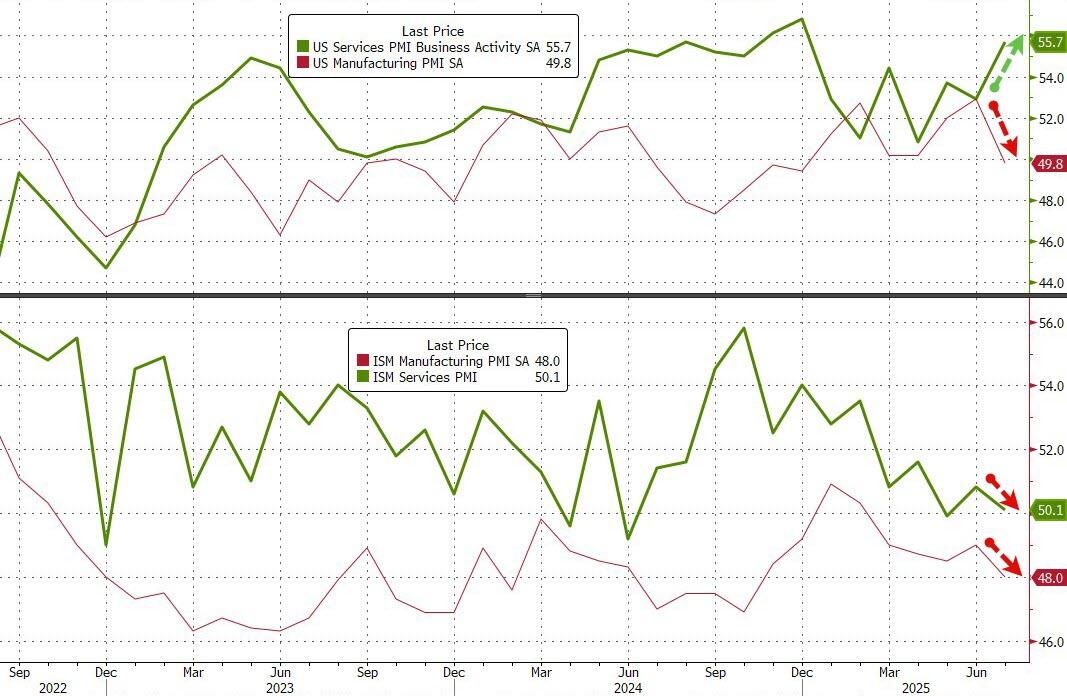

AUGUST 5/GOLD CLOSED UP $8.45 TO $3381.00 WHILE SILVER CLOSED UP $1.51 TO $37.85///PLATINUM CLOSED DOWN $16.85 TO $1320.30 WITH PALLADIUM CLOSING DOWN $6.35 TO $6.25//ZERO HEDGE HAS TWO IMPORTANT GOLD COMMENTARIES FOR YOU TONIGHT//USA WILL INCLUDE GOLD AND PLATINUM IN SWITZERLAND’S 39% TARIFF TO BE IMPLEMENTED BY TRUMP IN THE NEXT FEW DAYS//ISRAEL VS HAMAS UPDATES/TBN ISRAEL WITH THEIR DAILY REPORT//COVID UPDATES/VACCINE INJURY REPORTS//NEWSWIZE, NEWS ADDICTS/EVOL NEWS/DR PAUL ALEXANDER/USA DATA RELEASES ON PMI, S AND P AND ISM/ AND THEY ARE CONFUSING//HOST OF SWAMP STORIES FOR YOU TONIGHT//

190 H BMO CAPITAL MARKETS 5 323 C HSBC 3 363 H WELLS FARGO SECURITI 92 523 H INTERACTIVE BROKERS 2 657 C MORGAN STANLEY 4 657 H MORGAN STANLEY 50 661 C JP MORGAN SECURITIES 5 686 C STONEX FINANCIAL INC 35 690 C ABN AMRO CLR USA LLC 2 726 C PLUS500US FINANCIAL 25 737 C ADVANTAGE FUTURES 1 905 C ADM 2

TOTAL: 113 113 MONTH TO DATE: 20,239

JPMORGAN stopped 5/113

AUGUST

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 113 CONTRACTs NOTICES FOR 11,300 OZ or 0.3514 TONNES

total notices so far: 20,239 contracts for 2,023,900 OR 62.952 tonnes)

FOR AUGUST

XXXXXXXXXXXXXXXXXX

SILVER NOTICES:405 NOTICE(S) FILED FOR 2.025 million OZ/

total number of notices filed so far this month : 1469 CONTRACTS (NOTICES) for 7.345 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $8.45 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD FROM THE GLD/./

INVENTORY RESTS AT 954.80 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $1.51 AT THE SLV: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: //A HUGE WITHDRAWAL OF 1.119 MILLION OUT OF THE SLV/

