099 H DEUTSCHE BANK AG 134

118 C MACQUARIE FUTURES US 3

118 H MACQUARIE FUTURES US 3

167 C MAREX 247

285 C NANHUA USA-HK 8

323 C HSBC 62

435 H SCOTIA CAPITAL (USA) 13

657 H MORGAN STANLEY 160

661 C JP MORGAN SECURITIES 148

709 C BARCLAYS 38

737 C ADVANTAGE FUTURES 1 2

905 C ADM 3

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 411 CONTRACTs NOTICES FOR 41,100 OZ or 1.278 TONNES

total notices so far: 30,122 contracts for 3,012,200 OR 93.692 tonnes)

SILVER NOTICES:0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1720 CONTRACTS (NOTICES) for 8.600 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 26.345 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 15,000 OZ QUEUE JUMP//NEW STANDING ADVANCES AT 8.740 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE MONTH’S QUEUE JUMP OF 37.353 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK //NEW STANDING ADVANCES TO 97.90 TONNES OF GOLD (INCLUDES ALL MONTHLY QUEUE JUMPS) +10.4932 TONNES EX.FOR RISK = 108.3932 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 109.375 TONNES QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS 1667 CONTRACTS OI TO 158,722 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 250 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1677 CONTRACTS AND ADD TO THE 250 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF 1917 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR TINY GAIN IN PRICE OF $0.06 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 9.585 MILLION PAPER OZ

OCCURRED WITH OUR $0.06 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 0.74 PTS OR 0.02%

//Hang Seng CLOSED DOWN 53.95 PTS OR 0.21%

// Nikkei CLOSED DOWN 168.02 PTS OR 0.38% //Australia’s all ordinaries CLOSED DOWN 0.76%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1821 OFFSHORE CLOSED DOWN AT 7.1855/ Oil DOWN TO 62.90 dollars per barrel for WTI and BRENT DOWN TO 65.90 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1821 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1855 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A TINY SIZED 158 CONTRACTS TO 439,893 OI DESPITE OUR LOSS IN PRICE OF $4.05 WITH RESPECT TO MONDAY’S // TRADING.. WE LOST NO NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1447 ). WE HAD CONSIDERABLE T.A.S. LIQUIDATION //FRIDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1289 CONTRACTS (OR 4.009 TONNES). WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FRIDAY. THE CROOKS COULD NOT FLEECE ANY OF OUR NET LONGS AS THE COMEX LEVEL OI WAS EXTREMELY LOW AND THUS VERY VERY STICKY: AND AS SUCH THE OI ROSE A BIT DESPITE OUR LOSS IN PRICE.

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY:

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AS MENTIONED ABOVE: TONIGHT WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FOR AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST;

EARLY THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE FOR AUGUST OF A MONSTER 1750 CONTRACTS FOR 175,000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. WITH ALL THE CHAOS AT THE COMEX IT WAS NO SURPRISE THAT THEY ISSUED THEIR SECOND EXCHANGE FOR RISK, AUG 10 TOTALLING 776 CONTRACTS OR 77,600 OZ (2.418 TONNES).MUCH TO MY ANGER TONIGHT, THE CME ANNOUNCED ITS 3RD EXCHANGE FOR RISK OF 848 CONTRACTS TOTALLING 84,800 OZ OR 2.637 TONNES.

THUS THE TOTAL FOR AUGUST IS 3374 CONTRACTS OR 337,400OZ OR 10.4932 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS. THE RECEPIENT OF THIS LARGESS IS PROBABLY NOW THE BANK OF ENGLAND AS WE HAVE JUST LEARNED THAT THE FRBNY HAS RETURNED ONLY 14,000 OZ AS THEIR LOANS TO THE BIS REMAIN AT 34+ TONNES.(JULY 31 FIGURES) IT SEEMS NOW THAT THE BANK OF ENGLAND IS IN QUITE A HURRY TO GET ITS GOLD BACK!! (AND PROBABLE OWNER OF THOSE EXCHANGE FOR RISK CONTRACTS)

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 3 ISSUANCES FOR A MONSTER 3374 CONTRACTS OR 337,400 OZ ( 10.4932 TONNES)

AS I EXPLAINED ABOVE,:THE RECPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1926 CONTRACTS DESPITE OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 860 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED THREE WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 37.353 TONNES +10.4932 TONNES EX FOR RISK (3 ISSUANCES) //NEW STANDING 108.3932 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 235 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE 37.353 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES AND THEN AUGUST 12: 2.637 TONNES:/NEW STANDING ADVANCES TO 108.3932 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1447 EFP CONTRACT WAS ISSUED: : /DEC 1447 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1447 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- LITTLE LIQUIDATION OF OUR T.A.S. SPREADERS//FRIDAY

- MONTH END SPREADERS WILL APPEAR ON THE LAST WEEK OF AUGUST.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A SMALL SIZED SIZED 860 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING SMALL LOSS OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S FIRST THREE ISSUANCES OF EXCHANGE FOR RISK FOR 10.4932 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 1.058 TONNES TO WHICH WE ADD THURSDAY’S AUG 7 HUGE 5.4432 EXCHANGE FOR RISK, SATURDAY’S//MONDAY AUG 10 STRONG 776 CONTRACT ISSUANCE (77600 OZ) FOR 2.413 TONNES AND THEN WEDNESDAY.S AUGUST 12 FOR 2.637 TONNES/// TOTAL EX FOR RISK AUGUST = 10.4932 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

97.90 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

EQUALS

108.3932 TONNES TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A $4.05/ /) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD LITTLE T.A.S. SPREADER LIQUIDATION ///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH LAST THURSDAYS TRADING/RAID!.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: THREE SO FAR, AUGUST 7 THROUGH AUG 12 AT 3374 CONTRACTS FOR 337,400 OZ (10.4932 TONNES OF GOLD) TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 10.4932 TONNES

