099 H DEUTSCHE BANK AG 75

118 C MACQUARIE FUTURES US 18

118 H MACQUARIE FUTURES US 200

285 C NANHUA USA-HK 52

363 H WELLS FARGO SECURITI 4

435 H SCOTIA CAPITAL (USA) 60

624 H BOFA SECURITIES 499

661 C JP MORGAN SECURITIES 476

709 C BARCLAYS 11

732 C RBC CAP MARKETS 16

905 C ADM 13

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 712 CONTRACTs NOTICES FOR 71200 OZ or 1.4805 TONNES

total notices so far: 27,680 contracts for 2,768,000 OR 86.096 tonnes)

SILVER NOTICES:4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month : 1720 CONTRACTS (NOTICES) for 8.600 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 23.845 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 55,000 OZ QUEUE JUMP//NEW STANDING REMAINS AT 8.705 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 3.527 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE PRIOR: 5.4432 TONNES EX FOR RISK/AUG 7 AND AUG 11: 2.413 TONNES EX FOR RISK AND NOW YESTERDAY’S AUG. 12 OF 2.637 TONNES EX FOR RISK //NEW STANDING ADVANCES TO 92.258 TONNES OF GOLD +10.4932 TONNES EX.FOR RISK = 102.7512 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 87.83 TONNES QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1959 CONTRACTS OI TO 156,432 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 300 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 300 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 370 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1989 CONTRACTS AND ADD TO THE 300 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 2259 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.68 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 11.295 MILLION PAPER OZ

OCCURRED WITH OUR $0.68 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 17.55 PTS OR 0.48%

//Hang Seng CLOSED UP 643.99 PTS OR 2.58%

// Nikkei CLOSED UP 556.50 PTS OR 1.30% //Australia’s all ordinaries CLOSED DOWN 0.52%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1737 OFFSHORE CLOSED UP AT 7.1774/ Oil DOWN TO 62.91 dollars per barrel for WTI and BRENT UP TO 65.92 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1737 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1774 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6,535 CONTRACTS TO 446,152 OI DESPITE OUR GAIN IN PRICE OF $2.65 WITH RESPECT TO TUESDAY’S // TRADING.. WE LOST LITTLE NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2375 ). WE HAD CONSIDERABLE T.A.S. LIQUIDATION //TUESDAY TRADING AS WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3706 CONTRACTS (OR 11.527 TONNES). WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK TUESDAY.

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY:

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AS MENTIONED ABOVE: TONIGHT WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK!

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST;

EARLY THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE FOR AUGUST OF A MONSTER 1750 CONTRACTS FOR 175,000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. WITH ALL THE CHAOS AT THE COMEX IT WAS NO SURPRISE THAT THEY ISSUED THEIR SECOND EXCHANGE FOR RISK, AUG 10 TOTALLING 776 CONTRACTS OR 77,600 OZ (2.418 TONNES).MUCH TO MY ANGER TONIGHT, THE CME ANNOUNCED ITS 3RD EXCHANGE FOR RISK OF 848 CONTRACTS TOTALLING 84,800 OZ OR 2.637 TONNES.

THUS THE TOTAL FOR AUGUST IS 3374 CONTRACTS OR 337,400OZ OR 10.4932 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS. THE RECEPIENT OF THIS LARGESS IS PROBABLY NOW THE BANK OF ENGLAND AS WE HAVE JUST LEARNED THAT THE FRBNY HAS RETURNED ONLY 14,000 OZ AS THEIR LOANS TO THE BIS REMAIN AT 34+ TONNES.(JULY 31 FIGURES) IT SEEMS NOW THAT THE BANK OF ENGLAND IS IN QUITE A HURRY TO GET ITS GOLD BACK!!

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 3 ISSUANCES FOR A MONSTER 3374 CONTRACTS OR 337,400 OZ ( 10.4932 TONNES)

AS I EXPLAINED ABOVE,:THE RECPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 4160 CONTRACTS DESPITE OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 1,949 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED TWO WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS A QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS TODAY’S HUGE QUEUE JUMP OF 3.527 TONNES +10.4932 TONNES EX FOR RISK (3 ISSUANCES) //NEW STANDING 102.7512 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 235 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NONE COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 3.527 TONNES TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE + SATURDAY’S HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES AND THEN TODAY;S AUGUST 12: 2.637 TONNES:/NEW STANDING ADVANCES TO 102.7512 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2375 EFP CONTRACT WAS ISSUED: : /DEC 2375 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2375 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY

- MONTH END SPREADERS WILL APPEAR ON THE LAST WEEK OF AUGUST.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A FAIR SIZED SIZED 1949 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S FIRST THREE ISSUANCES OF EXCHANGE FOR RISK FOR 10.4932 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S MONSTER QUEUE JUMP OF 3.527 TONNES TO WHICH WE ADD THURSDAY’S HUGE 5.4432 EXCHANGE FOR RISK, SATURDAY’S STRONG 776 CONTRACT ISSUANCE (77600 OZ) FOR 2.413 TONNES AND THEN YESTERDAY AUGUST 12 FOR 2.637 TONNES TOTAL EX FOR RISK AUGUST = 10.4932 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

92.258 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

EQUALS

102.7512 TONNES TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $2.65/ /) BUT WERE SUCCESSFUL IN KNOCKING OFF A FEW NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION ///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID THIS WEEK.