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 482.964 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 841 CONTRACTS TO 160,958 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.50 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE FINALLY ARE MOVING MUCH HIGHER THAN THE BASE $34.40 SILVER PRICE BARRIER. WE HAD A HUGE SIZED GAIN OF 941 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL 100 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO MONDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $36.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON MONDAY WITH SILVER’S GAIN IN PRICE. THE PRICE HOWEVER FINISHED MILES ABOVE THE MAGIC NUMBER OF $36.00 SILVER SPOT PRICE CLOSING AT $37.34 . WE HAVE A MEGA HUGE T.A.S. ISSUANCE AT 1036 CONTRACTS ISSUED BY THE CME AND THAT STILL SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING ABOVE THE 38.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A SMALL 100 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 1036 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY’S// TRADING OR BEYOND/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 941 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.50.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A MEGA HUGE SIZED 1036 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.50) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY FEW NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE GAIN OF 941 CONTRACTS ON OUR TWO EXCHANGES WE HAD ZERO T.A.S. SPREADER LIQUIDATION

WE HAD A 100 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.70 MILLION OZ FOLLOWED BY TODAY’S HUGE 465 CONTRACT QUEUE JUMP OR AN ADDITIONAL 2.275 MILLION OZ WILL STAND FOR PHYSICAL ON THIS SIDE OF THE POND //NEW STANDING ADVANCES TO 7.650 MILLION OZ.

THUS:

INITIAL STANDING FOR AUGUST: 4.70 MILLION OZ FOLLOWED BY TODAY’S 2.275 MILLION OZ QUEUE JUMP//NEW STANDING; 7.650 MILLION OZ

WE HAD:

/ HUGE COMEX OI GAIN+// A SMALL SIZED EFP ISSUANCE 100 CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 1036 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A SMALL 39 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 3 DAY(S), total 1725 contracts: OR 8.625 MILLION OZ (575 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 8.625 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 8.625 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 841 CONTRACTS WITH OUR GAIN IN PRICE OF $0.50 IN SILVER PRICING AT THE COMEX// FRIDAY.,. . THE CME NOTIFIED US THAT WE HAD A SMALL 100 CONTRACT EFP ISSUANCE CONTRACTS: 100 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 5 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 2.275 MILLION OZ QUEUE JUMP//NEW STANDING ADVANCES TO 7.65 MILLION OZ

THE NEW TAS ISSUANCE MONDAY NIGHT (1036) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE IN TUESDAY THROUGH THURSDAY TRADING.

WE HAD 405 NOTICE(S) FILED TODAY FOR 2.025 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 6,905 OI CONTRACTS TO 444,682 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 1501 CONTRACTS //.

WE HAD A STRONG INCREASE IN COMEX OI (6905 CONTRACTS) . THIS OCCURRED WITH OUR GAIN OF $24.65 IN PRICE// MONDAY///.

LAST FOUR MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

AUGUST: 60.547 TONNES OF GOLD FOLLOWED BY TODAY’S SMALL QUEUE JUMP OF 0.1493 TONNES //NEW STANDING ADVANCES TO 64.221 TONNES OF GOLD/.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3665 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 444,682 /STILL EXTREMELY LOW AND WE NOW WITNESS A LOW COMEX OI WITH AN EXTREMELY HIGH PRICE OF GOLD

SILVER ALSO HAS A LOW COMEX OI OF 160,958 CONTRACTS BUT GAINING RAPIDLY!!

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,570 CONTRACTS WITH 6905 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 3665 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 10,570 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 940 CONTRACTS AND THESE ISSUANCES ARE USED TO INITIATE A RAID WHEN CALLED UPON. GOLD PRICE ON MONDAY ROSE BY $24.65

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(3665) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 6905 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 12,307 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR AUGUST AT 60.547 TONNES FOLLOWED BY TODAY’S 0.3919 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 64.6158 TONNES

NEW STANDING FOR GOLD, AUGUST CONTRACT AT 64.6158 TONNES OF GOLD

.

/ 3) ZERO T.A.S. LIQUIDATION AND MONTH END SPREADER LIQUIDATION DISAPPEARED FROM THE SCENE AS WE HAD 1)A $24.65 COMEX PRICE GAIN. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG GAIN OF 10,570 CONTRACTS ON OUR TWO EXCHANGES WE HAD BASICALLY ZERO LIQUIDATION OF OUR TAS SPREADERS/ /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND YOU CAN VISUALIZE THIS BY THE HUGE AMOUNTS OF QUEUE JUMPING WE HAVE BEEN HAVING LATELY

4) STRONG SIZED COMEX OI GAIN// 5) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (2510 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 940 T.A.S.CONTRACTS/

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

TOTAL EFP CONTRACTS ISSUED: 8065 CONTRACTS OR 806,500 OZ OR 25.085 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 2688 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN3 TRADING DAY(S) IN TONNES 25.085 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 25.085 TONNES DIVIDED BY 3550 x 100% TONNES = 0.0706% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

UNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 25.085 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 841 CONTRACTS OI TO 160,997 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 100 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 880 CONTRACTS AND ADD TO THE 100 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 941 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.50 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.705 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

SHANGHAI CLOSED UP 34.29 PTS OR 0.96%

//Hang Seng CLOSED UP 123.72 PTS OR 0.50%

// Nikkei CLOSED DOWN 258.84 PTS OR 0.64% //Australia’s all ordinaries CLOSED UP 1.20%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1881 OFFSHORE CLOSED DOWN AT 7.1945/ Oil DOWN TO 65.96 dollars per barrel for WTI and BRENT DOWN TO 68.60 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1881 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1945 AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 6905 CONTRACTS TO 444,682 OI WITH OUR CONSIDERABLE GAIN IN PRICE OF $24.85 WITH RESPECT TO MONDAY’S // TRADING.. WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3665 ). WE HAD NO T.A.S. LIQUIDATION //MONDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 12,071 CONTRACTS WITH MONTH END SPREADERS DISAPPEARING FROM THE SCENE ON AUGUST 1.

