LEASE RATES:

platinum ..OFF THE CHART//29.5%

gold: 6.0%

silver lease rate today//6.5%

099 H DEUTSCHE BANK AG 642

323 C HSBC 190

363 H WELLS FARGO SECURITI 248

661 C JP MORGAN SECURITIES 30 621

686 C STONEX FINANCIAL INC 4

690 C ABN AMRO CLR USA LLC 1 10

726 C PLUS500US FINANCIAL 1

737 C ADVANTAGE FUTURES 1

845 C GOLDMAN SACHS CLEARI 2

905 C ADM 22 7

991 H CME 115

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 947 CONTRACTs NOTICES FOR 94,700 OZ or 2.945 TONNES

total notices so far: 21,785 contracts for 2,178,500 OR 67.760 tonnes)

SILVER NOTICES:0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 1471 CONTRACTS (NOTICES) for 7.355 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 16.775 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 25,000 OZ QUEUE JUMP//NEW STANDING REMAINS AT 7.6750 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 2.587 TONNES + 5.4432 TONNES EX FOR RISK/AUG 7 //NEW STANDING ADVANCES TO 68.842 TONNES OF GOLD + 5.4432 TONNES EX FOR RISK = 74.2852 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 45.56 TONNES QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 789 CONTRACTS OI TO 160,473 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1500 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1500 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1500 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 789 CONTRACTS AND ADD TO THE 1500 E.FP. ISSUED

WE OBTAIN A GOOD SIZED GAIN OF 711 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.02 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 3.555 MILLION PAPER OZ

OCCURRED WITH OUR TINY $0.02 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

SHANGHAI CLOSED UP 5.67 PTS OR 0.16%

//Hang Seng CLOSED UP 157.08 PTS OR 0.63%

// Nikkei CLOSED UP 264.29 PTS OR 0.65% //Australia’s all ordinaries CLOSED DOWN 0.14%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1771 OFFSHORE CLOSED UP AT 7.1796/ Oil DOWN TO 64.91 dollars per barrel for WTI and BRENT DOWN TO 67.33 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1771 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1796 AGAINST US DOLLAR/ AND THUS STRONGER

ASIAN MARKETS THIS WEDNESDAY MORNING:

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1160 CONTRACTS TO 450,807 OI DESPITE OUR LOSS IN PRICE OF $8.15 WITH RESPECT TO WEDNESDAY’S // TRADING.. WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4680 ). WE HAD NO T.A.S. LIQUIDATION //WEDNESDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 6718 CONTRACTS

LAST WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. OR IT COULD BE THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY!!.THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY IS NOW 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

EARLY THIS THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE OF 1750 CONTRACTS FOR 175000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. I WILL PUT MY MONEY THAT THE RECIPIENT OF THIS IS OUR OWN FRBNY.

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 1 FOR A MONSTER 1750 CONTRACTS OR 175000 OZ ( 5.443 TONNES)

AS I EXPLAINED ABOVE,:THE RECPIENT OF EXCHANGE FOR RISK CAN BE EITHER:

- THE BANK OF ENGLAND

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 5840 CONTRACTS DESPITE OUR SMALL GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 915 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED LAST WEEK WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS A QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS TODAY’S STRONG QUEUE JUMP OF 1.629 TONNES//NEW STANDING 66.255 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 234 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NONE COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 2.587 TONNES PLUS AUGUST 7TH A HUGE 5.443 TONNES EX FOR RISK/NEW STANDING ADVANCES TO 74.2852 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4680 EFP CONTRACT WAS ISSUED: : /AUGUST 4680 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4680 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//WEDNESDAY

- MONTH END SPREADERS WILL APPEAR ON THE LAST WEEK OF AUGUST.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHTTHURSDAY MORNING WAS A SMALL SIZED SIZED 915 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S LOSS IN PRICE IN GOLD BUT A CORRESPONDING GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK LATE IN JULY AND THIS WAS FOLLOWED WITH AUGUST’S FIRST ISSUANCE OF EXCHANGE FOR RISK FOR 1,750 CONTRACTS OR 175000 OZ (5.4452 TONNES)

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S STRONG QUEUE JUMP OF 2.587 TONNES TO WHICH WE ADD TODAY’S HUGE 5.4432 EXCHANGE FOR RISK//NEW STANDING ADVANCES AS FOLLOWS:

68.842 TONNES NORMAL DELIVERIES +

5.4432 TONNES EXCHANGE FOR RISK

EQUALS

74.2852 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A $8.15/ /) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD LITTLE IF ANY T.A.S. SPREADER LIQUIDATION (AND MONTH END SPREADERS DISAPPEARED FROM THE SCENE) ///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID THIS WEEK.

THURSDAY MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /AUGUST TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: ONE SO FAR, AUGUST 7 AT 1750 CONTRACTS FOR 175000 OZ (5.443 TONNES OF GOLD)

THUS 68.842 TONNES OF GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 5.443 TONNES EXCHANGE FOR RISK = 74.2852 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE GAINED A STRONG SIZED TOTAL OF 20.89 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD WEDNESDAY’S HUGE QUEUE JUMP OF 2.587 TONNES OF GOLD AND THEN ADD TODAY’S 5.4432 TONNES OF EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 74.2852 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $8.15

WE HAD A HUGE 878 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 5840 CONTRACTS OR 584000 0Z (18.164 TONNES)

confirmed volume WEDNESDAY 175,872 contracts// poor

speculators have left the gold arena

END

INITIAL GOLD COMEX

AUGUST 7 CONTRACT MONTH

AUGUST 1/2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entry Out of JPMorgan 10,995.842 oz 342 kilobars total withdrawal 10,995.842 oz (0.342 tonnes) . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 947 notice(s) 94,700 OZ 2.945 TONNES |

| No of oz to be served (notices) | 348 contracts 34,800 OZ 1.082 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,785 notices 2,178,500 oz 67.760 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entry

Out of JPMorgan 10,995.842 oz

342 kilobars

total withdrawal 10,995.842 oz

(0.342 tonnes)

adjustments: 2

i) Loomis 385.812 oz dealer to customer//12 kilobars)

ii) Manfra 2893.590 oz dealer to customer (90 kilobars)

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 1295 CONTRACTS FOR A GAIN OF 233 CONTRACTS

WE HAD 599 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED A MONSTER SIZED 832 CONTRACTS OR A 83,200 OZ OF GOLD (2.587 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND. THIS REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD.