WEDNESDAY MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: THREE SO FAR, AUGUST 7 AT 3374 CONTRACTS FOR 337,400 OZ (10.4932 TONNES OF GOLD) WITH TODAY’S ISSUANCE OF 848 CONTRACTS FOR 84800 OZ OR 2.637 TONNES. TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 10.4932 TONNES

THUS 92.258 TONNES OF GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 10.4932 TONNES = 102.7512 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE LOST A STRONG SIZED TOTAL OF 11.527 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD LAST THURSDAY’S RECORD BREAKING QUEUE JUMP OF 10.8775 TONNES OF GOLD ON TOP OF YESTERDAY’S HUGE 1.7604 TONNES QUEUE JUMP AND THEN TODAY;S MASSIVE QUEUE JUMP OF 3.527 TONNES TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK/PRIOR FOR 10.4932 TONNES FOR RISK//NEW STANDING ADVANCES TO 102.7512 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR SMALL GAIN IN PRICE TO THE TUNE OF $2.65

WE HAD A SMALL 454 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 4160 CONTRACTS OR 416000 0Z (12.99 TONNES)

confirmed volume TUESDAY 220,255 contracts// fair

speculators have left the gold arena

END

INITIAL GOLD COMEX

AUGUST CONTRACT MONTH

AUGUST13 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entry . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 712 notice(s) 71,200 OZ 1.4805 TONNES |

| No of oz to be served (notices) | 1981 contracts 198,100 OZ 6.162TONNES |

| Total monthly oz gold served (contracts) so far this month | 27,680 notices 2,768,000 oz 86.096 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entry

adjustments: i) Brinks 96,453.000 oz (3000 kilobars)//dealer to customer

ii) Customer to dealer Loomis: 2300.29 oz

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 2693 CONTRACTS FOR A GAIN OF 781 CONTRACTS

WE HAD 353 CONTRACTS SERVED ON TUESDAY SO WE GAINED A HUGE SIZED 1134 CONTRACTS OR 113,400 OZ OF GOLD (3.527 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND.. THIS ALSO REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD AND THEIR APPETITE FOR THIS GOLD IS UNABATED!

SEPT LOST 223 CONTRACTS TO 5461

OCTOBER LOST 1529 CONTRACTS DOWN TO 62,429

We had 712 contracts filed for today representing 71,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 712 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 476 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (27,680 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 2693 CONTRACTS) minus the number of notices served upon today (712 x 100 oz per contract) equals 2,966,100 OZ OR 88.730TONNES TO WHICH WE ADD OUR THREE ISSUANCES OF 10.4932 TONNES OF EXCHANGE FOR RISK/AUG 7 , 11 AND 12TH = 102.7512 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (27,680 x 100 oz +we add the difference for front month of AUGUST (2693 OI} minus the number of notices served upon today (712 x 100 oz) which equals 2,966,100 OZ OR 92.588 TONNES + 10.4932 TONNES EX FOR RISK = 102.7512 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 102.7512 TONNES WHICH IS VERY STRONG FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,019,394.662 oz 62.811 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,622,416.431 oz

TOTAL REGISTERED GOLD 21,380,931.888 or 665.036 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,271,484.431 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,396,618 oz ((REG GOLD- PLEDGED GOLD)= 603.331tonnes // ( a bid drop of 10 tonnes

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE AUGUST 2025 SILVER CONTRACT//INITIAL

AUGUST 13 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 ENTRY i) Out of Loomis: 385.812 oz (12 kilobars) total withdrawal 385.312 oz |

| Deposits to the Dealer Inventory | 1 ENTRY into Asahi dealer 5,799.334 oz total deposit/dealer 5799.334 oz |

| Deposits to the Customer Inventory | 0 DEPOSIT ENTRY/CUSTOMER ACCOUNT |

| No of oz served today (contracts) | 4 CONTRACT(S) (20,000 OZ |

| No of oz to be served (notices) | 21 contracts (0.150 MILLION oz) |

| Total monthly oz silver served (contracts) | 1720 Contracts (8.60 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

1 ENTRY

into Asahi dealer 5,799.334 oz

total deposit/dealer 5799.334 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

0 DEPOSIT ENTRY/CUSTOMER ACCOUNT

700 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

1 ENTRY

i) Out of Loomis: 385.812 oz

(12 kilobars)

total withdrawal 385.312 oz

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 190.400 MILLION OZ//.TOTAL REG + ELIGIBLE. 507.041 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 25 OPEN INTEREST CONTRACTS FOR A LOSS OF 18 CONTRACTS. WE HAD 29 CONTRACTS SERVED ON TUESDAY SO WE GAINED 11 CONTRACTS OR AN ADDITIONAL 55,000 OZ WILL STAND AS THEY ENTERTAINED A HUGE QUEUE JUMP

SEPTEMBER LOST 4376 CONTRACTS DOWN TO 77,668 CONTRACTS.