THUS 97.90 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 10.4932 TONNES = 108/3932 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE GAIN A FAIR SIZED TOTAL OF 4.009 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD LAST AUG 8 RECORD BREAKING QUEUE JUMP OF 10.8775 TONNES OF GOLD ON TOP OF AUG 12 1.7604 TONNES QUEUE JUMP AND THEN WEDNESDAY;S AUG 13 MASSIVE QUEUE JUMP OF 3.527 TONNES AND THEN THURSDAY AUG 14 HUGE 2.463 TONNES QUEUE JUMP AND FRIDAY;S AUG 15 QUEUE JUMP OF .7030 TONNES AND THEN SATURDAY’S 1.617 TONNE QUEUE JUMP AND THEN TODAY’S 1.058 QUEUE JUMP TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK/PRIOR FOR 10.4932 TONNES FOR RISK//NEW STANDING ADVANCES TO 108.3932 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.05

WE HAD 637 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 1289 CONTRACTS OR 128,900 0Z (4.009 TONNES)

confirmed volume MONDAY 129,128 contracts// extremely poor//everybody vacating the comex???

speculators have left the gold arena

END

INITIAL GOLD COMEX

END

INITIAL GOLD COMEX

AUGUST CONTRACT MONTH

AUGUST98 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2 entries i) Out of Loomis: 32,015.190 oz ??? same amt going into Loomis/are they crazy ii) Out of Asahi: 42,128.330 oz total withdrawal: 74,143.520 oz . |

| Deposit to the Dealer Inventory in oz | 1 ENTRY i) Into the dealer Loomis 24,702.47 oz total deposit: 24,702.47 oz |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRY i) into Loomis customer acct: 32,015.190 oz total entry: 32,015.190 oz xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 411 notice(s) 41100 OZ 1.278 TONNES |

| No of oz to be served (notices) | 1353 contracts 135300 OZ 3.855 TONNES |

| Total monthly oz gold served (contracts) so far this month | 30,122 notices 2,971,100 oz 93.692 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

1 ENTRY

i) Into the dealer Loomis 24,702.47 oz

total deposit: 24,702.47 oz

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

1 ENTRY

i) into Loomis customer acct: 32,015.190 oz

total entry: 32,015.190 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

2 entries

i) Out of Loomis: 32,015.190 oz ???

same amt going into Loomis/are they crazy

ii) Out of Asahi: 42,128.330 oz

total withdrawal: 74,143.520 oz

adjustments: 1

a) out of Brinks 15,432.480 oz/customer acct to dealer account

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 1764 CONTRACTS FOR A LOSS OF ONLY 82 CONTRACTS

WE HAD 422 CONTRACTS SERVED ON MONDAY SO WE GAINED A HUGE SIZED 340 CONTRACTS OR 34,000 OZ OF GOLD (1.058 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND.. THIS ALSO REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD AND THEIR APPETITE FOR THIS GOLD IS UNABATED!

SEPT LOST 239 CONTRACTS TO 4710

OCTOBER LOST 418 CONTRACTS UP TO 61,539

We had 411 contracts filed for today representing 41,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 411 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 148 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (30,122 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 1764 CONTRACTS) minus the number of notices served upon today (411 x 100 oz per contract) equals 3,147,500 OZ OR 97.90 TONNES TO WHICH WE ADD OUR THREE ISSUANCES OF 10.4932 TONNES OF EXCHANGE FOR RISK/AUG 7 , 11 AND 12TH = 108.3932 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (30,122 x 100 oz +we add the difference for front month of AUGUST (1764 OI} minus the number of notices served upon today (411 x 100 oz) which equals 3,147,500 OZ OR 97.90 TONNES + 10.4932 TONNES EX FOR RISK = 108.3932 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 108.3932 TONNES WHICH IS HUGE FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,029,086.946 oz 63.11 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,629,130.617 oz

TOTAL REGISTERED GOLD 21,299,847.665 or 662.51 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,329.282.952 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,270,761 oz ((REG GOLD- PLEDGED GOLD)= 599.40tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE AUGUST 2025 SILVER CONTRACT//INITIAL

AUGUST 19 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 entries: |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 DEPOSIT ENTRY/CUSTOMER ACCOUNT i)Into Loomis 600,232.190 oz total deposit: 600,232.190 oz |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ |

| No of oz to be served (notices) | 25 contracts (0.125 MILLION oz) |

| Total monthly oz silver served (contracts) | 1720 Contracts (8.60 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

0 DEPOSIT ENTRY/CUSTOMER ACCOUNT

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i)Into Loomis 600,232.190 oz

total deposit: 600,232.190 o

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

0 entries:

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 190.400 MILLION OZ//.TOTAL REG + ELIGIBLE. 508.651 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 28 OPEN INTEREST CONTRACTS FOR A GAIN OF 3 CONTRACTS. WE HAD 0 CONTRACTS SERVED ON MONDAY SO WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ WILL STAND AT THE COMEX HAVING UNDERGONE A SMALLL QUEUE JUMP

SEPTEMBER LOST 2632 CONTRACTS DOWN TO 64,853 CONTRACTS.

OCTOBER GAINED 12 CONTRACTS TO 829

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or NIL oz

CONFIRMED volume; ON MONDAY 48.449 POOR//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1720 X5,000 oz = 8.600 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (28) AND the number of notices served upon today (0 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1720) Notices served so far) x 5000 oz + OI for the front month of AUGUST(28) minus number of notices served upon today (0)x 5000 oz equals silver standing for the AUGUST contract month equating to 8.740 MILLION OZ .

New total standing: 8.740 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.400 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/508.151 million. 41.33%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 965.37 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 493.726 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/S

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

Bond collapse is coming

Long maturity bond yields are breaking out on the upside. Steepening global yield curves signal an imminent crisis in all fiat currencies and financial assets, driving gold higher.

| Alasdair MacleodAug 19∙Paid |

Long maturity bond yields are breaking out on the upside. Steepening global yield curves signal an imminent crisis in all fiat currencies and financial assets, driving gold higher.