SEPT GAINED 145 CONTRACTS TO 6224

OCTOBER GAINED 2223 CONTRACTS UP TO 73,046

We had 947 contracts filed for today representing 94,700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 30 notices issued from their client or customer account. The total of all issuance by all participants equate to 947 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 621 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (21,785 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 1295 CONTRACTS) minus the number of notices served upon today (947 x 100 oz per contract) equals 2,213,300 OZ OR 68.842TONNES TO WHICH WE ADD OUR INITIAL ISSUANCE OF 5.443 TONNES OF EXCHANGE FOR RISK = 74.2852 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (21,785 x 100 oz +we add the difference for front month of AUGUST (1295 OI} minus the number of notices served upon today (943 x 100 oz) which equals 2,213,300 OZ OR 68.842 TONNES + 5.4432 TONNES EX FOR RISK = 74.2852 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 74.2852 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,018,562.121 oz 62.785 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,668,707.679 oz

TOTAL REGISTERED GOLD 21,294,614.127 or 662.351 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,374,093.552 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,276.714 oz ((REG GOLD- PLEDGED GOLD)= 599.58tonnes // ( a bid drop of 10 tonnes

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE AUGUST 2025 SILVER CONTRACT//INITIAL

AUGUST 7 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 ENTRIES i) Out of Asahi 832,602.800 oz ii) out of Delaware 984.600 oz total withdrawal 833,587.40 oz |

| Deposits to the Dealer Inventory | 0 |

| Deposits to the Customer Inventory | 2 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into Brinks 642,139.200 oz ii) Into Loomis: 329,293.49 oz total deposit 971,392.690 oz |

| No of oz served today (contracts) | 0 CONTRACT(S) (NIL OZ |

| No of oz to be served (notices) | 64 contracts (0.320 MILLION oz) |

| Total monthly oz silver served (contracts) | 1471 Contracts (7.355 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

0 deposit into dealer accounts

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into Brinks 642,139.200 oz

ii) Into Loomis: 329,293.49 oz

total deposit 971,392.690 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

2 ENTRIES

i) Out of Asahi 832,602.800 oz

ii) out of Delaware 984.600 oz

total withdrawal 833,587.40 oz

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 190.400 MILLION OZ//.TOTAL REG + ELIGIBLE. 506.121 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 64 OPEN INTEREST CONTRACTS FOR A GAIN OF 3 CONTRACTS. WE HAD 2 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 5 CONTRACTS OR AN ADDITIONAL 25,000 OZ WILL STAND AS THEY ENTERTAINED A HUGE QUEUE JUMP

SEPTEMBER LOST 2562 CONTRACTS DOWN TO 105,253 CONTRACTS.

OCTOBER GAINED 14 CONTRACTS TO 476

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or NIL oz

CONFIRMED volume; ON WEDNESDAY 48,133 poor//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1471 X5,000 oz = 7.355 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (64) AND the number of notices served upon today (0 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1471) Notices served so far) x 5000 oz + OI for the front month of AUGUST(64) minus number of notices served upon today (0)x 5000 oz equals silver standing for the AUGUST contract month equating to 7.6750 MILLION OZ .

New total standing: 7.6750 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.400 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/506.121 million. 41.50%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 952.79 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 485.870 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

3. CHRIS POWELL AND GATA GOLD DISPATCHES

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

3 CHRIS POWELL AND GATA DAILY DISPATCHES//other gold commentaries

New Fed study examines recent gold revaluations — elsewhere

Submitted by admin on Wed, 2025-08-06 17:02 Section: Daily Dispatches

5:04p ET Wednesday, August 6, 2025

Dear Friend of GATA and Gold:

Last week the Federal Reserve seemed to take note of the increasing speculation about the possibility of revaluing gold reserves to improve the financial position of governments and central banks and enable more money creation and debt reduction.

The notice took the form of a research study written by Fed economist Colin R. Weiss about gold revaluations undertaken by five countries in the last 28 years: Curacao/Saint Martin, Germany, Italy, Lebanon, and South Africa.

Weiss concludes that gold revaluation:

— Prevented the Banca d’Italia from having to report a loss in 2002.

— Provided funds that could have been used by Germany to avoid a fiscal deficit that would have impaired the country’s entry to the European Monetary Union, but in the end didn’t have to be used.

— Created money for Lebanon to use to rebuild after its civil war but did little to offset the country’s “larger structural challenges.”

— Offset some minor losses for the Curacao/Saint Martin central bank.

— Is too recent in South Africa to show that it has done much for that country.

Disappointingly, Weiss’ study does not cover the various gold revaluations undertaken throughout history by the United States —

— nor does it address how the United States might use gold revaluation to reduce its huge, growing, and increasingly worrisome debt, which is the main point of interest in recent discussions of gold revaluation. But the Fed may figure that simply acknowledging the gold revaluation issue is risky enough politically at the moment, what with the dollar showing signs of sustained weakness and with President Trump mocking Federal Reserve Chairman Jerome Powell practically every day and trying to hasten his replacement.

Weiss’ study is headlined “Official Reserve Revaluations: The International Experience” and it’s posted at the Fed’s internet site here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

KEVIN W TO US;

Ghana Gold Mines & Refineries

there sure are a lot of helicopter crashes involving defense ministers and heads of state. This one in Ghana where they were enroute to Ashanti region’s Obuasi.