OCTOBER GAINED 130 CONTRACTS TO 667

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 4 or 20,,000 oz

CONFIRMED volume; ON TUESDAY 103,055 HUGE//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1720 X5,000 oz = 8.600 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (25) AND the number of notices served upon today (4 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1720) Notices served so far) x 5000 oz + OI for the front month of AUGUST(25) minus number of notices served upon today (4)x 5000 oz equals silver standing for the AUGUST contract month equating to 8.705 MILLION OZ .

New total standing: 8.705 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.400 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/507.041 million. 41.47%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 964.22 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 485.462 MILLION OZ//

Trump v Putin in Alaska: Who has the upper hand?

It’s the Art of the Deal versus Putin’s patience. Place your bets!

| Alasdair MacleodAug 13 |

National Security Archive

MacleodFinance Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

President Trump is meeting President Putin in Alaska this coming Friday, to seek a truce on Ukraine. The back story is that Trump wants to extricate himself from America’s embarrassing failure to undermine Russia by means of a proxy war through Ukraine. Deep state operatives like Victoria Nuland (remember her?) spearheaded the Maidan revolution in 2013, following which Russia took Crimea. But this was almost certainly an extension of US deep state operations from the Colour revolution of 2004 onwards.

The context of US perfidy is an original commitment by Secretary James Baker to Michail Gobachev that NATO would not expand “one inch eastwards”. Will Putin trust the Americans? Highly unlikely.

The Americans have a record of reneging on commitments, so anything Trump says will almost certainly be taken with a pinch of salt. Apart from the predictable political propaganda, nothing substantive is likely to be come out of this meeting. In which case, it will be seen in the rest of the world as another Trump failure.

Trump must be acutely aware that he has to succeed in calling a halt to the war in Ukraine. He has even threatened BRICS countries and others buying Russian oil with additional tariffs. But his capriciousness with respect to tariffs has only undermined US credibility among the potential sanctioned and America’s enemies. And surely, Putin and China know that far from punishing BRICS, America is increasingly isolating herself from world trade and her influence is declining with it.

As Sun Zu put it, why interrupt the enemy when he is making all the mistakes? China, Russia, and their partners in trade are already advancing their plans to replace the dollar and isolate a belligerent America. They understand that the dollar is entering the final throes of its collapse as a fiat currency and have a plan B centred on a network of Shanghai Gold Exchange vaults in key jurisdictions, where gold will be exchangeable only for renminbi.

The deliciousness to come from what promises to be a half-baked Alaska is the impotence of the European Union and its out-of-touch leadership.

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

The gold swaps by the Frbny remains at 34 tonnes of gold having fallen slightly by only 14,000 oz

Not happy with this!!

(zerohedge)

BIS gold swaps held steady at 34 tonnes in July, GATA’s Robert Lambourne reports

Submitted by admin on Mon, 2025-08-11 20:50 Section: Daily Dispatches

8:55p ET Monday, August 12, 2025

Dear Friend of GATA and Gold:

Gold swaps undertaken by the Bank for International Settlements, the central bank of the central banks and often their broker in the gold market, fell slightly in July, by about 14,000 ounces, but, rounded off, remained at June’s 34-tonne mark, according to GATA consultant Robert Lambourne.

The information can be calculated from the bank’s monthly statement of account for July, published today:

The report implies that the bank was not recruited to intervene much in the gold market in June on behalf of its member central banks and that there continues to be little interest among them in incurring more gold liabilities or in letting their metal get far from home.

The report written by Lambourne on July 1 —

— provides some history on the swap transactions and their volatility since the bank in 2010 made it possible for its gold swaps to be calculated.

As recently as January 2022 the bank’s swaps exceeded 500 tonnes but they have fallen sharply since, indicating a change of policy toward or outlook on gold, a trend that seems to have correlated with increasing central bank acquisitions and repatriations, along with gold’s rising price.

Nevertheless, the BIS has a well-placed confidence that no mainstream financial news organization will ever ask it to explain the purposes of the swaps and to identify the parties to them, lest gold cease being the immensely powerful secret knowledge of the financial universe.

CHRIS POWELL, Secretary/Treasurer

END

ROBERT LAMBOURNE…

Global ‘mining mafia’ feeds China’s appetite for gold, investigation shows – The Washington Post

Chris and Harvey,

It certainly feels as if China is getting its hands on as much gold as it can now and is not really trying to hide this, but maybe is getting a little nervous about it again. This article highlights the trend of supporting illicit mining and highlights activities in Indonesia.

Over the last 6 months I’ve regularly checked DeepSeek for estimates of China’s gold holdings and it’s almost as if a change in approach has happened again.