We know that rising gold prices reflect falling currency values. Having consolidated previous rises for the last four months, gold appears ready to continue its upward trend. At the same time, long maturity bond yields in major credit markets are also signalling further increases. It would appear that these events are linked, and if so, a credit crisis from higher bond yields will undermine all credit values and will be reflected in far higher gold prices.

This article looks at how this credit crisis is likely to evolve.

Introduction

There is increasing concern over government debt, even leading to speculation that the US Treasury will mobilise its gold reserves to alleviate funding difficulties. And there is a growing realisation that President Trump’s spendthrift tendencies will not be covered by tariff revenues and that US debt is increasing at an accelerated rate. Currently at $37.25 trillion, it has increased by over $10 trillion in the last five years and is still accelerating.

It has to be financed at a time of growing reluctance to buy both dollars and longer maturity bonds at current yields. Consequently, government funding is increasingly short-term, notably in US treasuries where the Fed depends disproportionately on bank finance being directed into treasury bills. It is now becoming likely that the trigger point for an upcoming financial and systemic crisis will be a further lurch higher in global government bond yields. Yield is the price of risk, and risks of defaults are rising.

This article looks at government bond markets in the four major currencies. They all tell the same story, which is that long bond yields are going considerably higher, and very soon. Most likely, in the next few weeks yields will break out from their summer torpor, embarking on an unstoppable surge higher. The implications for all financial assets, particularly overvalued equities, are that they will crash. With capricious US tariff policies, it looks alarmingly like a September 1929 redux.

We have an extraordinary mismatch between investment expectations and what is happening to bond yields. Particularly at the long end, maturities are rising again, signalling higher yields to come. First, we look at Germany’s 30-year bund yield:

Germany’s bond market is the marker for the entire Eurozone debt market. After a 10-month consolidation from last October, the 30-year maturity yield is breaking out into new high ground. Over the same time period, the DAX equity index rose by 25% and is close to all-time highs. The kicker in this valuation lunacy is that Germany’s economy is being hollowed out, as respected economist Thorsten Polliet’s recent tweet shows:

Germany’s stock market is being driven by an unsustainable credit bubble, with investors partying on the slopes of an active volcano.

While Germany’s bond market is leading the way to asset destruction in the Eurozone, the US long bond is sending similar signals:

There can be little doubt about the strength of the underlying trend driving yields higher. And when, rather than if, the long bond’s yield leaves 5% behind there appears to be nothing to stop it going considerably higher.

The error made by investors schooled in Keynesian beliefs is to assume that the economy is probably heading into recession, permitting the Fed to accelerate its rate cutting programme as demand for credit declines. But with government borrowing soaring out of control while the means to pay for it (i.e. taxes based on private sector growth) deteriorating, longer maturity bond yields are bound to rise to reflect the very real credit risk of a debt trap. Then it is only a matter of time before the long bond yield goes above 5%, bursting the credit bubble which is fuelling the equity bull market. Since mid-May when the bond yield hit a multi-decade high at 5.1%, the S&P 500 has risen 15% and like Germany’s DAX is close to its all-time high.

The UK’s 30-year long gilt tells the same story, but even more aggressively.

Like the German bund, the long gilt’s yield has such strong rising momentum under it that not only is it already in new high ground, but it is set to accelerate rapidly higher. This timing is particularly awkward, because it looks like creating a financial crisis for the government ahead of the Autumn statement, whose date is yet to be announced but is usually in late-October or early-November.

Japan’s condition is also alarming. Our last chart is of the yield on the 30-year JGB bond:

This JGB’s yield is already rising exponentially, heading significantly higher and will lead the 10-year maturity higher which is the largest holding of the Bank of Japan. Japan’s financial condition, which everyone ignores, is chaotic and a collapse in its financial situation is increasingly inevitable.

Conclusion

We are beginning to see the shape of the next financial crisis. It will be triggered by rising bond yields — collapsing bond markets — and a growing realisation that instead of looking forward to lower interest rates they should be going higher, if the purchasing power of fiat currencies is to be protected.

It creates a dilemma for the four major central banks, because higher interest rates and bond yields will undermine over-valued financial assets and bankrupt zombie corporations faced with refinancing their over-leveraged balance sheets. Counterparty risk will spread rapidly through financial institutions, including banks. Collateral values will fall, forcing banks to liquidate leveraged market positions, potentially driving equities into freefall. And as buyers of last resort, central banks and finance ministries will almost certainly be overwhelmed.

This upcoming crisis marks the end of the fiat currency system. Not only will asset values collapse, wiping out personal wealth, but currency values will fail as well — currencies are simply central bank credit which without fixed rate convertibility into gold depend for their value entirely on its users’ faith in them.

The only escape route from this crisis is to preserve personal wealth as much as possible by holding corporeal money in everyone’s common law, which is physical gold and possibly silver.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 236

5. COMMODITY REPORT.

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 0.74 PTS OR 0.02%

//Hang Seng CLOSED DOWN 53.95 PTS OR 0.21%

// Nikkei CLOSED DOWN 168.02 PTS OR 0.38% //Australia’s all ordinaries CLOSED DOWN 0.76%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1821 OFFSHORE CLOSED DOWN AT 7.1855/ Oil DOWN TO 62.90 dollars per barrel for WTI and BRENT DOWN TO 65.90 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1821 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1855 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1826 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1855

HANG SENG CLOSED DOWN 53.95 PTS OR 0.21%

2. Nikkei closed DOWN 168.02 PTS OR 0.38%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 97.92/ EURO RISES TO 1.1673 UP 6 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.591//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.72…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7749/Italian 10 Yr bond yield UP to 3.598 SPAIN 10 YR BOND YIELD UP TO 3.328%

3i Greek 10 year bond yield UP TO 3.476

3j Gold at $3337.50 Silver at: 38.05 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 11 /100 roubles/dollar; ROUBLE AT 80.21

3m oil (WTI) into the 62 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.72// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.591% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8060 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9410 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.340 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.940 UP 0 BASIS PTS/