Ghana: Two ministers among eight killed in helicopter crash

GHANA’s Defense Minister Edward Omane Boamah and Environment Minister Ibrahim Murtala Muhammed were among the eight people killed in a helicopter crash on Wednesday.

Everyone on the military Z9 helicopter was killed in the accident in Ghana’s central Ashanti region, a government spokesperson said.

The Ghanaian Armed Forces said the air force helicopter took off in the morning from the capital, Accra, and was heading northwest into the interior toward the gold-mining area of Obuasi in Ashanti when it went off the radar.

AngloGold Ashanti (Ghana) Ltd

Location: Obuasi

Website:www.anglogoldashanti.com

Brief: Obuasi, an underground operation mining to a depth of 1,500m, is located in Ghana’s Ashanti region, approximately 60km south of Kumasi.

- Mineral Reserve – 7.11m oz of gold

- Gold production – 224k oz

- All-in sustaining cost – $1,777/oz

- Capital expenditure – $214m

- Workforce – 5,376

https://www.ghanagoldmines.com/

END

ROBERT LAMBOURNE TO US

A i on gold movements to China: how China is using arbitrage on the Weest

Harvey,

Here is a description of the gold arbitrage trade in Shanghai. This came from a different Chinese source to DeepSeek.

Excuse my cynicism but the underlying reality simply seems like this a mechanism for China to acquire more gold currently located in the West. I don’t see anything which suggests that any of the 36 tonnes of gold eventually leaves China.

Does the arbitrage opportunity signal that western prices are being suppressed? Surely western prices would move up to reduce or eliminate the arbitrage in a free market.

Regards,

Bob

Large volumes of physical gold have been relocated to Shanghai in the last few weeks, and the move is explicitly an arbitrage trade.

1. What has actually moved?

• ≈ 36 tonnes of 1-kilogram gold bars have been delivered into Shanghai Futures Exchange (SHFE) warehouses in a single month, lifting exchange inventory to a record high .

• The bars are coming from outside mainland China—Hong Kong, Switzerland and London vaults are the usual sources cited in trade reports .

• Brinks, Malca-Amit and Loomis have been running multiple “high-security charters” (armoured trucks + cargo flights) into Shanghai’s bonded zone, according to logistics brokers.

2. What is the arbitrage opportunity?

A classic cash-and-carry arbitrage:

A. Price gap Shanghai gold futures (August contract) trade at a US$ 60–120 / oz premium to spot London or Comex prices after adjusting for FX and local VAT rules [^32^]. Premium ≈ 3–6 %.

B. Buy spot / sell futures Traders buy 400-oz London Good-Delivery bars, fly them to Shanghai, re-melt into 1-kg bars (SHFE specification) and deliver into SHFE to close short futures positions. Locked-in spread minus freight, insurance, refining and FX hedging ≈ US$ 30–45 / oz profit.

C. Freight & costs All-in logistics cost US$ 0.80–1.20 / oz; refining and assay US$ 0.25 / oz; FX hedge < 0.1 %. Net margin still US$ 25–40 / oz—high for a near-risk-free trade.

Because the Shanghai premium has stayed wide for several weeks, banks and bullion houses keep repeating the trade and rolling the futures, which is why the inbound flow has been so large..

3. Why has the premium opened up?

• Capital controls – Mainland investors can’t easily buy cheaper gold abroad, so domestic demand outruns local supply.

• RMB weakness – Gold priced in yuan is an automatic hedge against further depreciation.

• Seasonal demand – Jewellers and retail dealers stock up ahead of Q4 wedding season and Lunar New Year (February 2024).

• Tight domestic credit – Local refiners face higher financing costs, so imported bars are the cheapest marginal supply.

Bottom line

Yes, physical gold is being flown into Shanghai right now, and the sole driver is an unusually wide Shanghai-versus-world price gap. The trade is profitable so long as the premium exceeds the ≈ US$ 5–6 / oz all-in cost of moving and re-branding the metal, which remains the case as of the latest data.

end

the article from above:

Record amount of gold floods into Shanghai warehouses on arbitrage play

Submitted by admin on Wed, 2025-08-06 12:59 Section: Daily Dispatches

By Yihui Xie

Bloomberg News

Tuesday, August 5, 2025

Bullion held in warehouses linked to the Shanghai Futures Exchange has jumped to an all-time high, another sign of resilient demand for gold investments in China.

More than 36 tons of gold bars have been registered for delivery against futures contracts, a quantity that has almost doubled over the past month. The build-up in stockpiles reflects a surge in arbitrage activity triggered by heavy demand for futures, which are trading at a large premium to the physical metal.

Traders and banks have moved to take advantage of the price gap, buying cheaper gold on the spot market and delivering it to the exchange’s warehouse. From there, it can be used to offset sales of futures, allowing them to close positions at a profit.

“This shows how strong gold trading demand is in China right now,” said John Reade, senior market strategist at the World Gold Council. “So many people were piling into futures that prices shot up above physical gold. That created an opportunity for others to step in and deliver gold into the system.” …

… For the remainder of the report:

end

black market: 918,000 rials to the dollar right now. They want to remove zeros to cut the cost of printing too many paper notes

London’s Financial Times

Iran proposes slashing zeros from currency after decades of decline

Submitted by admin on Tue, 2025-08-05 10:38 Section: Daily Dispatches

Meanwhile in the United States, nickels become pennies.

* * *

By Bita Ghaffari and Joseph Cotterill

Financial Times, London

Monday, August 4, 2025

Iran has proposed cutting four zeros from the rial after decades of inflation and economic pain eroded the value of the currency.

The parliament’s economic committee approved the general outlines of a government bill to re-denominate the rial on Sunday.

