118 C MACQUARIE FUTURES US 18

167 C MAREX 23

285 C NANHUA USA-HK 29

332 H STANDARD CHARTERED B 326

363 H WELLS FARGO SECURITI 7

435 H SCOTIA CAPITAL (USA) 57

661 C JP MORGAN SECURITIES 217

709 C BARCLAYS 10

732 C RBC CAP MARKETS 15

905 C ADM 4

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 353 CONTRACTs NOTICES FOR 35,300 OZ or 1.078 TONNES

total notices so far: 26,968 contracts for 2,696,800 OR 83.881 tonnes)

SILVER NOTICES:29 NOTICE(S) FILED FOR 145,000 OZ/

total number of notices filed so far this month : 1716 CONTRACTS (NOTICES) for 8.580 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 21.845 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 150,000 OZ QUEUE JUMP//NEW STANDING REMAINS AT 8.65000 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 1.7604 TONNES + 5.4432 TONNES EX FOR RISK/AUG 7 AND AUG 11: 2.413 TONNES EX FOR RISK AND NOW TODAY’S AUG. 12 OF 2.637 TONNES EX FOR RISK //NEW STANDING ADVANCES TO 88.730 TONNES OF GOLD + 5.4432 TONNES EX FOR RISK + 2.413 TONES EX FOR RISK AUG 11+ 2.637 TONNES AUG 12 = 99.223 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 80.447 TONNES QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 2082 CONTRACTS OI TO 154,473 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 200 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 370 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2082 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 1882 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.56 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 9.410 MILLION PAPER OZ

OCCURRED WITH OUR $0.56 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS MONDAY MORNING:

SHANGHAI CLOSED UP 18.37 PTS OR 0.60%

//Hang Seng CLOSED UP 62.87 PTS OR 0.25%

// Nikkei CLOSED UP 897.69 PTS OR 2.15% //Australia’s all ordinaries CLOSED UP 0.36%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1907 OFFSHORE CLOSED DOWN AT 7.1962/ Oil UP TO 63.82 dollars per barrel for WTI and BRENT UP TO 66.53 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1907 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1962 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A HUGE SIZED 15,133 CONTRACTS TO 452,687 OI WITH OUR LOSS IN PRICE OF $53.55 WITH RESPECT TO MONDAY’S // TRADING.. WE LOST SOME NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2430 ). WE HAD CONSIDERABLE T.A.S. LIQUIDATION //MONDAY TRADING AS WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 12,661 CONTRACTS (OR 39.88 TONNES)

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY:

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST;

EARLY THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE FOR AUGUST OF A MONSTER 1750 CONTRACTS FOR 175,000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. WITH ALL THE CHAOS AT THE COMEX IT WAS NO SURPRISE THAT THEY ISSUED THEIR SECOND EXCHANGE FOR RISK, AUG 10 TOTALLING 776 CONTRACTS OR 77,600 OZ (2.418 TONNES).MUCH TO MY ANGER TONIGHT, THE CME ANNOUNCED ITS 3RD EXCHANGE FOR RISK OF 848 CONTRACTS TOTALLING 84,800 OZ OR 2.637 TONNES.

THUS THE TOTAL FOR AUGUST IS 3374 CONTRACTS OR 337,400OZ OR 10.4932 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS. THE RECEPIENT OF THIS LARGESS IS PROBABLY NOW THE BANK OF ENGLAND AS WE HAVE JUST LEARNED THAT THE FRBNY HAS RETURNED ONLY 14,000 OZ AS THEIR LOANS TO THE BIS REMAIN AT 34+ TONNES.(JULY 31 FIGURES) IT SEEMS NOW THAT THE BANK OF ENGLAND IS IN QUITE A HURRY TO GET ITS GOLD BACK!!

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 3 ISSUANCES FOR A MONSTER 3374 CONTRACTS OR 337,400 OZ ( 10.4932 TONNES)

AS I EXPLAINED ABOVE,:THE RECPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 12,661 CONTRACTS WITH OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 1,688 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED TWO WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS A QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS TODAY’S HUGE QUEUE JUMP OF 1.7604 TONNES +10.4932 TONNES EX FOR RISK (3 ISSUANCES) //NEW STANDING 99.223 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 235 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NONE COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 1.7604 TONNES TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE + SATURDAY’S HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES AND THEN TODAY;S AUGUST 12: 2.637 TONNES:/NEW STANDING ADVANCES TO 99.223 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2430 EFP CONTRACT WAS ISSUED: : /DEC 2430 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2630 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY

- MONTH END SPREADERS WILL APPEAR ON THE LAST WEEK OF AUGUST.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED SIZED 1688 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S FIRST THREE ISSUANCES OF EXCHANGE FOR RISK FOR 10.4932 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S MONSTER QUEUE JUMP OF 1.7604 TONNES TO WHICH WE ADD THURSDAY’S HUGE 5.4432 EXCHANGE FOR RISK, SATURDAY’S STRONG 776 CONTRACT ISSUANCE (77600 OZ) FOR 2.413 TONNES AND THEN TODAY AUGUST 12 FOR 2.637 TONNES TOTAL EX FOR RISK = 10.4932 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

88.730 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

EQUALS

99.223 TONNES TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A $53.55/ /) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION ///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID THIS WEEK.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: THREE SO FAR, AUGUST 7 AT 3374 CONTRACTS FOR 337,400 OZ (10.4932 TONNES OF GOLD) WITH TODAY’S ISSUANCE OF 848 CONTRACTS FOR 84800 OZ OR 2.637 TONNES. TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 10.4932 TONNES

THUS 88.730 TONNES OF GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 10.4932 TONNES = 99.223 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE LOST A STRONG SIZED TOTAL OF 39.449 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD THURSDAY’S RECORD BREAKING QUEUE JUMP OF 10.8775 TONNES OF GOLD ON TOP OF TODAY’S HUGE 1.7604 TONNES QUEUE JUMP AND THEN ADD OUR THREE EXCHANGE FOR RISK FOR 10.4932 TONNES FOR RISK//NEW STANDING ADVANCES TO 99.223 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $53.55

WE HAD A HUGE22 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 12,683 CONTRACTS OR 1,268,300 0Z (39.449 TONNES)

confirmed volume MONDAY 262,930 contracts// good

speculators have left the gold arena

END

INITIAL GOLD COMEX

AUGUST CONTRACT MONTH

AUGUST11 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entry . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 353 notice(s) 35,300 OZ 1.078 TONNES |

| No of oz to be served (notices) | 1559 contracts 155,900 OZ 4.849TONNES |

| Total monthly oz gold served (contracts) so far this month | 26,968 notices 2,696,800 oz 83.881 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entry

adjustments: 0

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 1912 CONTRACTS FOR A LOSS OF 3420 CONTRACTS

WE HAD 3986 CONTRACTS SERVED ON MONDAY SO WE GAINED A HUGE SIZED 566 CONTRACTS OR 56,600 OZ OF GOLD (1.7604 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND.. THIS ALSO REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD AND THEIR APPETITE FOR THIS GOLD IS UNABATED!