LAST WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. OR IT COULD BE THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY!!.THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY IS NOW 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

EARLY THIS TUESDAY MORNING THE CME ANNOUNCED A ZERO EXCHANGE FOR RISK ISSUANCE!

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 0 SO FAR

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS GENERALLY THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE OR FRBNY FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 6TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH JULY WITH A TWO MONTH HIATUS)

DETAILS ON JULY COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 10,570 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 940 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED YESTERDAY WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS TODAY’S QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS TODAY’S STRONG QUEUE JUMP OF 0.3919 TONNES//NEW STANDING 64.6158 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 234 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NONE COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY A STRONG QUEUE JUMP OF 0.3919 TONNES/NEW STANDING ADVANCES TO 64.6158 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3665 EFP CONTRACT WAS ISSUED: : /AUGUST 3665 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3665 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY

MONTH END SPREADERS WILL APPEAR ON THE LAST WEEK OF AUGUST.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY WAS A SMALL SIZED SIZED 940 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS PAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S CONSIDERABLE GAIN IN PRICE IN GOLD AND SILVER AND A CORRESPONDING GAIN OF STRONG COMEX OI. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH THE RARE TWO ISSUANCES OF EXCHANGE FOR RISK! THE RAIDS THROUGHOUT LAST WEEK’S OPTION EXPIRY WEEK WERE USED TO LOWER THE HUGE DERIVATIVE LOSSES ENDURED BY THE BANKERS.

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S STRONG QUEUE JUMP OF 0.3919 TONNES//NEW STANDING ADVANCES TO 64.6158 TONNES.

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $24.65/ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION (AND MONTH END SPREADERS DISAPPEARED FROM THE SCENE) ///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID ON FRIDAY.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /JULY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

ANALYSIS JULY DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE GAINED A STRONG SIZED TOTAL OF 32.88 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD TUESDAY’S STRONG QUEUE JUMP OF 0.3919 TONNES OF GOLD//NEW STANDING ADVANCES TO 64.6158 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $26.45

WE HAD A HUGE 1501 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 10,570 CONTRACTS OR 1,057,000 0Z (32.88 TONNES)

1 entry i) Into Asahi dealer: 4822.65 oz (150 kilobars)

total deposit 4822.65 oz

.150 tonnes

Deposits to the Customer Inventory, in oz

DEPOSITS/CUSTOMER

1 ENTRY i) into Loomis: 2300.290 oz

total deposit customer Loomis 2300.29 oz

07 tonnes

total deposit in tonnage: 0.22 tonnes

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

113 notice(s) 11,300 OZ 0.3514 TONNES

No of oz to be served (notices)

535 contracts 535500 OZ 1.664 TONNES

Total monthly oz gold served (contracts) so far this month

20,239 notices 2,023,900 oz 62.952 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits:

1 ENTRIES

1 entry: i) Into the dealer Asahi: 4822.65 oz (150 kilobars)

total deposit 4822.65 oz

(0.15 tonnes)

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRY i) into Loomis: 2300.290 oz

total deposit customer Loomis 2300.29 oz

.07 tonnes

total deposit in tonnage: 0.22 tonnes

total weight customer and dealer: 4.49 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0

adjustments: 1

Brinks: customer to dealer; 4822.65 oz (150 kilobars)

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 648 CONTRACTS FOR A LOSS OF 2,499 CONTRACTS

WE HAD 2625 CONTRACTS SERVED ON MONDAY SO WE GAINED A GOOD SIZED 126 CONTRACTS OR A 12,600 OZ OF GOLD (0.3919 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND. THIS REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

SEPT GAINED 984 CONTRACTS TO 6067

OCTOBER GAINED 1582 CONTRACTS UP TO 70,933

We had 113 contracts filed for today representing 11,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and O notices issued from their client or customer account. The total of all issuance by all participants equate to 113 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (20,239 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 648 CONTRACTS) minus the number of notices served upon today (113 x 100 oz per contract) equals 2,077,400 OZ OR 64.6158TONNES

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (20,239 x 100 oz +we add the difference for front month of AUGUST (648 OI} minus the number of notices served upon today (113 x 100 oz) which equals 2,077,400 OZ OR 64.6158 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 64.6158 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL REGISTERED SILVER: 190.743 MILLION OZ//.TOTAL REG + ELIGIBLE. 506.311 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 461 OPEN INTEREST CONTRACTS FOR A GAIN OF 360 CONTRACTS. WE HAD 95 CONTRACTS SERVED ON MONDAY SO WE GAINED 455 CONTRACTS OR AN ADDITIONAL 2.275 MILLION OZ WILL STAND AS THEY ENTERTAINED A HUGE QUEUE JUMP

SEPTEMBER LOST 1158 CONTRACTS DOWN TO 108,526 CONTRACTS.