USA 2 YR BOND YIELD: 3.767 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.89

10 YR UK BOND YIELD: 4.7480 UP 1 PTS

10 YR CANADA BOND YIELD: 3.490 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 3.01 UP 1 PTS

2a New York OPENING REPORT

Global Stock Rally Fades As Ukraine Talks Continue, Focus Turns To Jackson Hole

Tuesday, Aug 19, 2025 – 08:25 AM

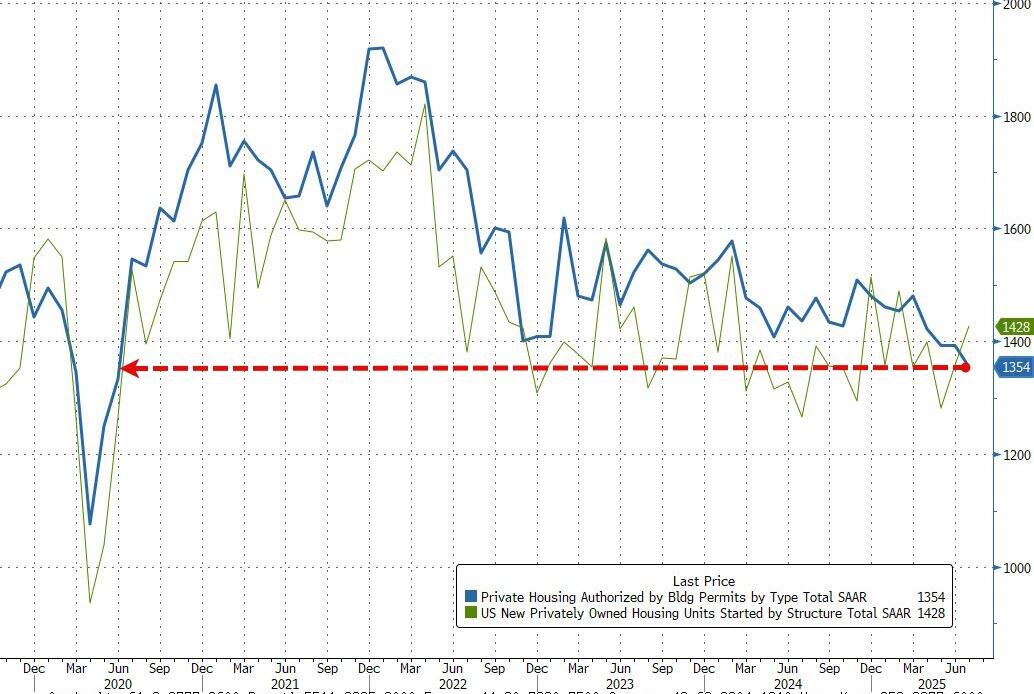

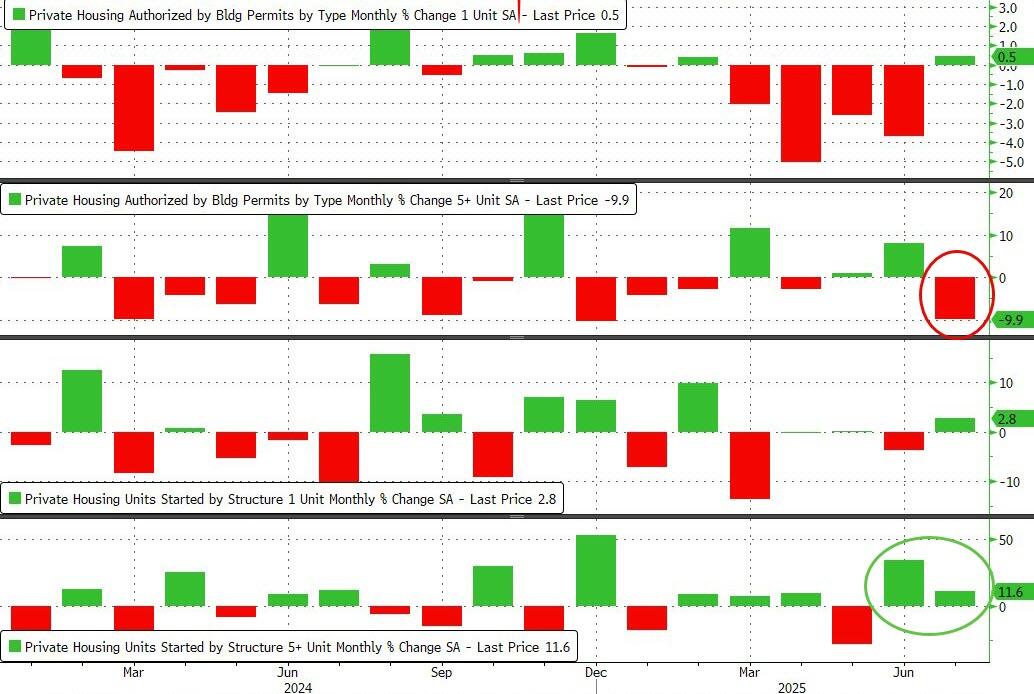

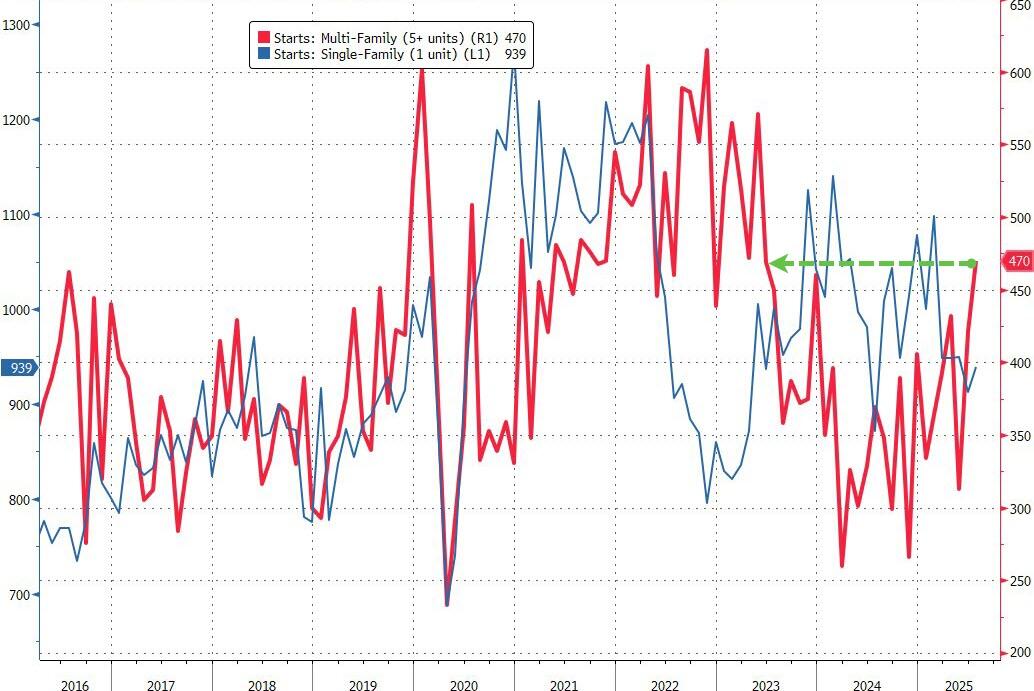

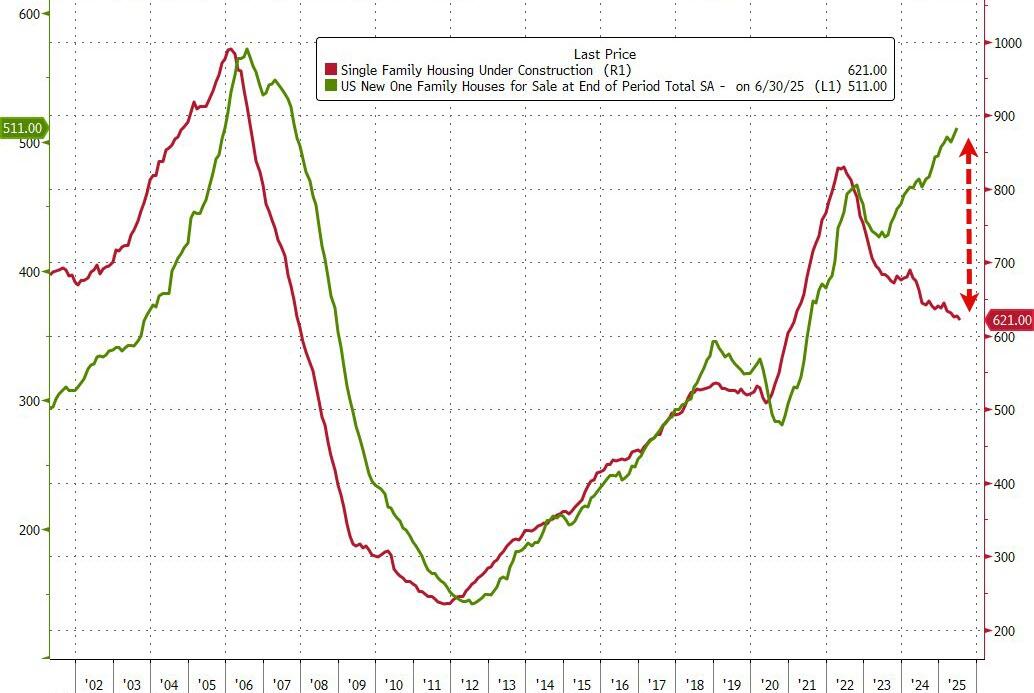

Futures are flat ahead of consumer-sector earnings kicking off today, starting with a miss by Home Depot this morning. As of 8:00am ET, S&P futures were unchanged while Nasdaq futures drop 0.1% as Mag7 names are mostly lower ex-NVDA. Semis are mostly weaker ex-INTC which gained more than 6% on news SoftBank would invest $2 billion in the chipmaker and the US would take a 10% stake. Defensives are slightly outperforming Cyclicals. Europe’s Stoxx 600 rose 0.5% as signs of progress toward a peace settlement in Ukraine lifted sentiment. The dollar nudged lower. Treasuries eked out gains after S&P Global Ratings affirmed its AA+ long-term rating for the US, with the 10-year rate falling one basis point to 4.32%. Commodities are weaker dragged lower by energy despite