AUGUST 14/SILVER T.A.S. RECORDED ITS SIXTH CONSECUTIVE HUGE ISSUANCE AND THEY GENERALLY RAID ON THE LAST DAY LIKE TODAY: GOLD CLOSED DOWN $20.80 TO $3336.90 WITH SILVER DOWN $0.52 TO $38.00//PLATINUM HOWEVER ROSE AGAIN BY $18.72 TO $1358.20 WITH PALLADIUM ALSO UP $11.95 TO $1145.90//GOLD COMMENTARY TONIGHT FROM ALASDAIR MACLEOD//COMMODITY REPORT ON OUR RARE EARTHS//CHINA’S NEW LOANS FALL BADLY INDICATING DEFLATION IS RIPPING THEM APART//MORE NEWS ON THE DECAY INSIDE THE UK//ISRAEL VS HAMAS UPDATES RE ISRAEL TBN//COVID UPDATES//EVOL NEWS/MIKE EVERY COMMENTARY ON YESTERDAY AND TODAY’S EVENTS//USA NEWS PPI RED HOT//JOBLESS CLAIMS REMAINS CONSTANT//SWAMP STORIES FOR YOU TONIGHT//

099 H DEUTSCHE BANK AG 207 118 C MACQUARIE FUTURES US 25 118 H MACQUARIE FUTURES US 2 285 C NANHUA USA-HK 70 363 H WELLS FARGO SECURITI 207 435 H SCOTIA CAPITAL (USA) 83 624 H BOFA SECURITIES 1145 10 661 C JP MORGAN SECURITIES 83 708 709 C BARCLAYS 311 732 C RBC CAP MARKETS 22 737 C ADVANTAGE FUTURES 4 905 C ADM 10 7

TOTAL: 1,447 1,447 MONTH TO DATE: 29,127

JPMORGAN stopped 708/1447

AUGUST

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 1447 CONTRACTs NOTICES FOR 144,700 OZ or 4.5007 TONNES

total notices so far: 29.127 contracts for 2,912, 700 OR 90.597 tonnes)

FOR AUGUST

XXXXXXXXXXXXXXXXXX

SILVER NOTICES:0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1720 CONTRACTS (NOTICES) for 8.600 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $20.80 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 964.22 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.52 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV: //

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 485.462 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 812 CONTRACTS TO 157,244 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG GAIN OF $0,62 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE FINALLY ARE MOVING MUCH HIGHER THAN THE BASE $34.40 SILVER PRICE BARRIER. WE HAD A HUGE SIZED GAIN OF 912 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL 100 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO WEDNESDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $36.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON TUESDAY WITH SILVER’S GAIN IN PRICE. THE PRICE FINISHED MILES ABOVE THE MAGIC NUMBER OF $36.00 SILVER SPOT PRICE CLOSING AT $38.52 . WE HAVE ANOTHER MEGA MEGA HUGE T.A.S. ISSUANCE AT 5,432 CONTRACTS ISSUED AND THIS IS VERY UNUSUAL AS THIS IS THE 6TH CONSECUTIVE MAJOR +5000 CONTRACT ISSUANCE BY THE CME AND THAT STILL SIGNALS DEEP DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 38.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A SMALL 100 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR MEGA MEGA HUGE SIZED 5437 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY’S// TRADING OR BEYOND/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUGE SIZED 909 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.62.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A MEGA MEGA HUMONGOUS SIZED 5437 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.62) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A STRONG GAIN OF 909 CONTRACTS ON OUR TWO EXCHANGES WE HAD SOME T.A.S. SPREADER LIQUIDATION AND THAT TEMPERED SILVER’S GAIN.

WE HAD A 100 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.70 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT EXCHANGE FOR PHYSICAL TRANSFER TO LONDON OR AN ADDITIONAL 5,000 OZ WILL NOT STAND FOR PHYSICAL ON THIS SIDE OF THE POND //NEW STANDING REDUCES AT 8.700 MILLION OZ.

THUS:

INITIAL STANDING FOR AUGUST: 4.70 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ EFP JTRANSFER//NEW STANDING; 8.700 MILLION OZ

WE HAD:

/ MEGA HUGE COMEX OI GAIN+// A SMALL SIZED EFP ISSUANCE 100 CONTRACTS (/ VI) A MEGA MEGA HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 5437 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED 3 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 9 DAY(S), total 4769 contracts: OR 23.845 MILLION OZ (529 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 23.845 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 23.845 MILLION OZ

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A MEGA HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 812 CONTRACTS WITH OUR STRONG GAIN IN PRICE OF $0.62 IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. . THE CME NOTIFIED US THAT WE HAD A SMALL 100 CONTRACT EFP ISSUANCE CONTRACTS: 100 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 5 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 55,000 OZ QUEUE JUMP//NEW STANDING REMAINS AT 8.700 MILLION OZ

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (5,437) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE IN THURSDAY TRADING.

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1477 OI CONTRACTS TO 444,675 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A LARGE 594CONTRACTS //.

WE HAD A DECREASE IN COMEX OI (1477 CONTRACTS) . THIS OCCURRED DESPITE OUR GAIN OF $9.65 IN PRICE// WEDNESDAY///.

LAST FOUR MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 2.463 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE PRIOR: 5.4432 TONNES EX FOR RISK/AUG 7 AND AUG 11: 2.413 TONNES EX FOR RISK AND NOW AUG. 12 OF 2.637 TONNES EX FOR RISK //NEW STANDING ADVANCES TO 94.722 TONNES OF GOLD +10.4932 TONNES EX.FOR RISK = 105.215 TONNES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1906 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 444,675 /STILL EXTREMELY LOW AND WE NOW WITNESS A LOW COMEX OI WITH AN EXTREMELY HIGH PRICE OF GOLD

SILVER ALSO HAS A LOW COMEX OI OF 157,244 CONTRACTS

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 429 CONTRACTS WITH 1477 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1906 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 429 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1306 CONTRACTS AND THESE ISSUANCES ARE USED TO INITIATE A RAID WHEN CALLED UPON. GOLD PRICE ON WEDNESDAY ROSE BY $9.65

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(1906) ACCOMPANYING THE FAIR SIZED DECREASE IN COMEX OI OF 1477 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1023 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR AUGUST AT 60.547 TONNES FOLLOWED BY TODAY’S 2.463 TONNES QUEUE JUMP + OUR INITIAL 5.4432 TONNES EX FOR RISK AUGUST 7 AND SATURDAY’;S 2.413 TONNES EX FOR RISK ISSUANCE + WEDNESDAY’S AUGUST 12 2.637 TONNES//NEW STANDING ADVANCES TO 105.215 TONNES

NEW STANDING FOR GOLD, AUGUST CONTRACT AT 105.215 TONNES OF GOLD

.