Shamseddin Hosseini, the head of the committee, said the new currency would still be known as the rial, with one unit equivalent to 10,000 rials in current terms.

The proposed reduction in digits is designed to simplify financial calculations and accounting, and lower the costs of printing banknotes. Hosseini said the new rial would itself be made up of 100 gherans.

Iran’s currency has undergone significant devaluation due to international sanctions, which have isolated the country from the global banking system and throttled its economy. …

… For the remainder of the report:

end

CANADA

Gold and Trump’s chaos were key to the TSX’s stellar performance this year

Submitted by admin on Mon, 2025-08-04 21:12 Section: Daily Dispatches

By Tim Kiladze

The Globe and Mail, Toronto

Monday, August 4, 2025

Canada’s benchmark stock index is outperforming both the S&P 500 and the tech-heavy Nasdaq Composite Index in 2025, and there is a single sector doing the heavy lifting: gold.

Despite the continuing tariff drama with the United States that disproportionately hurts Canada’s economy relative to the U.S., the S&P/TSX Composite Index is up 11.1% since the start of the year, including dividends, while the S&P 500 has climbed 6.9% and the Nasdaq has risen 7.3%.

Multiple sectors have performed well on the TSX this year, but gold producers in particular are dominating, comprising 15 of the 20 best share price returns. These companies are led by Lundin Gold Inc., which has put up a 120% return, including dividends.

Gold companies also make up four of the top-five TSX performers, including Dundee Precious Metals Inc., SSR Mining Inc., and Kinross Gold Corp. They all have total returns of at least 65% since the start of the year.

The only non-gold company in the group is Celestica Inc., a Canadian technology company that came back from the dead to strike it rich off the artificial-intelligence boom. …

… For the remainder of the report:

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 234

ANDREW INTERVIEWS: LONDON PAUL:

5. COMMODITY REPORT..copper

Dr. Copper Is Talking, But Is Anyone Listening?

Thursday, Aug 07, 2025 – 12:50 PM

Authored by Simon White, Bloomberg macro strategist,

The fall in copper’s ratio versus gold is telegraphing weaker US growth ahead.

Leading indicators have signaled for a while that the US is likely entering a cyclical slowdown.

There has been much controversy over the size of the payrolls revisions – and President Trump’s subsequent sacking of the Bureau of Labor Statistics chief – but they were already in the post.

However, another market-based indicator of cyclical growth — the copper-versus-gold ratio — is also pointing to a weak economic patch ahead.

It has usually been a good guide to the ups and downs of the economy, given it captures essentially risk-on versus risk-off behavior.

Its recent slump was, of course, driven by US copper tariffs, with a 50% levy added to most types of copper imports.

But the ratio has been falling for some time, and tracks the US manufacturing ISM closely.

Gold’s rally has also been driving the ratio lower, as central banks and global investors seek to have less exposure to the dollar.

There are always idiosyncratic explanations for why markets move, but that doesn’t mean longer-term relationships such as the one in the above chart can be waved away.

It’s quite possible that tariffs and dollar diversification are not good for US growth, and the copper/gold ratio is picking up on that.

It’s too early to say if the US will go into a recession. While many commentators make the common leap of assuming that slowdown = recession, the regime-shift nature of downturns is such that you simply can’t tell with a high degree of accuracy yet.

And certainly not with enough confidence to exit the market altogether.

Recession indicators will be key to monitor in the coming months.

end

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED UP 5.67 PTS OR 0.16%

//Hang Seng CLOSED UP 157.08 PTS OR 0.63%

// Nikkei CLOSED UP 264.29 PTS OR 0.65% //Australia’s all ordinaries CLOSED DOWN 0.14%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1771 OFFSHORE CLOSED UP AT 7.1796/ Oil DOWN TO 64.91 dollars per barrel for WTI and BRENT DOWN TO 67.33 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1771 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1796 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1771 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1796

HANG SENG CLOSED UP 157.08 PTS OR 0.63%

2. Nikkei closed UP 264.29 PTS OR 0.65%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 97.84/ EURO RISES TO 1.1685 UP 21 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.483//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.76…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6546/Italian 10 Yr bond yield UP to 3.4830 SPAIN 10 YR BOND YIELD UP TO 3.238%

3i Greek 10 year bond yield UP TO 3.347

3j Gold at $3296.15 Silver at: 38.27 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 67 /100 roubles/dollar; ROUBLE AT 79.33

3m oil (WTI) into the 64 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.76// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.483% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8047 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9408 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.230 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.825 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.716 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.68

10 YR UK BOND YIELD: 4.5320 DOWN 1 PTS

10 YR CANADA BOND YIELD: 3.408 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.957 UP 1 PTS

2a New York OPENING REPORT

US Futures, Global Markets Jump On Tariff Exemptions, Renewed Hopes For Ukraine Ceasefire

Thursday, Aug 07, 2025 – 08:30 AM

US equity futures are – what else – higher, and rapidly approaching a new all time high, boosted by exemptions in Trump’s plans for 100% tariffs on chips that are seen as bullish ways for most big tech firms to avoid levies. The mood was also cheered by a report that Trump and Putin are expected to meet for summit talks in the next few days while

hopes for a rate cut rise some more as additional Fed officials have dovish pivots. As of 8:15am ET, S&P futures are up 0.6% and Nasdaq 100 futures gain 0.7% with Mag7 higher led by AAPL while Semis are the global standout. Eli Lilly & shares plunged after the drugmaker reported underwhelming study results for its weight-loss pill. Shares of its main European rival, Novo Nordisk A/S, soared. Cyclicals are poised to rip, although as JPM notes “today appears to be setting up for an ‘Everything Rally’.” Bond yields are down 1bp across the curve but 10Y is +1bp; USD is flat but has erased ~25bp of overnight losses. Today’s macro data focus is on Jobless Claims, 1Y Inflation Expectations, Nonfarm Productivity, Labor Costs, Consumer Credit, and Inventories. While none, ex-Claims, are market moving it will help sharpen the macro picture on the labor market and consumer. At 12pm, Trump will sign an executive order that aims to allow private equity, real estate, cryptocurrency and other alternative assets in 401(k)s.