strength in precious and Ags. BBG flags a trade escalation from Friday where Trump expanded the metals tariffs to more than 400 consumer goods, including baby gear, and there is no exemption for goods already in transit; the article states this impacting $328bn of goods based on 2024 trade levels vs. $191bn before the expansion and is more than 6x levels from 2018. Today’s macro data focus is on housing starts and building permits; XHB has lagged SPX YTD by 138bp but has outperformed the SPX by 912bp over the last month.

In premarket trading, Mag 7 stocks are mostly lower (Nvidia +0.3%, Tesla -0.2%, Microsoft -0.05%, Alphabet -0.2%, Apple -0.2%, Amazon -0.2%, Meta -0.3%).

- Fabrinet (FN) falls 8% after the optical device maker said it expects to see a sequential dip in datacom segment revenue in its fiscal 1Q, citing supply constraints for some critical components.

- Home Depot (HD) shares reversed a 2% drop after a closely watched sales measure missed estimates last quarter, suggesting consumers are holding back on major purchases.

- Intel (INTC) is up 5% after SoftBank Group Corp. agreed to buy $2 billion of the chipmaker’s stock.

- Iovance (IOVA) jumps 15% after the biotech said Health Canada approved Amtagvi to treat certain patients with unresectable or metastatic melanoma.