/ 3) NO T.A.S. LIQUIDATION AS WE HAD 1)A $9.65 COMEX PRICE GAIN. WE HAD 2) NO NET LONG SPECS BEING CLIPPED AS WE HAD A SMALL GAIN OF 429 CONTRACTS ON OUR TWO EXCHANGES WE HAD NO LIQUIDATION OF OUR TAS SPREADERS/ /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND YOU CAN VISUALIZE THIS BY THE HUGE AMOUNTS OF QUEUE JUMPING WE HAVE BEEN HAVING LATELY ESPECIALLY TODAY’S HUGE JUMP OF 2.463 TONNES !!

4) SMALL SIZED COMEX OI LOSS// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (1906 CONTRACTS)/// FAIR T.A.S. ISSUANCE: 1036 T.A.S.CONTRACTS/

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

TOTAL EFP CONTRACTS ISSUED: 30,145 CONTRACTS OR 3,014,500 OZ OR 93.763 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 3349 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN9 TRADING DAY(S) IN TONNES 93.763 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 93.763 TONNES DIVIDED BY 3550 x 100% TONNES = 2.63% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

UNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 93.763 TONNES QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 812 CONTRACTS OI TO 157,244 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 100 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 370 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 809 CONTRACTS AND ADD TO THE 100 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 912 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.62 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.560 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED DOWN 17.02 PTS OR 0.46%

//Hang Seng CLOSED DOWN 94.35 PTS OR 0.37%

// Nikkei CLOSED DOWN 625.41 PTS OR 1.56% //Australia’s all ordinaries CLOSED UP 0.51%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1737 OFFSHORE CLOSED UP AT 7.1753/ Oil UP TO 62.98 dollars per barrel for WTI and BRENT UP TO 65.86 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1737 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1753 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1477 CONTRACTS TO 444,675 OI DESPITE OUR GAIN IN PRICE OF $9.65 WITH RESPECT TO WEDNESDAY’S // TRADING.. WE LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1906 ). WE HAD LITTLE T.A.S. LIQUIDATION //WEDNESDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 429 CONTRACTS (OR 1.334 TONNES). WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK WEDNESDAY.

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY:

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AS MENTIONED ABOVE: TONIGHT WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FOR AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST;

EARLY THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE FOR AUGUST OF A MONSTER 1750 CONTRACTS FOR 175,000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. WITH ALL THE CHAOS AT THE COMEX IT WAS NO SURPRISE THAT THEY ISSUED THEIR SECOND EXCHANGE FOR RISK, AUG 10 TOTALLING 776 CONTRACTS OR 77,600 OZ (2.418 TONNES).MUCH TO MY ANGER TONIGHT, THE CME ANNOUNCED ITS 3RD EXCHANGE FOR RISK OF 848 CONTRACTS TOTALLING 84,800 OZ OR 2.637 TONNES.

THUS THE TOTAL FOR AUGUST IS 3374 CONTRACTS OR 337,400OZ OR 10.4932 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS. THE RECEPIENT OF THIS LARGESS IS PROBABLY NOW THE BANK OF ENGLAND AS WE HAVE JUST LEARNED THAT THE FRBNY HAS RETURNED ONLY 14,000 OZ AS THEIR LOANS TO THE BIS REMAIN AT 34+ TONNES.(JULY 31 FIGURES) IT SEEMS NOW THAT THE BANK OF ENGLAND IS IN QUITE A HURRY TO GET ITS GOLD BACK!! (AND PROBABLE OWNER OF THOSE EXCHANGE FOR RISK CONTRACTS)

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 3 ISSUANCES FOR A MONSTER 3374 CONTRACTS OR 337,400 OZ ( 10.4932 TONNES)

AS I EXPLAINED ABOVE,:THE RECPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 429 CONTRACTS DESPITE OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 1,906 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED TWO WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS A QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS TODAY’S HUGE QUEUE JUMP OF 3.527 TONNES +10.4932 TONNES EX FOR RISK (3 ISSUANCES) //NEW STANDING 102.7512 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 235 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NONE COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 2.463 TONNES TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE + SATURDAY’S HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES AND THEN AUGUST 12: 2.637 TONNES:/NEW STANDING ADVANCES TO 105.215 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1906 EFP CONTRACT WAS ISSUED: : /DEC 1906 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1906 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

NO LIQUIDATION OF OUR T.A.S. SPREADERS//WEDNESDAY

MONTH END SPREADERS WILL APPEAR ON THE LAST WEEK OF AUGUST.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A FAIR SIZED SIZED 1906 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING SMALL LOSS OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S FIRST THREE ISSUANCES OF EXCHANGE FOR RISK FOR 10.4932 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S MONSTER QUEUE JUMP OF 2.463 TONNES TO WHICH WE ADD LAST THURSDAY’S HUGE 5.4432 EXCHANGE FOR RISK, SATURDAY’S STRONG 776 CONTRACT ISSUANCE (77600 OZ) FOR 2.413 TONNES AND THEN WEDNESDAY.S AUGUST 12 FOR 2.637 TONNES/// TOTAL EX FOR RISK AUGUST = 10.4932 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

94.722 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS) +

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $9.65/ /) AND WERE SUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD NO T.A.S. SPREADER LIQUIDATION ///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID THIS WEEK.

THURSDAY MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: THREE SO FAR, AUGUST 7 THROUGH AUG 12 AT 3374 CONTRACTS FOR 337,400 OZ (10.4932 TONNES OF GOLD) TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 10.4932 TONNES

THUS 94.722 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 10.4932 TONNES = 105.215 TONNES.