OCTOBER GAINED 76 CONTRACTS TO 450

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 405 or 2.025 MILLION oz

CONFIRMED volume; ON MONDAY 52,999 fair//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1469 X5,000 oz = 7.345 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (461) AND the number of notices served upon today (405 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1469) Notices served so far) x 5000 oz + OI for the front month of AUGUST(461) minus number of notices served upon today (113)x 5000 oz equals silver standing for the AUGUST contract month equating to 7.65 MILLION OZ .

New total standing: 7.650 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.743 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/506.311 million. 41.65%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 954.80 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 482.964 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

3. CHRIS POWELL AND GATA GOLD DISPATCHES

Gold and Trump’s chaos were key to the TSX’s stellar performance this year

Submitted by admin on Mon, 2025-08-04 21:12 Section: Daily Dispatches

By Tim Kiladze The Globe and Mail, Toronto Monday, August 4, 2025

Canada’s benchmark stock index is outperforming both the S&P 500 and the tech-heavy Nasdaq Composite Index in 2025, and there is a single sector doing the heavy lifting: gold.

Despite the continuing tariff drama with the United States that disproportionately hurts Canada’s economy relative to the U.S., the S&P/TSX Composite Index is up 11.1% since the start of the year, including dividends, while the S&P 500 has climbed 6.9% and the Nasdaq has risen 7.3%.

Multiple sectors have performed well on the TSX this year, but gold producers in particular are dominating, comprising 15 of the 20 best share price returns. These companies are led by Lundin Gold Inc., which has put up a 120% return, including dividends.

Gold companies also make up four of the top-five TSX performers, including Dundee Precious Metals Inc., SSR Mining Inc., and Kinross Gold Corp. They all have total returns of at least 65% since the start of the year.

The only non-gold company in the group is Celestica Inc., a Canadian technology company that came back from the dead to strike it rich off the artificial-intelligence boom. …

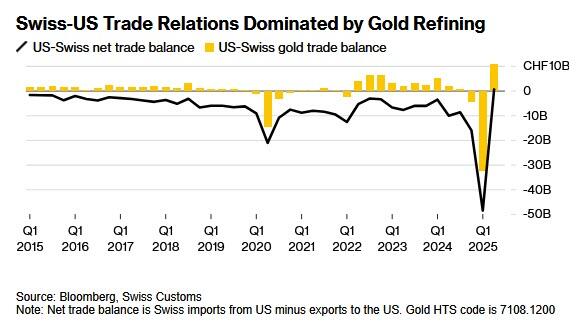

Swiss gold trading takes spotlight in trade talks with Trump

Submitted by admin on Mon, 2025-08-04 09:11 Section: Daily Dispatches

By Jan-Henrik Foerster and Jack Ryan Bloomberg News Monday, August 4, 2025

The trade imbalances that prompted President Donald Trump to slap hefty levies on Swiss imports have been driven by a small industry at the center of the world’s gold market.

The country is the world’s biggest gold-refining hub, thanks to a longstanding reputation for quality and discretion. Billions of dollars worth of gold is constantly flowing into and out of the nation, from mines in South America and Africa to banks in London and New York.

Flows of the precious metal cause big swings in the country’s trade balances, even if the Swiss refiners capture only a small portion of the value of the commerce.

Bullion is by far the country’s largest export good, according to Simon J. Evenett of IMD Business School. “Gold is special,” Evenett said. “It isn’t really manufactured in Switzerland. ‘Processed’ is a better word.”

The impact of the industry is more important than ever as the Trump administration focuses on leveling trade deficits. Record bullion exports of more than $36 billion made up more than two-thirds of Switzerland’s trade surplus with the U.S. in the first quarter, according to Swiss customs data. …

UK investors buy gold coins in record numbers to avoid capital gains tax

Submitted by admin on Fri, 2025-08-01 12:51 Section: Daily Dispatches

By Emma Agyemang and Emma Dunkley Financial Times, London Friday, August 1, 2025

UK investors have been buying gold coins in record numbers this year to mitigate against rises in capital gains tax and to cash in on the surging price of the precious metal.

Online bullion transactions hit record levels in the first quarter of the 2025-26 financial year, the Royal Mint said last week. Bullion coin sales were up 115% compared with the same period last year.

The World Gold Council painted a similar picture on Thursday, reporting that UK bar and coin demand was up 17% year-on-year.

Solomon Global, a UK company that sells gold bars and coins, also said this week that inquiries about its products had risen by 72% in the first half of the year, compared with the second half of 2024.

In a survey of 14,000 of its customers, tax was listed as the top motivator for buying gold coins — with 42% saying it was for tax reasons. The second top motivator, given by 26% of respondents, was “wealth protection.”

Bullion coins, including all gold, silver, and platinum coins, from The Royal Mint are exempt from capital gains tax for UK residents due to their status as legal tender.

