099 H DEUTSCHE BANK AG 23

118 C MACQUARIE FUTURES US 2

118 H MACQUARIE FUTURES US 32

285 C NANHUA USA-HK 6

435 H SCOTIA CAPITAL (USA) 10

624 H BOFA SECURITIES 10

661 C JP MORGAN SECURITIES 105 87

709 C BARCLAYS 29

732 C RBC CAP MARKETS 2

737 C ADVANTAGE FUTURES 4

905 C ADM 11 3

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 162 CONTRACTs NOTICES FOR 16,200 OZ or 0.5039 TONNES

total notices so far: 29,289 contracts for 2,928,900 OR 91.101 tonnes)

SILVER NOTICES:0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1720 CONTRACTS (NOTICES) for 8.600 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 24.845 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 25,000 OZ QUEUE JUMP//NEW STANDING REMAINS AT 8.725 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0.7030 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE PRIOR: 5.4432 TONNES EX FOR RISK/AUG 7 AND AUG 11: 2.413 TONNES EX FOR RISK AND NOW AUG. 12 OF 2.637 TONNES EX FOR RISK //NEW STANDING ADVANCES TO 95.433 TONNES OF GOLD (INCLUDES ALL MONTHLY QUEUE JUMPS) +10.4932 TONNES EX.FOR RISK = 105.926 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 99.259 TONNES QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A SMALL 30 CONTRACTS OI TO 157,214 AND FURTHER FROM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 100 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 370 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 30 CONTRACTS AND ADD TO THE 100 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF 70 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.52 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.35 MILLION PAPER OZ

OCCURRED WITH OUR $0.52 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 30.33 PTS OR 0.83%

//Hang Seng CLOSED DOWN 249.25 PTS OR 0.98%

// Nikkei CLOSED UP 729.05 PTS OR 1.71% //Australia’s all ordinaries CLOSED UP 0.69%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1805 OFFSHORE CLOSED DOWN AT 7.1842/ Oil UP TO 63.26 dollars per barrel for WTI and BRENT UP TO 66.17 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1805 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1842 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 4966 CONTRACTS TO 439,709 OI DWITH OUR LOSS IN PRICE OF $20.80 WITH RESPECT TO THURSDAY’S // TRADING.. WE LOST NO NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1767 ). WE HAD CONSIDERABLE T.A.S. LIQUIDATION //THURSDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 7935 CONTRACTS (OR 24.68 TONNES). WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK THURSDAY. THE CROOKS COULD NOT FLEECE ANY OF OUR NET LONGS AS THE COMEX LEVEL OI WAS EXTREMELY LOW AND VERY VERY STICKY.

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY:

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AS MENTIONED ABOVE: TONIGHT WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FOR AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST;

EARLY THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE FOR AUGUST OF A MONSTER 1750 CONTRACTS FOR 175,000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. WITH ALL THE CHAOS AT THE COMEX IT WAS NO SURPRISE THAT THEY ISSUED THEIR SECOND EXCHANGE FOR RISK, AUG 10 TOTALLING 776 CONTRACTS OR 77,600 OZ (2.418 TONNES).MUCH TO MY ANGER TONIGHT, THE CME ANNOUNCED ITS 3RD EXCHANGE FOR RISK OF 848 CONTRACTS TOTALLING 84,800 OZ OR 2.637 TONNES.

THUS THE TOTAL FOR AUGUST IS 3374 CONTRACTS OR 337,400OZ OR 10.4932 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS. THE RECEPIENT OF THIS LARGESS IS PROBABLY NOW THE BANK OF ENGLAND AS WE HAVE JUST LEARNED THAT THE FRBNY HAS RETURNED ONLY 14,000 OZ AS THEIR LOANS TO THE BIS REMAIN AT 34+ TONNES.(JULY 31 FIGURES) IT SEEMS NOW THAT THE BANK OF ENGLAND IS IN QUITE A HURRY TO GET ITS GOLD BACK!! (AND PROBABLE OWNER OF THOSE EXCHANGE FOR RISK CONTRACTS)

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 3 ISSUANCES FOR A MONSTER 3374 CONTRACTS OR 337,400 OZ ( 10.4932 TONNES)

AS I EXPLAINED ABOVE,:THE RECPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 3199 CONTRACTS WITH OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 1,056 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED TWO WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS A QUEUE JUMP OF 1.577 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS TODAY’S HUGE QUEUE JUMP OF 0.7030 TONNES +10.4932 TONNES EX FOR RISK (3 ISSUANCES) //NEW STANDING 105.926 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 235 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0.7030 TONNES TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE + SATURDAY’S HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES AND THEN AUGUST 12: 2.637 TONNES:/NEW STANDING ADVANCES TO 105.926 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1767 EFP CONTRACT WAS ISSUED: : /DEC 1767 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1767 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY

- MONTH END SPREADERS WILL APPEAR ON THE LAST WEEK OF AUGUST.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A FAIR SIZED SIZED 1056 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING SMALL LOSS OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S FIRST THREE ISSUANCES OF EXCHANGE FOR RISK FOR 10.4932 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.7030 TONNES TO WHICH WE ADD LAST THURSDAY’S HUGE 5.4432 EXCHANGE FOR RISK, SATURDAY’S STRONG 776 CONTRACT ISSUANCE (77600 OZ) FOR 2.413 TONNES AND THEN WEDNESDAY.S AUGUST 12 FOR 2.637 TONNES/// TOTAL EX FOR RISK AUGUST = 10.4932 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

95.433 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

EQUALS

105.926 TONNES TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A $20.80/ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF A FEW NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION ///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH YESTERDAYS TRADING!.