A few weeks ago it was estimated at c 40,000 tonnes and the latest estimate copied in the Appendix below is less than half of this, but it’s interesting that there is reporting of the illicit trade highlighted in the Washington Post article. It seems there is sensitivity to being seen to support illicit activity.

The big difference in the totals that DeepSeek reports always comes down to the level of privately held gold and all the evidence points to an acceleration of accumulation in the last 2 to 3 years. The high estimate that I’ve seen is c30,000 tonnes.

Almost regardless of the reported estimates it’s clear that China is buying gold rapidly.

If the USA is going to reset the gold price higher then to my mind, it’s inevitable that it needs some sort of accommodation with China.

The good news is that the BIS reports the Chinese total non financial debt to GDP ratio is 287% versus a figure of 249% for the USA. Hence China needs a gold price reset too in order to write off some of its debt, especially related to its ill-fated property overbuild.

As Chris will recall, GATA published a note several months ago suggesting that the USA needed a gold price reset to c$130,000 to get the non financial debt to GDP ratio back to pre 1980 levels. I am now seeing videos suggesting that a gold revaluation to $150,000 may be required. Doing anything remotely close to this, even via a series of resets, is going to require Chinese agreement.

We live in interesting times.

Bob

Appendix – DeepSeek on Chinese gold holdings today

—

**China’s Total Gold Holdings Estimate (Mid-2025)**

### **Official State Reserves (People’s Bank of China – PBOC)**

– **Holdings**: 2,300 tonnes (as of June 2025).

– **Recent Activity**: Added 2 tonnes in July 2025 (ninth consecutive month of purchases).

– **Strategic Context**: Gold represents 6.7% of China’s foreign reserves, driven by diversification from the U.S. dollar and geopolitical hedging.

### **Private Sector Holdings**

Includes retail investment (bars/coins), jewelry, and gold-backed financial products:

– **Shanghai Gold Exchange (SGE) Withdrawals**: ~1,200–1,300 tonnes projected for 2025 (seasonally adjusted).

– **Gold-Backed ETFs**: 198 tonnes (May 2025).

– **Retail & Jewelry**: Estimated 500–700 tonnes annual investment demand; 600–800 tonnes jewelry (weakened by high prices).

– **Total Private Holdings (Cumulative)**: 12,000–14,000 tonnes (based on SGE and World Gold Council data).

### **Mining Sector Inventories**

– **Annual Production**: ~350 tonnes (China is the world’s top producer).

– **Above-Ground Inventories**: 150–200 tonnes (working stocks held by major miners like Zijin Mining and Shandong Gold).

– **Illicit Mining**: Adds ~570 tonnes annually (largely unreported, enters global markets covertly).

### **Total Estimate**

| **Category** | **Tonnes** |

|———————|——————|

| Official Reserves | 2,300 |

| Private Holdings | 12,000–14,000 |

| Mining Inventories | 150–200 |

| **TOTAL** | **14,450–16,500**|

### **Key Caveats**

1. **Unreported Stocks**: Illicit mining and unofficial imports may add 500+ tonnes annually (untraceable).

2. **State Secrecy**: Analysts speculate PBOC’s actual reserves could be higher than reported.

3. **Market Volatility**: High gold prices ($3,380/oz in July 2025) may slow private demand.

### **Sources & Methodology**

– PBOC monthly disclosures (latest: June 2025).

– Shanghai Gold Exchange (SGE) withdrawal data.

– World Gold Council (WGC) reports and miner financial statements.

– Industry estimates for illicit mining (U.N. Trade Database, NGO reports).

end

Ultra-wealthy are piling into a centuries-old gold trade in Asia

Submitted by admin on Tue, 2025-08-12 11:43 Section: Daily Dispatches

By Diana Li and Sybilla Gross

Bloomberg News

via The Business Times, Singapore

Tuesday, August 12, 2025

HONG KONG — In Asia’s ultra-wealthy circles, some family offices are now bypassing the middlemen and jumping into the gold business itself. They are financing, shipping, and flipping bullion like traders.

Take Cavendish Investment, a multi-family office run by the former chairman of a Hong Kong jewelery company, which is allocating roughly a third of its portfolio this year to the physical gold trade, going a step beyond index trackers and vault holdings.

Precious metals dealers J. Rotbart & Co. and Goldstrom are also trading with the region’s ultra-rich clans.

Cavendish sources gold from small-scale mines in Kenya and elsewhere in Africa, flies it to Hong Kong, refines it, and sells it at market prices to wealthy clients across Asia and to Chinese strategic buyers. If this sounds like a 19th-century trading house, that’s about right. …

… For the remainder of the report:

end

Gold Reserve, Vitol battle for Citgo’s parent before sale hearing

Submitted by admin on Tue, 2025-08-12 16:22 Section: Daily Dispatches

By Marianna Parraga

Reuters

Monday, August 11, 2025

HOUSTON — Subsidiaries of miner Gold Reserve and commodities trader Vitol are nearing the finish line in a fiercely contested U.S. court-organized auction that will determine control of Venezuela-owned U.S. refiner Citgo Petroleum, according to two sources with knowledge of the process and court filings.