However, capital gains tax applies to all gold, silver, and platinum coins that are not produced by The Royal Mint. Gold and silver bullion bars are also subject to capital gains tax as they are not considered legal tender. …

JOHANNESBURG—Thousands of Chinese citizens remain in Ghana to mine gold illegally, despite a crackdown by authorities in Africa’s largest producer of the precious metal, according to law enforcement agencies in the capital, Accra.

They say the illegal miners appear to be taking advantage of the record-high gold price, which hit $3,500 in April, with much of the illicit metal being smuggled back to China.

Organized crime groups, sometimes headed by what appear to be Chinese businesspeople, are flooding Ghana with sophisticated machinery to mine gold at scales never seen before in some areas, resulting in widespread environmental damage and fueling unemployment, according to one expert who recently spoke to The Epoch Times.

According to several analysts, Chinese involvement in illegal mining in Ghana and across Africa reveals Beijing’s real motive for its increasingly strong presence on the continent: to exploit Africa’s natural resources.

With Ghana’s police now often arresting Chinese citizens accused of stealing gold, relations between President John Mahama’s administration and Beijing are strained.

Ghanaian officials have said the Chinese regime isn’t doing enough to prevent its nationals from committing crimes in one of West Africa’s strongest economies.

But China’s ambassador in Ghana is accusing locals of “galamsey,” as it’s known in the region, or small-scale illegal gold mining, and of drawing Chinese workers to Africa.

“The Chinese who are getting arrested are migrant workers who have come here to make a living,” Chinese Ambassador Tong Defa told The Epoch Times.

Grace Ansah-Akrofi, director of the Ghana Police Service’s Public Affairs, has a different view.

“While there are cases like those mentioned by the ambassador, it’s a bit far-fetched to say that it’s Ghanaian masterminds who are importing Chinese to commit crimes,” she told The Epoch Times. “We have our own people who are desperate enough to commit crimes.

“Our criminals are not going to call on [the] Chinese to do their work. It doesn’t make sense.”

Enoch Aikins, a researcher at South Africa’s Institute for Security Studies, traces the roots of Ghana’s galamsey crisis to a period between 2008 and 2013, when he said more than 50,000 Chinese entered the country to mine gold illegally.

“Ever since then, there has been a strong Chinese element in these kinds of crimes in Ghana; they originally came here because they knew the laws were lax, and they also bribed their way out of trouble,” Aikins told The Epoch Times.

“But now that things are tightening up and they find they are being pushed out of an industry that makes them rich, they are angry.”

In 2023, the government-mandated Inter-Ministerial Committee on Illegal Mining released a report that implicated several government officials in illegal mining.

The Mahama administration says its Office of the Special Prosecutor is investigating information in the report.

Ghana is Africa’s biggest gold producer, and the sixth-largest in the world, reporting an output of 151 metric tons in 2024, according to information from the Ghana Gold Board obtained by The Epoch Times.

About a third of its production comes from artisanal mining, some of it illegal, said Aikins.

Demand for gold, seen as a stable investment in times of economic uncertainty, has recently reached unprecedented highs, and costs almost $3,300 per ounce as of Aug. 1.

On the back of this, Chinese companies are investing billions of dollars in Ghana’s gold sector, said government spokesperson Felix Ofosu.

“We are grateful for the Chinese contribution to our economy, but surely this doesn’t mean we ignore abuses committed by Chinese citizens,” he told The Epoch Times.

In June, the Geneva-based Global Initiative Against Transnational Organized Crime (GI-TOC) released a report detailing how foreign nationals, particularly from China and Burkina Faso, have introduced new technologies and machinery to Ghana that are increasing gold output while contributing to environmental harm.

The GI-TOC investigation said foreigners, including Chinese, are working in concert with traditional chiefs and political elites to “benefit from or enable illicit mining operations.”

“Criminal groups are allegedly engaging in gold smuggling and money laundering through casinos and other businesses,” said the independent policy research institute.

Ofosu said court cases and investigations have revealed that “Chinese criminals are the ones who finance locals and give them technical support” to facilitate illegal mining.

He pointed to the case of En “Aisha” Huang, known in Ghana as the “Galamsey Queen.”

Deported several times between 2018 and 2022, Huang kept returning “because she couldn’t resist the lure” of Ghana’s gold, said Ansah-Akrofi.

In December 2023, Huang was sentenced to 4.5 years in prison and ordered to pay a $4,000 fine for running an illegal gold mining syndicate.

James Boafo, an expert in the environmental effects of illegal mining at Ghana’s University of Cape Coast, told The Epoch Times that “China’s hand is far from hidden” in the “destruction” happening in his country.

“Machinery brought into Ghana from China is causing a lot of damage,” he said. “Ghana’s traditional small-scale miners use very basic tools to extract gold, so they can reach only shallow depths.

“But these days, illegal miners are able to go very deep in the earth, thanks to excavators and bulldozers supplied by Chinese partners.

“In Ghana, now we have many polluted rivers because of this. Our water quality is seriously degraded, and drinking it is a problem.”

He added that criminal operations use rivers to sift gold dust and nuggets from the sediment.

“This activity causes entire river systems, across many thousands of kilometres, to be muddy,” Boafo said. “Then the operators use toxic substances like lead and mercury to take the gold from the water. Whether they are Chinese or Africans, they just don’t care.”