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: THREE SO FAR, AUGUST 7 THROUGH AUG 12 AT 3374 CONTRACTS FOR 337,400 OZ (10.4932 TONNES OF GOLD) TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 10.4932 TONNES

THUS 95.437 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 10.4932 TONNES = 105.926 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE LOST A FAIR SIZED TOTAL OF 9.90 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD LAST THURSDAY’S RECORD BREAKING QUEUE JUMP OF 10.8775 TONNES OF GOLD ON TOP OF TUESDAY’S 1.7604 TONNES QUEUE JUMP AND THEN WEDNESDAY;S MASSIVE QUEUE JUMP OF 3.527 TONNES AND THEN THURSDAY’S HUGE 2.463 TONNES QUEUE JUMP AND THEN TODAY;S QUEUE JUMP OF .7030 TONNES TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK/PRIOR FOR 10.4932 TONNES FOR RISK//NEW STANDING ADVANCES TO 105.926 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $20.80

WE HAD A HUGE 11,134 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 3199 CONTRACTS OR 319,900 0Z (9.95 TONNES)

confirmed volume THURSDAY 180,976 contracts// poor

speculators have left the gold arena

END

INITIAL GOLD COMEX

END

INITIAL GOLD COMEX

AUGUST CONTRACT MONTH

AUGUST15 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entry I) OUT OF ASAHI; 6088.672 OZ total withdrawal; 6088.672 oz . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER \0 ENTRY xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 162 notice(s) 16,200 OZ 0.5039 TONNES |

| No of oz to be served (notices) | 1393 contracts 139300 OZ 4.333 TONNES |

| Total monthly oz gold served (contracts) so far this month | 29,289 notices 2,928,900 oz 91.101 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entry

1 entry

I) OUT OF ASAHI; 6088.672 OZ

total withdrawal; 6088.672 oz

adjustments: one

out of Asahi: dealer to customer acct 42,128.330 oz

nil

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 1555 CONTRACTS FOR A LOSS OF 1221 CONTRACTS

WE HAD 1447 CONTRACTS SERVED ON THURSDAY SO WE GAINED A HUGE SIZED 226 CONTRACTS OR 22,600 OZ OF GOLD (0.7030 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND.. THIS ALSO REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD AND THEIR APPETITE FOR THIS GOLD IS UNABATED!

SEPT LOST 127 CONTRACTS TO 5051

OCTOBER LOST 282 CONTRACTS UP TO 61,554

We had 162 contracts filed for today representing 16,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 105 notices issued from their client or customer account. The total of all issuance by all participants equate to 162 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 87 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (29,289 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 1555 CONTRACTS) minus the number of notices served upon today (162 x 100 oz per contract) equals 3,068,200 OZ OR 95.433TONNES TO WHICH WE ADD OUR THREE ISSUANCES OF 10.4932 TONNES OF EXCHANGE FOR RISK/AUG 7 , 11 AND 12TH = 105.936 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (29,289 x 100 oz +we add the difference for front month of AUGUST (1555 OI} minus the number of notices served upon today (162 x 100 oz) which equals 3,068,200 OZ OR 95.433 TONNES + 10.4932 TONNES EX FOR RISK = 105.936 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 105.936 TONNES WHICH IS HUGE FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,016,810.364 oz 62.73 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,642,421.131 oz

TOTAL REGISTERED GOLD 21,308,803.358 or 662.79 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,327,528.901 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,291,993 oz ((REG GOLD- PLEDGED GOLD)= 600.06tonnes // ( a bid drop of 10 tonnes

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE AUGUST 2025 SILVER CONTRACT//INITIAL

AUGUST 15 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries: i) Out of Brinks: 10,142.490 oz total withdrawal: 10,142.490 |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into CNT 546,785.700 ooz total deposit 546,785.700 oz |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ |

| No of oz to be served (notices) | 25 contracts (0.125 MILLION oz) |

| Total monthly oz silver served (contracts) | 1720 Contracts (8.60 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into CNT 546,785.700 ooz

total deposit 546,785.700 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

1 entries:

i) Out of Brinks: 10,142.490 oz

total withdrawal: 10,142.490

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 190.400 MILLION OZ//.TOTAL REG + ELIGIBLE. 507.551 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 25 OPEN INTEREST CONTRACTS FOR A GAIN OF 5 CONTRACTS. WE HAD 0 CONTRACTS SERVED ON THURSDAY SO WE GAINED 5 CONTRACTS OR AN ADDITIONAL 25,000 OZ WILL STAND AT THE COMEX.

SEPTEMBER LOST 1864 CONTRACTS DOWN TO 70.294 CONTRACTS.