- Nexstar Media Group (NXST) rises 2% after agreeing to acquire all outstanding shares of Tegna (TGNA) for $22 per share in a cash deal valued at $6.2 billion. Tegna shares are up 3%.

- Opera Limited (OPRA) rise 3% after the software firm boosted its revenue guidance for the full year; the guidance beat the average analyst estimate.

- Palo Alto Networks (PANW) gains 6% after the security software company reported fourth-quarter results that beat expectations and gave a strong outlook.

- Peabody Energy (BTU) rises 7% after deciding to walk away from a $3.8 billion deal to buy Anglo American Plc’s steelmaking coal business following a fire at an Australian mine.

- Viking Therapeutics (VKTX) slumps 35% after the company announced top-line results from the Phase 2 clinical trial of its oral obesity drug.

The global stock rally has stalled as investors await new twist and turns in the Ukraine drama, awaited this Friday’s Jackson Hole symposium where Jerome Powell is set to unveil a new policy framework (and usher in a September rate cut), and watched earnings from the biggest US retailers. Money markets are currently betting the Fed will deliver its first rate cut for the year in September, as labor-market weakness outweighs inflation risks, with another move expected before year-end. Oil slipped as traders weighed the outlook for an end to the conflict in Ukraine and a potential future supply increase of Russian crude. Brent fell below $66 a barrel, extending a decline for the month to around 9%.

“With much of it priced in already, equities may need a new catalyst,” said Ipek Ozkardeskaya, a senior analyst at Swissquote Bank. “August through October is seasonally soft, and rising long-term bond yields could tempt investors to pocket recent gains.”

In other corporate news, Nvidia is said to be preparing a more powerful chip for China, according to Reuters. Apple is said to be expanding iPhone production in India as it seeks to lessen its reliance on China for US-bound models, Bloomberg News reported. The company is producing all four iPhone 17 models in India ahead of their debut next month, marking the first time that all new variations will ship from the South Asian country from the get-go. Tesla priced its updated, six-seat Model Y sport utility vehicle in the same range as local rival Li Auto’s extended-range L8 model, to win over middle-class families in China’s hyper-competitive market. Shein is said to be considering moving its base back to China to help sway Beijing authorities to sign off on its plans to go public.

In Europe, the Stoxx 600 climbed 0.6% to its highest level since March after Bloomberg reported US and European officials have started work on a Ukraine’s security plan. That is expected to include a package of guarantees that will open a path to a landmark meeting between presidents Vladimir Putin and Volodymyr Zelenskiy. Sweden’s Ambea and Sweco are among the biggest outperformers, on earnings and a broker upgrade, respectively. Defense stocks drop on Ukraine news, while London- and Warzaw-listed stocks exposed to the war-torn country gain. Here are the biggest movers Tuesday:

- Ambea gains as much as 9.5% after the Swedish care provider reported net sales for 2Q that beat the average analyst estimate. DNB Carnegie says the report shows “continued strong momentum” for the company

- Sweco gains as much as 5.2%, to the highest in more than a month, after DNB Carnegie reinstated coverage of the Swedish engineering consultancy with a price target just shy of the current Street-high

- Huber+Suhner shares rise as much as 9.8% to a record after the Swiss electrical components firm reported Ebit for the first half-year that beat estimates. Vontobel sees consensus estimates moving upward

- Shares in Ukraine-exposed companies surge in Warsaw and London amid revived hopes of a peace deal after Ukrainian President Zelenskiy and European leaders met US President Trump on Monday

- Odfjell Drilling gains as much as 11% and reaches a new all-time high after reporting second-quarter results. DNB Carnegie said the Norwegian offshore drilling firm’s report showed “continued strong performance”

- Applied Nutrition shares rise as much as 12%, the most on record, after the health supplements company said it anticipates revenue to be ahead of market expectations

- European defense companies’ shares are lower Tuesday amid prospects for a potential meeting between Ukrainian President Volodymyr Zelenskiy and Russian President Vladimir Putin

- DocMorris drops as much as 14% following the Swiss-based online pharmacy company’s first-half results. Analysts note that a significant step-up will be required in the second half to achieve the unchanged guidance

- Coloplast falls as much as 3.7%, the most in a month, after the Danish wound and ostomy care group reported disappointing third-quarter earnings, with sales and profit missing consensus estimates

- International Workplace shares slide as much as 18%, the most in three years, after guiding that full-year earnings are likely to come in toward the lower end of the range expected by analysts due to investments

- Basilea shares give up initial gains and head lower as much as 6.5% after the Swiss bio-pharmaceutical company reported results that ZKB analysts said showed a “disappointing” cashflow performance

- Skan shares fall as much as 12%, the most since July 2021, after the health care supplier reported weaker-than-expected results for the first half of 2025, with the Ebitda dropping to CHF0.9 million ($1.1 million)

Earlier in the session, Asian stocks declined for a second day, with South Korea and Australia leading losses, as markets take a breather after an extended rally. The MSCI Asia Pacific Index fell 0.2%, with Sydney-listed biotech CSL the biggest drag as it posted the worst decline on record after disappointing earnings. Equities also dropped in tech-heavy Hong Kong and Taiwan, while benchmarks advanced in Singapore, Malaysia and Vietnam. A gauge of Chinese equities reversed early gains after notching a record close Monday. Sentiment remains bullish, as gains from institutional money chasing these stocks bolster sentiment toward emerging markets and the broader Asian region. Indian shares also moved higher, on track for a fourth session of gains amid thawing relations with China and expectations of a boost in consumption from planned tax cuts.

In FX, the Bloomberg Dollar Spot Index is flat while the Swedish krona takes top spot among G-10 peers, rising 0.3% against the greenback.

Treasuries eked out gains after S&P Global Ratings affirmed its AA+ long-term rating for the US, with the 10-year rate falling one basis point to 4.32%. Treasury auctions resume Wednesday with $16 billion 20-year new issue; an $8 billion 30-year TIPS reopening is slated for Thursday.