SEPT LOST 453 CONTRACTS TO 5684

OCTOBER LOST 1287 CONTRACTS DOWN TO 63,954

We had 353 contracts filed for today representing 35,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 353 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 217 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (26,968 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 1912 CONTRACTS) minus the number of notices served upon today (353 x 100 oz per contract) equals 2,852,700 OZ OR 88.730TONNES TO WHICH WE ADD OUR THREE ISSUANCES OF 10.4932 TONNES OF EXCHANGE FOR RISK/AUG 7 , 11 AND 12TH = 99.223 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (26,968 x 100 oz +we add the difference for front month of AUGUST (1912 OI} minus the number of notices served upon today (353 x 100 oz) which equals 2,852,700 OZ OR 88.730 TONNES + 10.4932 TONNES EX FOR RISK = 99.223 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 10.4932 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,010,548.158 oz 62.536 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,584,987.719 oz

TOTAL REGISTERED GOLD 21,407,166.414 or 665.759 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,177,821.305 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,396,618 oz ((REG GOLD- PLEDGED GOLD)= 603.331tonnes // ( a bid drop of 10 tonnes

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE AUGUST 2025 SILVER CONTRACT//INITIAL

AUGUST 11 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 ENTRY i) Out of Delaware: 923.50 oz total withdrawal 923.500 oz |

| Deposits to the Dealer Inventory | 0 |

| Deposits to the Customer Inventory | 1 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into CNT 601,018.700 oz total deposit 601,018.700 oz |

| No of oz served today (contracts) | 29 CONTRACT(S) (145,000 OZ |

| No of oz to be served (notices) | 14 contracts (0.070 MILLION oz) |

| Total monthly oz silver served (contracts) | 1716 Contracts (8.580 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

0 deposit into dealer accounts

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into CNT 601,018.700 oz

total deposit 601,018.700 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

1 ENTRY

i) Out of Delaware: 923.50 oz

total withdrawal 923.500 oz

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 190.400 MILLION OZ//.TOTAL REG + ELIGIBLE. 507.041 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 43 OPEN INTEREST CONTRACTS FOR A LOSS OF 7 CONTRACTS. WE HAD 37 CONTRACTS SERVED ON MONDAY SO WE GAINED 30 CONTRACTS OR AN ADDITIONAL 150,000 OZ WILL STAND AS THEY ENTERTAINED A HUGE QUEUE JUMP

SEPTEMBER LOST 8855 CONTRACTS DOWN TO 82,046 CONTRACTS.

OCTOBER GAINED 13 CONTRACTS TO 537

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 29 or 145,,000 oz

CONFIRMED volume; ON MONDAY 108.159 HUGE//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1716 X5,000 oz = 8.580 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (43) AND the number of notices served upon today (29 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1716) Notices served so far) x 5000 oz + OI for the front month of AUGUST(43) minus number of notices served upon today (29)x 5000 oz equals silver standing for the AUGUST contract month equating to 8.650 MILLION OZ .

New total standing: 8.6500 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.400 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/507.041 million. 41.47%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 964.22 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 484.145 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

The death of fiat

The end of the 54-year fiat currency era is imminent — that is gold’s message. Increasing credit risk means higher interest rates, which will burst credit bubbles.

| Alasdair MacleodAug 12∙Paid |

The yield on the long bond is ready to break out on the upside over 5%, giving a technical target above 9%. Implications for all financial markets are dire.

Introduction

That central banks are ditching dollars for gold and have been for at least the last four years is an important message for us all. Geopolitics and even US politics are involved: but the fact that this widespread rebalancing of reserves is taking place is the clearest indication that the ultimate insiders to the currency game know that the dollar’s gig is nearly up.

Critics of the 54-year old anti-gold propaganda spreading out of the US and being repeated ad nauseum by its Keynesian epigones in the G7 are no longer dismissed as conspiracy theorists. Increasingly, the middle classes in these nations see the threat from rapacious governments taking their earnings and savings. And these defenceless victims of social democracy are only just beginning to understand that there is an additional theft of their wealth through the debasement of their currencies.

Initially, their wake-up call came from the bitcoin concept. The legal relationship between corporeal gold and incorporeal credit remains a mystery to them — but not to the insiders at central banks.

Reasoned economic and monetary theories, confirmed by historical evidence, tell us that currencies must return to gold standards to secure their values, circulating as trusted gold substitutes. Only then, can general economic progress resume. Getting there is going to be extremely difficult but is not the focus of this article. Instead, we must all focus on how to protect our personal wealth from the death throes of the dollar-based fiat currency system.

The debt-cum-credit bubble

One of today’s most common errors is to believe that the cost of debt is always controlled by central banks. When debt is not excessive, a central bank can manipulate interest rates and bond yields to some extent. But when debt is excessive and rising exponentially, it is creditors who have the final say.

These are the conditions emerging today. The authorities won’t admit it, but the US economy is sliding into recession, which with its government debt to GDP ratio at about 120% means that buyers of accelerating dollar debt issuance will see increasing risk of a debt trap. Bond yields will reflect that risk, and will rise accordingly.

Ever-higher bond yields are the consequence of a debt trap, which deters all buying of bonds. As yields rise and commercial banks attempt to avoid lending risk, the Fed will end up underwriting the entire credit system. Inevitably, the dollar’s purchasing power will be further undermined as currency and reserves flood the system, requiring yet higher interest compensation for holders of both short and long-term debt.

It is the engine that drives hyperinflation.

This outcome is supported by experience. In the UK, a sterling crisis in 1975 ended with the IMF being sent in to impose fiscal and spending discipline on the government of the day. In those times, gilt funding required coupons of over 15% and consumer price inflation hit 25%.

This external discipline is not available to the US, so it will be imposed by markets. There is no foreseeable limit on how low the dollar can go and how high bond yields and interest rates will rise. Already, the US Treasury is resorting to short-term finance because of poor demand for long-dated bonds at current yields.