In premarket trading, Mag 7 stocks are all higher (Apple +2%, Nvidia +1.4%, Meta +0.9%, Alphabet +0.6%, Microsoft +0.6%, Tesla +0.5%, Amazon +0.1%)..

- Airbnb (ABNB) is down 6% after warning that growth rates may not keep up later this year due to tough year-ago comparisons.

- Aris Water Solutions (ARIS), which helps manage water produced from oil drilling, climbs 20% after the company agreed to be bought by Western Midstream Partners in a ~$1.5b equity-and-cash transaction.

- Corning (GLW) gains 5% after Apple said it’s planning to onshore 100% of iPhone and Watch cover glass production to the US as part of an expanded $2.5 billion partnership with the high-tech glassmaker.

- CRH (CRH) jumps 8% after the building materials company narrowed its full-year adjusted Ebitda guidance to the high end of its prior range.

- Crocs (CROX) falls 13% after forecasting that 3Q revenue will be down about 11% to 9%.

- DoorDash (DASH) gains 8.9% after the food-delivery company reported second-quarter results that beat expectations and gave a positive forecast for Marketplace gross order value.

- Duolingo (DUOL) soars 23% after the language-learning software company reported second-quarter results that beat expectations on key metrics and raised its full-year forecast.

- Dutch Bros (BROS) is up 18% after the restaurant chain lifted its total revenue forecast for the full year.

- Eli Lilly & Co (LLY) plunges 12% after the company gave disappointing data from a late-stage trial of its new weight-loss pill.

- Fortinet (FTNT) tumbles 21% after the software company gave an update to its firewall refresh cycle. At least three analysts downgraded their rating on the stock saying the product refresh cycle is now looking like a “much smaller catalyst than expected.”

- Intuitive Machines (LUNR) gains 2% after the space services company said it would buy privately held aerospace company KinetX, expanding its deep-space navigation and flight dynamics capability.

- Peloton Interactive Inc. (PTON) gains 12% as the company preached confidence in a turnaround plan under new management.

- Sarepta (SRPT) is up 7% after the drugmaker reported second quarter revenue that beat the average analyst estimate.

- SharkNinja (SN) rises 5% after the home-appliance maker boosted its adjusted earnings per share forecast for the full year.

- Sunrun (RUN) jumps 18% after the solar energy company reported second-quarter revenue that beat the average analyst estimate.

- Upwork (UPWK) shares are up 12% after the online recruitment company reported second-quarter results that beat expectations and raised its full-year forecast.

- Vistra Corp. (VST) falls 7% after the residential electricity provider operating posted revenue for the second quarter that missed the average analyst estimate.

Market sentiment got a boost earlier after Trump announced that companies producing goods in the US, such as Apple, would be eligible for exemptions from his proposed 100% levy on chip imports. Increasing bets on a Federal Reserve interest-rate cut are also fueling optimism in stocks as sweeping new tariffs to reshape global trade officially took hold Thursday. Ironically the only major US semiconductor stock, Intel, plunged after Trump sa id on Truth Social CEO its has to resign.

“Risk sentiment is positive with a focus on peace deal hopes for Ukraine,” said Bob Savage, head of markets macro strategy at Bank of New York Mellon. “Also supporting the dollar down/stocks up narrative is ongoing September rate cut expectations for the FOMC. However, investors still face a pushback from the uncertainty over tariffs ahead.”

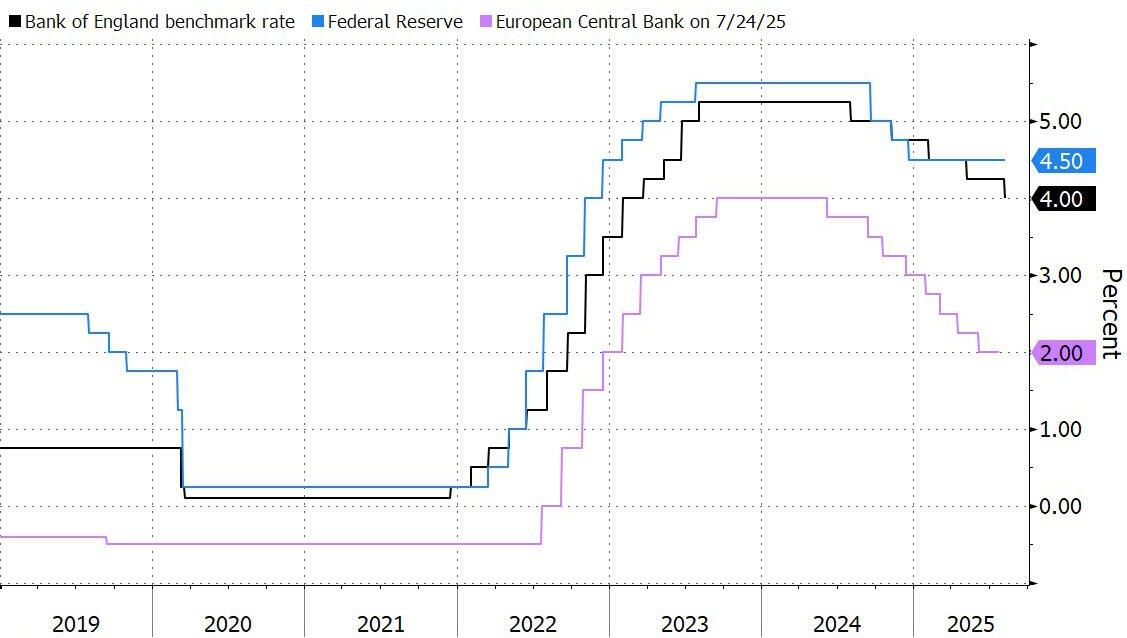

This morning, the BoE delivered a hawkish 25bps cut, with the vote split 5:4 for 25bps vs hold, and the statement noting that timing/extent of further cuts will be based on continued improvements in underlying inflation. The vote was the first ever revote in 28 years after the 4:4:1 vote in the first round failed to reach a majority.