OCTOBER GAINED 91 CONTRACTS TO 791

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or NIL oz

CONFIRMED volume; ON THURSDAY 64,397 good//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1720 X5,000 oz = 8.600 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (25) AND the number of notices served upon today (0 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1720) Notices served so far) x 5000 oz + OI for the front month of AUGUST(25) minus number of notices served upon today (0)x 5000 oz equals silver standing for the AUGUST contract month equating to 8.725 MILLION OZ .

New total standing: 8.725 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.400 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/507.041 million. 41.47%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 961.36 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 484.553 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

PMs — the lull before the storm

Expectations for Trump’s meeting with Putin in Alaska have been downplayed but diverted attention from a stalling US and global economy.

| Alasdair MacleodAug 15∙Paid |

Any independent observer will note that the outlook for the dollar is deteriorating, credit risk rising, and a debt trap is being sprung on the US Treasury. Tonight’s Alaska circus is a diversion from this reality.

Gold and silver continued to consolidate earlier gains this week, but the market underneath continues to tighten. In European morning trade today gold was $3340, down $60 from last Friday’s close, and silver was $37.90, down 40 cents. Comex volumes in both contracts declined over the week, in silver’s case from the noticeably high levels seen the previous week.

Market makers face a flight out of paper into gold

A stand-out feature was the scale of stand-for-deliveries in the Comex gold contract, at 90.6 tonnes from 31 July so far, reflecting the expiry of the August contract. 267.5 tonnes of silver were also stood for delivery. To put these numbers in context, 861 tonnes of gold have been stood for delivery since 1 January. Comex gold warehouse stocks total 1,201.3 tonnes and have begun to rise again. How much of this is gold yet to be delivered but in Comex warehouses is not known. This chart is from MacroMicro:

Of course, Comex is only part of the overall picture. And with respect to futures, the Shanghai futures exchange is opening direct access to non-Chinese entities which will take trading liquidity away from Comex. This move is consistent with the internationalisation of China’s capital markets, centred on gold and silver trading in yuan.

That is for the future. Meanwhile, Comex gold futures still remain relatively oversold with low participation. This is next:

At 450,000 contracts, open interest is close to oversold territory, yet the swaps taking the short side are close to record short in value terms:

This chart will update tonight to reflect last Tuesday’s position. But with open interest on 5 August at 449,647 contracts and a gold price $40 above today’s gross shorts were $92.3 billion held between 27 traders, and the net position was $80bn. It amounts to a serious squeeze on the market-making establishment, faced with converting paper into physical gold.

The only escape for the swaps is a reversal of the gold price’s drivers. But that is unlikely, with credit risk in the fiat dollar increasing. If anything, currency and financial markets face growing instability. The next chart updates the dollar’s TWI:

Not only is the dollar’s TWI heading lower technically, but Trump’s avowed policy is for a lower dollar and lower interest rates. The pressure on the Fed to reduce its funds rate have mounted to the extent that a 0.25% cut in September is a done deal, despite reservations about the course of inflation. Adding to the political interference is Trump’s appointment to the Fed of Stephen Miren, subject to Senate confirmation. As an inflation dove, presumably he will be in a position to be nominated as Chairman by Trump when Jay Powel’s term ends next year.

In contrast to political pressures for lower interest rates and a lower dollar, these same policies will drive longer maturity bond yields higher. And when the long bond yield breaks the 5% barrier, a consolidation will be completed projecting yields to 9% or more (move in from 2020 equals move out above 5%):

This would be devastating for the dollar and the entire fiat currency system.

Driving it will be an emerging debt trap, rapidly increasing the ratio of government debt to GDP. Outstanding debt is already rising at an increased pace, and the private sector, ex-budget deficit is contracting. Furthermore, the dollar is over owned by foreigners facing losses on dollars and underlying financial assets as the overall position unfolds.

Gold is the principal escape from this emerging catastrophe for the dollar. Other currency alternatives are simply unattractive. The next chart from Thorsten Polleit shows the catastrophe that is Germany, at the core of the Eurozone:

The euro is the largest component of the dollar’s TWI by far at over 50%.

When we emerge from our summer lethargy, markets will see something which macroeconomic textbooks say should not happen. Bond yields will be rising, and the gold price will rise as well. Where the textbooks are wrong is to ignore the risks arising from a dollar collapse; risks which the Fed under a new dovish chair will refuse to face, triggering massive flows out of the fiat dollar benefiting gold, which is real money and everyone’s final settlement.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 236

5. COMMODITY REPORT.

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED UP 30.33 PTS OR 0.83%

//Hang Seng CLOSED DOWN 249.25 PTS OR 0.98%

// Nikkei CLOSED UP 729.05 PTS OR 1.71% //Australia’s all ordinaries CLOSED UP 0.69%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1805 OFFSHORE CLOSED DOWN AT 7.1842/ Oil UP TO 63.26 dollars per barrel for WTI and BRENT UP TO 66.17 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1805 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1842 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1805 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1842