Essentially, the US Treasury relies increasingly on pay-day loans on a national scale, as the Fed holds short-term rates above those of the yen and euro. But we know what eventually happens to the rates on pay-day loans. And as the mighty US Treasury loses credibility, rates rocket or the dollar sinks — most likely both. That is what gold is telling us: it’s not that gold is rising, but the dollar is sinking. And since all fiat currencies operate on a loose dollar standard, they are going down with the dollar as well.

However, the dollar is even declining against other fiat currencies, reflected in its trade-weighted index which has lost 10.6% since mid-January:

The US government with its dollar are not the only highly indebted government and fiat combination. Other G7 economies are also struggling, declining even when their budget deficits are subtracted from GDP. Debt and matching credit bubbles are evident everywhere, from Japan to France, from Spain to the UK.

Most investors are myopic about the role of credit. But for every debt there is a credit, and increasingly that credit has fed into stocks. Margin finance is now over $1 trillion, and rising steeply:

However, toward the end of an equity bull market, bond yields begin to rise. This stretches valuation differences to the point where eventually the equity bubble bursts. Today, the valuation difference is already the highest on record, illustrated in the next chart:

By way of explanation, the chart has been constructed to show the close negative correlation between the long bond yield and the S&P Index over time by inverting the long bond yield and indexing both metrics to 100 in January 1985.

The principal aberrations in this correlation were the dot-com bubble, the Lehman crisis when bond yields and equities both fell, covid when the long bond yield was suppressed to one per cent, and today when the long bond yield has risen to 4.9% while the S&P continues to rise.

The correlation always reverts to its mean for obvious reasons. But relative to the long bond, equities are the most overvalued for forty years, and probably for all time.

Clearly, this is an extremely dangerous situation. Even without the long bond yield rising further, the correlation returning to its mean would see the S&P losing 75% to test the previous 2000 and 2007 highs. But bond yields are certain to rise from current levels. When, not if, the 30-year UST bond rises through 5% it will crash the equity market.

Meanwhile, credit continues to fuel asset values. M2 money supply has expanded by about $500 billion over the last two years, matching the increase in margin debt in the penultimate chart above. But riding the equity bubble is like living in the shadow of a volcano: all is fine and dandy until suddenly without warning it isn’t.

Other than equities and bonds, activities whose very existence will be challenged when the bubble pops include:

· Cryptocurrencies, which have no standing as legal tender and whose performance correlates closely with the more speculative technology stocks in NASDAQ, and which will just as surely be doomed by the credit bubble bursting.

· Without secure and trusted payments, the collapse in economic activity will almost certainly be far greater than that of the 1930s slump, creating additional problems for all credit.

· Financial collateral will be sold to cover loans or become worthless in bankruptcy.

· Debt finance availability will collapse, and over-indebted businesses will fail to refinance at rates they can afford. Even conservatively leveraged commercial operations will be threatened by higher bond yields and the absence of available bank credit to supplement cash flows.

· Residential property prices depend on mortgage finance, so will decline. Excess capacity in commercial real estate is already being revealed with much more to come.

· Key commodity derivatives are already facing physical liquidity constraints. The risk inherent in all OTC derivatives due to the risk of counterparty failure will outweigh their use for risk protection.

· Global trade will contract sharply, initially because of tariff disruption and then because settlement in failing fiat is undesired. Bartering goods one for another will become common.

This list is of just some examples of where the dangers to our wealth lie and is far from exhaustive. But there is only one solution for those seeking to protect their wealth and their families: get out of credit as much as you can and into real corporeal money without counterparty risk. And that is only gold, with silver as a subsidiary metal.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

The gold swaps by the Frbny remains at 34 tonnes of gold having fallen slightly by only 14,000 oz

Not happy with this!!

(zerohedge)

BIS gold swaps held steady at 34 tonnes in July, GATA’s Robert Lambourne reports

Submitted by admin on Mon, 2025-08-11 20:50 Section: Daily Dispatches

8:55p ET Monday, August 12, 2025

Dear Friend of GATA and Gold:

Gold swaps undertaken by the Bank for International Settlements, the central bank of the central banks and often their broker in the gold market, fell slightly in July, by about 14,000 ounces, but, rounded off, remained at June’s 34-tonne mark, according to GATA consultant Robert Lambourne.

The information can be calculated from the bank’s monthly statement of account for July, published today:

The report implies that the bank was not recruited to intervene much in the gold market in June on behalf of its member central banks and that there continues to be little interest among them in incurring more gold liabilities or in letting their metal get far from home.

The report written by Lambourne on July 1 —

— provides some history on the swap transactions and their volatility since the bank in 2010 made it possible for its gold swaps to be calculated.

As recently as January 2022 the bank’s swaps exceeded 500 tonnes but they have fallen sharply since, indicating a change of policy toward or outlook on gold, a trend that seems to have correlated with increasing central bank acquisitions and repatriations, along with gold’s rising price.

Nevertheless, the BIS has a well-placed confidence that no mainstream financial news organization will ever ask it to explain the purposes of the swaps and to identify the parties to them, lest gold cease being the immensely powerful secret knowledge of the financial universe.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 235