In commodities, Brent crude futures fell 1% to near $66 a barrel extending a decline for the month to around 9%, as traders weighed the outlook for an end to the conflict in Ukraine and a potential future supply increase of Russian crude. European natural gas futures are down 0.4%.

Looking at today’s calendar, the data slate includes July housing starts and building permits (8:30am New York time). Fed speaker slate includes Governor Bowman (10am and 2:10pm).

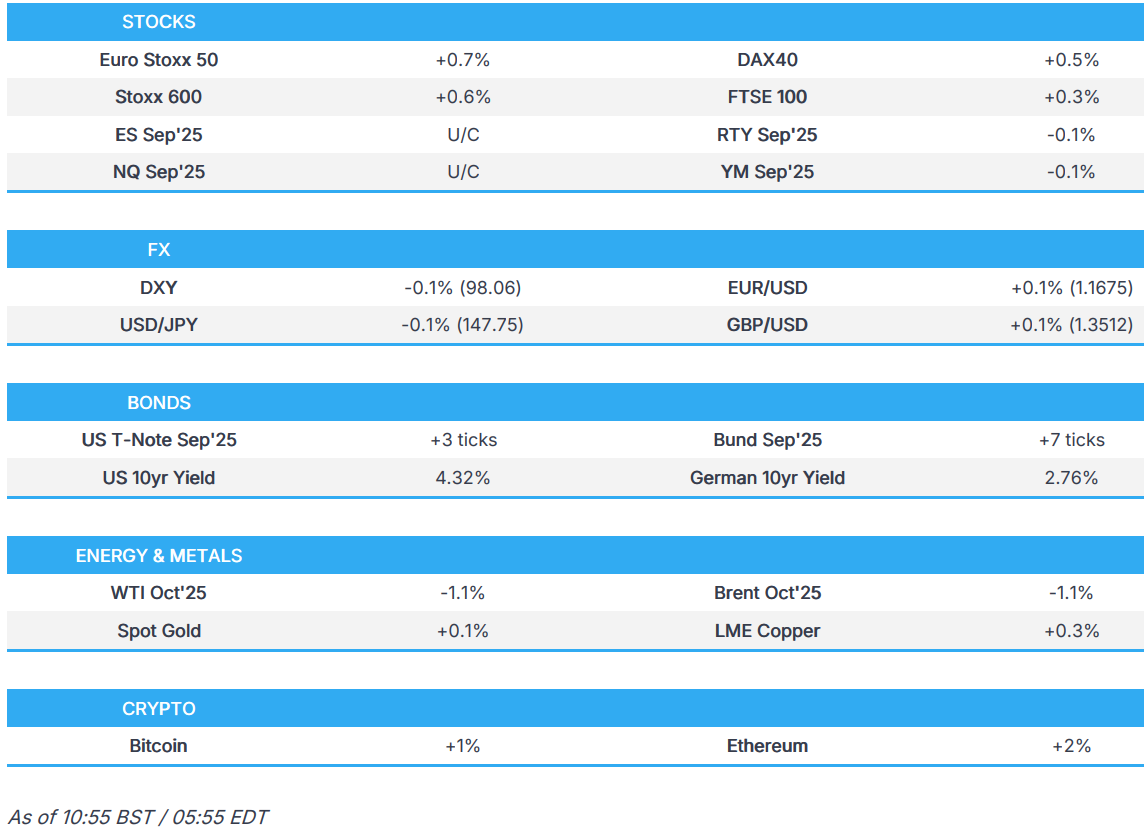

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini little changed

- Russell 2000 mini -0.2%

- Stoxx Europe 600 +0.5%

- DAX +0.4%

- CAC 40 +0.8%

- 10-year Treasury yield little changed at 4.33%

- VIX little changed at 14.96

- Bloomberg Dollar Index little changed at 1205.06

- euro +0.1% at $1.1675

- WTI crude -1.1% at $62.75/barrel

Top Overnight News

- President Trump on Monday urged Ukrainian President Volodymyr Zelensky and Russian President Vladimir Putin to meet face to face with him at a peace conference in a long shot U.S.-led bid to end the 3½-year-long war in Ukraine. Bloomberg reports that a summit between Putin and Zelenskiy may take place within two weeks, but the Kremlin has yet to confirm. WSJ, BBG

- S&P Global Ratings has affirmed the credit ratings of the U.S., saying it expects robust revenues from the Trump administration’s newly instituted tariff regime to help offset the expected fiscal deterioration resulting from recent legislative changes. WSJ

- Ukraine will promise to buy $100bn of American weapons financed by Europe in a bid to obtain US guarantees for its security after a peace settlement with Russia. FT

- Intel jumped premarket (INTC +5.8% pre) after SoftBank agreed to invest $2 billion, paying $23 per share — a slight discount to Intel’s last close. The deal would amount to about a 2% stake in the chipmaker. BBG

- NVDA is developing a new AI chip for China based on its latest Blackwell architecture that will be more powerful than the H20 model it is currently allowed to sell there, two people briefed on the matter said. RTRS

- Trump’s tariff war is speeding Beijing’s trade and investment drive into developing nations, potentially paving the way for a China-led trade order, S&P Global said. BBG

- Japan’s 20-year bond auction saw weaker demand than previous months, as investors remained wary of long-term debt given risks from rising spending and tax cuts. BBG

- Apple Inc. is expanding iPhone production in India at five factories, including a pair of recently opened plants, as it seeks to lessen its reliance on China for US-bound models. BBG

Trade/Tariffs

- Brazil’s government submitted its response to the US Section 301 investigation and said it urges the USTR to reconsider the initiation of the Section 301 investigation and to engage in constructive dialogue. It was separately reported that Brazil’s Finance Minister Haddad said Brazil is deadlocked with the US over 50% tariffs and reduction in high levies depends on Washington being open to talks, according to FT.

- India exempted import duty on cotton between August 19th to September 30th, according to a government order.