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE GAINED A SMALL SIZED TOTAL OF 1.334 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD LAST THURSDAY’S RECORD BREAKING QUEUE JUMP OF 10.8775 TONNES OF GOLD ON TOP OF TUESDAY’S 1.7604 TONNES QUEUE JUMP AND THEN WEDNESDAY;S MASSIVE QUEUE JUMP OF 3.527 TONNES AND THEN THURSDAY’S HUGE 2.463 TONNES QUEUE JUMP TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK/PRIOR FOR 10.4932 TONNES FOR RISK//NEW STANDING ADVANCES TO 105.215 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $9.65

WE HAD A LARGE 594 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 429 CONTRACTS OR 42,900 0Z (1.334 TONNES)

i) Into JPMorgan enhanced: 20,004.700 oz 50 London good delivery bars of 400 oz each

total deposit 20,004.700 oz

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

1447 notice(s) 144,700 OZ 4.5007 TONNES

No of oz to be served (notices)

1326 contracts 132600 OZ 4.1244 TONNES

Total monthly oz gold served (contracts) so far this month

29,127 notices 2,912,700 oz 90.597 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits:

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

1 ENTRY

i) Into JPMorgan enhanced: 20,004.700 oz 50 London good delivery bars of 400 oz each

total deposit 20,004.700 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entry

adjustments:

nil

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 2773 CONTRACTS FOR A GAIN OF 80 CONTRACTS

WE HAD 712 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED A HUGE SIZED 792 CONTRACTS OR 79,200 OZ OF GOLD (2.463 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND.. THIS ALSO REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD AND THEIR APPETITE FOR THIS GOLD IS UNABATED!

SEPT LOST 283 CONTRACTS TO 5178

OCTOBER LOST 589 CONTRACTS DOWN TO 61,836

We had 1447 contracts filed for today representing 144,700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1447 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 708 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (29,127 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 2773 CONTRACTS) minus the number of notices served upon today (1447 x 100 oz per contract) equals 3,045,300 OZ OR 94.722TONNES TO WHICH WE ADD OUR THREE ISSUANCES OF 10.4932 TONNES OF EXCHANGE FOR RISK/AUG 7 , 11 AND 12TH = 105.215 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (29.127 x 100 oz +we add the difference for front month of AUGUST (2773 OI} minus the number of notices served upon today (1447 x 100 oz) which equals 2,966,100 OZ OR 94.722 TONNES + 10.4932 TONNES EX FOR RISK = 105.215 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 105.215 TONNES WHICH IS HUGE FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

i) Out of Brinks: 60,748.400 oz ii) Out of Delaware: 2030.000 oz

total withdrawal: 62,778.46 oz

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 190.400 MILLION OZ//.TOTAL REG + ELIGIBLE. 507.041 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 20 OPEN INTEREST CONTRACTS FOR A LOSS OF 5 CONTRACTS. WE HAD 4 CONTRACTS SERVED ON WEDNESDAY SO WE LOST 1 CONTRACT OR AN ADDITIONAL 55,000 OZ WILL NOT STAND AS THEY WERE FERRIED OVER TO LONDON WHERE THEY TOOK DELIVERY ON THAT SIDE OF THE POND

SEPTEMBER LOST 5518 CONTRACTS DOWN TO 72,158 CONTRACTS.

OCTOBER GAINED 33 CONTRACTS TO 700

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or NIL oz

CONFIRMED volume; ON WEDNESDAY 73,929 HUGE//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1720 X5,000 oz = 8.600 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (20) AND the number of notices served upon today (0 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1720) Notices served so far) x 5000 oz + OI for the front month of AUGUST(20) minus number of notices served upon today (0)x 5000 oz equals silver standing for the AUGUST contract month equating to 8.705 MILLION OZ .

New total standing: 8.700 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.400 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/507.041 million. 41.47%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 964.22 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

According to its government, the UK economy grew 0.3% in Q2. Correction: this growth is entirely due to government spending. The private sector is in a developing slump.

The UK’s economy is in a mess. Anyone living here, particularly outside London and its environs sees shops, pubs, and businesses being closed, job offers declining, growing numbers on welfare, and hotels filling up with immigrants. Inside London, the strong hand of mayoral communism is destroying the conurbation. Lawlessness rages, with shops being pillaged by shoplifting gangs, and tourists being robbed of their watches and mobiles. Meanwhile, the police ignore criminal theft and are arresting ordinary protestors who disparage the loss of free speech.

MacleodFinance Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

However, the good news is that the economy is growing faster than all the other G7 nations in the first half of the year, according to Bloomberg.

You can’t fool all of the people all of the time. According to Bloomberg, “economists pointed out that much of the growth has been driven by higher public spending under Labour”. At last, it is being admitted that Keynesian stimulus has a downside.

In fact, increasing public spending is masking an outright slump in private sector activity. Clearly, the budget deficit is far worse than the consensus believes if it covers up a slump in the 80% of the economy which is comprised of small and medium sized businesses. All will become more obvious when Rachael from accounts produces her autumn statement.

Additionally, revenue assumptions in her fist budget are victims of the Laffer curve. The top 1% of earners pay 30% of all income tax: they are gone or going. Capital gains tax revenue is collapsing, despite asset inflation because why sell an asset and face a tax bill imposed by a regime which is openly hostile to you?

The residential housing market has ground to a halt for the same reason. No one is selling, leaving a huge CGT hole in government finances. The extreme socialists in government are doubling down, pushing for yet more taxes on the rich to cover the budget deficit, despite the mess they have already created and the lessons they refuse to learn.

Rachael was blubbing in Parliament when she realised her errors and will have cause to do so again. But those who will join her in misery are the hedge funds long of sterling and gilts, when they see yields rising and sterling falling.

Get out of sterling — it is wildly overvalued and due to crash.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

The gold swaps by the Frbny remains at 34 tonnes of gold having fallen slightly by only 14,000 oz

Not happy with this!!

(zerohedge)

BIS gold swaps held steady at 34 tonnes in July, GATA’s Robert Lambourne reports

Submitted by admin on Mon, 2025-08-11 20:50 Section: Daily Dispatches

8:55p ET Monday, August 12, 2025

Dear Friend of GATA and Gold:

Gold swaps undertaken by the Bank for International Settlements, the central bank of the central banks and often their broker in the gold market, fell slightly in July, by about 14,000 ounces, but, rounded off, remained at June’s 34-tonne mark, according to GATA consultant Robert Lambourne.

The information can be calculated from the bank’s monthly statement of account for July, published today:

The report implies that the bank was not recruited to intervene much in the gold market in June on behalf of its member central banks and that there continues to be little interest among them in incurring more gold liabilities or in letting their metal get far from home.

— provides some history on the swap transactions and their volatility since the bank in 2010 made it possible for its gold swaps to be calculated.