5. COMMODITY REPORT..LITHIUM

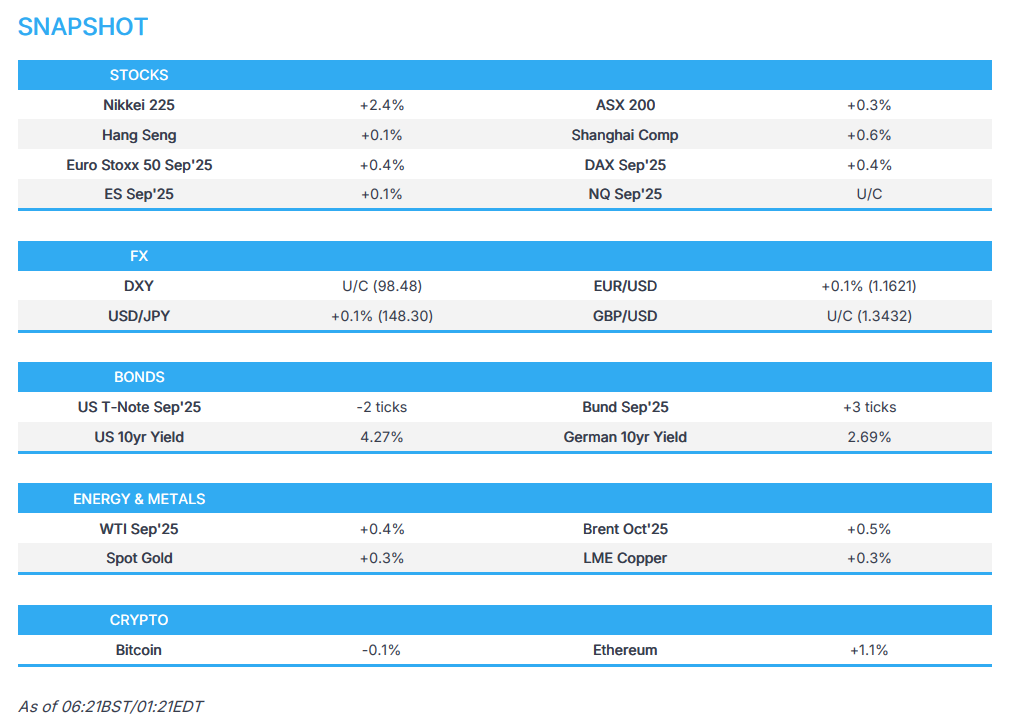

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 18.37 PTS OR 0.60%

//Hang Seng CLOSED UP 62.87 PTS OR 0.25%

// Nikkei CLOSED UP 897.69 PTS OR 2.15% //Australia’s all ordinaries CLOSED UP 0.36%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1907 OFFSHORE CLOSED DOWN AT 7.1962/ Oil UP TO 63.82 dollars per barrel for WTI and BRENT UP TO 66.53 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1907 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1962 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1907 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1962

HANG SENG CLOSED UP 62.87 PTS OR 0.25%

2. Nikkei closed UP 897.69 PTS OR 2.15%

3. Europe stocks SO FAR: MOSTLY ALL GREEN

USA dollar INDEX DOWN TO 98.35/ EURO FALLS TO 1.1615 DOWN 2 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.506//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.43…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6988/Italian 10 Yr bond yield UP to 3.515 SPAIN 10 YR BOND YIELD UP TO 3.262%

3i Greek 10 year bond yield UP TO 3.368

3j Gold at $3349.90 Silver at: 37.80 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 32 /100 roubles/dollar; ROUBLE AT 79.82

3m oil (WTI) into the 63 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.43// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.507% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8099 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9407 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.285 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.848 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.770 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.71

10 YR UK BOND YIELD: 4.5650 DOWN 4 PTS

10 YR CANADA BOND YIELD: 3.396 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.937 UP 1 PTS

2a New York OPENING REPORT

US Futures Flat Ahead Of CPI

Tuesday, Aug 12, 2025 – 08:22 AM

US equity futures are flat into today’s CPI print, which is expects to show a modest increase in YoY prints (full preview here) with bond yields reversing an earlier drop. As of 8:00am ET, S&P and Nasdaq futures were down 0.1%, with Mag7 names mixed in premarket trading: NVDA is lower as China asks firms to not use the H20 chips; Intel gains after its CEO met Trump last night with Trump posting positive comments after the meeting. European stocks erase early gains of as much as 0.4%. The dollar gains for the second day while US Treasuries trade flat, with the yield on 10-year notes at 4.29%. Commodities are higher led by Metals; gold is flat at $3350 as is bitcoin which trades just under $119K. Trump announced he would nominate labor stats critic EJ Antoni for head of BLS. US economic data slate focuses on the CPI print at 8:30am; we also get the July federal budget balance at 2pm.

In premarket trading, Mag 7 stocks are mixed (Tesla +0.3%, Microsoft +0.1%, Amazon -0.05%, Meta +0.02%, Alphabet -0.1%, Nvidia -0.1%, Apple -0.5%). Nvidia dipped after China urged local firms to avoid the chipmaker’s H20 processors, particularly for government-related purposes. The move will complicate Nvidia’s attempts to recoup billions in lost China revenue, as well as the Trump administration’s push to turn those sales into a US government windfall. Here are some other notable premarket movers:

- Cannabis producers are up and on course to extend Monday’s rally, after President Donald Trump said he was considering reclassifying marijuana as a less dangerous drug. Tilray Brands (TLRY) +18%, Canopy Growth (CGC) +8%

- Archer Aviation (ACHR) shares drop 9% after the flying taxi company a 2Q adjusted Ebitda loss that’s wider that expected.

- AST SpaceMobile (ASTS) gains 12% after the satellite firm set out an ambitious plan to launch 45 to 60 satellites during 2025 and 2026. The firm also said it received two additional early-stage contracts for the US government.

- Cardinal Health (CAH) falls 5% after posting 4Q results and agreeing to buy Solaris Health from Lee Equity Partners and Solaris Health physician owners.

- Celanese (CE) drops 15% after the chemical manufacturer provided a disappointing 3Q profit forecast as management expects a softening demand across most key end-markets in the second half of the year.

- Hanesbrands (HBI) soars 41% after the Financial Times reported that Canada’s Gildan Activewear is nearing a deal to acquire the US underwear maker at an enterprise value approaching $5b.

- Intel (INTC) is up 2% after President Trump said his meeting with CEO Lip-Bu Tan “was a very interesting one.”

- Liquidia (LQDA) jumps 9% after the drugmaker reported revenue for the second quarter that topped the average analyst estimate.

- On Holding (ONON) gains 10% after the Swiss sportswear firm raised its FY sales outlook. The firm also reported estimate-beating results, seeing strong demand in all regions.

- PubMatic (PUBM) slides 29% after the ad-tech company forecast current-quarter revenue well below analyst estimates, with demand disrupted by a recent platform migration at a major demand-side platform client.

- Shift4 Payments Inc. (FOUR) climbs 4% after Jared Isaacman, its founder and executive chairman, bought $16.3 million of shares.