Europe’s Stoxx 600 benchmark advanced more than 1%, with the the travel and leisure sector outperforming. A basket of equities exposed to Ukraine rose, while defense shares dropped, after the Kremlin said that presidents Vladimir Putin and Donald Trump will meet for summit talks within the next few days. Upbeat earnings from some of the region’s biggest companies helped boost sentiment, even after German industrial production suffered its biggest drop in almost a year in another setback for Europe’s largest economy. Here are the biggest movers Thursday:

- InterContinental Hotels jumps as much as 9.2%, to the highest level since March, after the company reported that revenue per available room for the first half of the year increased 1.8%. Pretax profit topped the analyst consensus

- Maersk gains as much as 6%, the most since May, after the Danish shipping and logistics giant boosted its full-year guidance and beat second-quarter estimates. Analysts say the guidance raise, while somewhat expected, is welcome

- Allianz gains as much as 4.3%, the most since April, after the German insurance group posted a strong second-quarter showing, with operating profit coming in ahead of expectations

- KBC jumps as much as 6.1%, trading at their highest level since 2007, after the Belgian bank beat expectations in the second quarter and improved its guidance for the full year, which analysts say will lead to consensus upgrades

- Harbour Energy shares rise as much as 21%, the steepest gain since December 2023, after the UK oil and gas company boosted guidance for production and cash flow, while announcing announcing a $100m buyback

- LINK Mobility gains as much as 9.7% after DNB Carnegie “significantly” raised its estimates for the Norwegian communications technology firm and reiterated its buy rating, while nearly doubling its price target

- Serco shares jump as much as 8.8%, to the highest since November 2014, after the outsourcing company reported earnings ahead of expectations and a strong order intake, accompanied by a new £50 million share buyback

- European defense stocks slump, while stocks with exposure to Ukraine and Russia gain, as traders take a cue from President Donald Trump’s diplomatic push to end the Ukraine war and US efforts to punish buyers of Russian crude. Rheinmetall shares fall as much as 7.2%, the most in two months, after analysts described the German defense firm’s results as weak. Jefferies points to soft orders and sales below expectations

- Carl Zeiss Meditec shares plunge as much as 14% to the lowest since August 2017 after analysts said the German health-care supplier’s 3Q Ebita miss was weighed down by its microsurgery business

- Hikma shares drop as much as 10% in London, the most intraday since February, after the pharmaceutical company missed core Ebidta estimates and lowered the margin guidance for its Injectables division for the full year

- Freenet shares fall as much as 9.5%, the most since May, after the German-listed mobile communications service provider cut its average revenue per user. Analysts at Berenberg note a marginally disappointing set of results

- Deutsche Telekom shares slide as much as 6.1% after the telecom operator reported sales and Ebitda that missed estimates in its home market Germany, with the company flagging intense rivalry in the local broadband market

- Siemens shares fall as much as 1.9% after the German industrial company posted what analysts called mixed results, highlighting a weaker performance in the Digital Industries division. Shares are still up almost 16% YTD

- Scout24 shares drop as much as 6.1% after the classifieds company reported detailed 2Q results. The shares had gained earlier in the week when the company raised its full-year guidance in a pre-release

Earlier in the session, Asian stocks rose, led by technology stocks as some of the region’s largest chipmakers were expected to win exemptions from Donald Trump’s threatened 100% chip tariff. The MSCI Asia Pacific Index advanced 1%, rising for the fourth straight day. Taiwan’s benchmark rose more than 2%, with notable gains in most other markets around the region. Thailand’s key index was on the brink of entering a bull market. Chipmakers TSMC and Samsung were among the biggest boosts to the MSCI index as investors saw their US manufacturing operations as freeing them from Trump’s newest levies. A gauge of regional tech stocks climbed by the most since June 24. Meanwhile, Indian equities fell after the US moved to double the tariff on imports from the South Asian nation to 50%. The higher rate is seen further hurting sentiment on a market already underperforming Asian peers on disappointing corporate earnings.

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The Antipodean currencies outperform their G-10 peers, rising 0.4% each against the greenback. EUR/USD briefly extended gains on news that Putin and Trump would meet within days, hitting a session high of almost $1.17, before falling back to $1.1648. GBPUSD rose, putting it on track for a fifth day of gains against the dollar, its longest winning streak since April.