As recently as January 2022 the bank’s swaps exceeded 500 tonnes but they have fallen sharply since, indicating a change of policy toward or outlook on gold, a trend that seems to have correlated with increasing central bank acquisitions and repatriations, along with gold’s rising price.

Nevertheless, the BIS has a well-placed confidence that no mainstream financial news organization will ever ask it to explain the purposes of the swaps and to identify the parties to them, lest gold cease being the immensely powerful secret knowledge of the financial universe.

CHRIS POWELL, Secretary/Treasurer

end

Bernhard Schnellmann: The gold market is too important to be left to private clubs

Submitted by admin on Thu, 2025-08-14 08:16 Section: Daily Dispatches

Is it too important to be left to be left to governments as well?

* * *

By Bernhard Schnellmann Financial Times, London Thursday, August 14, 2025

While gold continues to serve as a trusted store of value for investors and central banks alike, the institutions underpinning the global gold market remain largely private, opaque, and under-regulated.

The European Central Bank recently warned that under extreme events, the gold market poses financial stability risks. It said “vulnerabilities have arisen because commodity markets tend to be concentrated among a few large firms, often involve leverage and have a high degree of opacity deriving from the use of over-the-counter derivatives. … Disruptions in the physical gold market could increase the risk of a squeeze.

The warning is timely, if overdue.

At the heart of the gold trade lies the London Bullion Market Association — a private trade group that defines the standards by which gold is refined, traded, and stored.

Closely linked is London Precious Metals Clearing Limited, another private consortium that oversees the clearing and settlement of trades. Together, these institutions exercise significant influence over the functioning of the largest OTC bullion market.

Yet neither the LBMA nor the LPMCL has any official authority as regulator for the OTC precious metals market. Their operations, however, are fundamental to a global market used for everything from central bank reserve management to retail investment. …

The global rare earth metals market has seen a whirlwind of developments in the past few weeks, sending ripples through both supply chains and pricing. A series of U.S. and Chinese policy moves, from Washington’s unprecedented price support for rare earth magnets to Beijing’s export curbs, continue to reshape this critical sector.

U.S. Sets New Rare Earth Price Floor to Challenge China’s Dominance

The United States recently escalated its efforts to reduce dependence on China by directly intervening in pricing. In mid-July, the Department of Defense struck a multi-billion-dollar deal with MP Materials, America’s sole rare earth miner, guaranteeing a minimum price of $110 per kilogram for neodymium-praseodymium (NdPr) oxide.

That price floor, which is nearly double the current China-based market rate of around $60/kg, aims to incentivize domestic production of the super-strong magnets used in EV motors, wind turbines, and defense systems.

Officials and analysts describe the move as a game-changer for the industry. By establishing a higher Western pricing benchmark, the U.S. hopes to offset China’s long-standing tactic of undercutting prices to maintain its dominance. “This benchmark is now a new center of gravity in the industry that will pull prices up,” notes Adamas Intelligence, adding that it could bolster non-Chinese producers globally.

News of the U.S. price support immediately lifted Australian rare earth mining stocks. For instance, Lynas Corp jumped 20% to a three-year high on expectations that non-Chinese suppliers would benefit from a more level playing field. Market watchers say the initiative signals a strong push for North American supply chain independence and may spur similar policy support in allied countries.

China’s Export Curbs Squeeze Supply Chains

Meanwhile, China’s export policies have injected uncertainty into the rare earth market. Back in April, Beijing added seven rare earth metals, including heavy elements like dysprosium, terbium and samarium, to its export control list. A tentative thaw emerged in late July as trade negotiators worked to ease the standoff.

Under an earlier tariff truce, China agreed to begin removing its new rare earth export restrictions. In practice, Chinese authorities have started issuing export licenses to select U.S. customers, resulting in a sharp rebound of magnet shipments in June and July.

U.S. Trade Representative officials say progress is being made, but caution that the process is only “about halfway” toward fully restoring normal trade flows. Beijing insists its export controls are “non-discriminatory” and has signaled its willingness for talks. However, it also wields these measures as leverage, a reminder of rare earth metals’ role as a strategic pawn in the broader U.S.-China tech rivalry.

For procurement executives, the situation remains fluid. Contingency plans (such as qualifying alternative suppliers outside China or increasing inventories) are back on the agenda for manufacturing firms. To stay ahead of such geopolitical risks, many organizations are leveraging market intelligence tools like MetalMiner Select.

Global Supply Chain Shifts and New Mining Developments

The recent volatility around rare earth metals is spurring a broader realignment of supply chains as U.S. allies and major consumers collaborate to dilute China’s dominance. Notably, Japan and the EU announced plans for joint rare earth procurement in a public-private partnership aimed at securing a more stable supply.

These initiatives underscore a clear global trend of diversification where governments and companies alike, from Australia to North America, are investing in mining, processing and recycling capacity.

Mining news over the past month reflects this momentum. Australia’s Lynas Rare Earths, the largest producer outside China, reported record quarterly revenue in late July thanks to higher rare earth prices and strong demand. Lynas’s CEO noted that the market has become “more vibrant and buoyant” since China’s export curbs, with the company’s average selling price jumping to its highest level in three years.

To capitalize on its growth, Lynas is ramping up output and expanding downstream. The firm recently inked a deal with a South Korean company to build a 3,000-ton-per-year magnet manufacturing plant in Malaysia. The move will make Lynas the first commercial producer of certain heavy rare earth oxides outside China.

Prices Rise on Tight Supply and Robust Demand

Rare earth prices have climbed significantly in recent weeks, driven by a perfect storm of constrained supply and revived demand. In July alone, the benchmark China price for NdPr alloy jumped from roughly ¥545,000/mt at the start of the month to ¥635,000 by July 28.

Multiple factors are fueling this rally. On the supply side, China’s export restrictions and related bottlenecks have tightened material availability for overseas buyers. Industry analysts note that U.S. ore shipments to China effectively dropped to zero after MP Materials stopped exporting concentrate, removing over 300 metric tons of NdPr oxide equivalent per month from the global supply pool.

Meanwhile, Myanmar, a major source of heavy rare earth feedstock for China, announced plans to ban rare earth metals mining by the end of 2025, raising concerns about future supply. This comes as rumors of output cuts at a large Chinese producer have further stoked scarcity fears. On the demand side, manufacturers are ramping up purchases. With fresh clarity emerging around China’s magnet export rules as of July, many magnet makers have rushed to secure orders for Q3 and Q4 delivery, anticipating possible delays.