HANG SENG CLOSED DOWN 249.25 PTS OR 0.98%

2. Nikkei closed UP 729.05 PTS OR 1.71%

3. Europe stocks SO FAR: MOSTLY ALL GREEN

USA dollar INDEX UP TO 97.75/ EURO RISES TO 1.1681 UP 30 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.568//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.85…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7351/Italian 10 Yr bond yield UP to 3.550 SPAIN 10 YR BOND YIELD UP TO 3.290%

3i Greek 10 year bond yield UP TO 3.412

3j Gold at $3343.00 Silver at: 37.91 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 40 /100 roubles/dollar; ROUBLE AT 80.14

3m oil (WTI) into the 63 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.85// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.565% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8053 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9406 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.285 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.872 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.723 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40980

10 YR UK BOND YIELD: 4.6460 UP 1 PTS

10 YR CANADA BOND YIELD: 3.412 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.945 UP 0 PTS

2a New York OPENING REPORT

2b European opening report

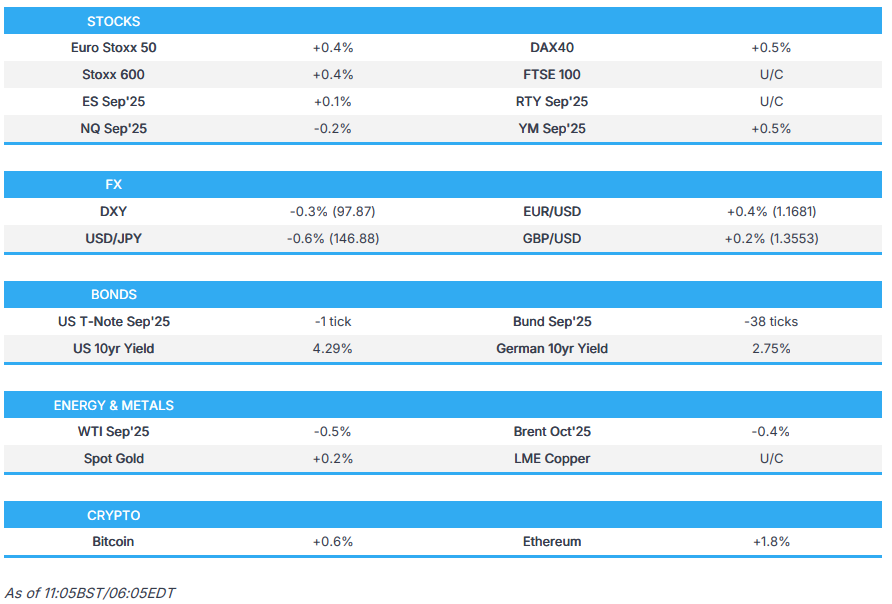

Modestly firmer risk tone into Tier 1 US data points & Alaska summit – Newsquawk US Market Open

Friday, Aug 15, 2025 – 06:33 AM

- Trump and Putin will meet in Alaska at 20:00BST/15:00ET, Trump will then depart just under seven hours later.

- European bourses began with gains, Euro Stoxx 50 +0.4%; follows a mostly higher APAC handover as soft Chinese data was shrugged off.

- US futures firmer, but have drifted off best in the European morning, ES +0.1%; UNH +12% and INTC +4.5% in the pre-market.

- USD gives back some of its PPI-inspired gains, JPY tops the G10 leaderboard after domestic data.

- A contained start for USTs into Tier 1 data points and the Alaska summit, Bunds dipped on the constructive European risk tone.

- Crude benchmarks lower despite the tone and USD, looking to the Putin-Trump meeting; XAU firmer.

- Looking ahead, highlights include US Retail Sales (Jul), US University of Michigan Prelim (Aug), Import/Export Prices (Jul), Industrial Production (Jul), Atlanta Fed GDP, Fed’s Goolsbee, Trump-Putin summit & Press Conference.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

ALASKA SUMMIT

- White House said US President Trump will participate in a bilateral program with the President of the Russian Federation in Alaska at 11:00 AM (15:00EDT/20:00BST) and will depart Alaska at 17:45 (21:45/02:45BST).

- Russian Foreign Ministry says Moscow expects Trump to visit Russia after the Alaska summit, according to Al Arabiya; “We have a clear position that we will present at the Alaska summit and hope to continue the dialogue” and “We do not speculate on anything in the future and we have clear arguments and positions that we will present during the Alaska summit”.

- Click for the Newsquawk preview on the Alaska summit.

TARIFFS/TRADE

- China is warning western companies against stockpiling rare earths or risk even greater shortages, according to FT.

- China’s MOFCOM files WTO lawsuit against Canada, regarding import restrictions on steel and other products.

EUROPEAN TRADE

EQUITIES

- European bourses began with gains, Euro Stoxx 50 +0.4%; with the STOXX 600 and Euro Stoxx 50 both set for a second straight week of advances.

- Follows a mixed Wall St. finish and a mostly higher APAC handover, as China was strong despite domestic data underwhelming for July and the Nikkei 225 was bolstered by Japanese GDP; though, the Hang Seng succumbed after JD.com earnings.

- In Europe, sectors have a positive bias with Basic Resources, Chemicals, and Autos leading; the latter support by the Volkswagen–Xpeng partnership expansion. Utilities hit by Fortum (-2.5%) numbers while Luxury has been tarnished by Chinese retail sales and Pandora (-12%) missing Q2 expectations.