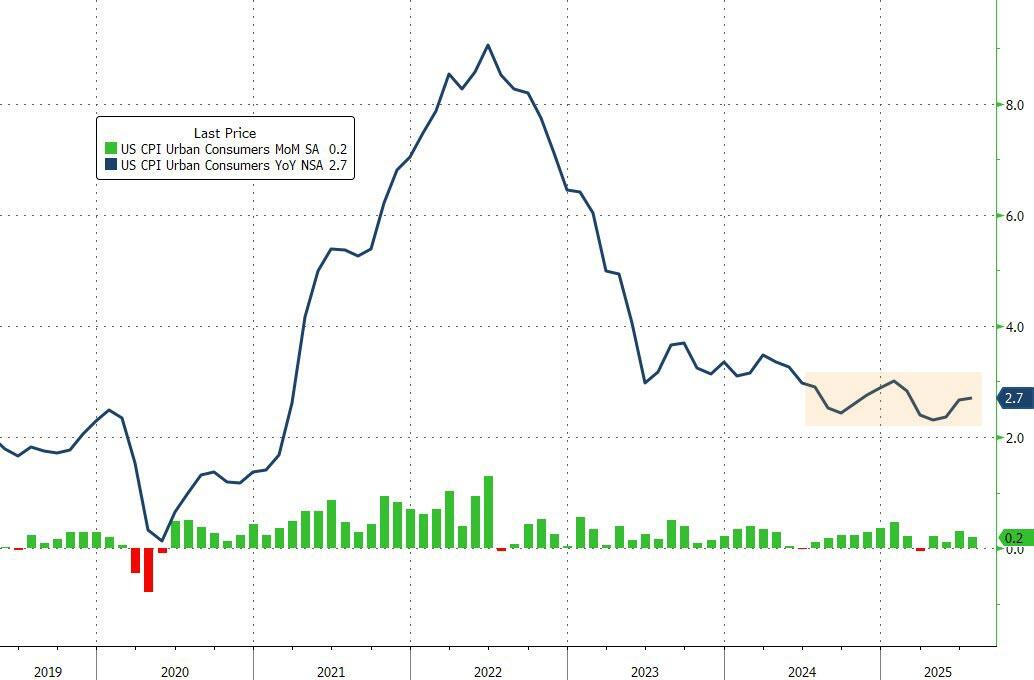

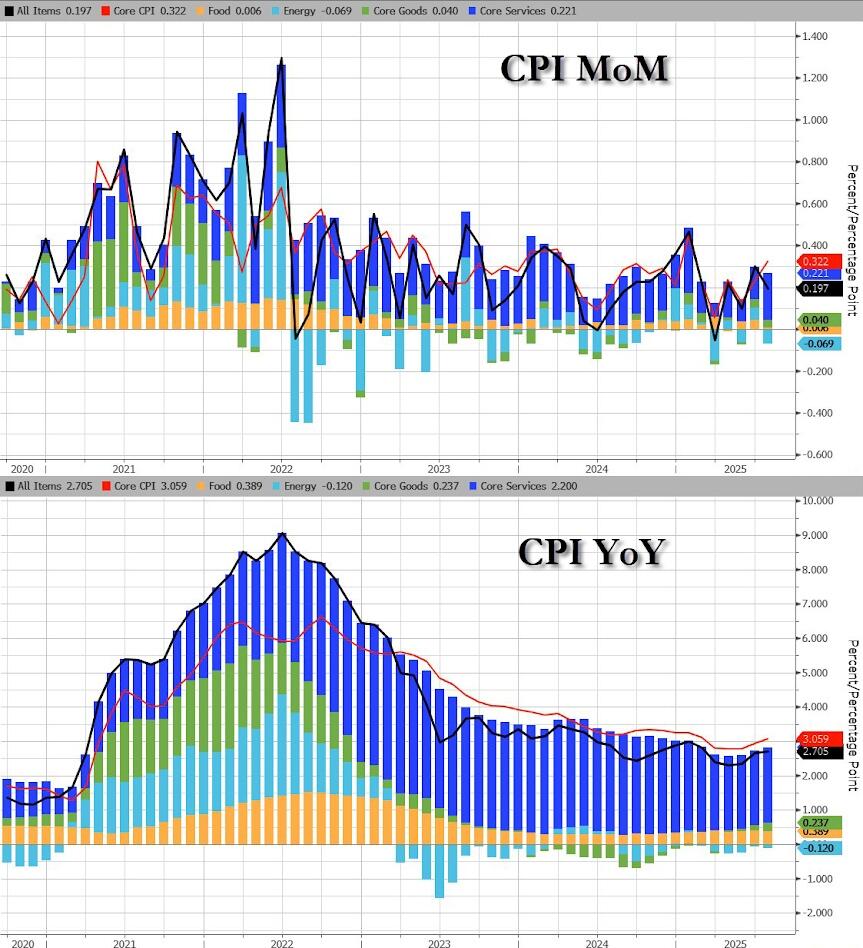

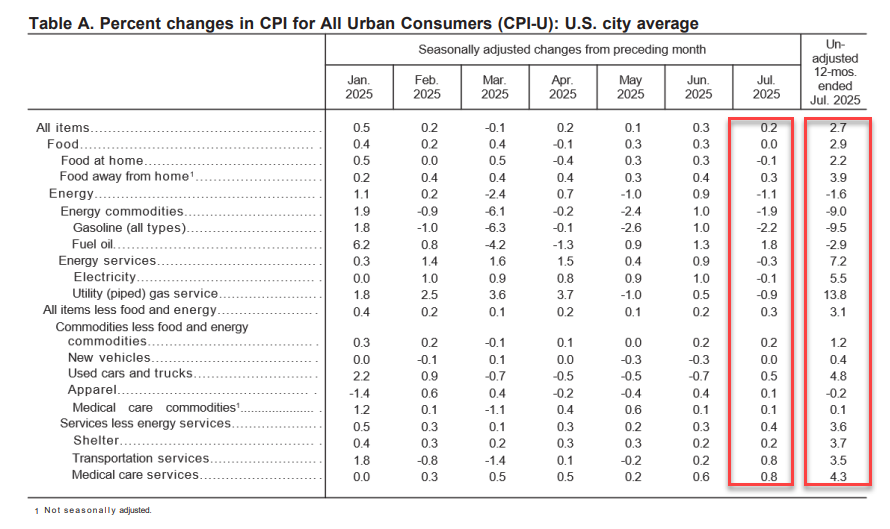

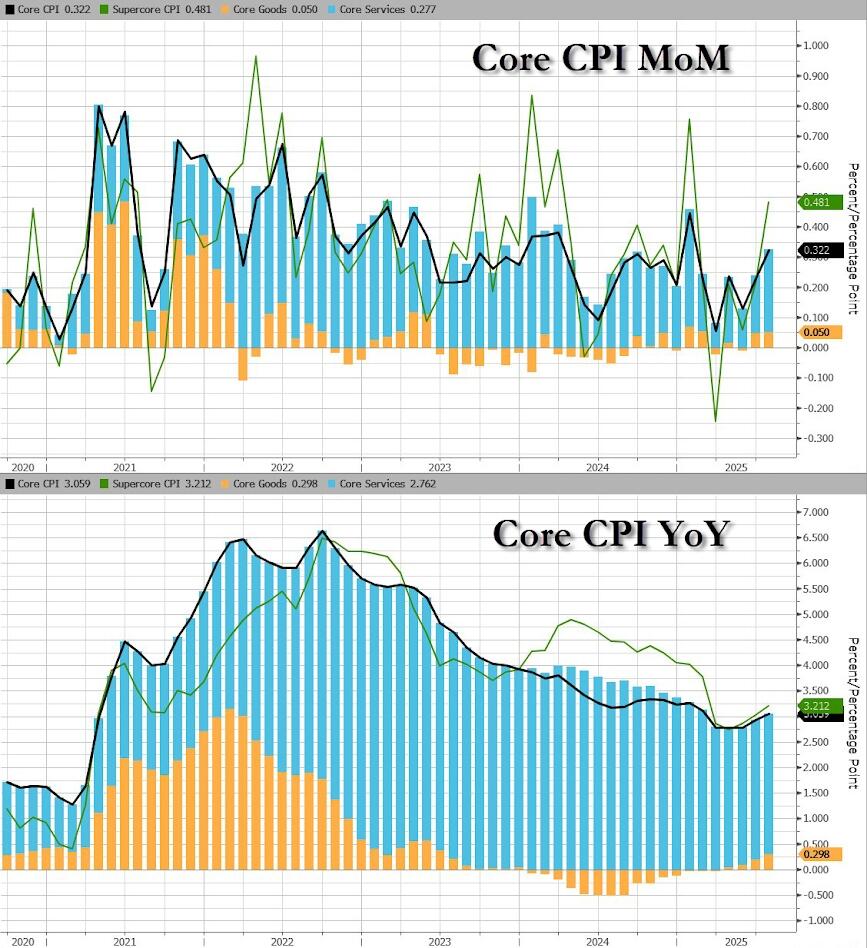

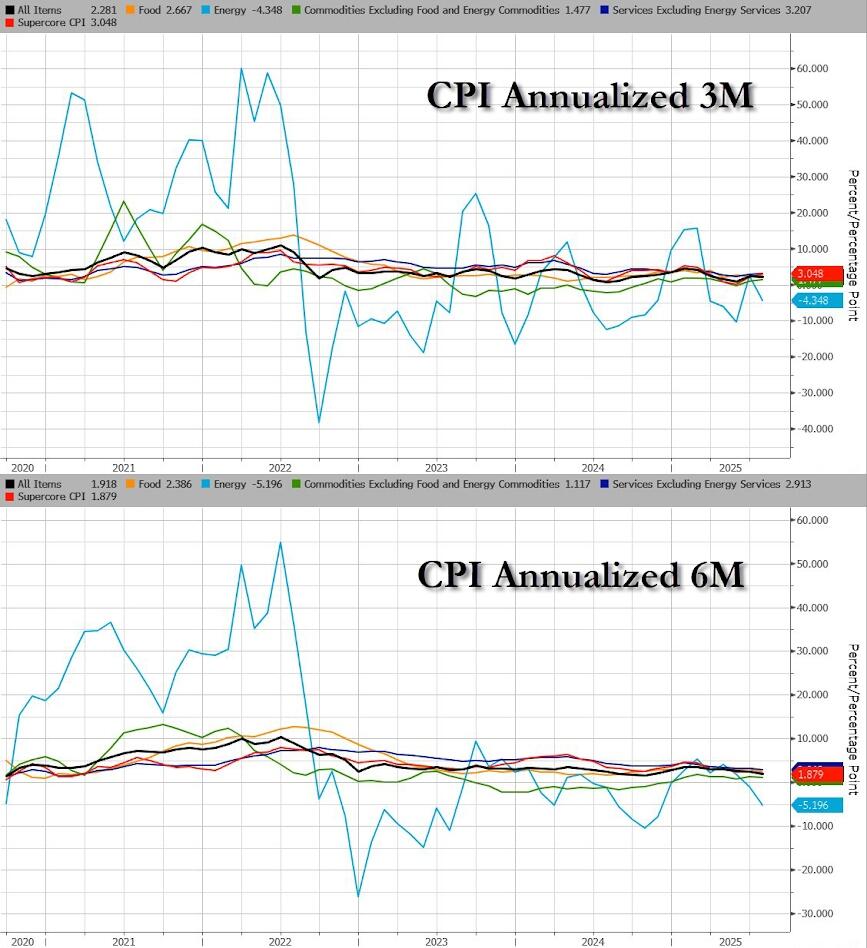

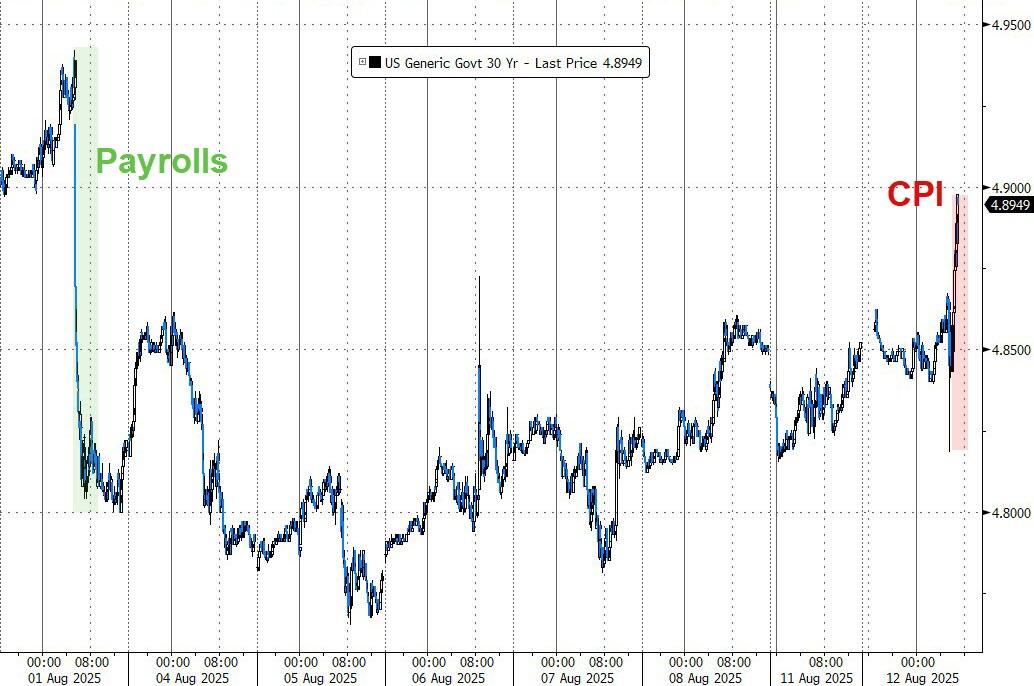

Today’s inflation report (full preview here) arrives after traders in recent weeks ramped up bets for Federal Reserve rate cuts this year, anticipating that officials will act to bolster a labor market showing signs of softening. Absent a shockingly hot number, the Fed is expected to cut rates next month. Still, investors will remain cautious to the risk of persistent price pressures and the potential for a stagflationary backdrop. Traders have priced in more than two rate cuts by December, with about an 80% probability of a quarter-point reduction next month. The core consumer price index, regarded as a measure of underlying inflation because it strips out volatile food and energy costs, is expected to show a 0.3% increase for July, compared to 0.2% in the previous month.

“Positive equity market sentiment over the past few months has been predicated in part on the Fed cutting rates,” said Daniel Murray, chief executive officer of EFG Asset Management. “If the CPI release causes the date of the first rate cut to be pushed out, there is clearly a risk that sentiment takes a hit.”

While price action could be skewed to the downside in the event of a hot print, there is also upside risk that investors might be overlooking, according to Goldman Sachs Group Inc. traders.

“What worries us is a rotation that could happen in the ‘market bullish’ scenario of a benign CPI,” said Shawn Tuteja, who oversees ETF and custom baskets volatility trading at the bank. “One way to hedge against that is buying cyclical calls, but another way in our view given levels and overall asymmetry, could be to strike some semis and AI hedges.”

Elsewhere, some investors and analysts also warned that Trump’s 90-day extension of the US-China trade truce could prolong uncertainty and pose a more persistent risk to inflation, clouding the outlook for Fed policymakers. “While it preserves the flow of goods under prior terms with 30% rate, it keeps the threat of them very much in place,” said Ahmad Assiri, a research strategist at Pepperstone. “For the Fed, this reinforces the difficulty of striking the right balance between supporting growth and containing inflation.”

European stocks rose before the key US inflation data. The Stoxx 600 rises 0.2%, led by energy, industrial and mining shares. US equity futures are little changed.