Short-Term Outlook for Rare Earth Metals

Looking ahead to the next few months, the rare earths market appears poised to remain firm. However, this does not mean it is free of risks. Most analysts agree that prices will stay elevated through the end of the third quarter. The demand pipeline is particularly robust, with electric vehicle makers, wind turbine manufacturers and electronics producers all planning for a strong finish to the year. This could mean continued short-term appetite for rare earth magnets.

This seasonal strength, combined with buyers’ ongoing restocking, provides a floor under prices in the near term. Additionally, the U.S. government’s price-support deal effectively establishes $110/kg as a new minimum benchmark for NdPr. Even if Chinese spot prices dip slightly, the incentive for Western producers to hold out for higher prices is now in place.

Potential Challenges

There are also a few wildcards that could swing the outlook, the trajectory of U.S.-China negotiations being chief among them. If diplomatic talks yield concrete resolutions, such as China fully lifting its export licensing requirements for rare earth metals, the rush to secure supply could ease, potentially taking some heat out of prices.

For metal procurement executives, this volatile environment calls for agility and informed strategy. In the short run, many are adopting a hedged approach: committing to some volumes now to avoid future price spikes, while holding contingency budgets in case prices pull back. Engaging alternate suppliers outside China, where possible, is another play—one that could gain traction as projects like the new Malaysian magnet plant or U.S. processing facilities come online.

Rare Earths MMI: Noteworthy Price Shifts

See why technical analysis is a superior forecasting methodology over fundamental analysis and why it matters for your metal buys.

Yttria prices dropped by 5.59% to $6,547.97 per metric ton.

Neodymium oxide prices surged by 16.36% to $73,418.65 per metric ton.

Praseodymium oxide prices rose by 12.7% to $73,868.14 per metric ton

Lastly, terbium oxide prices fell 2.91% to $984.56 per kilogram.

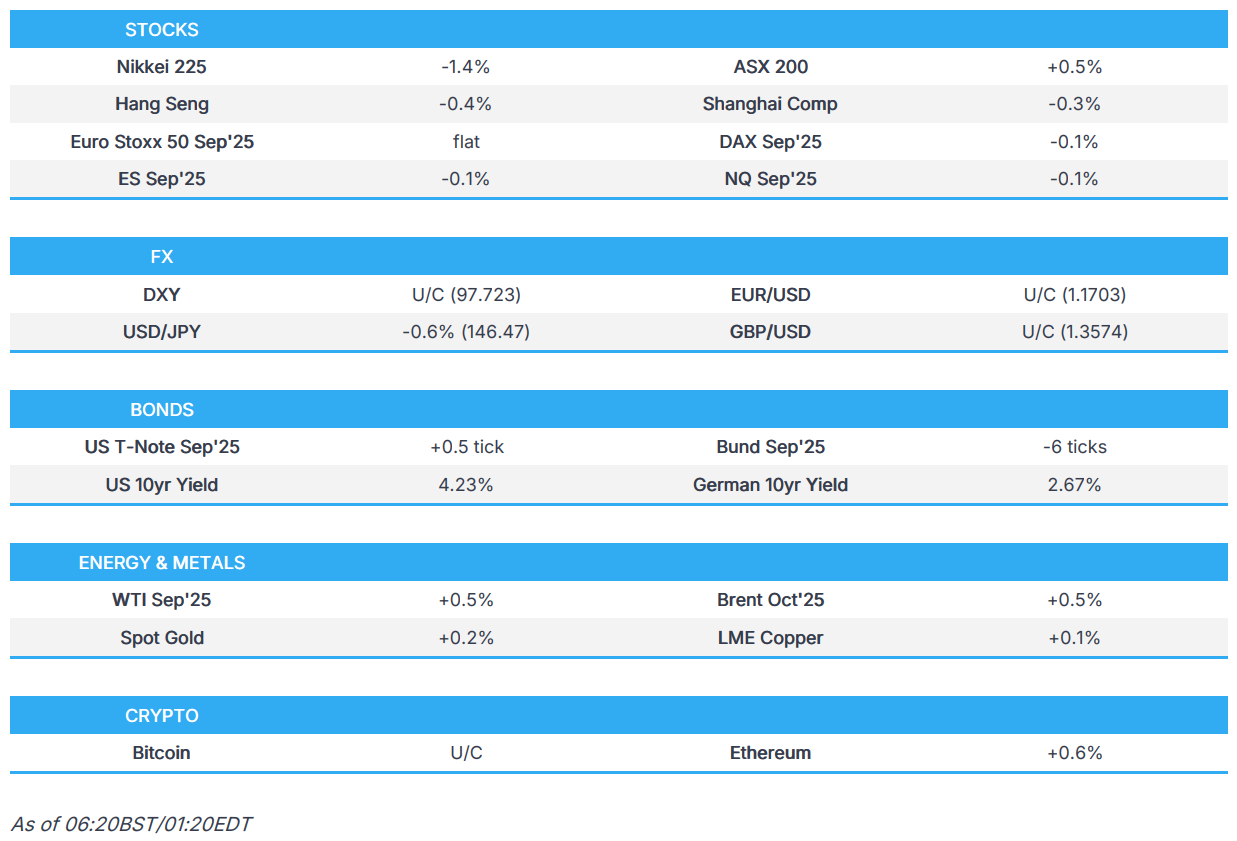

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED DOWN 17.02 PTS OR 0.46%

//Hang Seng CLOSED DOWN 94.35 PTS OR 0.37%

// Nikkei CLOSED DOWN 625.41 PTS OR 1.56% //Australia’s all ordinaries CLOSED UP 0.51%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1737 OFFSHORE CLOSED UP AT 7.1753/ Oil UP TO 62.98 dollars per barrel for WTI and BRENT UP TO 65.86 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1737 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1753 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1737 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1753

HANG SENG CLOSED DOWN 94.35 PTS OR 0.37%

2. Nikkei closed DOWN 625.41 PTS OR 1.45%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 97.77/ EURO FALLS TO 1.1672 DOWN 41 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.547//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.42…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6590/Italian 10 Yr bond yield DOWN to 3.458 SPAIN 10 YR BOND YIELD DOWN TO 3.213%

3i Greek 10 year bond yield DOWN TO 3.312

3j Gold at $3351.85 Silver at: 38.32 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 26 /100 roubles/dollar; ROUBLE AT 79.71