A court officer overseeing the bidding round last month recommended a $7.4-billion offer by a group led by a unit of Bermuda-based Gold Reserve as the auction’s winner, out of a total of five bids submitted, including one by a Vitol subsidiary. Delaware Judge Leonard Stark is expected to choose the winner after a final sale hearing on August 18

The decision will determine control of the crown jewel of Venezuela’s overseas assets, the seventh-largest U.S. refiner.

Despite Gold Reserve’s leadership status, its bid faces objections from parties in the case and holders of a Venezuelan bond, some of whom the Vitol unit is seeking to strike a deal with, in a move that could shake up the auction again. …

… For the remainder of the report:

end

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 235

5. COMMODITY REPORT..COFFEE

Coffee Analyst Warns Brazil Frost Could Deliver “Death Blow” To 2026 Harvest

Wednesday, Aug 13, 2025 – 02:45 AM

Maja Wallengren, Danish-born independent coffee market reporter and founder of SpillingTheBean, reports that severe frost has struck key coffee-producing areas in Brazil, including the entire Cerrado Mineiro region and parts of Southern Minas.

Wallengren warned that this “frost damage” event could be the “death blow” to the 2026 harvest, with production estimates now around 54 to 58 million bags versus prior estimates near 70% of capacity.

Given Brazil’s position as the world’s largest coffee producer, adverse weather conditions represent a potentially bullish catalyst for coffee futures in New York and warrant close market monitoring.

Here’s the report from Wallengren, which was first published on X:

BREAKING #KC BRAZIL FROST DAMAGE continues to be confirmed across ALL of Cerrado Mineiro #coffee region, and also across MANY municipalities in Southern Minas and parts of SP/AM, and REPEATING as @SpillingTheBean has said MANY TIMES over the last month, even if the physical and visible damage to coffee trees, farms and regions may appear to be less right now than the July-2021 frosts four years ago, the STRESS IMPACT on trees and farms ahead of the 2026 flowering is MASSIVELY more severe now than four years ago, as most Brazilian coffee growers have NOT YET RECOVERED from the last 5 years of non-stop weather disasters, and the ENTIRE BRAZIL arabica coffee park is SEVERELY weakened and fragile compared to 4 years ago, hence the 2026 harvest was already SEVERELY compromised to a max crop potential of 70% BEFORE the latest and ongoing COLD FRONT and FROST started to move across the main MG coffee belt and this current frost development is THE DEATH BLOW to the 2026 harvest which in VERY BEST case scenario at this point will be able to produce a MAX of 54M-58M bags !!

The Cerrado Mineiro region is a major coffee-growing area in Brazil, but its contribution to global coffee output is relatively small.

Here’s how it breaks down:

- The Cerrado Mineiro region produces about 5 million bags of coffee annually.

- Brazil, as a country, supplies around 35 to 40% of the world’s coffee.

- Brazil’s total output is around 64 million bags (based on around 37% share of about 60 million bags of global production).

- So, Cerrado Mineiro probably accounts for about 7 to 8% of Brazil’s coffee, which corresponds to roughly 2 to 3% of global coffee production.

Commenters on Wallengren’s post expressed surprise that coffee futures showed little reaction to the news. September arabica coffee in New York traded flat.

Will it take a few days for coffee desks to digest the problem?

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 17.55 PTS OR 0.48%

//Hang Seng CLOSED UP 643.99 PTS OR 2.58%

// Nikkei CLOSED UP 556.50 PTS OR 1.30% //Australia’s all ordinaries CLOSED DOWN 0.52%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1737 OFFSHORE CLOSED UP AT 7.1774/ Oil DOWN TO 62.91 dollars per barrel for WTI and BRENT UP TO 65.92 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1737 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1774 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1737 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1774

HANG SENG CLOSED UP 643.99 PTS OR 2.58%

2. Nikkei closed UP 556.50 PTS OR 1.30%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 97.47/ EURO RISES TO 1.1728 UP 50 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.517//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.23…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6971/Italian 10 Yr bond yield DOWN to 3.502 SPAIN 10 YR BOND YIELD DOWN TO 3.250%

3i Greek 10 year bond yield DOWN TO 3.351

3j Gold at $3365.20 Silver at: 38/56 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 63 /100 roubles/dollar; ROUBLE AT 80.07

3m oil (WTI) into the 62 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.23// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.517% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8025 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9410 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.256 DOWN 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.841 DOWN 5 BASIS PTS/

USA 2 YR BOND YIELD: 3.718 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.74