He said illegal mining operations fronted by the Chinese are also threatening Ghana’s cocoa industry.

“They destroy lands and forests and plantations,” Boafo said.

Well-resourced Chinese citizens are outcompeting local artisanal miners, who are consequently falling into unemployment and poverty, he noted.

Professor Gladys Ansah, who has investigated illegal mining for the University of Ghana, said Mahama’s government “should not let up” in its arrests and prosecutions of illegal miners, no matter their nationalities.

“Over the years, we’ve had a lot of committees and programs focused on getting rid of this,” she told The Epoch Times. “But they weren’t so effective, partly because our government didn’t want to offend China; so the Chinese were treated with kid gloves.”

As far back as 2013, Ansah said, a joint task force of military and police arrested 4,500 Chinese miners.

“They weren’t prosecuted; they were deported, and we paid for it because a lot of them came back and many are still here,” she said.

South African foreign policy analyst, Sanusha Naidu, told The Epoch Times that Chinese links to illegal harvesting of metals and minerals are “cementing” a growing perception in the continent that Beijing’s “real motive for being in Africa in such a big way is to exploit natural resources, by whatever means possible.”

END

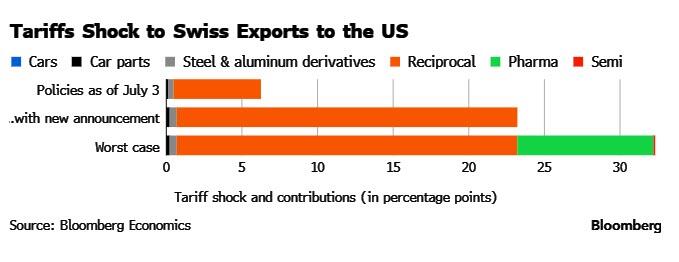

GOLD/SWITZERLAND

GOLD is included in the tariffs as well as Platinum. This will create chaos!!

Swiss President Rushes To Washington In Last Ditch Attempt To Appease Trump And Lower 39% Tariff

Tuesday, Aug 05, 2025 – 12:40 PM

Swiss President Karin Keller-Sutter (yes, president Karin) and her economy minister Guy Parmelin scrambled to fly to Washington on Tuesday in a last-minute bid for a deal to lower the 39% tariff imposed last week by Donald Trump.

The trip is to “facilitate meetings with the US authorities at short notice and hold talks,” the government said in a statement. Keller-Sutter’s office declined to say whether she expects to meet the American president and what trade concessions she might bring before Thursday’s deadline to implement the levy.

The scramble follows a day after the Swiss government said it is determined to win over the US on trade after last week’s shock announcement of 39% tariffs on exports to America.

“Switzerland enters this new phase ready to present a more attractive offer, taking US concerns into account and seeking to ease the current tariff situation,” it said in a statement on Monday, highlighting its foreign direct investments and research and development push in the US. It also excluded countermeasures for the time being.

With the new levies – the highest among industrial nations – scheduled to go into effect on Thursday, President and Finance Minister Karin Keller-Sutter convened an emergency meeting of the governing Federal Council to discuss how to proceed. Negotiators with the Swiss State Secretariat for Economic Affairs have already reached out to their US counterparts to try and find a way forward. Bern is focusing on getting at least a longer timeline than Thursday, according to an official close to the talks, adding that anything improving the current situation would be a win.

Trump’s tariff decision last week stunned the Swiss after talks ahead of the Aug. 1 deadline were said to look “promising.” A Thursday night call instead focused on Switzerland’s trade surplus in goods with the US. The Swiss government stressed on Monday that the overhang “is not the result of any ‘unfair trade practices’.”

Switzerland’s outsized gold exports are partly to blame for the distorted trade balance. The country is the world’s biggest refining hub for the precious metal, with billions of dollars worth of gold constantly flowing into and out of the nation. Pharmaceuticals, coffee and watches are the other main drivers.

According to Bloomberg Economics, if the 39% tariff rate came into effect across the board – especially on pharmaceuticals – that would put up to 1% of Switzerland’s economic output at risk over the medium term.

The paradox faced by Keller-Sutter and her Economy Minister, Guy Parmelin, is that any concessions may be politically costly without meaningfully curbing the trade deficit with the US that Trump has criticized.

“Switzerland has to get creative,” said Stefan Legge, a trade policy researcher at St Gallen University. He did not point out why it has to get creative, because if one listened to all the “expert” economists, the US had no leverage at all in tariff negotiations. Perhaps that wasn’t quite the case…

In any case, Keller-Sutter’s shuttle diplomacy follows an emergency government meeting on Monday where ministers agreed to present a new offer to the US. Gold, agriculture, planes, drugs, and energy are just some areas that may feature in any talks.

Here’s an overview of some concessions the Swiss could make according to Bloomberg:

Agricultural Tariffs

Switzerland abolished industrial tariffs in 2023, leaving levies on only 5% of its imports. The only area where the Swiss maintain tariffs is agriculture, motivated by a politically charged belief in self-reliance. Any concessions would surely infuriate farmers, who have previously pledged to “vehemently fight” any changes to the current regime. While the political pain would be large, the win for Trump would be rather symbolic since agriculture amounts to a small fraction of the economy.