3m oil (WTI) into the 62 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.62// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.547% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8063 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9420 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.212 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.806 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.672 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.80

10 YR UK BOND YIELD: 4.570 DOWN 3 PTS

10 YR CANADA BOND YIELD: 3.405 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.937 UP 0 PTS

2a New York OPENING REPORT

Futures Flat, Global Stock Rally Fizzles Ahead Of PPI Report

by Tyler Durden

Thursday, Aug 14, 2025 – 08:29 AM

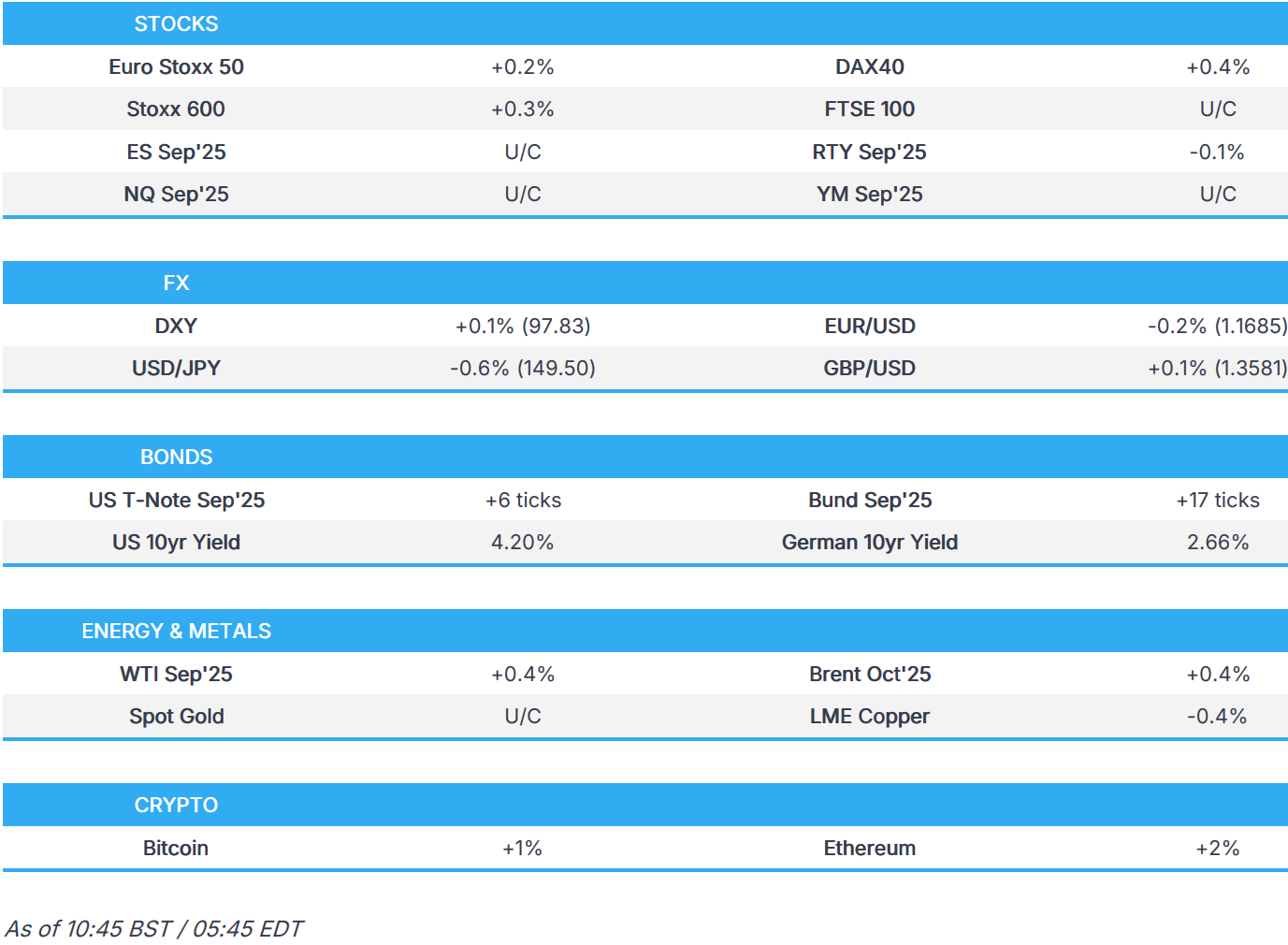

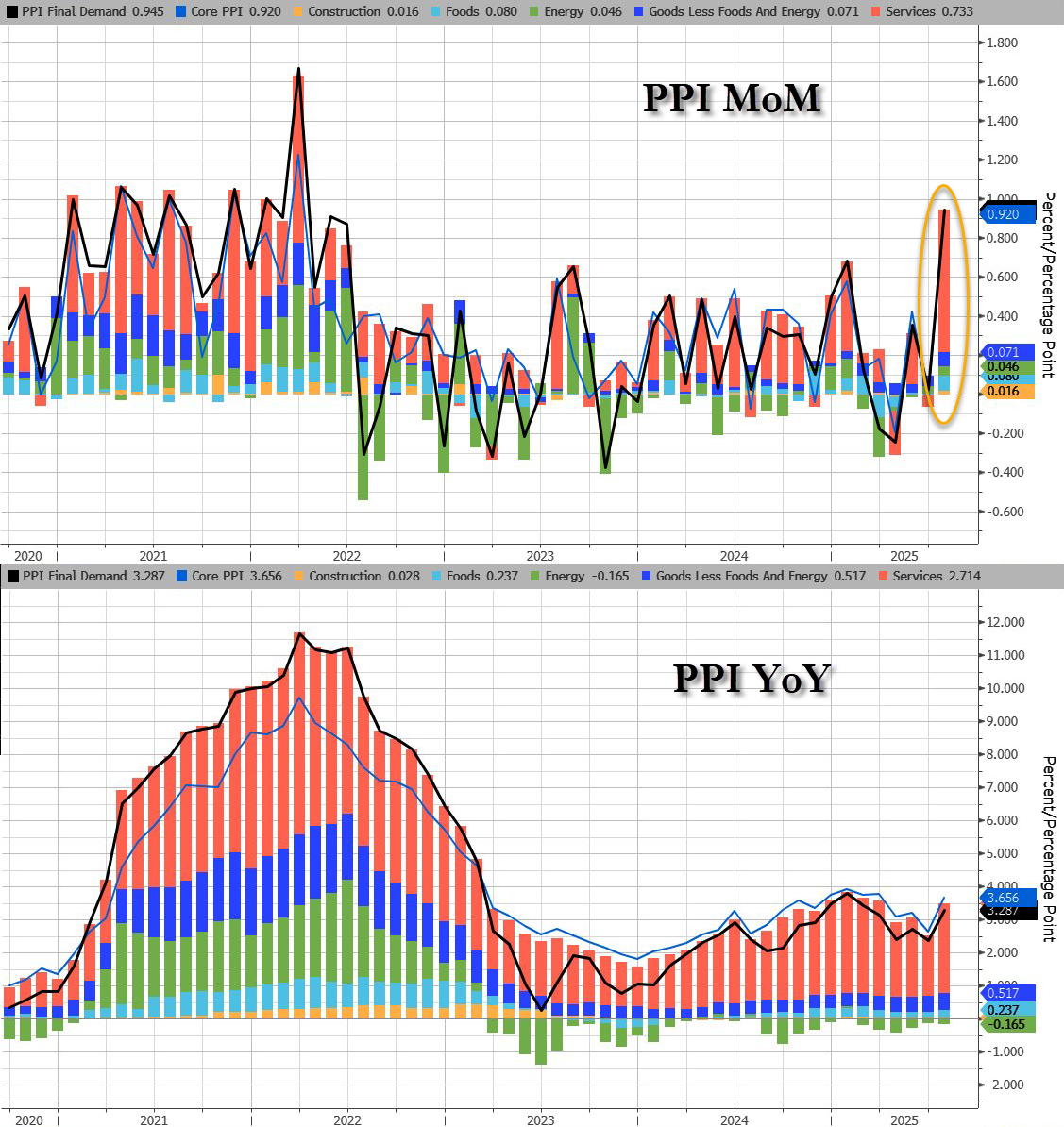

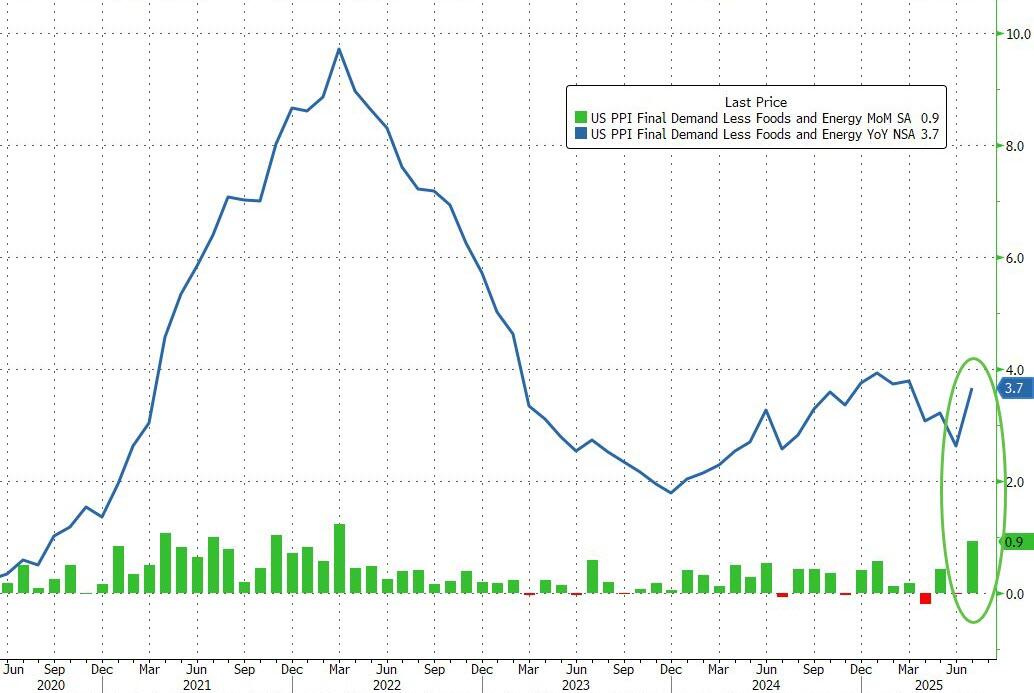