10 YR UK BOND YIELD: 4.608 DOWN 2 PTS

10 YR CANADA BOND YIELD: 3.435 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.969 UP 0 PTS

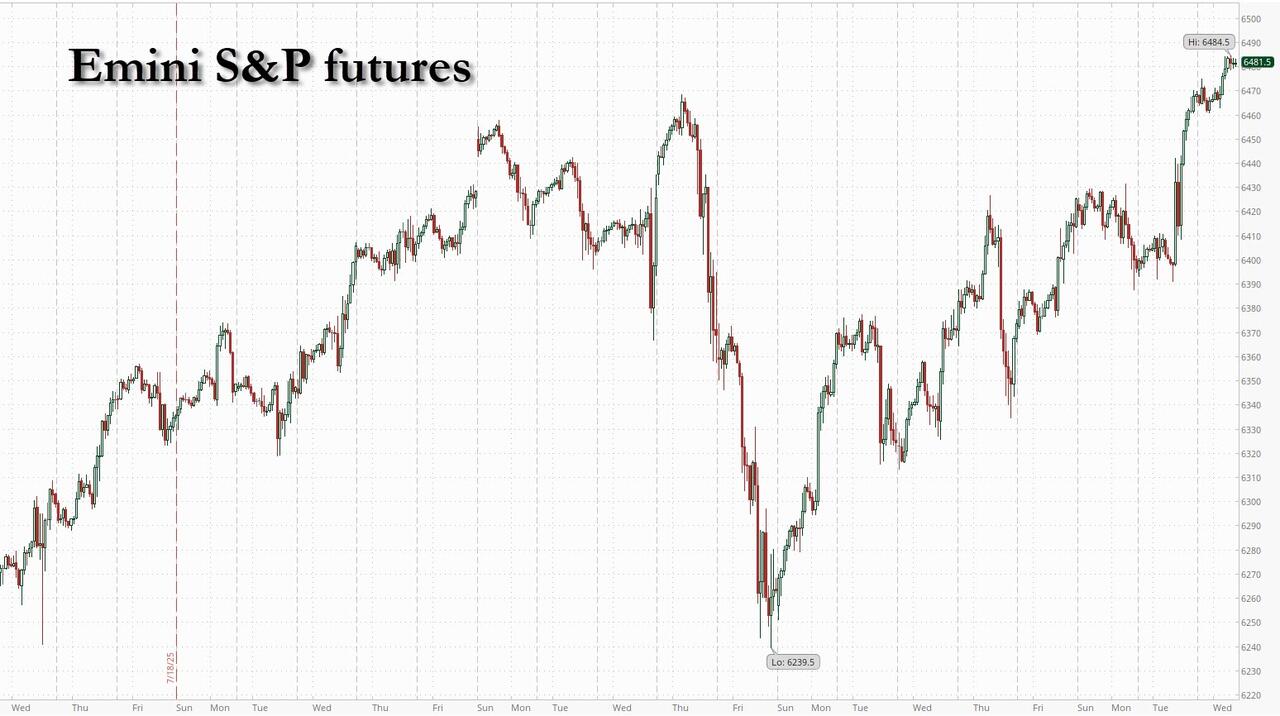

2a New York OPENING REPORT

Futures Trade At All-Time High As Global Market Euphoria Goes To 11

Wednesday, Aug 13, 2025 – 08:36 AM

US equity futures are higher led by small caps (again) as the CPI print induces further short covering ahead of a now certain September rate cut, and a beta chase. As of 8:15am, S&P 500 and Nasdaq 100 futures were 0.2% higher after both indexes closed at fresh record highs on Tuesday, but were comfortably outpaced by the Russell 2000 index, as smaller companies were lifted by a largely benign inflation reading. Pre-mkt, Mag7 and semis are higher with Cyclicals outperforming Defensives, ex-Energy. Bond yields are lower as the curve bull flattens and USD weakens; the market strengthens its view on rate cuts in Sep, Oct, and Dec. Bessent calls for a 50bp cut in Sep. Today’s macro data focus is on mtge apps ahead of tmrw’s PPI which should help solidify PCE views.

In premarket trading, Mag 7 stocks were mostly higher (Tesla +0.4%, Meta +0.2%, Alphabet +0.2%, Microsoft +0.09%, Amazon +0.1%, Apple +0.1%, Nvidia -0.2%).

- 180 Life Sciences Corp. (ATNF) is extending share price gains on Wednesday, rising 51%. The company rose 207% on Tuesday after announcing that it holds 82,186 ETH tokens.

- Brinker International Inc. (EAT) rises 9% after fourth-quarter earnings beat expectations with the Chili’s owner expecting that momentum to carry through in the next fiscal year, issuing an outlook eclipsing analyst predictions.

- Cava Group (CAVA) sinks 24% after the fast casual chain cut its restaurant comp sales forecast for the full year.

- CoreWeave (CRWV) is down 9% after posting steeper losses as it continued to build to meet demand from AI developers.

- Hanesbrands Inc. (HBI) falls 8% after Gildan Activewear agreed to buy the US underwear maker for about $2.2 billion in cash and stock, in its largest ever acquisition.

- Intapp Inc. (INTA) rises 22% after the software services company reported fourth-quarter results that beat expectations and gave an outlook that is seen as strong. Annual recurring revenue is seen as a highlight of the report. It also announced a stock repurchase program of up to $150 million.