- US futures in the green though have dipped from best across the European morning, ES +0.1%. Supported by a softer dollar, stable yields, and a constructive tone into the Trump–Putin meeting.

- YM +0.5% leads after 13F filings showed Berkshire Hathaway purchased over 5mln shares in UnitedHealth (+12.5%) during Q2. Elsewhere, Intel (+4.5%) gains in the pre-market after a Bloomberg report just before the US close that the Trump administration is in talks to take a stake, in order to support the Ohio chip facility.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is giving back some of its PPI-inspired gains, after the DXY briefly eclipsed its 200 DMA at 98.10 on Thursday. Currently, the index is towards lows in a 97.85-98.21 band, holding above Thursday’s 97.63 base. Ahead, we look to Retail Sales (headline and control seen slowing to 0.5% and 0.6% M/M respectively). Additionally, UoM, Industrial Production and Import & Export prices scheduled.

- However, the main focus is on the Alaska summit (preview available), though updates on this are not likely to hit until after-hours as the summit commences at 20:00BST/15:00ET.

- EUR is firmer though macro drivers for the bloc are light once again. Focus for the currency on the mentioned summit and US data, as such the dollar-side of the equation may well dictate price action. Currently, EUR/USD is at highs of 1.1688 within Thursday’s 1.1632-1.1715 range.

- USD/JPY under pressure after strong Japanese GDP metrics, with JPY currently topping the G10 leaderboard. Thus far, USD/JPY has delved as low as 146.76 but is still north of the 200DMA @ 146.47 and yesterday’s low @ 146.21.

- As is the case with the EUR, newsflow for the UK is very light. Cable is firmer and above the 1.3550 mark but remains within yesterday’s 1.3520-95 range.

- AUD/USD has made its way back onto a 0.65 handle with a current session peak @ 0.6514 vs. yesterday’s best @ 0.6568. Interim resistance is provided by the 200DMA @ 0.6520. NZD/USD sits towards the bottom end of yesterday’s 0.5908-91 range.

- PBoC set USD/CNY mid-point at 7.1371 vs exp. 7.1852 (Prev. 7.1337).

- CBRT Survey: end-2025 CPI 29.69% (prev. 29.66%)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A contained start to the day for USTs, a session that is bookended by Import Prices/Retail Sales and the Alaska summit. Holding around the unchanged mark in narrow 111-24+ to 111-30+ parameters, matching the low from Thursday and holding just ahead of 111-23 and 111-19+ from Wednesday and Tuesday respectively.

- Similarly, Bunds held around 129.56 opening levels for the first part of the session. However, the benchmark has come under gradual but notable pressure throughout the morning. Down to a 129.19 low and softer by c. 30 ticks at most. No clear or specific catalysts behind the move; instead, it appears to be a function of the constructive European risk tone discussed in Equities.

- For Bunds, if the 129.19 base is taken out, we look to 129.06 from Wednesday and below that the figure and then the 128.98 WTD low Tuesday.

- No specific market-moving newsflow for the UK today, with Gilts conforming to the bearish-bias seen in EGBs though to a lesser extent thus far. Potentially a function of the relatively underperformance seen in the FTSE 100; but, magnitudes are minimal and it is probably not worth reading too much into the action at this point in the session.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks are softer, despite the weaker USD and risk-on tone, as participants sites are firmly set on the summit between US President Trump and Russian President Putin later today; full primer available. In brief, the meeting has been repeatedly downplayed, Trump on Thursday sad there was a 25% chance the meeting is not a success and placed the emphasis on the importance of a 2nd meeting.

- Notably, Trump said a joint press conference is not something that has been discussed yet, a point that contrasts with the line from the WH Press Secretary and other reports heading into the summit.

- WTI currently resides in a 63.42-64.15/bbl range while Brent sits in a USD 66.36-67.06/bbl range, lower by around USD 0.50/bbl but around USD 0.25/bbl off worst levels.

- Spot gold is firmer, nursing some of the losses seen on Thursday amid USD strength and elevated yields post-PPI. XAU at the upper-end of a USD 3332-3348/oz band, within Thursday’s USD 3,329.85-3,374.80/oz range.

- Copper is rangebound but with a modest bullish bias, as the tailwinds from the risk tone have offset the disappointing Chinese data; retail sales (+3.7% Y/Y vs exp. 4.6%), factory output, and investment all slowing; factory and mining production rose 5.7% Y/Y (exp. 5.9%), the weakest since November, reflecting pressure from price war crackdowns and lingering Trump-era tariffs.

- Chile’s Codelco announced the smelter at the El Teniente copper mine has restarted.

- NHC says Erin is forecast to become a Hurricane today.

- Qatar lowers October term price for Al-Shaheen oil to USD 2.52/bbl above Dubai quotes, according to Reuters sources.

- Algeria is nearing a deal with Exxon (XOM) and Chevron (CVX) in a shale gas push, according to Bloomberg.

- LME publishes decision notice on market reports to boost liquidity; LME decided to implement, with some modification, all of the proposals set in the consultation on liquidity. Timeline for measures to come into force is February and March 2026.