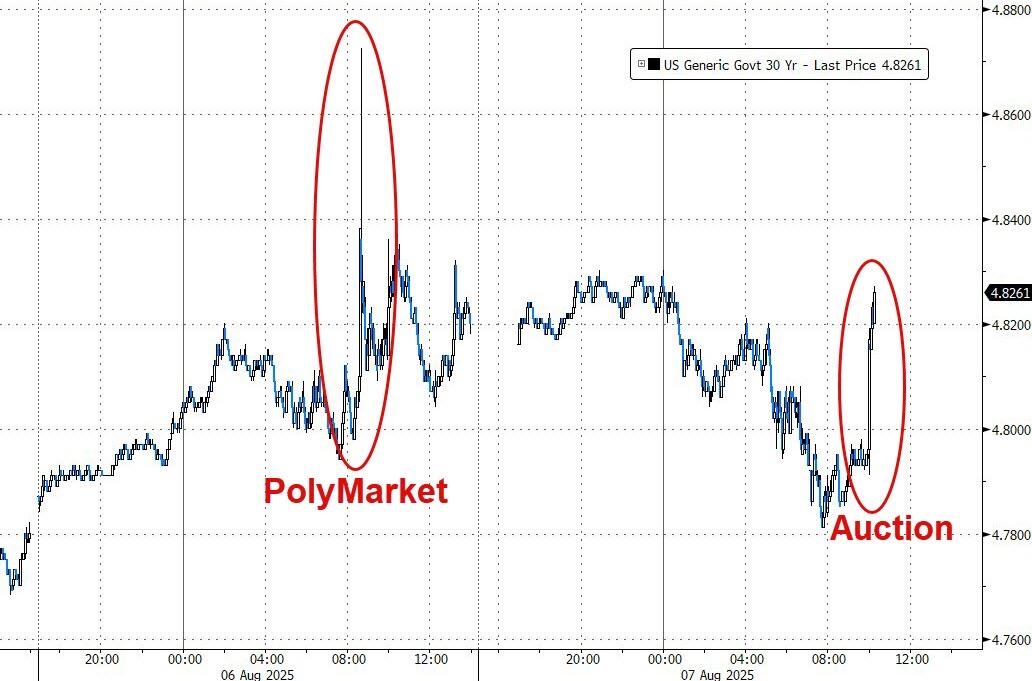

In rates, treasuries are steady, with yields broadly within one basis point of Wednesday’s close, despite slide in gilts which sharply underperform following a 4-4-1 Bank of England vote to cut rates by 25bp. US yields steady, marginally cheaper on the day with 10-year near 4.245%, outperforming gilts by around 4bp in the sector. UK 2-year yields higher by around 6bp on the day up to around 3.88% following the announcement. Bunds outperform, pushing German 10-year yields down 2 bps to 2.63%. In the US, focus turns to early data and then a $25 billion 30-year new-issue bond sale at 1pm New York time, which follows a 1.1bp tail on Wednesday’s 10-year note auction.

In commodities, oil prices erase an earlier drop following the Putin-Trump meeting news, with Brent now up 0.5% near $67.22 a barrel. Gold rises $8 to around $3,377/oz.