- KinderCare (KLC) tumbles 18% after the childhood-education company posted disappointing results for the second quarter, citing a softer-than-anticipated enrollment and lowering its outlook for the full year. The results prompted a downgrade at Barclays who says the 2Q miss was “the final straw for us.”

- Lumentum (LITE) climbs 3% after the maker of optical and photonic products reported fourth-quarter results that beat expectations, prompting an upgrade.

- SimilarWeb (SMWB) rises 18% after the web services company reported second-quarter revenue that beat expectations and raised its full-year forecast for adjusted operating profit.

- Venture Global Inc. (VG) jumps 10% after it prevailed over oil giant Shell Plc in an arbitration case over the sale of cargo from its first export plant.

- Webtoon (WBTN) gains 30% after the online comics company announced a deal with Walt Disney to bring about 100 series to its English-language app.

Stocks were set for another day of record highs, as money markets suggest a September Fed interest rate cut is all but nailed on after a goldilocks CPI report that showed less tariff price pressures. The data has bolstered bets that the Fed will resume rate cuts next month and act more aggressively to shield a labor market showing signs of strain. At the same time, the VIX gauge hits its lowest level this year as optimism over a softening rate stance is further buoyed by easing global trade tensions and a significantly stronger-than-expected US earnings season. Swaps are pricing in about a 95% chance of a quarter-point cut in September, up from about 80% before Tuesday’s inflation data, with at least three more similar moves expected by June.

“The bull case remains a convincing one, with earnings growth solid, and a cooler tone on trade continuing to prevail, all the while dovish policy expectations help to provide a cushion against any worries that the economy may be softening,” said Michael Brown, senior research strategist at Pepperstone.

US Treasury Secretary Scott Bessent told Bloomberg TV that rates should likely be 150-175 basis points lower. “We could go into a series of rate cuts here, starting with a 50 basis-point rate cut in September,” he said.

US equities have staged an astonishing rebound from their April lows, when US President Donald Trump’s tariffs upended markets. The S&P 500 is closing in on a 10% advance for the year, with most of the fresh gains coming in the past two months.

The volatility that has defined much of this year’s trading has eased, with the VIX falling to its lowest level since December. Treasury market swings have also subsided, as the ICE BofA MOVE Index, a measure of expected yield fluctuations, dropped to its lowest since January 2022.

“Quite simply there is a momentum drive higher here,” said Guy Miller, chief market strategist at Zurich Insurance Co. “The US economy is in stronger shape than many had expected and the risk of recession is continuing to diminish. Markets can go even higher.”

Investors will be watching US PPI on Thursday and retail sales the following day for fresh clues on how the US economy is holding up. Atlanta Fed President Raphael Bostic and Chicago Fed President Austan Goolsbee are scheduled to speak later Wednesday.

Europe’s Stoxx 600 rose 0.4%, tracking gains in Asia after a record close on Wall Street. Technology, personal care and health care lead in Europe, while energy and travel lag. US equity futures also edge higher. Glanbia jumps on lifted guidance, with Nordic Semiconductor also advancing, while Demant, Sixt and Persimmon all lost ground. Here are the biggest movers Wednesday:

- Glanbia shares climb as much as 13%, the most since 2009, after the food and nutrition company beat expectations in the first half and lifted its guidance for the full year

- RENK Group’s shares rise as much as 6.1%, the most since May, after the German defense company reported its second quarter revenue beat the average analyst estimate

- TUI shares gain after issuing third-quarter results in which the travel and tourism operator reported a strong beat on underlying Ebit. However, analysts note a slowdown in the group’s core package holiday unit

- Nordic Semiconductor shares rally as much as 13% to the highest since July 2024, after the chipmaker gave stronger-than-expected sales guidance for 3Q

- Evoke shares rise as much as 5.9% after the gambling company’s earnings surpassed expectations in the first half and leverage was pushed significantly lower, which analysts at Peel Hunt say could widen the appeal of the stock

- Safilo gains as much as 9.3%, hitting the highest since April 2023, as Berenberg starts coverage of the Italian eyewear company with a buy rating

- Hill & Smith shares rise as much as 12%, hitting their highest level since November, after the maker of infrastructure products reported a good set of results and a new £100m buyback

- E.ON shares rise as much as 2% after the company delivered broadly in-line results in the first half, with Ebitda coming in about 2% ahead of expectations, according to analysts

- Evolution falls as much as 10% after Bloomberg reported executives at the online gambling company were secretly filmed describing how its casino games made their way illegally to countries such as Iran, Sudan and China

- Beazley shares fall as much as 8.6%, the most in more than a year, after the British specialist insurer reported first-half results. Analysts at JPMorgan noted that Beazley reduced its FY premium-growth guidance

- Straumann shares drop as much as 4.5%, the worst performance in the Stoxx 600 Health Care Index early Wednesday, after the Swiss dental equipment company reported in-line revenue for the first half-year