- Click for a detailed summary

NOTABLE EUROPEAN HEADLINES

- CNB Minutes (Aug): Governor Michl emphasised the need to keep real rates positive, particularly in a situation of elevated general government deficits

NOTABLE US HEADLINES

- Fed Chair Powell is to speak 10:00EDT/15:00BST on August 22nd at Jackson Hole, according to the Fed schedule.

GEOPOLITICS

- US President Trump reiterated a second meeting with Putin and Zelensky will be more important and thinks they will make peace, while he added the Putin meeting is not a reward and they will get peace in the near future if it is a good meeting.

CRYPTO

- Bitcoin is in the green, at the upper-end of parameters for the day but currently just shy of the USD 120k mark.

APAC TRADE

- APAC stocks predominantly traded in the green after the region mostly shrugged off the indecisive performance seen on Wall St in the aftermath of the much hotter-than-expected PPI report, although the upside was capped overnight amid disappointing Chinese activity data and as participants await the Trump-Putin meeting on Friday.

- ASX 200 extended on record highs with the advances led by outperformance in mining, energy and the utilities sectors.

- Nikkei 225 rallied above the 43,000 level with sentiment lifted following stronger-than-expected Japanese GDP data.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark dragged lower by losses in tech as JD.com’s shares were pressured following a drop in its earnings, while the mainland ultimately weathered the miss on Chinese activity data which showed retail sales fell short of the most pessimistic of analyst forecasts.

NOTABLE ASIA-PAC HEADLINES

- China’s stats bureau said China’s economy maintained a steady trend in July, despite external changes and extreme weather conditions, but added the external environment remains complex and severe. The stats bureau said China is to effectively unlock potential domestic demand and will keep employment, the market and expectations stable, as well as promote interplay between domestic and international economic flows. It also stated that high temperatures and floods in some regions created short-term hits on economic growth in July and the survey-based jobless rate rose in July due to factors including the college graduation season. Furthermore, it said efforts are needed to consolidate the foundation of economic recovery and that China’s exports face some pressure due to external uncertainties and some firms face more difficulties.

DATA RECAP

- Chinese Industrial Output YY (Jul) 5.7% vs. Exp. 5.9% (Prev. 6.8%)

- Chinese Retail Sales YY (Jul) 3.7% vs. Exp. 4.6% (Prev. 4.8%)

- Chinese Urban Investment (YTD)YY (Jul) 1.6% vs. Exp. 2.7% (Prev. 2.8%)

- Chinese Unemployment Rate Urban Area (Jul) 5.2% (Prev. 5.0%)

- Chinese China House Prices MM (Jul) -0.3% (Prev. -0.3%); YY (Jul) -2.8% (Prev. -3.2%)

- Japanese GDP QQ (Q2) 0.3% vs. Exp. 0.1% (Rev. 0.1%)

- Japanese GDP QQ Annualised (Q2) 1.0% vs. Exp. 0.4% (Prev. -0.2%, Rev. 0.6%)