Earlier in the session, Asian equities advanced as global trade worries eased after Trump’s China tariff move. The MSCI Asia Pacific Index rose as much as 0.8%, led by Japanese shares which hit a record high after trading resumed following Monday’s holiday. Japanese and Korean chip stocks were given a boost by Trump’s signal he would be open to allowing Nvidia to sell a scaled-back version of its Blackwell AI chip to China.

In rates, treasuries are little changed ahead of July CPI data at 8:30am New York time, with UK and German yields higher after data including a smaller-than-expected drop in UK payrolls. US yields remain within 1bp of Monday’s closing levels with 10-year near 4.29%; UK and German 10-year counterparts are higher by 4bp and 1.4bp after a smaller-than-expected drop in payrolls prompted traders to trim bets on interest-rate cuts by the Bank of England this year.

In FX, the pound gains 0.3%, topping the G-10 leader board with the Swiss franc. The Aussie dollar underperforms after the RBA cut rates and trimmed its 2025 growth outlook.

UK 10-year yields rise 3 bps to 4.59%. The pound gains 0.3%, topping the G-10 leader board with the Swiss franc. The Aussie dollar underperforms after the RBA cut rates and trimmed its 2025 growth outlook. The Stoxx 600 rises 0.2%, led by energy, industrial and mining shares. US equity futures are little changed. Nvidia slips 0.3% premarket after

In commodities, WTI crude is steady near $64, and spot gold climbs $7 to $3,349/oz.

Looking at today’s calendar, US economic data slate includes the CPI print at 830a, and July federal budget balance at 2pm. Fed speaker slate includes Barkin (10am) and Schmid (10:30am). Lastly, notable earnings include CoreWeave and Circle Internet Group.

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini unchanged

- Russell 2000 mini +0.2%

- Stoxx Europe 600 +0.2%

- DAX -0.2%

- CAC 40 +0.3%

- 10-year Treasury yield -1 basis point at 4.28%

- VIX little changed at 16.26

- Bloomberg Dollar Index little changed at 1207.61

- euro little changed at $1.161

- WTI crude +0.1% at $64.03/barrel

Top Overnight News

- Beijing has urged local companies to avoid using Nvidia Corp.’s H20 processors, particularly for government-related purposes, complicating the chipmaker’s attempts to recoup billions in lost China revenue after the Trump administration reversed an effective US ban on such sales. Beijing’s worried about location-tracking and remote shutdown capabilities, which Nvidia has previously denied. BBG