Gold

Trump’s aides claim that Switzerland’s out-sized trade deficit with the US is why the president imposed such high levies. On average, two thirds of last year’s $38 billion deficit was due to shipments of bullion. That’s because of the price of the metal itself rather than any added value by Swiss refineries, which largely focus on resizing bars. “Gold is special,” said Simon J. Evenett of IMD Business School in Lausanne. “It isn’t really manufactured in Switzerland. Processed is a better word.”

One fix could be a high tariff, say of 50%, just on gold, hitting refineries but with a limited wider economic fallout. Alternatively, handing over buillon trade to the central bank or another state institution could provide a justification for taking it out of statistics on both sides of the Atlantic. But it’s not clear if this would appease Trump.

Planes

Switzerland is currently buying 36 F-35 fighter jets from Lockheed Martin Corp. for its air force, but has run into disagreements over the price. According to the Swiss, a fixed price of 6 billion francs ($7.4 billion) was contractually agreed, which voters backed in a plebiscite, but the US now wants as much as $1.3 billion more to account for higher production costs and inflation.

Accepting the higher charge, and possibly symbolically ordering one or two more planes, could help convince Trump, given how arms purchases featured in his other trade deals. But voters might balk at that.

Drugs, Investments and Energy

One of Trump’s major peeves is pharmaceuticals, where Switzerland specializes. Novartis AG and Roche Holding AG have already announced plans to invest huge sums in the US over the next few years, and the Swiss government could pressure them to cut prices there too. While that might align with the interests of the companies themselves to to get out of Trump’s crosshairs, officials can’t actually force them to do so. An easier approach could be to gather pledges for US investments by Swiss companies. Such a package could be combined with a pledge to buy US energy, in particular liquefied natural gas. While the landlocked country is focused on hydroelectric and nuclear power, it does use a small amount of gas, primarily in the winter.

“We could buy oil, arms and LNG and we could give concessions on agriculture and at least give our best endeavor to put pressure on Swiss pharmaceutical companies to lower prices,” said Thomas Borer, a former Swiss diplomat.

Something Else

Switzerland’s rude awakening in its diplomacy with Washington has forced officials to realize that winning over Trump himself is key, rather than talking to underlings. So perhaps a gesture such as a present to charm the president could do the trick, said St Gallen’s Legge. He cited the example of the birth certificate of Trump’s German grandfather that Chancellor Friedrich Merz brought him in June. “Maybe it would be best to give him a golden Swiss watch,” Legge said.

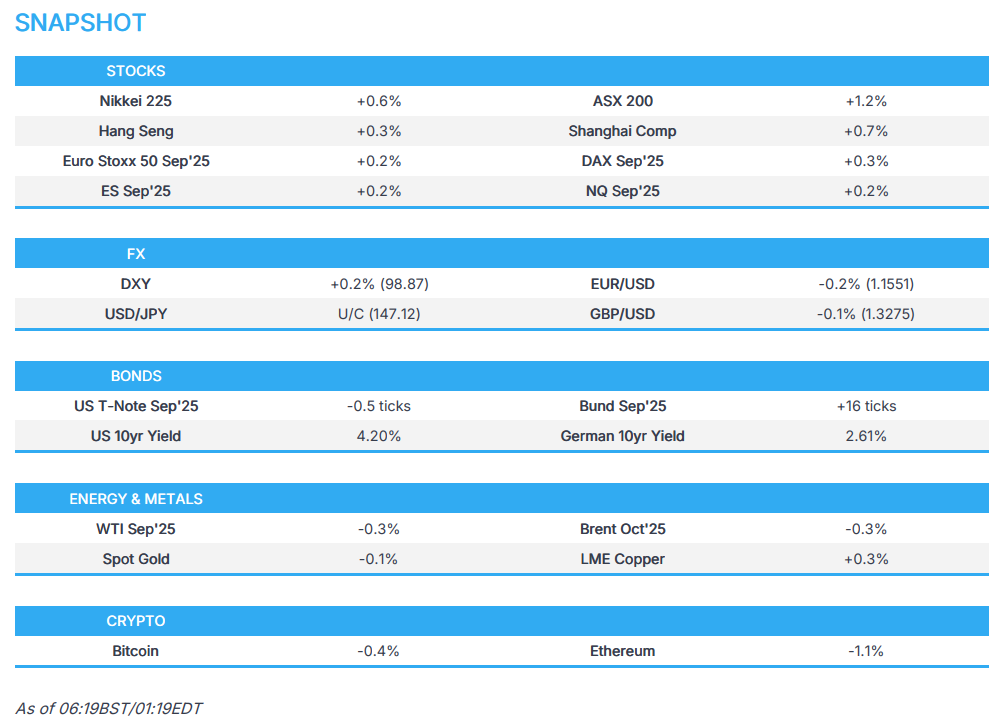

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 34.29 PTS OR 0.96%

//Hang Seng CLOSED UP 123.72 PTS OR 0.50%

// Nikkei CLOSED DOWN 258.84 PTS OR 0.64% //Australia’s all ordinaries CLOSED UP 1.20%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1881 OFFSHORE CLOSED DOWN AT 7.1945/ Oil DOWN TO 65.96 dollars per barrel for WTI and BRENT DOWN TO 68.60 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1881 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1945 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1881 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1945