2c) Asian opening report

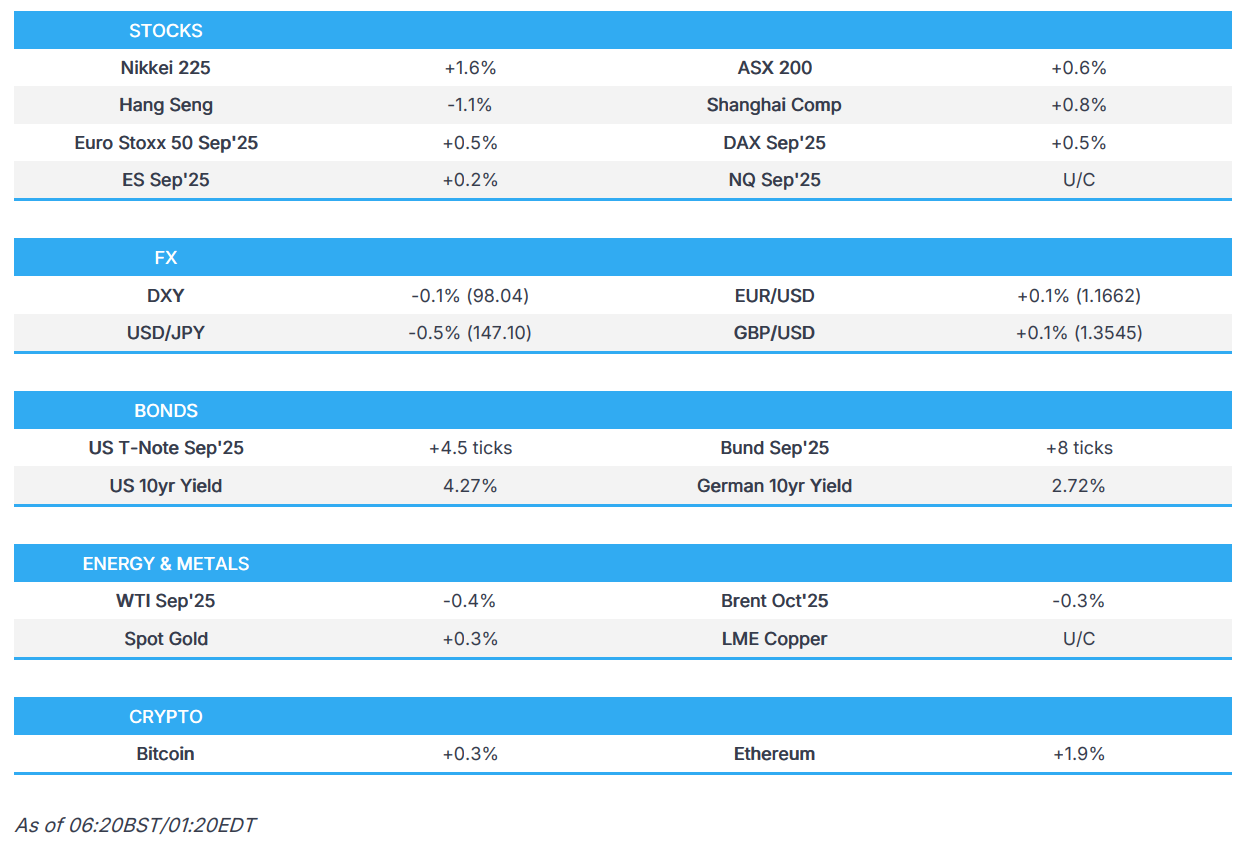

Mostly firmer APAC trade into the Alaska summit – Newsquawk Europe Market Open

Friday, Aug 15, 2025 – 01:52 AM

- APAC stocks predominantly traded in the green after the region mostly shrugged off the indecisive performance seen on Wall St.

- US President Trump will participate in a bilateral program with the President of the Russian Federation in Alaska at 11:00 AM (15:00EDT/20:00BST) and will depart Alaska at 17:45 (21:45/02:45BST), according to the White House.

- Potential Fed Chair pick Zervos backed aggressive interest rate cuts, according to CNBC; Fed Chair Powell is to speak 10:00EDT/15:00BST on August 22nd at Jackson Hole, according to the Fed schedule.

- Nikkei 225 rallied above the 43,000 level and JPY was boosted with sentiment lifted following stronger-than-expected Japanese GDP data.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.5% after the cash market closed with gains of 0.9% on Thursday.

- Looking ahead, highlights include German WPI (Jul), US Retail Sales (Jul), US University of Michigan Prelim (Aug), Import/Export Prices (Jul), Industrial Production (Jul), Atlanta Fed GDP, Trump-Putin summit & Joint Press Conference.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks were choppy and the major indices ultimately finished flat, although the Russell 2000 underperformed, with index futures initially pressured in the premarket as recent bets of a Fed September rate cut were slightly trimmed on inflationary fears following a hot US PPI report.

- However, stocks then staged a recovery during US trade, albeit in a choppy fashion, as participants turned their attention to the Trump-Putin meeting on Friday.

- SPX +0.01% at 6,467, NDX -0.07% at 23,832, DJI +0.01% at 44,927, RUT -1.35% at 2,297.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said Brazil is one of the worst trade partners and imposes ‘tremendous tariffs’ on US goods.

- China is warning western companies against stockpiling rare earths or risk even greater shortages, according to FT.

NOTABLE HEADLINES

- Fed Chair Powell is to speak 10:00EDT/15:00BST on August 22nd at Jackson Hole, according to the Fed schedule.

- Fed’s Barkin (2027 voter) said business sentiment has picked up in some ways, but not yet on the hiring side, while credit card and other data are providing a sense that July consumer data may be stronger. Furthermore, Barkin said it is still early days for companies adapting supply chains to account for tariffs.

- Potential Fed Chair pick Zervos backed aggressive interest rate cuts, according to CNBC.

- US President Trump said inflation is down to a perfect number and there is hardly any inflation at all, while he added that 401(k)s and the stock market are soaring.

- Trump admin is said to discuss the US taking a stake in Intel (INTC) and is discussing with Intel a plan that would bolster Ohio expansion, according to Bloomberg.

APAC TRADE

EQUITIES

- APAC stocks predominantly traded in the green after the region mostly shrugged off the indecisive performance seen on Wall St in the aftermath of the much hotter-than-expected PPI report, although the upside was capped overnight amid disappointing Chinese activity data and as participants await the Trump-Putin meeting on Friday.

- ASX 200 extended on record highs with the advances led by outperformance in mining, energy and the utilities sectors.

- Nikkei 225 rallied above the 43,000 level with sentiment lifted following stronger-than-expected Japanese GDP data.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark dragged lower by losses in tech as JD.com’s shares were pressured following a drop in its earnings, while the mainland ultimately weathered the miss on Chinese activity data which showed retail sales fell short of the most pessimistic of analyst forecasts.

- US equity futures were somewhat mixed overnight following the prior day’s indecisive performance but with Dow futures climbing on the back of a double-digit surge in UnitedHealth shares after-hours as 13F filings showed Berkshire Hathaway purchased over 5mln shares in the insurer during Q2.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.5% after the cash market closed with gains of 0.9% on Thursday.