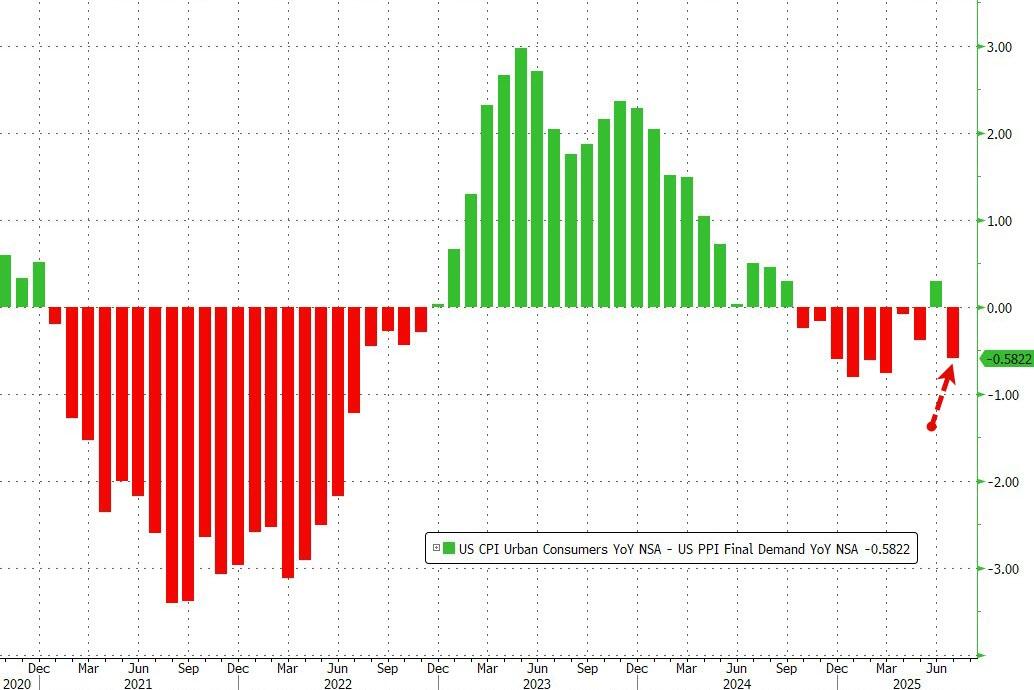

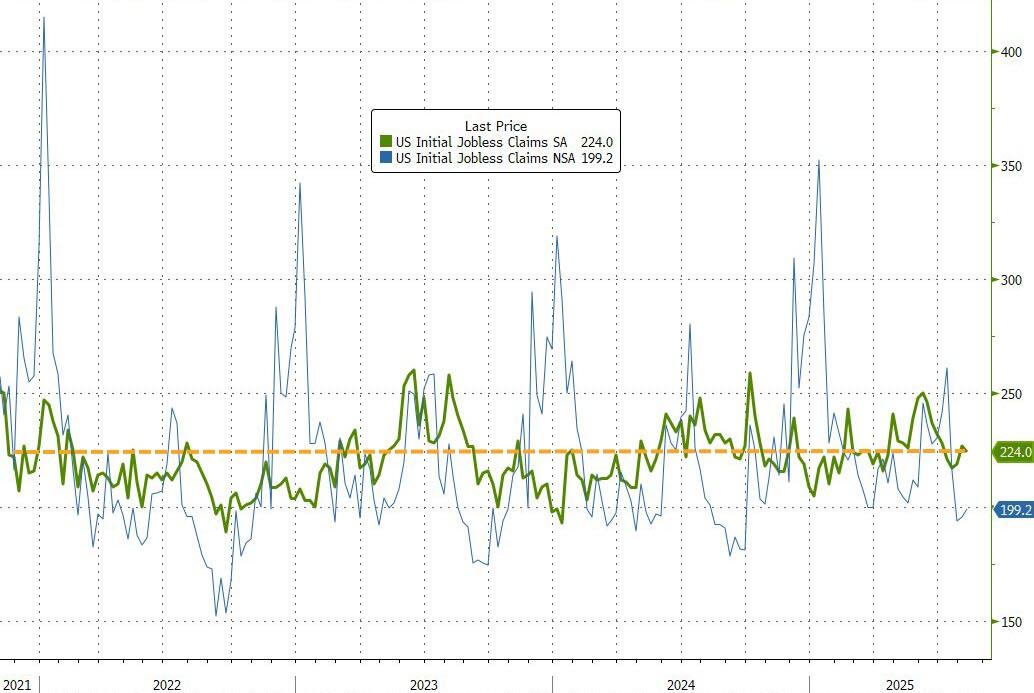

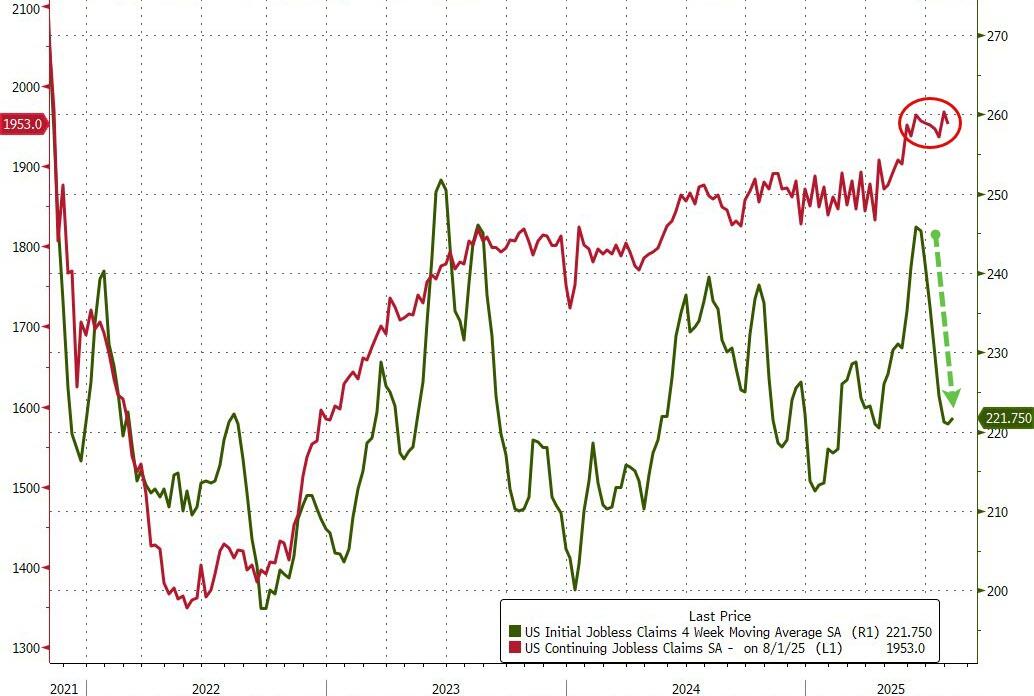

The global market rally stalled and US equity futures are flat with small caps underperforming (SPX and NDX made new ATHs yesterday while the Russell still sits ~5% below its ATH) into this morning’s PPI print, where the market may confirm CPI’s trend as well as solidifying PCE estimates. As of 8:00am, S&P 500 futures were flat changed after the benchmark notched a record close for a second straight session; Nasdaq futures dropped 0.2% after Cisco shares fell after issuing a cautious full-year revenue outlook. Europe’s Stoxx 600 rose 0.3%. Pre-mkt, Mag7 names are mostly higher with Semis weaker; Defensives looking stronger than Cyclicals with healthcare leading. Bond yields are lower as the curve bull flattens: the yield on 10-year notes dropping two basis points to 4.21%. Bitcoin retreated 1.7% from an all-time high and the USD is flat. Today’s macro data focus is on PPI and Initial Jobless Claims; an in-line print in both should support stocks. JPMorgan says that should the rally resume, look for RTY to close the gap to tech/large caps.

In premarket trading, Magnificent Seven stocks are mixed (Microsoft +0.3%,Tesla +0.4%, Meta -0.01%, Amazon +0.2%, Alphabet -0.06%, Nvidia +0.09%, Apple +0.07%).

Bullish (BLSH) rises 15% a day after the crypto exchange operator and CoinDesk owner raised $1.1 billion in an initial public offering.

Bumble (BMBL) falls 11% after holders offered to sell shares at a 11% discount to the closing price.

Cisco Systems (CSCO) slips 1.4% after the largest maker of machines that run computer networks and the internet gave a lukewarm forecast for the current fiscal year.