- Japan-India framework to focus on chips, mineral resources, and AI, according to reports citing Nikkei

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following the ultimately flat performance stateside amid a lack of fresh macro catalysts, as focus centred on geopolitical updates and amid cautiousness ahead of Powell’s speech at Jackson Hole on Friday. ASX 200 pulled back from record highs with heavy losses in healthcare as CSL shares fell by a double-digit percentage after the announcement to spin-off its flu vaccine business and cut 15% of its workforce, while tech was at the other end of the spectrum and miners also gained post-BHP earnings despite the mining giant reporting a 26% drop in FY underlying profit. Nikkei 225 swung between gains and losses after failing to sustain the initial upward momentum that had lifted the index to a fresh record high. Hang Seng and Shanghai Comp kept afloat following a firm liquidity effort by the PBoC which injected CNY 580bln through its 7-day reverse repo operation, while there were also comments on Monday by Chinese Premier Li who said the nation should consolidate and expand the positive trend in the economy, as well as stabilise market expectations and should continue to stimulate consumption potential.

Top Asian News

- China’s Foreign Minister Wang Yi held talks with his counterpart in India and said their countries should establish a correct strategic understanding, as well as regard each other as partners and opportunities, not as rivals or threats, while he added that China is ready to uphold the principle of cordiality and mutual benefit.

- China Jan-July Fiscal Revenue +0.1% Y/Y; Expenditures +3.4% Y/Y.

- XPeng (9868 HK) Q2 (CNY) Adj. EPS -0.20 (exp. -0.36, prev. -0.19 Y/Y), Revenue 18.27bln (exp. 18.11bln); Q3 deliveries: Vehicles to be between 113-118k.

- Russian Defence Ministry says they have conducted strikes on oil refinery supplying fuel to Ukrainian armed forces, according to Ifax.

European bourses (STOXX 600 +0.4%) opened modestly firmer across the board, with cautious optimism stemming from the recent US President Trump/Ukrainian President Zelensky/EU Leaders meeting. On that, Trump described it as a very good meeting, while he also called Russian President Putin to begin arrangements for a Putin-Zelensky meeting, which would be followed by a trilateral meeting with Trump. Reportedly, security agreements were discussed; on territorial developments, Zelensky suggested it would be a discussion between Ukraine and Russia. As the morning progressed, stocks have gradually climbed higher and currently sit at highs. European sectors hold a positive bias, but the breadth of the market is fairly narrow. Consumer Products takes the top spot, joined closely by Basic Resources and Retail; nothing really company-specific is driving the upside in these sectors, but largely benefiting from the slightly positive risk tone.

Top European News

- UK’s ONS says Friday’s scheduled retail sales data release has been delayed until September 5th

FX

- DXY is relatively rangebound this morning with a slight negative bias and price action contained to either side of the 98.00 mark. Currently in a narrow 97.99-98.32 parameter vs Monday’s 97.77-98.19 range. The theme over the last couple of days has been geopolitics, with deliberations over the Russia-Ukraine war in Washington concluding for now. Overall, there has been no breakthrough in Monday’s discussions, although talks may advance with a possible Zelensky–Putin meeting in two weeks, their first since the war began. Despite the mild optimism, betting markets remain pessimistic, with Polymarket pointing to a 38% chance of a Russia-Ukraine ceasefire this year.

- EUR/USD is holding a mild upward bias after finding support at its 50 DMA (1.1641) following Monday’s slide under 1.1700, with very little newsflow from the bloc aside from the comments from various European leaders following the multilateral meeting on Ukraine at the White House. EUR/USD resides in a current 1.1640-1.1685 range with the 50 DMA at 1.1641.

- Modest gains in the JPY, albeit in tandem with USD weakness, with little in terms of fresh catalysts from Japan. USD/JPY trades in either side of 148.00 in a 147.53-148.11 parameter, vs Monday’s 147.06-147.99 range, with the 50 DMA at 146.60 and the 200 DMA at 149.22.

- GBP continues to struggle for direction as newsflow from the UK remains very quiet, although there were reports that UK Chancellor Reeves is considering replacing stamp duty with a new property tax. GBP/USD trades in a 1.3486-1.3529 range (vs Monday’s 1.3501-1.3568), with the 50 DMA at 1.3501 today.

- Antipodeans are essentially flat vs the Dollar today, continuing the tentative risk tone seen in overnight trade.

- PBoC set USD/CNY mid-point at 7.1359 vs exp. 7.1846 (Prev. 7.1322)

Fixed Income

- A contained start to the day for USTs after the pressure that began towards the end of the European day and intensified into the mid-US morning. The pullback occurred as the White House meetings got underway and, ultimately, as the tone from the meeting was a positive one with progress made towards a trilateral summit and then security guarantees. On the guarantees, they are seemingly set to be formed of a coalition of the willing, which will be coordinated by the US. Currently, USTs are at a 111-15 trough, near enough unchanged on the session. If USTs conform to the bearish bias in EGBs, then Monday’s 111-13+ base is the first focal point before a bit of a gap until 110-23+ from the first week of August.

- As mentioned above, EGBs were slightly softer at this moment in time. Lower by as much as 10 ticks at worst. Pressure is seemingly a function of two bearish supply-side factors: 1) upcoming issuance, with Germany selling EUR 4.5bln of 2030 debt; 2) the funding security guarantees for Ukraine. Currently, the low point is 128.73. If we return to and move below this, Monday’s 128.70 base and then last week’s 128.64 trough comes into view. The German 2030 auction was well received, drawing a better-than-prior b/c – which helped to flip Bunds into positive territory.

- Gilts trade similar to Bunds but modestly underperforming. Thus far, to a 90.43 base with downside of just over 15 ticks at most. Taking out Monday’s 90.52 base and bringing levels from May into view. Given this, the UK 10yr yield is at a fresh WTD peak of 4.76%, approaching 4.69% from end-May.

- UK sells GBP 1.6bln 1.125% 2035 I/L Gilt: b/c 3.1x (prev. 3.35x) & real yield 1.728% (prev. 1.588%).

Commodities