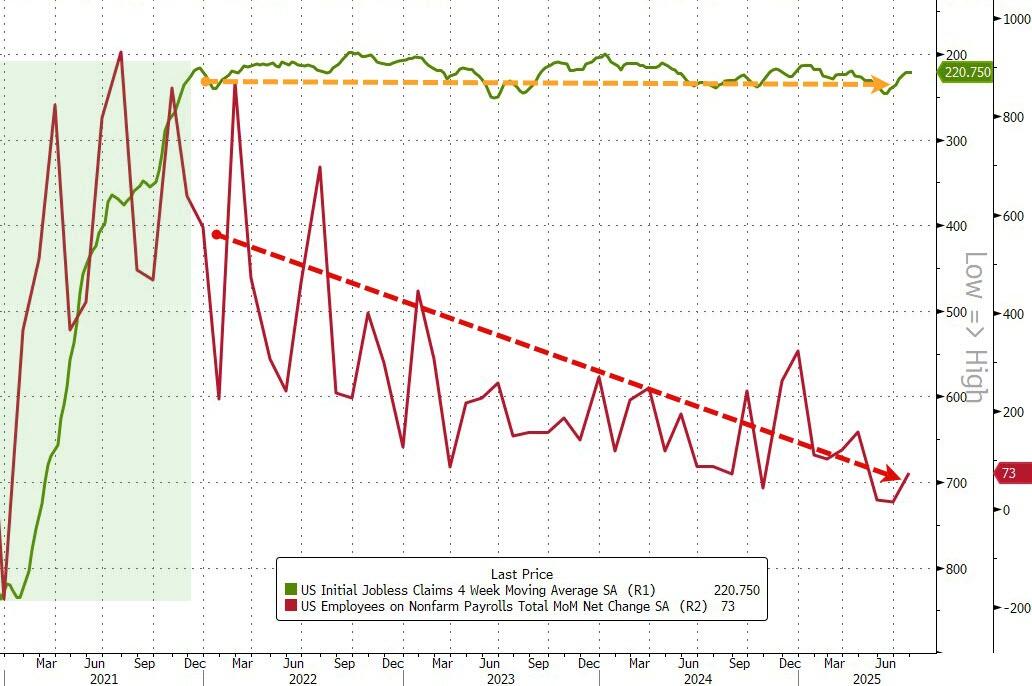

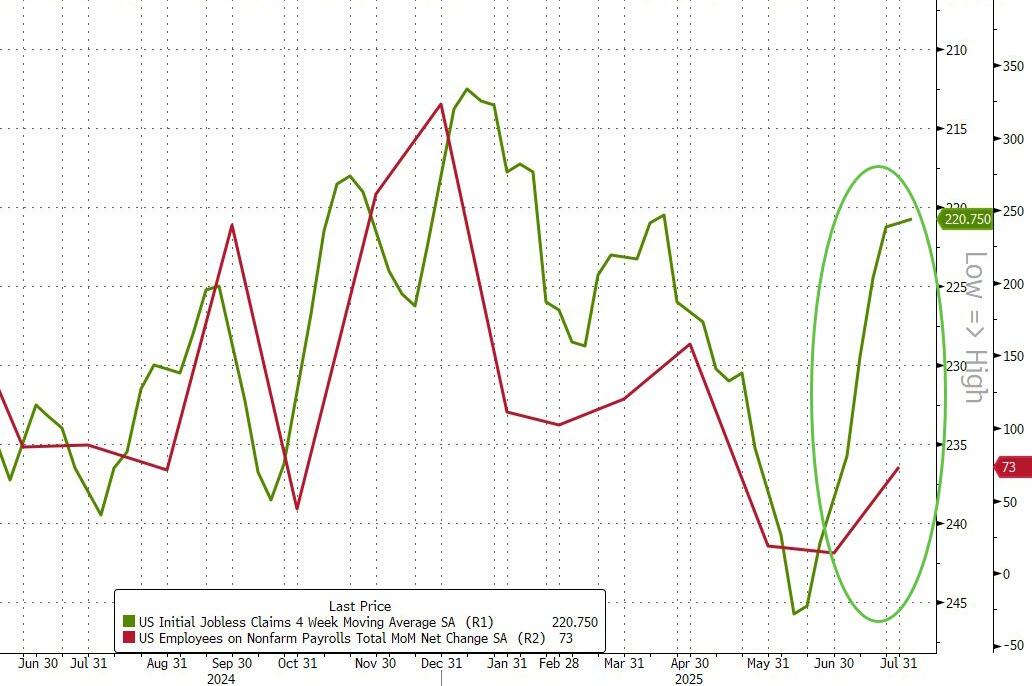

Looking ahead today, Trump will sign an executive order that aims to allow private equity, real estate, cryptocurrency and other alternative assets in 401(k)s. Data-wise we have 2Q preliminary nonfarm productivity and unit labor costs and weekly jobless claims (8:30am), June final wholesale inventories (10am), July NY Fed 1-year inflation expectations (11am) and June consumer credit (3pm). Fed speakers scheduled include Bostic in a virtual fireside chat on monetary policy (10am)

Market Snapshot

- S&P 500 mini +0.6%

- Nasdaq 100 mini +0.7%

- Russell 2000 mini +0.8%

- Stoxx Europe 600 +0.8%

- DAX +1.7%

- CAC 40 +1.2%

- 10-year Treasury yield little changed at 4.23%

- VIX -0.6 points at 16.13

- Bloomberg Dollar Index -0.1% at 1202.97

- euro +0.2% at $1.1678

- WTI crude +0.6% at $64.73/barrel

Top Overnight News

- Trump said, regarding the Fed pick, that the interview process has started and it is probably down to three candidates, while he added that the two Kevins are very good, and a temporary governor is to be named in the next few days.

- U.S. trading partners are lobbying the White House for exemptions to sweeping new tariffs that went into force on Thursday, as countries seek ways to muffle the impact on their economies of President Trump’s push to reorder global trade. The diplomatic effort shows months of trade talks are far from over despite the run of agreements trumpeted by the White House in the past month. WSJ

- President Trump has claimed that his sweeping tariff regime will reshore American companies and revive manufacturing in the U.S. So far, that hasn’t happened. Economic activity tied to manufacturing has shrunk for most of Trump’s second term. From March to July, U.S. manufacturing activity contracted. The Manufacturing PMI last registered at 48, below the 50 score that differentiates growth and decline. WSJ

- The Kremlin said Thursday that a meeting between presidents Donald Trump and Vladimir Putin has been agreed in principle and will happen in the “coming days,” teeing up their first in-person encounter of Trump’s second term. NBC

- Trump said he may punish China with additional tariffs over its purchases of Russian oil. Trade adviser Peter Navarro played down the likelihood, saying higher duties “may hurt the US.” BBG

- Trump will sign an executive order today that aims to allow private equity, real estate, cryptocurrency and other alternative assets in 401(k)s. BBG

- China’s exports grew at a faster clip in July, showing that U.S. tariffs so far haven’t curtailed China’s export machine, although trade with America has fallen. Trade numbers for Jul come in ahead of expectations, including exports (+7.2% vs. the Street +5.6%) and imports (+4.1% vs. the Street -1%). WSJ

- Japan cut its growth forecast for the current fiscal year as US tariffs and persistent inflation weigh on the economy. BBG

- Caught between rising costs from tariffs and belt-tightening consumers, big retailers are clashing with the producers of consumer brands such as Nivea-maker Beiersdorf and brewer Heineken as they look to avoid sticker shock that could hurt sales. The disputes – which have dented some brands’ sales – underscore the challenge for consumer goods makers and sellers, with inflation and tariffs pushing up input costs and price spikes in commodities such as coffee. RTRS

- Fed’s Daly (2027 voter) said there’s cautiousness which is tempering growth but not stalling out, while she commented that they will likely need to adjust policy in the coming months and can’t wait for perfect clarity to act. Daly also commented that tariffs are unlikely to boost inflation persistently in a way that monetary policy would need to offset. She also noted that the labour market has softened and additional slowing would be unwelcome. Furthermore, Daly said they need to recalibrate monetary policy to match risks to the Fed’s goals.

Trade/Tariffs

- US President Trump said they are going to be putting a very large tariff on chips and semiconductors, which will be at approximately 100%, but added “if you’re building in the US, there will be no charge.”

- US President Trump posted late on Wednesday that “RECIPROCAL TARIFFS TAKE EFFECT AT MIDNIGHT TONIGHT! BILLIONS OF DOLLARS, LARGELY FROM COUNTRIES THAT HAVE TAKEN ADVANTAGE OF THE UNITED STATES FOR MANY YEARS, LAUGHING ALL THE WAY, WILL START FLOWING INTO THE USA.”

- US official said the 15% tariff will stack on top of pre-existing tariff rates applied to imports from Japan, unlike in the case of the European Union, according to Kyodo.

- South Korea claimed Samsung Electronics (005930 KS) and SK Hynix (000660 KS) will not be subject to 100% US tariffs, while Taiwan said TSMC (2330 TT) is exempt from US President Trump’s 100% chip tariff.

- Apple (AAPL) suppliers are reportedly betting on a tariff carve-out for India-made iPhones, according to Nikkei sources.

- Maersk (MAERSKB DC): “The effective container-weighted import tariff on US imports is estimated at 24% as per the Presidential Executive Order dated 31 July, up from 5% in 2024”

A more detailed look at global markets courtesy of Newsquawk