- Sixt shares dipped as much as 6.4% after the German vehicle rental company reported second quarter results. Baader analysts say results are neutral or slightly negative for short-term performance of the share price

- Demant drops as much as 5%, to the lowest in more than three months, after once again lowering its guidance. Analysts at JPMorgan see the cut to outlook as “unhelpful” even if not a major shock after recent comments from peers

- Persimmon shares fall as much as 3.1% as first-half results from the UK housebuilder included comments on the margin outlook that Citi analysts said may weigh on estimates for 2026

- Deutsche PBB shares drop as much as 10% to the lowest since June after the bank reported that its withdrawal from the US had a one-off negative impact of €314 million ($368 million)

Earlier in the session, Asian equities advanced, with Hong Kong and Japan helping to lead the charge, as bets on Federal Reserve rate cuts fueled investor appetite for risk assets. The MSCI Asia Pacific Index rose as much as 1.5%, poised for a third day of gains and touching its highest since February 2021. Tencent was among the biggest boosts before its earnings report, along with TSMC and Alibaba. Gains were also notable in Thailand and South Korea, while benchmarks in Taiwan and Indonesia flirted with record highs. The Hang Seng Tech Index jumped more than 3%, with regional tech stocks also getting a lift from the Nasdaq 100’s climb to a fresh record overnight. Meanwhile, Chinese shares extended their recent strength even amid a lack of major catalysts, with ample domestic liquidity cited as a tailwind for the market. The upbeat mood came after a modest rise in US prices eased concerns that trade-related costs could spill over into broader price pressures. That drove expectations for easier Fed policy, with money markets nearly pricing in a full 25 basis point reduction next month. Here Are the Most Notable Asian Movers

- City Developments shares rise as much as 8.5% after the Singapore developer told analysts that planned divestments will allow the company to deliver “nice surprise” dividends by the end of the year.

- Hindalco’s shares rose as much as 5.7%, the most since April 11, after analysts raised their price targets on the stock following first-quarter net income that beat the average estimate.

- Asics Corp. shares jumped as much as 18% after raising its full-year forecast, predicting record earnings and bringing forward mid-term targets by a year.

- Shares of One 97 Communications Ltd. surged to the highest level in over three years after its unit received approval from India’s central bank to operate as an online payment aggregator.

- Wilmar International shares slipped as much 1.4% in Singapore after the food processing company’s first-half profit was dented by weak refining margins and a higher tax rate.

- LG Display soars by a daily record of 22% in Seoul trading on expectations that the South Korean tech company will benefit from a potential US ban on OLED products made by Chinese rival BOE.

In FX, the Bloomberg Dollar Spot Index falls 0.4%, extending its post-CPI fall as traders boost bets on an interest-rate cut by the Fed in September. The pound, kiwi and Swedish krona gain 0.6% each against the greenback.

In rates, Treasuries climb, pushing US 10-year yields down 3 bps to 4.25% with short-end tenors extending their post-CPI rally and long-end outperforming, pulling 2s10s and 5s30s spreads from Tuesday’s highs US yields richer by 2.5bp to 4bp across tenors with the curve flatter, tightening 2s10s and 5s30s spreads by 1.3bp and 0.5bp; 10-year, down nearly 4bp at 4.25% near session low, trails Germany’s by about 1bp. European government bonds also advance. As dust settles from Tuesday’s July CPI data, Fed-dated OIS contracts price in around 23bp of easing for the September policy meeting and a combined 61bp over this year’s three remaining meetings. In SOFR options, recent activity has included demand to hedge risk of a 50bp cut in September

In commodities, WTI crude futures fall 0.4% and below $63 a barrel and Brent dropped to $66 a barrel after the International Energy Agency said oil markets are on track for a record surplus next year as demand growth slows and supplies swell. Spot gold climbs $15 as the metal, which pays no interest, typically benefits from a lower rate environment.

Looking to the day ahead now, and it’s a quiet one on the calendar, but central bank speakers include Barkin (8am), Goolsbee (1pm) and Bostic (1:30pm) and earnings releases include Cisco.

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.2%

- Russell 2000 mini +0.6%

- Stoxx Europe 600 +0.4%

- DAX +0.7%

- CAC 40 +0.4%

- 10-year Treasury yield -3 basis points at 4.25%

- VIX -0.2 points at 14.53

- Bloomberg Dollar Index -0.4% at 1198.69

- euro +0.4% at $1.1727

- WTI crude -0.3% at $62.97/barrel

Top overnight news

- The U.S. government’s budget deficit grew nearly 20% in July to $291 billion despite a nearly $21 billion jump in customs duty collections from President Donald Trump’s tariffs, with outlays growing faster than receipts, the Treasury Department said on Tuesday. ZH

- Treasury Secretary Bessent expects Fed Board Nominee Stephen Miran’s Senate confirmation by September. Bessent also suggested that the Fed should consider a 50bps rate cut in September after it held rates steady in July, citing revised data showing weaker job growth in May and June as a key factor for a larger easing move. BBG