- Trump posted that he met with Intel CEO Lip-Bu Tan along with Commerce Secretary Lutnick and Treasury Secretary Bessent, while he stated “The meeting was a very interesting one. His success and rise is an amazing story. Mr. Tan and my Cabinet members are going to spend time together, and bring suggestions to me during the next week.”

- Elon Musk accused Apple of favoring OpenAI in its app store and said xAI will take legal action. BBG

- US imports from China slowed sharply ahead of the Aug. 11 tariff deadline. Although the new 90-day delay agreement offers temporary relief, the drop in shipments signals potential risks to American growth and corporate margins. BBG

- Xi Jinping called for coordinated efforts against unilateralism and protectionism — language usually used by China to criticize US trade policy — in a phone conversation with Brazil’s President Lula da Silva. BBG

- Trump said that he plans to nominate E.J. Antoni, the chief economist at the Heritage Foundation, to lead the Bureau of Labor Statistics. Antoni, a longtime critic of the agency’s handling of jobs data, had the support of conservatives like former White House chief strategist Steve Bannon. The position requires Senate confirmation. WSJ

- Britain’s jobs market has weakened again, official data showed, with payrolls falling for a sixth month and vacancies dropping further, but wage growth stayed strong, underscoring why the Bank of England is so cautious about cutting interest rates (payrolled employees -8K in Jul, wages elevated at +5%). RTRS

- Australia’s central bank lowered rates by 25bp overnight (as expected), and signaled further easing going forward (“updated staff forecasts for the August meeting suggest that underlying inflation will continue to moderate to around the midpoint of the 2–3 per cent range, with the cash rate assumed to follow a gradual easing path”). RBA

- Intel’s stock rose premarket (INTC 3% pre mkt) after CEO Lip-Bu Tan appeared to reset his strained relationship with Trump during a White House meeting. The president called Tan’s success “amazing” and said discussions will continue. BBG

Trade/Tariffs

- China issued a statement on US economic and trade ties in which it stated that China will suspend tariffs for 90 days and will retain an additional 10% tariff rate, while it will adopt and maintain all necessary measures to suspend or remove non-tariff measures taken against the US.