HANG SENG CLOSED UP 123.72 PTS OR 0.50%

2. Nikkei closed UP 258.84 PTS OR 0.64%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 98.80/ EURO FALLS TO 1.1543 DOWN 41 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.473//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.46…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6292/Italian 10 Yr bond yield DOWN to 3.458 SPAIN 10 YR BOND YIELD DOWN TO 3.205%

3i Greek 10 year bond yield DOWN TO 3.307

3j Gold at $3273.00 Silver at: 37.50 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 14 /100 roubles/dollar; ROUBLE AT 79.96

3m oil (WTI) into the 65 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.46// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.471% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8099 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9347 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.215 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.805 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.704 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.69

10 YR UK BOND YIELD: 4.5370 UP 2 PTS

10 YR CANADA BOND YIELD: 3.385 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.942 DOWN 0 PTS

2a New York OPENING REPORT

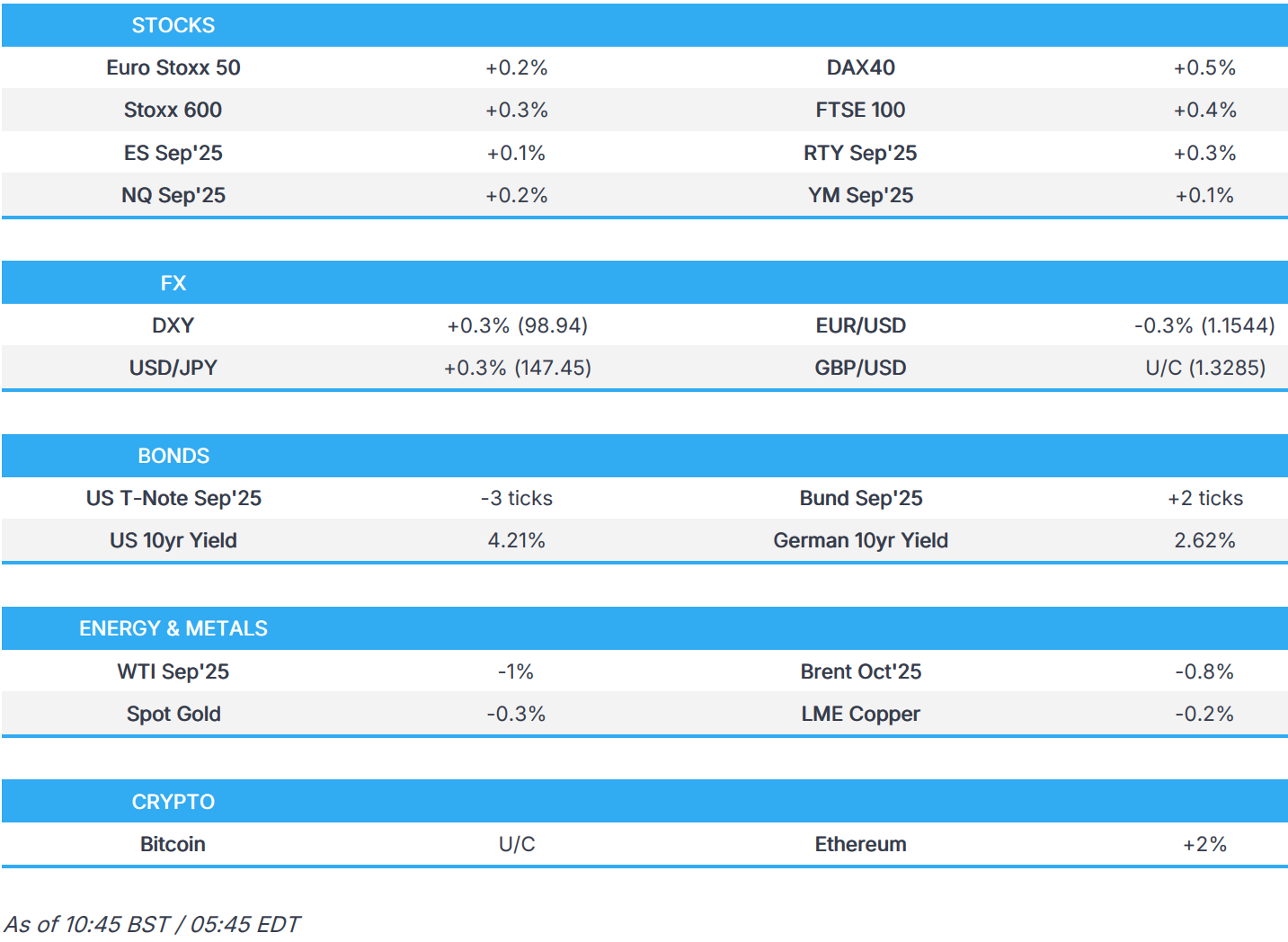

Futures Rise Again Because Why Not

Tuesday, Aug 05, 2025 – 08:26 AM