FX

- DXY marginally softened but remained above the 98.00 level after having recently climbed on the back of the hot PPI data, which exceeded all analyst expectations and saw a slight unwinding of Fed rate cut bets although money market pricing is still heavily leaning towards a 25bps rate cut in September, but it is no longer fully priced in.

- EUR/USD regained some composure after it recently gave way to the resurgence in the dollar with the single currency not helped by the mixed data releases from the EU.

- GBP/USD attempted to claw back some losses after retreating from resistance just shy of the 1.3600 level yesterday despite firmer-than-expected UK GDP data.

- USD/JPY pulled back overnight with the Japanese currency supported following stronger-than-expected Japanese GDP.

- Antipodeans languished around this week’s lows with price action constrained following disappointing Chinese activity data.

- PBoC set USD/CNY mid-point at 7.1371 vs exp. 7.1852 (Prev. 7.1337).

- Russian government abolished mandatory repatriation and sale of foreign currency proceeds by exporters, according to Interfax.

FIXED INCOME

- 10yr UST futures got some slight reprieve after yesterday’s data-triggered bear flattening that saw prices slump beneath the 112.00 level, while participants now await more US data releases, including Retail Sales, Industrial Production, Empire State Manufacturing, University of Michigan, Export & Import prices, as well as the US-Russia summit in Alaska.

- Bund futures attempted to pick themselves up from the prior day’s trough after falling back beneath the 130.00 level.

- 10yr JGB futures were lacklustre with demand hampered by stronger-than-expected GDP data and after a weaker-than-previous 10yr inflation-indexed JGB auction.

COMMODITIES

- Crude futures paused after recent advances heading into the Trump-Putin meeting and with the White House tempering expectations for any breakthrough at today’s talks.

- Russian Deputy PM Novak supported the energy ministry’s idea to extend the ban on gasoline exports through September.

- Spot gold nursed some losses after declining yesterday alongside a firmer dollar and higher yields due to the hot PPI data.

- Copper futures were rangebound as tailwinds from the mostly positive risk tone were offset by disappointing Chinese data.

- Chile’s Codelco announced the smelter at the El Teniente copper mine has restarted.

CRYPTO

- Bitcoin gradually rebounded from the prior day’s trough and returned to above the USD 119k level.

NOTABLE ASIA-PAC HEADLINES

- China’s stats bureau said China’s economy maintained a steady trend in July, despite external changes and extreme weather conditions, but added the external environment remains complex and severe. The stats bureau said China is to effectively unlock potential domestic demand and will keep employment, the market and expectations stable, as well as promote interplay between domestic and international economic flows. It also stated that high temperatures and floods in some regions created short-term hits on economic growth in July and the survey-based jobless rate rose in July due to factors including the college graduation season. Furthermore, it said efforts are needed to consolidate the foundation of economic recovery and that China’s exports face some pressure due to external uncertainties and some firms face more difficulties.

- Japan is to propose an Africa-Indian Ocean logistics network for trade and resources, according to Nikkei.

DATA RECAP

- Chinese Industrial Output YY (Jul) 5.7% vs. Exp. 5.9% (Prev. 6.8%)

- Chinese Retail Sales YY (Jul) 3.7% vs. Exp. 4.6% (Prev. 4.8%)

- Chinese Urban Investment (YTD)YY (Jul) 1.6% vs. Exp. 2.7% (Prev. 2.8%)

- Chinese Unemployment Rate Urban Area (Jul) 5.2% (Prev. 5.0%)

- Chinese China House Prices MM (Jul) -0.3% (Prev. -0.3%)

- Chinese China House Prices YY (Jul) -2.8% (Prev. -3.2%)

- Japanese GDP QQ (Q2) 0.3% vs. Exp. 0.1% (Rev. 0.1%)

- Japanese GDP QQ Annualised (Q2) 1.0% vs. Exp. 0.4% (Prev. -0.2%, Rev. 0.6%)

GEOPOLITICS

MIDDLE EAST

- Iran said it is working with Russia and China to stop European sanctions, according to journalist Elster.

RUSSIA-UKRAINE

- US President Trump reiterated a second meeting with Putin and Zelensky will be more important and thinks they will make peace, while he added the Putin meeting is not a reward and they will get peace in the near future if it is a good meeting.

- White House said US President Trump will participate in a bilateral program with the President of the Russian Federation in Alaska at 11:00 AM (15:00EDT/20:00BST) and will depart Alaska at 17:45 (21:45/02:45BST).

3A NORTH KOREA/SOUTH KOREA

SOUTH KOREA//NORTH KOREA/

3B JAPAN/

3C CHINA

CHINA

4. European affairs and NATO

UK

British People Have Had Enough…

Friday, Aug 15, 2025 – 03:30 AM

Authored by Steve Watson via Modernity.news,

In a striking display of public discontent, close to 750,000 people at time of writing have signed an official parliamentary petition demanding an immediate general election in the UK.

Titled “Call an immediate general election,” the petition argues that the public seeks urgent change from the current Labour government, which won power just over a year ago in July 2024.

Under UK rules, any petition surpassing 100,000 signatures triggers consideration for a parliamentary debate, a threshold this one has far exceeded—it has also prompted a government response, with a debate now pending.