- China updated its export control lists and noted firms can apply to trade with entities under the list and it halted measures on 12 US entities on the export list, while it said it will grant licences if exporters meet requirements and it is suspending adding some US firms to the export control list for 90 days.

- China urges firms not to use NVIDIA (NVDA) H20 chips in new guidance, according to Bloomberg

- China’s Commerce Ministry has launched an anti-dumping investigation into Canadian pea starch and announced preliminary investigation results on Canadian canola seed. The ministry also released preliminary findings on imports of halogenated butyl rubber from Canada, Japan, and India. Meanwhile, the Chinese Foreign Ministry urged the US to take practical steps to stabilise global chip supply chains.

- South Africa’s Trade Minister stated the country stands ready to utilise its trade remedy measures to safeguard and protect domestic industry.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks shrugged off the weak lead from Wall St and traded mostly higher with outperformance in Japan on return from the extended weekend and following a deluge of earnings, while participants also reflected on the recent US-China trade truce extension. ASX 200 eked slight gains and extended on record highs with only mild tailwinds seen after the RBA delivered a widely expected 25bps rate cut. Nikkei 225 surged on return from the long weekend and followed suit to the record-setting performance in the TOPIX with the index underpinned following a slew of earnings releases and recent currency weakness. Hang Seng and Shanghai Comp kept afloat following the confirmation of a 90-day extension to the US-China tariff truce with the new deadline set for November 9th.

Top Asian News

- Chinese President Xi held talks with Brazilian President Lula, with the call said to have lasted about an hour and both presidents highlighted willingness to identify new business opportunities between the two economies.

- US President Trump and South Korean President Lee are to hold a summit on August 25th where they will discuss economic cooperation and economic security partnership, as well as the evolving strategic alliance between the two countries.

- RBA cut the Cash Rate by 25bps to 3.60%, as expected with the decision unanimous, while it reiterated that inflation has continued to moderate and the outlook remains uncertain as well as noted that maintaining price stability and full employment is the priority. RBA stated that underlying inflation will continue to moderate to around the midpoint of the 2–3% range, with the cash rate assumed to follow a gradual easing path, and it noted that monetary policy is well placed to respond decisively to international developments if they have material implications for activity and inflation in Australia. Furthermore, it stated the cut was due to underlying inflation continuing to decline back towards the midpoint of the 2–3% range and labour market conditions easing slightly.

- RBA Governor Bullock stated there had been no discussions of a larger rate cut, while noting that current forecasts imply the Cash Rate may need to be lower to ensure price stability, with the Board to take decisions on a meeting-by-meeting basis and not ruling out back-to-back rate cuts. She added that the recovery in house prices has been gradual so far, though forecasts are dependent on further rate cuts, and without these, targets would likely be missed. Governor Bullock also said she places little emphasis on the neutral rate, while noting that if the Fed were to lower rates too quickly, it would have global implications. Furthermore, she highlighted that policy remains forward-looking, with the assumption that rates can continue to be lowered.

- Italy PM Meloni seeks to shrink Chinese holdings at key Italian companies, according to Bloomberg.

European bourses (STOXX 600 +0.3%) began the session firmer, and continue to hold this bias but in rangebound trade into US CPI. European sectors traded mostly in the green (bar Tech) for the entire morning, given the slightly upbeat tone ahead of CPI. Energy trades at the top of the pile with Basic resources nipping at its heels for most of the morning – the latter lifted by strength in underlying iron ore prices.

Top European News

- German investor confidence sinks as costs of trade deal hit home

- UK loses fewer jobs than expected, clouding path to rate-cut

FX

- USD is broadly flat vs. peers in the run-up to today’s eagerly anticipated US inflation report. Expectations are for core M/M inflation to rise to 0.3% from 0.2% with the Y/Y rate seen rising to 3.0% from 2.9%. On the Fed, Bloomberg reports that Fed Governor Bowman, Fed Vice Chair Jefferson, and Dallas Fed President Logan are now also in the running for the Chair position. Elsewhere, on the trade front, US President Trump has signed an Executive Order that will extend the tariff suspension on China for another 90 days, as expected. DXY is contained within Monday’s 98.03-99.67 range.

- EUR is steady vs. the USD as the narrative surrounding the Eurozone remains the same. That narrative being that the ECB is holding policy steady with inflation under control but mindful of any potential growth headwinds in Q3 as the impact of the US tariffs on the Bloc filters through into the data. Today’s ZEW deteriorated from the priors and also missed expectations, although it prompted no move in the EUR. EUR/USD has made its way back onto a 1.16 handle, but still some way off Monday’s best at 1.1675.

- JPY is fractionally weaker vs. the USD as Japanese participants returned to the market and sent the Nikkei 225 to a record high. Incremental macro drivers for Japan are lacking. USD/JPY has eclipsed Monday’s best at 148.25 with a current session high at 148.44.

- Cable is higher in the wake of the latest UK jobs report, which failed to show a marked deterioration in the labour market that some had been positioned for. The ILO unemployment rate held steady at 4.7%, employment change showed a larger-than-expected pick up to 238k from 134k, the contraction in HRMC payrolls change slowed to -8k from -26k and wage growth came in a touch softer than forecast on a headline basis. Overall, the takeaway is that the UK labour market is softening, but the rate of change appears to be slowing. Cable has advanced further on a 1.34 handle but is still shy of Monday’s 1.3477 peak.

- AUD is the marginal laggard across the majors in the wake of the latest RBA policy announcement, which saw the central bank pull the trigger on a widely expected 25bps rate cut. The decision to do so was unanimous, and the accompanying policy statement reiterated language that inflation has continued to moderate and the outlook remains uncertain. The central bank also simultaneously released its Quarterly Statement on Monetary Policy which showed a downgrade to the estimate of Australia’s long-run productivity growth to 0.7% from 1.0% and with trend GDP growth now seen around 2.0%, down from 2.25%. AUD/USD has slipped onto a 0.64 handle with a session low at 0.6494.